the road to an economic miracle - financial newsletters ... · pdf fileand trusted techniques...

TRANSCRIPT

Japan 2013: One Sure-Fire Strategy from the Land of the Rising Sun

page 2

Welcome to Bull’s Eye Investor! With today’s markets swinging up and down without any rhyme or reason, it’s evident that the old rules of investing no longer apply. The tried and trusted techniques of buying and holding a blue-chip stock or – gasp – buying US government bonds have left those unwilling to change their antiquated thinking in the dust. To succeed in this new investing paradigm, you need to adapt. But that can be easier said than done, as in order to adapt and stay ahead of the curve, you also need the advice of someone with the right tools and experience.

That’s where we come in.

Here at Bull’s Eye Investor, we pin down trends to find out not where the market will be next week or the week after, but where it will be six months to several years from now. We strive to bring you not only the sectors poised to outperform, but the specific company or security that will most capitalize on this trend.

Right now, Japan is in our sights. But in order to fully understand the possibilities that lie in the Japanese markets, it’s helpful to get a brief history of the country since World War II.

The Road to an Economic MiracleAfter Japan’s defeat in World War II, the country was in shambles. The Allied powers occupied post-war Japan until 1952 and slowly helped the war-torn country transition into a democratic state. Reforms included the establishment of the Constitution of Japan, the abolition of the secret police, women’s suffrage, and the Fundamental Law of Education. This period also saw the conviction and execution of several pre-war Japanese politicians,

but Emperor Hirohito – whom many Japanese viewed as a living god – escaped prosecution, even though he was instrumental in the Japanese war effort. Even the mere prosecution of the emperor was thought to be an act that would surely destabilize Japan, so the Allies opted to keep him around, though stripping him of all material power.

This turned out to be a good move by the Allies, as Japan would emerge as one of the US’s chief trading partners, as well as a strategic military ally during the Cold

War. The “economic miracle” that rose from the ashes of post-war Japan was fostered with aid from the United States, initially through the Korean War, when American “special procurements” accounted for nearly 30% of Japanese exports.

Japan 2013: One Sure-Fire Strategy from the Land of the Rising Sun

page 3

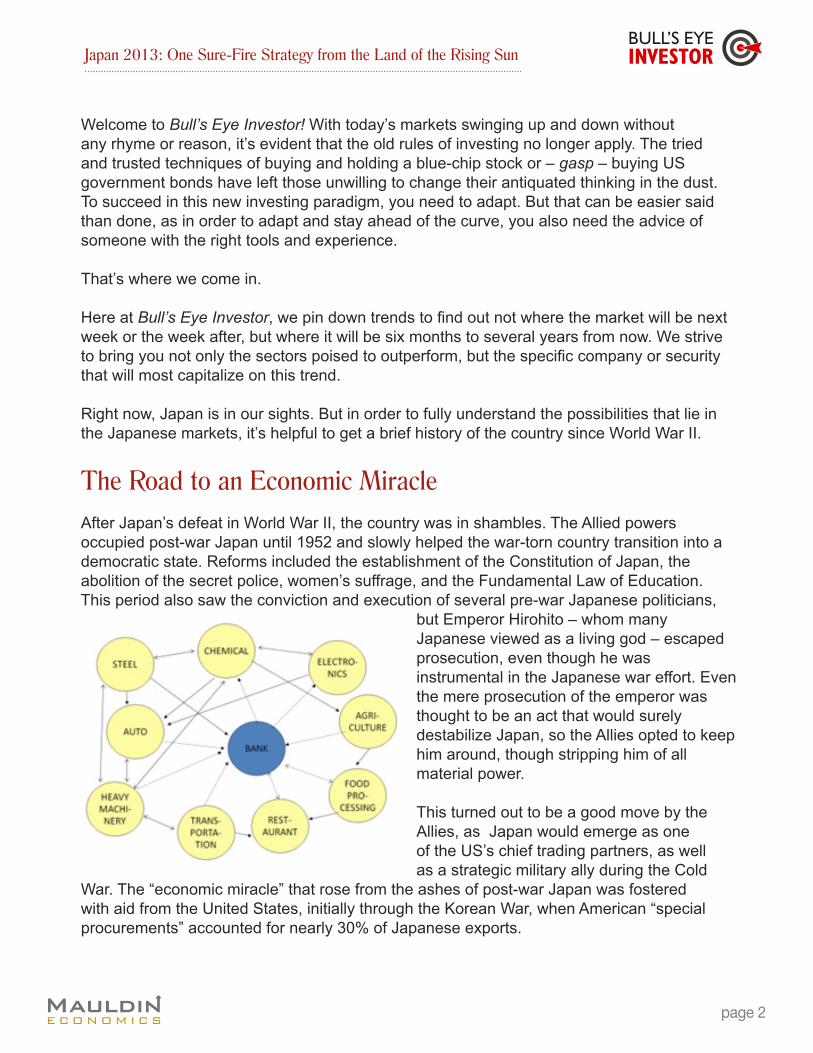

However, this miracle was chiefly fueled by the efforts of the Japanese government through the Ministry of International Trade and Industry (MITI) and the extraordinary cooperation and alignment of the keiretsu, which are organized business groups with complementary businesses and cross-shareholdings. These companies would own small portions of shares in each other’s firms centered around a core bank, thus partially insulating the companies from stock market fluctuations and takeover attempts.

For example, the likes of Sumitomo, Mitsubishi, Fuyo (Fuji), and Mitsui were built around a foundation of a bank and a trading company, but orbiting them were steel and chemical companies, automobile manufacturers, electronics firms, and life insurance companies, along with a web of other interdependent manufacturers, suppliers, and distributors. All of these companies were tied together through a complex cross-holding structure.

The keiretsu also employed another economic stabilizer known as shushin-koyo, or lifetime employment, that sought to not only provide stability in the labor market but to foster a sense of community between the company and its employees. This is often seen as a byproduct of the economic conditions in the 1920s, where major Japanese corporations began to accrue the same prestige that had traditionally been reserved for powerful feudal landowners.

“(Chalmers Johnson, 1982) The particular speed, form, and consequences of Japanese economic growth are not intelligible without reference to the contributions of the Ministry of International Trade and Industry (MITI).”

Though the keiretsu served as a source of stability in the private sector, the MITI was the main engine behind Japan’s resurgence, and it used its regulatory powers to ensure the keiretsu worked towards the common goal of getting Japan back on its feet. The MITI coordinated various industries, including keiretsu, toward a specific aim of aligning national production goals and the interests of the private sector.

One of MITI’s main policies was one of low tariffs for the import of technology. Known as the Foreign Capital Law, the rule granted the ministry power to negotiate the price and conditions of technology imports, which allowed the MITI to promote industries it deemed promising, while the low-cost imports allowed for rapid industrial growth. Eventually, the MITI was granted the ability to regulate all imports with the abolition of the Economic Stabilization Board and the Foreign Exchange Control Board in August 1952.

MITI even established the Japan Development Bank, which provided the private sector with low-cost loans. Eventually, the Japanese Development Bank introduced access to the Fiscal Investment and Loan Plan (FLIP), which was a massive pooling of individual and national savings. At the time, FLIP controlled four times the savings of the world’s largest commercial bank. This allowed FLIP to maintain an abnormally high number of Japanese construction

Japan 2013: One Sure-Fire Strategy from the Land of the Rising Sun

page 4

firms, which helped spur the country’s much-needed infrastructure development. However, there seemed to be an oversupply problem, as Japan had more than twice the number of construction firms of any nation with a comparable GDP.

These loose lending practices via the Japan Development Bank, import controls by the MITI to stave off foreign goods, and a policy of pursuing heavy industrialization led the keiretsu to focus on expanding their reach at the expense of maximizing profitability. This paradigm has left its mark on Japanese companies to this day, and was the foundation for the unimaginable asset bubble that formed in Japan’s economy over the next few decades.

Kicking into High Gear

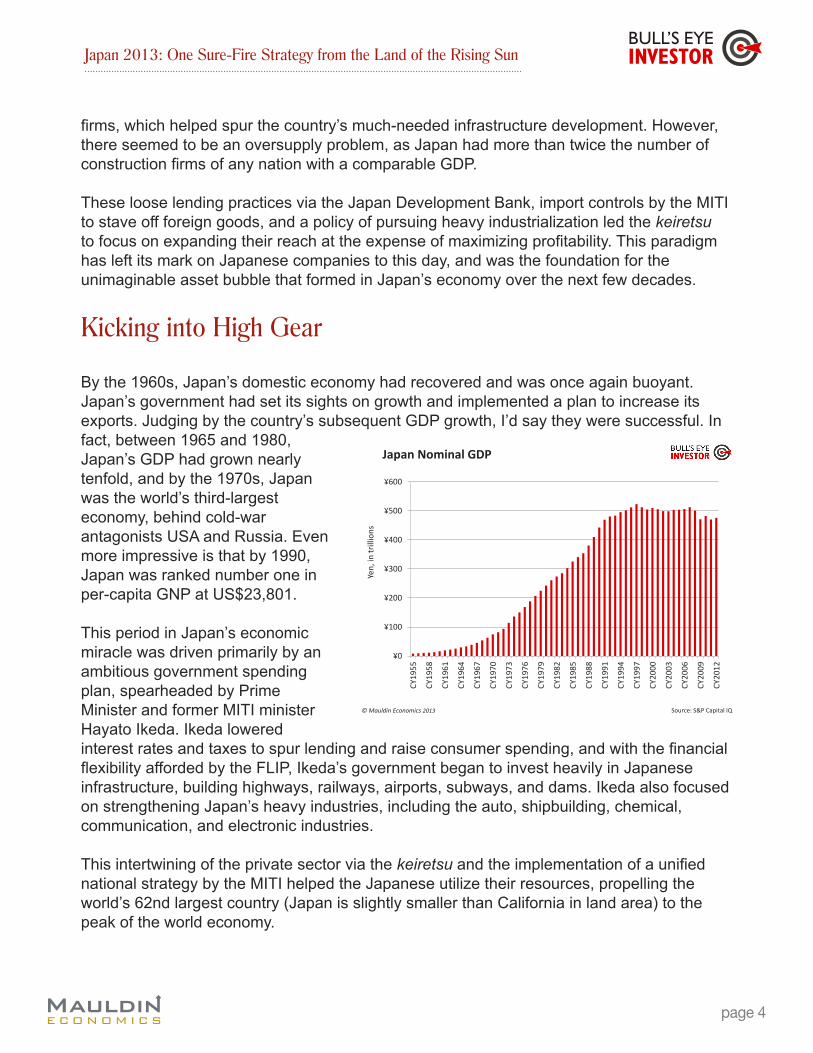

By the 1960s, Japan’s domestic economy had recovered and was once again buoyant. Japan’s government had set its sights on growth and implemented a plan to increase its exports. Judging by the country’s subsequent GDP growth, I’d say they were successful. In fact, between 1965 and 1980, Japan’s GDP had grown nearly tenfold, and by the 1970s, Japan was the world’s third-largest economy, behind cold-war antagonists USA and Russia. Even more impressive is that by 1990, Japan was ranked number one in per-capita GNP at US$23,801.

This period in Japan’s economic miracle was driven primarily by an ambitious government spending plan, spearheaded by Prime Minister and former MITI minister Hayato Ikeda. Ikeda lowered interest rates and taxes to spur lending and raise consumer spending, and with the financial flexibility afforded by the FLIP, Ikeda’s government began to invest heavily in Japanese infrastructure, building highways, railways, airports, subways, and dams. Ikeda also focused on strengthening Japan’s heavy industries, including the auto, shipbuilding, chemical, communication, and electronic industries.

This intertwining of the private sector via the keiretsu and the implementation of a unified national strategy by the MITI helped the Japanese utilize their resources, propelling the world’s 62nd largest country (Japan is slightly smaller than California in land area) to the peak of the world economy.

¥0

¥100

¥200

¥300

¥400

¥500

¥600

CY19

55

CY19

58

CY19

61

CY19

64

CY19

67

CY19

70

CY19

73

CY19

76

CY19

79

CY19

82

CY19

85

CY19

88

CY19

91

CY19

94

CY19

97

CY20

00

CY20

03

CY20

06

CY20

09

CY20

12

Yen,

in tr

illio

ns

Japan Nominal GDP

© Mauldin Economics 2013 Source: S&P Capital IQ

Japan 2013: One Sure-Fire Strategy from the Land of the Rising Sun

page 5

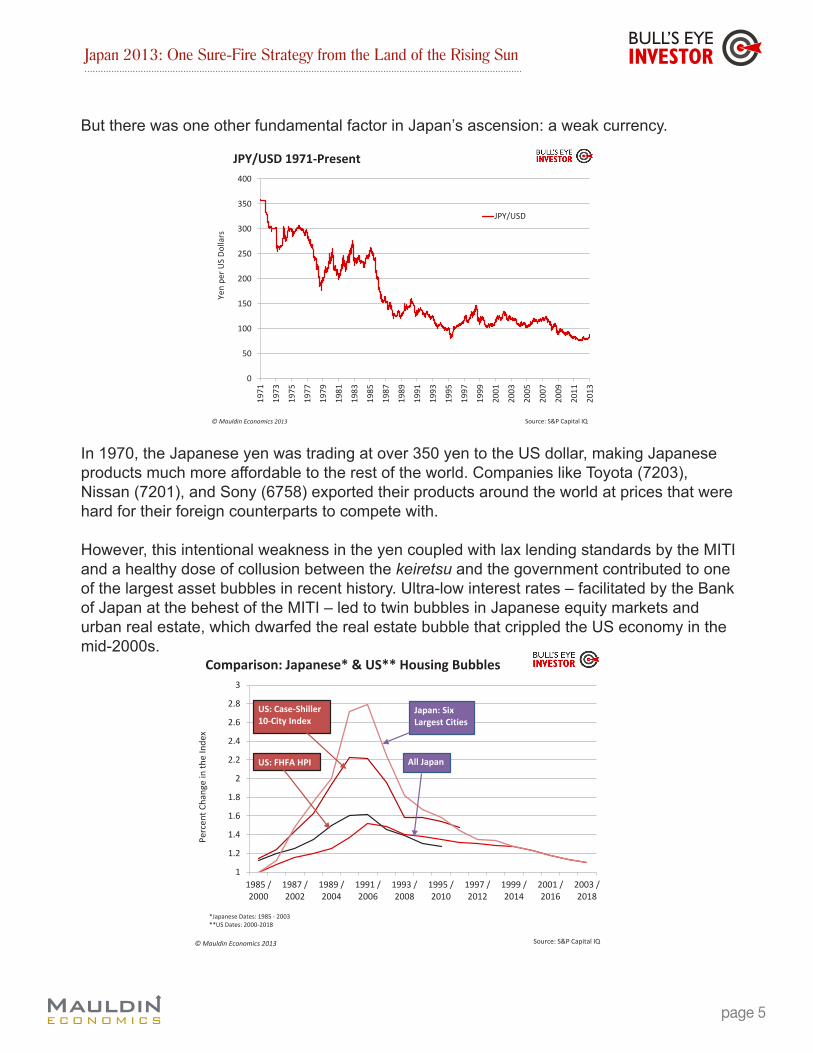

But there was one other fundamental factor in Japan’s ascension: a weak currency.

In 1970, the Japanese yen was trading at over 350 yen to the US dollar, making Japanese products much more affordable to the rest of the world. Companies like Toyota (7203), Nissan (7201), and Sony (6758) exported their products around the world at prices that were hard for their foreign counterparts to compete with.

However, this intentional weakness in the yen coupled with lax lending standards by the MITI and a healthy dose of collusion between the keiretsu and the government contributed to one of the largest asset bubbles in recent history. Ultra-low interest rates – facilitated by the Bank of Japan at the behest of the MITI – led to twin bubbles in Japanese equity markets and urban real estate, which dwarfed the real estate bubble that crippled the US economy in the mid-2000s.

0

50

100

150

200

250

300

350

400

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

JPY/USD

JPY/USD 1971-Present

© Mauldin Economics 2013

Yen

per U

S Do

llars

Source: S&P Capital IQ

1

1.2

1.4

1.6

1.8

2

2.2

2.4

2.6

2.8

3

1985 /2000

1987 /2002

1989 /2004

1991 /2006

1993 /2008

1995 /2010

1997 /2012

1999 /2014

2001 /2016

2003 /2018

Comparison: Japanese* & US** Housing Bubbles

Source: S&P Capital IQ

*Japanese Dates: 1985 - 2003 **US Dates: 2000-2018

US: Case-Shiller 10-City Index

US: FHFA HPI

Japan: Six Largest Cities

All Japan

Perc

ent C

hang

e in

the

Inde

x

© Mauldin Economics 2013

Japan 2013: One Sure-Fire Strategy from the Land of the Rising Sun

page 6

Once the Bank of Japan and the Japanese Finance Ministry understood the monstrous bubbles they had blown, they abruptly raised interest rates in late 1989. This caused both the equity and housing bubbles to burst simultaneously. Japan’s banking system was left with thousands of bad loans and an inability to lend, creating an army of what economists call “zombie banks.”

(Michael Schuman, Time Magazine) In a pathetic attempt to avoid losses, Japanese banks kept pumping fresh funds into debt-ridden, unprofitable firms to keep them afloat. These companies came to be known as zombie firms – they appeared to be living but were actually dead, too burdened by debt to do much more than live off further handouts. One economist called Japan a “loser’s paradise.”

The classic zombie was retail chain Daiei, which limped along for years, crushed by debt and multibillion-dollar losses, as banks kept bailing out the firm. Daiei, with nearly 100,000 employees at the time, was considered by politicians too big to fail. It was only after Japan began solving its zombie problem, rather than perpetuating it, that the country’s financial crisis was finally resolved.

Many of these zombie banks were eventually allowed to fail, spurring a wave of consolidation within the Japanese banking sector. When the dust settled, only four national banks were left standing.

If any of you were thinking that this sounded eerily similar to the events from 2008 and 2009, this is the point in the story where a divergence occurs. The biggest factor to take into account is that the Japanese are traditionally a nation of savers, not consumers (like the US). This allowed the government to finance their debt domestically, due in large part to an

ageing population that had amassed considerable savings over the previous three decades.

That doesn’t mean the Japanese galloped off into the sunset on a horse made of Japanese savings accounts. Far from it! In fact, one of the most apparent effects of this policy was the drastic drop in Japan’s trade balance, which fell from a 2.4% surplus in 1992 to a 10% deficit in 1998. -¥60,000

-¥50,000

-¥40,000

-¥30,000

-¥20,000

-¥10,000

¥0

¥10,000

¥20,000

Budget Surpluses and Deficits, 1980-2016 (Projected)

Source: S&P Capital IQ

Billi

ons o

f Yen

© Mauldin Economics 2013

Japan 2013: One Sure-Fire Strategy from the Land of the Rising Sun

page 7

A (Not So) New Approach

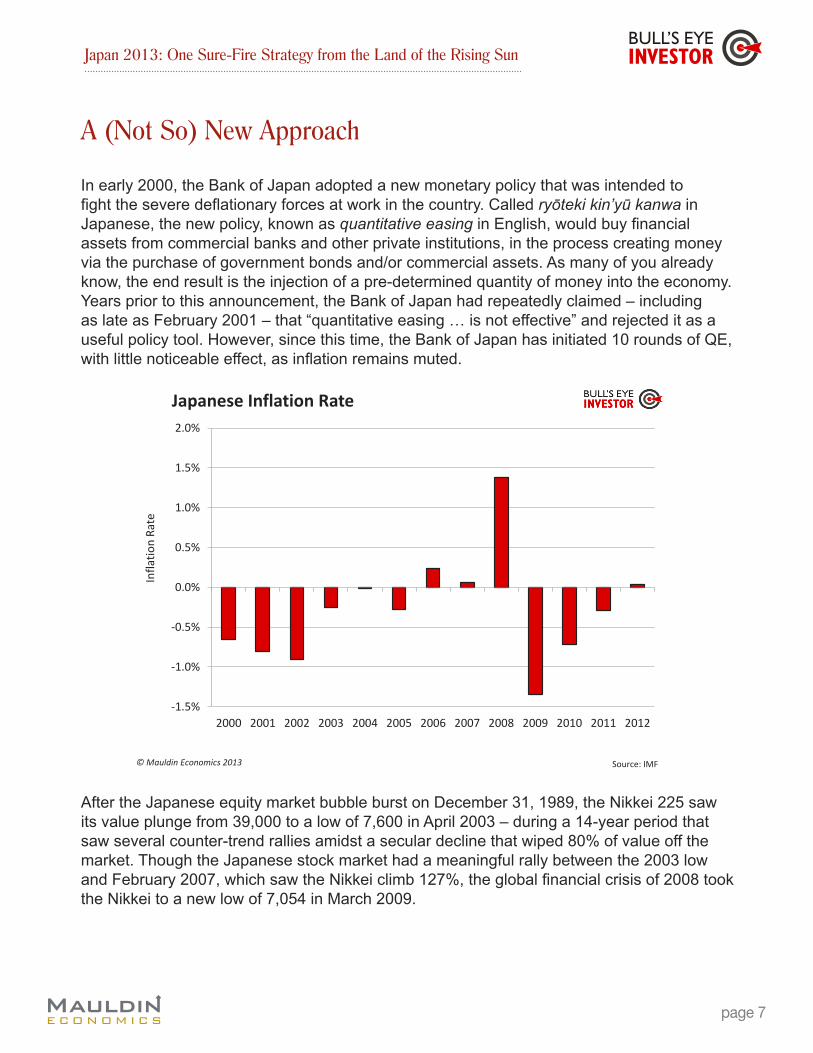

In early 2000, the Bank of Japan adopted a new monetary policy that was intended to fight the severe deflationary forces at work in the country. Called ryōteki kin’yū kanwa in Japanese, the new policy, known as quantitative easing in English, would buy financial assets from commercial banks and other private institutions, in the process creating money via the purchase of government bonds and/or commercial assets. As many of you already know, the end result is the injection of a pre-determined quantity of money into the economy. Years prior to this announcement, the Bank of Japan had repeatedly claimed – including as late as February 2001 – that “quantitative easing … is not effective” and rejected it as a useful policy tool. However, since this time, the Bank of Japan has initiated 10 rounds of QE, with little noticeable effect, as inflation remains muted.

After the Japanese equity market bubble burst on December 31, 1989, the Nikkei 225 saw its value plunge from 39,000 to a low of 7,600 in April 2003 – during a 14-year period that saw several counter-trend rallies amidst a secular decline that wiped 80% of value off the market. Though the Japanese stock market had a meaningful rally between the 2003 low and February 2007, which saw the Nikkei climb 127%, the global financial crisis of 2008 took the Nikkei to a new low of 7,054 in March 2009.

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Japanese Inflation Rate

© Mauldin Economics 2013 Source: IMF

Infla

tion

Rate

Japan 2013: One Sure-Fire Strategy from the Land of the Rising Sun

page 8

Today, the country is still in the grip of deflation, and its stock market has been moving sideways for nearly 20 years.

Enter Shinzo Abe

However, this “Lost Decade” – as Japan’s economic malaise has been dubbed, despite it running for twice that length of time – could soon come to an end. Just last month, the Liberal Democratic Party (LDP), the powerhouse of Japanese politics for decades before they were thrown out of office in 2009, regained power behind former Prime Minister Shinzo Abe. Abe had been elected in September of 2006 as the youngest post-WWII prime minister; however, his cabinet was repeatedly enmeshed in controversy, which ultimately led to his resignation in September 2007, less than one year after his election.

This time around, Abe was elected on a platform of, amongst other things, criticism of the Bank of Japan for not giving the economy enough monetary stimulus. Abe has made it clear that he feels the Bank of Japan hasn’t been printing money fast enough, and judging by his landslide win in the most recent election, it seems the Japanese people agree with him.

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

1980

1981

1982

1983

1984

1986

1987

1988

1989

1991

1992

1993

1994

1995

1997

1998

1999

2000

2002

2003

2004

2005

2006

2008

2009

2010

2011

Nikkei 225 1980-Present

© Mauldin Economics 2013 Source: S&P Capital IQ

Inde

x Va

lue

Japan 2013: One Sure-Fire Strategy from the Land of the Rising Sun

page 9

The new prime minister has promised to target a 2% inflation rate – down from an initial 3%. He’s also made it clear that if the country’s central bank doesn’t cave to his wishes, he will alter the central bank’s charter so he can directly influence its policies. Abe will also be nominating three new board members in the coming months, including a new Bank of Japan governor, and one would suspect that those in good enough graces to have Abe’s approval would be more than happy to do his bidding.

Apart from Abe’s desire for a resurgence of Japanese nationalism (which is a discussion for another day), he has also organized a buoyant government spending package worth approximately JPY 10 trillion ($114 billion USD), or roughly 2% of Japan’s 2011 GDP. Not only has Abe publicly stated that he feels no inclination to respect the unseated Democratic Party of Japan’s self-imposed JPY 44 trillion annual debt limit, but he has gone so far as to consider investing directly in certain Japanese companies to help spur growth.

Abe has also made it clear that reducing regulations are a key facet of his plan. Arbitrary regulations – many of which are related to Japan’s farming operations – have allowed certain Japanese companies to benefit from de facto monopolies, a trend Abe has vowed to reverse.

And, early though it is, it looks as though Abe is getting what he wants. In late January of this year, the central bank pledged to expand Abe’s open-ended asset purchasing scheme, buying about 13 trillion yen ($140 billion US) in assets per month starting January 2014, including Japanese government bonds and treasury bills. In the meantime, the central bank’s current asset purchase scheme will continue.

Competitive Devaluation: The New Normal

Since 2009, the list of central banks worldwide that have been debasing their currencies through repeated doses of quantitative easing has swelled to include all major economic powerhouses, including: the Bank of England, the Swiss National Bank, the ECB, the People’s Bank of China, and, last but certainly not least, the Federal Reserve.

Debasing one’s currency ceteris paribus is one thing, but everyone knows a global powerhouse doesn’t operate in a vacuum. Once you find yourself in a situation where multiple countries are trying to debase their currencies, things get a bit trickier. And even though leading developed countries all agreed at the G20 Summit in February 2013 to avoid targeting lower exchange rates to secure a competitive advantage, actions speak louder than words, and so far we haven’t seen any major economy switch off their presses.

Even though Japan was also a part of the G20 agreement, we believe they will stay the course and continue their policy of weakening the yen by targeting a 2% inflation rate. This has two desired effects:

Japan 2013: One Sure-Fire Strategy from the Land of the Rising Sun

page 10

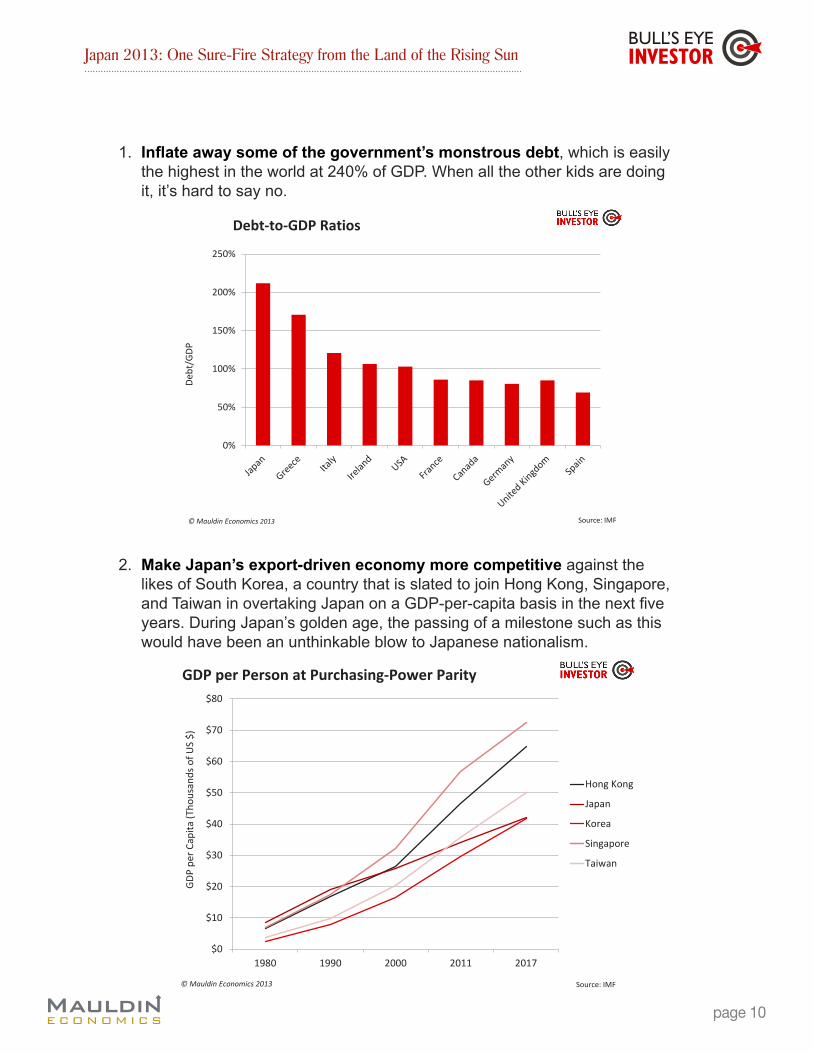

1. Inflate away some of the government’s monstrous debt, which is easily the highest in the world at 240% of GDP. When all the other kids are doing it, it’s hard to say no.

2. Make Japan’s export-driven economy more competitive against the likes of South Korea, a country that is slated to join Hong Kong, Singapore, and Taiwan in overtaking Japan on a GDP-per-capita basis in the next five years. During Japan’s golden age, the passing of a milestone such as this would have been an unthinkable blow to Japanese nationalism.

0%

50%

100%

150%

200%

250%

Source: IMF

Debt-to-GDP Ratios

Debt

/GDP

© Mauldin Economics 2013

$0

$10

$20

$30

$40

$50

$60

$70

$80

1980 1990 2000 2011 2017

Hong Kong

Japan

Korea

Singapore

Taiwan

© Mauldin Economics 2013

GDP

per C

apita

(Tho

usan

ds o

f US

$)

Source: IMF

GDP per Person at Purchasing-Power Parity

Japan 2013: One Sure-Fire Strategy from the Land of the Rising Sun

page 11

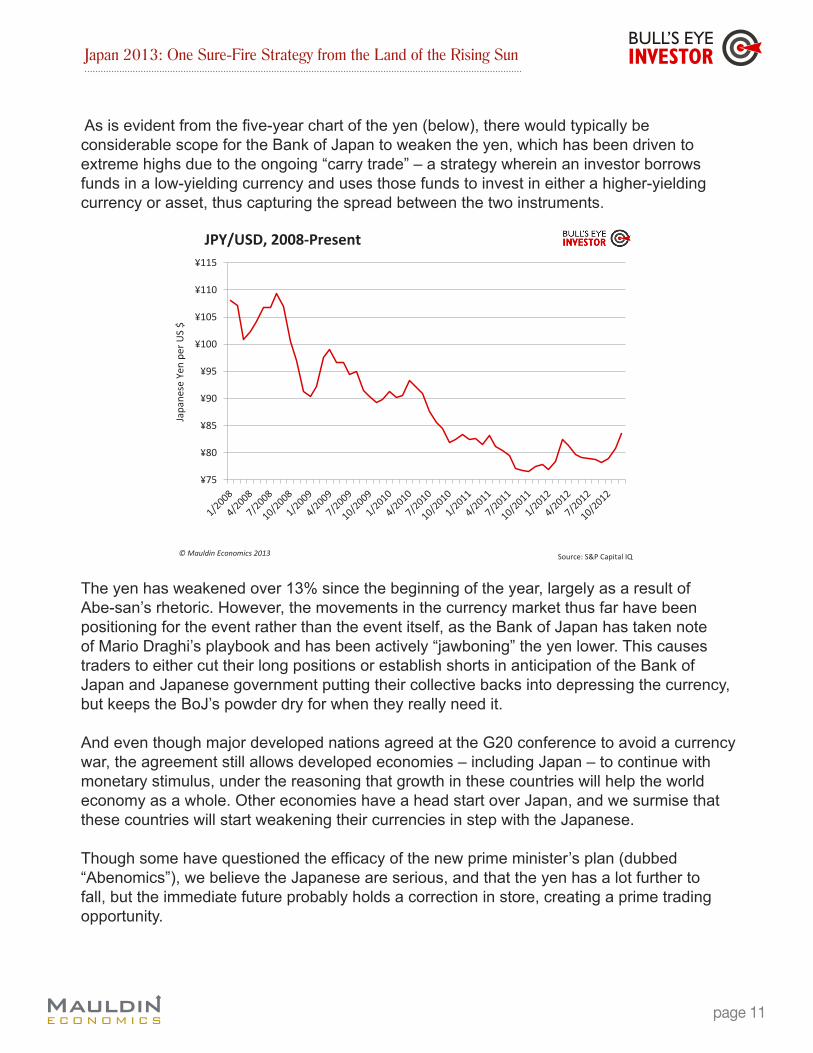

As is evident from the five-year chart of the yen (below), there would typically be considerable scope for the Bank of Japan to weaken the yen, which has been driven to extreme highs due to the ongoing “carry trade” – a strategy wherein an investor borrows funds in a low-yielding currency and uses those funds to invest in either a higher-yielding currency or asset, thus capturing the spread between the two instruments.

The yen has weakened over 13% since the beginning of the year, largely as a result of Abe-san’s rhetoric. However, the movements in the currency market thus far have been positioning for the event rather than the event itself, as the Bank of Japan has taken note of Mario Draghi’s playbook and has been actively “jawboning” the yen lower. This causes traders to either cut their long positions or establish shorts in anticipation of the Bank of Japan and Japanese government putting their collective backs into depressing the currency, but keeps the BoJ’s powder dry for when they really need it.

And even though major developed nations agreed at the G20 conference to avoid a currency war, the agreement still allows developed economies – including Japan – to continue with monetary stimulus, under the reasoning that growth in these countries will help the world economy as a whole. Other economies have a head start over Japan, and we surmise that these countries will start weakening their currencies in step with the Japanese.

Though some have questioned the efficacy of the new prime minister’s plan (dubbed “Abenomics”), we believe the Japanese are serious, and that the yen has a lot further to fall, but the immediate future probably holds a correction in store, creating a prime trading opportunity.

¥75

¥80

¥85

¥90

¥95

¥100

¥105

¥110

¥115

JPY/USD, 2008-Present

© Mauldin Economics 2013

Japa

nese

Yen

per

US

$

Source: S&P Capital IQ

Japan 2013: One Sure-Fire Strategy from the Land of the Rising Sun

page 12

So how do we capitalize on this?

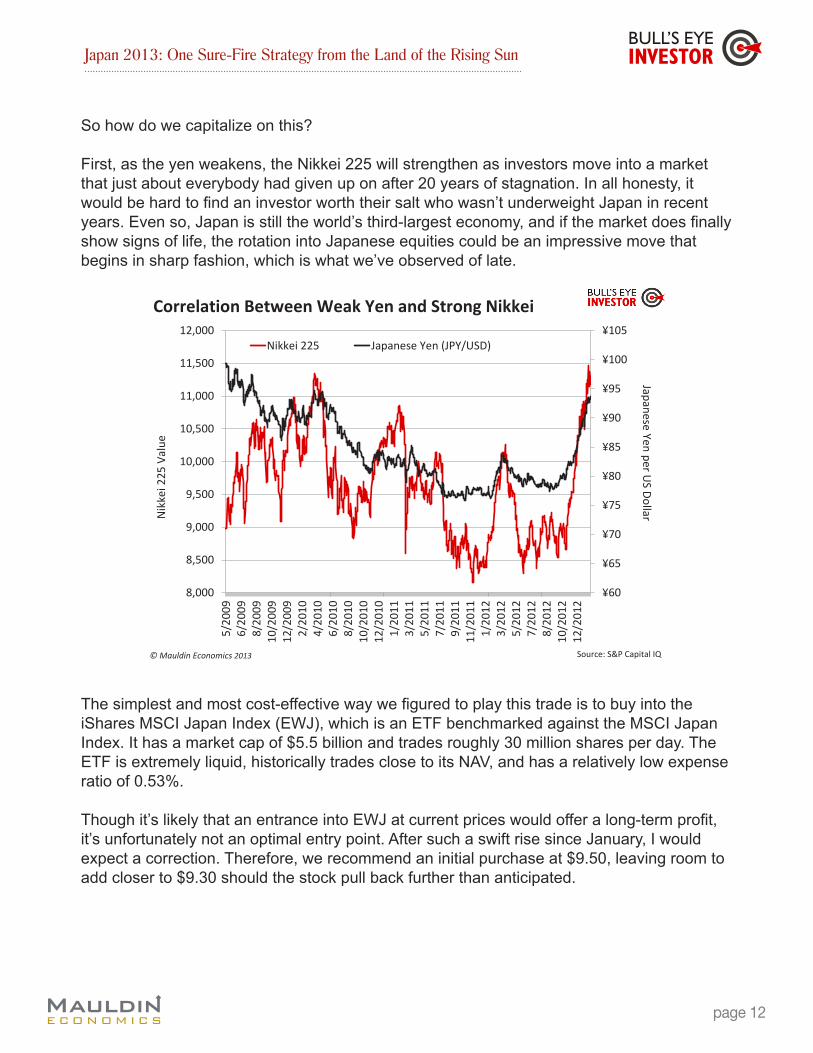

First, as the yen weakens, the Nikkei 225 will strengthen as investors move into a market that just about everybody had given up on after 20 years of stagnation. In all honesty, it would be hard to find an investor worth their salt who wasn’t underweight Japan in recent years. Even so, Japan is still the world’s third-largest economy, and if the market does finally show signs of life, the rotation into Japanese equities could be an impressive move that begins in sharp fashion, which is what we’ve observed of late.

The simplest and most cost-effective way we figured to play this trade is to buy into the iShares MSCI Japan Index (EWJ), which is an ETF benchmarked against the MSCI Japan Index. It has a market cap of $5.5 billion and trades roughly 30 million shares per day. The ETF is extremely liquid, historically trades close to its NAV, and has a relatively low expense ratio of 0.53%.

Though it’s likely that an entrance into EWJ at current prices would offer a long-term profit, it’s unfortunately not an optimal entry point. After such a swift rise since January, I would expect a correction. Therefore, we recommend an initial purchase at $9.50, leaving room to add closer to $9.30 should the stock pull back further than anticipated.

¥60

¥65

¥70

¥75

¥80

¥85

¥90

¥95

¥100

¥105

8,000

8,500

9,000

9,500

10,000

10,500

11,000

11,500

12,000

5/20

096/

2009

8/20

0910

/200

912

/200

92/

2010

4/20

106/

2010

8/20

1010

/201

012

/201

01/

2011

3/20

115/

2011

7/20

119/

2011

11/2

011

1/20

123/

2012

5/20

127/

2012

8/20

1210

/201

212

/201

2

Nikkei 225 Japanese Yen (JPY/USD)

Correlation Between Weak Yen and Strong Nikkei

© Mauldin Economics 2013

Nik

kei 2

25 V

alue

Japanese Yen per U

S Dollar

Source: S&P Capital IQ

Japan 2013: One Sure-Fire Strategy from the Land of the Rising Sun

page 13

That said, going long on Japanese equities leaves significant exposure to the yen. Since we are assuming that the Bank of Japan is serious about weakening the yen, a short position in the yen is a sensible way to mitigate the dampening effect that the bank’s success would have on absolute dollar returns in EWJ.

That’s why we believe those going long EWJ should also enter a position in ProShares UltraShort Yen ETF (YCS), which is a nice, liquid vehicle by which to express this view.

Due to its leveraged nature – the ETF attempts to produce 2x the inverse of the daily performance of the yen – this is not a long-term buy-and-hold position. Instead, YCS should be used as a hedge for a long stock position, as it can do a good job in dispersing the negative effects of any central bank action.

However, like EWJ, it has run up significantly since the beginning of the year, so we would look to enter the trade at the same time as buying EWJ, since, on a pullback in the Nikkei, YCS should follow suit.

If an investor were to take this approach, only $500 worth of YCS would need to be purchased to cover every $1,000 of EWJ (though it’s worth noting that the 2x performance of YCS is subject to tracking errors, and exposure needs to be monitored carefully to ensure the EWJ long remains hedged).

An outright position in YCS would be recommended if the ETF were to trade down to $48.

For those of you who’d be more comfortable simply buying one security instead of the two we mentioned above, there is a third option: the WisdomTree Japan Hedged Equity Fund (DXJ). This ETF is perfect for those who are looking to invest in Japanese equities, while at the same time avoiding exposure to changes in the rate between the Japanese yen and the US dollar. Since the fund uses a hedging strategy, DXJ’s returns are not impacted by a falling yen, unlike unhedged funds like EWJ. DXJ also differs from EWJ in that it’s a dividend-weighted index (i.e., funds with higher dividend payouts have the highest weighting). The fund also excludes companies that generate 80% or more of their revenue from Japan, skewing the index towards companies with a large global revenue base.

What We’ll Be Watching For

The surge in the Nikkei since January has caused Shinzo Abe’s approval rating to skyrocket. In fact, Abe has the highest approval rating since the popular Junichiro Koizumi – whom many consider Abe’s mentor – stepped down in 2006. One event that could push Abe’s approval ratings into the stratosphere would be if he could convince the recently unseated Democratic Party of Japan to back his nomination for BOJ chief, Haruhiko Kuroda.

Japan 2013: One Sure-Fire Strategy from the Land of the Rising Sun

page 14

Kuroda, who has been the president of the Asian Development Bank since 2005, has made it clear that he will do whatever it takes to end Japan’s 15 years of deflation, should he be confirmed as governor. Kuroda contends that a 2% inflation target for 2013 and beyond is possible, and that a strategy of buying derivatives and stakes in Japanese companies in addition to government bonds should be on the table. He advocated a similar inflation target more than a decade ago, which is one reason Abe handpicked him to succeed the ousted Masaaki Shirakawa.

Prime Minister Abe’s advisers say they expect Kuroda to at least catch up with the open-ended monetary stimulus adopted by the Federal Reserve since the 2008 financial crisis. Former member of the Bank of Japan’s governing Policy Board Nobuyuki Nakahara said Kuroda’s first steps would most likely be to sharply increase purchases of corporate bonds and real-estate-linked securities.

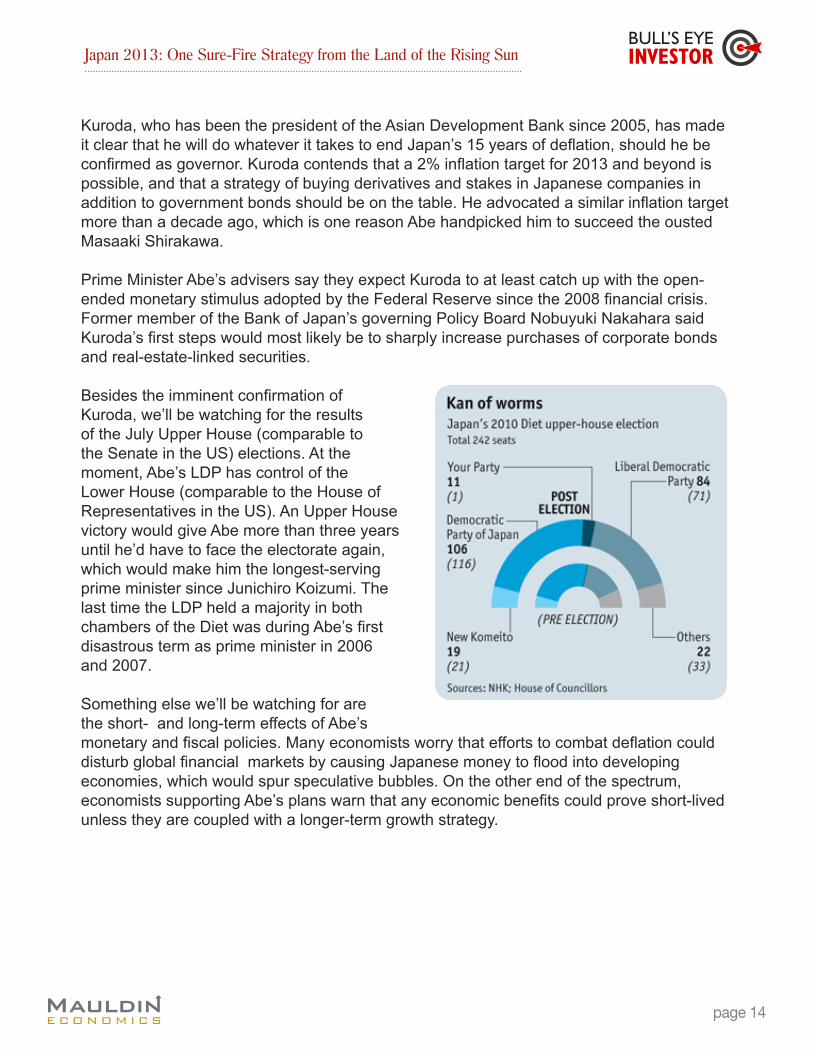

Besides the imminent confirmation of Kuroda, we’ll be watching for the results of the July Upper House (comparable to the Senate in the US) elections. At the moment, Abe’s LDP has control of the Lower House (comparable to the House of Representatives in the US). An Upper House victory would give Abe more than three years until he’d have to face the electorate again, which would make him the longest-serving prime minister since Junichiro Koizumi. The last time the LDP held a majority in both chambers of the Diet was during Abe’s first disastrous term as prime minister in 2006 and 2007.

Something else we’ll be watching for are the short- and long-term effects of Abe’s monetary and fiscal policies. Many economists worry that efforts to combat deflation could disturb global financial markets by causing Japanese money to flood into developing economies, which would spur speculative bubbles. On the other end of the spectrum, economists supporting Abe’s plans warn that any economic benefits could prove short-lived unless they are coupled with a longer-term growth strategy.

Japan 2013: One Sure-Fire Strategy from the Land of the Rising Sun

page 15

One plan Abe has been pursuing along these lines is the Trans-Pacific Partnership (TPP). The TPP is an effort to expand the Trans-Pacific Strategic Economic Partnership Agreement (TPSEP), which is a free-trade agreement, signed in 2005, between Brunei, Chile, New Zealand, and Singapore. The TPSEP affects trade in goods, rules of origin, trade remedies, sanitary and phytosanitary measures, technical barriers to trade, trade in services, intellectual property, and government procurement policy. The original agreement also called for a 90% reduction of all tariffs between member countries. The TPP intends to expand this agreement to include Australia, Canada, Malaysia, Mexico, Peru, the United States, Vietnam, and, most recently, Japan.

Japan has been a formal observer during these talks since 2010, along with the US, Canada, and Australia. However, disagreements over Japan’s protectionist agricultural policies, which include (among others) a 778% rice tariff, have prevented the country from becoming a full-fledged member. Japanese farmers – who are historically vocal supporters of Abe’s LDP – claim such a deal would mean the collapse of their industry, even though a 2010 government study estimates the pact would add ¥3.2 trillion to Japan’s GDP.

Earlier this month, Abe made his intentions known in a speech to parliament:

“The future of Japan’s economic growth depends on us having the willpower and the courage to sail without hesitation onto the rough seas of global competition.”

However, Abe’s support for the TPP could hurt his party’s chances at winning the Upper House elections in July, as the rural farming districts have underpinned the LDP’s half-century domination of politics. So we’ll be watching developments in the TPP negotiations – along with Abe’s approval rating and the July Upper House elections – extremely closely.

Japan 2013: One Sure-Fire Strategy from the Land of the Rising Sun

page 16

Use of this content, the Mauldin Economics website, and related sites and applications is provided under the Mauldin Economics Terms & Conditions of Use.

Unauthorized Disclosure Prohibited

The information provided in this publication is private, privileged, and confidential information, licensed for your sole individual use as a subscriber. Mauldin Economics reserves all rights to the content of this publication and related materials. Forwarding, copying, disseminating, or distributing this report in whole or in part, including substantial quotation of any portion the publication or any release of specific investment recommendations, is strictly prohibited.

Participation in such activity is grounds for immediate termination of all subscriptions of registered subscribers deemed to be involved at Mauldin Economics’ sole discretion, may violate the copyright laws of the United States, and may subject the violator to legal prosecution. Mauldin Economics reserves the right to monitor the use of this publication without disclosure by any electronic means it deems necessary and may change those means without notice at any time. If you have received this publication and are not the intended subscriber, please contact [email protected].

Disclaimers

The Mauldin Economics website, Yield Shark, Thoughts from the Frontline, Thoughts from the Frontline Audio, Outside the Box, Over My Shoulder, World Money Analyst, Bull’s Eye Investor, Things That Make You Go Hmmm…, Just One Trade, and Conversations are published by Mauldin Economics, LLC. Information contained in such publications is obtained from sources believed to be reliable, but its accuracy cannot be guaranteed. The information contained in such publications is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. The opinions expressed in such publications are those of the publisher and are subject to change without notice. The information in such publications may become outdated and there is no obligation to update any such information. You are advised to discuss with your financial advisers your investment options and whether any investment is suitable for your specific needs prior to making any investments.

John Mauldin, Mauldin Economics, LLC and other entities in which he has an interest, employees, officers, family, and associates may from time to time have positions in the securities or commodities covered in these publications or web site. Corporate policies are in effect that attempt to avoid potential conflicts of interest and resolve conflicts of interest that do arise in a timely fashion. Mauldin Economics, LLC reserves the right to cancel any subscription at any time, and if it does so it will promptly refund to the subscriber the amount of the subscription payment previously received relating to the remaining subscription period. Cancellation of a subscription may result from any unauthorized use or reproduction or rebroadcast of any Mauldin Economics publication or website, any infringement or misappropriation of Mauldin Economics, LLC’s proprietary rights, or any other reason determined in the sole discretion of Mauldin Economics, LLC.

Affiliate Notice

Mauldin Economics has affiliate agreements in place that may include fee sharing. If you have a website or newsletter and would like to be considered for inclusion in the Mauldin Economics affiliate program, please go to http://affiliates.pubrm.net/signup/me. Likewise, from time to time Mauldin Economics may engage in affiliate programs offered by other companies, though corporate policy firmly dictates that such agreements will have no influence on any product or service recommendations, nor alter the pricing that would otherwise be available in absence of such an agreement. As always, it is important that you do your own due diligence before transacting any business with any firm, for any product or service.

© Copyright 2013 by Mauldin Economics, LLC.