the j.p. morgan covered bond handbook 2011 - wikileaks · europecredit research 12 september 2011...

TRANSCRIPT

www.morganmarkets.com

EuropeCredit Research12 September 2011

The J.P. Morgan Covered Bond Handbook 2011Taking the strain

European ABS & CB Research

Gareth Davies, CFA AC

(44-20) 7325-7283

Flavio Marco Rusconi AC

(44-20) 7777-4461

J.P. Morgan Securities Ltd.

See page 302 for analyst certification and important disclosures.J.P. Morgan does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

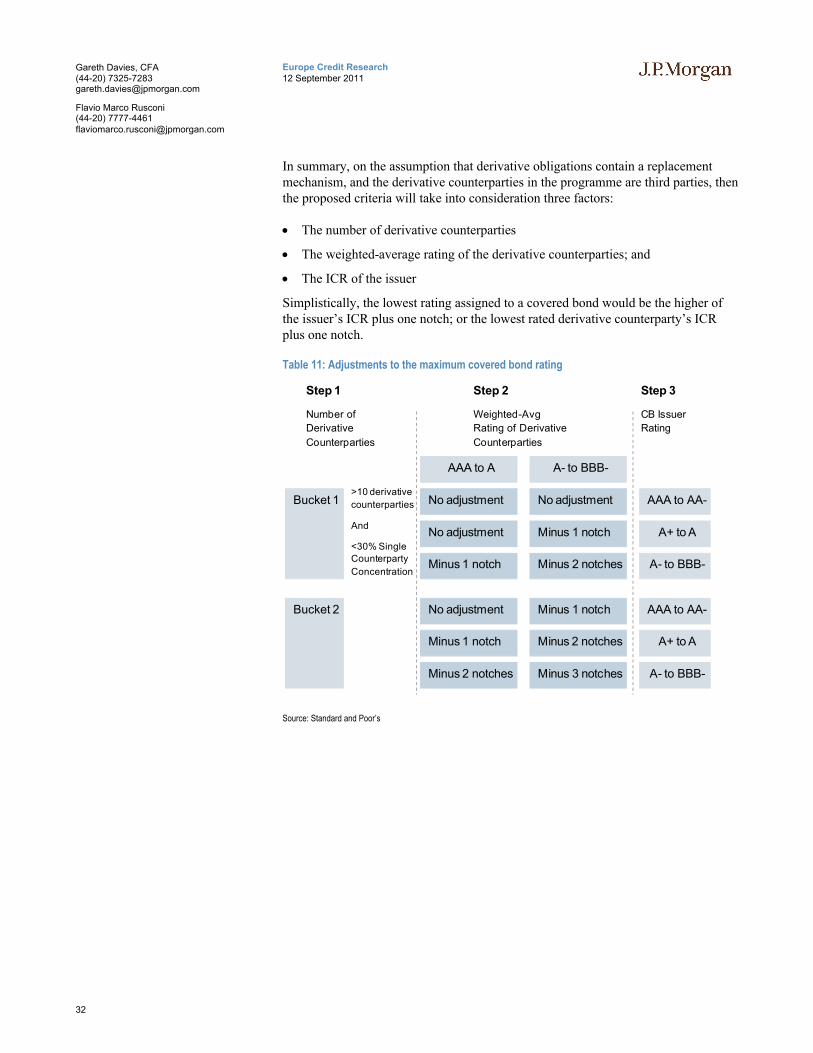

We write this year’s Handbook from something of a position of strength for the industry. Over the course of the past twelve months we have seen product expansion across many metrics: from the number of jurisdictions providing a stable regulatory framework for covered bond issuance; to the number of originators relying on covered bonds as part of their funding mix; and of course to the number of investors, both credit- and rates-focused who now engage with the asset class.

This is an even greater achievement when considering the broad market themes that have characterised the past twelve months. With the continuing peripheral European sovereign crisis elevating concerns about the health of the region’s banks, and further exacerbated by what is proving to be a relatively weak economic recovery (at best), the appetite for adding bank debt (even when secured) has been tested severely. Covereds as an asset class appear to have passed this test.

That being said however, we remain aware of potential roadbumps in the medium-term outlook. We identify the developing regulatory regime as the primary protagonist – we believe the regulatory backdrop is potentially becoming skewed in favour of covered bonds to such a degree, that it is damaging the diversity of alternate bank funding opportunities, and by derivation, potentially harming the ability of today’s covered product to grow at a more measured and sustainable pace. We would welcome a more balanced environment where covereds play a role in bank funding, but not the role.

As usual, we split the Handbook into two discrete sections, first providing an overview of market and product themes, followed by the larger, second segment which provides a jurisdiction-by-jurisdiction, issuer-by-issuer overview of those institutions that have accessed the international capital markets.

Hard copies of this publication are available by contacting the analysts.

2

Europe Credit Research12 September 2011

Gareth Davies, CFA(44-20) [email protected]

Flavio Marco Rusconi(44-20) [email protected]

Foreword

What a difference a year makes! At the time of publication of our last Handbook in September 2010, we wrote something of a ‘love letter’ to credit investors; suggesting they increase their engagement with an asset class that had historically been outside their traditional investment criteria. The onslaught of the European sovereign crisis augmented our investment rationale, with pricing pushing a number of covered sub-segments to levels where value could also be identified from a credit perspective. In last year’s publication, we welcomed the opportunity that both regulatory support and pricing linked more closely to alternative bank funding instruments in a number of jurisdictions had brought to the market.

We therefore write this year’s Handbook from something of a position of strength for the industry. Over the course of the past twelve months we have seen product expansion across many metrics: from the number of jurisdictions providing a stable regulatory framework for covered bond issuance; to the number of originators relying on covered bonds as part of their funding mix; and of course to the number of investors, both credit- and rates-focused who now engage with the asset class.

This is an even greater achievement when considering the broad market themes that have characterised the past twelve months. With the continuing peripheral European sovereign crisis elevating concerns about the health of the region’s banks, and further exacerbated by what is proving to be a relatively weak economic recovery (at best), the appetite for adding bank debt (even when secured) has been tested severely. Covereds as an asset class appear to have passed this test.

That being said however, we remain aware of potential roadbumps in the medium-term outlook (as credit analysts the glass is always half empty). While analysts responsible for other products may envy the relative health of the covered bond markets, our caution stems from what we see as the potential for over-reliance on the asset class.

In this, we identify the developing regulatory regime as the primary protagonist–we believe the regulatory backdrop is potentially becoming skewed in favour of covered bonds to such a degree, that it is damaging the diversity of alternate bank funding opportunities, and by derivation, potentially harming the ability of today’s covered product to grow at a more measured and sustainable pace. Looking ahead to the next twelve months, we would welcome a more balanced environment where covereds play a role in bank funding, but not the role.

Document structureAs usual, we split the Handbook into two discrete sections, first providing an overview of market and product themes, followed by the larger, second segment which provides a jurisdiction-by-jurisdiction, issuer-by-issuer overview of those institutions that have accessed the international capital markets.

We hope this Handbook proves useful for investors over the course of the next twelve months, and of course welcome any feedback on its form and content.

Credit where credit is due

The last year has demonstrated the increasing appeal of covered

bonds on a global basis…

…despite substantial headwinds

Can one have too much of a good thing? Yes…

Lots of eggs. Lots of baskets. Please!

3

Europe Credit Research12 September 2011

Gareth Davies, CFA(44-20) [email protected]

Flavio Marco Rusconi(44-20) [email protected]

Table of ContentsForeword ...................................................................................2

Primary Market Outlook ...........................................................9

The last twelve months–‘the boy done good' ............................................................9

The next twelve months–Magic 8 ball time............................................................14

Secondary Market Outlook ....................................................15

The last twelve months–Vow to thee, my country ..................................................15

The next twelve months–More of the same ............................................................17

Our covered bond recommendations...................................18

Product overview....................................................................20

Covered Bonds: a “bluffer’s guide” .......................................................................20

What exactly is a covered bond?............................................................................21

Covered bonds vs. RMBS......................................................................................23

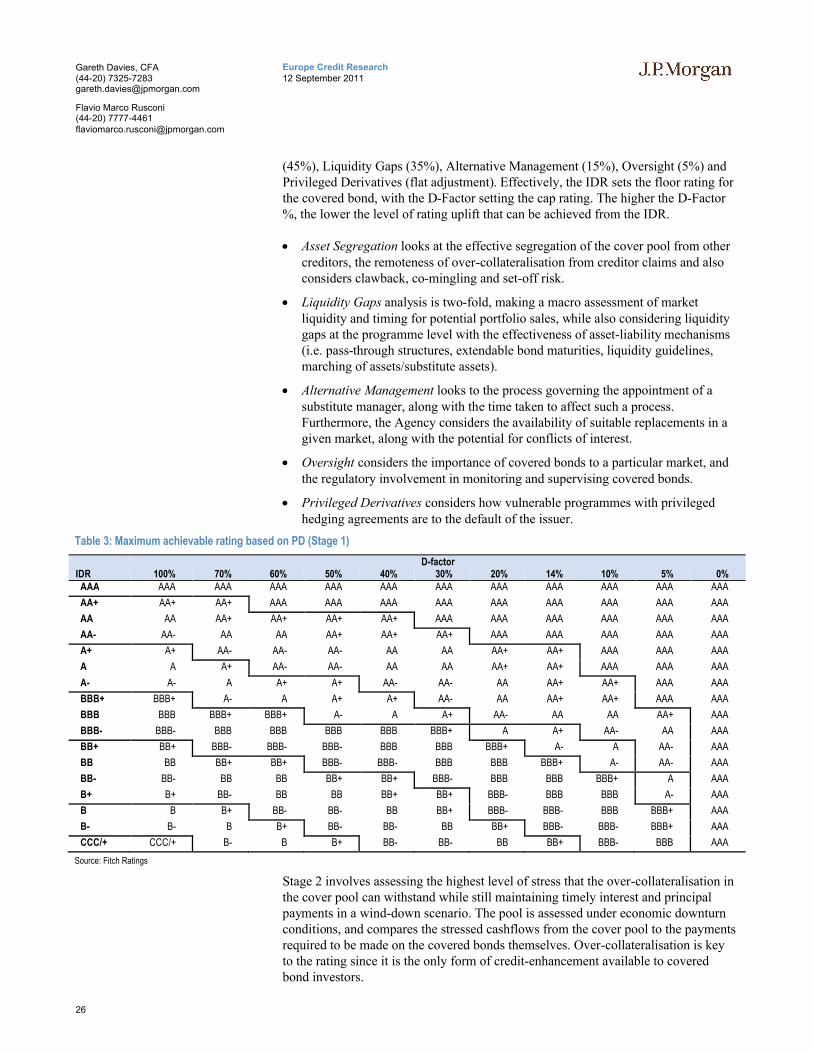

Rating Agencies .....................................................................25

DBRS ...................................................................................................................25

Fitch Ratings.........................................................................................................25

Moody’s ...............................................................................................................28

Standard & Poor’s.................................................................................................29

Austrian Covered Bonds .......................................................36

Legislative snapshot ..............................................................................................36

Austrian covered bond & macro backdrop .............................................................37

BAWAG PSK.......................................................................................................38

Erste Bank Group..................................................................................................39

HYPO NOE Gruppe..............................................................................................40

Kommunalkredit Austria AG.................................................................................41

UniCredit Bank Austria.........................................................................................42

Canadian Covered Bonds......................................................44

Legislative snapshot ..............................................................................................44

Canadian covered bond & macro backdrop ............................................................45

Bank of Montreal ..................................................................................................46

Caisse Centrale Desjardins du Quebec ...................................................................48

CIBC ....................................................................................................................50

National Bank of Canada.......................................................................................52

Royal Bank of Canada...........................................................................................53

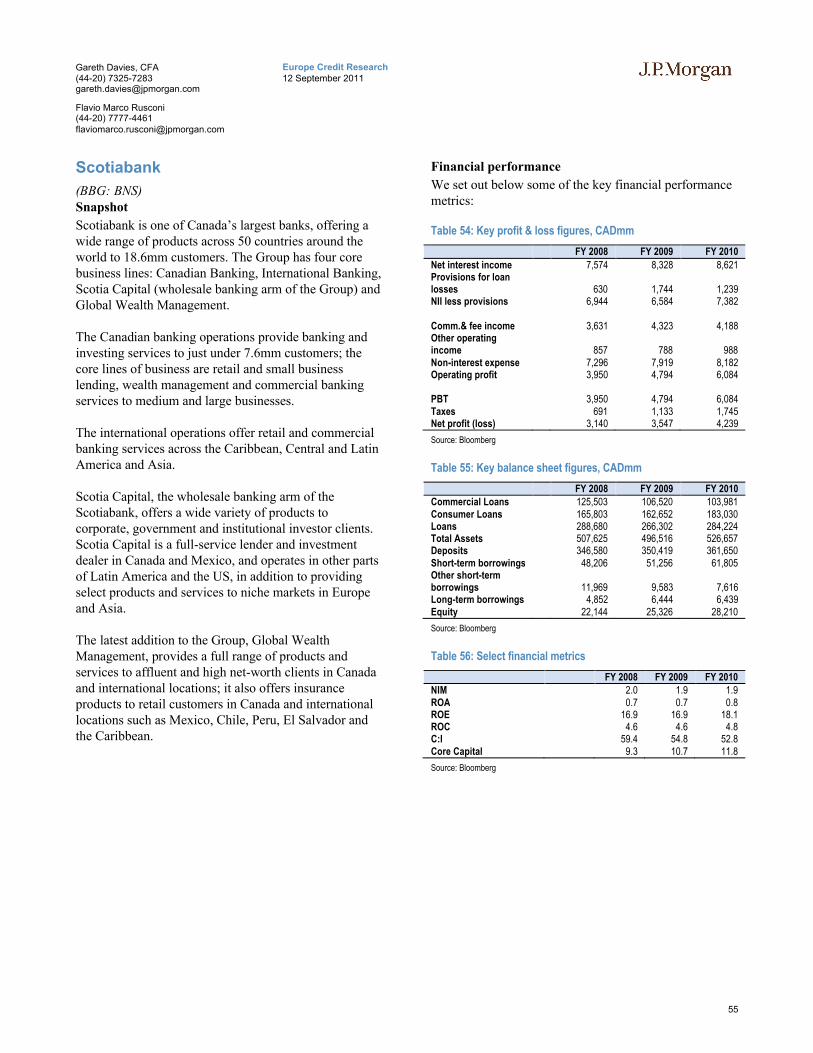

Scotiabank ............................................................................................................55

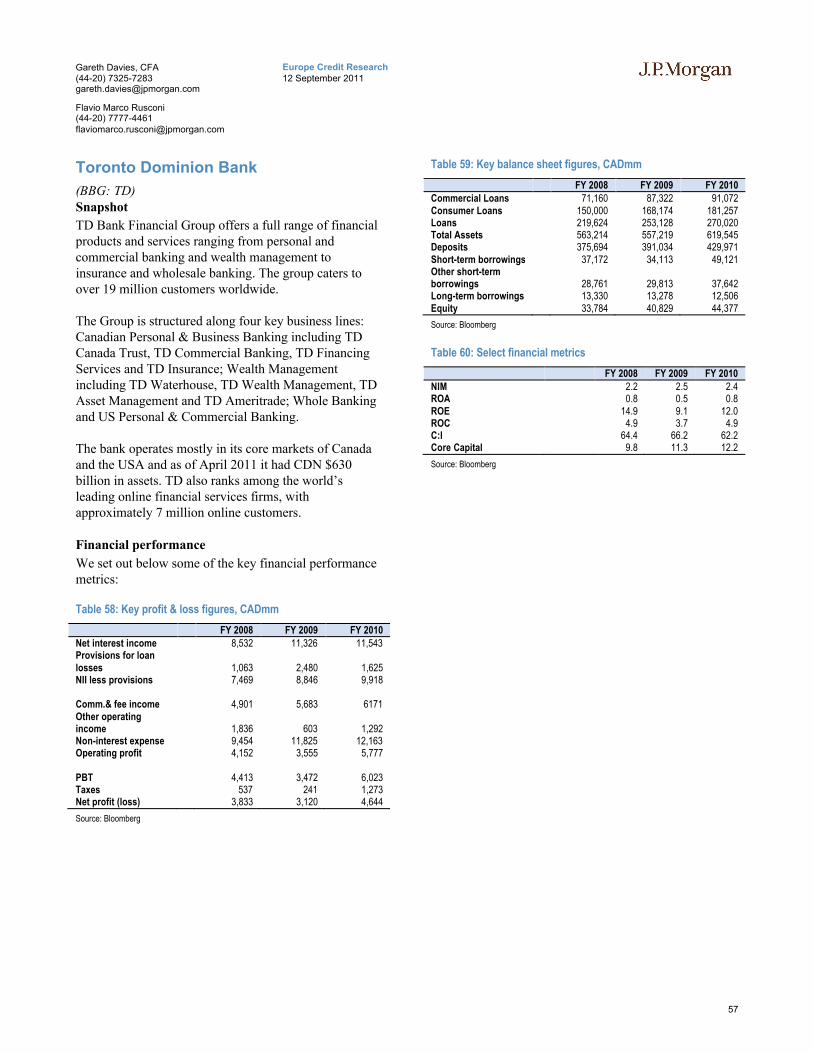

Toronto Dominion Bank........................................................................................57

Danish Covered Bonds ..........................................................60

Legislative snapshot ..............................................................................................60

Danish covered bond & macro backdrop................................................................61

BRF Kredit AS......................................................................................................62

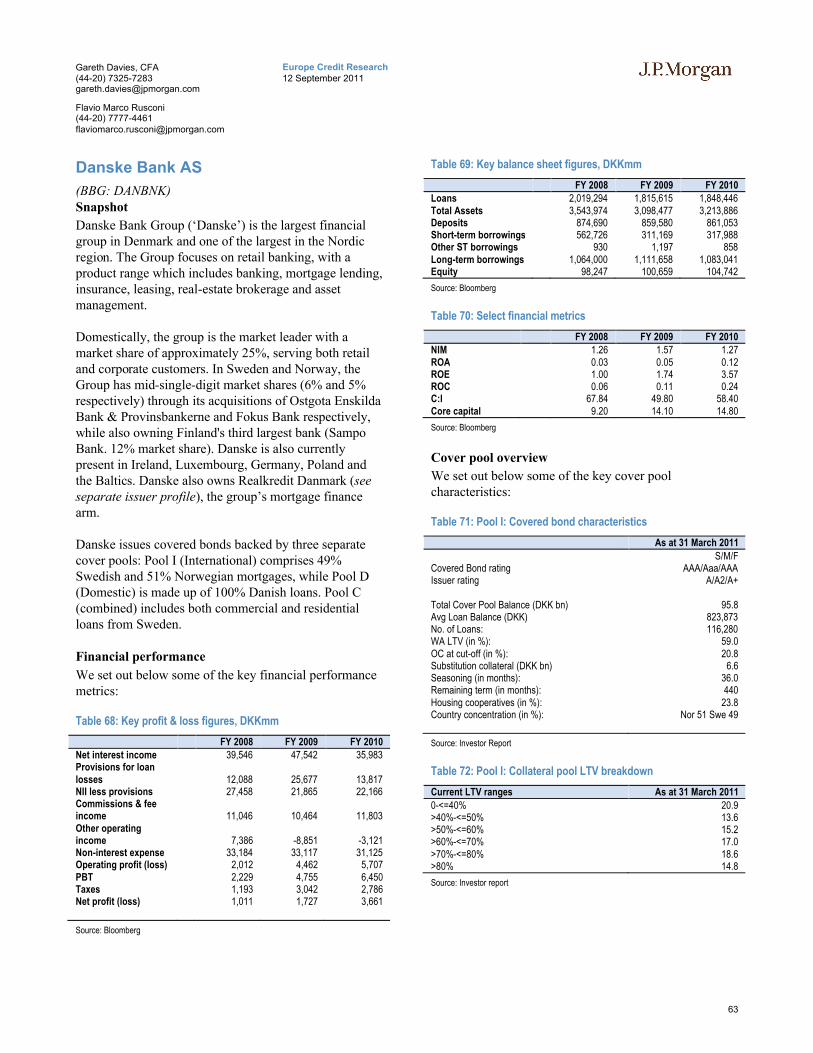

Danske Bank AS...................................................................................................63

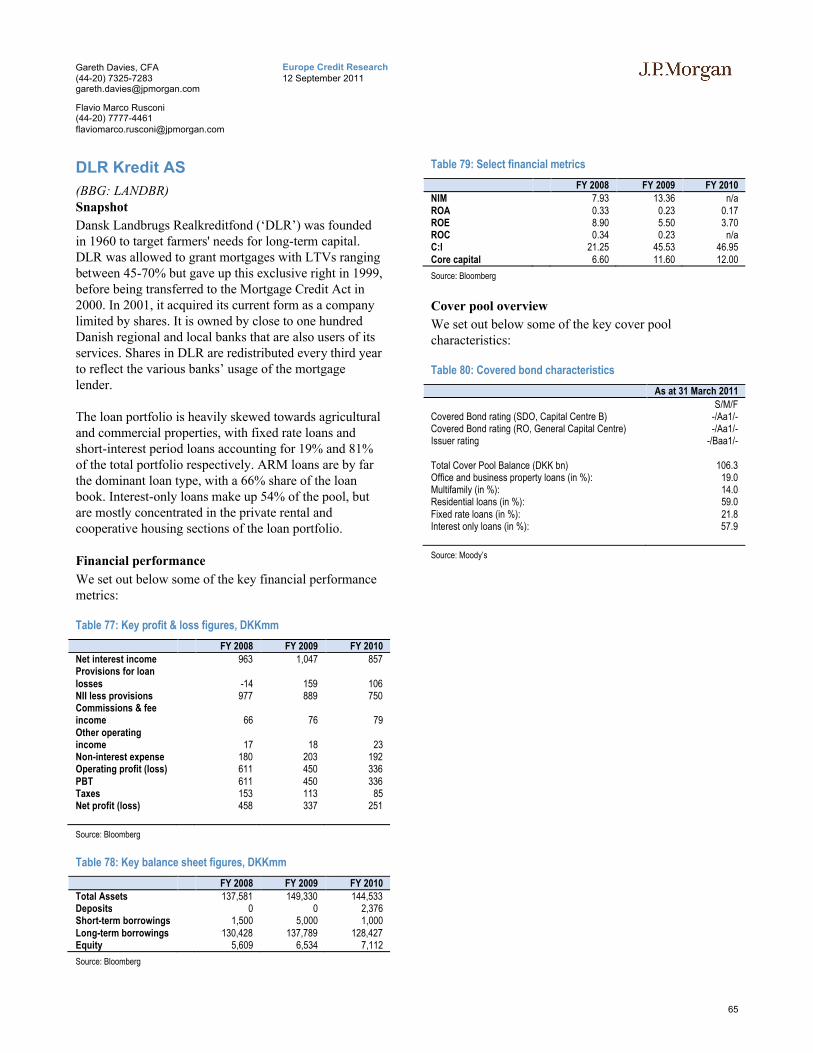

DLR Kredit AS.....................................................................................................65

4

Europe Credit Research12 September 2011

Gareth Davies, CFA(44-20) [email protected]

Flavio Marco Rusconi(44-20) [email protected]

Nordea Kredit AS..................................................................................................66

Nykredit Realkredit AS (‘Nykredit’)......................................................................67

Realkredit Danmark AS (‘Realkredit’)...................................................................68

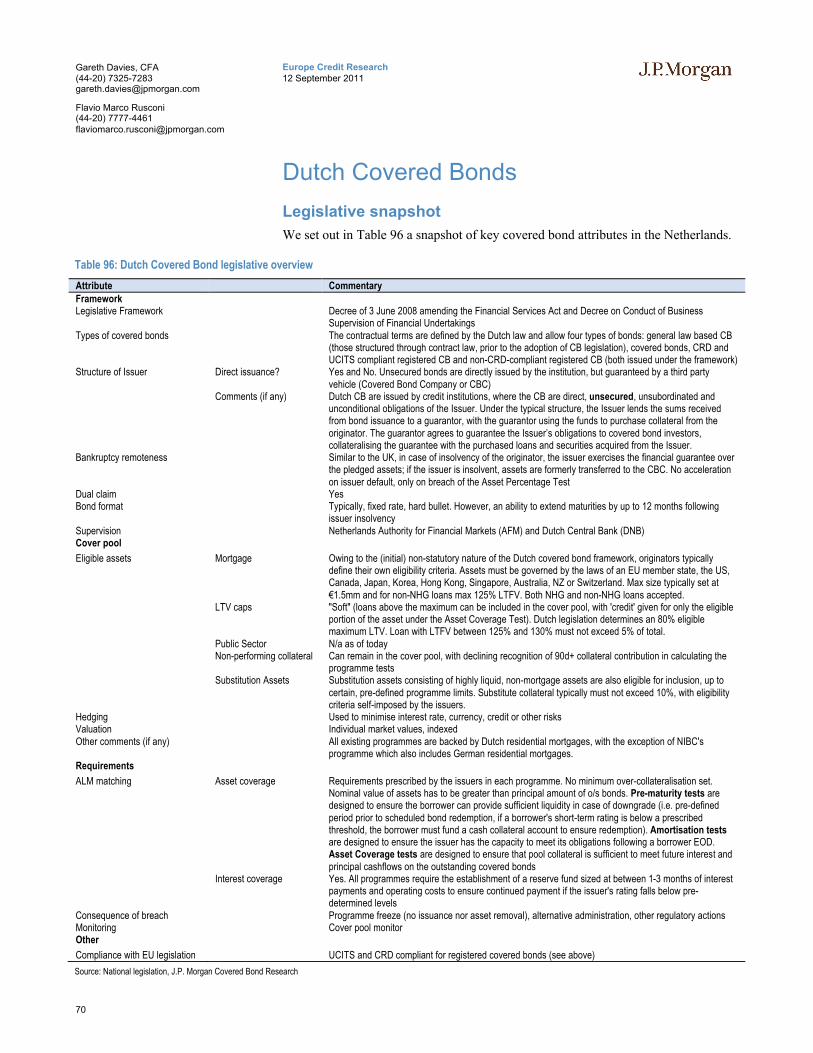

Dutch Covered Bonds............................................................70

Legislative snapshot ..............................................................................................70

Dutch covered bond & macro backdrop .................................................................71

ABN Amro Bank NV (‘ABN’)..............................................................................72

Achmea Hypotheekenbank NV ('Achmea’)............................................................73

ING Bank NV (‘ING’) ..........................................................................................74

NIBC Bank NV (‘NIBC’)......................................................................................75

SNS Bank NV (‘SNS’)..........................................................................................77

Finnish Covered Bonds .........................................................80

Legislative snapshot ..............................................................................................80

Finnish covered bond & macro backdrop...............................................................81

Aktia Real Estate Mortgage Bank plc ....................................................................82

Nordea Bank Finland Oyj......................................................................................83

OP Mortgage Bank (‘OP’).....................................................................................84

Sampo Housing Loan Bank ...................................................................................85

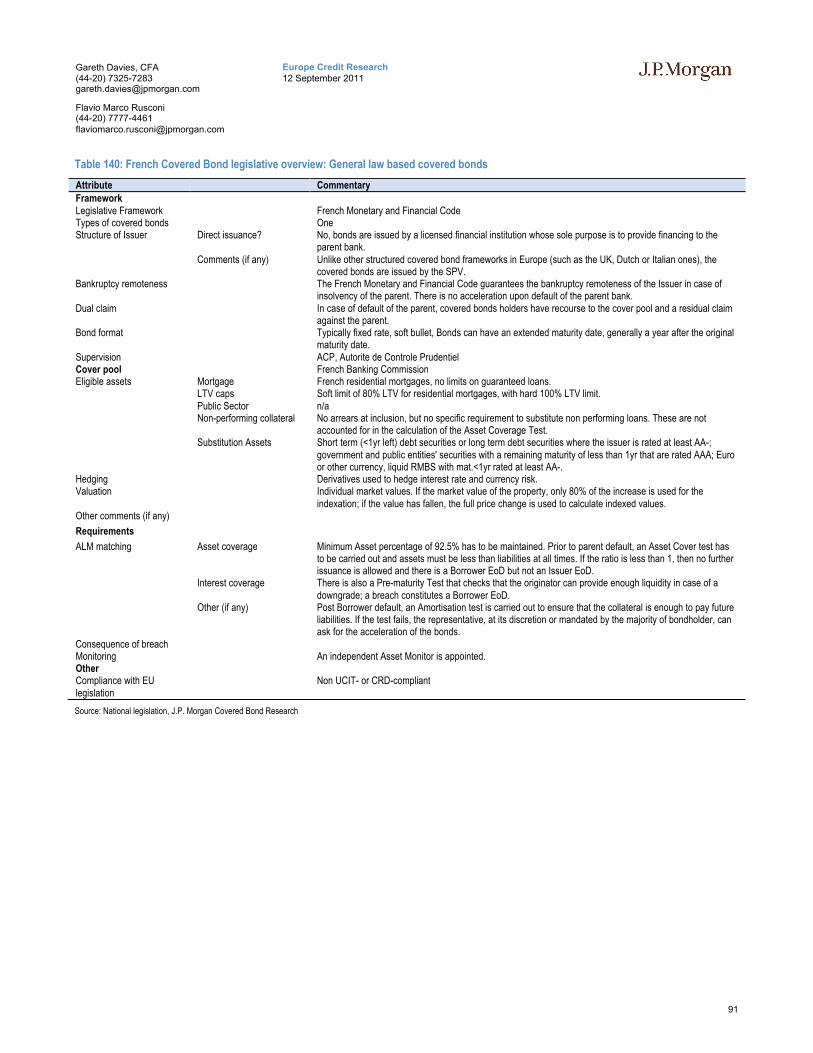

French Covered Bonds ..........................................................88

Legislative snapshot ..............................................................................................88

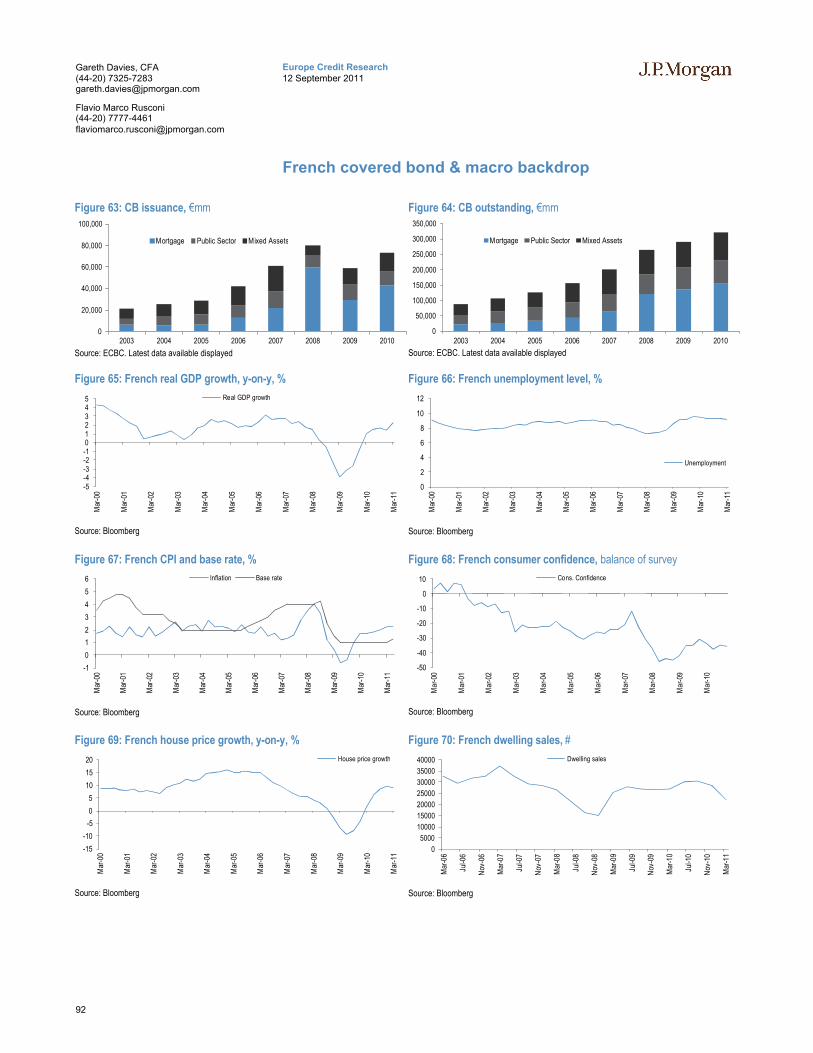

French covered bond & macro backdrop................................................................92

AXA Bank Europe SCF ........................................................................................93

Banques Populaires SCF .......................................................................................94

BNP Paribas Home Loan SFH...............................................................................95

BNP Paribas Public Sector SCF.............................................................................96

BPCE SFH............................................................................................................97

Caisse de Refinancement de l’Habitat....................................................................98

CIF Euromortgage SCF.........................................................................................99

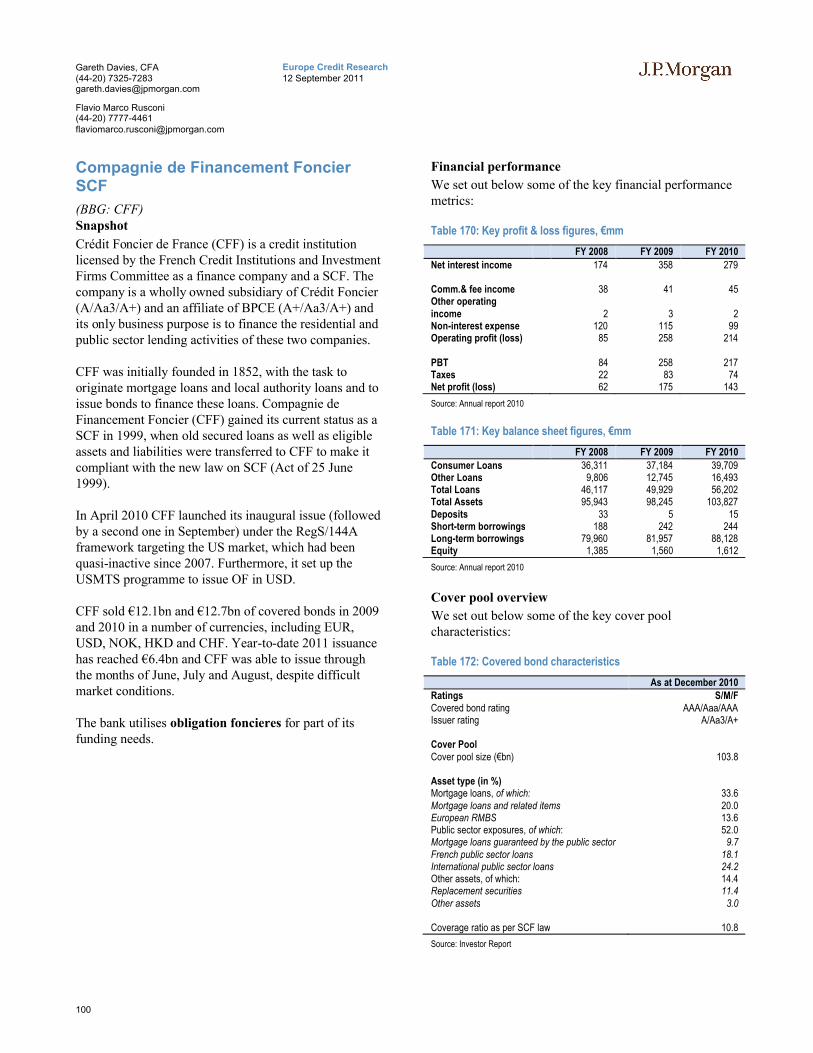

Compagnie de Financement Foncier SCF ............................................................100

Crédit Agricole Home Loans SFH .......................................................................101

Crédit Mutuel Arkéa Home Loans SFH ...............................................................102

Crédit Mutuel-CIC Home Loans SFH..................................................................103

Dexia Municipal Agency SCF .............................................................................104

General Electric SCF...........................................................................................105

Groupe Caisse d’Épargne Covered Bonds............................................................106

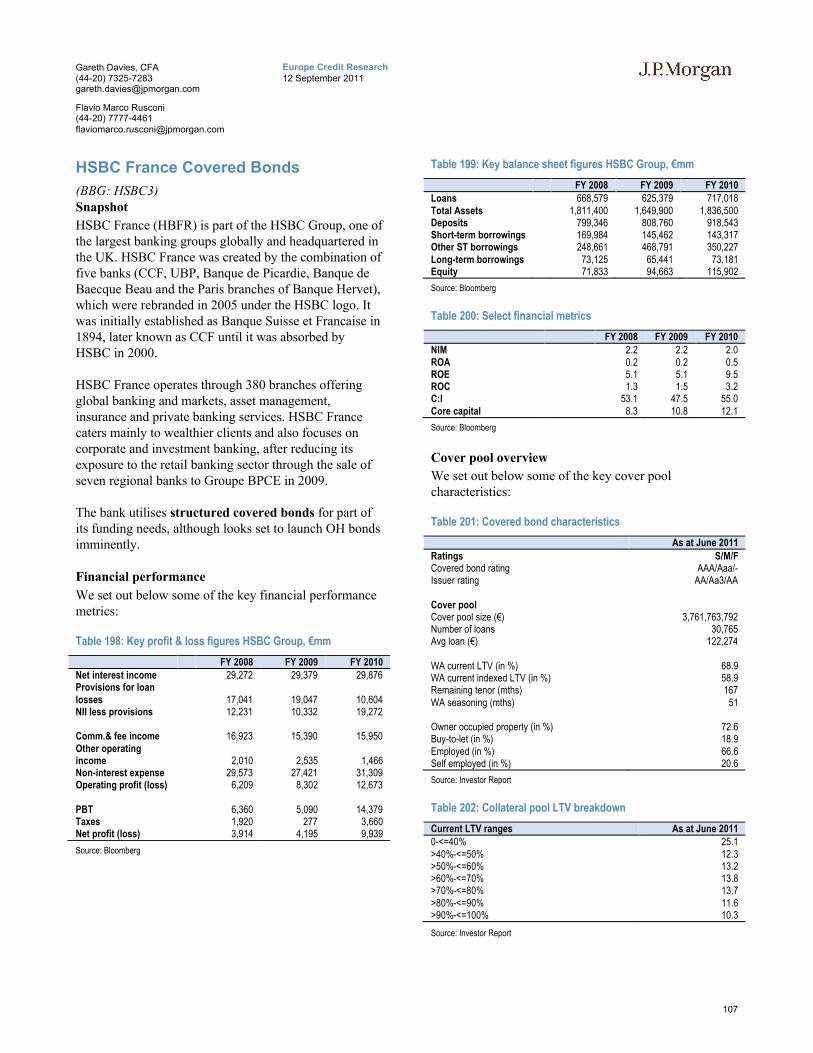

HSBC France Covered Bonds..............................................................................107

Société Générale SCF..........................................................................................108

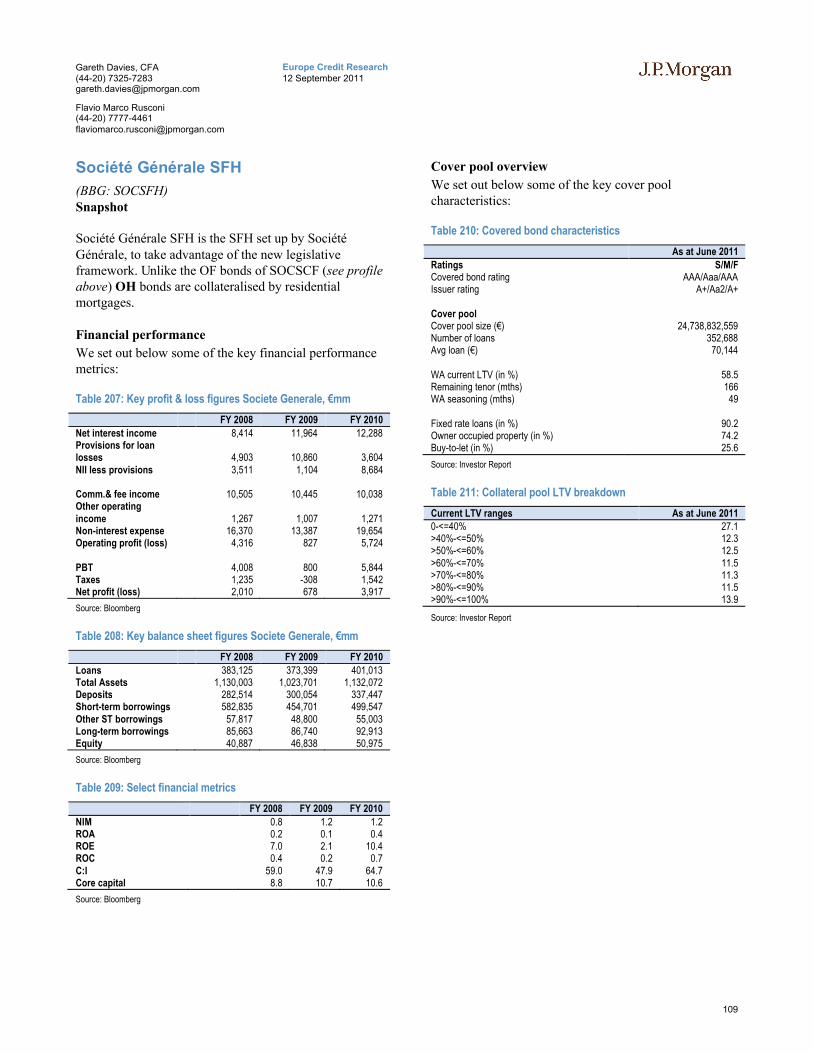

Société Générale SFH .........................................................................................109

German Covered Bonds ......................................................112

Legislative snapshot ............................................................................................112

German covered bond & macro backdrop ............................................................113

Aareal Bank AG..................................................................................................114

Bayerische Landesbank (BayernLB)....................................................................116

Berlin-Hannoversche Hypothekenbank................................................................118

Bremer Landesbank ............................................................................................119

5

Europe Credit Research12 September 2011

Gareth Davies, CFA(44-20) [email protected]

Flavio Marco Rusconi(44-20) [email protected]

Corealcredit Bank AG.........................................................................................121

DekaBank Deutsche Girozentrale ........................................................................122

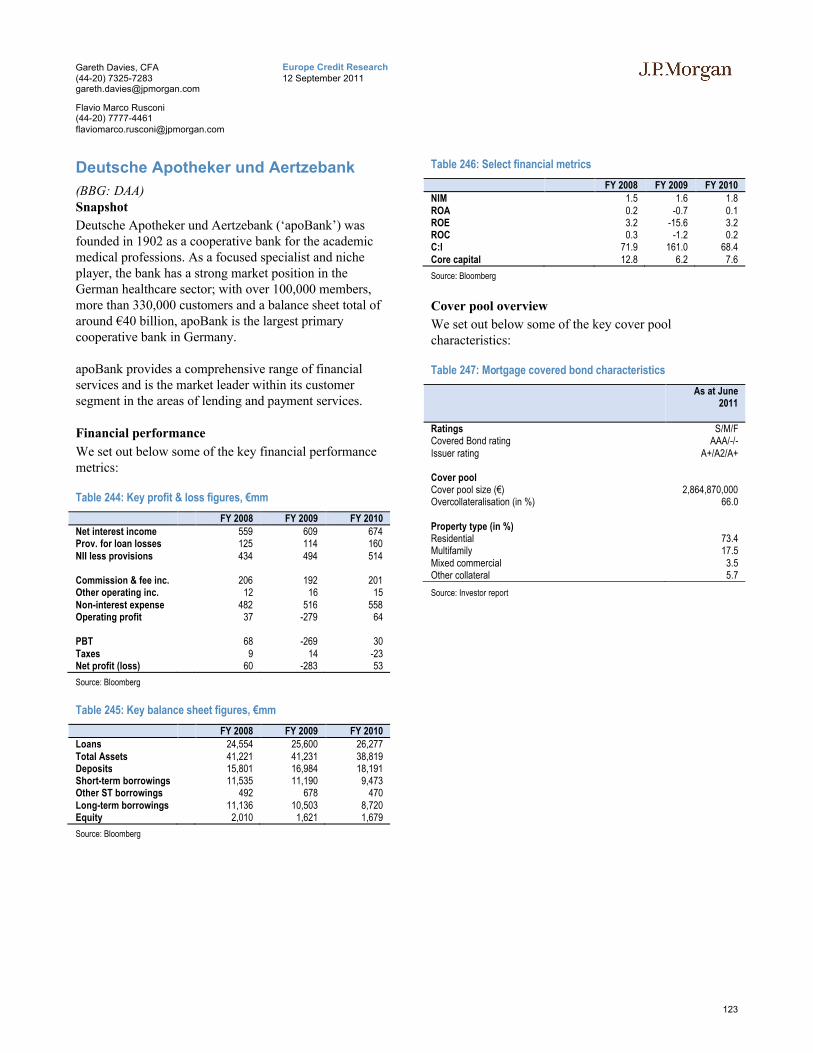

Deutsche Apotheker und Aertzebank...................................................................123

Deutsche Bank ....................................................................................................124

Deutsche Genossenshafts-Hypothekenbank (DG Hyp) .........................................125

Deutsche Hypo Hannover (Deutsche Hypothekenbank) .......................................126

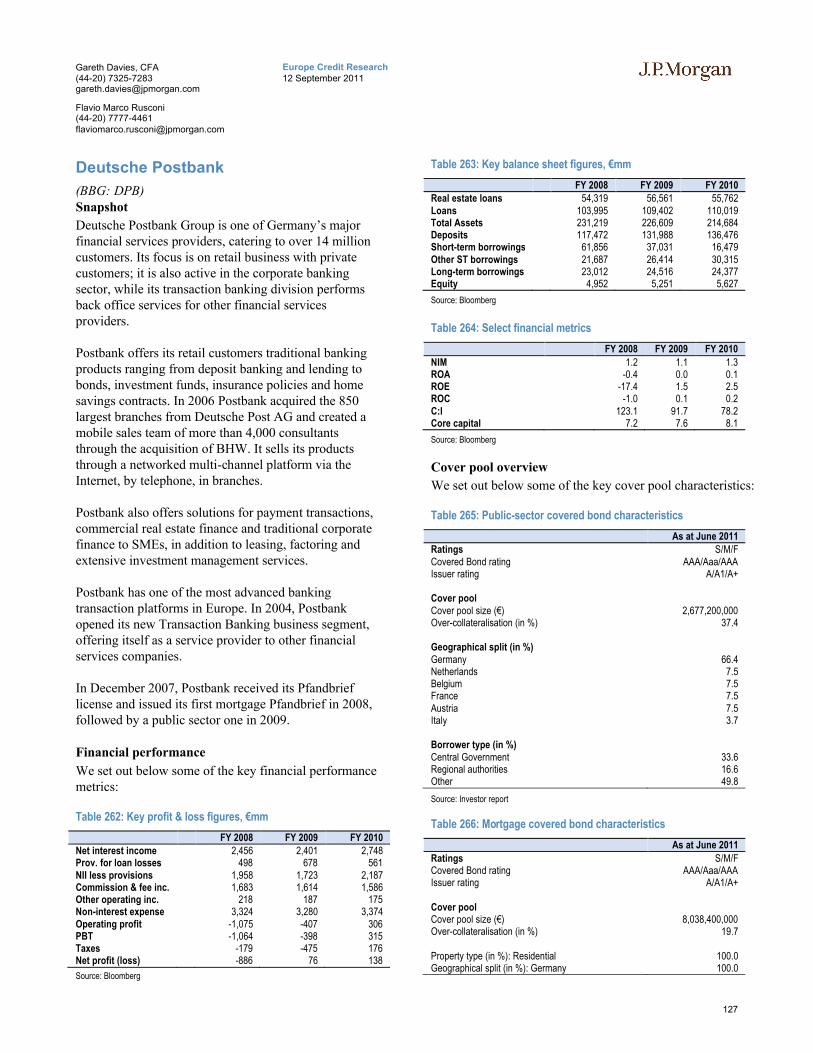

Deutsche Postbank ..............................................................................................127

Deutsche Schiffsbank..........................................................................................128

Dexia Kommunalbank Deutschland.....................................................................129

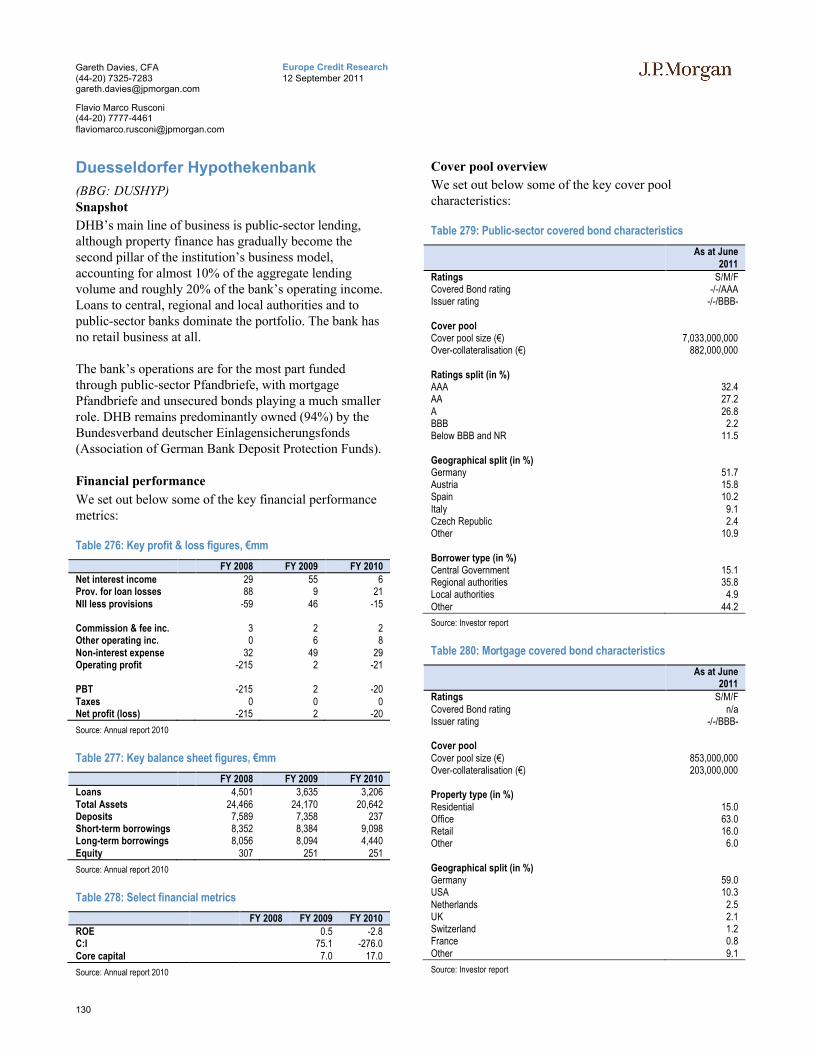

Duesseldorfer Hypothekenbank...........................................................................130

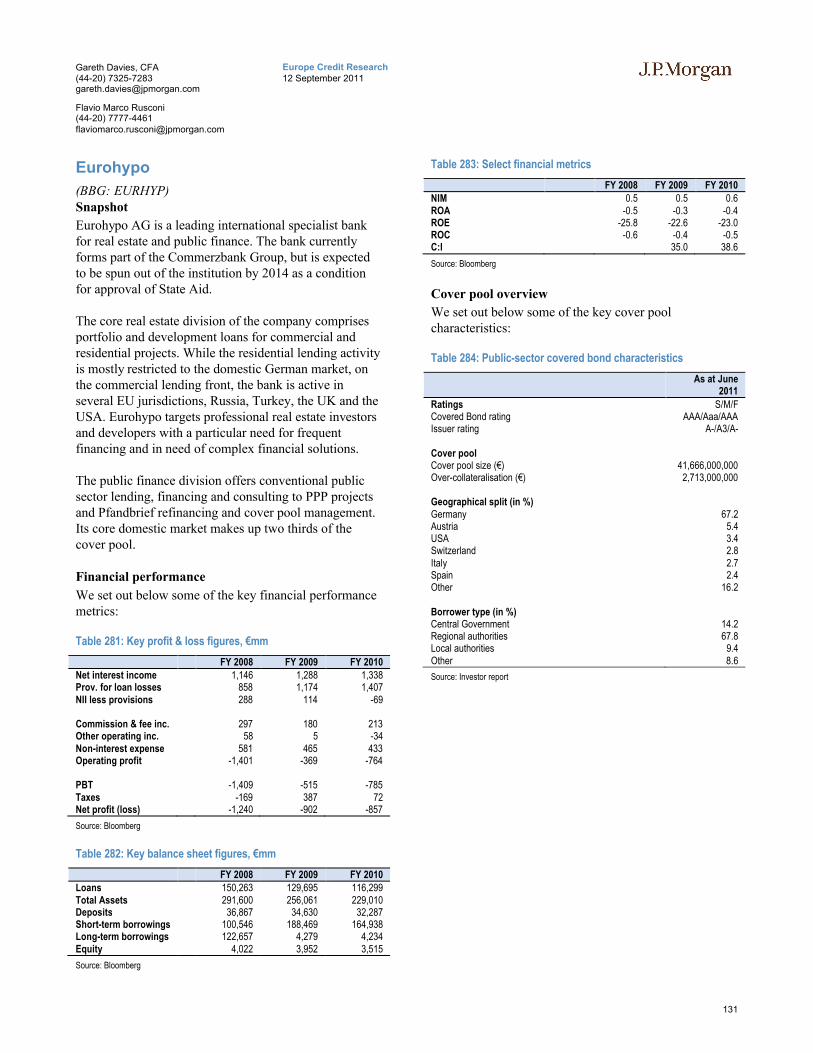

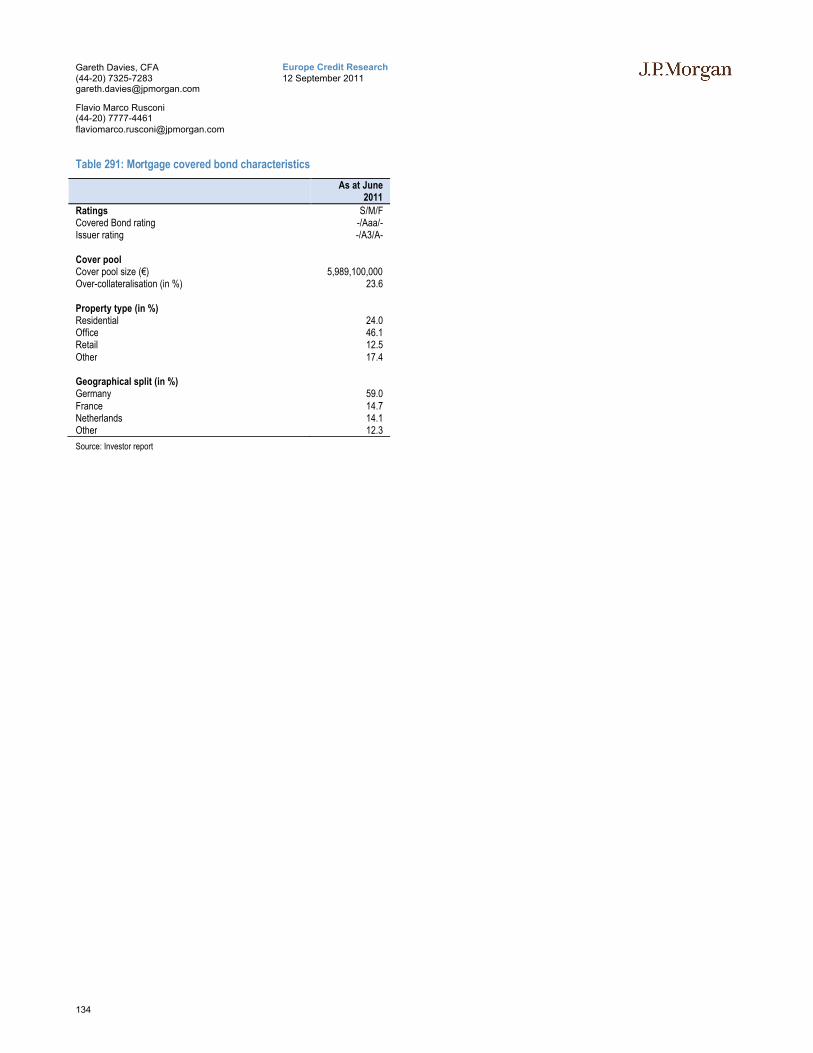

Eurohypo ............................................................................................................131

HSH Nordbank ...................................................................................................133

ING DiBa ...........................................................................................................135

Landesbank Baden Württemberg (LBBW)...........................................................136

Landesbank Berlin ..............................................................................................137

Landesbank Hessen-Thueringen ..........................................................................139

Landesbank Saar .................................................................................................140

Muenchener Hypothekenbank .............................................................................141

Norddeutsche Landesbank...................................................................................142

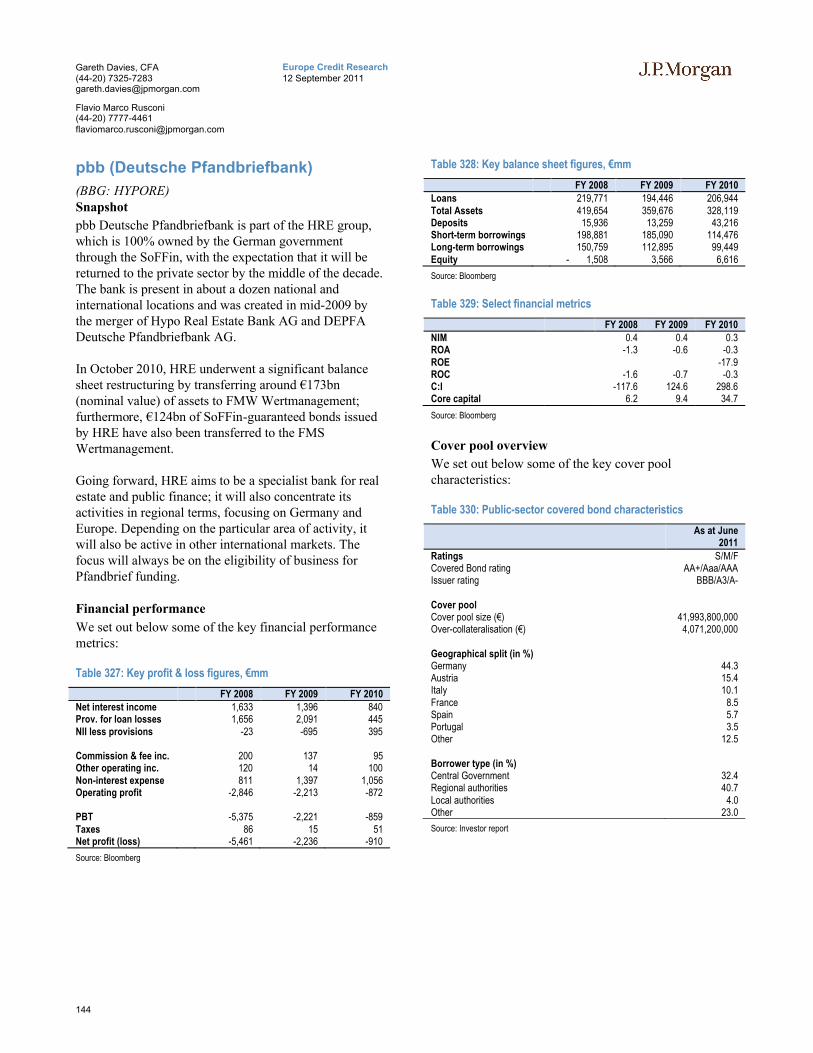

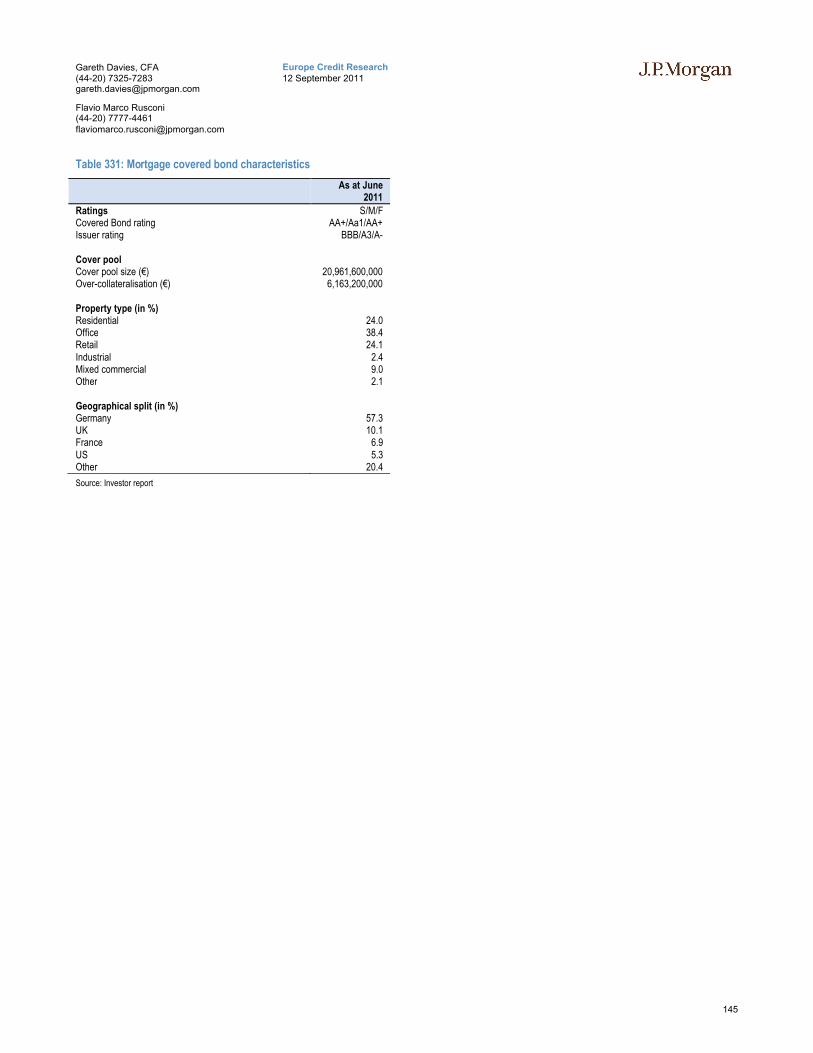

pbb (Deutsche Pfandbriefbank)............................................................................144

SEB AG..............................................................................................................146

Unicredit Bank AG (HypoVereinsbank) ..............................................................147

Westdeutsche Immobilienbank ............................................................................148

WestLB ..............................................................................................................149

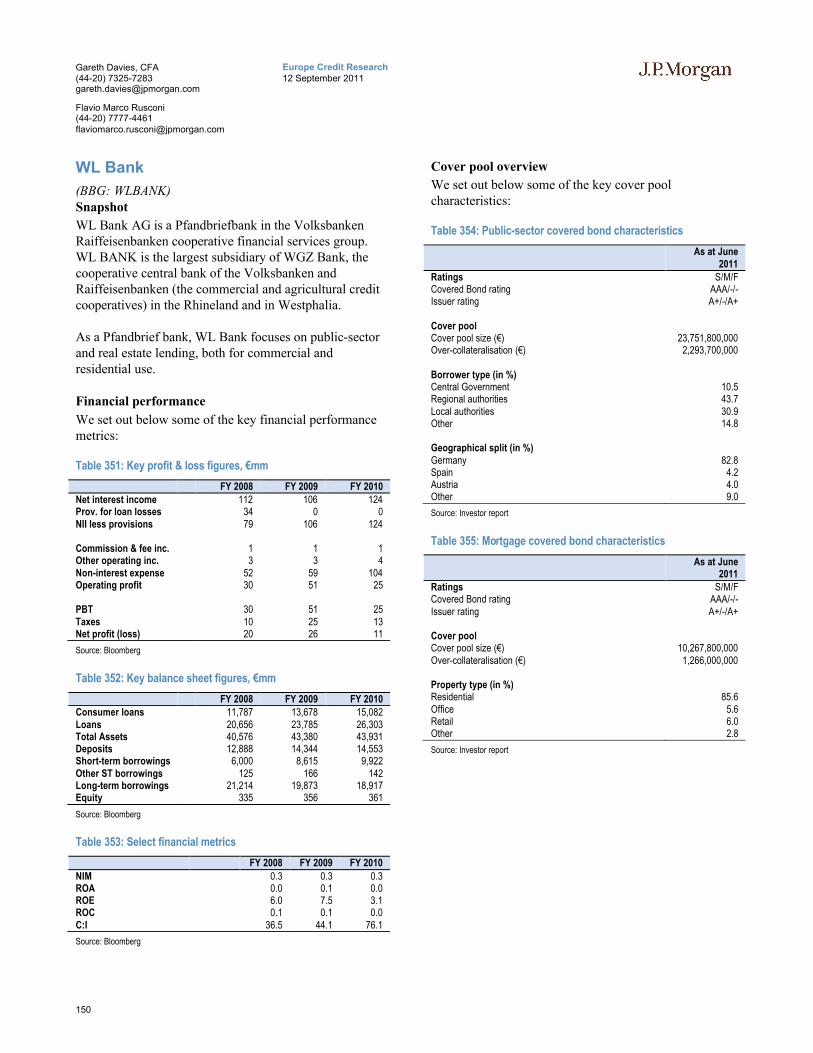

WL Bank ............................................................................................................150

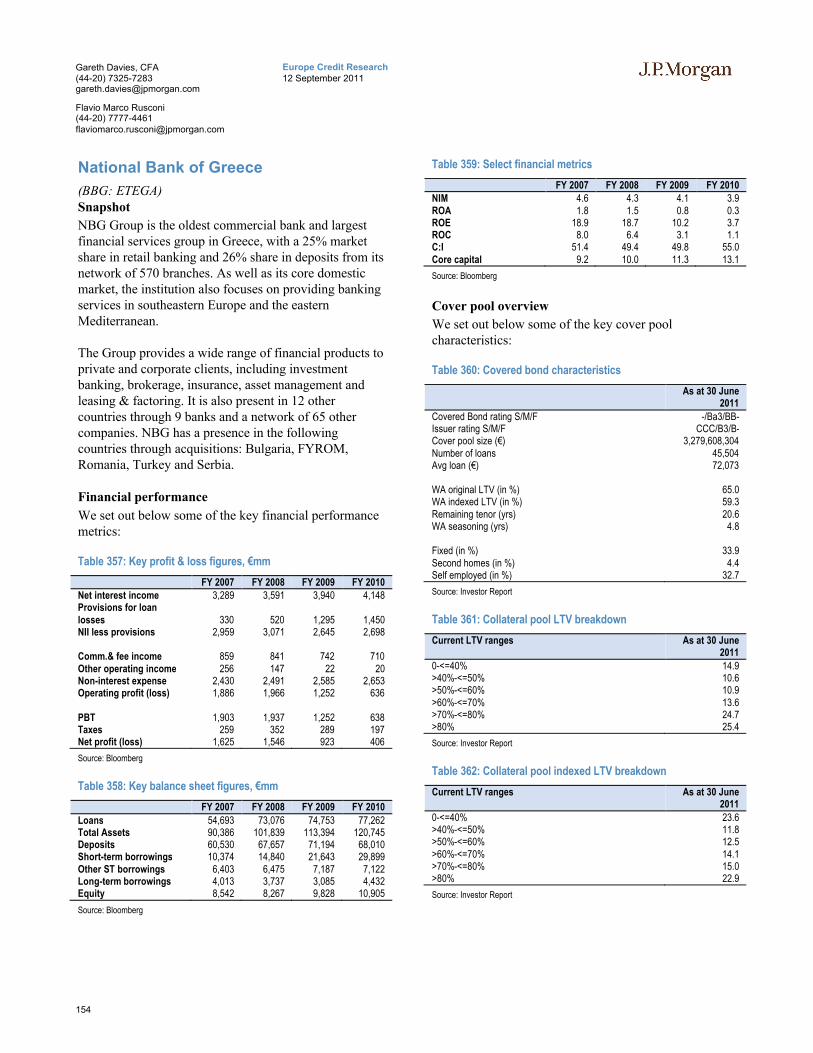

Greek Covered Bonds..........................................................152

Legislative snapshot ............................................................................................152

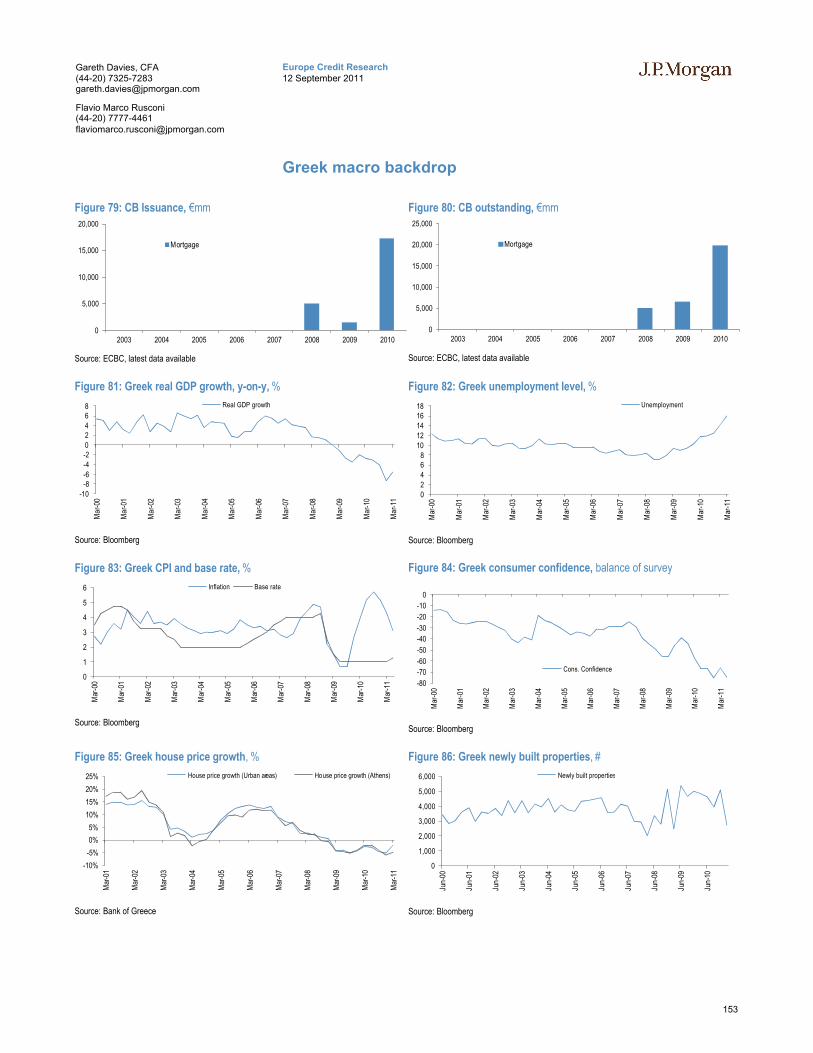

Greek macro backdrop ........................................................................................153

National Bank of Greece .....................................................................................154

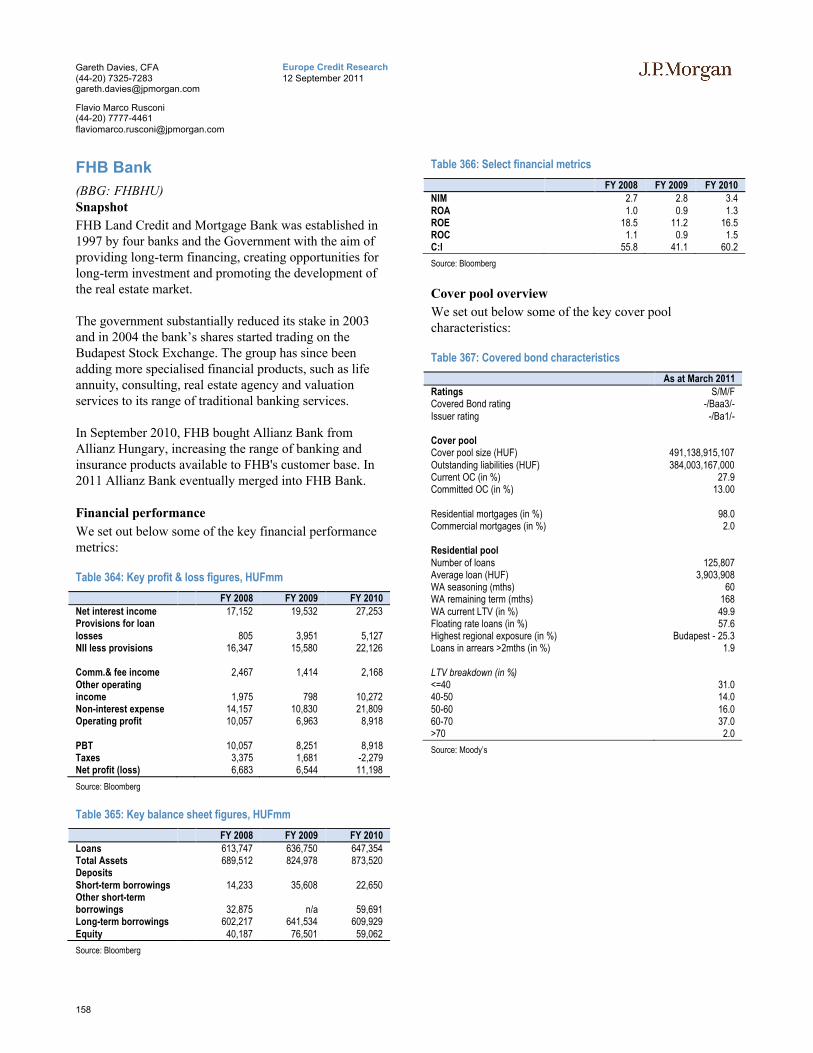

Hungarian Covered Bonds ..................................................156

Legislative snapshot ............................................................................................156

Hungarian covered bond & macro backdrop ........................................................157

FHB Bank...........................................................................................................158

OTP Bank...........................................................................................................159

Irish Covered Bonds ............................................................162

Legislative snapshot ............................................................................................162

Irish covered bond & macro backdrop .................................................................163

AIB Mortgage Bank (‘AIBMB’)..........................................................................164

Bank of Ireland Mortgage Bank (‘BoIMB’) .........................................................165

Depfa ACS Bank (‘DACS’) ................................................................................166

EBS Mortgage Finance (‘EBS’)...........................................................................167

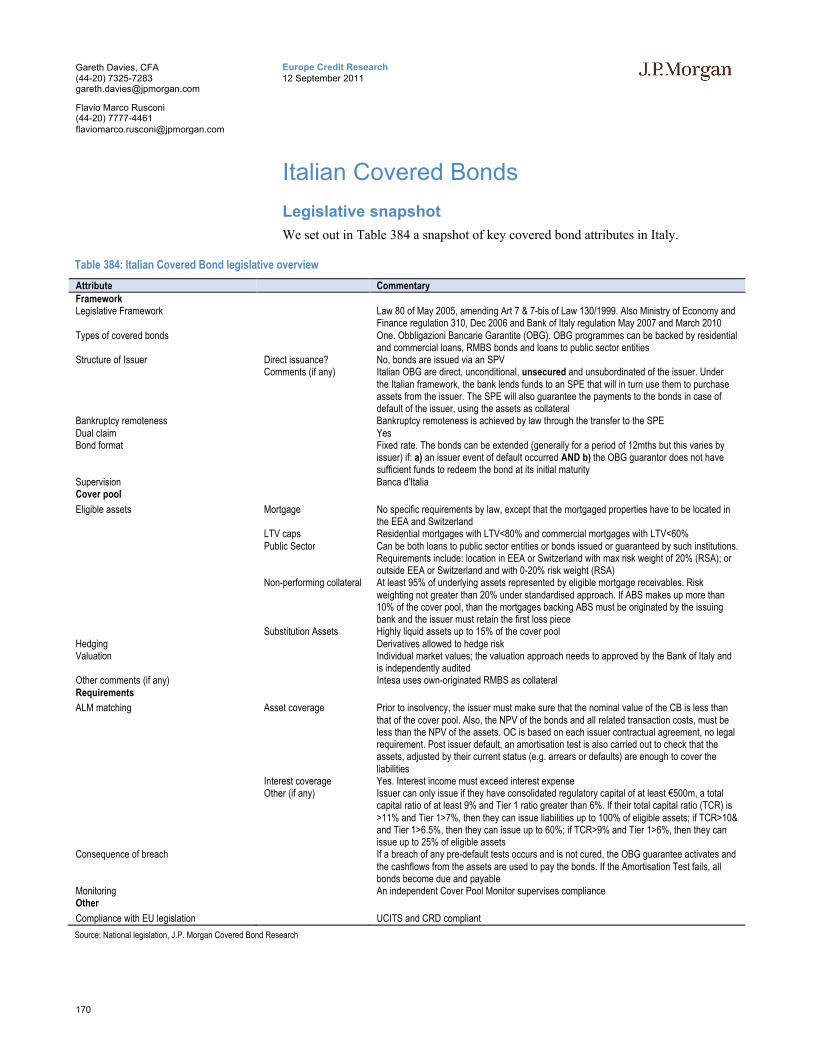

Italian Covered Bonds..........................................................170

Legislative snapshot ............................................................................................170

Italian covered bond & macro backdrop...............................................................171

6

Europe Credit Research12 September 2011

Gareth Davies, CFA(44-20) [email protected]

Flavio Marco Rusconi(44-20) [email protected]

Banca Carige (‘Carige’) ......................................................................................172

Banca Monte dei Paschi di Siena (‘BMPS’) .........................................................173

Banca Popolare di Milano (‘BPM’) .....................................................................174

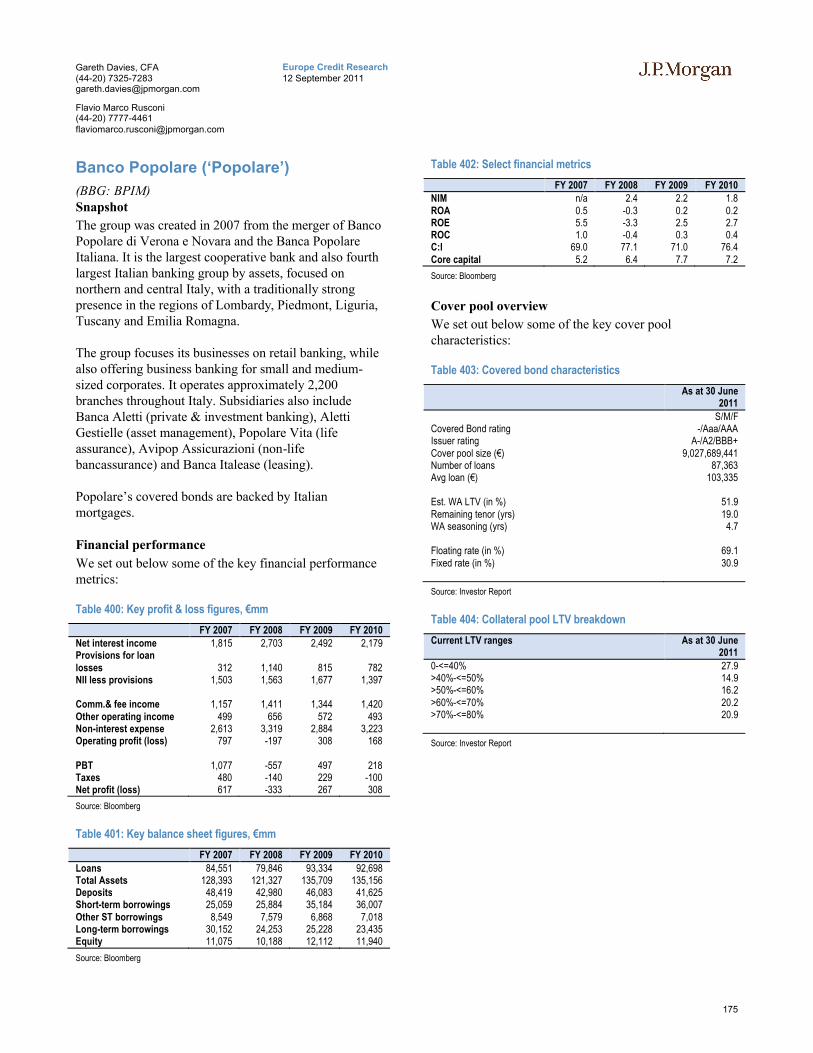

Banco Popolare (‘Popolare’)................................................................................175

Credito Emiliano (‘Credem’)...............................................................................176

Intesa Sanpaolo (‘Intesa’) ....................................................................................177

UBI Banca (‘UBI’)..............................................................................................179

Unicredit Group (‘Unicredit’)..............................................................................180

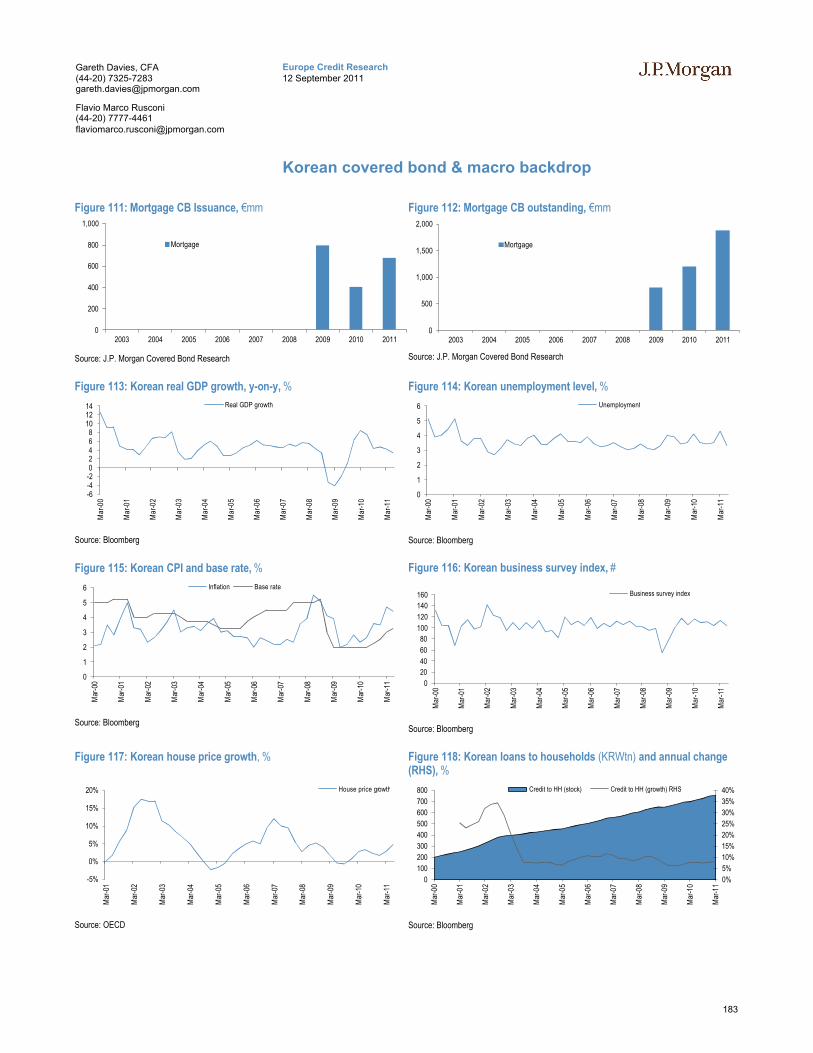

Korean Covered Bonds........................................................182

Legislative snapshot ............................................................................................182

Korean covered bond & macro backdrop .............................................................183

Kookmin Bank....................................................................................................184

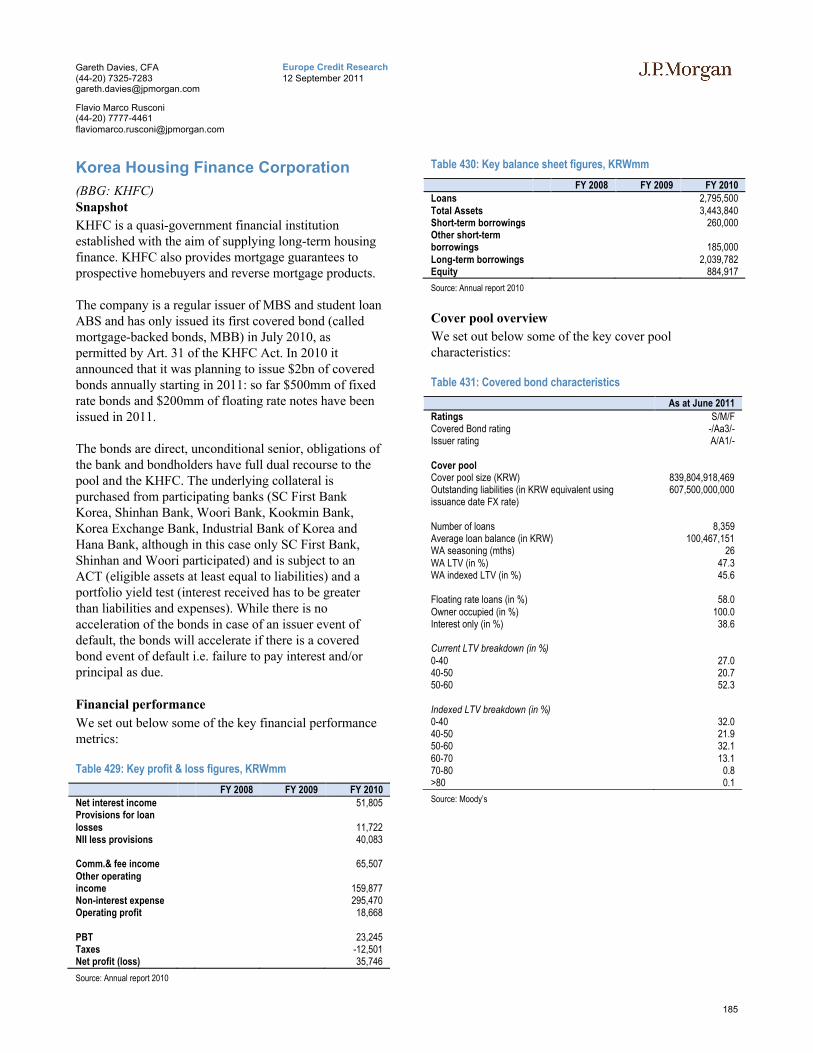

Korea Housing Finance Corporation....................................................................185

Luxembourgish Covered Bonds .........................................188

Legislative snapshot ............................................................................................188

Luxembourgish covered bond backdrop...............................................................189

Dexia LdG Banque..............................................................................................190

Erste Europaeische Pfandbrief und Kommunalbank (EEPK) ................................191

Eurohypo Luxembourg SA..................................................................................192

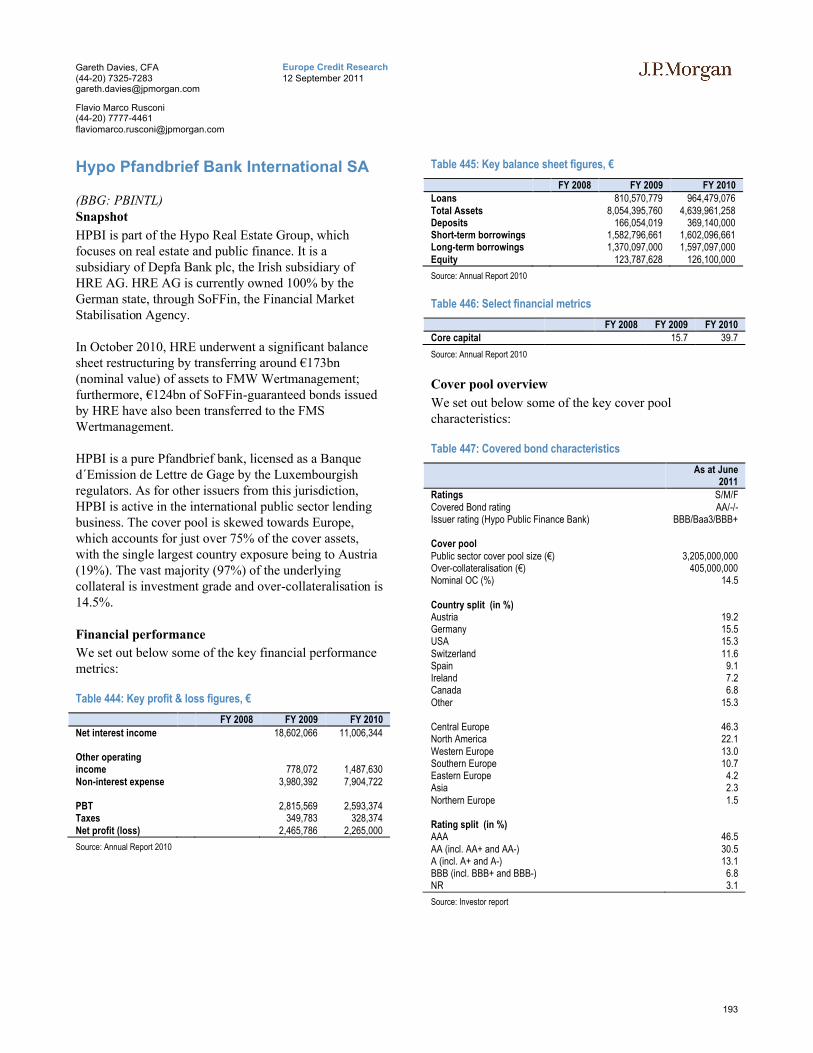

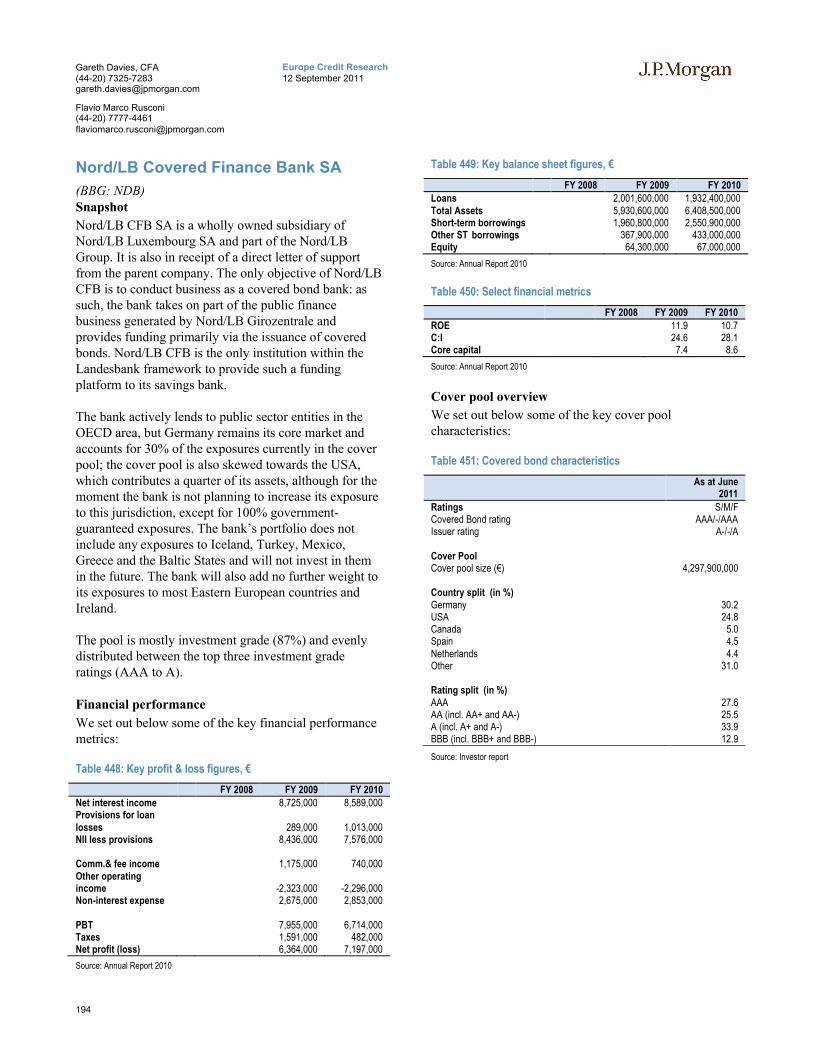

Nord/LB Covered Finance Bank SA....................................................................194

New Zealand Covered Bonds ..............................................196

Legislative snapshot ............................................................................................196

New Zealand covered bond & macro backdrop ....................................................197

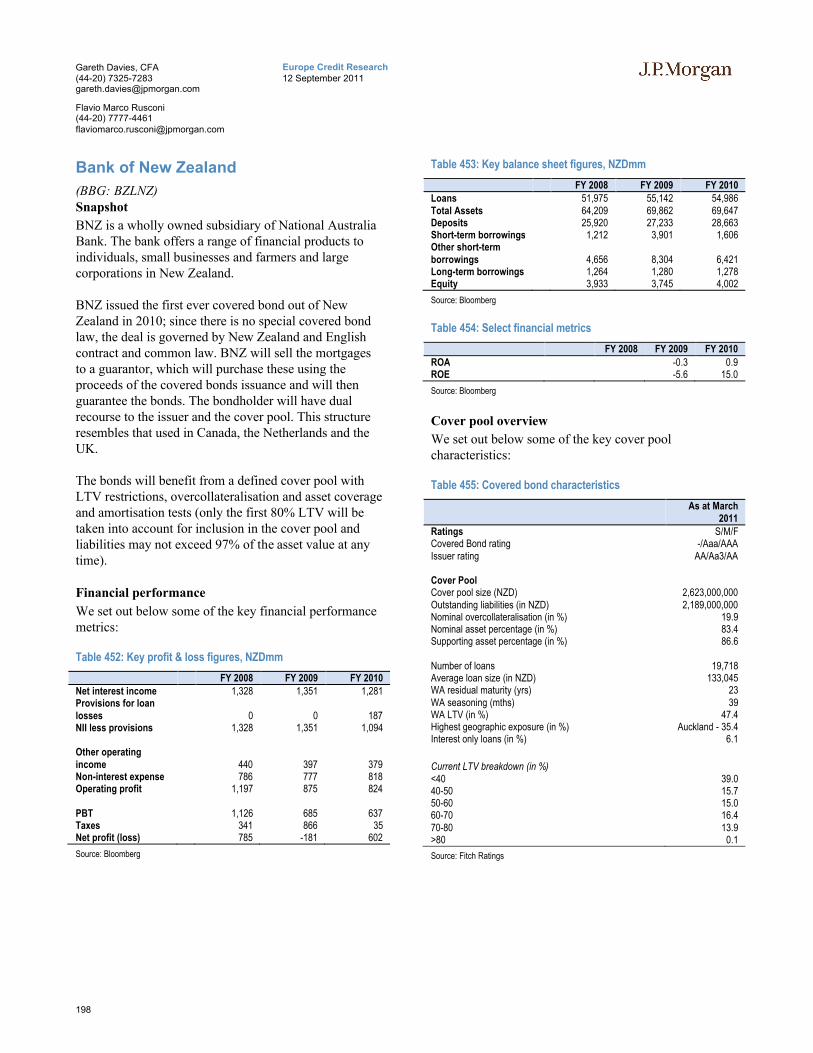

Bank of New Zealand..........................................................................................198

Westpac New Zealand.........................................................................................199

Norwegian Covered Bonds..................................................202

Legislative snapshot ............................................................................................202

Norwegian covered bond & macro backdrop .......................................................203

DnB NOR Boligkreditt ASA (‘DNB’) .................................................................204

Nordea Eiendomskreditt ......................................................................................205

SpareBank 1 Boligkreditt ASA............................................................................206

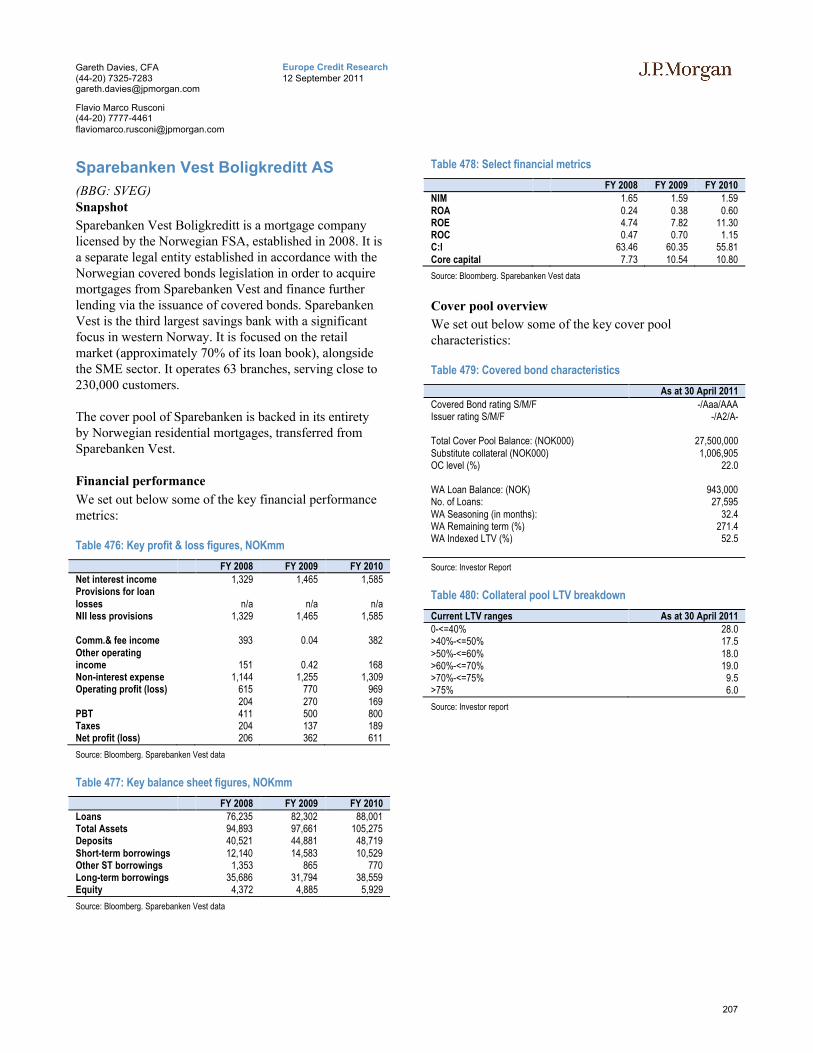

Sparebanken Vest Boligkreditt AS.......................................................................207

Terra Boligkreditt AS..........................................................................................208

Portuguese Covered Bonds ................................................210

Legislative snapshot ............................................................................................210

Portuguese covered bond & macro backdrop .......................................................211

Banco Comercial Portugues (‘Millennium bcp’) ..................................................212

Banco Espirito Santo (‘BES’)..............................................................................213

Banco Portugues de Investimento (‘BPI’) ............................................................214

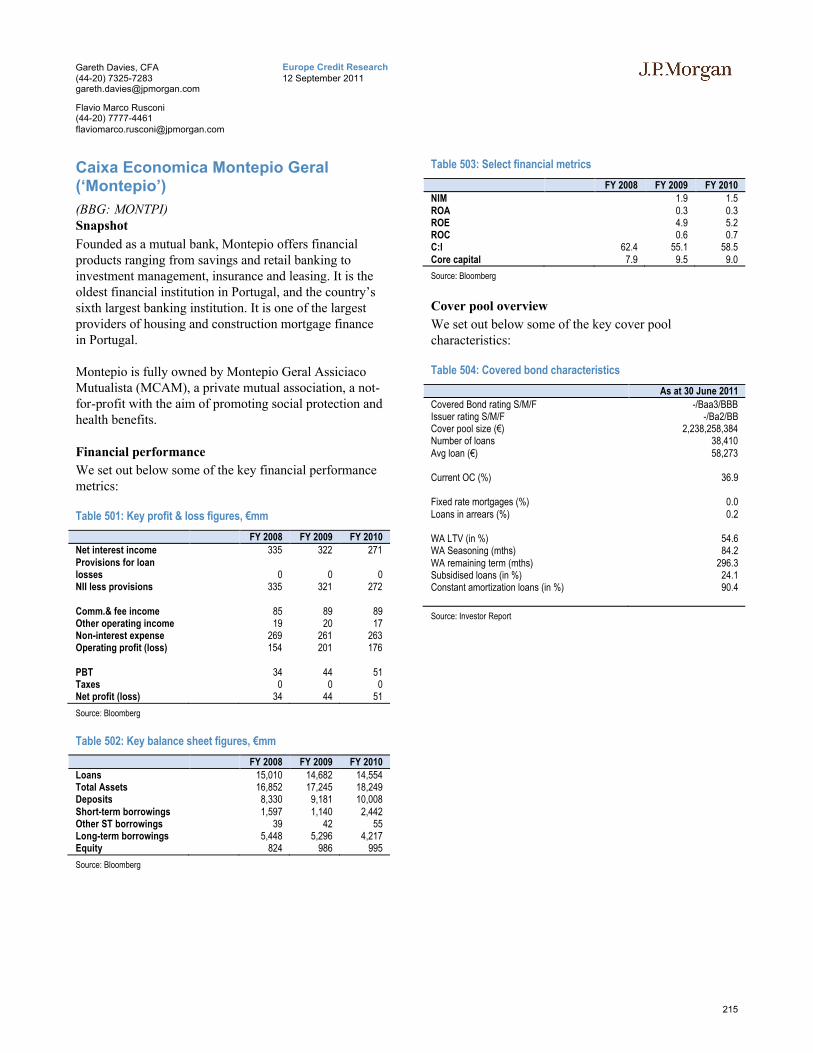

Caixa Economica Montepio Geral (‘Montepio’)...................................................215

Caixa Geral de Depositos (‘CGD’) ......................................................................216

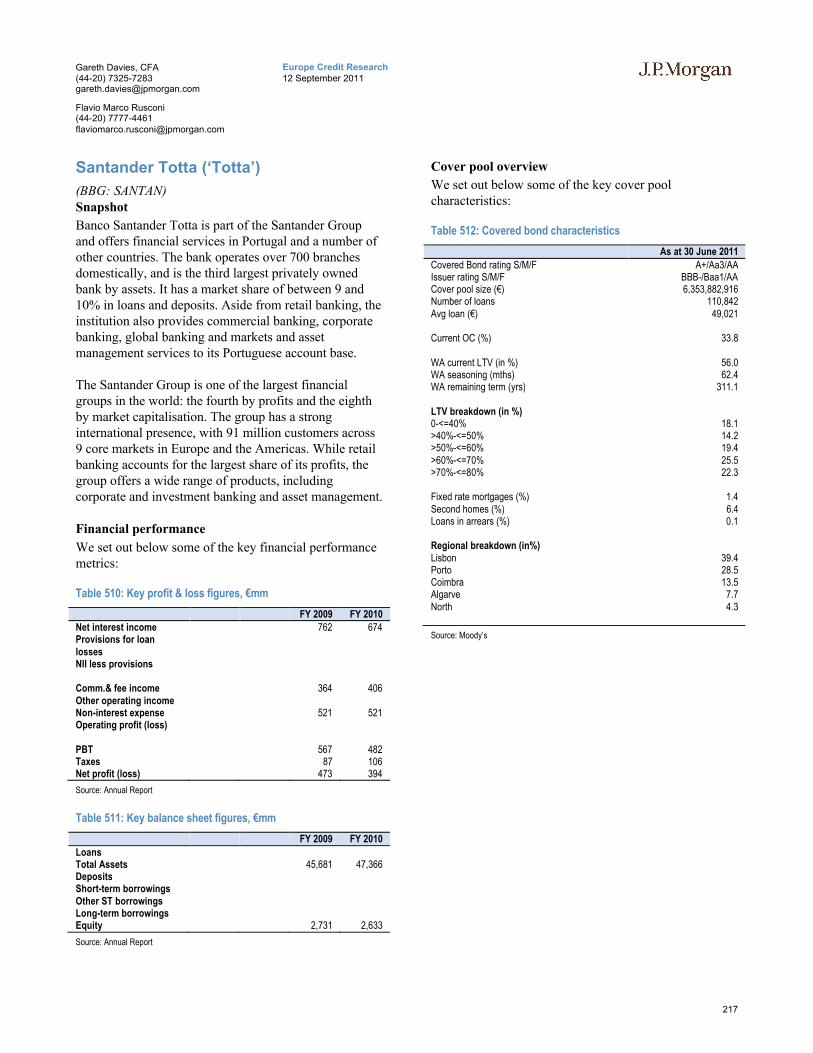

Santander Totta (‘Totta’) .....................................................................................217

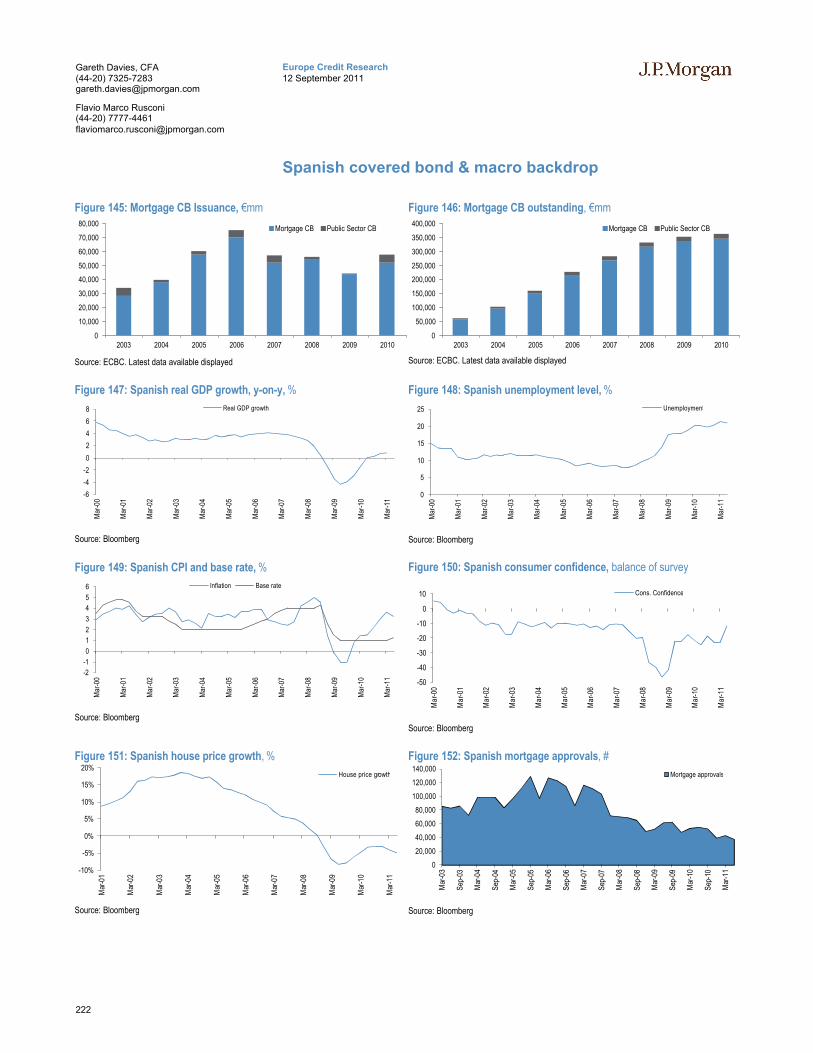

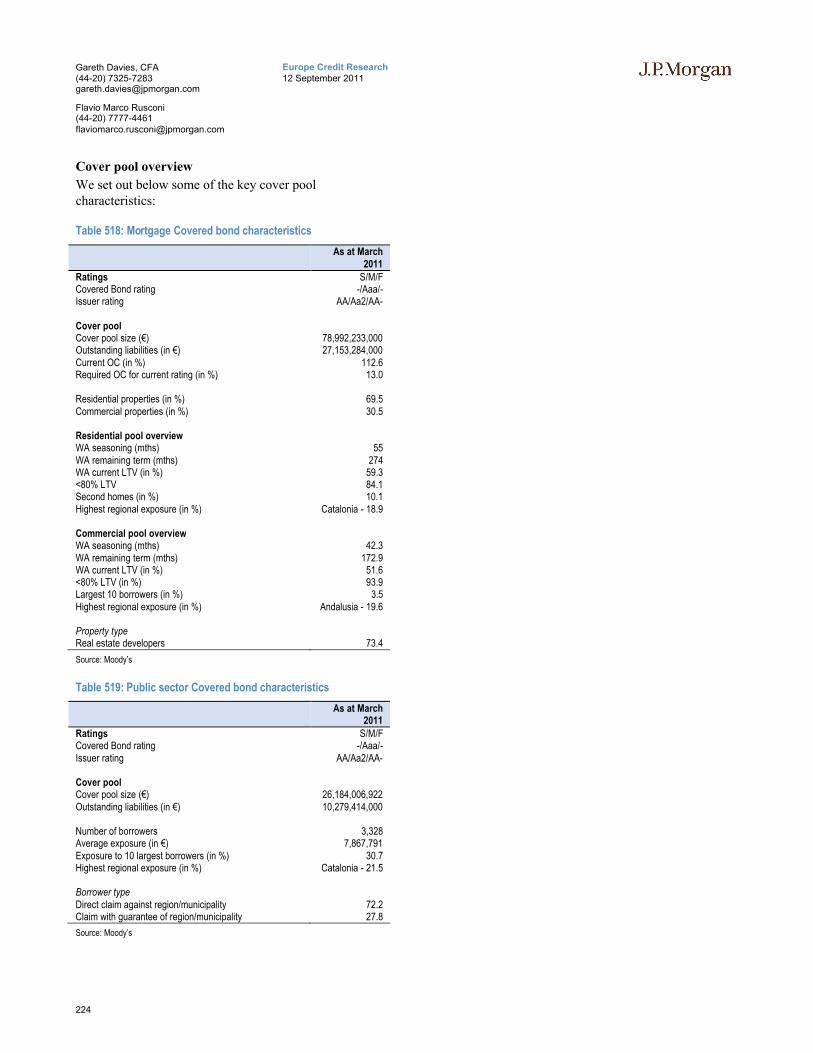

Spanish Covered Bonds ......................................................220

Legislative snapshot ............................................................................................220

7

Europe Credit Research12 September 2011

Gareth Davies, CFA(44-20) [email protected]

Flavio Marco Rusconi(44-20) [email protected]

Spanish covered bond & macro backdrop ............................................................222

Standalone programmes: .....................................................................................223

Banco Bilbao Vizcaya Argentina (‘BBVA’) ........................................................223

Banco CAM........................................................................................................225

Banco Espanol de Credito (‘Banesto’) .................................................................227

Banco Pastor .......................................................................................................228

Banco Popular Espanol........................................................................................230

Banco Sabadell ...................................................................................................232

Banco Santander .................................................................................................234

Bankia ................................................................................................................236

Bankinter ............................................................................................................238

Bilbao Bizkaia Kutxa (‘BBK’) ............................................................................240

Caixa d’Estalvis de Catalunya, Tarragona i Manresa (‘CatalunyaCaixa’)..............242

CaixaBank ..........................................................................................................244

Caja de Ahorros y Monte de Piedad de Guipúzcoa y San Sebastián (‘Kutxa’).......246

Caja Vital Kutxa .................................................................................................247

Cajamar Caja Rural .............................................................................................248

Ibercaja ...............................................................................................................250

Santander Consumer Finance ..............................................................................251

Unicaja ...............................................................................................................252

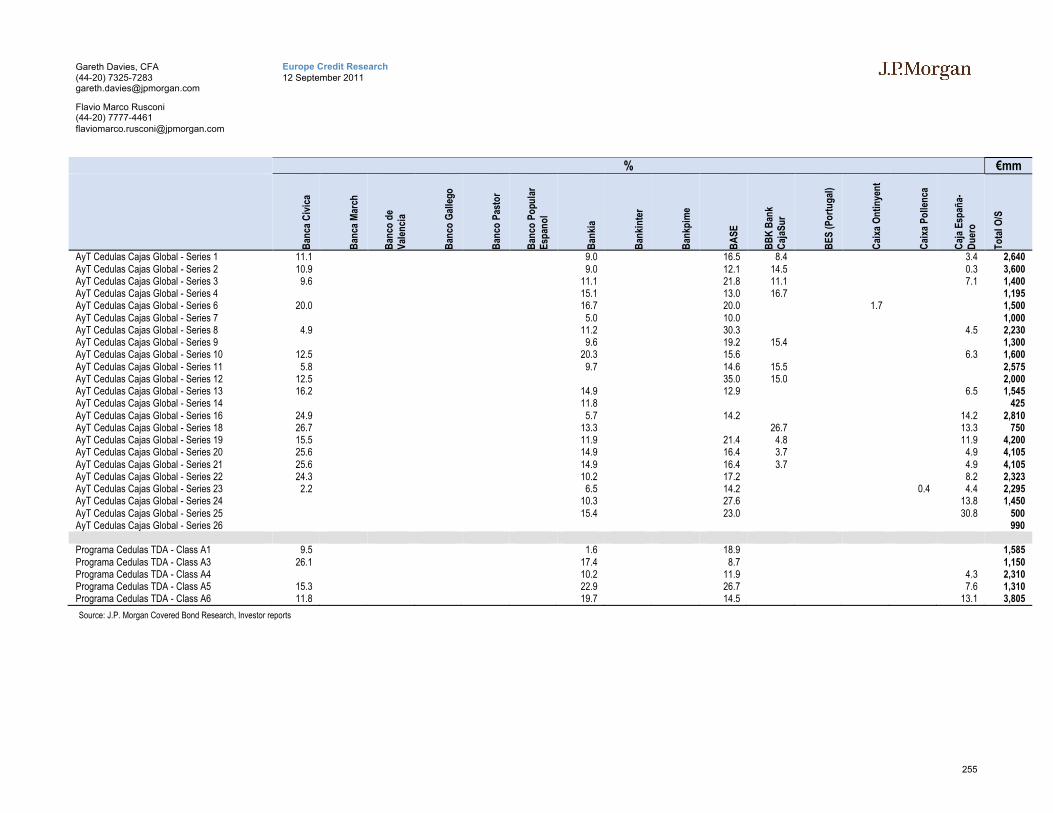

Multi-Cedulas .....................................................................................................253

Programmes........................................................................................................253

Swedish Covered Bonds .....................................................260

Legislative snapshot ............................................................................................260

Swedish covered bond & macro backdrop ...........................................................261

Landshypotek AB ...............................................................................................262

Länsförsäkringar Hypotek AB.............................................................................263

Nordea Hypotek AB............................................................................................264

Skandinaviska Enskilda Banken AB....................................................................265

Stadshypotek Mortgage AB.................................................................................266

Swedbank Mortgage AB .....................................................................................267

Swedish Covered Bond Corporation ....................................................................268

Swiss Covered Bonds..........................................................270

Legislative snapshot ............................................................................................270

Swiss covered bond backdrop..............................................................................271

Credit Suisse Group AG......................................................................................272

UBS AG .............................................................................................................273

UK Covered Bonds...............................................................276

Legislative snapshot ............................................................................................276

UK covered bond & macro backdrop...................................................................277

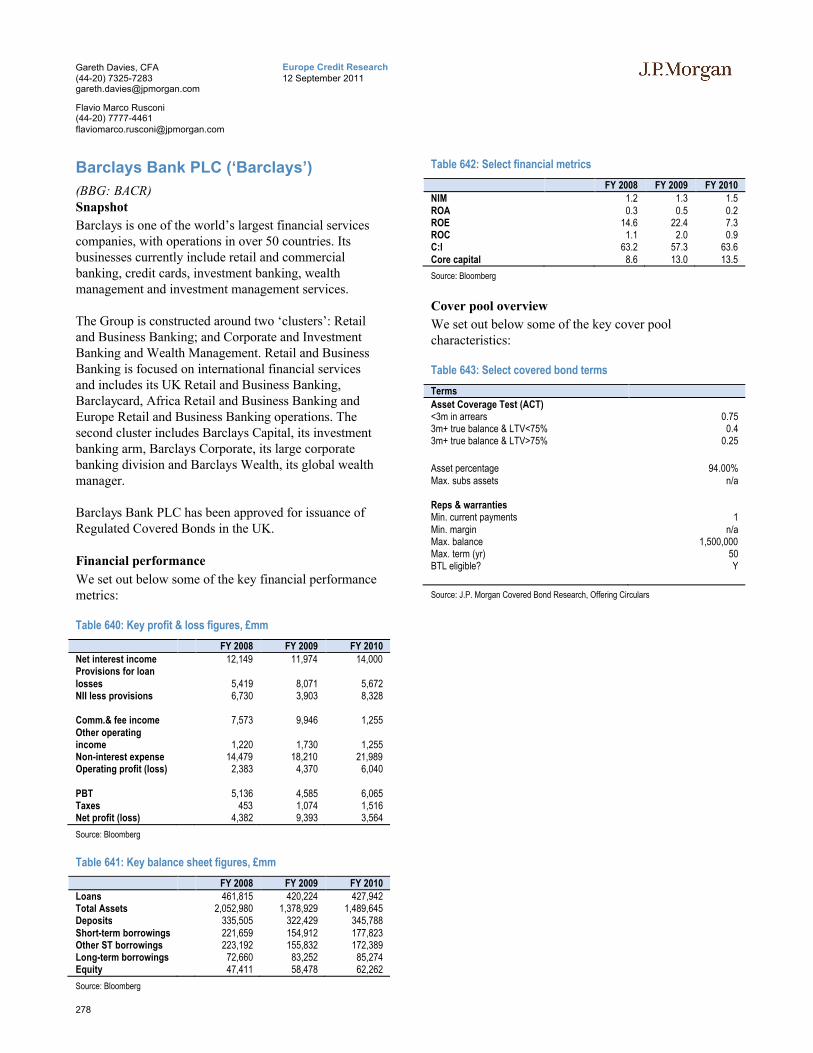

Barclays Bank PLC (‘Barclays’)..........................................................................278

Bradford & Bingley PLC (‘Bradbi’) ....................................................................280

Coventry Building Society (‘Coventry’) ..............................................................281

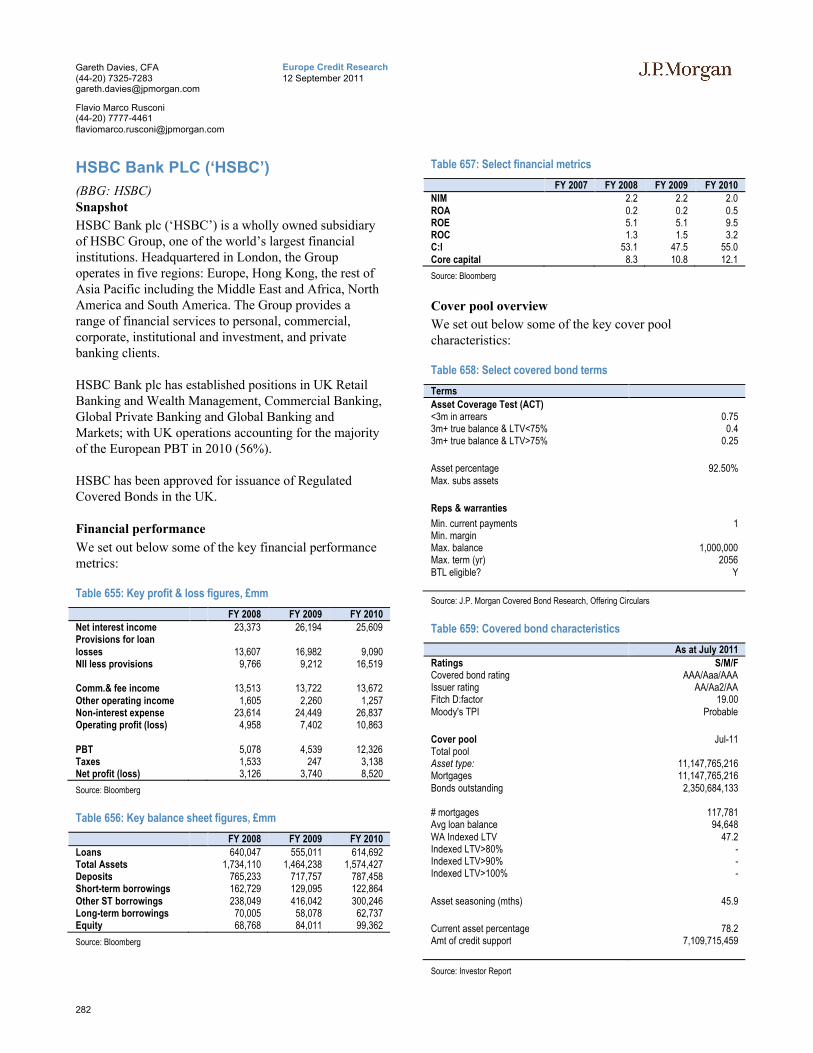

HSBC Bank PLC (‘HSBC’) ................................................................................282

Leeds Building Society (‘Leeds’).........................................................................283

8

Europe Credit Research12 September 2011

Gareth Davies, CFA(44-20) [email protected]

Flavio Marco Rusconi(44-20) [email protected]

Lloyds Banking Group PLC (‘Lloyds’)................................................................284

Nationwide Building Society (‘Nationwide’) .......................................................285

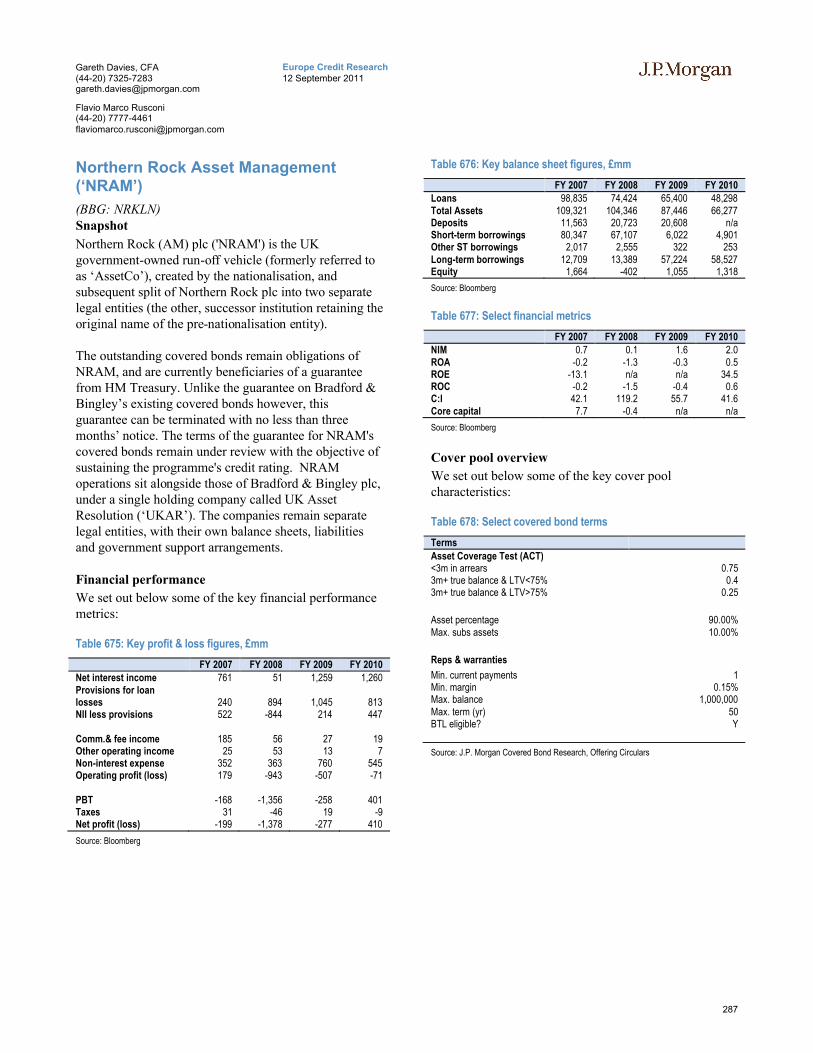

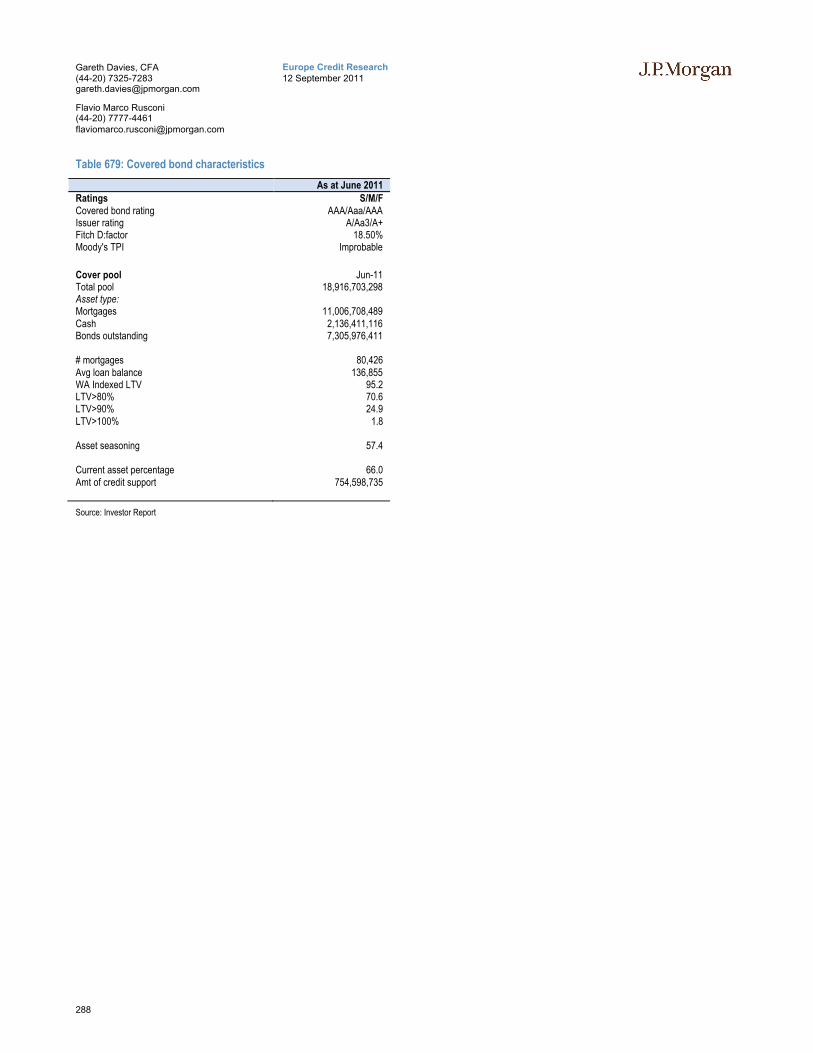

Northern Rock Asset Management (‘NRAM’) .....................................................287

Royal Bank of Scotland PLC (‘RBS’)..................................................................289

Santander UK plc (‘Santander’)...........................................................................291

Yorkshire Building Society (‘Yorkshire’) ............................................................293

US Covered Bonds...............................................................296

Legislative snapshot ............................................................................................296

US covered bond & macro backdrop ...................................................................297

Bank of America .................................................................................................298

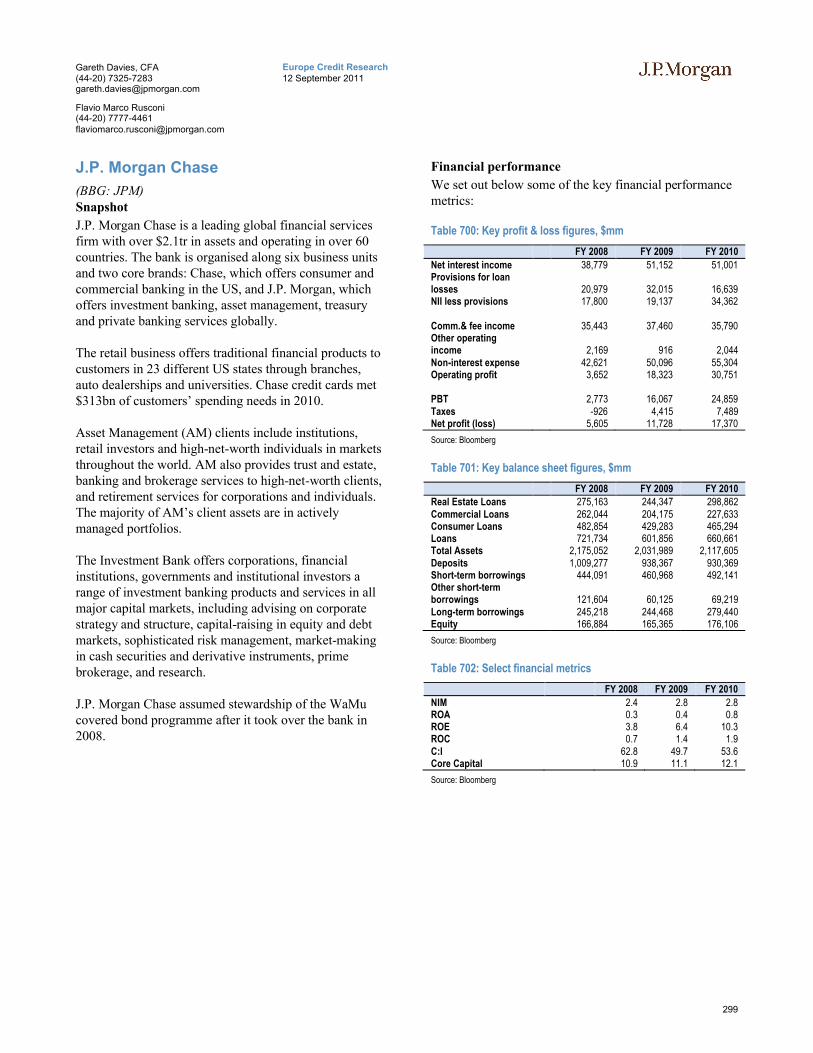

J.P. Morgan Chase ..............................................................................................299

9

Europe Credit Research12 September 2011

Gareth Davies, CFA(44-20) [email protected]

Flavio Marco Rusconi(44-20) [email protected]

Primary Market Outlook

The past twelve months–‘the boy done good'

Recent issuance trends

We have recorded benchmark covered bond issuance of €255bn to the 1st September (see Figure 1). This compares to full-year issuance of €276bn in 2010, or an increase of 31% over the comparable eight-month period last year. Even when considering that 2011 has seen a number of months with minimal levels of issuance owing to broad macro market dislocation (see Figure 2), it remains impressive that the amount issued in the ‘functioning’ 5 months has still exceeded 2010 levels.

Figure 1: Covered Bonds issuance, €mm

Source: Dealogic, J.P. Morgan Covered Bonds Research. Benchmark issuance only

Even when adjusting for newer issuance jurisdictions (in particular Canada where issuance volumes have picked up dramatically), we see 2011 levels comparing favourably to those of 2010. Looking further back to issuance volumes in 2007 as a representative ‘steady state’ year (i.e. pre credit crisis), total issuance amounts were approximately €200bn, showing significant progression in market size since 2007 (potentially by FY2011, +€100bn or +50% over four years).

Figure 2: Monthly Covered Bonds issuance, €mm

Source: Dealogic, J.P. Morgan Covered Bonds Research. Benchmark issuance only

Figure 3: Covered bonds outstanding, top 5 jurisdictions, €mm

Source: ECBC. All issuance

Issuance–digging a little deeper

Breaking the aggregate issuance figures down into 'tiers' of countries, we take as a starting point the classifications proposed in 2010’s Handbook, with the caveat of a few ‘jurisdictional switches’ (we redesignate the ‘Peripheral’ category which previously contained only smaller issuance markets in 2010, as now including markets affected by the European sovereign crisis. We switch the smaller countries into the ‘Outer Core’ grouping). Our amended classifications are set as follows:

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

2007 2008 2009 2010 2011 YTD

Cov. Bonds (Not retained)

0

10,000

20,000

30,000

40,000

50,000

60,000

Oct

-10

Nov

-10

Dec

-10

Jan-

11

Feb

-11

Mar

-11

Apr

-11

May

-11

Jun-

11

Jul-1

1

Aug

-11

Sep

-11

0

300,000

600,000

900,000

1,200,000

1,500,000

1,800,000

2,100,000

2,400,000

2,700,000

2003 2004 2005 2006 2007 2008 2009 2010

Germany Spain Denmark France Sweden Other

Covered bond issuance

continues to expand its role in funding the world's banks

10

Europe Credit Research12 September 2011

Gareth Davies, CFA(44-20) [email protected]

Flavio Marco Rusconi(44-20) [email protected]

‘Inner core’ jurisdictionsThree jurisdictions jump to the fore when considering the longest-standing and most established covered bond markets: Denmark, France and Germany. Most covered bonds issued out of these jurisdictions offer a greater degree of liquidity and are supported by a strong domestic investor base.

These bonds tend to price the tightest in the new issue market. Individual issuer credit risk is often perceived to be of less importance in these markets owing to the systemic importance of the product to the respective jurisdiction.

‘Outer core’ jurisdictionsThis classification includes all other Western European jurisdictions along with jurisdictions recently joining or about to join the covered bond community, including Canada, Korea, New Zealand and the US.

Peripheral jurisdictionsWe aggregate exposures to those markets most affected by the European sovereign crisis: Greece, Ireland, Italy, Portugal and Spain.

Figure 4: Issuance volumes by country tier, €mm

Source: J.P. Morgan Covered Bonds Research. Benchmark issuance only

Turning first to the ‘Inner core’ we see that issuance over time has been consistently increasing out of France, with Danish issuers mostly active on the domestic, non-benchmark DKK market (see Figure 5). Significantly, the issuance of public-sector backed pfandbrief has fallen over time–exacerbating a trend that started pre-2007 and driving the German contribution to annual issuance down to just €45bn in 2010 vs €102bn in 2008.

0

50,000

100,000

150,000

200,000

2008 2009 2010 2011 YTD

Inner core Outer core Periphery

‘Traditional’ issuance jurisdictions have become less

prolific issuers

11

Europe Credit Research12 September 2011

Gareth Davies, CFA(44-20) [email protected]

Flavio Marco Rusconi(44-20) [email protected]

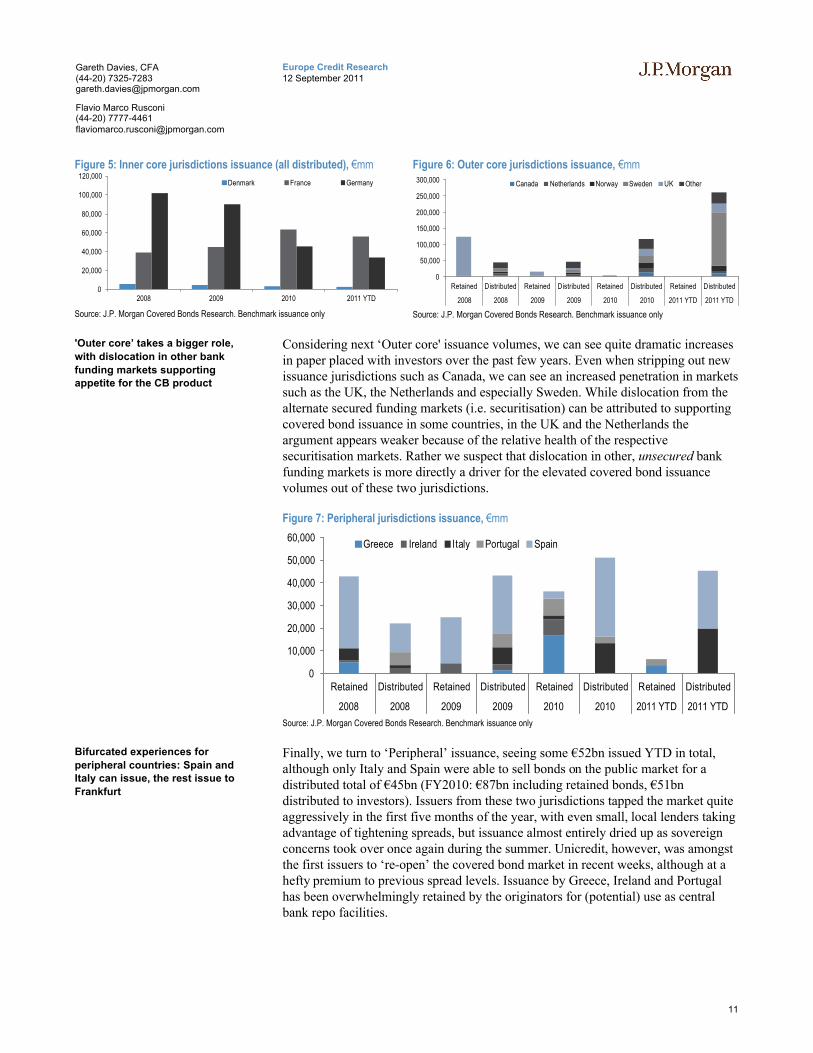

Figure 5: Inner core jurisdictions issuance (all distributed), €mm

Source: J.P. Morgan Covered Bonds Research. Benchmark issuance only

Figure 6: Outer core jurisdictions issuance, €mm

Source: J.P. Morgan Covered Bonds Research. Benchmark issuance only

Considering next ‘Outer core' issuance volumes, we can see quite dramatic increases in paper placed with investors over the past few years. Even when stripping out new issuance jurisdictions such as Canada, we can see an increased penetration in markets such as the UK, the Netherlands and especially Sweden. While dislocation from the alternate secured funding markets (i.e. securitisation) can be attributed to supporting covered bond issuance in some countries, in the UK and the Netherlands the argument appears weaker because of the relative health of the respective securitisation markets. Rather we suspect that dislocation in other, unsecured bank funding markets is more directly a driver for the elevated covered bond issuance volumes out of these two jurisdictions.

Figure 7: Peripheral jurisdictions issuance, €mm

Source: J.P. Morgan Covered Bonds Research. Benchmark issuance only

Finally, we turn to ‘Peripheral’ issuance, seeing some €52bn issued YTD in total, although only Italy and Spain were able to sell bonds on the public market for a distributed total of €45bn (FY2010: €87bn including retained bonds, €51bn distributed to investors). Issuers from these two jurisdictions tapped the market quite aggressively in the first five months of the year, with even small, local lenders taking advantage of tightening spreads, but issuance almost entirely dried up as sovereign concerns took over once again during the summer. Unicredit, however, was amongst the first issuers to ‘re-open’ the covered bond market in recent weeks, although at a hefty premium to previous spread levels. Issuance by Greece, Ireland and Portugal has been overwhelmingly retained by the originators for (potential) use as central bank repo facilities.

0

20,000

40,000

60,000

80,000

100,000

120,000

2008 2009 2010 2011 YTD

Denmark France Germany

0

50,000

100,000

150,000

200,000

250,000

300,000

Retained Distributed Retained Distributed Retained Distributed Retained Distributed

2008 2008 2009 2009 2010 2010 2011 YTD 2011 YTD

Canada Netherlands Norway Sweden UK Other

0

10,000

20,000

30,000

40,000

50,000

60,000

Retained Distributed Retained Distributed Retained Distributed Retained Distributed

2008 2008 2009 2009 2010 2010 2011 YTD 2011 YTD

Greece Ireland Italy Portugal Spain

'Outer core’ takes a bigger role,

with dislocation in other bank

funding markets supporting appetite for the CB product

Bifurcated experiences for

peripheral countries: Spain and Italy can issue, the rest issue to

Frankfurt

12

Europe Credit Research12 September 2011

Gareth Davies, CFA(44-20) [email protected]

Flavio Marco Rusconi(44-20) [email protected]

Pricing patterns: it’s all in the brand

Launch spreads and origination patterns give a clear indication of the ability of issuers from each jurisdictional tier to access the market. Issuers from the ‘Inner core’ jurisdictions appear able to tap the market at virtually any time, regardless of periods of broad market volatility (Figure 8). Furthermore, as shown for France, within-jurisdiction tiering seems to be primarily driven by bond maturity, rather than by the issuer itself (more akin to a ‘rates perspective’).

‘Outer core’ jurisdictions offer a more diverse mix. Certain jurisdictions, such as the Nordics, display a pattern closer to that of ‘Inner core’ ones, while others, such as the UK, do not seem to be able to brave the markets on their own and often come to the market in clusters. Furthermore, in the UK, launch spreads seem to be primarily driven by issuer name, rather than by maturity: some of the smaller building societies have to offer wider spreads than those paid by the larger banks, regardless of maturity (a ‘credit’ perspective). Interestingly, Santander UK also appears to price wider than other more ‘domestic' names.

Figure 8: French launch spreads vs MS, bp

Source: J.P. Morgan Covered Bonds Research. Benchmark issuance only

Figure 9: UK launch spreads vs MS, bp

Source: J.P. Morgan Covered Bonds Research. Benchmark issuance only

The ‘open-closed’ pattern seen in the UK is even more in evidence in the peripheral countries, where issuers are particularly sensitive to the tone of the broader market. Both Spanish and Italian issuers have taken advantage of the window of opportunity offered by the relative calm on the sovereign front earlier in the year and issuers of all sizes and shapes came to the market. There is also very little differentiation in terms of maturity, but there is a significant gap between spreads offered by large, more established financial institutions and smaller, regional lenders. In Spain in particular, issuers such as BBVA or Santander are able to pay much tighter spreads on longer maturity bonds than those paid by the savings banks (Figure 11) as an example.

Figure 10: Italian launch spreads vs MS, bp

Source: J.P. Morgan Covered Bonds Research. Benchmark issuance only

Figure 11: Spanish launch spreads vs MS, bp

Source: J.P. Morgan Covered Bonds Research. Benchmark issuance only

0

20

40

60

80

100

Sep

-10

Sep

-10

Oct

-10

Oct

-10

Nov

-10

Nov

-10

Dec

-10

Dec

-10

Dec

-10

Jan-

11

Jan-

11

Feb

-11

Feb

-11

Mar

-11

Mar

-11

Apr

-11

Apr

-11

May

-11

May

-11

Jun-

11

Jun-

11

Jun-

11

Jul-1

1

Jul-1

1

Aug

-11

Aug

-11

Sep

-11

<3yrs 3-5yrs 5-7yrs 7-10yrs >10yrs0

50

100

150

200

Sep

-10

Sep

-10

Oct

-10

Oct

-10

Nov

-10

Nov

-10

Dec

-10

Dec

-10

Dec

-10

Jan-

11

Jan-

11

Feb

-11

Feb

-11

Mar

-11

Mar

-11

Apr

-11

Apr

-11

May

-11

May

-11

Jun-

11

Jun-

11

Jun-

11

Jul-1

1

Jul-1

1

Aug

-11

Aug

-11

Sep

-11

<3yrs 3-5yrs 5-7yrs 7-10yrs >10yrs

0

50

100

150

200

250

Sep

-10

Sep

-10

Oct

-10

Oct

-10

Nov

-10

Nov

-10

Dec

-10

Dec

-10

Dec

-10

Jan-

11

Jan-

11

Feb

-11

Feb

-11

Mar

-11

Mar

-11

Apr

-11

Apr

-11

May

-11

May

-11

Jun-

11

Jun-

11

Jun-

11

Jul-1

1

Jul-1

1

Aug

-11

Aug

-11

<3yrs 3-5yrs 5-7yrs 7-10yrs >10yrs

0

50

100

150

200

250

300

350

Sep

-10

Sep

-10

Oct

-10

Oct

-10

Nov

-10

Nov

-10

Nov

-10

Dec

-10

Dec

-10

Jan-

11

Jan-

11

Feb

-11

Feb

-11

Mar

-11

Mar

-11

Apr

-11

Apr

-11

May

-11

May

-11

May

-11

Jun-

11

Jun-

11

Jul-1

1

Jul-1

1

Aug

-11

Aug

-11

<3yrs 3-5yrs 5-7yrs 7-10yrs >10yrs

Inner core jurisdictions look to have market access even in

periods of volatility

The most ‘credit-linked’ jurisdictions appear to have

more occasional market access

13

Europe Credit Research12 September 2011

Gareth Davies, CFA(44-20) [email protected]

Flavio Marco Rusconi(44-20) [email protected]

How does this compare to the performance of other bank funding instruments?

As we have noted above, covered bond issuance volumes have shown significant progression over the past four years. In Figure 12 below we set out the issuance volumes of two equally important bank funding instruments to see whether the absolute success of covered bonds is also observable in relative terms.

Figure 12: ABS, Senior Unsecured, Covered Bonds issuance, €mm

Source: J.P. Morgan Covered Bonds Research. Benchmark issuance only

Readers can clearly see that while covered bond issuance has gone from strength to strength over the period in question, the two largest alternative bank funding sources have recorded significant declines in issuance. Turning to each separately, we have seen senior unsecured issuance volumes decline from €264bn in 2007, to €159bn in 2010 (and €127bn YTD 2011). Undoubtedly some of this decline can be attributed to an investor aversion to specific issuers or jurisdictions, but equally important in our view has been the uncertainty created by proposed regulatory initiatives surrounding the senior unsecured product itself. We note that the proposed adoption of explicit bail-in language for senior unsecured bonds from 2013 has undermined investor confidence in the risk profile of the instrument. While this uncertainty persists, investors will naturally demand additional compensation for the perceived additional risk, making economically feasible senior unsecured issuance out of the reach of most (European) issuers.

Turning to the securitisation market, we see a dramatic change in issuance volumes following the onset of the credit crunch, with €325bn of bonds placed with investors in the first eight months of 2007, compared to €51bn over the same period in 2011. Furthermore, there has been a significant divergence in the fortunes of individual issuing jurisdictions, with the UK and the Netherlands (and to a lesser extent, Italy) able to access the distributed RMBS markets at regular intervals, while other countries have been frozen out of the market owing to the basis between current asset spreads and required liability costs. Furthermore, as we noted in last year’s Handbook, the regulatory environment for both securitisation issuance and investment has been tightened since 2007 from a myriad of sources (CRD III, IV, BIS Liquidity Regime, Solvency II etc). Much as for senior unsecured debt, this has undoubtedly skewed the landscape in favour of covered bonds.

As we noted in our introduction, we remain aware of potential roadbumps in the medium-term outlook for the asset class (as credit analysts the glass is always half empty), seeing the developing regulatory regime as skewing the incentives in favour of covered bonds to such a degree, that it is damaging the diversity of alternate bank funding opportunities, and by derivation, potentially harming the ability of today’s covered product to grow at a more measured and sustainable pace.

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

2007 2008 2009 2010 2011 YTD

ABS (Not retained) Snr unsec. Cov. Bonds (Not retained)

Covered bonds do well both absolutely and relatively

Uncertainty as to the risk profile of senior unsecured debt has

translated into additional supply

of covered bonds

Securitisation markets remain open for Northern European

issuers, but regulatory initiatives

have also altered the incentives in these markets

Regulatory backdrop could put too much pressure on the asset

class

14

Europe Credit Research12 September 2011

Gareth Davies, CFA(44-20) [email protected]

Flavio Marco Rusconi(44-20) [email protected]

The next twelve months–Magic 8 ball time

We are either brave or foolish to try and predict the next twelve months, recognising the close link between sentiment for covered bonds and that for financial and government risk more broadly. Letting the reader decide which is the more appropriate interpretation, we set out our thoughts on the next 12 months below:

Who is going to be doing what?

From the issuer perspective, we expect the ‘Inner core’ jurisdictions to be relatively unaffected by the vagaries of peripheral crisis (barring a significant event). Danish, German and French issuers are likely to be able to continue accessing the markets relatively uninterrupted, albeit with potentially wider access points in particular for French issuers, where sentiment appears less resilient to continued sovereign crisis uncertainty.

For 'Outer core' countries, we see a number of subsets in expected ability to access the markets. For the Scandinavian issuers, we would expect them to be able to access both the Euro and Dollar markets (largely US, but also AUD) broadly uninterrupted over the course of the next twelve months (assuming the same caveat as above). For the UK and Netherlands, we continue to expect to see a greater reliance on the covered product – less as an alternative to RMBS, which still remains a functioning market in both jurisdictions, but more likely as an alternative to senior unsecured issuance. For non-European issuers, including Canadian, New Zealand and (shortly) Australian institutions, we expect to see ever increasing issuance predominantly targeted at the domestic or quasi-domestic markets.

For peripheral countries, we need to split the group into two: those already in the epicentre of the sovereign storm (Greece, Ireland and Portugal) and those one or two steps removed (Italy and Spain). Somewhat perversely, the outlook for issuance from Greece, Ireland and Portugal is easier to communicate, with our hypothesis that we will see no distributed issuance from any of the three jurisdictions for the foreseeable future. For Italy and Spain, we can adopt the same approach, seeing 'national champions' as able to fund over the majority of the year, alongside smaller players being able to fund only in times of market stability.

From the investor perspective, we expect to see a continuation of recent trends with respect to investor engagement. If we bifurcate the investor base into traditional 'rates' and newer 'credit' investors, we would expect the rates subset to show a larger appetite in terms of notionals from broadly the same number of accounts, driven largely by regulatory incentives (particularly Solvency II). In comparison, for credit investors we would expect both the breadth, in terms of number of accounts, and depth, in terms of the willingness of these accounts to invest in the covered asset class, to continue to expand over the course of the next twelve months.

In aggregate, with forecast total benchmark issuance of approximately €300bn for FY2011, it would not seem outlandish to expect between €325-350bn in FY2012 given continued dislocation in alternative bank funding sources and an expanding international footprint for the product.

‘Inner core’ and colder ‘Outer core’ countries to have almost

uninterrupted access to covered

bond funding

Wetter ‘Outer core’ countries to rely more on CB as a

replacement for senior

unsecured bonds, with Commonwealth countries

relying more on investors closer

to home

No market access for those at the centre of the peripheral

storm, occasional access for

those one or two steps away

More investors expected

15

Europe Credit Research12 September 2011

Gareth Davies, CFA(44-20) [email protected]

Flavio Marco Rusconi(44-20) [email protected]

Secondary Market Outlook

The last twelve months–Vow to thee, my country

After stabilising in the second half of 2010 and actually seeing some tightening in the opening months of 2011 as sovereign concerns initially subsided, covered bond spreads succumbed to broader financial market deterioration as the peripheral saga continued to play out in front of the market’s eyes. Despite the absolute widening evident in many jurisdictions, covered bonds as an asset class have significantly outperformed the broader ‘financials’ sector (Figure 13), although some of the more liquid RMBS asset classes, such as UK prime RMBS, have proved to be even more resilient in price terms.

Figure 13: Cross-asset class spreads comparison, bp

Source: J.P. Morgan Covered Bonds Research

Figure 14: Selected Covered Bond spreads, bp

Source: J.P. Morgan Covered Bonds Research

Understandably, not all covered bonds were affected in the same way by the sovereign headwinds: while French, German and UK spreads proved relatively resilient and widened only modestly during the latest bout of volatility, Spanish prices have been a lot more sensitive to the mood swings of the wider market. Figure 14 shows how these have spiked initially in May-June 2010, during the first Greek crisis, then again in December 2010-January 2011, on the back of the Irish crisis and finally resumed rising in June 2011, when sovereign concerns spread to Spain itself along with Italy.

The different relationship between covered bond spread performance and trends in broader market sentiment in the various jurisdictions is perhaps more clear in the charts below. We compare sovereign CDS, used as a measure of stress on a specific jurisdiction, with senior unsecured and covered bond spreads from selected issuers in those countries.

In Germany (Figure 15), covered bonds are clearly the most resilient of all asset classes considered, even more so than sovereign CDS, which has gapped wider over the summer months.

0

50

100

150

200

250

300

Jan-

10

Feb

-10

Mar

-10

Apr

-10

May

-10

Jun-

10

Jul-1

0

Aug

-10

Sep

-10

Oct

-10

Nov

-10

Dec

-10

Jan-

11

Feb

-11

Mar

-11

Apr

-11

May

-11

Jun-

11

Jul-1

1

Aug

-11

Sep

-11

iTraxx Europe Senior Fin. 5yrs JPM Maggie CB 3 - 5 Yr

UK RMBS AAA Euro FL 5 Yr

0

50

100

150

200

250

300

350

Jan-

10

Feb

-10

Mar

-10

Apr

-10

May

-10

Jun-

10

Jul-1

0

Aug

-10

Sep

-10

Oct

-10

Nov

-10

Dec

-10

Jan-

11

Feb

-11

Mar

-11

Apr

-11

May

-11

Jun-

11

Jul-1

1

Aug

-11

Sep

-11

France CB 3 - 5 Years Germany CB 3 - 5 Years

UK CB 3 - 5 Years Spain CB 3 - 5 Yr

Although wider, not as wide as other instruments

Tiered price performance for

those jurisdictions with feet ‘closest to the fire’

Pfandbrief appear more

defensive than even the sovereign

16

Europe Credit Research12 September 2011

Gareth Davies, CFA(44-20) [email protected]

Flavio Marco Rusconi(44-20) [email protected]

Figure 15: German CDS, Senior unsecured and Covered bond spreads, bp

Source: Bloomberg

Figure 16: UK CDS, Senior unsecured and Covered bond spreads, bp

Source: Bloomberg

Similarly, in the UK, covered bond spreads have remained broadly stable (Figure 16), whereas senior unsecured prices have significantly widened whilst even the sovereign CDS has come under pressure, although by a lesser degree than elsewhere in Europe.

In Italy and Spain, on the other hand, there is a much closer link between the various asset classes, with CDS, senior unsecured and covered spreads moving more or less in unison. Interestingly, in Italy and even more so in Spain, the traditionally tight differential between senior unsecured and covered bonds seems to have widened significantly over the recent months, perhaps suggesting that investors have started better appreciating the extra layer of security offered by the cover pool.

Figure 17: Italian CDS, Senior unsecured and Covered bond spreads, bp

Source: Bloomberg

Figure 18: Spanish CDS, Senior unsecured and Covered bond spreads, bp

Source: Bloomberg

And another thing…The close links between sovereign, issuer and the covered bond spread are also reflected in the ratings of the three instruments (see later Rating Agency section for an explicit explanation of the relationships), which in turn often have a second order consequence on the pricing of the covered instrument (as in, the lower the rating, the lower the price). While Figure 19 sets out the average covered bond rating by jurisdiction according to data from S&P, Figure 20 shows the direct impact that the rating of the sovereign (and in turn on the domestic banks) can have on the ratings of outstanding covered bond programmes.

-20

0

20

40

60

80

100

120

140

160

Jan-

10

Feb

-10

Mar

-10

Apr

-10

May

-10

Jun-

10

Jul-1

0

Aug

-10

Sep

-10

Oct

-10

Nov

-10

Dec

-10

Jan-

11

Feb

-11

Mar

-11

Apr

-11

May

-11

Jun-

11

Jul-1

1

Aug

-11

Deutsche Bank CB 2016 Deutsche Bank Snr. Unsec. 2017

Germany 5yrs CDS

0

50

100

150

200

250

300

350

400

Jan-

10

Feb

-10

Mar

-10

Apr

-10

May

-…

Jun-

10

Jul-1

0

Aug

-10

Sep

-10

Oct

-10

Nov

-10

Dec

-10

Jan-

11

Feb

-11

Mar

-11

Apr

-11

May

-…

Jun-

11

Jul-1

1

Aug

-11

BoS CB 2016 Lloyds Snr. Unsec. 2016 UK 5yrs CDS

0

100

200

300

400

500

Jan-

10

Feb

-10

Mar

-10

Apr

-10

May

-10

Jun-

10

Jul-1

0

Aug

-10

Sep

-10

Oct

-10

Nov

-10

Dec

-10

Jan-

11

Feb

-11

Mar

-11

Apr

-11

May

-11

Jun-

11

Jul-1

1

Aug

-11

Sep

-11

Intesa CB 2017 Intes Sen. Unsec. 2017 Italy 5yrs CDS

0

100

200

300

400

500

Jan-

10

Feb

-10

Mar

-10

Apr

-10

May

-…

Jun-

10

Jul-1

0

Aug

-10

Sep

-10

Oct

-10

Nov

-10

Dec

-10

Jan-

11

Feb

-11

Mar

-11

Apr

-11

May

-…

Jun-

11

Jul-1

1

Aug

-11

Sep

-11

BBVA CB 2016 BBVA Sen. Unsec. 2015 Spain 5yrs CDS

Close relationship between

government, bank and covered

debt in peripheral markets

17

Europe Credit Research12 September 2011

Gareth Davies, CFA(44-20) [email protected]

Flavio Marco Rusconi(44-20) [email protected]

Figure 19: Average covered bond and issuer rating by country

Source: Standard & Poor’s

Figure 20: Average unused notches and maximum number of notches uplift, #

Source: Standard & Poor’s

Most visibly, we see that those countries most affected by the sovereign crisis (Portugal and Ireland in this particular universe) also have the least ‘headroom’ between any future potential issuer/sovereign downgrades and a direct, second-order impact on the rating of covered bonds in the jurisdiction.

The next twelve months–More of the same

Who is going to be doing what?

In thinking about likely secondary spread trajectories over the coming months, we adopt the same caveat we used when thinking about issuance volumes–i.e. barring any significant event in the sovereign space. Assuming this, we actually expect the current price tiering relationships to remain broadly intact.

By that we mean we would expect to see ‘Inner core’ jurisdictions along with Scandinavian paper to remain broadly unchallenged, offering investors liquidity, but also a less generous pick-up to sovereigns. We would envisage that investors into these asset classes would therefore remain predominantly made up of the more traditional investor base, along with those 'credit like' accounts who are perhaps either new to the asset class and deploying a strategy of slowly building their experience in the sector, or those seeking refuge from the sovereign crisis. If there are any areas of potential technical weakness in this category, we could expect to see French spreads underperform relative to other jurisdictions in this grouping.

For jurisdictions in the ‘middle of the pack’ in spread terms, we would expect increased supply (see earlier section) to be broadly offset by increased client engagement as alternative instruments undershoot in terms of issuance volumes. The UK would be a prime example of this in our opinion, where both ‘traditional’ and ‘new’ investors participate alongside one another. Similarly, Tier One Spanish and Italian names are likely to find the same pockets of interest from both sides of the aisle.

For paper from the distressed jurisdictions of Greece, Ireland and Portugal we would expect to see faster money continue to focus their attention. While we undoubtedly see opportunities to add risk in these segments, the potential for further downgrades (to below investment grade) is likely to mitigate the interest of more 'permanent' covered bond investors, potentially leaving these instruments as longer term investments for anyone who adds positions as opposed to ‘trading assets’.

910111213141516171819

FIN

FR

A

CA

N

DE

N

NLD

NO

R

SP

A

GE

R

ITA

SW

E

UK

LUX

US

IRE

PO

R

Average covered bond rating

Average issuer credit ratingAAAAA+AAAA-A+AA-BBB+BBBBBB-BB+

0

2

4

6

8

US

PO

R UK

LUX

IRE

ITA

NLD

NO

R

CA

N

FIN

SP

A

FR

A

SW

E

GE

R

DE

N

Average of uplift (notches) usedAverage of unused notchesMaximum number of notches uplift (for low ALMM classification)

18

Europe Credit Research12 September 2011

Gareth Davies, CFA(44-20) [email protected]

Flavio Marco Rusconi(44-20) [email protected]

Our covered bond recommendations

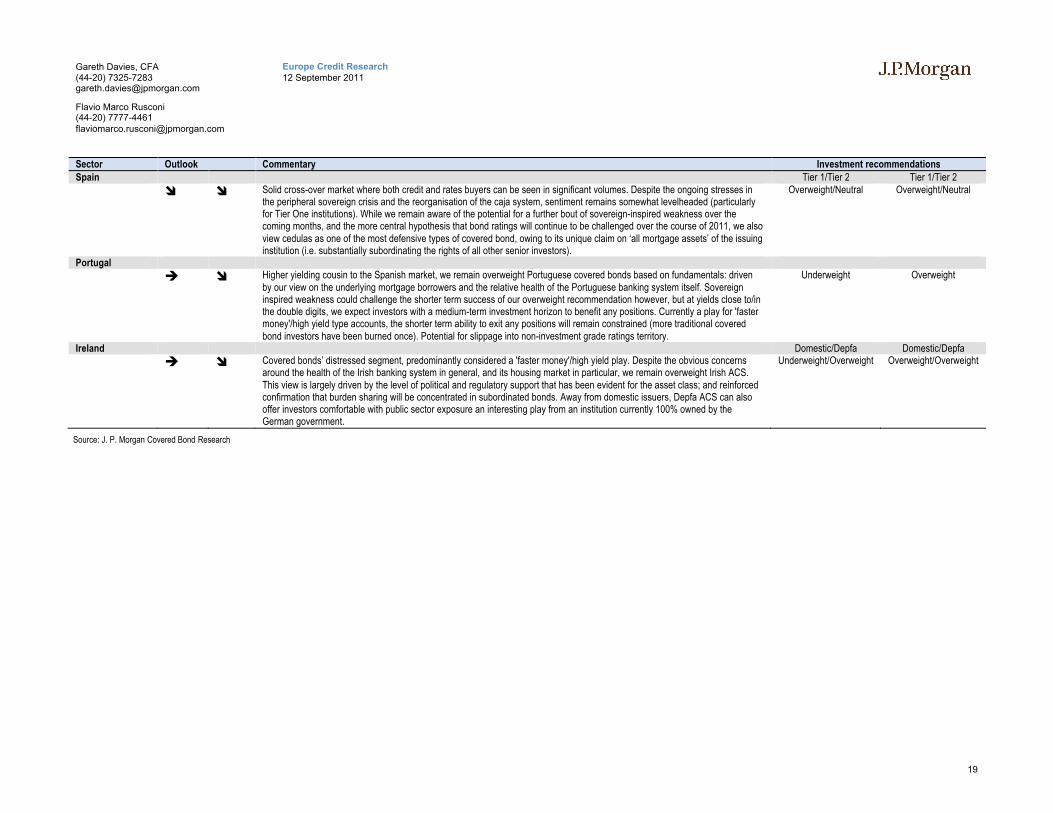

Table 1: Selected Covered Bond recommendations by jurisdiction

Sector Outlook Commentary Investment recommendations

Germany Technical Fundamentals ‘Rates’ perspective ‘Credit’ perspective

The core jurisdiction in the European CB market. Overwhelmingly a “rates buyer” market, and owing to the relatively tight levels of pfandbrief will offer little interest to a credit investor unless liquidity (or the perception of liquidity) is the over-arching driver of investment). Significant redemptions of bonds (particularly public sector backed outstandings) combined with a loyal investor base will likely support pfandbrief levels, despite our view that investors are not being compensated appropriately for the credit risk assumed in the underlying pools.

Neutral Underweight

France

The ‘second’ internationally active market in Europe, with a combination of both ‘legislative’ and ‘structured’ (although now also legislative) products available to investors (OF or OH). While supply has been elevated during the past twelve months, spreads have been relatively resilient. Generically we prefer OH to OF based on our preference for mortgage assets over public sectorexposures, compounded by the typical premium which OH bonds tend to come at in relation to OFs. Furthermore, we would expect OH bonds to perform better than OF bonds over the next few months, owing to some accounts approaching line limits on the more frequent OF names.

Underweight Underweight

Scandinavia

Solidly performing covered markets, with few 'credit' concerns with respect to sovereign or issuer strength. Has benefitted in spread terms both from the addition of northern European demand to the domestic investor base, along with the tapping of overseas dollar markets (US, Australia). Could see some mild spread tightening in EUR as paper diverted to further afield investors. Positions in these markets offer both liquidity and remain relatively removed from the European sovereign crisis.

Overweight Neutral

Netherlands

The last predominantly “rates” market. With the current pick-up of senior unsecured paper relative to Dutch covered bonds, we do not expect any significant pricing revisions over the next few months. As ‘hybrid' secured researchers, we see more value in adding securitisation exposure in the Netherlands however.

Neutral Neutral

UK

We remain overweight UK covered bonds, appreciating the strength of the guarantor structure (as for Netherlands and Italy). Furthermore, owing to the nascent start of a domestic, GBP covered bond market, we also recognise the potential for performance in the existing largely EUR-denominated UK covered bonds, as both future supply is directed into the GBP market and continental investors appreciate the pick-up to some of the tighter, northern European markets. For the more ‘adventurous’ investors, we also see particular appeal in covered bonds of now state-supported institutions (Bradbi and NRAM) which benefit from HM Treasury guarantees (Bradbi to runoff, NRAM revocable with 3 months notice).

Overweight Overweight

Italy

While we very much appreciate the SPV structure deployed in OBGs, like the underlying mortgage collateral and the financial health of most Italian households, and see the predominantly domestically funded Italian banks as unlikely to ‘over issue’ OBGs, we switch our overweight recommendation to an underweight based on the seemingly significant potential for political backflips with respect to adopting credible austerity measures to stem sovereign contagion. On a HTM perspective, we would remain overweight based on technicals, but on a MTM basis, we see the political backdrop as too volatile to justify further investment.

Underweight Underweight

19

Europe Credit Research12 September 2011

Gareth Davies, CFA(44-20) [email protected]

Flavio Marco Rusconi(44-20) [email protected]

Sector Outlook Commentary Investment recommendationsSpain Tier 1/Tier 2 Tier 1/Tier 2

Solid cross-over market where both credit and rates buyers can be seen in significant volumes. Despite the ongoing stresses in the peripheral sovereign crisis and the reorganisation of the caja system, sentiment remains somewhat levelheaded (particularly for Tier One institutions). While we remain aware of the potential for a further bout of sovereign-inspired weakness over the coming months, and the more central hypothesis that bond ratings will continue to be challenged over the course of 2011, we also view cedulas as one of the most defensive types of covered bond, owing to its unique claim on ‘all mortgage assets’ of the issuing institution (i.e. substantially subordinating the rights of all other senior investors).

Overweight/Neutral Overweight/Neutral

Portugal

Higher yielding cousin to the Spanish market, we remain overweight Portuguese covered bonds based on fundamentals: driven by our view on the underlying mortgage borrowers and the relative health of the Portuguese banking system itself. Sovereign inspired weakness could challenge the shorter term success of our overweight recommendation however, but at yields close to/in the double digits, we expect investors with a medium-term investment horizon to benefit any positions. Currently a play for 'faster money'/high yield type accounts, the shorter term ability to exit any positions will remain constrained (more traditional covered bond investors have been burned once). Potential for slippage into non-investment grade ratings territory.

Underweight Overweight

Ireland Domestic/Depfa Domestic/Depfa

Covered bonds’ distressed segment, predominantly considered a 'faster money'/high yield play. Despite the obvious concerns around the health of the Irish banking system in general, and its housing market in particular, we remain overweight Irish ACS. This view is largely driven by the level of political and regulatory support that has been evident for the asset class; and reinforced confirmation that burden sharing will be concentrated in subordinated bonds. Away from domestic issuers, Depfa ACS can also offer investors comfortable with public sector exposure an interesting play from an institution currently 100% owned by the German government.

Underweight/Overweight Overweight/Overweight

Source: J. P. Morgan Covered Bond Research

20

Europe Credit Research12 September 2011

Gareth Davies, CFA(44-20) [email protected]

Flavio Marco Rusconi(44-20) [email protected]

Product overview

Covered Bonds: a “bluffer’s guide”

We set out below a cheat-sheet for readers new to the asset class, providing a synopsis of the main characteristics of the product and an overview of the major markets.

Table 2: Covered bond cheat-sheet

What is a covered bond? Covered bonds are secured, senior, bullet instruments of an issuer (typically a bank), that provide investors with recourse to both the issuing institution and the underlying, revolving collateral pool.

How do CBs differ from RMBS? The main differences between RMBS and covered bonds can be summarised as: a) amortisation: RMBS generally have a pass-through structure based on the repayment of collateral, while CBs generally have a hard or soft bullet profile; b) credit enhancement: covered bonds have much simpler structures than ABS and rely on over-collateralisation as a form of credit enhancement. This can vary according to the usage of the programme by the issuer but a minimum OC has to be maintained; this is monitored through asset and interest coverage tests typically monitored by third parties, which ensure that the asset pool and its proceeds are enough to match the issuer's CB liabilities. In RMBS, credit enhancement is given by subordination and structural features and, except for certain structures, it generally increases as the deal de-levers; c) unlike securitisation, where investors benefit from recourse to the collateral pool only, CB investors benefit from dual recourse to both the issuer and the cover pool.

What types of CB structures exist? There are three broad CB structures: a) CB can be issued off the balance sheet of the originator, with the collateral pool remaining with the originator, albeit ring-fenced for covered bond investors (for example in Austria and Germany); b) a financial institution establishes a limited function subsidiary, which in turn issues covered bonds (for example France’s OF, Norway); c) in countries without specific CB legislation, CB are typically unsecured obligations of the issuer, with funds raised from the issuance of CB lent to a guarantor (typically a limited liability SPV), which uses the loan to acquire collateral from the originator. This entity then acts as guarantor to the unsecured bonds, agreeing to repay bondholders on insolvency of the issuer (for example UK, Canada, Netherlands, Italy).

What type of collateral is accepted? CB legislation (or transactions docs when no CB legislation exists) typically definesthe list of collateral eligible to be included in the cover pool. The main types of assets used as primary collateral are public sector exposures, residential and commercial mortgages and shipping loans. In some cases, a max LTV is specified. The EC’s CRD also allows senior MBS (both residential and commercial) issued by securitisation entities, where at least 90% of the underlying mortgages comply with the above rules for unsecured mortgage exposures. The MBS must be rated Credit Quality Step 1, and can only form 10% of the collateral pool (self-originated MBS receive a waiver from the 10% cap). Substitute assets up to a given threshold (typically 10-15%) can also be included in cover pools.

What type of risk are investors exposed to? Investors are generally exposed to issuer's risk until its default, after which they are exposed to the credit risk of the cover pool. If there are CBs outstanding after the cover pool has been extinguished, CB investors will have a residual claim to the bankruptcy estate of the issuer which will rank pari passu with that of senior unsecured bondholders

Do cover bonds accelerate upon the issuer’s default? No, CBs do not necessarily accelerate on insolvency of the issuing institution. Only the failure of the programme to make payments as and when due results in the acceleration of the obligations.

Which jurisdictions are the largest issuers? The largest issuer, by outstanding amount, is Germany, followed by Spain, Denmark, France and Sweden. As CBs gain popularity with regulators, issuers and investors, more jurisdictions are starting to push for dedicated covered bond legislation (for example Canada and the US).

Source: J.P. Morgan Covered Bond Research

21

Europe Credit Research12 September 2011

Gareth Davies, CFA(44-20) [email protected]

Flavio Marco Rusconi(44-20) [email protected]

As in last year’s Handbook, we once again set out below to define the core characteristics of the covered bond product, despite recognising that by making some generic statements, we ignore some of the multiple nuances that issuance from hundreds of issuers and tens of jurisdictions necessarily implies. We update this segment to reflect changes to legislative frameworks and the rating methodologies of the main agencies.

For more detail on individual jurisdictions, please see the respective country sectionstowards the back of this publication.

What exactly is a covered bond?

In a sentence…Covered bonds are secured, senior, bullet instruments of an issuer (typically a bank), that provide investors with recourse to both the issuing institution and the underlying, revolving collateral pool.

Structural FormCovered bonds are typically thought of as bonds issued from the balance sheet of an originating bank, with the revolving collateral pool remaining with the originator, albeit ringfenced for covered bond investors in case of institutional insolvency. This model is deployed in a number of significant issuing jurisdictions (for example, Austria, Finland, Germany, Greece, Hungary, Portugal Spain and Sweden); however,there are also two other forms of covered bond structures common in a number of jurisdictions.

The most simplistic alternate structure can be accurately described by its name: ‘Specialist Banking Principle’, whereby a ‘full service’ financial institution establishes a limited function subsidiary, which in turn issues the covered bonds, backed by assets transferred from the originator. This form is typical in Ireland, andFrance (for Obligations Fonciere), Luxembourg and Norway.

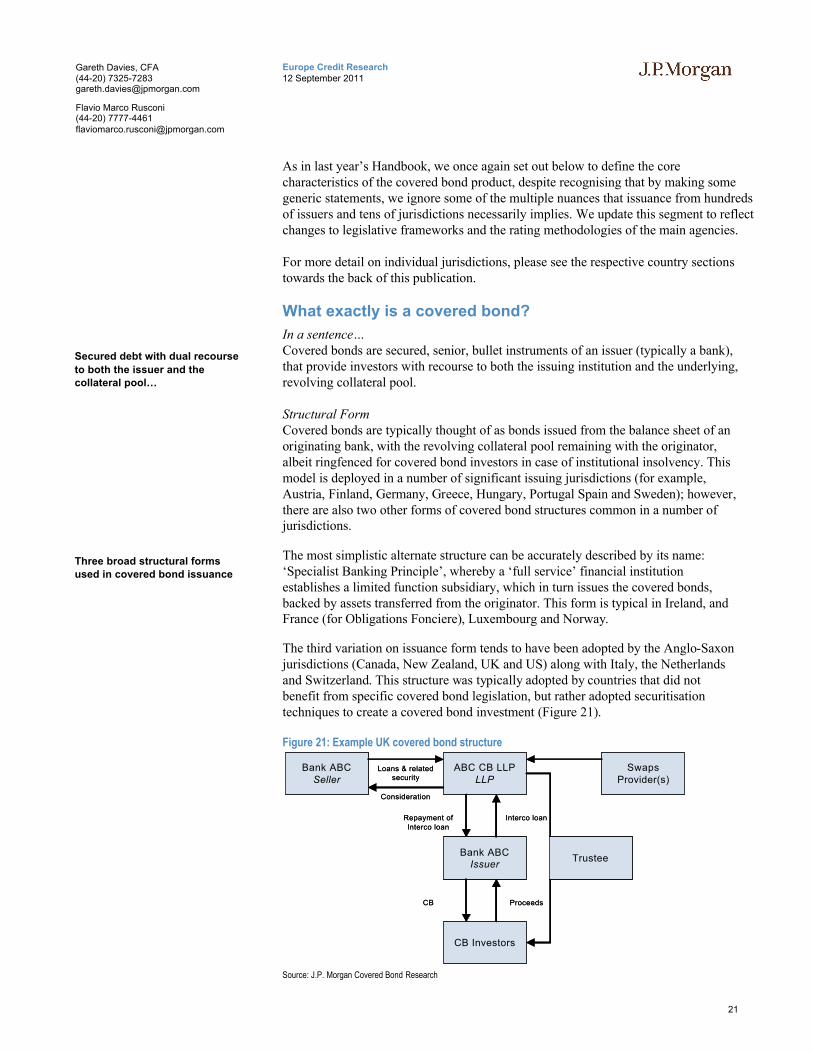

The third variation on issuance form tends to have been adopted by the Anglo-Saxon jurisdictions (Canada, New Zealand, UK and US) along with Italy, the Netherlandsand Switzerland. This structure was typically adopted by countries that did not benefit from specific covered bond legislation, but rather adopted securitisation techniques to create a covered bond investment (Figure 21).

Figure 21: Example UK covered bond structure

Source: J.P. Morgan Covered Bond Research

Bank ABCSeller

ABC CB LLPLLP

Bank ABCIssuer

CB Investors

SwapsProvider(s)

Consideration

Loans & related security

ProceedsCB

Interco loanRepayment of Interco loan

Trustee

Bank ABCSeller

ABC CB LLPLLP

Bank ABCIssuer

CB Investors

SwapsProvider(s)

Consideration

Loans & related security

ProceedsCB

Interco loanRepayment of Interco loan

Trustee

Secured debt with dual recourse

to both the issuer and the collateral pool…

Three broad structural forms used in covered bond issuance

22

Europe Credit Research12 September 2011

Gareth Davies, CFA(44-20) [email protected]

Flavio Marco Rusconi(44-20) [email protected]