the lawyer's mba - association of corporate · pdf file · 2015-10-29the...

TRANSCRIPT

The Lawyer's MBA

October 27, 2015

2 Presented by WilmerHale

• Understanding key financial concepts is critical to the ability of in-house attorneys to advise their business clients in the context of capital raising transactions

• Being an effective counselor requires an understanding of the legal aspects of different capital structures

• In-house counsel may be called upon to structure and negotiate key deal terms, including appropriate financial covenants, and monitor ongoing compliance

Why are we here today?

3 Presented by WilmerHale

Financial accounting• Financial statements and accounting terminology• How it is used in making investment and financing decisionsWorkshop – Calculating and understanding the impact of financial metrics

Financing the business• Capital structure considerations• Sources of capital

Understanding equity and debt financing • Types and sources of equity and capital• Key terms and considerations• Negotiating financial covenants in debt agreements Workshop – Drafting financial covenants in commercial agreements

What we will cover

4 Copyright © 2015 Deloitte Development LLC. All rights reserved.

• 8:00-8:30AM Registration/Check-in

• 8:30-9:45AM Welcome and Introduction to Financial Statements

• 9:45-10:15AM Workshop Activities

• 10:15-10:30AM Break

• 10:30-12:00PM Financing the Business Part I

• 12:00-12:45PM Lunch

• 12:45-2:15PM Financing the Business Part II

• 2:15-2:30PM Break

• 2:30-3:15PM Workshop Activities

• 3:15-3:30PM Debrief/Wrap-up

Agenda

Module 1 - Introduction to Accounting &Financial Statements

6 Module 1 – Introduction to Accounting & Financial Statements Copyright © 2015 Deloitte Development LLC. All rights reserved.

• Financial reporting building blocks and concepts

• US GAAP financial statements and analysis points− Balance sheet− Income statement− Statement of owner's or stockholder’s equity − Statement of cash flows− Notes to the financial statements

• Common accounting terminology

• Introduction to financial statement fraud

• Summary of learning points

• Questions and answers

Agenda

Note: Any definition not sourced are from Financial Accounting/Kermit D. Larson, Paul B. Miller – 5th Edition.

Financial Reporting Building Blocks and Concepts

8 Module 1 – Introduction to Accounting & Financial Statements Copyright © 2015 Deloitte Development LLC. All rights reserved.

Financial statement reporting:A full set of financial statements

Set of financial statements

Balance sheet

Statement of cash flows

Statement of owners’ or stockholders’ equity

Notes to the financial statements

Income statement

Description

• Shows the financial position (assets and liabilities) of the company at the end of the period.

• Shows the results of the operations for the period.

• Shows cash inflows (receipts) and outflows (uses) for the period.

• Explains investments by and distributions to owners during the period.

• Provides qualitative data.

9 Module 1 – Introduction to Accounting & Financial Statements Copyright © 2015 Deloitte Development LLC. All rights reserved.

Sources of financial statements/reporting

Public• www.sec.gov− Form 10-K — Annually, audited financial

statement with notes, and Management Discussion & Analysis (MD&A)

− Form 10-Q — Quarterly, reviewed financial statements, MD&A

− Form 20-F — Foreign Private Issuer− Form 8-K — Filed for significant events− Form S-1 — Initial registration

proceedings− Form S-3 — Debt/Equity offerings− Other Filings

Private

• Company website

• Dun & Bradstreet

• Hoover’s

• Dow Jones Interactive

10 Module 1 – Introduction to Accounting & Financial Statements Copyright © 2015 Deloitte Development LLC. All rights reserved.

• Provide useful information in:− Investment and credit decisions − Assessing cash flow prospects

• Provide useful information about:− Enterprise resources, claims to those resources, and changes in the resources− Economic resources, obligations, and owners’ equity− Enterprise performance and earnings− Liquidity, solvency, and funds flows

Financial statement reporting: Objective

“…intended to provide information that is useful in making business and economic decisions.”

Source: FASB Statement of Financial Accounting Concepts No. 1

11 Module 1 – Introduction to Accounting & Financial Statements Copyright © 2015 Deloitte Development LLC. All rights reserved.

• Accounting information used for Financial Reporting requires:

− Relevance: capacity to make a difference in a decision◦ Predictive Value: increases the likelihood of forecasting the outcome of events◦ Feedback Value (timely): enables users to confirm or correct prior expectations

− Reliability: information is reasonably free from error and bias◦ Representatively Faithful (validity): information represents what it purports to

represent◦ Verifiable: ability to ensure that information represents what it purports to represent◦ Neutral: absence of bias to attain a predetermined result

Financial reporting concepts

Source: CON 2, Qualitative Characteristics of Accounting Information

12 Module 1 – Introduction to Accounting & Financial Statements Copyright © 2015 Deloitte Development LLC. All rights reserved.

• The significance of information, especially quantitative information, depends on the users ability to relate it to some benchmark:

− Comparability◦ The quality of information that enables users to identify similarities in and differences

between two sets of economic phenomena

− Consistency◦ Conformity from period to period with unchanging policies and procedures

Financial reporting concepts (cont.)

Source: CON 2, Qualitative Characteristics of Accounting Information

US GAAP Financial Statements and Analysis Points

14 Module 1 – Introduction to Accounting & Financial Statements Copyright © 2015 Deloitte Development LLC. All rights reserved.

• “Generally Accepted Accounting Principles”• Rules or conventions that govern what, when, and how to

record transactions• Prescribes what information should be disclosed and how it

should be disclosed• Promulgated primarily by the Financial Accounting

Standards Board (“FASB”)• Cash vs accrual accounting

GAAP

15 Module 1 – Introduction to Accounting & Financial Statements Copyright © 2015 Deloitte Development LLC. All rights reserved.

• Established accounting standards promulgated by the London-based International Accounting Standards Board (IASB)

• IFRS is a broad, globally accepted set of accounting standards:− Principles-based approach with a greater emphasis on interpretation and

application of principles− Less extensive body of literature than U.S. GAAP, with limited industry-specific

guidance and less detailed application guidance

• IFRS will require more exercise of judgment, supportedby contemporaneous analysis and documentation

• No definitive plan or timeline of mandating IFRS in U.S.

IFRS

16 Module 1 – Introduction to Accounting & Financial Statements Copyright © 2015 Deloitte Development LLC. All rights reserved.

• Corporate attorneys will need to work with management to confirm strong documentation of policies, procedures, and protocols to reduce the risk of litigation based upon the application of management’s judgments and estimates

• M&A attorneys involved in the drafting of contracts will need to consider the impact of IFRS on earn-outs, credit agreements, purchase agreements, sales contracts, and bonus plans

• White collar defense and corporate investigation attorneys may see a shift in cases to IFRS based regulatory proceedings

• Malpractice attorneys will need to prepare themselves for the way audits are performed under IFRS

How will IFRS impact attorneys

Balance Sheet

18 Module 1 – Introduction to Accounting & Financial Statements Copyright © 2015 Deloitte Development LLC. All rights reserved.

Classification of Assets

Assets

TangibleAssets

(physical)

CurrentAssets

(<1 year)

Non-CurrentAssets

(>1 year)

Intangible Assets

(not physical)

CurrentAssets

(<1 year)

Non-CurrentAssets

(>1 year)

examplescash

inventory

examplesproperty plant

equipment

examplecopyrights patents

licenses (expiring <1 year)

examplescopyrights patentslicenses goodwill

19 Module 1 – Introduction to Accounting & Financial Statements Copyright © 2015 Deloitte Development LLC. All rights reserved.

Classification of Liabilities

Liabilities

KnownAmounts

Current Liabilities(<1 year)

Non-CurrentLiabilities(>1 year)

Estimated Amounts

Current Liabilities(<1 year)

Non-CurrentLiabilities(>1 year)

examplelitigation accrual

exampleaccountspayable

examplenotes

payable

exampleproduct warranty liability

20 Module 1 – Introduction to Accounting & Financial Statements Copyright © 2015 Deloitte Development LLC. All rights reserved.

As of December 26, 2014 (in thousands)Example: Dynamites, Inc. Balance Sheet

ASSETSCurrent assets:

Cash and equivalents 13,150$ Marketable securities 25,594 Accounts receivable, net of allowance of $25 7,792 Inventory 4,043 Prepaid expenses 2,375 Taxes 8,893 Restricted assets 27,346

Total current assets 89,193

Property and equipment, net 198,679 Other assets 21,891 Intangible assets* 11,383

Total assets 321,146$

LIABILITIES AND STOCKHOLDERS' EQUITYCurrent liabilities:

Unearned franchise fees 1,186$ Accounts payable 19,274 Accrued compensation and benefits 19,536 Accrued Expenses 4,855 Current portion of deferred lease credits - System-wide payables 28,344 Current portion of long-term debt 641

Total current liabilities 73,836

Long-term liabilities:Other liabilities 989 Deferred income taxes 24,669 Deferred lease credits, net of current portion 14,763 Long-term debt 3,203

Total liabilities 117,460

Commitments and contingencies (notes 4 & 8)Stockholders' equity:

Common stock 72,708 Retained earnings 131,167 Accumulated other compensation loss (189)

Total stockholders' equity 203,686Total liabilities and stockholders' equity 321,146$

* One type of intangible asset is goodwill which will be discussed in detail later in the module.Data is for illustrative purposes only.

21 Module 1 – Introduction to Accounting & Financial Statements Copyright © 2015 Deloitte Development LLC. All rights reserved.

• How liquid are the assets?

• How leveraged is the company?

• What is the breakdown between short-term and long-term debt?

• What is the quality of the assets?

Several things to look for on the balance sheet

22 Module 1 – Introduction to Accounting & Financial Statements Copyright © 2015 Deloitte Development LLC. All rights reserved.

If Dynamites wanted to assess its liquidity, which of the following elements could be useful?

a) Cash

b) Accounts receivable

c) Marketable securities

d) All of the above

Knowledge Check

Income Statement

24 Module 1 – Introduction to Accounting & Financial Statements Copyright © 2015 Deloitte Development LLC. All rights reserved.

Revenue• Inflows or other enhancements of assets of an entity or settlements of its

liabilities from delivering or producing goods, rendering services, or other activities that constitute the entity’s ongoing major or central operations

Gains• Gains are increases in equity (net assets) from peripheral or incidental

transactions of an entity and from other transactions and other events and circumstances affecting the entity, except those that result from revenues or investments by owners.

SOURCE: SFAC 6, Elements of Financial Statements

Income Statement Elements

25 Module 1 – Introduction to Accounting & Financial Statements Copyright © 2015 Deloitte Development LLC. All rights reserved.

Expenses• Outflows or other “using up” of assets or “incurrence” of liabilities from delivering

or producing goods, rendering services, or other activities that constitute the entity’s ongoing major or central operations.

Losses• Losses are decreases in equity (net assets) from peripheral or incidental

transactions of an entity and from other transactions and other events and circumstances affecting the entity, except those that result from expenses or distributions to owners.

SOURCE: SFAC 6, Elements of Financial Statements

Income Statement Elements

26 Module 1 – Introduction to Accounting & Financial Statements Copyright © 2015 Deloitte Development LLC. All rights reserved.

For the years ended December 26, 2014 and December 27, 2013 (in thousands)

Example: Dynamites, Inc. Income Statement

Dec. 26, 2014 Dec. 27, 2013

Revenue:Restaurant sales 459,527$ 355,623$ Franchise royalties and fees 42,970 37,198

Total revenue 502,497 392,821

Costs and Expenses:Restaurant operating costs 366,778 290,339 Depreciation and amortization 31,972 25,113 General and administrative 46,561 34,587 Preopening 9,329 5,379 Loss on asset disposals and store closures 1,236 1,314

Total costs and expenses 455,876 356,732

Income from operations 46,621 36,089 Investment income 76 438 Earnings before income taxes 46,697 36,527 Income tax expense 14,397 11,930 Net earnings 32,300$ 24,597$

Data is for illustrative purposes only.

27 Module 1 – Introduction to Accounting & Financial Statements Copyright © 2015 Deloitte Development LLC. All rights reserved.

• Is the company profitable?

• What portion of the income is from non-recurring/non-operating transactions?− Were there any one-time occurrences during the year?− Have any operations been discontinued?

• Are there any expense items that seem out of line?

Several things to look for on the income statement

Statement of Owners’ or Stockholders’ Equity

29 Module 1 – Introduction to Accounting & Financial Statements Copyright © 2015 Deloitte Development LLC. All rights reserved.

• Presents the changes (the composition of additional capital, dividends, earnings) in owners’ equity over a certain period of time

• Reconciles the balance of the retained earnings account from the beginning to the end of the period

• Shows the interaction between the income statement (net income) and the balance sheet (retained earnings)

Statement of Changes in Owners’ Equity

30 Module 1 – Introduction to Accounting & Financial Statements Copyright © 2015 Deloitte Development LLC. All rights reserved.

For the year ended December 26, 2014 (in thousands)

Example: Dynamites, Inc. Statement of Stockholders’ Equity

OtherRetained Comprehensive

Shares Amount Earnings (Loss) Income TotalBalance at December 27, 2013 18,214,065 65,647$ 98,866$ (6)$ 164,507$

Net earnings - - 32,300 - 32,300Other comprehensive loss - - - (183) (183)Comprehensive income - - - - 32,117Purchase and cancelation of common stock - - 1 - 1Shares issued under employee

stock purchase plan 30,127 879 - - 879Shares issued from restricted stock units 142,797 - - - -Units effectively repurchased for

required employee withholding taxes (45,539) (4,183) - - (4,183)Exercise stock options 36,470 216 - - 216Tax benefit from stock issued - 2,858 - - 2,858Stock-based compensaton - 7,291 - - 7,291Balance at December 26, 2014 18,377,920 72,708$ 131,167$ (189)$ 203,686$

Common Stock

Data is for illustrative purposes only.

Statement of Cash Flows

32 Module 1 – Introduction to Accounting & Financial Statements Copyright © 2015 Deloitte Development LLC. All rights reserved.

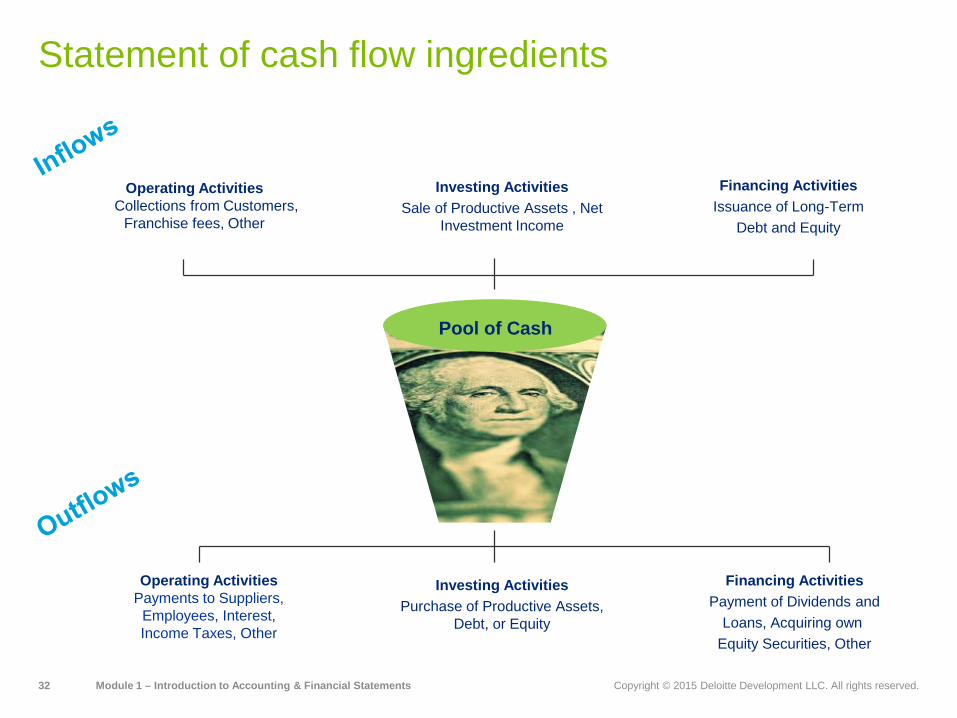

Statement of cash flow ingredients

Operating ActivitiesCollections from Customers,

Franchise fees, Other

Investing ActivitiesSale of Productive Assets , Net

Investment Income

Financing ActivitiesIssuance of Long-Term

Debt and Equity

Operating ActivitiesPayments to Suppliers,

Employees, Interest, Income Taxes, Other

Investing ActivitiesPurchase of Productive Assets,

Debt, or Equity

Financing ActivitiesPayment of Dividends and

Loans, Acquiring own Equity Securities, Other

Pool of Cash

33 Module 1 – Introduction to Accounting & Financial Statements Copyright © 2015 Deloitte Development LLC. All rights reserved.

For the year ended December 26, 2014 (in thousands)

Example: Dynamites, Inc. Statement of Cash Flows (Indirect Method)

CASH FLOWS FROM OPERATING ACTIVITIES:Net Earnings 32,300$ Adjustments to reconcile net earnings to cash provided by operations:

Depreciation 31,389 Amortization 583 Loss on asset disposals and store closures 1,076 Deferred lease credits 2,326 Deferred income taxes 8,209 Stock-based compensation 7,291 Excess tax benefit from stock issuance (2,857) Changes in operating assets and liabilities, net effect of acquisition:

Trading securities (203) Accounts receivable (783) Inventory (1,179) Prepaid expenses 13 Other assets (1,633) Unearned franchise fees (165) Accounts payable 11,322 Income taxes 2,093 Accrused expenses 5,185

Net cash provided by operating activities 94,967$

CASH FLOWS FROM INVESTING ACTIVITIES:Purchase of property and equipment (83,353)$ Purchase of marketable securities (62,228) Proceeds of marketable securities 73,239 Acquisition of franchised restaurants (21,615)

Net cash used by investing activities (93,957)

CASH FLOWS FROM FINANCING ACTIVITIES:Issuance of Common Stock 1,095 Excess tax benefit from stock issuance 2,858 Tax payments for restricted stock units (1,589)

Net cash provided by financing activities 2,364 Effect of exchange rate changes on cash and cash equivalents (30)

Net increase in cash and cash equivalents 3,344 Cash and cash equivalents at beginning of year 9,806 Cash and cash equivalents at end of year 13,150$

Data is for illustrative purposes only.

34 Module 1 – Introduction to Accounting & Financial Statements Copyright © 2015 Deloitte Development LLC. All rights reserved.

• Does the company have positive cash flow?

• Did the company’s cash position change significantly?

• How is the company using its cash?

• What were the sources of the company’s funds?

• Comparison of Income Statement to Cash Flow Statement:− Strong income from continuing operations versus weak cash flow provided by

operating activities

• Assess the ability of the company to meet its obligation, pay dividends, need for external financing

Several things to look for on the cash flow statement

35 Module 1 – Introduction to Accounting & Financial Statements Copyright © 2015 Deloitte Development LLC. All rights reserved.

Relationships Among Financial Statement Line Items

Income Statement Balance Sheet

Revenue 502,497$ AssetsCost of Sales 366,778 Cash 13,150$ Depreciation and Amortization 31,972 Other Current Assets 76,043 Other Operating Expenses 57,126 Property & Equipment 306,988 Other Non-Operating Expenses 14,321 Accumulated Depreciation (108,309) Net Income 32,300$ Other Non-Current Assets 33,274

Total Assets 321,146$ Cash Flow Statement

Net Income 32,300$ LiabilitiesDepreciation and Amortization 31,972 Current Liabilities 73,836$ Other Cash Flow From Operating 30,695 Long-Term Liabilities 43,624 Cash Flow From Operations 94,967 Total Liabilities 117,460 Cash Flow From Investing (93,957) Shareholders' Equity 203,686 Cash Flow From Financing 2,364 Total Liabilities + Equity 321,146$

Effect of exchange rate changes Statement of Stockholders' Equityon cash and cash equiv. (30) Beginning Balance 164,507$ Increase in Cash 3,344 Net Income 32,300 Beginning Cash Balance 9,806 Other Comprehensive loss (183) Ending Cash Balance 13,150$ Stock & Option Repurchase (3,087)

Other Equity Transactions 10,149 Total Stockholders' Equity 203,686$

B

C

D

E

Data is for illustrative purposes only.

Notes to the Financial Statements

37 Module 1 – Introduction to Accounting & Financial Statements Copyright © 2015 Deloitte Development LLC. All rights reserved.

Provides further explanations and may provide the only explanations for significant transactions and contains required disclosures

Financial statement reporting:Notes to the financial statements

• Overview of the business

• Significant accounting policies‒ Revenue recognition‒ Principles of consolidation‒ Property, plant & equipment‒ Intangible assets & goodwill‒ Long-term debt

• Discontinued operations

• Business combinations

• Debt offerings and credit risk

• Income taxes

• Related party transactions

• Subsequent events

• Commitments and Contingencies

38 Module 1 – Introduction to Accounting & Financial Statements Copyright © 2015 Deloitte Development LLC. All rights reserved.

• Information often results from approximate, rather than exact measures.– Example: Estimates include the allowance for doubtful accounts receivable,

carrying value of certain intangibles, contingencies, etc.

• Information is based upon historical data and does not measure or discuss management’s plans for the future.– Example: The benefits of a company’s restructuring plan might not benefit the

company until several years after the plan is announced/implemented.

• Information is generally recorded at cost and may not reflect the current market value.– Example: Generally, fixed assets are accounted for at cost, and not at their fair

market value (FMV). For example, a building built in the 1950s will be recorded at the amount for which it was constructed and not at its FMV in 2012.

Financial statement reporting:Limitations on financial statements

Common Accounting Terminology

40 Module 1 – Introduction to Accounting & Financial Statements Copyright © 2015 Deloitte Development LLC. All rights reserved.

• A measure of the significance of a transaction or event. A transaction is considered material if its omission or misstatement would affect the judgment of a reasonable person relying on the financial statements.

Materiality

Source: Staff Accounting Bulletin (SAB) No. 99

41 Module 1 – Introduction to Accounting & Financial Statements Copyright © 2015 Deloitte Development LLC. All rights reserved.

• A prudent reaction to uncertainty to try to confirm that uncertainty and risks inherent in business situations are adequately considered.− If two estimates of amounts to be received or paid in the future are about

equally likely, conservatism dictates using the less optimistic estimate; however, if two amounts are not equally likely, conservatism does notnecessarily dictate using the more pessimistic amount rather than the more likely one.

Conservatism

42 Module 1 – Introduction to Accounting & Financial Statements Copyright © 2015 Deloitte Development LLC. All rights reserved.

Definition

“a contingency is defined as an existing condition, situation, or set of circumstances involving uncertainty as to possible gain or loss to an enterprise that will ultimately be resolved when one or more future events occur or fail to occur. Resolution of the uncertainty may confirm the acquisition of an asset or the reduction of a liability or the loss or impairment of an asset or the incurrence of a liability.”

Contingencies

Source: ASC 450, Accounting for Contingencies

43 Module 1 – Introduction to Accounting & Financial Statements Copyright © 2015 Deloitte Development LLC. All rights reserved.

Loss contingency

Determination and consideration of facts by company management and auditors

Probable (high) Reasonably possible (medium) Remote (low)

Can amount be reasonably estimated?

Is loss guarantee of indebtedness?

Accrual, with disclosure required Disclosure required Neither accrual nor

disclosure required

*Includes estimation of range of loss, in which case the minimum amount is accrued and the amount of the range is disclosed

Probability that future event(s) will confirm loss

YesNo

NoYes*

44 Module 1 – Introduction to Accounting & Financial Statements Copyright © 2015 Deloitte Development LLC. All rights reserved.

• Pro Forma — provides information about the continuing impact of a particular transaction by showing how it might have affected historical financial statements if a transaction (acquisition or disposition) had been consummated at an earlier time. − Example:◦ For a business combination, the financial statements shall include certain pro forma

information, such as the “results of operations for the current period as though the business combination(s) had been completed at the beginning of the period”

◦ Source, ASC 805, Business Combinations

• Historical — measures income or presents a financial position for past events. The information as reported in historical financial statements is a summarized presentation of the operations of the business during a specific period of time.

Pro Forma vs. Historical financial statements

45 Module 1 – Introduction to Accounting & Financial Statements Copyright © 2015 Deloitte Development LLC. All rights reserved.

• GAAP are the rules that govern what, when, and how to record transactions and prescribe what information should be disclosed and how it should be disclosed in the financial statements.

• Non-GAAP amounts are amounts that are not defined in the GAAP accounting literature, such as EBITDA (Earnings Before Interest, Taxes, Depreciation & Amortization)

• Public companies are required to reconcile Non-GAAP measures to the corresponding GAAP measure

• Area of manipulation on which regulators focus their attention

GAAP vs. Non-GAAP measures

46 Module 1 – Introduction to Accounting & Financial Statements Copyright © 2015 Deloitte Development LLC. All rights reserved.

If Dynamites determined that the probability of a future loss was probable, but the dollar impact could not be reasonably estimated, what action could you suggest Dynamites take?

a) Book an accrual for an amount agreed upon by management

b) Disclose the future event in the notes to the financial statements providing adequate detail

c) Both a) and b)

d) No action is required

Knowledge Check

Introduction to Financial Statement Fraud

48 Module 1 – Introduction to Accounting & Financial Statements Copyright © 2015 Deloitte Development LLC. All rights reserved.

Source: 2014 ACFE Report to the Nation on Occupational Fraud & Abuse

Fraud Types

• Asset Misappropriation – billing (fictitious services, inflated invoices, etc.), payroll, expense reimbursement schemes • Corruption – wrongly using influence in a business transaction• Financial Statement Fraud – falsification of statements (overstating revenue, understating expenses, etc.)

49 Module 1 – Introduction to Accounting & Financial Statements Copyright © 2015 Deloitte Development LLC. All rights reserved.

Accounting anomalies

Internal control symptoms

Analytical anomalies

Lifestyle symptoms

Behavioral symptoms

Tips and complaints

Categories of Fraud Symptoms

─Source: Internal Auditor Magazine, October 1996, “Employee Fraud” by W. Steve Albrecht─www.theiia.org

Summary of Learning Points

51 Module 1 – Introduction to Accounting & Financial Statements Copyright © 2015 Deloitte Development LLC. All rights reserved.

• A set of financial statements includes the following:− Balance sheet− Income statement− Statement of cash flows− Statement of stockholders' equity− Notes to the financial statements

It is important to understand (1) how to read them, (2) how they relate to each other and (3) how to pull insights from them all.

• Terms such as: materiality, conservatism, and contingency are often used to describe accounting matters.

• Financial statement fraud is an intentional act designed to misstate financial performance in order to deceive financial statement users.

Summary of Learning Points

Module 2 – Financing the Business Part I

53 Module 2 – Financing the Business Part I Copyright © 2015 Deloitte Development LLC. All rights reserved.

• Capital structure

• Cost of capital and time value of money

• Equity capital and investors

• Required rates of return

• Financing example

• Capital budgeting

• Summary of learning points

• Questions and answers

Agenda

Capital Structure

55 Module 2 – Financing the Business Part I Copyright © 2015 Deloitte Development LLC. All rights reserved.

• Funding a start-up business

• Funding growth after a business is established− Dynamites is looking to fund its international growth plans

• Opportunistically refinancing – “optimizing” the capital structure

• Funding working capital

• Funding major growth initiatives – capital expenditures or acquisitions− Dynamites needs capital to fund the potential acquisition of an international company

• Extending maturities

• Restructuring when financial performance is suffering

What are the basic reasons for raising capital?

56 Module 2 – Financing the Business Part I Copyright © 2015 Deloitte Development LLC. All rights reserved.

What are the basic reasons for raising capital?

$

FundingRequirements

Start-UpCapital

GrowthCapital

Major Initiatives

Typical Capital Structure

100% Equity

LimitedDebt

Optimal Debt and

Equity

Time

Working Capital

57 Module 2 – Financing the Business Part I Copyright © 2015 Deloitte Development LLC. All rights reserved.

Elements of capital structure

The capital structure of a company is the mix of different sources of capital issued by the company to finance its operations.• Sources of Capital:

– Debt: Bonds, bank loans– Equity: Ordinary shares (common stock), Preference shares (preferred stock)– Hybrids: warrants, convertible bonds

CapitalStructure

Operating Assets

Operating Liabilities

Debt

Preference Shares

Ordinary Shares

58 Module 2 – Financing the Business Part I Copyright © 2015 Deloitte Development LLC. All rights reserved.

Balance SheetAs of December 28, 1990 US$

ASSETS

Cash and Equivalents $503,444

Accounts Receivable 5,556

Inventory 3,000

Total Current Assets $512,000

Net Plant, Property & Equipment 239,583

Net Intangible Assets (Liquor License) 14,750

Total Assets $766,333

LIABILITIES

Accounts Payable 3,000

Interest Bearing Debt -

Total Liabilities $3,000

MEMBERS EQUITY

Members Equity 800,000

Retained Earnings (36,667)

Total Members Equity $763,333

Total Liabilities & Members Equity $766,333

CapitalStructure

Debt

Equity

Operating Assets

Operating Liabilities

Data is for illustrative purposes only.

59 Module 2 – Financing the Business Part I Copyright © 2015 Deloitte Development LLC. All rights reserved.

Knowledge Check #1

What was Dynamites' capital structure as an early stage company in December 1990?

A. 100% equity / 0% debtB. 75% equity / 25% debtC. 50% equity / 50% debtD. 5% equity / 95% debt

CapitalStructure

Operating Assets

Operating Liabilities

Debt

Preference Shares

Ordinary Shares

60 Module 2 – Financing the Business Part I Copyright © 2015 Deloitte Development LLC. All rights reserved.

Secured Bank Loans

Enterprise Value Coverage

Unsecured NoteMezzanine Unsecured

Note

Institutional B/C Tranches

2nd Lien Loans/ Notes

Secured Bank Loan

1st Lien Note

Common Equity/ Shareholder Loan Common Equity/

Shareholder Loan

Hybrid PreferredCommon Equity/ Shareholder Loan

Debt

Elements of capital structure (cont.)

Capital structures can range from simple to complex

Payment-in-Kind Loans / Notes

Cost of Capital and Time Value of Money

62 Module 2 – Financing the Business Part I Copyright © 2015 Deloitte Development LLC. All rights reserved.

Time Value of Money

• Money has a time value because money can be invested with the expectation of earning a positive rate of return− In other words, a dollar received today is worth more than a dollar received tomorrow− TIME allows you the opportunity to postpone consumption and earn INTEREST− That is because today’s dollar can be invested so that we have more than one dollar

tomorrow

Which would you prefer -- $10,000 today or$10,000 in 5 years?

$10,000Present Value = $6,210

10% interest

0 1 2 3 4 5

63 Module 2 – Financing the Business Part I Copyright © 2015 Deloitte Development LLC. All rights reserved.

Time Value of Money ExerciseKnowledge Check #2

$1,000,000Deposit now (closest answer)?

A. $1,200,000B. $200,000D. $900,000

3.5% interest

0 1 2 3 4 5 6

Dynamites wants to buy a new software system that will revolutionize the way customers order their food. The new software system will not be ready for six years but Dynamites has put its name on the list to buy the system. The new software system will cost the company $1 million dollars. Company management wants to reserve some cash and put it away in a bank account until they actually make the purchase. How much money should they put in the bank account now in order to have $1 million in six years assuming the bank account earns an interest rate of 3.5%?

64 Module 2 – Financing the Business Part I Copyright © 2015 Deloitte Development LLC. All rights reserved.

Cost of Capital

Debt versus Equity

• A company’s cost of debt is typically less than its cost of equity – debt has seniority over

equity– debt has a fixed return – the interest paid on

debt is tax-deductible

• It may appear that a company should use as much debt and as little equity as possible due to the cost difference, but this ignores the potential problems associated with debt

65 Module 2 – Financing the Business Part I Copyright © 2015 Deloitte Development LLC. All rights reserved.

Capital Strategy

Stability• Tenor• Financial/

other covenants

Costs• Interest

margin• Other fees

Financing requirements• New transactions• Existing business

requirements

Security considerations• Assets• Guarantees• Unencumbered assets

Supporting business objectives

Stability of debt

Properly structured security

Financial flexibility

Optimal Capital Structure – A Practical Approach

• Theoretical approaches to “optimal” capital structure result in a cash rich and debt light company.

• The optimal allocation of capital may be sourced from various instruments and the choice of instruments is based on the prevailing capital market conditions.

• There are a number of interactive and practical considerations that drive this decision, including the specific objectives of the company, the requirement for a stable financing structure for the business, the asset security package available for debt and financial flexibility within the company’s cash flows.

66 Module 2 – Financing the Business Part I Copyright © 2015 Deloitte Development LLC. All rights reserved.

Rank the cost of capital from lowest to highest.

A. Debt, preferred equity, common equityB. Preferred equity, common equity, debtC. Common equity, debt, preferred equity

Dynamites uses primarily equity capital to fund the business. What are some reasons that they may not have used debt even though it would reduce the overall cost of capital?

Knowledge Check #3

Equity Capital and Investors

68 Module 2 – Financing the Business Part I Copyright © 2015 Deloitte Development LLC. All rights reserved.

• Long term capital

• Generally comes with no repayment schedule

• Dividends can be paid to equity holders

• Most “expensive” capital

Basics of Equity Capital

69 Module 2 – Financing the Business Part I Copyright © 2015 Deloitte Development LLC. All rights reserved.

• Common stock− A voting interest and ownership in an entity. Stock ownership typically does not entitle owners to

scheduled dividends and returns can be highly variable

• Preferred stock− Characterized by a “preferred returns” usually in the form of scheduled or guaranteed dividend

payments. Typically a non-controlling interest

• Partnership shares− Structure in which multiple partners, or general partners together control the business.

Partnerships are not taxed at the entity level and profits are passed to the partners and taxed at the individual level

• Limited partnerships shares− Structure in which a group of partners, one or more of which are considered “general partners,”

control the business, while the rest are passive partners or investors.

• Limited liability companies member interests− A hybrid structure that blends the characteristics of partnerships and corporations

Types of Equity Capital

Source: investopedia.com

70 Module 2 – Financing the Business Part I Copyright © 2015 Deloitte Development LLC. All rights reserved.

Seed/Start Up: • Typically $200,00 to $1 million• Provided by friends & families, nonprofit venture development groups, and grants • Crowdsourcing: Online matching of investors on a micro loan (equity) basis• Alpha and Beta stage products – early testing phase

Early Stage:• $1-5 million• Angel investors, regional venture capital firms, high net worth individuals• Beta stage product or early adoption period

Growth Stage: • $5 million+• Variety of sources including venture capital, strategic investors, debt capital and hybrids• Scaling products and services up to full capacity• Venture capital investors may start to think about how to exit down the road and look for ways to pull

out capital

Companies have different capital circumstances at each stage of growth and may approach different capital providers at each stage of the process. Each stage has very different risk profiles and each investor pool has different tolerances for those risks.

Capital Sources & Stage of Company

71 Module 2 – Financing the Business Part I Copyright © 2015 Deloitte Development LLC. All rights reserved.

If Dynamites were to raise $30 million of equity capital during the middle stage of growth, from whom would it most likely receive interest in investing?

A. Angel investors

B. Venture Funds

C. Private Equity

D. Public equity market

Knowledge Check #4

Required Rates of Return

73 Module 2 – Financing the Business Part I Copyright © 2015 Deloitte Development LLC. All rights reserved.

Required Rates of Return

$

Time

Seed / Start Up

IPO Stage

Stage

Expected Rate of Return 1

Growth: 1st Stage

Growth: 2nd Stage

Growth: 3rd-4th Stage

Mature Stage

50-70% 25-35%40-60% 30-45% 7-20%35-50%

InvestorTypes

Owner, Friends & Family

Funds, Institutions

Angels, Venture Capital

Private Equity, Strategic

Funds, insurance, pensions

1) See Appendix A for more detailed information

Financing Example

75 Module 2 – Financing the Business Part I Copyright © 2015 Deloitte Development LLC. All rights reserved.

Sample Capitalization Table

1. The Johnson brothers each invested $200,000 of personal savings in 1990, which gave them each 25 percent ownership of Dynamites

2. At the same time, friends and family collectively provided $400,000 of additional capital to help start the business. The investment provided friends and family with a 50 percent ownership stake in Dynamites.

A capitalization table (cap table) details the ownership of the company

1

2

Stage 1 – Initial Investments

Common Stock # of Shares % Ownership $ Investment Share Price

Andrew Johnson 2,000,000 25% $200,000 $0.10

Bob Johnson 2,000,000 25% $200,000 $0.10

Friends & Family 4,000,000 50% $400,000 $0.10

Total Common Stock 8,000,000 100% $800,000

1

Data is for illustrative purposes only.

76 Module 2 – Financing the Business Part I Copyright © 2015 Deloitte Development LLC. All rights reserved.

Balance SheetAs of December 28, 1990 US$

ASSETS

Cash and Equivalents $503,444

Accounts Receivable 5,556

Inventory 3,000

Total Current Assets $512,000

Net Plant, Property & Equipment 239,583

Net Intangible Assets (Liquor License) 14,750

Total Assets $766,333

LIABILITIES

Accounts Payable 3,000

Interest Bearing Debt -

Total Liabilities $3,000

MEMBERS EQUITY

Members Equity 800,000

Retained Earnings (36,667)

Total Members Equity $763,333

Total Liabilities & Members Equity $766,333

As of December 28, 1998 US$

ASSETS

Cash and Equivalents $3,297,671

Accounts Receivable 36,390

Inventory 19,651

Total Current Assets $3,353,712

Net Plant, Property & Equipment 1,566,048

Net Intangible Assets (Liquor License) 99,891

Total Assets $5,019,651

LIABILITIES

Accounts Payable 19,651

Interest Bearing Debt -

Total Liabilities $19,651

SHAREHOLDERS EQUITY

Shareholders Equity 2,800,000

Retained Earnings 2,200,000

Total Shareholders Equity $5,000,000

Total Liabilities & Shareholders Equity $5,019,651

Data is for illustrative purposes only.

77 Module 2 – Financing the Business Part I Copyright © 2015 Deloitte Development LLC. All rights reserved.

• Based on market research as well as a few preliminary, non-binding offers to buy Dynamites, the Johnson brothers believed the value of Dynamites was approximately $3,000,000• This valuation implies a $0.38 share price ($3,000,000 value / 8,000,000 shares)

• In order to expand the business regionally, the Johnson brothers estimated that they need an additional $2,000,000 of capital• Two separate venture capital firms agreed to provide Dynamites with $1,000,000 each at a price of

$0.38 per share

Sample Capitalization Table (cont.)

Stage 1 – Initial Investments

Common Stock

Original # of Shares

Original % Ownership

Original Investment

AndrewJohnson 2,000,000 25% $200,000

Bob Johnson 2,000,000 25% $200,000

Friends &Family 4,000,000 50% $400,000

VC Firm 1 N/A N/A N/A

VC Firm 2 N/A N/A N/A

Total 8,000,000 100% $800,000

Stage 2 – Expansion Stage

New # of Shares

New % Ownership

New / Current Value

2,000,000 15% $750,000

2,000,000 15% $750,000

4,000,000 30% $1,500,000

2,666,667 20% $1,000,000

2,666,667 20% $1,000,000

13,333,333 100% $5,000,000

Difference

Inc / (Dec) in Value

$550,000

$550,000

$1,100,000

$0

$0

$4,200,000

Data is for illustrative purposes only.

Capital Budgeting

79 Module 2 – Financing the Business Part I Copyright © 2015 Deloitte Development LLC. All rights reserved.

Capital Budgeting Overview

Capital budgeting is often the most important functions financial managers perform

What is capital budgeting?

• Analysis of potential capital projects to undertake• Long-term decisions involving large expenditures• Projects selected are expected to produce a cash inflow over a period of time

Steps in making a capital budgeting decision:

• Estimate cash flows (inflows & outflows)• Assess risk of cash flows• Determine appropriate cost of capital or discount rate for project• Evaluate cash flows via Net Present Value, Internal Rate of Return, Payback Period or several other methods • Make Accept/Reject Decision• Payments to stakeholders (i.e. dividends, debt payments)

Sample capital budgeting categories include:

• Upgrade or replace to continue profitable operations• Upgrade or replace to reduce costs• Expansion of existing products or markets• Expansion into new products/markets• Research and Development (R&D)• Safety and/or environmental projects• Mergers & Acquisitions

80 Module 2 – Financing the Business Part I Copyright © 2015 Deloitte Development LLC. All rights reserved.

Capital Planning Framework

Capital budgeting and planning is the process by which a firm sets capital allocation targets and builds towards an “optimized” portfolio of projects. This is achieved by: Establishing an iterative capital budgeting

process that allocates funding down to the direct ownership level

Developing an effective project prioritization methodology that quantities value and risk considerations

Implementing a capital management governance structure with clear roles and responsibilities

Capital ExpendituresBalance Sheet& Cash FlowWorking Capital

Dividend Policy

ShareRepurchase

Secured

Unsecured

Equity

The Business

The Stakeholders

The Market Raise

Minimize cost of capital

DeployMaximize

value creation

DistributeSignal

to the market

Cash Mobility

DeployMaximize

value creation

Executable Strategies with Measureable Results

Debt Repayment

Capital Budgeting – The Bigger Picture

81 Module 2 – Financing the Business Part I Copyright © 2015 Deloitte Development LLC. All rights reserved.

Allocation of Funds to Capital Projects

Capital can be invested to create shareholder value in several different ways.

Options for Investing Capital

Capital Investment Projects and Maintaining Capital

Assets

Merger and Acquisition Transactions

Investment in Securities or Minority Investments in

Other Companies

Investment in information technology systems

Investment in production equipment and machinery

Building or purchasing of new facilities

Maintenance of plant, property and equipment such as machinery and buildings

The incremental discretionary expenditures required to execute capital projects

R&D investments

Purchase of another company

Merger with a company that requires capital outlay

Purchase of investment securities

Purchase of a minority stake in another company

Opt

ion

Illus

trativ

e Ex

ampl

es

82 Module 2 – Financing the Business Part I Copyright © 2015 Deloitte Development LLC. All rights reserved.

Example – Payback Period

Dynamites wants to invest in a new clean-energy fryer. Management is deciding between a $1,000,000 fryer and a $1,400,000 fryer, each with different cash flow expectations. If the decision were based on the payback period alone, which project should the Company undertake?

What is the payback period for each Project?

Weakness of this approach: Time value of money is ignored as well as the cash flows that occur after the payback period

Year Project A Project B

0 -$1,000,000 -$1,400,000

1 100,000 600,000

2 500,000 600,000

3 800,000 600,000

2.5 years 2.25 years

83 Module 2 – Financing the Business Part I Copyright © 2015 Deloitte Development LLC. All rights reserved.

Example – Net Present ValueDynamites’ Management also evaluates each major project on an expected Net Present Value (NPV) method. The Net Present Value considers the time value of money and discounts the expected future cash inflows, net of the outflows, of the project to today’s value at an assumed interest rate.

Project A includes a new fryer that enhances the range of flavor possibilities. Project B is a new technology that reduces amount of oil needed which reduces operating costs.

While Project B has a faster payback period (2.25 years) than Project A (2.5 years), the NPV (assuming a 10% discount rate) of Project A is higher than Project B, which suggests that Project A would be the preferable project if only one project could be pursued.

Project A

Year 0 Year 1 Year 2 Year 3

Cash Flow (1,000,000) 100,000 500,000 800,000

NPV Year 0 (1,000,000)

NPV Year 1 90,909

NPV Year 2 413,223

NPV Year 3 601,053

Total NPV 105,184

Project B

Year 0 Year 1 Year 2 Year 3

Cash Flow (1,400,000) 600,000 600,000 600,000

NPV Year 0 (1,400,000)

NPV Year 1 545,455

NPV Year 2 495,868

NPV Year 3 450,789

Total NPV 92,111Data is for illustrative purposes only.

Summary of Learning Points

85 Module 2 – Financing the Business Part I Copyright © 2015 Deloitte Development LLC. All rights reserved.

• Capital Structure− The capital structure of a company is the mix of different securities issued by the company to finance its operations

• Cost of Capital and Time Value of Money− A dollar received today is worth more than a dollar received tomorrow− The FUTURE cash flows are discounted at the cost of capital to arrive at their PRESENT VALUE − The risk inherent in the future cash flows is reflected in the discount rate− A company’s cost of debt is always less than its cost of equity

• Equity Capital and Investors− The different types of equity capital are:

◦ Common equity, preferred equity, limited and general partnership shares− There are many different sources of equity capital that differ based on how developed the company is and the need for

the capital.

• Required Rates of Return− Companies have different capital circumstances at each stage of growth and may approach different capital providers

at each stage of the process. − Each stage has very different risk profiles and each investor pool has different tolerances for those risks

• Capital Budgeting − Capital budgeting and planning is the process by which a company sets capital allocation targets and builds towards

an “optimized” portfolio of projects− Capital can be invested to create shareholder value in several different ways

Summary of Learning Points

Module 3 – Financing the Business Part II

87 Module 3 – Financing the Business Part II Copyright © 2015 Deloitte Development LLC. All rights reserved.

Agenda

• Overview of debt capital raising considerations

• Types of debt capital investors

• Types of debt capital investments and credit enhancements

• Examples of hybrid capital

• Ways to source capital and typical debt raise process overview

• Credit documentation overview

• Credit metrics overview

• Summary of learning points

• Questions and answers

Ways to Source Capital and the Capital Raising Process

89 Module 3 – Financing the Business Part II Copyright © 2015 Deloitte Development LLC. All rights reserved.

Capital Sources

Directly from Debt Providers− Traditional Banks

− Alternative Debt Capital Providers

− Founder’s Contributions

− Friends and Family

− Venture Capital

− Angel Investors

Indirectly through Arrangers of Debt and Equity Capital

– Investment Bankers

– Deal Brokers

– Placement Firms

Directly from Equity Providers– Founder’s Contributions

– Friends and Family

– Venture Capital

– Angel Investors

– Small Business Private Equity Investors

– Private Equity Investors

– Public Equity

90 Module 3 – Financing the Business Part II Copyright © 2015 Deloitte Development LLC. All rights reserved.

Detailed review of historical financial results, projections and existing capital structure

Coordinate multiple levels of funding

Understand client strategic objectives and conduct an “optimal” capital structure review

Review terms and conditions to ensure compliance with market standards

Set out and discuss potential funding sources

Present opportunity to a selected group of lenders/investors

Assist the Company in the creation and presentation of management meetings with potential lenders

Provide indicative views on pricing, structuring and covenant packages

Review legal agreements produced by the company’s advisors

Identify opportunity2–4 weeks

Lender/investor negotiation6–8 weeks

Financing execution3–4 weeks

Inter-creditor issues resolved

Timely closing

Typical Debt Raise Process Through an Investment Bank

Agree on a list of potential lenders/ investors with the company

Gather due diligence information

Work with management to create a Confidential Information Memorandum and draft of term sheet

Advise management on selection of favored terms

Manage the negotiation process with the lenders/investors

Assist the company with due diligence requests from the lenders/investors

Create a competitive process and generate proposals from lenders

Types of Debt Capital Investors

92 Module 3 – Financing the Business Part II Copyright © 2015 Deloitte Development LLC. All rights reserved.

Debt Capital Providers

• Traditional Banks

– Large National Banks (LC)

– Foreign Banks (LC)

– Regional Banks (MM, LC)

– Community Banks (ES, MM)

LC = Large Cap

MM = Middle Market

ES = Early Stage

• Alternative Debt Capital Providers

– Senior Debt Funds (MM, LC)

– Opportunity Funds (MM, LC)

– Mezzanine Funds (MM)

– Collateralized Loan Obligation Funds (MM, LC)

– SBIC Funds (ES, MM)

– Business Development Companies (ES, MM)

– Hedge Funds (MM, LC)

– Venture Debt Funds (ES)

– Distressed Debt Funds (ES, MM, LC)

– High Net Worth Individuals (ES)

Types of Debt Capital

94 Module 3 – Financing the Business Part II Copyright © 2015 Deloitte Development LLC. All rights reserved.

What are the basic reasons for raising Debt Capital?

Extend Maturities

Opportunistically Refinance

Funding Growth –Organic and Acquisitions

RestructuringFunding Working Capital

Why Raise Debt Capital?

95 Module 3 – Financing the Business Part II Copyright © 2015 Deloitte Development LLC. All rights reserved.

• Secured Debt v. Unsecured Debt

• Senior Debt v. Junior Debt

Basic Ways to Describe Debt Capital

96 Module 3 – Financing the Business Part II Copyright © 2015 Deloitte Development LLC. All rights reserved.

Secured Bank Loans

Enterprise Value Coverage

Unsecured NoteMezzanine Unsecured

Note

Institutional B/C Tranches

2nd Lien Loans/ Notes

Secured Bank Loan

1st Lien Note

Common Equity/ Shareholder Loan Common Equity/

Shareholder Loan

Hybrid PreferredCommon Equity/ Shareholder Loan

Debt

Elements of Capital Structure

Capital structures can range from simple to complex

Payment-in-Kind Loans / Notes

97 Module 3 – Financing the Business Part II Copyright © 2015 Deloitte Development LLC. All rights reserved.

Types of Debt

More Collateral or Quicker Repayment = Less Risk = Less Cost

Revolver

Term Loan A (“TLA”)

Term Loan B (“TLB”)

Second Lien Loan

Mezzanine Debt

Subordinated Debt

Asset Based Loan (“ABL”)

Revolver

Revolving Credit Facility secured by the Company’s working capital assets with availability subject to a Borrowing Base (formula based, periodic (usually monthly) calculation of the maximum amount of borrowing the assets support)

Revolving Line of Credit that is usually pari passu with other senior secured debt (specifically the Term Loans) and is not subject to a Borrowing Base

Senior secured Term Loan, often referred to as “Bank Debt”, as banks typically invest in this tranche; banks often invest in what is referred to as the “Pro Rata Facility” which is a strip of the Revolver and the Term Loan A

Senior secured Term Loan, often referred to as the “Institutional” tranche, as institutional investors typically invest in the TLB, which most often has lower scheduled amortization than the Term Loan A (often 1% per year)

Senior secured term debt that is subordinated in right to the collateral to the first lien debt (Revolver, TLA, and TLB), but typically not subordinated in right to ongoing cash interest payment

Subordinated, usually unsecured debt investment typically seen in middle market (where middle market is defined as companies with annual revenues ranging from $50 million to $1 billion) transactions and often has equity like characteristics (equity co-invest, warrants, options)

We will touch on various subordinated debt investments including mezzanine, subordinated, high-yield debt, holdco, and seller notes

Unitranche LoanA type of facility that combines senior and subordinated debt into one debt instrument where a single blended interest rate is paid to a single lender. Unitranche loans are designed to simplify debt structure and accelerate the closing process. Eliminates intercreditor issues

Commercial PaperAn unsecured, short-term debt instrument issued by a corporation, typically for the financing of accounts receivable, inventories and meeting short-term liabilities. Maturities on commercial paper rarely range longer than 270 days

L + 350

L + 350

L + 400

L + 400

L + 500

L + 900

L + 650

12% Cash + 2% PIK + 3%

Warrants

10%-20%

Indicative Pricing

98 Module 3 – Financing the Business Part II Copyright © 2015 Deloitte Development LLC. All rights reserved.

Products Which Provide Credit EnhancementLetter of Credit (operational)• An issuer provides a written commitment, called a

“Letter of Credit” or “LC”, supporting the payment owed by a debtor to a separate creditor, subject to certain conditions stated in the LC. In the event that the debtor is unable to make timely or accurate payment, the creditor or “beneficiary” of the LC can present the LC to the issuer for payment, after which the issuer of the LC would be required to fund the outstanding amount.

• Letter of Credit can be a cheap way to obtain credit enhancement as fees in today’s environment can be less than 1% of the LC amount

• Letters of Credit are frequently used between companies and their vendors, as well as for international transactions where local or common law may be substantially different

• The ability to issue Letters of Credit is commonly packaged under Revolving Credit Facilities used for working capital for companies doing business overseas or that require extended payment terms to their vendors

Guarantee (of debt)• A guarantee is a type of indemnity where the

guarantor promises to repay investors should the primary issuer default on its obligations or fail to provide timely payment

• The primary purpose of a guarantee is to achieve certain terms and conditions for the borrower that would otherwise only be available to a more credit-worthy borrower

• Guarantees can provide savings for the issuer as the credit enhancement can typically provide lower interest rates for securities

• Guarantees can be provided by commercial entities, financial institutions as well as by individuals

• Guarantees can come in several forms:

• Payment

• Financial performance

• Limited

• Unlimited

Second Source of Repayment = Reduced Risk

Examples of Hybrid Capital

100 Module 3 – Financing the Business Part II Copyright © 2015 Deloitte Development LLC. All rights reserved.

• PIK Loans – Loans on which interest is paid-in-kind, or accrued, rather than paid in cash on a current basis

• Subordinated debt with warrants – Loans that contain a type of equity participation

• Convertible debt – Debt that can be converted into equity

• Participating preferred stock – Preferred Stock that participates in the growth or “upside” of the common equity

Examples of Hybrid Capital

Debt and Equity Documentation Overview

102 Module 3 – Financing the Business Part II Copyright © 2015 Deloitte Development LLC. All rights reserved.

• Credit Agreements− Typically for senior/secured/second-lien debt

• Subordinated Debt Subscription Agreements and Indentures− Typically for Subordinated Debt/High Yield Bonds/Hybrids

• Inter-creditor Agreements− An agreement between two lenders with the same borrower

• Stockholder Agreements, Membership Agreements, Stock Certificates− Typically for various equity investments

Major Types of Capital Documentation

103 Module 3 – Financing the Business Part II Copyright © 2015 Deloitte Development LLC. All rights reserved.

Events of Default • Events that will cause the Borrower to be in default of the agreement and remedies available to lenders after default

Important Sections of a Credit AgreementThe Loans • Description of the loans including: amount, interest and repayment rate

Collateral • Details the collateral pledged as security for the loans

The Guarantee • Details the terms of guarantees being provided by the borrower

Representations and Warranties

• Representations made by the Borrower prior to close

Conditions Precedent

• Conditions that should be satisfied before effectiveness of agreement

Affirmative Covenants

• Actions that the Borrower should take on a go forward basis, including financial covenants

Negative Covenants

• Actions the Borrower may not take on a go forward basis

Administrative Agent

• Detail of the roles of the Administrative Agent in management of the loan

Lender Voting Rights

• Details what % of Lenders may accept Amendments, Waivers and Consents

Credit Metrics Overview

105 Module 3 – Financing the Business Part II Copyright © 2015 Deloitte Development LLC. All rights reserved.

• Credit metrics are the principal means to measure performance and risk for a creditor over time

• Metrics provide an objective measure for both creditor and borrower to analyze and provide the basis for continued communication

• Most importantly, metric ranges help lenders determine interest rates and other features (term etc.) and monitor risk of the loan

Credit Metrics Overview

Credit Rating Agencies

• Standard & Poor’s

• Fitch Ratings

• Moody’s

Observations

• Headline metrics are somewhat consistent

• Proprietary metrics and algorithms exist for lenders and agencies

106 Module 3 – Financing the Business Part II Copyright © 2015 Deloitte Development LLC. All rights reserved.

Interest Coverage

Fixed Charge Coverage

Liquidity / Availability

Loan to Enterprise Value

Return Analyses

Leverage

Specific Metrics in Credit Analysis

Ratio of Debt to TTM EBITDA – commonly tested leverage ratios include senior leverage, total leverage, and net leverage; quick test of the level of debt on the Company; helpful in assessing financial condition and in comp analysis

Ratio of EBITDA to Cash Interest – measurement of the companies ability to meet its debt service obligations

Ratio of EBITDA less CAPEX to Fixed Charges (interest, taxes, and scheduled debt amortization) – measurement of the Company’s ability to produce sufficient cash flow to cover its fixed obligations including debt service

Liquidity is availability under the Revolver plus the cash on the balance sheet –measurement of ability to continue to support operations and service debt in the event cash flow from operations is insufficient in a given period

Ratio of debt to enterprise value of the Company – provides an indication of how much deterioration in enterprise value the Company could withstand before the debt becomes impaired

Current Yield, Yield to Maturity, Yield to Call, and Effective Spread – various return analyses to assess whether or not an investment addresses investment criteria and/or the relative attractiveness of one investment vs. another

Credit metrics can be defined in many ways, the definitions on this page are examples.

107 Module 3 – Financing the Business Part II Copyright © 2015 Deloitte Development LLC. All rights reserved.

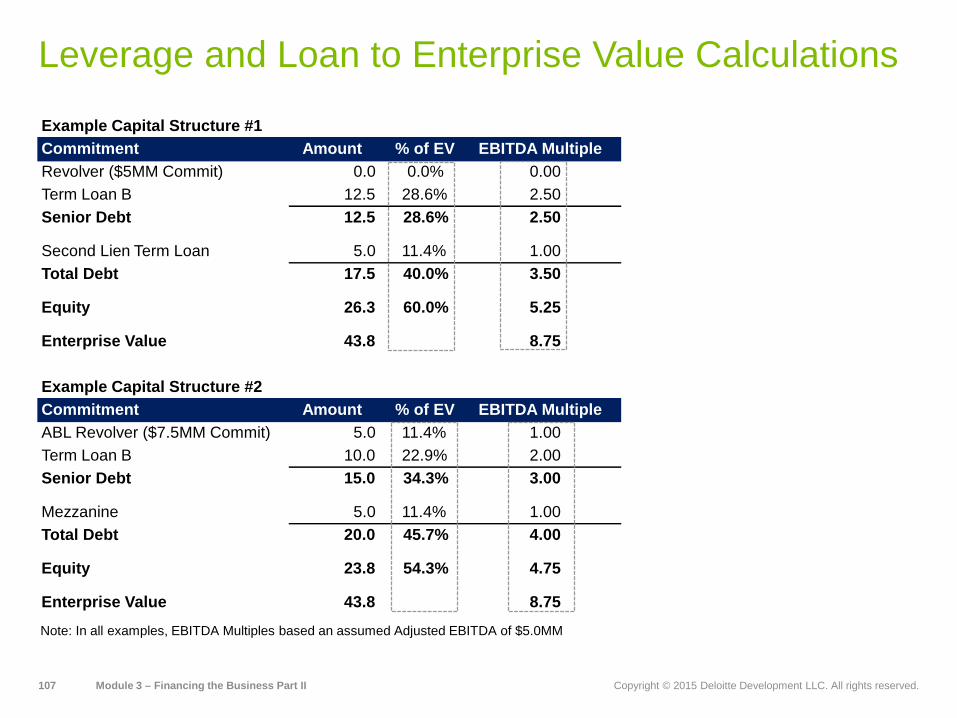

Leverage and Loan to Enterprise Value Calculations

Note: In all examples, EBITDA Multiples based an assumed Adjusted EBITDA of $5.0MM

Example Capital Structure #1Commitment Amount % of EV EBITDA MultipleRevolver ($5MM Commit) 0.0 0.0% 0.00Term Loan B 12.5 28.6% 2.50Senior Debt 12.5 28.6% 2.50

Second Lien Term Loan 5.0 11.4% 1.00Total Debt 17.5 40.0% 3.50

Equity 26.3 60.0% 5.25

Enterprise Value 43.8 8.75

Example Capital Structure #2Commitment Amount % of EV EBITDA MultipleABL Revolver ($7.5MM Commit) 5.0 11.4% 1.00Term Loan B 10.0 22.9% 2.00Senior Debt 15.0 34.3% 3.00

Mezzanine 5.0 11.4% 1.00Total Debt 20.0 45.7% 4.00

Equity 23.8 54.3% 4.75

Enterprise Value 43.8 8.75

Summary of Learning Points

109 Module 3 – Financing the Business Part II Copyright © 2015 Deloitte Development LLC. All rights reserved.

Summary of Learning Points

• Debt is a critical part of capital structures and is raised for a wide variety of reasons

• Debt capital comes in many forms and from many different types of providers

• Appropriate debt capital for a company is often determined by the company’s stage of development

• Primary debt considerations include: pricing, term, security, repayment terms, availability, and financial covenants

• Financial covenants are common – be familiar with the calculation of leverage, interest coverage, fixed charge coverage

• Debt documents, such as credit agreements, are written contracts containing definitive terms between lenders and borrowers

• Hybrid capital, which has certain advantages, can sometimes replace debt capital

• Companies can hire advisors to help them raise debt or equity capital, usually a 4-6 month process

Appendix – Module 1

111 Appendix – Module I Copyright © 2015 Deloitte Development LLC. All rights reserved.

• Established accounting standards promulgated by the London-based International Accounting Standards Board (IASB)

• IFRS is a broad, globally accepted set of accounting standards:− Principles-based approach with a greater emphasis on interpretation and

application of principles− Less extensive body of literature than U.S. GAAP, with limited industry-specific

guidance and less detailed application guidance

• IFRS will require more exercise of judgment, supported by contemporaneous analysis and documentation

• No definitive plan or timeline of mandating IFRS in U.S.

IFRS

112 Appendix – Module I Copyright © 2015 Deloitte Development LLC. All rights reserved.

• Corporate attorneys will need to work with management to determine strong documentation of policies, procedures, and protocols to reduce the risk of litigation based upon the application of management’s judgments and estimates

• M&A attorneys involved in the drafting of contracts will need to consider the impact of IFRS on earn-outs, credit agreements, purchase agreements, sales contracts, and bonus plans

• White collar defense and corporate investigation attorneys may see a shift in cases to IFRS based regulatory proceedings

• Malpractice attorneys will need to prepare themselves for the way audits are performed under IFRS

How will IFRS impact attorneys

Appendix – Module 2

114 Module 3 – Financing the Business Part II Copyright © 2015 Deloitte Development LLC. All rights reserved.

Commercial Paper Overview

Pricing

Security / Collateral

Potential Borrowers

Cons

Variable pricing linked to LIBOR (e.g. one-month LIBOR plus 3.50%) with an unused fee (e.g. 50 bps on unused amounts); with typically a very small spread based on the short term nature of Commercial Paper as well as based on the typically high credit worthiness of the issuer

Commercial paper is not usually backed by collateral, so only firms with high-quality debt ratings will easily find buyers without having to offer a substantial discount (higher cost) for the debt issue. The proceeds from this type of financing can only be used on current assets such as accounts receivable and inventories and are not allowed to be used on fixed assets, such as a new plant

Companies with significant working capital assets inventory and accounts receivable and established access to capital markets may find commercial paper to be a useful funding source for its working capital circumstances

Short term nature of commercial paper requires frequent refinancing and is only available to companies having already demonstrated access to public debt markets

Pros Typically low cost, and does not need to be registered with the Securities and Exchange Commission (SEC) as long as it matures before nine months 270 days

Tenor 30 – 270 days

Repayment Due at maturity

The description of debt security terms above is an example. Actual debt security terms take many forms.

115 Module 3 – Financing the Business Part II Copyright © 2015 Deloitte Development LLC. All rights reserved.

ABL Overview

Pricing

Security / Collateral

Potential Borrowers

Cons

Variable pricing linked to LIBOR (e.g. one-month LIBOR plus 3.50%) with an unused fee (e.g. 50 bps on unused amounts); the spread and the unused fee will depend on the quality of the Borrower and the return requirements of the Lender (if it is not a “bankable” deal, a higher spread will need to be paid to an alternative investor)

Secured by the working capital assets of the Company; in some cases, lenders will require a lien on the assets of the business; in many cases, there will be a bifurcated collateral package where the ABL Lender will have a first priority secured interest in the working capital assets and a second priority secured interest in the other assets of the business and the Term Loan Lender will have a first priority secured interest in the other assets and a second priority secured interest in the working capital assets

Companies with significant working capital assets (inventory and accounts receivable) and seasonal companies (e.g. consumer products companies, retailers, auto manufacturers) with seasonal builds in working capital

Significant reporting and collateral monitoring requirements

Pros Low cost financing in situations where asset quality is strong and cash flow may be inconsistent

Tenor 3 – 5 years

Repayment Due at maturity

The description of debt security terms above is an example. Actual debt security terms take many forms.

116 Module 3 – Financing the Business Part II Copyright © 2015 Deloitte Development LLC. All rights reserved.

Pricing

Security / Collateral

Potential Borrowers

Cons

Tenor

Revolver

3 – 5 years

Variable pricing linked to LIBOR (e.g. three-month LIBOR plus 4.0%) with an unused fee (e.g. 50 bps on unused amounts); the spread and the unused fee will depend on the quality of the Borrower and will often be tied to a leverage based grid; LIBOR floors are common

First priority secured interest in the assets of the business, generally on a pari passu basis with other senior secured debt (Term Loans); in many cases, the Revolver and Term Loans will be under one Credit Agreement

Companies with strong cash flow that may lack significant “lendable” working capital assets; used for general corporate purposes

Availability subject to meeting financial covenants of loan facility and maturity is often prior to maturity of Term Loans; unused fees

Pros Available low cost liquidity for working capital and/or strategic objectives under a cash flow facility structure

Repayment Due at maturity

The description of debt security terms above is an example. Actual debt security terms take many forms.

117 Module 3 – Financing the Business Part II Copyright © 2015 Deloitte Development LLC. All rights reserved.

Pricing

Security / Collateral

Potential Borrowers

Cons

Tenor

Term Loan A

5 – 7 years

Variable pricing linked to LIBOR (e.g. three-month LIBOR plus 4.0%); the spread will depend on the quality of the Borrower and will sometimes be tied to a leverage based grid; LIBOR floors are common

First priority secured interest in the assets of the business, generally on a pari passu basis with other senior secured debt (Revolver and/or other Term Loans); in many cases, the Revolver and the Term Loan Facilities will be under one Credit Agreement

Companies with strong cash flow capable of servicing meaningful amortization schedules

Significant scheduled amortization strains cash flow

Pros Low cost; smaller, more “club”-like lender groups

RepaymentMeaningful scheduled amortization that often increases each year (e.g. amortization in years 1 through 5 of 5%, 5%, 15%, 25%, 50%, respectively); cash flow sweeps also possible

The description of debt security terms above is an example. Actual debt security terms take many forms.

118 Module 3 – Financing the Business Part II Copyright © 2015 Deloitte Development LLC. All rights reserved.

Pricing

Security / Collateral

Potential Borrowers

Cons

Tenor

Term Loan B

5 – 7 years

Variable pricing linked to LIBOR (e.g. three-month LIBOR plus 5.0%); the spread will depend on the quality of the Borrower and will sometimes be tied to a leverage based grid; LIBOR floors are common

First priority secured interest in the assets of the business, generally on a pari passu basis with other senior secured debt (Revolver and/or other Term Loans); in many cases, the Revolver and the Term Loan Facilities will be under one Credit Agreement

Companies with strong cash flow

Short tenor; often syndicated to large granular group of institutional lenders that can be difficult to deal with when seeking an accommodation

Pros Low cost; longer term

RepaymentRelatively low scheduled amortization compared to a Term Loan A (1% per year is the norm in the broadly syndicated institutional term loan market); cash flow sweeps are common on TLBs

The description of debt security terms above is an example. Actual debt security terms take many forms.

119 Module 3 – Financing the Business Part II Copyright © 2015 Deloitte Development LLC. All rights reserved.

Pricing

Security / Collateral

Potential Borrowers

Cons

Tenor

Second Lien Term Loan

5 – 7 years

Variable pricing linked to LIBOR (e.g. three-month LIBOR plus 9.0%); the spread will depend on the quality of the Borrower and will sometimes be tied to a leverage based grid; LIBOR floors are common

Second priority secured interest in assets of the business, effectively a third priority interest in situations where an ABL Facility and a Term Loan Facility have first and second priority secured interests in the collateral; a Second Lien Loan is not subordinated to the interest payment of the First Lien Loans (payments cannot typically be “blocked” by senior creditors)

Companies with strong cash flow

Often creates difficult inter-creditor issues due to multiple liens on assets

Pros Lower cost than Mezzanine or Subordinated Debt

Repayment Due at maturity

The description of debt security terms above is an example. Actual debt security terms take many forms.

120 Module 3 – Financing the Business Part II Copyright © 2015 Deloitte Development LLC. All rights reserved.

Pricing

Security / Collateral

Potential Borrowers

Cons

Tenor

Unitranche Loan

5 – 7 years

Variable pricing linked to LIBOR (e.g. three-month LIBOR plus 6.5%); the spread will depend on the quality of the Borrower and typically be a blend of senior and second lien pricing depending on the capital structure and balance sheet assets

First priority secured interest in the assets of the business, generally on a pari passu basis with other senior secured debt (Revolver and/or other Term Loans); in many cases, the Revolver and the Term Loan Facilities will be under one Credit Agreement

Companies with balance sheet assets and strong cash flow that may be looking to only deal with a single lender group and/or simplify their capital structure

Can have limited flexibility should problems arise. May not necessarily result in the “best” pricing terms given the blended nature of the interest rate

Pros Simplified capital structure with a single facility and a single lender. Usually results in a streamlined due diligence and closing process

Repayment Due at maturity

The description of debt security terms above is an example. Actual debt security terms take many forms.

121 Module 3 – Financing the Business Part II Copyright © 2015 Deloitte Development LLC. All rights reserved.

Pricing

Security / Collateral

Potential Borrowers

Cons

Tenor

Mezzanine Debt

5 – 7 years

Fixed rate pricing which usually includes a portion paid-in-kind (“PIK”) and often includes an equity interest (e.g. 12% cash pay plus 2% PIK plus 3% warrants);

Usually unsecured, but subordinated to first lien debt

Middle market companies and LBOs (Leveraged Buy Out)

Higher cost

Pros Available long-term unsecured financing for middle market companies; allows for retention of equity; used often in private equity LBOs

Repayment Due at maturity

The description of debt security terms above is an example. Actual debt security terms take many forms.

122 Module 3 – Financing the Business Part II Copyright © 2015 Deloitte Development LLC. All rights reserved.

Subordinated Debt

Pricing

Security / Collateral

Potential Borrowers

Cons

Tenor 5 – 30 years (depends on Company, situation, and type of Subordinated Debt)