there are many reasons to choose carrington mortgage...

TRANSCRIPT

Bank and/or Credit Union Cover Letter 20131021

There are many reasons to choose Carrington Mortgage Services, LLC (CMS) as your wholesale lending partner. We have a wide range of loan products, competitive pricing, and unmatched commitment to help our partners succeed.

To become approved with CMS you will need to complete the following steps:

• Complete the Bank and/or Credit Union Application • Execute the following documents:

o Anti-Money Laundering and Suspicious Activity Attestation o Anti-Steering/Safe Harbor Attestation o Fair Lending Attestation o Loan Fraud Statement o Compensation Agreement for Banks and/or Credit Union o Relationship Agreement for Banks and/or Credit Union o Pipeline Manger System Administrator Form o W-9, Request for Taxpayer Identification Number and Certification o Corporate Resolution

• Provide the following documents: o Loan Officer List o QC Audit Policy and Procedures

• When all required items are completed send them to: [email protected]

Please note that Carrington Mortgage Services, LLC (CMS) follows the requirements of the Dodd-Frank Act and the final rules issued by the Consumer Financial Protection Bureau (CFPB).

Once you are approved, Pipeline Manager Administrator credentials will be sent which will allow your selected Pipeline Manager Administrator to set-up users in your office. This will allow them to view real time loan status, updates and tracking.

Your Account Executive can assist you with this process and is happy to answer any questions that you may have.

We look forward to working with you!

Carrington Mortgage Services, LLC

BANK/CREDIT UNION

APPLICATION

1610 E. St Andrew Place, Suite B-150, Santa Ana, CA 92705 Page 1 of 2 Rev. 10/22/13

APPLICATION INFORMATION

Application Type: Conventional

FHA

VA

Account Executive:

COMPANY INFORMATION

Regulatory Entity’s Name:

Entity’s Name, dba:

Address:

Entity’s NMLS ID:

City:

FDIC/NCUA:

State:

Business Tax ID:

Zip:

State of Incorporation/Org:

Website address:

MERS ID:

Company Phone Number:

Parent Company:

Number of Employees:

CONTACT INFORMATION

First Name:

Last Name:

Title:

Phone:

Email:

INSURANCE AND BOND INFORMATION

Fidelity Bonds Carrier Name: Amount of Bond:

Expiration: Phone:

Applicant agrees to maintain a minimum Fidelity Bond of $300,000 while approved to submit loans? Yes No

State Surety Bonds Carrier Name: Amount of Bond:

Expiration: Phone:

Applicant agrees to maintain Surety Bonds in accordance with state regulations? Yes No

Error and Omissions Carrier Name: Policy Number:

Expiration: Policy Amount:

Phone Number:

Applicant agrees to maintain a minimum Fidelity and Error and Omissions coverage? Yes No

BANK/CREDIT UNION

APPLICATION

1610 E. St Andrew Place, Suite B-150, Santa Ana, CA 92705 Page 2 of 2 Rev. 10/22/13

DISCLOSURES

In the event that you answered yes to the Disclosure statements 1-10 an explanation must be provided.

Question Answer

1. Has your entity ever been named as a defendant in a lawsuit, been involved in any criminal proceedings or litigation in the past 7 years?

2. Have any officers ever been named as a defendant in a lawsuit, been involved in any criminal proceedings or litigation in the past 7 years?

3. Have any corporate officers ever been convicted of a crime?

4. Has your entity and/or principals or corporate officers, ever had a real estate or other professional license suspended, revoked or received any other disciplinary action from a regulatory agency?

5. Has any lender enforced or attempted to enforce the Hold Harmless or Repurchase clause of their correspondent or broker agreement with your company and/or principals or officers within the past 12 months?

6. Has your entity ever had a Mortgage Insurance Master Policy cancelled or suspended for any reason?

7. Has your entity ever had unfavorable findings with regard to mortgage operations, included in any audit examination or report by FHA, VA, FNMA, FHLMC or any regulatory, supervisory or investigating agency?

8. Has any officer, director, or principal of your entity ever been affiliated with any company business that was suspended by FHA, VA, FNMA or FHLMC?

9. Has there been a material change in your entity’s Board of Directors or Officers in the past 12 months?

10. Does applicant have a process in place to insure compliance with high cost and anti-predatory lending statues for all applicable federal, state and if necessary local laws?

11. Does applicant have written hiring policies and procedures for checking all employees, including management, involved in the origination of mortgage loans (including application through closing) against U.S. General Services Administration (GSA), Excluded Party List?

12. Does applicant have written hiring policies and procedures for checking all employees, including management, involved in the original of mortgage loans (including application through closing) against the HUD Limited Denial of Participation List (LDP)?

13. Does your entity use contract processing services?

If yes, please provide explanation:

14. Does your entity have an Anti-Money Laundering program in place?

15. Have you initiated or terminated any affiliate relationships in the past 12 months?

16. Does the entity follow the recommended quality control guidelines for responsible lending of either Fannie Mae or Freddie Mac?

17. Is your entity currently approved or sponsored to submit VA loans?

18. Is your entity currently approved or sponsored to submit FHA loans?

AFFILIATE RELATION

Question Answer

1. Do any controlling owners, directors, principals, or officers have a direct or indirect ownership in a Real Estate Sales company?

2. Do any controlling owners, directors, or officers have a direct or indirect ownership in an Appraisal company?

3. Do any controlling owners, directors, principals, or officers have a direct or indirect ownership in a Title Company/Settlement Agent/Escrow Company or Closing Attorney? If you answered yes, the Settlement Agency must be approved for closing.

4. Do any controlling owners, directors, principals, or officers have a direct or indirect ownership in a construction or Home Improvement company?

5. Do any controlling owners, directors, principals, or officers have a direct or indirect ownership in a Credit Repair company?

6. Do any controlling owners, directors, principals, or officers have a direct or indirect ownership in any other general affiliates?

ANTI-MONEY LAUNDERING

AND SUSPICIOUS ACTIVITY

ATTESTATION FOR

BANKS/CREDIT UNIONS

Carrington Mortgage Services, LLC Page 1 of 1 1610 E. St Andrew Place, Suite B-150 Santa Ana, CA 92705 Rev 10/22/13

The entity named below represents that he/she has implemented a program consistent with the federal rules concerning Anti-Money Laundering (AML) programs and Suspicious Activity Report (SAR) filing requirements for Residential Mortgage Lenders and Originators (RMLO) as outlined in 31 CFR Parts 1010 and 1028 (Final Rule).

The following summary is provided for reference only and is not intended to be relied upon as compliance advice.

According to the Final Rule, the entity must, (1) develop and implement an AML program and (2) file a SAR to report any fraudulent attempts to obtain a mortgage or launder money by use of proceeds of other crimes to purchase residential real estate.

Under the Final Rule, the entity’s AML program must be in writing, be reviewed and updated annually and must assess the risk assessment across all of the entity’s products, services, customers and geographic locations. Additionally, the entity’s AML program must have, at a minimum:

Internal policies, procedures and controls,

A designated Compliance Officer,

An employee training program, and

An independent audit function.

According to the Final Rule, the entity must file a SAR within thirty (30) days of becoming aware of a transaction that:

Involves funds derived from illegal activity or are conducted to hide funds or assets derived from illegal activity;

Is designed to evade Bank Secrecy Act requirements;

Has no business or apparent lawful purpose, or

Involves the use of the company to facilitate criminal activity.

By signing below, the entity agrees and attests to his/her compliance with the terms as set forth in the Final Rule.

___________________________________________ ______________________________ Entity’s Name Entity’s NMLS Number __________________________ ______________________________ ___________ Officer’s Record Printed Name Officer’s Record Signature Date

ANTI-STEERING/SAFE

HARBOR ATTESTATION FOR

BANKS/CREDIT UNIONS

Carrington Mortgage Services, LLC Page 1 of 1 1610 E. St Andrew Place, Suite B-150 Santa Ana, CA 92705 Rev 10/22/13

A loan originator must not direct or “steer” a consumer to consummate a transaction based on the fact that the loan originator will receive greater compensation from the creditor in the transaction than in other transactions the originator offered or could have offered to the consumer, unless the consummated transaction is in the consumer’s interest. Section 226.36 (e) (2) of Regulation Z provides a “safe harbor” if the consumer is presented with loan options that meet certain conditions for each type of transaction in which the consumer expressed an interest.

An Anti-Steering Disclosure on all Lender-Paid transactions is required. Carrington Mortgage Services, LLC (CMS) will reject loan packages on Lender-Paid transactions that are not in compliance with Regulation Z or that do not comply with the following anti-steering requirements.

The Anti-Steering Disclosure must:

Indicate the types of transactions the consumer is interested in;

Clearly indicate the options presented for each type of transaction the consumer is interested in;

Indicate the option selected by the consumer; and

Be signed and dated by the Loan Originator and the consumer(s).

The loan originator must retain the applicable rate sheets obtained from the creditors from whom the loan originator obtained loan options in order to demonstrate compliance with Regulation Z.

To meet the Regulation Z requirements for safe harbor, the Anti-Steering Loan Options Disclosure must:

Disclosure must be titled, “Anti-Steering Loan Option Disclosure”, “Anti-Steering Disclosure of Loan Options” or “Loan Option Disclosure”

Include Borrower(s) name and identifying information such as a loan number or property address

Disclose loan options for each “Type of Transaction” in which the consumer expressed an interest. All options must be a similar type of transaction:

o Fixed Rate Loans

o Adjustable Rate Loans

Disclose three (3) options to the consumer(s) for which they likely qualify;

o Option 1 – Loan with the lowest interest rate

o Option 2 – Loan with the lowest interest rate without negative amortization, a prepayment penalty, interest only payments, a balloon payment in the first seven (7) years of the life of the loan, a demand feature, shared equity or shared appreciation

o Option 3 – Loan with the lowest total dollar amount for origination points or fees or discount points

Must be signed by Loan Officer and must include the Loan Officer’s NMLS license number

Must be signed by all Borrowers that will be listed on the Note

I have read the foregoing and understand CMS’ position on Anti-Steering.

__________________________________________________ _______________________________ Entity’s Name Entity’s NMLS Number ________________________________________ _____________________________________ ___________ Officer’s Printed Name Officer’s Signature Date

FAIR LENDING ATTESTATION

FOR BANKS/CREDIT UNIONS

Carrington Mortgage Services, LLC Page 1 of 2 1610 E. St Andrew Place, Suite B-150 Santa Ana, CA 92705 Rev 10/22/13

Carrington Mortgage Services, LLC (CMS) recognizes its responsibility to proactively avoid supporting any type of abusive or predatory lending practice, both in its own originations and in its dealings with any mortgage related professionals. CMS does not engage in abusive lending practices and refuses to do business with those who do.

Fair lending practices are incorporated into several federal and state laws that make it illegal for lenders to discriminate based on race, color, religion, age, sex or national origin. These include the Housing Financial Discrimination Act, the Equal Credit Opportunity Act, the Home Mortgage Disclosure Act, and the Federal Fair Housing Act. A summary of each is provided below. The summaries are not intended to be relied upon as compliance advice.

The Housing Financial Discrimination Act:

Known as the Holden Act, it is intended to prevent discrimination in housing accommodations such as improved or unimproved real estate that is used or intended to be used as a residence, will be occupied by the owners, and is not more than four units.

A lender is not allowed to discriminate based on race, color, religion, sex, age or national origin regarding the availability of financial assistance for the purpose of improvements, rehabilitation, purchasing, construction, or refinancing.

Lenders cannot deny loans or adversely vary the terms of loans due to conditions or trends in the neighborhood that are unrelated to the credit history of the applicant.

A lender cannot utilize inconsistent appraisal practices in determining whether the loan is granted to individuals due to their race, color, religion, sex, age or national origin.

The Equal Credit Opportunity Act:

A lender is obligated to notify a borrower of its intentions concerning a loan within a specified period of time, usually thirty days, after a loan application has been received.

If there are adverse actions from the lender, the borrower is entitled to a written statement as to why the action was taken. An adverse action is in the form of a denial, revocation of credit, a refusal of credit or a change in terms of an existing credit arrangement or other status.

The lender is subject to punitive damages and actual damages if it fails to comply.

The Home Mortgage Disclosure Act:

The Secretary of the Business, Transportation, and Housing Agency investigates and monitors the lending practices and patterns of lenders.

The Secretary may take actions if it is found that the lender willfully discriminated against any individual based on race, color, sex, religion, age, or national origin.

If a lender is found to have engaged in such discriminatory practices and patterns that violate the law, the Secretary can recommend that state funds be withheld from the lender.

The Fair Housing Act

The Federal Fair Housing Act of 1969 was created to provide fair housing throughout the United States, barring all racial, religious, or sexual discrimination, private or public, in the sale or rental of real property.

Designed as a rational means of stating effective policy, the fair housing act implements standards to which Congress has given the highest national priority, giving all citizens the same rights to purchase, inherit, sell, lease, and convey title to real estate personal property.

Incorporated in its purpose are provisions to prohibit and remedy acts of discrimination. It established procedures to provide protection within constitutional limits for fair housing with the intentions of ending unfair and unwanted biases in the housing market.

Together, these separate acts work hand in hand to prohibit discrimination by lenders and those involved in the mortgage industry and to set a standard of fair play for all citizens, regardless of race, color, religion, age, sex, or national origin.

FAIR LENDING ATTESTATION

FOR BANKS/CREDIT UNIONS

Carrington Mortgage Services, LLC Page 2 of 2 1610 E. St Andrew Place, Suite B-150 Santa Ana, CA 92705 Rev 10/22/13

By signing below, the entity agrees and attests to his/her compliance with the Home Mortgage Disclosure Act, the Equal Credit Opportunity Act, the Federal Fair Housing Act, the Housing Financial Discrimination Act and other laws are incorporated requiring fair lending practices.

_____________________________________________________ _____________________________ Entity’s Name Entity’s NMLS Number _________________________________________ _____________________________________ ___________ Officer’s Printed Name Officer’s Signature Date

LOAN FRAUD STATEMENT

FOR BANKS/CREDIT UNIONS

1610 E. St Andrew Place, Suite B-150, Santa Ana, CA 92705 Page 1 of 2 Rev. 10/22/13

It is the policy of Carrington Mortgage Services, LLC (CMS) to support the elimination of loan fraud within the mortgage lending industry. All approved entities should be advised that a licensed entity bears the responsibility for all actions, performed in the course of business, of his or her employees and licensees. The following are examples of prohibited conduct:

Submission of inaccurate information, including false statements on loan applications

and falsification of documents purporting to substantiate credit, employment, deposit and asset information or personal information including identity, ownership/non-ownership of real property.

Inaccurate representations of current occupancy or intent to maintain required occupancy as agreed to in the security instrument.

Lack of due diligence by Entity, Loan Officer, Interviewer or Processor, including failure to obtain or divulge all information required by the application and failure to request information as dictated by Borrower’s response to other questions that warrant further investigation.

Forgery or misrepresentation of any information, including partially or predominantly accurate information.

Accepting and using information or documentation which is known or suspected to be false or inaccurate. An example of which would include processing multiple owner-occupied loans from a single applicant where information differs on each application.

Permitting an applicant or interested third party to assist with the processing of the loan.

Failure of entity to disclose any relevant or material information known by the entity which if known by Lender would cause Lender to deny the loan request.

Consequences of Loan Fraud The consequences of loan fraud are far reaching and expensive. CMS stands behind the quality of its loan production. Fraudulent loans may not be sold in the secondary market and if sold, will require repurchase by CMS. Fraudulent loans harm our reputation and strain our

relationship with Investors.

LOAN FRAUD STATEMENT

FOR BANKS/CREDIT UNIONS

1610 E. St Andrew Place, Suite B-150, Santa Ana, CA 92705 Page 2 of 2 Rev. 10/22/13

The consequences to those who participate in loan fraud are severe. Potential Consequences to the entity:

Criminal persecution, which may result in possible fines and imprisonment.

Loss of license.

Loss of approval status with CMS.

Inability to access lenders caused by exchange of legally permissible information between lenders, mortgage insurance companies, Freddie Mac, Fannie Mae, police agencies and federal regulatory agencies.

Civil action by CMS.

Civil action by the Borrower and/or parties to the transaction.

Potential Consequences to the Borrower:

Acceleration of debt as mandated in the security instrument.

Criminal prosecution which may result in fines and imprisonment.

Civil action by CMS and/or other parties to the transaction.

Termination of Employment.

Forfeiture of any professional licenses.

Adverse, long term effect on credit history. I have read the foregoing and understand CMS’ position on loan fraud.

__________________________________________ _______________________ Entity’s Name Entity’s NMLS Number _____________________________________ _________________________________ ________ Officer’s Printed Name Officer’s Signature Date

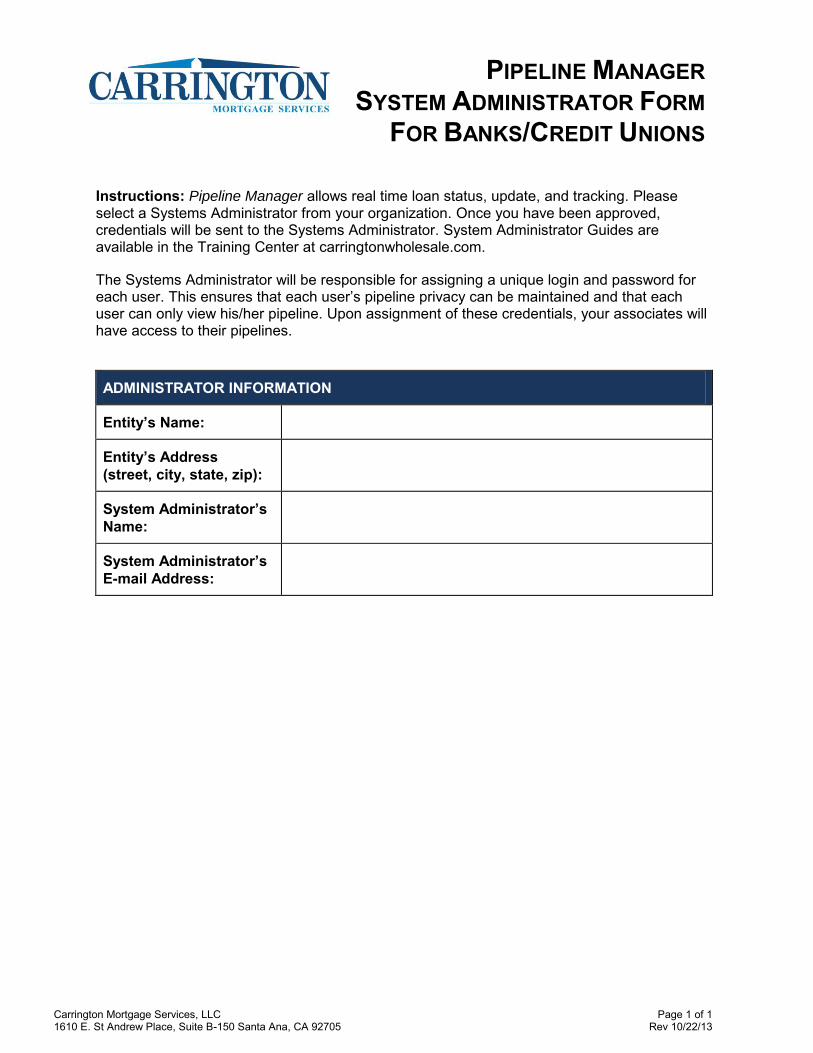

PIPELINE MANAGER SYSTEM ADMINISTRATOR FORM

FOR BANKS/CREDIT UNIONS

Carrington Mortgage Services, LLC Page 1 of 1 1610 E. St Andrew Place, Suite B-150 Santa Ana, CA 92705 Rev 10/22/13

Instructions: Pipeline Manager allows real time loan status, update, and tracking. Please select a Systems Administrator from your organization. Once you have been approved, credentials will be sent to the Systems Administrator. System Administrator Guides are available in the Training Center at carringtonwholesale.com.

The Systems Administrator will be responsible for assigning a unique login and password for each user. This ensures that each user’s pipeline privacy can be maintained and that each user can only view his/her pipeline. Upon assignment of these credentials, your associates will have access to their pipelines.

ADMINISTRATOR INFORMATION

Entity’s Name:

Entity’s Address

(street, city, state, zip):

System Administrator’s

Name:

System Administrator’s

E-mail Address:

Carrington Mortgage Services, LLC Page 1 of 1

1610 E. St Andrew Place, Suite B-150 Santa Ana, CA 92705 Rev 05/13/13

CORPORATE RESOLUTION

I hereby certify that I am the Secretary of ________________________________________, a Corporation

in the State of _____________________________, and that as such Secretary, I have custody of the

records of this Corporation, and by virtue of such action, the Board of Directors passed the following

resolution at a meeting date _____________________, 20____, which is now in force and is not in conflict

with the Charter of Bylaws of the Corporation.

RESOLVED, that the officers and agents of this Corporation appointed and named below are hereby

authorized in the name of and on the behalf of the Corporation to enter in an agreement and Carrington

Mortgage Services, LLC and its operating subsidiaries ("CMS”) to sell and/or broker mortgage loans, and that

these individuals are each and severally authorized to sign on said agreement and on behalf of the

Corporation and to effect any changed with respect thereto.

FUTHER RESOLVED, that these individuals are each and severally authorized to enter into commitments with

CMS and to execute any and all other documents on behalf of the Corporation.

FUTHER RESOLVED, this Corporation is authorized to sign an agreement as required by CMS.

FUTHER RESOLVED, that which is authorized shall remain in force until CMS receives, at its office, a certified copy of a resolution of this Corporation to the contrary, revoking all previous authorizations heretofore given. The revocation of previous authorization with respect to said account shall not affect the validity of any item signed by the person or persons, who at the time, were authorized to act.

1)

Authorize Agent (Print or Type Name)

Applicant Agent (Signature)

2)

Authorize Agent (Print or Type Name)

Applicant Agent (Signature)

3)

Authorize Agent (Print or Type Name)

Applicant Agent (Signature)

4)

Authorize Agent (Print or Type Name)

Applicant Agent (Signature)

In witness where of, I have executed this resolution in my capacity of Secretary of this Corporation this

________day ______, in the year ___________.

Secretary Signature

INSTRUCTIONS TO PRINTERSFORM W-9, PAGE 1 of 4MARGINS: TOP 13mm (1⁄ 2 "), CENTER SIDES. PRINTS: HEAD to HEADPAPER: WHITE WRITING, SUB. 20. INK: BLACKFLAT SIZE: 216mm (81⁄ 2 ") 3 279mm (11")PERFORATE: (NONE)

Give form to therequester. Do notsend to the IRS.

Form W-9 Request for TaxpayerIdentification Number and Certification

(Rev. October 2007) Department of the TreasuryInternal Revenue Service Name (as shown on your income tax return)

List account number(s) here (optional)

Address (number, street, and apt. or suite no.)

City, state, and ZIP code

Pri

nt o

r ty

pe

See

Sp

ecifi

c In

stru

ctio

ns o

n p

age

2.

Taxpayer Identification Number (TIN)

Enter your TIN in the appropriate box. The TIN provided must match the name given on Line 1 to avoidbackup withholding. For individuals, this is your social security number (SSN). However, for a residentalien, sole proprietor, or disregarded entity, see the Part I instructions on page 3. For other entities, it isyour employer identification number (EIN). If you do not have a number, see How to get a TIN on page 3.

Social security number

or

Requester’s name and address (optional)

Employer identification number Note. If the account is in more than one name, see the chart on page 4 for guidelines on whosenumber to enter. Certification

1. The number shown on this form is my correct taxpayer identification number (or I am waiting for a number to be issued to me), and I am not subject to backup withholding because: (a) I am exempt from backup withholding, or (b) I have not been notified by the InternalRevenue Service (IRS) that I am subject to backup withholding as a result of a failure to report all interest or dividends, or (c) the IRS hasnotified me that I am no longer subject to backup withholding, and

2.

Certification instructions. You must cross out item 2 above if you have been notified by the IRS that you are currently subject to backupwithholding because you have failed to report all interest and dividends on your tax return. For real estate transactions, item 2 does not apply.For mortgage interest paid, acquisition or abandonment of secured property, cancellation of debt, contributions to an individual retirementarrangement (IRA), and generally, payments other than interest and dividends, you are not required to sign the Certification, but you mustprovide your correct TIN. See the instructions on page 4. SignHere

Signature ofU.S. person ©

Date ©

General Instructions

Form W-9 (Rev. 10-2007)

Part I

Part II

Business name, if different from above

Cat. No. 10231X

Check appropriate box:

Under penalties of perjury, I certify that:

13 I.R.S. SPECIFICATIONS TO BE REMOVED BEFORE PRINTING

DO NOT PRINT — DO NOT PRINT — DO NOT PRINT — DO NOT PRINT

TLS, have youtransmitted all R text files for this cycle update?

Date

Action

Revised proofsrequested

Date

Signature

O.K. to print

Use Form W-9 only if you are a U.S. person (including aresident alien), to provide your correct TIN to the personrequesting it (the requester) and, when applicable, to: 1. Certify that the TIN you are giving is correct (or you arewaiting for a number to be issued), 2. Certify that you are not subject to backup withholding, or

3. Claim exemption from backup withholding if you are a U.S.exempt payee. If applicable, you are also certifying that as aU.S. person, your allocable share of any partnership income froma U.S. trade or business is not subject to the withholding tax onforeign partners’ share of effectively connected income.

3. I am a U.S. citizen or other U.S. person (defined below).

A person who is required to file an information return with theIRS must obtain your correct taxpayer identification number (TIN)to report, for example, income paid to you, real estatetransactions, mortgage interest you paid, acquisition orabandonment of secured property, cancellation of debt, orcontributions you made to an IRA.

Individual/Sole proprietor

Corporation

Partnership

Other (see instructions) ©

Note. If a requester gives you a form other than Form W-9 torequest your TIN, you must use the requester’s form if it issubstantially similar to this Form W-9.

● An individual who is a U.S. citizen or U.S. resident alien, ● A partnership, corporation, company, or association created or

organized in the United States or under the laws of the UnitedStates, ● An estate (other than a foreign estate), or

Definition of a U.S. person. For federal tax purposes, you areconsidered a U.S. person if you are:

Special rules for partnerships. Partnerships that conduct atrade or business in the United States are generally required topay a withholding tax on any foreign partners’ share of incomefrom such business. Further, in certain cases where a Form W-9has not been received, a partnership is required to presume thata partner is a foreign person, and pay the withholding tax.Therefore, if you are a U.S. person that is a partner in apartnership conducting a trade or business in the United States,provide Form W-9 to the partnership to establish your U.S.status and avoid withholding on your share of partnershipincome. The person who gives Form W-9 to the partnership forpurposes of establishing its U.S. status and avoiding withholdingon its allocable share of net income from the partnershipconducting a trade or business in the United States is in thefollowing cases: ● The U.S. owner of a disregarded entity and not the entity,

Section references are to the Internal Revenue Code unlessotherwise noted.

● A domestic trust (as defined in Regulations section301.7701-7).

Limited liability company. Enter the tax classification (D=disregarded entity, C=corporation, P=partnership) ©

Exempt payee

Purpose of Form

INSTRUCTIONS TO PRINTERSFORM W-9, PAGE 2 of 4MARGINS: TOP 13 mm (1⁄ 2"), CENTER SIDES. PRINTS: HEAD to HEADPAPER: WHITE WRITING, SUB. 20. INK: BLACKFLAT SIZE: 216 mm (81⁄ 2") 3 279 mm (11")PERFORATE: (NONE)

Form W-9 (Rev. 10-2007) Page 2

Sole proprietor. Enter your individual name as shown on yourincome tax return on the “Name” line. You may enter yourbusiness, trade, or “doing business as (DBA)” name on the“Business name” line.

13 I.R.S. SPECIFICATIONS TO BE REMOVED BEFORE PRINTING

DO NOT PRINT — DO NOT PRINT — DO NOT PRINT — DO NOT PRINT

Other entities. Enter your business name as shown on requiredfederal tax documents on the “Name” line. This name shouldmatch the name shown on the charter or other legal documentcreating the entity. You may enter any business, trade, or DBAname on the “Business name” line.

If the account is in joint names, list first, and then circle, thename of the person or entity whose number you entered in Part Iof the form.

Specific Instructions Name

Exempt Payee

5. You do not certify to the requester that you are not subjectto backup withholding under 4 above (for reportable interest anddividend accounts opened after 1983 only). Certain payees and payments are exempt from backupwithholding. See the instructions below and the separateInstructions for the Requester of Form W-9.

Civil penalty for false information with respect towithholding. If you make a false statement with no reasonablebasis that results in no backup withholding, you are subject to a$500 penalty. Criminal penalty for falsifying information. Willfully falsifyingcertifications or affirmations may subject you to criminalpenalties including fines and/or imprisonment.

Penalties Failure to furnish TIN. If you fail to furnish your correct TIN to arequester, you are subject to a penalty of $50 for each suchfailure unless your failure is due to reasonable cause and not towillful neglect.

Misuse of TINs. If the requester discloses or uses TINs inviolation of federal law, the requester may be subject to civil andcriminal penalties.

If you are an individual, you must generally enter the nameshown on your income tax return. However, if you have changedyour last name, for instance, due to marriage without informingthe Social Security Administration of the name change, enteryour first name, the last name shown on your social securitycard, and your new last name.

If you are exempt from backup withholding, enter your name asdescribed above and check the appropriate box for your status,then check the “Exempt payee” box in the line following thebusiness name, sign and date the form.

4. The IRS tells you that you are subject to backupwithholding because you did not report all your interest anddividends on your tax return (for reportable interest anddividends only), or

3. The IRS tells the requester that you furnished an incorrectTIN,

2. You do not certify your TIN when required (see the Part IIinstructions on page 3 for details),

You will not be subject to backup withholding on paymentsyou receive if you give the requester your correct TIN, make theproper certifications, and report all your taxable interest anddividends on your tax return.

1. You do not furnish your TIN to the requester,

What is backup withholding? Persons making certain paymentsto you must under certain conditions withhold and pay to theIRS 28% of such payments. This is called “backup withholding.” Payments that may be subject to backup withholding includeinterest, tax-exempt interest, dividends, broker and barterexchange transactions, rents, royalties, nonemployee pay, andcertain payments from fishing boat operators. Real estatetransactions are not subject to backup withholding.

Payments you receive will be subject to backupwithholding if:

If you are a nonresident alien or a foreign entity not subject tobackup withholding, give the requester the appropriatecompleted Form W-8.

Example. Article 20 of the U.S.-China income tax treaty allowsan exemption from tax for scholarship income received by aChinese student temporarily present in the United States. UnderU.S. law, this student will become a resident alien for taxpurposes if his or her stay in the United States exceeds 5calendar years. However, paragraph 2 of the first Protocol to theU.S.-China treaty (dated April 30, 1984) allows the provisions ofArticle 20 to continue to apply even after the Chinese studentbecomes a resident alien of the United States. A Chinesestudent who qualifies for this exception (under paragraph 2 ofthe first protocol) and is relying on this exception to claim anexemption from tax on his or her scholarship or fellowshipincome would attach to Form W-9 a statement that includes theinformation described above to support that exemption.

Note. You are requested to check the appropriate box for yourstatus (individual/sole proprietor, corporation, etc.).

4. The type and amount of income that qualifies for theexemption from tax. 5. Sufficient facts to justify the exemption from tax under theterms of the treaty article.

Nonresident alien who becomes a resident alien. Generally,only a nonresident alien individual may use the terms of a taxtreaty to reduce or eliminate U.S. tax on certain types of income.However, most tax treaties contain a provision known as a“saving clause.” Exceptions specified in the saving clause maypermit an exemption from tax to continue for certain types ofincome even after the payee has otherwise become a U.S.resident alien for tax purposes. If you are a U.S. resident alien who is relying on an exceptioncontained in the saving clause of a tax treaty to claim anexemption from U.S. tax on certain types of income, you mustattach a statement to Form W-9 that specifies the following fiveitems: 1. The treaty country. Generally, this must be the same treatyunder which you claimed exemption from tax as a nonresidentalien. 2. The treaty article addressing the income.

3. The article number (or location) in the tax treaty thatcontains the saving clause and its exceptions.

Also see Special rules for partnerships on page 1.

Foreign person. If you are a foreign person, do not use FormW-9. Instead, use the appropriate Form W-8 (see Publication515, Withholding of Tax on Nonresident Aliens and ForeignEntities).

● The U.S. grantor or other owner of a grantor trust and not thetrust, and ● The U.S. trust (other than a grantor trust) and not thebeneficiaries of the trust.

Limited liability company (LLC). Check the “Limited liabilitycompany” box only and enter the appropriate code for the taxclassification (“D” for disregarded entity, “C” for corporation, “P” for partnership) in the space provided. For a single-member LLC (including a foreign LLC with adomestic owner) that is disregarded as an entity separate fromits owner under Regulations section 301.7701-3, enter theowner’s name on the “Name” line. Enter the LLC’s name on the“Business name” line. For an LLC classified as a partnership or a corporation, enterthe LLC’s name on the “Name” line and any business, trade, orDBA name on the “Business name” line.

INSTRUCTIONS TO PRINTERSFORM W-9, PAGE 3 of 4MARGINS: TOP 13 mm (1⁄ 2"), CENTER SIDES. PRINTS: HEAD to HEADPAPER: WHITE WRITING, SUB. 20. INK: BLACKFLAT SIZE: 216 mm (81⁄ 2") 3 279 mm (11")PERFORATE: (NONE)

I.R.S. SPECIFICATIONS TO BE REMOVED BEFORE PRINTING

DO NOT PRINT — DO NOT PRINT — DO NOT PRINT — DO NOT PRINT

Form W-9 (Rev. 10-2007) Page 3

13

Part I. Taxpayer IdentificationNumber (TIN) Enter your TIN in the appropriate box. If you are a residentalien and you do not have and are not eligible to get an SSN,your TIN is your IRS individual taxpayer identification number(ITIN). Enter it in the social security number box. If you do nothave an ITIN, see How to get a TIN below.

How to get a TIN. If you do not have a TIN, apply for oneimmediately. To apply for an SSN, get Form SS-5, Applicationfor a Social Security Card, from your local Social SecurityAdministration office or get this form online at www.ssa.gov. Youmay also get this form by calling 1-800-772-1213. Use FormW-7, Application for IRS Individual Taxpayer IdentificationNumber, to apply for an ITIN, or Form SS-4, Application forEmployer Identification Number, to apply for an EIN. You canapply for an EIN online by accessing the IRS website atwww.irs.gov/businesses and clicking on Employer IdentificationNumber (EIN) under Starting a Business. You can get Forms W-7and SS-4 from the IRS by visiting www.irs.gov or by calling1-800-TAX-FORM (1-800-829-3676). If you are asked to complete Form W-9 but do not have a TIN,write “Applied For” in the space for the TIN, sign and date theform, and give it to the requester. For interest and dividendpayments, and certain payments made with respect to readilytradable instruments, generally you will have 60 days to get aTIN and give it to the requester before you are subject to backupwithholding on payments. The 60-day rule does not apply toother types of payments. You will be subject to backupwithholding on all such payments until you provide your TIN tothe requester.

If you are a sole proprietor and you have an EIN, you mayenter either your SSN or EIN. However, the IRS prefers that youuse your SSN. If you are a single-member LLC that is disregarded as anentity separate from its owner (see Limited liability company(LLC) on page 2), enter the owner’s SSN (or EIN, if the ownerhas one). Do not enter the disregarded entity’s EIN. If the LLC isclassified as a corporation or partnership, enter the entity’s EIN. Note. See the chart on page 4 for further clarification of nameand TIN combinations.

Note. Entering “Applied For” means that you have alreadyapplied for a TIN or that you intend to apply for one soon. Caution: A disregarded domestic entity that has a foreign ownermust use the appropriate Form W-8.

9. A futures commission merchant registered with theCommodity Futures Trading Commission, 10. A real estate investment trust,

11. An entity registered at all times during the tax year underthe Investment Company Act of 1940, 12. A common trust fund operated by a bank under section584(a), 13. A financial institution,

14. A middleman known in the investment community as anominee or custodian, or 15. A trust exempt from tax under section 664 or described insection 4947.

THEN the payment is exemptfor . . .

IF the payment is for . . .

All exempt payees except for 9

Interest and dividend payments

Exempt payees 1 through 13.Also, a person registered underthe Investment Advisers Act of1940 who regularly acts as abroker

Broker transactions

Exempt payees 1 through 5

Barter exchange transactionsand patronage dividends

Generally, exempt payees 1 through 7

Payments over $600 requiredto be reported and directsales over $5,000 See Form 1099-MISC, Miscellaneous Income, and its instructions. However, the following payments made to a corporation (including grossproceeds paid to an attorney under section 6045(f), even if the attorney is acorporation) and reportable on Form 1099-MISC are not exempt frombackup withholding: medical and health care payments, attorneys’ fees, andpayments for services paid by a federal executive agency.

The chart below shows types of payments that may beexempt from backup withholding. The chart applies to theexempt payees listed above, 1 through 15.

1 2

7. A foreign central bank of issue, 8. A dealer in securities or commodities required to register in

the United States, the District of Columbia, or a possession ofthe United States,

2

The following payees are exempt from backup withholding: 1. An organization exempt from tax under section 501(a), any

IRA, or a custodial account under section 403(b)(7) if the accountsatisfies the requirements of section 401(f)(2), 2. The United States or any of its agencies orinstrumentalities, 3. A state, the District of Columbia, a possession of the UnitedStates, or any of their political subdivisions or instrumentalities, 4. A foreign government or any of its political subdivisions,agencies, or instrumentalities, or 5. An international organization or any of its agencies orinstrumentalities. Other payees that may be exempt from backup withholdinginclude: 6. A corporation,

Generally, individuals (including sole proprietors) are not exemptfrom backup withholding. Corporations are exempt from backupwithholding for certain payments, such as interest and dividends. Note. If you are exempt from backup withholding, you shouldstill complete this form to avoid possible erroneous backupwithholding.

1

1. Interest, dividend, and barter exchange accountsopened before 1984 and broker accounts considered activeduring 1983. You must give your correct TIN, but you do nothave to sign the certification. 2. Interest, dividend, broker, and barter exchangeaccounts opened after 1983 and broker accounts consideredinactive during 1983. You must sign the certification or backupwithholding will apply. If you are subject to backup withholdingand you are merely providing your correct TIN to the requester,you must cross out item 2 in the certification before signing theform.

Part II. Certification

For a joint account, only the person whose TIN is shown inPart I should sign (when required). Exempt payees, see ExemptPayee on page 2.

To establish to the withholding agent that you are a U.S. person,or resident alien, sign Form W-9. You may be requested to signby the withholding agent even if items 1, 4, and 5 below indicateotherwise.

Signature requirements. Complete the certification as indicatedin 1 through 5 below.

INSTRUCTIONS TO PRINTERSFORM W-9, PAGE 4 of 4MARGINS: TOP 13 mm (1⁄ 2"), CENTER SIDES. PRINTS: HEAD to HEADPAPER: WHITE WRITING, SUB. 20. INK: BLACKFLAT SIZE: 216 mm (81⁄ 2") 3 279 mm (11")PERFORATE: (NONE)

Form W-9 (Rev. 10-2007) Page 4

I.R.S. SPECIFICATIONS TO BE REMOVED BEFORE PRINTING

DO NOT PRINT — DO NOT PRINT — DO NOT PRINT — DO NOT PRINT

Give name and EIN of:

For this type of account:

3. Real estate transactions. You must sign the certification.You may cross out item 2 of the certification.

A valid trust, estate, or pension trust

6.

Legal entity 4

4. Other payments. You must give your correct TIN, but youdo not have to sign the certification unless you have beennotified that you have previously given an incorrect TIN. “Otherpayments” include payments made in the course of therequester’s trade or business for rents, royalties, goods (otherthan bills for merchandise), medical and health care services(including payments to corporations), payments to anonemployee for services, payments to certain fishing boat crewmembers and fishermen, and gross proceeds paid to attorneys(including payments to corporations).

The corporation

Corporate or LLC electingcorporate status on Form 8832

7.

The organization

Association, club, religious,charitable, educational, or othertax-exempt organization

8.

5. Mortgage interest paid by you, acquisition orabandonment of secured property, cancellation of debt,qualified tuition program payments (under section 529), IRA,Coverdell ESA, Archer MSA or HSA contributions ordistributions, and pension distributions. You must give yourcorrect TIN, but you do not have to sign the certification.

The partnership

Partnership or multi-member LLC

9.

The broker or nominee

A broker or registered nominee

10.

The public entity

Account with the Department ofAgriculture in the name of a publicentity (such as a state or localgovernment, school district, orprison) that receives agriculturalprogram payments

11.

Privacy Act Notice

List first and circle the name of the person whose number you furnish. If only one personon a joint account has an SSN, that person’s number must be furnished. Circle the minor’s name and furnish the minor’s SSN. You must show your individual name and you may also enter your business or “DBA” name on the second name line. You may use either your SSN or EIN (if you have one),but the IRS encourages you to use your SSN. List first and circle the name of the trust, estate, or pension trust. (Do not furnish the TINof the personal representative or trustee unless the legal entity itself is not designated inthe account title.) Also see Special rules for partnerships on page 1.

Note. If no name is circled when more than one name is listed,the number will be considered to be that of the first name listed.

Disregarded entity not owned by anindividual

The owner

12.

13

You must provide your TIN whether or not you are required to file a tax return. Payers must generally withhold 28% of taxable interest, dividend, and certain otherpayments to a payee who does not give a TIN to a payer. Certain penalties may also apply.

Section 6109 of the Internal Revenue Code requires you to provide your correct TIN to persons who must file information returns with the IRS to report interest,dividends, and certain other income paid to you, mortgage interest you paid, the acquisition or abandonment of secured property, cancellation of debt, orcontributions you made to an IRA, or Archer MSA or HSA. The IRS uses the numbers for identification purposes and to help verify the accuracy of your tax return.The IRS may also provide this information to the Department of Justice for civil and criminal litigation, and to cities, states, the District of Columbia, and U.S.possessions to carry out their tax laws. We may also disclose this information to other countries under a tax treaty, to federal and state agencies to enforce federalnontax criminal laws, or to federal law enforcement and intelligence agencies to combat terrorism.

1

2 3

4

Secure Your Tax Records from Identity Theft Identity theft occurs when someone uses your personalinformation such as your name, social security number (SSN), orother identifying information, without your permission, to commitfraud or other crimes. An identity thief may use your SSN to geta job or may file a tax return using your SSN to receive a refund.

What Name and Number To Give the Requester Give name and SSN of:

For this type of account:

The individual

1.

Individual The actual owner of the account or,

if combined funds, the firstindividual on the account

2.

Two or more individuals (jointaccount)

The minor 2

3.

Custodian account of a minor(Uniform Gift to Minors Act) The grantor-trustee

1

4.

a. The usual revocable savingstrust (grantor is also trustee) The actual owner

1

b. So-called trust account that isnot a legal or valid trust understate law The owner

3

5.

Sole proprietorship or disregardedentity owned by an individual

Call the IRS at 1-800-829-1040 if you think your identity hasbeen used inappropriately for tax purposes.

1

To reduce your risk: ● Protect your SSN, ● Ensure your employer is protecting your SSN, and ● Be careful when choosing a tax preparer.

Victims of identity theft who are experiencing economic harmor a system problem, or are seeking help in resolving taxproblems that have not been resolved through normal channels,may be eligible for Taxpayer Advocate Service (TAS) assistance.You can reach TAS by calling the TAS toll-free case intake lineat 1-877-777-4778 or TTY/TDD 1-800-829-4059. Protect yourself from suspicious emails or phishingschemes. Phishing is the creation and use of email andwebsites designed to mimic legitimate business emails andwebsites. The most common act is sending an email to a userfalsely claiming to be an established legitimate enterprise in anattempt to scam the user into surrendering private informationthat will be used for identity theft. The IRS does not initiate contacts with taxpayers via emails.Also, the IRS does not request personal detailed informationthrough email or ask taxpayers for the PIN numbers, passwords,or similar secret access information for their credit card, bank, orother financial accounts. If you receive an unsolicited email claiming to be from the IRS,forward this message to [email protected]. You may also reportmisuse of the IRS name, logo, or other IRS personal property tothe Treasury Inspector General for Tax Administration at1-800-366-4484. You can forward suspicious emails to theFederal Trade Commission at: [email protected] or contact them atwww.consumer.gov/idtheft or 1-877-IDTHEFT(438-4338).

Visit the IRS website at www.irs.gov to learn more aboutidentity theft and how to reduce your risk.

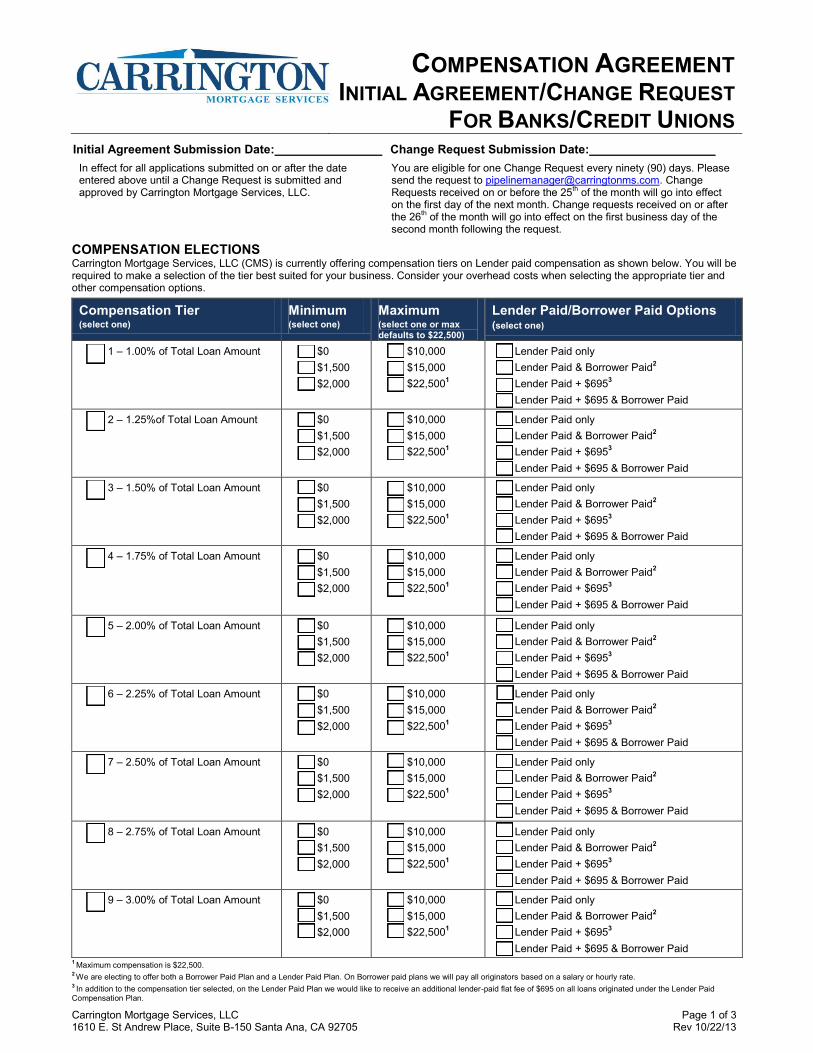

COMPENSATION AGREEMENT INITIAL AGREEMENT/CHANGE REQUEST

FOR BANKS/CREDIT UNIONS

Carrington Mortgage Services, LLC Page 1 of 3 1610 E. St Andrew Place, Suite B-150 Santa Ana, CA 92705 Rev 10/22/13

Initial Agreement Submission Date: Change Request Submission Date:

In effect for all applications submitted on or after the date entered above until a Change Request is submitted and approved by Carrington Mortgage Services, LLC.

You are eligible for one Change Request every ninety (90) days. Please send the request to [email protected]. Change Requests received on or before the 25

th of the month will go into effect

on the first day of the next month. Change requests received on or after the 26

th of the month will go into effect on the first business day of the

second month following the request.

COMPENSATION ELECTIONS Carrington Mortgage Services, LLC (CMS) is currently offering compensation tiers on Lender paid compensation as shown below. You will be required to make a selection of the tier best suited for your business. Consider your overhead costs when selecting the appropriate tier and other compensation options.

Compensation Tier (select one)

Minimum (select one)

Maximum (select one or max defaults to $22,500)

Lender Paid/Borrower Paid Options (select one)

1 – 1.00% of Total Loan Amount $0

$1,500

$2,000

$10,000

$15,000

$22,5001

Lender Paid only

Lender Paid & Borrower Paid2

Lender Paid + $6953

Lender Paid + $695 & Borrower Paid

2 – 1.25%of Total Loan Amount $0

$1,500

$2,000

$10,000

$15,000

$22,5001

Lender Paid only

Lender Paid & Borrower Paid2

Lender Paid + $6953

Lender Paid + $695 & Borrower Paid

3 – 1.50% of Total Loan Amount $0

$1,500

$2,000

$10,000

$15,000

$22,5001

Lender Paid only

Lender Paid & Borrower Paid2

Lender Paid + $6953

Lender Paid + $695 & Borrower Paid

4 – 1.75% of Total Loan Amount $0

$1,500

$2,000

$10,000

$15,000

$22,5001

Lender Paid only

Lender Paid & Borrower Paid2

Lender Paid + $6953

Lender Paid + $695 & Borrower Paid

5 – 2.00% of Total Loan Amount $0

$1,500

$2,000

$10,000

$15,000

$22,5001

Lender Paid only

Lender Paid & Borrower Paid2

Lender Paid + $6953

Lender Paid + $695 & Borrower Paid

6 – 2.25% of Total Loan Amount $0

$1,500

$2,000

$10,000

$15,000

$22,5001

Lender Paid only

Lender Paid & Borrower Paid2

Lender Paid + $6953

Lender Paid + $695 & Borrower Paid

7 – 2.50% of Total Loan Amount $0

$1,500

$2,000

$10,000

$15,000

$22,5001

Lender Paid only

Lender Paid & Borrower Paid2

Lender Paid + $6953

Lender Paid + $695 & Borrower Paid

8 – 2.75% of Total Loan Amount $0

$1,500

$2,000

$10,000

$15,000

$22,5001

Lender Paid only

Lender Paid & Borrower Paid2

Lender Paid + $6953

Lender Paid + $695 & Borrower Paid

9 – 3.00% of Total Loan Amount $0

$1,500

$2,000

$10,000

$15,000

$22,5001

Lender Paid only

Lender Paid & Borrower Paid2

Lender Paid + $6953

Lender Paid + $695 & Borrower Paid 1 Maximum compensation is $22,500.

2 We are electing to offer both a Borrower Paid Plan and a Lender Paid Plan. On Borrower paid plans we will pay all originators based on a salary or hourly rate.

3 In addition to the compensation tier selected, on the Lender Paid Plan we would like to receive an additional lender-paid flat fee of $695 on all loans originated under the Lender Paid

Compensation Plan.

COMPENSATION AGREEMENT INITIAL AGREEMENT/CHANGE REQUEST

FOR BANKS/CREDIT UNIONS

Carrington Mortgage Services, LLC Page 2 of 3 1610 E. St Andrew Place, Suite B-150 Santa Ana, CA 92705 Rev 10/22/13

COMPENSATION CHANGES Compensation changes may only be made on a quarterly basis. Changes must be made by the 25th of each month (or the next business day). Any changes made will become effective on the first day of the month immediately following the change date. Any changes made will not affect loans in process. It will only affect applications submitted on the first day of the month in which the new compensation tier becomes effective. A new Compensation Election Form will be required each time the compensation tier is changed.

ADDITIONAL PROVISIONS:

I understand that all loans registered after April 6, 2011 with Lender Paid Compensation will be administered in accordance with Regulation Z §226.25 and §226.36

I understand that this compensation selection applies to all l loans submitted with the Lender Paid Compensation per the Lender Paid Compensation Agreement then in effect.

I understand that payment of compensation must be properly disclosed per all legal and Regulatory requirements.

I understand that I cannot collect compensation by any other means or from any other party in transactions with Lender Paid Compensation.

I will not steer or direct a consumer to consummate a loan transaction in order to receive greater compensation per Regulation Z.

I certify that all Loan Originator Compensation Agreements and payments are in compliance for Borrower Paid and Lender Paid Plans. And that Loan Originators in my employment comply with all applicable laws and regulations including but not limited to Regulation Z.

In order to ensure borrowers are not charged excessive or unfair fees in connection with a residential mortgage loan transaction, and to ensure compensation is commensurate with services they perform, the entity cannot pass third party processing fees on to the borrower as a separate charge on lender paid transactions.

A lender’s compensation includes compensation intended to cover costs associated with the processing of a mortgage loan. Therefore, if an entity elects to outsource all or part of the processing of a loan to a third party entity (regardless of affiliation), no additional or separate charge is allowed as the costs of such third party processing is already part of the compensation.

In Borrower paid compensation transactions, the entity will negotiate compensation directly with the consumer. The consumer may pay bona fide third party costs by paying cash at closing or by financing them through the loan principal or interest rate. However, compensation cannot be paid by more than one source. If the borrower pays the entity, compensation is comprised of the origination fee and a processing fee that cannot exceed the amount designated by the entity on a Lender Paid transaction. Additionally, the Borrower will need to provide a statement requesting the change and the reason for the change

Due to High Cost restrictions in the state of Illinois, the maximum compensation for the entity is 2.75%.

I understand that as an Officer of the entity, I am responsible for complying with all aspects of TILA, including but not limited to, compensation to my Loan Officers. If I select a Brower-Paid Plan for a specific loan, I must compensate the Loan Officer on either a salary or hourly basis. Bonuses are allowed as long as they are not based on a specific loan. For example, bonuses are allowed to be paid on overall volume or quality. If I select a Lender Paid Plan for a specific loan, I may compensate the Loan Officer on a fixed percentage of the loan amount with or without a fixed minimum or maximum dollar amount, but cannot vary with different levels or tiers of loan amounts. I may also split the compensation with the Loan Officer as long as the amount is a fixed percentage or fixed dollar amount. I may not pay the Loan Officer on a loan’s terms or conditions or interest rate. I may not compensate a Loan Officer on factors that are considered proxies such as the credit score or debt-to-income ratio. If I have multiple branches with the same NMLS number, all Loan Officers of each branch must only be paid based on the compensation agreement in place for their branch, and may not submit loans

COMPENSATION AGREEMENT INITIAL AGREEMENT/CHANGE REQUEST

FOR BANKS/CREDIT UNIONS

Carrington Mortgage Services, LLC Page 3 of 3 1610 E. St Andrew Place, Suite B-150 Santa Ana, CA 92705 Rev 10/22/13

through another branch on a different compensation agreement. If I choose to submit one loan under a Borrower Paid Plan and another loan under a Lender Paid Plan, I must still pay each Loan Officer in accordance with TILA as stated above. I understand that I must have written compensation agreements in place with my Loan Officers.

These compensation agreements may change periodically but cannot change by loan. Thus if the Loan Officer is on a salary and I change a loan from one Plan to the other, I must continue to pay the Loan Officer on a salary. Also, if my processor also originates even one loan, then I must comply with this regulation and pay the processor as above. There may be other forms of acceptable and unacceptable compensation.

I understand and acknowledge that Carrington Mortgage Services, LLC reserves the right to audit my compliance with this Agreement as it deems appropriate. I represent and warrant that I have the authority to sign this document on behalf of the entity listed below:

_____________________________________ _________________________________________

Entity’s Name Entity’s NMLS Number

_________________________________________________________________________________________________________________________

Entity’s Address Street City State Zip

_________________________________________ _________________________________________

Officer’s Name Officer’s Email Address

_________________________________________ _________________________________________

Officer’s Signature Date

BANK/CREDIT UNION AGREEMENT

Carrington Mortgage Services, LLC Page 1 of 14 1610 E. St Andrew Place, Suite B-150 Santa Ana, CA 92705 Rev 10/22/13

THIS BANK/CREDIT UNION AGREEMENT (“Agreement”) is made on _____________, ______ by and

between Carrington Mortgage Services, LLC, a Delaware Corporation with its corporate office located at

1610 E. Saint Andrew Place, Suite B-150, Santa Ana, California 92705 (“Lender”) and

_______________________________________ a _____________________ with his/her/its principal place

of business located at __________________________________________________________ (“Entity”;

Lender and Entity are hereinafter collectively referred to as the “Parties” and individually as a “Party”).

RECITALS

1. Entity is a duly licensed mortgage entity engaged in the business of taking mortgage loan

applications from consumers for residential mortgage loans, aiding and assisting consumers in the

pre-qualification for residential mortgage loans, choosing a mortgage product, completing a

mortgage loan application and processing those applications on behalf of the consumer in

exchange for a fee.

2. Entity desires to submit residential mortgage loan applications and obtain mortgage loans from

Lender for its applicants.

3. Lender extends credit to qualified applicants for mortgage loans secured by first and/or second

liens on residential real property.

4. Lender and Entity desire to establish a relationship whereby Entity may submit residential mortgage

loan application packages to Lender for possible acceptance of such applications in accordance

with the terms and conditions set forth in this agreement.

NOW THEREFORE, in consideration of the promises and mutual covenants contained in this agreement,

Lender and Entity agree as follows:

ARTICLE 1 DEFINITIONS

“Applicant” means the person or persons who submit an Application to the Entity that the Entity

subsequently submits to Lender and who, if Lender agrees to fund the Mortgage Loan, will be liable to

Lender as the borrower on the Note upon Closing.

“Application” means a completed credit application for a Mortgage Loan, the terms and conditions of which

Lender shall specify and provide to the Entity, including without limitation, terms and conditions relating to

the principal amount, credit terms, rates, security and other requirements.

“Entity” means the loan originator set forth above who generated the Application and submitted it to Lender.

“Closing,” “Close” or “Closed” means the funding of a Mortgage Loan by Lender.

“Fee Agreement” means a written disclosure and fee agreement between Entity and each Applicant

establishing the Entity’s compensation for its services and the payment thereof.

“Investor” means the owner of the Mortgage Loan after it has been sold on the secondary market.

“Lender” means Carrington Mortgage Services, LLC, the mortgage company that may agree to fund the

Mortgage Loan.

“Mortgage” means the document or documents evidencing a security interest in or lien on the Mortgaged

Property and any other collateral securing repayment of the Note, including without limitation any mortgage,

deed of trust, deed to secure debt or security deed.

BANK/CREDIT UNION AGREEMENT

Carrington Mortgage Services, LLC Page 2 of 14 1610 E. St Andrew Place, Suite B-150 Santa Ana, CA 92705 Rev 10/22/13

“Mortgage Loan” means a residential mortgage loan secured by a first or second lien on the Mortgaged

Property, evidenced by a Note, Mortgage, and any other documents or instruments evidencing borrower’s

indebtedness and the collateral securing repayment thereof.

“Mortgage Loan Program” means the criteria established by Lender and/or an Investor, as reflected by

Lender’s guidelines, setting forth those Mortgage Loans available to eligible, prospective borrowers for

Closing in accordance with the terms of this Agreement.

“Mortgaged Property” means the residential real property improved by a one- to- four family dwelling

securing payment of the related Mortgage Loan.

“Note” means the promissory note evidencing a borrower’s obligation to repay a Mortgage Loan.

“Underwrite” or “Underwriting” means the examination of an Applicant’s Application, credit history, income

and financial resources, assets and appraisal for the purpose of determining whether to extend credit to the

Applicant.

ARTICLE 2 DUTIES OF ENTITY

2.1 Entity shall take Applications and collect financial information for Applicants at its offices in its

own name through its employees, agents and independent contractors.

2.2 If the Entity contracts out for services through a third party service, such as contract processing,

the Entity is ultimately responsible for the actions, errors and omissions of contract processor’s

actions relative to the loan file, loan documents, financial documents and the Applicant.

2.3 Entity shall comply with the procedures established by Lender for the submission of Applications

under the Mortgage Loan Programs available to the Entity. Entity shall be responsible for

determining whether each Application meets the terms and requirements of the available

Mortgage Loan Programs, and Lender shall have no obligation to accept submission of any

Application for Underwriting that does not fully comply with the terms and requirements of the

applicable Mortgage Loan Program.

2.4 Entity shall provide to Lender, at its sole cost and expense for each Mortgage Loan submitted,

the Application signed by Applicant, the appraisal, such credit and financial information necessary

to investigate, Underwrite and fully review the Application, and any and all other documents

required or requested by Lender. Entity shall assist Lender in obtaining any additional information

needed by Lender in order to facilitate the Closing of the Mortgage Loan. The Application and all

other documents submitted to Lender in connection with a proposed Mortgage Loan shall

become the property of Lender. All information submitted to the Lender shall be independently

verified and may be declined at Lender’s sole discretion. Entity shall have no authority

whatsoever to negotiate any terms or conditions of a Mortgage Loan on Lender’s behalf.

2.5 Entity shall analyze Applicant’s income and indebtedness, and determine the maximum

reasonable Mortgage Loan obligations that Applicant can bear that provide benefit to Applicant.

Entity shall explain to Applicant how the housing costs and monthly payments would vary under

each Mortgage Loan Program and shall assist Applicant in determining the appropriate Mortgage

Loan Program.

BANK/CREDIT UNION AGREEMENT

Carrington Mortgage Services, LLC Page 3 of 14 1610 E. St Andrew Place, Suite B-150 Santa Ana, CA 92705 Rev 10/22/13

2.6 Entity shall keep the Applicant apprised of Applicant’s status with their Application and

communicate any changes within a reasonable amount of time. Entity shall assist the Applicant

with understanding and clearing any credit problems and maintain regular contact with the

Applicant, real estate agents and Lender at all times.

2.7 Entity has no authority to obligate, commit or bind Lender to any agreement for any purpose

without Lender’s prior written consent, and the Entity shall not represent or warrant to any

Applicant that Lender has finally approved, or will approve or Close, any Mortgage Loan until

Lender so notifies the Entity in writing.

2.8 To the extent approved by Lender, Entity shall provide to Applicant any and all federal, state and

local disclosures required by law, rule or regulation, including without limitation the Good Faith

Estimates required under the Real Estate Settlement and Procedures Act of 1974, 12 U.S.C. §§

2601 et seq. (“RESPA”), and any disclosure required under the Truth in Lending Act, 15 U.S.C.

§§ 1601 et seq., as implemented by Regulation Z (“TILA”), the Fair Credit Reporting Act, 15

U.S.C. §§ 1681 et seq. (“FCRA”), and the Equal Credit Opportunity Act, 15 U.S.C. §§ 1691 et

seq., as implemented by Regulation B (“ECOA”).

2.9 Entity shall comply with all federal, state and local laws, rules and regulations, including the

disclosure requirements and prohibitions contained therein, applicable to the conduct of its

business, including, without limitation, the following: (i) ECOA and Regulation B, (ii) the Fair

Housing Act, 42 U.S.C. §§ 3601 et seq. (“FHA”) and the regulations promulgated pursuant

thereto, (iii) the Home Mortgage Disclosure Act, 12 U.S.C. §§ 2801 et seq., (“HMDA”) and

Regulation C, (iv) FCRA, (v) RESPA and Regulation X, (vi) TILA and Regulation Z, (vii) the Home

Ownership and Equity Protection Act, 15 U.S.C. §§ 1601 et seq., (viii) the Flood Disaster

Protection Act, 42 U.S.C. §§ 4001 et seq., (ix) the Gramm-Leach-Bliley Act, (x) Consumer

Finance Protection Bureau, (xi) state, county and municipal anti-predatory lending laws and

ordinances, (xii) state mortgage laws, and (xiii) any and all other laws, rules and regulations

applicable to the Entity, including those governing fraud, compensation, consumer credit

transactions, predatory and abusive lending and mortgage banks and credit unions. In

connection with ECOA and Regulation B, Entity shall not discourage or pre-screen any Applicant

or in any other manner violate the terms of the ECOA and Regulation B. Entity shall ensure that

all compensation that it receives in connection with any transaction complies with the loan

origination compensation requirements set forth in Regulation Z. Entity shall maintain available

for Lender’s inspection, and shall deliver to Lender upon demand, evidence of compliance with all

federal, state and local requirements.

2.10 Entity warrants that it understands the distinction between an “application” and an “inquiry” within

the meaning of HMDA and ECOA, and that, unless otherwise set forth in this Agreement, or

unless notified by Lender, it is responsible for complying with the recordkeeping and disclosure

requirements of those laws with respect to “applications” that it receives. Entity shall timely notify

Lender of all “applications” that it has placed with Lender. Entity shall be responsible for

determining if an Application is “incomplete” or has been “withdrawn” as those terms are

construed under HMDA and ECOA, and shall timely apprise Lender of these decisions. In such

circumstances, Entity will complete and send the appropriate notice to Applicant in accordance

with ECOA and all applicable law, with a copy to Lender. In the event that Lender decides that it

will not approve a particular Mortgage Loan submitted by the Entity, Lender will not deliver to any

Applicant an “Adverse Action” notice. Rather, Lender shall deliver a completed Adverse Action

notice to the Entity specifying the reasons Lender has declined to Close the Mortgage Loan.

Entity shall then send the Adverse Action notice to Applicant in compliance with ECOA and any

other applicable federal, state and local laws.

BANK/CREDIT UNION AGREEMENT

Carrington Mortgage Services, LLC Page 4 of 14 1610 E. St Andrew Place, Suite B-150 Santa Ana, CA 92705 Rev 10/22/13

2.11 Entity shall promptly notify Lender if (A) any substantial change in the ownership, financial

condition or management of the Entity occurs, within thirty (30) days of change, (B) Entity

relocates their office(s) notification will occur within fifteen (15) days, (C) Entity knows or has

reason to believe that any information in any Application or other document delivered to Lender is

or becomes untrue or fails to state any material fact or (D) any government or other agency has

made any adverse finding or taken any adverse actions with respect to Entity, or its owners,

directors, officers or employees.

2.12 Entity shall execute and deliver all such instruments and take all such actions as Lender may

reasonably request from time to time in order to effect the purposes of this Agreement and to

consummate the transactions contemplated hereby. Without limiting the generality of the

foregoing, Entity shall cooperate with Lender with respect to a submitted Mortgage Loans after

Closing, if Lender requests Entity’s assistance with a non-performing or defaulted Mortgage Loan.

The obligations under this Section 2.12 are continuing and shall survive the termination of this

Agreement.

ARTICLE 3 DUTIES OF LENDER

3.1 Lender shall Underwrite or cause to be Underwritten every eligible Application submitted pursuant

to this Agreement. Lender shall have no obligation to issue a commitment, or other comparable

document for, or to Close, a Mortgage Loan which it determines, in its sole discretion, does not

meet Lender or Investors’ Underwriting requirements. Lender, in its sole discretion, may decline

any Application that does not comply with the terms of this Agreement or does not meet Lender

or Investors’ guidelines. Lender shall notify Entity promptly of such declination.

3.2 Lender and Entity agree that Lender may rely on the information, authenticity and accuracy of all

signatures and information supplied to it by Entity in connection with each Mortgage Loan,

including without limitation any Application. Lender’s decision not to conduct an independent

investigation with respect to the information, authenticity and accuracy of all signatures and

information provided to it by Entity shall not affect or modify the representations, warranties and

covenants made by Entity under Article 5 or the rights available to Lender for any breach thereof.

3.3 If Lender determines that the Application meets its Underwriting standards, it may, in its sole

discretion, issue a commitment or other comparable document in its name to Applicant setting

forth the terms and conditions under which it will Close the Mortgage Loan, provided that nothing

in this Agreement shall be construed as creating any obligation on the part of Lender to accept or

approve such Application or to Close any such Mortgage Loan. If Lender determines that the

Mortgage Loan does not meet its Underwriting standards, it will issue a notice of declination to

the Applicant in compliance with all federal, state and local laws, rules and regulations. Lender

shall have no obligation or liability to Entity for any Mortgage Loan which is not approved by

Lender or for any delays in determining whether a Mortgage Loan meets Underwriting standards.

3.4 Upon the issuance of a commitment or other comparable document in Lender’s name to

Applicant, Lender shall proceed with the Closing of the Mortgage Loan under the terms and

conditions of its commitment or other comparable document to Applicant, and Entity shall provide

such assistance in this regard as required by Lender so as to close the Mortgage Loan in a timely

and efficient manner.

BANK/CREDIT UNION AGREEMENT

Carrington Mortgage Services, LLC Page 5 of 14 1610 E. St Andrew Place, Suite B-150 Santa Ana, CA 92705 Rev 10/22/13

ARTICLE 4 RATES AND LOCK-INS

Entity shall comply with the guidelines that Lender may distribute from time to time concerning interest

rates and lock-ins that apply to a particular Mortgage Loan Program offered by Lender.

ARTICLE 5 REPRESENTATIONS, WARRANTIES, AND COVENANTS OF ENTITY

As an inducement to Lender to enter into this Agreement and to consummate the Closing of each

Mortgage Loan from an Application submitted by Entity, Entity hereby represents, warrants and

covenants to Lender, as of the date of execution of this Agreement, as of the date that Entity submits

each Application to Lender for approval and as of the date of Closing of each Mortgage Loan, as follows:

5.1 Entity is a natural person or an entity, as the case may be, as set forth in the first paragraph of

this Agreement. Entity is duly organized, validly existing and in good standing under the laws of

the state of its organization. Entity has the full legal power, capacity and authority to enter into

this Agreement and any related agreements and instruments and to perform its obligations

thereunder. The execution and delivery of this Agreement and any related agreements and

instruments, and the consummation of the transactions contemplated thereby, have been duly

and validly authorized by all necessary action. This Agreement and any related agreements and

instruments constitute the legal, valid and binding obligations of the Entity and are enforceable

against the Entity in accordance with their terms.

5.2 Entity is properly licensed, or is exempt from licensing, and is qualified to do business in all

jurisdictions where it originates Mortgage Loans, where it conducts the activities contemplated by

this Agreement and where its business or operations otherwise require such qualification, and is

in full compliance with the Secure and Fair Enforcement for Mortgage Licensing Act, 12 U.S.C. §§

5101 et seq., to the extent applicable. Entity has obtained and shall maintain in good standing all

lender’s and/or Entity’s licenses to originate first and/or subordinate lien residential mortgage

loans, filings, permits, foreign qualifications, business licenses and other licenses as may be

required by applicable, federal, state or local laws, rules or regulations. Copies of all lender’s

and/or Entity’s licenses held by the Entity and that authorize Entity to engage in the business of

residential mortgage loans have been, and renewals will be, provided to Lender. Entity shall

promptly notify Lender of the cancellation, renewal or issuance of any Lender’s and/or Entity’s

mortgage loan licenses and shall promptly provide a copy thereof to Lender upon receipt of such