the sigma perspective luis a. seco president and ceo

TRANSCRIPT

Hedge fund investingThe Sigma Perspective

Luis A. Seco

President and CEO, Sigma Analysis & Management

Sigma Analysis & Management

The Fields Institute

222 College Street

Toronto, Ontario M5T 3J1

Agenda

History of a decade (1994-2004): myths and facts

Hedge Fund Indices: the likely mistake for 2005

The perspective on hedge fund investments

Conclusions

Sigma Analysis & Management

Marriage between business and academia: the RiskLab

Risk Management and Asset Management background

Founded in 1999 as an institutional advisor. In 2002 became manager for family offices. In 2004 it joined Quadrexx to bring a risk-controlled product to the retail market.

11 employees in Canada, US and UK.

Clients: Canadian banks and pension plans, US family offices, Insurance Companies and Pensions.

History of a decade: 1994-2004

CSFB Hedge Fund Index

1000

1500

2000

2500

3000

3500

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Interest rate vol Credit crunch Interest rate vol

The myth of 1998: Fixed income is bad”

CSFB Hedge Fund Index - Fixed Income 1998

850

900

950

1000

1050

1 2 3 4 5 6 7 8 9 10 11 12 13

Facts (1998)

“Fixed Income arbitrage” suffered generalized losses: -8%

“equity hedged” obtained generalized gains: +13% (M.F. +20%)

A balanced hedge fund portfolio would have been OK in 1998.

Investors decide to avoid Fixed Income as a style.

The myth of 2003:“Hedge funds (equity hedged) are good”

1000

1100

1200

1300

Dec-02 Jan-03 Feb-03 Mar-03 Apr-03 May-03 Jun-03 Jul-03 Aug-03 Sep-03 Oct-03 Nov-03 Dec-03

HFRI Convertible Arbitrage Index

HFRI Distressed Securities Index (Offshore)

HFRI Equity Hedge Index

HFRI Equity Market Neutral Index

HFRI Event-Driven Index

HFRI Fixed Income: Arbitrage Index

HFRI Fixed Income: Mortgage-Backed Index

HFRI Merger Arbitrage Index

HFRI Relative Value Arbitrage Index

Facts: 2003

Most hedge fund styles obtained great returns.

The style “equity hedge” came out on top: +17%.

Investors moved en-masse to this style for 2004, forgetting all others.

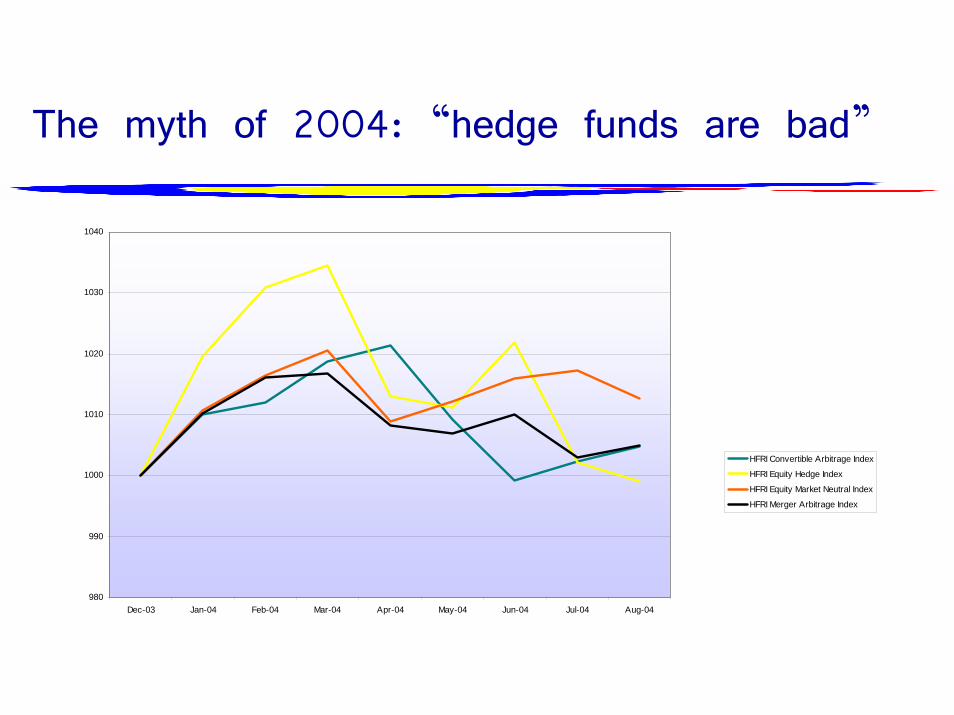

The myth of 2004: “hedge funds are bad”

980

990

1000

1010

1020

1030

1040

Dec-03 Jan-04 Feb-04 Mar-04 Apr-04 May-04 Jun-04 Jul-04 Aug-04

HFRI Convertible Arbitrage Index

HFRI Equity Hedge Index

HFRI Equity Market Neutral Index

HFRI Merger Arbitrage Index

The facts: 2004

“Equity hedge” lost, as a style, in 2004.

Many investors, who trusted this (the most common), lose confidence.

Speculation arises as to whether hedge funds continue to bring value to investors portfolios.

Myth and science in 2004

980

1000

1020

1040

1060

1080

1100

Dec-03 Jan-04 Feb-04 Mar-04 Apr-04 May-04 Jun-04 Jul-04 Aug-04

HFRI Convertible Arbitrage Index

HFRI Distressed Securities Index (Offshore)

HFRI Equity Hedge Index

HFRI Equity Market Neutral Index

HFRI Event-Driven Index

HFRI Fixed Income: Arbitrage Index

HFRI Fixed Income: Mortgage-Backed Index

HFRI Merger Arbitrage Index

HFRI Relative Value Arbitrage Index

Many hedge fund strategies have performed poorly in 2004... but quite a few of them seem to be recovering, and some have not been affectedby the "bad times"at all.

Science: lessons from history

Hedge funds continue to provide diversifying returns.

One should never favor one style against another based on simplistic rear-looking arguments.

The main property of hedge funds is their low correlation: this should not be destroyed with directional bets or unfounded decisions.

Hedge Funds indices

The myth of 2005?

Hedge Funds

Hedge Funds, unlike traditional investments, show little cohesion.

This is what makes them attractive: they add diversification.

Because of hedge fund diversity, a hedge fund index is going to fail to capture anything of interest; they are plain fund-of-funds

Differences with stock indices

Index constituence is a function of liquidity, operations, etc. not performance.

Unlike stock indices, investors don’t like their hedge funds to be included in hedge fund investable indices

Alpha and beta

995

1000

1005

1010

1015

1020

1025

1030

Dec-03 Jan-04 Feb-04 Mar-04 Apr-04 May-04 Jun-04 Jul-04 Aug-04

Sigma Convertible Arbitrage Subindex

HFRI Convertible Arbitrage Index

Even w ithin a strategy w hose index is performing poorly, returns can be remarkably diverse. The index may be an inaccurate indicator of w hat may be achievable w ithin the strategy.

beta

alpha

Indices in 2003

980

985

990

995

1000

1005

1010

1015

1020

1025

1030

Dec-03 Jan-04 Feb-04 Mar-04 Apr-04 May-04 Jun-04 Jul-04 Aug-04

CSFB-Tremont HFI Investible Hedge Fund

HFRXGL Index

S&P Hedge Fund Index

Index correlations

CSFB Hedge Investible Index 1.00MSCI Composite Equal-Weighed Index 0.47 1.00MSCI Composite Asset-Weighed Index 0.51 0.98 1.00S&P Hedge Fund Index 0.41 0.90 0.94 1.00Van Global Hedge Fund Index 0.80 0.48 0.51 0.41 1.00

How to invest in Hedge Funds

What investors should keep in mind

Absence of correlation continues to be the best aspect of hedge fund investing.

Correlations change, and an investment should not be left to diversification exposure, which affects the portfolio in the most difficult times.

There are many mediocre hedge funds, but there are still many which are excellent.

Risks to avoid: distressed alignment

Risks to avoid: distressed alignment

Equity vs Fixed Income CTA vs Fixed Income

Equity vs Fixed Income

Other risks

Style risk

Concentration

Valuation

Liquidity

Operational risk

Blow-up

Other risks

Style risk

Concentration

Valuation

Liquidity

Operational risk

Blow-up

Non-diversifiable

Non-diversifiable

Non-diversifiable

diversifiable

diversifiable

diversifiable

The Reference Portfolio

Identify the risks.

Get a target return.

Produce a risk tolerance.

Mathematize the simultaneous risk mitigation problem.

Do the math

Investment design

Get a low risk hedge fund foundation: modest return, minimal risk.

Performance independent of market events

Get proper liquidity for the underlying hedge funds

Lever on the low risk levels of the foundation to enhance returns

Conclusions

Don’t buy last year’s returns

Travel with the airline which is aware of the risks.

Play hockey with good goalies and defense, not just forwards.

Have a balanced diet.