the role of environmental initiatives in encouraging companies to engage in environmental reporting

TRANSCRIPT

doi:10.1016/j.emj.2005.10.014

European Management Journal Vol. 23, No. 6, pp. 702–716, 2005

� 2005 Elsevier Ltd. All rights reserved.

Printed in Great Britain

0263-2373 $30.00

The Role ofEnvironmentalInitiatives inEncouragingCompanies to Engagein EnvironmentalReporting

ROBERT DIXON, Durham Business School

GEHAN A. MOUSA, Benha University

ANNE WOODHEAD, Durham University

A number of studies have indicated that the envi-ronmental disclosure of corporations is still at avery low level even though they are faced withincreasing pressures from diverse stakeholdergroups, including governmental agencies, toaddress environmental concerns. In spite of thesubstantial contingent financial exposure createdby the superfund legislation in the US for chemicaland similar firms, disclosures of liabilities are a rel-atively recent phenomenon (Milne and Patten,2002). In an attempt to encourage and help corpora-tions to engage in environmental reporting, someinternational organisations have produced environ-mental initiatives. This study considers a range ofthese initiatives, put forward by different organisa-tions as an attempt to aid the development of socialand environmental disclosures. The question,which the study attempts to answer, is whetherthese initiatives help corporations to overcome theobstacles preventing the production of moredetailed environmental reports.� 2005 Elsevier Ltd. All rights reserved.

702 Europe

Keywords: Corporate social reporting, Environ-mental management system, Independent verifica-tion, Environmental Auditing, Environmentalindicators

Introduction

Environmental issues present a number of challengesfor companies. One particular aspect is the disclosureof the issues to a variety of groups. This is particularlytrue, in the light of growing pressure from stakehold-ers (such as, investors, customers and shareholders)on companies to improve their performance in thisarea. This in turn increases the importance of environ-mental disclosure, especially elements which reporton the financial impacts of environmental matters.The need for consistency has provided a motiva-tion for international organisations to provide frame-works to improve the reporting of environmentalissues.

an Management Journal Vol. 23, No. 6, pp. 702–716, December 2005

ENVIRONMENTAL INITIATIVES

Awareness of environmental issues has been risingduring the last 20 years and environmental pressuregroups have been growing in most countries. A num-ber of countries have environmental laws and regu-lations to protect the environment. These lawsimpose sanctions on offending companies; therefore,environmental issues may have a material effect oncompanies either directly or indirectly. Consider forexample, in the 1960s, the asbestos industry soldproducts that caused health damage in the 1980sand 1990s. Today, asbestos as a product is mostlyphased out and in some cases insurance companies(which have not caused the damage) are having tofoot the financial bill. The consequent financial liabil-ities for pollution, illnesses, and clean up liabilitiesfor asbestos are estimated to be $2 trillion alone inthe U.S. (Schaltegger, et al., 1996).

Among the major disasters in the 1980s were Bhopal(Union Carbide), Schweizerhalle (Sandoz), andPrince William Sound (Exxon), all of which had sub-stantial financial consequences for the companies in-volved (Patten, 1992). In 1984 a cloud of poisonousmethyl iso-cyanate leaked from union Carbide’s Pes-ticide Plant, located on the outskirts of Bhopal, India.Its effect on human life was devastating with approx-imately 4,000 deaths and 200,000 injuries. The finan-cial impact was also pronounced and virtuallyimmediate. Within five trading days of the chemicalleak the market value of Union Carbide’s commonstock fell approximately 27.9% from US $ 3,443 mil-lion to US $ 2,483 million (Balcconire and Patten1994). On March 24, 1989 Oil Tanker Exxon Valdezran aground in Prince William Sound on Alaska’sWest Coast. Forty million litres of crude oil spilledinto the sea, causing enormous damage to the marineflora and fauna $16.5 billion: ($3.5 million for cleanup, $1.5 million in compensation and the rest aspunitive penalties). (Patten, 1992, Schaltegger et al.,1996). In the USA, a legislative Act of 1980 [referredto as the ‘‘Superfund Law’’], enables the US Environ-mental Protection Agency (EPA) to enforce landfillremediation by companies. The EPA can also requireany person or company involved to carry the total ofall remediation costs, no matter what proportion therespective party has actually caused (Roussey, 1992).

In 1992, Monsanto Company made a provision forliabilities to clean up waste sites, which was almost83% of its 1991 net income (McMurray, 1992). During1990, Atlantic Richfield Company (ARCo) added$220 million to its reserves relating to future environ-mental clean up costs. On December 31, 1990, suchreserves totaled $737 million (Roussey, 1992, P. 51).Even banks, in the US, which have given mortgagesor which manage closed properties can be held lia-ble. The costs of cleaning up superfund sites were ex-pected in 1993 to exceed $500 billion in the next 40 to50 years (EIU, 1993).

The US Environmental Protection Agency (EPA) or-dered in 1991 a major manufacturer of electronic

European Management Journal Vol. 23, No. 6, pp. 702–716, December 20

parts to pay an estimated $14.9 million to clean a con-tamination site in upstate New York (Roussey, 1992,P. 48). In 1993, the E. I. Dupont de Nemours andcompany spent approximately $500 million for capi-tal projects related to environmental goals and envi-ronmental expenses were about $1 billion (Shields,and Boer, 1997). Also, the management of AmocoYork town refinery estimated that its environmentalcosts were approximately 3% of operating costs,but the environmental costs were determined to beapproximately 22% of operating costs (Shields andBoer, 1997).

It can be argued that environmental risk is one areaof risk that has grown in importance and can be sum-marized as follows:

v Fines for pollution of land, water, or air.v Penalties may be imposed on a company.v Clean up costs for land sites.v Liability for disposal of hazardous wastes.v System breaks down allowing environmental

problems to occur.v Loss of employee time and / or employee law

suits due to safety hazards.v Product liability suits or recall costs.v Loss of the public confidence (damaged reputa-

tion or corporate image).v Loss of market share when environmental inci-

dents occur.v A company may lose its license or be shut down

(Flesher, 1996; Specht, 1992; Natale and Ford,1995; Gray, et al., 1993).

Companies need to be able to respond to environ-mental challenges effectively. Where they faceincreasing pressures from the public to demonstratesocial responsibility towards the environment, manycompanies seek to confirm their social responsibilityby using social and environmental reports (Hoog-hiemstra, 2000; Elkington, 1997; Adams et al., 1998;Patten, 1992; Gray et al., 1995). Moreover, a varietyof studies (Epstein and Freedman, 1994; Patten,1992; Gamble et al., 1995; Neu et al., 1998; Tilt, 1994;Mastrandonas and Strife, 1992; Deegan and Rankin,1999) argue that a number of groups who use pub-lished annual reports actually take environmentalperformance into account and environmental infor-mation is material for them. However, legitimacytheory provides an explanation of why a number ofcompanies may need to engage in environmental dis-closure and how these companies use suchdisclosure.

Dowling and Pfeffer (1975, p. 27) point out that ‘‘theorganization can attempt, through communication,to alter the definition of social legitimacy so that itconforms to the organization’s present practices, out-put and values or the organization can attempt againthrough communication, to become identified withsymbols, values, or institutions which have a strongbase of social legitimacy’’.

05 703

ENVIRONMENTAL INITIATIVES

Gray et al., (1993, p. 3) defined corporate socialreporting as ‘‘the process of communicating the so-cial and environmental effects of organizations’ eco-nomic action to particular interest groups withinsociety and to society at large’’.

Companies through the process of communication(environmental and social reporting), may seek toinfluence the public’s perception towards their oper-ations. They attempt to create a good image andmake self-congratulatory claims (Patten, 1992; Dee-gan and Rankin, 1996, 1997, 1999).

Hooghiemstra (2000) argues that companies use cor-porate social reporting as a corporate communicationinstrument. The main aim of this instrument is toinfluence people’s perceptions of the company andinfluence corporate image or reputation. Elkington(1997) points out that corporate social reporting isviewed as a public relations vehicle designed to offerreassuranceand tohelpwith feel-good imagebuilding.

Deegan et al., (2000) argue that companies use socialdisclosure as a useful device to reduce the effectsupon a corporation of events that are perceived tobe unfavorable to a corporation’s image. Gray et al.(1995) argue that companies use their social reportsto construct themselves and their relationships withothers as they strive to create and maintain the con-ditions for their continued profitability and growth.The authors pointed out that corporate social reportsserve to rationalize and justify the corporate entitynot merely describing effective management, butlegitimizing corporate power and maintaining confi-dence of the public. Adams et al. (1998) report thatUK financial executives see the most important roleof annual reports as being to help to improve the im-age or reputation of the company and UK companiesuse the report as a means of advertising their socialresponsibility.

Environmental reporting may give companies theopportunity to gain many benefits for example thereport of KPMG (1997, pp. 15–17) states that:-

‘‘many business opportunities arise from good envi-ronmental practice. These include the marketing ben-efits arising from reputation for environmental careand improving public relations for the company’’.Therefore, this may encourage other companies toengage in environmental reporting.

It can be argued that the need for social and environ-mental disclosure stems from:-

v The increase of environmental regulations andpressure groups who ask for clean air, clean waterand sustainable development. Also these groupshave a right to know about the social and environ-mental implications of an organization’s opera-tions at all times.

704 Europe

v The increase of environmental risks.v The desire of a company to improve image or gain

marketing benefits by using social environmentaldisclosure to impact on the public’s perceptiontowards companies’ operations.

However, environmental disclosure of companies isstill low. A number of companies prefer not to en-gage in environmental reports because these compa-nies may face obstacles to produce detailedenvironmental reports. A number of environmentalinitiatives are established to help companies to pro-duce such reports. The next section presents someof these initiatives to recognize whether these initia-tives can assist companies to produce environmentalreports.

A Review of Key Environmental Initiatives

The British Standard (BS 7750)

In 1991, the British Standards Institutions (BSI) is-sued BS 7750 which is a specification for an environ-mental management system to preventenvironmental damage by focusing on the use ofenvironmental auditing (Rezaee, et al. 1995). BS7750 was developed as a response to concern aboutenvironmental risks and damage (both real and po-tential). Compliance to the standard is voluntaryfor companies, and complements required compli-ance to statutory legislation (http://www/quality.co.uk/bs7750,2001). BS 7750 helps to put in place asystem, which is used to describe the company’senvironmental management, evaluate its perfor-mance and to define policy, practices, objectivesand targets, and provides a catalyst for continuousimprovement (http://www.quality.co.uk/bs7750),2001, p. 1). It confirms the quality of environmentalmanagement systems and the quality could be low,for example, permitting unacceptable levels of wastedischarge (Carty, 1993, p. 40). It requires that theoperation of the environmental management system‘‘should be internally audited and evaluated on aregular, pre-determined basis’’ (Maltby, 1995, p.15). Furthermore, Carty (1993) points out that BS7750 is merely an internal management system with-out external reporting requirements, but it gives afoundation for compliance with the ECO-Manage-ment and audit Scheme (EMAS). BS 7750 describesaudits as assessments of the effectiveness of the envi-ronmental management system, as well as, theachievement of environmental objectives. It recom-mends that all parts of the organisation should beexternally audited at least every three years. Also,parts of the organisation having a particular potentialto cause environmental harm or damage should beaudited at least once a year. The primary functionof an audit is to assess compliance and the effective-ness of previous corrective action. Audits may also

an Management Journal Vol. 23, No. 6, pp. 702–716, December 2005

ENVIRONMENTAL INITIATIVES

suggest remedial measures to overcome environ-mental performance (Sayre, 1996, p. 137; Wever,1996; Carty, 1993; Rezaee et al., 1995; www.qual-ity.co.uk/bs7750.htm, 2001). Sayre (1996) argues thatBS 7750 asserts that organisations must conduct theirbusiness within a structured management system,integrated with overall management activity andaddressing significant environmental effects, the sys-tem documents, procedures and instructions, speci-fies environmental objectives and consequenttargets, control documents and operations, maintainsa record of legislative, regulatory and policy require-ments. Environmental management audits and re-views are inherent in this standard.

It can be argued that BS 7750 does not establish spe-cific requirements for environmental performance, itjust requires compliance with applicable legislationwith a commitment to continuous improvement.This means companies can carry out these activitiesin different ways. Therefore, environmental informa-tion from companies, even if these companies are inthe same sector, will not be comparable. This stan-dard does not discuss the qualification of the personwho should perform these audits.

The International Organisation forStandardisation (ISO)

The International Organisation for Standardisation(ISO) formed a Technical Committee (TC 207) todevelop an international environmental standard.The result of the committee’s efforts is the ISO14000 series, which is a standard for an environ-mental management system (Sayre, 1996; ISO14001, 1996). Registration for the ISO 14000 seriesis voluntary for any company (whatever its size).Once the organisation is registered follow up envi-ronmental audits are required. These audits can becarried out by the organisations own personnel,and/or by external parties selected by the organisa-tion. In any case, the person conducting the auditshould be in a position to do so objectively andimpartially and should be properly trained(www.jrwenviro.com/ISO-guid.htm, 2001). The ISO14000 series consists of standards on environmentalmanagement systems. This series also covers manyissues concerning environmental auditing. Thereare environmental management audits, complianceaudits, and audits of environmental statements(see Table 2).

The ISO 14001 standard (1996, p. 10) defines an envi-ronmental management system (EMS) as: ‘‘The partof the overall management system that includesorganisational structure, planning activities, respon-sibilities, practices, procedures, processes and re-sources for developing, implementing, achieving,reviewing and maintaining the environmentalpolicy’’.

European Management Journal Vol. 23, No. 6, pp. 702–716, December 20

Wever (1996, p. 74) points out that:- ISO 14001defines environmental aspects as elements of acompany’s activities, products and services, whichare likely to interact with the environment anddetermines some types of data that might be useful(such as, legislative and regulatory requirements,codes of practice, emissions to air, contamination ofland,. . .).

Fredericks (1997, p. 85) states that:- the most impor-tant concept underlying the ISO 14010 and 14011environmental standards and the EMS audit guide-lines is the verification process that audits provide.The environmental auditor’s primary role is todetermine compliance or conformance—not perfor-mance.

ISO 14010 (1996, p. 19) goes on to define an envi-ronmental auditor as a person qualified to per-form environmental audits. The qualificationcriteria are specified in ISO 14012 (1996). This stan-dard deals with the necessary education, work expe-rience and training for an effective environmentalauditor, the qualification of environmental audi-tors, and the environmental auditor registrationbody.

The ISO 14000 series encourages internal and exter-nal communication. ISO 14004 (1996, pp. 18-19) statesthat an organisation can communicate environmentalinformation in a variety of ways:

v externally, through an annual report, regulatory,and government records, industry associationpublications, the media, and paid advertising;

v organisation of open days, the publication of tele-phone numbers where complaints and questionscan be directed;

v internally, through bulletin board postings, inter-nal newspapers, meeting and electronic mailmessages.

The ISO 14001 standard does not set absolute envi-ronmental performance requirements. It applies onlyto those environmental aspects, which the companycan control and over which it can be expected to havean influence. It does not itself state specific criteriafor performance (ISO 14001, 1996, p. 1). Mathewsand Reynolds (2001) state that:- ‘‘It is a peculiarityof the ISO 14001 standard that organisations may selfdeclare, thus, the verification process is not per-formed by an external verifier. There is also no regis-trar to formalise the registration. Most organisationsthat attempt ISO 14001 implementation seek externalhelp with verification and registration. This may re-late to the desire to legitimise the environmentalactivities of the organisation and enhance public per-ception of environmental performance’’. ISO 14001requires that a company establishes and maintainscompliance with five key requirements (ISO 14001,1996, p. 17, as follows:-

05 705

ENVIRONMENTAL INITIATIVES

1. Environmental policy: (a company should ensurecommitment to an Environmental ManagementSystem and define its policy).

2. Planning: (a company should formulate a plan tofulfil its environmental policy).

3. Implementation: (a company should develop thecapabilities and support mechanisms necessaryto achieve its environmental policy, objectivesand targets).

4. Checks and balances: (a company should mea-sure, monitor and evaluate its environmentalperformance).

5. Review: (a company should review and continu-ally improve its environmental management sys-tem, with the objective of improving its overallenvironmental performance).

The ECO-Management and Audit Scheme (EMAS)

In many countries, there is an increasing pressure,and in some cases legal insistence, for public report-ing of corporate environmental performance, gener-ally based on regular environmental audits. TheEuropean Community’s Eco-Management and AuditScheme (EMAS 1993) is a good example. Promul-gated in June 1993, this scheme has been adoptedby many European countries (Ralf, 1995; Coopersand Lybrand, 1995; Maltby, 1995; Hillary, 1995; Lang-ford, 1995). EMAS contains 21 articles and 5 annexes.They cover a range of issues, such as, objectives, theenvironmental statement, accreditation and supervi-sion of accredited environmental verifiers, the listof accredited environmental verifiers, and registra-tion of sites. EMAS is a voluntary registrationscheme, which enables companies to demonstrate acommitment to improving their environmental per-formance by establishing an environmental manage-ment system and reporting publicly on theirperformance (Carty, 1993).

The overall objective of the EMAS is to promote con-tinuous environmental performance improvementsof industrial activities by committing companies to:-

v establish and implement environmental policies,programmes and management systems,

v periodically evaluate in a systematic and objectiveway the performance of the site elements; and,

v provide environmental performance informationto the public (Hillary, 1995, p. 35).

Companies participating in EMAS will have to regis-ter with the national body designated for that pur-pose by each member State. In order to register, acompany must carry out an initial environmental re-view of its sites and, on the basis of this, establish anenvironmental protection system (the criteria forwhich are set out in an annex to EMAS) coveringall site activities. Companies will have to file an envi-ronmental statement (validated by authorised envi-

706 Europe

ronmental auditors). Once registered, a companywill have to have environmental audits and publishthe results. The environmental audits will have tobe carried out at least every three years and coverall of the business’s activities (Accountancy, 1992Hillary, 1995; Langford, 1995). Furthermore, underEMAS, companies will be required to have an envi-ronmental policy and an environmental manage-ment system, and to have quantifiable targets forcontinuous improvement of performance (Maltby,1995).

Fundamental to EMAS is the public environmentalstatement and its validation by accredited environ-mental verifiers. A site’s environmental statementwill include a description of the site’s activities, anassessment of all the significant environmental is-sues, a summary of figures on pollution emissions,waste, production, consumption of raw material, en-ergy and water, and noise, a presentation of the com-pany’s environmental policy and the site’sprogramme and management system, the deadlinefor the next statement, and the name of the accred-ited environmental verifier (Hillary, 1995, Carty,1993).

EMAS requires that a company has to file an environ-mental statement validated by authorised environ-mental auditors (Accountancy, 1992). Accreditedenvironmental verifiers have two clear roles. First,to check that the elements of EMAS, i.e. the environ-mental policy, the management system, pro-grammes, review and audit are in place,operational and carried out in accordance with theappropriate specifications in the annexes of EMAS.Second, as well as, checking the reliability and cover-age of the information in the environmental state-ment, the verifiers will have to validate thatinformation (details on the accreditation of environ-mental verifiers and their function are outlined in an-nex III of the regulation) (Hillary, 1995). The secondpurpose is to check the company has made provisionfor legal compliance, check that the frequency of theaudit cycle is three years or less and that it addressesenvironmental performance, and that the data in theenvironmental statement is a fair representation ofthe company performance. There are barriers forsmall companies to participate in EMAS, such as,the management time required to implement aninternal environmental management system, andthe cash costs to achieve certification and registrationof the EMAS (Coopers and Lybrand, 1995, p. 3).EMAS has a number of the weaknesses in that theprocess is voluntary, no specific performance stan-dards are laid down and no standardised report is is-sued. It does not address disclosure issues, such as,the problems of the quality of environmental infor-mation and environmental indicators. EMAS is ademanding system requiring both internal and exter-nal auditing for environmental issues, and then, topublish the results of these audits. These require-ments may have a strong impact on corporate image.

an Management Journal Vol. 23, No. 6, pp. 702–716, December 2005

ENVIRONMENTAL INITIATIVES

Therefore, many companies may not be not willingto participate in EMAS or at least, companies willestimate the commercial costs and benefits of partic-ipation before taking a decision.

The Copenhagen Charter (1999)

The Copenhagen Charter (CC) (1999) is a manage-ment guide to stakeholder dialogue and reporting.It consists of three parts. Part one concentrates onthe effects of stakeholder reporting which is usedby management as a valuable tool for improving dia-logue and communication with the company’s stake-holders. These reports aim at creating external valuefor the company in the form of stronger stakeholderrelationships and an improved corporate image orreputation. This gives the company competitiveadvantage in the form of, attracting and motivatingthe best employees, building customer loyalty andsecuring access to investor capital. Stakeholderreporting can also be seen as a form of ‘‘insurancepolicy’’ protecting the company’s reputation, therebyminimising the risk of potential financial losses in thefuture (The Copenhagen Charter, 1999). Part two ofthe Charter discusses the principles of stakeholderreporting. Laying the groundwork includes the com-mitment of top management in the area of the com-pany’s objectives and resources. The embeddingprocess includes identifying key stakeholders, strate-gies, values, critical success factors, and performanceindicators. The communication process includes pre-paring the report, publishing the report, and consult-ing stakeholders about performance and values. Thethird part of the Charter addresses ‘‘credibility instakeholder reporting’’. It involves accounting princi-ples, information relevance, and verification by anindependent party.

The responsibility for the quality and credibility ofstakeholder reporting ultimately rests with manage-ment. However, obtaining verification of the processand results from an independent party may enhanceboth quality and credibility. The verifier would reacha conclusion by assessing the relationship betweenfour factors: the subject matter, the criteria used inthe report, the process, and the quantity and qualityof evidence (The Copenhagen Charter, 1999, pp. 8–9).It can be argued that the Copenhagen Charterprovides a theoretical statement about the need forstakeholder reporting. However the absence of thecharacteristics of a conceptual framework or stan-dards in the CC can be inferred from the following:-

v It states that management will determine key per-formance indicators.

v It does not provide standards or guidance con-cerning the design of the reports.

v It ignores a number of important issues such as,how independent verification can be achievedand by whom.

European Management Journal Vol. 23, No. 6, pp. 702–716, December 20

Institute of Social and Ethical Accountability(AA1000 and AA2000)

The Institute of Social and Ethical Accountabilitylaunched the Accountability 1000 (AA1000) standardISEA (1999). The AA1000 standard provides both aframework that organisations can use to understandand improve their ethical accountability and a meansfor others to judge the validity of ethical claimsmade. Also, AA1000 focuses on securing the qualityof social and ethical accounting, auditing and report-ing. The AA1000 standard covers both internal andexternal audit. It also addresses some issues includ-ing the scope of the audit process, role of singleand multiple auditors, content, format, and languageof the audit report and audit opinion, including theconcept of ‘‘going concern’’ and qualified audit opin-ions, levels of assurance conveyed by the audit re-ports, links between AA1000 and IFAC, IASs, andthe quality control of auditors’ work. Stakeholders’engagement is crucial to each stage for buildingaccountability and trust between the organisationand stakeholders. An organisation needs to identifyits stakeholders and their requirements. This willhelp an organisation to improve the quality of infor-mation supplied to stakeholders and demonstrateclear social and ethical performance. AA2000accountability management has been built on ananalysis of the use of AA1000 and other standardstools, and an assessment of the needs expressed bycorporations and their stakeholders for quality pro-cesses of accountability management ISEA (2001).AA2000 focuses on developing five areas: innovationand learning, stakeholder engagement, managementsystems, assurance and governance, and risk man-agement. It can be argued that the AA1000 standarddoes not provide guidance or suggested content ofthe social and ethical reports. It also does not identifysocial or ethical performance indicators. There is nomethod to calculate accountability for companiesand how they may present it in their reports. It doesnot establish standards or principles for publiclyavailable environmental and social reports.

The Global Reporting InitiativeGuidelines (GRI 2000)

The GRI (2000) is a major structured guide aimed atproducing standardised disclosure of economic,environmental and social information in annual re-ports. GRI (2000) programme worked to design andbuild acceptance of a common framework for report-ing on the linked aspects of sustainability (economic,environmental and social). The GRI released theguidelines as an exposure draft for public commentand testing through the Spring of 2000. The Guide-lines have the following objectives (GRI, 2000, p. 1)to:-

v present a clear picture of the human and ecologi-cal impact of business,

05 707

ENVIRONMENTAL INITIATIVES

v facilitate informed decisions about investments,v provide stakeholders with reliable information

that is relevant to their needs,v provide a management tool to help the reporting

organisation evaluate its performance and pro-gress improvement,

v establish widely accepted external reporting prin-ciples, and

v promote transparency and credibility.

The Guidelines are intended to be applicable to anysize and type of organisation. Application of theGRI Guidelines is voluntary. Also, the GRI Guide-lines provide a framework for reporting and promot-ing comparability between reporting organisationswhilst recognising the practical considerations of col-lecting and presenting information across diversereporting organisations. The report of GRI (2000)comprises four parts:

v Part A sets out background on the need for andnature of the GRI, plus general guidance on thedesign and applicability of the Guidelines.

v Part B outlines reporting the principles and prac-tices underlying the GRI (such as, the going con-cern principle, the conservation principle, andthe materiality principle). Also, part B containsqualitative characteristics for GRI reporting (suchas, relevance, reliability, clarity, comparability,timeliness and verifiability, classification of per-formance reporting elements, ratio indicatorsand the disclosure of reporting practices).

v Part C sets out the framework for structuring aGRI report, specific content, and guidance forcompiling the various parts of the report.

v Part D consists of four annexes: 1, resources forselecting and applying indicators, 2, guidance onincremental application of the guidelines, 3, guid-ance on verification, and 4, guidance on ratioindicators.

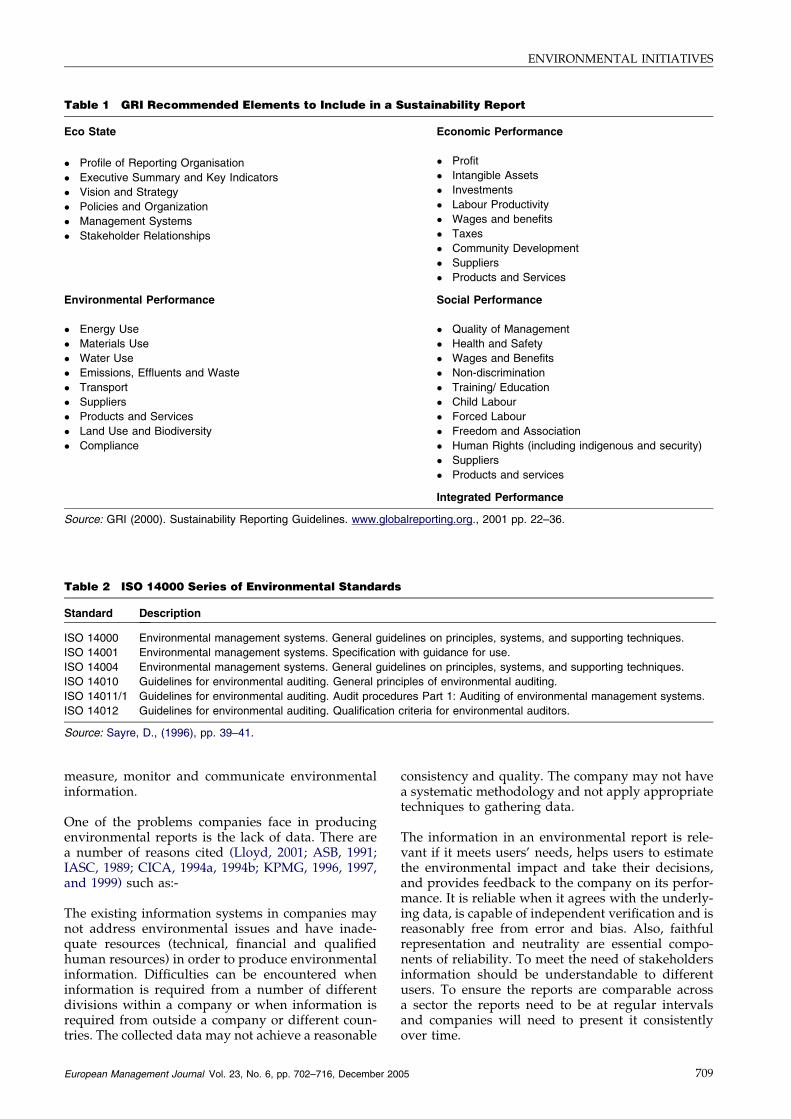

GRI (2000) has developed a set of SustainabilityReporting Guidelines on economic, environmentaland social performance. These Guidelines providesome recommendations for reporting elements. Thefollowing Table 1 identifies these elements.

The GRI Guidelines encourage companies to under-take independent verification processes for GRI re-ports. Independent verification can increase thequality, usefulness, and credibility of a company’sreporting. It considers an additional degree ofassurance about the reliability and completeness ofGRI reports. The GRI Guidelines provide approachesaimed at improving the verification processes in con-junction with independent verification. Theseinclude:-

v internal auditing of systems and procedures formeasuring, recording, and reporting performancedata,

708 Europe

v independent evaluations and commentaries byexternal experts regarding an organisation’s eco-nomic, environmental, and social performanceand/or management processes, and

v a clear statement by a member of the board ofdirectors or chief executive officer that a reporthas been prepared in accordance with the GRIGuidelines.

Whilst the GRI Guidelines do not provide a standardfor environmental performance disclosure, they doprovide generally applicable indicators such as, en-ergy (Joules), materials (Tonnes or Kilograms) to as-sist the preparer to generate information, whichshould be comparable and verified. The Guide-lines do not provide guidance for implementing datacollection, information and reporting system, or pro-cedures for preparing reports. They are silent onsome important issues such as, verification proce-dures, verifier qualification, and legal require-ments to report. The Guidelines do howeverrefer to the qualitative characteristics for organi-sations’ reports but they do not describe how com-panies can achieve these characteristics in theirreports.

Some Critical Issues ConcerningEnvironmental Initiatives

The literature available on these initiatives indicates:there is no general acceptance of the format of envi-ronmental reports and their contents, how verifica-tion should be carried out, what should beincluded in a verification statement or opinion, andwho should carry out verification (although someinitiatives mention the involvement of independentauditors concerning environmental issues). The cur-rent position leaves a difficult choice, as there areno widely accepted or global standards concerningverification of environmental reporting. There is nocommon understanding of the various approachesto verifying environmental reports or to the appro-priateness of these approaches for the different typesof subject matters environmental reports may in-clude. There are widely different users with manydifferent areas of interest. Previous initiatives havenot provided methods, or indicators to measure theenvironmental performance of companies. There isan absence of a widely accepted set of standards orguidelines for carrying out environmental reportingand verification of these reports by the independentauditor, and on the qualifying criteria for such anauditor.

The drawbacks of these initiatives can be consid-ered as a limiting factor to the development of envi-ronmental disclosure by companies. Businesseswishing to engage in environmental disclosure facea lack of reliable and credible methodologies to

an Management Journal Vol. 23, No. 6, pp. 702–716, December 2005

Table 1 GRI Recommended Elements to Include in a Sustainability Report

Eco State Economic Performance

� Profile of Reporting Organisation

� Executive Summary and Key Indicators

� Vision and Strategy

� Policies and Organization

� Management Systems

� Stakeholder Relationships

� Profit

� Intangible Assets

� Investments

� Labour Productivity

� Wages and benefits

� Taxes

� Community Development

� Suppliers

� Products and Services

Environmental Performance Social Performance

� Energy Use

� Materials Use

� Water Use

� Emissions, Effluents and Waste

� Transport

� Suppliers

� Products and Services

� Land Use and Biodiversity

� Compliance

� Quality of Management

� Health and Safety

� Wages and Benefits

� Non-discrimination

� Training/ Education

� Child Labour

� Forced Labour

� Freedom and Association

� Human Rights (including indigenous and security)

� Suppliers

� Products and services

Integrated Performance

Source: GRI (2000). Sustainability Reporting Guidelines. www.globalreporting.org., 2001 pp. 22–36.

Table 2 ISO 14000 Series of Environmental Standards

Standard Description

ISO 14000 Environmental management systems. General guidelines on principles, systems, and supporting techniques.

ISO 14001 Environmental management systems. Specification with guidance for use.

ISO 14004 Environmental management systems. General guidelines on principles, systems, and supporting techniques.

ISO 14010 Guidelines for environmental auditing. General principles of environmental auditing.

ISO 14011/1 Guidelines for environmental auditing. Audit procedures Part 1: Auditing of environmental management systems.

ISO 14012 Guidelines for environmental auditing. Qualification criteria for environmental auditors.

Source: Sayre, D., (1996), pp. 39–41.

ENVIRONMENTAL INITIATIVES

measure, monitor and communicate environmentalinformation.

One of the problems companies face in producingenvironmental reports is the lack of data. There area number of reasons cited (Lloyd, 2001; ASB, 1991;IASC, 1989; CICA, 1994a, 1994b; KPMG, 1996, 1997,and 1999) such as:-

The existing information systems in companies maynot address environmental issues and have inade-quate resources (technical, financial and qualifiedhuman resources) in order to produce environmentalinformation. Difficulties can be encountered wheninformation is required from a number of differentdivisions within a company or when information isrequired from outside a company or different coun-tries. The collected data may not achieve a reasonable

European Management Journal Vol. 23, No. 6, pp. 702–716, December 20

consistency and quality. The company may not havea systematic methodology and not apply appropriatetechniques to gathering data.

The information in an environmental report is rele-vant if it meets users’ needs, helps users to estimatethe environmental impact and take their decisions,and provides feedback to the company on its perfor-mance. It is reliable when it agrees with the underly-ing data, is capable of independent verification and isreasonably free from error and bias. Also, faithfulrepresentation and neutrality are essential compo-nents of reliability. To meet the need of stakeholdersinformation should be understandable to differentusers. To ensure the reports are comparable acrossa sector the reports need to be at regular intervalsand companies will need to present it consistentlyover time.

05 709

Table 3 Content Requirements for Environmental Reports

Basic elements to be included in environmental reports

1. A description of the company’s activities

v the impact of environmental issues on land, air, water, natural resource, and non-renewable resources.

2. Environmental policy and management commitment, such as:-

v legislative compliance

v employee involvement

v natural resource conservation

v health and safety

v environment protection

3. Plans and targets, such as:-

v company commitment

v continually improving environmental performance

v reducing the level of pollution(air emissions, water, energy and effluent discharges)

4. A description of the environmental management systems

v how the company achieves its objectives

v how the company provides information to meet its stakeholders’ requirements

v what are the company capabilities (e.g. technology, programs, training and procedures)

v the mechanisms for continuous improvement

v details of the methodology, i.e., ways, processes and procedures, which control the process of producing information

5. Quantitative data on environmental performance can be categorised into:-

(a) non-financial data, such as:-

v waste disposal

v emissions into air, land and water

v accidents and incidents

v energy consumption

(b) financial data, such as:-

v environmental expenditures and costs

v environmental provisions for liabilities and risks

v estimation of environmental contingencies

v capitalisation of costs

v remediation costs

(c) environmental indicators

v description of the types of environmental indicators and description of the reasons for – their use

(d) Description of the methodology and ways used for collecting data and information in the report

6. Environmental audits

(details of environmental audits undertaken, such as, the type of audit, the purpose, scope and procedures of auditing)

7. Environmental improvements achieved, such as:-

v reducing the level of pollution (air-water-land)

v repairing environmental damages

8. Negative impacts, such as:-

v fines and penalties

v information about poor performance

v prosecutions and accidents

v breaches of regulatory requirements

v details of corrective actions

9. Independent verification (third party)

independent opinion about many issues, such as:-

v the fairness of the statements in the environmental report

v compliance with policies and procedures

v the effectiveness of the environmental management systems

v the methodology, scope, procedures and process, which relate to environmental audits and collecting evidence of auditing

v description of the scope of responsibility

v the qualifications of a third party

10. Other information, such as:

v an opportunity to cover other useful information about environmental issues

Source: Authors.

ENVIRONMENTAL INITIATIVES

The accuracy of data will need to be audited,checked, and verified. This can be difficult, as there

710 Europe

will be a need to translate scientific and technicaldata into understandable indicators. There is a need

an Management Journal Vol. 23, No. 6, pp. 702–716, December 2005

Table 4 FEE Environmental Reporting

Assumptions and principles Qualitative characteristics of environmental reporting

1. The entity assumption

2. The accruals basis of accounting

3. The going concern assumption

4. The materiality principle

1. Relevance

2. Reliability

3. Clarity

4. Neutrality

5. Completeness

6. Prudence

7. Comparability

8. Timeliness

9. Credibility

Source: (FEE), (2000), pp. 15–25.

Table 5 CICA Criteria in Environmental Reporting

Key criteria Implications for environmental reporting

1. Comparability

2. Completeness

3. Consistency

4. Materiality

5. Neutrality

6. Relevance

7. Reliability

8. Timeliness

9. Understandability

v Industry standards / benchmarks

v Compliance with standard

v Disclosure should cover the whole area of environmental aspects

v The basis for measurement and disclosure should remain consistent over time

v The level of aggregation of data must be considered in

the light of impact on the environment

v Disclosure is free from bias

v Environmental disclosures are relevant for users

v Disclosure should be independently audited

v Disclosure on a regular basis

v Disclosure is understandable for different users

Additional criteria might include

v Accessibility

v Degree of Commitment

v Subsidiarity

v Status

Source: The CICA, (1994), pp. 175–177.

ENVIRONMENTAL INITIATIVES

to identify the best way to present data and informa-tion in environmental reporting and choose the suit-able level for data aggregation.

Environmental indicators and benchmarks are essen-tial for credibility in environmental reporting. Theymake the information easier to interpret and under-stand for different users. Environmental indicatorsallow meaningful comparisons between companies’performance (CICA, 1994b; GRI, 2000) The most re-cent set of environmental indicators is provided inannex 4 of GRI (2000). There are difficulties in gath-ering data and suitable information. Uncertaintiesare inherent in how to estimate and measure the im-pact of environmental issues in some areas e.g. whenaccruing costs for future site restoration and deter-mining contingent liabilities. The indicators may bebased on estimates and may change because theassumptions and calculations underlying the esti-

European Management Journal Vol. 23, No. 6, pp. 702–716, December 20

mates can be very complex. Questions remain ofhow to choose suitable scientific and technical waysto calculate the indicators and what is the appropri-ate benchmark of environmental performance?

Whilst it has been shown, there is no generally ac-cepted framework for the contents of environmentalreporting, some initiatives have suggested potentialcontents of reports. For example, under GRI, envi-ronmental reporting consists of nine parts. IAPC(1995) suggests examples of contents of reporting,such as: a description of the company’s activities,environmental policy, EMS, accounting policies,quantitative performance data. CICA (1994b), onthe other hand, points out that environmental report-ing consists of: organisation’s profile, environmentalpolicy, activities and targets, EMS, environmentalperformance analysis, glossary, and third party opin-ion (Table 1).

05 711

Principles of

GRI reporting

Qualitative

characteristics for

GRI reporting

v The reporting entity principle

v The reporting scope principle

v The reporting period principle

v The going concern principle

v The conservation principle

v The materiality principle

v Relevance

v Reliability

v Clarity

v Comparability

v Timeliness

v Verifiability

ENVIRONMENTAL INITIATIVES

The Copenhagen Charter (1999) refers to the contentsof environmental reporting as including a briefpresentation of the company, an overview of themarket in which the company operates, its strategyand values, operational actions, targets and results,accounting principles, the verification statement(Table 2).

The two reports AA1000 and AA2000 refer to some keyissues concerning environmental reporting, such as,(stakeholder engagement, planning, accounting andauditing, communication, verification) without dis-cussing contents of reports as a whole. KPMG(1999, 1997, 1996) in a survey of environmentalreporting practice refer to contents of reporting, suchas:- environmental policy statement, EMS, qualitativedata on environmental performance, plans and tar-gets, bad news, auditing, independent verification.It is possible to pull the requirements together asshown in Table 3.

Although there is no consensus on what should beincluded in a verification statement or opinion,there is a wide acceptance of the importance toverify environmental reports by a third party. Sincesome stakeholders tend to be inherently suspiciousof voluntary disclosure by companies, reportingcompanies must convince their stakeholders thatthe data and information in the report are reliable.Independent verification by a third party can en-hance the quality, usefulness, and credibility ofinformation used within the reporting companies,(CICA, 1994a, 1994b; KPMG, 1999, 1997, 1996; GRI,2000). There is no standard format for a third partyopinion, but there are a number of studies, whichsuggest examples of information which shouldbe covered by a third party (CICA, 1994a, 1994b;GRI, 2000; ISO14000; EMAS; KPMG, 1999, 1997,1996; IAPC, 1995; Hillary, 1995; Langford, 1995)such as:

v The fairness of the statements in the environmen-tal report.

v Compliance with legal requirements.v Risks and uncertainty involved in preparing the

environmental information.v Environmental risks and contingent liabilities.

Unlike financial reporting, environmental report-ing has not been guided by widely acceptedstandards and principles that can be used in report-ing environmental information. In the absence ofthese standards and principles, there are vari-ous opinions on this matter. One approach sug-gested by FEE (2000) believes that someassumptions, principles and qualitative characteris-tics, which are used in financial reporting to makepublished information useful and credible, can beappropriately modified for environmental reports.Its arguments can be summarised in the followingTable 4:

712 Europe

v The Canadian Institute of Chartered Accountantssuggests some further criteria should be consid-ered in environmental reporting in the followingTable 5:-

v The GRI (2000) suggested the following broadprinciples:

As can be seen from these, there is no agreement onprinciples and standards for environmental reports.The absence of professional guidance relating toenvironmental issues is considered a significant bar-rier limiting some companies involved in environ-mental disclosure. Gray et al., (1998, p. 303) statethat ‘‘the increasing concern with stakeholders,growing anxiety about business ethics and corporatesocial responsibilities and the increasing importanceof ethical investment have all raised the need fornew accounting and accounting methods through,which organisations and their participants can ad-dress such matters’’.

One of the barriers to developing environmentalreporting is the limited level of public demand forenvironmental information. The reasons may bedue to the fact that environmental awareness is stilllow, people need to become aware of many issueson how to protect the environment and its impacton business. Environmental awareness is challengingcompanies to re-examine their operational processesand products. Companies may need time to be readyfor this challenge. There is also a need to increasestakeholders’ engagement with their companies, thismay in turn encourage companies to produce envi-ronmental reports. The value of stakeholders is akey determinant of a company’s’ success. It is diffi-cult to imagine a company that is seeking to have agood corporate image and trust in its relations with-out achieving its stakeholders’ needs. (The CC 1999,CICA, 1994a, 1994b; http://www.stakeholder.dk,2002; Lloyd, 2001).

Because environmental reports are voluntary, manycompanies may choose not to disclose environmentalinformation to avoid attracting public attention,which may impact on their reputation or image

an Management Journal Vol. 23, No. 6, pp. 702–716, December 2005

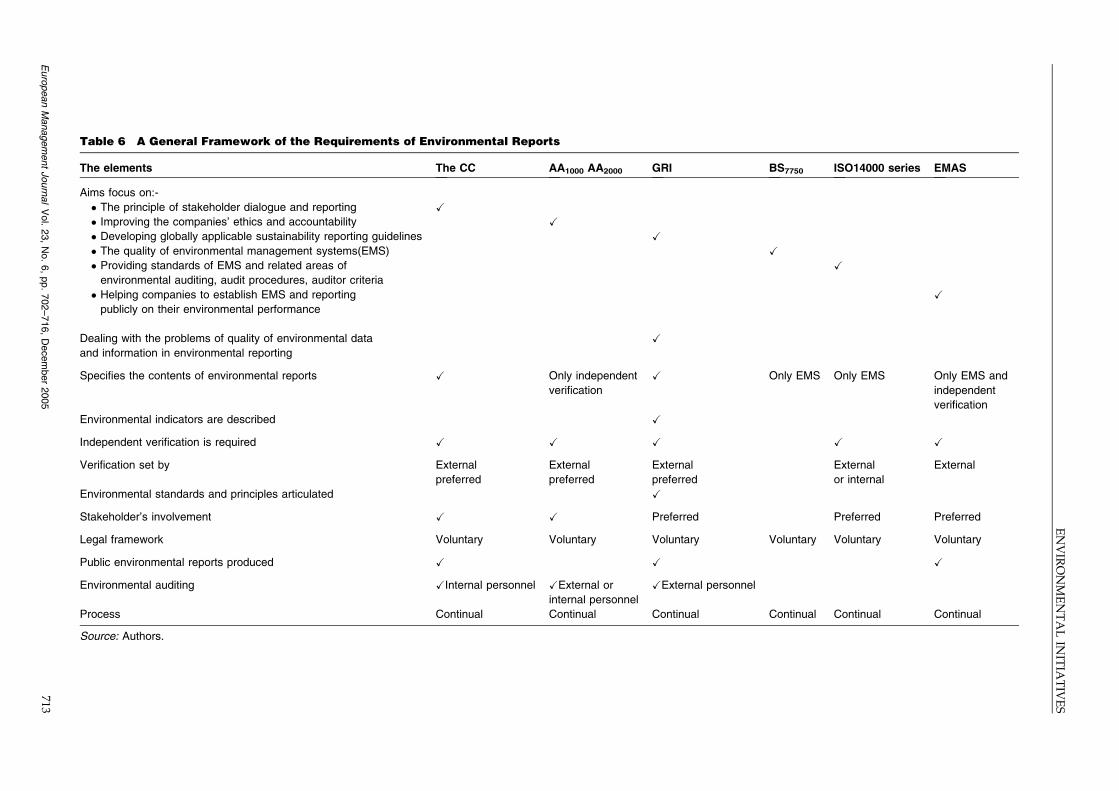

Table 6 A General Framework of the Requirements of Environmental Reports

The elements The CC AA1000 AA2000 GRI BS7750 ISO14000 series EMAS

Aims focus on:-

� The principle of stakeholder dialogue and reporting X

� Improving the companies’ ethics and accountability X

� Developing globally applicable sustainability reporting guidelines X

� The quality of environmental management systems(EMS) X

� Providing standards of EMS and related areas of

environmental auditing, audit procedures, auditor criteria

X

� Helping companies to establish EMS and reporting

publicly on their environmental performance

X

Dealing with the problems of quality of environmental data

and information in environmental reporting

X

Specifies the contents of environmental reports X Only independent

verification

X Only EMS Only EMS Only EMS and

independent

verification

Environmental indicators are described X

Independent verification is required X X X X X

Verification set by External

preferred

External

preferred

External

preferred

External

or internal

External

Environmental standards and principles articulated X

Stakeholder’s involvement X X Preferred Preferred Preferred

Legal framework Voluntary Voluntary Voluntary Voluntary Voluntary Voluntary

Public environmental reports produced X X X

Environmental auditing XInternal personnel XExternal or

internal personnel

XExternal personnel

Process Continual Continual Continual Continual Continual Continual

Source: Authors.

ENVIRONMENTALIN

ITIA

TIV

ES

EuropeanManagementJournal

Vol.

23,

No.

6,

pp.

702–716,

Decem

ber

2005

713

ENVIRONMENTAL INITIATIVES

and generate problems with governmental agencies.Companies may prefer not to engage in environmen-tal reports because it may be expensive and require arange of different resources (such as, financial-tech-nical-qualified persons). The lack of resources maybe considered a barrier for some companies, espe-cially, small companies, to engage in environmentalreports. (KPMG, 1999, 1997, 1996; CICA, 1994a,1994b). Developing environmental reports may even-tually need legal requirements to make reportsmandatory.

In order to pull the analysis of the initiatives withinthe literature together, a general framework of therequirements of environmental reports has been pro-duced as shown in Table 6. This Table effectivelysummarises all the necessary elements suggested inthe literature. This framework has then been usedto identify in what way the initiatives have made acontribution.

Conclusions

It has become a requirement for companies to ad-dress environmental issues in order to comply withregulation in some countries, maintain customers,and thrive in an ever more critical global economy.A number of international organisations have madeefforts to help the development of social and envi-ronmental disclosures such as, CC (1999), AA1000and AA2000, GRI 2000, BS7750, ISO 14000, andEMAS. Despite all of these efforts, there are still nogenerally accepted rules and principles concerningmany issues. These issues include what should bethe contents of environmental reports, which indica-tors should be used in reporting, as well as, the prob-lems of collecting and analysing environmental data,other concerns include how verification of environ-mental reports should be carried out, the absenceof professional standards and finally guidelines forenvironmental reporting. All these drawbacksactually provide companies with an excuse to avoidenvironmental disclosure. Therefore, there is aneed to achieve coherent and integrated efforts toachieve a generally accepted framework of environ-mental reports by cooperation between accountancybodies, academics and practitioners. The require-ments of this framework need to cover thefollowing:-

1. Identifying the aims of environmental reports.2. Addressing the problems of achieving the quality

of environmental data and information in environ-mental reports.

3. Determining the contents of environmentalreporting.

4. Suggesting environmental indicators, which canbe used in environmental reporting to be compa-rable between different companies.

714 Europe

5. Providing generally accepted environmental stan-dards and principles.

6. Specifying a number of issues concerning theindependent verification such as, how it will beachieved and by whom.

7. Encouraging stakeholders’ involvement in theircompanies’ policies towards environmentalmatters.

8. Identifying legal and detailed requirements forenvironmental reports by companies.

9. Encouraging companies to conduct environmentalauditing and to engage in publicly environmentalreports.

More impetus given to produce a coherent generallyaccepted framework would potentially improve boththe supply of, and the demand for environmentalreports.

References

Accountancy, ‘‘European Briefing’’, June 1992, pp. 58–59.

Adams, C.A., Hill, W. and Roberts, C. (1998) CorporateSocial Reporting Practices in Western Europe: Legit-imating Corporate Behavior. British Accounting Review30(1), 1–21.

(ASB) Accounting Standards Board, ‘‘The Objective ofFinancial Statements and the Qualitative Characteris-tics Draft-Statement Principles’’, (London, ASB Lim-ited, July 1991).

Carty, P. (1993). Standard Sets Environmental Goals Accoun-tancy (May), 40–41.

(CICA) The Canadian Institute of Chartered Accountants,‘‘Environmental Stewardship Management Account-ability and the Role of Chartered Accountants’’,(Toronto, CICA, 1994a).

(CICA) The Canadian Institute of Chartered Accoun-tants, ‘‘Reporting on Environmental Performance’’,(Toronto, CICA, 1994b).

Coopers and Lybrand, ‘‘Eco-Management and AuditScheme (EMAS)-Positioning your Business’’, (London,Business in the Environment-Coopers and Lybrand,1995).

Deegan, C. and Rankin, M. (1996) Do Australian Compa-nies Report Environmental News Objectively? AnAnalysis of Environmental Disclosures by FirmsProsecuted Successfully by the Environmental Protec-tion Authority. Accounting, Auditing and AccountabilityJournal 9(2), 50–67.

Deegan, C. and Rankin, M. (1999) The EnvironmentalReporting Expectations Gap: Australian Evidence.British Accounting Review(31), 313–349.

Deegan, C., Rankin, M. and Voght, P. (2000) Firms’Disclosure Reactions to Major Social Incidents: Aus-tralian Evidence. Accounting forum 24(1), 101–130.

Dowling, J. and Pfeffer, J. (1995) Organisational legitimacysocietal values and organisational behavior, PacificSociological Review, Vol. 18, no. 1, January, pp. 122–136.

(EIU) the Economist Intelligence Unit & American Inter-national Underwriters, (1993), ‘‘EnvironmentalFinance. Evaluation Risk and Exposure in the1990s’’, New York: EIU.

Elkington, J. (1997) Cannidals with Froks-the Triple Bottom-Line. Oxford, Capstone.

Epstein, M. and Freedman, M. (1994) Social Disclosure andthe Individual Investor. Accounting, Auditing andAccountability Journal 7(4), 94–109.

an Management Journal Vol. 23, No. 6, pp. 702–716, December 2005

ENVIRONMENTAL INITIATIVES

FEE (Federation des Experts Comptables Europeens),(2000). ‘‘ Towards a Generally Accepted Frameworkfor Environmental Reporting’’ a Paper Issued by theEnvironmental Working Party of the European Fed-eration of Accountants, Brussels, (FEE), July.

Fredericks, Isis, ‘‘ISO 14001 Lead Auditing Handbook’’,Vancouver. B. C., Management Alliance, 1997.

Flesher, D. (1996) Internal Auditing Standards and Practices-AOne Semester Course. The Institute of Internal Auditors,New York.

GRI (2000) Sustainability Reporting Guidelines. www.globalreporting.org., 2001 pp. 22–36.

Gamble, G., Hsu, K., Kite, D. and Robin, R. (1995)Environmental Disclosures in Annual Reports and 10Ks: An Examination. Accounting Horizons 9(3), 34–54,September.

Gray, R., Kouhy, R. and Lavers, S. (1995) Corporate Socialand Environmental Reporting: A Review of the Liter-ature and a Longitudinal Study of UK Disclosure.Accounting, Auditing, and Accountability Journal 8(2),47–77.

Gray, R., Bebbington, J. and Walters, D. (1993) Accountingfor Environment-The Greening of Accountancy, Part II’’.The Chartered Association of Certified Accountants,Paul & Chapman Publishing Ltd., London.

Gray, R., Collison, D., and Bebbington, J., (1998). ‘‘Envi-ronmental and Social Accounting and Reporting’’, inFinancial Reporting Today: Current and EmergingIssues’’, (London, I CAEW, 1998).

Hillary, R. (1995) Developments in Environmental Audit-ing. Managerial Auditing Journal 10(8), 34–39.

Hooghiemstra, R. (2000) Corporate Communication andImpression Management — New Perspectives WhyCompanies Engage in Corporate Social Reporting.Journal of Business Ethics(27), 55–68.

(IAPC) International Auditing Practices Committee, ‘‘TheAudit Profession and the Environment’’, DiscussionPaper Issued by the International Federation ofAccountants, (New York, (IFA), 1995).

(IASC) International Accounting Standards Committee,‘‘Framework for the Preparation and Presentation ofFinancial Statements’’, (London, IASC, 1989).

KPMG, ‘‘International Survey of Environmental Report-ing’’, http://www.wimm.nl/publications.kpmg1999.pdf, 1999.

KPMG, (1996). ‘‘International Survey of EnvironmentalReporting’’, (London, KPMG, 1996).

KPMG, (1997). ‘‘UK Survey of Environmental Reporting’’,(London, KPMG, 1997).

Langford, R. (1995) Accountants and the Environment.Accountancy, 128–129.

Lloyd, K., (2001). ‘‘The Role of Corporate EnvironmentalReporting in a Canada Information System for theEnvironment Final Report’’, Straton Inc., www.stratos-sts.com.

Maltby, J. (1995) Environmental Audit: Theory andPractices. Managerial Auditing Journal 10(8), 15–26.

Mathews, M., Reynolds, M., ‘‘Structures for Non-Tradi-tional Accounting Disclosures in the 21stCentury’’,(Massey University, New Zealand, UnpublishedPaper Presented at Northumbria University, UK,2001).

McMurray, S., (1992). ‘‘Monsanto Doubles Liability Provi-sion for Treating Toxic Waste to $ 245 Million’’, WallStreet Journal (WSJ), March 23, A7.

Natale, S. and Ford, J. (1995) The Social Audit and Ethics.Management Auditing 9(1), 29–33.

Neu, D., Warsame, H. and Pedwell, K. (1998) ManagingPublic Impressions: Environmental Disclosures inAnnual Reports. Accounting Organizations and Society23, 265–282.

Patten, D. (1992) Intra-Industry Environmental Disclosuresin Response to the Alaskan Oil Spill: A Note on

European Management Journal Vol. 23, No. 6, pp. 702–716, December 20

Legitimacy Theory. Accounting, Organizations and Soci-ety 17(5), 471–475.

Ralf, B. (1995) Environmental and Social Impact Assessment.London, International Association for Impact Assess-ment, pp. 283–303.

Rezaee, Z., Szendi, J. and Aggarwal, R. (1995) CorporateGovernance and Accountability for EnvironmentalConcerns. Managerial Auditing Journal 10(8), 27–33.

Roussey, R.S. (1992) Practice Note: Auditing Environmen-tal Liabilities. Auditing: A Journal of Practice and Theory,Spring 11(1), 47–57.

Sayre, D. (1996) Inside ISO 14000 the Competitive Advantageof Environmental Management. Lucie Press, London.

Schaltegger, S., Muller, K. and Hindrichsen, H. (1996)Corporate Environmental Accounting. John Wiley &Sons, England.

Shields, D. and Boer, G. (1997) Research in EnvironmentalAccounting. Journal of Accounting and Public Policy16(2), 117–125, Summer.

Specht, L.B. (1992) The Auditor SAS 54 and EnvironmentalViolations. Journal of Accountancy (December), 69–79.

The Copenhagen Charter, http://www.stakeholder.dk,1999.

The European Standard ISO 14012, ‘‘Guidelines for Envi-ronmental Qualification Criteria for EnvironmentalAuditors’’, Published (in English), (London, BritishStandards Institute BSI, 1992).

The European Standard EN ISO 14010, ‘‘Guidelines forEnvironmental Auditing General Principles’’, Pub-lished (in English), (London, British Standards Insti-tute BSI, 1996).

The European Standard ISO 14001, ‘‘Environmental Man-agement Systems-Specification with Guidance forUse’’, Published (in English), (London, British Stan-dards Institute BSI, 1996).

The European Standard ISO 14004, ‘‘Environmental Man-agement Systems-General Guidelines on Principles,Systems and Supporting Techniques’’, Published (inEnglish) (London, British Standards Institute BSI,1996).

The Institute of Social and Ethical Accountability, AA1000Standard, http://www.accountability.org.uk/intro5.htm, 1999.

The Institute of Social and Ethical Accountability, AA2000Accountability Management, http://www.account-ability.org.uk/aa2000.htm, 2001.

Tilt, C. (1994) The Influence of External Pressure Groups onCorporate Social Disclosure: Some Empirical Evi-dence. Accounting, Auditing and Accountability Journal7(4), 47–72.

Wever, G. (1996) Strategic Environmental Management UsingTQEM and ISO 14000 for Competitive Advantage. JohnWiley and Sons Inc, London.

Further reading

Brown, N. and Deegans, C. (1999) The Public Disclosure ofEnvironmental Performance Information-a Dual Testof Media Agenda Setting Theory and LegitimacyTheory. Accounting and Business Research 37(1), 21–41.

Building Stakeholder Relations, http://www.stake-holder.dk, 2002.

Deegan, C. and Rankin, M. (1997) The Materiality ofEnvironmental Information to Users of AccountingReports. Accounting, Auditing and Accountability Journal10(4), 562–583.

(EMAS) Eco-Management and Audit Scheme, (2001).http://www.quality.co.uk/emas.

ISO 14001 Guidance, (http://www.jrwenviro.com/ISO-guid), 2001.

Mastrandonas, A. and Strife, P. (1992) Corporate Environ-mental Communications: Lessons from Investors.Columbia Journal of World Business(27).

05 715

ENVIRONMENTAL INITIATIVES

Milne, M. and Patten, D. (2002) Securing OrganisationalLegitimacy-an Experimental Decision Case Examin-ing the Impact of Environmental Disclosures. Account-ing, Auditing and Accountability Journal 15(3),372–405.

O’Dwyer, B., ‘‘The Sate of Corporate EnvironmentalReporting in Ireland’’, (London, Certified AccountantsEducation Trust for the Association of CharteredCertified Accountants, 2001).

ROBERT DIXON, Dur-ham Business school,Durham University, MillLane, Durham City DH13LB. E-mail: [email protected]

Robert Dixon is Professorof Management Account-ing and Deputy Deanwith research interests inenvironmental reportingand control. Currently, he

is working on health service finance and control andaccounting issues in Africa and Eastern Europe.

GEHAN A. MOUSA,Accounting Department,Faculty of Commerce,Benha University, Benha,Egypt, E-mail: [email protected]

Gehan Mousa is Lecturerin Accounting. She holds aPh.D. from DurhamUniversity.

716 Europe

The European Standard EN ISO 14011, ‘‘Guidelines forEnvironmental Auditing-Audit nProcedures-Auditingof Environmental Management System’’, Published(in English), (London, British Standards Institute BSI,1996).

What are Environmental Indicators? http://www.denrec.state.de.us/newpages/cza/whatis.htm, 2002.

World Resources 1998-1999, http://www.igc.org/wri/wr98-99/wr98-toc.htm, 2002.

ANNE WOODHEAD,Durham Business School,Durham University, MillLane, Durham City DH13LB. E-mail: [email protected]

Anne Woodhead is Lec-turer in Accounting withresearch interests in envi-ronmental reports andtheir audit, corporate gov-ernance and the role ofnon-executive directors.

an Management Journal Vol. 23, No. 6, pp. 702–716, December 2005