the value of patents for vc-backed firms

TRANSCRIPT

The Value of Patents for VC-Backed Firms: Preliminary evidence from Semiconductors,

Software, and Medical Devices

Rosemarie ZiedonisRoss School of Business, University of Michigan

based on joint research with David Hsu, Wharton

Symposium on Intellectual Property and Entrepreneurship, Berkeley Center for Law andTechnology and Kauffman Foundation, Boalt School of Law

March 2008

Sample & DataSample & Data

VC-backed U.S. startups founded 1987-99• semiconductor devices (Information Technology)• medical devices (Life Sciences)• software (Information Technology)

Primary sources:• DowJones VentureSource database• Delphion.com• Lexis/Nexis, Factiva

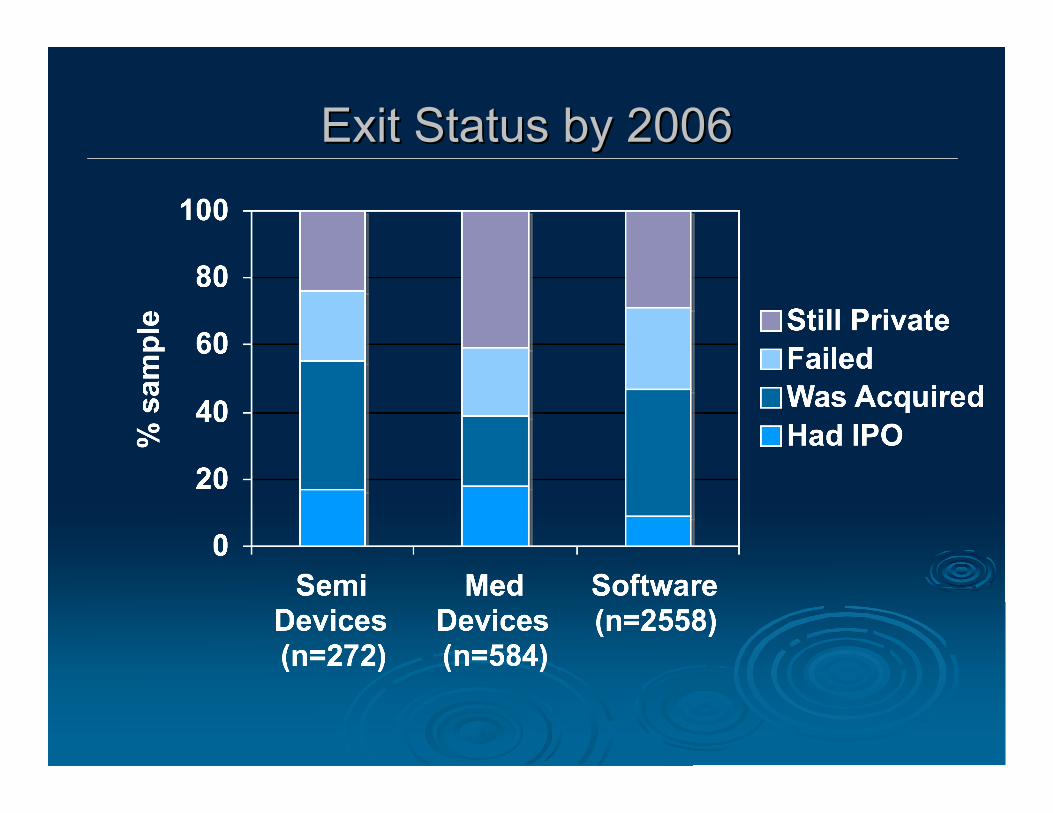

Exit Status by 2006Exit Status by 2006

What % of these firms patent?What % of these firms patent?

% with U.S. patents granted% with U.S. patents granted

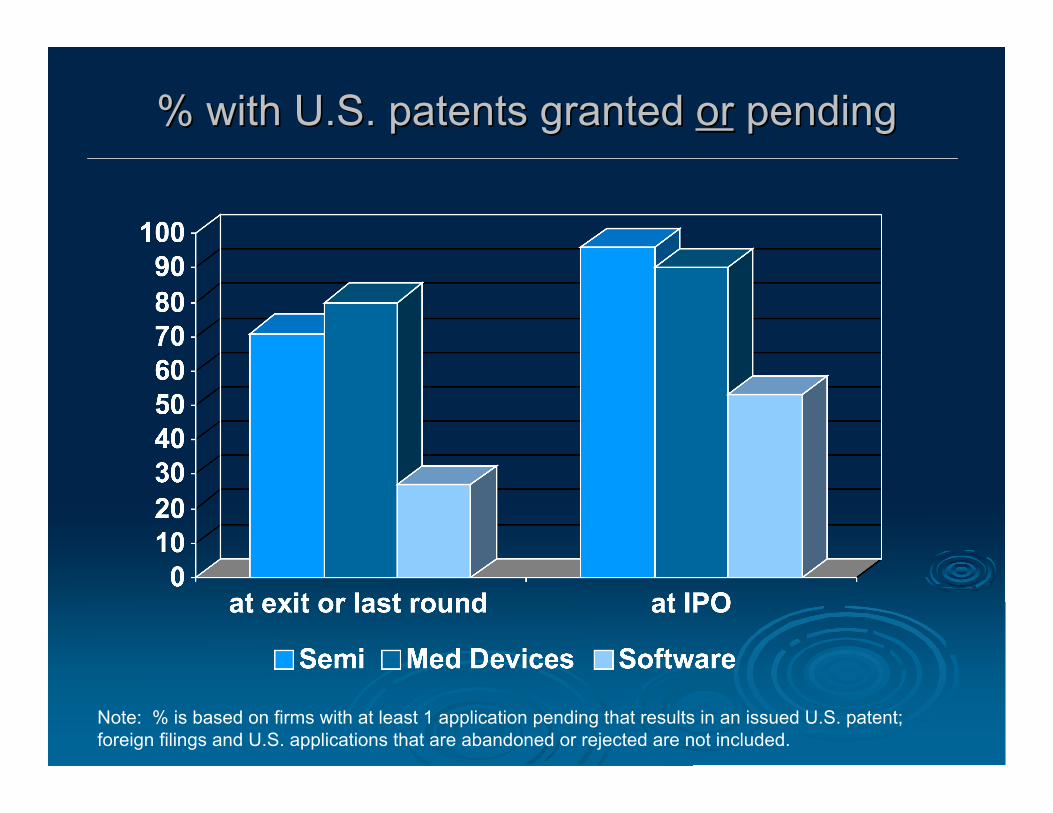

% with U.S. patents granted % with U.S. patents granted oror pending pending

Note: % is based on firms with at least 1 application pending that results in an issued U.S. patent;foreign filings and U.S. applications that are abandoned or rejected are not included.

% with U.S. patents pending at IPO% with U.S. patents pending at IPO(IPO subset only; 3-yr moving average)(IPO subset only; 3-yr moving average)

How How intensivelyintensively do startups in these do startups in thesesectors seek patent protection?sectors seek patent protection?

Rough proxy: What share of financial resources do theyRough proxy: What share of financial resources do theydevote to the task?devote to the task?

Ave # successful U.S. applications filed per $10Ave # successful U.S. applications filed per $10million raised in pre-exit funding roundsmillion raised in pre-exit funding rounds

Note: Cumulative amount raised is measured in constant 2000-year dollars.

A Closer Look “within IT”

Estimates #1:

Patent “Propensity”

Is there a significant difference betweensoftware and semiconductors in the

propensities to file patents?

Are there important changes over time?

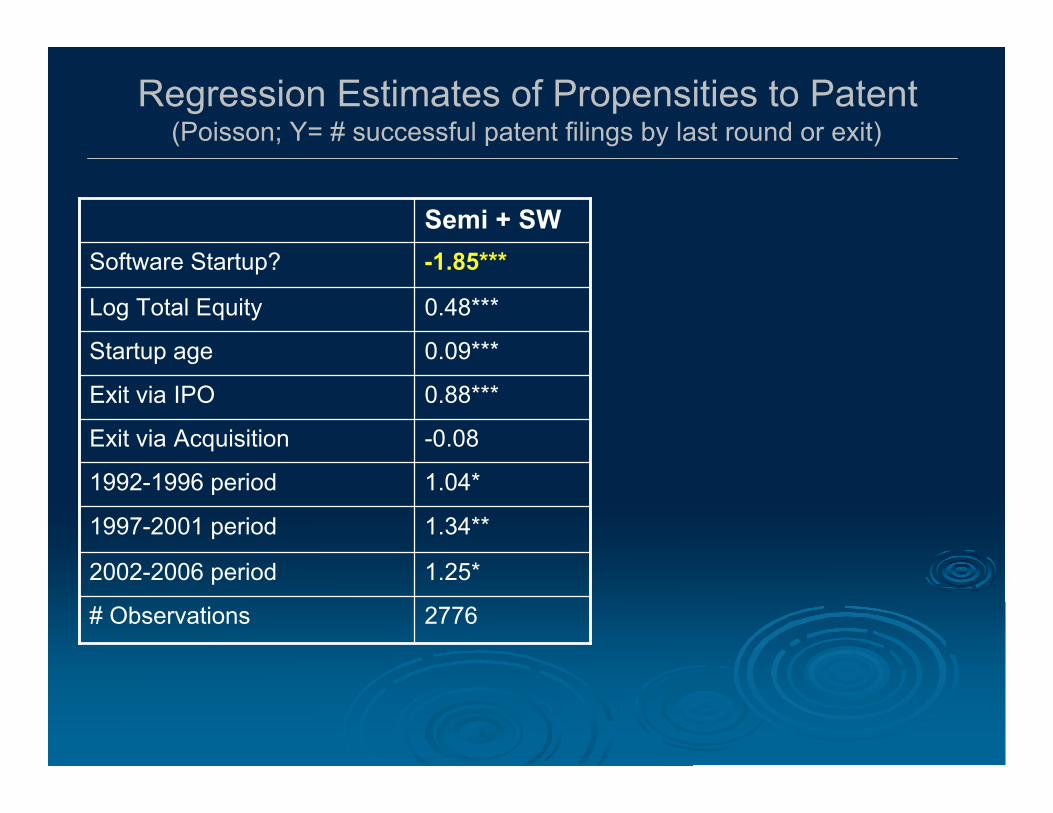

Regression Estimates of Propensities to Patent(Poisson; Y= # successful patent filings by last round or exit)

2776# Observations

1.25*2002-2006 period

1.34**1997-2001 period

1.04*1992-1996 period

-0.08Exit via Acquisition

0.88***Exit via IPO

0.09***Startup age

0.48***Log Total Equity

Software Startup?

Semi + SW

Regression Estimates of Propensities to Patent(Poisson; Y= # successful patent filings by last round or exit)

2776# Observations

1.25*2002-2006 period

1.34**1997-2001 period

1.04*1992-1996 period

-0.08Exit via Acquisition

0.88***Exit via IPO

0.09***Startup age

0.48***Log Total Equity

-1.85***Software Startup?

Semi + SW

Regression Estimates of Propensities to Patent(Poisson; Y= # successful patent filings by last round or exit)

25062702776# Observations

1.70**1.301.25*2002-2006 period

1.90**1.201.34**1997-2001 period

1.371.121.04*1992-1996 period

0.01-0.20-0.08Exit via Acquisition

1.12***0.69***0.88***Exit via IPO

0.09***0.10***0.09***Startup age

0.53***0.40***0.48***Log Total Equity

-----1.85***Software Startup?

Software OnlySemi OnlySemi + SW

Regression Estimates of Propensities to Patent(Poisson; Y= # successful patent filings by last round or exit)

25062702776# Observations

1.70**1.301.25*2002-2006 period

1.90**1.201.34**1997-2001 period

1.371.121.04*1992-1996 period

0.01-0.20-0.08Exit via Acquisition

1.12***0.69***0.88***Exit via IPO

0.09***0.10***0.09***Startup age

0.53***0.40***0.48***Log Total Equity

-----1.85***Software Startup?

Software OnlySemi OnlySemi + SW

Estimates #2:Estimates #2:

Patent Patent ““ValueValue””

[goal = to estimate the magnitude with which, if at[goal = to estimate the magnitude with which, if atall, changes in a startupall, changes in a startup’’s patent filings ares patent filings areassociated with upward adjustments in theassociated with upward adjustments in the

estimated net present value of the firm]estimated net present value of the firm]

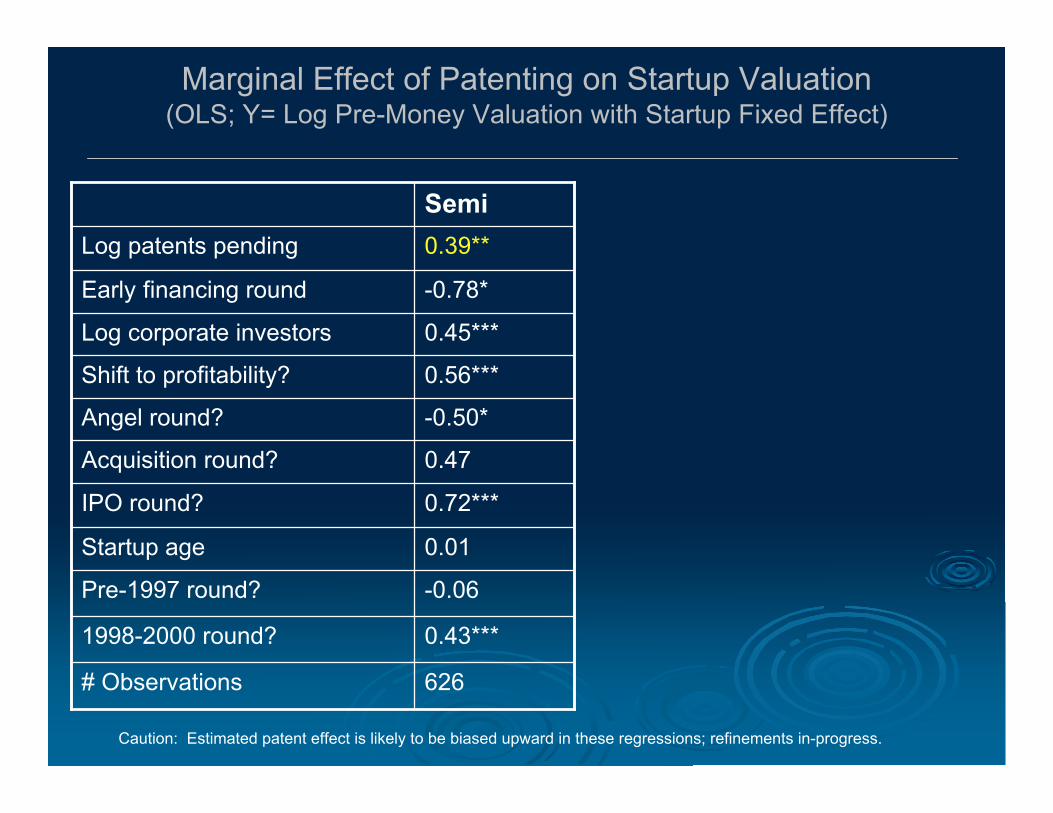

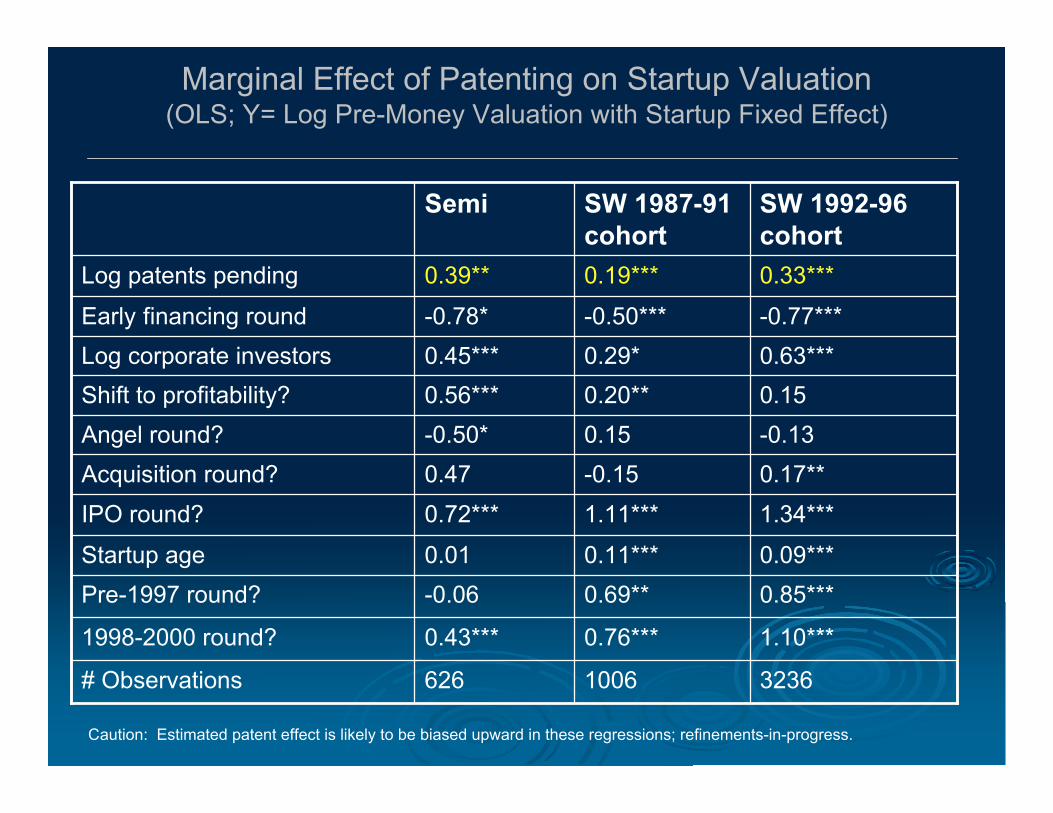

Marginal Effect of Patenting on Startup Valuation(OLS; Y= Log Pre-Money Valuation with Startup Fixed Effect)

-0.06Pre-1997 round?

0.43***1998-2000 round?

626# Observations

0.01Startup age

0.72***IPO round?

0.47Acquisition round?

-0.50*Angel round?

0.56***Shift to profitability?

0.45***Log corporate investors

-0.78*Early financing round

0.39**Log patents pending

Semi

Caution: Estimated patent effect is likely to be biased upward in these regressions; refinements in-progress.

Marginal Effect of Patenting on Startup Valuation(OLS; Y= Log Pre-Money Valuation with Startup Fixed Effect)

0.85***0.69**-0.06Pre-1997 round?

1.10***0.76***0.43***1998-2000 round?

32361006626# Observations

0.09***0.11***0.01Startup age

1.34***1.11***0.72***IPO round?

0.17**-0.150.47Acquisition round?-0.130.15-0.50*Angel round?0.150.20**0.56***Shift to profitability?0.63***0.29*0.45***Log corporate investors-0.77***-0.50***-0.78*Early financing round

0.33***0.19***0.39**Log patents pending

SW 1992-96cohort

SW 1987-91cohort

Semi

Caution: Estimated patent effect is likely to be biased upward in these regressions; refinements-in-progress.

SummarySummary• Considerable entrepreneurial-firm resources are devotedtoward the filing of patents, especially in the two devicesectors

• Within IT, an apparent “regime change” within software?• steady climb in % startups filing patents pre-IPO• significant increase in residual growth rate of patenting• younger cohorts appear to capture greater value fromowning patents than do older cohorts of software startups

• Patents clearly “matter” to many startups in all three sectors.But why? How do patent filings or awards affect the financingand innovation activities of new ventures?