the seven secrets of distribution november 2010 daniel enskat head of global consulting

TRANSCRIPT

The Seven Secrets of Distribution

November 2010

Daniel Enskat

Head of Global Consulting

2

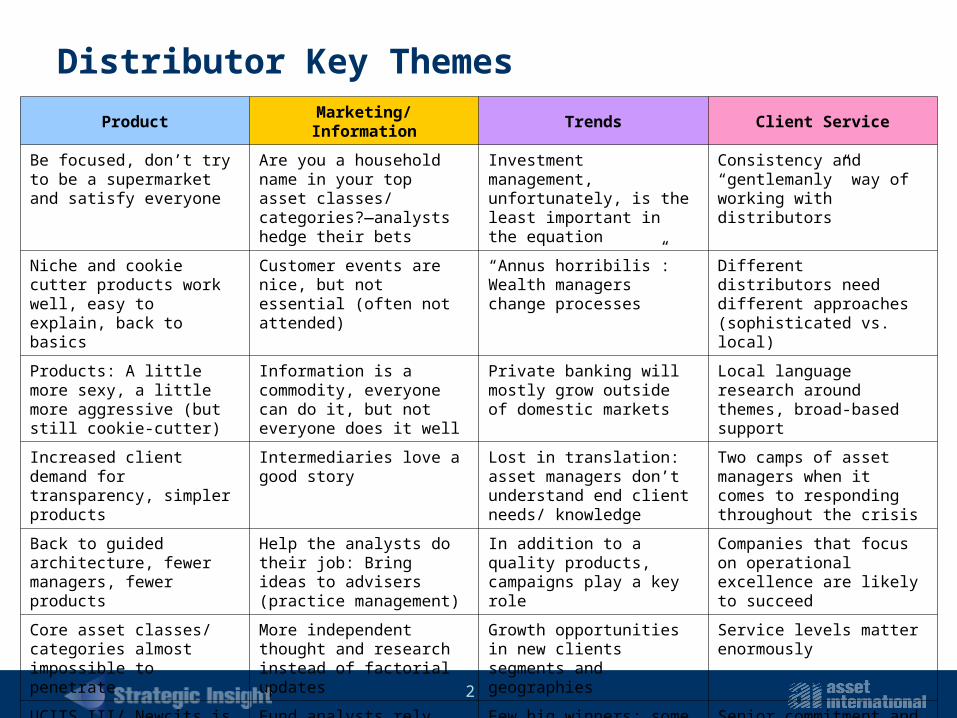

Distributor Key ThemesProduct Marketing/ Information Trends Client Service

Be focused, don’t try to be a supermarket and satisfy everyone

Are you a household name in your top asset classes/ categories?—analysts hedge their bets

Investment management, unfortunately, is the least important in the equation

Consistency and “gentlemanly” way of working with distributors

Niche and cookie cutter products work well, easy to explain, back to basics

Customer events are nice, but not essential (often not attended)

“Annus horribilis”: Wealth managers change processes

Different distributors need different approaches (sophisticated vs. local)

Products: A little more sexy, a little more aggressive (but still cookie-cutter)

Information is a commodity, everyone can do it, but not everyone does it well

Private banking will mostly grow outside of domestic markets

Local language research around themes, broad-based support

Increased client demand for transparency, simpler products

Intermediaries love a good story

Lost in translation: asset managers don’t understand end client needs/ knowledge

Two camps of asset managers when it comes to responding throughout the crisis

Back to guided architecture, fewer managers, fewer products

Help the analysts do their job: Bring ideas to advisers (practice management)

In addition to a quality products, campaigns play a key role

Companies that focus on operational excellence are likely to succeed

Core asset classes/ categories almost impossible to penetrate

More independent thought and research instead of factorial updates

Growth opportunities in new clients segments and geographies

Service levels matter enormously

UCITS III/ Newcits is a hot topic, but limited cash flows (for now); naïve approach of hedge funds

Fund analysts rely more on industry aggregators and local sites

Few big winners; some firms blacklisted for the next few years

Senior commitment and communication

3

-200

0

200

400

600

800

1,000

Asia Europe US

Other

Bond

Mixed

Equity

-200

0

200

400

600

800

1,000

Asia Europe US

Source: Strategic Insight Simfund GL, MF

-200

0

200

400

600

800

1,000

1,200

1,400

1,600

Asia Europe US

Source: Strategic Insight Simfund GL, MF

Global Mutual Fund Flows by Region, Asset Class

In US$ Billion

BondMixedEquity

Other

Source: Strategic Insight Simfund GL, MF

5-Year (2005-2009) 2005-2008 2009-1H’2010

4

Distribution Channels by Market

*Please note: insurance companies are not yet authorized to sell mutual funds in China, and currently there are no IFAs available to Chinese retail investors. Source: Strategic Insight estimates, Asian Industry Associations

0%

20%

40%

60%

80%

100%

Japan China* Korea India Hong Kong Taiwan Singapore

Bank Securities Firm Insurance IFAs Direct

*Please note: Insurance companies are not authorized to sell mutual funds in China, and currently there are no IFAs available to Chinese retail investors. Source: Strategic Insight estimates, Asian Industry Associations

Distribution Channel Breakout in Asia by MarketDistribution Channels – Asia

5

Distribution Channels by Market

Distribution Channels – Europe

0%

20%

40%

60%

80%

100%

Italy France UK Germany Spain Switzerland Nordics

Retail bank Private bank IFA Direct Fund of funds Insurance Other*

* For the Nordics, this category mainly encompasses pensions/ investment wrappersSource: Strategic Insight estimates, European Industry Associations

Distribution Channel Breakout in Europe by Market

0%

20%

40%

60%

80%

100%

Italy France UK Germany Spain Switzerland Nordics

Retail bank Private bank IFA Direct Fund of funds Insurance Other*

* For the Nordics, this category mainly encompasses pensions/ investment wrappersSource: Strategic Insight estimates, European Industry Associations

Distribution Channel Breakout in Europe by Market

6

Global Distribution Opportunity Matrix

7

Highest Cash Flow Non-US Long-term Funds YTD 8-10 In US$ Billion

Net Flows

Portfolio Category YTD 2009 2008 2007 Templeton Global Bond Bond Global 13.9 5.2 -0.1 3.2

Carmignac Patrimoine Mixed Balanced Flex 10.9 14.2 3.3 -0.2

PIMCO GIS Total Return Bd Bond USD 8.3 5.3 -0.4 0.1

Nomura Global High Yield Bond F(Envmt Crny) Bond High Yield 8.0 Pictet-Emerging Local Currency Debt Bond Emg Mkts 6.2 1.2 -0.6 0.7

Templeton Global Total Return Bond Global 6.1 1.4 -0.2 1.9

AllianceBernstein-Global High Yield Bond High Yield 4.6 4.8 -2.1 1.6

DaiwaSB Short Term AU Bond OP Bond Asia Pacific 4.1 2.1 1.0 -0.4

Fidelity US REIT Fund Real Estate 4.1 0.7 0.0 0.0

Carmignac Securite Bond Europe 4.0 3.7 0.1 0.2

Standard Life Inv Glo Abs Ret Strategies Absolute Return 4.0 1.8 1.7

Daiwa Brazil Bond Open Bond Emg Mkts 3.6 3.6 0.0

MitsubishiUFJ Emerging Country Bond F Bond Emg Mkts 3.4 1.9

SMAM SMBC Nikko New World Bond F(BRL) Bond Emg Mkts 2.9 3.0

AXA IM FIIS US Short Duration High Yield Bond High Yield 2.9 0.3 0.0 0.5

Julius Baer BF Absolute Return Absolute Return 2.8 1.4 -1.8 1.3

PIMCO GIS Global Inv Grd Crdt Bond Global 2.7 2.8 1.1 0.1 Templeton Asian Growth Equity Asia Pacific 2.7 2.0 -2.1 1.8

Fidelity Funds - US High Yield Bond High Yield 2.6 1.2 -0.2 -0.1

Fonditalia Core 1 Mixed Conservative 2.5 1.1 0.1

Total above 81.9 59.4 -0.6 11.1

*Combines various currency linked versions of the fund

Note: excludes internal fund of funds, with exception of Japan

Source: Strategic Insight Simfund GL

Top Selling Non-US Long-Term Funds

Net Flows Historically, Ranked by YTD August 2010 (In US$ Billion)

Source: Strategic Insight Simfund GL

8

Fund SelectionUnits

More Power

Fund Selection Units Post-Crisis

MoreComplexity

MoreConcentration

9

0%

20%

40%

60%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

0%

20%

40%

60%

Asia

Europe + UCITS to Non-European Investors

US

Source: Strategic Insight Simfund GL

Middle EastLatin-America

Europe

0%

20%

40%

60%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

0%

20%

40%

60%

Asia

Europe + UCITS to Non-European Investors

US

Source: Strategic Insight Simfund GL

Middle EastLatin-America

Europe

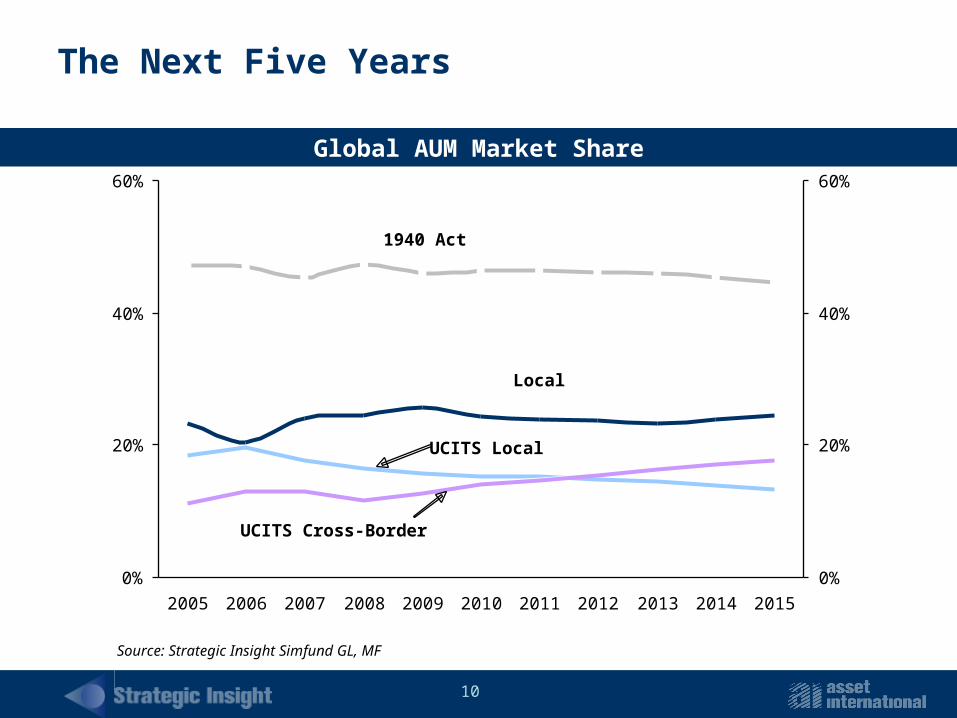

The Next Five Years

Global AUM Market Share

10

0%

20%

40%

60%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

0%

20%

40%

60%

Local

1940 Act

Source: Strategic Insight Simfund GL, MF

UCITS Cross-Border

UCITS Local

The Next Five Years

Global AUM Market Share

11

Challenges and Investment Dichotomies

• Turn speculators into investors• Pensions• Cumbersome sales processes• Emerging Markets• Head office centricity• Brand, staff, language • The long-term view• Local market perception

• US vs. global• Developed vs. Emerging• Local vs. Offshore• Investment Themes vs.

Solutions• Active vs. Passive• Relative vs. Absolute Returns• Fee-based vs. Commission-

based• Traditional vs. Alternative

Industry Key Challenges Investment Dichotomies

12

Strategic Insight

www.StrategicInsightGlobal.comwww.Sionline.com

www.SimFundFiling.com

Contact the Strategic Insight Global team:+1.212.217.6885 [email protected]