three essays on institutional investment a thesis

TRANSCRIPT

THREE ESSAYS ON INSTITUTIONAL INVESTMENT

A thesis submitted to the University of Manchester for the degree of

Doctor of Philosophy

in the Faculty of Humanities.

2012

Nida Abdioglu Manchester Business School

2

LIST OF CONTENTS

ABSTRACT .................................................................................................................. 6

DECLARATION ......................................................................................................... 7

COPYRIGHT STATEMENT ..................................................................................... 7

DEDICATION .............................................................................................................. 8

ACKNOWLEDGEMENTS ......................................................................................... 8

CHAPTER 1- INTRODUCTION ............................................................................... 9

1.1.Motivation .......................................................................................................... 12

1.2.Purpose of The Thesis ........................................................................................ 16

1.3.Main Results ....................................................................................................... 23

1.4.Contribution ........................................................................................................ 26

1.5.Structure of The Thesis ...................................................................................... 28

CHAPTER 2- FOREIGN INSTITUTIONAL INVESTMENT: IS GOV ERNANCE QUALITY AT HOME IMPORTANT? ........................ ........................................... 29

2.1.Introduction ........................................................................................................ 29

2.2.Literature Review ............................................................................................... 33

2.3.Hypotheses ......................................................................................................... 37

2.4.Data and Methodology ....................................................................................... 41

2.4.1.Data .............................................................................................................. 41

2.4.2.Variables ...................................................................................................... 43

2.4.3.Methodology ................................................................................................ 48

2.5.Empirical Results ................................................................................................ 50

2.5.1.Descriptive Analyses ................................................................................... 50

2.5.2.Foreign Institutional Ownership and Country Governance ........................ 53

2.6.Robustness Tests ............................................................................................... 55

2.7.Conclusion .......................................................................................................... 60

CHAPTER 3- THE SARBANES-OXLEY ACT AND FOREIGN INSTITUTIONAL INVESTMENT IN THE US ................ ..................................... 79

3.1.Introduction ........................................................................................................ 79

3.2.Development of Hypotheses ............................................................................... 83

3

3.3.Data and Methodology ....................................................................................... 87

3.3.1.Independent Variables ................................................................................. 88

3.3.2.Methodology ................................................................................................ 92

3.3.3.Descriptive Statistics ................................................................................... 93

3.4. Empirical Results ............................................................................................... 94

3.4.1. SOX Effect on FIO ..................................................................................... 94

3.4.2. SOX Effect on Foreign Institutional Investors’ Firm Level Preferences ... 95

3.4.3.Passive FIO and SOX .................................................................................. 97

3.5.Robustness Tests ................................................................................................ 98

3.5.1.Am I Simply Reporting A Time Trend? ...................................................... 98

3.5.2.Macro Effects............................................................................................. 100

3.5.3.Further Tests .............................................................................................. 101

3.6.Conclusions ...................................................................................................... 102

CHAPTER 4- FIRM INNOVATION AND INSTITUTIONAL INVEST MENT: THE ROLE OF THE SARBANES-OXLEY ACT ................................................ 118

4.1.Introduction ...................................................................................................... 118

4.2.Hypothesis ........................................................................................................ 123

4.3.Data and Methodology ..................................................................................... 126

4.3.1.The Variables ............................................................................................. 127

4.3.2.Methodology .............................................................................................. 130

4.3.3.Descriptive Statistics ................................................................................. 131

4.4.Empirical Results .............................................................................................. 132

4.4.1.Univariate Analysis ................................................................................... 132

4.4.2.Multivariate Analyses ................................................................................ 133

4.5.Robustness Tests .............................................................................................. 135

4.5.1.The Effect of Increased Liquidity .............................................................. 135

4.5.2.Multivariate Difference-in-Differences Analysis ...................................... 137

4.6.Conclusion ........................................................................................................ 139

CHAPTER 5- CONCLUSION ................................................................................ 152

5.1.Summary of Findings and Future Research ..................................................... 152

5.2.Limitations ........................................................................................................ 156

REFERENCES ........................................................................................................ 161

4

LIST OF TABLES

Table 2.1.Institutional Ownership ............................................................................... 61

Table 2.2.Summary Statistics ....................................................................................... 62

Table 2.3.Correlation Matrix........................................................................................ 63

Table 2.4.Determinants of Foreign Institutional Ownership ....................................... 64

Table 2.5.Investment Preferences for Above/Below US Governance Quality at Home.. ...................................................................................................................................... 66

Table 2.6.Investment Preferences of Grey and Independent Foreign Institutional Investors .................................................................................................................... 68

Table 2.7.Alternative Proxies for Governance Quality at Home ................................. 70

Table 2.8.Alternative Specifications: SOX and Firm Fixed Effects ............................ 72

Appendix A: Ownership by Foreign Institutional Investor’s Country of Domicile. ... 75

Appendix B: Time Series Change in Governance Quality (GQ) by Country .............. 76

Appendix C: Details of the Directors’ Index (DINDEX) ............................................ 77

Table 3.1.Descriptive Statistics .................................................................................. 104

Table 3.2.Correlation Matrix...................................................................................... 106

Table 3.3.The SOX Effect on Foreign Institutional Investment ................................ 108

Table 3.4.The SOX Effect on the Firm-Level Preferences of Foreign Investors ..... 110

Table 3.5.Heterogeneous Effect of the Sarbanes-Oxley Act ..................................... 112

Table 3.6.Difference-in-Differences using Accelerated Filers .................................. 114

Table 3.7.Macro and Industry Effects ........................................................................ 116

Table 4.1.Descriptive Statistics .................................................................................. 141

Table 4.2.Correlation Matrix...................................................................................... 142

Table 4.3.Univariate Difference-in-Differences Results ........................................... 144

Table 4.4.The Effect of Innovation on the Relation between IO and SOX ............... 145

Table 4.5.The Effect of Increased Liquidity .............................................................. 148

Table 4.6.Multivariate Difference-in-Differences Results ....................................... 150

5

LIST OF FIGURES

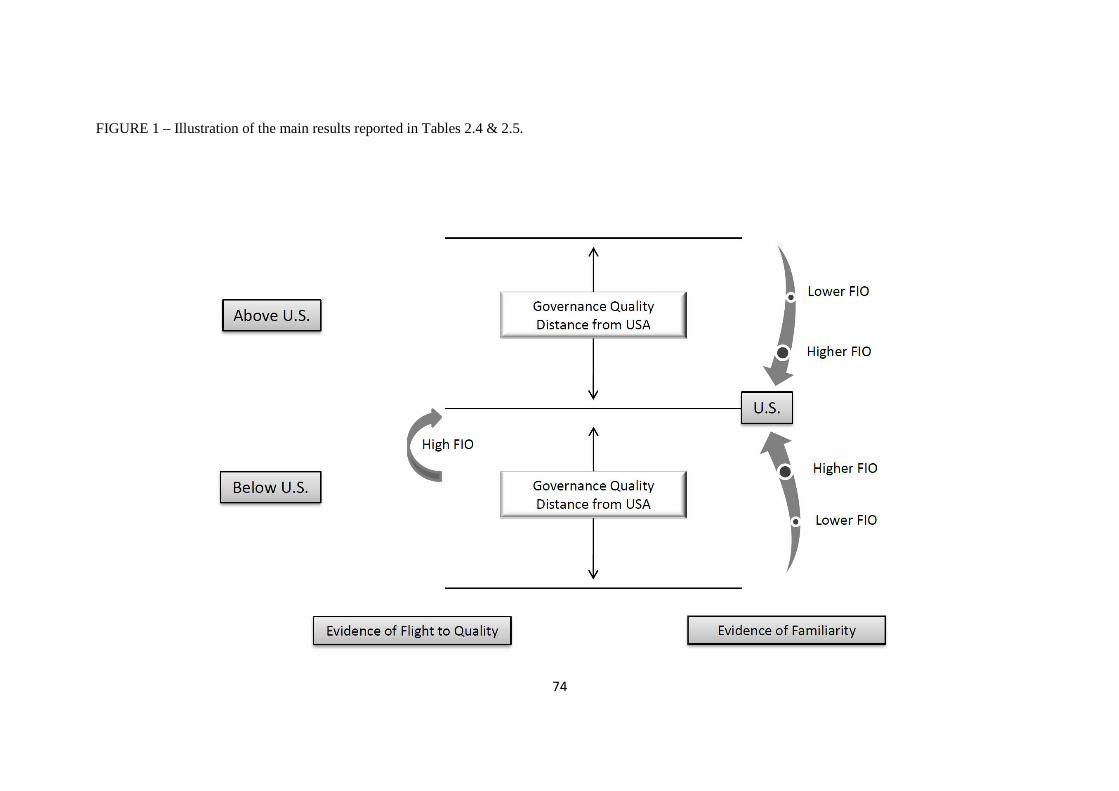

Figure 1: Illustration of the main results reported in Tables 4 & 5 .............................. 74

This thesis contains 43,951 words including title page, tables and footnotes.

6

ABSTRACT The University of Manchester Nida Abdioglu Doctor of Philosophy Three Essays on Institutional Investment 28/05/2012

This thesis investigates the investment preferences of institutional investors in the United States (US). In the second chapter, I analyse the impact of both firm and country-level determinants of foreign institutional investment. I find that the governance quality in a foreign institutional investor’s (FII) home country is a determinant of their decision to invest in the US market. My findings indicate that investors who come from countries with governance setups similar to that of the US invest more in the United States. The investment levels though, are more pronounced for countries with governance setups just below that of the US. My results are consistent with both the ‘flight to quality’ and ‘familiarity’ arguments, and help reconcile prior contradictory empirical evidence. At the firm level, I present unequivocal evidence in favour of the familiarity argument. FII domiciled in countries with high governance quality prefer to invest in US firms with high corporate governance quality.

In the third chapter, I investigate the impact of the Sarbanes-Oxley Act (SOX) on foreign institutional investment in the United States. I find that, post-SOX, FII increase their equity holdings in US listed firms. This result is mainly driven by passive, non-monitoring FII, who have the most to gain from the SOX-led reduction in firm information asymmetry, and the consequent reduction in the value of private information. The enactment of SOX appears to have changed the firm-level investment preferences of FII towards firms that would not be their traditional investment targets based on prudent man rules, e.g., smaller and riskier firms. In contrast to the extant literature, which mostly documents a negative SOX effect for the US markets, my chapter provides evidence of a positive SOX effect, namely the increase in foreign investment.

In the fourth chapter, I examine the effect of SOX on the relation between firm innovation and institutional ownership. I find that US firms investing in innovation attract more institutional capital post-SOX. Prior literature highlights two SOX effects that could cause this result: a decreased level of information asymmetry (direct effect) and increased market liquidity (indirect effect). My findings support the direct effect, as I find that the positive relation between innovation and institutional ownership is driven by passive and dedicated institutional investors. A reduction in firms’ information asymmetry is beneficial for these investors while they gain less from increased market liquidity. Overall, my results indicate that SOX is an important policy that has strengthened the institutional investor’s support for firm innovation.

7

DECLARATION

No portion of the work referred to in the thesis has been submitted in support of an application for another degree or qualification of this or any other university or other institute of learning.

COPYRIGHT STATEMENT

The author of this thesis (including any appendices and/or schedules to this thesis) owns

certain copyright or related rights in it (the “Copyright”) and she has given The University of Manchester certain rights to use such Copyright, including for administrative purposes.

Copies of this thesis, either in full or in extracts and whether in hard or electronic copy, may be made only in accordance with the Copyright, Designs and Patents Act 1988 (as amended) and regulations issued under it or, where appropriate, in accordance with licensing agreements which the University has from time to time. This page must form part of any such copies made.

The ownership of certain Copyright, patents, designs, trade marks and other intellectual property (the “Intellectual Property”) and any reproductions of copyright works in the thesis, for example graphs and tables (“Reproductions”), which may be described in this thesis, may not be owned by the author and may be owned by third parties. Such Intellectual Property and Reproductions cannot and must not be made available for use without the prior written permission of the owner(s) of the relevant Intellectual Property and/or Reproductions.

Further information on the conditions under which disclosure, publication and commercialisation of this thesis, the Copyright and any Intellectual Property and/or Reproductions described in it may take place is available in the University IP Policy (see http://www.campus.manchester.ac.uk/medialibrary/policies/intellectual-property.pdf), in any relevant Thesis restriction declarations deposited in the University Library, The University Library’s regulations (see http://www.manchester.ac.uk/library/aboutus/regulations) and in The University’s policy on presentation of Theses.

8

DEDICATION

I would like to dedicate this thesis to my family and to everyone who loves me.

ACKNOWLEDGEMENTS

I deeply thank my supervisors Dr. Konstantinos Stathopoulos and Dr. Arif Khurshed for their excellent supervision during my PhD. I would also like to thank all the members of staff at Manchester Business School who provided useful feedbacks during the end of year reviews. I am indebted to Turkish Government who provided me funding for my PhD. My friends in Manchester also deserve thanks for their friendship and support. Finally, I must express my gratitude to my family for their continued support during my studies.

9

CHAPTER 1: INTRODUCTION

Institutional investors are the dominant owners of most of the listed United States (US)

firms. Current estimates show that nearly 70% of the equity of US firms is owned by

domestic and foreign institutional investors and that over the last decade, foreign

institutional investment has almost doubled. A report by the US Department of Treasury

(2010) shows an increase in the level of foreign investment in US firms from $1.395

trillion in 2002 to $2.252 trillion in 2009. Although the level of foreign institutional

investment has increased, not much is known about the reasons why foreign

institutional investors have increased their investment in the United States. My research

sheds some light on this issue. I also examine the investment preferences of both the

domestic and foreign institutional investors.

There is some literature on the role of corporate governance quality of target firms and

governance quality of target countries in determining institutional investment in the

US1. According to a survey made by McKinsey (2002), a vast majority of institutional

investors prefer to invest in firms with high corporate governance quality and countries

with high governance quality. However, our understanding of the role of the corporate

governance setups of the home country (country of origin) of the foreign institutional

investors in influencing their decision to invest in the US is rather limited. In the first

empirical chapter, I examine the effect of home country governance quality on the

investment preferences of foreign institutional investors who invest in US firms. If

foreign investors have a low level of governance quality in their home country, they

may try to find better investment opportunities in a globalised world and may invest in

higher governance quality countries such as the United States. Foreign institutional

1 i.e. Ferreira and Matos (2008); Leuz et al. (2008).

10

investors in my sample are quite diverse and come from many different corporate

governance backgrounds. This simplifies investigating the impact of home country

governance quality on foreign institutional investment.

As a response to the corporate scandals such as those of Enron and Worldcom, the US

government brought in the Sarbanes-Oxley Act (SOX) of 2002. William H. Donaldson,

chairman of SEC, explains the results of SOX as: “Since its enactment in the summer

of 2002, the Act has affected dramatic change across corporate America and beyond,

and is helping to re-establish investor confidence in the integrity of corporate

disclosures and financial reporting.” (SEC, 2005)2. Engel et al. (2007) also state that

since the enactment of SOX puts in place new disclosure rules and adds penalties to

corporate frauds, US listed firms have to increase their corporate transparency. Ever

since SOX was enacted, there has been an ongoing debate on its merits and

disadvantages. However, this debate has largely overlooked SOX’s impact on foreign

institutional investment in the US. Given that SOX has resulted in higher transparency

and better corporate governance of US firms (Engel et al., 2007), has foreign

institutional investment in US firms increased post-SOX? My second empirical chapter

sheds some light on this issue. Since foreign investors originate from outside the US,

information asymmetry level of the stocks they invest in the US are an important

consideration for these investors. Thus, I expect that increased transparency and better

corporate governance of US firms might attract more foreign institutional investment to

the US market post-SOX.

2 Article title: Testimony Concerning the Impact of the Sarbanes-Oxley Act; accessed April, 2012;

source: http://www.sec.gov/news/testimony/ts042105whd.htm

11

A common problem for studies examining structural breaks in an economy is the

potential for capturing confounding effects. Recently, there is consensus in the literature

that one way of mitigating concerns regarding confounding effects is through the use of

difference-in-differences (DD) estimations. Therefore, in order to isolate the effect of

SOX from other institutional changes in the last decade, I use DD estimations. Since I

compare two groups (non-accelerated vs. accelerated filers) over the same time period, I

avoid the problem of omitted trends. Secondly, by making a time-series comparison

(before and after SOX enactment) between the two groups, I control for the impact of

unobserved, omitted variables in the analysis. The key assumption in the DD analysis is

that in the absence of the enactment of SOX, there would have been no difference in the

average change in foreign institutional investment (FII). Since I find significant results

in DD estimation, I can state that there is a SOX effect on FII.

In the final empirical chapter of my thesis, I use the enactment of SOX as a setting to

test the relation between firm innovation and institutional investment (both domestic

and foreign). Johnston and Madura (2009) support the SOX-led improvement in the

information efficiency of the US market by reporting better IPO performance for US

firms. Since SOX has resulted in lower information asymmetry of US firms (Johnston

and Madura, 2009), the monitoring costs of institutional investors should reduce post-

SOX. Hence, I explore whether institutional investors have increased their investments

in highly innovative firms post-SOX, which are known as stocks with high information

asymmetry.

This thesis is structured into three separate essays on institutional investment. The

purpose of the thesis is to examine the investment preferences of institutional investors

investing in US firms. In this chapter, I aim to provide a brief outline of my thesis. The

12

motivation behind this thesis is outlined in section 1. In section 2, I summarise the main

hypotheses and research questions for each empirical chapter. The main results and

contribution of the thesis are given in sections 3 and 4, respectively. Section 5 provides

guidelines about the structure of the thesis.

1.1. Motivation

Berle and Means (1932) note that the separation of ownership and control could lead

executives to act in their own interests without taking into account the interests of

shareholders. However, internal and external control mechanisms constrain the

executives’ activities. The existence of institutional investors in a firm is one of the

external control mechanisms (Gillan and Starks, 2003). Institutional investors affect the

management’s actions through a high level of ownership in corporations. Their

involvement in monitoring and controlling activities is expected to reduce the agency

problems (Shleifer and Vishny, 1986; Maug, 1998; Noe, 2002). On the one hand,

institutional investors can affect the management of the firm through the threat of

exiting the investment, that is, voting with their feet (Parrino et al., 2003). In other

words, they could sell their shares and drive the price of the firm down if they were

dissatisfied with the firm’s management (Palmiter, 2002). Since the managers’

compensation is tied to share prices, the presence of institutional investors in a firm may

help to reduce the agency cost with disciplining managers and thus improve corporate

governance (Admati and Pfleiderer, 2009).

On the other hand, since it is not easy to sell large holdings, institutional investors

sometimes prefer to retain their investments and force management to act in the

13

shareholders’ interests (Demiralp et al., 2011). They have an incentive to monitor the

management of the firm since they cannot always sell the shares of firms with which

they are dissatisfied (Coffee, 1991; Gillan and Starks, 2000). For instance, Parrino et al.

(2003) find that, although some institutional investors vote with their feet when they are

dissatisfied with forced CEO turnover, over 45% of them prefer to stay with the firm

and influence change. Since the institutional investors have an impact on the

management of the firms through voting with their feet or monitoring ability, it is

important to understand the investors’ investment preferences for the firm management.

This role of institutional investors is one of the reasons that have motivated me to

examine their investment preferences.

Further, the difficulty of exiting also affects the investment preferences of institutional

investors. As a result of the difficulty of selling large shares, institutional investors have

an incentive to invest in reliable firms. In other words, they follow the prudent man rule

by investing in reliable assets, such as stocks with high corporate governance quality

and less information asymmetry (Badrinath et al., 1989). The behaviour of institutional

investors towards corporate governance quality and/or information asymmetry is the

motivation behind my investigation of their investment preferences in cases of low/high

information asymmetry and/or governance quality in their home country. In other

words, I explore whether foreign institutional investors’ preferences about investing in

prudent stocks show differences according to their home country governance quality

while investing in US firms. I am inspired by familiarity argument dominated in the

behaviour of foreign institutional investors to create this idea. Since foreign institutional

investors want to minimize information costs when investing abroad, they invest in

familiar stocks. I categorize stocks with high level of corporate governance quality in

14

the US as familiar stocks for the foreign investors who have high level of governance

quality in their country of origin.

The preferences of institutional investors regarding information asymmetry is applicable

to country-level as well as firm-level preferences. As a result of their incomplete

information about foreign markets, the cost of investing abroad is high for these

investors. Because of the information asymmetry cost, they avoid investing abroad. As a

result, a home bias phenomenon occurs (Tesar and Werner, 1995). In other words,

institutional investors prefer to hold more domestic assets than foreign assets. However,

with globalisation, foreign investment abroad has started to increase (Leuz et al., 2009;

Bekaert et al., 2002). The US Department of Treasury 2010 report shows an increase in

foreign holdings of US equities, from $1.395 trillion in 2002 to $2.252 trillion in 2009.3

A recent report by the Congressional Research Service (Jackson, 2010) also

demonstrates the rise in foreign investment in US financial assets over recent years. An

important question thus arises: What is the reason for the recent increase in the level of

foreign institutional investment in the United States? I explore some of the reasons

behind this increase in the second and third chapters. Given the growing level and

importance of foreign capital across firms, it is important to understand the factors that

attract investors to foreign markets. In the second chapter, I argue that one of these

factors is the home country governance quality of foreign institutional investors. In the

third chapter, it is the new regulation enacted in the US: SOX. Understanding the

motivation behind the high level of foreign capital inflow to the US market will help

regulators of the market to arrange the market conditions in a way to attract more

foreign investment.

3 Out of the total foreign investment in the US market, 80% is foreign institutional investment.

15

One of the most important contribution of this thesis is to show home country

governance quality as an investment determinant of foreign institutional investment. I

show the US market, a high governance quality market, as a safe place to invest

especially for the foreign investors who have low level of governance quality in their

home country. The lower level of information asymmetry cost they encounter in the US

market drives this result. Secondly, I argue that the enactment of SOX should affect the

investment level and preferences of foreign institutional investors investing in the US.

Since a higher level of foreign institutional investment can now be seen in the US

markets, the market conditions that might have induced this rise should be identified. A

change in market conditions might have been caused by a regulation enacted in the US.

SOX is seen as a significant milestone in the improvement of corporate governance in

the country. It was implemented in response to a series of corporate scandals and its aim

is to reinforce investor confidence in the capital markets, by imposing high levels of

disclosure on US listed firms. The increased transparency in the US market should have

resulted in lower levels of information asymmetry in US firms and thus reduced the

costs of monitoring managerial actions. Therefore, the improved market conditions

should have altered the attitudes of foreign institutional investors towards US listed

firms. This is my motivation in the third chapter where I examine foreign institutional

investors’ investment preferences after the enactment of SOX. In addition, lower

information asymmetry post-SOX should reduce the monitoring costs of institutional

investors, thus they should face lower agency costs. As a result, their behaviour in

relation to highly innovative firms, which are known to have high information

asymmetry, should change post SOX. I examine this relation in the fourth chapter.

16

1.2. Purpose of the Thesis

Merton’s (1987) model suggests that information costs have an impact on investor

behaviour. Since investors believe stocks they know nothing about to be risky, they

prefer not to invest in them. Thus, the level of information asymmetry in a stock affects

the behaviour of investors4. In addition, the behaviour of institutional investors is

affected by the prudent man rule (Del Guercio, 1996). In line with this rule, they invest

in fiduciary assets such as large firms, less leveraged firms, firms with less information

asymmetry, those with high governance quality, and the like5. Overall, prudent man rule

and information cost arguments show how the investment preferences of institutional

investors can be affected. In this thesis, I examine how effective these arguments are for

foreign (chapters 2 and 3) and overall institutional investors’ (chapter 4) preferences.

In general, I was inspired by the abovementioned theories, while examining the

investment preferences of institutional investors. In particular, in the second chapter, I

investigate whether the investment preferences of foreign institutional investors are

affected by their home countries’ governance quality. The research questions I created

for this chapter are as follows: 1) Does the governance quality of the home country play

any role in the foreign institutional investor’s decision to invest in the US? 2) Does

country-level governance quality affect the foreign institutional investors’ preferences

for specific US firms? By finding answers for these research questions, I investigate the

reasons of high level of foreign institutional investment in US firms. These research

4 For instance, Coval and Moskowitz (1999) highlight the importance of information costs by showing

investors’ willingness to hold the stocks of local companies. The information cost affects the behaviour of foreign investors as well as local investors. Kang and Stulz (1997) provide evidence in support of this argument, by finding more foreign investment in large firms. Since large firms are more information-efficient, they are preferred by foreign investors. 5 Chung et al. (2010) argue that high governance quality results in higher transparency and thus lower information asymmetry between insiders and outsiders.

17

questions are important in the sense that they aim to show how the home country

governance quality of the foreign investors is a determinant of their investment

preferences. They are also important in terms of showing how foreign investors trade

off information costs associated with investing abroad. Home country governance

quality of the foreign investors might be a determinant of foreign institutional

investment, as the lack of governance quality in their country might force them to seek

safer investment opportunities. By investing in a more informationally efficient

environment (US market), foreigners might reduce the information cost they encounter

at home.

Firstly, I argue that the decisions of foreign institutional investors regarding their

investment in a country with higher governance quality, the US, should vary according

to their home country’s governance quality. Prior literature generally examines how

country and firm-level policies affect the investment allocations of institutional

investors. Aggarwal et al. (2005) find that strong governance environments attract more

institutional investment. In particular, US mutual funds invest more in firms in

emerging-market countries with stronger accounting standards, shareholder rights, and

legal frameworks. Furthermore, Chan et al. (2005) report that foreign institutional

investors invest in countries they are familiar with and which have a high level of stock

market development. Li et al. (2006) find that institutional investors invest more in

countries with strong shareholder rights, effective legal enforcement and extensive

financial disclosure. All of these papers examine the impact of the governance quality in

the countries targeted by institutional investors. However, in the second chapter of this

thesis, I investigate the effect of the governance quality of a foreign institutional

investor’s home country on that investor’s investment preferences. I argue that low-

quality governance in a country results in weak investor protection, low information

18

disclosure and thus high information asymmetry. It is well known from the literature

that investors prefer to invest in high-quality governance countries and therefore

countries with a high level of investor protection (Aggarwal et al., 2011; Leuz et al.,

2009). This behaviour is in line with the prudent man rule. Even if a firm has a high

level of governance quality itself, if it is domiciled in a country with low governance

quality, it will benefit less from the capital markets (Doidge et al., 2007). Having high

firm-level governance quality cannot substitute for the governance quality at the country

level (Klapper and Love, 2004). For these reasons, I expect that the quality of the

governance environment should be a determinant of institutional investment. However,

in contrast to the literature, I expect that governance quality in the home country of the

investor will be influential on his investment preferences besides the target country’s

governance quality.

Further, in line with the good country bias theory of Giannetti and Koskinen (2010),

investors domiciled in countries with weak investor protection should prefer to invest

more in countries with higher investor protection than their home country. Therefore, a

good country bias should be seen in the investment preferences of institutional

investors. In other words, an impact of flight to quality will be seen in the investment

behaviour of foreign institutional investors who have lower governance quality at home

than exists in the US. They invest in the US to gain the benefit of high governance

quality.

In addition, I expect that the flight to quality by foreign institutional investors might

vary according to the relative distances in governance quality between the home country

and the US. This argument allows me to test the familiarity bias on foreign institutional

investment. In this case, I define a country as familiar to the US if it has similar

governance quality to that in the US. I expect a greater amount of foreign institutional

19

investment in US firms to come from countries with similar governance quality to the

US. Put differently, foreign investors prefer to invest in familiar environments. Since

familiar stocks help investors to reduce the costs associated with uncertainty, they prefer

to invest in familiar stocks (Chan et al., 2005). In sum, I predict that both the effect of

familiarity and flight to quality are likely to co-exist in the investment behaviour of

foreign institutional investors. The difference in governance quality between the home

country and the US will determine the combination of the two effects.

Secondly, an additional strand of the literature investigating the investment preferences

of institutional investors has typically focused on firm-level determinants of

institutional ownership, such as size, dividend yield and firm performance (Ferreira and

Matos, 2008; Kang and Stulz, 1997; Dahlquist and Robertsson, 2001; Falkenstein,

1996; Gompers and Metrick, 2001; Almazan et al., 2005), with almost no attention

given to home country governance quality. However, I investigate whether the home

country governance quality has any effect on the firm-level preferences of institutional

investors. According to Kang and Stulz (1997), foreign institutional investors invest in

stocks they know in order to avoid the information cost of investing in stocks they do

not. The former are known as familiar stocks. In this thesis, I define a firm as familiar to

a foreign investor if that firm has a similar level of information asymmetry (or

governance quality) as exists in the investor’s country of origin. I do not expect to

observe homogeneous preferences among the foreign institutional investors. I argue that

those with low information asymmetry in their home country invest in US stocks with

low information asymmetry. In other words, foreign institutional investors give

importance to familiarity in stock characteristics when they invest abroad. Since

familiarity decreases the information cost, familiar stocks are more attractive to foreign

investors.

20

In the third chapter, I examine how the enactment of SOX affects the investment

preferences of foreign institutional investors. Since the level of information asymmetry

in the market is expected to decrease as a result of the SOX implementation, I expect

foreign institutional investors to be attracted to US firms, post-SOX. Accepting the

changes in the US market transparency, I argue that finding answers to the following

research questions will be an important contribution to the literature: 1) What has been

the impact of SOX on investments by foreign institutional investors? 2) Have the

investment preferences of foreign institutional investors been affected by SOX? These

questions are important for the SOX literature, because I will demonstrate a new benefit

of SOX: foreign institutional investment. Further, it is important to show how an

improvement in market conditions attracts foreign investment in US firms. It is also

important to see whether enactment of a new regulation in the US market changes the

level and investment preferences of foreign institutional investors for specific US firms.

Although prudent man rule may dictate the investment preferences of foreign

institutional investors, an increase in the reliability of information in US firms with

SOX might result with new preferences for institutional investors.

Given the importance of information asymmetry for foreign institutional investors’

investment choices, I examine the impact of a reduction in the information asymmetry

level in the US market, through the enactment of SOX, on the level of foreign

institutional investment in US firms. A strand of the extant literature discusses the

benefits, and mostly the costs, of SOX. For example, Zhang (2007) finds negative

cumulative abnormal returns around SOX-related events for a sample of US firms.

Litvak (2007) concludes that there is a decline in the stock prices of foreign firms that

are subject to SOX, whereas he finds an increase in the stock prices of foreign firms not

21

subject to SOX. Ribstein (2002) and Romano (2005) find that high expected reporting,

regulatory and legal costs of listing on US exchanges are among the disadvantages of

SOX. Li et al. (2008) and Jain and Rezaee (2006) respectively report positive stock

price and positive abnormal return reactions to legislative events surrounding SOX.

Coates (2007) shows that enhanced trust in US capital markets is a benefit of SOX.

Unlike the existing literature, I argue that the level of foreign institutional ownership

has increased since the enactment of SOX. One of the main results of the enactment of

SOX is the increased disclosure, and decreased information asymmetry in the US

market.6 I expect that the reduction in information asymmetry should affect the

investment decisions of foreign institutional investors. Since one of the investment

determinants for institutional investors is a high level of corporate disclosure (Bushee

and Noe, 2000), they should be more attracted to investing in the US market post-SOX.

In addition, in the second hypothesis of chapter 3, I argue that foreign institutional

investors invest in non-prudent stocks as well as prudent stocks, post-SOX. Historically,

institutional investors have invested in reliable stocks, in line with the prudent man rule

(Badrinath et al., 1989).7 Since the foreign institutional investors come from outside the

US, information efficiency in the US market is more important for them. Given that

SOX has increased the information efficiency in the market, US assets should now be a

more reliable investment for foreign institutional investors. In particular, the assets that

used to be non-prudent must be more reliable post-SOX. Thus, I expect to find foreign

investment in these stocks as well.

6 Johnston and Madura (2009) present evidence of the increased information efficiency in the US market,

post-SOX.

7 Large firms, firms with high liquidity and those with a high book-to-market ratio can be shown to be examples of prudent stocks (Del Guercio, 1996).

22

In the final hypothesis of chapter 3, I separate foreign institutional investors into active

and passive ones. According to Brickley et al. (1988), passive investors (such as banks

and insurance companies) have a close business relationship with the management of

the firms in which they invest. Since they do not want to damage their relationship with

the firm, they face high costs of monitoring and do not expend effort collecting private

information about the firm (Chen et al., 2007). Thus, a reduction in the value of private

information will be beneficial for them. On the other hand, active institutional investors

(such as investment companies, independent investment advisors and public pension

funds) do not have close business ties with their investee firms (Brickley et al., 1988)

and they face lower legal restrictions (Jiao and Liu, 2009). As a result, they collect and

use private information (Almazan et al., 2005). A reduction in the value of private

information reduces the advantage of active investors. Given that SOX has increased the

information transparency in the US market, the value of private information should have

decreased post-SOX. Thus, I argue that passive institutional investment should now be

more pronounced in the US market than active. In particular, passive institutional

investment should be greater in firms with higher levels of private information.

In the final empirical chapter, I analyse how the reduction of information asymmetry by

SOX has affected the behaviour of institutional investors towards highly innovative

stocks, which are those with high information asymmetry. I have one main research

question in the last empirical chapter: Do highly innovative firms attract more

institutional investment after the enactment of SOX? It is important to investigate this

research question in order to determine whether this policy has resulted in a

strengthening of institutional investor support for firm innovation.

23

Because of their high level of information asymmetry,8 highly innovative firms cannot

attract institutional investment (Bushee, 1998; Graves and Waddock, 1990; Jacobs,

1991; Porter, 1992). For instance, since R&D expenditures are idiosyncratic, they

cannot easily be monitored. As a result, a high level of information asymmetry occurs

between insiders and outsiders in high-R&D firms (Aboody and Lev, 2000). As I have

mentioned in the above paragraphs, SOX has changed the information efficiency of the

US market. It imposes high disclosure requirements on US listed firms and has thus

made the US market more transparent (Engel et al., 2007). The enactment of SOX has

improved the reliability of public financial information and resulted in increased

investor confidence in financial reports. As a result, liquidity has increased in the US

market post-SOX (Jain et al., 2008). I predict that this increased information efficiency

and/or increased market liquidity has strengthened the relation between institutional

investment and firm innovation, post-SOX. Highly innovative firms should attract more

institutional investment with the reduced information asymmetry post-SOX.

1.3. Main Results

In the second chapter, I find that foreign institutional investors who have low

governance quality at home, invest more in US firms. This result supports the flight-to-

quality argument regarding the investment behaviour of institutional investors. In

addition, I find more foreign institutional investment in US firms from countries whose

governance quality is similar to that of the US. Thus, I support the familiarity argument

at the country level. However, investors from countries whose governance quality is just

below (above) that of the US, invest more (less) in US firms. I conclude that the flight-

8 See Mohd (2005), Aboody and Lev (2000), Barth and Kasznik (1999), Barth and McNichols (2001) and Boone and Raman (2001).

24

to-quality and familiarity arguments have complementary effects on the investment

preferences of foreign institutional investors.

In addition, I examine the differences in the investment preferences of foreign

institutional investors. Although prior studies have examined the firm-specific

investment preferences of these investors, none has investigated the impact of the home

country’s governance quality on these preferences. I find that foreign institutional

investors who originate from countries with high governance quality, invest in firms

with high governance quality in the US. Thus, at the firm level, my result is consistent

with the familiarity argument.

In the third chapter, I investigate the economic effect of the enactment of SOX in the

US market, by examining the foreign institutional investment in the US, post-SOX. I

find an increased level of foreign institutional investment in US firms post-SOX. I argue

that the increased level of corporate disclosure, and the resulting decrease in

information asymmetry in the US, has made the US market a more reliable target for

foreign institutional investors and, as a result, they have increased their investment in it.

I find that this result is mainly driven by passive institutional investors. The value of

private information decreases in the US market post-SOX as a result of increased

information efficiency. Since passive investors do not have private information about

their investee firms, a decrease in the value of private information is more beneficial for

them.

Finally, I investigate the effect of SOX on the firm-specific investment preferences of

foreign institutional investors. I find that foreign institutional investors invest in both

prudent and non-prudent stocks post-SOX. According to Del Guercio (1996),

institutional investors prefer to invest in prudent stocks, in line with prudent man

behaviour. Since the information disclosure in a country is more important for foreign

25

institutional investors, the decreased information asymmetry due to the enactment of

SOX makes the non-prudent stocks more attractive for these investors. Stocks which

were not the traditional target for foreign institutional investors should be more accurate

and reliable and, as a result, should attract more foreign institutional investment post-

SOX. In line with this argument, I find that foreign institutional investors invest in

smaller stocks, stocks with higher leverage and those with lower dividend yields.

In the fourth chapter, I investigate the impact of SOX on the relation between

innovation and overall institutional ownership. I find that highly innovative firms attract

more institutional investment post-SOX. Since my results are driven by passive

institutional investors, I conclude that reduced information asymmetry in the US market

strengthens the relation between institutional ownership and innovation. I also find

more dedicated institutional ownership in highly innovative firms, post-SOX. As a

result, I conclude that the increased level of liquidity post-SOX cannot explain the

positive relation between innovation and institutional ownership. If this was the case, I

should have found a more pronounced non-dedicated institutional investment. Since

non-dedicated investors trade frequently, market liquidity is an important determinant of

their investment preferences.

Although each essay is a separate empirical study, all of them have a common thread:

institutional investment. In the second and third chapters, I examine the investment

preferences of foreign institutional investors. However, I explore the investment

preferences of all institutional investors in the fourth chapter. Second and third chapters

are connected through foreign institutional investment where as third and fourth

chapters are connected through SOX. Each empirical chapter highlights the importance

of the level of information asymmetry in the stock market (or in a firm) to the

investment preferences of institutional investors. However, the application of this idea is

26

different in each empirical chapter. In the second chapter, I show that the high

information efficiency of the US market attracts more foreign institutional investment

from less information-efficient countries. Thus, besides the importance of the target

country’s information efficiency, the information asymmetry level in the home country

of the foreign investor is important for his investment preferences. Further, in the third

and fourth chapters I show that a regulation, SOX, has changed the investment

preferences of institutional investors. In the third chapter, I show that, with the reduced

information asymmetry level in the US market post-SOX, foreign institutional

investment has increased. In addition, since the market is more reliable post-SOX, the

foreign institutional investors invest in less prudent stocks as well as prudent ones.

Following this idea, I find in the fourth chapter that the reduction in the level of

information asymmetry in the US market, post-SOX, has made highly innovative firms

more attractive to institutional investors. Put differently, in the third and fourth chapters

I argue that the confidence of investors in the US market has increased post-SOX and

institutional investors have started to invest in less prudent stocks.

1.4. Contribution

This thesis’ contribution is centred on its investigation of the investment preferences of

foreign and overall institutional investors investing in the US. Although foreign

institutional investment shows an increasing pattern in the US stock market, the existing

literature mainly focuses on aspects of US institutional investment, in the US or abroad.

By investigating the recent trends in foreign institutional investment in the US market,

in the second and third chapters, I differentiate my study from the existing literature.

Past literature generally examines how country and firm-level policies affect the

investment allocations of institutional investors, for example, Ferreira and Matos

27

(2008), Kang and Stulz (1997) and Leuz et al. (2009). However, I highlight the

importance of home country (as opposed to target country) governance quality as a

determinant of foreign institutional investment. I contribute to the literature by showing

the negative effect of home country governance quality on foreign institutional

investors’ investment decisions when they invest in the US. This result is an important

contribution to the literature. By finding evidence of this behaviour by foreign

institutional investors, this thesis provides a guide to foreigners about how they can

trade off the information costs associated with foreign investment. The evidence also

gives some idea to foreigners of how they might minimise the information cost. For

instance, foreign institutional investors can target familiar stocks to achieve this benefit.

Although prior literature shows flight-to-quality and familiarity arguments as alternative

explanations for the investment preferences of institutional investors, I report a

complementary effect between these two arguments9. These two arguments coexist for

the investment preferences of foreign institutional investors. Another contribution of

this thesis is the reported evidence in favour of the familiarity argument in the

investment preferences of foreign institutional investors when they invest in the US10.

This thesis also contributes to the SOX literature by demonstrating its effect on

institutional ownership. SOX was enacted as a result of some high-profile corporate

governance scandals in the US. Since its implementation, the effect of SOX on the US

economy has been an open question. The existing literature generally examines the

benefits, and mostly the costs, of SOX on firms listed in the US exchanges. However,

none so far have examined its effect on institutional investment. I report a benefit of

9 I find that foreign institutional investors from countries with low governance quality invest more in US firms. I also find that the foreign institutional investment in the US is more pronounced from countries with a similar level of governance quality to the US. 10 Foreigners who have high governance quality at home invest more in US firms with high governance quality.

28

SOX, in terms of increased foreign institutional investment since its enactment. I also

show how SOX has changed the investment preferences of foreign institutional

investors. Since its enactment, they not only invest in prudent stocks but in non-prudent

stocks as well.

Finally, I contribute to the innovation literature by examining the impact of SOX on the

relation between innovation and institutional ownership. I show that an improvement in

the information efficiency of the US market, with SOX, results with attracting

institutional investment to innovative firms. The existing literature generally examines

the relation between innovation and institutional ownership. However, none of them has

examined an effect of a regulation on this relation. By investigating the impact of SOX

on this relation, I contribute to the literature.

1.5. Structure of the Thesis

The thesis is organised as follows: In the second chapter, I examine the effect of

governance quality at home on the investment preferences of foreign institutional

investors. In the third chapter, I investigate the effect of SOX on the investment

preferences of foreign institutional investors. In the fourth chapter, I discuss the role of

SOX in determining the relation between innovation and institutional ownership. The

fifth chapter concludes.

29

CHAPTER 2: FOREIGN INSTITUTIONAL INVESTMENT: IS GOV ERNANCE QUALITY AT HOME IMPORTANT?

2.1. Introduction

Investors allocate only a small fraction of their wealth to foreign markets, a practice

typically referred to as the ‘home bias puzzle’ (Tesar and Werner, 1995). Kang and

Stulz (1997) identify explicit and implicit barriers as the most important explanation of

the home bias puzzle.11 Information asymmetry is one of the barriers that foreign

investors encounter when they invest abroad. Since the foreign investors have an

informational disadvantage relative to local investors, the cost of investing abroad is

high for them and it is this cost that prevents them from investing in foreign markets.12

However, recent trends document an increase in foreign investment as a result of

globalisation. With globalisation, foreign capital has become an important source of

finance in many capital markets and foreign investors have started to allocate more of

their money abroad (Leuz et al., 2009; Bekaert et al., 2002).

Over the last decade, equity ownership by foreign institutional investors in United

States (US) firms has almost doubled in size. In 1999, nearly 4% of the equity in S&P

1500 firms13 was in the hands of foreign institutional investors. This had increased to

8% by 2008. According to the 2008 US Treasury report on institutional holdings,

$2.969 trillion worth of capital is in the hands of foreign institutional investors. This

substantial and growing foreign investment in the US motivates the investigation of the

11

One explicit barrier is the constraint on foreign exchange transactions. Political risk and information asymmetry differences between foreign and domestic investors are examples of implicit barriers. 12Several studies, such as Brennan and Cao (1997), Kang and Stulz (1997), report the information disadvantage of foreign investors relative to domestic investors. Dvorak (2003) also discusses the information asymmetry between foreign and domestic investors. 13

S&P Composite 1500 covers approximately 85% of the US market capitalisation.

30

determinants of foreign investment. The fact that most of it is channelled through

institutional investors justifies the research focus of this chapter.

Although foreign institutional investors have grown in size and importance in the US

market, most of the academic studies on institutional ownership focus on aspects of US

institutional investment, either within the US or abroad with almost no attention being

paid to foreign institutional investment in the United States. Further, studies that focus

on the determinants of institutional ownership have always considered firm- specific

variables, such as financial performance, liquidity, size, volatility and corporate

governance setups (for example see Dahlquist and Robertsson, 2001; Almazan et al.,

2005; Li et al., 2006). The role of country-level governance quality has largely been

ignored.14

In this chapter, I examine the investment preferences of foreign institutional investors

investing in US firms and investigate the role of country-level governance quality on

their investment preferences. Specifically, I address two important research questions:

First, does the governance quality of the home country15 play any role in the foreign

institutional investor’s decision to invest in the US? Second, does country- level

governance quality affect the foreign institutional investor’s preferences for specific US

firms?

So far, the existing literature finds that, in order to avoid high levels of investment costs,

foreign institutional investors place importance on the country-level governance quality

of the countries they invest in (Li et al., 2006; Leuz et al., 2009). However, in this

chapter I argue that the governance quality of the foreign institutional investors’ own

14 Notable exemptions are the studies by Kim et al. (2011) and Forbes (2010); I refer to these papers in detail below. 15 Home country is the foreign institutional investors’ country of domicile.

31

countries affects their investment preferences as well. If they have low-quality

governance at home, their costs when investing at home might be much higher than the

costs they bear when investing abroad. This trades off the information asymmetry costs

associated with foreign investment. In line with the ‘good country bias’ theory of

Giannetti and Koskinen (2010), I argue that weak investor protection, low information

disclosure and, therefore, high information asymmetry result from low-quality

governance in a country. Thus, institutional investors who are domiciled in a country

with weak investor protection are inclined to invest in foreign countries that provide

higher-quality corporate governance than their home country. As a result, a good

country bias is seen in the investment preferences of foreign institutional investors.

Putting this a different way, I expect to see a pronounced effect of flight to quality in the

investment behaviour of foreign institutional investors who have lower governance

quality at home than exists in the United States. Still, one should acknowledge the

possibility of higher institutional investment levels from countries with similar

(therefore, even just above that of the US) levels of governance quality. Based on the

familiarity argument (Chan et al., 2005), institutional investors prefer the familiar to the

unfamiliar, since the former allows them to reduce the costs associated with investment

uncertainty and ‘prudent man rule’ mandates. Therefore, I argue that both biases, flight

to quality and familiarity, affect foreign institutional investment preferences in the US

market. My argument allows for heterogeneity in the investment preferences of foreign

institutional investors based on the relative distance in governance quality between the

US and the home country.

Furthermore, although prior studies (i.e., Ferreira and Matos, 2008; Kang and Stulz,

1997) have examined the relation between foreign institutional investment and firm-

specific characteristics, they have not investigated whether this relation depends on the

32

home country’s governance quality. I argue that foreigners do not have homogeneous

preferences when choosing the firms they invest in. Foreign institutional investors who

have low information asymmetry at home (high governance quality) invest in low

information asymmetry US stocks (high corporate governance quality stocks). This

prediction is in line with the familiarity argument. Foreign institutional investors look

for familiarity in stock characteristics when they invest abroad, because familiarity will

reduce the information costs and, as a result, the home bias will decrease. I proxy

familiarity with the similarity between the level of information asymmetry a foreign

investor is exposed to at home and the level they experience in the target firm.16

I find that foreign institutional investors who have low governance quality at home

invest more in the US market. To my knowledge, this study is among the first in the

literature to focus on home country governance quality as a determinant of foreign

institutional investment preferences. In addition, I examine differences in the choices of

institutional investors, based on the different levels of governance quality they

experience at home. I split my sampled countries into those with governance quality

above and below that of the US (the Above-US and Below-US groups) and thus

investigate separately foreign institutional investment from countries with higher and

lower governance quality than the United States. Foreign institutional investors from

countries with similar (just above/below) governance quality to that of the US invest

more in the US market. Thus, I also find support for the familiarity argument at the

country level: the closer the foreign institutional investors are to the US, in terms of the

governance quality they experience at home, the more they invest in the US. These

16 The literature uses several proxies for familiarity. I present some of them in Section 3.

33

findings suggest a complementary effect (instead of a substitution one) between the

familiarity and flight to quality arguments.

At the firm level, my results show that foreign institutional investors who come from

countries with high governance quality invest in US firms with good corporate

governance systems. Thus, the home country’s level of governance affects the

investor’s portfolio choices abroad. I argue that the familiarity bias holds even for firm-

level preferences. My results also indicate that this effect is driven by grey investors,

who do not actively monitor the management teams of the firms they invest in, and

therefore have the most to gain from a reduction in information asymmetry.

The rest of the chapter is structured as follows. In Section 2, I provide an overview of

the literature on the investment preferences of foreign institutional investors and

highlight my contributions. Section 3 presents my hypotheses. My data and

methodology follow in Section 4. Section 5 discusses the empirical results. Section 6

presents my robustness tests. Section 7 provides my conclusions.

2.2. Literature Review

Prior empirical work that examines the investment preferences of foreign institutional

investors typically investigates the preferences of US institutional investors when

investing abroad. Leuz et al. (2009) analyse the foreign holdings of US investors and

document that the typical US investor invests less in countries with weak legal

institutions and poor information frameworks. Aggarwal et al. (2005) examine the

investment choices of US mutual funds in emerging markets. They find that strong

accounting standards, shareholder rights and legal frameworks attract more US

34

investment. Ferreira and Matos (2008) also find that foreign institutional investors

invest more in countries that have strong governance systems. Having analysed the

equity holdings of mutual funds from 26 developed countries, Chan et al. (2005) report

that high levels of foreign institutional investment are expected in countries with low

expropriation risk. Li et al. (2006) use the degree of enforcement of shareholder rights

as a proxy for a country’s governance quality. They find a positive association between

the degree of enforcement and foreign institutional investment. Finally, Gelos and Wei

(2005) find that international institutional investors invest in more transparent

markets.17

All the above papers examine the effect of the governance quality of the countries in

which the institutional investors are investing (target country) and establish a significant

link with foreign investment levels (capital inflows). However, I argue that foreign

institutional investment preferences are not homogeneous with regard to country-level

governance quality. By examining the differences between the home country’s

governance quality and a benchmark, i.e., the level of governance in the US, I study the

sources and impact of this heterogeneity. My research design allows me to examine the

impact of each country’s governance quality (home country) on the level of foreign

investment in the US by institutional investors domiciled in that country (capital

outflows). Two recent papers investigate foreign investment in the US market. Cai and

Warnock (2006) study the security-level investment preferences of foreign and domestic

institutional investors in the United States. They identify a preference of institutional

investors for domestic multinationals. They argue that this is a safe way of achieving

international diversification. The scope and focus of my study is different. In particular,

17 La Porta et al. (1997, 1998 and 2000) also examine the effect of country-level governance quality on investment decisions.

35

I relate investment preferences to home governance quality and investigate the

investment patterns of foreign institutional investors both at the country and firm levels.

I find that the heterogeneity in countries’ governance quality around the globe explains

the investment choices in the US market.

The paper closest to this study is that of Forbes (2010). She studies the level of foreign

investment in the US and concludes that foreign investors hold a greater amount of their

wealth in the United States, if they have a less developed financial market at home.

There are significant differences between my study and that of Forbes (2010). Forbes

(2010) studies the holdings of all types of foreign investors, including government

agencies and other official institutions. In contrast, I focus on private institutional

investment; I expect market-based considerations, e.g., governance quality, to be the

main driver of the decision making of this group of informed investors. Political, and

other non-market based, influences are expected to carry less weight in the investment

choices of this group. Also, Forbes (2010) investigates foreign holdings in both the

equity and debt markets. There are substantial differences in the profiles of investments

in equities and liabilities, e.g., risk characteristics and exposure, investment horizon,

investor types. To avoid capturing systematic differences in the investor profiles, which

might affect my results in unpredictable ways, I focus only on the equity markets. In

addition, my research design helps me to explore the heterogeneity in the governance

quality of countries with substantially different profiles to that of the United States. My

findings on the co-existence of the flight to quality and familiarity biases extend those

provided by Forbes (2010) and help us to reconcile the conflicting evidence she offers

with that of other studies (e.g., Aggarwal et al., 2005). Finally, but equally importantly,

I also provide security-level analyses, which highlight the importance of governance

36

quality at home for the firm-level investment preferences of foreign investors, which

Forbes (2010) does not consider; I turn to this literature below.

The literature examines the effect of firm-level governance quality on foreign

institutional investment, without taking into account the effect of the home country’s

governance quality. The definition of ‘good governance’ varies between studies.18 Kang

and Stulz (1997), Ahearne et al. (2004) and Aggarwal et al. (2005) use the ADR

(American Depository Receipt) issuance as a proxy for strong shareholder rights, or a

reduction in asymmetric information, for foreign firms and find that firms with ADR

issuance have high levels of US ownership. Leuz et al. (2009) also conclude that US

institutional investors invest less in foreign stocks with high information asymmetry and

high monitoring costs. Furthermore, Giannetti and Simonov (2006) show, for the

Swedish market, that foreigners invest less in firms with high levels of outside investor

expropriation.19

A recent study by Kim et al. (2011) finds that if an investor’s country has a low level of

disparity between ownership and control, the investor does not invest in high-disparity

firms in the Korean market. My study is different to that of Kim et al. (2011) in the

following ways: First, Kim et al. (2011) use the disparity between control and

ownership as their proxy for corporate governance risk, hence concentrating on the risk

of tunnelling by controlling shareholders. I capture the country-level governance quality

using the World Bank KKM (Kaufmann et al., 2008) indicators. These six key

18 McKinsey and Company (2002) report the following ranking in the investors’ governance priorities: strong shareholder rights (for 33% of investors), good accounting standards (for 32% of investors), more effective disclosure (for 31% of investors), and stronger enforcement (for 27% of investors). 19 Other studies examine the effect of firm-level accounting variables on institutional investment. For example, Dahlquist and Robertsson (2001), Kang and Stulz (1997), Gompers and Metrick (2001), Falkenstein (1996), Ferreira and Matos (2008) and Khurshed et al. (2011).

37

indicators provide a more holistic representation of a country’s governance level.20

Second, Kim et al. examine the behaviour of all investors, retail and institutional. I

concentrate on institutional investors since they are informed, highly-skilled traders, and

therefore my conjectures on their investment preferences, based on the governance

quality at home and abroad (the processing of which information requires expert

knowledge and tools), appear more robust. Third, Kim et al. examine the investment

preferences of foreign investors in an emerging market, i.e., Korea; it is unclear what

the foreign investors’ perceptions of the overall governance quality of Korea are (thus it

is unclear whether this factor affects the heterogeneity of foreign investors investing in

this country). However, I study foreign investment in the US, which undoubtedly has a

strong corporate governance system, thus allowing the maximum possible degree of

investor heterogeneity. Finally, my research design helps us to reconcile the results

reported in Kim et al. (2011) with the conflicting evidence provided by prior studies.

2.3. Hypotheses

Domestic investors prefer to invest more in their local market than abroad. This ‘home

bias puzzle’ (Lewis, 1999) is mainly attributed to the higher information asymmetry

costs associated with investing abroad. Given that domestic investors have more

information about the domestic economy, foreign investors suffer from adverse

selection problems and require a premium in order to compete with domestic investors.

However, there is a considerable and growing amount of foreign institutional

investment in the United States (see Table 2.1). This indicates that the US market offers

20

Beltratti et al. (2009) and Caprio et al. (2011) use the KKM measures as proxies for country-level governance quality.

38

investment opportunities to foreign investors that can give them the required premium

to compensate them for their adverse selection problems. Given the recent high levels of

foreign investment in the US, I explore the factors that attract high level of foreign

institutional investment to the US market. I argue that the level of investor protection is

one of the most important factors in drawing foreign investment to the United States.

Investor protection is defined as “...the extent of the laws that protect investors’ rights

and the strength of the legal institutions that facilitate law enforcement” (Defond and

Hung, 2004; p. 269). The level of investor protection depends on the governance quality

of a country. It is well-documented in the literature that investors prefer to invest in

countries with high-quality governance, and thus a high level of investor protection, for

e.g. Aggarwal et al. (2005) and Leuz et al. (2009). Even if a firm has good internal

corporate governance, if it is domiciled in a country with weak governance quality, it

benefits less from the domestic capital markets. It cannot reduce its cost of capital to the

level it would obtain if it was domiciled in a country with good governance (Doidge et

al., 2007). Firms cannot compensate for the absence of a high-quality governance

environment. They can improve the quality of their internal corporate governance

quality but this cannot substitute for the quality of legal rules (Klapper and Love, 2004).

In line with this argument, I predict that one of the most important determinants of

institutional investment is the quality of the governance environment. I expect the level

of governance at home to affect the level of institutional investment abroad, as investors

try to identify better investment opportunities in a globalised environment.

The good country bias theory of Giannetti and Koskinen (2010) helps me to build my

first hypothesis. I argue that institutional investors domiciled in countries with low

levels of investor protection, are inclined to seek investment opportunities in foreign

39