think secular, act cyclical: the pragmatist's guide to water....

TRANSCRIPT

Think Secular, Act Cyclical: The Pragmatist's Guide to Water.

INVESTMENT CONCLUSION:

While catchy hyperbolic sound bites such as "The Oil of the 21st Century" have become de rigueur among mediapundits, the long-term "themes" surrounding water (water scarcity, water quality, and aging infrastructure) actually havelittle bearing on stock performance over the shorter 1-5 year horizon considered by most investors. Sure, these themesabsolutely have merit, and over the long-term allocating a portion of assets to the space will likely boost returns, but thereality is that water equipment and technology companies are for the most part cyclical businesses exhibiting volatiledemand patterns and susceptible company-specific issues (after all, oil was the oil of the 20th century, but that didn't stopTexaco from filing the then-largest bankruptcy in U.S. history in 1987). With this in mind, we believe the most practicalmeans of approaching the space is to acknowledge the compelling themes underlying the sector and screen for companiespositioned to benefit from them over time, but to base tactical investment decisions on a disciplined assessment of theunique cyclical realities facing each company. We base our tactical stock calls in large part on our framework of the FourDemand Channels: Municipal, Industrial, Construction, and Agriculture. In this deep-dive primer, we examine each ofthese key demand channels from the ground up, and also outline the adjacent regulated water utility space.

KEY POINTS:

• The "Big Three" Themes. Here are the water themes in a nutshell: (a) populations are migrating to arid regions(think Phoenix), and this is straining water resources in some areas - a.k.a. "Water Scarcity"; (b) the continuedproliferation of industrial and commercial activity creates pollution issues, requiring more stringent regulations toensure safe drinking water - a.k.a. "Water Quality"; and (c) established population centers (think NYC, Philadelphia)must continually invest to keep water systems in working order - a.k.a. "Aging Infrastructure".

• Be wary of blind theme investing. The paradox of investing in the water space is that while each of these keythemes has merit and will drive commercial opportunities, it is impossible to quantify and/or forecast the impact ofthese issues on demand even under relatively extended investment time horizons of 5+ years. As a result, we believethese themes are useful as a backdrop for thinking about the long-term opportunities on the horizon, but in terms oftactical stock picking they are useless at best and dangerous at worst (we've seen many victims, including ourselvesat times, take the thematic bait only to be caught off guard by the cyclical realities of the business).

• The Four Demand Channels: The path to alpha generation. Among the least appreciated aspects of industrialsinvesting is that in mature industries (unlike, say, technology or healthcare), major shifts in market share big enoughto drive stock calls are extremely rare. As a result, scarce time resources are best spent divining whether the pie itselfwill expand or contract (and by how much) rather than focusing on how the pie will be divvied up. Our demandchannel framework drives our research process, with the four channels being: Municipal (city Water & WWauthorities), Industrial (water-intensive industries such as energy, bio-pharma, and food & beverage), Construction(water infrastructure for use in residential and commercial structures), and Agriculture (i.e. irrigation).

• A guide to tactical investing in the water space. This primer is designed as a guide and desk reference for investorslooking at the water space, laying out the fundamental factors driving each of the four demand channels anddiscussing the key indicators we monitor to gauge the trajectory of demand. In the end, we believe that the vastmajority of stock performance in the water sector can be ascribed to directional trends in the four demand channels,and that this is where investors seeking to generate alpha in the space should focus their attention.

Ryan M. Connors 215.665.1359

Kenneth J. Dorell 215.665.6439

[email protected] & Agriculture

November 13, 2013

Equity Research

Industry Report

Research Analyst Certifications and Important Disclosuresare on page 65 of this report

Introduction to the Four Key Demand Channels

Secular themes supply the long-term investment rational within the subsets of the broader water industry, yet the

cyclical tendencies within each end-market make appreciating the demand determinants vital to the investment

process. As such, our analysis is structured into the four key demand channels of municipal, industrial, construction,

and agriculture, with the fifth section dedicated to the investor-owned water utility industry.

Municipal: Capital expenditures dictate growth opportunity. The budgets of municipalities are divided

between operational expenditures and capital expenditures, with the latter representing the market opportunity for

water infrastructure companies as capital spending represents incremental spending on water product upgrades

ranging from pipe, pump, and meters to the construction of entire plants. With an estimated size of $31.5 billion in

2012 (measured by U.S. Utility CapEx), the highly fragmented market is served by a variety of companies that offer

products spanning from pumps (supplied by companies like Gorman-Rupp [GRC-Buy]) to advanced infrastructure

diagnostics systems (offered by Mueller Water Products [MWA–Buy]).

Industrial: Water treatment regulations & conservation efforts provide recurring demand. Expected to grow

at an annual compounded rate of 6% through 2016, the industrial water equipment market is expanding due in large

part to two secular trends: water scarcity and water quality. With tightened regulations and a renewed focus on water

efficiency, companies are taking a proactive approach to ensure compliance with increasingly stringent regulations

governing both water usage and effluent quality. Indeed, secular drivers provide a longer-term tailwind, yet

investment in water products is largely determined by the investment cycle of each relevant industry. The industrial

demand channel exhibits a relatively high degree of correlation with the broader industrial economy, and as a result,

trends in capacity utilization, industrial production, and industrial capital investment exert a significant influence on

the trajectory of demand for relevant water products.

Construction: Residential and non-res. building erection necessitates water infrastructure. In contrast to the

―megatrend‖ growth stories in the industrial, agriculture, and municipal end markets, the construction market for

water products is more cyclical than its secular counterparts. Driven predominately by macroeconomic factors,

including financing availability, income levels and general consumer outlook, the construction market is split

between two segments: residential and nonresidential. Indeed, every structure includes some degree of water

infrastructure, but there are certain key structures that are highly water intensive. For instance, the full service

nature of a household provides a swift tailwind for plumbing products, as do commercial structures such as lodging

and hospitals. These buildings amplify many of the residential uses for water to mass scale, resulting in extremely

water intensive operations that require complex and reliable systems.

Agriculture: Industry-best practices drive irrigation adoption/applications on the farmstead. The most

influential (and direct) water end-market in agriculture belongs to irrigation, yet the application of precision

agriculture and new, more efficient farm machinery also aids in the movement to reduce water consumption. In

order to anticipate demand trends in these markets, we follow a number of different metrics that amalgamate to

convey a general direction of the ag demand channel: net farm income, farmland values, corn prices, the corn

balance sheet, and farm debt. Shifts in the market conditions typically constitute commensurate shifts in the

performance of the ag companies, though certain conditions may supply different conclusions for each product

offering.

See pages 3-4 for a detailed Table of Contents providing easy reference to the contents of this report.

o Sidenote: For those viewing this document electronically, clicking the desired title on the table of

contents will direct you to the section referenced within the document.

- 2 -

Janney Montgomery Scott Equity Research: Water & Agriculture

Table of Contents

Municipal Demand Channel: An Overview ............................................................................................. 5

Municipal Demand Channel: The Market Opportunity ........................................................................... 6

Focus Issue #1: Pipe Replacement Estimates Out of Touch with ―Urban Reality‖ ......................... 7

Municipal Demand Channel: Growth Dynamics ..................................................................................... 8

Key Upcoming Industry Events ................................................................................................................ 9

Focus Issue #2: Bottled Water Consumption Provides Homes with ―Second Line‖ ..................... 10

Municipal Demand Channel: Key Macroeconomic Indicators ............................................................... 11

Municipal Demand Channel: Sub-sectors & Key Players ...................................................................... 14

Focus Issue #3: The Role of Water Metering in Driving Conservation ........................................ 15

Municipal Demand Channel: Key Players Comparable Analysis .......................................................... 16

Industrial Demand Channel: An Overview ............................................................................................ 17

Industrial Demand Channel: The Market Opportunity ........................................................................... 18

Focus Issue #4: ―Virtual Water‖ – A Holistic Measure of Water Consumption ........................... 19

Industrial Demand Channel: Growth Dynamics ..................................................................................... 21

Focus Issue #5: The Water/Energy Nexus ..................................................................................... 22

Industrial Demand Channel: Key Macro Indicators ............................................................................... 25

Industrial Demand Channel: Subsectors and Key Players in Each ......................................................... 28

Focus Issue #6: Water Treatment Stokes Conservation ................................................................. 29

Industrial Demand Channel: Key Players Comparable Analysis ........................................................... 30

Construction Demand Channel: An Overview ...................................................................................... 31

Construction Demand Channel: Market Opportunity ............................................................................. 32

Construction Demand Channel: Residential Growth Dynamics ............................................................. 33

Construction Demand Channel: Nonresidential Growth Dynamics ....................................................... 34

Construction Demand Channel: Key Indicators ..................................................................................... 35

Commercial Demand Channel: Subsectors and Key Players in Residential Market .............................. 39

Construction Demand Channel: Subsectors and Key Players in Nonresidential Market ....................... 40

Construction Demand Channel: Key Players Comparable Analysis ...................................................... 40

Agriculture Demand Channel: Irrigation Overview ............................................................................. 42

Agriculture Demand Channel: Irrigation Market Opportunity ............................................................... 43

Focus Issue #7: Precision Ag Adoption in Early Stages (Even in Developed Countries) ............. 44

Agriculture Demand Channel: Growth Dynamics .................................................................................. 45

- 3 -

Janney Montgomery Scott Equity Research: Water & Agriculture

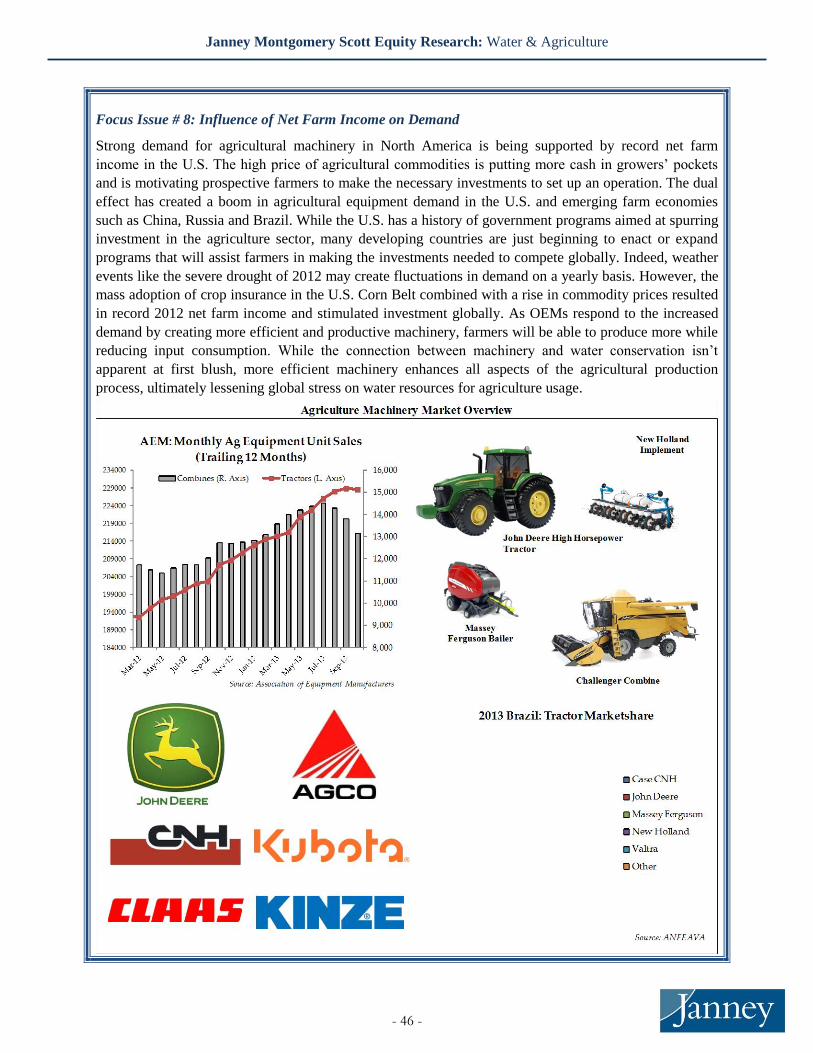

Focus Issue # 8: Influence of Net Farm Income on Demand ......................................................... 46

Agriculture Demand Channel: Key Indicators ........................................................................................ 47

Agriculture Demand Channel: Irrigation Key Players and Product Offerings ....................................... 50

Agriculture Demand Channel: Key Players Comparable Analysis ........................................................ 51

Regulated Water Utilities: An Overview ............................................................................................... 52

Regulated Water Utilities: Market Opportunity ...................................................................................... 53

Regulated Water Utilities: Growth Dynamics ........................................................................................ 54

Regulated Water Utilities: Regulatory Climate Indicator .............................................................. 55

Regulated Water Utilities: Key Players .................................................................................................. 58

Appendix .................................................................................................................................................... 59

Analyst Disclosures………………………………………………………………………………………. 65

- 4 -

Janney Montgomery Scott Equity Research: Water & Agriculture

Municipal Demand Channel: An Overview

A large portion of the play on water infrastructure companies is their exposure to municipal investment,

which is susceptible to numerous influences that drive the demand of water products. The budgets of

water utilities are divided between operational expenditures and capital expenditures, with the latter

representing the market opportunity for water infrastructure companies as capital spending represents the

incremental spending on water product upgrades ranging from pipe, pump, and meters to the construction

of entire plants. With an estimated size of $31.5 billion in 2012 (measured by U.S. Utility CapEx), the

highly fragmented market is served by a variety of

companies that offer products spanning from

pumps (supplied by companies like Gorman-Rupp

[GRC-Buy]) to advanced infrastructure diagnostics

systems (offered by Mueller Water Products

[MWA–Buy]). Forecasted by Global Water

Intelligence to reach a size of $46.4 billion by

2016, utility capital expenditures are expected to

expand at a 10% clip from 2012-2016, with

drinking water and wastewater capital expenditures

operating at a projected CAGR of 11.5% and 9.4%

over that time, respectively.1

The deterioration of water infrastructure in the

United States represents the primary growth driver

for water products companies, yet, as 84% of

drinking water systems (and 98% of wastewater

systems) in the United States are publicly-operated,

the financial condition of municipal governments

plays a key role in determining the trajectory of

demand in the short-term. As a result, economic

indicators that track bond issuance, hiring, pricing,

and tax collection trends of municipalities are

useful in assessing the likely trajectory of spending.

While water utilities are notoriously methodical in

their operational and investment trends, there is a

definite correlation between economic prosperity

and increased utility capital expenditures as

housing construction translates into increased

property tax revenue, a key funding mechanism for local municipalities (~80% of local tax revenue).

This influence in spending results in cyclicality for companies that serve the municipal sector, evidenced

in the sharp downturn of many companies exposed to municipal spending in 2008 (see: Badger Meter

[BMI-Neutral] or Xylem [XYL-BUY]). While Badger and Franklin Electric (FELE-NR) represent two

subsectors of the municipal market (Metering and Pumps), the sector is also served by engineering and

construction, water filtration, piping and storage, and infrastructure diagnostics firms that provide

products and services over the full lifecycle of municipal water infrastructure projects.

1 Water Market USA 2011. Oxford, United Kingdom: American Water Intelligence, 2011. Print.

New Water Network

13%

Water Network

Rehab

36%

New Water Treatment

Plant

5%

Water Treatment

Plant

Upgrades23%

New Water Resources

23%

Utility Water CapEx: 2013E

Source: AWI

Size: $15.3 bln

New Wastewater

Network

49%

Wastewater Network

Rehab

9%

New Wastewater Treatment

Plant37%

Related Assets

5%

Utility Wastewater CapEx: 2013E

Source: AWI

Size: $19.6 bln

- 5 -

Janney Montgomery Scott Equity Research: Water & Agriculture

Municipal Demand Channel: The Market Opportunity

Water infrastructure in the United States is

experiencing a prolonged deterioration that has

accelerated throughout the past two decades, with

renovations being deferred in many cases as a

result of trimmed budgets. Aging water and sewer

infrastructure has become so dire that it was cited

as the most important industry issue by water

utilities, above managing capital costs and funding

availability in a report by industry consultant Black

and Veatch. With macro data suggesting a rebound

is likely (seen through improvements in bond

issuance, municipal water pricing and record

property tax receipts) and pent-up projects being

unleashed, investment in some key areas of water

infrastructure is expected to increase. Alternately,

some areas of aging infrastructure are unlikely to

see ―in-kind‖ replacement as demographics shift

and consumer preference continues to shift toward

alternative delivery methods (see pages 7 & 10).

Estimates on the cost of bringing the United States‘

water infrastructure up to date within the next 20

years range from $335 billion to $1 trillion, with

the EPA estimating a cost of $384 billion to

upgrade U.S drinking water infrastructure in a

recent study. While we are somewhat skeptical of

the aging infrastructure theme, the reduced

spending in recent years by municipalities

tightening their belts has resulted in pent-up

demand for structural upgrades that we expect will

result in heightened project activity.

Distrib

65%

Treatment

19%

Storage

10%Source 5%

Other 1%

Water Infrastructure Upgrade Needs by

Function

Source: EPA

$0m

$5,000m

$10,000m

$15,000m

$20,000m

$25,000m

$30,000m

2007 2008 2009 2010 2011 2012 2013E 2014E 2015E 2016E

US Utility Capital Expenditure Profile

Utility Water Capex Utility Wastewater CAPEX

Source: American Water Intelligence

1990 2000 2005 2009 2013

Drinking Water Wastewater

B-

C

DD+

D- D-

A Deteriorating Report Card:

ASCE Grades U.S. Water Infrastructure

Source: ASCE

D- D-

D D

Major investments are needed to shore-up U.S. water

infrastructure. At 7% per year, water tariffs are growing

faster in North America than in any other region of the

world, a positive indicator that funding will be available.

- 6 -

Janney Montgomery Scott Equity Research: Water & Agriculture

Focus Issue #1: Pipe Replacement Estimates Out of Touch with “Urban Reality”

Officials in Youngstown, Ohio made

national news in 2006 by

acknowledging that the city was

unlikely to rebound from decades of

steep population loss, embarking on a

plan to deliberately downsize all aspects

of the city. Essentially, Youngstown‘s

still-unfolding plan (an example of what

urban planners have dubbed the

―Shrinking Cities‖ movement) boils

down to managing decline by

concentrating population in resilient

neighborhoods and decommissioning

sections of the city that are deemed to

have crossed the line of no return on the

vicious cycle of population loss, blight,

and crime. With the EPA and other

groups presuming full renovation of

infrastructure in their estimates, Youngstown‘s final step of razing whole blocks of abandoned homes,

thus eliminating the need for water mains there, leads to likely over-projections of needed investment in

similar cities. A Few cities are following Youngstown‘s lead, and with 22% of water main mileage within

declining urban populations and tightened municipal budgets (in addition to heightened public scrutiny on

overspending), other cities are likely to take similar approaches.

A reasonable counterpoint to this argument is that migration patterns will create demand in the suburbs

and Sun Belt cities that are gaining population (driving infrastructure demand). Unfortunately, while this

is true in the long-term, these areas were

developed so aggressively during the

housing boom that there is now

significantly underutilized infrastructure.

While strides towards reducing the housing

glut are being taken, a prolonged hangover

period for basic water infrastructure

demand is still impacting these areas,

causing the pipe market in particular to

meaningfully lag housing starts on the way

back up. In fact, juxtaposing the housing

overbuild in the suburbs/Sun Belt against

continued urban decline in the Rust Belt,

one way of looking at the issue is that a

considerable portion of the necessary water

infrastructure spending already took place –

in the form of water distribution networks

serving new housing developments.

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

$200

$250

$300

$350

$400

$450

$500

$550

$600

$650

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

U.S. Pipe Revenue (L, Bar) vs. U.S. Housing Starts (R, Line)

Figures in millions Source: Mueller Water Co; U.S. Census Bureau

4%

-26% -26%

92%

-61%

-35%

-57% -63%

-25% -23%

NYC

Ch

icag

o

Ph

ila.

L.A

.

Det

roit

Bal

t.

Cle

ve.

St. L

ou

is

Was

h.

Bo

sto

n

The 10 LargestU.S. Cities in 1950:

Pop. Change: 1950-2010

Source: U.S. Census Bureau

- 7 -

Janney Montgomery Scott Equity Research: Water & Agriculture

Municipal Demand Channel: Growth Dynamics

The growth profile of municipal spending

must be dissected in disparate ways as it is

subject to both secular and cyclical trends.

Cyclical. Municipal spending is subject to

macroeconomic conditions since it derives

much of its funding from taxes. With

property tax, sales receipts, and income tax

representing 91% of local tax revenue,

municipalities are exposed to trends in

housing (property tax), unemployment and

nonfarm payrolls (income tax) and

consumer expenditures (general sales

receipts). In the case of water infrastructure

spending, funding is principally derived

from rates charged for water consumption, which steadies the amount of spending on operational

expenditures. However, even water consumption revenue benefits from healthy macro conditions as

customer growth is driven by housing construction and commercial/industrial usage is cyclical.

Secular. While macro conditions certainly influence municipal spending (recent trends confirm this),

conventional wisdom holds that the poor condition of water infrastructure throughout the country

provides a significant long-term opportunity for companies serving the municipal market. While we

recognize this (citied in earlier estimates of water infrastructure investment needs), we believe that there

are also prominent trends that dilute the magnitude of water infrastructure needs in the U.S., most notably

the shift in favor towards bottled drinking water and shrinking cities phenomenon. Nevertheless, external

to the water infrastructure argument there remains compelling industry dynamics that present growth

opportunities for those selling into the water municipal channel. A focus on water quality and

conservation is driving demand for products ranging from advanced reverse osmosis treatment facilities

to meters fitted with AMI technology that allows for

enhanced leak detection. As consumers become

more cognizant of their water consumption and

water quality and utilities strive towards pressure

optimization of water systems to reduce non-revenue

water, the market for higher-end products that

expand beyond the basic needs of water distribution

and treatment is gaining traction rapidly.

Additionally, from a timing perspective, companies

servicing water utilities exhibit smoother returns

than those selling to industries like electric utilities,

as water projects are of much lesser size than that of

electric utilities, which leads to a reduced reliance

on large projects and a lower degree of lumpiness

for companies selling into the water utility sector.

Property Tax78%

General Sales/ Gross

Receipts

8%

Individual Income

4%

Corp Income1%

Other9%

Local Tax Revenue Distribution

Source: U.S. Census Bureau

Pipes36%

Pumps23%

Valves6%

Meters2%

Control/ Chemical

feed

systems1%

Filtration/ Treatment

22%

Other10%

Utility Water/WW Utility Market by

Equipment Type: 2013E

Source: AWI

- 8 -

Janney Montgomery Scott Equity Research: Water & Agriculture

Key Upcoming Industry Events

Water Quality Association Aquatec (WQA Aquatec)

Description:

Website: www.wqa-aquatec.com

Upcoming

Conferences:

American Water Works Assocation Annual Conference Exhibition (AWWA ACE)

Description:

Website: www.awwa.org

Upcoming

Conferences:

2014 AWWA ACE

Boston, Massachusetts

June 8th-12th, 2014

2016 AWWA ACE

Chicago, Illinois

June 12th-15th, 2016

2018 AWWA ACE

Las Vegas, NV

June 11th-15th, 2018

2015 AWWA ACE

Anaheim, CA, USA

June 7th-11th, 2015

2017 AWWA ACE

Philadelphia, Pennsylvania

June 11th-14th, 2017

Water Environment Federations Technical Exhibition Conference (WEFTEC)

Description:

Website: www.weftec.org

Upcoming

Conferences:

87th Annual WEFTEC

New Orleans Morial

Convention Center

New Orleans, LA

October 18th-22nd, 2014

WQA is “a one stop event that connects technologies, know-how, education, training, networking, and

business opportunities to multiple water industries”. The conference provides insight into the opportunities

and market conditions in the residential, commercial, and industrial end-markets for water products.

American Water Works Assocation is an organization boasting 50,000 members worldwide, including the

majority of the relevant U.S. water infrastructure companies. The Association's conference is designed to

introduce new trends, technology, and opportunities in the space as well as serving as a platform to discuss

recent ramifications from shifts in the legislative lanscape.

WEFTEC is the biggest meeting of its kind in North America and offers thousands of water quality

professionals from around the world the best water quality education and traning days available. It also

provides a water quality exhibition that provides access to the industry's cutting edge technology.

Key Water Industry Events

2014 WQA Aquatec

Orange County Convention Center

West Building, West Hall B

Orlando, Florida

March 18th-21st, 2014

- 9 -

Janney Montgomery Scott Equity Research: Water & Agriculture

Focus Issue #2: Bottled Water Consumption Provides Homes with “Second Line”

To understand why the inflection point in water

infrastructure investment has stubbornly failed

to realize, it helps to first consider a related

industry topic – the notion of a ―dual pipe‖ water

distribution system. Ingested water represents a

relatively small portion of household water

consumption (less than 3%), yet under a single-

pipe system, all other household applications

must utilize this expensive water. The solution,

say ―dual-pipe‖ advocates, is to have one line

bring top-quality drinking water into the home,

and another bring ―gray water‖ (water treated,

but to a lesser standard) for non-potable

applications. The dual pipe idea makes sense

from a water quality perspective (it makes no

sense to flush toilets with potable water), but

suffers from a fatal, insurmountable flaw: the

massive capital cost associated with such a system makes it a non-starter.

On the surface the solution to the aging infrastructure ―crisis‖ seems slow in materializing, yet the free

market is already dealing with the situation in real-time. An increasing number of people already

effectively operate under a virtual dual pipe system, with the existing drinking water service line

functioning as the ―gray water‖ pipe for non-potable applications and bottled water (or, increasingly,

point-of-use filtration systems) acting as the ―potable water‖ pipe. These alternatives have a strong

advantage in capital aversion, as bottled water utilizes existing civil (roads, rails) and commercial

(beverage industry bottling and distribution capabilities) infrastructure to bring drinking water to

consumers, while point-of-use filtration ―free rides‖ on the existing distribution network (inverting the

traditional utility model by transporting water first, treating it second). Equally important, bottled water

in particular leverages consumers‘ willingness to pay up for a source of drinking water they trust.

0% 20% 40% 60% 80% 100%

20-39

40-59

60+

Water Consumption by Age Group(Cups per day)

Tap Bottled

Source: USDA

Potable Water Landscape

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

5

5.5

6

6.5

7

7.5

8

8.5

9

9.5

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Bottled Water & Water Filter Sales

Bottled Water Consumption - Gallons in Billions (L-Axis)

Filters - Units in Thousands (R-Axis)

Filters 5-yr CAGR: 9.2%

Source: IRI & Bottled Water.org

Water Bottles 10-yr CAGR: 5.8%Bathing

23%

Toilets

28%

Lawn &

Pools 29%

Laundry

10%

Drink &

Cook 2% Other 9%

Water Usage by Application

Source: freedrinkingwater.com

- 10 -

Janney Montgomery Scott Equity Research: Water & Agriculture

Municipal Demand Channel: Key Macroeconomic Indicators

As referenced previously, there are several key economic indicators that help handicap near-term trends

in municipal infrastructure spending and investment. These include: U.S. residential housing starts and

permits, local tax receipts, municipal bond issuance, and the water & wastewater CPI.

U.S. Residential Building Permits. Residential permits offer a reliable forward-looking indicator of

trends in residential construction. As building permits expand and lead to increased construction, this

drives an incremental increase in homes needing water and wastewater services, increasing

municipalities‘ income. This increased income leads to heightened investment, a positive for companies

with exposure to the municipal demand channel. Housing Starts are also a relevant indicator to follow, but

lacks the forward looking benefit of permits.

Municipal Bond Issuance. Municipal bond flotation is a key driver of capital spending for local

government, particularly in the case of large-scale water projects. While the debate rages on whether or

not municipal bonds should continue to offer tax-free interest to investors (which is the asset class‘s most

attractive feature) it continues to be an enormous source of funding for munis. Key benefits of following

municipal issuance include (a) the forward-looking aspect of the data (capital raised in the municipal

bond market is typically deployed 1-2 years after issuance) and (b) the readily accessible nature of real-

time data.

Local Tax Receipts. Local tax revenues are the chief source of funding for municipalities, with stronger

tax receipts customarily translating into budget increases, which determine the level of both capital

investment and, to a lesser extent, operational expenditures in local water infrastructure. While water rates

make up the dominant share of water utility funding (~60% of municipal water utilities are structured as

financially independent ―enterprise funds‖), tax revenue is still a critical driver of spending trends over

the course of the economic cycle.

Municipal Water & Wastewater Pricing. The source of income directly attributable to water and

wastewater infrastructure investment is the charge for water and wastewater services. Many water

utilities continue to charge below cost for their service, yet increases in pricing move the industry toward

a more sustainable ―full cost‖ pricing model that will catalyze infrastructure investment in the

intermediate-term. In recent years, prices have been increasing at multiples of inflation in the broader

economy.

- 11 -

Janney Montgomery Scott Equity Research: Water & Agriculture

Municipal Demand Channel: Economic Indicators – Continued

0

500

1,000

1,500

2,000

2,500

U.S. Residential Permits (000s)

After reaching record heights in 2005 (permits are a leading indicator of the housing cycle), U.S.

Residential permits experienced an extended slump from 2006 to mid 2009. The recovery in permit

activity (though still well below 2005 levels) bodes well for water infrastructure companies that sell into

the residential construction industry.

Source: US Census Bureau

$200,000

$250,000

$300,000

$350,000

$400,000

$450,000

$500,000

$550,000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013E

U.S. Municipal Bond Issuancein Millions

Source: Bloomberg; JMS Estimates

Municipal bond issuance worked its way higher during the recession as local governments scrambled for funding amid lower tax receipts. This trend took a breather in 2011, but the "above average" borrowing resumed in 2012 as record-low interest rates enticed municipalities.

Lending has since normalized as economic conditions improve and interest rates work their way up. Overall, we view the increased funding from tax receipts as a preferred method of funding for munis.

- 12 -

Janney Montgomery Scott Equity Research: Water & Agriculture

Municipal Demand Channel: Economic Indicators – Continued

3%

4%

5%

6%

7%

Feb

-04

Jul-

04

De

c-04

May

-05

Oct

-05

Mar

-06

Au

g-06

Jan

-07

Jun

-07

No

v-07

Ap

r-08

Sep

-08

Feb

-09

Jul-

09

De

c-09

May

-10

Oct

-10

Mar

-11

Au

g-11

Jan

-12

Jun

-12

No

v-12

Ap

r-13

Sep

-13

Municipal Water & Wastewater Pricing (Year/Year Rate of Change)

Source: U.S. Bureau of Labor

Water pricing has been outpacing broader measures of inflation for years. While downward pressure on interest rates has the ability to

pressure water pricing, tariff growth still runs well above inflation levels even in such an environment, as utilities use rate increases as a method

for financing infrastructure and water sourcing needs.

$0

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

$700,000

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

Local Tax Collections(in millions)

Local Taxes

Property Taxes

Source: United States Census Bureau

Local tax collections have expanded over 150% in the past two decades, and although local tax revenue declined from 2009 to 2011,

collections have since rebounded to reach record levels in 2013.

- 13 -

Janney Montgomery Scott Equity Research: Water & Agriculture

Municipal Demand Channel: Sub-sectors & Key Players

The products and services offered in the municipal sector represent vital components at each stage of the

water treatment and distribution process, creating a set of complementary goods (as opposed to

substitutes per se). The supply of potable water is first made possible through engineering and

construction, during which firms like Stantec (TSX:STN–NR) work with municipalities in developing

water plants that treat and distribute raw source water to service the needs of the community. Water

treatment (filtration, purification, etc.) is involved in this process as well, as water utilities are required to

treat water to meet the potable standards outlined by the EPA in the Safe Water Drinking Act. With point-

of-use filtration and wastewater treatment becoming more mainstream, these products are also used at the

back end of the water distribution cycle. Mueller Water (MWA-Neutral) and its privately held peers

provide the distribution vehicle, as piping is laid underground for water mains and ancillary systems.

While pipes provide the vehicle for distributing water, pumps represent the engine, creating water

pressure to transport the water, with valves managing the flow. A multitude of companies operate in this

area, ranging from Gorman-Rupp (GRC-BUY) and Xylem (XYL-BUY) who service high-volume pump

needs to Watts (WTS-BUY) who extends its value offerings to those beyond the municipal system.

Water metering is where the transaction between the consumer and the utility is recognized, and it is

essential for the service provider to properly account for customer usage. There are numerous types of

meters available (PD, impeller, magnetic), but the area that is getting much notoriety and investment is in

the data transmission space, where there are two distinct groups: manual-read and automated (AMR).

AMR technology allows for accurate and timely consumption monitoring, as transmitters communicate

meter readings to the water utility through either walk-by or drive-by sensors, effectively eliminating the

need for manual meter checking. AMI transmission systems take this one step further, leveraging fixed-

communications systems that enable the utility to gather consumption data in house. The evolution of

AMI involves two-way communication (both to the utility and back to the customer), which allows

consumers to adjust their consumption through water-efficient ―best practices‖.

Product Description Companies

Transmission &

Distribution

Underground distribution systems that facilitate

water transportation. Storage primarily involves

reservoir construction.

FSTR, MWA,

NES, NWPX

Pumps/Valves

Primarily flow control devices that promote water

quality, conservation, and safety and are integral

components to water systems of any size or type.

GRC, FLS, IEX,

MWA, PNR, XYL

Engineering &

Construction

Provides consulting, engineering, program

management, construction management, and

technical services for water, natural resources,

environment, infrastructure and energy sectors.

AEC, LAYN, STN,

TTEK, URS

Metering

Flow measurement and control devices that apply

to various applications servicing commercial,

industrial and residential customers.

BMI, Elster*, ITRI,

MWA, ROP, SSNI

Infrastructure

Diagnostics

Services aging infrastructure in the form of water

systems for leak detection, water inefficiencies,

and pressure abnormalities.

MWA, PUR (TSX)

Filtration

Offers filtration materials, systems, and consumer

products that service water, air, food and beverage,

and industrial process streams.

AOS, CCC, PLL,

XYL

*Privately Held

Products & Services Offered to Municipal Customers

- 14 -

Janney Montgomery Scott Equity Research: Water & Agriculture

Focus Issue #3: The Role of Water Metering in Driving Conservation

A strong driver for water efficiency in addition to

minimizing treatment costs for utilities is water

metering. Currently, over a quarter of the water that

is used worldwide is non-revenue water, or the

difference between the water put into a distribution

system and the volume that is billed to customers.

The three types of non-revenue water are: physical

losses, commercial losses, and unbilled authorized

consumption. Physical losses represent the leakage

from all parts of the system and overflows at the

utility‘s storage tanks, typically derived from poor

management of plant operations. Commercial

losses are drawn from customers with meters under

registration, with losses resulting from meter errors or water theft. Unbilled authorized consumption is

water that is used for public goods (i.e. firefighting).

According to the World Bank, nearly 50 billion cubic meters of non-revenue water is used each year,

representing a $14.6 billion annual loss of treated water. While full scale introduction of water metering

would not capture the majority of this revenue, it would ultimately improve the efficiency of water

distribution by identifying systems with water loss in order to more acutely focus infrastructure

improvements. This translates into fewer costs borne by utilities (less non-rev water) for the purchase and

treatment of water and subsequently, lower rates for consumers who would no longer compensate utilities

for non-revenue water. Companies have been noticing the benefits of metering especially, with automated

meter reading technology growing from close to zero a decade ago to 33% today. This significant

improvement highlights the popularity of water metering solutions, but also shows that despite public

presumption of metering installations flattening out, there is still ample opportunity.

12%

21% 21%3%

9%14%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

Developed Countries Eurasia Developing

Countries

Global Non-Revenue Water Breakdown*

Physical Losses NRW Commercial Losses NRW

15%

30%

35%

*Percent of Water System Input Source: WHO, World Bank, Janney Captail Markets

- 15 -

Janney Montgomery Scott Equity Research: Water & Agriculture

Municipal Demand Channel: Key Players Comparable Analysis

Ticker PriceMarket

CapSales Ent. Value Fwd P/E

EV/

EBITDA

JMS

Analyst

Water

Exposure

Sourcing & Distribution

LB Foster Co. FSTR $43.75 $451.9 $582.2 $355.9 15.2x 6.8x NR Low

Northwest Pipe Co. NWPX $37.40 $353.4 $496.5 $431.8 24.9x 8.8x NR High

Nuverra Environmental Solutions, Inc. NES $1.46 $379.5 $600.8 $904.7 NM 13.2x NR Medium

Average 20.1x 9.6x

Pumps & Valves

Gorman-Rupp Co. GRC $39.43 $828.1 $388.7 $803.3 23.7x 15.3x Connors High

IDEX Corporation IEX $69.74 $5,657.2 $1,994.3 $6,041.9 21.2x 12.9x Knight Medium

Mueller Water Products, Inc. MWA $8.80 $1,392.5 $1,120.8 $1,869.7 26.5x 11.8x Connors High

Pentair Ltd. PNR $68.05 $13,564.7 $7,313.9 $16,020.2 17.9x 18.6x NR High

Watts Water Technologies, Inc. WTS $58.61 $2,068.9 $1,470.2 $2,150.0 21.3x 11.7x Connors High

Xylem Inc. XYL $33.94 $6,261.5 $3,773.0 $7,069.5 18.3x 12.4x Connors High

Average 21.5x 13.8x

Engineering & Construction

AECOM Technology Corporation ACM $28.96 $2,919.3 $8,153.5 $3,616.5 12.1x 7.7x NR Low

Layne Christensen Company LAYN $15.25 $299.2 $974.3 $393.9 NM 15.7x NR High

Stantec Inc. STN $67.26 $3,120.9 $1,773.8 $3,286.2 18.9x 12.8x NR Medium

Tetra Tech Inc. TTEK $26.42 $1,704.0 $2,029.5 $1,771.0 16.9x 14.3x NR High

Tutor Perini Corporation TPC $21.36 $1,027.7 $4,190.6 $1,675.2 9.3x 6.7x NR Low

Average 14.3x 11.4x

Metering

Arad Ltd. TASE:ARD $26.17 $647.2 $139.0 $649.8 0.0x 9.0x NR High

Badger Meter Inc. BMI $51.76 $744.2 $327.4 $804.7 24.0x 15.8x Connors High

Itron, Inc. ITRI $43.50 $1,703.0 $1,948.5 $2,002.6 15.6x 11.9x Connors Medium

Mueller Water Products, Inc. MWA $8.80 $1,392.5 $1,120.8 $1,869.7 26.5x 11.8x Connors High

Roper Industries Inc. ROP $125.63 $12,476.3 $3,158.9 $14,622.2 20.8x 14.6x NR Medium

Silver Spring Networks, Inc. SSNI $19.42 $915.3 $279.8 $773.6 28.0x NM NR Medium

Average 19.1x 12.6x

Infrastructure Diagnostics

Mueller Water Products, Inc. MWA $8.80 $1,392.5 $1,120.8 $1,869.7 27.5x 11.8x Connors High

Pure Technologies Ltd. TSX:PUR $6.42 $328.0 $59.1 $288.3 32.1x 24.7x NR High

Average 29.8x 18.3x

Filtration/Treatment

Calgon Carbon Corporation CCC $20.48 $1,118.3 $556.6 $1,136.9 21.1x 11.6x NR High

Pall Corporation PLL $81.87 $9,068.7 $2,648.1 $8,769.6 24.0x 15.3x Knight Low

Watts Water Technologies, Inc. WTS $58.61 $2,068.9 $1,470.2 $2,150.0 21.3x 11.7x Connors High

Xylem Inc. XYL $33.94 $6,261.5 $3,773.0 $7,069.5 18.3x 12.4x Connors High

Average 21.2x 12.7x

*Company Descriptions Located in Appendix Source: CapIQ, Company Documents

Municipal Demand Channel: Publicly Traded Company Comp Sheet

- 16 -

Janney Montgomery Scott Equity Research: Water & Agriculture

Industrial Demand Channel: An Overview

Expected to grow at an annual compounded rate of 6% through 2016, the industrial water equipment

market is expanding due in large part to two secular trends: water scarcity and water quality. With

tightened regulations and a renewed focus on water efficiency, companies are taking a proactive approach

to ensure compliance with increasingly stringent regulations governing both water usage and effluent

quality. Indeed, secular drivers provide a longer-term tailwind, yet investment in water products is largely

determined by the investment cycle of each relevant industry. The industrial demand channel exhibits a

relatively high degree of correlation with the broader industrial economy, and as a result, trends in

capacity utilization, industrial production, and industrial capital investment exert a significant influence

on the trajectory of demand for relevant water products.

Improving fundamentals in the U.S. manufacturing sector are augmenting the secular drivers by creating a

cyclical tailwind, with expanding industries such as hydraulic fracturing providing incremental demand

for water transmission and treatment equipment. With this noted, there can be significant shifts in the end

market conditions of the industrial sector, which makes it prudent to continually monitor the economic

trends emerging in the sector. The forward looking indicators that we follow include: the Architecture

Billings Index (ABI), U.S. Capacity Utilization and U.S. Industrial Production Index. The industrial

indicators provide insight into the investment trends in many of the largely cyclical and water dependent

industrial sectors, including the pulp and paper and mining industries. In addition, as the oil and gas

industry‘s water consumption expands (expected 24% 5-yr CAGR vs. 6% for all industrial markets), U.S.

construction spending on Energy and Manufacturing has become a vital metric to follow in projecting

demand for water equipment and technology.

Industrial Water Equipment Market Dynamics

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

$4,500

2007 2008 2009 2010 2011 2012E 2013E 2014E 2015E 2016E

Industrial Water & Wastewater Equipment Market

CAGR: 6%

Numbers in Milliions

Municipal WW

Treatment

Plants87%

Industrial Effluent

Discharge

13%

Wastewater Violations

Source: Public Interest Research Group; GWI/AWI

- 17 -

Janney Montgomery Scott Equity Research: Water & Agriculture

Industrial Demand Channel: The Market Opportunity

Agriculture consumes 70% of the world‘s water (with

the industrial sector using 22% globally), yet when

considering strictly high-income countries the

industrial sector leapfrogs into pole position,

comprising 59% of total water usage. With

globalization driving significant investment in

manufacturing capacity for developing economies, the

industrial sector is arguably the most important leg of

the water equipment growth story in the coming

decades. Indeed, since the United States already stands

as a high-income country it may seem that the market

opportunity for water equipment products is relatively

muted compared to its developing counterparts,

particularly considering its ―service-oriented‖

economy. However, the infusion of cheap energy has

reawakened the United States manufacturing sector,

opening up opportunities in the next few decades as

certain industries refocus on domestic production. In

addition, the country‘s stature as a developed country

enables it to focus on water quality and consumption

improvements amid this uptick, furthering its position

as a leader in driving improved water quality standards

in the industrial sector.

The $2.8 billion

industrial water

equipment market‘s

primary consumer is

the Pharmaceutical

industry ($520 million),

which finds water

particularly useful for a

number of applications

because of its unique

chemical properties.

While pharmaceutical

is expected to remain

the primary demand

channel for water

equipment in the industrial market, over the next five years certain industries are expected to eclipse

pharma‘s CAGR of 6%, including Oil & Gas (24%), Power (7%), and Chemicals (8%).

304

266

136

43

31

22

6

4

1

0 200 400

Russia

India

China

Global Average

USA

France

Germany

Japan

UK

Water Footprint per Unit Value Added(m

3/1,000 USD)

Source: Waterfootprint.com

Source: GWI/AWI

Industrial Water & Wastewater Treatment End Market: 2007 vs. 2016E

18%

14%

13%

11%7%

6%

5%

26%

2016E

Size: $3.8 bln

16%3%

12%

12%

11%9%

6%

31%

2007

Pharmaceutical

Oil & Gas

Food & Bev.

Power

Pulp/Paper

Electronics

Mining

Other

Size: $2.7 bln

- 18 -

Janney Montgomery Scott Equity Research: Water & Agriculture

Focus Issue #4: “Virtual Water” – A Holistic Measure of Water Consumption

The concept of ―Virtual Water‖ measures the volume of water required to produce goods and services,

with the term ―virtual‖ reflecting the fact that finished products contain little of the ―actual‖ water used in

its production. Much of the water efficiency discussion focuses on personal consumption (43,000

gallons/year), but this is minor relative to the nearly 700,000 gallons/year per capita required to enable

modern lifestyles. While academic literature on the concept of virtual water focuses on farming, which

accounts for about 70% of water consumption, the concept is also highly relevant for many industrial

companies, particularly as industry becomes a larger consumer of water. Indeed, many companies not

associated with the so-called ―water industry,‖ such as Dow Chemical (DOW-NR), International Paper

(IP-NR), Intel Corp. (INTC-NR) and U.S. Steel (X-NR), among others, rely upon trillions of gallons of

freshwater annually as a critical component of their everyday processes. With water scarcity and water

quality issues of growing concern worldwide, the business of helping companies minimize their virtual

water footprint should see consistent growth for many years to come.

Though discussions on water usage and conservation efforts often focus on residential consumption, the

concept of virtual water helps to illustrate the actual water usage patterns of modern society. Products

seemingly unrelated to the water industry in actuality are core to the rationale for investing in the water

sector, as the massive use of water highlights the criticality of enhancing water efficiency in these

everyday applications. In particular, companies whose products and services help farmers and industrial

customers use water as efficiently as possible (and to optimize their effluent water quality) should

continue to see a strong secular tailwind in the years ahead. This applies to a wide range of companies,

including those providing efficient irrigation systems (Lindsay Corporation-LNN, Valmont Industries-

VMI) and those working with industrial customers to optimize water usage patterns (Xylem-XYL). This

issue of water conservation is a vital component to the discussion going on today about a budding, water-

intensive activity to be discussed later: hydraulic fracturing.

ProductVirtual

Water Comments Product

Virtual

Water Comments

Egg 35 gall. Chicken feed production. Coffee (8 oz) 37 gall. 1,100 cups of water per cup.

Cotton T-Shirt 530 Cotton farming, processing. Hamburger 650 Raising livestock water intensive.

Bottle of Beer 20 Barley production, brewing. Loaf of Bread 170 10 gallons of water per slice.

Plastic (1 lb) 240Among most water intense

industries in water/sales dollar.Car 38,600 Metal, rubber, vinyl production.

Glass of Wine 32 Vineyards water intensive. Cheese (1 lb) 2,970 2.5 gall. of milk per lb of cheese.

Bag of Potato

Chips 50 Potato production. Milk (1 gal) 1,000 Dairy farming, processing.

Leather Shoes 2,100 Cattle ranching. Microchip 32 Many plants in arid regions.

Source: Hoekstra, Waterfootprint.org, Janney Montgomery Scott LLC Note: All virtual water content figures in gallons.

Virtual Water Content: Water Required to Produce Everyday Products

- 19 -

Janney Montgomery Scott Equity Research: Water & Agriculture

Focus Issue #4: “Virtual Water” – A Holistic Measure of Water Consumption – Cont’d

.

0.5

2

9

27

93

110

354

474

827

1,082

0 200 400 600 800 1,000 1,200

INTC

GM

XOM

NKE

EXC

X

BUD

IP

WLK

MCD

Water & the Income Statement: Gallons per Dollar of Sales

Source: Company Reports, waterfootprint.org

With a tremendous amount of "virtual water" embedded in

everyday items, water efficiency is increasingly relevant to

companies not typically associated with the "Water Sector."

McDonald's uses a whopping

1,082 gallons of virtual water to

generate $1 in revenue.

0

2,000

4,000

6,000

8,000

10,000

12,000

Japan China USA Brazil Australia Russia Italy

Average Virtual Water Content of Selected Products (yd3/ton)

Corn Wheat Soybeans Beef

Global

Average

The virtual water content of products varies greatly from place to place

as a result of differences in climate, farming techniques and land

quality. Due to the large amounts of time and feed required to raise

cattle, beef production requires relatively massive amounts of water.

14,410

27,700

27,500

22,400

22,200

20,275

17,25016,430

Source: waterfootprint.org

- 20 -

Janney Montgomery Scott Equity Research: Water & Agriculture

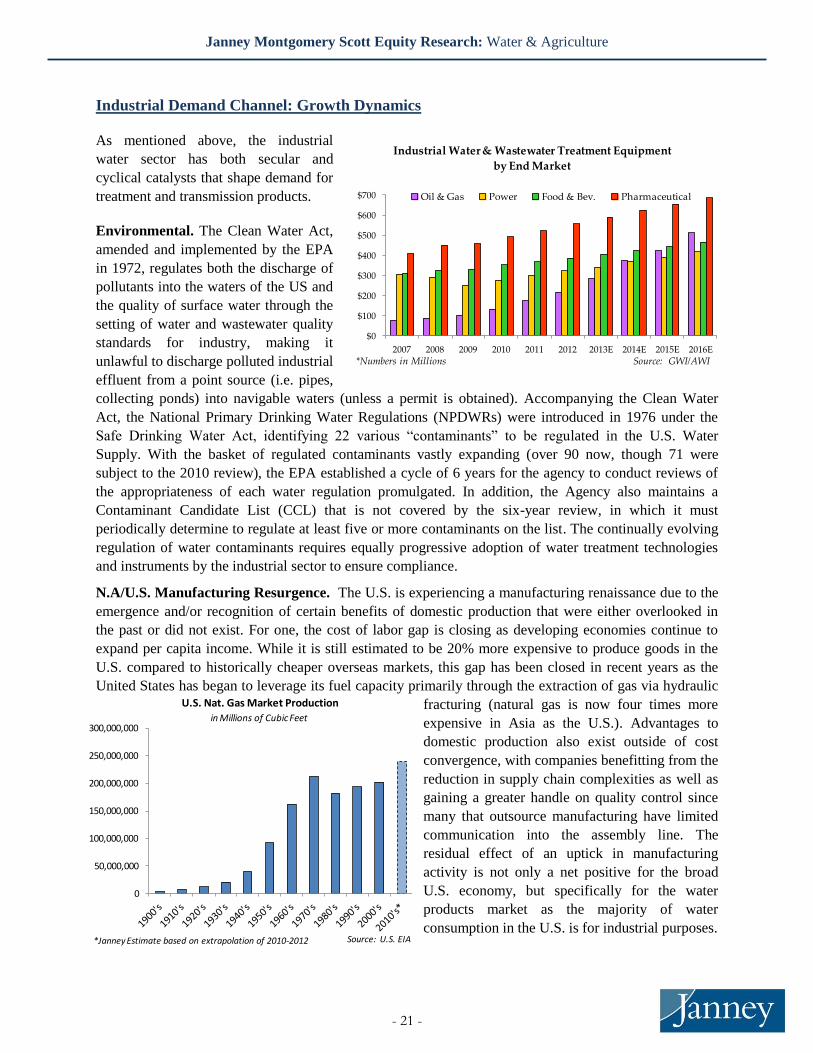

Industrial Demand Channel: Growth Dynamics

As mentioned above, the industrial

water sector has both secular and

cyclical catalysts that shape demand for

treatment and transmission products.

Environmental. The Clean Water Act,

amended and implemented by the EPA

in 1972, regulates both the discharge of

pollutants into the waters of the US and

the quality of surface water through the

setting of water and wastewater quality

standards for industry, making it

unlawful to discharge polluted industrial

effluent from a point source (i.e. pipes,

collecting ponds) into navigable waters (unless a permit is obtained). Accompanying the Clean Water

Act, the National Primary Drinking Water Regulations (NPDWRs) were introduced in 1976 under the

Safe Drinking Water Act, identifying 22 various ―contaminants‖ to be regulated in the U.S. Water

Supply. With the basket of regulated contaminants vastly expanding (over 90 now, though 71 were

subject to the 2010 review), the EPA established a cycle of 6 years for the agency to conduct reviews of

the appropriateness of each water regulation promulgated. In addition, the Agency also maintains a

Contaminant Candidate List (CCL) that is not covered by the six-year review, in which it must

periodically determine to regulate at least five or more contaminants on the list. The continually evolving

regulation of water contaminants requires equally progressive adoption of water treatment technologies

and instruments by the industrial sector to ensure compliance.

N.A/U.S. Manufacturing Resurgence. The U.S. is experiencing a manufacturing renaissance due to the

emergence and/or recognition of certain benefits of domestic production that were either overlooked in

the past or did not exist. For one, the cost of labor gap is closing as developing economies continue to

expand per capita income. While it is still estimated to be 20% more expensive to produce goods in the

U.S. compared to historically cheaper overseas markets, this gap has been closed in recent years as the

United States has began to leverage its fuel capacity primarily through the extraction of gas via hydraulic

fracturing (natural gas is now four times more

expensive in Asia as the U.S.). Advantages to

domestic production also exist outside of cost

convergence, with companies benefitting from the

reduction in supply chain complexities as well as

gaining a greater handle on quality control since

many that outsource manufacturing have limited

communication into the assembly line. The

residual effect of an uptick in manufacturing

activity is not only a net positive for the broad

U.S. economy, but specifically for the water

products market as the majority of water

consumption in the U.S. is for industrial purposes.

0

50,000,000

100,000,000

150,000,000

200,000,000

250,000,000

300,000,000

U.S. Nat. Gas Market Production

Source: U.S. EIA*Janney Estimate based on extrapolation of 2010-2012

in Millions of Cubic Feet

$0

$100

$200

$300

$400

$500

$600

$700

2007 2008 2009 2010 2011 2012 2013E 2014E 2015E 2016E

Industrial Water & Wastewater Treatment Equipment

by End Market

Oil & Gas Power Food & Bev. Pharmaceutical

Source: GWI/AWI*Numbers in Millions

- 21 -

Janney Montgomery Scott Equity Research: Water & Agriculture

Focus Issue #5: The Water/Energy Nexus

Water and energy have a codependent relationship, with the water industry needing energy to treat and

distribute water, and the energy industry needing water for everything from discovery to production and

refining. Representing 15% of the world‘s total water consumption (second only to the Agriculture

industry which requires an astounding 70%), the energy industry uses water for fuel extraction, refining

and processing, transporting and power generation, harboring a massive water equipment end market.

Energy Market Opportunity. The U.S. has long boasted the most formidable energy industry in the

world, yet the mass introduction of revolutionary drilling techniques to release ―trapped‖ oil and gas in

shale rock formations (i.e. horizontal drilling) that started in the late 1990s has taken it to new levels, with

the IEA projecting the U.S. to pass Saudi

Arabia as the largest oil producer by 2020

and become entirely energy self-reliant by

2035 (The U.S. is still the world‘s largest oil

consumer, after all). At the helm of this

transformation is America‘s transition to

natural gas, as the country‘s natural gas

potential has been estimated by the Potential

Gas Committee to be 2,384 trillion cubic feet,

which is double the estimate from ten years

ago and represents enough fuel to sustain the

U.S. economy for 110 years by itself.

As the principal fuel recovered from

hydraulic fracturing, natural gas now represents 26% of total gas consumption (vs. 17% in 1950),

representing 30% of electricity generation (vs. 18% in 1950).2 This presents an incremental opportunity

to water equipment companies as the U.S. energy industry

continues build out, and although the process water

requirement for shale gas is not massive, there is a need to

handle significant water flow as drilling brings about

produced water that must be treated (an expensive process).

In addition to the natural gas revolution is the move towards

ethanol, which is the second most water-intensive fuel type

without considering the amount of water required to produce

the underlying grains (the inclusion makes it larger than the

previously most consumptive fuel type by a factor of 10).3

With mandates set in place by the Federal government that

require 15 billion gallons of grain-based fuel per year, ethanol

production could expand even further behind efforts to raise

the 10% ethanol blends fuel requirement to 15%. Whether or

not Federal policies remain conducive to ethanol production is

yet to be seen, and while we concede that continued ethanol

production would signify sustained opportunity for water

2 "Annual Energy Review 2011." EIA.gov. U.S. Energy Information Administration, n.d. Web. 19 June 2013.

<www.eia.gov/totalenergy/data/annual/pd 3 Water Market USA 2011. Oxford, United Kingdom: American Water Intelligence, 2011. Print.

0

50

100

150

200

250

300

Water Consumption by Fuel Type(Gallons of Water/Million BTU)

Source: GWI/AWI

- 22 -

Janney Montgomery Scott Equity Research: Water & Agriculture

equipment, the benefit of U.S. energy independence alone remains indisputable and should provide

incremental opportunity to water treatment and distribution products regardless of the fuel composition.

Power Market Opportunity. The United States

consumes more electricity than the entire European

Union over the course of a year, or if you prefer, uses

more power than Russia, India, Japan, Canada and

Brazil combined.4 Thermoelectric power plants produce

89% of the United States‘ total energy, distinguishing

them as the primary users of water in the power market.

The industry‘s water footprint makes up 39% of U.S.

water withdrawals, though this only translates to 3.3%

of the U.S.‘s water consumption since much of that

water is returned to the water system from which it is

drawn. In determining the water consumption of

thermoelectric power generation, it is important to

consider the type of cooling technology implemented

since water efficiencies vary dramatically. An open-

loop cooling tower, or once-through, is sent through the system to condense the steam from the turbine

once, then returned to the original source of water about 20 degrees warmer.5 Despite net consumption

being low, the large water intake presents potential bottlenecks during drought conditions, while the

discharge of markedly warmer water carries negative environmental effects as well. Closed-loop cooling

has become the method of choice for recently constructed power plants as a result of these side effects.

The technology more efficiently uses the withdrawn water, which, although significantly increases a

plant‘s water consumption, translates into a smaller withdrawal footprint due to the recycling of cooling

water. Another alternative, although less popular, is dry cooling towers, which use air and turbines as the

cooling mechanism. While effectively eliminating water consumption, it does reduce plant efficiency due

to its reliance on ambient weather conditions (including humidity and temperature).6

4 "Central Intelligence Agency." The World Factbook. N.p., n.d. Web. 8 Nov. 2013.

<https://www.cia.gov/library/publications/the-world-factbook/rankorder/2233rank.html>. 5-6

Mielke, Erik, Laura Diaz Anadon, and Venkatesh Narayanamurti. "Water Consumption of Energy Resource

Extraction, Process and Conversion." Belfer Center for Science and International Affairs [Harvard Kennedy School]

Oct. 2010.

Tower TechnologySteam Turbine (coal,

gas,biomass)

Steam Turbine

(Nuclear)

Combined-

Cycle Turbine

IGCC

(coal)

Capital Cost of

Cooling Tech

Once-through 35,030 42,530 13,780 $19/kW

Closed-loop 480 830 260 389 $28/kW

Dry 30 30 30 $182/kW

Tower TechnologySteam Turbine (Coal,

Gas, Biomass)

Steam Turbine

(Nuclear)

Combined-

Cycle Turbine

IGCC

(coal)

Capital Cost of

Cooling Tech

Once-through 315 415 115 $19/kW

Closed-loop 405 575 195 369 $28/kW

Dry 15 15 15 $182/kW

Source: Electric Power Research Institute, Energy Technology Innovation Policy Research Group

Consumption (gal/MWh)

Withdrawals (gal/MWh)

Power Plant Cooling Towers Water Footprint

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

Annual Electricity ConsumptionBillions of MWH

Source: CIA World Factbook

- 23 -

Janney Montgomery Scott Equity Research: Water & Agriculture

Is Fracking Water Footprint Gradually Becoming a Thumbprint?

A combination of an abundant domestic supply and an increasing focus on low-emissions energy has

driven the EIA to project natural gas to comprise 50% of the total U.S. Gas supply by 2035. Hydraulic

fracturing technology is a popular method of extraction, unlocking natural gas through fracturing dense

shale rock formations. The fracturing of the shale rock is traditionally done with pressurized fluids

composed of at least 90% water. This provides significant opportunity for both local utilities and flow

control companies as one horizontal well in a shale formation requires 2-5 million gallons of water. After

the water is used it is then treated to remove contaminants, providing significant commercial

opportunities for water treatment companies at the end of the process as well. Indeed, fracking presents

significant opportunity for water utilities, such as Aqua America (WTR – Neutral) and American Water

(AWK – BUY), which both are engaged in frack-related water supply initiatives, but opponents fear

fracking will compromise water quality in neighboring communities. While the general concern for long-

term water quality is valid, some view its concern in fracking as exaggerated as commissioned studies

continue to represent inconclusive evidence as to the impacts of fracking on groundwater quality.

Post-fracking, millions of gallons of flowback (typically 20-50% of total water used) carries chemicals

used and collected in the fracking process that must be disposed of properly to avoid groundwater

contamination. Companies such as Nuverra (NUV-NR) provide services for the treatment and disposal of

this waste; however the popular method of dumping it in disposal wells has been linked to earthquakes in

Ohio. Waterless alternatives are gaining momentum as public outcries against the water footprint of

fracking grow louder (though hydrofracking remains by far the most prevalent method). Alternative

methods provide environmental benefits as well as economic, whereas Liquefied Propane Gas (LPG)

gel‘s unique advantage—developed by GASFRAC Energy Services (GFS-NR)—is that it reverts to vapor

while underground, which allows for 1) the propane‘s return to the surface in a recoverable form and 2)

the elimination of toxic flowback water. Nitrogen-based fracking fluids, such as Baker Hughes‘s

VaporFrac (BHI-NR), provide similar environmental benefits as nitrogen is simply released into the air

after the process, vastly reducing the cleanup of toxic flowback. Another method developed by Chimera

(CHMR-NR) uses helium, eliminating the need for heat or steam. While these techniques can carry a 50%

premium to conventional hyrdrofracking, those costs are mitigated by the savings from 75% reduced

truck traffic and highly reduced clean up costs. In addition, the alternative methods could skirt

moratoriums on fracking in states like New York who have blocked hydrofracking.

- 24 -

Janney Montgomery Scott Equity Research: Water & Agriculture

Industrial Demand Channel: Key Macro Indicators

Architecture Billings Index (ABI). The Architecture Billings Index is derived from a survey of

architectural firm principals and partners by the American Institute of Architects that tracks business

conditions the participants are facing (referred to as ―Work-on-the-boards‖). The ABI itself is a diffusion

index from this survey that uses a reading of ‗50‘ as neutral (i.e. neither expansion nor contraction).

While its predictive track record is debatable, the reading remains widely viewed as a leading economic

indicator of non-residential construction by about 9-12 months.

U.S. Capacity Utilization. The United States Federal Reserve publishes a monthly reading of the

industrial capacity utilization in the economy, expressed in a percent form. The reading indicates how

much ―slack‖ there is in the U.S. productive landscape, i.e. how much room there is for manufacturing

expansion without having to deploy capital expenditures to increase production. The reading is extremely

high-level, but does provide some indication of impending cap-ex cycles, which can drive demand for

water-related industrial infrastructure products.

U.S. Industrial Production Index. The Industrial Production Index is an economic indicator published

monthly by the Federal Reserve that measures the real output of manufacturing, mining, electric and gas

industries located within the United States. The index measures production relative to 2007, with the

average reading in 2007 assigned a ―100‖ value, and is constructed by over 300 individual series that are

comprised of market groups (products and materials) and industry groups (durable and nondurable

manufacturing, mining, etc.). Similar to capacity utilization, industrial production provides a gauge of

manufacturing activity that ultimately drives investment in industrial facilities.

U.S. Construction Spending on Power and Manufacturing. U.S. Construction Put in Place is a

monthly measure in millions of USD calculated by the U.S. Census Bureau aggregating both private and

public spending. The U.S. Private construction for Power and Manufacturing is of particular interest

given the industries‘ water dependency. The data sets‘ greatest flaw is that it is a lagging economic

indicator, but it does add to the mosaic of information on the critical industrial demand channel.

- 25 -

Janney Montgomery Scott Equity Research: Water & Agriculture

Industrial Demand Channel: Key Macro Indicators – Continued

25

30

35

40

45

50

55

60

65

Jan

-06

May

-06

Sep

-06

Jan

-07

May

-07

Sep

-07

Jan

-08

May

-08

Sep

-08

Jan

-09

May

-09

Sep

-09

Jan

-10

May

-10

Sep

-10

Jan

-11

May

-11

Sep

-11

Jan

-12

May

-12

Sep

-12

Jan

-13

May

-13

Sep

-13

Architectural Billings Index (ABI)

Source: The American Institute of Architects (AIA)

Contraction ↓

Source: The American Institute of Architects (AIA)

Expansion ↑

Commercial construction fell off dramatically during the recession, and the ABI reflected that,

posting 31 consecutive months of negative readings. While commercial construction has yet

to return to the U.S. in the fashion residential construction has, incrementally positive readings

bode well for non-residential markets.

65.0%

67.0%

69.0%

71.0%

73.0%

75.0%

77.0%

79.0%

81.0%

83.0%

Sep-02 Sep-03 Sep-04 Sep-05 Sep-06 Sep-07 Sep-08 Sep-09 Sep-10 Sep-11 Sep-12 Sep-13

Capacity Utilization

Source: U.S. Federal Reserve

Capacity Utilization fell off dramatically during the recession as a sharp reduction in demand left

companies operating well below their productive capacities. The U.S. has since rebounded off its July

2009 trough and continues to approach the 80% level that often spurs investment in new capacity.

- 26 -

Janney Montgomery Scott Equity Research: Water & Agriculture

Industrial Demand Channel: Key Macro Indicators – Continued

80

85

90

95

100

105

9/1/

2000

3/1

/20

01

9/1/

2001

3/1/

2002

9/1

/20

02

3/1/

2003

9/1/

2003

3/1

/20

04

9/1/

2004

3/1/

2005

9/1

/20

05

3/1/

2006

9/1/

2006

3/1

/20

07

9/1/

2007

3/1/

2008

9/1

/20

08

3/1/

2009

9/1/

2009

3/1

/20

10

9/1/

2010

3/1/

2011

9/1

/20

11

3/1

/20

12

9/1/

2012

3/1

/20

13

9/1

/20

13

Industrial Production (Indexed to 2007)

IndustrialProduction fell off dramatically due to the financial downturn in 2008-2009. Activity has

rebounded significantly since, reaching pre-recession levels as manufacturing strength has helped to drive

the U.S. economy back to prosperity.

Source: U.S. Federal Reserve

0

20,000

40,000

60,000

80,000

100,000

120,000

Ap

r-03

Au

g-03

De

c-03

Ap

r-04

Au

g-04

De

c-04

Ap

r-05

Au

g-05

De

c-05

Ap

r-06

Au

g-06

De

c-06

Ap

r-07

Au

g-07

De

c-07

Ap

r-08

Au

g-08

De

c-08

Ap

r-09

Au

g-09

De

c-09

Ap

r-10

Au

g-10

De

c-10

Ap

r-11

Au

g-11

De

c-11

Ap

r-12

Au

g-12

De

c-12

Ap

r-13

Au

g-13