the story of 8 metros & 7800 towns - unmetro.in3...the story of 8 metros & 7800 towns the...

TRANSCRIPT

The story of 8 metros & 7800 towns

The Big Picture

11 SEPTEMBER 2013

The big deal

2

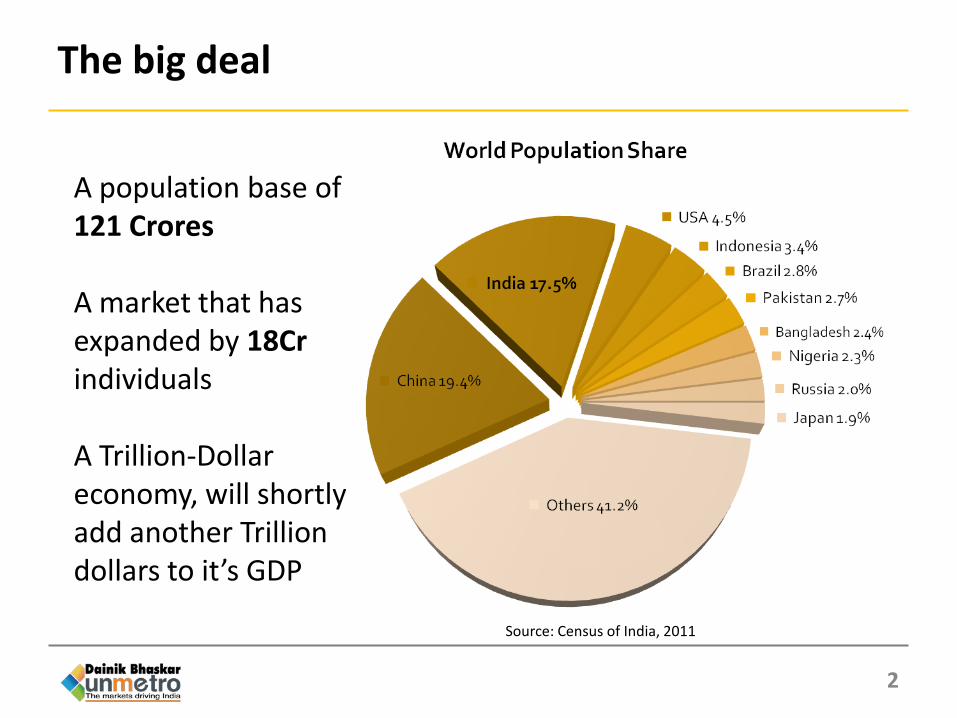

A population base of 121 Crores A market that has expanded by 18Cr individuals A Trillion-Dollar economy, will shortly add another Trillion dollars to it’s GDP

Source: Census of India, 2011

Urban India continues to call the shots

3

IndiaNo.

Admin Units

% Share of HHs

% Share of Pop

% Decadal Growth

Total HH Income (Rs.Crs)

% Share

Urban India 7,798 33% 32% 32% 50,15,000 55%

Rural India 6,40,867 67% 68% 13% 40,42,300 45%

Source: Indicus Analytics Market Skyline of India 2013

A distinct decadal growth skew combined with a higher share of income on a lower population base continues to present Urban India as an attractive proposition.

522 Cities of the Future

4

Town Class Pop StrataNo.

Admin Units

% Distribution

of HHs

Ave HH Size

Top-8 Metros MDKCBHPA 8 17% 4.39

Tier 1 >10L 41 16% 4.62Tier 2 6-10L 27 5% 4.53

Tier 3 2-6L 161 13% 4.53Tier 4 1-2L 293 10% 4.55

Large Towns 50k-1L 659 11% 4.66Medium Towns 20k-50k 2003 15% 4.71

Small Towns 10k-20k 2230 8% 4.62Very Small Towns <10k 2376 4% 4.58

Urban India 7,798 100% 4.57

Source: Indicus Analytics Market Skyline of India 2013

Layered just below the Top-8 Metros are 522 Cities Accounting for 44% of Urban HHs Presenting a seamless layer of transition for marketers

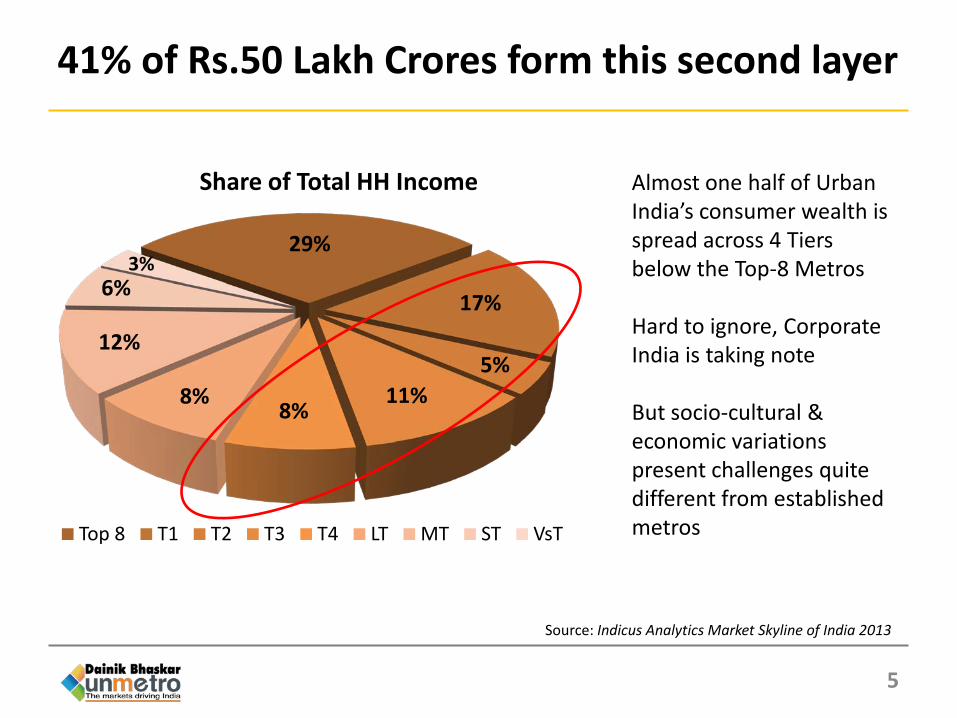

41% of Rs.50 Lakh Crores form this second layer

5

Source: Indicus Analytics Market Skyline of India 2013

29%

17%

5% 11%

8% 8%

12%

6% 3%

Share of Total HH Income

Top 8 T1 T2 T3 T4 LT MT ST VsT

Almost one half of Urban India’s consumer wealth is spread across 4 Tiers below the Top-8 Metros Hard to ignore, Corporate India is taking note But socio-cultural & economic variations present challenges quite different from established metros

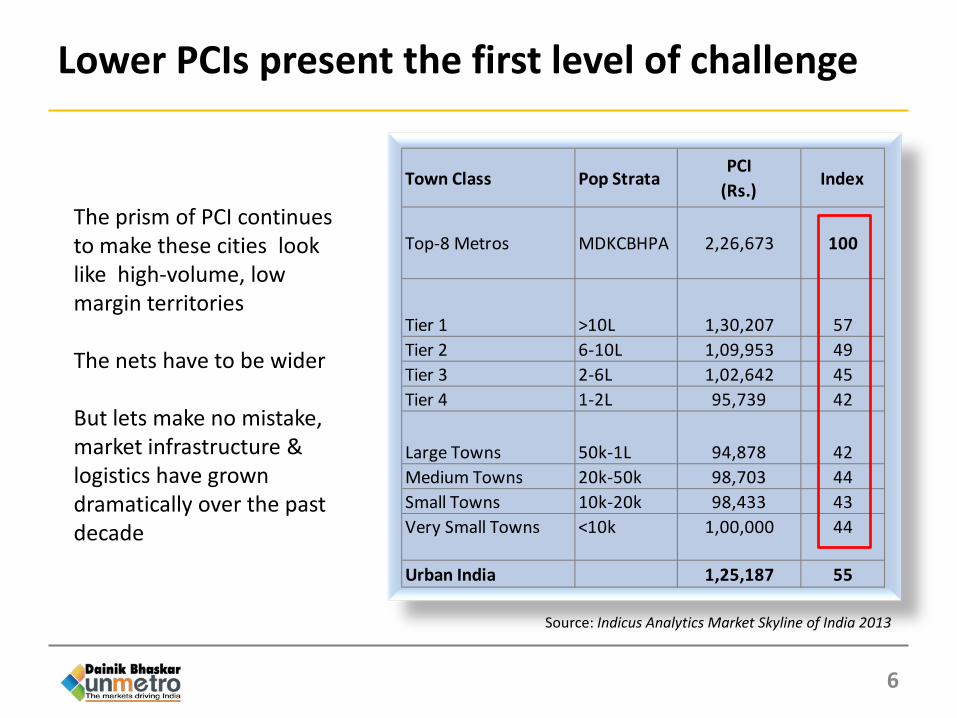

Lower PCIs present the first level of challenge

6

Town Class Pop StrataPCI

(Rs.) Index

Top-8 Metros MDKCBHPA 2,26,673 100

Tier 1 >10L 1,30,207 57Tier 2 6-10L 1,09,953 49Tier 3 2-6L 1,02,642 45Tier 4 1-2L 95,739 42

Large Towns 50k-1L 94,878 42Medium Towns 20k-50k 98,703 44Small Towns 10k-20k 98,433 43Very Small Towns <10k 1,00,000 44

Urban India 1,25,187 55

Source: Indicus Analytics Market Skyline of India 2013

The prism of PCI continues to make these cities look like high-volume, low margin territories The nets have to be wider But lets make no mistake, market infrastructure & logistics have grown dramatically over the past decade

But there’s always been a Middle India even in established Metros

7

Pop-Strata Base <75k 75k - 1.5L 1.5L - 3L 3L - 5L 5L - 10L >10L

Metros 100 21% 16% 17% 12% 13% 22%

Tier 1 100 31% 18% 17% 11% 11% 13%

Tier 2 100 35% 18% 17% 10% 10% 10%

Tier 3 100 36% 18% 17% 10% 9% 9%

Tier 4 100 38% 18% 16% 10% 9% 8%

Towns 100 39% 18% 16% 10% 9% 8%

Distribution of Urban HHs by Rs.Income per annum

Source: Indicus Analytics Market Skyline of India 2013

Accounts for just

30% of all Urban HHs

in India

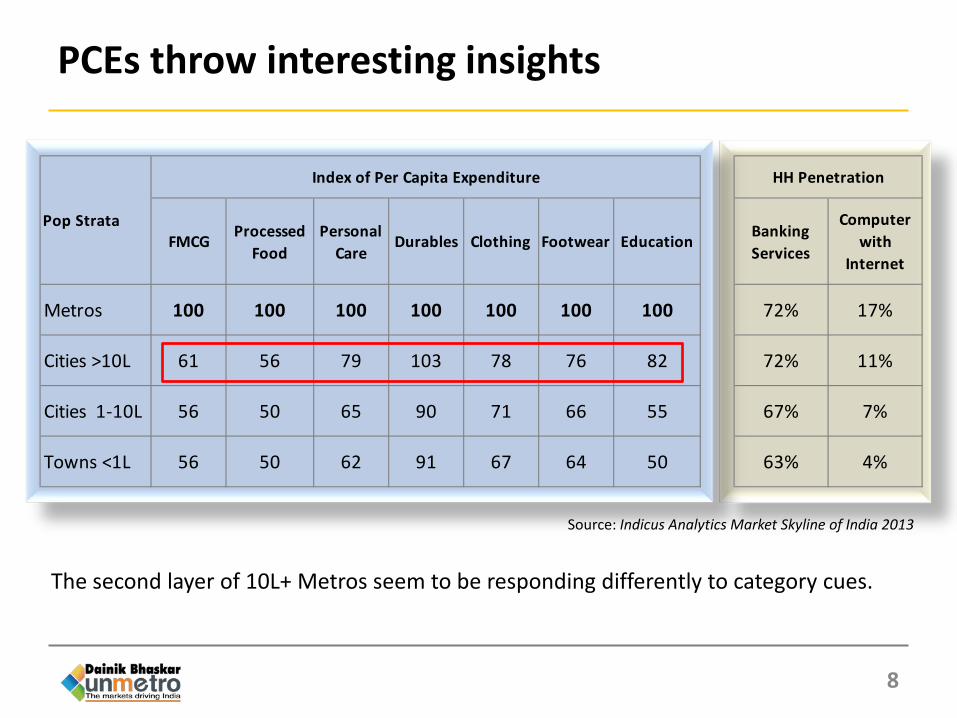

PCEs throw interesting insights

8

FMCG Processed Food

Personal Care

Durables Clothing Footwear Education Banking Services

Computer with

Internet

Metros 100 100 100 100 100 100 100 72% 17%

Cities >10L 61 56 79 103 78 76 82 72% 11%

Cities 1-10L 56 50 65 90 71 66 55 67% 7%

Towns <1L 56 50 62 91 67 64 50 63% 4%

Index of Per Capita Expenditure HH Penetration

Pop Strata

Source: Indicus Analytics Market Skyline of India 2013

The second layer of 10L+ Metros seem to be responding differently to category cues.

Category consumption bases are in place

9

27%

16%

24% 33%

Processed Food Rs. 1,85,931 Crs

Metros Cities >10L Cities 1L-10L Cities <1L

25%

16%

25% 34%

FMCG Rs. 2,92,240 Crs

23%

18%

26% 33%

Personal Care Rs. 31,178 Crs

Source: Indicus Analytics Market Skyline of India 2013

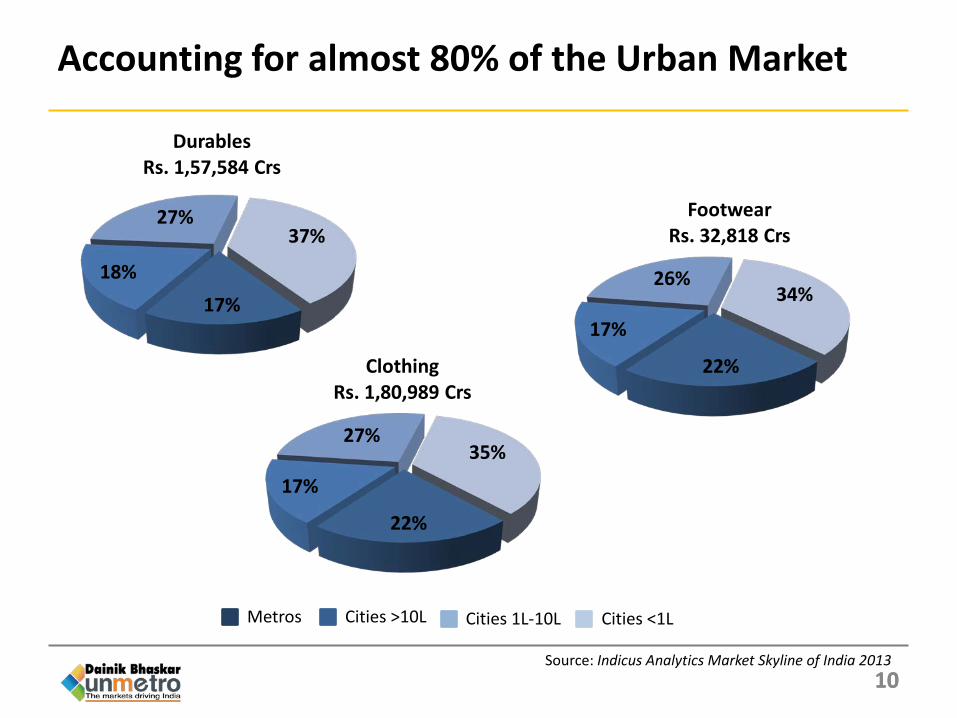

Accounting for almost 80% of the Urban Market

10 10

17% 18%

27% 37%

Durables Rs. 1,57,584 Crs

Metros Cities >10L Cities 1L-10L Cities <1L

22%

17%

27% 35%

Clothing Rs. 1,80,989 Crs

22%

17%

26% 34%

Footwear Rs. 32,818 Crs

Source: Indicus Analytics Market Skyline of India 2013

Consumer essentials are falling in place

11

Metros Cities >10L Cities 1L-10L Cities <1L

18% 18%

29% 35%

HHs Availing Banking Services

25%

21%

24% 30%

Education Rs. 84,062 Crs

35%

22% 25%

18%

HHs Computer with Internet

Source: Indicus Analytics Market Skyline of India 2013

And this is the Real Story of India Unmetro’ed

12

Microwave Ovens

Air Conditioners

Four Wheelers

Computers

Washing Machines

DVD Players

Refrigerators

Two Wheelers

6%

10%

9%

17%

28%

35%

54%

28%

40L+ 10L-40L 1L-10L <1L

40L+ 10-40L 1-10L <1L

Two Wheelers 4% 6% 7% 8%

Refrigerators 7% 9% 9% 12%

DVD Players 17% 18% 18% 23%

Washing Machines 10% 13% 13% 18%

Computers 14% 20% 21% 26%

Four Wheelers 8% 14% 14% 15%

Air Conditioners 12% 21% 21% 23%

Microwave Ovens 14% 28% 28% 31%

DURABLESCAGR 2007 - 2012

PENETRATION 2012

Source: IRS 2008 R1 & 2012 Q4

Lifestyle drivers are in cruise mode

13

Branded Soups

Processed Cheese

Deodorants

Ketchup / Sauces

Instant Noodles

Soft Drinks

Nail Polish

Toilet Cleaners

Shampoos

6%

8%

15%

26%

51%

45%

22%

51%

75%

40L+ 10L-40L 1L-10L <1L

PENETRATION 2012

Source: IRS 2008 R1 & 2012 Q4

40L+ 10-40L 1-10L <1L

Shampoos 5% 7% 6% 6%

Toilet Cleaners 10% 12% 11% 14%

Nail Polish 8% 8% 7% 8%

Soft Drinks 3% 4% 6% 6%

Instant Noodles 14% 23% 21% 24%

Mineral Water 5% 10% 8% 11%

Chocolates 7% 10% 7% 9%

Ketchup / Sauces 7% 13% 13% 14%

Deodorants 16% 22% 14% 17%

Processed Cheese 10% 21% 15% 19%

Branded Soups 17% 27% 21% 18%

FMCGCAGR 2007 - 2012

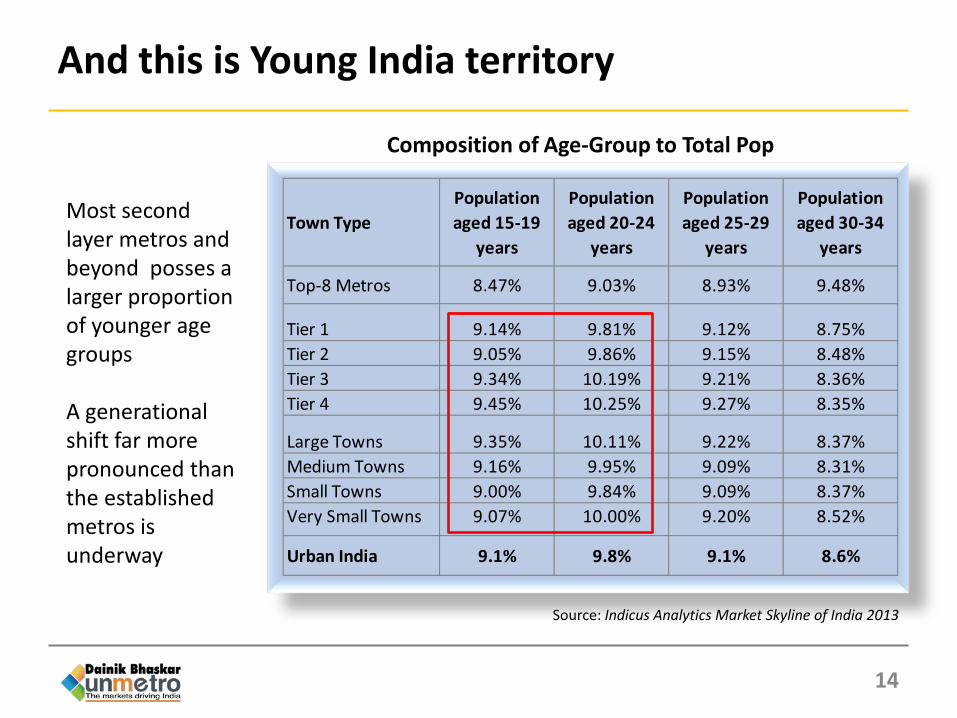

And this is Young India territory

14

Town TypePopulation aged 15-19

years

Population aged 20-24

years

Population aged 25-29

years

Population aged 30-34

years

Top-8 Metros 8.47% 9.03% 8.93% 9.48%

Tier 1 9.14% 9.81% 9.12% 8.75%Tier 2 9.05% 9.86% 9.15% 8.48%Tier 3 9.34% 10.19% 9.21% 8.36%Tier 4 9.45% 10.25% 9.27% 8.35%

Large Towns 9.35% 10.11% 9.22% 8.37%Medium Towns 9.16% 9.95% 9.09% 8.31%Small Towns 9.00% 9.84% 9.09% 8.37%Very Small Towns 9.07% 10.00% 9.20% 8.52%

Urban India 9.1% 9.8% 9.1% 8.6%

Composition of Age-Group to Total Pop

Source: Indicus Analytics Market Skyline of India 2013

Most second layer metros and beyond posses a larger proportion of younger age groups A generational shift far more pronounced than the established metros is underway

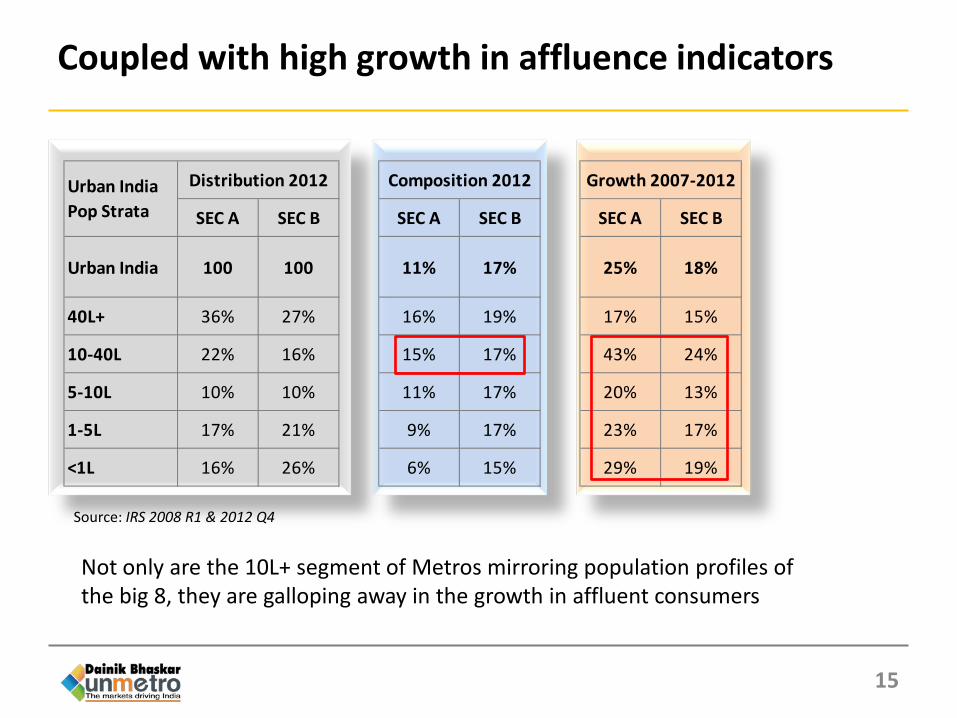

Coupled with high growth in affluence indicators

15

Not only are the 10L+ segment of Metros mirroring population profiles of the big 8, they are galloping away in the growth in affluent consumers

SEC A SEC B SEC A SEC B SEC A SEC B

Urban India 100 100 11% 17% 25% 18%

40L+ 36% 27% 16% 19% 17% 15%

10-40L 22% 16% 15% 17% 43% 24%

5-10L 10% 10% 11% 17% 20% 13%

1-5L 17% 21% 9% 17% 23% 17%

<1L 16% 26% 6% 15% 29% 19%

Urban India Pop Strata

Distribution 2012 Composition 2012 Growth 2007-2012

Source: IRS 2008 R1 & 2012 Q4

An extremely media-mature urban India

16

Source: IRS 2008 R1 & 2012 Q4

0%

25%

50%

75%

100%

C&S AD-TR AD-AIR Radio Internet

40L+ 10L-40L 5L-10L 1L-5L <1L

0%

25%

50%

75%

100%

C&S AD-TR AD-AIR Radio Internet

40L+ 10L-40L 5L-10L 1L-5L <1L

MEDIA REACH - ALL ADULTS MEDIA REACH - SEC A

Traditional media continues to hold fort very strongly across Urban Tiers

AD-TR: Any Daily–Total Readership AD-AIR: Any Daily–Average Issue Readership

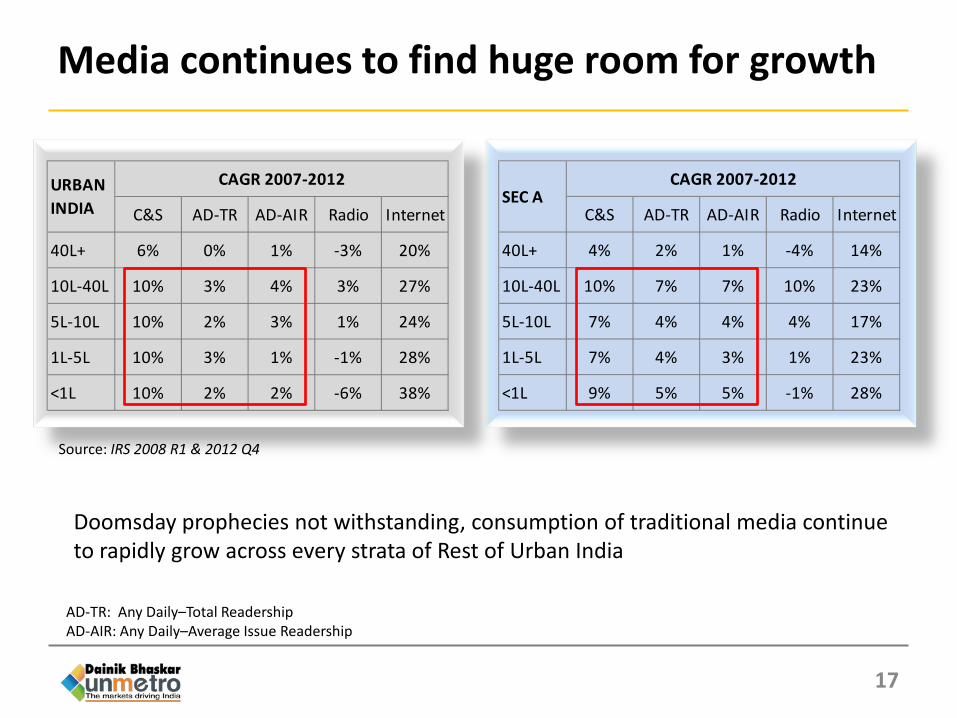

Media continues to find huge room for growth

17

C&S AD-TR AD-AIR Radio Internet

40L+ 6% 0% 1% -3% 20%

10L-40L 10% 3% 4% 3% 27%

5L-10L 10% 2% 3% 1% 24%

1L-5L 10% 3% 1% -1% 28%

<1L 10% 2% 2% -6% 38%

URBAN INDIA

CAGR 2007-2012

C&S AD-TR AD-AIR Radio Internet

40L+ 4% 2% 1% -4% 14%

10L-40L 10% 7% 7% 10% 23%

5L-10L 7% 4% 4% 4% 17%

1L-5L 7% 4% 3% 1% 23%

<1L 9% 5% 5% -1% 28%

SEC ACAGR 2007-2012

Source: IRS 2008 R1 & 2012 Q4

Doomsday prophecies not withstanding, consumption of traditional media continue to rapidly grow across every strata of Rest of Urban India

AD-TR: Any Daily–Total Readership AD-AIR: Any Daily–Average Issue Readership

CONSUMER CLASSIFICATION AND FINALLY A PONDER

18

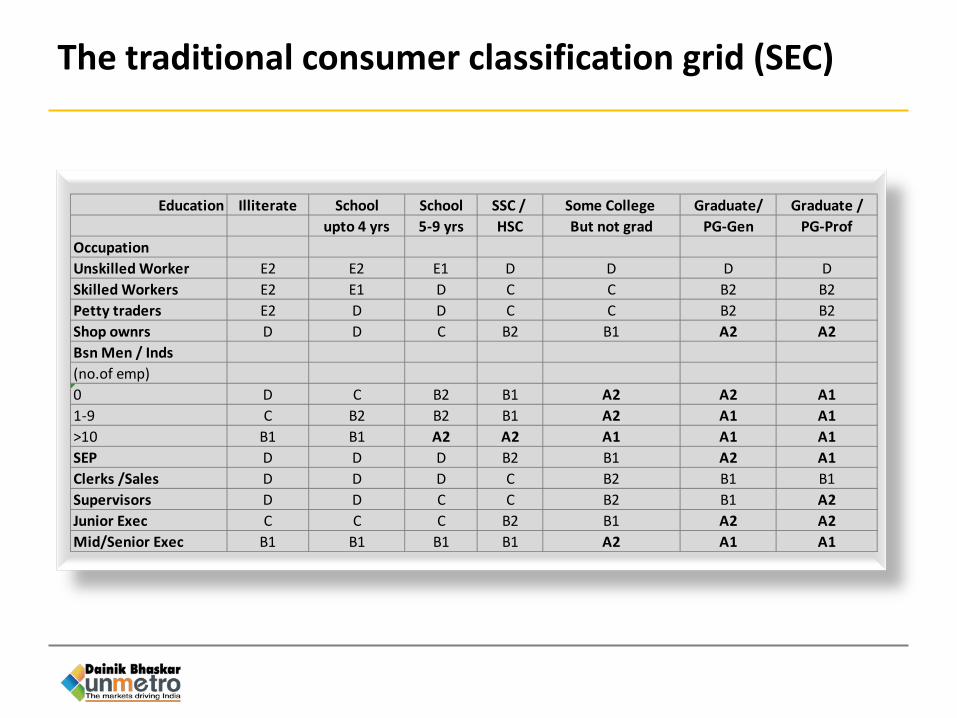

The traditional consumer classification grid (SEC)

Education Illiterate School School SSC / Some College Graduate/ Graduate /upto 4 yrs 5-9 yrs HSC But not grad PG-Gen PG-Prof

OccupationUnskilled Worker E2 E2 E1 D D D DSkilled Workers E2 E1 D C C B2 B2Petty traders E2 D D C C B2 B2Shop ownrs D D C B2 B1 A2 A2Bsn Men / Inds(no.of emp)0 D C B2 B1 A2 A2 A11-9 C B2 B2 B1 A2 A1 A1>10 B1 B1 A2 A2 A1 A1 A1SEP D D D B2 B1 A2 A1Clerks /Sales D D D C B2 B1 B1Supervisors D D C C B2 B1 A2Junior Exec C C C B2 B1 A2 A2Mid/Senior Exec B1 B1 B1 B1 A2 A1 A1

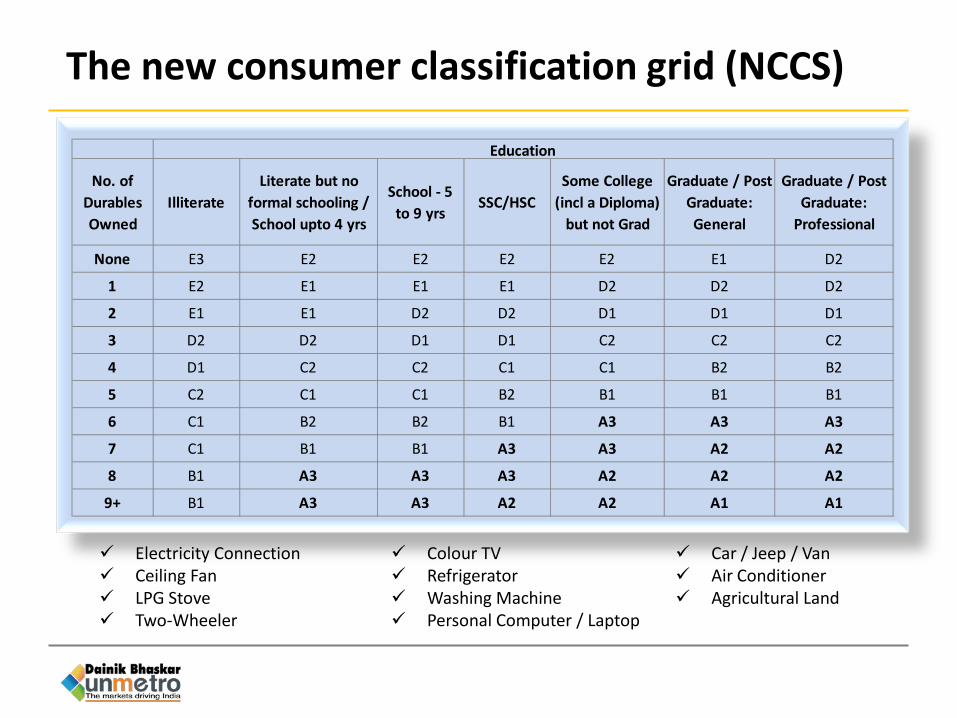

No. of Durables Owned

IlliterateLiterate but no

formal schooling / School upto 4 yrs

School - 5 to 9 yrs

SSC/HSCSome College

(incl a Diploma) but not Grad

Graduate / Post Graduate: General

Graduate / Post Graduate:

Professional

None E3 E2 E2 E2 E2 E1 D2

1 E2 E1 E1 E1 D2 D2 D2

2 E1 E1 D2 D2 D1 D1 D1

3 D2 D2 D1 D1 C2 C2 C2

4 D1 C2 C2 C1 C1 B2 B2

5 C2 C1 C1 B2 B1 B1 B1

6 C1 B2 B2 B1 A3 A3 A3

7 C1 B1 B1 A3 A3 A2 A2

8 B1 A3 A3 A3 A2 A2 A2

9+ B1 A3 A3 A2 A2 A1 A1

Education

Electricity Connection Ceiling Fan LPG Stove Two-Wheeler

Colour TV Refrigerator Washing Machine Personal Computer / Laptop

Car / Jeep / Van Air Conditioner Agricultural Land

The new consumer classification grid (NCCS)

Are we under-estimating the depth of our markets?

21

Source: IRS 2012 Q4

SEC All A1 A2 B1 B2 C D E1 E2 R1 R2 R3 R4

Pop Crs 91.3 1.1 2.1 2.4 2.5 6.1 6.8 3.4 5.0 3.0 9.6 25.8 23.4

Distribution 100 1% 2% 3% 3% 7% 7% 4% 6% 3% 11% 28% 26%

NCCS All A1 A2 A3 B1 B2 C1 C2 D1 D2 E1 E2 E3

Pop Crs 91.3 1.2 2.9 4.8 5.5 6.9 9.6 9.6 11.7 13.0 14.4 8.5 3.2

Distribution 100 1% 3% 5% 6% 8% 11% 10% 13% 14% 16% 9% 3%

The NCCS brings alive the concept of “Middle India” into sharp focus

The problem gets magnified across Urban India

22

The redistribution of affluence segmentation opens up huge possibilities in assessing & monitoring a market

A B C D EPop (Crs) 29.6 3.3 5.0 6.1 6.8 8.4Distribution 100 11% 17% 21% 23% 28%

Pop (Crs) 29.6 6.3 6.4 8.1 6.0 2.6Distribution 100 21% 22% 27% 20% 9%

Urban India

SEC

NCCS

Source: IRS 2012 Q4

NCCS completely turns classification on its head

23

Base-line consumer classification usually has enormous implications in decisions pertaining to entering new markets and the nature of investments to be made

A 42%

B 38%

C 16%

DE 4%

SEC Composition of NCCS-A Urban India

A 83%

B 14%

NCCS Composition of SEC-A Urban India

Source: IRS 2012 Q4

The real rise of Unmetro India

24

A B C D E

40L+ 78% 36% 23% -34% -82%

10L-40L 88% 37% 28% -24% -80%

5L-10L 116% 35% 33% -17% -77%

1L-5L 106% 19% 41% -3% -67%

<1L 118% 25% 38% 9% -57%

URBAN INDIA

NCCS vs SEC Variance

Source: IRS 2012 Q4

Enumerating HH affluence through a more direct metric of Product ownership alters the consumer segment landscape of Urban India

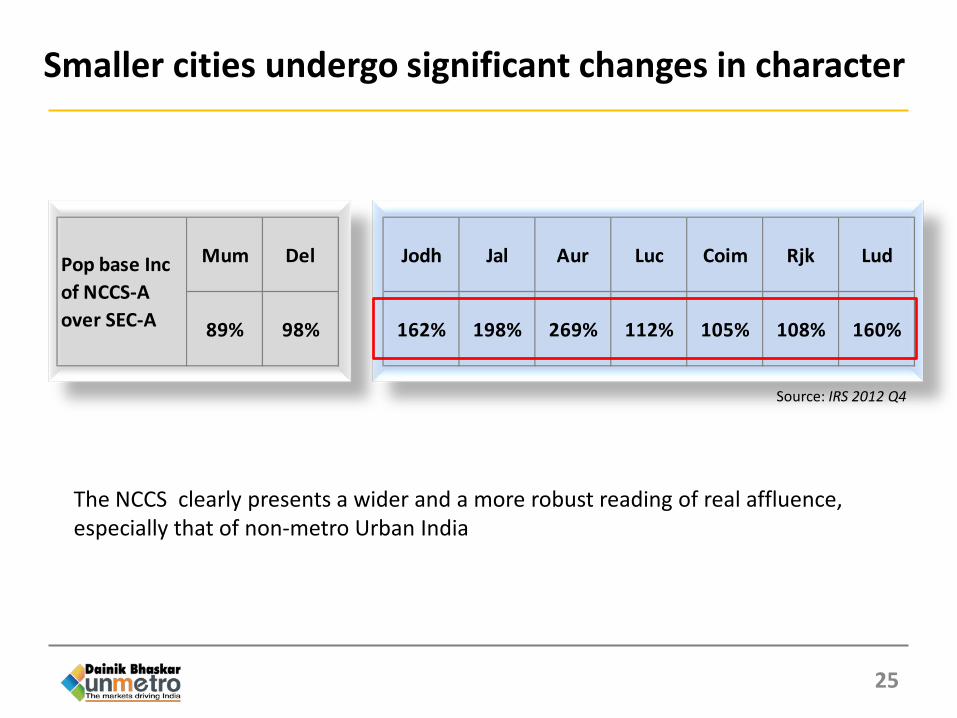

Smaller cities undergo significant changes in character

25

Mum Del Jodh Jal Aur Luc Coim Rjk Lud

89% 98% 162% 198% 269% 112% 105% 108% 160%

Pop base Inc of NCCS-A over SEC-A

Source: IRS 2012 Q4

The NCCS clearly presents a wider and a more robust reading of real affluence, especially that of non-metro Urban India

Thank you

26