the new service economy. development of the u.s. service sector

Post on 20-Dec-2015

215 views

TRANSCRIPT

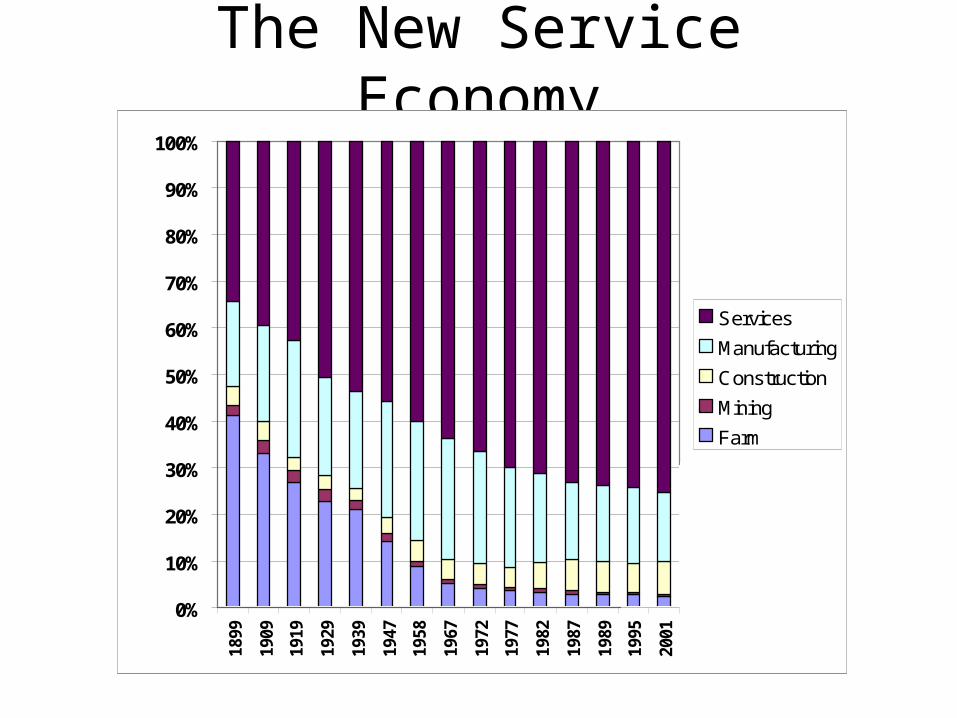

The New Service Economy

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1899

1909

1919

1929

1939

1947

1958

1967

1972

1977

1982

1987

1989

1995

2001

Services

Manufacturing

Construction

Mining

Farm

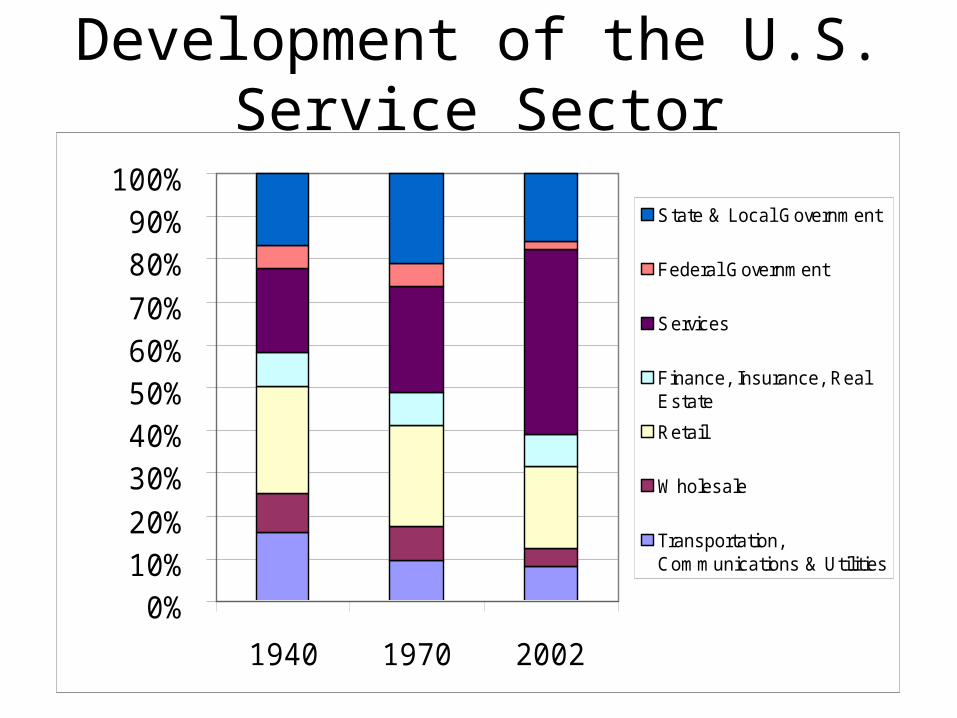

Development of the U.S. Service Sector

0%10%20%

30%40%50%60%70%

80%90%

100%

1940 1970 2002

State & Local Government

Federal Government

Services

Finance, Insurance, RealEstate

Retail

W holesale

Transportation,Communications & Utilities

Decomposition of Services

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1940 1970 2002

Consumer Services

Health Services

Producer Services

Producer ServicesWhy the rapid growth?

(1) Growth in intermediate demands

(2) Growth in final demands

(3) Slow productivity improvement (?historic?)

(4) Trade in Services & Import Substitution

An An overview of some key trends, largely drawn from Beyers research.

The Growing Investment In IT

Source:Digital Economy 2003

The Increase in Productivity Growth

Source:DigitalEconomy 2003

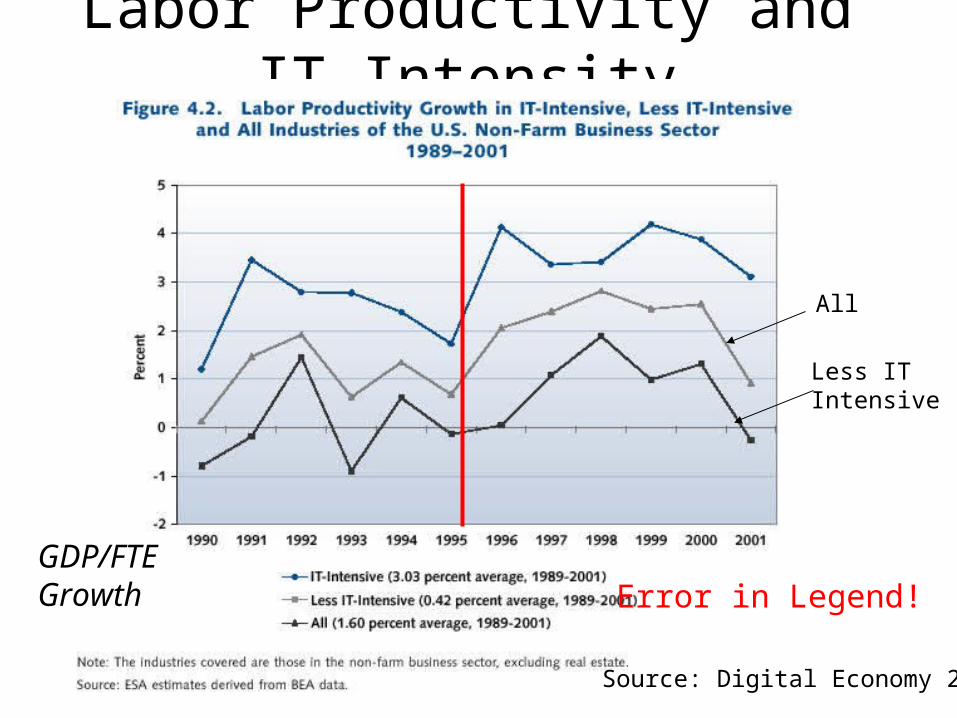

Labor Productivity and IT Intensity

Source: Digital Economy 2003

Error in Legend!

All

Less ITIntensive

GDP/FTEGrowth

Labor Productivity Growth

Source: DigitalEconomy 2003

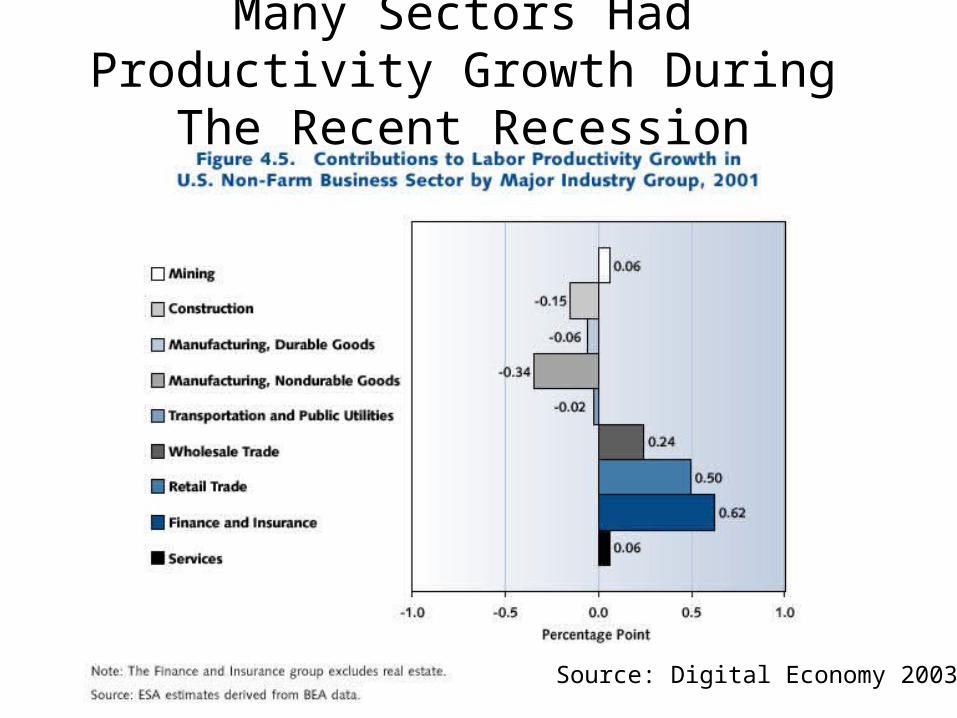

Many Sectors Had Productivity Growth During The Recent Recession

Source: Digital Economy 2003

Beyers Producer Services Research

• Funded by NSF and ERS

• Telephone Interviews with 665 producer service establishments

• Located in Urban and Rural Areas

• Typical Interview lasted about 45 minutes

• Selected findings

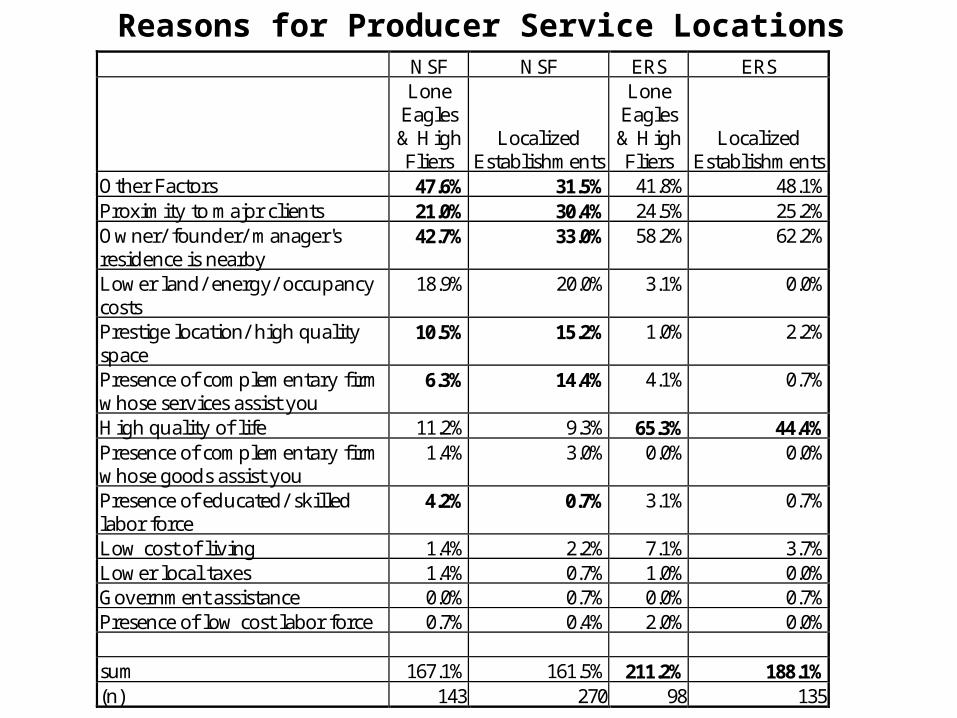

NSF NSF ERS ERSLone

Eagles& HighFliers

LocalizedEstablishments

LoneEagles& HighFliers

LocalizedEstablishments

Other Factors 47.6% 31.5% 41.8% 48.1%Proximity to major clients 21.0% 30.4% 24.5% 25.2%Owner/ founder/ manager'sresidence is nearby

42.7% 33.0% 58.2% 62.2%

Lower land/ energy/ occupancycosts

18.9% 20.0% 3.1% 0.0%

Prestige location/ high qualityspace

10.5% 15.2% 1.0% 2.2%

Presence of complementary firmwhose services assist you

6.3% 14.4% 4.1% 0.7%

High quality of life 11.2% 9.3% 65.3% 44.4%Presence of complementary firmwhose goods assist you

1.4% 3.0% 0.0% 0.0%

Presence of educated/ skilledlabor force

4.2% 0.7% 3.1% 0.7%

Low cost of living 1.4% 2.2% 7.1% 3.7%Lower local taxes 1.4% 0.7% 1.0% 0.0%Government assistance 0.0% 0.7% 0.0% 0.7%Presence of low cost labor force 0.7% 0.4% 2.0% 0.0%

sum 167.1% 161.5% 211.2% 188.1%(n) 143 270 98 135

Reasons for Producer Service Locations

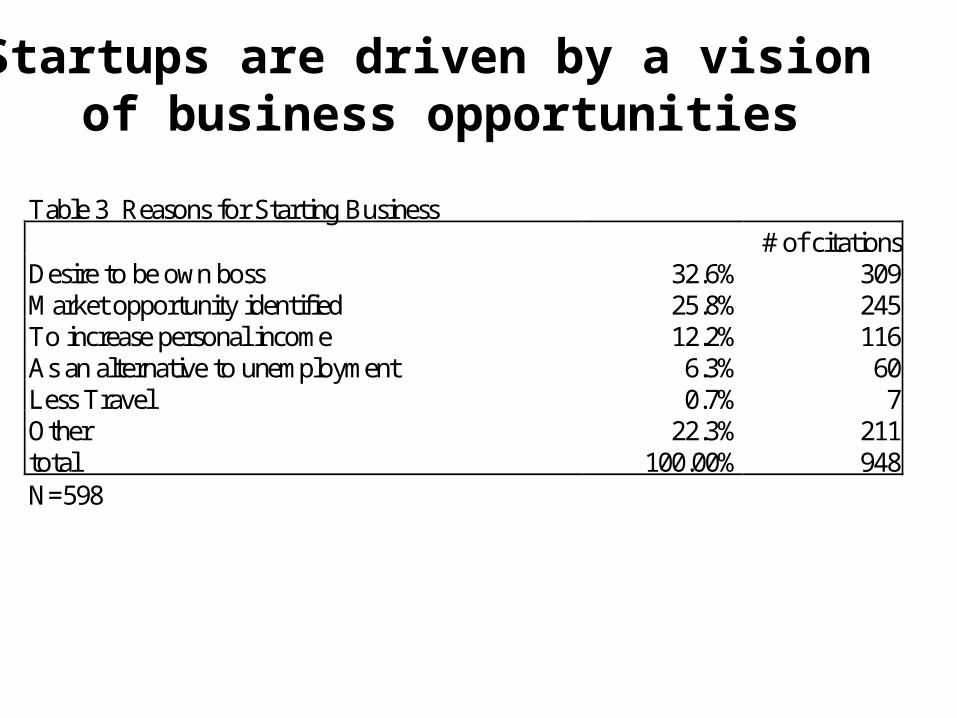

Table 3 Reasons for Starting Business# of citations

Desire to be own boss 32.6% 309Market opportunity identified 25.8% 245To increase personal income 12.2% 116As an alternative to unemployment 6.3% 60Less Travel 0.7% 7Other 22.3% 211total 100.00% 948N=598

Startups are driven by a vision of business opportunities

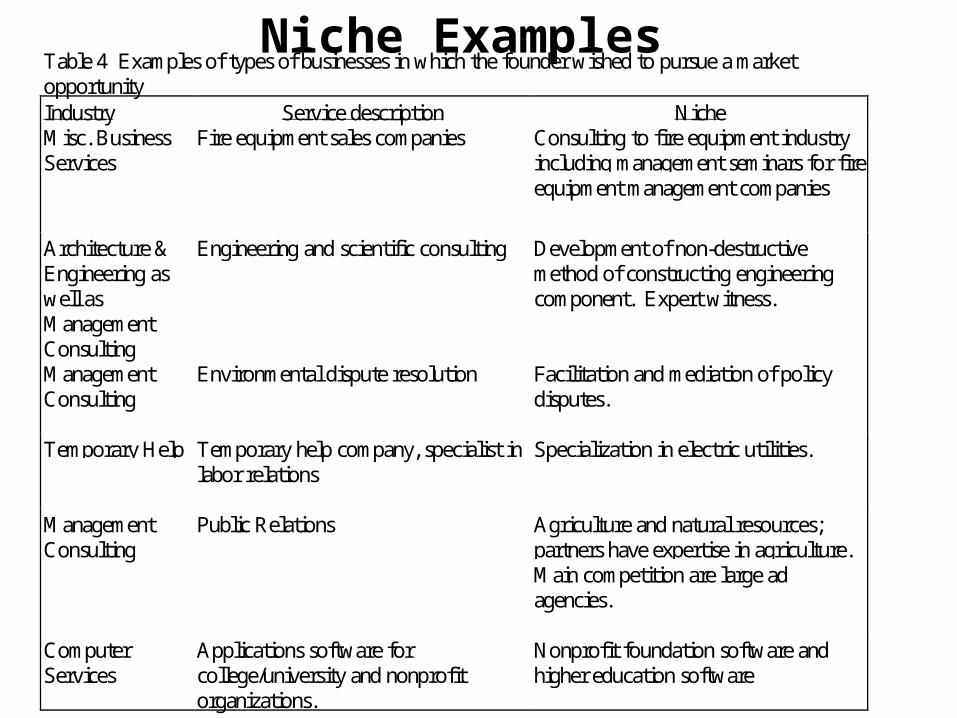

Table 4 Examples of types of businesses in which the founder wished to pursue a marketopportunityIndustry Service description NicheMisc. BusinessServices

Fire equipment sales companies Consulting to fire equipment industryincluding management seminars for fireequipment management companies

Architecture &Engineering aswell asManagementConsulting

Engineering and scientific consulting Development of non-destructivemethod of constructing engineeringcomponent. Expert witness.

ManagementConsulting

Environmental dispute resolution Facilitation and mediation of policydisputes.

Temporary Help Temporary help company, specialist inlabor relations

Specialization in electric utilities.

ManagementConsulting

Public Relations Agriculture and natural resources;partners have expertise in agriculture.Main competition are large adagencies.

ComputerServices

Applications software forcollege/university and nonprofitorganizations.

Nonprofit foundation software andhigher education software

Niche Examples

Table 6 Percentage of establishments considering factor highly important as a reason forchanging their services.

Why Types of Services Have Changed: Total

Percent ofEstablishments

Citing OneFactor

Percent ofEstablishmentsCiting Multiple

FactorsChange in Market 44.5% 28.3% 52.7%Change in Client Expectations 36.1% 15.2% 45.2%Use of Computers and IT 31.1% 26.1% 31.5%Change in Government Regulations 23.9% 19.6% 21.9%Change in Employee Skills 18.9% 10.9% 20.5%

(Sample size) n=238 n=92 n=146

Most Companies are dynamic in changing their services,driven by changes in IT and a variety of related factors

How Establishments Organize to Do New Work

$65,000

$70,000

$75,000

$80,000

$85,000

$90,000

Ro

uti

ne

No

nro

uti

ne

Mix

ed

Pro

pri

eto

rs0%10%20%30%40%50%60%70%80%90%100%

Median Sales/ Employee

Median SalesGrowth Past 5Years

Ansoff’s Box

Presen

tNew

Product

/serv

ice

technolo

gies

Present New

Market type

New

Pre

sent

Mar

ket

geo

grap

hy

A

B

C

9 Strategies beyond A, B, and C

A - no changeB - all changeC - only geog. changes

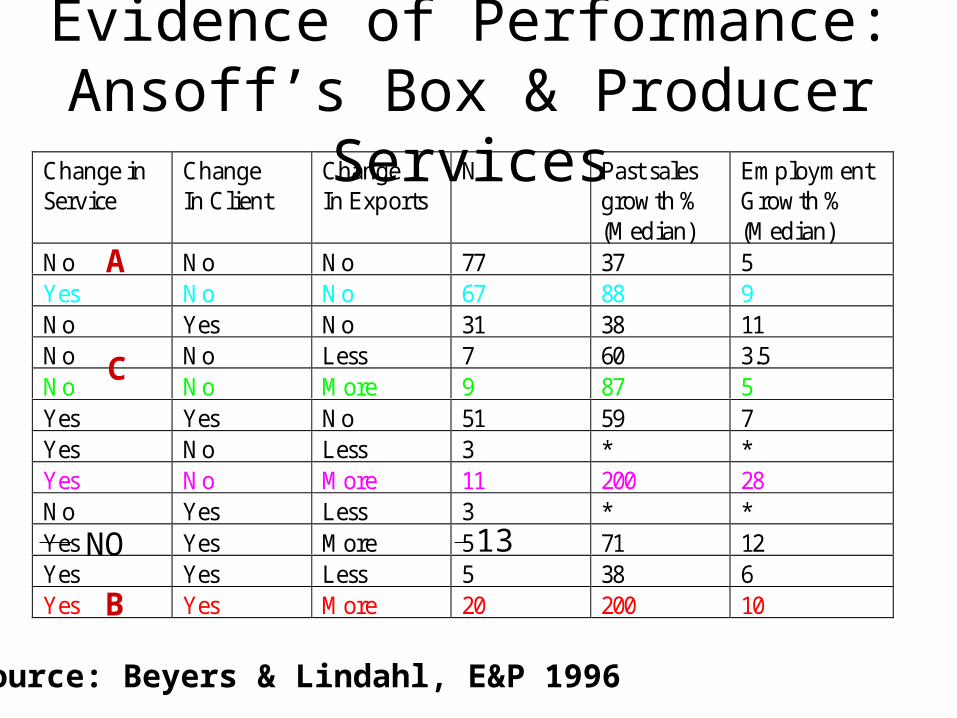

Evidence of Performance: Ansoff’s Box & Producer Services

Source: Beyers & Lindahl, E&P 1996

Change inService

ChangeIn Client

ChangeIn Exports

N Past salesgrowth %(Median)

EmploymentGrowth %(Median)

No No No 77 37 5Yes No No 67 88 9No Yes No 31 38 11No No Less 7 60 3.5No No More 9 87 5Yes Yes No 51 59 7Yes No Less 3 * *Yes No More 11 200 28No Yes Less 3 * *Yes Yes More 5 71 12Yes Yes Less 5 38 6Yes Yes More 20 200 10

A

B

C

NO 13

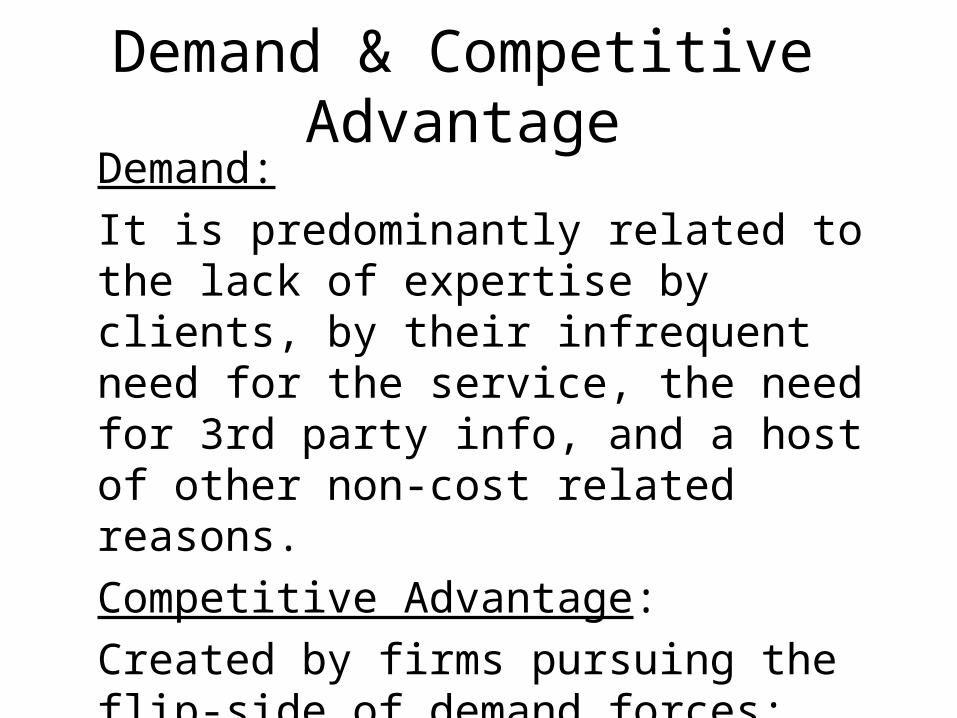

Demand & Competitive AdvantageDemand:

It is predominantly related to the lack of expertise by clients, by their infrequent need for the service, the need for 3rd party info, and a host of other non-cost related reasons.

Competitive Advantage:

Created by firms pursuing the flip-side of demand forces: Differentiation, specialization, niching, collaboration, use of specialized subcontractors, etc. Not Cost.

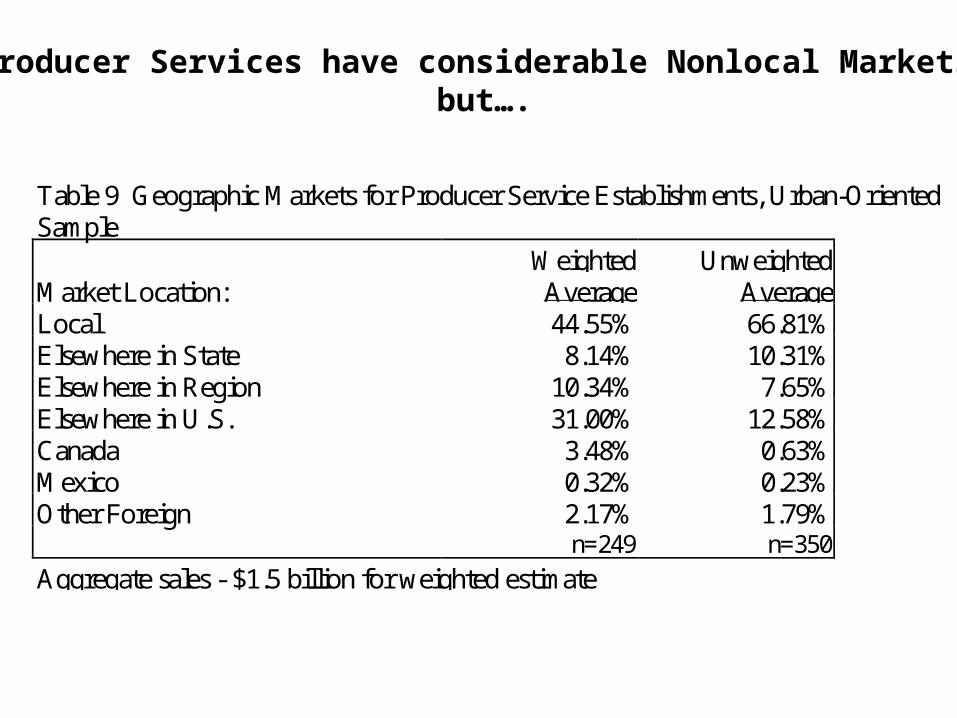

Table 9 Geographic Markets for Producer Service Establishments, Urban-OrientedSample

Market Location:WeightedAverage

UnweightedAverage

Local 44.55% 66.81%Elsewhere in State 8.14% 10.31%Elsewhere in Region 10.34% 7.65%Elsewhere in U.S. 31.00% 12.58%Canada 3.48% 0.63%Mexico 0.32% 0.23%Other Foreign 2.17% 1.79%

n=249 n=350

Aggregate sales - $1.5 billion for weighted estimate

Producer Services have considerable Nonlocal Markets,but….

Figure 3 Frequency of Export Market Percentages

0

20

40

60

80

100

120

140

96

-10

0

86

-95

76

-85

66

-75

56

-65

46

-55

36

-45

26

-35

16

-25

6-1

5

0-5

% Nonlocal Sales

# o

f o

bs

erv

ati

on

s

Rural

Urban

Producer Service Businesses have Bifurcated Markets:They Tend to be Local or Export

Local FirmsLone Eagles & High Fliers

These data are indicative of market orientation of New Economy firms

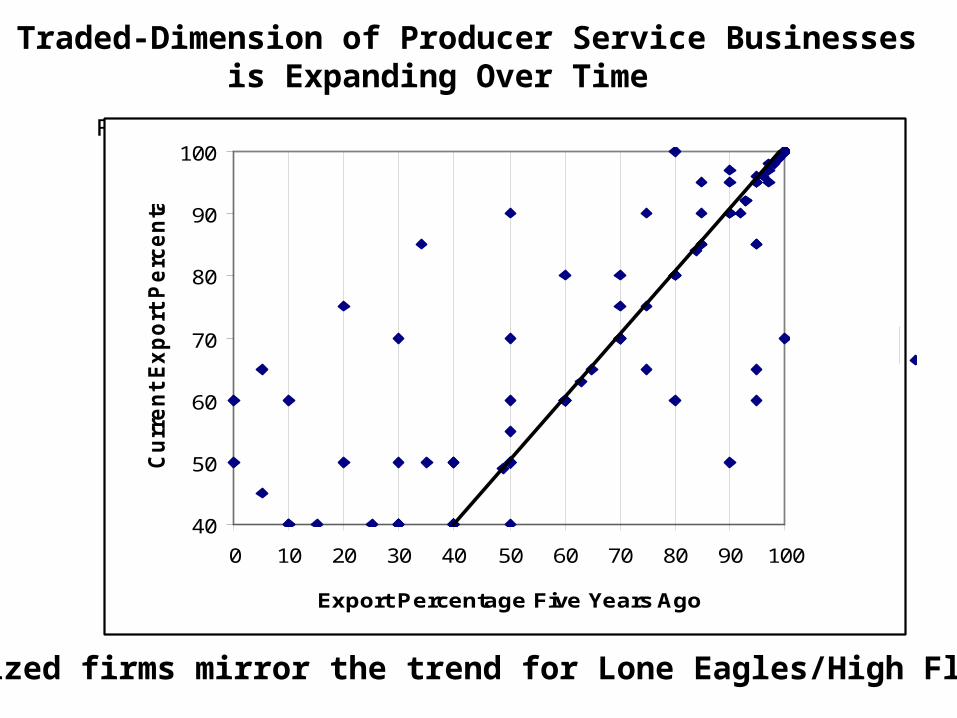

Figure 4 Lone Eagles and High Fliers: Exports Five Years Ago and Exports Today*

40

50

60

70

80

90

100

0 10 20 30 40 50 60 70 80 90 100

Export Percentage Five Years Ago

Cu

rre

nt

Ex

po

rt P

erc

en

tag

e

The Traded-Dimension of Producer Service Businesses is Expanding Over Time

Localized firms mirror the trend for Lone Eagles/High Fliers

Possible Development Sequence

Table 3 Percentage of Establishments Considering Factors to be Highly Important as aMeans of Producing and Delivering Their Services (1)

Current (2)

Increases (3)

Decreases Face to face conversations at clients offices 40.8% 0.6% 2.0% Face to face conversations at establishment office 46.2% 2.0% 2.7% Telephone Conversations 47.1% 2.6% 0.7% Video Conferencing 0.0% 1.1% 0.5% Computer File Transfer - via modem direct 11.7% 14.3% 0.4% - via E mail, internet 6.8% 9.9% Zero via LAN 2.6% 3.2% Zero via WAN 0.8% 1.4% Zero via Mail/Courier 10.5% 11.7% 0.4% Written/Graphical Documents - face to face @ client 36.1% 1.2% 1.0% - face to face @ estab. 28.3% 0.5% 1.6% - mail/courier 39.1% 1.7% 0.7% - Fax 39.4% 24.2% Zero Other: Satellite Uplinks 0.6% 1.1% Zero Other 3.0% 1.1% Zero 76.4% 10% Number of highly important cites/business 3.13

Source: (Beyers 2000)

Face to Face Communication Is Key and is Not Diminishing in Its Importance

Recognition of Producer Services as a Part of the Economic Base

• Historic metro concentration

• Recent rural deconcentration

• Role in “Edge Cities”

• The “New Economy.”

• --Producer Services as a progenitor to the New Economy:

–now multimedia, online retail, .com,–.org, .edu; telemedicine, teleservices, tele?; content providers; media conduits; delivery agents, etc.

Implications for Settlements for the New Economy

? Will this fuel decentralization of work?

? Or, will the power of agglomerations ?continue? To win out?

? What will happen to Edge Cities? Central Cities? What difference does it make where we focus on….Friday Harbor, Roslyn, Enterprise, Driggs, Missoula, Bellevue, Bend,

Beaverton, Darrington, Sun City, Corvallis

New Points?