the of water for food production and trade in the...

TRANSCRIPT

The role of water for food production and trade in the Americas

Claudia Ringlera, Insa Flachsbarthb, Tingju Zhua and Mark W. Rosegranta

Environment and Production Technology DivisionBotin Foundation, Spain &CEIGRAM, Universidad Politécnica de

Madrid, Spain

“Water: Food for the Land”, Buenos Aires, ArgentinaSeptember 25th, 2013,

Ministerial Meeting of the Ministers of Agriculture of the American Hemisphere

Today, 36% of population, 39% of grain production, and 22% of global GDP are at risk due to water stress

How many people live in water short areas (%)?

How much GDP is generated in water scarce regions (%)?

> 50

< 2020 - 3030 - 4040 - 50

No data

> 40%

20 - 40%

0 - 20%

2010

36

18

46

> 40%

0 - 20%

1922

2010

20 - 40%

59

2010

2.5 Bnpeople

9.4 trillion USD2

Water stress, percent of total renewable water withdrawn

Source: Veolia Water & IFPRI 2011

Under BAU, 52% of the population, 49% of cereal production, and 45% of GDP will be at risk due to water stress by 2050

> 40%

20 - 40%

0 - 20%

2050

52

1632

2010

36

18

46

> 40%20 - 40%

0 - 20%

2050

45

25

30

2010

2219

59

Business as usual, 2050 How many people live in water short areas?

How much GDP is generated in water scarce regions?

▪ 4.7 Bnpeople ▪ Increase

by 90% compared to 2010

▪ 63 trillion USD▪ Increase

by 570% compared to 2010

Water stress, percent of total renewable water withdrawn

> 50

30 - 4040 - 50< 20

20 - 30

No data

Source: Veolia Water & IFPRI 2011

Outline

Drivers of Change Affecting Water and Food

Impacts on Water Resources

Impacts on Food

Technology and Policy Options

Summary

www.ifpri.org

DRIVERS OF CHANGE AFFECTING WATER & FOOD

www.ifpri.org

Water & Food Availability are (Adversely) Affected by a Series of Global Drivers

1. Population growth & urbanization2. Economic growth and changing diets3. Higher energy prices (increased HP demand)4. Growing demand for non‐food crops (biofuels)5. Growing water demand for domestic/ industrial/

environmental uses6. Declining water quality and degradation of resources7. Climate variability and climate change8. Slowing investments in agriculture & water (some change

in Sub‐Saharan Africa)9. Unsustainable use & poor management

www.ifpri.org

Annual Average Growth in Population, Baseline Projections between 2010 and 2050

0

0,5

1

1,5

2

2,5

Percen

t Growth Rate pe

r Year

Source: based on UN medium variant (2011).

www.ifpri.org

(Nominal) GDP growth most rapid elsewhere, but significant growth in South America as well

(current US$ billion)

Source: PwC forecasts of GDP (PPP), January, 2011.

2015 2050 growth

Venezuela 342 959 3.0 Chile 330 1297 4.0

Peru 273 1567 5.1

Argentina 524 2276 4.3 Canada 1967 5045 2.7

Mexico 1406 7117 4.7 Brazil 2700 10273 3.9

India 2308 22221 6.7

USA 18012 52562 3.1 China 11020 79234 5.8

www.ifpri.org

Per capita water availability, 2010 and projected 2050 (m3/cap)

Source: IFPRI IMPACT Model, September 2011 simulations

0

10000

20000

30000

40000

50000

2010 2050

www.ifpri.org

Share Urban Population, 1990, 2010 andprojected 2050 (%)

Source: UN World Urbanization Prospects, 2011 revision

0102030405060708090100

Caribbean CentralAmerica

SouthAmerica

Canada USA World

1990 2010 2050

www.ifpri.org

Change in dietary patterns, 1990 to 2007(calories/cap/day)

Source: FAOSTAT Food Balance Sheets. Accessed September 2013.

0

500

1000

1500

2000

2500

3000

3500

4000

GUA_1990 GUA_2007 BRA_1990 BRA_2007 USA_1990 USA_2007

Cereals Animal products Starches Veg Oils Sugars Fruits/Veggies Other calories

www.ifpri.org

Irrigation investments are not increasing much (bn 1995 USD)

02468

101214

1961-1965

1966-1970

1971-1975

1976-1980

1981-1985

1986-1990

1991-1995

1996-2000

Year

Inve

stm

ent (

billi

on 1

995

US$

)

SSA EAP excluding China LACMENA SA excluding India IndiaChina Total

Sources: African Development Bank, Asian Development Bank, Inter American Development Bank, World Bank; Rosegrant, Valmonte-Santos and Basani 2005 and Upali Amarasinghe

www.ifpri.org

Nitrogen loadings‐cropland43 million ton/yr

Source: IFPRI 2013

www.ifpri.org

Nitrogen loadings‐pasture9 million ton/yr

Source: IFPRI 2013

www.ifpri.org

Food and oil prices are increasingly linked (biofuels and energy intensity of agriculture)

www.ifpri.org

IMPACTS ON WATER RESOURCES

DECLINING SUPPLY &GROWING DEMAND

www.ifpri.org

Mean Annual Runoff Changes under CSIRO‐A1b Scenario in 2050Relatively drier and lower temp increase

Source: IFPRI IGHM simulation (2013)

www.ifpri.org

Mean Annual Runoff Changes under MIROC‐a1b Scenario in 2050relatively hotter and wetter

Source: IFPRI IGHM simulation (2013)

www.ifpri.org

Changes in total water demand, by climate scenario (in billion cubic meters)

0

50

100

150

200

250

300

LatinAmericaCaribbean NorthAmerica

2010 2050 CSIRO_A1b CSIRO_B1 MIROC_A1b MIROC_B1

IFPRI Impact simulations.

www.ifpri.org

13% 6%

5%

76%

Water Demand Shares by SectorLAC, 2010 and projected 2050 (NO CC)

14%

13%

4%69%

Domestic

Industrial

Livestock

Irrigation

Total: 149 BCM Total: 214 BCM, 43% increase

2010 2050

IFPRI Impact simulations.

www.ifpri.org

0.5

0.6

0.7

0.8

0.9

1

2000 2030 2050

NAE

0.5

0.6

0.7

0.8

0.9

1

2000 2030 2050

ESAP

0.5

0.6

0.7

0.8

0.9

1

2000 2030 2050

LAC

0.5

0.6

0.7

0.8

0.9

1

2000 2030 2050

SSA

0.5

0.6

0.7

0.8

0.9

1

2000 2030 2050

CWANA

0.5

0.6

0.7

0.8

0.9

1

2000 2030 2050

Developing countries

Projected Declining Irrigation Water Supply Reliability

www.ifpri.org

IMPACTS ON FOOD

INCREASING PRICES &GROWING FOOD INSECURITY

www.ifpri.org

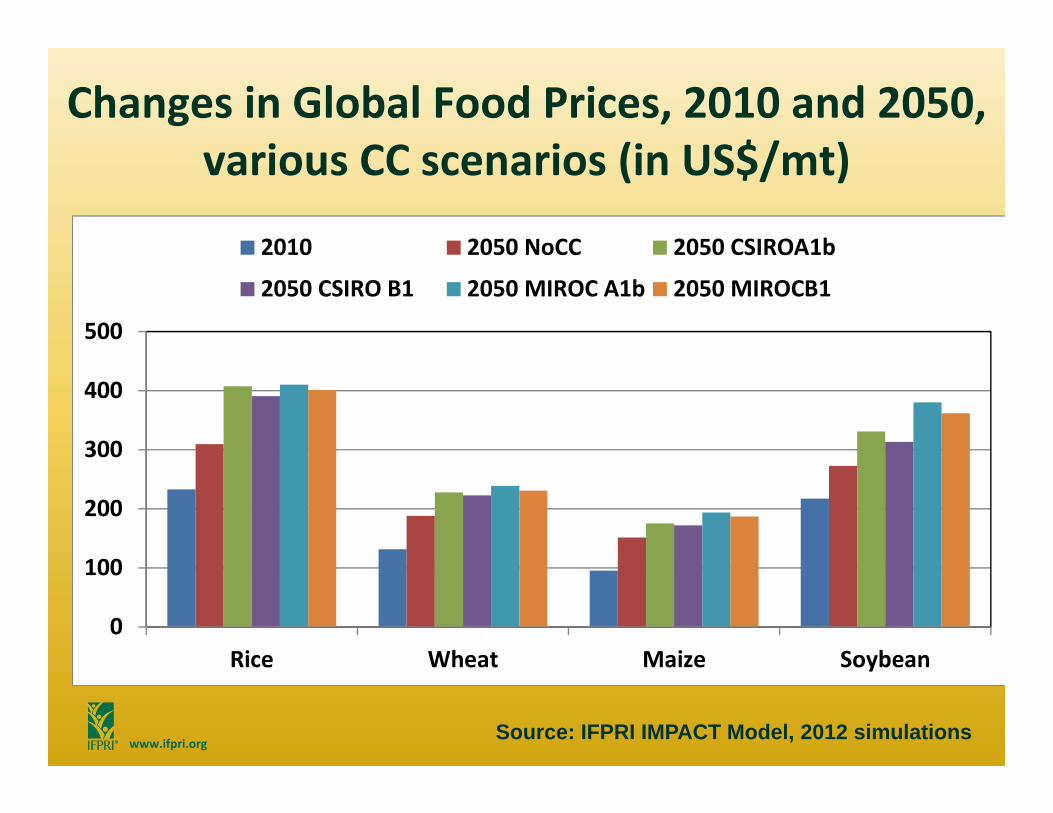

Changes in Global Food Prices, 2010 and 2050, various CC scenarios (in US$/mt)

Source: IFPRI IMPACT Model, 2012 simulations

0

100

200

300

400

500

Rice Wheat Maize Soybean

2010 2050 NoCC 2050 CSIROA1b

2050 CSIRO B1 2050 MIROC A1b 2050 MIROCB1

www.ifpri.org

Source of Cereal Production Growth, 2010 ‐ 2050 (%/year)

‐20020406080100120

Percen

t Cha

nge

Area Expansion Yield Improvement

Source: IFPRI IMPACT Model, September 2011 simulations

www.ifpri.org

Net Trade in Cereals‐Projections, 2010 and 2050, various CC scenarios

Source: IFPRI IMPACT Model, 2012 simulations

‐20

‐10

0

10

20

30

40

50

60

ARG BRA MEX UNS

2010 2050NOCC 2050CSIRO_A1b

2050CSIRO_B1 2050MIROC_A1b 2050MIROC_B1

www.ifpri.org

Net Trade Soybean‐Projections, 2010 and 2050, various CC scenarios

Source: IFPRI IMPACT Model, 2012 simulations

‐

10

20

30

40

50

60

ARG BRA UNS

2010 2050NOCC 2050CSIRO_A1b

2050CSIRO_B1 2050MIROC_A1b 2050MIROC_B1

www.ifpri.org

TECHNOLOGY AND POLICY OPTIONS

ARE HIGHLY LOCALIZED

www.ifpri.org

Technologies PoliciesWater supply

Desalinization, treatment, Trans-boundary water transfer, water harvesting, dams

Regulations on priority uses,water quality regulations and enforcement

Water demand

Water use efficiency improvement through drip/new crop breeds,

Water charges, rationing, taxes, basin-wide management, water-energy-food nexus coordination

Solution space

www.ifpri.org Source: Background paper for the Bonn 2011 Nexus Conference: The Water, Energy and Food Security Nexus

People &Nature

Policies along the Water‐Energy‐Food Nexus

Improving Crop Productivity and Water Use Efficiency

Breeding can influence biomass/unit of water through transpiration rates and efficiency of biomass per unit of transpiration• Use of biotechnology and marker‐assisted selection is a

necessity for significant progress in the longer term• Many interlinked processes and factors underlie plant water

needs; additional progress depends on combination of disciplines

• Incorporating physiological and agronomic expertise into the design of transgenic experiments is crucial in realizing improvements in water productivity

www.ifpri.org

IMPROVED IRRIGATION TECHNOLOGIES Irrigation was triggered whenever

crop needed water (automatic). Improved irrigation technologies

effectively saved water.

Change in irrigation water use by region

Source: IFPRI crop model results 2012

Management Practices for More Efficient Water Use

Enhanced water infiltration: mulching; deep tillage; contour farming; special terraces (e.g., flat‐channel)

Decrease soil water evaporation: conservation tillage (e.g., no‐till or minimum till)

Deficit irrigation: apply predetermined percentage of calculated potential plant water

• Mild soil drying results in restricted shoot and leaf growth, reducing competition within the plant for reproductive development, increasing the harvest index and crop yield

Advanced irrigation technology (drip, micro‐sprinkler, real‐time management)

Water Rights and Markets: Advantages• Empowerment of water user by requiring consent and compensation for water transfers

• Markets in tradable water rights induce users to consider the full opportunity cost of water, providing incentives to conserve and gain additional income through the sale of saved water

• Incentives for water users to internalize the external costs imposed by their water use, reducing the pressure to degrade resources

• Particularly useful with climate variability/climate change

Water Rights, Water Pricing and Water Markets

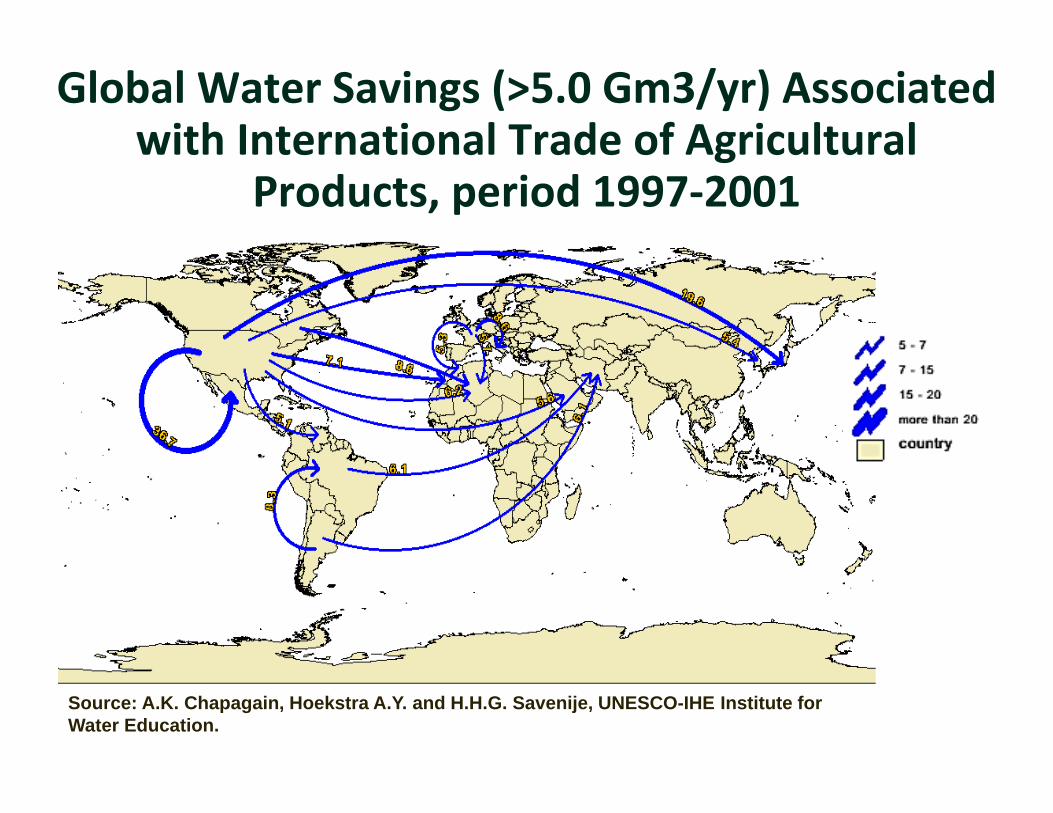

Global Water Savings (>5.0 Gm3/yr) Associated with International Trade of Agricultural

Products, period 1997‐2001

Source: A.K. Chapagain, Hoekstra A.Y. and H.H.G. Savenije, UNESCO-IHE Institute for Water Education.

www.ifpri.org

Invest more in agricultural R&D ‐ targeted increasingly to water productivity, not just land productivity

Modernize crop water productivity breeding programs in the Americas through provision of genomics, high throughput gene‐sequencing, bio‐informatics and computer tools

Reduce subsidies that distort production decisions and encourage water use beyond economically appropriate levels• Fertilizer, energy, water subsidies• Savings invested in activities that boost farm output and

income

Key Policies

www.ifpri.org

Rise in real prices of natural resources increases importance of market‐based approaches for managing environmental services and demands solutions that support water, energy and food security

Increased investment in household water supply & sanitation, but also irrigation, emphasizing technology (drip, micro‐sprinkler, real‐time management), and selected surface and groundwater storage systems

Given the scarcity of public resources, these investments need to increasingly involve Public‐Private Partnerships (PPP).

Focus on addressing growing water quality challenges

Key Policies

www.ifpri.org

NA significantly water‐scarcer than LAC, but both regions do well compared to Asia and SSA

The important food trade role of LAC and NA will put growing pressure on water resources in the region

This pressures will be compounded by climate change, either nationally or through increased demand for regional products

This needs increased focus on “water‐smart” breeding, machinery, other inputs and storage investments across the water‐energy‐food nexus, with attention to both water quantity and quality

Summary