the korean economy: resilience amid turbulence15.1% asean 10.4% japan 7.1% others 19.8% central...

TRANSCRIPT

November 17, November 17, 20082008

The Korean Economy: Resilience amid TurbulenceThe Korean Economy: Resilience amid Turbulence

Dr. Il Dr. Il SaKongSaKong

Special Economic Adviser to the PresidentSpecial Economic Advisor to the President

Republic of KoreaRepublic of Korea

November 17, 200November 17, 2008

2

1. Recent Macroeconomic Developments

2. Korea’s External Position & Financial Strengths

3. Government’s Policy Responses

4. Korea : Economic Outlook for 2009 envisioned by Korean Government

3

GDP Growth Trend : Gradual Slowdown

GDP Growth Trend (%)

12.1

10.8

1.6

11.0

4.4

4.9(1.7)

Q2 Q3Q2Q1Q4Q3Q1

8.98.69.016.96.911.411.911.37.3Import

9.712.511.817.09.311.012.111.88.5Export

-0.9-1.2-1.1-0.4-0.13.71.20.10.2Construction Investment

4.90.71.46.52.310.97.67.85.7Facility Investment

1.12.33.44.64.84.14.54.53.6Private Consumption

3.9(0.6)

4.8(0.8)

5.8(0.8)

5.71.6

5.1(1.5)

4.0(1.0)

5.05.14.2GDP Growth(qoq, %)

2008200720062005

44

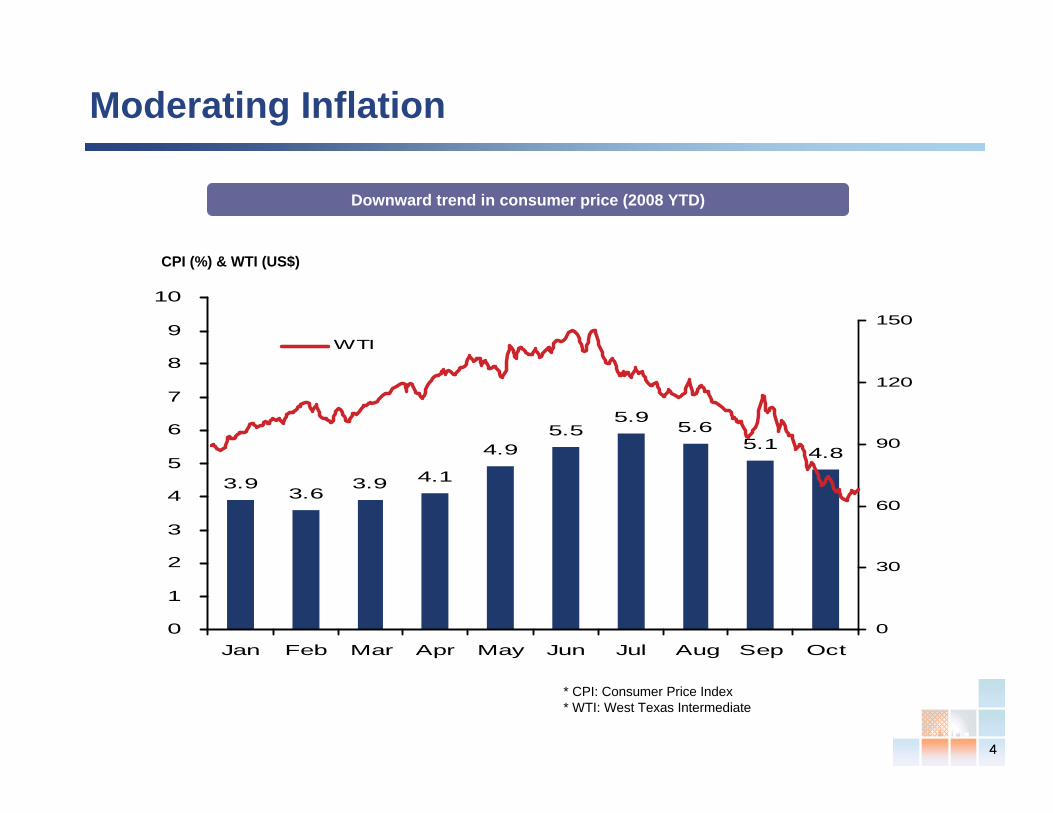

Moderating Inflation

CPI (%) & WTI (US$)

Downward trend in consumer price (2008 YTD)

3.93.6

3.9 4.1

4.95.5

5.95.6

5.1 4.8

0

1

2

3

4

5

6

7

8

9

10

Jan Feb Mar Apr May Jun Jul Aug Sep Oct0

30

60

90

120

150

WTI

* CPI: Consumer Price Index* WTI: West Texas Intermediate

5

Job Market Situation

Unemployment Rate Job Creation Trend

299282

296

210

173

141

295 289264 279

0

50

100

150

200

250

300

350

2005 2006 2007 Q107 Q207 Q307 Q407 Q108 Q208 Q308

3.1%

3.2%

3.4%

3.7%

3.1%3.1%

3.5%

3.2%

3.6%

3.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

2005 2006 2007 Q107 Q207 Q307 Q407 Q108 Q208 Q308

Unemployment Rate (%) New Jobs Created (YoY, ‘000)

6

-0.13

5.0(e)

-5.20

Q1 08 Q2 08 Q3 08 Q4 08 (e,KDI)

2009 (e,KDI)

Trade and Current Account Balance

2008 Current account and Trade balance (US$ bn)

Current account surplus is expected in 4Q08

Robust export growth Diversified export products

Diversified export markets

Source: Bank of Korea

China22.1%

North America13.3%

EU15.1%

ASEAN10.4%

Japan 7.1%

Others19.8%

Central &South America

6.9%

Middle East5.3%

Source: KITA (as of 2007)

Semiconductor11%

Chemicals10%

Automobile10%

Mobile communication

8%

Machinery8%

Others26%

Textile4%

Shipbuilding7%

Home appliance5% Steel 6%

Computer 5%

Exports (US$ bn, YoY Growth, %)

23.0%

Export (USD billion)

36721.3%

37114.1%325

14.4%28411.8%254

30.9%19419.8%162

8.0%0

100

200

300

400

2002 2003 2004 2005 2006 2007 Jan-Oct2008

7

1. Macroeconomic Performance

2. Korea’s External Position & Financial Strengths

3. Government’s Policy Responses

4. Korea : Economic Outlook for 2009 envisioned by Korean Government

8

Foreign Reserves, Bank & Corporate Sector’s Soundness

Asian Financial Crisis (late 1997) 1

Foreign Exchange

Banking Sector

173% 386% 368% 3

US$ 212.3bn 2Foreign Currency Reserves US$ 8.9bn

ST External Debt a / FX Reserves 717%

Current External Debt b / FX reserves 973%

Total External Debt / FX Reserves 1,957%

11.6% 30.7% 3

7.0%

6.0%Bank NPL Ratio

BIS Ratio

1 as of end of 19972 as of October 20083 as of June 2008, Basel I4 as of end of 2007

Corporate Sector404.8% 4106.5% 4

115.0%

424.6%Debt to Equity Ratio

Interest Coverage Ratio

a. Short-Term Debt: Debt with original maturity shorter than 1 year b. Current Debt: Debt with remaining maturity shorter than 1 year

Current

9

Bonds Deposits Others

Korea’s Foreign Reserves

74 96 103 121155

199 210239 262 264 258 239

212

4086

132178224270

1999 2000 2001 2002 2003 2004 2005 2006 2007 Q108 Q2 Q3 Oct

Total foreign exchange reserves

FX reserves (US$ bn)

161169

281286

556996

212

Hong KongSingapore

KoreaTaiwan

IndiaRussiaJapanChina

Largest global reserve holders (October 2008)

1 Includes Hong Kong (AA+), Slovenia (AA), Portugal (AA-), Italy (A+), Chile (A+), Czech Republic (A) and Estonia (A). Credit ratings by S&P. Source: IMF.

Median of peers1: US$ 29.2bn

FX reserves (US$ bn)

Source: Bank of Korea

Are Korea’s FX reserves liquid enough?

Deposit19.3

(9.1%)

Total reserves (US$ bn)

Bonds mostly rated AA or above

192.5(90.7%)

1,906 Others 0.5 (0.2%)

1 Primarily due to government’s provision of FX reservesto banking sector

1

10

Korea’s External Debt Total External Debt and Short-term Debt

419.8

175.7

222.3

0

50

100

150

200

250

300

350

400

450

Total Debt Current debt Short term debt

(86.1% of Reserves)

* Short-term debt: Debt with original maturity shorter than 1 year * Current debt: Debt with remaining maturity shorter than 1 year

(68.1% of Reserves)

(US$ bn)

(39% of GDP)

Hedges forshipbuilders'export andoverseasfinancialinvestment (22%)

Cash Advances forShipbuiling Contracts (12%)

Hea

Proportion of total debt without default risk

No default risk(34%)

External debt structure (US$ bn)

External debt owed by banks (US$ bn)

127.4( 61%)

83.1(39%)

Domestic banks

Foreign bank branches

1111

Soundness of Banking Sector

Moderate Loan-to-Deposit Ratio

Moderating Loan Growth Low Delinquency Ratio

4.2

2.92

1.11.6 1.8

5.04.2

Q4 07 Q1 08 Q2 08 Q3 08

SME Leding HH Lending

Loan Growth (%)

128.2%124.2%126.5%123.7% 126.8%

103.2%104.6%105.4%104.2%104.2%

2007 Jun-08 Jul-08 Aug-08 Sep-08

꺾은선형 1 Deposits including CDs

Loan-to-Deposit Ratio (%)

Delinquency Ratio (%)

Source: Financial Supervisory Services

1.0%

1.4% 1.5%

1.1%

1.5%1.5%

0.7% 0.6%0.7%0.6%0.5%0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2007 May-08 Jun-08 Jul-08 Aug-08 Sep-08

SME Lending HH Lending

Sufficient Room to Withstand Default Risks

Absorptive Capacity for the impact of default risk

─ Coverage ratio is approximately 186%

─ LTV ratio is approximately 47%

Well-diversified lending

─ Manufacturing (35.2%), Real estate (17.1%), Wholesale and Retail (14.3%), Construction (9.7%)

Stringent risk management system implemented after Asian Financial Crisis

1212

Household Debt and Real Estate Bubble?

Household Financial Debt to Financial Asset Ratio (%)

Household Debt to GDP Ratio (%)

83

67

99100

0

20

40

60

80

100

120

Korea(08 June) U.S.(07 Mar) U.K.(07 Mar) Japan(07 Mar)

45

23

3532

0

20

40

Korea (Jun 08) U.S. (Dec 07) U.K. (Dec 07) Japan (Dec 07)

Real Estate to HH Asset Ratio (%)77

4246

34

0

20

40

60

80

Korea (Jun 08)) U.S. (Dec 05) U.K. (Dec 05) Japan (Dec 05)

1313

Improving loan to value ratio Stricter regulation on mortgage than other countries

Source: Bank of Korea Financial Stability Report, April 20081 Financial Surplus = Financial Asset Increase - Financial Liability Increase.2 Financial assets and liabilities exclude trade credits and other miscellaneous non-interest-bearing financial assets and debts.

LTV ratio (%)

60%

60-70%

Direct

37.3%

Hong Kong

-

60%(Portion)

Mixed

52.4%

Germany

--40%DTI Limit

Korea U.S. Japan

Mortgage/ GDP 33.4% 72.3% 36.2%

Regulation System Direct Indirect Indirect

LTV Limit 40-60% - Indirect

47.9

49.5

52.2

47.547

44

48

52

56

2005 2006 2007 1Q08 2Q08

Household Debt and Real Estate Bubble (II)

14

Why then Some Negative Perceptions?

(a) High trade dependency (Export / Import as % of GDP, as of 2007)Korea (38.7 / 37.2), US (8.4 / 14.6), Japan (16.3 / 14.2), China (37.5 / 29.4), UK (15.9 / 22.5), Germany (41.1 / 33.0), Spore (185.5 / 163.2), HK (166.4 / 177.7)

(b) Open capital market- Foreign investors’ share in Korea’s KOSPI: 42% (2004) → 29% (Nov 2008)cp) US (11.3%, Jun 07), Taiwan (30.9%, Oct 08), France (38.2%, Sep 07),

Mexico (35.5%, Jun 08), UK (40.0%, end 06), OECD average (25%)

(1) Korea’s high openness

- The 1997-98 currency crisis and impact on investors’ psychology

(2) Psychological

factors

Two Main Reasons

Performance of KOSPI (2008 YTD)

1,124

900

1,100

1,300

1,500

1,700

1,900

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov

Clo

sing

Pric

e (K

RW

)

KOSPI

15

1. Macroeconomic Performance

2. Korea’s External Position & Financial Strengths

3. Government’s Policy Responses

4. Korea : Economic Outlook for 2009 envisioned by Korean Government

16

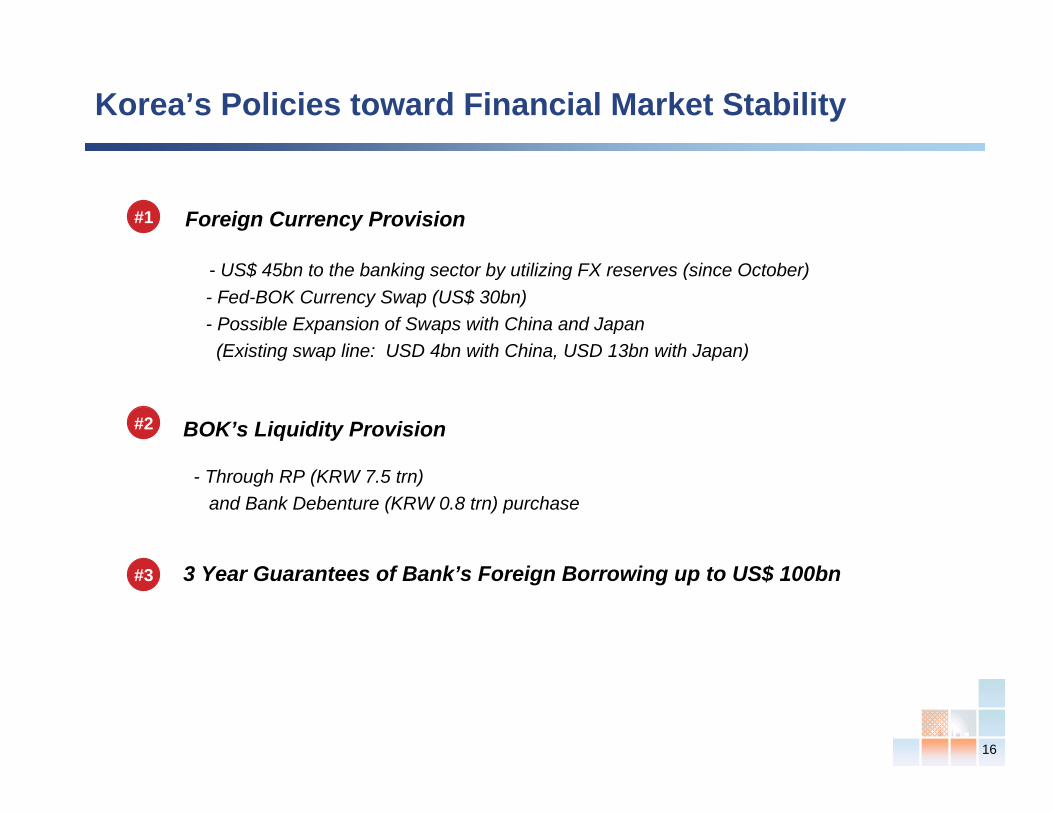

Korea’s Policies toward Financial Market Stability

Foreign Currency Provision

- US$ 45bn to the banking sector by utilizing FX reserves (since October)- Fed-BOK Currency Swap (US$ 30bn) - Possible Expansion of Swaps with China and Japan

(Existing swap line: USD 4bn with China, USD 13bn with Japan)

BOK’s Liquidity Provision

- Through RP (KRW 7.5 trn)and Bank Debenture (KRW 0.8 trn) purchase

3 Year Guarantees of Bank’s Foreign Borrowing up to US$ 100bn

#1

#2

#3

17

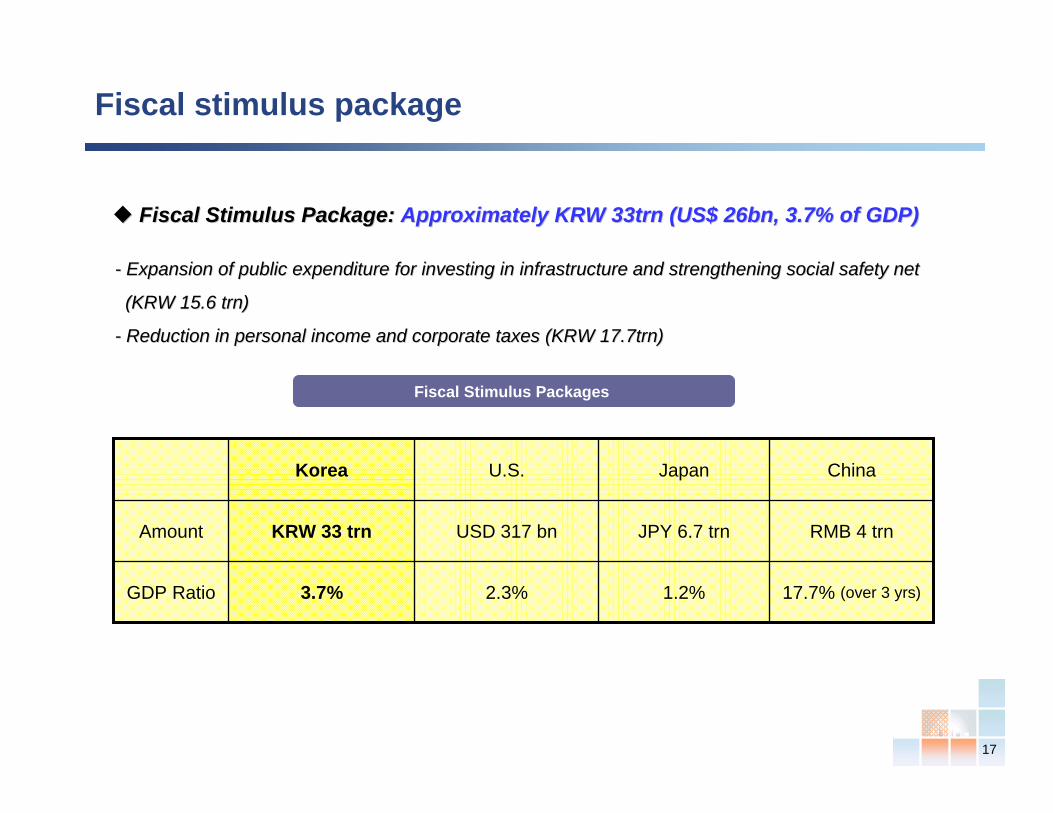

Fiscal Stimulus Package: Fiscal Stimulus Package: Approximately KRW 33trn (US$ 26bn, 3.7% of GDP)Approximately KRW 33trn (US$ 26bn, 3.7% of GDP)

-- Expansion of public expenditure for investing in infrastructureExpansion of public expenditure for investing in infrastructure and strengthening social safety net and strengthening social safety net

(KRW 15.6 (KRW 15.6 trntrn))

-- Reduction in personal income and corporate taxes (KRW 17.7trn)Reduction in personal income and corporate taxes (KRW 17.7trn)

Fiscal stimulus package

1.2%

JPY 6.7 trn

Japan

17.7% (over 3 yrs)2.3%3.7%GDP Ratio

RMB 4 trnUSD 317 bnKRW 33 trnAmount

ChinaU.S.Korea

Fiscal Stimulus Packages

1818

Korea’s Strong Fiscal Strength enabling Further Stimulus

Relatively Low Debt LevelTrend of Korea’s fiscal balance

1.2%

3.3%

1.0% 0.7% 0.4% 0.4%

3.8%

2.1%

1.1%

0%

1%

2%

3%

4%

2000 2001 2002 2003 2004 2005 2006 2007 2Q08

Source: Ministry of Strategy and Finance

Comparison with other countries

-0.4-1.3

-0.5 -0.3

-2.5

-0.7

-2.9

-0.4

-2

2.1

(4)

(2)

0

2

4

Korea (A

)AA m

edian

A med

ian

Hong K

ong (AA+)

Slovenia

(AA)

Portugal

(AA-)

Taiwan

(AA-)

Italy

(A+)

China (A+)

Iceland

(A)

Source: S&P Sovereign Risk Indicator, July 2008

180.0%

33.0%

62.0%

72.0%66.0%

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

200%

Korea US Japan Germany France

OECD Average: 77%

Fiscal surplus (% of GDP)

Consolidated fiscal balance (% of GDP) Government debt to GDP (%)

Source: OECD and IMF

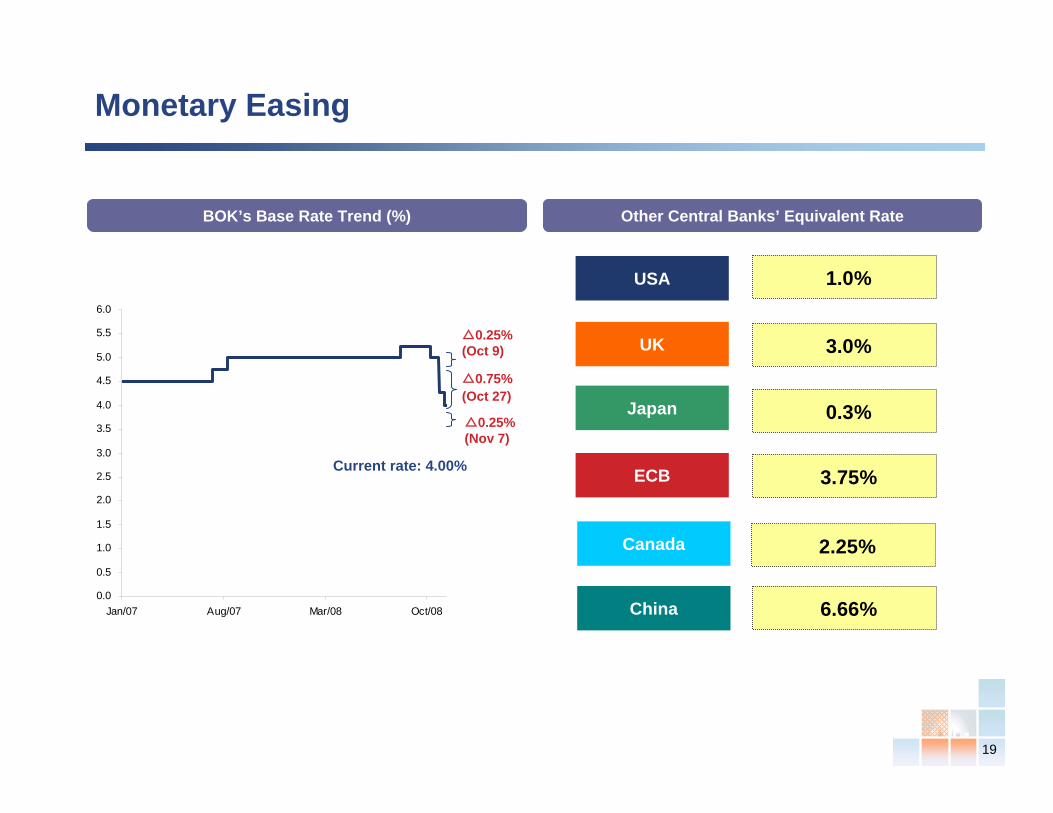

19

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

Jan/07 Aug/07 Mar/08 Oct/08

Monetary Easing

Current rate: 4.00%

△0.25%(Nov 7)

BOK’s Base Rate Trend (%) Other Central Banks’ Equivalent Rate

△0.75%(Oct 27)

△0.25%(Oct 9)

USA

Japan

UK

Canada

ECB

China

1%1.0%

1%3.0%

1%0.3%

1%3.75%

1%2.25%

1%6.66%

20

1. Recent Macroeconomic Developments

2. Current Issues & Answers

3. Government’s Policy Responses

4. Korea : Economic Outlook for 2009 envisioned by Korean Government

21

4. Korea: Economic Outlook for 2009 envisioned by Korean Government

Around 1%p

•Continued deregulations

•Enhancement of labor market flexibility

70,000 ~ 80,000

Around 3% 120,000 ~ 130,000Original Forecast

Policy Effect

0.3%p● Tax cut (2009 : KRW 10.3tn)

+α● Deregulation & monetary easing

0.5%p

0.4%p0.03%p0.1%p

● Additional Fiscal Measures (Nov. 3)

- Expenditure (KRW 11 tn) - Tax cut (09: KRW 0.9 tn) - Front-loading of Expenditure

0.2%p● Tax credit (KRW4.4 tn)

● Supplementary budget (KRW 4.6 tn)

Around 4% 190,000 ~ 210,000

GDP Growth Job Creation

After Stimulus

22

Thank You