the lebanon brief -...

TRANSCRIPT

Your Investment Reference

THE

LEBANON BRIEF

ISSUE 938

Week of Ocotber 5-10 2015

ECONOMIC RESEARCH DEPARTMENT

BLOMINVEST Bank Headquarters

Bab Idriss, Beirut, Lebanon

T (01) 991 784/2 F (+961) 1 991 732

www.blom.com.lb

S A L

ISSUE 937 Week of October 5 –10, 2015

S A L

TABLE OF CONTENT

FINANCIAL MARKETS 3

Equity Market 3

Foreign Exchange Market 5

Money & Treasury Bills Markets 5

Eurobond Market 6

ECONOMIC AND FINANCIAL NEWS 7

Contraction of the Private Sector Economy Slackened in September; BLOM PMI inched up to 48.1 7

BDL’s Total Assets Increased by 0.18% m-o-m to $91.63B in September 8

Lebanon Recorded a $1.65B Deficit on its Balance of Payments by August 2015 9

Lebanon Ranked 113th out of 140 in the Global Competitiveness Index 10

Commercial Bank Assets Expanded by 3.37% to $181.62B by August 11

Tourist Spending Progressed at 5% by September 2015 12

CORPORATE DEVELOPMENTS 13

Bank of Beirut Announces its Redemption on its Preferred Shares Class “H” 13

Baque De L’Industrie Et Du Travail S.A.L. Increased Capital by LBP 5.4B ($3.65M) 13

Launching of the “First National Dollar Fund” by First National Bank 14

FOCUS IN BRIEF 15

Marble and Granite Industry in Lebanon 15

This report is published for information purposes only. The information herein has been compiled from, or based upon sources we believe to be

reliable, but we do not guarantee or accept responsibility for its completeness or accuracy. This document should not be construed as a

solicitation to take part in any investment, or as constituting any representation or warranty on our part. The consequences of any action taken on

the basis of information contained herein are solely the responsibility of the recipient.

The Lebanon Brief Page 3 of 18

ISSUE 937 Week of October 5 –10, 2015

S A L

FINANCIAL MARKETS

Equity Market

Stock Market

09/10/2015 02/10/2015 % Change

BLOM Stock Index* 1,145.09 1,145.79 -0.06%

Average Traded Volume 92,568 1,340,000 -93.09%

Average Traded Value 1,006,771 12,540,000 -91.97% *22 January 1996 = 1000

Trading activity weakened on the Lebanese Stock

Exchange this week, which was characterized by

two political dialogue sessions and a demonstration

on Thursday. The BLOM Stock Index (BSI) barely

changed, going down by a marginal 0.06%, to

1.145.09 points. In addition, in details, the average

traded volume and value went down from 1.34M

shares worth $12.54M to 92,568 shares worth

$1.00M. As for the market capitalization, it

remained relatively stable at $9.52B.

Globally, the Morgan Stanley Emerging Markets

Index (MSCI), the S&P Pan Arab Composite Large-

Mid-Cap Index and the S&P AFE 40 Index recorded

respective gains of 6.36%, 2.83%, and 2.31%,

respectively, over the week.

Most Gulf States saw weekly improvements in their

bourses mainly due to a 10.41% rally in oil prices.

Thus, Saudi Arabia, Qatar and Egypt were the best

performers regionally, increasing by 4.68%, 2.63%,

and 2.48%, respectively, from Friday 2nd of

October’s level. On the other hand, the bourses of

Bahrain, Tunisia and Muscat were the worst

performers, dropping by weekly 1.69%, 0.92%, and

0.21%%, respectively.

Back to the Beirut Stock Exchange, the banking

sector captured 83.46% of the total traded value

during the week while the real estate sector and

the industrial sector grasped the remaining 11.41%

and 5.13%, respectively. In the banking sector, the

GDR shares of BLOM and that of Audi lost 0.10% and

1.00% to end the week at $9.65 and $5.94,

respectively. BLOM common shares also dropped by

0.53% to end the week at $9.40, while the common

shares of Audi and Byblos increased by a weekly

0.34% and 0.63% to respective quotes of $5.99 and

$1.61. On a weekly basis, the BLOM Preferred

Shares Index (BPSI) didn’t change, remaining at

105.29 points. This was attributed to Audi

preferred shares class “H” going up by a 0.10%

weekly to $101.10, which was offset by BLOM

preferred shares 2011 declining by 0.10% to $10.15,

over the same period. In the real estate sector,

Solidere shares class “A” gained 0.10% to $10.08

while the class “B” shares declined by 0.50% to

$10.04. In the industrial sector, Holcim shares

traded with no change in price.

Banking Sector

Mkt 09/10/2015 02/10/2015 % Change

BLOM (GDR) BSE $9.65 $9.66 -0.10%

BLOM Listed BSE $9.40 $9.45 -0.53%

BLOM (GDR) LSE $9.55 $9.60 -0.52%

Audi (GDR) BSE $5.94 $6.00 -1.00%

Audi Listed BSE $5.99 $5.97 0.34%

Audi (GDR) LSE $5.92 $6.00 -1.33%

Byblos (C) BSE $1.61 $1.60 0.63%

Byblos (GDR) LSE $75.00 $75.00 0.00%

Bank of Beirut (C) BSE $18.40 $18.40 0.00%

BLC (C) BSE $1.70 $1.70 0.00%

Fransabank (B) OTC $27.00 $27.00 0.00%

BEMO (C) BSE $1.90 $1.90 0.00%

Mkt 09/10/2015 02/10/2015 % Change

Banks’ Preferred Shares Index *

105.29 105.29 0.00%

Audi Pref. E BSE $100.70 $100.70 0.00%

Audi Pref. F BSE $100.60 $100.60 0.00%

Audi Pref. G BSE $101.10 $101.00 0.10%

Audi Pref. H BSE $101.00 $101.00 0.00%

Byblos Preferred 08 BSE $100.90 $100.90 0.00%

Byblos Preferred 09 BSE $25.80 $25.80 0.00%

Bank of Beirut Pref. E BSE $26.00 $26.00 0.00%

Bank of Beirut Pref. I BSE $26.00 $26.00 0.00%

Bank of Beirut Pref. H BSE $10.15 $10.16 -0.10%

BLOM Preferred 2011 BSE $100.50 $100.50 0.00%

BEMO Preferred 2013 BSE $100.00 $100.00 0.00%

* 25 August 2006 = 100

1130

1150

1170

1190

1210

1230

1250

Oct-14 Jan-15 Apr-15 Jul-15 Oct-15

BLOM Stock Index

HI: 1,236.40

LO: 1,134.83

The Lebanon Brief Page 4 of 18

ISSUE 937 Week of October 5 –10, 2015

S A L

Real Estate

Mkt 09/10/2015 02/10/2015 % Change

Solidere (A) BSE $10.08 $10.07 0.10%

Solidere (B) BSE $10.04 $10.09 -0.50%

Solidere (GDR) LSE $10.00 $10.00 0.00%

On the London Stock Exchange, Audi and BLOM

GDR shares lost 1.33% and 0.52% to settle at

respective quotes of $5.92 and $9.55.

During the coming weeks, the Lebanese Bourse

will keep on mimicking investors’ attitude

towards the country’s main security, political

and economic issues.

Manufacturing Sector

Mkt 09/10/2015 02/10/2015 % Change

HOLCIM Liban BSE $15.00 $15.00 0.00%

Ciments Blancs (B) BSE $4.00 $4.00 0.00%

Ciments Blancs (N) BSE $3.10 $3.10 0.00%

Funds

Mkt 08/10/2015 01/10/2015 % Change

BLOM Cedars Balanced

Fund Tranche “A” ----- $7,412.56 $7,464.15 -0.69%

BLOM Cedars Balanced

Fund Tranche “B” ----- $4,866.54 $4,925.18 -1.19%

BLOM Cedars Balanced

Fund Tranche “C” ----- $5,629.89 $5,669.08 -0.69%

BLOM Bond Fund ----- $9,484.65 $9,484.65 0.00%

Retail Sector

Mkt 09/10/2015 02/10/2015 % Change

RYMCO BSE $3.23 $3.23 0.00%

ABC (New) OTC $27.00 $27.00 0.00%

Tourism Sector

Mkt 09/10/2015 02/10/2015 % Change

Casino Du Liban OTC $323.00 $323.00 0.00%

SGHL OTC $7.00 $7.00 0.00%

The Lebanon Brief Page 5 of 18

ISSUE 937 Week of October 5 –10, 2015

S A L

Foreign Exchange Market

Lebanese Forex Market

09/10/2015 02/10/2015 %Change

Dollar / LP 1,510.00 1,511.00 -0.07%

Euro / LP 1,706.94 1,683.12 1.42%

Swiss Franc / LP 1,563.63 1,541.57 1.43%

Yen / LP 12.54 12.55 -0.08%

Sterling / LP 2,314.77 2,284.62 1.32%

NEER Index** 166.22 167.40 -0.70%

*Close of GMT 09:00+2 **Nominal Effective Exchange Rate; Base Year Jan 2006=100 **The unadjusted weighted average value of a country’s currency relative to all major currencies being traded within a pool of currencies. The NEER represents the approximate relative price a consumer will pay for an imported good.

Demand for the Lebanese Pound in the Lebanese Forex

market strengthened versus the Dollar during the week

ending October 9, 2015 with the exchange rate moving

within the peg range from $/LP 1,509–1,513 with a mid-

price of $/LP 1,511 to $/LP 1,508-1,512 with a mid-price

of $/LP 1,510. Foreign assets (excluding gold) at the

Central Bank dropped by a monthly 0.89% to reach $38.25B

at the end of September 2015. As for the dollarization rate

of private sector deposits, it slid from 65.71% in December

2014 to 64.96% by August this year.

Nominal Effective Exchange Rate (NEER)

On the US front, mixed economic data came out this week

which kept the dollar at a topsy turvy state. In details,

better than expected jobless claims was offset by ISM

(Service Sector Index) and Non-Farm Payrolls (NFP) data,

which were lower than expected in the U.S. during

September. The Dollar’s descent was accentuated by the

latest Federal Reserve minutes of meeting, which was

released on Thursday. The report mainly illustrated the

dovish attitude of the Fed during the meeting on

September 17th. Accordingly, over the past week, the Euro

appreciated by 1.48% against the dollar to €/$ 1.1323. The

price of gold increased by a weekly 3.95% to reach

$1,153.83/ounce at 15:30 pm Beirut time.

By Friday 9th of October, 2015, 15:30 pm Beirut time, the

dollar-pegged LP depreciated against the euro going from

€/LP 1,683.12 one week earlier to €/LP 1,706.94,

representing a 1.42% increase. The Nominal effective

exchange Rate (NEER) decreased by 0.70% to 166.22

points, narrowing its year-to-date gains to 12.83%.

Money & Treasury Bills Markets

Money Market Rates

Treasury Yields

08/10/2015 01/10/2015 Change bps

3-M TB yield 4.39% 4.39% 0

6-M TB yield 4.87% 4.87% 0

12-M TB yield 5.08% 5.08% 0

24-M TB coupon 5.84% 5.84% 0

36-M TB coupon 6.50% 6.50% 0

60-M TB coupon 6.74% 6.74% 0

08/10/2015 01/10/2015 Change bps

Overnight Interbank 3.00% 2.75% 0

BDL 45-day CD 3.57% 3.57% 0

BDL 60-day CD 3.85% 3.85% 0

During the week ending September 24, 2015, broad Money M3

increased by LP 551B ($365.27M), to reach LP 183,968B

($122.04B) posting a 5.22 % yearly growth and a 3.70% y-t-d

uptick. Similarly, M1 expanded by LP 413B ($274.22M) over

the mentioned period, due to the increase in demand

deposits by LP 329B ($218.24M) and the LP 84B ($55.72M)

expansion in money in circulation.

Total deposits (excluding demand deposits) increased by LP

137B ($491.05M) during the week ending September 24, given

the $2M growth in deposits denominated in foreign currencies

and the LP 135B increase in term and saving deposits in LP.

Over the above mentioned period, the broad money

dollarization rate experienced a down tick from 58.01% on

September 17, to 57.84% on September 24.

In the TBs auction held on the 24h of September 2015, the

Ministry of Finance raised LP 212B ($150.00M), through the

issuance of bills and notes maturing in 3M, 1Y and 5Y. The

highest demand was achieved on the 5Y notes, which grasped

a 67% share of total subscriptions, while the 1Y and 3M bills

captured the remaining 25% and 8%, respectively. The 3M and

1Y bills respectively yielded at 4.39% and 5.08%, while the

coupon rate on the 5Y notes stood at 6.74%.

129

132

135

138

141

144

147

150

153

156

159

162

165

168

Oct-14 Dec-14 Feb-15 Apr-15 Jun-15 Aug-15 Oct-15

The Lebanon Brief Page 6 of 18

ISSUE 937 Week of October 5 –10, 2015

S A L

Eurobond Market

Eurobonds Index and Yield

08/10/2015 01/10/2015 Change Year to Date

BLOM Bond Index (BBI)* 104.786 104.793 -0.01% -1.22%

Weighted Yield** 5.96% 5.96% 0 94

Weighted Spread*** 547 460 87 117

*Base Year 2000 = 100; includes US$ sovereign bonds traded on the OTC market

** The change is in basis points ***Against US Treasuries (in basis points)

Lebanese Government Eurobonds

Maturity - Coupon

08/10/2015

Price*

01/10/2015

Price*

Weekly

Change%

08/10/2015

Yield

01/10/2015

Yield

Weekly

Change bps

2016, Nov - 4.750% 100.4 100.57 -0.17% 4.36% 4.20% 16

2017, Mar - 9.000% 105.38 105.5 -0.11% 5.10% 5.07% 3

2017, Oct - 5.000% 99.75 99.63 0.12% 5.13% 5.19% -6

2018, Jun - 5.150% 99.5 99.5 0.00% 5.35% 5.35% 0

2018, Nov - 5.150% 99.25 99.25 0.00% 5.41% 5.41% 0

2019, Apr - 5.500% 100 100.25 -0.25% 5.50% 5.42% 8

2020, Mar - 6.375% 102.13 102.25 -0.12% 5.82% 5.79% 3

2020, Apr - 5.800% 99.75 100 -0.25% 5.86% 5.80% 6

2021, Apr - 8.250% 109.75 109.5 0.23% 6.14% 6.19% -6

2022, Oct - 6.100% 99.25 99.63 -0.38% 6.23% 6.17% 7

2023, Jan - 6.000% 99 99 0.00% 6.17% 6.17% 0

2024, Dec - 7.000% 104.25 104.5 -0.24% 6.38% 6.34% 3

2025, Jun - 6.250% 98.5 98.5 0.00% 6.41% 6.41% 0

2026, Nov - 6.600% 100 100.13 -0.13% 6.60% 6.58% 2

2027, Nov - 6.750% 100.75 100.88 -0.13% 6.66% 6.64% 2

Mid Prices ; BLOMINVEST bank

During the past week of regular political dialogues it seems that investors were in a “wait and see” approach regarding demand

forlong term notes while medium and short term maturities saw a decline in demand. The BLOM Bond Index (BBI), which tracks the

performance of the Lebanese Eurobonds, slightly dropped by 0.01%, during the week, to 104.786 points. In addition, the BBI was

outperformed by the JP Morgan Emerging Markets’ Bond Index that gained 1.71%, during the same period, to 675 points. The yield

on the Lebanese Eurobonds maturing in 5Y gained 6 basis points (bps) to 6.00% while that of the 10Y remained at last Thursday’s

level of 6.48%.

In the US, treasuries experienced a bearish week despite ISM (Service Sector Index) data, which illustrated a sluggish expansion in

the U.S. service sector in addition to lower than expected Non-Farm Payrolls (NFP) in the U.S. during September. In fact, what

could be holding back US fixed income securities was the awaited minutes of meetings from the Federal Reserve that took place

last month and released on Thursday, regarding interest rates hike. The 5Y and 10Y yields increased by 3 bps and 7 bps to 1.40%

and 2.12%, respectively. Consequently, the spread between the yields on the 5Y Lebanese Eurobonds and their US comparable

widened from 457 bps to 460 bps while that of the 10Y narrowed by from 443 bps last week to 436.

Lebanon’s 5Y Credit Default Swaps (CDS) narrowed from 405-428 bps to 395-405 bps. The 5Y CDS quotes of Saudi Arabia and of

Brazil contracted from 119-129 bps and 460-468 bps to 117-122 bps and 420-426 bps, respectively. As for Turkey their 5Y CDS

quotes also went down from 311-315 bps to 270-274 bps this week. In contrast, Dubai’s 5Y CDS quotes broadened from 180-194 bps

to 190-195 bps.

4.50%

5.00%

5.50%

6.00%

Oct-14 Dec-14 Feb-15 Apr-15 Jun-15 Aug-15 Oct-15

Weighted Effective Yield of Eurobonds

The Lebanon Brief Page 7 of 18

ISSUE 937 Week of October 5 –10, 2015

S A L

ECONOMIC AND FINANCIAL NEWS

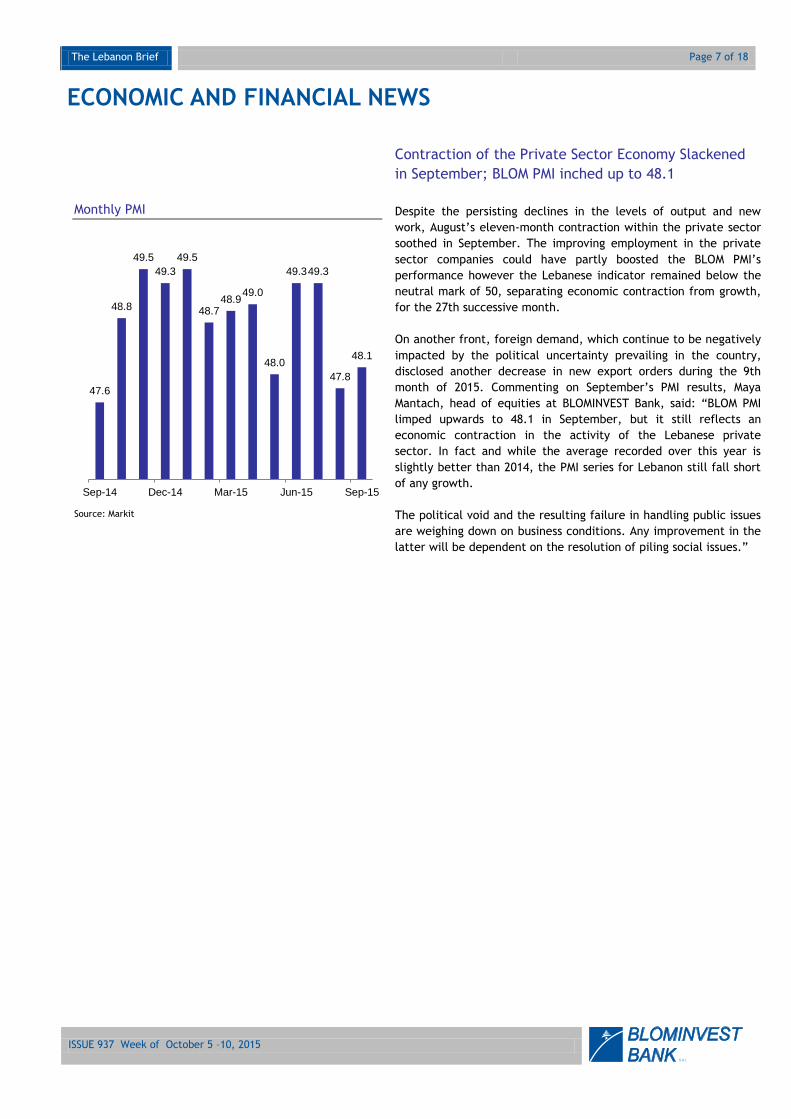

Monthly PMI

Source: Markit

Contraction of the Private Sector Economy Slackened

in September; BLOM PMI inched up to 48.1

Despite the persisting declines in the levels of output and new

work, August’s eleven-month contraction within the private sector

soothed in September. The improving employment in the private

sector companies could have partly boosted the BLOM PMI’s

performance however the Lebanese indicator remained below the

neutral mark of 50, separating economic contraction from growth,

for the 27th successive month.

On another front, foreign demand, which continue to be negatively

impacted by the political uncertainty prevailing in the country,

disclosed another decrease in new export orders during the 9th

month of 2015. Commenting on September’s PMI results, Maya

Mantach, head of equities at BLOMINVEST Bank, said: “BLOM PMI

limped upwards to 48.1 in September, but it still reflects an

economic contraction in the activity of the Lebanese private

sector. In fact and while the average recorded over this year is

slightly better than 2014, the PMI series for Lebanon still fall short

of any growth.

The political void and the resulting failure in handling public issues

are weighing down on business conditions. Any improvement in the

latter will be dependent on the resolution of piling social issues.”

47.6

48.8

49.5

49.3

49.5

48.7 48.9

49.0

48.0

49.3 49.3

47.8

48.1

Sep-14 Dec-14 Mar-15 Jun-15 Sep-15

The Lebanon Brief Page 8 of 18

ISSUE 937 Week of October 5 –10, 2015

S A L

BDL’s Total Assets by September (in $B)

Source: BDL

BDL’s Total Assets Increased by 0.18% m-o-m to

$91.63B in September

The Central Bank’s (BDL) balance sheet posted a 0.18% monthly

increase in total assets to $91.63B in September 2015.

In details, foreign assets, constituting 41.74% of total assets, fell by

0.89% from the previous month, to $38.25B while gold reserves

(11.31% shares of total assets) also declined monthly by 0.76% to

$10.36B, over the same period. The latter drop occurred due to the

1.75% fall in international gold quote to 1,115.09 $/ounce during

the month of September. In contrast, securities portfolio (18.36% of

total assets) increased by 0.75% to $16.82B over the same period.

Worth mentioning, loans to financial sector (5.25% share of total

assets) also grew by 2.53% month-on-month to reach $4.81B.

On the liabilities section, financial sector deposits ticked up by

0.87% to $74.08B, grasping 80.85% of the total liabilities.

Meanwhile, public sector deposits (5.54% share of total liabilities)

experienced a 12.58% monthly decline to $5.08B.

60.14

70.77

77.38 78.6

85.43

91.63

2010 2011 2012 2013 2014 2015

The Lebanon Brief Page 9 of 18

ISSUE 937 Week of October 5 –10, 2015

S A L

Balance of Payments Up to August (In $ M)

Source: BDL

Lebanon Recorded a $1.65B Deficit on its Balance of

Payments by August 2015

Lebanon’s Balance of payments (BoP) deficit reached $1.65B by

August 2015, almost four times higher than the $432.9M recorded a

year earlier. In fact, the deficit level was the worst since 2012 and

was mainly due to the decline in capital inflows and Foreign Direct

Investment (FDIs) as a result of the ongoing domestic developments

and the regional upheavals. In fact, Net Foreign Assets (NFA) of

the Central Bank (BDL) grew by $1.46B until August 2015, while

that of the commercial banks fell by $3.11B, over the same period.

In August alone, Lebanon’s Balance of Payments (BoP) also

recorded a deficit of $332.0M, for the 5th time this year. In details,

Net Foreign Assets (NFA) of the Central Bank (BDL) contracted by

$407.2M in August 2015 , while that of the commercial banks added

$75.2M from the prior month.

289.7

2,013.3

4,367

2,753.9

-1,237.3

-1,839.4

-957.2

-432.9

-1,648.9

2007 2008 2009 2010 2011 2012 2013 2014 2015

The Lebanon Brief Page 10 of 18

ISSUE 937 Week of October 5 –10, 2015

S A L

Lebanon’s Global Competitiveness Index Ranking

2015-2016

Rank (out of 140)

Score (1-7)

Travel & Tourism Competitiveness Index (TTCI) 113 3.8

Basic Requirements 121 3.7

Institutions 128 3.2

Infrastructure 116 2.7

Macro-Economic Environment 139 2.6

Health and Primary Education 30 6.3

Efficiency Enhancers 71 4.0

Higher Education Training 58 4.5

Goods Market Efficiency 56 4.4

Labor Market Efficiency 109 3.8

Financial Market Development 78 3.8

Technological Readiness 66 4.0

Market Size 77 3.6

Innovation and Sophistication Factors 67 3.6

Business Sophistication 61 4.1

Innovation 95 3.1

Source: World Economic Forum

Lebanon Ranked 113th out of 140 in the Global

Competitiveness Index

In its annual Global Competitiveness Index (GCI) 2015-2016 report,

the World Economic Forum ranked Lebanon 113th globally

(Switzerland being 1st) out of 140 countries and 10th out of the

Arab counties ranked.

The GCI is divided into three main categories; “Basic

Requirements”, “Efficiency Enhancers”, and “Innovation and

Sophistication Factors”. These sub-indices are further divided into

12 pillars, from Health and Primary Education, Macro Environment,

Goods Market Efficiency, Labor market Efficiency to Innovation.

For instance, Lebanon ranked 121 in “Basic Requirements”

category. This is on the back of the country ranking a lowly 139 in

Macro Environment, in addition to “Institutions” being placed 128.

However, Lebanon would have been ranked much lower if it

weren’t for its competitiveness in “Health and Primary Education”,

where it ranked 30th out of 140.

Lebanon retained the 77th place in the “Efficiency Enhancers”

category. It was good in terms of Goods Market Efficiency, in which

Lebanon ranked 56th. On the contrary, Lebanon showed poor drive

in regarding Labor Market Efficiency ranking 109 out of 140

countries.

In “Innovation and Sophistication Factor” category, Lebanon was

placed 67th as it ranked in Business Sophistication at 61st position

and yet Innovation pushed the ranking downwards, as it was placed

in the 95th position.

The Lebanon Brief Page 11 of 18

ISSUE 937 Week of October 5 –10, 2015

S A L

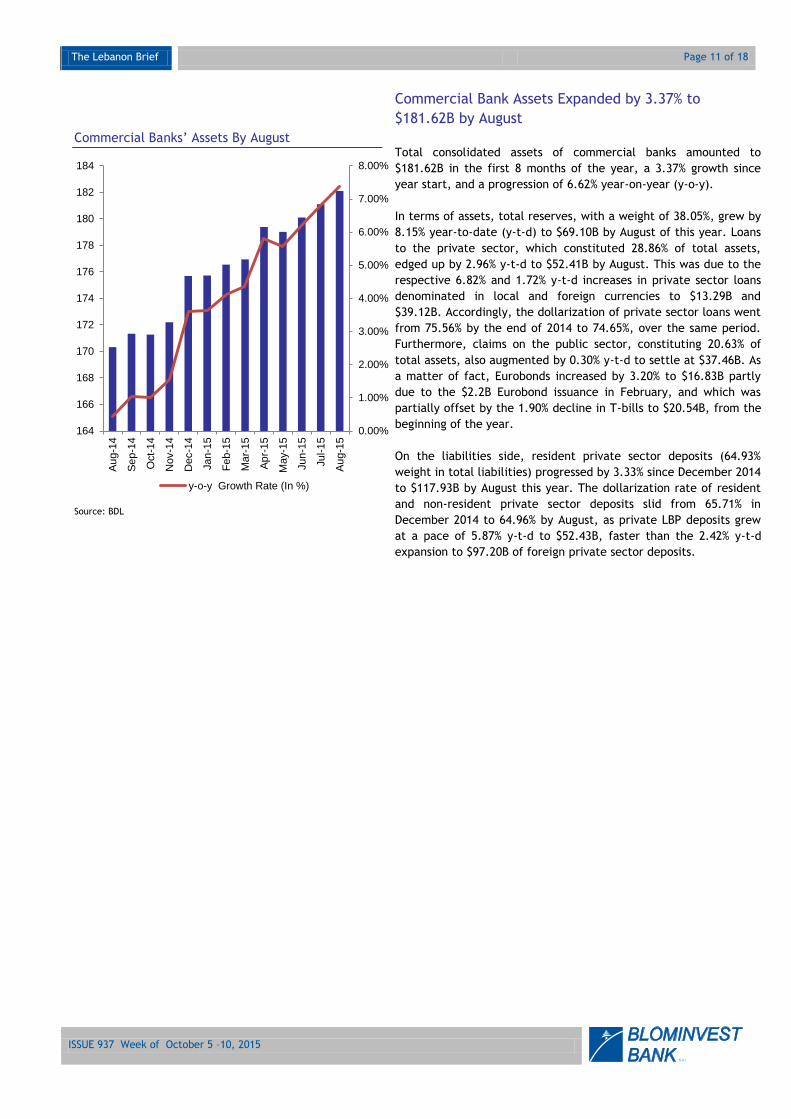

Commercial Banks’ Assets By August

Source: BDL

Commercial Bank Assets Expanded by 3.37% to

$181.62B by August

Total consolidated assets of commercial banks amounted to

$181.62B in the first 8 months of the year, a 3.37% growth since

year start, and a progression of 6.62% year-on-year (y-o-y).

In terms of assets, total reserves, with a weight of 38.05%, grew by

8.15% year-to-date (y-t-d) to $69.10B by August of this year. Loans

to the private sector, which constituted 28.86% of total assets,

edged up by 2.96% y-t-d to $52.41B by August. This was due to the

respective 6.82% and 1.72% y-t-d increases in private sector loans

denominated in local and foreign currencies to $13.29B and

$39.12B. Accordingly, the dollarization of private sector loans went

from 75.56% by the end of 2014 to 74.65%, over the same period.

Furthermore, claims on the public sector, constituting 20.63% of

total assets, also augmented by 0.30% y-t-d to settle at $37.46B. As

a matter of fact, Eurobonds increased by 3.20% to $16.83B partly

due to the $2.2B Eurobond issuance in February, and which was

partially offset by the 1.90% decline in T-bills to $20.54B, from the

beginning of the year.

On the liabilities side, resident private sector deposits (64.93%

weight in total liabilities) progressed by 3.33% since December 2014

to $117.93B by August this year. The dollarization rate of resident

and non-resident private sector deposits slid from 65.71% in

December 2014 to 64.96% by August, as private LBP deposits grew

at a pace of 5.87% y-t-d to $52.43B, faster than the 2.42% y-t-d

expansion to $97.20B of foreign private sector deposits.

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

164

166

168

170

172

174

176

178

180

182

184

Au

g-1

4

Se

p-1

4

Oct-

14

Nov-1

4

Dec-1

4

Jan

-15

Fe

b-1

5

Ma

r-15

Ap

r-15

Ma

y-1

5

Jun

-15

Jul-1

5

Au

g-1

5

y-o-y Growth Rate (In %)

The Lebanon Brief Page 12 of 18

ISSUE 937 Week of October 5 –10, 2015

S A L

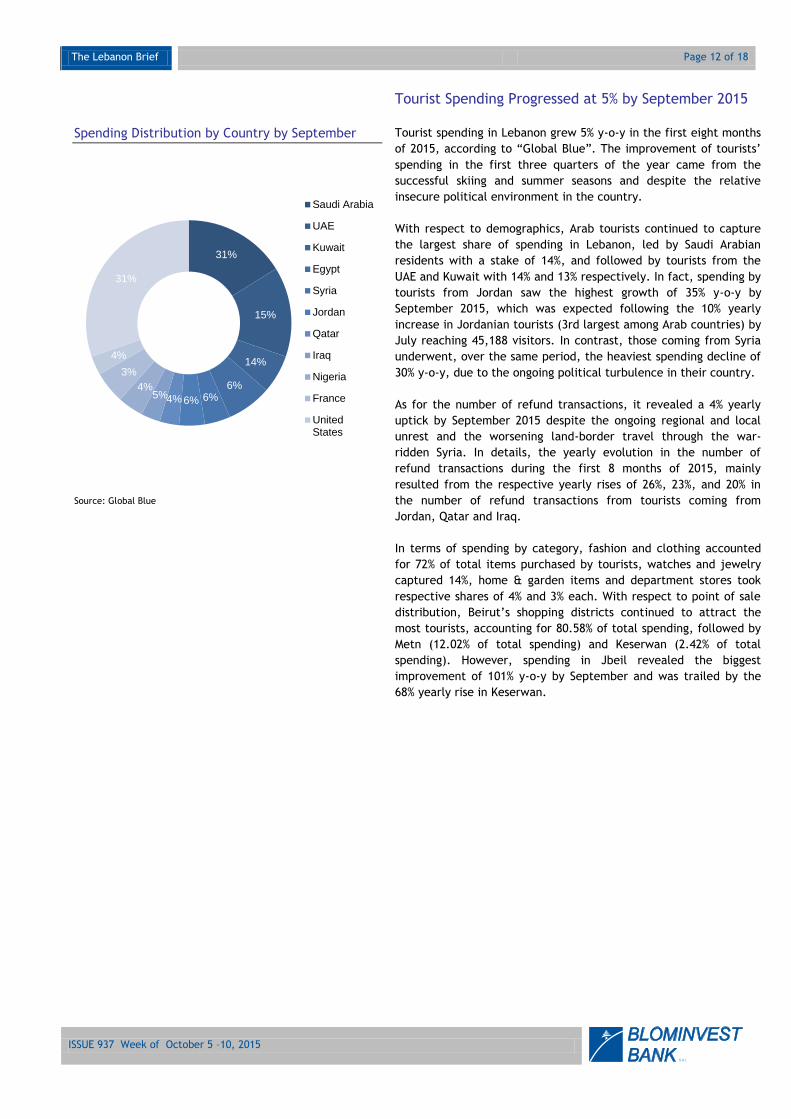

Spending Distribution by Country by September

Source: Global Blue

Tourist Spending Progressed at 5% by September 2015

Tourist spending in Lebanon grew 5% y-o-y in the first eight months

of 2015, according to “Global Blue”. The improvement of tourists’

spending in the first three quarters of the year came from the

successful skiing and summer seasons and despite the relative

insecure political environment in the country.

With respect to demographics, Arab tourists continued to capture

the largest share of spending in Lebanon, led by Saudi Arabian

residents with a stake of 14%, and followed by tourists from the

UAE and Kuwait with 14% and 13% respectively. In fact, spending by

tourists from Jordan saw the highest growth of 35% y-o-y by

September 2015, which was expected following the 10% yearly

increase in Jordanian tourists (3rd largest among Arab countries) by

July reaching 45,188 visitors. In contrast, those coming from Syria

underwent, over the same period, the heaviest spending decline of

30% y-o-y, due to the ongoing political turbulence in their country.

As for the number of refund transactions, it revealed a 4% yearly

uptick by September 2015 despite the ongoing regional and local

unrest and the worsening land-border travel through the war-

ridden Syria. In details, the yearly evolution in the number of

refund transactions during the first 8 months of 2015, mainly

resulted from the respective yearly rises of 26%, 23%, and 20% in

the number of refund transactions from tourists coming from

Jordan, Qatar and Iraq.

In terms of spending by category, fashion and clothing accounted

for 72% of total items purchased by tourists, watches and jewelry

captured 14%, home & garden items and department stores took

respective shares of 4% and 3% each. With respect to point of sale

distribution, Beirut’s shopping districts continued to attract the

most tourists, accounting for 80.58% of total spending, followed by

Metn (12.02% of total spending) and Keserwan (2.42% of total

spending). However, spending in Jbeil revealed the biggest

improvement of 101% y-o-y by September and was trailed by the

68% yearly rise in Keserwan.

31%

15%

14%

6% 6% 6% 4% 5%

4%

3%

4%

31%

Saudi Arabia

UAE

Kuwait

Egypt

Syria

Jordan

Qatar

Iraq

Nigeria

France

UnitedStates

The Lebanon Brief Page 13 of 18

ISSUE 937 Week of October 5 –10, 2015

S A L

CORPORATE DEVELOPMENTS

Year-to-Date Performance of BoB Preferred

Shares Class H

Source: BLOMINVEST Research Department

Characteristics of Capital Increase

Previous Capital LBP 5.2B

Capital After Issuance of Common Shares

LBP 10.60B

Number of Common Shares Issued 5.4M

Price/Share LBP 1,000

Source: MidClear

Bank of Beirut Announces its Redemption on its

Preferred Shares Class “H”

Bank of Beirut S.A.L. announces to the owners of preferred shares

class H that the Board of Directors decided in its meeting held on

26/09/2015, to redeem the Class H Preferred shares. This comes

consistent with Article B4, 4th paragraph of the 3rd decision taken

by the Extraordinary General Assembly of shareholders on

13/11/2008.

Baque De L’Industrie Et Du Travail S.A.L. Increased

Capital by LBP 5.4B ($3.65M)

On the 17th of March 2015, the general ordinary shareholders

assembly of Banque De L’Industrie Et Du Travail (BIT) S.A.L

convened to discuss the increase of the bank’s capital. On the 16th

of September, BIT decided to increase its capital by LBP 5.40B

($3.65M) from LBP 5.2B ($3.45) to LBP 10.60B ($7.03M), through the

issuance of 5.4M new common nominal shares. The price of a share

is LBP 1,000 ($0.66). Furthmore, this has been authorized by

MidClear on the 7th of October, 2015.

25.2

25.4

25.6

25.8

26

26.2

26.4

26.6

The Lebanon Brief Page 14 of 18

ISSUE 937 Week of October 5 –10, 2015

S A L

NFB Financial Highlights

Dec 31, 2014 March 31, 2015

Total Assets ($B) 3.93 3.81

Customer s' Deposits and credit Accounts ($B)

3.24 3.09

Total Equity ($M) 266.18 274.21

Net Profit ($M) 6.26 7.54

*On March 31, 2014

Source: Bank’s Website

Launching of the “First National Dollar Fund” by First

National Bank

First National Bank Launched a fund, on the 7th of October 2015

named “First National Dollar Fund“, Authorized by MidClear, the

fund will be mainly a mixture of investment in fixed income

securities denominated in Dollars and preferred shares. Returns

may vary between the range of 5.50% and 5.75% net of fess,

commission and taxes. Worth mentioning that the minimum

subscription is $10,000 per investor.

The Lebanon Brief Page 15 of 18

ISSUE 937 Week of October 5 –10, 2015

S A L

FOCUS IN BRIEF

Marble and Granite Industry in Lebanon

Owing to the fact that no 2 places on earth have the exact same geological composition or experience, or the same

geological forces, natural stones are like fingerprints, each one is unique. This means that natural stone of the same type

can also vary widely. This is why, even if a country is a producer of natural stones, it has to import from other countries to

have a wide variety of these stones.

Due to the usage of natural stone as building and decoration material, the trade of natural stone became very important. In

parallel with technological developments, the natural stone extraction and processing have been increased with a minimum

loss in recent decades. This report focuses on two types of natural stones: granite and marble.

According to Global Trade Atlas, the international trade of stone products reached a value of $25.65B, growing by 1.87%

compared to 2013’s value of $25.18B. From a quantity perspective, 85.9M tones of natural stones were traded in 2014,

compared to 80M tones in 2013. China is the world’s largest exporter of natural stores with a market share of 35.8%,

followed by Italy and Turkey with respective shares of 13.5% and 12.1%.

As for the international demand of natural stones, it stood at 39M tones, for a total value of around $11.22B, with a 5.6%

increase in quantity and a 2.7% increase in value compared to 2013. The leading country for imports was China with a 21.9%

share, followed by the United States (19.8%) and Japan (6%).

Granite is a versatile natural stone product that can be used almost everywhere, and mainly for kitchen countertops. Due

to its high density, granite does not host bacteria. Combined with the fact that it does not respond to acid, granite is

among the most sanitary countertop materials available. Because of its low absorption rate, granite is less prone to staining

and is also heat resistant making it ideal for surface tops. This makes granite the most durable of all surfaces used in

counter top construction. Granite is also used for immense structural works due to its high compressive strength. Granite’s

rich and varied colors, stiffness, and density, make it the ideal choice for flooring, vanities, as well as exterior applications.

Next to diamond, granite is the hardest natural stone available. Granite surface tops have a smooth and high gloss finish

that exacts the elegance and beauty of the material while maintaining its durability.

As for marble, it has been valued for thousands of years for its rich palette of beautiful colors and appearance. Marble

stones consist of limestone that has undergone heat and pressure. Variations of whiteness of pure marbles are due to the

mixture of foreign substances, which form streaks and clouds. Very few rocks have as many uses as marble. It is used for its

beauty in architecture and sculpture. It is used for its chemical properties in pharmaceuticals and agriculture. It is used for

its optical properties in cosmetics, paint and paper. It is used because it is an abundant, low-cost commodity in crushed

stone prepared for construction projects. Marble has many unique properties that make it a valuable rock in many different

industries.

The size of the marble and granite market in Lebanon is around $96.61M, with more than 400 factories and 600 traders.

Although there are a lot of marble factories, there are only 2 granite producers, the biggest being Middle East Granite. This

can be attributed mainly to the fact that the machines that cut and polish crude granite are more expensive than that of

marble, and require more sophisticated techniques. Moreover, the demand for granite is much lower than the demand for

marble.

Due to the severe rivalry in the market, no one company can control the prices of its products. The prices follow the

international market. According to Jamil Saadeh, owner of Saadeh for General Trading, the markup for granite and marble

is usually 30%.

Depending on the quality, color, and origin of marble slabs, the majority of demand is concentrated at a price range of

$35/m2 to $90/m2. The lighter the color of the marble and the fewer layers it has, the more expensive it is. Similarly, the

majority of demand for granite slab ranges from a price of $50/m2 to $180/m2, also depending on the quality, color and

origin of the stone.

Within the respective ranges, certain people choose the cheaper stones because they are not well-informed about their

quality and the cutting and polishing services provided by the factory or the trader. Construction companies and real estate

The Lebanon Brief Page 16 of 18

ISSUE 937 Week of October 5 –10, 2015

S A L

developers usually opt for marble and granite with low prices, since they are for commercial use. In contrast, people

renovating their houses or building their own, in addition to hotels and malls choose more expensive natural stones.

No tariff is imposed on crude marble and granite imported. However, except for the ones imported from the EU and Arab

countries, a 25% custom duty is imposed on finished granite and marble. Nevertheless, customs are not well informed about

the quality and costs of the stones, which is leading to the billing of inaccurate invoices. Hence many traders are taking

advantage of this and importing marble and granite at very low costs.

This manipulation has caused several granite and marble factories to seize their activities because of the fierce and unfair

competition they are facing. According to Jad Rizk from Ets Nabil G. Rizk, the Lebanese marble factories are facing tough

competition from imports, especially Egyptian marble. The lowest price of raw marble sold at his factory is around $30/m2.

However, Lebanese importers are selling finished Egyptian marble at a price of $13/m2.

Other than having the know-hows and the high costs of installing a marble and/or granite factory, there are no barriers to

enter this market. As a trader, the only barrier to entry is the 25% custom duty on finished marble and granite imports.

Like all industries in Lebanon, demand for natural stones is affected by the economic and political situation locally and that

of Lebanon’s trade partners. Therefore, production declined after the Arab spring and the war in Syria. In addition, due to

the political developments in the country that led to a recession in the construction sector, local demand for marble and

granite decreased. However, according to Arabian Marble Habre, since companies usually take long-term projects of around

4 years, production trails behind demand.

Regarding trade of natural stones, customs data show that Lebanon has been a net importer of marble and granite for the

past 4 years, with a trade deficit reaching $77.46M in 2014.

Imports and Exports of Crude Marble ($M) Import and Exports of Finished Marble ($M)

Source: Customs

Crude marble imports have been on the rise. The value of crude marble imports increased by 24.82% compared to 2013, to

reach $30.47M in 2014. In terms of quantity, imported raw marble grew 3.23% to 159,312 tons in 2014. In the first 8 months

of 2015, the value of crude marble imports decreased by 43.01% with a 37.55% decline in volume. Lebanon imports 54.78%

of crude marble from Italy, 13.81% from Turkey and 7.65% from Egypt.

Similarly, finished marble imports edged up 31.23% to $41.41M, with a 31.60% growth in quantity to 184,680 tons. For the

first 8 month of 2015, the value and volume of finished marble imported increased by 23.64% and 5.95%, respectively,

compared to the same period of 2014. 53.10% is imported from Egypt, 12.34% from Italy, and 8.33% from Spain.

Looking at crude marble exports, they increased 31.63% to $1.68M, with only a 1.23% increase in quantity to 12,393 tons.

However, comparing 2014 to 2011 and 2012, a 52.25% and 43.31% plunges in the value of crude marble exports is revealed,

with a 44.75% and 45.36% declines in the number of tons. This is mainly due to the Arab Spring, which halted exports to the

Arab markets. For the first 8 months of 2015, the value of crude marble imported dropped by 30.87% with a 21.99%

decrease in volume. Italy is the main importer of Lebanese crude marble with a 35.64% share, followed by Egypt and the

United Arab Emirates with respective shares of 26.89% and 9.73%

28.70 28.07

24.41

30.47

3.89 3.27 1.41 1.86

2011 2012 2013 2014

Import Export

28.16

33.26

31.56

41.41

9.16

12.68 13.89

11.06

2011 2012 2013 2014

Import Export

The Lebanon Brief Page 17 of 18

ISSUE 937 Week of October 5 –10, 2015

S A L

In the meantime, there was a 20.35% decrease in the value of finished marble exported to $11.06M, with a 25.63%

plummet in the quantity to 6,068 tons. This trend continued in 2015, where up to August, the value of finished marble

exported plunged by 32.66% annually, with a 28.92% decline in quantity. 44.14% of finished marble is exported to Saudi

Arabia, 23.42% to Qatar and 9.07% to Jordan. According to Jad Rizk from Ets Nabil G. Rizk, production of raw marble has

been declining since 2005, due to the closing of marble quarries. In turn, this led to a decline in marble exports. For

instance, Ets Nabil G. Rizk used to export polished tiles to markets of the US, UK, Australia, Qatar, UAE, and KSA by more

than 85 containers per annum. However, after the closing of quarries, their export activity stopped.

Imports & Exports of Crude Granite ($thousands) Imports & Exports of Finished Granite ($thousands)

Source: Customs

Regarding crude granite imports, there was a 26.17% yearly decrease in the value of crude granite to $866,000, coupled

with a 12.37% decrease in the volume to 2,727 tons in 2014. During the first 8 months of 2015, the value of crude granite

imported increased by 19.03%, where the volume more than doubled surging by 102%. 52.24% of crude granite is imported

from Italy, 18.78% from China, and 13.60% from Spain.

Finished granite imports also saw a 4.92% annual decline to $16.13M, but at a 1.39% higher volume of 65,554 tons in 2014.

Up to August 2015 finished granite imports decreased by 4.86% in value and by 6.59% in volume. 48.41% of finished granite

is imported from India, 46.74% from China, and 1.99% from Italy. The decline in granite imports could be attributed to the

shift in demand towards a new artificial stone: Quartz. Quartz is considered new, modern, and has the advantage of finding

all colors in plain over granite. However it is almost double the cost of granite.

Concerning exports, crude granite saw a 4.25% rise to $270,000, however at a 39.58% decline in quantity to 316 tons.

Similarly, for the first 8 months of 2015, crude granite exports increased by 14.07% in value and 62.68% in volume. 96.43%

of the crude granite is exported to Belgium, while the rest, 3.25%, is exported to Kuwait.

Finished granite exports augmented by 14.25% to $521,000 with a 38.93% increase in quantity to 678 tons, in 2014. On the other hand, up to August 2015, finished granite saw a 33.33% yearly decline in value and a 66.55% drop in quantity. 30.22% of finished marble is exported to Ghana, 24.82% to Congo, and 15.83% to Liberia. The growth of the marble and granite industry hinges on the development of the real estate and construction sectors. When the real estate and construction activities were booming in the period of 2008-2009, the natural stones industry was thriving. Pressures from the Syrian war and the fragile domestic situation stalled the real estate sector, which in turn started the downward spiral of the marble and granite industry. With no recovery perceived until now on the political and economic front, many marble and granite factories are considering to open in Gulf countries.

1,582

843

1,173

866

167 24

259

270

2011 2012 2013 2014

Import Export

15,382

16,651 16,960

16,126

411 572 488

678

2011 2012 2013 2014

Import Export

The Lebanon Brief

Page 18 of 18

Your Investment Reference

S A L

Research Department: Wael Khoury [email protected] Lana Saadeh [email protected] Riwa Daou [email protected] Mirna Chami [email protected]

Marwan Mikhael [email protected]