global vc investment landscape cost to start enterprise ...€¦ · cost to start enterprise and...

TRANSCRIPT

Venture Capital Insights® – 2Q14

Global VC investment landscapeCost to start enterprise and consumerventure-backed companies

August 2014

Venture Capital Insights® – 2Q14Page 1

Insights development team

► Bryan Pearce, Global Leader, Entrepreneur Of The Year TM and GlobalVenture Capital Advisory Group, EY

► Jeff Grabow, United States, Venture Capital Leader, EY► Sandra Feldner Vandergriff, Americas Venture Capital Advisory Group, EY► Shanta Kumari, EY Knowledge, EY► Aseem Goyal, EY Knowledge, EY► Prof. George Foster, Graduate School of Business, Stanford University► Dr. Martin Haemmig, Adjunct Professor, Globalization of Venture Capital,

CeTIM and former Senior Advisor on Venture Capital,Stanford University (SPRIE)

► Prof. Steven Kaplan, Graduate School of Business, University of Chicago

*All data contained in this is sourced to Dow Jones VentureSource unless otherwise noted.

Venture Capital Insights® – 2Q14Page 2

Venture Capital Insights

This edition of Venture Capital Insights analyzes global VC investments and exits from 2008 through1H14. The presentation also provides an overview of the dollars required to scale a company in theenterprise and consumer sectors and current ownership status of those venture-funded companies.

Content overview:1 Global VC investments

2 Global VC exit landscape – IPO and M&A

3 VC investment in enterprise and consumer segments by round class

3.1 Cost to start up enterprise and consumer venture-backed companies

3.2 VC investment in enterprise and consumer segments by geography

3.3 Median amount raised and valuations by round class (by year of investment)

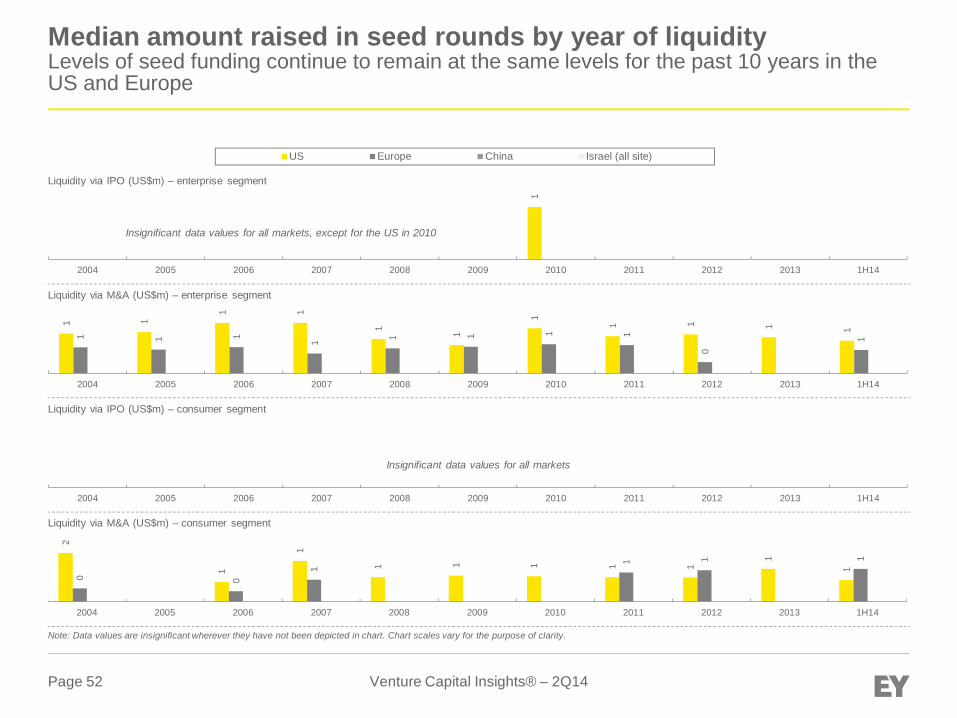

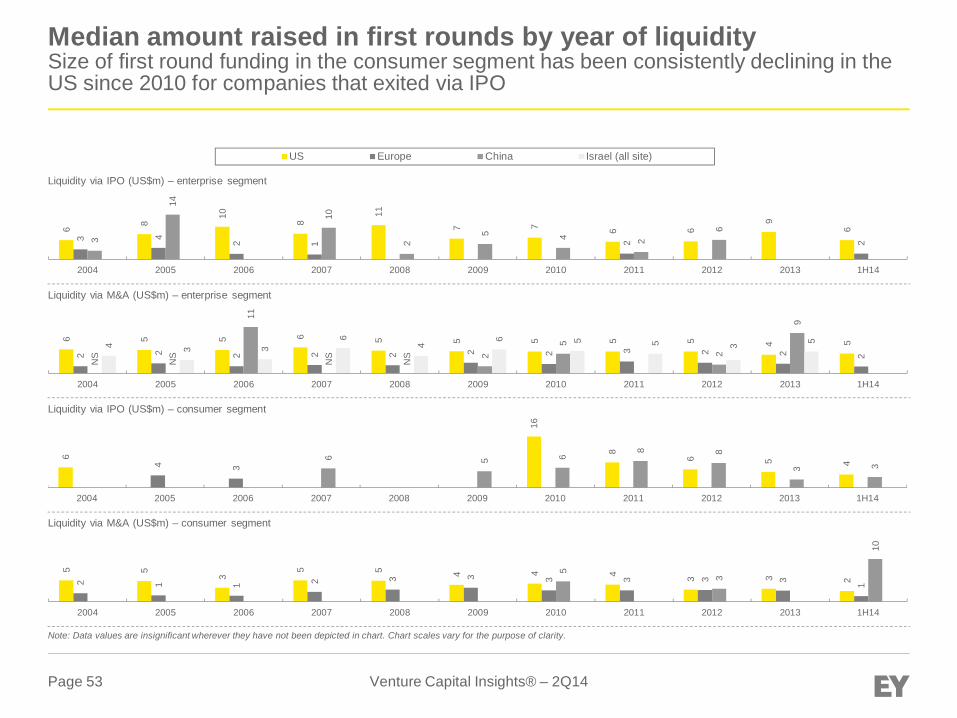

3.4 Median amount raised and valuations by round class (by year of liquidity)

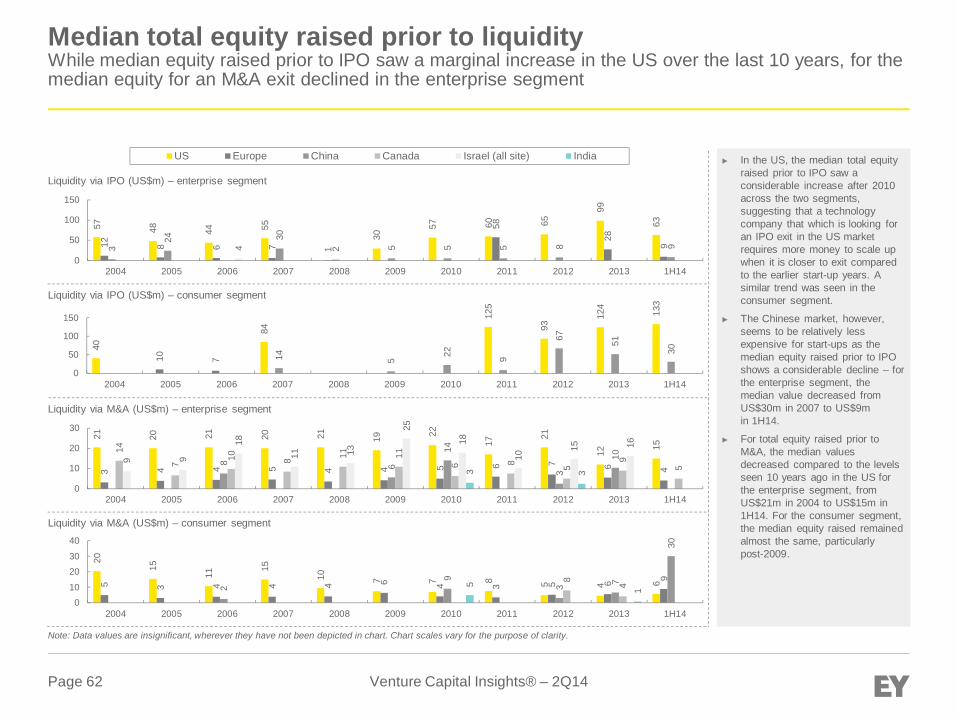

3.5 Median total equity raised prior to liquidity, valuations and time to liquidity

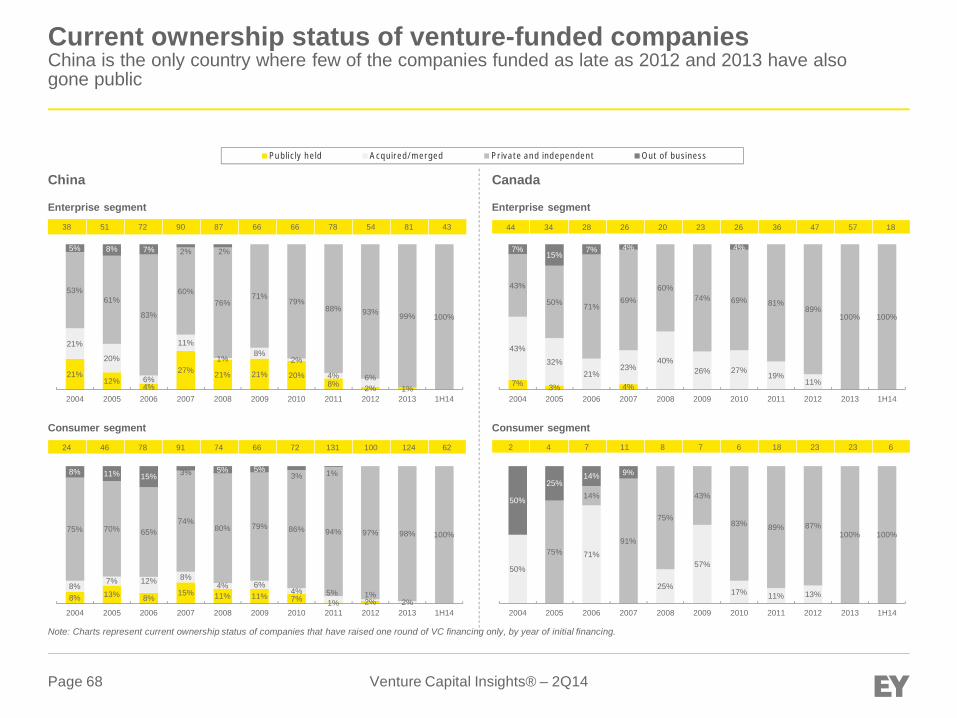

4 Current ownership status of venture-funded companies

Section 1: Global VC investment landscapeAnalysis by geography, hotbed, sectors, stages of development and round classes

Venture Capital Insights® – 2Q14Page 4

Section 1: Global venture capital investment landscapeSummary

Global VC investment activity

► Globally, 2Q14 recorded the highest quarterly VC investments US$21.1b since 1Q01 levels. Subsequently, VCinvestments for the first half of 2014 reached US$37.8b, the highest first-half total since 2001.

► VC investment activity saw significant growth in the dollar amounts invested across all markets. Compared to the1Q14, the dollar amount invested in 2Q14 was up 26%, with an increase of 3% in number of rounds.

► Europe saw the highest increase in dollars raised, up 42% for 2Q14 versus the previous quarter; the US and Chinasaw increases of 21% and 19%, respectively, for the same period.

► The Bay Area continues to account for close to half of the dollar amount invested in the 15 major VC hotbeds: 49% for1Q14 and 47% in 2Q14. The top two deals of the quarter were San Francisco-based companies, one of which was aUS$1.2b investment in Uber Technologies Inc., at a post-valuation of US$18.2b.

► Consumer services and business and financial services were the two most attractive sectors for 2Q14 in valueand volume.

► Companies operating at revenue generation stage continue to attract larger investments, primarily in the later –round classes.

► For1H14, median deal values at later round class were at their all-time high for all VC markets, except for China.However, China still recorded the highest median value at this stage, globally.

► By stage of development, 1H14 saw a significant increase in median values across all stages, particularly in the US,Europe and China.

Venture Capital Insights® – 2Q14Page 5

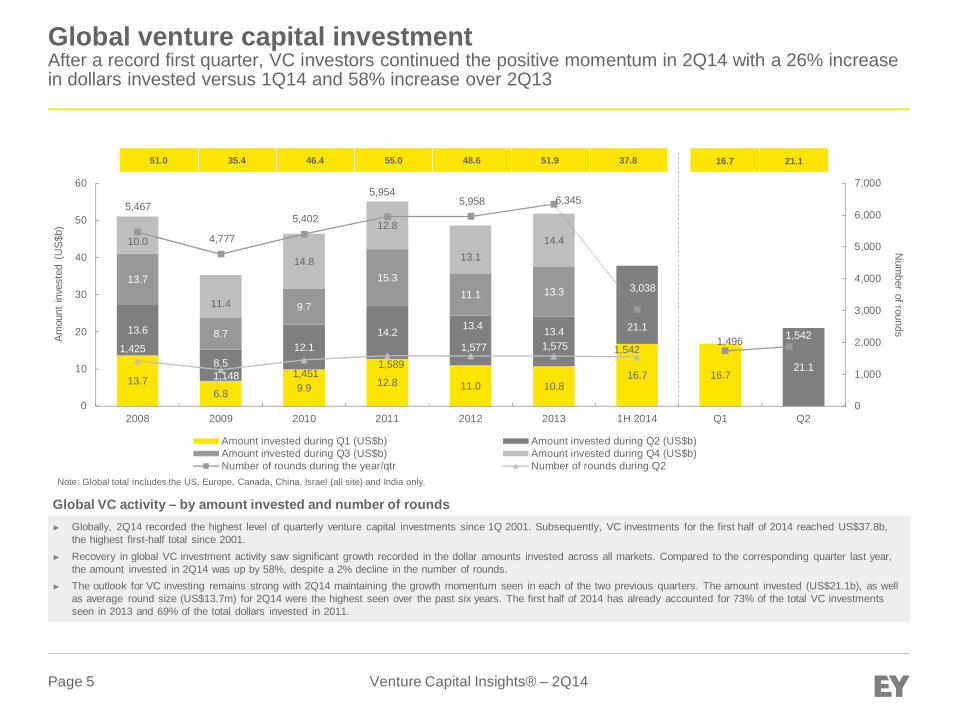

► Globally, 2Q14 recorded the highest level of quarterly venture capital investments since 1Q 2001. Subsequently, VC investments for the first half of 2014 reached US$37.8b,the highest first-half total since 2001.

► Recovery in global VC investment activity saw significant growth recorded in the dollar amounts invested across all markets. Compared to the corresponding quarter last year,the amount invested in 2Q14 was up by 58%, despite a 2% decline in the number of rounds.

► The outlook for VC investing remains strong with 2Q14 maintaining the growth momentum seen in each of the two previous quarters. The amount invested (US$21.1b), as wellas average round size (US$13.7m) for 2Q14 were the highest seen over the past six years. The first half of 2014 has already accounted for 73% of the total VC investmentsseen in 2013 and 69% of the total dollars invested in 2011.

Global VC activity – by amount invested and number of rounds

Global venture capital investmentAfter a record first quarter, VC investors continued the positive momentum in 2Q14 with a 26% increasein dollars invested versus 1Q14 and 58% increase over 2Q13

13.76.8 9.9 12.8 11.0 10.8

16.7 16.7

13.6

8.512.1

14.2 13.4 13.4 21.1

21.1

13.7

8.7

9.7

15.311.1 13.3

10.0

11.4

14.8

12.8

13.114.4

5,467

4,777

5,402

5,9545,958 6,345

3,038

1,425

1,148 1,4511,589

1,577 1,575 1,542

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

0

10

20

30

40

50

60

2008 2009 2010 2011 2012 2013 1H 2014 Q1 Q2

Num

berofrounds

Am

ount

inve

sted

(US

$b)

Amount invested during Q1 (US$b) Amount invested during Q2 (US$b)Amount invested during Q3 (US$b) Amount invested during Q4 (US$b)Number of rounds during the year/qtr Number of rounds during Q2

Note: Global total includes the US, Europe, Canada, China, Israel (all site) and India only.

51.0 35.4 46.4 55.0 48.6 51.9 37.8 16.7 21.1

1,496 1,542

Venture Capital Insights® – 2Q14Page 6

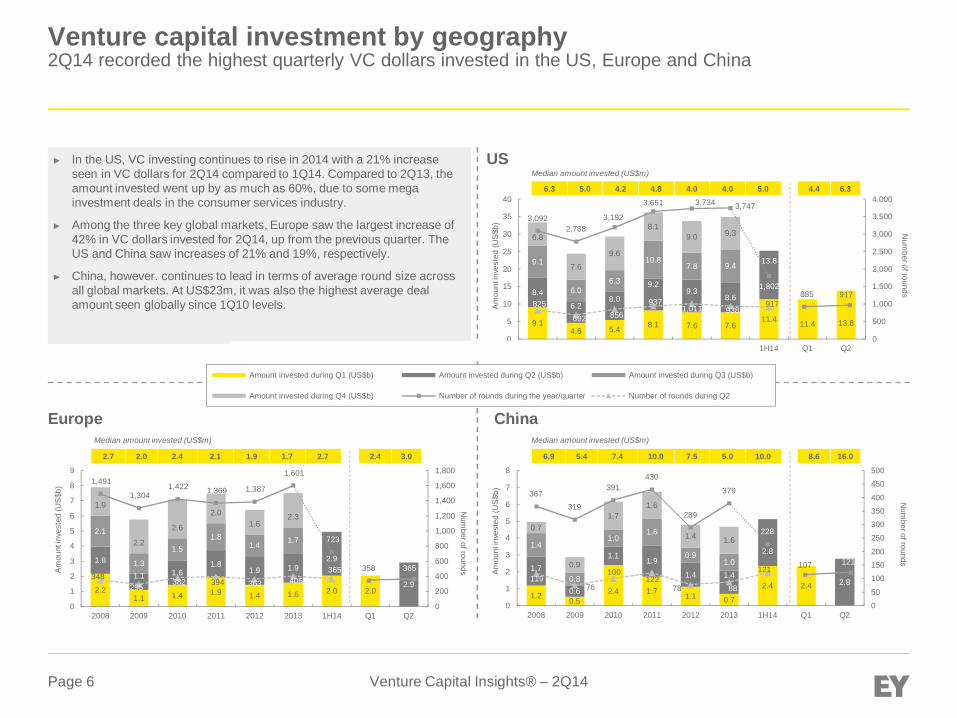

US

Europe

► In the US, VC investing continues to rise in 2014 with a 21% increaseseen in VC dollars for 2Q14 compared to 1Q14. Compared to 2Q13, theamount invested went up by as much as 60%, due to some megainvestment deals in the consumer services industry.

► Among the three key global markets, Europe saw the largest increase of42% in VC dollars invested for 2Q14, up from the previous quarter. TheUS and China saw increases of 21% and 19%, respectively.

► China, however. continues to lead in terms of average round size acrossall global markets. At US$23m, it was also the highest average dealamount seen globally since 1Q10 levels.

China

Venture capital investment by geography2Q14 recorded the highest quarterly VC dollars invested in the US, Europe and China

9.14.6 5.4 8.1 7.6 7.6

11.4 11.4 13.8

8.4

6.28.0

9.29.3

8.6

13.89.1

6.06.3

10.87.8 9.4

6.8

7.6

9.6

8.19.0 9.3

3,0922,788

3,192

3,651 3,734 3,747

1,802

825

692 856937

1,011 938917

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

0

5

10

15

20

25

30

35

40

2008 2009 2010 2011 2012 2013 1H14 Q1 Q2

Num

berofrounds

Am

ount

inve

sted

(US

$b)

6.3 5.0 4.2 4.8 4.0 4.0 5.0

Median amount invested (US$m)

4.4 6.3

885 917

2.21.1 1.4 1.9 1.4 1.6 2.0 2.0

1.8

1.1 1.61.8

1.9 1.92.9

2.9

2.1

1.3

1.51.8

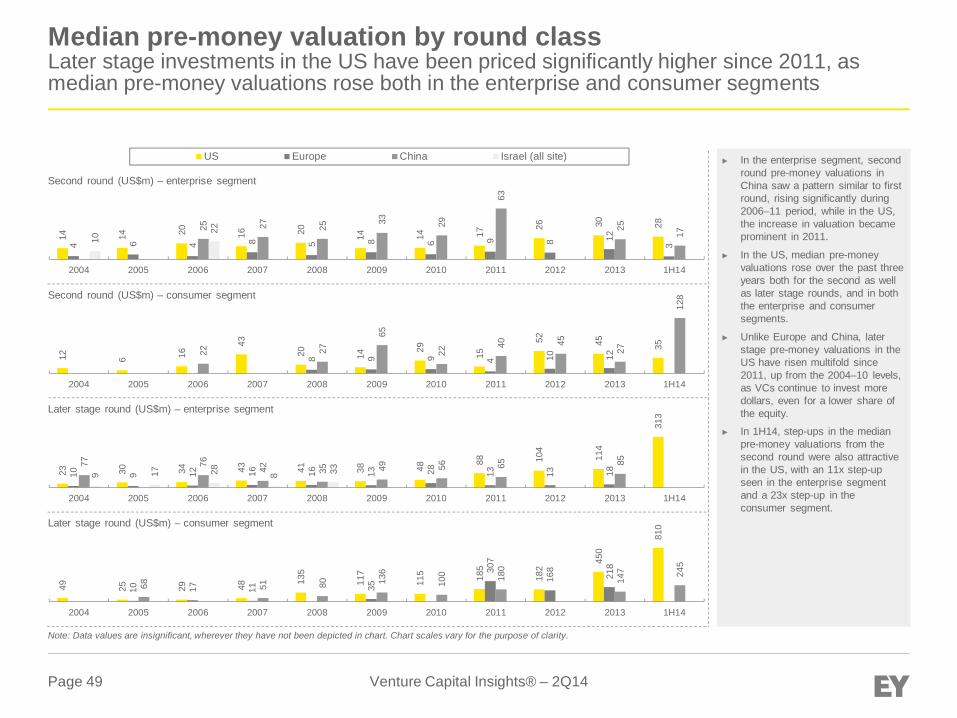

1.4 1.7

1.9

2.2

2.6

2.01.6

2.3

1,491

1,3041,422 1,369 1,387

1,601

723

348295

382 394 363 406365

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

0

1

2

3

4

5

6

7

8

9

2008 2009 2010 2011 2012 2013 1H14 Q1 Q2

Num

berofroundsAm

ount

inve

sted

(US

$b)

1.20.5

2.4 1.7 1.1 0.7

2.4 2.4

1.7

0.6

1.1 1.9

1.4 1.4

2.8

2.8

1.4

0.8

1.01.6

0.91.0

0.7

0.9

1.71.6

1.4 1.6

367319

391430

289

379

228

11976

100122

78 88

121

0

50

100

150

200

250

300

350

400

450

500

0

1

2

3

4

5

6

7

8

2008 2009 2010 2011 2012 2013 1H14 Q1 Q2

Num

berofrounds

Am

ount

inve

sted

(US

$b)

Median amount invested (US$m)Median amount invested (US$m)

2.7 2.0 2.4 2.1 1.9 1.7 2.7 2.4 3.0 6.9 5.4 7.4 10.0 7.5 5.0 10.0 8.6 16.0

358 365 107 121

050

Amount invested during Q1 (US$b) Amount invested during Q2 (US$b) Amount invested during Q3 (US$b)

Amount invested during Q4 (US$b) Number of rounds during the year/quarter Number of rounds during Q2

Venture Capital Insights® – 2Q14Page 7

Venture capital investment by geographyContinued recovery in amount invested by VCs was evident across all markets, although number ofdeals declined in Israel and Canada, compared to 1Q14

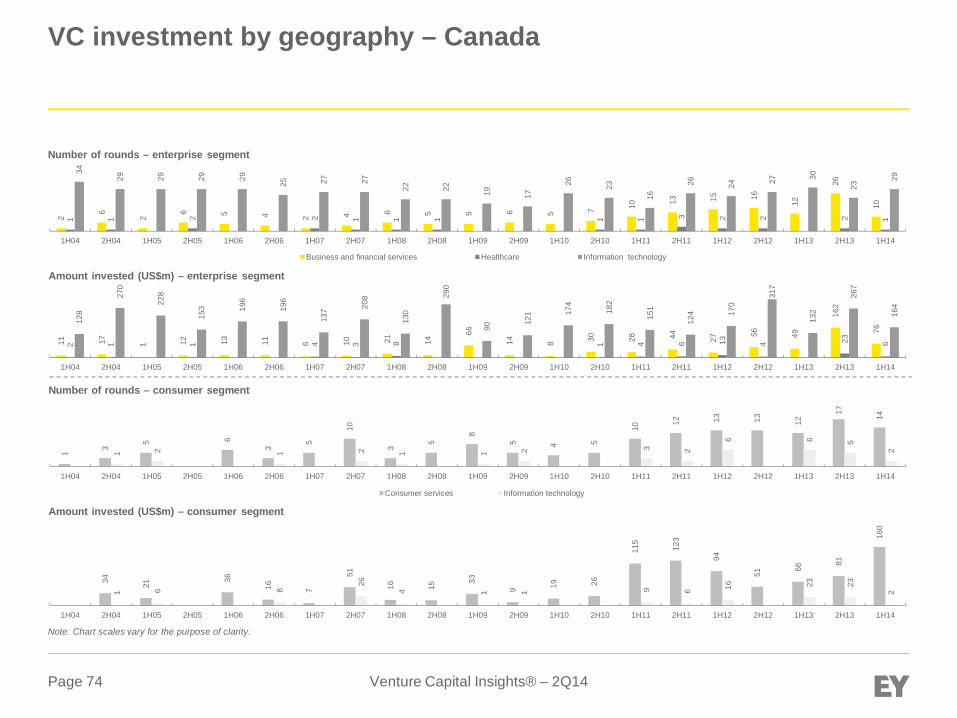

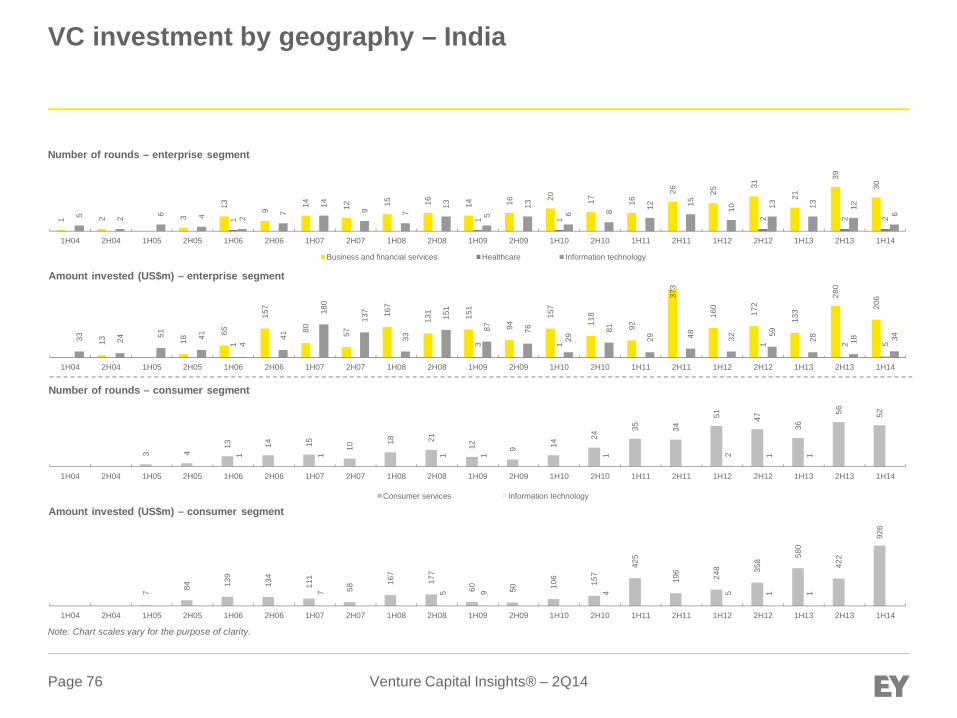

► Canada saw the steepest growth 134% in the amount of VC investment,compared to 1Q14, followed by India at 92%.

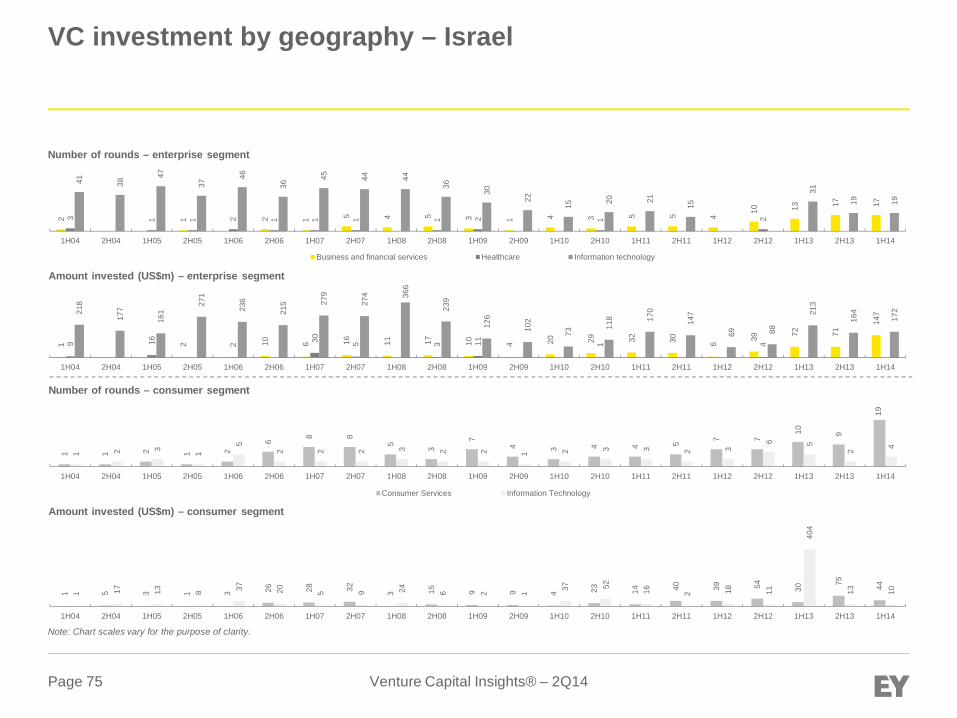

► Compared to 2Q13, Israel was the only market that saw a decline in VCinvestments, both in terms of deals and dollars. Compared to 1Q14,however, the amount invested rose by 6% on account of recovery inhealthcare and information technology (IT) sector.

► The outlook for VC investmenting in Canada and India is positive, with1H14 investments significantly exceeding 1H13 levels. However, Israel hasyet to cross 2013 halfway mark.

0.80.2 0.3 0.3 0.3 0.3 0.3 0.3

0.6

0.2

0.90.6

0.20.6 0.4

0.4

0.5

0.3

0.20.4

0.3

0.4

0.3

0.2

0.5 0.6

0.4

0.4

289

178

163 180 163196

96

75

41

5454

3352

42

0

50

100

150

200

250

300

350

0

1

2

3

2008 2009 2010 2011 2012 2013 1H 2014 Q1 Q2

Num

berofrounds

Am

ount

inve

sted

(US

$b)

0.2 0.1 0.20.4

0.2 0.2 0.2 0.2

0.10.1

0.2

0.4

0.2 0.2 0.40.4

0.30.1

0.4

0.3

0.3 0.30.2

0.2

0.2

0.1

0.30.4

11092

114

143151

182

80

27 26 25

37 40 40 38

0

20

40

60

80

100

120

140

160

180

200

0

1

2

2008 2009 2010 2011 2012 2013 1H 2014 Q1 Q2

Num

berofrounds

Am

ount

inve

sted

(US

$b)

0.2 0.2 0.2 0.3 0.4 0.4 0.4 0.4

0.9

0.1 0.20.4

0.30.6

0.8

0.8

0.4

0.1 0.2

0.4 0.4

0.5

0.2

0.30.3

0.4 0.4

0.4

11896

120

181

234240

109

3118 34

45 52 51 59

0

50

100

150

200

250

300

0

1

2

2008 2009 2010 2011 2012 2013 1H 2014 Q1 Q2

Num

berofrounds

Am

ount

inve

sted

(US

$b)

42 38

54 4250 59

Canada5.0 4.6 4.0 5.0 2.7 2.1 2.3

Median amount invested (US$m)

1.5 5.9

IndiaMedian amount invested (US$m)

7.0 4.2 6.4 5.0 3.7 3.9 4.1 3.0 5.0

Israel (all site)Median amount invested (US$m)

5.0 4.0 5.0 7.0 4.0 4.8 4.8 4.0 5.4

050

Amount invested during Q1 (US$b) Amount invested during Q2 (US$b) Amount invested during Q3 (US$b)

Amount invested during Q4 (US$b) Number of rounds during the year/quarter Number of rounds during Q2

Venture Capital Insights® – 2Q14Page 8

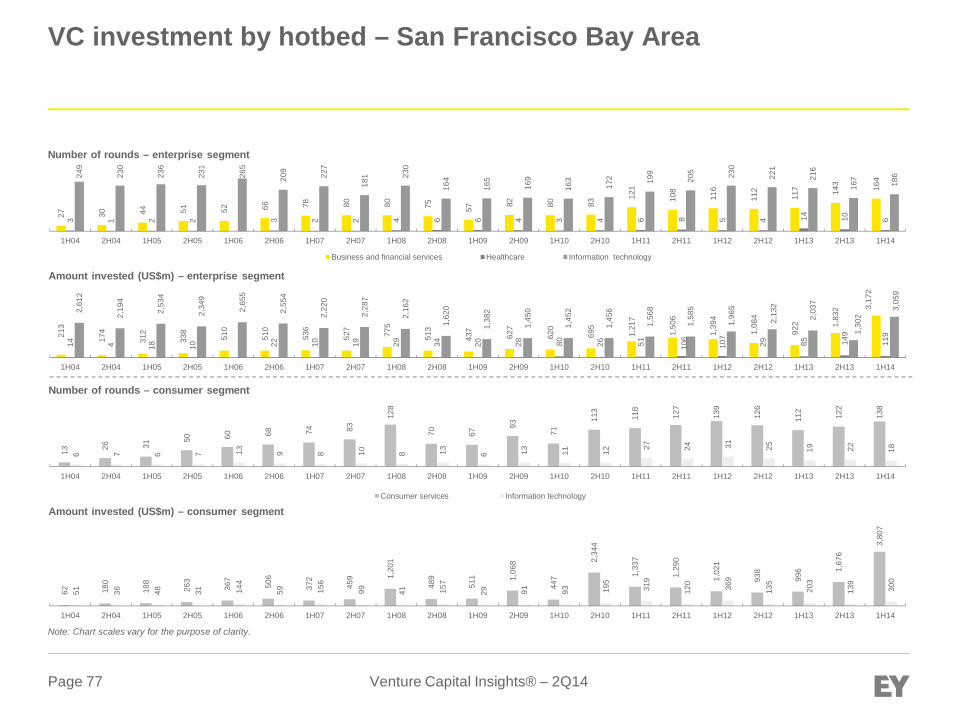

► The Bay Area continued to account for close to half of the dollar amount invested in the top 15 major VC hotbeds- -- 49% in 1Q14 and 47% in 2Q14, up from 2008–13 when itaccounted for less than 38% of the total dollars invested. The top two deals of the quarter were San Francisco-based companies, one of which was a US$1.2b investment inUber Technologies Inc., at a post-valuation of US$18.2b.

► Increased VC investing in India saw Bengaluru move up three ranks from 15th, for the first time since 2009. Beijing, the most attractive VC hotbed in the Asia-Pacific region,continues its climb and is now among in the top five.

Venture capital investment by hotbedBeijing was the only non-US destination among the top five VC hotbeds for 2Q14; the Bay Areacontinues its dominance in attracting the top two deals of the quarter

6

23

33

13

42

38

46

22

74

97

71

66

102

122

323

Numberof rounds

108

139

178

278

364

376

439

473

541

821

856

1,114

1,190

1,575

7,400

Switzerland

Illinois

Potomac

Bengaluru

Israel (all site)

Canada

Germany

Shanghai

France

UK

S. Calif

Beijing

New England

NY Metro

Bay Area

Amount invested(US$m)

Top five hotbeds1

US$12.1b(77% of the total2)

Top five hotbeds1

684(63% of the total2)

113

385

394

421

572

634

881

901

954

981

1,509

1,820

2,306

3,234

8,786

Bengaluru

Switzerland

Shanghai

Illinois

Canada

Potomac

Israel (all site)

Beijing

France

Germany

UK

NY Metro

S. Calif

New England

Bay Area

Amount invested(US$m)

Top five hotbeds1

US$17.7b(74% of the total2)

2009 2Q14

316

384

730

832

1,084

1,214

1,282

1,655

1,951

1,996

2,759

3,344

3,835

3,933

14,075

Bengaluru

Switzerland

Illinois

Germany

Shanghai

Canada

France

Potomac

Israel (all site)

UK

Beijing

NY Metro

New England

S. Calif

Bay Area

Amount invested(US$m)

Top five hotbeds1

US$27.9b(71% of the total2)

2011

412

564

570

730

1,092

1,105

1,242

1,521

1,707

2,106

2,305

3,264

3,491

3,891

13,488

Switzerland

Illinois

Bengaluru

Shanghai

France

Canada

Potomac

Germany

Israel (all site)

Beijing

UK

S. Calif

NY Metro

New England

Bay Area

Amount invested(US$m)

Top five hotbeds1

US$26.4b(71% of the total2)

2013

83

134

139

161

193

251

340

342

517

669

704

775

1,056

1,263

6,278

Bengaluru

Switzerland

Illinois

Canada

Potomac

France

Germany

Israel (all site)

UK

S. Calif

Shanghai

Beijing

NY Metro

New England

Bay Area

Amount invested(US$m)

Top five hotbeds1

US$10.1b(78% of the total2)

1Q14

*Data on Israel is based on Israel (all site).

1 Top five hotbeds by amount invested. 2 Total of 15 major VC hotbeds listed above.

Venture Capital Insights® – 2Q14Page 9

Venture capital investment by industryConsumer services and business and financial services were the two hottest sectors in 2Q14

By number of rounds:► The business and financial services sector continues to be ranked first globally. The IT sector in the US was displaced from its number one ranking in 2Q14 for the first time

since 1Q08.► Compared to 2Q13, the increase in deal count was the highest in business and financial services at 18%, followed by consumer services at 6%, while the IT sector saw a

decline of 17%.By amount invested:► The amount invested in both the business and financial services and consumer services sectors doubled versus the amount invested in 2Q13.► Even though there is an increased focus by VC investors on cloud-based and mobile technology types of companies, the consumer services sector saw top three deals of the

quarter, with a total investment of US$19.5b.

1,693

240

1,165

240

1,304

186

1,115

Information technology

Industrial goods and materials

Healthcare

Energy and utilities

Consumer services

Consumer goods

Business and financial services

2011

1,779

206

1,074

176

1,424

183

1,092

Number of rounds

Amount invested (US$b)

726

74

514

52

746

112

803

Note: There are also some deals for which sector has not been assigned.

2012 2013 1H14 1Q14 2Q14

366

31

242

23

366

63

398

360

43

272

29

380

49

405

11.51.9

12.34.7

13.1

2.1

9.5

Information technology

Industrial goods and Materials

Healthcare

Energy and utilities

Consumer services

Consumer goods

Business and financial services2011

12.7

1.5

10.6

2.4

11.1

1.4

8.6

8.4

0.5

6.6

0.7

11.8

0.7

9.0

2012 2013 1H14 1Q14 2Q14

4.4

0.2

2.9

0.4

4.4

0.3

4.3

4.0

0.4

3.7

0.3

7.5

0.4

4.8

12.4

1.4

11.8

1.7

12.0

1.8

10.8

1,719

207

1,113

160

1,474

208

1,451

Venture Capital Insights® – 2Q14Page 10

Venture capital investment by country2Q14 was the strongest quarter in the US, Europe and China for dollars invested

By number of rounds:► In 2Q14, the number of rounds in the US and Europe grew marginally when compared to the previous quarter. For the developing economies ‒ India and China ‒ deal volume

increased by 18% and 13%, respectively, due to strong deal activity in the consumer services sector.► The number rounds in Canada and Israel declined 10% and 22% respectively, in 2Q14 compared to 1Q14. In Israel, slow deal activity in the consumer services sector,

particularly in the consumer information services subsector was behind the decline. In Canada, the information technology sector saw only 13 deals compared to 18 deals in thepast quarter.

By amount invested:► VC activity picked up across all markets in 2Q14, with the US, Europe and China seeing growth of 21%, 45% and 22%, respectively. Even investing in the smaller VC markets

grew impressively, with Canada and India showing \100% growth each over the last quarter and Israel grew by 33%.► Subsequently, the average deal size also grew across all markets for 2Q14 compared to 1Q14. For the largest VC market, the US, average deal size increased by 17%, and in

Europe, it grew by 42%. India, Israel and Canada also saw big gains in average deal sizes with 69%, 71% and 121%, respectively.

181

180

143

430

1,369

3,651

India

Israel

Canada

China

Europe

US

234

163

151

289

1,387

3,734

Number of rounds

Amount invested (US$b)

240

196

182

379

1,601

3,747

109

96

80

228

723

1,802

50

54

42

107

358

885

59

42

38

121

365

917

1.5

2.0

1.2

6.7

7.5

36.2

India

Israel

Canada

China

Europe

US

1.6

1.2

0.9

4.8

6.4

33.7

1.9

1.7

1.1

4.7

7.5

34.9

1.3

0.7

0.5

5.1

4.9

25.2

0.4

0.3

0.2

2.3

2.0

11.4

0.8

0.4

0.4

2.8

2.9

13.8

2011 2012 2013 1H14 1Q14 2Q14

2011 2012 2013 1H14 1Q14 2Q14

Venture Capital Insights® – 2Q14Page 11

Venture capital investment by round class and stage of developmentCompanies operating at revenue generation stage continued to attract large investments primarily,through later round classes

1,622

1,067

2,279

626

Later stageSecond round

First roundSeed round

2011

1,537

995

2,355

733

Number of rounds

Amount invested (US$b)

2012 2013 1H14 1Q14 2Q14

1,532

1,225

2,591

697

866

638

1,196

207

392

283

612

138

474

355

584

69

27.7

10.8

12.0

0.6

Later stage

Second round

First round

Seed round

2011

25.5

8.2

10.5

0.5

2012 2013 1H14 1Q14 2Q14

26.8

10.3

10.9

0.5

21.2

6.8

5.7

0.2

8.3

2.9

2.6

0.1

12.9

4.0

3.1

0.1

297

3,664

1,427

559

Profitable

Generating revenue

Product development

Startup

2011

231

3,858

1,293

571

Number of rounds

Amount invested (US$b)

2012 2013 1H14 1Q14 2Q14

270

4,344

1,242

486

144

2,262

515

115

71

1,095

255

74

5.6

36.1

12.2

1.1

Profitable

Generating revenue

Product development

Startup

2011

3.4

35.8

8.6

0.7

2012 2013 1H14 1Q14 2Q14

4.7

37.8

8.7

0.6

4.2

28.9

4.5

0.2

2.2

12.3

2.1

0.1

2.0

16.6

2.4

0.1

By stage of development

By round class

73

1,167

260

41

Venture Capital Insights® – 2Q14Page 12

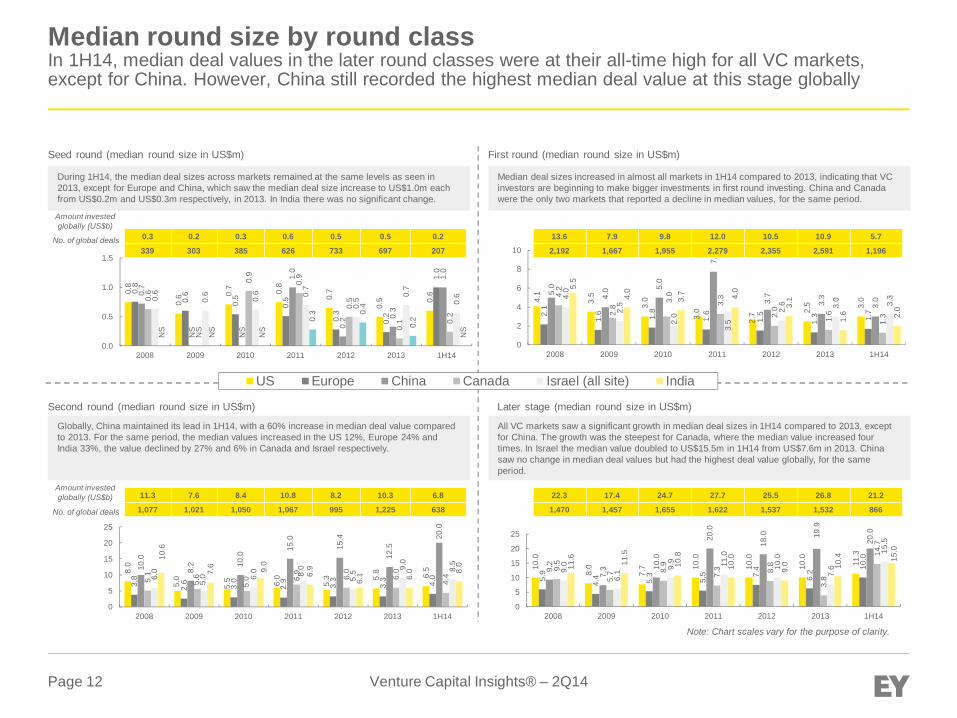

Median round size by round classIn 1H14, median deal values in the later round classes were at their all-time high for all VC markets,except for China. However, China still recorded the highest median deal value at this stage globally

10.0

8.0

7.7 10

.0

10.0

10.0

11.3

5.9

4.4 5.3

5.5 7.

4

6.2 10

.0

9.2

7.3 10

.0

20.0

18.0 19

.9

20.0

9.5

5.7 8.

9

7.3 8.

8

3.8

14.7

9.0

6.1 9.

9 11.0

10.0

7.6

15.5

11.6 11.5

10.8

10.0

9.0 10

.4 15.0

0

5

10

15

20

25

2008 2009 2010 2011 2012 2013 1H14

8.0

5.0

5.5 6.0

5.3 5.

8 6.5

3.8

2.6 3.0

2.9

3.3

3.3 4.0

10.0

8.2 10

.0

15.0

15.4

12.5

20.0

5.1

5.6

5.0 6.

9

6.0

6.0

4.46.

0

5.0 6.

0 8.0

5.5 9.

0

8.5

10.6

7.6 9.0

6.9

6.1 6.0 8.

0

0

5

10

15

20

25

2008 2009 2010 2011 2012 2013 1H14

4.1

3.5

3.0

3.0

2.7 2.

5 3.0

2.1

1.6 1.8

1.6

1.5

1.3 1.7

5.0

4.0 5.

0

7.7

3.7

3.3

3.04.

2

2.8

3.0

3.3

2.0

1.6

1.3

4.0

2.5

2.0

3.5

2.6 3.0 3.3

5.5

4.0

3.7 4.0

3.1

1.6 2.0

0

2

4

6

8

10

2008 2009 2010 2011 2012 2013 1H14

0.8

0.6 0.

7 0.8

0.7

0.5 0.

60.8

0.6

0.5

0.5

0.3

0.2

1.0

0.7

NS

NS

1.0

0.2 0.

3

1.0

0.6

NS

0.9

0.9

0.5

0.1 0.

2

0.6

0.6

0.6 0.

7

0.5 0.

7

0.6

NS

NS

NS

0.3 0.

4

0.2

NS

0.0

0.5

1.0

1.5

2008 2009 2010 2011 2012 2013 1H14

Seed round (median round size in US$m)

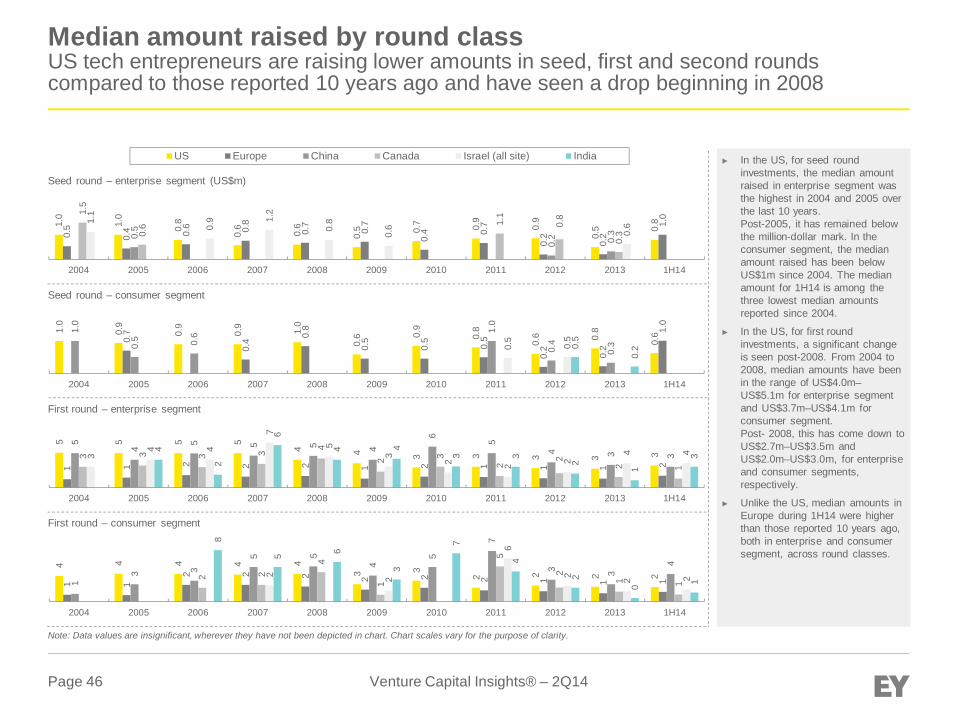

During 1H14, the median deal sizes across markets remained at the same levels as seen in2013, except for Europe and China, which saw the median deal size increase to US$1.0m eachfrom US$0.2m and US$0.3m respectively, in 2013. In India there was no significant change.

First round (median round size in US$m)

Median deal sizes increased in almost all markets in 1H14 compared to 2013, indicating that VCinvestors are beginning to make bigger investments in first round investing. China and Canadawere the only two markets that reported a decline in median values, for the same period.

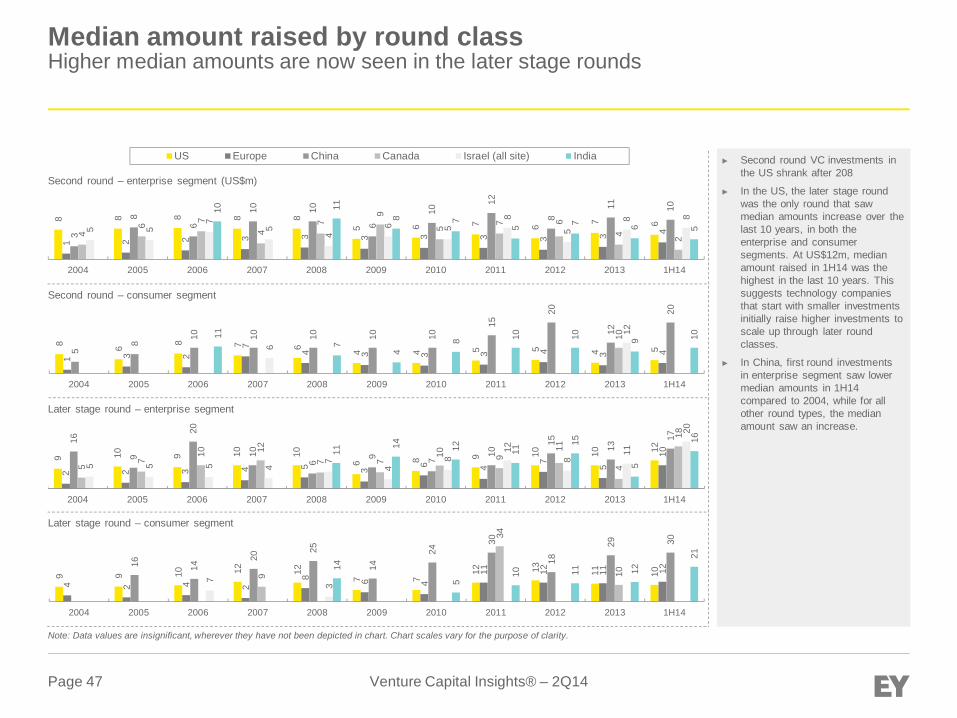

Second round (median round size in US$m)

Globally, China maintained its lead in 1H14, with a 60% increase in median deal value comparedto 2013. For the same period, the median values increased in the US 12%, Europe 24% andIndia 33%, the value declined by 27% and 6% in Canada and Israel respectively.

Later stage (median round size in US$m)

All VC markets saw a significant growth in median deal sizes in 1H14 compared to 2013, exceptfor China. The growth was the steepest for Canada, where the median value increased fourtimes. In Israel the median value doubled to US$15.5m in 1H14 from US$7.6m in 2013. Chinasaw no change in median deal values but had the highest deal value globally, for the sameperiod.

Note: Chart scales vary for the purpose of clarity.

0.3 0.2 0.3 0.6 0.5 0.5 0.2

339 303 385 626 733 697 207

Amount investedglobally (US$b)

No. of global deals

Amount investedglobally (US$b)

No. of global deals

13.6 7.9 9.8 12.0 10.5 10.9 5.7

2,192 1,667 1,955 2,279 2,355 2,591 1,196

US Europe China Canada Israel (all site) India

11.3 7.6 8.4 10.8 8.2 10.3 6.8

1,077 1,021 1,050 1,067 995 1,225 638

22.3 17.4 24.7 27.7 25.5 26.8 21.2

1,470 1,457 1,655 1,622 1,537 1,532 866

Venture Capital Insights® – 2Q14Page 13

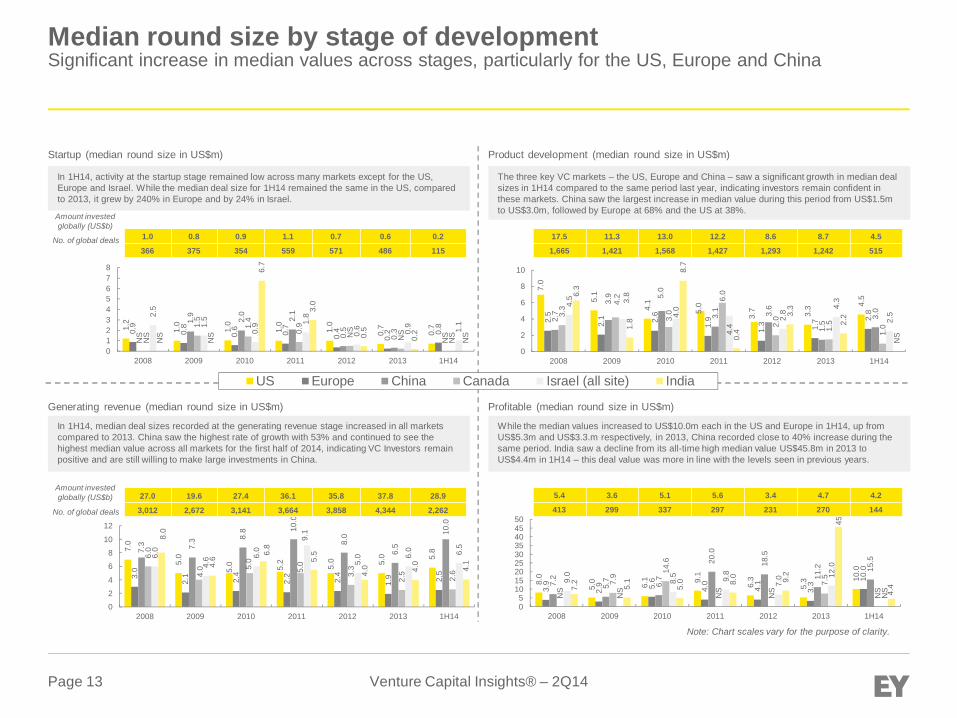

Median round size by stage of developmentSignificant increase in median values across stages, particularly for the US, Europe and China

7.0

5.0

5.0 5.2

5.0 5.

0 5.8

3.0

2.1 2.4

2.2

2.4

1.9 2.5

7.3 7.3 8.

8 10.0

8.0

6.5

10.0

6.0

4.0 5.

0

5.0

3.3

2.5

2.6

6.0

4.6 6.

0

9.1

5.0 6.

0 6.5

8.0

4.6

6.8

5.5

4.0 4.0

4.1

0

2

4

6

8

10

12

2008 2009 2010 2011 2012 2013 1H14

8.0

5.0 6.1 9.

1

6.3

5.3 10

.0

3.9

2.9 5.

6

4.0

4.1

3.3 10

.0

7.2

5.7 6.7

20.0

18.5

11.2 15

.5

NS

7.9 14

.6

NS

NS

7.5

NS

9.0

NS

8.5 9.8

7.0 12

.0

NS7.

2

5.1

5.0 8.

0 9.2

45.8

4.4

05

101520253035404550

2008 2009 2010 2011 2012 2013 1H14

7.0

5.1

4.1

5.0

3.7 3.3 4.

5

2.5

2.1 2.6

1.9

1.3 1.7 2.

8

2.7

3.9 5.

0

3.1 3.6

1.5

3.03.3

4.2

3.0

6.0

2.0

1.5

1.0

4.5 3.8

4.0

4.4

2.8 4.

3

2.5

6.3

1.8

8.7

0.4

3.3

2.2

NS

0

2

4

6

8

10

2008 2009 2010 2011 2012 2013 1H14

1.2

1.0

1.0

1.0

1.0

0.7

0.70.9

0.8

0.6 0.7

0.4

0.2 0.

8

NS

1.9

2.0

2.1

0.5

0.3

NS

NS

1.5

1.4

0.9

NS

NS

NS

2.5

1.5

0.9 1.

8

0.6 0.9 1.1

NS

NS

6.7

3.0

0.5

0.2

NS

012345678

2008 2009 2010 2011 2012 2013 1H14

Startup (median round size in US$m)

In 1H14, activity at the startup stage remained low across many markets except for the US,Europe and Israel. While the median deal size for 1H14 remained the same in the US, comparedto 2013, it grew by 240% in Europe and by 24% in Israel.

Product development (median round size in US$m)

The three key VC markets ‒ the US, Europe and China ‒ saw a significant growth in median dealsizes in 1H14 compared to the same period last year, indicating investors remain confident inthese markets. China saw the largest increase in median value during this period from US$1.5mto US$3.0m, followed by Europe at 68% and the US at 38%.

Generating revenue (median round size in US$m)

In 1H14, median deal sizes recorded at the generating revenue stage increased in all marketscompared to 2013. China saw the highest rate of growth with 53% and continued to see thehighest median value across all markets for the first half of 2014, indicating VC Investors remainpositive and are still willing to make large investments in China.

Profitable (median round size in US$m)

While the median values increased to US$10.0m each in the US and Europe in 1H14, up fromUS$5.3m and US$3.3.m respectively, in 2013, China recorded close to 40% increase during thesame period. India saw a decline from its all-time high median value US$45.8m in 2013 toUS$4.4m in 1H14 ‒ this deal value was more in line with the levels seen in previous years.

Note: Chart scales vary for the purpose of clarity.

Amount investedglobally (US$b)

No. of global deals 1.0 0.8 0.9 1.1 0.7 0.6 0.2

366 375 354 559 571 486 115

17.5 11.3 13.0 12.2 8.6 8.7 4.5

1,665 1,421 1,568 1,427 1,293 1,242 515

Amount investedglobally (US$b)

No. of global deals

27.0 19.6 27.4 36.1 35.8 37.8 28.9

3,012 2,672 3,141 3,664 3,858 4,344 2,262

5.4 3.6 5.1 5.6 3.4 4.7 4.2

413 299 337 297 231 270 144

US Europe China Canada Israel (all site) India

Section 2: Global VC exit landscape – IPO and M&AAnalysis by geography

Venture Capital Insights® – 2Q14Page 15

Section 2: Global VC exit landscape – IPO and M&ASummary

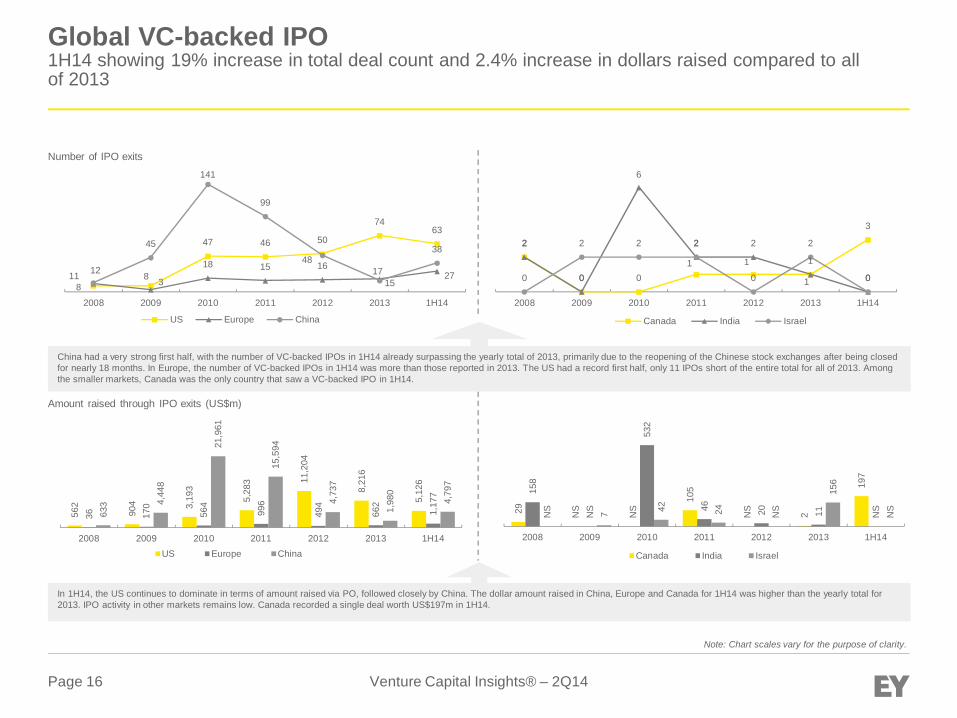

Global VC-backed IPOs

► The first half of 2014 showed a positive start for the year, with a 19.1% increase in the total deal count and 2.4%increase in the dollars raised, versus all of 2013.

► China had a very strong first half, with the number of VC-backed IPOs in 1H14 already surpassing the yearly total of2013, primarily due to the reopening of the Chinese stock exchanges, which had been closed for nearly 18 months.

► In Europe, the number of VC-backed IPOs in 1H14 were more than all of those for 2013: in the US 1H14 was onlyshort 11 IPOs to reach entire total for all of 2013.

► Among the smaller investing markets, Canada was the only country that saw a VC-backed IPO for the first halfof 2014.

► For 1H14, the US dominates in terms of the dollar amounts raised via IPO, followed closely by China. The dollaramounts raised in China, Europe and Canada for 1H14 was higher than the yearly total for 2013. IPO activity in allother markets remained low, with Canada recording a single deal worth US$197m in 1H14.

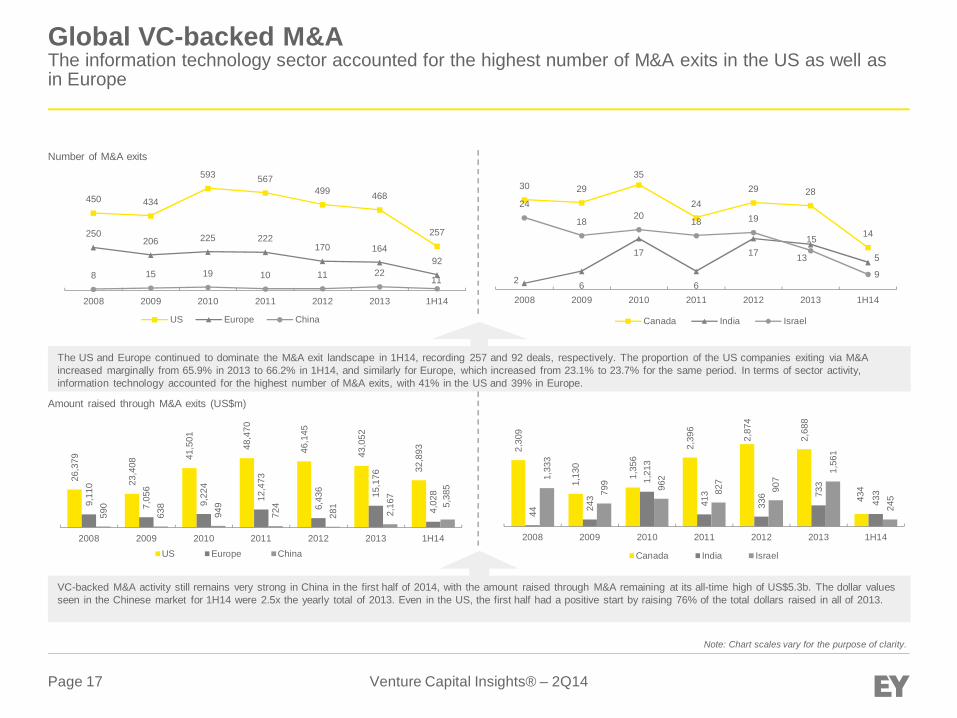

Global VC-backed M&As

► The US and Europe continued to dominate the M&A exit landscape in 1H14, with 257 and 92 deals, respectively. Interms of sector activity, information technology accounted for highest number of M&A exits, in the US it accounted for41% of the M&A activity, and in Europe it accounted for 39%.

► VC-backed M&A activity remained very strong in China in the first half of 2014, with the amount raised via M&A atan all-time high of US$5.3b. The exit values recorded in the Chinese market during 1H14 were 2.5x the yearly totalof 2013.

► Even in the US, the first half of the year had a positive start, with 1H14 already reporting 76% of the total dollars raisedcompared to the entire year of 2013.

Venture Capital Insights® – 2Q14Page 16

29 NS

NS

105

NS

2

197

158

NS

532

46 20 11 NS

NS 7 42 24 NS

156

NS

2008 2009 2010 2011 2012 2013 1H14

Canada India Israel

Amount raised through IPO exits (US$m)

In 1H14, the US continues to dominate in terms of amount raised via PO, followed closely by China. The dollar amount raised in China, Europe and Canada for 1H14 was higher than the yearly total for2013. IPO activity in other markets remains low. Canada recorded a single deal worth US$197m in 1H14.

Global VC-backed IPO1H14 showing 19% increase in total deal count and 2.4% increase in dollars raised compared to allof 2013

562

904 3,19

3

5,28

3 11,2

04

8,21

6

5,12

6

36 170

564

996

494

662

1,17

7

633 4,

448

21,9

61

15,5

94

4,73

7

1,98

0

4,79

7

2008 2009 2010 2011 2012 2013 1H14US Europe China

Note: Chart scales vary for the purpose of clarity.

2

0 01 1 1

3

2

0

6

2 2

1 00

2 2 2

0

2

0

2008 2009 2010 2011 2012 2013 1H14

Canada India Israel

88

47 46 50

7463

11 3

18 15 16 17 2712

45

141

99

48

15

38

2008 2009 2010 2011 2012 2013 1H14

US Europe China

China had a very strong first half, with the number of VC-backed IPOs in 1H14 already surpassing the yearly total of 2013, primarily due to the reopening of the Chinese stock exchanges after being closedfor nearly 18 months. In Europe, the number of VC-backed IPOs in 1H14 was more than those reported in 2013. The US had a record first half, only 11 IPOs short of the entire total for all of 2013. Amongthe smaller markets, Canada was the only country that saw a VC-backed IPO in 1H14.

Number of IPO exits

Venture Capital Insights® – 2Q14Page 17

2,30

9

1,13

0

1,35

6

2,39

6

2,87

4

2,68

8

434

44 243

1,21

3

413

336 73

3

433

1,33

3

799 962

827

907

1,56

1

245

2008 2009 2010 2011 2012 2013 1H14

Canada India Israel

Amount raised through M&A exits (US$m)

VC-backed M&A activity still remains very strong in China in the first half of 2014, with the amount raised through M&A remaining at its all-time high of US$5.3b. The dollar valuesseen in the Chinese market for 1H14 were 2.5x the yearly total of 2013. Even in the US, the first half had a positive start by raising 76% of the total dollars raised in all of 2013.

Global VC-backed M&AThe information technology sector accounted for the highest number of M&A exits in the US as well asin Europe

26,3

79

23,4

08

41,5

01

48,4

70

46,1

45

43,0

52

32,8

93

9,11

0

7,05

6

9,22

4

12,4

73

6,43

6 15,1

76

4,02

8

590

638

949

724

281

2,16

7

5,38

5

2008 2009 2010 2011 2012 2013 1H14US Europe China

Note: Chart scales vary for the purpose of clarity.

30 2935

2429 28

14

2 6

17

6

1715

9

24

18 20 18 19

13 5

2008 2009 2010 2011 2012 2013 1H14

Canada India Israel

450 434

593 567499 468

257250206 225 222

170 16492

8 15 19 10 11 2211

2008 2009 2010 2011 2012 2013 1H14

US Europe China

The US and Europe continued to dominate the M&A exit landscape in 1H14, recording 257 and 92 deals, respectively. The proportion of the US companies exiting via M&Aincreased marginally from 65.9% in 2013 to 66.2% in 1H14, and similarly for Europe, which increased from 23.1% to 23.7% for the same period. In terms of sector activity,information technology accounted for the highest number of M&A exits, with 41% in the US and 39% in Europe.

Number of M&A exits

Section 3: Investment in enterprise and consumerventure-backed companiesAnalysis by geography round class, median amount raised and pre-money valuation

Venture Capital Insights® – 2Q14Page 19

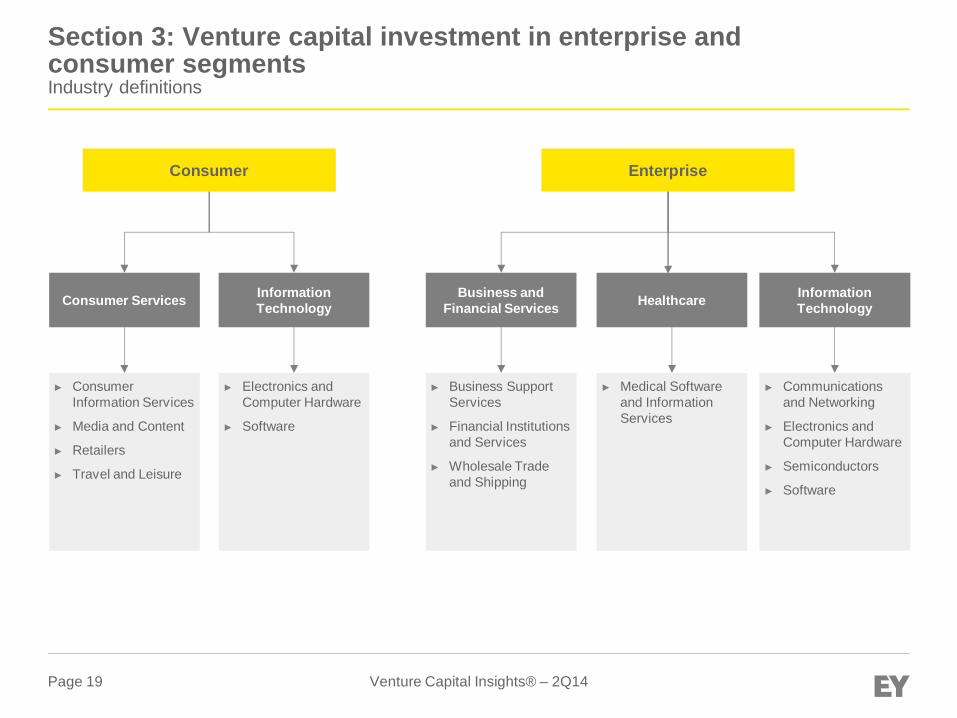

Section 3: Venture capital investment in enterprise andconsumer segmentsIndustry definitions

Consumer Enterprise

Consumer Services InformationTechnology

Business andFinancial Services Healthcare Information

Technology

► ConsumerInformation Services

► Media and Content

► Retailers

► Travel and Leisure

► Electronics andComputer Hardware

► Software

► Business SupportServices

► Financial Institutionsand Services

► Wholesale Tradeand Shipping

► Medical Softwareand InformationServices

► Communicationsand Networking

► Electronics andComputer Hardware

► Semiconductors

► Software

Venture Capital Insights® – 2Q14Page 20

Section 3: Venture capital investment in enterprise andconsumer segmentsExecutive summary – enterprise segment

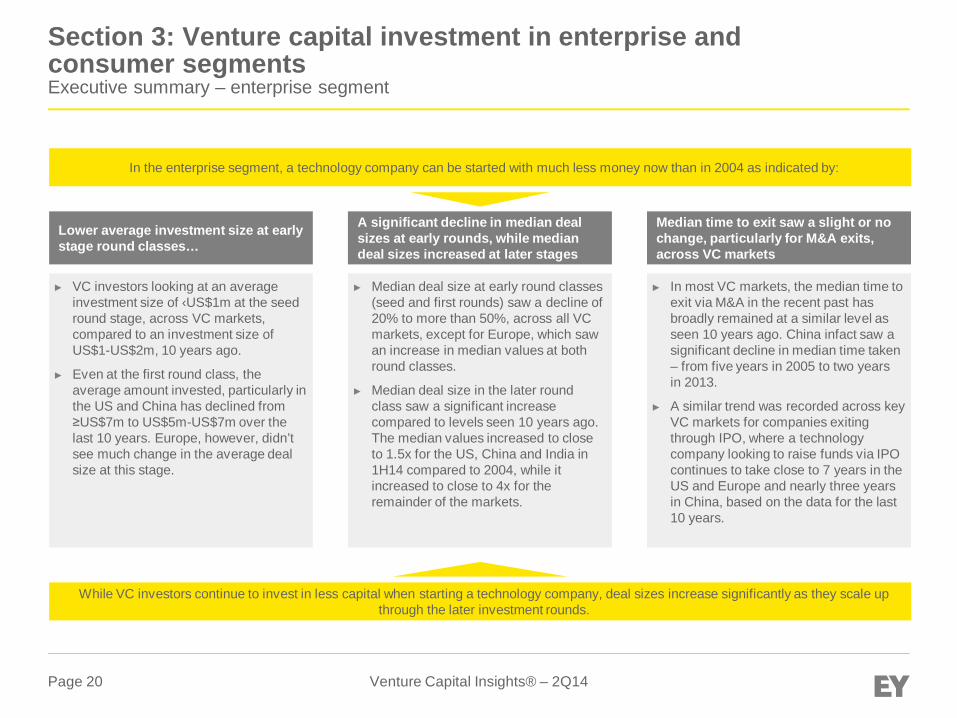

In the enterprise segment, a technology company can be started with much less money now than in 2004 as indicated by:

While VC investors continue to invest in less capital when starting a technology company, deal sizes increase significantly as they scale upthrough the later investment rounds.

► VC investors looking at an averageinvestment size of ‹US$1m at the seedround stage, across VC markets,compared to an investment size ofUS$1-US$2m, 10 years ago.

► Even at the first round class, theaverage amount invested, particularly inthe US and China has declined from≥US$7m to US$5m-US$7m over thelast 10 years. Europe, however, didn’tsee much change in the average dealsize at this stage.

Lower average investment size at earlystage round classes…

► Median deal size at early round classes(seed and first rounds) saw a decline of20% to more than 50%, across all VCmarkets, except for Europe, which sawan increase in median values at bothround classes.

► Median deal size in the later roundclass saw a significant increasecompared to levels seen 10 years ago.The median values increased to closeto 1.5x for the US, China and India in1H14 compared to 2004, while itincreased to close to 4x for theremainder of the markets.

A significant decline in median dealsizes at early rounds, while mediandeal sizes increased at later stages

► In most VC markets, the median time toexit via M&A in the recent past hasbroadly remained at a similar level asseen 10 years ago. China infact saw asignificant decline in median time taken– from five years in 2005 to two yearsin 2013.

► A similar trend was recorded across keyVC markets for companies exitingthrough IPO, where a technologycompany looking to raise funds via IPOcontinues to take close to 7 years in theUS and Europe and nearly three yearsin China, based on the data for the last10 years.

Median time to exit saw a slight or nochange, particularly for M&A exits,across VC markets

Venture Capital Insights® – 2Q14Page 21

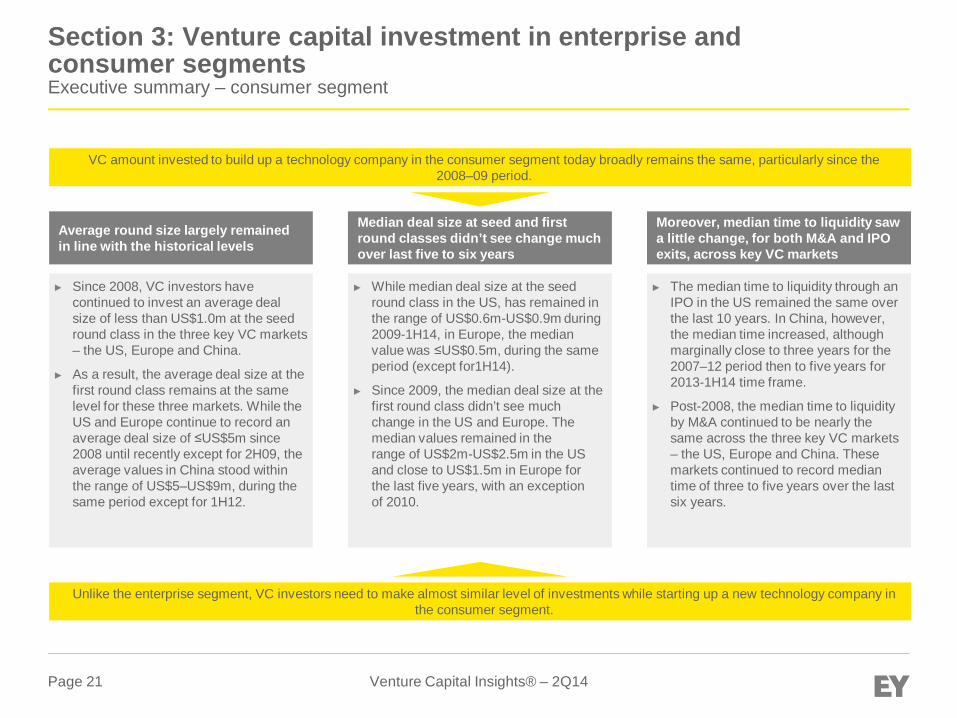

Section 3: Venture capital investment in enterprise andconsumer segmentsExecutive summary – consumer segment

► Since 2008, VC investors havecontinued to invest an average dealsize of less than US$1.0m at the seedround class in the three key VC markets– the US, Europe and China.

► As a result, the average deal size at thefirst round class remains at the samelevel for these three markets. While theUS and Europe continue to record anaverage deal size of ≤US$5m since2008 until recently except for 2H09, theaverage values in China stood withinthe range of US$5–US$9m, during thesame period except for 1H12.

► While median deal size at the seedround class in the US, has remained inthe range of US$0.6m-US$0.9m during2009-1H14, in Europe, the medianvalue was ≤US$0.5m, during the sameperiod (except for1H14).

► Since 2009, the median deal size at thefirst round class didn’t see muchchange in the US and Europe. Themedian values remained in therange of US$2m-US$2.5m in the USand close to US$1.5m in Europe forthe last five years, with an exceptionof 2010.

► The median time to liquidity through anIPO in the US remained the same overthe last 10 years. In China, however,the median time increased, althoughmarginally close to three years for the2007–12 period then to five years for2013-1H14 time frame.

► Post-2008, the median time to liquidityby M&A continued to be nearly thesame across the three key VC markets– the US, Europe and China. Thesemarkets continued to record mediantime of three to five years over the lastsix years.

VC amount invested to build up a technology company in the consumer segment today broadly remains the same, particularly since the2008–09 period.

Unlike the enterprise segment, VC investors need to make almost similar level of investments while starting up a new technology company inthe consumer segment.

Average round size largely remainedin line with the historical levels

Median deal size at seed and firstround classes didn’t see change muchover last five to six years

Moreover, median time to liquidity sawa little change, for both M&A and IPOexits, across key VC markets

Section 3.1: Venture capital investment in enterprise andconsumer segmentsAnalysis by geography

Venture Capital Insights® – 2Q14Page 23

Section 3.1: VC investment in enterprise and consumer segmentsSummary by geography

Enterprise segment

► For the US and Europe, the average deal sizes have broadly remained the same over the last 10 years. While for the US, it has been close toUS$10m, except in 1H14, which saw an average of US$14m, Europe has seen average deal sizes of US$5m over the same time frame. Thisindicates that the VC investors have been investing similar amounts of money to build technology companies across these two markets since1H04 up until 1H14.

► Over the last 10 years, China saw higher average values ‒ for 1H08-1H12 period, the market had average values of US$10m or more, exceptfor 2H09. While the average deal size declined during 2H12-2H13 potentially due to IPO markets being closed for 18 months, in 1H14, itrebounded to US$16m to reach the highest level seen over the last 10 years.

► Smaller markets like Canada and Israel saw a mixed trend in average deal sizes over the last 10 years. However, developing markets such asIndia, building a technology company primarily in BFSI and the information technology (IT) sub-sectors has become cheaper, as reflected byfalling average deal sizes over the same period. After seeing average deal sizes close to US$10m for 2H06-1H09 period, India saw a sharpdecline, with average deal value dropping down to nearly US$6m-US$8m for the 2H09-1H14 period, with the exception for 2H11, which saw anaverage value of US$10m.

Consumer segment

► In the consumer segment, building a technology company across the consumer services and IT sub-sectors is the least expensive in Europe asthe European market continued to see the lowest average deal size compared to the US and Chinese markets in 1H14. The average deal sizein Europe remained below US$10m mark for the first half of 2014, although it was the highest seen in the last 10 years at US$8m.

► While the US average deal size remained broadly in line with the historical levels, China saw a huge jump over the last 10 years, largely drivenby consumer services sector. The average value in China grew from US$10m during 1H04-2H07 time period to ≥US$12m since 1H08 up untilrecently, with the exception in 2009, which saw an average deal size of US$9m, suggesting VC investors continued to remain optimistic ininvesting, albeit largely in the later round classes, to build a technology company in the consumer segment in China.

► In Canada and Israel, the average deal size largely stayed close to US$5m for the last 10 years, there are a few exceptions where there mayhave been a few megadeals that resulted in a skewed deal size in the consumer segment. In India, however, the average values declined fromas high as US$21m in 2H05 to below US$10m mark since 1H07, largely driven by the consumer services sub-sector.

Venture Capital Insights® – 2Q14Page 24

1,50

1

1,49

6

1,53

5

1,55

1

1,42

1

1,25

3 1,43

3 1,65

5

1,70

6

1,79

0

875

748

755

640 71

5

556

471

498

481

513 582

319

63 74 112

139

125

102

107

118

90 120

8473 66 59 62 54 45 59 64 84 90 4082 84 84 93 85 56 42 45 45 78 369 13 32 46 51 48 52 69 80 87 36

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 1H14

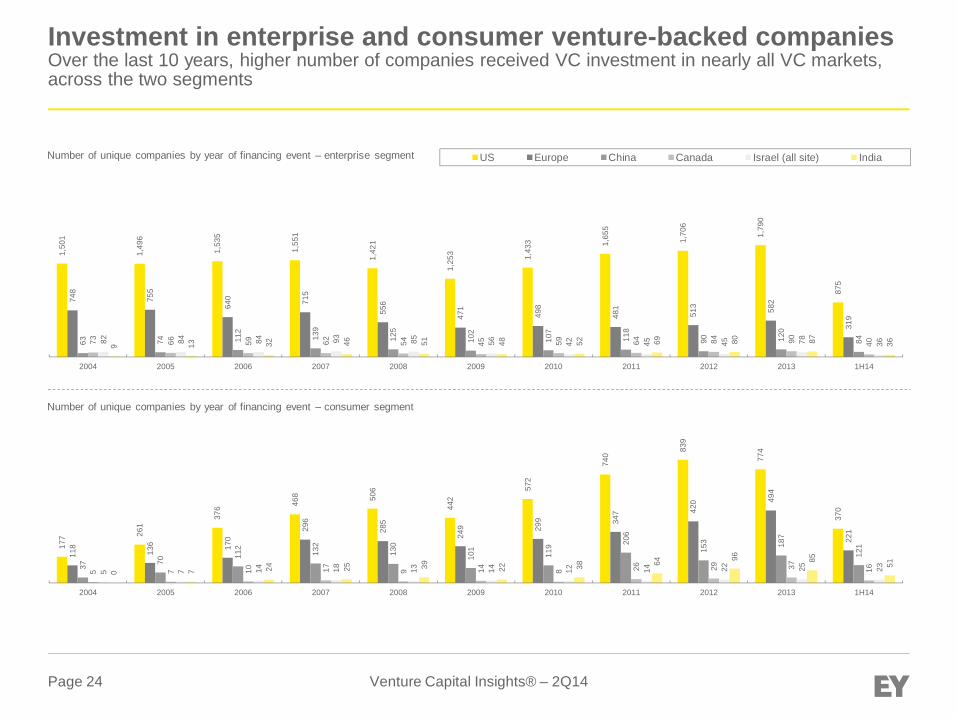

Number of unique companies by year of financing event – enterprise segment US Europe China Canada Israel (all site) India

177 26

1

376 46

8 506

442

572

740

839

774

370

118

136 17

0

296

285

249 29

9 347 42

0 494

221

37 70

112

132

130

101

119 20

6

153 18

7

121

5 7 10 17 9 14 8 26 29 37 165 7 14 18 13 14 12 14 22 25 230 7 24 25 39 22 38 64 96 85 51

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 1H14

Number of unique companies by year of financing event – consumer segment

Investment in enterprise and consumer venture-backed companiesOver the last 10 years, higher number of companies received VC investment in nearly all VC markets,across the two segments

Venture Capital Insights® – 2Q14Page 25

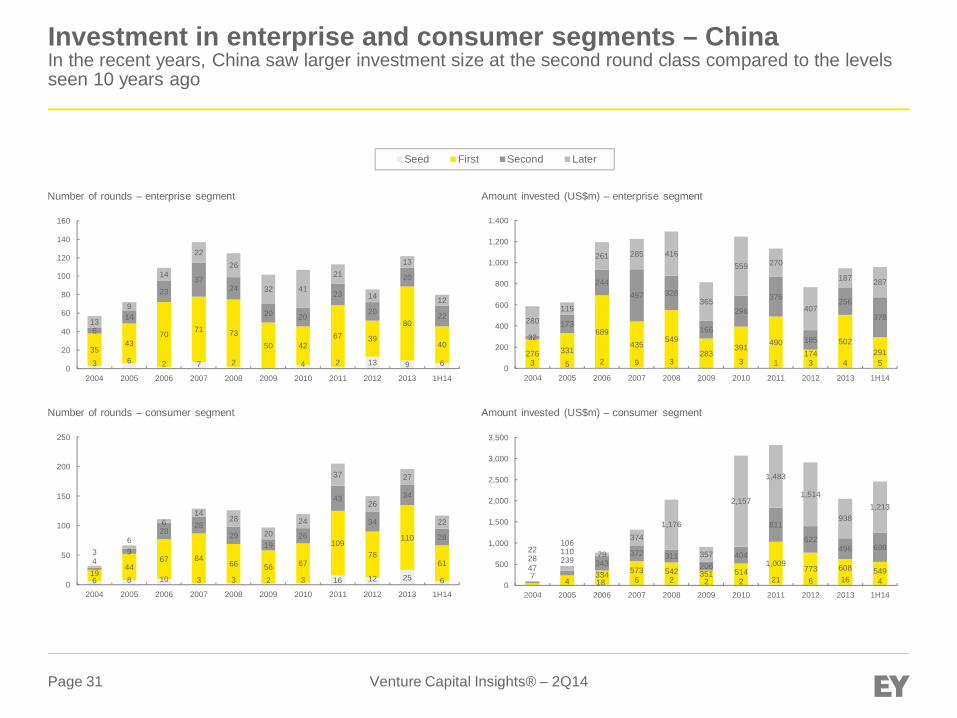

Investment in enterprise and consumer venture-backed companiesVC investors continue to make larger investments in China across the two segments, particularlypost-2010

1,57

2

1,57

0

1,60

6

1,61

4

1,47

3

1,30

9

1,52

5

1,73

7

1,77

6

1,89

2

894

785

786

670

737

570

485

516

492

521

607

320

66 81 118

146

128

104

112

121

92 127

8473 68 63 63 57 47 62 69 86 93 4084 87 87 97 90 58 43 46 47 80 3610 13 32 49 51 49 52 69 81 87 38

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 1H14

Number of rounds – enterprise segment

Amount invested (US$m) – enterprise segment

Number of rounds – consumer segment

Amount invested (US$m) – consumer segment

192 27

9 396 48

5

537

466 59

9 793 88

3

814

377

122

147

174 31

1

290

261

308

359 43

5 519

229

37 76 120

136

133

103

128 21

9

154

203

124

5 7 10 17 9 16 9 27 32 40 165 7 15 20 13 14 12 14 23 26 230 7 28 26 40 22 39 69 101

93 52

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 1H14

13,7

84

14,3

40

16,7

71

15,9

27

13,3

29

9,37

1

11,5

12

14,4

66

15,1

45

16,1

64

12,3

62

2,20

9

2,46

1

2,51

5

2,98

1

2,82

5

1,61

7

2,68

3

2,11

7

1,86

2

1,99

6

1,79

3

597

704

1,24

0

1,27

2

1,31

3

834

1,29

1

1,44

2

911

1,07

3

1,37

2

428

395

417

369

462

290

394

357

587

633

246

404

451

463

610

636

252

242

379

207

520

319

69 110

267

454

482

411

387

541

424

462

244

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 1H14

1,46

1

2,14

0

3,21

4

3,95

3

4,35

7

3,25

0 5,39

9

7,21

2

6,48

3

6,84

9

6,20

7

434

490

800

1,13

9

1,20

0

1,34

2

1,14

2

2,03

0

2,07

6

2,60

2

1,73

5

115

493

859

1,37

0

2,21

1

928

3,12

7

3,76

2

2,92

8

2,76

8

3,46

4

35 27 61 83 35 44 45 253

162

193

163

24 25 86 73 48 22 115

71 122

521

540 91 272

175

349

119

268

621

611

1,00

3

926

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 1H14

US Europe China Canada Israel (all site) India

Venture Capital Insights® – 2Q14Page 26

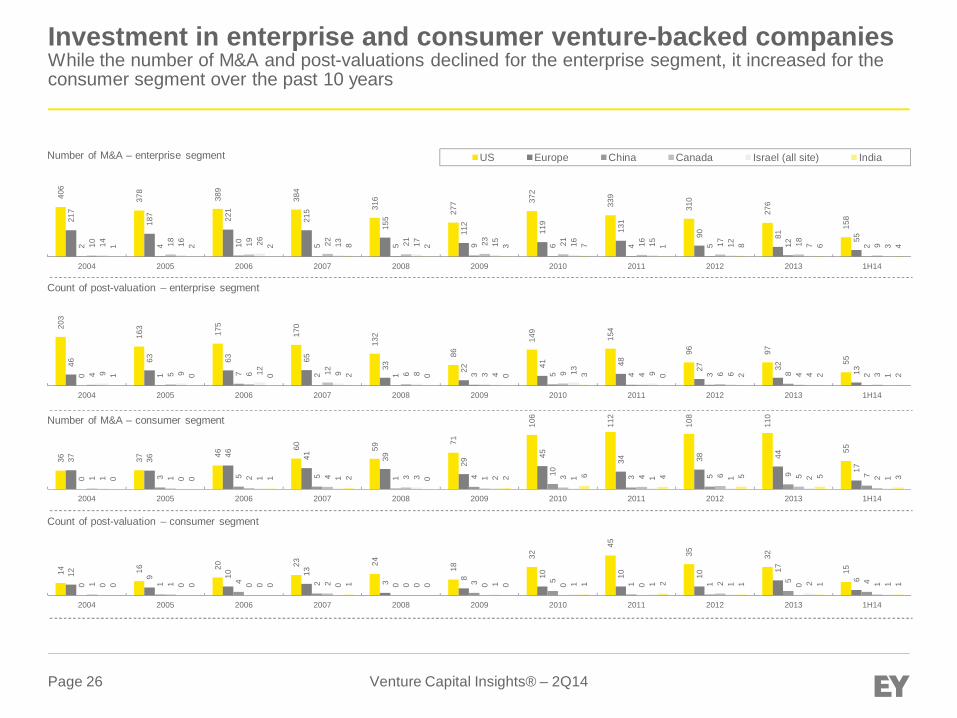

Investment in enterprise and consumer venture-backed companiesWhile the number of M&A and post-valuations declined for the enterprise segment, it increased for theconsumer segment over the past 10 years

406

378

389

384

316

277 37

2

339

310

276

15821

7

187 221

215

155

112

119

131

90 81 55

2 4 10 5 5 9 6 4 5 12 210 18 19 22 21 23 21 16 17 18 914 16 26 13 17 15 16 15 12 7 31 2 2 8 2 3 7 1 8 6 4

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 1H14

Number of M&A – enterprise segment

Count of post-valuation – enterprise segment

Number of M&A – consumer segment

Count of post-valuation – consumer segment

36 37 46

60 59

71

106

112

108

110

55

37 36 46 41 39 29

45

34 38 44

17

0 3 5 5 1 4 10 3 5 9 71 1 2 4 3 1 3 4 6 5 21 0 1 1 3 2 1 1 1 2 10 0 1 2 0 2 6 4 5 5 3

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 1H14

203

163

175

170

132

86

149

154

96 97

5546 63 63 65

33 22 41 48 27 32 130 1 7 2 1 3 5 4 3 8 24 5 6 12 6 3 9 4 6 4 39 9 12 9 8 4 13 9 6 4 11 0 0 2 0 0 3 0 2 2 2

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 1H14

14 16 20 23 24

18

32

45

35 32

1512 9 10 13

3 8 10 10 10

17

6

0 1 4 2 0 3 5 1 1 5 41 1 0 2 0 0 0 0 2 0 10 0 0 0 0 1 1 1 1 2 10 0 0 1 0 0 1 2 1 1 1

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 1H14

US Europe China Canada Israel (all site) India

Section 3.2: Venture capital investment in enterprise andconsumer segmentsAnalysis by key geographies and round class

Venture Capital Insights® – 2Q14Page 28

Section 3.2: Venture capital investment in enterprise andconsumer segmentsSummary by key geographies and round class

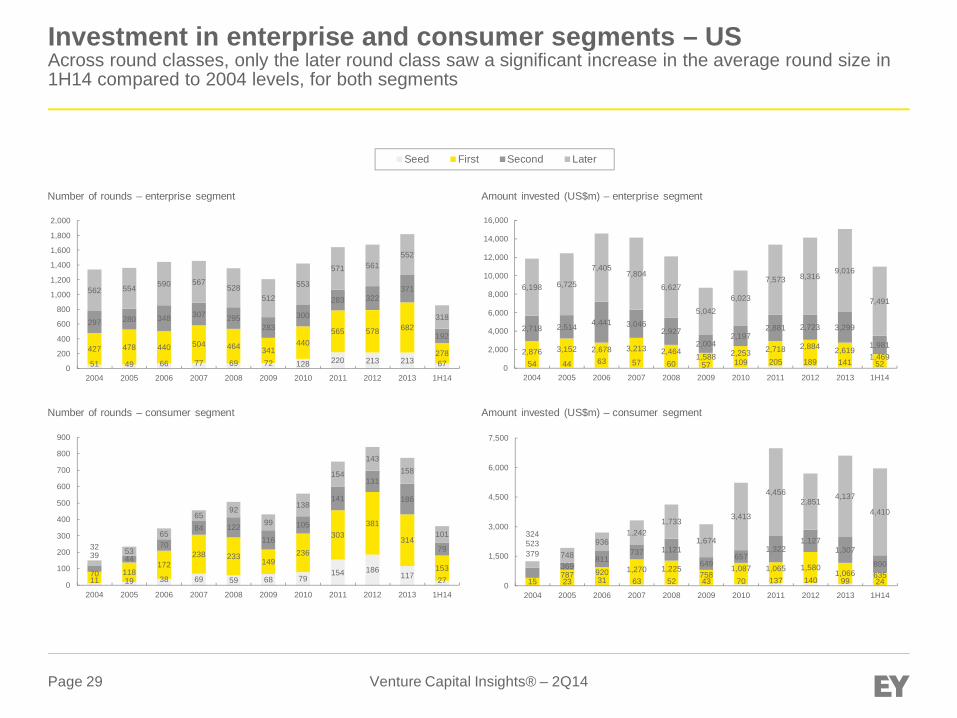

Enterprise segment► Global investment patterns show that a technology company could be started in 2014 with lower initial amount invested than in

2004, as evident from lower investment sizes at early rounds.

► Proportion of seed and first rounds in total deal count increased in the last 10 years, while that of later rounds has decreased.For the seed round, it has doubled from 4% in 1H04 to 8% in 1H14, while for later stage rounds, it dropped down from 39% to30%, respectively, during the same period. This implies that VC funding activity at early stages has became more frequent in therecent past, compared to that of 10 years ago.

► In terms of the dollar amount invested, there was a reverse in the investing pattern as the average round size at seed rounddropped down from US$1.1m in 1H04 to US$0.7m in 1H14, and the average round size in later stage rounds surged fromUS$8.9m to US$21.8m. This indicates that the technology companies are now able to start with much less capital than in 2004and scale it up later with much larger deals.

Consumer segment► The average deal sizes for seed, first and second rounds largely remained in line with the historical levels for the three key VC

markets – the US, Europe and China – indicating VC investors continue to make similar level of dollar investments while buildingup technology companies in these markets for the past 10 years.

► While the average values for seed round remained ≤US$1m across these three markets, China recorded significantly higheraverage deal sizes for the first and second rounds when compared to the US and Europe. Since 1H11, the US and Europe sawan average deal size of ≤US$5m for the first round and nearly US$10m for the second round. For China, the average deal valueswere close to US$10m, with an exception of 2H12–2H13 and, US$15m–US$20m for first and second rounds, respectively, for thesame period.

► Across these key markets, the average deal sizes at the later round class has increased significantly over the last 10 years.This suggests that VC investors are increasingly making larger investments to help the technology company scale up with anintent to have a successful exit via IPO or M&A.

Venture Capital Insights® – 2Q14Page 29

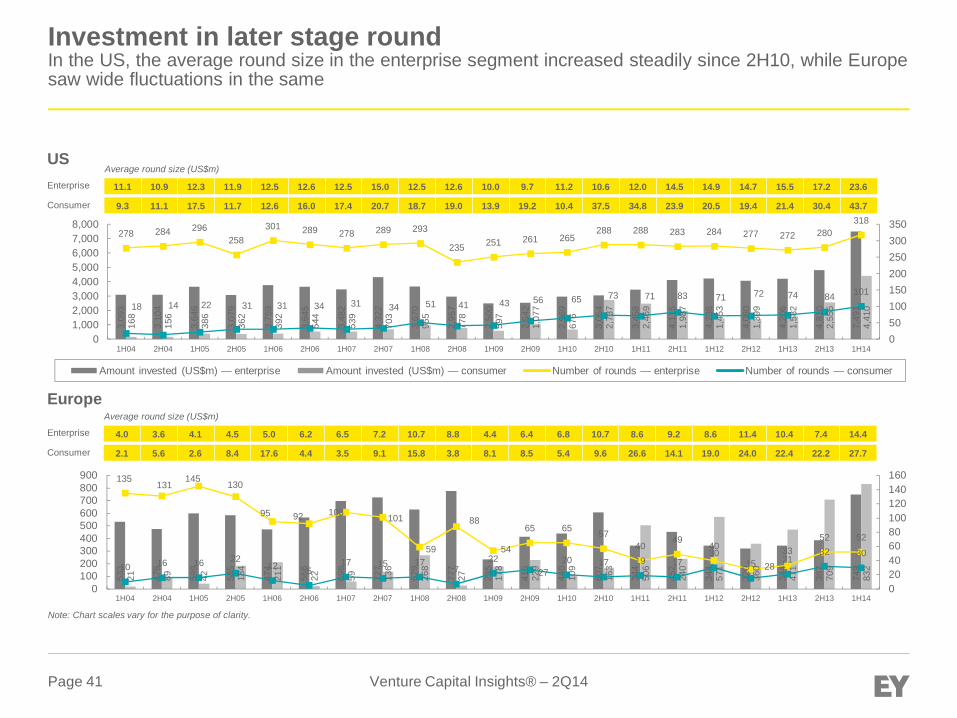

Investment in enterprise and consumer segments – USAcross round classes, only the later round class saw a significant increase in the average round size in1H14 compared to 2004 levels, for both segments

11 19 38 69 59 68 79154 186

117 2770 118

172238 233

149236

303381

314

15339 44

70

84 122116

105

141

131

186

7932 53

65

6592

99

138

154

143158

101

0

100

200

300

400

500

600

700

800

900

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 1H14

Number of rounds – consumer segment

15 23 31 63 52 43 70 137 140 99 24

379

787 920 1,270 1,225758

1,087 1,065 1,5801,066 635

523

369811

737 1,121

649657

1,3221,127

1,307

890

324

748936

1,2421,733

1,674

3,413

4,4562,851

4,137

4,410

0

1,500

3,000

4,500

6,000

7,500

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 1H14

Amount invested (US$m) – consumer segment

51 49 66 77 69 72 128 220 213 213 67

427 478 440 504 464 341440

565 578 682

278

297 280 348 307 295283

300

283 322371

192

562 554 590 567528

512

553

571 561552

318

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 1H14

54 44 63 57 60 57 109 205 189 141 522,876 3,152 2,678 3,213 2,464

1,588 2,253 2,718 2,884 2,6191,469

2,718 2,514 4,441 3,0462,927

2,0042,197

2,881 2,723 3,299

1,981

6,198 6,725

7,4057,804

6,627

5,0426,023

7,573 8,3169,016

7,491

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 1H14

Seed First Second Later

Number of rounds – enterprise segment Amount invested (US$m) – enterprise segment

Venture Capital Insights® – 2Q14Page 30

Investment in enterprise and consumer segments – EuropeThe consumer segment saw the average deal size increasing to US$28m in 1H14 from US$4m in 2004,while for enterprise, it increased from US$4m to US$14m

16 20 35 35 25 30 34 43 79 61 18

246 279 268 317246 223 232 251

262 315

182

171 150 121122

12185 90 86

83109

62

266 275187

209

147119 122 89

6885

52

0

100

200

300

400

500

600

700

800

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 1H14

11 15 24 28 22 24 24 34 45 22 12510 703 795 885 791 446 637 701 632 712 524

559 403539 530 541

391375

498 493 503376

1,0101,185

1,0401,425 1,406

650

1,048 796664 731

749

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 1H14

4 6 7 21 27 22 24 44 59 7411

57 63 109

195 162108

177186

230266

12514

1520

29 56

59

4868

73

88

4826

38

17

32 2449

3736

45

53

30

0

100

200

300

400

500

600

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 1H14

2 6 3 14 18 14 14 24 20 24 11

223 121339

597 494 596 571 670 589 537 361

70 9492

261 330 298 258398 502 774

271

110 226233

196 295407

272

747931

1,180

832

0

500

1,000

1,500

2,000

2,500

3,000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 1H14

Number of rounds – consumer segment Amount invested (US$m) – consumer segment

Number of rounds – enterprise segment Amount invested (US$m) – enterprise segment

Seed First Second Later

Venture Capital Insights® – 2Q14Page 31

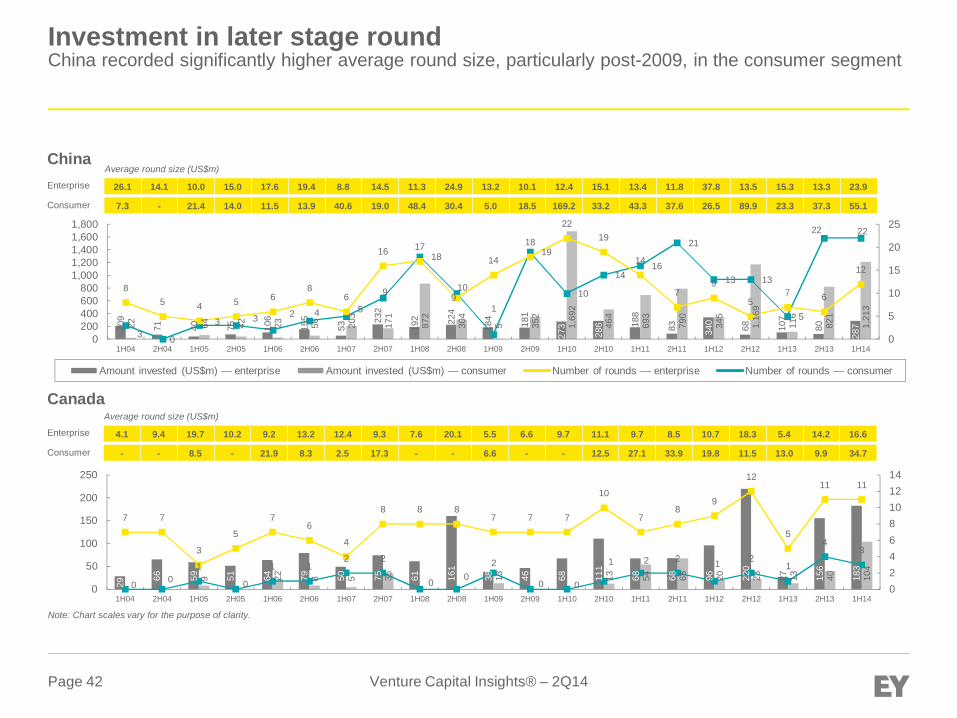

Investment in enterprise and consumer segments – ChinaIn the recent years, China saw larger investment size at the second round class compared to the levelsseen 10 years ago

6 8 10 3 3 2 3 16 12 25 619

4467 84

66 56 67

10978

110

6149

2828

2919

26

43

34

34

28

36

614

28

2024

37

26

27

22

0

50

100

150

200

250

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 1H14

7 4 18 6 2 2 2 21 6 16 447

239

334 573 542 351 5141,009

773 608 54928

110343

372 311206

404

811

622496 69822

10679

3741,176

357

2,157

1,483

1,514

9381,213

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 1H14

3 6 2 7 2 4 2 13 9 6

3543

70 71 7350 42

67 39

80

40

6

14

2337

24

20 20

23

20

20

2213

9

14

2226

32 41

21

14

13

12

0

20

40

60

80

100

120

140

160

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 1H14

3 5 2 9 3 3 1 3 4 5276 331

689435

549

283391 490

174502

291

32

173

244497 328

166

296

376

185

256

378280115

261 285 416

365

559 270

407

187 287

0

200

400

600

800

1,000

1,200

1,400

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 1H14

Number of rounds – enterprise segment Amount invested (US$m) – enterprise segment

Number of rounds – consumer segment Amount invested (US$m) – consumer segment

Seed First Second Later

Venture Capital Insights® – 2Q14Page 32

33 21 24 20 40 24 38 19 43 17 24 34 46 63 89 115

100

89 82 59 523 12 10 13 15 16 33 30 34 18 15 28 32 38 57 80 74 66 43 56 24

4 7 12 718 20

38 3140

1931

37

40 39

67

8799

87

58 59

272823 28 21

36 30 4334

4821

3537

66 62

105115

126

87

124

89

67

020406080100120140

020406080

100120140

1H04 2H04 1H05 2H05 1H06 2H06 1H07 2H07 1H08 2H08 1H09 2H09 1H10 2H10 1H11 2H11 1H12 2H12 1H13 2H13 1H14

Investment in seed roundCompared to the consumer segment, the proportion of seed rounds in total deal count for the enterprisesegment has been consistently higher in the US in last 10 years, except in 1H14

US

Note: Chart scales vary for the purpose of clarity.

Europe

1.2 0.9 0.8 1.0 1.1 0.8 0.9 0.5 0.9 0.8 0.7 0.9 0.7 1.0 0.9 1.0 0.8 1.0 0.7 0.7 0.8

Amount invested (US$m) — enterprise Amount invested (US$m) — consumer Number of rounds — enterprise Number of rounds — consumer

0.8 1.7 0.8 1.8 0.8 0.8 0.9 1.0 0.9 1.0 0.5 0.8 0.8 1.0 0.9 0.9 0.7 0.8 0.7 0.9 0.9

Average round size (US$m)

Enterprise

Consumer

0.6 0.8 0.6 0.9 0.6 0.7 0.9 0.8 1.0 0.8 1.3 0.6 0.5 0.8 0.6 0.9 0.9 0.4 0.4 0.4 0.7

0.4 - 1.9 0.6 0.4 0.4 0.6 0.7 0.8 0.5 0.8 0.6 0.7 0.5 0.6 0.5 0.5 0.3 0.4 0.3 1.0

Average round size (US$m)

Enterprise

Consumer

6 5 8 6 11 12 13 15 10 12 13 12 6 18 10 24 23 23 6 16 122 4 2 1 2 7 7 12 6 4 10 4 10 14 10 9 11 10 14 11

4 0 2 4 2

5 129

1611

5 17 6

1822 22 20

39

23

51

11106

137

18 17 1520

1015

10

2012

2217

26 25

54

17

44

18

0

10

20

30

40

50

60

0

5

10

15

20

25

30

1H04 2H04 1H05 2H05 1H06 2H06 1H07 2H07 1H08 2H08 1H09 2H09 1H10 2H10 1H11 2H11 1H12 2H12 1H13 2H13 1H14

Venture Capital Insights® – 2Q14Page 33

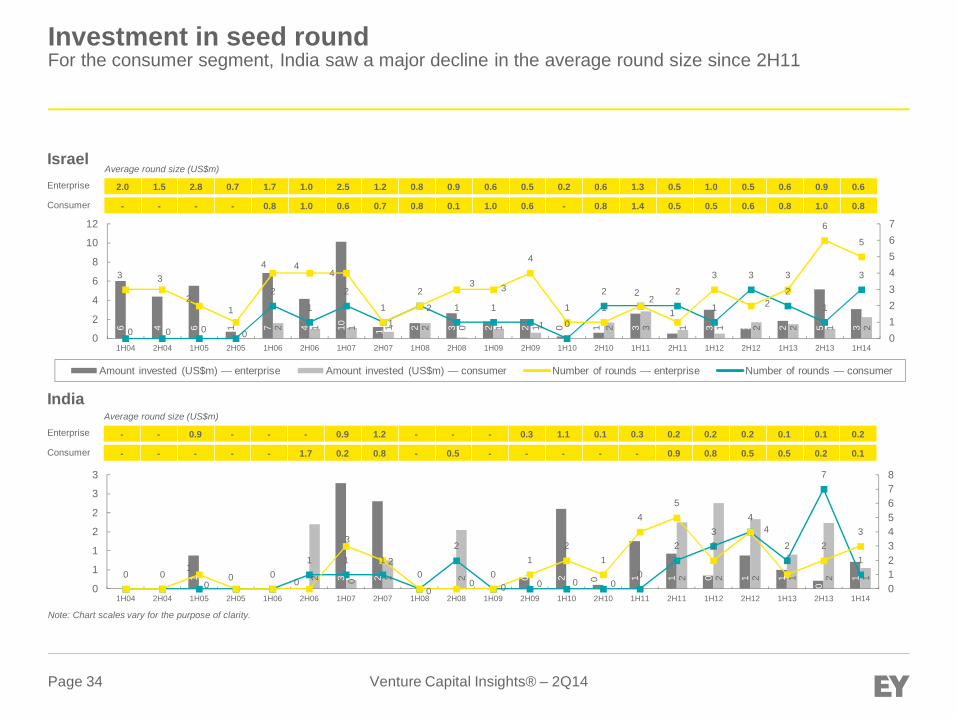

Investment in seed roundLower round sizes are seen in China and Canada compared to 10 years ago

China- 1.0 0.3 1.2 0.9 - 1.0 1.8 2.0 0.6 - - 0.8 0.7 0.4 0.8 0.3 0.2 0.6 0.4 0.8

1.8 0.9 0.5 0.8 2.8 0.7 1.4 3.0 0.7 0.5 0.6 1.5 0.5 0.5 1.1 1.4 0.6 0.2 0.5 0.7 0.7

Average round size (US$m)

Enterprise

Consumer

Canada

1.5 1.5 0.7 1.1 0.6 3.0 1.6 1.1 0.6 0.3 0.7 0.7 - 1.2 0.7 0.9 0.6 1.1 0.5 0.9 0.3

- 1.0 0.5 - - - 0.7 0.8 - 0.5 0.5 0.7 - 0.3 0.6 0.6 0.7 0.1 0.5 0.2 -

Average round size (US$m)

Enterprise

Consumer

3 1 4 2 5 4 2 1 2 1 0 1 3 1 2 2 54 4 3 1 14 4 3 3 1 1 1 1 1 1 6 15 4 1 4 12 4

2

4

7

1

5 5

2 1 2 1 1

1

21

5

11

75

9

16

6

0

3 3 32

0

52

11

00

3 1 1 1

9

44

56

024681012141618

02468

1012141618

1H04 2H04 1H05 2H05 1H06 2H06 1H07 2H07 1H08 2H08 1H09 2H09 1H10 2H10 1H11 2H11 1H12 2H12 1H13 2H13 1H14

3 5 3 7 2 3 3 2 1 0 2 1 2 2 3 3 6 3 6 11 1 1 1 0 1 1 1 2 1 4 1 2 00

1 1

0 0 0

21

0

1 11 0

2

3

2

6 6

4

3

0

23

4

6

3

12 2 2

1

3

1

02

3

3

6 66 6

4

01234567

01234567

1H04 2H04 1H05 2H05 1H06 2H06 1H07 2H07 1H08 2H08 1H09 2H09 1H10 2H10 1H11 2H11 1H12 2H12 1H13 2H13 1H14

Note: Chart scales vary for the purpose of clarity.

Amount invested (US$m) — enterprise Amount invested (US$m) — consumer Number of rounds — enterprise Number of rounds — consumer

Venture Capital Insights® – 2Q14Page 34

Investment in seed roundFor the consumer segment, India saw a major decline in the average round size since 2H11

Israel2.0 1.5 2.8 0.7 1.7 1.0 2.5 1.2 0.8 0.9 0.6 0.5 0.2 0.6 1.3 0.5 1.0 0.5 0.6 0.9 0.6

- - - - 0.8 1.0 0.6 0.7 0.8 0.1 1.0 0.6 - 0.8 1.4 0.5 0.5 0.6 0.8 1.0 0.8

Average round size (US$m)

Enterprise

Consumer

India

- - 0.9 - - - 0.9 1.2 - - - 0.3 1.1 0.1 0.3 0.2 0.2 0.2 0.1 0.1 0.2

- - - - - 1.7 0.2 0.8 - 0.5 - - - - - 0.9 0.8 0.5 0.5 0.2 0.1

Average round size (US$m)

Enterprise

Consumer

Note: Chart scales vary for the purpose of clarity.

1 3 2 0 2 0 1 1 0 1 1

0

12 0 1 2 2 2 2 1 2 10 00

01 1 1

0

2

00 0 0

0

23

4

2

7

11

0 0

3

2

00 0

12

1

45

2

4

12

3

012345678

0

1

1

2

2

3

3

1H04 2H04 1H05 2H05 1H06 2H06 1H07 2H07 1H08 2H08 1H09 2H09 1H10 2H10 1H11 2H11 1H12 2H12 1H13 2H13 1H14

6 4 6 1 7 4 10 1 2 3 2 2 0 1 3 1 3 1 2 5 32 1 1 1 2 0 1 1 2 3 1 1 2 2 1 20 0 0 0

2

1

2

1

2

1 1

1 0

2 2 2

1

3

2

1

33 3

21

4 44

12

3 3

4

1 12

1

3

2

3

6

5

01234567

0

2

4

6

8

10

12

1H04 2H04 1H05 2H05 1H06 2H06 1H07 2H07 1H08 2H08 1H09 2H09 1H10 2H10 1H11 2H11 1H12 2H12 1H13 2H13 1H14

Amount invested (US$m) — enterprise Amount invested (US$m) — consumer Number of rounds — enterprise Number of rounds — consumer

Venture Capital Insights® – 2Q14Page 35

Investment in first roundIn Europe, while the consumer segment saw a decline in the average round size over the last 10 years,the enterprise segment saw an increase of close to 50% in 1H14 compared to 1H04

US7.3 6.2 7.7 5.6 6.4 5.7 6.3 6.4 5.2 5.4 4.9 4.5 5.0 5.2 5.1 4.5 5.4 4.6 3.7 4.0 5.3

6.8 4.3 8.9 5.2 5.9 5.0 4.8 5.8 5.1 5.5 2.9 6.6 4.1 5.0 3.3 3.7 4.7 3.5 3.4 3.4 4.1

Average round size (US$m)

Enterprise

Consumer

Europe

2.0 2.1 2.4 2.7 3.2 2.7 3.2 2.4 3.6 2.9 1.8 2.1 2.7 2.8 2.3 3.3 2.3 2.5 2.2 2.3 2.9

3.5 4.3 1.3 2.4 2.5 3.5 3.1 3.1 3.5 2.6 2.1 8.4 3.5 3.0 4.8 2.6 3.1 2.1 2.5 1.5 2.9

Average round size (US$m)

Enterprise

Consumer

Note: Chart scales vary for the purpose of clarity.

1,55

8

1,31

8

1,77

6

1,37

6

1,51

5

1,16

3

1,71

1

1,50

2

1,19

0

1,27

4

742

846

988

1,26

5

1,37

1

1,34

7

1,51

2

1,37

2

1,23

0

1,38

9

1,46

9

211 16

8

416

371

428

492

538

732

689

535

178

580

412

675

480

584

984

596

519

547

63531 39 47 71 73

99 111 127 13598

6188 101

135 145 158211

170 154 160 153

213 214 232 246 237203

271233 227 237

153188 198

242268

297 279 299334 348

278

050100150200250300350400

0200400600800

1,0001,2001,4001,6001,8002,000

1H04 2H04 1H05 2H05 1H06 2H06 1H07 2H07 1H08 2H08 1H09 2H09 1H10 2H10 1H11 2H11 1H12 2H12 1H13 2H13 1H14

230

280

306

397

437

358

526

359

388

403

181

264

339

298

301

400

293

339

318

394

524

94 129

35 85 106

234

271

325

283

211

103

493

280

291

401

270

331

258

346

191

361

27 30 27 36 4267

89106

82 80

49 59

7998

84 102 108122 141

125 125115131 130

149137 131

167150

109

137

99124 125

107131

120 127 135147

168182

020406080100120140160180200

0

100

200

300

400

500

600

1H04 2H04 1H05 2H05 1H06 2H06 1H07 2H07 1H08 2H08 1H09 2H09 1H10 2H10 1H11 2H11 1H12 2H12 1H13 2H13 1H14

Amount invested (US$m) — enterprise Amount invested (US$m) — consumer Number of rounds — enterprise Number of rounds — consumer

Venture Capital Insights® – 2Q14Page 36

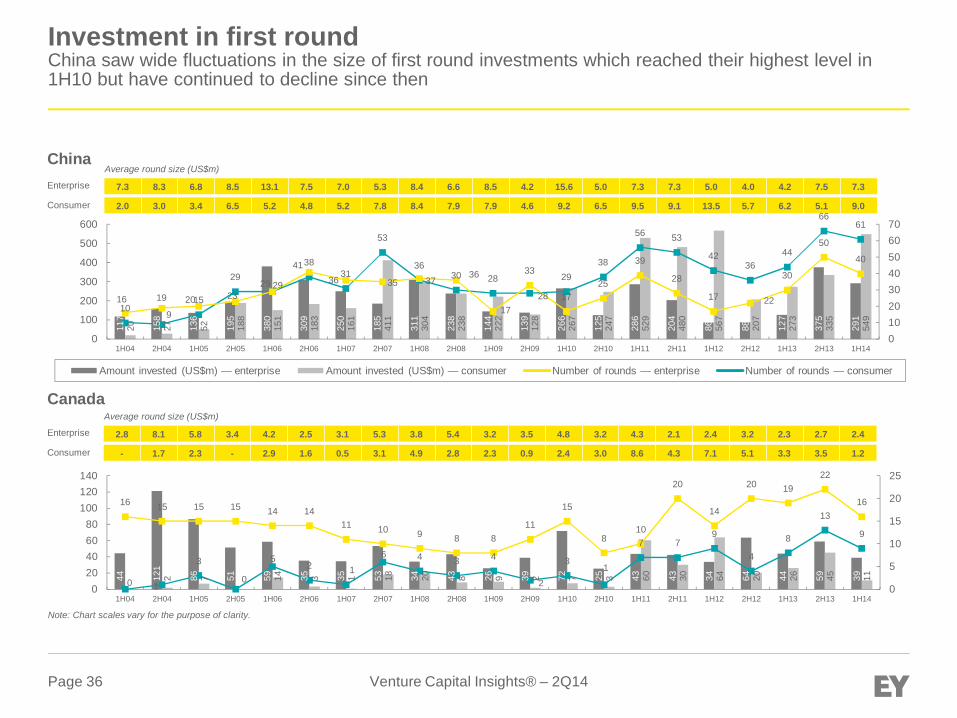

Investment in first roundChina saw wide fluctuations in the size of first round investments which reached their highest level in1H10 but have continued to decline since then

China7.3 8.3 6.8 8.5 13.1 7.5 7.0 5.3 8.4 6.6 8.5 4.2 15.6 5.0 7.3 7.3 5.0 4.0 4.2 7.5 7.3

2.0 3.0 3.4 6.5 5.2 4.8 5.2 7.8 8.4 7.9 7.9 4.6 9.2 6.5 9.5 9.1 13.5 5.7 6.2 5.1 9.0

Average round size (US$m)

Enterprise

Consumer

Canada

2.8 8.1 5.8 3.4 4.2 2.5 3.1 5.3 3.8 5.4 3.2 3.5 4.8 3.2 4.3 2.1 2.4 3.2 2.3 2.7 2.4

- 1.7 2.3 - 2.9 1.6 0.5 3.1 4.9 2.8 2.3 0.9 2.4 3.0 8.6 4.3 7.1 5.1 3.3 3.5 1.2

Average round size (US$m)

Enterprise

Consumer

Note: Chart scales vary for the purpose of clarity.

117

158

136

195

380

309

250

185

311

238

144

139

266

125

286

204

86 88 127

375

291

20 27 52 188

151

183

161

411

304

238

222

128

267

247

529

480

567

207

273

335

549

109

15

2929

3831

53

3630 28

28

2938

56 53

4236

44

6661

16 19 20 2329

4136 35 37

36

17

33

1725

39

28

17 22

30

50

40

010203040506070

0

100

200

300

400

500

600

1H04 2H04 1H05 2H05 1H06 2H06 1H07 2H07 1H08 2H08 1H09 2H09 1H10 2H10 1H11 2H11 1H12 2H12 1H13 2H13 1H14

44 121

86 51 59 35 35 53 34 43 26 39 72 25 43 43 34 64 44 59 392 7 14 3 1 18 20 8 9 2 7 3 60 30 64 20 26 45 110 1

3

0

52 1

6 4 3 4

2

31

7 79

4

8

13

9

16 15 15 15 14 1411 10 9 8 8

11

15

810

20

14

20 1922

16

0

5

10

15

20

25

020406080

100120140

1H04 2H04 1H05 2H05 1H06 2H06 1H07 2H07 1H08 2H08 1H09 2H09 1H10 2H10 1H11 2H11 1H12 2H12 1H13 2H13 1H14

Amount invested (US$m) — enterprise Amount invested (US$m) — consumer Number of rounds — enterprise Number of rounds — consumer

Venture Capital Insights® – 2Q14Page 37

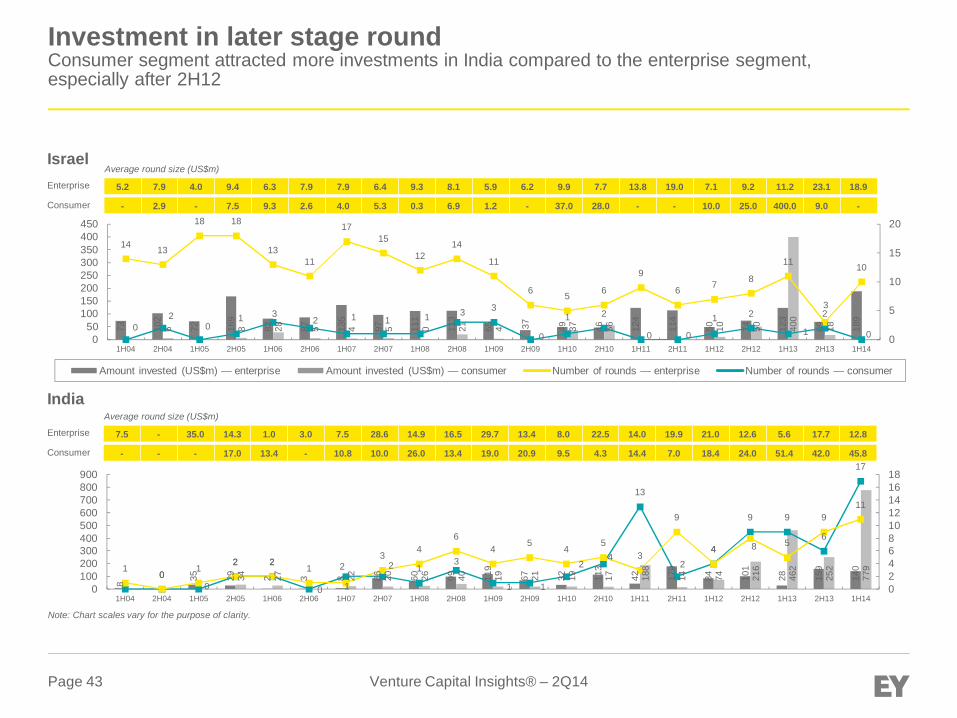

Investment in first roundIn the enterprise segment, India recorded significantly high investments in the 2006-07 period, afterwhich the average round size saw a sharp decline

Israel3.7 3.4 3.2 6.0 4.1 3.5 7.6 5.1 5.3 5.1 3.4 3.8 3.0 4.7 1.9 4.9 2.0 3.0 3.7 4.4 5.1

- - 3.6 - 3.1 5.7 3.9 2.6 1.7 - 1.6 1.6 1.4 - 4.1 15.5 5.4 1.9 2.8 3.9 2.6

Average round size (US$m)

Enterprise

Consumer

India

2.5 12.2 3.8 6.1 4.9 14.0 10.7 7.2 6.8 7.5 4.1 3.7 5.4 4.0 3.8 5.4 2.5 2.8 2.3 2.5 3.2

- - 2.2 25.2 10.2 9.8 6.3 3.4 8.1 7.4 3.3 3.6 10.0 6.4 4.9 3.4 2.7 3.5 1.0 2.7 2.4

Average round size (US$m)

Enterprise

Consumer

Note: Chart scales vary for the purpose of clarity.

41 38 45 79 53 38 121

107

85 66 52 23 21 33 13 44 14 30 78 79 6615 3 17 28 10 5 6 2 4 16 31 27 13 25 16 410 04

01 3

74 3

0

4

1

30

42 5

7

9

4

16

11 1114 13 13

11

16

21

1613

15

6 7 7 79

710

2118

13

0

5

10

15

20

25

020406080

100120140

1H04 2H04 1H05 2H05 1H06 2H06 1H07 2H07 1H08 2H08 1H09 2H09 1H10 2H10 1H11 2H11 1H12 2H12 1H13 2H13 1H14

5 24 15 31 59 154

215

86 89 135

50 62 75 40 65 92 58 68 39 70 327 50 112

69 63 17 121

89 20 25 50 84 63 61 99 99 15 72 57

0 0

3

2

117

10

5

15

12

6 7 5

1313

18

37

28

15

2724

2 2 4 5

12 11

20

1213

18

12

1714

10

17 17

2324

17

28

10

0510152025303540

0

50

100

150

200

250

1H04 2H04 1H05 2H05 1H06 2H06 1H07 2H07 1H08 2H08 1H09 2H09 1H10 2H10 1H11 2H11 1H12 2H12 1H13 2H13 1H14

Amount invested (US$m) — enterprise Amount invested (US$m) — consumer Number of rounds — enterprise Number of rounds — consumer

Venture Capital Insights® – 2Q14Page 38

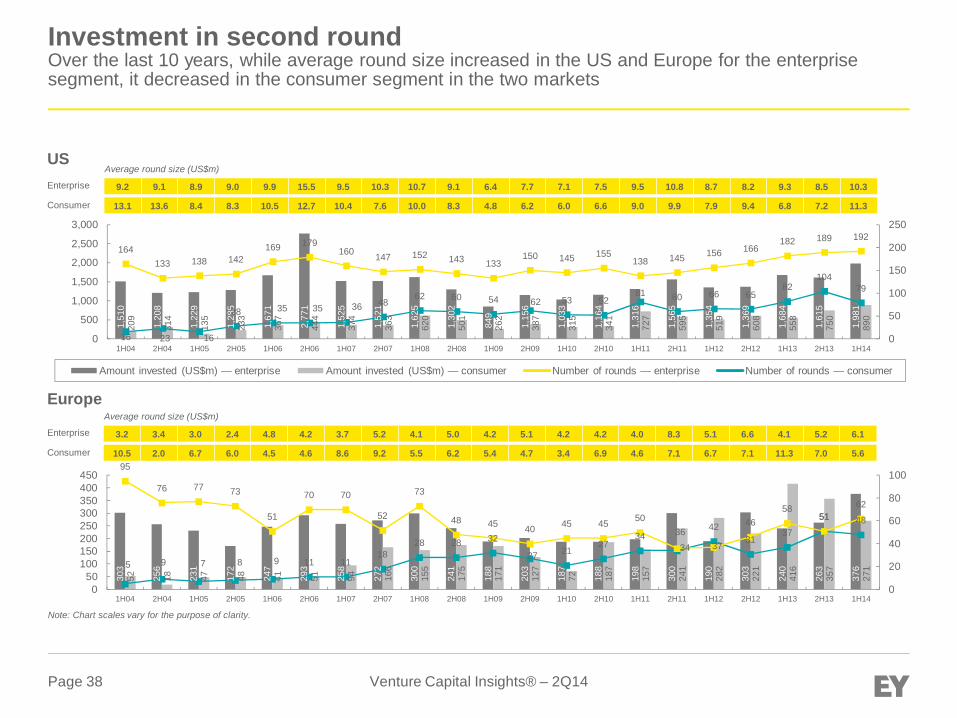

Investment in second roundOver the last 10 years, while average round size increased in the US and Europe for the enterprisesegment, it decreased in the consumer segment in the two markets

US9.2 9.1 8.9 9.0 9.9 15.5 9.5 10.3 10.7 9.1 6.4 7.7 7.1 7.5 9.5 10.8 8.7 8.2 9.3 8.5 10.3

13.1 13.6 8.4 8.3 10.5 12.7 10.4 7.6 10.0 8.3 4.8 6.2 6.0 6.6 9.0 9.9 7.9 9.4 6.8 7.2 11.3

Average round size (US$m)

Enterprise

Consumer

Europe

3.2 3.4 3.0 2.4 4.8 4.2 3.7 5.2 4.1 5.0 4.2 5.1 4.2 4.2 4.0 8.3 5.1 6.6 4.1 5.2 6.1

10.5 2.0 6.7 6.0 4.5 4.6 8.6 9.2 5.5 6.2 5.4 4.7 3.4 6.9 4.6 7.1 6.7 7.1 11.3 7.0 5.6

Average round size (US$m)

Enterprise

Consumer

Note: Chart scales vary for the purpose of clarity.

1,51

0

1,20

8

1,22

9

1,28

5

1,67

1

2,77

1

1,52

5

1,52

1

1,62

5

1,30

2

849

1,15

6

1,03

3

1,16

4

1,31

6

1,56

5

1,35

4

1,36

9

1,68

4

1,61

5

1,98

1

209

314

135

233

367

444

374

363

620

501

262

387

315

341

727

595

519

608

558

750

890

16 23 16

28 35 35 36 4862 60 54 62 53 52

81 60 66 6582

10479

164133 138 142

169 179160 147 152 143 133

150 145 155138 145 156 166

182 189 192

0

50

100

150

200

250

0

500

1,000

1,500

2,000

2,500

3,000

1H04 2H04 1H05 2H05 1H06 2H06 1H07 2H07 1H08 2H08 1H09 2H09 1H10 2H10 1H11 2H11 1H12 2H12 1H13 2H13 1H14

303

256

231

172

247

293

258

272

300

241

188

203

187

188

198

300

190

303

240

263

376

52 18 47 48 41 51 94 166

155

175

171

127

72 187

157

241

282

221

416

357

2715 9 7 8 9 11 11

1828 28 32

27 2127

3434

4231

37

51 48

95

76 77 73

51

70 70

52

73

48 45 40 45 45 5036

37

4658

5162

0

20

40

60

80

100

050

100150200250300350400450

1H04 2H04 1H05 2H05 1H06 2H06 1H07 2H07 1H08 2H08 1H09 2H09 1H10 2H10 1H11 2H11 1H12 2H12 1H13 2H13 1H14

Amount invested (US$m) — enterprise Amount invested (US$m) — consumer Number of rounds — enterprise Number of rounds — consumer

Venture Capital Insights® – 2Q14Page 39

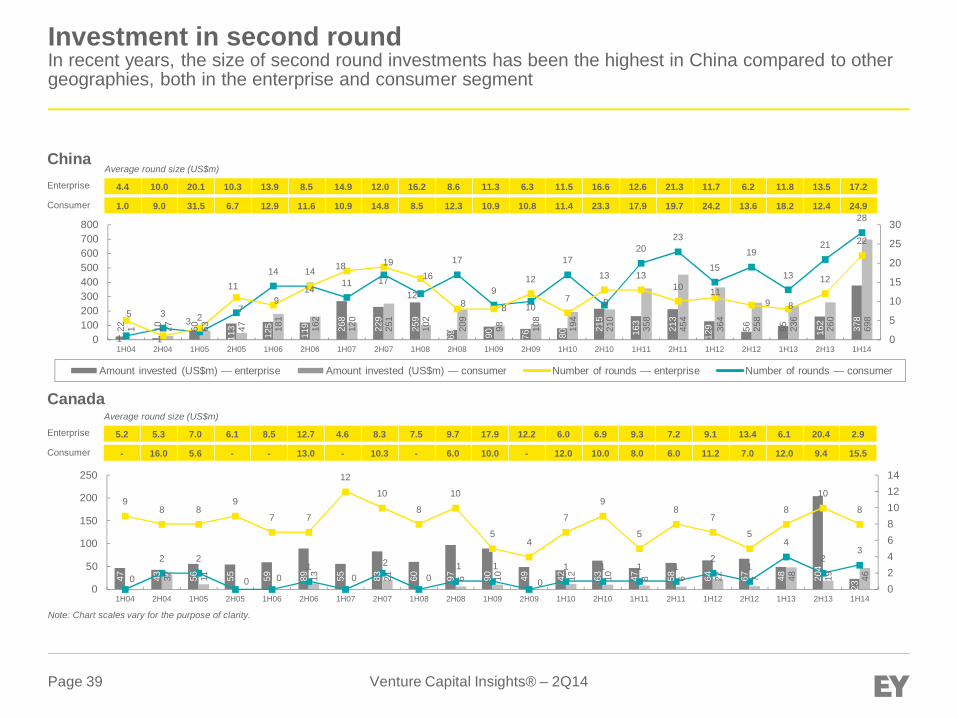

Investment in second roundIn recent years, the size of second round investments has been the highest in China compared to othergeographies, both in the enterprise and consumer segment

China4.4 10.0 20.1 10.3 13.9 8.5 14.9 12.0 16.2 8.6 11.3 6.3 11.5 16.6 12.6 21.3 11.7 6.2 11.8 13.5 17.2

1.0 9.0 31.5 6.7 12.9 11.6 10.9 14.8 8.5 12.3 10.9 10.8 11.4 23.3 17.9 19.7 24.2 13.6 18.2 12.4 24.9

Average round size (US$m)

Enterprise

Consumer

Canada

Amount invested (US$m) — enterprise Amount invested (US$m) — consumer Number of rounds — enterprise Number of rounds — consumer

5.2 5.3 7.0 6.1 8.5 12.7 4.6 8.3 7.5 9.7 17.9 12.2 6.0 6.9 9.3 7.2 9.1 13.4 6.1 20.4 2.9

- 16.0 5.6 - - 13.0 - 10.3 - 6.0 10.0 - 12.0 10.0 8.0 6.0 11.2 7.0 12.0 9.4 15.5

Average round size (US$m)

Enterprise

Consumer

Note: Chart scales vary for the purpose of clarity.

22 10 60

113

125

119 26

8

229

259

69 90 76 80

215

163

213

129 56 95 162

378

1 27 63 47 181

162

120

251

102

209

98 108

194

210

358

454

364

258

236

260

698

1

3 27

14 1411 17

12

17

9

10

17

9

2023

1519

13

21

28

5

1

3

119

14

18 1916

8 8

12

7

13 1310 11

9 8

12

22

0

5

10

15

20

25

30

0100200300400500600700800

1H04 2H04 1H05 2H05 1H06 2H06 1H07 2H07 1H08 2H08 1H09 2H09 1H10 2H10 1H11 2H11 1H12 2H12 1H13 2H13 1H14

47 43 56 55 59 89 55 83 60 97 90 49 42 63 47 58 64 67 48 204

23

32 11 13 21 6 10 12 10 8 6 22 7 48 19 460