the roar of the tiger - first avenue · the roar of the tiger ... • weighted average holding...

TRANSCRIPT

The Roar of the

Tiger

Nick Dennis

Vision 1998...

“... to be the worlds most admired food and pharmaceutical company in

emerging markets.”

Vision 2008...

“... to be the worlds most admired branded consumer packaged goods

company in emerging markets.”

Most “admired” criteria...

Financial returns

Reputation for innovation

Ability to attract, retain and develop the best people

Strategy 2008...

• Profitable top-line growth

• Number 1 or 2 in category

• Growth via organic, acquisitions or Africa

• Virtuous circle

Tiger Brands Case Study Turning Tiger into the “P&G of Africa”

3 Investing in the highest order of value

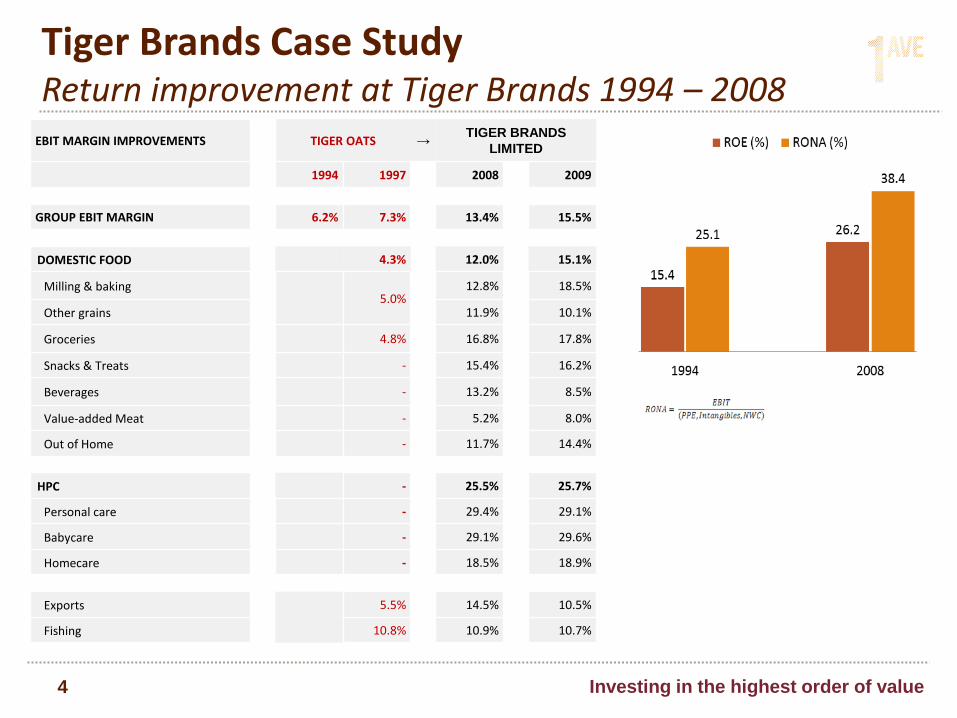

Tiger Brands Case Study Return improvement at Tiger Brands 1994 – 2008

4 Investing in the highest order of value

EBIT MARGIN IMPROVEMENTS TIGER OATS → TIGER BRANDS

LIMITED

1994 1997 2008 2009

GROUP EBIT MARGIN 6.2% 7.3% 13.4% 15.5%

DOMESTIC FOOD 4.3% 12.0% 15.1%

Milling & baking 5.0%

12.8% 18.5%

Other grains 11.9% 10.1%

Groceries 4.8%

16.8% 17.8%

Snacks & Treats - 15.4% 16.2%

Beverages -

13.2%

8.5%

Value-added Meat - 5.2% 8.0%

Out of Home - 11.7% 14.4%

HPC - 25.5% 25.7%

Personal care - 29.4% 29.1%

Babycare - 29.1% 29.6%

Homecare - 18.5% 18.9%

Exports 5.5% 14.5% 10.5%

Fishing 10.8% 10.9% 10.7%

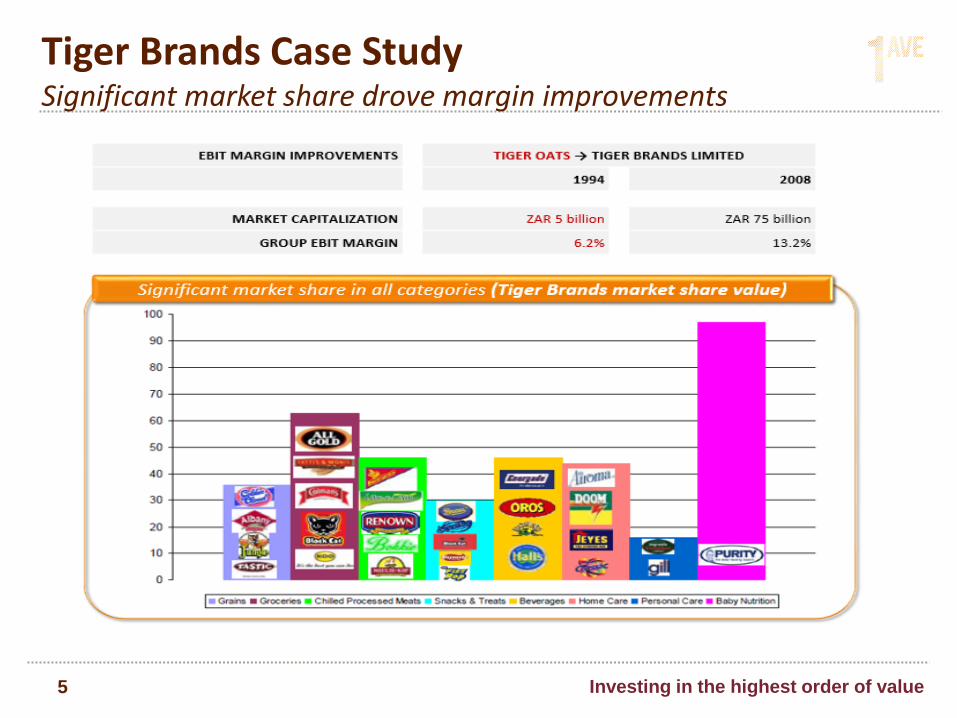

Tiger Brands Case Study Significant market share drove margin improvements

5 Investing in the highest order of value

Tiger Brands Case Study Core competency —‘value-adding’ bolt on acquisitions to augment margins

6 Investing in the highest order of value

Tiger Brands Case Study Branding capability

7 Investing in the highest order of value

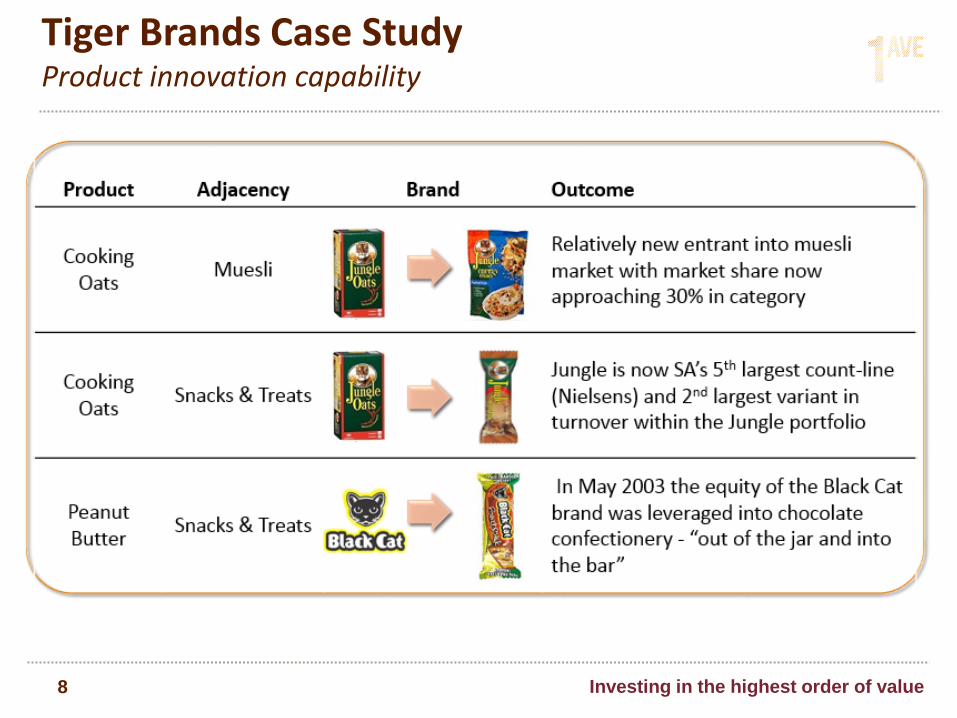

Tiger Brands Case Study Product innovation capability

8 Investing in the highest order of value

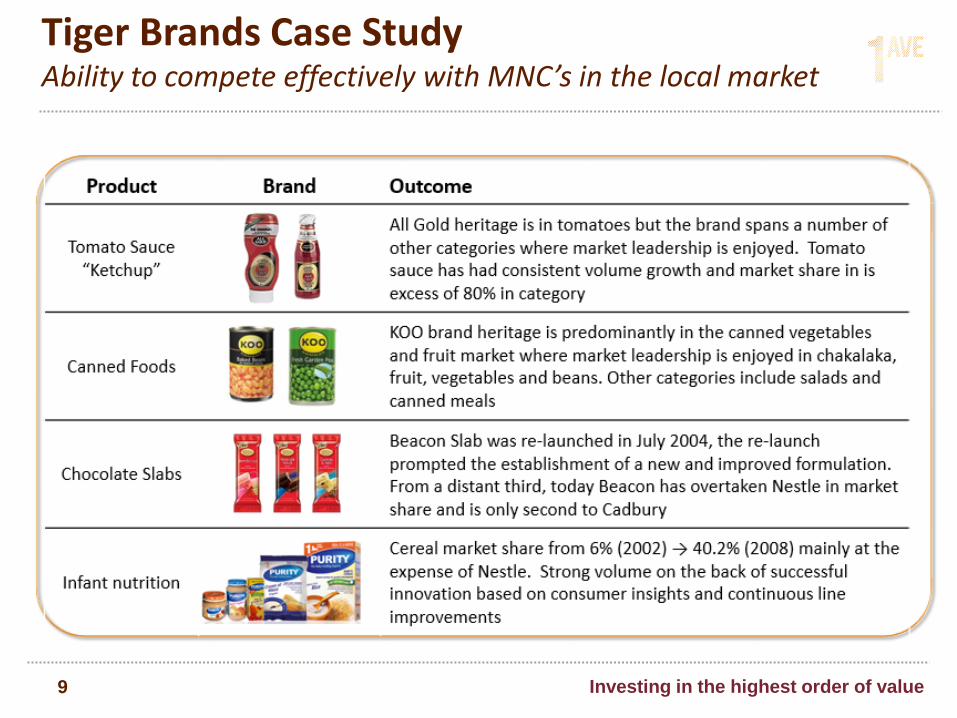

Tiger Brands Case Study Ability to compete effectively with MNC’s in the local market

9 Investing in the highest order of value

What am I up to now?

10 Investing in the highest order of value

Lodestone Brands FMCG operating company grown by acquisition

11 Investing in the highest order of value

• Lodestone Brands was founded

by the current management

team in 2009

• Raised $170 million

• Vision to build ‘’a mini P&G’’

equivalent in sub-Saharan

Africa through acquiring and

integrating branded FMCG

companies.

• Access to deep industry

expertise through well

established FMCG network

• Significant acquisition pipeline

developed

Lodestone Brands Group at a glance

12 Investing in the highest order of value

• Weighted average holding period 2.7 years since acquiring control of

each subsidiary

• Significant work done in professionalizing group since acquiring

subsidiary companies

• Meaningful on-cost without immediate payback

• Specific areas include marketing, customer, supply chain and finance

Lodestone Brands FMCG operating company grown by acquisition

13 Investing in the highest order of value

• Effective 1 June 2014, bought

out all minorities i.e. acquired

100% of each subsidiary →

enable more effective merger

synergies to be extracted

• Anticipated merger synergies to

accrue over next 24 – 36 months

and include; • Rationalization of sugar

confectionery businesses into one

business

• Field selling & merchandising → one

common agent

• Procurement aggregation

• Warehouse and logistics

aggregation

• Common ERP system

• Back office rationalisation

Lodestone Brands High level overview

14 Investing in the highest order of value

Questions?