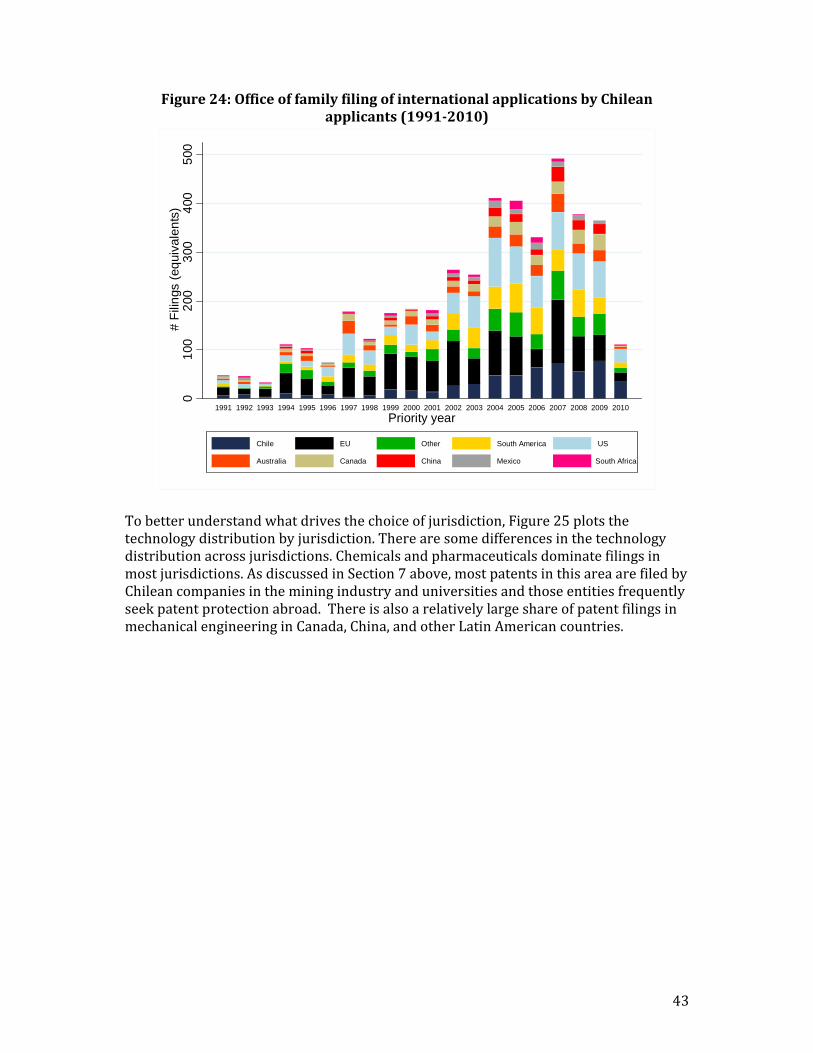

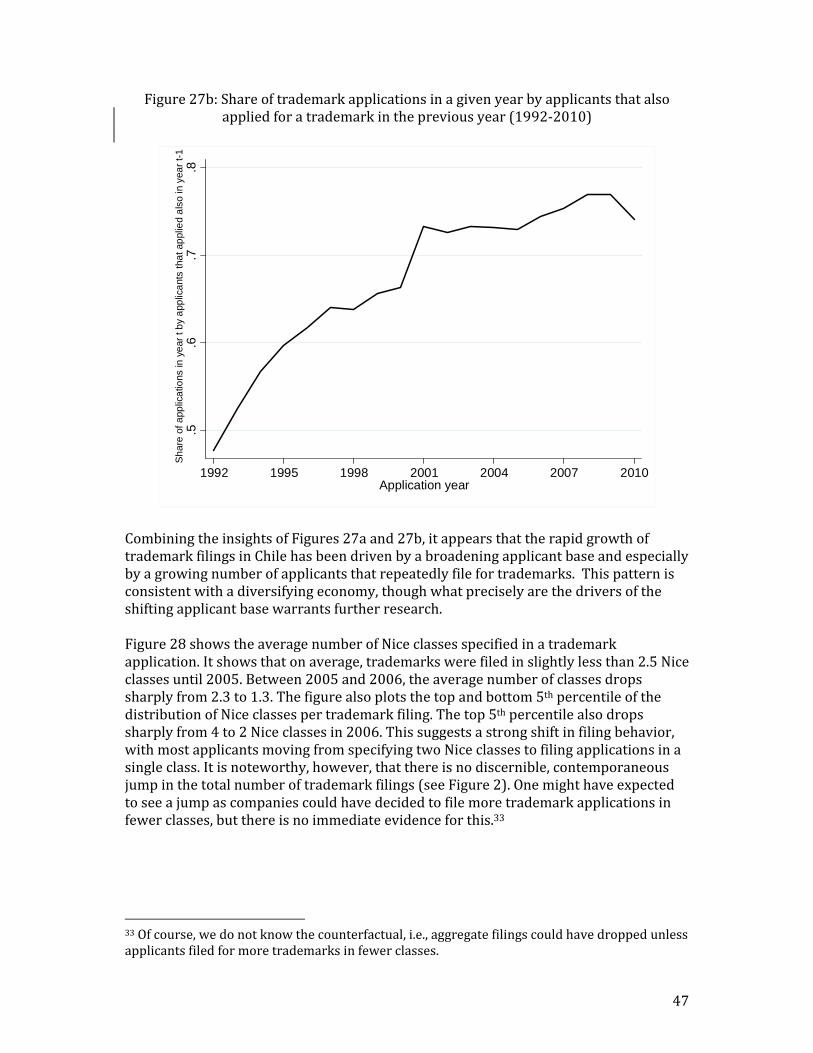

the use of intellectual property in chilebhhall/papers/abudfinkhallhelmers13... · 1 the use of...

TRANSCRIPT

1

The Use of Intellectual Property in Chile

INAPI-WIPO

March 2013

PreparedbyMariaJoseAbud,CarstenFink,BronwynHall,andChristianHelmers.ThestudyhasbenefitedfromcommentsfromCarmenPazAlvarez,GustavoCrespi,AisénEtcheverry,AdanGonzalez,MaríaCatalinaOlivos,MaximilianoSantaCruz,NicolasSchubert,LuzSosa,andPilarTrivelli.

2

ContentsExecutive Summary ................................................................................................................................. 4

1. Introduction ....................................................................................................................................... 7

2. The IP system in Chile ....................................................................................................................... 10

3. Overall trends .................................................................................................................................... 14

4. Origin of applications ....................................................................................................................... 18

5. Applicant distribution....................................................................................................................... 20

6. Applicant types ................................................................................................................................. 24

7. Filings by technology and class ........................................................................................................ 26

8. Grant ratios and lags ......................................................................................................................... 31

9. IP bundles ......................................................................................................................................... 35

10. Co‐assignment of patents .............................................................................................................. 37

11. Patent filings abroad ...................................................................................................................... 40

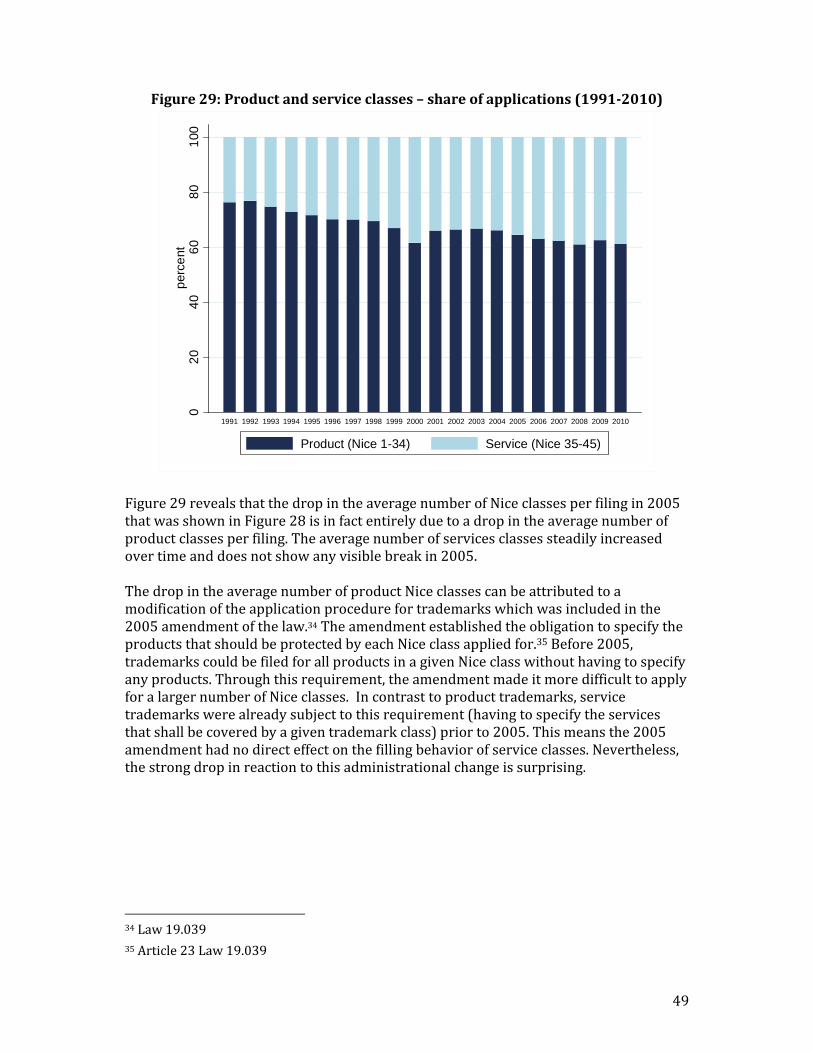

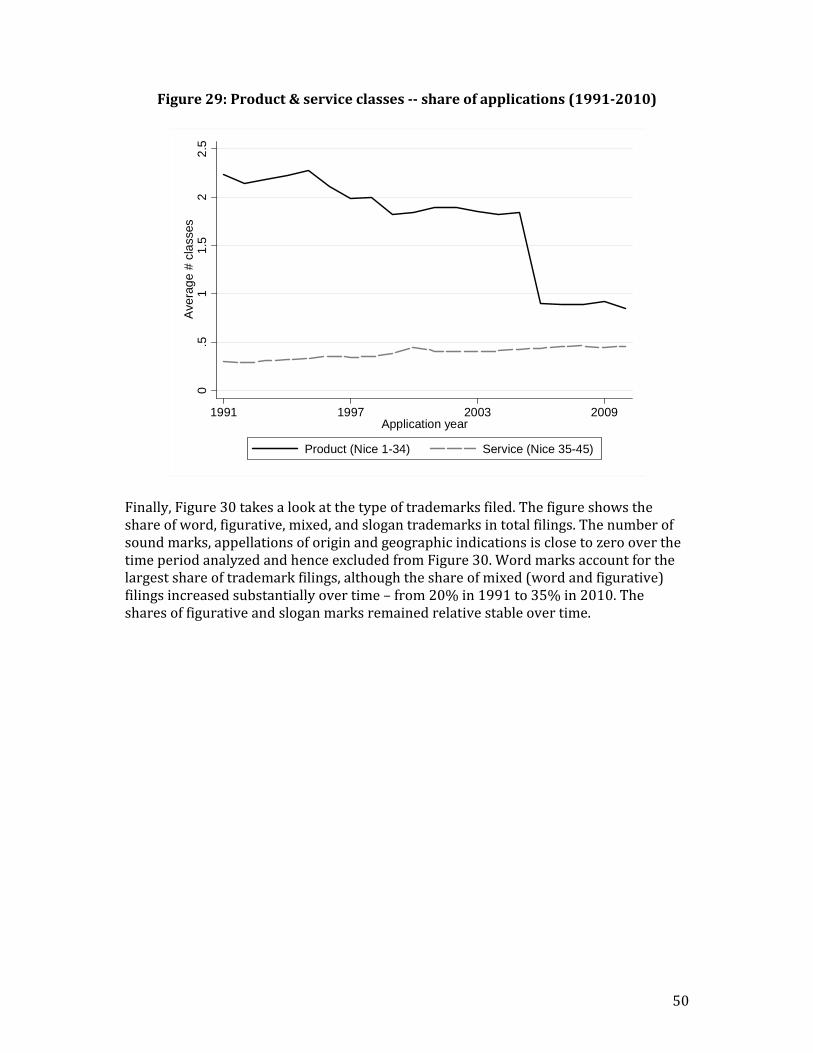

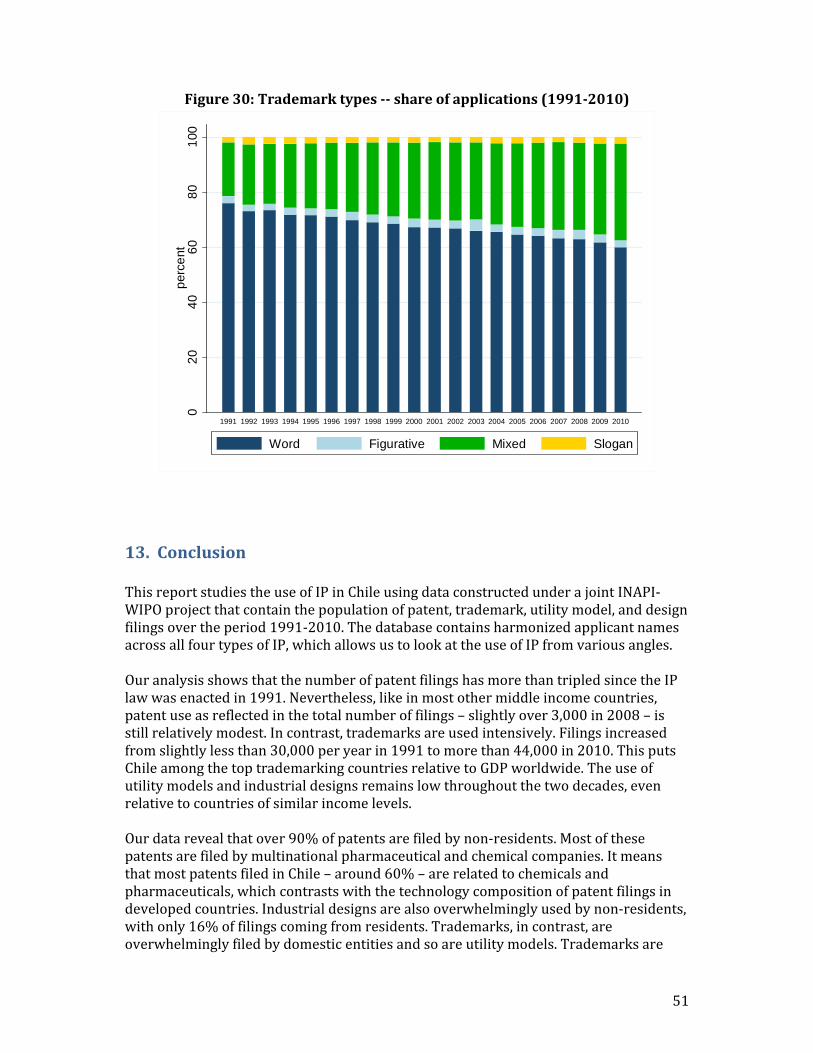

12. A closer look at trademark activity ................................................................................................ 45

13. Conclusion ...................................................................................................................................... 51

References ............................................................................................................................................ 54

Appendix 1: The IP system in Chile ....................................................................................................... 55

Appendix 1.1: Application Procedure for Trademarks...................................................................... 55

Appendix 1.2: Intellectual Property Rights Enforcement ................................................................. 56

Appendix 1.3: Restrictions on patentability ...................................................................................... 57

Appendix 1.4: Application procedure for patents, utility models, industrial designs, drawings and

integrated circuit topographies ........................................................................................................ 59

Appendix 2: The INAPI‐WIPO Intellectual Property database .............................................................. 62

Appendix 2.1 Introduction ................................................................................................................ 62

Appendix 2.2 Description of the Raw Data ....................................................................................... 62

2.2.1 Characteristics of the raw data ............................................................................................ 62

Appendix 2.3 Data challenges ........................................................................................................... 63

2.3.1 Identification of unique RUT for each applicant .................................................................. 64

2.3.2. Identification of unique RUT for each applicant ................................................................. 65

Appendix 2.4 Data Base Design ........................................................................................................ 66

2.4.1 Trademark Data ................................................................................................................... 66

3

2.4.2 Patent Data .......................................................................................................................... 68

Appendix 2.5 Combining Trademark and Patent Data ..................................................................... 69

Appendix 2.6 Trademark Data .............................................................................................................. 72

2.6.1 Nice classes .......................................................................................................................... 72

2.6.2 Priority information ............................................................................................................. 72

2.6.3 Trademark type and use ...................................................................................................... 72

2.6.4 Application, publication and registration date .................................................................... 72

2.6.5 Legal status .......................................................................................................................... 73

Appendix 2.7 Patent Data ..................................................................................................................... 73

2.7.1 IPCs ....................................................................................................................................... 73

2.7.2 Priority Information ............................................................................................................. 74

2.7.3 Application, grant, and lapse date ....................................................................................... 74

2.7.4 Legal Status .......................................................................................................................... 74

4

ExecutiveSummaryThepastdecadeshaveseenprofoundchangesintheuseoftheintellectualproperty(IP)systemworldwide. Severalforceshavedriventhesechanges. First, investmentinthecreation of intangible assets has markedly increased. Second, the increasedinternational integrationofnational economieshasprompted companies toobtain IPprotectionmoreoften inmultiple jurisdictions, including anumberofmiddle incomeeconomies. Third, national intellectual property policies have undergone substantialreforms. Fourth, technological advances and evolving business models – driven bytechnological opportunities, complexity and competitive pressures – have ledcompanies to adapt their innovation management, often leading to more active IPmanagementandfilingstrategies.TheresultingchangesintheIPlandscapeshavepromptednumerousnewquestionsonthe role that the IP system plays in the innovation process. So far the economicsliterature has heavily focused on high income countries and does not provide muchevidence on the role of IP in middle income economies. There appear to be twounderlying reasons. First, in absolute terms, these countries have seen the largestincreases in IP use and questions of IP protection have gathered considerable publicinterest.Second,effortsbyIPofficesinhighincomecountriesandacademicresearchershave led to the creation of micro‐level patent and trademark databases that haveenabled a wide range of empirical investigations. To date, no comparable datainfrastructureexistsformiddleincomeeconomies.ThisstudyreportsontheoutcomeofajointeffortbytheNationalIndustrialPropertyInstituteofChile (INAPI)and theWorld IntellectualPropertyOrganization (WIPO) tobuild a comprehensive database on the use of IP in Chile. This database contains allpatent,trademark,utilitymodel,andregistereddesignfilingsforChileovertheperiod1991‐2010. One key contribution of the data construction work was to harmonizeapplicantnamesanduniquely identifyapplicants forall four formsof IP. Inaddition,the datawerematched to firm‐level data of the National Statistical Institute (INE) –specifically,themanufacturingcensus(ENIA)aswellasfivewaves(1997‐2008)oftheChileaninnovationsurvey(INNOVACION).ChileoffersaninterestingsettingtostudytheroleofIPintheinnovationprocessofamiddle income economy. Chile has achieved considerable economic growth over thepast decades, but still relies heavily on commodities and agricultural products as itsexport base. Chile has also proactively integrated into theworld economy through alarge number of bilateral and regional trade agreements. It has modified its IP lawseveral times during the past two decades, strengthening IP protection significantly.Chile also has a large number of research active universities. Shifting the sources ofeconomicgrowthtowardsnewsectorsandgainsineconomy‐wideproductivitythroughinnovationisanimportantimperativeforChileanpolicymakers. Thenewdatabase–henceforththeINAPI‐WIPOdatabase–enablesnewinvestigationsthat candeepenourunderstandingof the role thatpatentsplay inChile’s innovation

5

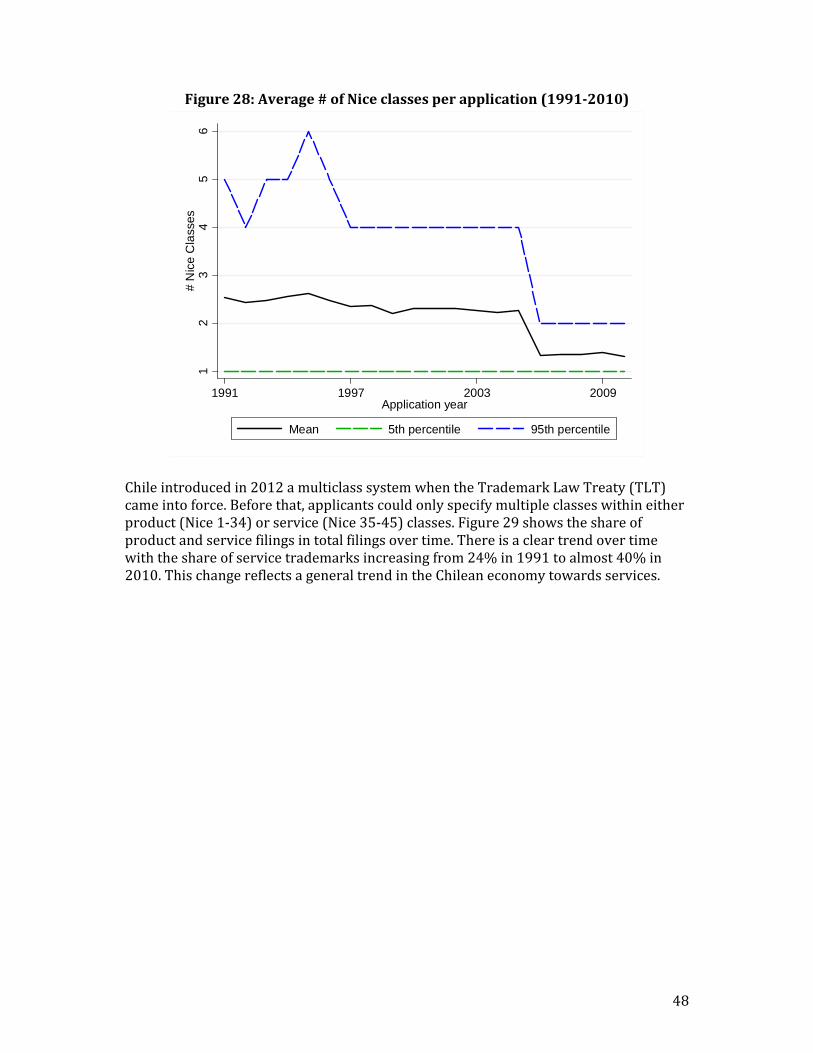

systemandexplorenewquestionsthathavenotbeenconsideredsofar.Asafirststep,thispaperprovidesadescriptiveoverviewofIPuseinChile.OuranalysisshowsthatthenumberofpatentfilingshasmorethantripledsincetheIPlaw was enacted in 1991. Nevertheless, like in most other middle income countries,patentuseasreflectedinthetotalnumberof filings–slightlyover3,000in2008– isstill relativelymodest. In contrast, trademarks are used intensively. Filings increasedfromslightlylessthan30,000peryearin1991tomorethan44,000in2010.ThisputsChile among the top trademarking countries relative to GDP worldwide. The use ofutilitymodels and industrial designs remains low throughout the two decades, evenrelativetocountriesofsimilarincomelevels.Our data reveal that non‐residents file over 90% of patents in Chile. Multinationalpharmaceutical and chemical companies file most of these patents – in contrast todevelopedcountries,whereso‐calledcomplex technology industriesaccount formostpatent filings. Industrialdesignsarealsooverwhelminglyusedbynon‐residents,withonly16%offilingscomingfromresidents.Trademarks,incontrast,areoverwhelminglyfiledbydomesticentitiesandsoareutilitymodels.Trademarksarewidelyusedacrosstheeconomy.Agriculturalproductsaccountforthelargestshareoftrademarkfilings,acategory which includes wine and fruit products. There is also a large share oftrademarksrelatedtopharmaceuticals.The great majority of patents are assigned to companies. However, a considerablenumber of Chilean universities file for patents and they are among the top residentpatentees. Other top resident patentees are companies in the mining industry andchemical and consumer product companies. Trademark filings come from bothcompaniesandindividuals.Incontrasttopatents,severalChileancompaniesareamongthetoptrademarkfilers,mostlycompaniesintheconsumergoodsindustry.Lookingat theoriginofnon‐resident filings, thedata show that thegreatmajorityofnon‐resident filingsacrossall four IP formscome from theUnitedStatesandEurope.Other SouthAmerican countries, in contrast, account foronly a small shareof filings.Forpatentstheyrepresentonly2%ofallfilingsbetween1991and2010,whereastheUS and EU combined account for more than 80% of filings. Pharmaceutical andconsumergoodscompaniesaccountformostofthesepatentfilings.The analysis also looks at the joint use of different IP rights. More than 90% ofapplicants only apply for trademarks and less than 5% of applicants apply only forpatents. Applicants that apply for more than a single type of IP right are rare; theyaccount for only 2% of applicants. The joint use of different IP rights is limited topatentsandtrademarksaswellastrademarksandindustrialdesigns.Abreakdownbyapplicant type shows that a large share of universities files for both patents andtrademarks.Thedatashowthattrademarkscovered,onaverage,in2.5Niceclassesuntil2005.Duetoachange in the law in2005, theaveragenumberofclassesdeclinedsharply to1.3classes in2006.A fall in theaveragenumberofproduct classesexplains thisdecline.Theaveragenumberofservicesclasses, incontrast,steadily increasedovertime.This

6

reflects the nature of the legal change in 2005,which did not affect filings in serviceclasses.The INAPI‐WIPO dataset can identify co‐assignment patterns in patent filings. Co‐assignments are interesting as they reveal underlying research co‐operation betweenuniversitiesand industryaswellasamongproductmarket competitors.Like inothercountries, co‐assignedpatentsaccount forasmall shareofpatent filings inChile–onaverage less than 3% between 1991 and 2010. We find that most patents are co‐assigned among non‐resident companies and in fact there is little evidence forinternational cooperation. The share of co‐assigned patents with resident and non‐residentassigneesisonly8%.Co‐assignmentsinvolvinguniversitiesaccountforaround20%ofco‐assignedpatents,whichsuggestsasignificantamountofuniversity‐industrycollaboration.Finally,weanalyzeinternationalpatentfilingsthathaveatleastoneChileanassigneeorinventor.We show that only a small fraction among resident patentees also files forpatentprotectionabroad.Nevertheless,theshareincreasedfrom2%in1992toaround10% from 2006 onward. The data also show that half of the inventions underlyinginternationalpatentfamiliesassignedtoChileanresidentsoriginateinChile.Themostimportant foreign offices of first filing are theUS and Europe. Other SouthAmericancountries,incontrast,arerarelythejurisdictionoffirstfiling.China,Mexico,andSouthAfrica emerge from 2000 onward as important destinations for patents by Chileanapplicants. International filings by Chilean residents in most jurisdictions aredominatedbypatentsrelatedtothemining industryandchemicalsaswellaspatentsfiledbyuniversities.Overall,thisstudyoffersanexampleofempiricalresearchthatcanbeconductedontheuseofIPinamiddleincomeeconomyonceanappropriatedatainfrastructurehasbeenputinplace.ItalsoshowstheimportanceofincludingotherIPrightsbeyondpatentsinthistypeofanalysisandofanalyzingtheuseofthedifferentformsofIPincombinationratherthanisolation.ThedescriptiveevidenceprovidedinthisstudyprovidesusefulinsightsinbetterunderstandingtheroleofIPinChile’seconomy.Ofcourse,descriptiveevidencecanonlygosofarinfullyevaluatingtheeffectsofIPpolicychoicesonapplicantbehaviorandeconomicperformance.Deeperanalysisonthebasisofthenewlyavailabledatainfrastructureisneeded.Indeed,twoanalyticalstudies–ontheincidenceandeffectsoftrademarksquattingaswellasontheroleofpatentsinthedomesticpharmaceuticalsector–arecurrentlyunderwayandwillbemadeavailableseparately.

7

1.IntroductionThepastdecadeshaveseenprofoundchangesintheuseoftheintellectualproperty(IP)systemworldwide.Severalforceshavedriventhesechanges.First,investmentinthecreationofintangibleassetshasmarkedlyincreased.Forexample,globalR&Dexpenditurealmostdoubledinrealtermsfrom1993to2009.Availabledatasimilarlysuggestrisinginvestmentinotherintangibleassets,suchasdesignsandbranding.1Second,theincreasedinternationalintegrationofnationaleconomies–oftenreferredtoasglobalization–haspromptedintellectualpropertyholderstomorefrequentlyseekprotectionabroadand,indeed,inagreaternumberofcountries.2Third,nationalintellectualpropertypolicieshaveundergonesubstantialreformswithfar‐reachingimplicationsonthebehaviorofIPapplicants.Internationalagreements–notablytheAgreementonTrade‐RelatedAspectsofIntellectualPropertyRights(TRIPS)–havebeenanimportantdriveroflegalreforms.AsaresultdevelopingcountrieshaveseenasignificantstrengtheningofIPrightsoverthepasttwodecades.Therehavealsobeenincreasedeffortstowardstheharmonizationofproceduralstandardsandthecreationofregionalandinternationalfilingsystems.Technologicaladvanceshaveoftencontributedtolegalreforms,astheycreatedtheneedtoadaptIPpoliciestotheevolvingnatureoftechnologicalprogress.Finally,evolvingbusinessmodels–drivenbytechnologicalopportunitiesandcompetitivepressures–haveledcompaniestoadapttheirinnovationmanagementstrategies,importantlyaffectingthewaytheyusetheIPsystem.TheshiftingIPlandscapeshavepromptednumerousnewquestionsontherolethattheIPsystemplaysintheinnovationprocess.Forexample,howimportantaredifferentIPrightsforfirmstoappropriatereturnstoinvestmentsinnewtechnologyfields?Howdodensepatentlandscapesforcomplextechnologiesaffectinnovativebehaviorandcommercializationstrategies?HowcanIPofficesbestmanagethegrowinginflowsofapplicationsandpromotethedeliveryofqualityservices?Aricheconomicliteraturehasemergedthatoffersimportantempiricalperspectivesontheseandotherquestions.3However,thisliteratureheavilyfocusesonhighincomecountriesand,morerecently,alsoChina.Thisfocusappearstohavetwounderlyingreasons.First,inabsoluteterms,thesecountrieshaveseenthelargestincreasesinIPuseandquestionsofIPprotectionhavegatheredconsiderablepublicinterest.Second,effortsbyIPofficesinhighincomecountriesandacademicresearchershaveledtothecreationofmicro‐levelIPdatabasesthathaveenabledawiderangeofempiricalinvestigations.ThepatentdatabasespublishedbytheNationalBureauofEconomicResearch(NBER)intheUnitedStatesandthePatstatdatabasepublishedbythe

1SeeWIPO(2011a)forareviewoftheavailableevidence.2WIPO(2011b),forexample,showsthatinternationalfilingshavecontributedsubstantiallytothegrowthinpatentapplicationsworldwide.3Chapter2inWIPO(2011a)reviewssomeofthemostimportantstudiesinthefieldofpatents.

8

EuropeanPatentOffice(EPO)aregoodexamplesofsuchefforts.4AdditionaleffortstocombineIPdatawithmicro‐levelinformationonfirmperformanceandinventorbehaviorhavefurtherenrichedthedatainfrastructureavailabletoresearchers.Equivalentstudiesonmiddleincomecountries–exceptChina–remainscarce.5However,suchstudiesareofgreatinterest.ManymiddleincomeeconomieshavesimilarlyseenrapidgrowthinIPuse,oftendrivenbybothforeignanddomesticfilings,eveniftheabsolutenumbersremainsmallinaworldwidecontext.6Relativetothesizeoftheireconomies,certainmiddleincomecountriesevenseemoreintensiveuseofIP–especiallytrademarks–thanmosthighincomecountries.Manymiddleincomeeconomieshavebeenabletoigniteeconomicgrowthonthebackoflowwages,naturalresources,oracombinationofboth.Astheseeconomiescontinuetodevelop,theymaybeginorintensifythedevelopmentofinnovationdomestically.ThequestioniswhichroleIPcanplayinthisprocess–whetheritisgenerateddomesticallyorabroad.7Thedifferentstructureofmiddleincomeeconomies,theevolvingnatureofinnovativeactivity,andtheinstitutionalcontextsuggestthatthisrolediffersfromthatinhighincomeeconomies.PolicymakersinmiddleincomecountriesthuscannotrelyexclusivelyontheevidencegeneratedinadvancedeconomiesindesigningIPandinnovationpolicies.Theystandtobenefitfromempiricalresearchspecifictotheireconomies.OnecriticalconstrainttowardssuchresearchhasbeenthelackofanIPdatainfrastructure.TheEPO’sPatstatdatabaseoffersrichunitrecordpatentdataforalargenumberofmiddleincomecountries,butitisincompleteformanymiddleincomecountriesandcannotbestraightforwardlycombinedwithothermicrodatasources.Inanycase,Patstatonlycoverspatentsandutilitymodels.FullyexploitingthepotentialofIPdatarequiresdedicatedinvestmentsinnewdatabases.ThispaperreportsononesucheffortundertakenforChile.AspartofaprojectunderWIPO’sCommitteeonDevelopmentandIntellectualProperty(CDIP),INAPIincollaborationwithWIPOcreatedadatabasethatcontainsallpatent,trademark,utilitymodel,andregistereddesignfilingsforChileovertheperiod1991‐2010.8Onekey

4Seehttps://sites.google.com/site/patentdataproject/Homeandhttp://www.epo.org/searching/subscription/raw/product‐14‐24.html.5ThepatentsystemoftheRepublicofKoreahasalsoseenconsiderablestudy,butKoreaalreadyreachedhighincomestatusin1995.6SeeWIPO(2012)foranoverview.Chinaagainisanexception,asitemergedasthelargestrecipientofIPfilingsforallmajorformsofIPin2012.7Itisimportanttokeepinmindthatthereisnoone‐to‐onerelationshipbetweenIPandinnovation.Therefore,IPstatisticsprovidelimitedinformationoninnovationandbroadereconomicperformance.EveryIPtitledescribesadifferentintangibleasset.Thereisalargeliteraturepointingtoahighlyskeweddistributionofthoseassets.Fewpatentsyieldhigheconomicreturns.Ontheotherhand,thisdoesnotimplythatIPstatisticshavenouse.IPactivitycorrelatesinmeaningfulwayswithothermeasuresofinnovativeactivity–attheleveloffirms,industries,andeconomies.Indeed,IPstatisticsremainoneofthefewwidelyavailableindicatorsofinnovationavailabletoanalysts.8SeeWIPOdocumentCDIP/5/7.

9

contributionofthedataconstructionworkwastoharmonizeapplicantnamesanduniquelyidentifyapplicantsforallfourformsofIP.Inaddition,thedatawerematchedtofirm‐leveldataoftheNationalStatisticalInstitute(INE)–specifically,themanufacturingcensus(ENIA)aswellasfivewaves(1997‐2008)oftheChileaninnovationsurvey(INNOVACION).9Chileoffersaninterestingexampleofamiddleincomecountrythathasachievedconsiderableeconomicgrowthoverthepastdecades,butthatstillreliesheavilyoncommoditiesandagriculturalproductsasitsexportbase.Chilehasalsoproactivelyintegratedintotheworldeconomythroughalargenumberofbilateralandregionaltradeagreements.IthasmodifieditsIPlawseveraltimesduringthepasttwodecades,strengtheningIPprotectionsignificantly.Shiftingthesourcesofeconomicgrowthtowardsnewsectorsandgainsineconomy‐wideproductivitythroughinnovationisanimportantimperativeforChileanpolicymakers.Accordingly,Chilehasanumberofdedicatedprogramstopromoteinnovation.Forexample,theChileanEconomicDevelopmentAgency(CORFO)currentlyhasover30initiativesdesignedtopromoteinnovation,innovativeentrepreneurship,andtechnologytransfer.Chilealsohasotherdedicatedinnovationfunds,suchastheFundforAgrarianInnovation,whichhasafocusonagriculturalinnovation.Inaddition,thereistheFundofScientificandTechnologicalDevelopment,whichseekstopromoteR&Dprojectsofuniversitiesandpublicresearchinstitutesinconjunctionwithprivatecompanies.AnotherrelevantpolicyistheScientificMillenniumInitiative,whichaimstopromotethedevelopmentofscientificandtechnologicalresearch,throughthecreationandfinancingofscientificresearchinstitutes.ExistingstudiesontheChileaninnovationsystemofferimportantinsightsintothedeterminantsofcompanies’innovativeactivitiesasmeasuredintheChileaninnovationsurveys.However,asformostothermiddleincomecountries,therearefewempiricalstudiesontheuseofIPthatcouldinformpolicy.ExistingstudiestypicallyanalyzequestionsrelatedtoIPonlyinpassing,mostlyasoneaspectamongmanyrelatedtoinnovation,technologytransfer,exportingorproductivity.Chile’sinnovationsurveys,conductedfrom1992onwards,offersomeinformationonIPuse;however,theyrelyonrespondents’self‐reporteduseofIPandcoveronlycertainsegmentsontheChileaneconomy.ThelimitedempiricalliteratureontheChileanIPsystemhasbeenprimarilyconcernedwithpatentsand,inparticular,thelowuseofpatentsbyChileanresidents(OECD,2007;Amorósetal.,2008;KatzandSpence,2008).AccordingtotheOECD(2007),thelowpatentintensityinChilecanlargelybeexplainedbythreefactors.First,thereisalimitedcapabilityinChiletogenerateinnovativeandfirst‐to‐the‐worldproductsandprocesses.Second,Chilehasanindustrialspecializationinsectorswithalowpropensitytopatent,suchasminingandservices.WhilethereisagrowingChileanpharmaceuticalindustry,itislargelyfocusedontheproductionofgenericsandbranddrugsunderlicensingcontracts.Third,whileChilehasanumberofsuccessfulexporters,theyrelymainlyonimportedtechnologiesandhenceareunlikelytorelyon

9ThisreportdoesnotincludeananalysisofthematcheddatabutfocusesonananalysisofIPfilingsmoregenerally.

10

patentsfortheirbusinessmodel.ThelowuseofpatentsbyChileanresidentsstandsinstarkcontrasttotheirheavyuseofthetrademarksystem.However,despitethelargenumberoftrademarkapplicationsinChile,therearenoempiricalstudiesontheuseoftrademarksintheChileaneconomy.Thenewdatabase–henceforththeINAPI‐WIPOdatabase–enablesnewinvestigationsthatcandeepenourunderstandingoftherolethatIPrightsplayinChile’sinnovationsystemandexplorenewquestionsthathavenotbeenconsideredsofar.Asafirststep,thispaperprovidesadescriptiveoverviewofIPuseinChile.Thepaper’sdiscussionisstructuredasfollows.Asbackground,Section2willofferashortintroductionintothemainfeaturesofChile’sIPsystem.ThefollowingsectionswillthendiscussdifferentdimensionsofIPuse–focusing,inparticular,onoveralltrends(Section3),theoriginofIPapplications(Section4),theapplicantdistribution(Section5),applicanttypes(Section6),filingsbytechnologyandclass(Section7),grantratiosandlags(Section8),IPbundles(Section9),co‐assignmentpatternsofpatents(Section10),patentfilingsabroad(Section11),andadditionalperspectivesonthetrademarksystem(Section12).Aconcludingsectionsummarizesthekeyfindingsofthedescriptiveanalysisandpointstopotentialavenuesforfutureresearch.Thepaper’sappendixprovidesadditionaldetailsonthelegalIPregimeinChileaswellasadetaileddescriptionofthemethodologyusedtoconstructthedata.

2.TheIPsysteminChileThe Intellectual property system in Chile is administeredby various institutions. TheMinistry of Education is in charge of the Copyright Register,10the Ministry ofAgriculture is in charge of plant breeder’s rights aswell as in part of appellations oforiginforwinesandspiritsandofundisclosedinformationregardingagrochemicals.11The Ministry of Health is in charge of undisclosed information regardingpharmaceutical products12 and the Ministry of Foreign Affairs is in charge ofinternational negotiations and of the coordination of an inter‐ministerial technicalcommitteefortheimplementationofinternationalcommitments.13INAPIisthemainGovernmentagencyinchargeofindustrialpropertyrightssince2009.Besidesactingastheregisterforpatents,trademarks,industrialdesigns,utilitymodels,andappellationsof origin, INAPIalso functions as a first instance court inoppositionandnullityprocedures. In addition, it has several other important functions: INAPI isadvisor to thePresidentofChileonall issuesconcerning industrialproperty; it is theagencyinchargeofrecommendingtheaccessiontoIPtreaties;anditistaskedwiththe

10TheMinistryofEducationhasanIntellectualPropertyDepartmentwhichispartoftheDirectorateforLibraries,ArchivesandMuseumsoftheMinistry.11ThroughtheCattleandAgriculturalServiceoftheMinistry.12TherelevantbodyisthePublicHealthInstituteoftheMinistry.13ThroughtheIntellectualPropertyDepartment,whichispartoftheGeneralDirectorateforInternationalEconomicRelationsoftheMinistry.

11

promotionof IP and thedisseminationof knowledge,particularly of information thathasfalleninthepublicdomain.Thelawonindustrialproperty(Law19.039),whichcoverstrademarks,inventionpatents,utilitymodels,geographicalindications,appellationsoforigin,integratedcircuittopographies,drawingsandindustrialdesigns,enteredintoforceinOctober1991.Sincethenthelawhasundergonethreemajoramendments.Thefirstamendment(Law19.996)waspublishedinMarch2005andenteredintoforceinDecember,2005.ThislawadaptedChileanlegislationtoTRIPS,mainlythroughchangestooppositionproceedings,trademarkableandpatentablesubjectmatter,andthestatutorylifetimeofpatents.Italsoincorporatedindustrialdrawings,geographicalindications,appellationsoforiginandintegratedcircuittopographiesintonationallegislation.Finally,italsointroducedtradesecrecyandcivilactionsforIPenforcement–before2005,IPinfringementwasonlysanctionedbycriminalcourts.Thesecondmajoramendment(Law20.160)enteredintoforceinJanuary,2007.ItadaptedChileanlegislationtofreetradeagreementssignedsincethe2000s.ThisamendmentcontainsmainlychangesregardingcancellationproceduresforallIPrightsandthedefinitionofsubjectmattereligibleforgeographicalindicationsandappellationsoforigin.Italsoincorporatessoundmarksintothelaw.Thethirdamendment(Law20.569)enteredintoforceinFebruary,2012.ThislawincorporatedcertainprovisionsagreedbyChilethroughthesignatureoftheTrademarkLawTreaty(TLT)andthePatentCooperationTreaty(PCT).Thissectionoffersabriefdescriptionofthelegalregimeapplicabletopatents,trademarks,utilitymodelsandindustrialdesignswhicharecoveredbytheanalysis.14TrademarksTrademarksaredefinedassignsthatdistinguishproducts,services,orindustrialandcommercialestablishmentsinthemarket.Since2007,atrademarkcanalsobeusedtoprotectslogansorsoundsmarks.Atrademarkcanbeclassifiedasaword,figurativeormixedmark.Wordmarksprotectawordorwordswithorwithoutidiomaticmeaningoracombinationoflettersand/ornumbers.Figurativetrademarksarelabelswithpictures,images,symbolsordrawings.Mixedtrademarksareacombinationofbothwordandfigurativetrademarks–thatis,labelsthathaveawordorwordswithorwithoutidiomaticmeaningoracombinationoflettersand/ornumbers,combinedwithpictures,images,symbolsordrawings.ChileisnotpartoftheMadridSystemfortheInternationalRegistrationofMarks,whichmeansthatnon‐residentapplicantshavetofiledirectlywithINAPItoobtainatrademarkinChile.DetailsontheregistrationprocedurefortrademarkscanbefoundinAppendix1.1.Trademarkrightslastforaperiodof10yearsfromthegrantdatebutcanberenewedindefinitely.Unlikesomeothercountries,INAPIdoesnotrequiretheapplicanttoproveactualuseofthetrademark,neitherattheinitialfilingstagenorattherenewalstage.

14Thediscussiondoesnotcovergeographicalindications,appellationsoforiginandintegratedcircuittopographies(thatis,semiconductormaskprotection).

12

Duringtheapplicationprocess,thirdpartiescanfileanoppositionduringa30dayperiodfollowingthepublicationofthemark.INAPIdoesnotnotifythirdpartieswhohaveprevioustrademarkapplicationsorregistrationsthatcouldjustifyanopposition.Ifnooppositioniffiled,thetotalprocessingtimeofanapplicationuntilitsregistrationisapproximatelyninemonths.Ifthereisanopposition,theproceduremaytakeonaveragesevenmonthslonger.Atrademarkcanalsobecancelledpost‐grant.Anypersoncanrequestthecancellationofaregisteredtrademark.Atrademarkcanonlybecancelledwithinfiveyearsafteritwasregistered.Thisrestrictiondoesnotapplywhenatrademarkwasobtainedinbadfaith.DetailsoncancellationproceduresareprovidedinAppendix1.1.IfINAPIcancelsatrademark,thetrademarkisconsideredvoidasofthegrantdate.Ifatrademarkwasdismissedorcancelledduetotheexistenceofafamousandwell‐knowntrademarkabroad,theownerofthetrademarkhas90daystoregisterthetrademark.Oncethe90dayperiodlapses,anyinterestedpartycanapplyforthetrademark.AccordingtoChileanlaw,trademarkcounterfeitingissanctionedbybothcivilandcriminallawdependingonthetypeofinfringement.DetailsabouttheenforcementoftrademarksareprovidedinAppendix1.2.PatentsThemostimportantchangestothescopeofpatentprotectionoccurredintheareaofpharmaceuticals.In1991,activechemicalandpharmaceuticalingredientsbecamepatenteligible,whereasbefore1991onlytheproductionprocesscouldbepatented.Theamendmentin2005restrictedthepatenteligibilityofnewusesofknownsubstances.Priorto2005,newuseswerepatentableiftheysolvedatechnicalproblemorchangedtheessentialqualitiesoftheinvention.Followingtheamendment,thelawrequiresthatbothconditionsbesatisfied.Moreover,tobepatenteligible,thenewusehastobesupportedbyempiricalevidence.InChile,softwareperseisnotpatenteligibleandprotectedbycopyright.15Appendix1.3providesdetailsonpatenteligiblesubjectmatter.Beforethe2005amendment,thestatutorylifetimeofapatentwas15yearsfromthegrantdate.Theamendmentchangedthisinto20yearsfromthedateoffilling.Thistermisnotrenewable.Thereisa45daytermduringwhichthirdpartiescanpresentanoppositiontoapatentapplication.Oppositionispossibleonthegroundsthatanapplicationdoesnotmeetoneormoreofthepatentabilityrequirements.Thegroundsforcancellationhaveremainedthesamesince1991.Anypersoncanrequestthecancellationofagrantedpatent.The2005amendmentreducedthetimeframeduringwhichapatentcanbecancelledfrom10to5yearscountingfromthedateofgrant.Incontrasttotrademarks,badfaithdoesnotsuspendthisrestriction.Appendix1.4providesfurtherdetails.

15Law17336ofIntellectualProperty.

13

Asfortrademarks,patentinfringementcanbesanctionedbybothcivilandcriminallawdependingonthetypeofinfringement.DetailsaboutenforcementareprovidedinAppendix1.2.UtilitymodelsUtilityModelsaresimilartopatents,butgenerallyapplytolesscomplextechnicalinventionsthanpatents.Utilitymodelscanprotectinstruments,apparatus,tools,devicesorobjectswhichcanbedescribedinclaimform.Thelegalprotectionofutilitymodelsappliestoanindividualobject,butprotectionofseveralelementsoraspectsofanobjectcanbeclaimedinasingleapplication(Article56Law19309).Utilitymodelsdifferfrompatentsinthefollowingways:

Utilitymodelsareexemptoftheinventivesteprequirementofinventionpatents. Utilitymodelsonlyneedtobenewandhaveindustrialapplicability. Utilitymodelslastforanon‐renewabletermof10yearscountingfromthe

applicationdate. Theregistrationprocedureforautilitymodelinvolvesthesamestepsand

deadlinesasforapatent(seeAppendix1.4).However,becausethetechnologyinvolvedisgenerallylesscomplexandnoveltyisnotassessed,theprocedureforutilitymodelsisgenerallyfasterandsimplerthaninthecaseofinventionpatents.Allfeesarethesameasforpatents,exceptfortheexaminationfeewhichischeaperforutilitymodelsthanforpatents.16

Utilitymodelscanonlybeobtainedforproducts,notforprocesses.Accordingly,utilitymodelsaremorerelevantforcertaintechnologicalareassuchasmechanicalorelectricalengineering.

IndustrialdesignsanddrawingsIndustrialdesignsareanythree‐dimensionalshapesandindustrialorhandicraftitemsthatcanbeusedasatemplatefortheproductionofotherunits.Industrialdesignsmustbedistinguishablefromsimilarthreedimensionalobjects,eitherbytheirshape,geometricconfiguration,ornamentationoracombinationofthesecharacteristics(Article62Law19309).Industrialdrawingsincludeanysetorcombinationoffigures,linesorcolorsthataredevelopedonaflatsurface.Industrialdrawingsmustbecapableofbeingpartofanindustrialproductandprovideanewlooktotheproduct.Industrialdesignsanddrawingsdifferfrompatentsinthefollowingways:

IndustrialDesignsanddrawingsareexemptoftheinventivestepandindustrialapplicabilityrequirementsofpatents.Theyareonlyrequiredtobenew.Designsanddrawingsareconsiderednewiftheydiffersignificantlyfromknowndrawingsorindustrialdesignsoriftheydifferfromcombinationsof

16Forpatentsthefeeis$427.000Chileanpesos(approx.US$900dollars).Forutilitymodels,thefeeis$343.000(approx.US$730dollars).

14

characteristicsofknowndrawingsandindustrialdesigns(Article62Law19039).ThepriorartsearchisconductedsearchingforindustrialdesignsanddrawingsprotectedunderthesameLocarnoclassificationininternationalofficessuchastheUSPTOortheOfficeforHarmonizationintheInternalMarket(OHIM).Fordrawings,noveltymeansanewphysiognomy,fordesignsanewappearance.

Industrialdesignsanddrawingsarevalidforanon‐renewabletermof10yearsfromthedateoffiling.

Theapplicationprocedureforindustrialdesignsanddrawingsinvolvesthesamestepsanddeadlinesasforpatents(seeAppendix1.4).However,industrialdesignsanddrawingsdonotcontainclaims.

Allfeesarethesameasforpatentsexceptfortheexaminationfeewhichislowerforindustrialdesignsanddrawings.17

3.OveralltrendsOverthepasttwodecades,INAPIhasseenrapidgrowthintheuseofmostIPforms.Figure1presentsthefilingtrendforpatents,utilitymodels,andindustrialdesignsovertheperiod1991‐2010.Patentfilingshavemorethantripledfrom775applicationsperyearin1991toover3,000in2008.Whileitisdifficulttopreciselyquantifythedriversoftheobservedgrowthinpatentfilings,threefactorsappeartostandout:

asdescribedintheprevioussection,Chile’spatentreformin1991expandedthescopeofpatentprotectiontonewsubjectmatter,notablypharmaceuticalproducts;

theChileaneconomyhasexperiencedrobustgrowthsincetheearly1990s,promptinggreaterinterestbyinnovatorsintheChileanmarket;

thepasttwodecadeshaveseengreaterrelianceonthepatentsystemworldwide,andChilehasbecomemorecloselyintegratedintotheglobaleconomy.

Despitetheextensionofthestatutorypatentlifefrom15to20yearsin2005bythefirstamendmenttotheIntellectualPropertyLaw(seeSection2),thereisnovisibletrendbreakinthenumberoffilings.Thenumberoffillingsbeginstorisealreadyin2004aheadoftheamendment.

17Forpatentstheexaminerfeeis$427.000Chileanpesos(approx.US$900dollars)andforindustrialdesignsanddrawingsitis$287.000(approx.US$600dollars).

15

Figure1:#patent,utilitymodel,designfilings(1991‐2010)

01

000

200

03

000

# F

ilin

gs

1991 1995 1999 2003 2007Filing year

PatentsUtility ModelsDesigns

Frommid‐2009to2010,patentfilingsdroppedsharplyduetoChile’saccessiontothePatentCooperationTreaty(PCT),effectiveasofJune2,2009.InsteadofdirectlyfilinginChile,mostnon‐residentapplicantsoptedforaPCTinternationalapplication,affordingthemupto18monthstoformadecisiononwhethertoapplyforprotectioninChile.Thistransitionalfilingdeclinecametoanendatthebeginningof2011,whichisnotcoveredbyourdata,asnon‐residentapplicantsbegantoenterthePCTnationalphaseinChile.ItisimportanttokeepthisPCTaccessioneffectinmindwhenlookingatpatentfilingfiguresfor2009and2010intheremainderoftheanalysis.IndustrialdesignsandutilitymodelsarefarlesspopularinChile.Thenumberofannualutilitymodelandindustrialdesignfilingsincreasedfrom17to62and131to451between1991and2008,respectively.FilingactivityforthesetwoIPformsaremodestnotonlycomparedtopatents,butalsocomparedtoothercountries(seeFigure2).

16

Figure2:Utilitymodelandindustrialdesignfilings,2008‐2010average

0

1'000

2'000

3'000

4'000

5'000

6'000

7'000

8'000

Australia Austria Brazil Chile CzechRepublic

Indonesia Mexico Philippines Thailand Turkey

Utilitymodels Industrialdesigns

Note:Thecountrieswereselectedmainlytoillustrategreateruseofutilitymodelsindifferentpartsoftheworld;theselectionisnotrepresentative;indeed,therearemanycountriesshowinglimiteduseoftheseIPformssimilartoChile.Inaddition,itisimportanttokeepinmindthatcountrysizeinfluencestheleveloffilingactivity.

Source:WIPOStatisticsDatabase.

Inthecaseofutilitymodels,oneexplanationfortheirlimiteduseinChileisthatINAPIsubstantivelyexaminesutilitymodels–asdescribedintheprevioussection.Manyothercountriesoperateasimplerregistrationsystemwithoutsubstantiveexamination;forapplicantsinthosecountries,theutilitymodelsystemthusofferseasy‐to‐obtainprotectionasanalternativetothepatentsystem.Inthecaseofindustrialdesigns,oneexplanationseemstobethatdesignersrely–moresothaninothercountries–onthecopyrightsysteminprotectingtheircreativeoutputs.However,theempiricalimportanceofthissubstitutioneffectisnotclearandotherfactorssuchastherelativelyhighfeesmayalsoplayarole.Figure3presentsthefilingtrendfortrademarks,showingamarkedincreaseofapplicationsfromslightlylessthan30,000peryearin1991tomorethan44,000in2010.ThisisaremarkablylargenumberforacountryofChile’ssize.

17

Figure3:#trademarkfilings(1991‐2010)

300

003

5000

400

004

5000

500

00#

Fili

ngs

1991 1995 1999 2003 2007Filing year

Asinthecaseofpatents,Chile’srapidlygrowingeconomycanpartlyaccountforthemarkedincreaseinfilings.However,thegrowthintrademarkapplicationshasbeenfasterthanthegrowthofrealGDP.Inaddition,Chileexhibitsamongthemostintensiveuseoftrademarksintheworld,ascapturedbytheratiooftrademarkfilingstoGDP(Table1).WhatliesbehindboththegrowingandabsolutepopularityoftrademarksinChilewarrantsfurtherinvestigation.

Table1:TrademarkfilingstoGDPratio,top‐10listin2010

1 Paraguay 43,7982 RepublicofMoldova 35,4153 Mongolia 32,4134 Chile 20,3885 Bulgaria 18,0616 Luxembourg 15,5927 Iceland 13,8288 CostaRica 13,1559 CzechRepublic 13,12410 NewZealand 12,962

Note:Thevaluesshownareresidentclasscountper100US$billionofconstant2005GDPinpurchasingpowerparities,bycountryoforigin.Theuseofclassratherthanapplicationcountsenablesbettercomparisonsacrosscountries,assomecountriesoperateasingle‐classfilingsystemandothers–likeChile–amulti‐classfilingsystem.(Unfortunately,availabledatadonotallowforcountsofuniquemarks).Theuseoforiginratherthanofficedataenablesbettercomparisonforthosecountriesthataremembersofregionalfilingoffices.

Source:WIPOStatisticsDatabase.

18

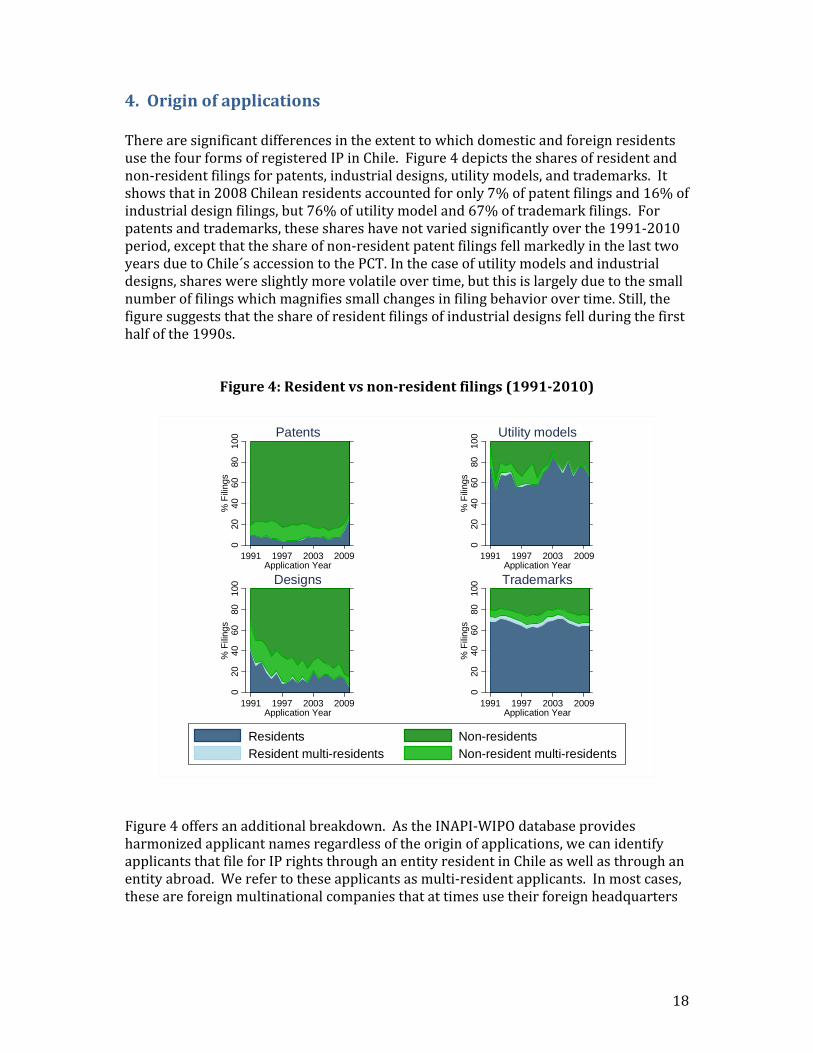

4.OriginofapplicationsTherearesignificantdifferencesintheextenttowhichdomesticandforeignresidentsusethefourformsofregisteredIPinChile.Figure4depictsthesharesofresidentandnon‐residentfilingsforpatents,industrialdesigns,utilitymodels,andtrademarks.Itshowsthatin2008Chileanresidentsaccountedforonly7%ofpatentfilingsand16%ofindustrialdesignfilings,but76%ofutilitymodeland67%oftrademarkfilings.Forpatentsandtrademarks,theseshareshavenotvariedsignificantlyoverthe1991‐2010period,exceptthattheshareofnon‐residentpatentfilingsfellmarkedlyinthelasttwoyearsduetoChile´saccessiontothePCT.Inthecaseofutilitymodelsandindustrialdesigns,shareswereslightlymorevolatileovertime,butthisislargelyduetothesmallnumberoffilingswhichmagnifiessmallchangesinfilingbehaviorovertime.Still,thefiguresuggeststhattheshareofresidentfilingsofindustrialdesignsfellduringthefirsthalfofthe1990s.

Figure4:Residentvsnon‐residentfilings(1991‐2010)

020

4060

8010

0%

Fili

ngs

1991 1997 2003 2009Application Year

Patents

020

4060

8010

0%

Fili

ngs

1991 1997 2003 2009Application Year

Utility models

020

4060

8010

0%

Fili

ngs

1991 1997 2003 2009Application Year

Designs

020

4060

8010

0%

Fili

ngs

1991 1997 2003 2009Application Year

Trademarks

Residents Non-residentsResident multi-residents Non-resident multi-residents

Figure4offersanadditionalbreakdown.AstheINAPI‐WIPOdatabaseprovidesharmonizedapplicantnamesregardlessoftheoriginofapplications,wecanidentifyapplicantsthatfileforIPrightsthroughanentityresidentinChileaswellasthroughanentityabroad.Werefertotheseapplicantsasmulti‐residentapplicants.Inmostcases,theseareforeignmultinationalcompaniesthatattimesusetheirforeignheadquarters

19

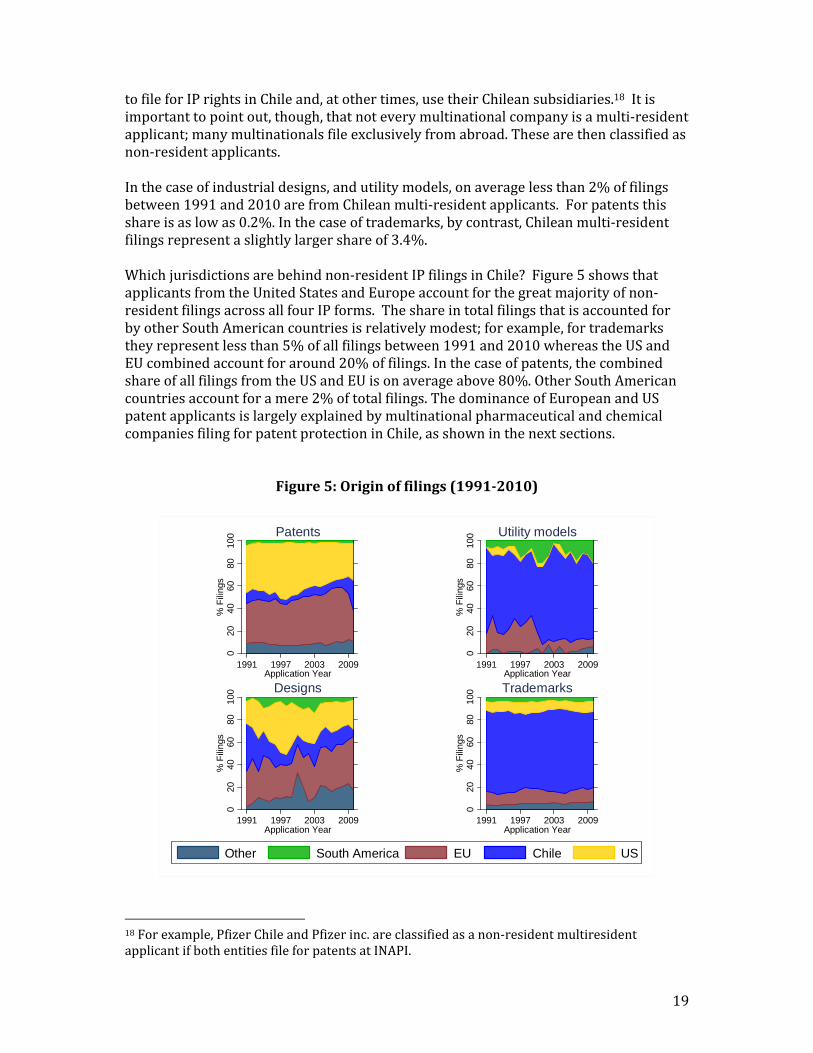

tofileforIPrightsinChileand,atothertimes,usetheirChileansubsidiaries.18Itisimportanttopointout,though,thatnoteverymultinationalcompanyisamulti‐residentapplicant;manymultinationalsfileexclusivelyfromabroad.Thesearethenclassifiedasnon‐residentapplicants.Inthecaseofindustrialdesigns,andutilitymodels,onaveragelessthan2%offilingsbetween1991and2010arefromChileanmulti‐residentapplicants.Forpatentsthisshareisaslowas0.2%.Inthecaseoftrademarks,bycontrast,Chileanmulti‐residentfilingsrepresentaslightlylargershareof3.4%.Whichjurisdictionsarebehindnon‐residentIPfilingsinChile?Figure5showsthatapplicantsfromtheUnitedStatesandEuropeaccountforthegreatmajorityofnon‐residentfilingsacrossallfourIPforms.TheshareintotalfilingsthatisaccountedforbyotherSouthAmericancountriesisrelativelymodest;forexample,fortrademarkstheyrepresentlessthan5%ofallfilingsbetween1991and2010whereastheUSandEUcombinedaccountforaround20%offilings.Inthecaseofpatents,thecombinedshareofallfilingsfromtheUSandEUisonaverageabove80%.OtherSouthAmericancountriesaccountforamere2%oftotalfilings.ThedominanceofEuropeanandUSpatentapplicantsislargelyexplainedbymultinationalpharmaceuticalandchemicalcompaniesfilingforpatentprotectioninChile,asshowninthenextsections.

Figure5:Originoffilings(1991‐2010)

020

4060

8010

0%

Fili

ngs

1991 1997 2003 2009Application Year

Patents

020

4060

8010

0%

Fili

ngs

1991 1997 2003 2009Application Year

Utility models

020

4060

8010

0%

Fili

ngs

1991 1997 2003 2009Application Year

Designs

020

4060

8010

0%

Fili

ngs

1991 1997 2003 2009Application Year

Trademarks

Other South America EU Chile US

18Forexample,PfizerChileandPfizerinc.areclassifiedasanon‐residentmultiresidentapplicantifbothentitiesfileforpatentsatINAPI.

20

5.ApplicantdistributionIPfilingsareunevenlydistributedacrossapplicants.Typically,asmallshareofapplicantsaccountsforalargeshareoffilings.HowconcentratedfilingsareacrossapplicantsdiffersforthefourIPforms.Onewaytoexplorethisistolookatthelistsoftop‐10applicants.19Inthecaseofpatents(Table2),thetop‐10applicantsareallforeignresidents–inparticular,USandEuropeanmultinationals–inlinewiththelargeshareofnon‐residentfilingsdescribedabove.Inaddition,9ofthetop‐10applicantsarefromthechemical,pharmaceutical,andconsumergoodsindustries.TheoneoutlieristheU.S.telecommunicationsequipmentcompanyQualcomm,withatotalof639applicationsbetween1991and2010.Aswillbefurtherdiscussedbelow,thestrongpresenceofacompanyfromtheinformationandcommunicationstechnology(ICT)sectorseemsunusualforasmallmiddle‐incomeeconomywithanindustrialstructurelikeChile;itseemsduetoQualcomm’sspecificbusinessmodelandglobalIPstrategy.Interestingly,Qualcomm’sapplicationsgrewrapidlyfrom2001to2006(withapeakof100filingsin2006),butfellsharplyafter2007–pointingtoachangeinQualcomm’spatentingstrategy.

Table2:Top10applicants‐‐patents(1991‐2010)

Rank Name # Filings % Total Industry Country

1 Procter & Gamble 1,894 4.31% Consumer goods US

2 Unilever 1,402 3.19% Consumer goods NL

3 Pfizer* 1,027 2.34% Pharma US

4 Bayer 940 2.14% Pharma & Chemicals DE

5 Hoffmann‐La Roche 870 1.98% Pharma CH

6 BASF 807 1.84% Chemicals DE

7 Novartis 686 1.56% Pharma CH

8 Wyeth* 683 1.55% Pharma US

9 Boehringer Ingelheim 660 1.50% Pharma DE

10 Qualcomm 639 1.45% Telecommunication US

Total 9,608 21.86%

* Pfizer and Wyeth merged in 2009

19TherankingsshouldnotbeinterpretedtosuggestthatcompanieswithmoreIPfilingsaremoreinnovativethanothers.Thismaynotnecessarilybethecaseascompaniescanchoosebetweenarangeofdifferentmechanismstoprotectandappropriatereturnstoinnovation,registeredIPisonlyonesuchmechanism.Moreover,thereisnoone‐for‐onecorrespondencebetweenthenumberofIPrightsfiledandthecommercialvalueoftheunderlyinginventionsortheircontributiontotechnologicalprogress.

21

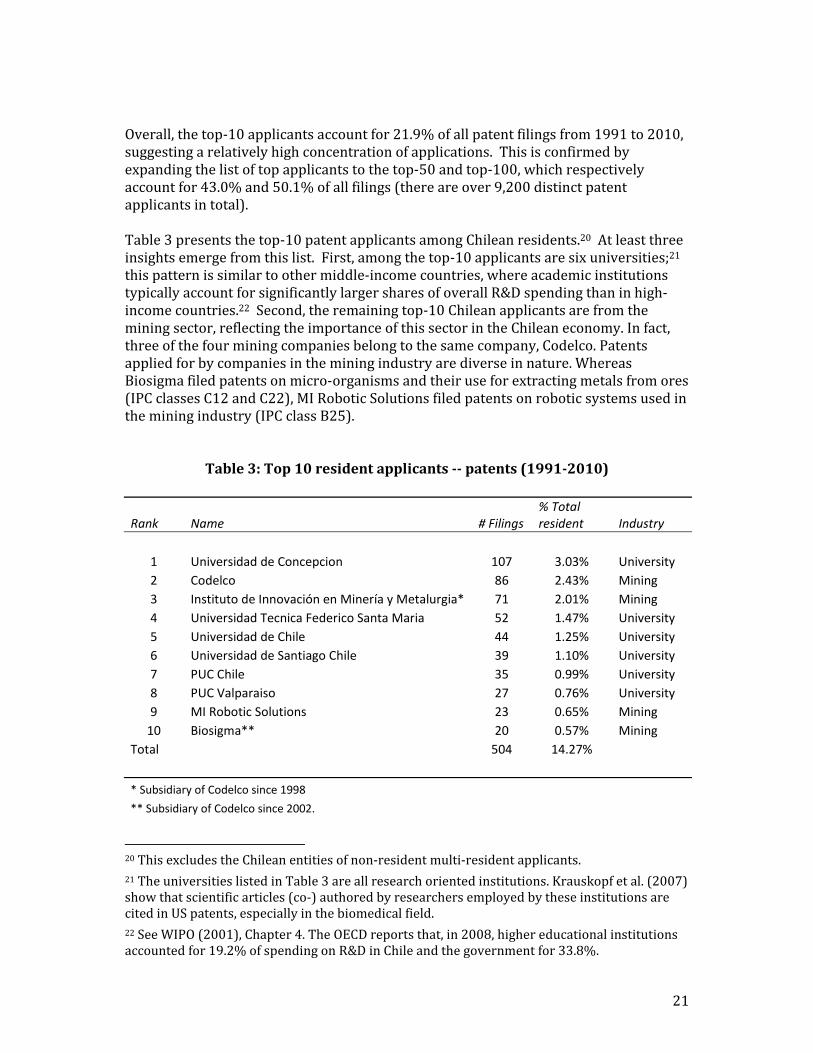

Overall,thetop‐10applicantsaccountfor21.9%ofallpatentfilingsfrom1991to2010,suggestingarelativelyhighconcentrationofapplications.Thisisconfirmedbyexpandingthelistoftopapplicantstothetop‐50andtop‐100,whichrespectivelyaccountfor43.0%and50.1%ofallfilings(thereareover9,200distinctpatentapplicantsintotal).Table3presentsthetop‐10patentapplicantsamongChileanresidents.20Atleastthreeinsightsemergefromthislist.First,amongthetop‐10applicantsaresixuniversities;21thispatternissimilartoothermiddle‐incomecountries,whereacademicinstitutionstypicallyaccountforsignificantlylargersharesofoverallR&Dspendingthaninhigh‐incomecountries.22Second,theremainingtop‐10Chileanapplicantsarefromtheminingsector,reflectingtheimportanceofthissectorintheChileaneconomy.Infact,threeofthefourminingcompaniesbelongtothesamecompany,Codelco.Patentsappliedforbycompaniesintheminingindustryarediverseinnature.WhereasBiosigmafiledpatentsonmicro‐organismsandtheiruseforextractingmetalsfromores(IPCclassesC12andC22),MIRoboticSolutionsfiledpatentsonroboticsystemsusedintheminingindustry(IPCclassB25).

Table3:Top10residentapplicants‐‐patents(1991‐2010)

Rank Name # Filings % Total resident Industry

1 Universidad de Concepcion 107 3.03% University

2 Codelco 86 2.43% Mining

3 Instituto de Innovación en Minería y Metalurgia* 71 2.01% Mining

4 Universidad Tecnica Federico Santa Maria 52 1.47% University

5 Universidad de Chile 44 1.25% University

6 Universidad de Santiago Chile 39 1.10% University

7 PUC Chile 35 0.99% University

8 PUC Valparaiso 27 0.76% University

9 MI Robotic Solutions 23 0.65% Mining

10 Biosigma** 20 0.57% Mining

Total 504 14.27%

* Subsidiary of Codelco since 1998

** Subsidiary of Codelco since 2002.

20ThisexcludestheChileanentitiesofnon‐residentmulti‐residentapplicants.21TheuniversitieslistedinTable3areallresearchorientedinstitutions.Krauskopfetal.(2007)showthatscientificarticles(co‐)authoredbyresearchersemployedbytheseinstitutionsarecitedinUSpatents,especiallyinthebiomedicalfield.22SeeWIPO(2001),Chapter4.TheOECDreportsthat,in2008,highereducationalinstitutionsaccountedfor19.2%ofspendingonR&DinChileandthegovernmentfor33.8%.

22

Third,theoveralllevelofpatentingbythetop‐10Chileanapplicantsappearssmall.Overthe1991‐2010period,thetopChileanapplicant–UniversidaddeConcepcion–filedonlyforatotalofslightlyover100patents.MiningcompanyCodelco,togetherwithitssubsidiaries,filed177patentsintotaloverthe20‐yearperiod.Takentogether,thetop‐10Chileanapplicantsaccountforonlyaround1%ofallpatentapplicationsfiledduring1991‐2010.Yet,theyaccountforasizeable14%ofallfilingsbyChileanresidents,pointingtoaskeweddistributionoffilingsamongresidentssimilartooverallfilings.Itisimportantnottoassumeaone‐to‐onecorrespondencebetweenthelevelofpatentingactivityandthelevelofinnovationinChile.Thepatentoutputofuniversities,forexample,dependsonalargenumberofinstitutionalconditions.Inaddition,littleisknownaboutthepreciseimportanceofpatentprotectionfortheminingsector;technologiesusedinminingareheterogeneousandsecrecymaywellbeaviablealternativeforminingcompaniestoprotectnewtechnologiesfrombeingcopied.Incontrasttopatents,Chileancompaniesdominatethelistoftop‐10trademarkapplicants(Table4).Onlythreeforeignmultinationalsareinthislist.Sixofthetop‐10trademarkapplicantsarefromthepharmaceutical,consumergoods,andfoodproductindustries,whichalsodominatethelistoftop‐10patentapplicants.Inaddition,threeofthetop‐10applicantsareretailers–includingtop‐rankedFalabella–andoneisatelecommunicationsserviceprovider,suggestingmorewidespreaduseoftrademarksacrosseconomicsectors.Thisisalsoreflectedintheslightlymorebalanceddistributionoftrademarkfilings:thetop‐10applicantsonlyaccountfor3.9%ofallfilings;thetop‐50accountfor11.2%andthetop‐100for15.4%.Still,duetolargenumberofapplicants(thereare142,500distinctapplicantsintotal),thedistributionisneverthelessrelativelyskewed.

Table4:Top10applicants‐‐trademarks(1991‐2010)

Rank Name # Filings % Total Industry Country

1 Falabella 4,334 0.57% Retail CL

2 Unilever 3,430 0.45% Consumer goods NL

3 Distribucion y Servicio* 3,344 0.44% Retail CL

4 Laboratorio Chile 2,889 0.38% Pharma CL

5 Laboratorio Recalcine 2,841 0.37% Pharma CL

6 Entel 2,722 0.36% Telecommunication CL

7 Carozzi 2,648 0.35% Food CL

8 Nestle 2,596 0.34% Food CH

9 Cencosud 2,473 0.32% Retail CL

10 Johnson & Johnson 2,359 0.31% Pharma US

Total 29,636 3.87%

* Controlled by Walmart since 2009

23

Finally,Tables5and6presentthetop‐10applicantlistsforutilitymodelsandindustrialdesigns,respectively.Inthecaseofutilitymodels,itisinterestingtonotethatthetop‐3applicantsareforeignmultinationals,eventhoughChileanresidentsaccountformostutilitymodelfilingsoverall(seeabove).However,therelativelylowtotallimitstheextenttowhichonecanderivegeneralizablepatternsfromthistop‐10list.Inthecaseofdesigns,theyconfirmthedominanceofforeignapplicantswithalltop‐10applicants–acrossarelativelywiderangeofsectors–comingfromabroad.

Table5:Top10applicants–utilitymodels(1991‐2010)

Rank Name # Filings % Total Industry Country

1 Telefonica 35 2.84% Telecommunication ES

2 Unilever 16 1.30% Consumer goods NL

3 Multibras 10 0.81% Consumer goods BR

4 Osvaldo Froilan Vilches Perez 7 0.57% CL

5 Falabella 7 0.57% Retail CL

6 Giampaolo Giorgi Guidugli 6 0.49% CL

7 Banco Estado Chile 6 0.49% FIRE* CL

8 Quinones Farfan 6 0.49% Business Services CL

9 Nathurmal Dinani Kishor 6 0.49% CL

10 Alejandro Eduardo Espinoza Gonzalez 6 0.49% CL

Total 105 8.52%

*Finance,insurance,andrealestate

Table6:Top10applicants–industrialdesigns(1991‐2010)

Rank Name # Filings % Total Industry Country

1 Unilever 302 4.94% Consumer goods NL

2 Philips 197 3.22% Electronics NL

3 Honda 190 3.11% Motot vehicles US

4 Sony 165 2.70% Electronics JP

5 Colgate‐Palmolive 164 2.68% Cosmetics DE

6 Telefonica 124 2.03% Telecommunication ES

7 Dart Industries 114 1.87% Manufacturing CH

8 Procter & Gamble 98 1.60% Consumer goods US

9 Bticino 81 1.33% Electronics IT

10 Goodyear 74 1.21% Manufacturing US

11 Nokia 74 1.21% ICT FI

Total 1,583 25.91%

24

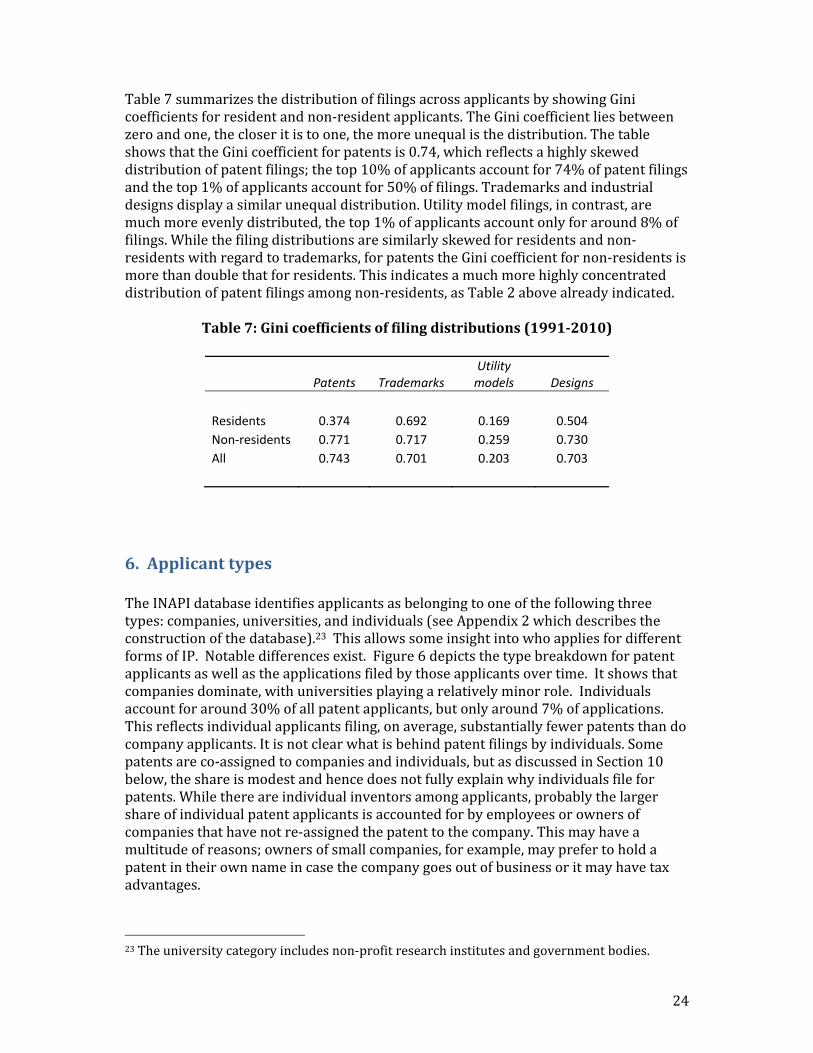

Table7summarizesthedistributionoffilingsacrossapplicantsbyshowingGinicoefficientsforresidentandnon‐residentapplicants.TheGinicoefficientliesbetweenzeroandone,thecloseritistoone,themoreunequalisthedistribution.ThetableshowsthattheGinicoefficientforpatentsis0.74,whichreflectsahighlyskeweddistributionofpatentfilings;thetop10%ofapplicantsaccountfor74%ofpatentfilingsandthetop1%ofapplicantsaccountfor50%offilings.Trademarksandindustrialdesignsdisplayasimilarunequaldistribution.Utilitymodelfilings,incontrast,aremuchmoreevenlydistributed,thetop1%ofapplicantsaccountonlyforaround8%offilings.Whilethefilingdistributionsaresimilarlyskewedforresidentsandnon‐residentswithregardtotrademarks,forpatentstheGinicoefficientfornon‐residentsismorethandoublethatforresidents.Thisindicatesamuchmorehighlyconcentrateddistributionofpatentfilingsamongnon‐residents,asTable2abovealreadyindicated.

Table7:Ginicoefficientsoffilingdistributions(1991‐2010)

Patents Trademarks Utility models Designs

Residents 0.374 0.692 0.169 0.504

Non‐residents 0.771 0.717 0.259 0.730

All 0.743 0.701 0.203 0.703

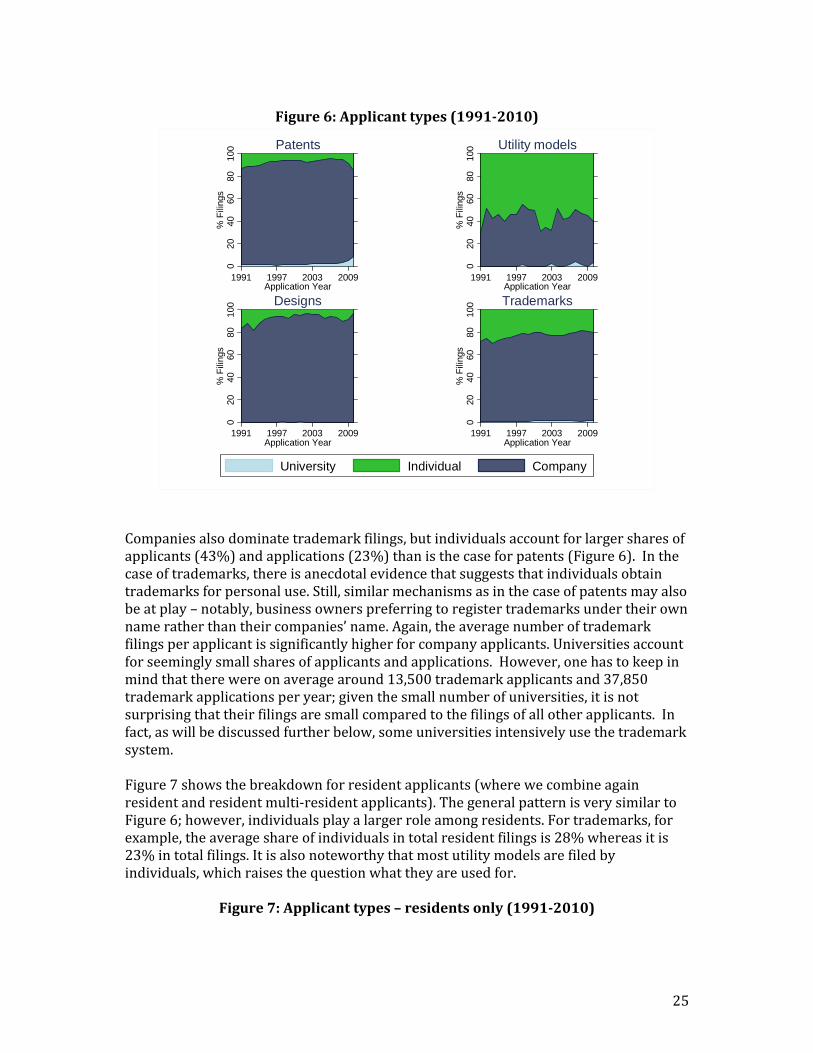

6.ApplicanttypesTheINAPIdatabaseidentifiesapplicantsasbelongingtooneofthefollowingthreetypes:companies,universities,andindividuals(seeAppendix2whichdescribestheconstructionofthedatabase).23ThisallowssomeinsightintowhoappliesfordifferentformsofIP.Notabledifferencesexist.Figure6depictsthetypebreakdownforpatentapplicantsaswellastheapplicationsfiledbythoseapplicantsovertime.Itshowsthatcompaniesdominate,withuniversitiesplayingarelativelyminorrole.Individualsaccountforaround30%ofallpatentapplicants,butonlyaround7%ofapplications.Thisreflectsindividualapplicantsfiling,onaverage,substantiallyfewerpatentsthandocompanyapplicants.Itisnotclearwhatisbehindpatentfilingsbyindividuals.Somepatentsareco‐assignedtocompaniesandindividuals,butasdiscussedinSection10below,theshareismodestandhencedoesnotfullyexplainwhyindividualsfileforpatents.Whilethereareindividualinventorsamongapplicants,probablythelargershareofindividualpatentapplicantsisaccountedforbyemployeesorownersofcompaniesthathavenotre‐assignedthepatenttothecompany.Thismayhaveamultitudeofreasons;ownersofsmallcompanies,forexample,mayprefertoholdapatentintheirownnameincasethecompanygoesoutofbusinessoritmayhavetaxadvantages.

23Theuniversitycategoryincludesnon‐profitresearchinstitutesandgovernmentbodies.

25

Figure6:Applicanttypes(1991‐2010)

020

4060

8010

0%

Fili

ngs

1991 1997 2003 2009Application Year

Patents

020

4060

8010

0%

Fili

ngs

1991 1997 2003 2009Application Year

Utility models

020

4060

8010

0%

Fili

ngs

1991 1997 2003 2009Application Year

Designs

020

4060

8010

0%

Fili

ngs

1991 1997 2003 2009Application Year

Trademarks

University Individual Company

Companiesalsodominatetrademarkfilings,butindividualsaccountforlargersharesofapplicants(43%)andapplications(23%)thanisthecaseforpatents(Figure6).Inthecaseoftrademarks,thereisanecdotalevidencethatsuggeststhatindividualsobtaintrademarksforpersonaluse.Still,similarmechanismsasinthecaseofpatentsmayalsobeatplay–notably,businessownerspreferringtoregistertrademarksundertheirownnameratherthantheircompanies’name.Again,theaveragenumberoftrademarkfilingsperapplicantissignificantlyhigherforcompanyapplicants.Universitiesaccountforseeminglysmallsharesofapplicantsandapplications.However,onehastokeepinmindthattherewereonaveragearound13,500trademarkapplicantsand37,850trademarkapplicationsperyear;giventhesmallnumberofuniversities,itisnotsurprisingthattheirfilingsaresmallcomparedtothefilingsofallotherapplicants.Infact,aswillbediscussedfurtherbelow,someuniversitiesintensivelyusethetrademarksystem.Figure7showsthebreakdownforresidentapplicants(wherewecombineagainresidentandresidentmulti‐residentapplicants).ThegeneralpatternisverysimilartoFigure6;however,individualsplayalargerroleamongresidents.Fortrademarks,forexample,theaverageshareofindividualsintotalresidentfilingsis28%whereasitis23%intotalfilings.Itisalsonoteworthythatmostutilitymodelsarefiledbyindividuals,whichraisesthequestionwhattheyareusedfor.

Figure7:Applicanttypes–residentsonly(1991‐2010)

26

020

4060

8010

0%

Fili

ngs

1991 1997 2003 2009Application Year

Patents

020

4060

8010

0%

Fili

ngs

1991 1997 2003 2009Application Year

Utility models

020

4060

8010

0%

Fili

ngs

1991 1997 2003 2009Application Year

Designs

020

4060

8010

0%

Fili

ngs

1991 1997 2003 2009Application Year

Trademarks

University Individual Company

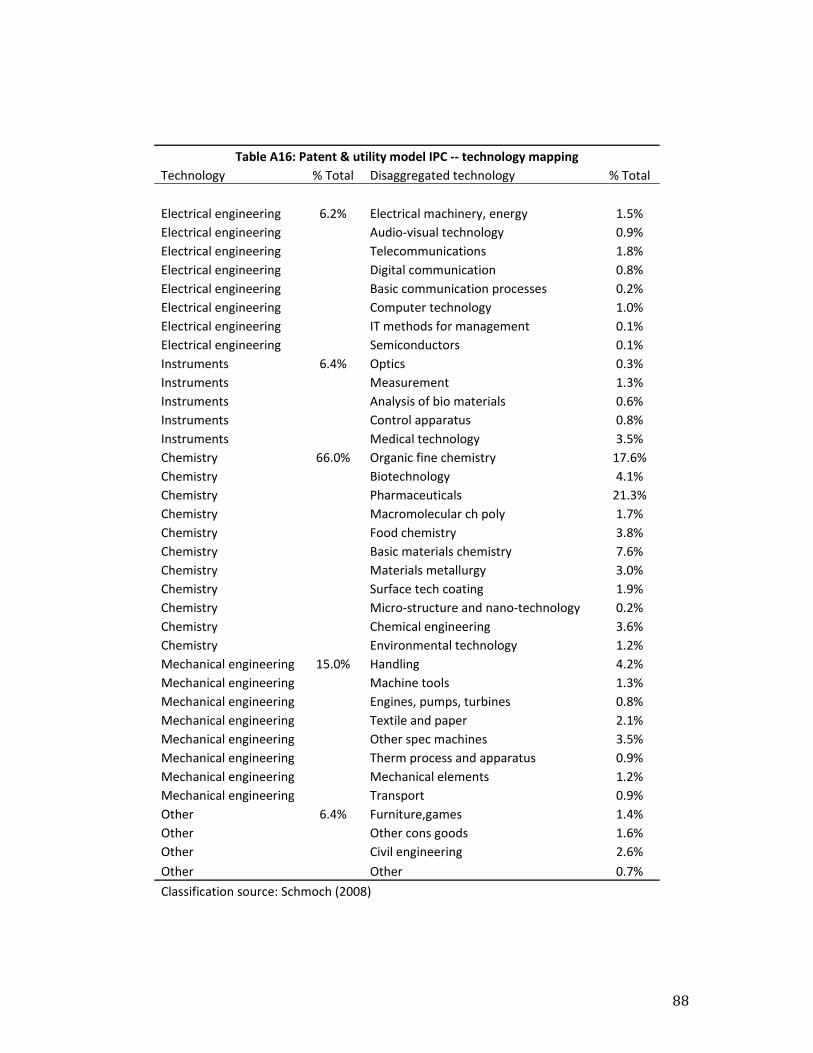

7.FilingsbytechnologyandclassWhicheconomicsectorsgeneratemostIPrights?IPapplicationsdonotcontaindirectinformationonanapplicant’ssectoralaffiliation,butitispossibletobreakdownIPfilingsbyfieldoftechnology(forpatents)andbygoods/servicesclass(fortrademarks).ThesebreakdownsprovideindirectinformationonthetypeofeconomicactivitybehinddifferentIPapplications.Table2alreadyillustratedthestrongpresenceofthepharmaceuticalandchemicalsectorsamongthetop‐10patentapplicants.Figure8confirmstheprominenceofthetechnologyfieldsassociatedwiththesetwosectorsinoverallpatentfilings.From1991to2010,theyaccountedforaround60%ofallpatentapplications.24

24WemapIPCclasssymbolsintotechnologyclassesemployingtheconcordancetablebySchmoch(2008).

27

Figure8:Patent(IPC)‐technologymapping(1991‐2010)

Electrical Eng.

Instruments

Chemistry/Pharma

Mechanical Eng.

Other

02

04

06

08

01

00%

Fili

ngs

1991 1997 2003 2009Application Year

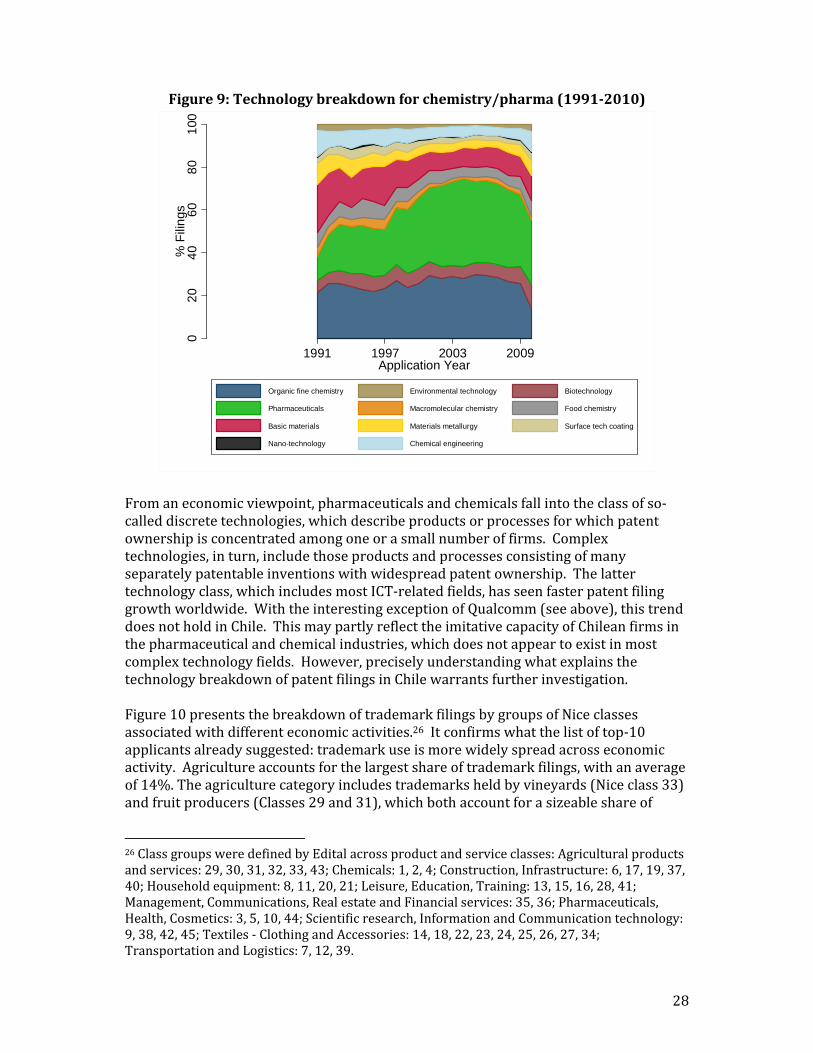

Note:The“Other”categorycontainsfurnitureandgames,otherconsumergoods,andcivilengineering.ThetechnologybreakdowndepictedinFigure8differsmarkedlyfromthatobservedatthepatentofficesofhigh‐incomecountries.Lookingatpatentfilingsworldwide,whicharedominatedbyfilingsathigh‐incomeoffices,thepharmaceuticalandchemicalsectorsaccountforaround23%ofallfilings.25Otherfields–notablythoseassociatedwithinformationandcommunicationstechnologies(ICTs)–haveseencomparativelygreaterfilingactivity.Figure9showsabreakdownforthebroadchemistry/pharmacategoryinto11technologysubcategories.Thefigureshowsthatorganicfinechemistryandpharmaceuticalpatentsaccountforoverhalfofallfilingsoverthe1991‐2010period.Pharmaceuticalpatentsincreasedmarkedlyfromaround11%in1991toover40%in2004reflectingthechangesintheIPlawin1991.

25Thissharereferstoallpatentfilingspublishedbetween1990and2010,asavailableintheWIPOStatisticsDatabase.

28

Figure9:Technologybreakdownforchemistry/pharma(1991‐2010)

02

04

06

08

01

00%

Fili

ngs

1991 1997 2003 2009Application Year

Organic fine chemistry Environmental technology Biotechnology

Pharmaceuticals Macromolecular chemistry Food chemistry

Basic materials Materials metallurgy Surface tech coating

Nano-technology Chemical engineering

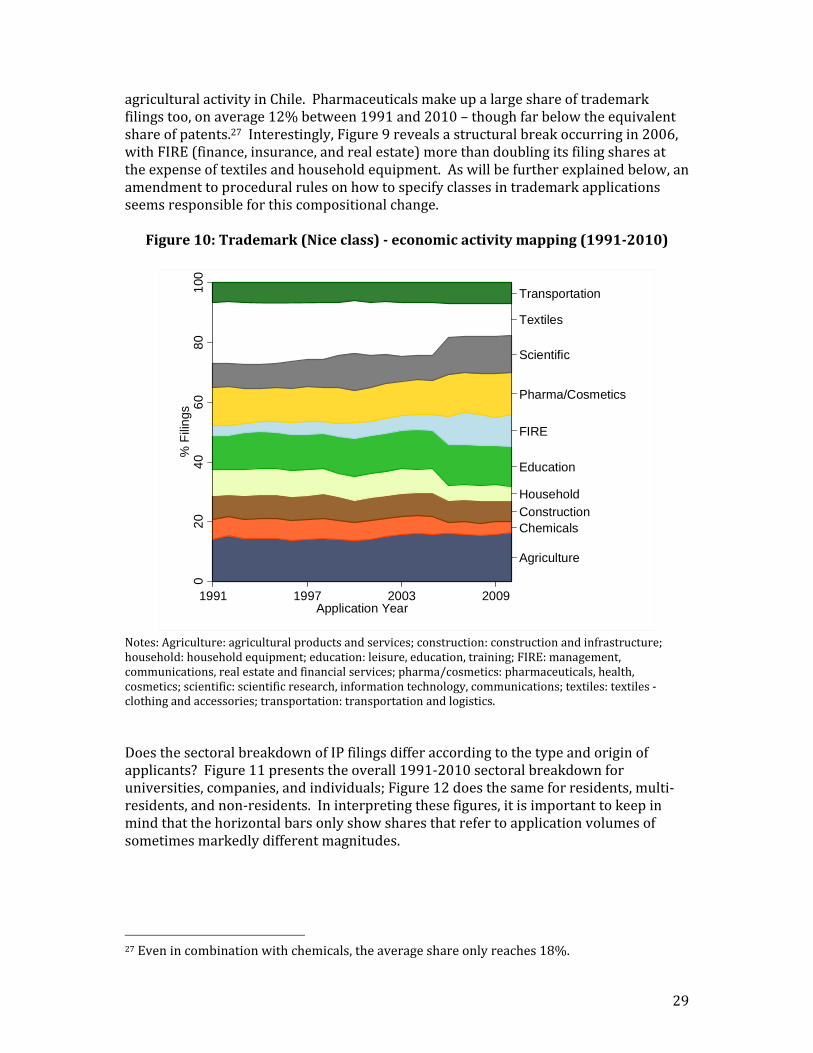

Fromaneconomicviewpoint,pharmaceuticalsandchemicalsfallintotheclassofso‐calleddiscretetechnologies,whichdescribeproductsorprocessesforwhichpatentownershipisconcentratedamongoneorasmallnumberoffirms.Complextechnologies,inturn,includethoseproductsandprocessesconsistingofmanyseparatelypatentableinventionswithwidespreadpatentownership.Thelattertechnologyclass,whichincludesmostICT‐relatedfields,hasseenfasterpatentfilinggrowthworldwide.WiththeinterestingexceptionofQualcomm(seeabove),thistrenddoesnotholdinChile.ThismaypartlyreflecttheimitativecapacityofChileanfirmsinthepharmaceuticalandchemicalindustries,whichdoesnotappeartoexistinmostcomplextechnologyfields.However,preciselyunderstandingwhatexplainsthetechnologybreakdownofpatentfilingsinChilewarrantsfurtherinvestigation.Figure10presentsthebreakdownoftrademarkfilingsbygroupsofNiceclassesassociatedwithdifferenteconomicactivities.26Itconfirmswhatthelistoftop‐10applicantsalreadysuggested:trademarkuseismorewidelyspreadacrosseconomicactivity.Agricultureaccountsforthelargestshareoftrademarkfilings,withanaverageof14%.Theagriculturecategoryincludestrademarksheldbyvineyards(Niceclass33)andfruitproducers(Classes29and31),whichbothaccountforasizeableshareof

26ClassgroupsweredefinedbyEditalacrossproductandserviceclasses:Agriculturalproductsandservices:29,30,31,32,33,43;Chemicals:1,2,4;Construction,Infrastructure:6,17,19,37,40;Householdequipment:8,11,20,21;Leisure,Education,Training:13,15,16,28,41;Management,Communications,RealestateandFinancialservices:35,36;Pharmaceuticals,Health,Cosmetics:3,5,10,44;Scientificresearch,InformationandCommunicationtechnology:9,38,42,45;Textiles‐ClothingandAccessories:14,18,22,23,24,25,26,27,34;TransportationandLogistics:7,12,39.

29

agriculturalactivityinChile.Pharmaceuticalsmakeupalargeshareoftrademarkfilingstoo,onaverage12%between1991and2010–thoughfarbelowtheequivalentshareofpatents.27Interestingly,Figure9revealsastructuralbreakoccurringin2006,withFIRE(finance,insurance,andrealestate)morethandoublingitsfilingsharesattheexpenseoftextilesandhouseholdequipment.Aswillbefurtherexplainedbelow,anamendmenttoproceduralrulesonhowtospecifyclassesintrademarkapplicationsseemsresponsibleforthiscompositionalchange.

Figure10:Trademark(Niceclass)‐economicactivitymapping(1991‐2010)

Agriculture

ChemicalsConstruction

Household

Education

FIRE

Pharma/Cosmetics

Scientific

Textiles

Transportation

02

04

06

08

01

00%

Fili

ngs

1991 1997 2003 2009Application Year

Notes:Agriculture:agriculturalproductsandservices;construction:constructionandinfrastructure;household:householdequipment;education:leisure,education,training;FIRE:management,communications,realestateandfinancialservices;pharma/cosmetics:pharmaceuticals,health,cosmetics;scientific:scientificresearch,informationtechnology,communications;textiles:textiles‐clothingandaccessories;transportation:transportationandlogistics.DoesthesectoralbreakdownofIPfilingsdifferaccordingtothetypeandoriginofapplicants?Figure11presentstheoverall1991‐2010sectoralbreakdownforuniversities,companies,andindividuals;Figure12doesthesameforresidents,multi‐residents,andnon‐residents.Ininterpretingthesefigures,itisimportanttokeepinmindthatthehorizontalbarsonlyshowsharesthatrefertoapplicationvolumesofsometimesmarkedlydifferentmagnitudes.

27Evenincombinationwithchemicals,theaverageshareonlyreaches18%.

30

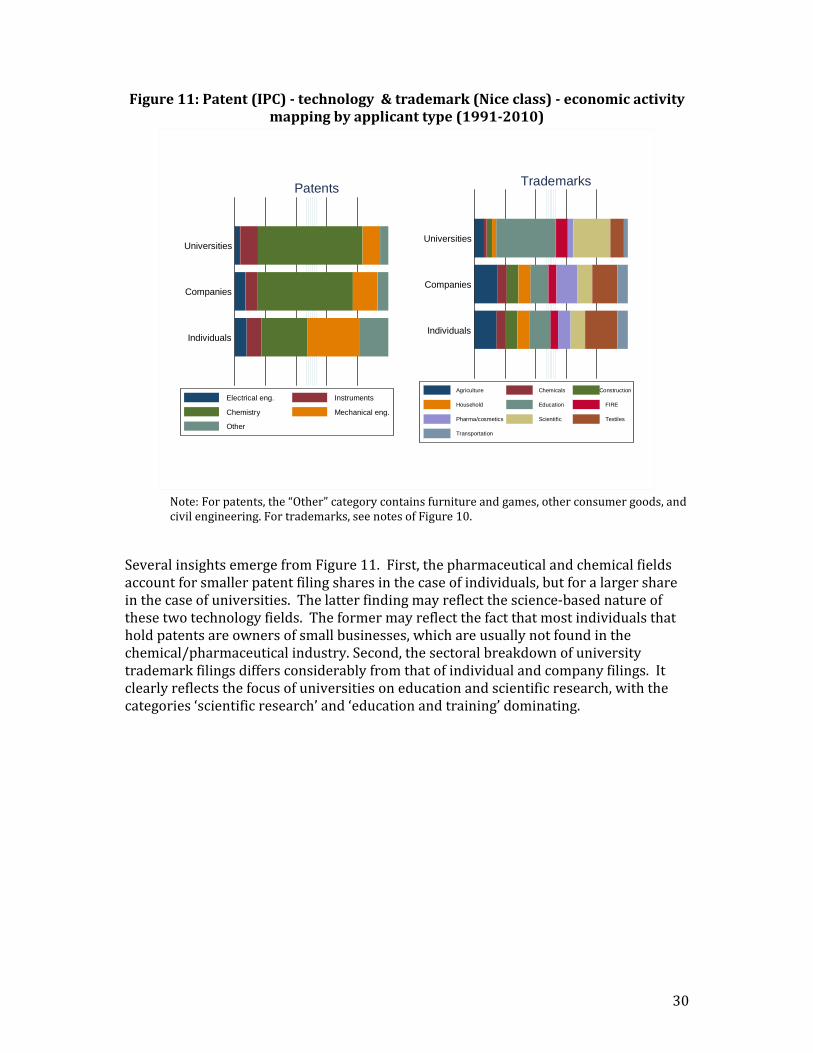

Figure11:Patent(IPC)‐technology&trademark(Niceclass)‐economicactivitymappingbyapplicanttype(1991‐2010)

Individuals

Companies

Universities

Patents

Electrical eng. Instruments

Chemistry Mechanical eng.

Other

Individuals

Companies

Universities

Trademarks

Agriculture Chemicals Construction

Household Education FIRE

Pharma/cosmetics Scientific Textiles

Transportation

Note:Forpatents,the“Other”categorycontainsfurnitureandgames,otherconsumergoods,andcivilengineering.Fortrademarks,seenotesofFigure10.

SeveralinsightsemergefromFigure11.First,thepharmaceuticalandchemicalfieldsaccountforsmallerpatentfilingsharesinthecaseofindividuals,butforalargershareinthecaseofuniversities.Thelatterfindingmayreflectthescience‐basednatureofthesetwotechnologyfields.Theformermayreflectthefactthatmostindividualsthatholdpatentsareownersofsmallbusinesses,whichareusuallynotfoundinthechemical/pharmaceuticalindustry.Second,thesectoralbreakdownofuniversitytrademarkfilingsdiffersconsiderablyfromthatofindividualandcompanyfilings.Itclearlyreflectsthefocusofuniversitiesoneducationandscientificresearch,withthecategories‘scientificresearch’and‘educationandtraining’dominating.

31

Figure12:Patent(IPC)‐technology&trademark(Niceclass)‐economicactivitymappingbyresident(1991‐2010)

Non-residents

Non-resident multi-resident

Resident multi-residents

Residents

Patents

Electrical eng. Instruments

Chemistry Mechanical eng.

Other

Non-residents

Non-resident multi-residents

Resident multi-residents

Residents

Trademarks

Agriculture Chemicals Construction Household

Education FIRE Pharma Scientific

Textiles Transportation

Note:Forpatents,the“Other”categorycontainsfurnitureandgames,otherconsumergoods,andcivilengineering.Fortrademarks,seenotesofFigure10.

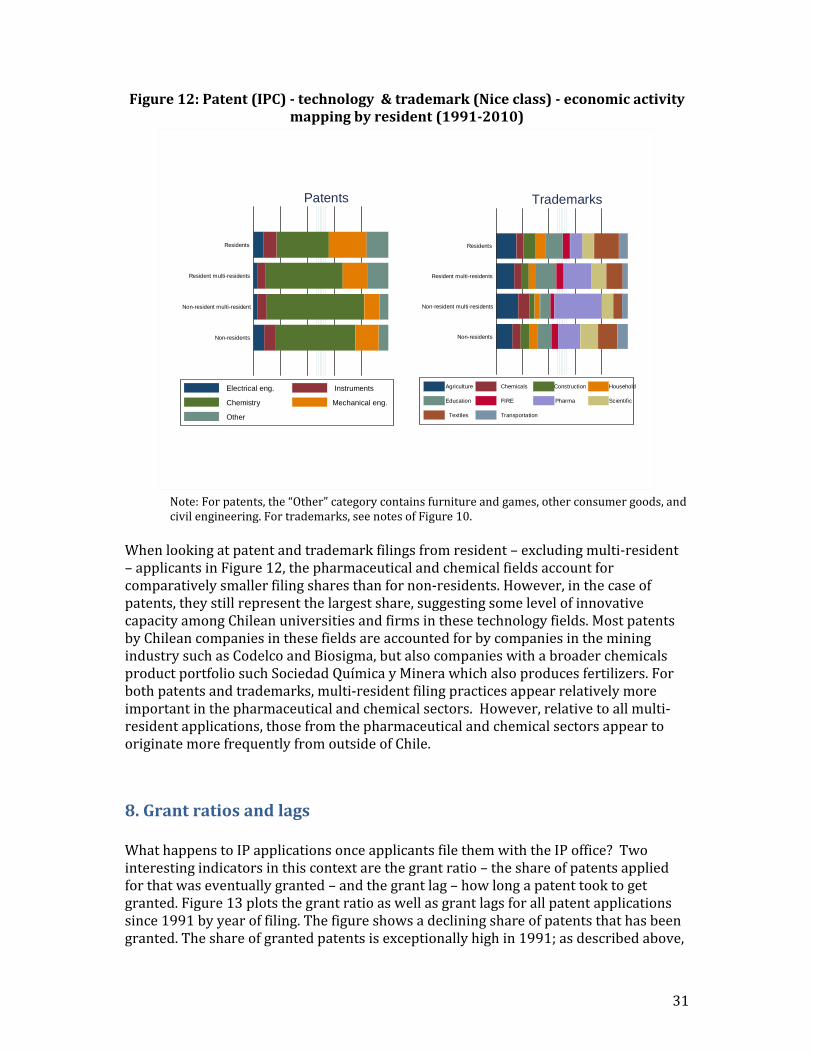

Whenlookingatpatentandtrademarkfilingsfromresident–excludingmulti‐resident–applicantsinFigure12,thepharmaceuticalandchemicalfieldsaccountforcomparativelysmallerfilingsharesthanfornon‐residents.However,inthecaseofpatents,theystillrepresentthelargestshare,suggestingsomelevelofinnovativecapacityamongChileanuniversitiesandfirmsinthesetechnologyfields.MostpatentsbyChileancompaniesinthesefieldsareaccountedforbycompaniesintheminingindustrysuchasCodelcoandBiosigma,butalsocompanieswithabroaderchemicalsproductportfoliosuchSociedadQuímicayMinerawhichalsoproducesfertilizers.Forbothpatentsandtrademarks,multi‐residentfilingpracticesappearrelativelymoreimportantinthepharmaceuticalandchemicalsectors.However,relativetoallmulti‐residentapplications,thosefromthepharmaceuticalandchemicalsectorsappeartooriginatemorefrequentlyfromoutsideofChile.

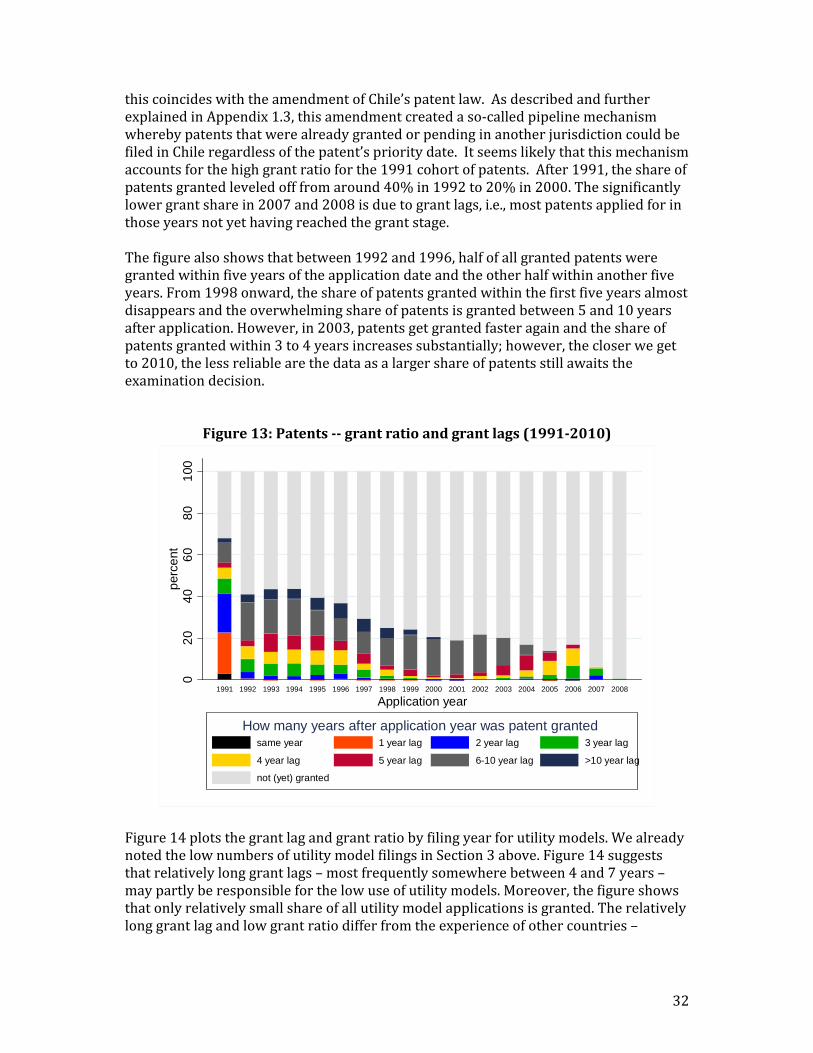

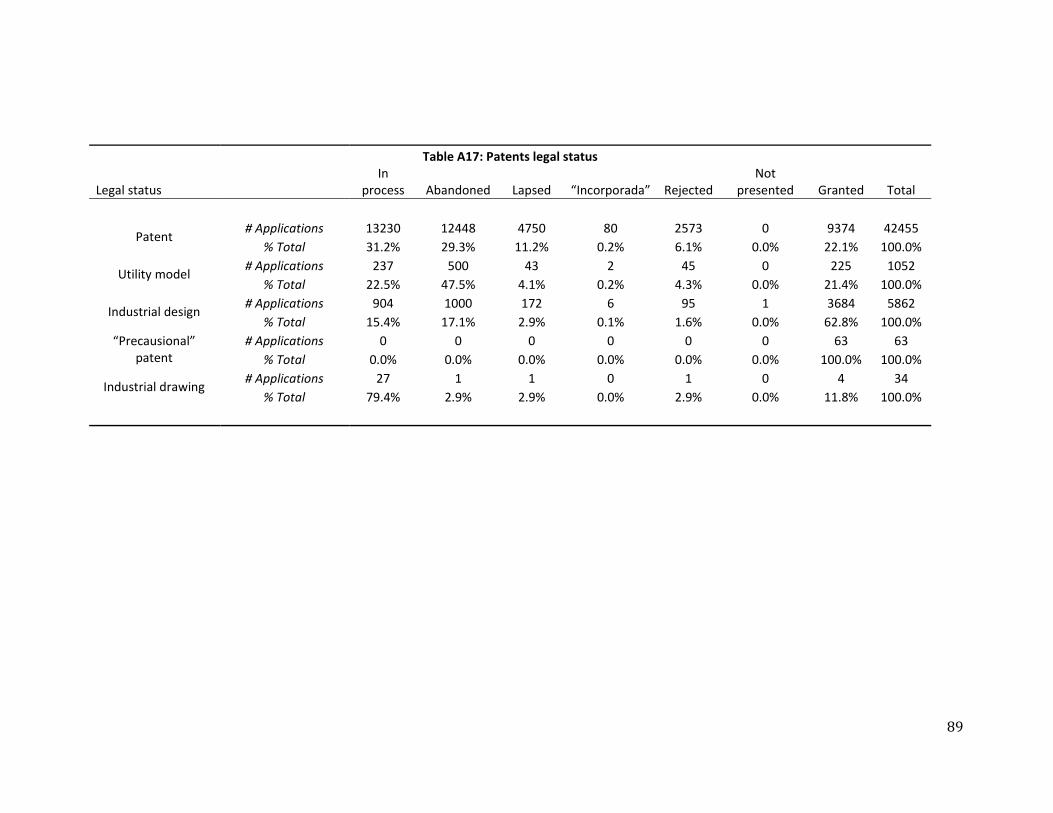

8.GrantratiosandlagsWhathappenstoIPapplicationsonceapplicantsfilethemwiththeIPoffice?Twointerestingindicatorsinthiscontextarethegrantratio–theshareofpatentsappliedforthatwaseventuallygranted–andthegrantlag–howlongapatenttooktogetgranted.Figure13plotsthegrantratioaswellasgrantlagsforallpatentapplicationssince1991byyearoffiling.Thefigureshowsadecliningshareofpatentsthathasbeengranted.Theshareofgrantedpatentsisexceptionallyhighin1991;asdescribedabove,

32

thiscoincideswiththeamendmentofChile’spatentlaw.AsdescribedandfurtherexplainedinAppendix1.3,thisamendmentcreatedaso‐calledpipelinemechanismwherebypatentsthatwerealreadygrantedorpendinginanotherjurisdictioncouldbefiledinChileregardlessofthepatent’sprioritydate.Itseemslikelythatthismechanismaccountsforthehighgrantratioforthe1991cohortofpatents.After1991,theshareofpatentsgrantedleveledofffromaround40%in1992to20%in2000.Thesignificantlylowergrantsharein2007and2008isduetograntlags,i.e.,mostpatentsappliedforinthoseyearsnotyethavingreachedthegrantstage.Thefigurealsoshowsthatbetween1992and1996,halfofallgrantedpatentsweregrantedwithinfiveyearsoftheapplicationdateandtheotherhalfwithinanotherfiveyears.From1998onward,theshareofpatentsgrantedwithinthefirstfiveyearsalmostdisappearsandtheoverwhelmingshareofpatentsisgrantedbetween5and10yearsafterapplication.However,in2003,patentsgetgrantedfasteragainandtheshareofpatentsgrantedwithin3to4yearsincreasessubstantially;however,thecloserwegetto2010,thelessreliablearethedataasalargershareofpatentsstillawaitstheexaminationdecision.

Figure13:Patents‐‐grantratioandgrantlags(1991‐2010)

02

04

06

08

01

00p

erce

nt

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Application year

same year 1 year lag 2 year lag 3 year lag

4 year lag 5 year lag 6-10 year lag >10 year lag

not (yet) granted

How many years after application year was patent granted

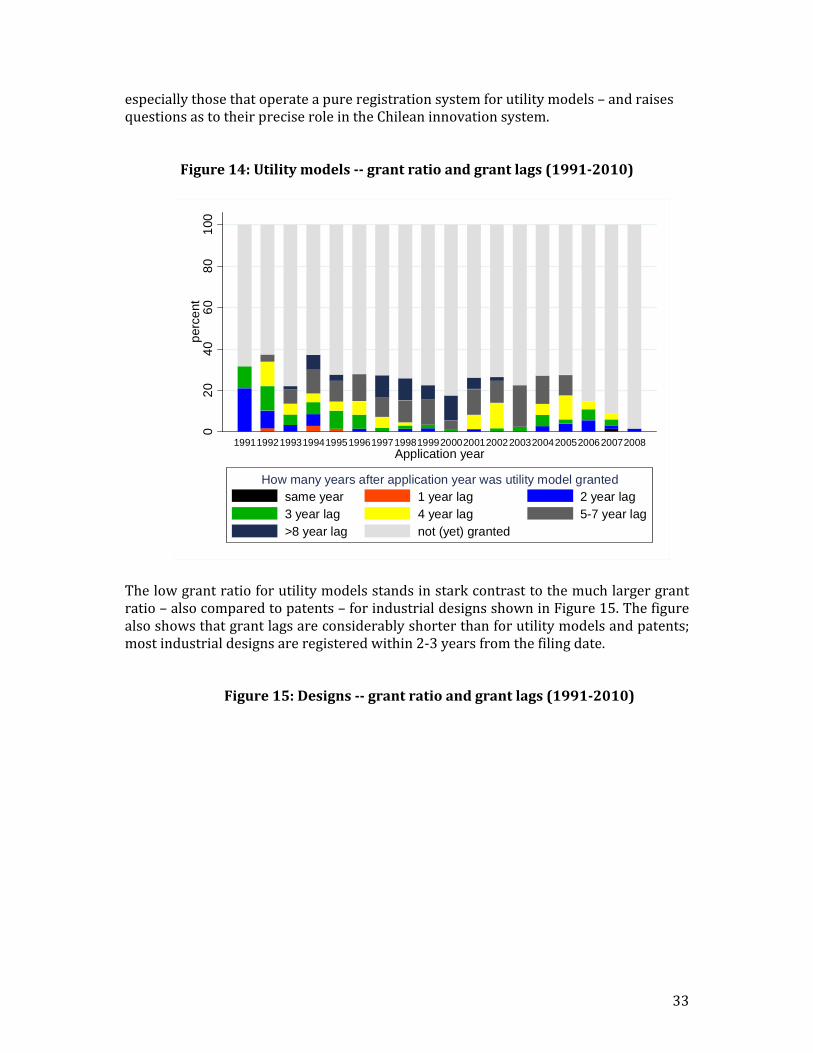

Figure14plotsthegrantlagandgrantratiobyfilingyearforutilitymodels.WealreadynotedthelownumbersofutilitymodelfilingsinSection3above.Figure14suggeststhatrelativelylonggrantlags–mostfrequentlysomewherebetween4and7years–maypartlyberesponsibleforthelowuseofutilitymodels.Moreover,thefigureshowsthatonlyrelativelysmallshareofallutilitymodelapplicationsisgranted.Therelativelylonggrantlagandlowgrantratiodifferfromtheexperienceofothercountries–

33

especiallythosethatoperateapureregistrationsystemforutilitymodels–andraisesquestionsastotheirpreciseroleintheChileaninnovationsystem.

Figure14:Utilitymodels‐‐grantratioandgrantlags(1991‐2010)

02

04

06

08

01

00p

erce

nt

199119921993199419951996199719981999200020012002200320042005200620072008Application year

same year 1 year lag 2 year lag3 year lag 4 year lag 5-7 year lag>8 year lag not (yet) granted

How many years after application year was utility model granted

Thelowgrantratioforutilitymodelsstandsinstarkcontrasttothemuchlargergrantratio–alsocomparedtopatents–forindustrialdesignsshowninFigure15.Thefigurealsoshowsthatgrantlagsareconsiderablyshorterthanforutilitymodelsandpatents;mostindustrialdesignsareregisteredwithin2‐3yearsfromthefilingdate.

Figure15:Designs‐‐grantratioandgrantlags(1991‐2010)

34

02

04

06

08

01

00p

erce

nt

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Application year

same year 1 year lag 2 year lag3 year lag 4 year lag 5-7 year lag8-10 year lag not (yet) granted

How many years after application year was design granted

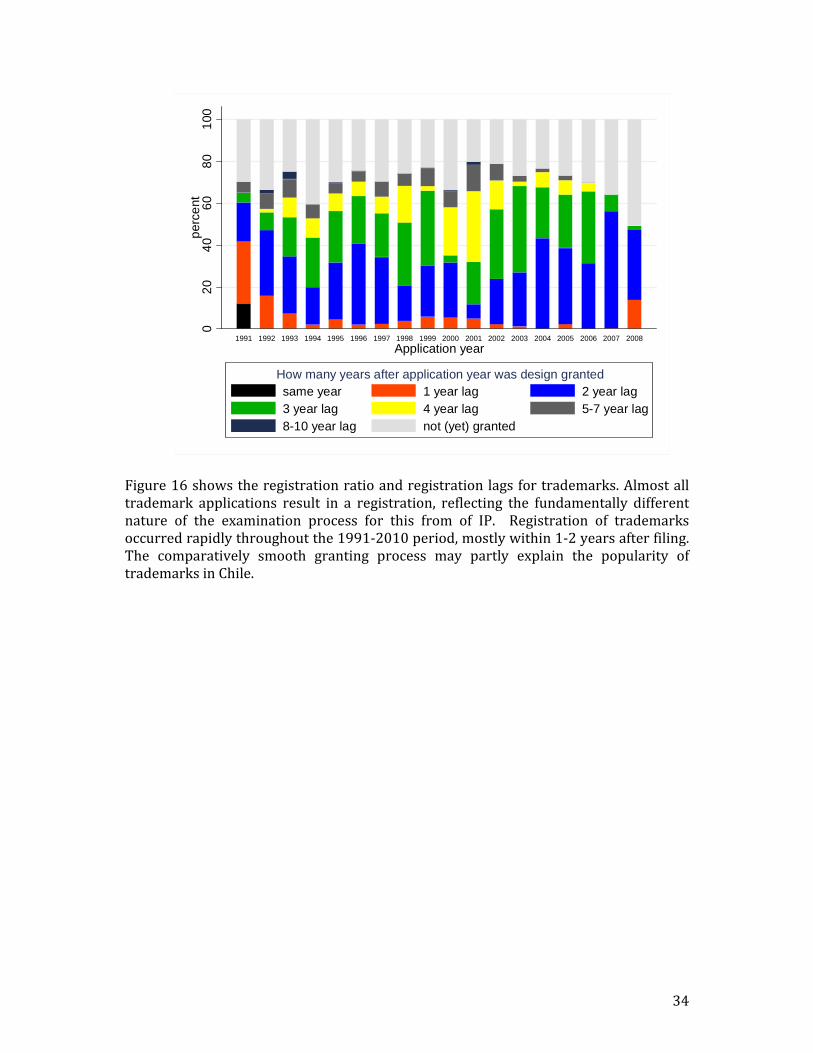

Figure16showstheregistrationratioandregistrationlagsfortrademarks.Almostalltrademark applications result in a registration, reflecting the fundamentally differentnature of the examination process for this from of IP. Registration of trademarksoccurredrapidlythroughoutthe1991‐2010period,mostlywithin1‐2yearsafterfiling.The comparatively smooth granting process may partly explain the popularity oftrademarksinChile.

35

Figure16:Trademarks‐‐grantratioandgrantlags(1991‐2010)

02

04

06

08

01

00p

erce

nt

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Application year

same year 1 year lag 2 year lag3 year lag 4 year lag 5-10 year lag>10 year lag not (yet) registered

How many years after application was trademark registered

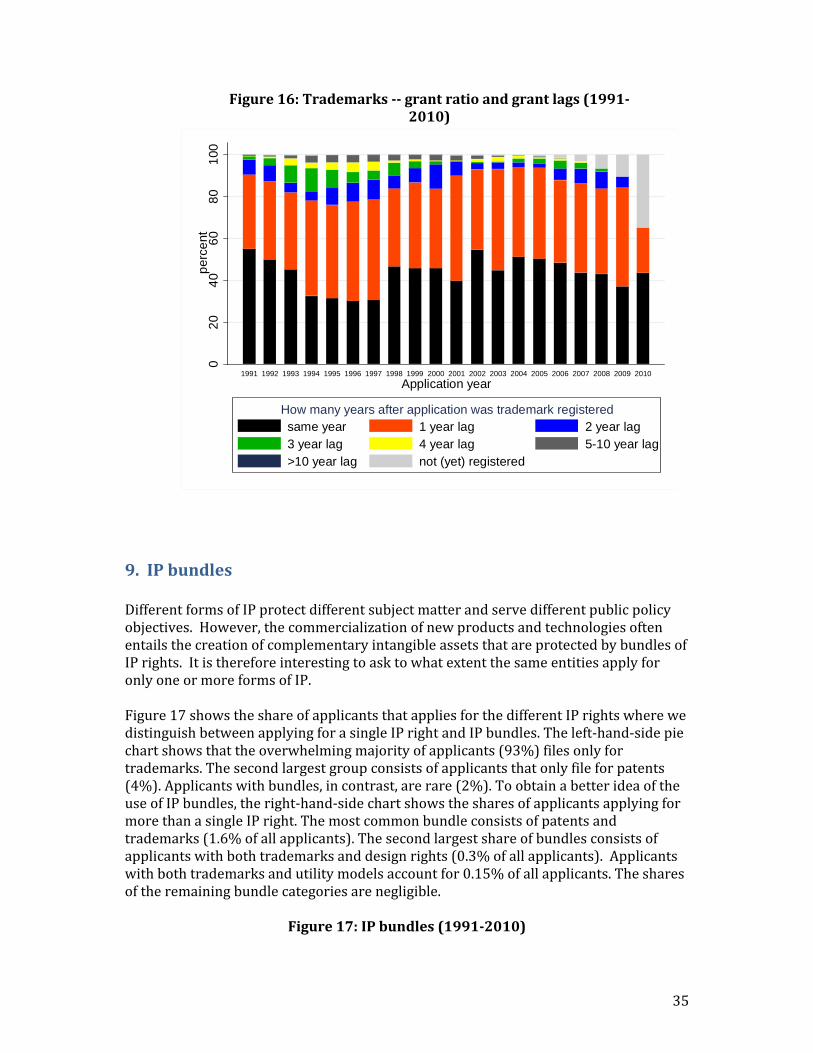

9.IPbundlesDifferentformsofIPprotectdifferentsubjectmatterandservedifferentpublicpolicyobjectives.However,thecommercializationofnewproductsandtechnologiesoftenentailsthecreationofcomplementaryintangibleassetsthatareprotectedbybundlesofIPrights.ItisthereforeinterestingtoasktowhatextentthesameentitiesapplyforonlyoneormoreformsofIP.Figure17showstheshareofapplicantsthatappliesforthedifferentIPrightswherewedistinguishbetweenapplyingforasingleIPrightandIPbundles.Theleft‐hand‐sidepiechartshowsthattheoverwhelmingmajorityofapplicants(93%)filesonlyfortrademarks.Thesecondlargestgroupconsistsofapplicantsthatonlyfileforpatents(4%).Applicantswithbundles,incontrast,arerare(2%).ToobtainabetterideaoftheuseofIPbundles,theright‐hand‐sidechartshowsthesharesofapplicantsapplyingformorethanasingleIPright.Themostcommonbundleconsistsofpatentsandtrademarks(1.6%ofallapplicants).Thesecondlargestshareofbundlesconsistsofapplicantswithbothtrademarksanddesignrights(0.3%ofallapplicants).Applicantswithbothtrademarksandutilitymodelsaccountfor0.15%ofallapplicants.Thesharesoftheremainingbundlecategoriesarenegligible.

Figure17:IPbundles(1991‐2010)

36

Patent only Trademark only Utility only

Design only Bundle

All

Patent & TM Patent & utility

Patent & design TM & utility

TM & design Design & utility

Patent & design & utility TM & design & utility

Patent & TM & design & utility

Only bundles

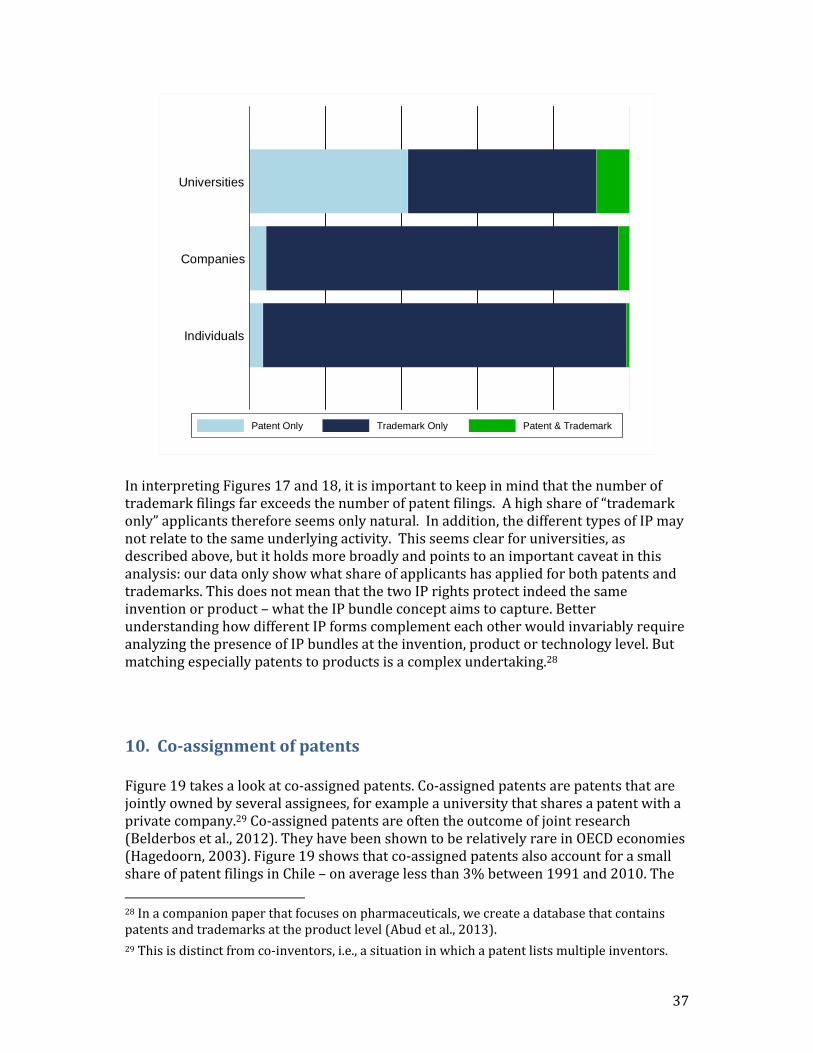

Figure18illustratesthepresenceofIPbundlesbyapplicanttypes.GiventhelimiteduseofutilitymodelsanddesignrightsinChile,Figure18islimitedtopatentsandtrademarks.Itshowsthat9%ofalluniversityapplicantshaveappliedforatleastonetrademarkandonepatentoverthe1991‐2010period.Strikingly,42%ofuniversityapplicantsappliedonlyforpatentsand49%onlyfortrademarks.Theshareofcompaniesorindividualsthatonlyapplyforpatentsisalotsmaller(5%and4%respectively).Assumingthattrademarkslargelyservecommercializationpurposes,thelargeshareofuniversitiesthatonlyfileforpatentsreflectsagaintheresearchmandateofuniversities.Nevertheless,halfofallIPactiveuniversitiesfileonlyfortrademarkprotection.Mostofthesetrademarksrelatetodegreeprogramsandthebrandofuniversitiesmoregenerally.Thiscouldindicatethatsomeuniversitiesspecializeinteachingandadoptabrandingstrategythatincorporatestheuseoftrademarks.TheshareofuniversitieswithIPbundlesis11%.TheIPbundlesshareisconsiderablysmallerforcompanies,standingat3%anditisclosetozeroforindividuals.Figure18:IPbundles(patents&trademarks)byapplicanttype(1991‐2010)

37

Individuals

Companies

Universities

Patent Only Trademark Only Patent & Trademark

IninterpretingFigures17and18,itisimportanttokeepinmindthatthenumberoftrademarkfilingsfarexceedsthenumberofpatentfilings.Ahighshareof“trademarkonly”applicantsthereforeseemsonlynatural.Inaddition,thedifferenttypesofIPmaynotrelatetothesameunderlyingactivity.Thisseemsclearforuniversities,asdescribedabove,butitholdsmorebroadlyandpointstoanimportantcaveatinthisanalysis:ourdataonlyshowwhatshareofapplicantshasappliedforbothpatentsandtrademarks.ThisdoesnotmeanthatthetwoIPrightsprotectindeedthesameinventionorproduct–whattheIPbundleconceptaimstocapture.BetterunderstandinghowdifferentIPformscomplementeachotherwouldinvariablyrequireanalyzingthepresenceofIPbundlesattheinvention,productortechnologylevel.Butmatchingespeciallypatentstoproductsisacomplexundertaking.28

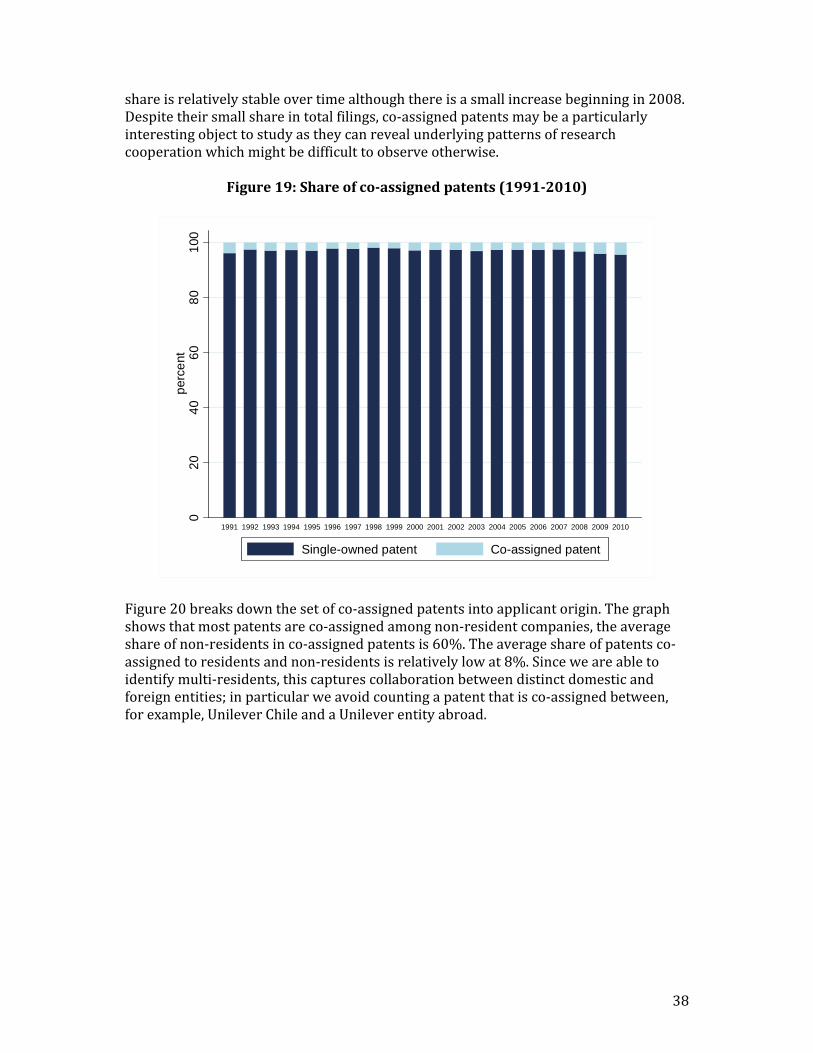

10.Co‐assignmentofpatentsFigure19takesalookatco‐assignedpatents.Co‐assignedpatentsarepatentsthatarejointlyownedbyseveralassignees,forexampleauniversitythatsharesapatentwithaprivatecompany.29Co‐assignedpatentsareoftentheoutcomeofjointresearch(Belderbosetal.,2012).TheyhavebeenshowntoberelativelyrareinOECDeconomies(Hagedoorn,2003).Figure19showsthatco‐assignedpatentsalsoaccountforasmallshareofpatentfilingsinChile–onaveragelessthan3%between1991and2010.The

28Inacompanionpaperthatfocusesonpharmaceuticals,wecreateadatabasethatcontainspatentsandtrademarksattheproductlevel(Abudetal.,2013).29Thisisdistinctfromco‐inventors,i.e.,asituationinwhichapatentlistsmultipleinventors.

38

shareisrelativelystableovertimealthoughthereisasmallincreasebeginningin2008.Despitetheirsmallshareintotalfilings,co‐assignedpatentsmaybeaparticularlyinterestingobjecttostudyastheycanrevealunderlyingpatternsofresearchcooperationwhichmightbedifficulttoobserveotherwise.

Figure19:Shareofco‐assignedpatents(1991‐2010)

02

04

06

08

01

00p

erce

nt

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Single-owned patent Co-assigned patent

Figure20breaksdownthesetofco‐assignedpatentsintoapplicantorigin.Thegraphshowsthatmostpatentsareco‐assignedamongnon‐residentcompanies,theaverageshareofnon‐residentsinco‐assignedpatentsis60%.Theaverageshareofpatentsco‐assignedtoresidentsandnon‐residentsisrelativelylowat8%.Sinceweareabletoidentifymulti‐residents,thiscapturescollaborationbetweendistinctdomesticandforeignentities;inparticularweavoidcountingapatentthatisco‐assignedbetween,forexample,UnileverChileandaUnileverentityabroad.

39

Figure20:Shareofco‐assignedpatentsresidentsandnonresidents(1991‐2010)

02

04

06

08

01

00p

erce

nt

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Non-residents Residents Residents & non-residents

Togainmoreinsightintoanycollaborationpatternsunderlyingtheco‐assignmentofpatents,Figure21plotstheshareofpatentsco‐assignedbetweendifferentapplicanttypes.Co‐assignmentsinvolvinguniversitiesaccountforaround20%ofco‐assignedpatentsoverthewhole1991‐2010period.Thesharefluctuatesconsiderably–between4%in1992and50%in2010,thoughthePCTtransitionlikelybiasesthesharesfor2010(seeabove).Figure21alsoshowsthatasizeableshareofpatentsisco‐assignedamongindividuals.Itislikelythattheseindividualsarealsoco‐inventors.Mostpatentsareco‐assignedbetweencompaniesreflectingresearchcollaborationacrosscompanies,potentiallyevenproductmarketcompetitors.30

30BenaventeandLauterbach(2007)findfortheirdatafromthe4thwaveoftheChileaninnovationsurveythataround6%ofinnovativecompaniescooperatewithproductmarketcompetitors.Theshareofinnovativecompaniesthatcooperatewithuniversitiesiswith7%slightlylarger.

40

Figure21:Shareofco‐assignedpatentsbyapplicanttype(1991‐2010)

02

04

06

08

01

00p

erce

nt

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Company Company & Individual Individual

University University & Company Univ. & Individual

University, Company & Individual

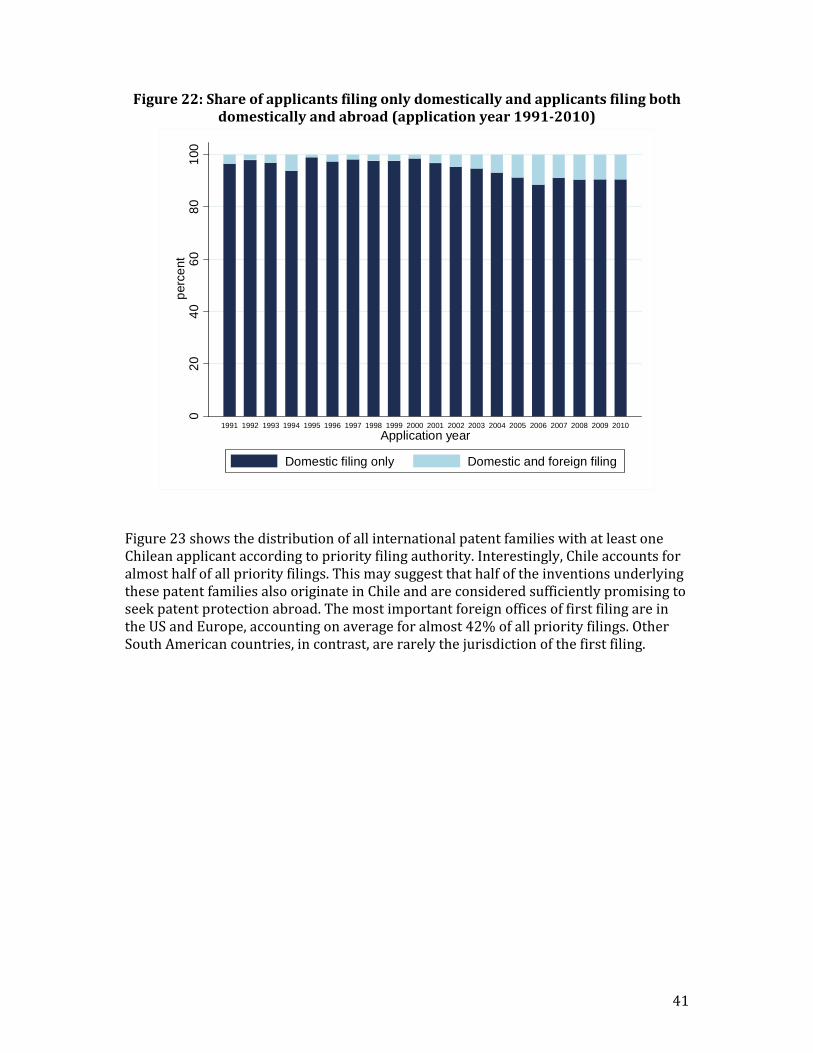

11.PatentfilingsabroadInthissectionwecombinedataonpatentfilingsbyChileanresidentsabroadwiththeINAPIdatabase.WeextractedfromtheEPOPatstatdatabase(versionSeptember2012)allpatentapplicationsthatlistaChileanapplicantorinventor.31Toavoiddoublecounting,welookatinternationalfilingsattheequivalent–orpatentfamily–level.Tobeginwith,wefoundatotalof1,236patentfamiliesthatlistChileanapplicants.Whenwerestrictthedatatofamilieswithaprioritydatebetween1991and2010,weareleftwith903patentfamilies.WethencleanedandharmonizedtheapplicantnamesassociatedwiththesepatentfamiliesandmatchedthemwiththeapplicantnamesintheINAPI‐WIPOdatabase.Figure22plotstheshareofChileanresidentapplicantsthatfileforapatentbothdomesticallyandabroad.Thisshareliesbelow15percentthroughoutthe1991‐2010perdiod,thoughthereisaclearupwardtrendfrom2001onward.ThisislikelytoreflectanincreasinglysuccessfulexportorientationofatleastsomeChileancompanies.

31Notethatthedatacoveragevariesacrossjurisdictions.WhilePatstatprovidescompletecoverageforexamplefortheUS,China,andallmembersoftheEuropeanPatentConvention,filingsareincompleteespeciallyformiddleincomecountriessuchasSouthAfricaorBrazil.

41

Figure22:Shareofapplicantsfilingonlydomesticallyandapplicantsfilingbothdomesticallyandabroad(applicationyear1991‐2010)

02

04

06

08

01

00p

erce

nt

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Application year

Domestic filing only Domestic and foreign filing

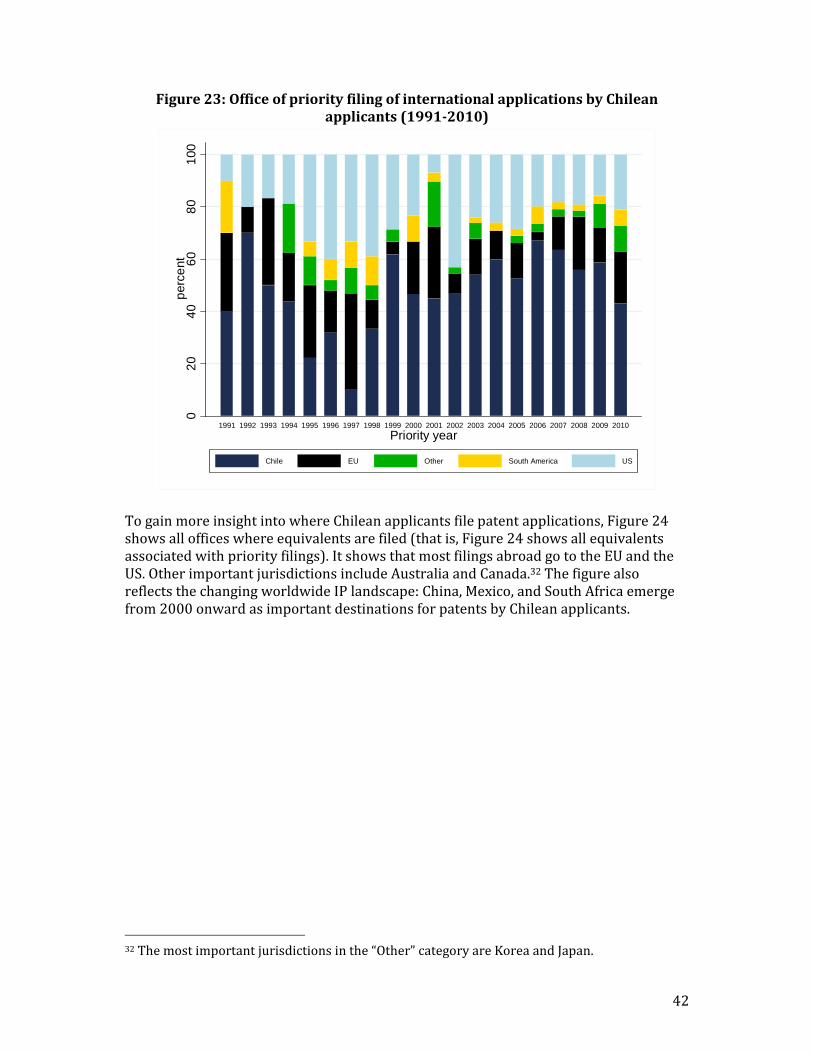

Figure23showsthedistributionofallinternationalpatentfamilieswithatleastoneChileanapplicantaccordingtopriorityfilingauthority.Interestingly,Chileaccountsforalmosthalfofallpriorityfilings.ThismaysuggestthathalfoftheinventionsunderlyingthesepatentfamiliesalsooriginateinChileandareconsideredsufficientlypromisingtoseekpatentprotectionabroad.ThemostimportantforeignofficesoffirstfilingareintheUSandEurope,accountingonaverageforalmost42%ofallpriorityfilings.OtherSouthAmericancountries,incontrast,arerarelythejurisdictionofthefirstfiling.

42

Figure23:OfficeofpriorityfilingofinternationalapplicationsbyChileanapplicants(1991‐2010)

02

04

06

08

01

00p

erce

nt

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Priority year

Chile EU Other South America US