©the national board of accountants and auditors, …nbaa.go.tz/2019/march/final.pdf(i ) explain why...

TRANSCRIPT

©The National Board of Accountants and Auditors, November 2018

Contents

Questions Page

C1 – Corporate Reporting ………………………………………. 1

C2 – Auditing and Assurance …….......……................................. 13

C3 – Business and Corporate Finance ………………………….. 23

C4 – Public Finance and Taxation II ………………………….. 32

Suggested Answers Page

C1 – Corporate Reporting …………………………………… 42

C2 – Auditing and Assurance …….......……............................ 60

C3 – Business and Corporate Finance ……………………… 78

C4 – Public Finance and Taxation II ……………………… 93

Final Level, November 2018 1

EXAMINATION : FINAL LEVEL

SUBJECT : CORPORATE REPORTING

CODE : C1

EXAMINATION DATE : WEDNESDAY, 31ST OCTOBER 2018

TIME ALLOWED : THREE HOURS (9:00 A.M. – 12:00 NOON)

---------------------------------------------------------------------------------------------------------

GENERAL INSTRUCTIONS

1. There are TWO Sections in this paper. Sections A and B which comprise SIXquestions.

2. Answer question ONE in Section A.

3. Answer ANY THREE questions in Section B.

4. In total, answer FOUR questions.

5. Show clearly all your workings in the respective answers where applicable.

6. Calculate your answers to the nearest one decimal point where necessary.

7. This question paper comprises 12 printed pages.

________________________

Final Level, November 20182

------------------------------------------------------------------------------------------------------SECTION A

Compulsory question------------------------------------------------------------------------------------------------------

QUESTION 1

(a) Utata is a private mutual fund registered under the laws of Tanzania for over 20years. Utata obtains funds from a large group of investors and provides thoseinvestors with returns and investment management services. Utata’s mainbusiness line has been to acquire portfolios of undervalued investments fromdiverse range of entities and later resell the investment at lucrative prices. Utatacurrently report all its investments on a ‘fair value through profit or loss’ basis.Early January 2017, Utata purchased 71% of the equity shares of Tanzania JuiceCompany (TJC). Following this acquisition some directors have feelings thatthe investment in TJC constitutes Utata’s controlling power, to direct relevantactivities of TJC, and consequently the latter has to be consolidated inaccordance with International Financial Reporting Standards (IFRSs). Othershave retained the long standing policy of Utata that, TJC will be treated like anyother investments. Utata asserts to comply with IFRSs. Utata’s board ofdirectors have approached you to present to them guidance on the divergentviews of the directors.

REQUIRED:

Prepare briefing notes to assist you in your presentation on how to deal with thematter in accordance with IFRSs. (8 marks)

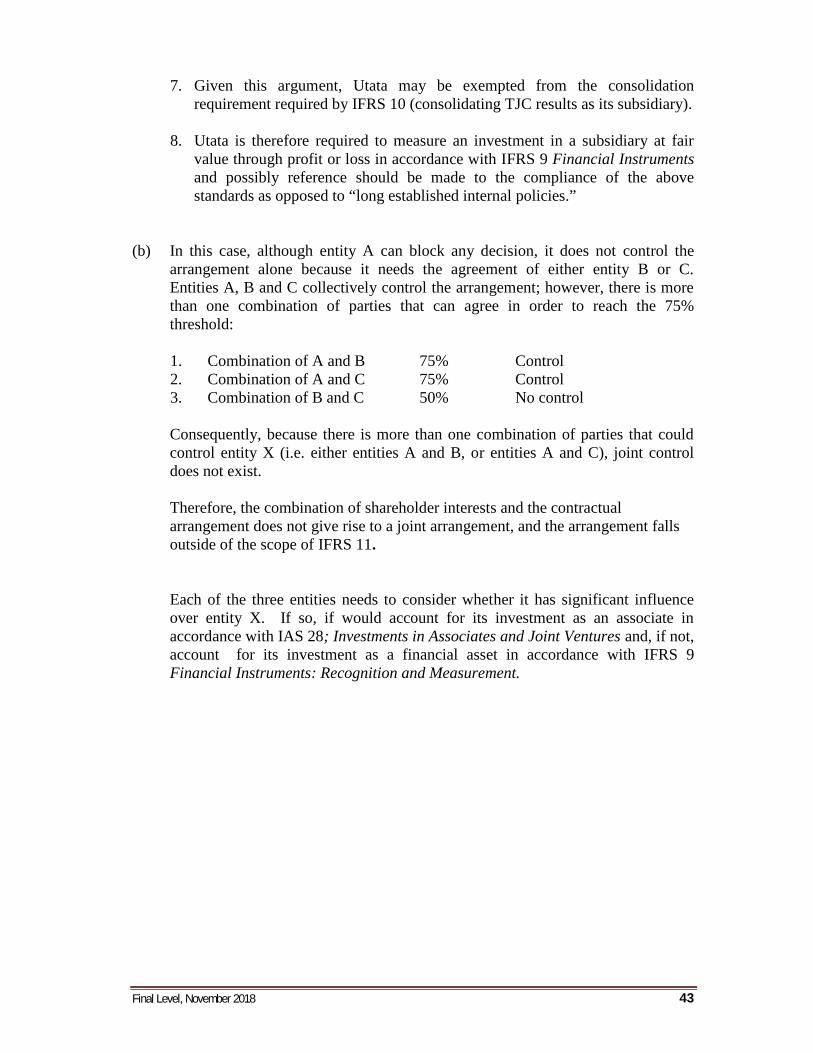

(b) Three parties A, B and C establish a separate legal entity (entity X) in which thethree parties have different shares of voting rights. Entity X’s activitiesconstitute a business (as defined in IFRS 3: Business Combination). The partiesA, B and C have 50%, 25% and 25% voting rights respectively in entity X. Acontractual arrangement entered into by the three parties specifies that at least75% of votes are required to make decisions about the relevant activities.

REQUIRED:

Assess the appropriate accounting treatment of entity X by each of the threeparties A, B and C with reference to their agreements on matters of voting anddecisions. (6 marks)

Final Level, November 2018 3

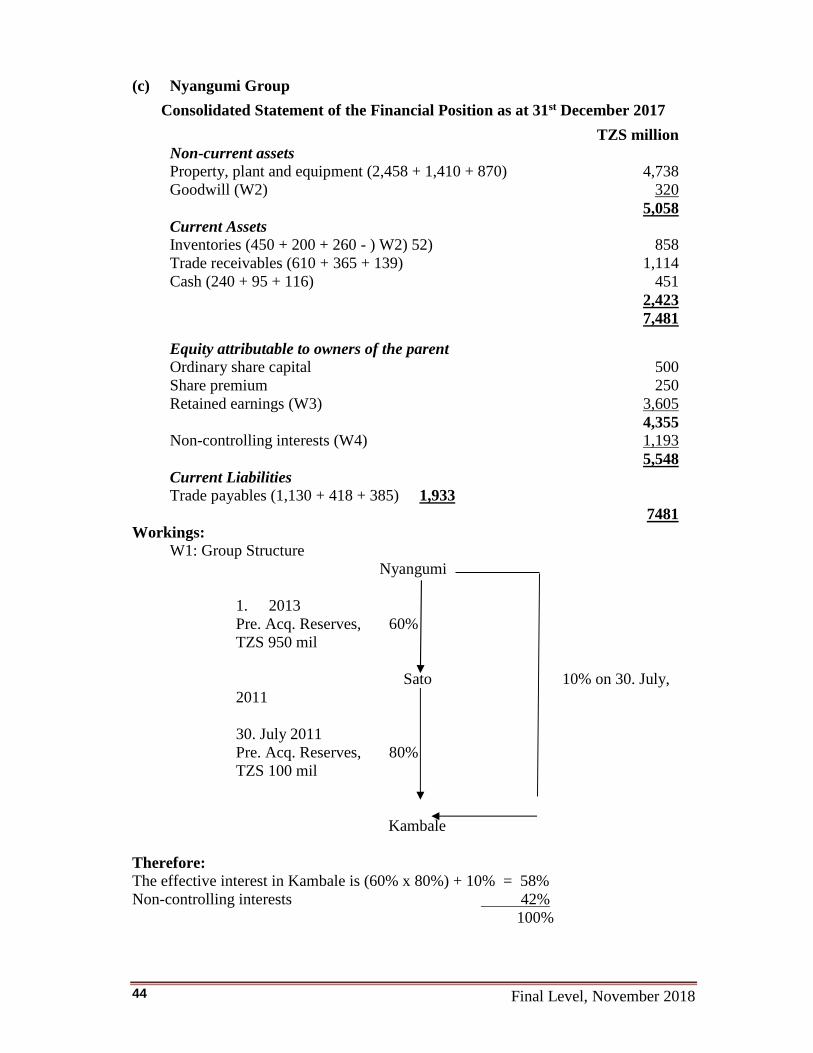

(c) You are given the following statements of financial position pertaining toNyangumi, Sato and Kambale entities as at 31st December 2017.

NyangumiTZS. million

SatoTZS.

million

KambaleTZS. million

Non-current assetsProperty, plant and equipment 2,458 1,410 870Investment in Sato 900 - -Investment in Kambale 27 240 -

3,385 1,650 870Current assetsInventories 450 200 260Trade receivables 610 365 139Cash 240 95 116

1,300 660 5154,685 2,310 1,385

EquityOrdinary share capital 500 200 100Share premium 250 120 50Retained earnings 2,805 1,572 850

3,555 1,892 1,000Current liabilitiesTrade payables 1,130 418 385

4,685 2,310 1,385

The following additional information is given:(1) On 1st January 2013 Nyangumi, a public limited company acquired 60% of

Sato, a public limited company. On 31st July 2011 Nyangumi acquired 10%of Kambale, a public limited company, and on the same day Sato acquired80% of Kambale.

(2) During the year 2017, Sato sold goods to Kambale for TZS.260 millionincluding a mark-up of 25%. All these goods remain in inventories at theyear end?

(3) The retained earnings of the three companies at the acquisition dates was(figures in millions of TZS.):

As at 31st July 2011 As at 1st January 2013Nyangumi 1,610 1,860Sato 700 950Kambale 40 100

(4) The book values of the identifiable net assets at the acquisition date areequivalent to their fair values. The fair value of Nyangumi’s 10% holdingin Kambale on 1st January 2013 was TZS.50 million

(5) Nyangumi and Sato hold their investments in subsidiaries at cost in theirseparate financial statements.

Final Level, November 20184

(6) It is the group policy to value the non-controlling interests at fair value atacquisition. The directors valued the non-controlling interests in Sato atTZS.536 million and Kambale at TZS.210 million on 1st January 2013.

(7) No impairment losses have been necessary in the consolidated financialstatements to date.

REQUIRED:

Prepare the consolidated statement of financial position of Nyangumi group asat 31st December 2017. (Show all the workings clearly) (26 marks)

(Total : 40 marks)

---------------------------------------------------------------------------------------------------------SECTION B

There are FIVE questions. Answer any THREE questions----------------------------------------------------------------------------------------------------------------------------- ----------------

QUESTION 2

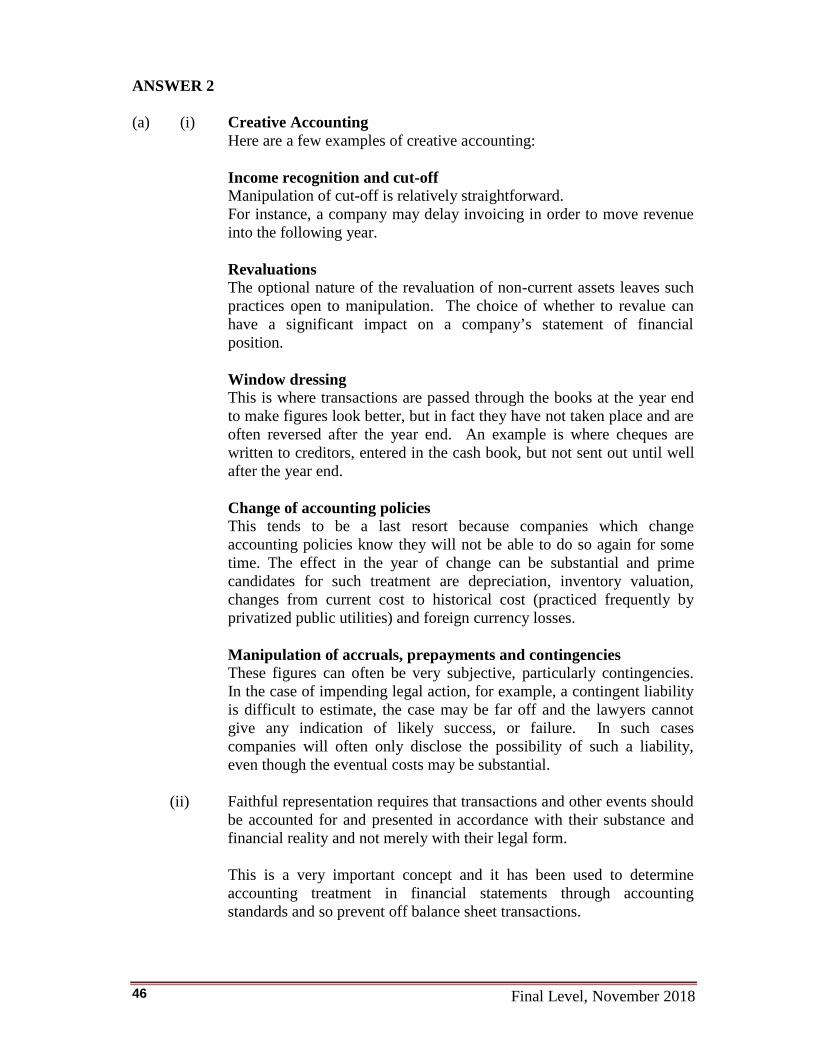

(a) In producing the Conceptual Framework for Financial Reporting and some ofthe current IFRSs, the International Accounting Standards Board (IASB) hashad to address the potential problem that the management of some companiesmay choose to adopt inappropriate accounting policies. These could have theeffect of portraying an entity’s financial position in a favourable manner. Insome countries this is referred to as ‘creative accounting’.

REQUIRED:

(i) Describe in broad terms, common ways in which management canmanipulate financial statements to indulge in ‘creative accounting’ andwhy they would wish to do so. (4 marks)

(ii) Explain with examples how IFRS seek to limit creative accounting ineach of the following areas of accounting:

Group accounting Financing non-current assets Measurement and disclosure of current assets (6 marks)

(b) Alpha, a public listed corporation, is considering how it should raise TZS.10billion of finance which is required for a major and vital non-current assetrenewal scheme that will be undertaken during the current year to 31st

December 2018. Alpha is particularly concerned about how analysts are likelyto react to its financial statements for the year to 31st December 2018. Presentforecasts suggest that Alpha’s earning per share and its financial gearing ratiosmay be worse than market expectations. Mr. Wanyemi, Alpha’s FinanceDirector, is in favour of raising the finance by issuing a convertible loan. Hehas suggested that the coupon (interest) rate on the loan should be 5%; this isbelow the current market rate of 9% for this type of loan. In order to make the

Final Level, November 2018 5

stock attractive to investors the terms of conversion into equity would be veryfavourable to compensate for the low interest rate.

REQUIRED:

(i) Explain why the Finance Director believes the above scheme mayfavourably improve Alpha’s earnings per share and gearing. (3 marks)

(ii) Describe how the requirements of IAS 33: Earnings per share and IAS32: Financial Instruments; presentation are intended to prevent theabove effects. (4 marks)

(c) The IASB Conceptual Framework requires information to reflect the substanceof a transaction for it to be reliable.

The substance of a transaction is its commercial effect. Normally this is thesame as its legal form but for complex transactions, this may not be the case.The general principle that results from the IASB Conceptual Framework is thatwhere the legal form of the transaction does not reflect its substance, the legalform should be set aside in order to reflect substance. This is known assubstance over form accounting.

REQUIRED:

Explain briefly why it is important for transactions to be accounted usingsubstance rather than legal form, and describe how financial statements can beadversely affected if the substance of transactions is not recorded. (3 marks)

(Total : 20 marks)

Final Level, November 20186

QUESTION 3

Wise Plan Ltd is a public company that would like to acquire 100% of a suitable privatecompany. It has obtained the following extracts of draft financial statements for twocompanies, Knowledge and Ourplan. They operate in the same industry and theirmanagements have indicated that they would be receptive to a takeover.

STATEMENT OF FINANCIAL POSITION AS AT 30TH SEPTEMBER 2018Knowledge Ourplan

TZS"000,000"

TZS"000,000"

TZS"000,000"

TZS"000,000"

AssetsNon-Current AssetsFreehold factory (note i) 4,400 nil

Owned plant (note ii) 5,000 2,200

Leases plant (note ii) nil 5,300

9,400 7,500Current AssetsInventory 2,000 3,600

Trade receivables 2,400 3,700

Bank 600 5,000 nil 7,300

Total Assets 14,400 14,800Equity and LiabilitiesEquity shares of TZS.1,000 each 2,000 2,000

Property revaluation reserve 900 nil

Retained earnings 2,600 3,500 800 800

5,500 2,800Non-Current LiabilitiesFinance lease obligation (note iii) nil 3,200

7% loan notes 3,000 nil

10% loan notes nil 3,000

Deferred tax 600 100

Government grants 1,200 4,800 nil 6,300Current LiabilitiesBank overdraft nil 1,200

Trade payables 3,100 3,800

Government grants 400 nil

Finance lease obligations (note iii) nil 500

Provisions 600 4,100 200 5,700Total Equity and Liabilities 14,400 14,800

Final Level, November 2018 7

STATEMENT OF PROFIT OR LOSS FOR THE YEAR ENDED30 SEPTEMBER 2018

Knowledge OurplanTZS

"000,000"TZS

"000,000"Revenue 12,000 20,500Cost of sales (10,500) (18,000)Gross profit 1,500 2,500Operating expenses (240) (500)Finance costs - Loan (210) (300)

- Overdraft nil (10)

- Lease nil (290)

Profit before tax 1,050 1,400Income tax expense (150) (400)Profit for the year 900 1,000Note: dividend paid during the year 250 700

Additional notes(i) Both companies operate from similar premises.(ii) Additional details of the two companies’ plants are:

Knowledge OurplanTZS “000,000” TZS “000,000”

Owned plant – cost 8,000 10,000Leased plant – original fair value Nil 7,500

There were no disposals of plant during the year by either company.

(iii) The interest rate implicit within Ourplan’s finance leases is 7.5% per annum. Forthe purpose of calculating ROCE and gearing, all finance lease obligations aretreated as long-term interest bearing borrowings.

(iv) The following ratios have been calculated for Knowledge and can be taken to becorrect:

Return on year end capital employed (ROCE) 14.8%(capital employed taken as shareholders’ funds pluslong-term interest bearing borrowings – see note (iii) above)

Gross profit margin 12.5%Operating profit margin 10.5%Current ratio 1.2:1Closing inventory holding period 70 daysTrade receivables’ collection period 73 daysTrade payables’ payment period (using cost of sales) 108 daysGearing (see note (iii) above) 35.3%

Final Level, November 20188

REQUIRED:

(a) Calculate for Ourplan the ratios equivalent to all those given for Knowledgeabove. (6 marks)

(b) Assess the relative performance and financial position of Knowledge and Ourplanfor the year ended 30th September 2018 to inform the directors of Wise Plan Ltdin their acquisition decision. (8 marks)

(c) Discuss potential problems of using ratios for comparison purposes, and proposeother relevant factors/information that should be considered by Wise Plan Ltd intheir acquisition decision. (6 marks)

(Total: 20 marks)

QUESTION 4

(a) Due to the complexity of International Financial Reporting Standards (IFRSs),judgements used at the time of transition to IFRSs have often resulted in priorperiod adjustments and changes in estimates being disclosed in financialstatements. The selection of accounting policies and estimation techniques areintended to aid comparability and consistency in financial statements.However, IFRSs also place particular emphasis on the need to take into accountqualitative characteristics and the use of professional judgement when preparingfinancial statements. Although IFRSs may appear prescriptive, the achievementof all the objectives for a set of financial statements will rely on the skills of thepreparer. Entities should follow the requirements of IAS 8: AccountingPolicies, Changes in Accounting Estimates and Errors when selecting orchanging accounting policies, changing estimation techniques, and correctingerrors. However, the application of IAS 8 is additionally dependent upon theapplication of materiality analysis to identify issues and guide reporting. Inmany cases, entities have to consider the acceptability of the use of hindsight intheir reporting.

REQUIRED:

(i) Discuss how judgment and materiality play a significant part in theselection of an entity’s accounting policies. (5 marks)

(ii) Explain the circumstances under which an entity may change itsaccounting policies, setting out how a change of accounting policy isapplied and the difficulties faced by entities where a change inaccounting policy is made. (7 marks)

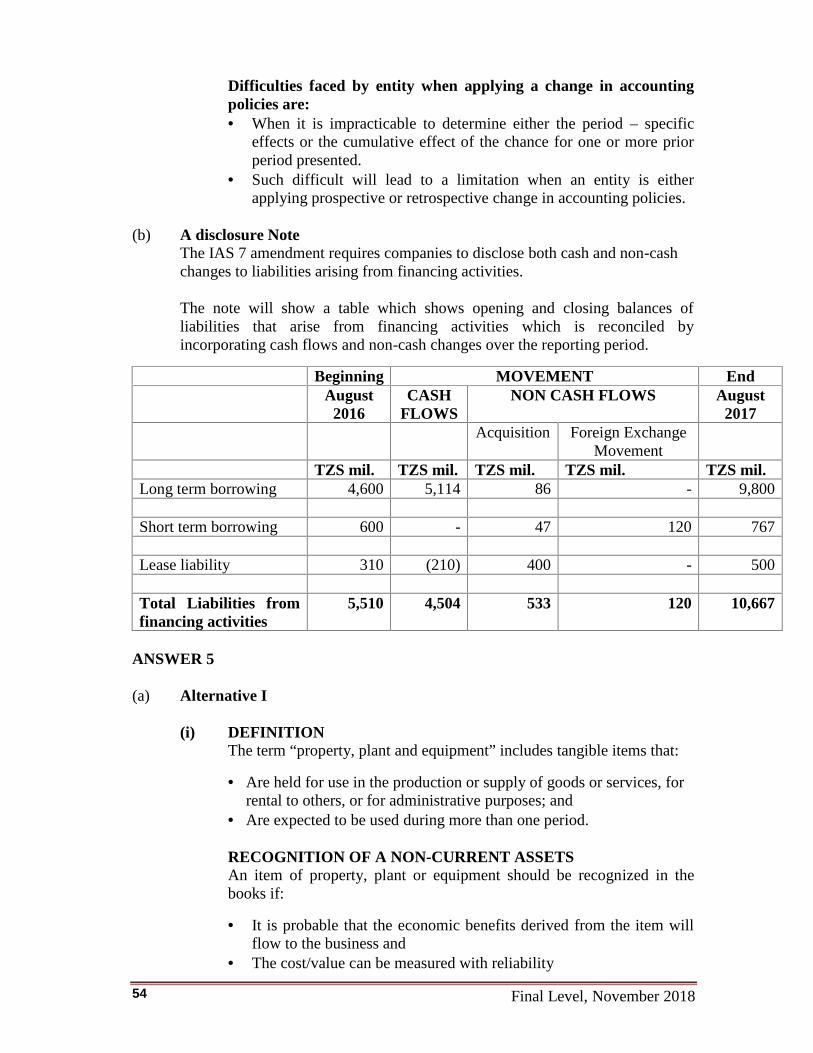

(b) The International Accounting Standards Board (IASB) had publishedamendments to IAS 7 'Statement of Cash Flows' which recently becameeffective (for annual periods that began on or after 1st January 2017). Theamendments were intended to clarify IAS 7 and improve information providedto users of financial statements about an entity's financing activities. These

Final Level, November 2018 9

require companies to disclose additional information that will assist investors inmaking net debt reconciliation.

Mtiririko Limited, a public listed company, has prepared a statement of cashflows for the year ended 31st August 2018. Under financing activities, it hasshown an increase in long-term borrowings to TZS.9,800 million, increase ofshort term borrowings to TZS.767 million and a decrease of lease liability toTZS.500 million.

As at 31st August 2017, Mtiririko Limited had shown in its financial statementslong term borrowings of TZS.4,600 million, short term borrowings of TZS.600millIion and capital element of lease liability of TZS.310 million.

During the year ended 31st August 2018 Mtiririko Limited acquired 90% ofshareholdings of Pambana Ltd for TZS.780 million. Pambana took a short termloan of TZS.47 million and a long term loan of TZS.86.million. Furthermore,during the year, Mtiririko took out a long term loan of TZS.6,114 million fromABCD bank and on 31st August 2018 the company paid TZS.1,400 million(Principal element being TZS.1,000 million and interest being TZS.400 million)to the bank as a liability payment installment. The TZS.400 million interest wasshown under operating activities in the statement of cash flows.

During the year Mtiririko also entered into a finance lease agreement to leaseequipment for TZS.400 million and had paid TZS.210 million in arrear off thecapital element of the lease liabilities. Interest of TZS.70 million on the leasewas also shown under operating activities in the statement of cash flows.

At the beginning of the year there was an American supplier whom Mtiririkoowed US Dollar 132,000, equivalent to TZS.190 million as at 1st September2017, but due to currency fluctuation the amount owing increased to TZS.310million at 31st August 2018. The company also had an overdraft of TZS.400million as at 31st August 2018.

REQUIRED:

Show the note to the statement of cash flows, required under the amended IAS7, which sets out the components of financing activities. (8 marks)

(Total : 20 marks)

Final Level, November 201810

QUESTION 5

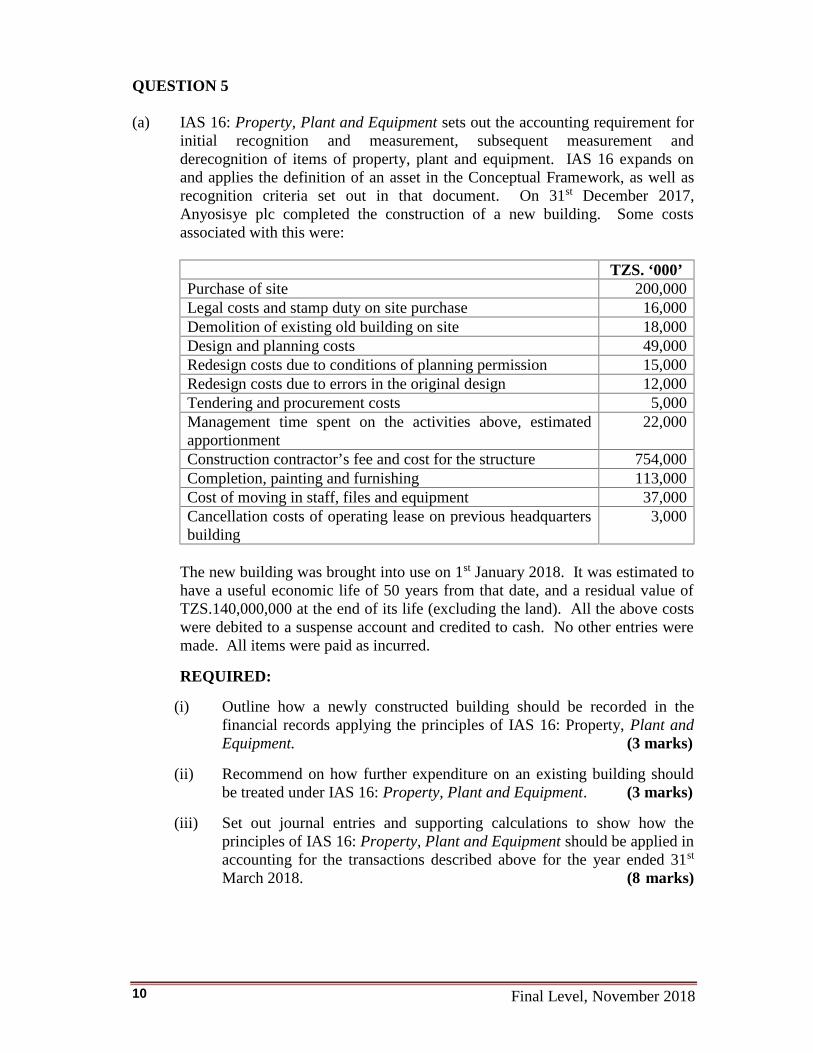

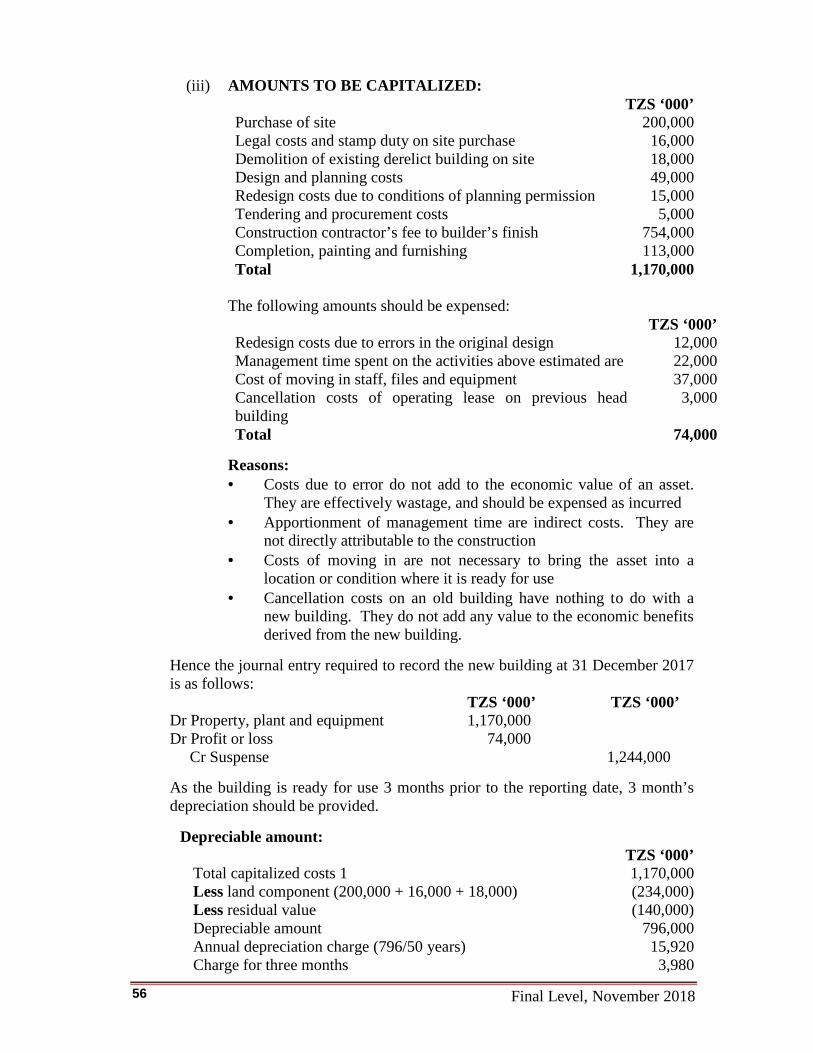

(a) IAS 16: Property, Plant and Equipment sets out the accounting requirement forinitial recognition and measurement, subsequent measurement andderecognition of items of property, plant and equipment. IAS 16 expands onand applies the definition of an asset in the Conceptual Framework, as well asrecognition criteria set out in that document. On 31st December 2017,Anyosisye plc completed the construction of a new building. Some costsassociated with this were:

TZS. ‘000’Purchase of site 200,000Legal costs and stamp duty on site purchase 16,000Demolition of existing old building on site 18,000Design and planning costs 49,000Redesign costs due to conditions of planning permission 15,000Redesign costs due to errors in the original design 12,000Tendering and procurement costs 5,000Management time spent on the activities above, estimatedapportionment

22,000

Construction contractor’s fee and cost for the structure 754,000Completion, painting and furnishing 113,000Cost of moving in staff, files and equipment 37,000Cancellation costs of operating lease on previous headquartersbuilding

3,000

The new building was brought into use on 1st January 2018. It was estimated tohave a useful economic life of 50 years from that date, and a residual value ofTZS.140,000,000 at the end of its life (excluding the land). All the above costswere debited to a suspense account and credited to cash. No other entries weremade. All items were paid as incurred.

REQUIRED:

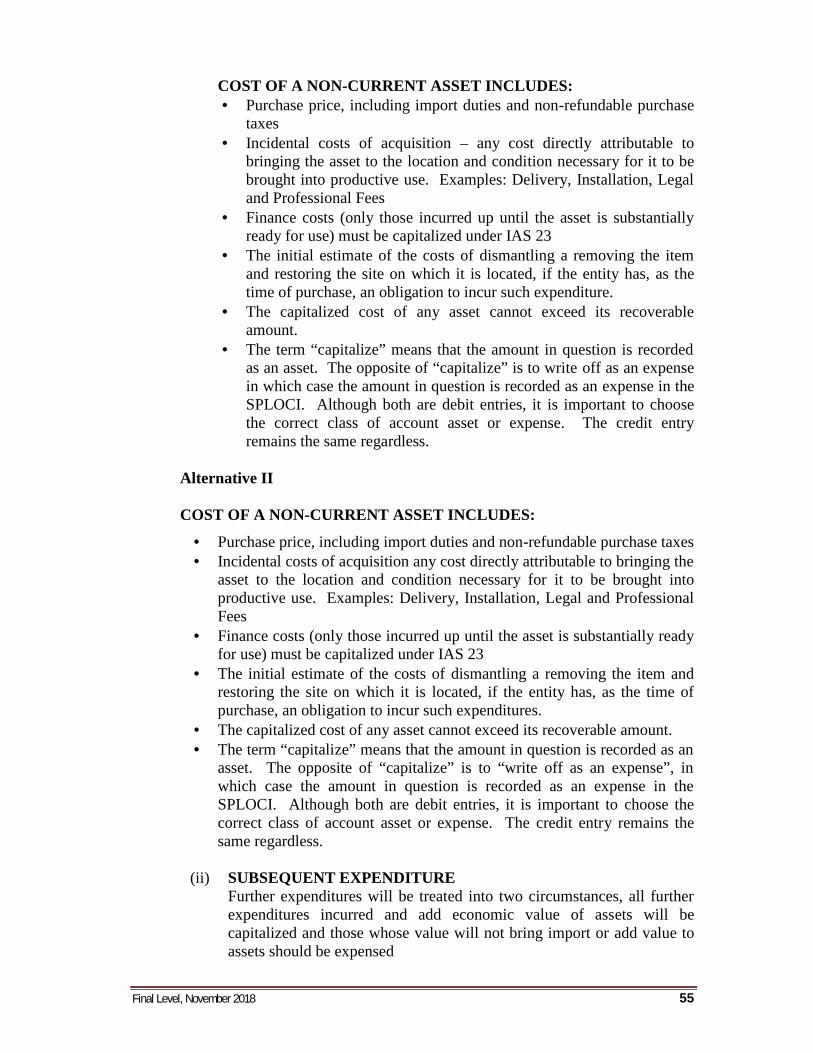

(i) Outline how a newly constructed building should be recorded in thefinancial records applying the principles of IAS 16: Property, Plant andEquipment. (3 marks)

(ii) Recommend on how further expenditure on an existing building shouldbe treated under IAS 16: Property, Plant and Equipment. (3 marks)

(iii) Set out journal entries and supporting calculations to show how theprinciples of IAS 16: Property, Plant and Equipment should be applied inaccounting for the transactions described above for the year ended 31st

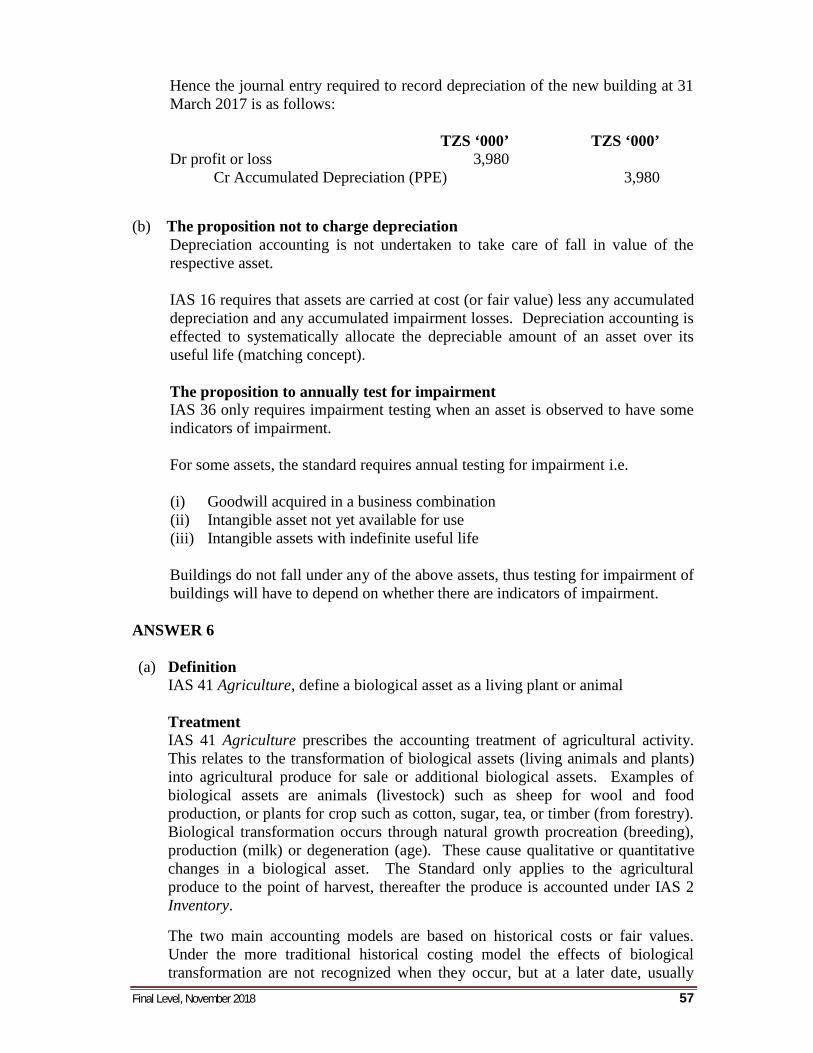

March 2018. (8 marks)

Final Level, November 2018 11

(b) Kavenuka is a Senior Assistant Accountant at Anyosisye plc in (a) above. Hehas recommended that no depreciation should be charged to the building, sinceit is hardly the case that its value will fall in the near future. He recommendsinstead, that impairment testing be done every year to confirm whether its valueis decreasing or not.

REQUIRED:

Comment on the propositions of Kavenuka with reference to relevantInternational Financial Reporting Standards (IFRSs). (6 marks)

(Total : 20 marks)QUESTION 6

(a) Agriculture is one of the world's largest industry. In some countries it is themainstay of the gross domestic product. Yet until January 2003 when the IASBissued IAS 41 Agriculture, no major accounting standard setting body hadissued a comprehensive pronouncement on this topic. IAS 41 introduced whatsome would say are radical changes in the way agricultural enterprises shouldaccount for biological assets.

REQUIRED:

Define biological assets and explain how IAS 41 requires them to be treated inthe financial statements. (5 marks)

(b) Miti Safi na Nyuki Brothers (MSNB) is a Limited Company that wasincorporated to invest in forest and bee resources in general and to collectforestry and beekeeping revenues. As at 30th June 2018, it had a forestplantation in the Sourthen Highland part of Tanzania in Njombe regionconsisting of 250,000 Eucalyptus trees that were planted 2 years earlier.

Maturity and ideal harvesting age of Eucalyptus trees are dependent on theintended purpose or market. The harvesting age significantly varies from 3 to 4years (construction poles), 8 to 15 years (transmission poles) to as late as 20years for timber production. The company’s weighted average cost of capital is9% per annum.

The accountants of the MSNB were unable to value the 250,000 Eucalyptustrees for inclusion in the company’s statement of financial position as biologicalassets as only mature Eucalyptus trees for timber production had established fairvalues by reference to a quoted price in an active market. The fair value(inclusive of current transport costs) for a mature tree for timber production ofthe same grade as in the plantation is:

As at 1st July 2017: TZS 6,000 As at 30th June 2018: TZS 7,000

Final Level, November 201812

REQUIRED:

(i) Determine the amount of the biological asset to be reported as at 1st July2017 and 30th June 2018. (3 marks)

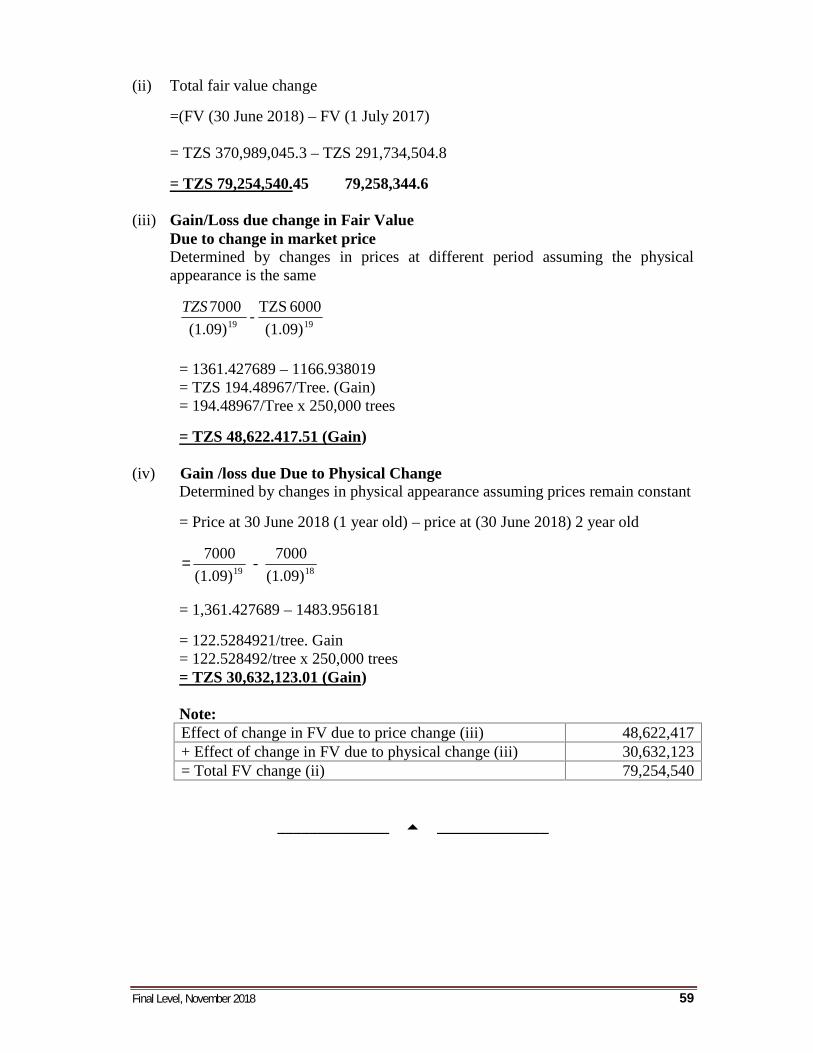

(ii) Determine the total fair value change of the immature trees during theyear ended 30th June 2018. (2 marks)

(iii) Determine the gain or loss due to changes in fair values as a result of theeffects of change in market price, and (5 marks)

(iv) Determine the gain or loss due to changes in fair values as a result of thephysical change (growth) of the trees in the forest plantation. (5 marks)

(Total: 20 marks)

________________ _______________

Final Level, November 2018 13

EXAMINATION : FINAL LEVEL

SUBJECT : AUDITING AND ASSURANCE

CODE : C2

EXAMINATION DATE : TUESDAY, 30TH OCTOBER 2018

TIME ALLOWED : THREE HOURS (9:00 A.M. – 12:00 NOON)

---------------------------------------------------------------------------------------------------------

GENERAL INSTRUCTIONS

1. There are TWO Sections in this paper. Sections A and B which comprise atotal of SIX questions.

2. Answer question ONE in Section A.

3. Answer ANY THREE questions in Section B.

4. In total answer FOUR questions.

5. Marks are shown at the end of each question.

6. Presentation, clarity of expression, logic of arguments and the use of lucidEnglish will be taken into account in the assessment of candidates’performance.

7. This question paper comprises 10 printed pages.

________________________

Final Level, November 201814

---------------------------------------------------------------------------------------------------------SECTION A

Compulsory question---------------------------------------------------------------------------------------------------------

QUESTION 1

(a) Your firm has five offices all over Tanzania and it specialises in the provision ofaudit and tax advisory services to clients in the entertainment and mediaindustries. The Finance Director of Nguvu Ltd (Nguvu) has recently requestedyour firm to accept appointment as external auditor for the year ended 30th

September 2018.

Nguvu’s previous auditors have not been reappointed. Nguvu is a music eventscompany that has its head office in Dar es Salaam. It organises and performseven live-music events held in the same seven locations in Tanzania each year.Music events are large-scale events, held outdoors, where a variety of musiciansperform live on an open-air stage. The musicians performance vary betweenlocations from year to year. Each event is held over a weekend (Saturday andSunday) between June and August.

Tickets can be purchased online in advance from Nguvu’s website or on the dayof the event at the entrance gate. Online tickets are available for the followingyear’s event one week after the current year’s events have been completelyperformed. The online Tickets bought are paid for by credit card. Ticketspurchased at the entrance gate can be paid for by credit card or by cash. Cashcollected at the entrance gate is periodically transferred to the on-site cash officeduring the day.

Customers who purchase their tickets online are required to present theirbooking confirmation at the ‘wristband exchange’ where they receive awristband to wear during the event. Wristbands are colour-coded according tothe day of the event for which the ticket has been purchased. Customers whopurchase their tickets on the day of the event receive their wristband at theentrance gate. No customers are permitted to enter the event venue without thecorrect wristband.

Nguvu arranges musicians to perform at the events through the musician’sagent. Fees to well known musicians are usually agreed and paid in advance,either in Tanzanian shillings or in the musician’s local currency. Somemusicians ask for a portion of their fee to be paid in cash (Tanzanian shillings)on the day of their performance. Less well-known musicians are fully paid incash (Tanzania shillings) at the end of their performance. Cash fees arecollected by musicians, or their agents, at the on-site cash office.

Nguvu recruits a number of stewards for the duration of each event whose roleis to provide information and directions to customers. Other temporary staff areemployed to work at the entrance gate or in the wristband exchange. Stewardsand temporary staff are paid in cash at the on-site cash office at the end of eachevent.

Final Level, November 2018 15

Permission to hold each event has to be obtained annually from both the localpolice authority and the local council that is governing the local area where theevent is taking place. The local council determines the maximum number oftickets that may be sold for each day of an event.

The Finance Director of Nguvu has provided you with the followinginformation:(1) At one of the events in August 2018, a customer was seriously injured

after he gained access through the lighting pole and tried to climb it for abetter view of the stage. He fell down and got injured. He was unable towork since the accident event. Nguvu is currently being sued for damagesafter a national newspaper started a campaign on behalf of the injuredcustomer. There were no signs warning customers against climbing thelighting poles and no steward was present near the pole to guide thecustomers.

(2) During 2018, the weaker economic climate and unpredictable coldweather resulted in a decline in ticket sales. This, coupled with increasingcosts from the suppliers, has led to Nguvu’s decision to investigate thepossibility of expansion of its business to overseas. Negotiations areunderway to purchase the right to organize and perform an event in Kitwetown of Zambia. The purchase is to be funded by a bank loan currentlybeing considered by Nguvu’s bankers. As part of the loan negotiation thebank will require a copy of the audited financial statements.

The Finance Director has requested that the audit be completed and audit reportsigned by 3rd April 2019 so that the bank loan could be granted and the purchaseof the rights to perform the event in Kitwe be finalised by 10th April 2019. Inaddition to carrying out the statutory audit, the Finance Director has requestedyour firm to carry out a review of the controls at each event, in particular, thecontrols over cash and the wristband exchange process.

In the forthcoming year, he would like you to undertake a review of controls intwo events. The remaining five events should be reviewed in subsequent years,with two events being reviewed in 2020, other two events in 2021 and the finalevent in 2022. He has requested you to attend the Nguvu board meeting aftereach review so as to discuss your firm’s findings and present yourrecommendations.

REQUIRED:

(i) Explain the matters that you would consider and the procedures that youwould perform in order to decide whether to accept the appointment asexternal auditors of Nguvu. (4 marks)

(ii) Explain the matters that you would consider and the procedure that youwould perform in order to decide whether to accept the additional work oncontrols proposed by the Finance Director. (4 marks)

Final Level, November 201816

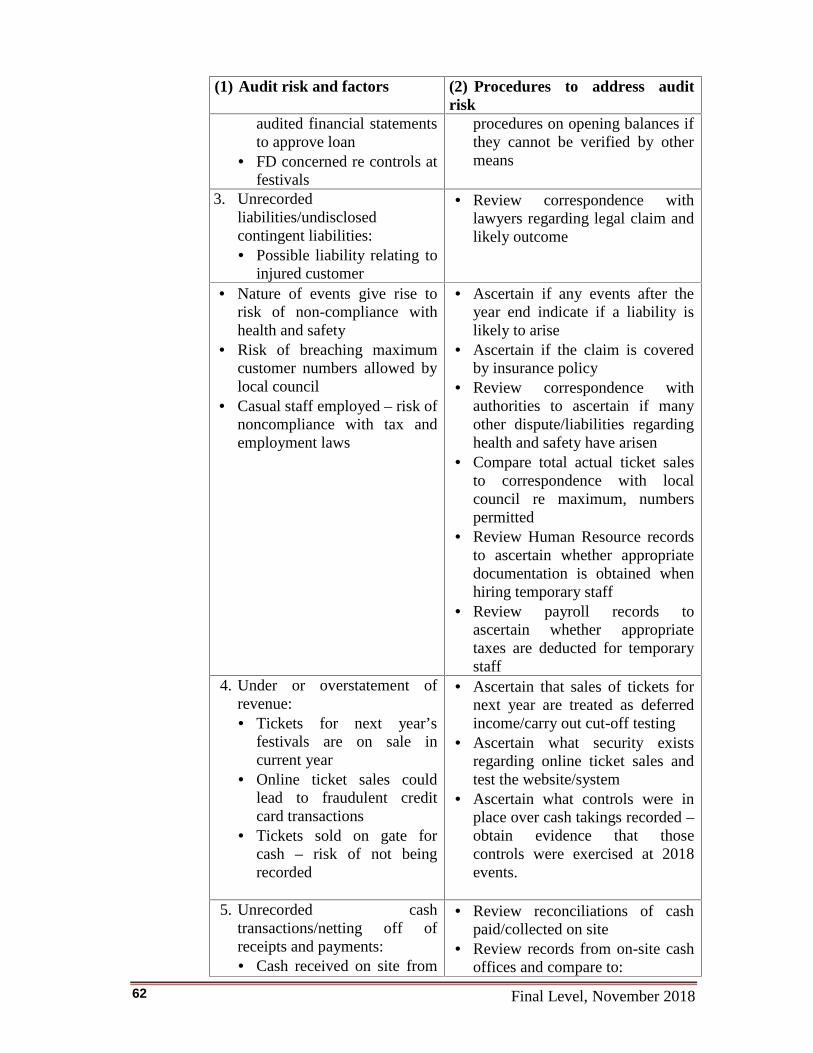

(iii) Identify, from the information provided in the scenario, the principal auditrisks in respect of the financial statements of Nguvu for the year ended30th September 2018. For each risk, list the factors which lead to itsidentification and outline the procedures that should be included in theaudit plan in order to address it. (12 marks)

(b) During your firm’s external audit of Hanyegwa Company Ltd (Hanyegwa) theaudit manager in charge has informed the firm that Hanyegwa has offered him arole as its new finance director. The audit manager first discussed the role withHanyegwa at the planning meeting for this year’s audit and that he intends toaccept the offer.

REQUIRED:

Outline the ethical issues arising and the safeguards that your firm should adopt.(4 marks)

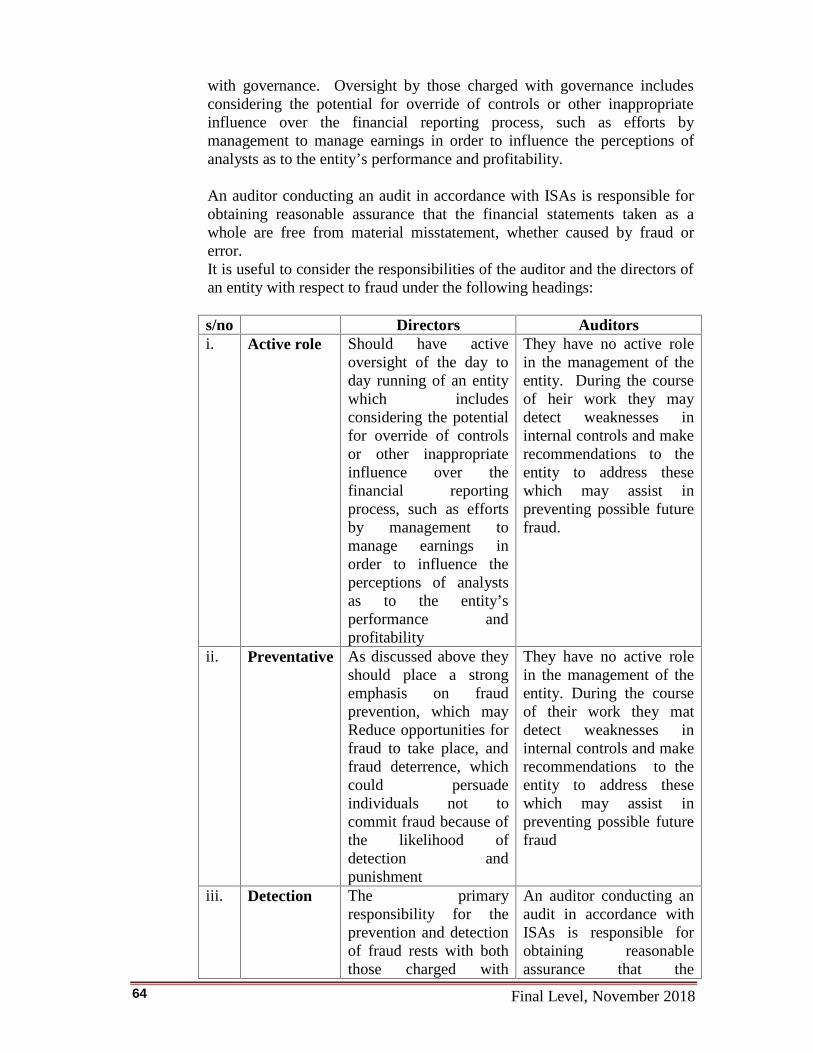

(c) You are the training officer in a firm of Certified Public Accountants and youhave scheduled an induction course to a group of new audit trainee staff on thearea of fraud and error. On discussing with the trainees prior to the inductionprogramme, a number of them have stated that, they are aware that the issue offraud and error is something they will likely face while performing their duties.They have advised that they are unsure as to what are their responsibilities andthose of the directors in these two areas. Having reflected on this, you havedecided to prepare for them the explanatory notes with regard to audit matterspertaining to fraud and error.

REQUIRED:

Prepare the notes for the audit trainee staff on your induction course which:(i) Differentiate between “the responsibilities of the auditor” and “those of

the directors” with respect to fraud. (6 marks)

(ii) Discuss the steps that auditors should take when fraud is suspected.(6 marks)

(d) You are completing the audit of Kizibo Ltd where the overall materiality levelis TZS.25,000,000 for the year ended 30th June 2018. During the course of theaudit, you have discovered that the directors of Kizibo had not revealed aboutone of the locations where a physical inventory count took place on 30th June2018. The value of inventory held on this premises is included in the draftaccounts at a value of TZS.27,400,000.

REQUIRED:

Outline how the above scenario will impact on the audit report if the auditorcannot carry out alternative audit procedures to determine the existence of theinventory in the unrevealed location. (4 marks)

(Total: 40 marks)

Final Level, November 2018 17

---------------------------------------------------------------------------------------------------------SECTION B

There are FIVE questions. Answer ANY THREE questions---------------------------------------------------------------------------------------------------------

QUESTION 2

(a) Auditors always conduct their audit with a view to determine whether or not thefinancial statements are materially misstated. For this reason, auditors usuallydetermine a materiality level to be used in conduct of the audit and also aperformance materiality level may be set at less than the materiality for thefinancial statements as a whole.

REQUIRED:

(i) Explain why it is necessary for the auditor to determine the materialityfigure at the planning stage of the audit. (4 marks)

(ii) Distinguish between materiality for the financial statements as a whole andperformance materiality. (4 marks)

(b) You are the audit manager for three clients of your audit firm and you arereviewing audit files and draft audit reports submitted by your subordinates onyour request. Extracts of the proposed audit opinions for the three clients are asgiven below:

Tegeta LtdConsistent losses that the company has been incurring for the past four yearsplus its serious liquidity problems do cast doubt on the going concernassumption made by management in the preparation of the company’s financialstatements.

Management has however assured the auditors that the parent company is readyand has given assurance that they will provide financial assistance to Tegeta Ltdto cover its short term working capital. To substantiate this, the parent companyhas issued a letter of comfort to the auditors. You are sure that the companywill continue to trade only if the assistance promised is materialized. Thedirectors have disclosed this fact in the financial statements in their director’sreport. The audit senior has recommended that a qualified opinion should beissued.

Maringo LtdThe year-end of Maringo Ltd is 30th September. Maringo Ltd planned toconduct a physical inventory count on 30th September 2018. However, thewarehouse caught fire which was caused by an electrical fault in the warehouse.The fire destroyed 40% of the inventory together with all the inventory recordsand therefore making it difficult for the company to reliably determine the valueof the remaining stock as there were no record to rely upon. They could

Final Level, November 201818

however estimate stock values based on selling prices and profit margins foreach line of inventory.

The audit senior stated that he was unable to obtain any reliable evidence on thevalue of inventory which he considered material to the financial statements.The audit senior has recommended that a qualified audit opinion should beissued with an emphasis of matter paragraph.

Makuti LtdThe year-end of Makuti Ltd is 31st December. In mid-February before thefinalization of the audit, one of the major customers of Makuti Ltd known asMikonge Ltd went into liquidation. At a meeting with all creditors of MikongeLtd, the liquidator announced that all creditors would only get 20% of theamount that Mikonge Ltd owes them.

Makuti Ltd refused to amend the receivables figure arguing that as at the end ofthe period, Mikonge Ltd was in good stand and capable to pay Makuti Ltd theamount outstanding.

The audit senior agreed with the accounting treatment of Makuti Ltd andrecommended that an unmodified audit opinion be issued.

REQUIRED:

Comment on the suitability of each of the recommended audit opinions aboveby clearly stating the arguments for or against the recommendations.(12 marks)

(Total: 20 marks)

QUESTION 3

You are planning the audit of Crash Bang Ltd., whose principal activities aremotorcycle courier services, and the repair and maintenance of commercialmotorcycles. You have been provided with the summaries of financial statements forthe year ended 30th June 2018.

Draft 2018TZS. ‘000’

Actual 2017TZS. ‘000’

Summary statement of Profit or LossRevenue 109,710 115,600Cost of sales (102,030) (104,740)Gro,ss profit 7,680 10,860Administrative expenses (7,820) (7,790)Interest payable and similar charges (2,350) (1,850)Net (loss) profit (2,490) 1,220

Final Level, November 2018 19

Draft 2018TZS. ‘000’

Actual 2017TZS. ‘000’

Summary statement of financial positionNon-current assets 51,780 46,700Current assets

Inventory (parts and consumables) 950 610Receivables 29,750 23,690

30,700 24,300Current liabilities

Bank loan 2,500 -Overdraft 12,450 9,130Trade payables 15,130 12,450Lease obligations 2,070 -Other payables 2,030 1,490

34,180 23,070Long-term liabilities

Bank loan 7,500 10,000Lease obligations 4,730 ____-

12,230 10,000Net assets 36,070 37,930

You have been informed by the Managing Director of crash Bang that the fall inrevenue is due to:

(1) The loss of a longstanding customer who shifted to a competitor, in July, 2018(2) A decline in trade in the repair and maintenance of commercial motorcycles

Due to the reduction in the repairs business, the company has decided to close theworkshop and sell the equipment and spares inventory. No entries resulting from thisdecision are reflected in the draft financial statements.

During the year, the company replaced a number of vehicles, funding them by acombination of leasing and an increased overdraft facility. The facility was to bereviewed in January 2019 when the audited financial statements will be available.

The draft financial statements show a loss for year 2018 but the forecasts indicate areturn to profitability in 2019 as the Managing Director is optimistic about generatingadditional revenue from new contracts.

REQUIRED:

(a) (i) State any five circumstances particular to Crash Bang Ltd. which mayindicate that the company is not a going concern. (5 marks)

(ii) Explain why the circumstances in (i) above give cause for concern.(5 marks)

(b) Describe any five audit procedures to be performed in respect of going concernat Crash Bang. (10 marks)

(Total : 20 marks)

Final Level, November 201820

QUESTION 4

(a) You are the Internal Audit Manager of the Internal Audit Department of KiboTextiles Mills Ltd. (KTML). Your Department is auditing the company’sprocurement system. Extracts from your system notes, which are reliablycorrect (contain no errors) are provided as follows:

Details of the Ordering Department(1) There are six members of staff, one purchasing manager and five

purchasing clerks.(2) The department receives about 75 orders per day. Many orders for

duplicate items come from different departments in the organization.(3) Initial evaluation of internal controls is very high.

Procurement systems:

Ordering Department All orders are raised on pre-numbered purchase requisitions and sent to

the Ordering Department. In the Ordering Department, each requisition is signed by the Purchasing

Manager. Then the Purchasing Clerk transfers the order information ontoan order form and identifies the appropriate supplier for the goods.

One copy of the two-copied order form is sent to the supplier and thesecond copy to the Accounts Department. The requisition is thendestroyed.

Goods Received Notes (GRNs) from the Inward Department are separatedfrom Damaged Goods Notes (DGNs). The DGNs are filed while theGRNs forwarded to the Accounts Department.

Goods Inwards Department All goods received are checked for damage. Damaged goods are returned

to the supplier and a Damaged Goods Note (DGNs) is completed. For undamaged items, a two-copied pre-numbered Goods Received Note

(GRN) is filled.

- One copy of GRN is sent to the Ordering Department attached with theDGN.

- Second copy is filed in order of the reference number for goods beingordered (obtained from the supplier’s goods dispatcheddocumentation), in the goods Inwards Department.

Accounts DepartmentThe GRNs are matched with the orders awaiting the receipt of the invoice (s).

REQUIRED:

Using the system notes provided:

Final Level, November 2018 21

(i) Identify and explain the internal control weaknesses and provide arecommendation to overcome each weakness. (8 marks)

(ii) Identify and explain the additional weaknesses that should be raised by avalue for money audit and provide a suitable recommendation toovercome each weakness. (6 marks)

(b) Independence of the external audit function is the critical component requiredfor the establishment of a positive statutory environment for the work of theController and Auditor General (CAG). However, despite the requirement forthe auditors to become independent, various factors such as ineffectivelegislature, bad vices such as corruption, and political, economic, and socialinfluences may affect the impact of audit findings. In these circumstances,complete independence is unrealistic.

REQUIRED:

Describe criteria used to determine whether the Controller and Auditor General(CAG) maintains adequate independence. (6 marks)

(Total : 20 marks)

QUESTION 5

(a) The report to management, which in some respects is a report on the ability andeffectiveness of management, is as useful to shareholders as the financialstatements and should be distributed to the shareholders and not just to themanagement team.

REQUIRED:

Discuss this proposition giving the arguments for or against it. (10 marks)

(b) A waste disposal company has breached tax regulations, environmentalregulations and health safety regulations. The company auditors have beenapproached by the tax authorities, the government body supervising the awardof licences to such companies and a trade union representative. All of them haveasked the auditors to provide them with information about the company. Theauditors have also been approached by the police who are investigating asuspected fraud perpetrated by the managing director of the company and theywish to ask the auditor certain questions about the company.

REQUIRED:

Describe how the auditors should respond to these types of request. (10 marks)(Total: 20 marks)

Final Level, November 201822

QUESTION 6

(a) Briefly describe different models in which internal audit services could bedelivered. (2 marks)

(b) MONO is a listed Construction Company based in the north of the country,whose activities encompass housebuilding and development. Its annual revenueis TZS.550 million and profit before tax is TZS.70 million.

You are the audit senior involved with the audit of MONO for the year ended31st December 2017. The following matters have come to your attention duringthe review stage of the audit in April 2018.1. Customer going into liquidation

One of MONO’s major commercial customers has gone into liquidationshortly after the year-end. As at the year-end, the customer owed thecompany TZS7.5 million.

2. Claim for unfair dismissalOne of the company’s construction workers, Mwakaje Njeri, wasdismissed in November 2017 after turning up to work in a drunkcondition. In December 2017, Mr Njeri opened a case against thecompany for unfair dismissal. Lawyers of the company have advisedthat it is very unlikely that he will be successful in his claim.

3. In March 2018, a fire started as a result of vandalism at one of thecompany’s ten storage depots. The fire destroyed TZS.200 millionworth of building materials.

REQUIRED:

For each of the three above mentioned events at MONO:

(i) Describe additional audit procedures you will carry out. (6 marks)

(ii) State whether the accounts will need to be amended and explain yourreasoning. (6 marks)

(iii) Discuss its potential impact on the audit report, fully explaining youranswers. (6 marks)

(Total: 20 marks)

________________ _______________

Final Level, November 2018 23

EXAMINATION : FINAL LEVEL

SUBJECT : BUSINESS AND CORPORATE FINANCE

CODE : C3

EXAMINATION DATE : THURSDAY, 1ST NOVEMBER, 2018

TIME ALLOWED : THREE HOURS (9:00 A.M. – 12:00 NOON)

------------------------------------------------------------------------------------------------------

GENERAL INSTRUCTIONS

1. There are TWO Sections in this paper. Sections A and B whichcomprise a total of SIX questions.

2. Answer question ONE in Section A.

3. Answer ANY THREE questions in Section B.

4. In total answer FOUR questions.

5. Marks are shown at the end of each question.

6. Show clearly all your workings in the respective answers where applicable.

7. This question paper comprises 9 printed pages.

_________________

Final Level, November 201824

------------------------------------------------------------------------------------------------------SECTION A

Compulsory Question------------------------------------------------------------------------------------------------------

QUESTION 1

(a) Fast-Fast Ltd (trading as FF) provided ferry services along the Indian Oceancoast between Dar es Salaam and Bagamoyo. The company has approached yourfirm for assistance in preparing a business plan to obtain finance for a plannedexpansion of its services. FF’s directors have produced a draft business plan andhave requested your help in completing certain sections of it. They have alsoasked for advice in supplementing the plan in order to maximize the possibilityof raising new finance.

Given below are extracts from the draft business plan prepared by Fast-Fastmanagement.

(1) IntroductionFast Fast Ltd (FF) provides commuter ferry services between Dar es Salaamand Bagamoyo. The business was founded in 1999 by two entrepreneurs,Anton Pembe and Adriano Binamungu, who have spent the majority of theirworking life and leisure time on boats. Anton and Adriano are the onlydirectors and managers, and each owns 50% of FF’s equity.

(2) Description of current servicesCurrently, FF’s commuter ferry service runs between Dar es Saaam andBagamoyo a major tourist and residential area, 40 kilometers outside Dar esSalaam every 2 hours at peak times and every 3 hours off-peak, five days aweek. It stops at piers along the coast where the commuter embark anddisembark and connects to all major commuter bus and rail interchanges. FFalso runs daytime leisure services at weekends and on public holidays.

FF’s boats are fast, modern and fuel-efficient, with a capacity of 200passengers. Coastal services do not suffer from the congestion problems andinterruptions faced by the rail and bus networks and, as a result, journeytimes are more predictable and the majority of services run on time.Standing and overcrowding are not permitted under health and safetyregulations, so all passengers travel in airline-style seats. To date, FF has aperfect safety record. An added attraction for commuters is that an extensivewireless network is available along the coast, allowing internet access forcommuters.

FF’s fares are higher than other forms of public transport because commutersare prepared to pay a premium for these benefits. Tickets for journeysoperate in a similar fashion to other forms of public transport, with theoption to purchase single and return tickets. There are concessionary faresfor students and the elderly and discounts are available for those regular

Final Level, November 2018 25

passengers who purchase season tickets (which allow unlimited travel, at anytime during the period for which the season ticket is valid).

In order to utilize the boats outside the core commuter hours, FF offers acheaper “Ruvu-Saddani” ticket which allows leisure passengers to visit someof Dar es Salam and Bagamoyo tourist and cultural attractions. This ticket isvalid on any off-peak service. FF operates additional services for a varietyof exhibitions and media events held at a wharf-side conference andexhibition centre. It has also recently approached a hotel chain which ownsa wharf-side hotel with a view to transporting its clients from the airport.

(3) Expansion planFF has a strong record of growth and profitability. Having started in 1999with a single boat carrying less than 1,500 passengers a week, the fleet hasgrown to seven boats, carrying more than 20,000 passengers per week. Lastyear passenger journeys on the service increased by over 50%, due mainly tothe increase in commercial and housing developments along the coast.

FF has also benefits from the government’s initiative to promote use of theocean as more environmentally friendly form of public transport. This hasresulted in increased demand for FF’s service, plus government finance. FFwants to expand its services by increasing the capacity and frequency ofservices on existing routes. Research suggests that the recent increase inpassenger volumes is sufficient to merit eight boats a day during peak times,i.e offering a service every one and half hour instead of the current two hoursinterval between boats.

Dar es Salaam will host a major sport event in 2020 which represent anothergrowth opportunity for ocean transport. The sport event will necessitatesignificant increased transport in the months leading up to carter for thespecific transport needs of spectators, athletes and workers at coast-sidevenues.

In addition to the short-term increase in demand generated by the sportevent, the government plans for further commercial and residentialdevelopment of wharf-side indicates that there will be longer termopportunities to provide ongoing commuter services in the future. In orderto capitalize on these opportunities, FF needs to invest in some new, largerboats, for which finance is being sought. Two options are available – FF canpurchase the boats outright or lease them for a minimum period of five years.FF’s existing boats have been financed by a combination of mandatorycontributions from coast side developers, government grants and loans takenout by FF.

(4) CompetitionThe City Coastal Authority (CCA) is a government body responsible forregulating services along the coast and operating the costal piers. FF is theonly company that has fulfilled the necessary criteria to be licensed by theCCA to provide coastal based commuter services, so it has no direct

Final Level, November 201826

competition. However, a variety of alternative public transport options areavailable to commuters, including the bus and rail networks.

In addition to these other forms of transport, FF’s tourist business facescompetition from small operators offering ocean boats and specificsightseeing tours by bus. The volume of tourists is very variable and isinfluenced by disposable income, exchange rates and the weather.

REQUIRED:

Acting as a consultant, prepare the following sections for inclusion in thebusiness plan:

(i) A SWOT Analysis of FF’s current strategic position. (12 marks)

(ii) An analysis of FF’s critical success factors. (8 marks)

(b) Remsi Baraka, the CEO of Fahami Enterprises, is considering a merger withEmpire Inc., which is led by Matayo Mtoni. The merger of their two firms willenable the creation of a very large diversified conglomerate, with businessesranging from office supplies sporting goods, industrial paints, consumerelectronics, and video games. A hired consultant has advised Baraka and Mtonithat the merger could create a great deal of value, because the new combinedentity can use several lucrative yet mature “cash cows” within Empire Inc. tofund the growth of several promising, but not yet highly profitable, youngbusinesses within Fahami Enterprises. Baraka and Mtoni have decided to seek asecond opinion from you, a long experienced consultant.

REQUIRED:

Explain to the two CEOs how the Boston Consulting Group (BCG) matrix canbe used in the light of the advice from the consultant. In your explanations,point out the meaning and logic of the model (matrix). (8 marks)

(c) Acquisition is one of growth strategies that a firm can employ. Sometimes anacquisition attempt can turn hostile when management of the target firm resistadvances from the suitor.

REQUIRED:

(i) Explain the meaning of a “hostile takeover” and any two alternatives toa hostile takeover which do not necessarily involve approach to themanagement of the target firm. (4 marks)

(ii) Discuss any four defensive strategies that a takeover target can employin a hostile takeover situation. In your explanation, indicate thecircumstances in which each strategy is likely to work for the takeovertarget and possible adverse consequences if the takeover does not gothrough. (8 marks)

(Total: 40 marks)

Final Level, November 2018 27

------------------------------------------------------------------------------------------------------SECTION B

There are FIVE questions. Answer ANY THREE questions.------------------------------------------------------------------------------------------------------

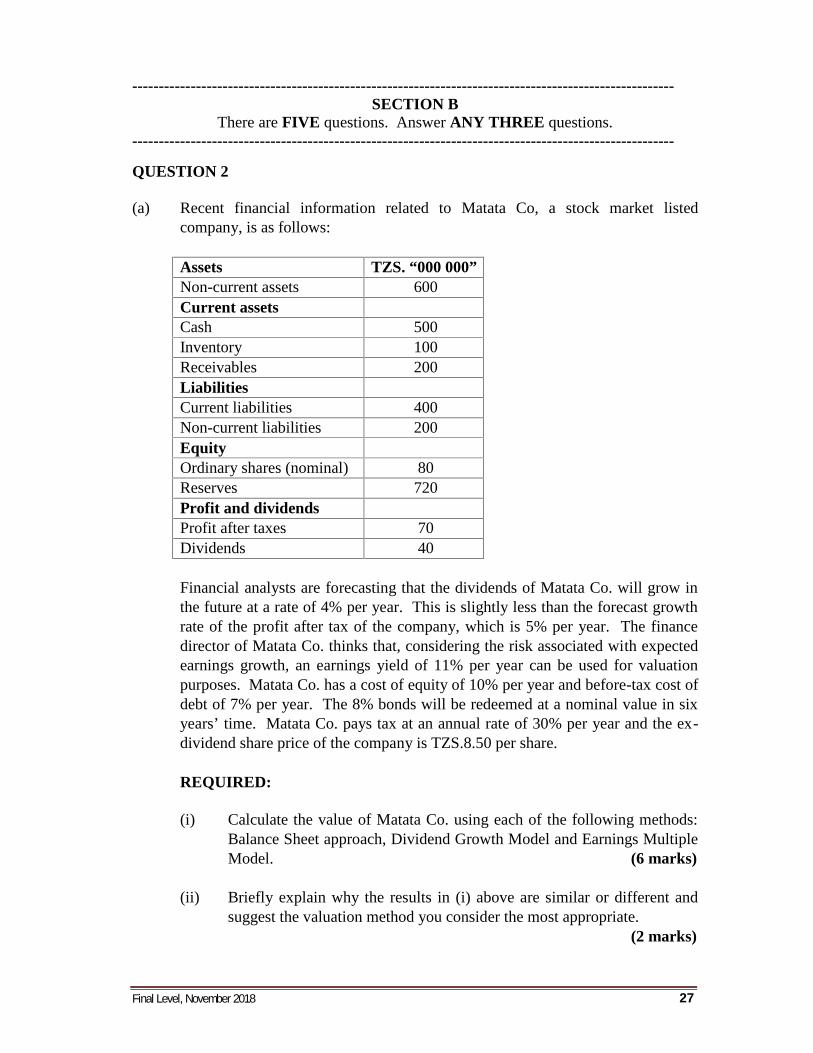

QUESTION 2

(a) Recent financial information related to Matata Co, a stock market listedcompany, is as follows:

Assets TZS. “000 000”Non-current assets 600Current assetsCash 500Inventory 100Receivables 200LiabilitiesCurrent liabilities 400Non-current liabilities 200EquityOrdinary shares (nominal) 80Reserves 720Profit and dividendsProfit after taxes 70Dividends 40

Financial analysts are forecasting that the dividends of Matata Co. will grow inthe future at a rate of 4% per year. This is slightly less than the forecast growthrate of the profit after tax of the company, which is 5% per year. The financedirector of Matata Co. thinks that, considering the risk associated with expectedearnings growth, an earnings yield of 11% per year can be used for valuationpurposes. Matata Co. has a cost of equity of 10% per year and before-tax cost ofdebt of 7% per year. The 8% bonds will be redeemed at a nominal value in sixyears’ time. Matata Co. pays tax at an annual rate of 30% per year and the ex-dividend share price of the company is TZS.8.50 per share.

REQUIRED:

(i) Calculate the value of Matata Co. using each of the following methods:Balance Sheet approach, Dividend Growth Model and Earnings MultipleModel. (6 marks)

(ii) Briefly explain why the results in (i) above are similar or different andsuggest the valuation method you consider the most appropriate.

(2 marks)

Final Level, November 201828

(b) Discuss the weaknesses of the Dividend Growth Model in the valuation of acompany and its shares. (4 marks)

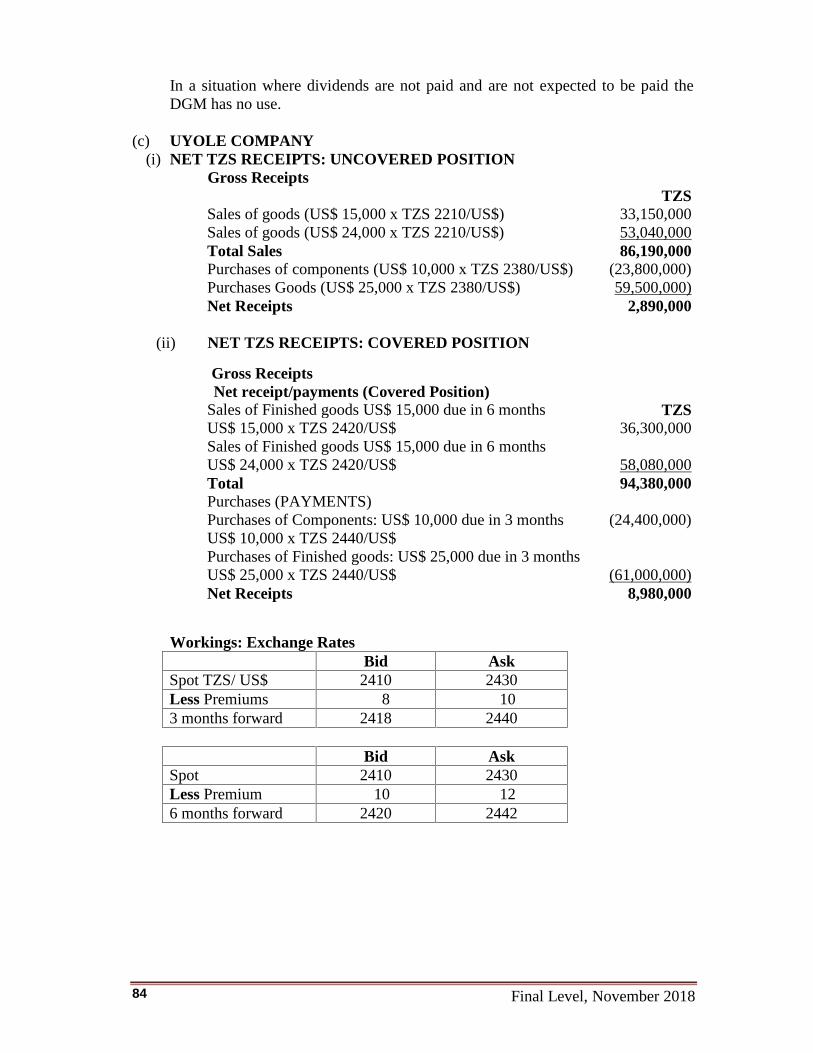

(c) Uyole Company is a medium size Tanzanian company with export and importtrade links with US companies. The following transactions are due within thenext six months:

Purchase of components, cash payment due in 3 monthUSTZS.10,000 Sales of finished goods, cash receipts due in 6 months USTZS.15,000 Purchase of finished goods for resale, cash payment

due in 3 months USTZS.25,000 Sales of finished goods, cash receipt due in 6 months USTZS.24,000

Exchange rates quoted in the foreign currency market are as follows:

Spot (TZS/US TZS.) 2,410 – 2,4303 months forward 8.00 – 10.00 Premium6 months forward 10 – 12 premium

The company decides to cover the above transactions in the forward market andthe actual spot rates in 3 months and 6 months turned out to be as follows:

3 months: TZS/USTZS.: 2,370 – 2,3806 months: TZS/USTZS.: 2,210 – 2,230

REQUIRED:

(i) Determine the net TZS receipts which Uyole Company might expect toreceive for both its three and six-month transactions if the transactionsremained uncovered. (4 marks)

(ii) Determine the net TZS receipts which Uyole Company would receive forboth its three and six month transactions if they were covered in theforward market. (4 marks)

(Total : 20 marks)

QUESTION 3

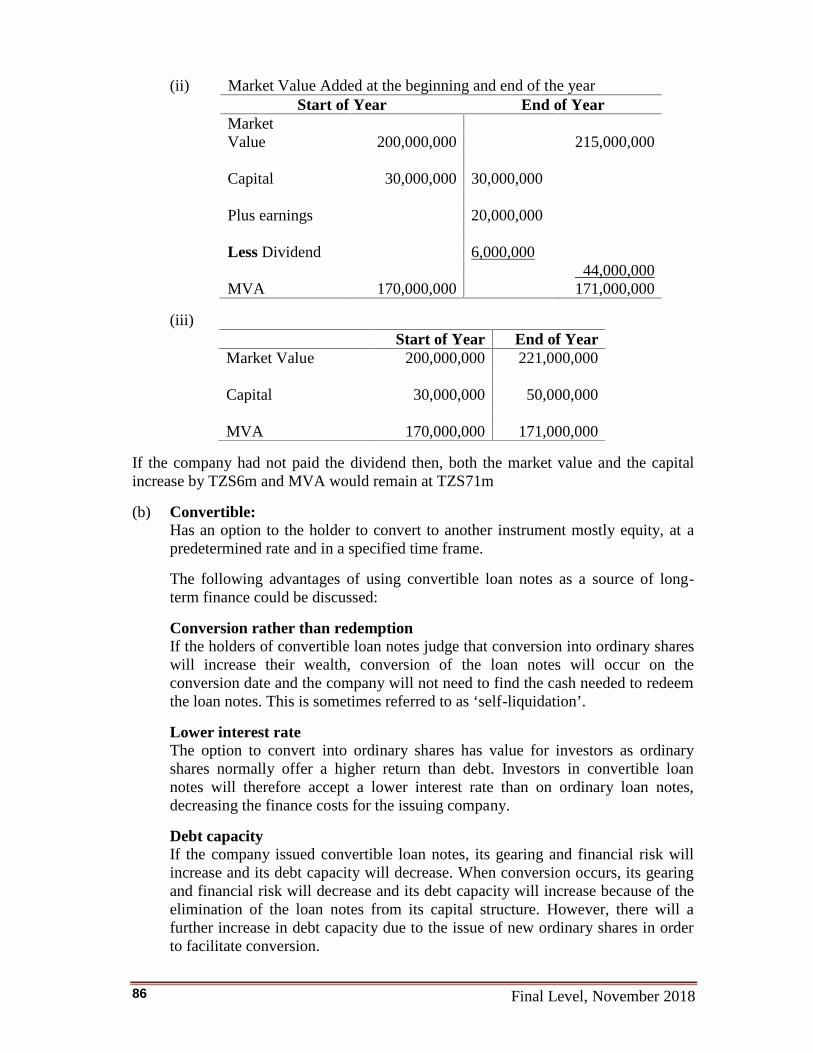

(a) Pefa Ltd is a clothing company founded five years ago with equity finance. Atthe beginning of last year it had an equity with market value of TZS.200 million,which increased to TZS.215 million by the end of the year. This was aftergenerating TZS.20 million of post-tax profit in the year and the payment of aTZS.6 million dividends. The capital invested in the firm by shareholders overthe company’s life by purchasing shares and retained earnings amounted toTZS.30 million at the start of the year.

Final Level, November 2018 29

REQUIRED:

(i) Briefly explain the market value added concept and its limitations.(4 marks)

(ii) Compute the market value added at the beginning and at the end of thepast year for Pefa Ltd. (4 marks)

(iii) What would have been the market value added at the beginning and theend of the past year had the dividend not been paid? (4 marks)

(b) Explain the meaning of a convertible loan note as a source of long term finance.Briefly discuss any two advantages of using a convertible loan note. (4 marks)

(c) Explain the meaning of term “overtrading”. Discuss any four indications that afirm may be overtrading. (4 marks)

(Total: 20 marks)

QUESTION 4

(a) Using examples, explain each of the following concepts and its applicability incorporate finance:

(i) Forward rate agreement (3 marks)

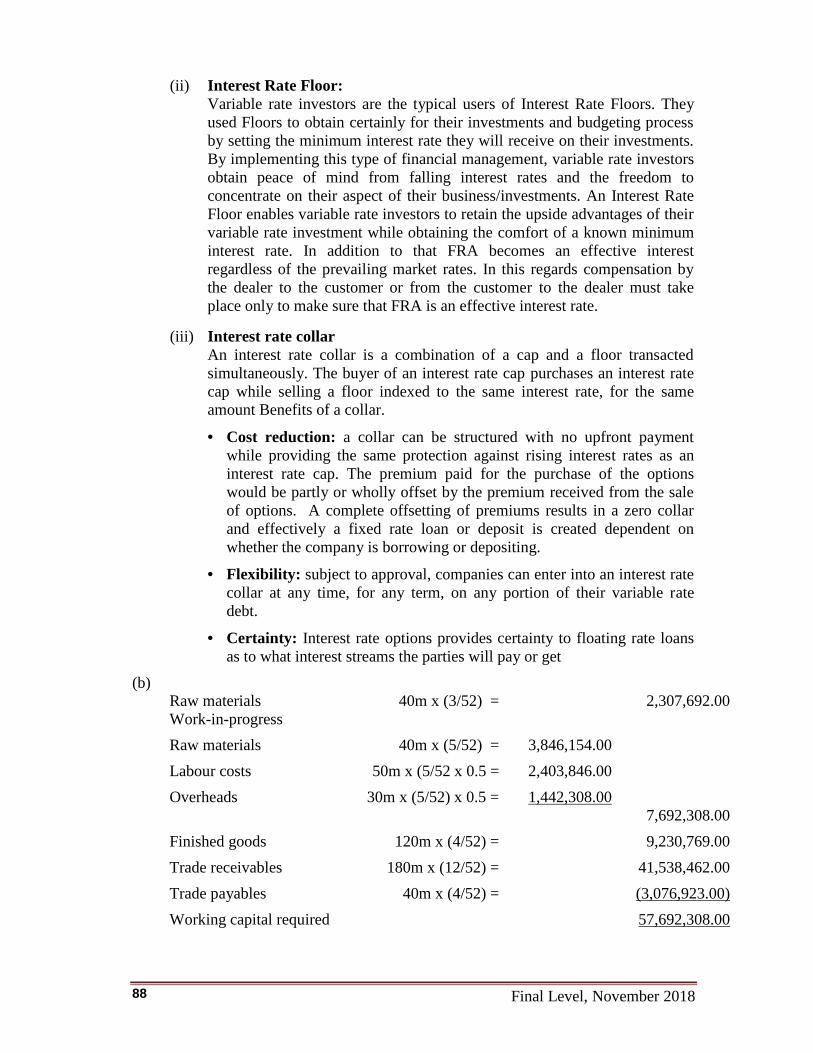

(ii) Interest rate floor (3 marks)

(iii) Interest rate collar (3 marks)

(b) Maswa Enterprises is a company involved in the manufacture of farmimplements. The managing director believes that one of the reasons mostcompanies in this industry die is poor management of working capital. MaswaEnterprises expects credit sales of TZS.180,000,000 in the next year and hasbudgeted production costs as follows:

TZS.Raw materials 40,000,000Direct labour 50,000,000Production overheads 30,000,000Total production costs 120,000,000

Raw materials are in inventory for an average of three weeks and finished goodsare in inventory for an average of four weeks. All raw materials are added at thestart of the production cycle, which takes five weeks and incurs labour costs andproduction overheads at a constant rate.

Suppliers of raw materials allow four weeks’ credit, whereas customers aregiven 12 weeks to pay.

Final Level, November 201830

REQUIRED:

(i) Compute Maswa Enterprises working capital requirement. (8 marks)

(ii) Determine Maswa Enterprises’ cash conversion cycle. (3 marks)(Total : 20 marks)

QUESTION 5

(a) Baama Company has decided to acquire a new truck. One alternative is to leasethe truck on a 4-year contract for a lease payment of TZS.10,000,000 per year,with payment to be made at the beginning of each year. The lease payment istax allowable and includes maintenance. Alternatively, Baama could purchasethe life span of truck outright for TZS.40,000,000 financed with a bank loan.The bank loan will be amortized over 4 years period at an interest rate of 10percent per year, payment to be made at the end of each year. Under theborrow-to-purchase arrangement, Baama would have to maintain the truck at acost of TZS.1,000,000 per year; payable at year-end. After its life span of 4years the truck will have a salvage value of TZS.10,000,000 at which timeBaama plans to replace the truck irrespective of whether it leases or buys.

Baama has a marginal tax rate of 40 percent. The depreciation rates underborrow-to-purchase are 25%, 30%, 14% and 6% of the purchase price for thefirst, second, third and fourth year respectively.

REQUIRED:

Compute the present value of the cost of each alternative and advise whether thetruck should be bought outright or leased. (12 marks)

(b) Explain the meaning of hybrid securities as used by firms in raising finance.Explain the features and advantages of any three hybrid securities. (8 marks)

(Total: 20 marks)

QUESTION 6

(a) On 30th October, 2018 Ibra Trading Company exported goods to a customer inUtopia. The Utopia customer was invoiced for UD100,000 (UD = Utopiandollar) payable on 30th January, 2019. In the foreign exchange market, thefollowing quotes were available:

Foreign Exchange Market Quotes (30th October, 2018)Spot TZS/UD 846 - 85230th December, 2018 Forward 836 - 84230th January, 2019 Forward 833 - 839

The management of Ibra Trading Company wishes to hedge the foreignexchange exposure with traded currency options. January 2019 exchangetraded options have the following characteristics:

Final Level, November 2018 31

UD Exchange Traded optionsUD Calls UD Puts

Exercise price TZS.837 TZS.835Option cost TZS.4 TZS.3Maturity 30th January, 2019 30th January, 2019Option contract Size UD10,000 UD10,000

REQUIRED:

(i) Illustrate how Ibra Trading Company can make use of the UD Optionsto guard its foreign exchange exposure. What will be the cost of the UDoption? (Hint: Set up a hedge position). (5 marks)

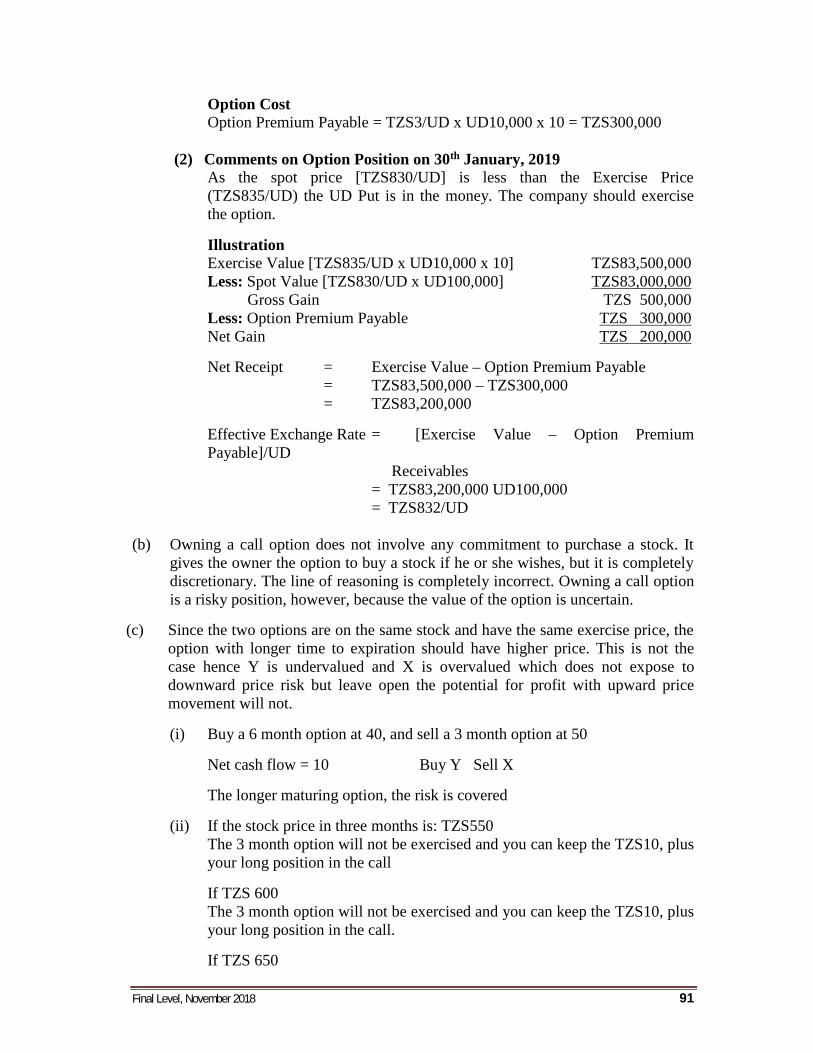

(ii) Comment on the UD option position on 30th January, 2019 if theTZS/UD spot rate on that date is TZS/UD 830 – 833 and illustrate theaction to be taken by the company to benefit from the option position.What would be the net receipts from the transaction and the resultingeffective exchange rate? (5 marks)

(b) An investment advisor to your company claimed that buying a call option isvery dangerous because it commits the owner to purchasing a stock at a laterdate. At that time, the stock may be undesirable. Therefore, owning a calloption is a risk position.

REQUIRED:

Give your views on the validity of this claim. (4 marks)

(c) Consider two call options on the same stock with the following features:

Option Exercise Price Time to expiration Premiumx TZS.600 3 months TZS.50y TZS.600 6 months TZS.40

REQUIRED:

If it is possible to take both long and short positions, comment on the pricing ofthese options and possible strategy to exploit any mispricing. In yourexplanations, point out the profit or loss that you will make in three months’time if the pricing of the stock is TZS.550, TZS. 600 or TZS.650. (6 marks)

(Total: 20 marks)

________________ _______________

Final Level, November 201832

EXAMINATION : FINAL LEVEL

SUBJECT : PUBLIC FINANCE AND TAXATION II

CODE : C4

EXAMINATION DATE : FRIDAY, 2ND NOVEMBER, 2018

TIME ALLOWED : THREE HOURS (2:00 P.M. – 5:00 P.M.)

---------------------------------------------------------------------------------------------------------

GENERAL INSTRUCTIONS

2. There are TWO Sections in this paper. Sections A and B which comprise atotal of SIX questions.

2. Answer question ONE in Section A

3. Answer ANY THREE questions in Section B.

4. In total answer FOUR questions.

5. Marks are shown at the end of each question.

6. Show clearly all your workings in the respective answers where applicable.

7. Calculate your answers to the nearest one decimal point where necessary.

8. This question paper comprises 10 printed pages.

_________________

Final Level, November 2018 33

---------------------------------------------------------------------------------------------------------SECTION A

Compulsory Question---------------------------------------------------------------------------------------------------------

QUESTION 1

A Case

(a) ABBY PLC, a French based manufacturer of high quality watches has recentlyconsidered establishing a subsidiary in Tanzania where its watches are highlydemanded. Various departments of ABBY PLC were asked to supply relevantinformation for a capital budgeting analysis. All relevant information are asfollows:

1. Initial investment:An estimated Euros 300,000 will be needed for the project. Out of thatamount, Euros 50,000 will be used as working capital and the remainingamount will be used to acquire non-current assets for the project.

2. Project life:The project is expected to end in four years. The host government haspromised to make payment to the parent company of TZS.150,000,000(which is equivalent to the salvage value of the non-current assets) in orderto purchase the plant after four years.

3. Price and demand:The estimated price and demand schedules during each of the next fouryears are as shown below:

Year Price per unit(TZS.)

Demand in Tanzania(UNITS)

1 5,000 60,000

2 5,000 60,000

3 6,000 100,000

4 7,000 100,000

4. Costs:The variable costs (for materials, labour and overheads) per unit wereestimated and consolidated as shown below:

Year Variable Costs per unit (TZS.)1 2,0002 2,0003 2,5004 3,000

Final Level, November 201834

The company is also expecting to incur TZS.20 million per year as rentalcosts and additional annual overhead expenses of TZS.30 million.

5. Host country taxes on income earned by a subsidiary:The Tanzanian Government will allow ABBY PLC to establish thesubsidiary and will impose a 30% corporate tax rate on its profits. Inaddition, it will impose a 10% tax on repatriated income.

6. French Government taxes on income earned by ABBY PLC’s subsidiary:The French Government will charge 15% of foreign earned income.

7. Capital Deductions:All non-current assets of the subsidiary will qualify for capital deductions.The tax laws in Tanzania will allow the subsidiary to provide depreciationallowance for the company’s non-current assets at a straight line methodafter deducting a salvage value of the assets.

8. Exchange rates: the spot exchange rate for one Euro (€) is TZS.3,000.

REQUIRED:

(i) With the use of the provisions of the Income Tax Act, CAP 332 discussthe nature and taxation of ABBY PLC’s planned subsidiary. (4 marks)

(ii) Calculate the expected net profit and expected corporate tax for thesubsidiary during the whole period of the project as per the requirementof Income Tax Act, CAP 332. (14 marks)

(iii) Calculate the expected repatriated income and repatriated tax during thewhole period of the project as per Section 72 of the Income Tax Act,CAP 332. (16 marks)

(b) Assume AEJ Ltd is a Tanzanian company based in Canada and that during theyear of income ended 31st December 2017, it earned a total profit equivalent toTZS.89,000,000 and it was taxed an equivalent of TZS.7,000,000.

REQUIRED:

With the use of the provisions of the Income Tax Act, CAP 332, determine theamount of tax chargeable in Tanzania with foreign tax relief and without foreigntax relief. (6 marks)

(Total: 40 marks)

Final Level, November 2018 35

---------------------------------------------------------------------------------------------------------SECTION B

There are FIVE questions. Answer ANY THREE questions---------------------------------------------------------------------------------------------------------

QUESTION 2

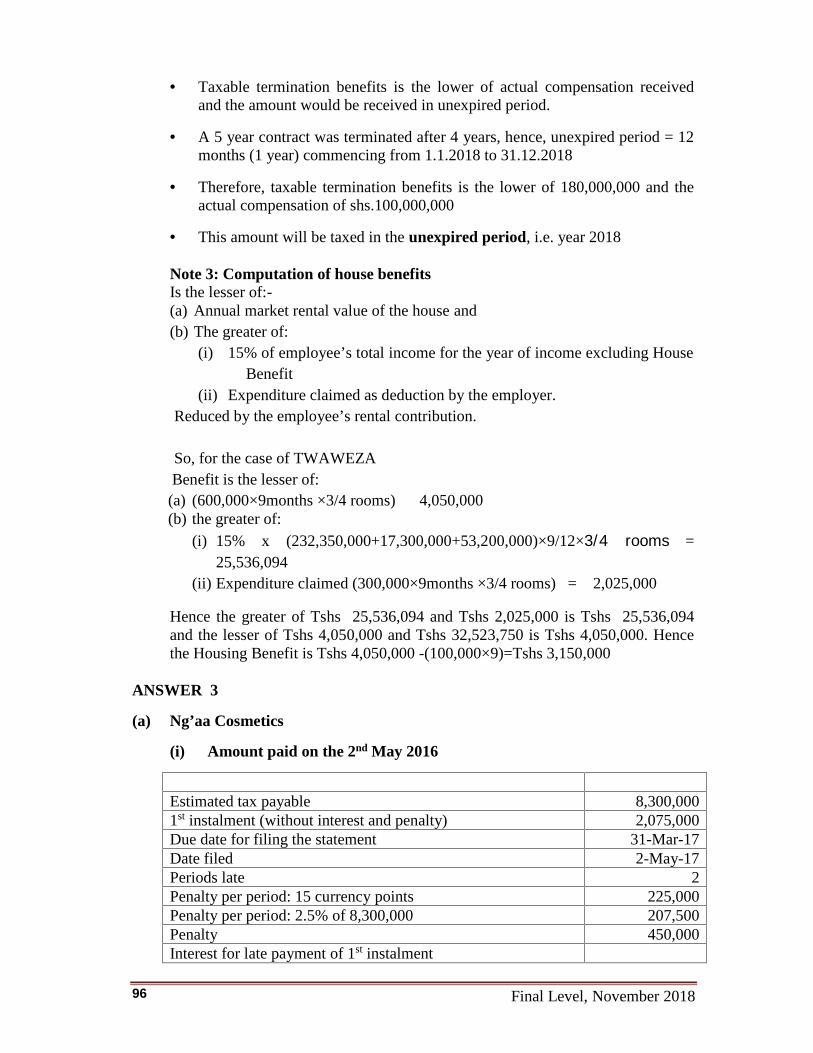

(a) Analyze the main features which distinguish the concept of ‘permanentestablishment’ from a ‘permanent home’. (2 marks)

(b) Mrs. Twaweza is a resident employee of WAZAWA Investments LimitedCompany (WAZAWA), working as a Consultant and Technical Engineer undera fixed employment contract of five years effective from 1st January 2014.WAZAWA is a resident company with several business lines of which one isdealing with mining activities, for which Mrs Twaweza is solely employed.

The company has a housing scheme, under which it provides accommodation toall employees who then suffer an 8 percent deduction on their salaries as rentcontribution. She was, however, employed under a differential schemearrangement which provided for among other things a free house.

During the year 2017, she was entitled to a monthly salary of TZS.15,000,000;monthly duty allowance, TZS.500,000; entertainment allowance,TZS.1,000,000 per month, which she was required to account; and TZS.300,000per month to meet travelling expenses. She was, however, not required toaccount for the travelling expenses.As part of the contract, she was also provided with the following benefits:

1. A residential house for which she was required to pay a token rentamounting to TZS.100,000 per month in respect of the part occupied. It is amodern 4-rooms house, in which one room is used to keep variousequipments used in her employment. These equipments were bought by theemployer to assist her perform the duties efficiently. Landlords in the nearbyarea charge similar houses a monthly rent of TZS.600,000. Company wasclaiming a monthly deduction of TZS.300,000 in respect of the house.

During the first two years and three months of her employment, that is, until31st March 2017 she was accommodated in a hotel. The employer paid allaccommodation costs directly to the hotel during this period, includingmeals TZS.20,000,000 and TZS.30,000,000 as accommodation. This was alump sum amount.

2. Security and housemaid services and utility charges amounting in aggregateto TZS.3,000,000 per month were met by the employer.

3. Free use of company’s motor vehicle. This was a Toyota Land cruiser(3000cc) newly purchased for her. She was using this car while on dutyonly. Employer was claiming expenditure amounting to TZS.1,500,000 permonth in respect of the car.

Final Level, November 201836

4. The company has a loan policy which entitles all employees who havesuccessfully passed 12 months’ probation period a loan of up toTZS.120,000,000 at a subsidized 4 percent annual interest rate. Mrs.Twaweza secured the full amount loan on 1st January 2016 and agreed topay it in 24 monthly instalments, using average method, starting 31st

January 2016. The statutory rate has been stable at 12 percent per monthsince 2014.

5. She was contributing a 5 percent to an unapproved retirement fund, andanother 5 percent to an approved retirement benefit fund.

The employer made the following contributions on behalf of Mrs Twaweza:

6. 10 percent of her monthly basic salary as employer’s contribution to anapproved retirement benefit scheme. This contribution is not included in theemployee’s taxable income.

7. 5 percent of her monthly basic salary as a contribution to a privateunapproved retirement benefit scheme. This was the same scheme in whichthe employee was making her first package of contribution in (5) above.

8. 3 percent of her monthly basic salary to cover life insurance policy for herhusband, five children and herself to an insurance company.

Following her aggressive involvement in political movement during the year2017, her contract was terminated effective from 1st January 2018 as this wasagainst company’s ideology. As a result of this termination, she was paid alump sum compensation of TZS.100,000,000.

Other information:

9. Mrs Twaweza has reported unadjusted trading profits of TZS.60,000,000from her grocery and kuku projects for the year ended 31st December 2017.

10. During the year 2017, she received dividends of TZS.1,500,000 from sharesinvested in a nonresident corporation many years ago. Also, she receivedaccumulated rent of TZS.8,000,000 from one of her tenant in her residentialpremises situated in the nearby area. This rent was outstanding in respect ofeight months of the year 2016, and it was reported as income from tradingactivity. During the same year 2017 she received TZS.2,500,000 as interestfrom the money deposited in a private foreign bank. This interest wascomputed on the basis of bank balance of TZS.125,000,000.

11. During 2017, she received service fees amounting to TZS.10,000,000 inrespect of technical advices provided to a neighbouring mining company.This income is included in her profits from the business activities.

12. Provisional assessment on the income tax payable for the year 2017 on hergrocery and kuku businesses estimated a quarterly instalment of

Final Level, November 2018 37

TZS.1,200,000. This was previously deducted from the books whencomputing reported trading profit.

13. On 30th June 2017 she received TZS.5,300,000 as gains from an interest inan unapproved retirement fund. This was only a part of her 5 percentmonthly contribution made to the fund.

REQUIRED:

On the basis of the above information, and guided by the relevant provisions inthe Income Tax Act, calculate for the year of income 2017.(i) Total taxable income from employment (12 marks)(ii) Taxable compensation and the years of assessment (2 marks)(iii) Total chargeable income (4 marks)

(Total : 20 marks)

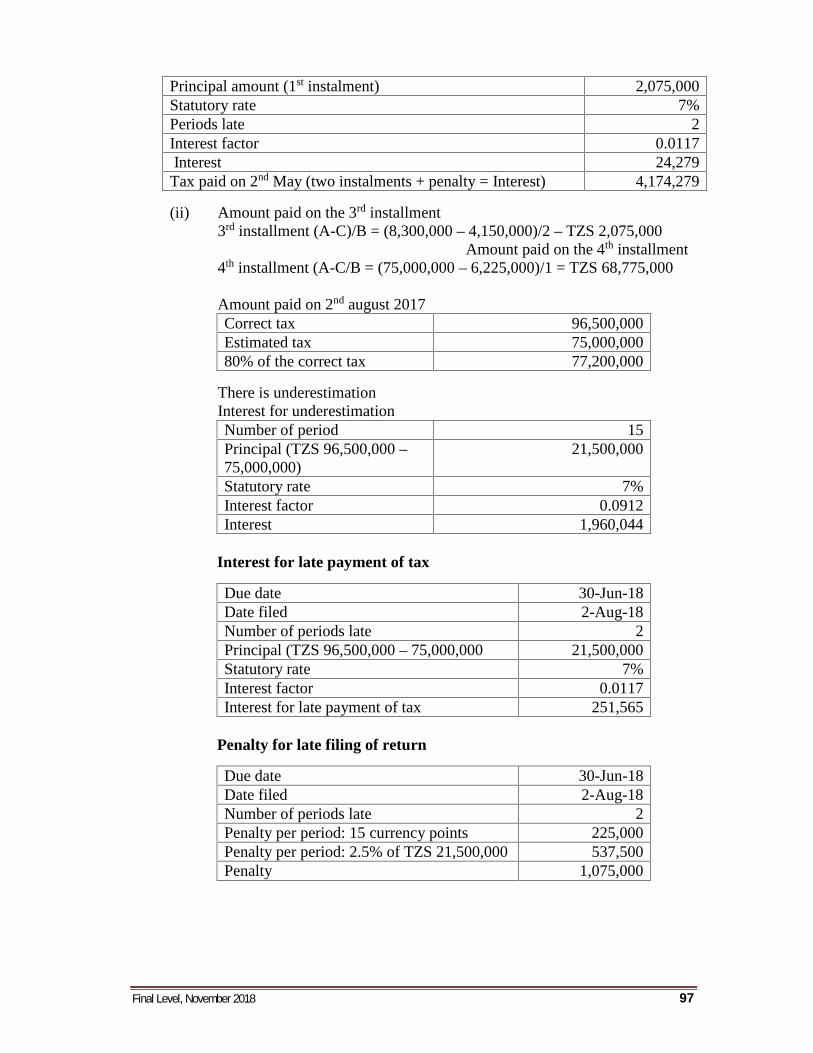

QUESTION 3

(a) Ng’aa Cosmetics, a corporation, filed a statement of estimated tax for the year2016 (1st January 2016 – 31st December 2016) on 2nd May 2016, estimating atax payable amounting to TZS.8,300,000. The company paid on this date itsdues for the first two instalments. The 3rd installment was paid on its due dateand on 31st December 2016 the company revised its estimated income toTZS.250,000,000 and paid the respective fourth installment. There was no taxpaid through the withholding system during the year of income. The return ofincome filed by the company on 2nd August 2017 showed a total ‘principal’ taxof TZS.96,500,000 based on the company’s income for the year of income2016, and paid the tax due on the same date.

Where relevant, payments made on each specific dates include any applicableinterest/penalty due at the date of payment. Income tax rate is 30 percent.

REQUIRED:

Calculate:(i) The amount paid on the 2nd May 2016. (4 marks)

(ii) Amount paid on the 3rd instalment. (1 mark)

(iii) Amount paid on the 4th instalment. (1 mark)

(iv) Amount paid on 2nd August 2017 (6 marks)

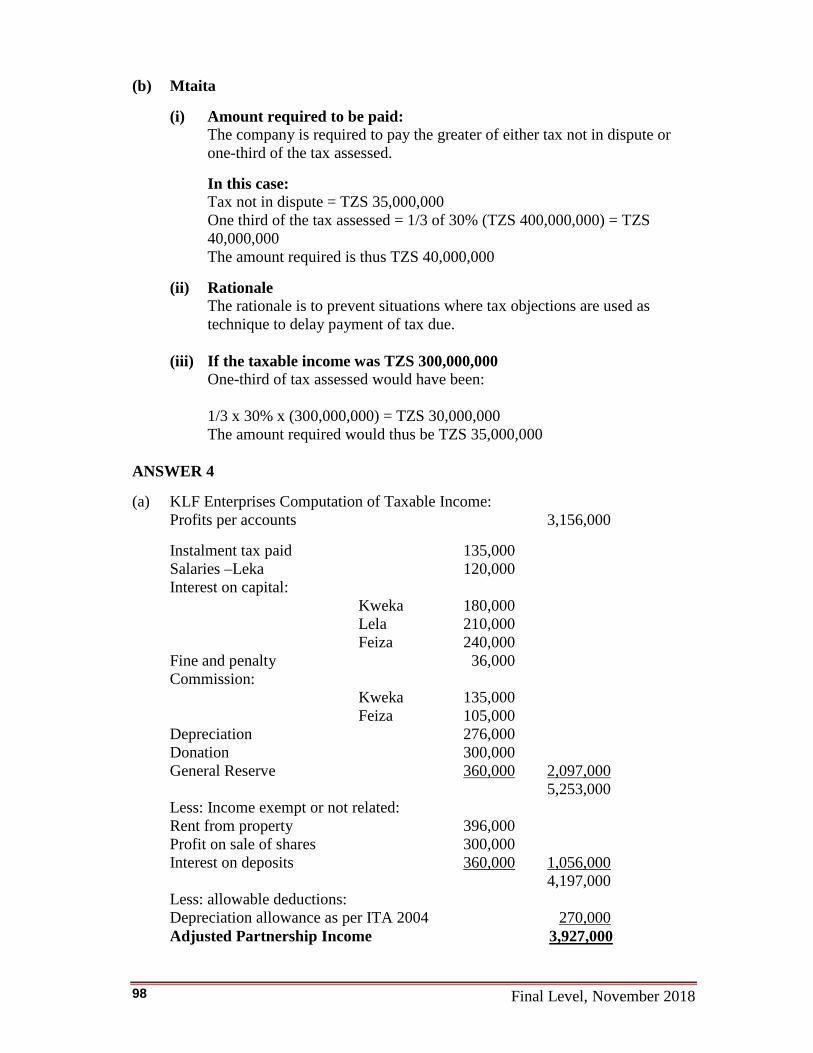

(b) Mtaita (T) Ltd received a notice of assessment from the Commissioner on 25th

June 2017, showing that its taxable income for the year is TZS.400,000,000, andthey are supposed to pay corporation tax based on this amount. Upon receipt ofthis notice, the accountants and the finance director are surprised as theircomputations reveal an amount of tax payable to be only TZS.35,000,000. They

Final Level, November 201838

thus file a notice of objection, with the Commissioner on 8th July 2017 clearlyspecifying the grounds for such objection, and indicating their computationschedules to support that tax should be TZS.35,000,000. However, they missone thing to make their notice of objection valid, i.e. there is an amount of taxthey are supposed to pay pending final determination, and they can’t figure outhow much is this amount.

REQUIRED:

(i) Calculate the amount of tax that Mtaita Ltd was required to pay to maketheir notice of objection valid. (4 marks)

(ii) Explain the rationale for the provision you have applied in computingthe amount in (i) above. (2 marks)

(iii) Calculate the amount in (i) above if the Commissioner’s assessmentshowed a taxable income of TZS.300,000,000. (2 marks)

(Total : 20 marks)

QUESTION 4

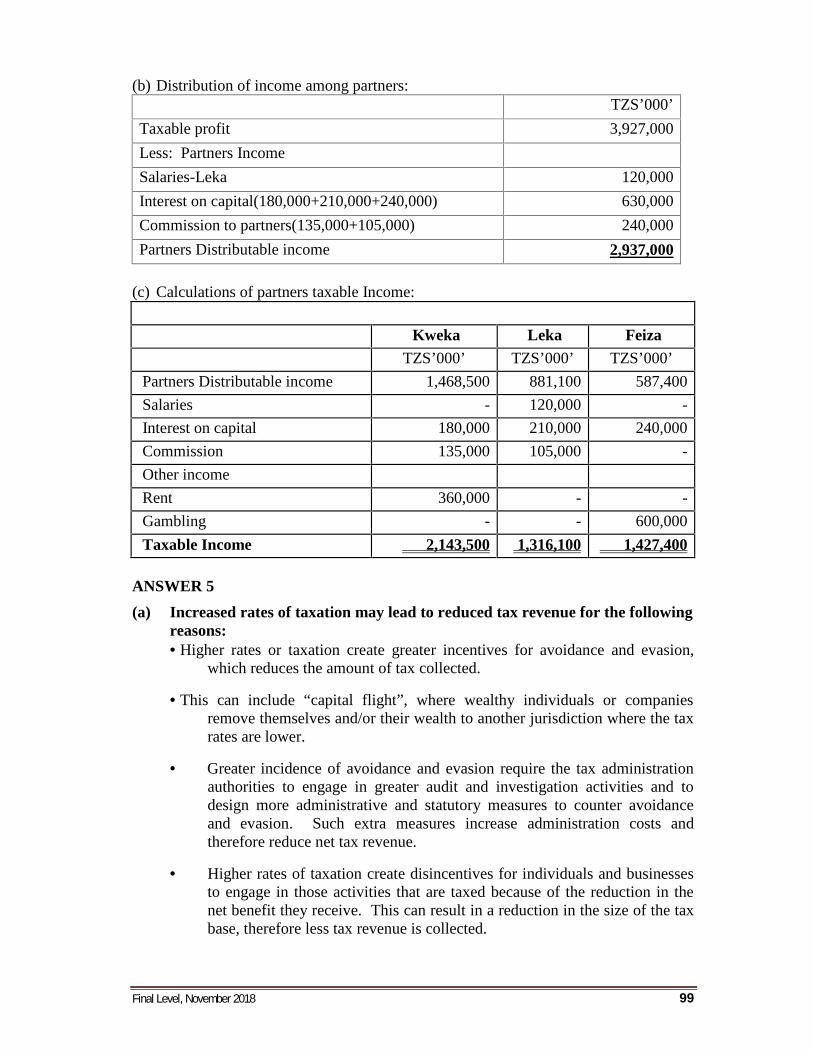

Mr. Kweka, Mr. Leka and Mr. Feiza are partners trading under the name KLFEnterprise. They share profit and losses in the ratio of 5:3:2 respectively. Given belowis the Statement of Profit or Loss of the Partnership for the year ended 31st December2017.

TZS. ‘000’ TZS. ‘000’Office expenses 612,000 Gross profit 6,900,000Instalment tax paid 135,000 Discount received 240,000Rent and rates 450,000 Profit on sale of shares 300,000Salaries and wages 840,000 Rent from property 396,000Printing stationery 192,000 Miscellaneous receipts 450,000Advertisement 219,000 Interest on fixed deposit 360,000Interest on capital:Kweka 180,000Leka 210,000Feiza 240,000Commission to partners:Kweka 135,000Leka 105,000Legal charges 246,000Depreciation 276,000Bad debts 204,000Donation to famine relief 300,000Electricity 138,000General reserve 360,000Showroom expenses 351,000General expenses 297,000Net profit 3,156,000 ________

8,646,000 8,646,000

Final Level, November 2018 39

The partners have provided the following information in support of the accounts:

(i) It has been the practice to value the stocks at cost price, however, the closinginventory at 31st December 2017 – TZS.540,000,000 has been valued at amarket price which is less by 10% of its cost price.

(ii) Salaries and wages include ‘salaries’ amounting to TZS.120,000,000 paid toLeka.

(iii) Advertising includes TZS.30,000,000 spent on advertising campaign tointroduce new product in the market.

(iv) Legal charges include TZS.36.000,000 paid as a fine and penalty.

(v) Capital allowance has been agreed with the Commissioner responsible forIncome Tax at TZS.270,000,000.

(vi) Mr. Leka has got no other income.

(vii) Mr. Kweka’s other income includes TZS.360,000,000 from rent. He hasbrought forward business loss of TZS.405,000,000 from the assessment of theyear of income for 2016 of the partnership.

(viii) Mr. Feiza has income for TZS.600,000,000 from gamble winnings. He hasbrought forward business loss of TZS.405,000,000 from the assessment of theyear of income for 2016 of the partnership.

REQUIRED:

(a) Compute the total taxable income from the partnership business. (10 marks)

(b) Distribute the profit amongst the partners for the year 2017. (5 marks)

(c) Ascertain the profit amongst the partners for the year of income 2017.(5 marks)(Total: 20 marks)

QUESTION 5

(a) While governments can borrow to fund expenditure, loans must ultimately berepaid through taxation. Taxation is therefore key to supporting governmentexpenditure, it is important to understand how a government can design aneffective tax system.

REQUIRED:

Explain why an increase in rates of taxation may not necessarily lead to anincrease in net revenue from taxation. (10 marks)

(b) Vavene Company Limited is a mining company in Makete, Njombe. The mainline of business for the company is mining of coal in Makete and sometimes goldin Mbeya.

Final Level, November 201840

During the year of income 2016 the company incurred the followingexpenditures in relation to mining:

(i) TZS.800 million to explore the nearby area for an expansion of the mine.The exploration was successful and therefore expanded the mine at a totalcost of TZS.2,150,000,000.

(ii) TZS.100 million to reinforce the underground rails and roads as well asthe underground drainage.

(iii) The only road to the mine (of about 1.5 km) was also improved forTZS.20,000,000.

(iv) Compensation to the residents around the additional mine was to the tuneof TZS.700 million.

(v) Some of the additional capital expenditure was set off to the tax accountsrelated to the Mbeya mining, this was to the tune of TZS.500 million.This was necessitated by the fact that the company made an excessiveloss of TZS.2,200,000,000 during the year of income 2015.

(vi) During the year of income 2016 the company managed to realize a profitof TZS.1,900,000,000.

(vii) In order to make life easy for the mining, the company bought twominibuses worth TZS.20,000,000 each.

(viii) Three lorries worth TZS.40,000,000 each were also bought to facilitatetransportation of the soil to the clearing sites.

REQUIRED:

Compute the Capital deductions admissible to the company during the year ofincome 2016. (10 marks)

(Total: 20 marks)

QUESTION 6

(a) Explain the nature of ‘juridical double taxation’. (2 marks)

(b) Explain three unilateral methods of eliminating double taxation. (6 marks)

(c) Public finance is not just about money. Its subject matter includes not only allaspects of public sector finances but also the structure of the public sector andfiscal institutions as well as the broad objectives and rationale for thegovernment activities.

Final Level, November 2018 41

REQUIRED:

(i) Discuss different forms that the government may use to intervene theeconomy. (4 marks)

(ii) Evaluate how different types of government expenditure affects theGross Domestic Product (GDP) growth in the short run and in the longrun. (8 marks)

(Total: 20 marks)

_______________________

Final Level, November 201842

SUGGESTED SOLUTIONSC 1- CORPORATE REPORTING

NOVEMBER 2018

ANSWER 1