the philippine economy - ateneo.edu philippine economy has been on a roll. ... atm sectoral growth...

TRANSCRIPT

The Philippine Economy:

Eagle Watch Briefing for Ateneo CCE Ateneo Rockwell Campus, Makati City

17 August 2017

Cielito F. Habito Professor, Ateneo de Manila

University

How Are We Doing? What’s in Store?

Storyline 1. The economy has been on a roll.

2. Investment has been surging, and trade (and tourism) is picking up.

3. Inclusive growth is finally happening.

4. Our foreign linkages all matter.

5. Dark clouds are looming.

6. We continue to lag behind.

7. We need to be forward-looking.

1. The Philippine economy has been on a roll.

Positive trends on prices, jobs & GDP

‘PiTiK’ Test in 2016

Presyo: Inflation at historical lows (2016 – 1.8%)

Trabaho: Unemployment rate finally breaks below 5% (Oct ‘16 – 4.7%)

Kita: 2016 GDP growth of 6.8% (Fastest in ASEAN & East Asia)

Presyo, 2016

Inflation Trends 9.3%

3.2% 3.8%

4.4%

3.2% 2.9% 4.2%

July 2017: 2.8%

1.4% 1.8%

Trabaho, 2016 Unemployment Rate at a record low (below 5%)

Kita, 2016 Industry: Strong Driver

But Agriculture Was the Bad News

PH: Fastest GDP Growth in East Asia

Sources: WB, BSP

2016 (Q3)

2. Investment has been surging; trade (& tourism) is picking up. Change actually began in 2010.

Source: PSA

Investment: Surging Since 2010

Private Construction

Durable Equipment

Fixed Investment

Growth Rate (%)

Trade is Picking Up Exports doubled its growth

rate in Q1-2017

Tourism: Riding High • Domestic tourism surge • DOT “More fun” campaign • More open skies • ASEAN cruise circuit • Large gaming industry investments

• Medical tourism, retirement estates

• Airport upgrading in PPP projects

ATM Sectoral Growth Performance Agriculture: the unfortunate laggard

Average Annual Growth, 2012-2015 (%)

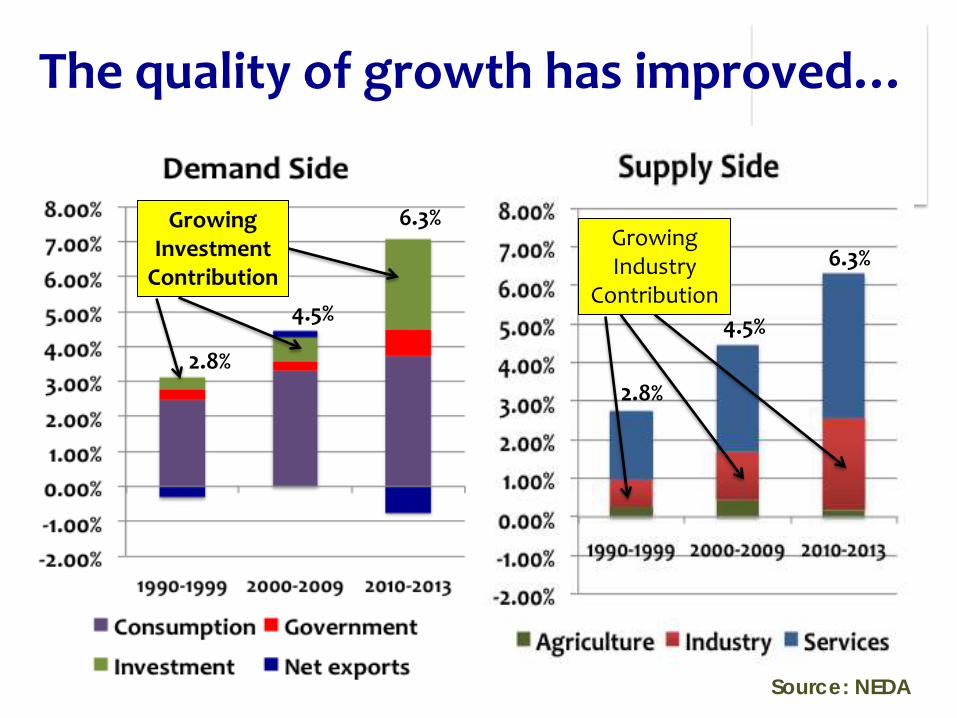

3. Inclusive growth is finally happening.

Economic growth on a broader base.

The quality of growth has improved…

Source: NEDA

2.8%

4.5%

6.3% Growing Investment

Contribution

2.8%

4.5%

6.3% Growing Industry

Contribution

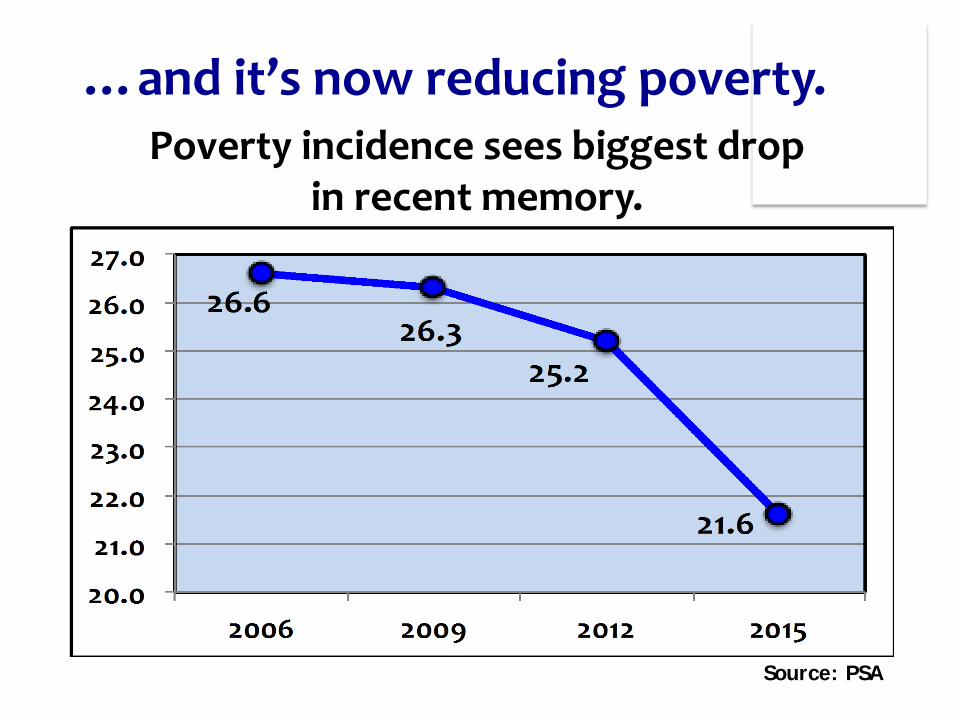

…and it’s now reducing poverty.

Source: PSA

Poverty incidence sees biggest drop in recent memory.

Unemployment Rate dropped below 5% …

…even with slower OFW deployment.

Much more jobs are being generated.

4. Dark clouds are looming. First Quarter numbers moved the wrong way.

Latest PiTiK Data (Q1-2017)

Prices: Inflation Rate: 3.4% (28 month high); Mar-Apr ’17 – 3.4%

Jobs: Unemployment Rate up again, at 6.6% (Jan) & 5.7% (Apr) (following a 3-year decline)

GDP Growth: Still fast, but slowing down (6.9% 6.4%)

>> Current Account: Back in deficit after 15 years of surplus

Inflation in 2017 2-3 Times Faster vs. 2016

1.3% 0.9% 1.1% 1.1% 1.1% 1.6% 1.9% 2016:

Source: PSA, Rappler (Graphic)

Unemployment Rises Anew

Overall GDP Slows Down …even with turnaround in Agriculture

Why the Slowdown? Slackened Spending

Downside Risks • Persistent infrastructure shortcomings

(e.g., Telecoms and Internet,Transport sector rigidities)

• FDI slowdown due to domestic issues

• Backlash from EU, US (?)

• Restrictive policies

• Build, Build, Bust? (Undue dependence on ODA vs. PPP, implementation bottlenecks)

• UP rather than UST (Uncoordinated Policies vs. Unity, Solidarity & Teamwork)

5. Our foreign linkages all matter. ‘Independent foreign policy’ must mean friendship with all.

Our foreign linkages: Which ones matter the most to us in trade?

Sources: PSA, BSP

Our foreign linkages: Which ones matter the most to us in FDI?

Sources: PSA, BSP

Our foreign linkages: Which ones matter the most to us in remittances?

Sources: PSA, BSP

Our Major Economic Partners: Where are opportunities largest?

Source: WB

GDP (US$ Trillion), 2015

‘Inclusiveness’ applies to our foreign linkages too.

6. We continue to lag behind. Recent improvements just haven’t been good enough.

Sources: ADB, BSP

Gap has actually widened

We’re still trailing in exports…

Sources: ADB, BSP

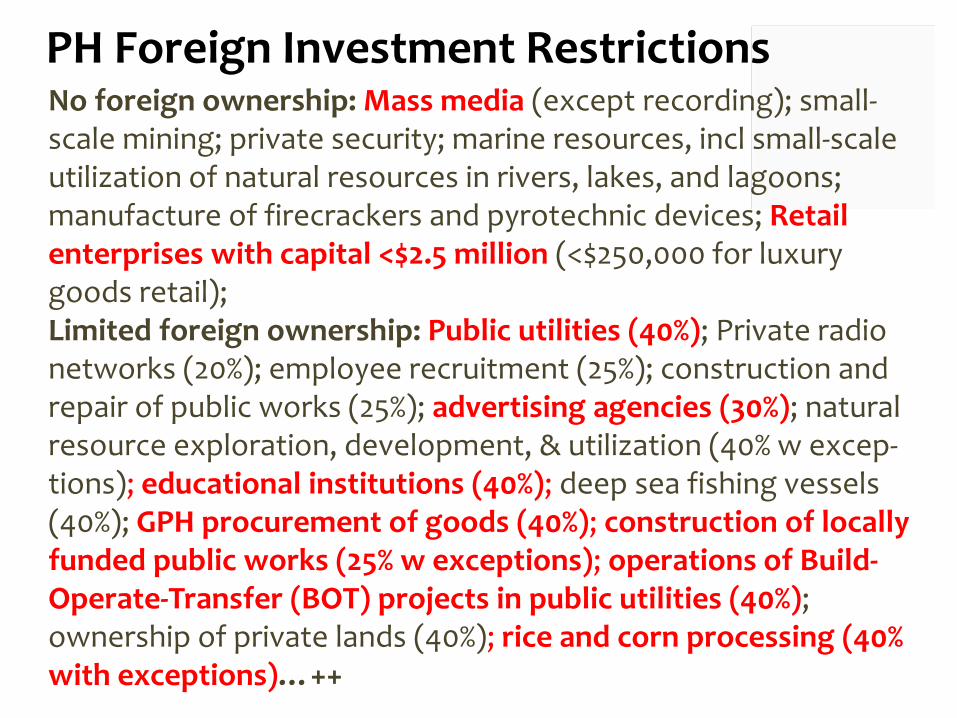

…and in Foreign Direct Investments (even after eight-fold expansion)

2016: $7.9B

PH Foreign Investment Restrictions No foreign ownership: Mass media (except recording); small-scale mining; private security; marine resources, incl small-scale utilization of natural resources in rivers, lakes, and lagoons; manufacture of firecrackers and pyrotechnic devices; Retail enterprises with capital <$2.5 million (<$250,000 for luxury goods retail); Limited foreign ownership: Public utilities (40%); Private radio networks (20%); employee recruitment (25%); construction and repair of public works (25%); advertising agencies (30%); natural resource exploration, development, & utilization (40% w excep-tions); educational institutions (40%); deep sea fishing vessels (40%); GPH procurement of goods (40%); construction of locally funded public works (25% w exceptions); operations of Build-Operate-Transfer (BOT) projects in public utilities (40%); ownership of private lands (40%); rice and corn processing (40% with exceptions)…++

• Poverty rose from 24.9% in 2003 to 26.5% in 2009, and again in 2013-2014 (24.625.8%)

• Income of richest 20% is 8.4x that of poorest 20% - vs. Thailand (6.9x) Vietnam (6.0x) Sri Lanka (5.8x)

High Poverty, Wide Inequality Still Our Main Challenge

7. We need to be forward-looking. Major challenges are on the horizon.

Fourth Industrial Revolution

• Building on the ongoing Third, and rapidly taking it to new heights

• Fusion of technologies across physical, digital and biological spheres (nanotechnology, brain research, 3D printing, mobile networks, battery technology, etc.)

• ‘Disruptive technologies’

The Age of Disruption is Here

• Digital cameras killed Kodak, Fuji within a few years from 1998 (when Kodak still dominant)

• Biggest transport company in the world owns no vehicles (Uber); biggest accommodations provider owns no properties (Airbnb)

• With IBM’s Watson: Legal advice within seconds; cancer diagnosis 4x more accurate than medical practitioners

• Tesla: Redefining energy and power industry

Greatest Challenges: • Will new types of jobs

be enough to offset massively displaced ones?

• How do we avoid a world of joblessness, low productivity and inequality?

• How do we make sure that IR4 improves the state of the world? How do we ensure sustainability?

• Is Ambisyon Natin 2040 on the right track?

PH Long Term Outlook: A Silent Crisis

Fact 2: • 33.5% (1 out of 3) Filipino children < 5 years

old suffer from stunting (hence permanently impaired from reaching full brain & physical development)

• Another 7% are wasted (underweight)

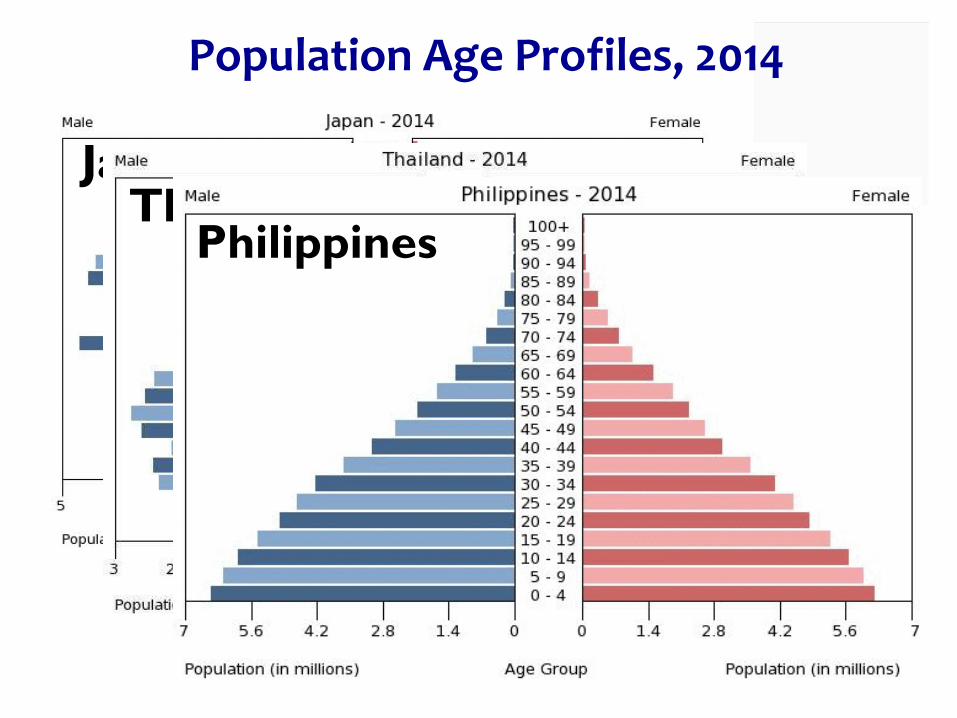

Fact 1: • In 2050, working age Filipinos will well

exceed the dependent elderly & young (“Demographic Sweet Spot”)

Population Age Profiles, 2014

Japan Thailand

Philippines

Population Age Profiles, 2050

Japan

Thailand

Philippines Stunted Generation

Demographic Sweet Spot?

or Demographic Time Bomb?

The Way Forward For sustained growth: Build, build, build Ease trade and investment restrictions Reduce regulatory burden

For inclusive development: Concerted MSME promotion and support Inclusive value chains (vs. vertical integration) Wider competition & market contestability Investments in Human Development & social

protection – and especially…