the intellectual structure of accounting research - a...

TRANSCRIPT

Working Paper: Please do not cite without permission of the authors!

The Intellectual Structure of Accounting Research - A Bibliometric Analysis

Alexander Just, Utz Schäffer Otto Beisheim School of Management, Vallendar, Germany Matthias Meyer, Kühne School of Logistics and Management, Technical University Hamburg-Harburg, Germany

Abstract: Accounting research has developed over the

years and established itself as a well regarded scientific field in the scholarly community. Today there is an intensive discussion about the future direction of accounting research and the field is seen to be at a “tipping point”. To understand the past and present structure of the field, this study employs citation and co-citation analysis. The aim is to show the references that influenced accounting research the most and map the intellectual structure of accounting research. Citation and co-citation analysis are established bibliometric approaches (Osareh 1996a) which originate from the information sciences and have been used widely as quantitative methods for evaluating the literature in a field. The methods rely on the fact that the references that publishing researchers cite determine the impact of a reference and furthermore establish direct links between papers (co-citations) in the mass of scholarly literature. As a result of these co-citations, the references constitute a complex network of ideas that researchers themselves have connected, associated, and organized (Garfield 1993). Thus, it represents a method to map the intellectual structure of a field (White and Griffith 1981).

We use data from all articles published from 1990 until 2007 in the five leading academic journals in accounting research (Bonner, Hesford et al. 2006), namely Accounting, Organizations and Society (AOS), Contemporary Accounting Research (CAR), Journal of Accounting and Economics (JAE), Journal of Accounting Research (JAR) and The Accounting Review (TAR). Our database comprises of 2,758 articles with a total of 109,482 citations. We merged the data with data from the Accounting Research Directory (ARD) which enables us to classify the articles along several dimensions like research method, mode of reasoning, school of thought or foundation discipline. The 18 years time horizon makes it possible to sub-divide the sample in three equal groups, each spanning six years. As a result we are able to visualize the intellectual structure of accounting research and show the development of the field over the past 18 years.

Introduction The development of accounting research in recent

decades is frequently referred to as a “scientific revolution” (e.g. (Wells 1976); (Beaver 1981); (Reiter and Williams 2002)). The publications by Ball/Brown (1968), Beaver (1968) and Watts/Zimmermann (1978) are commonly seen as milestones in a fundamental scientific transformation of the discipline, such as has taken place in most areas of business research in a similar way although at a different time and with different characteristics. In accounting, this transformation is often described as the progression from a predominantly normative research

using deductive reasoning to a highly empirical discipline with a theoretical foundation that closely follows the related disciplines of finance and economics (e.g. (Reiter and Williams 2002); (Fülbier and Sellhorn 2006)). The shift took place in the 1960s and was accompanied by administrative and regulatory changes in accounting (Wells 1976). As a result rather harsh shift took place in the dominant school of thought of accounting research. A priori research was not longer regarded as having any value, nor advancing the state of knowledge significantly (Dopuch and Revsine 1973). The academic community started to look at methods already used in finance and economics and consequently applied these methods to study accounting problems (Laughlin 1981). It was believed that scientific methods are better suited to solve business problems (Whitley 1988). And by today, a priori research almost entirely vanished from the field.

As a result of this development accounting research nowadays is characterized as dominated by a professional elite (Lee 1997; Lee and Williams 1999), propagating an economics-based monolithic paradigm (Lukka and Mouritsen 2002) with closed and self-referential sub-groups that do not tend to communicate with each other (James and Lee 2006). For others, this development is not yet mono-paradigmatic enough. In their eyes, the still too diverse and fragmented set of research prevents the development of a consistent and reliable body of knowledge (Zimmerman 2001) .

Thus it may be a good time to evaluate the development and present structure of the field since 1990. To achieve this, we will employ bibliometric methods to examine highly cited references in contemporary accounting research and analyze the co-occurrence of references within articles to derive co-citation networks which enable us to map the intellectual structure of accounting research. We set two goals for our research:

1. To identify the publications that had the greatest impact on our discipline and trace their evolving research utility over time. The hypothesis is to find the field heavily to be heavily influenced by economics and finance and pre-dominantly employing quantitative methods.

2. To identify and visualize the evolution of the major knowledge groups and show general relations between them.

In the next section, we provide an overview of the literature which previously used bibliometric methods in accounting research and related disciplines. Following that, we explain the database for the analysis and describe the methods used. We then focus on the description of the two

Working Paper: Please do not cite without permission of the authors!

methods, citation and co-citation analysis. We will then present the results and finally discuss the resulting overall picture and the implications.

Literature Review Bibliometrics were first used in information science but

rapidly gained acceptance in other disciplines. There is a considerable body of literature in business administration which uses bibliometric methods to analyze a wide variety of issues. Citation and Co-citation analysis are the most common bibliometric methods. Citation analysis answers the question what articles are cited most often. It is possible to examine the growth in citations over time, identify when the major articles were written, how the popularity processed over time, and if an article is still useful for current researchers. Co-citation analysis is based on the analysis of works which are commonly cited together. Co-Citations studies can illustrate what topics, authors, journals, and research methods were essential, and which marginal, to the field, and how they evolved over time (Pilkington and Meredith 2009).

In accounting research one of the first citation analyses was performed by McRae in 1974. The article is based on the analysis of citations in 17 accounting journals for the period January 1968 to December 1969 and examines the flow of messages between the accounting system and other knowledge systems (McRae 1974). Hofstedt (1976) also examines the interaction of accounting and other disciplines using the example of behavioral accounting research. He starts with evaluating the present state of behavioral accounting research using citation analysis and analyzes the quantity and quality of its interactions with the more basic social sciences and more applied disciplines (Hofstedt 1976). Brown, Gardner and Vasarhelyi are three authors who intensively used bibliometrics to study academic accounting research. In 1985 Brown and Gardner published two papers using citation analysis to assess the overall impact of major research journals and articles on contemporary accounting research. In their first publication they identify articles exerting the greatest impact on the field (Brown and Gardner 1985) and in the second they evaluate the research contributions of accounting faculties, doctoral programs, and individuals to contemporary accounting research (Brown and Gardner 1985). Only two years later Brown, Gardner and Vasarhelyi perform an analysis on journal basis to evaluate the research contributions of Accounting Organizations and Society (AOS) during the years 1976 – 1984 (Brown, Gardner et al. 1987). In 1989 the authors use four attribute dimensions that, in their view, have impacted contemporary accounting literature between 1976 and 1984 the most to develop a model that predicts attribute levels for the years 1985 and 1986 (Brown, Gardner et al. 1989).

Another prominent author using bibliometrics during that time was Robert J. Bricker. In his first article he used a citation analysis to investigate how accounting researchers accumulated and retained knowledge in the period from 1983 to 1986. His research reveals a strong tendency to cite

more recent literature. This is depicted as a positively skewed distribution of the age structure of sources towards more recent articles. At the same time, the average age of cited sources at eleven years is relatively high compared to four years half-life period in the natural sciences (Bricker 1988). Still, Bricker concludes that accounting research is moving toward the citation patterns used in natural sciences. In his opinion, the differences in the average age of sources can be explained by the relatively high importance attached to previous research, and/or by the fact that the discipline is comparatively young and not yet fully developed. He sees a further possible explanation in the fact that accounting research is a hybrid between the natural science model and the model used by the humanities and cultural sciences. His second article is the only study that deals directly with the structure of accounting research and thus the knowledge exchange between different lines of research (Bricker 1989). In his co-citation analysis for the period from 1983-1986 he derives a dendogram for accounting research based on a cluster analysis. He draws the conclusion that, at a detailed level of observation, some clusters – for instance the "financial”, “positive accounting”, “market based” and “time series” clusters – are very well integrated into the overall structure of accounting research, whereas this is less the case in other areas of research such as “statistical auditing”, “tax” and “studies in academic accounting”. Based on these results, he investigates the breadth of content of individual major accounting journals in more detail. He finds that articles from JAR and TAR are present in a large number of clusters, while AOS and JAE are not found so often (Bricker 1989).

In 1996 Lawrence Brown publishes another article using citation analysis to identify influential accounting articles, individuals, Ph.D. granting institutions and faculties (Brown 1996). He identifies a total of 26 “classics” – articles that have been cited at least four times a year since they were published. The study is also interesting as it creates a link to the structural dimension. Based on the classification system of the Accounting Research Directory, he identifies seven “paradigms” of accounting research and assigns the individual “classics” to them as far as possible (see table 1 in the appendix). In his study most of the identified “classics” can be assigned to the “capital markets” and “positive theory” paradigms, but no “classics” among the accounting journals were identified for the “behavioral” and “agency” paradigms.1 Overall, this classification approach covers a relatively broad spectrum. This suggests that the discussion covers a wide range of perspectives ranging from economics-oriented approaches, capital market theory or information economics to mathematical procedures, psychological and historical studies. We must emphasize, however, that this classification has not yet been examined empirically and should be assessed purely as a conjecture on the structure of the discussion.

1 However, Brown (1996) includes neither monographs nor

sources from other disciplines in his analysis which acts in the favor of the capital market/positive theory category.

Working Paper: Please do not cite without permission of the authors!

The publication analysis by Lukka/Kasanen (1996) is a study that deals with the exchange of knowledge in accounting. The authors analyze the institutional barriers in the knowledge production process of accounting research using Bourdieu’s concept of elites. The authors on the one hand identify a powerful “US elite” grouped around the journals TAR, JAR and JAE, and on the other hand a mainly “European elite” formed around the journal AOS. The “US elite” has its strengths in the field of quantitative empirical analysis and analytical models, while the elite grouped around AOS specializes in investigating “organizational and social issues”, often using qualitative methods ((Lukka and Kasanen 1996); see also (Williams and Rodgers 1995) and (Lee 1995) with similar conclusions). Another study on the interdisciplinary structure of accounting research should be mentioned in this context: Reiter and Williams (2002) use a citation analysis to show that accounting research cites sources from economics and finance to a much greater extent than vice versa which indicates a one-way knowledge transfer from economics/finance to accounting.

As an extension to the earlier study by Hofstedt (1976), Meyer and Rigsby (2001) analyze the topical content and research methods used in the journal Behavioral Research in Accounting (BRIA), leading to an analysis of the impact of the journal on the accounting literature (Meyer and Rigsby 2001). Solomon and Trotman (2003) also deal with a single journal, AOS, by reviewing the papers published in the journal during the period 1976 - 2000 that report auditing judgment and decision experiments. Furthermore the authors employ citation analysis for judging scholarly impact and draw comparisons with other leading research journals (Solomon and Trotman 2003). The degree of relative isolation of managerial accounting research from related disciplines and whether economics-based management accounting research papers make a greater contribution than papers based on another foundation discipline is in the focus of a study by Mensah et al. (2004). Furthermore there are many articles using citation analysis to rank accounting journals, PhD programs or faculties in respect to their impact on the field (Brown 2003; Brown and Laksmana 2004; Beattie and Goodacre 2006; Reinstein and Calderon 2006; Milne 2008; Chan, Seow et al. 2009; Coyne, Summers et al. 2009).

While there are few co-citation studies in accounting, they have been conducted in cognate fields to study a variety of issues. In Operations Management Pilkington and Liston-Heyes (1999) used citation analysis to plot sub-fields in Operations Management. They found five main categories and showed that North American and European researcher place significantly different emphasis on each of these categories. In a recent update of this study Pilkington and Fitzgerald (2006) identify changes and emerging topics in the discipline’s categories. Nerur et al. (2008) update an earlier study by Ramos-Rodriguez et al. (2004) to reveal the intellectual structure of the strategic management field. In information science Zhao and Strotmann (2008) study the evolution of information science in the first decade of the web by performing an enriched author co-citation analysis. Karki

(1996) examines the relationships between the sociology of science and information science literature and finds that an exchange of ideas only takes place when discussing “scholarly communication”. In entrepreneurial research Gregoire (2006) uses co-citation analysis to investigate whether there is conceptual convergence in entrepreneurship research and Schildt et al. (2006) identify scholarly communities in entrepreneurial research. Bibliometric methods were also employed to identify networks between research published in the Journal of Supply Chain Management (Carter, Leuschner et al. 2007). Similarly Charvet et al. (2008) assed the intellectual structure of the entire field.

As one can see, bibliometrics is a long established and proved method for statistically analyzing the literature in a field (Small 1973; Garfield 1993; Small 1993). Especially citation analysis has been frequently used in accounting research while the use of co-citation analysis is rare. To our knowledge except of the early attempts by Gamble et al. (1987) who tried to trace the development of agency thought with the aid of co-citation analysis, and the previously mentioned study by Bricker (1989), there has been no study in accounting using co-citation analysis to assess the intellectual structure of the field. In this article we are aiming at filling this gap by combining citation and co-citation analysis to fulfill the goals set in the introduction. In the next paragraph we will introduce the methodology and present the database used in our study.

Methodology and Data The scope of bibliometrics is “to shed light on the

processes of written communication and of the nature and course of development of a discipline” (Pritchard 1969). The major bibliometric techniques are publication analysis, citation analysis and co-citation analysis.

Publication analysis is a descriptive analysis of the nature of publications. Most often a publication analysis covers a pre-determined time-frame in which all publications in a certain discipline are recorded. These articles are then listed in accordance to publication date, journal and additionally classified along several dimensions like research method, focus, or paradigm. The publications represent the core of knowledge in a discipline under study.

Citation analysis is the most established bibliometric approach. It has been used vastly as a quantitative method for evaluating the literature in different disciplines (Osareh 1996a). The underlying assumption is that by referring to another author’s work, the citing author gives direct credit to the other author’s views. In other words, citations are seen as a formal acknowledgment that one document receives from another (Osareh 1996a). Citation analysis is based on the assertion that heavily cited articles are likely to have a greater influence than less cited articles (Culnan 1986). Undisputable this assumption has its weaknesses but with an appropriate selection and a sufficient large sample the method provides useful insights into “the field’s view of itself” (White and Griffith 1981). However,

Working Paper: Please do not cite without permission of the authors!

as Garfield (1979) points out, there are some dangers with citation analysis. First, the inferences are based on the first author and not all authors. As a result important information about the second author’s contribution is missing. But since we concentrate our analysis on publications and not authors as unit of analysis we are not facing this weakness. Second, there is the problem of including negative (referring to an article as a bad example), and self-citation. We will deal with this issue like others did in previous studies (Pilkington and Meredith 2009) and assume these citations to be equally distributed among authors. As a result every citation to a major publication will have the same value in our analysis.

Citation analysis fails to visualize the structure of influence within a field, which is the main advantage of co-citation analysis. Co-citation analysis is based on “the frequency with which two documents are cited together” (Small 1973) and offers the possibility to map the intellectual structure and dynamic of science (Osareh 1996b). It is possible to identify relationships among authors, topics, journals, keywords or research methods and illustrate the structural groupings of these relationships and to how these groups relate to each other (Small 1973).

In a typical co-citation analysis, the relationship of cited references is evaluated based on the co-occurrence of references within articles. Co-citations represent a close relationship between two articles, either because they belong to the same topic area or because their topic areas are closely connected (Cawkell 1976; Garfield 1993). One of the main advantages of the methodology is that it is possible to unearth relationships that those providing the information are not aware of and/or are not transparent due to the complexity of the topic. Even though many co-citations may be unrelated on the first sight, a sufficiently large sample of cited articles enables researchers to mitigate the looseness created by some articles that focus on diverse topics or streams. As a result the summary of co-cited articles makes it possible to draw conclusions on the internal structure and the degree of fragmentation of a research discipline. The number of co-citations is interpreted as a measure of the proximity of the sources or their authors, whereby a certain threshold of co-citations must exist in order for them to be interpreted. It is important to note that the networks derived are not groups of individuals that are actually linked like it is the case in social network analysis. The members of a cluster rather form a group with shared perspectives on a certain research area or topic.

Co-citation research embraces a large number of different methods to determine co-citation clusters. It is critically important when gathering the source data for the co-citation analysis that only appropriate articles are selected to represent the area of investigation. The standard approach in most co-citation analysis is to use a panel of experts to identify a prominent panel of authors. Then all the papers are identified and retrieved that cite any of their articles. These data represent the population for the co-citation analysis on an author level, where authors act as proxies for their ideas and contributions (Pilkington and

Meredith 2009). By using five accounting journals as source population instead of a representative set of authors, we are able to perform the analysis on a publication level, giving a more detailed representation of the topics discussed in accounting research.

Given that 2,758 articles selected for analysis had approximately 110,000 cited references, it was impossible to include all of them in the analysis. Typically, the researcher has to set a threshold regarding the popularity of the references contained in the analysis, leaving out information on cited documents that do not have a significant impact. For the purposes of our study, we chose a method that has been used successfully in comparable studies to generate distinctive and sharply defined lines of research (Chen 2001; Ahlgren 2003; Gmür 2003). The analysis focuses on the approx. 200 most-cited publications of each period of investigation. This number of articles is sufficient to identify the most influential lines of research and bears a manageable complexity.

Co-citation counts were computed and assembled in a matrix with the identically ordered articles in the rows and columns. The absolute co-citation values are not suitable for generating clearly defined clusters. The reason for this being that the most-cited sources tend to be co-cited more frequently than sources that are cited less often, even though the latter might be more closely related in terms of content. Therefore the absolute co-citation value between two sources needs to be put in appropriate relation to the frequency of citation. The statistical method used to standardize the raw co-citation counts is the so-called CoCit score. It has been proofed to be well suited and applied in numerous studies (Gmür 2003; Meyer, Lorscheid et al. 2009). This relative co-citation value for two sources A and B is scaled to a range between 0 and 1 and is calculated using the following formula:

For representation purposes it is necessary to set a threshold for the co-citation strength. Therefore the approximately 200 strongest co-citation relationships2 are selected based on the CoCit score. The threshold value for the first period was calculated at 0.210, for the second at 0.231, and for the third period at 0.175. These minimum values, which indicate the average distance between the publications in the area of research, only diverge slightly over the course of time and correspond to minimum values in similar studies (Gmür 2003). The resulting co-citation network comprises several clusters that can take the form of isolated pairs, co-citation chains, co-citation stars or a large number of groups of different sizes. In this paper, we include a knowledge group or cluster in our representation when a group has at least three sources that are linked by at least three strong co-citation relationships.

2 If the two-hundredth article shares the rank with other articles

that have the same number of citations, these articles are also included in the analysis.

( )( ) ( )BABA

ABAB citationcitationmeancitationcitationMinimum

citationcoCoCit;;

2

×−

=

Working Paper: Please do not cite without permission of the authors!

We will now turn our attention to the data used for the citation and co-citation analysis. Articles and there corresponding citations were taken from the Social Science Citation Index (SSCI) and are made up of the bibliographies of 2,758 articles published between 1990 and 2007 in AOS, CAR, JAE, JAR and TAR. The journals were selected based on the following considerations: First, they are characterized in various studies and consistently over a long period of time as the five international leading journals (Bonner, Hesford et al. 2006; Reinstein and Calderon 2006). Secondly, the study by Lowe/Locke (2005) proves that the journals selected cover both major "camps” in accounting research, thus guaranteeing adequate representation of accounting as a discipline. Another aspect in this regard is that all five journals have been listed in the Accounting Research Directory (ARD) since it was established and together they cover well over half of the sources included in it.

By choosing the period of investigation from 1990 to 2007 our analysis ties to the previously described studies published by Robert Bricker (Bricker 1988; 1989) and Lawrence Brown et al. (1996). The first two studies deal with the period from 1983 to 1986, while the latter was carried out for the period from 1963 to 1992. As the co-citation structures can vary randomly from year to year, we decided to divide the timeframe into three six-year periods. In this way, we generated three comparable periods encompassing around 900 articles and 36,000 sources each.

Table 1: Overview of the number of included articles and references

1990-1995

2001-2007

1996-2001

1990-2007

Number of articles 952 993 813 2.758 Number of references

32.722 46.188 30.572 109.482

Average number of references per article

34,37 46,51 37,60 39,70

Average age of reference

9,54 11,50 10,25 10,59

The data taken from the SSCI were adjusted to eliminate input errors. These occurred in roughly 20% of the sources in the SSCI, mainly because the sources were levied in-correctly or inconsistently in the first place, or the source was already misspelled in the citing article. We included all articles recorded in the SSCI under the categories “article”, “note” or “review”, but omitted introductory articles by the editor (editorials) or book reviews. Furthermore, we removed all sources that did not specify an author, which is often the case in statistical documents, publications by institutions and associations or articles in popular magazines. Finally, we combined different editions of a single monograph in the most-cited edition. One of the major difficulties we experienced while gathering the data was the incomplete coverage of the journal CAR by the

SSCI. We therefore levied the missing sources manually to match the coverage period of CAR in our analysis with those of the other journals.

Classification of data To be able to differentiate thematic, paradigmatic and

methodological differences in the co-citation clusters, we additionally classified the articles. In a first step, we looked for possible thematic points of focus (see table 2). The thematic grouping was done by examining the title of an article.

Table 2: Classification of the thematic foci Thematic focus Description

Earnings management

Articles which fall into this thematic area mainly deal with the information content of earning announcements, the relation between stock market returns and earning announcements as well as mandatory accounting changes and the consequences of accounting choices

Disclosure

Articles in this category mainly deal with the information value of discretionary disclosures, voluntary disclosures and the consequences of disclosing information

Executive Compensation

Articles predominantly deal with agency/moral hazard issues, measuring and evaluating managerial performance and management compensation

Auditing Services

Articles are looking into audit pricing and audit quality issues, the effects of auditor experience and audit judgment

Accounting Systems & Data

Articles focus on the historic aspect of social and organizational contextual factors of accounting systems, the use of accounting data, budgeting and management control systems

Analyst forecasts

These articles deal with the decision-making of analysts and the consequences of analyst forecasts

Valuation The focus in this topic area is on valuation issues and clean surplus accounting

Corporate Governance

The articles here deal with the separation of ownership and control, SEC enforcements as well as conservatism in accounting

Miscellaneous

Diverse category among others, articles deal with accounting choice in the context of commercial banks, the relevance and boundaries of financial statements

Working Paper: Please do not cite without permission of the authors!

When it was not possible to allocate the article to one of the groups, the abstract was examined. This classificaion resulted in eight different categories. In a second step we did a classification using information from the Accounting Research Directory to identify the research method, mode of reasoning and school of thought of the articles (see table 1 in the appendix for the description of the dimensions of the ARD). In a last step we allocated shared paradigms to the knowledge groups. The classification of the paradigms is based on an analysis by Brown (1996) in which he defines so-called “classics” in accounting research and identifies the corresponding paradigm for these classics (see table 2 in the appendix for paradigm classification).

The Accounting Research Database (ARD) used for the classification of the articles is a proprietary database summarizing the taxonomic and citation characteristics of major accounting research journals. It was created over two decades ago by Vasarhelyi and Berk (1984) as a record of the taxonomic classification of articles which appeared in the five leading accounting journals. Over the years both the content and scope evolved and it now encompasses twelve scholarly accounting journals, and includes citation analysis data as well. It has been employed in numerous research papers, such as Brown, Gardner and Vasarhelyi (1987), Vasarhelyi, Bao, and Berk (1988), Bricker (1989), and Badua, Previts, and Vasarhelyi (2002). The ARD was created to facilitate the research of accounting academics and practitioners and taxonomically categorizes the major articles published since 1963 in the following journals: Journal of Accounting Research (JAR), The Accounting Review (TAR), Accounting, Organizations and Society (AOS), Journal of Accounting, Auditing and Finance (JAAF), Journal of Accounting and Economics (JAE), Auditing: Journal of Theory and Practice (AUD), Contemporary Accounting Research (CAR), the Accounting Historians

Journal (AHJ), the Journal of Accounting and Public Policy (JAPP), and the Journal of Information Systems (JIS) (Badua 2006).

Results GENERAL

Figure 1 shows the publication-year distribution of cited paper for every period going back to 1950. Although our database includes references prior to this point, the growth of citations does not start from 1975 onwards. The figure shows a typical age structure for the “obliteration by incorporation” model over all three periods (Merton 1968; Bricker 1988). This model, usually attributed to the natural sciences, is based on the assumption that researchers primarily draw on articles that immediately precede their work. It is therefore closely linked to the idea of a research front that consists of a limited number of articles and proceeds gradually ((Hess 1997), p. 77). Newly written articles incorporate knowledge from previous articles. Furthermore, at regular intervals, the state of knowledge is condensed in the form of reviews. Older articles and the findings documented within them are archived, as their content has been merged into newer articles.

Figure 1 clearly shows a positively skewed distribution of the number of sources per year toward sources from more recent publications. Each curve peaks at sources that are approx. five years old. By comparing the curves of individual periods, we see that the research front progresses gradually and the majority of sources disappears into the scientific archive. This leads to the conclusion that the discipline is fairly stable and has not grown more dynamic over the last year. This can also be seen in the high average source ages (see table 1) compared to natural sciences where the average source age has found to be between 4 to 5 years (De Solla Price 1965; Bricker 1988; Cole 1994).

Figure 1: Citations to a Year (per period)

Working Paper: Please do not cite without permission of the authors!

Bricker (1988) explained this comparably high source age with the relatively young age of the discipline. More than two decades later we can rule out this possible explanation. The data rather indicate that accounting research attaches importance to its articles over a longer period of time, even if this does not cancel out the basic theme of “obliteration by incorporation”. This will be supported by the results of the citation analysis. As we will see, the most-cited sources especially in the middle and last third are relatively dynamic whereas there is continuity at the top of the ranking. This means that a small number of the most-cited articles and monographs can be seen as stable points of reference that prevail over a longer period of time while others gained or lost popularity over the course of time. CITATION

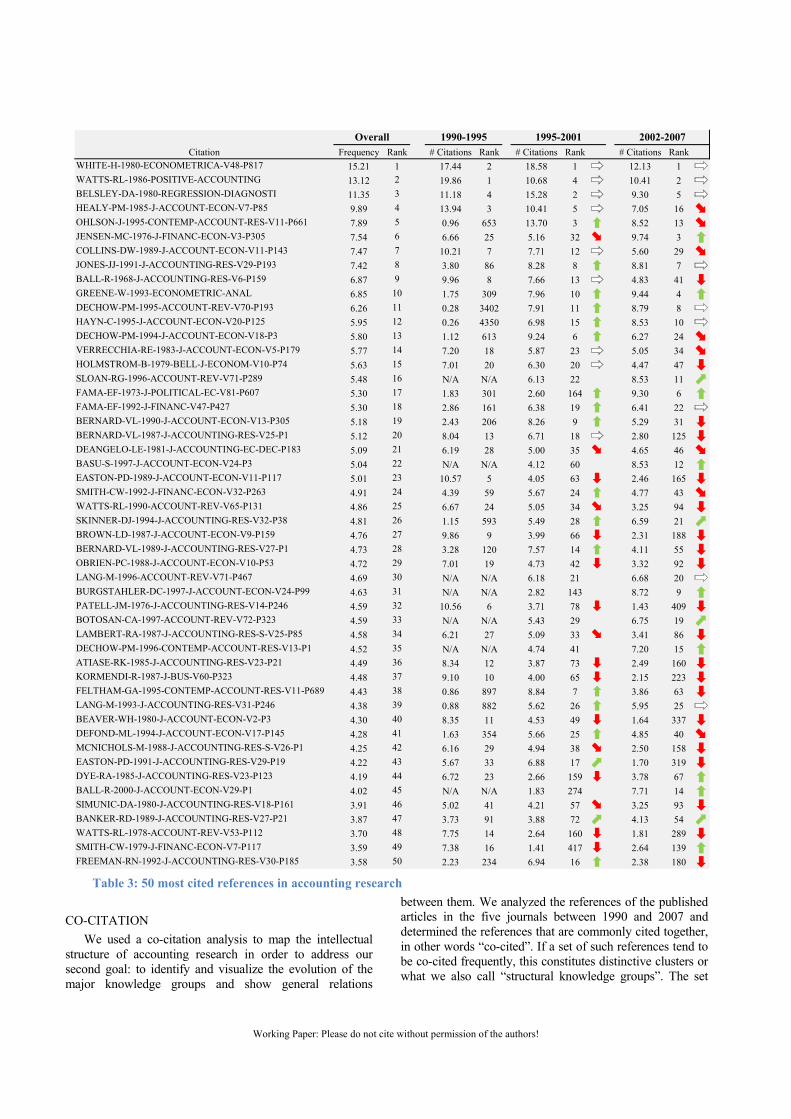

We employ citation analysis to achieve our first goal, identifying the publications that had the greatest impact on accounting research and trace their evolution over time. Table 3 lists the 50 most cited publications in the five journals under study. Since the different journals publish a different amount of issues per year and since there are significant differences in the citation frequency among the journals (as indicated in table 1), the citation frequency was normalized with the number of citations made by each journal in each time-period. The normalization approach is a standard approach in multi-journal citation studies (Pilkington and Meredith 2009). The values given in the column “Frequency” are the sum of normalized citations for the respective publication over the five journals. The normalized citation frequencies are also broken down into three time-periods to be able to trace the development over time. This makes it possible to see how the most popular publications stand the test of time and either fade away or become more popular.

We will first take a look at the structure of the most cited publications over the entire 18 years time-horizon. The 50 publications consist of 39 articles from accounting journals, 3 books and 8 articles from outside the accounting area. Not surprisingly the 39 publications that appeared in accounting journals were all published in four of the five journals under study. On the one hand, this concentration stresses the importance of these journals for the field and symbolizes the importance of the knowledge that is transmitted by these journals. On the other hand the concentration could be the result of a sampling error since authors tend to cite within the journal they publish and editors want articles to be built on research previously published in their journals. It is noteworthy that none of the publications in the top-50 appeared in the UK-based journal AOS. This indicates that accounting research is mainly influenced by US-journals and that AOS does not play a significant role in the knowledge accumulation of the discipline.

We find three monographs among the top-50 references and they are all ranked among the top-10 publications in

accounting research. The famous book by Watts and Zimmerman (1986) on positive accounting theory is the second most cited publication and Belsley’s work on Regression Diagnostics the third. The last monograph among the top-50 is Greene’s book on econometric analysis. The nature of the monographs stresses the quantitative alignment of accounting research.

Furthermore there are 8 articles among the top-50 references that do not belong to the area of accounting research but exceed a significant influence on the discipline. All were mainly published in finance and economics journals. 3 of the articles are from the Journal of Financial Economics, the others appeared in the Bell-Journal of Economics, Journal of Political Economy, Journal of Finance and the Journal of Business. The most cited publication is also an article from another discipline: Halbert White’s article “Heteroskedasticity-Consistent Covariance Matrix Estimator and a Direct Test for Heteroskedasticity” that appeared in Econometrica in 1980.

Taking a closer look at the 39 publications that appeared in the major accounting journals offers some interesting insights. 15 of the most-cited articles were published in JAE and JAR respectively, 6 appeared in TAR, 3 in CAR. Using the classification of the ARD, it can be shown that 32 of the 39 papers use archival data, 6 analytical internal logic and only 1 field survey as a research method. 35 articles use quantitative techniques as mode of reasoning and there are only 2 qualitative studies (2 fall into the mixed category). The dominant school of thought employed in 36 articles is statistical modeling with a focus on the test of the efficient market hypothesis. There are only 2 papers that contribute to accounting theory. The dominant research area is financial accounting research. 33 of the papers can be attributed to this ares. There are 4 managerial and two auditing papers. 28 articles are founded in accounting research, while 10 papers use finance and economics as major source of information. The overall results support the hypothesis raised in the beginning. The discipline can be described as highly quantitative. Most of the studies use archival data and deal with testing the efficient market hypothesis. The data furthermore reveal a high influence of theories from the economics and finance literature. A priori research is almost not present which is shown by the marginal number of accounting theory papers.

Taking a look at the changes over time it gets obvious that this development gained momentum in recent times. Most of the articles that gained popularity are quantitative articles while the articles either relying on analytical internal logic or belonging to the accounting theory school of thought predominately lost popularity. We will analyze the dynamics of the intellectual structure in-depth in the next sub-section by looking at the knowledge groups in accounting research, their evolution and development over time.

Working Paper: Please do not cite without permission of the authors!

CO-CITATION

We used a co-citation analysis to map the intellectual structure of accounting research in order to address our second goal: to identify and visualize the evolution of the major knowledge groups and show general relations

between them. We analyzed the references of the published articles in the five journals between 1990 and 2007 and determined the references that are commonly cited together, in other words “co-cited”. If a set of such references tend to be co-cited frequently, this constitutes distinctive clusters or what we also call “structural knowledge groups”. The set

Citation Frequency Rank # Citations Rank # Citations Rank # Citations RankWHITE-H-1980-ECONOMETRICA-V48-P817 15.21 1 17.44 2 18.58 1 12.13 1WATTS-RL-1986-POSITIVE-ACCOUNTING 13.12 2 19.86 1 10.68 4 10.41 2BELSLEY-DA-1980-REGRESSION-DIAGNOSTI 11.35 3 11.18 4 15.28 2 9.30 5HEALY-PM-1985-J-ACCOUNT-ECON-V7-P85 9.89 4 13.94 3 10.41 5 7.05 16OHLSON-J-1995-CONTEMP-ACCOUNT-RES-V11-P661 7.89 5 0.96 653 13.70 3 8.52 13JENSEN-MC-1976-J-FINANC-ECON-V3-P305 7.54 6 6.66 25 5.16 32 9.74 3COLLINS-DW-1989-J-ACCOUNT-ECON-V11-P143 7.47 7 10.21 7 7.71 12 5.60 29JONES-JJ-1991-J-ACCOUNTING-RES-V29-P193 7.42 8 3.80 86 8.28 8 8.81 7BALL-R-1968-J-ACCOUNTING-RES-V6-P159 6.87 9 9.96 8 7.66 13 4.83 41GREENE-W-1993-ECONOMETRIC-ANAL 6.85 10 1.75 309 7.96 10 9.44 4DECHOW-PM-1995-ACCOUNT-REV-V70-P193 6.26 11 0.28 3402 7.91 11 8.79 8HAYN-C-1995-J-ACCOUNT-ECON-V20-P125 5.95 12 0.26 4350 6.98 15 8.53 10DECHOW-PM-1994-J-ACCOUNT-ECON-V18-P3 5.80 13 1.12 613 9.24 6 6.27 24VERRECCHIA-RE-1983-J-ACCOUNT-ECON-V5-P179 5.77 14 7.20 18 5.87 23 5.05 34HOLMSTROM-B-1979-BELL-J-ECONOM-V10-P74 5.63 15 7.01 20 6.30 20 4.47 47SLOAN-RG-1996-ACCOUNT-REV-V71-P289 5.48 16 N/A N/A 6.13 22 8.53 11FAMA-EF-1973-J-POLITICAL-EC-V81-P607 5.30 17 1.83 301 2.60 164 9.30 6FAMA-EF-1992-J-FINANC-V47-P427 5.30 18 2.86 161 6.38 19 6.41 22BERNARD-VL-1990-J-ACCOUNT-ECON-V13-P305 5.18 19 2.43 206 8.26 9 5.29 31BERNARD-VL-1987-J-ACCOUNTING-RES-V25-P1 5.12 20 8.04 13 6.71 18 2.80 125DEANGELO-LE-1981-J-ACCOUNTING-EC-DEC-P183 5.09 21 6.19 28 5.00 35 4.65 46BASU-S-1997-J-ACCOUNT-ECON-V24-P3 5.04 22 N/A N/A 4.12 60 8.53 12EASTON-PD-1989-J-ACCOUNT-ECON-V11-P117 5.01 23 10.57 5 4.05 63 2.46 165SMITH-CW-1992-J-FINANC-ECON-V32-P263 4.91 24 4.39 59 5.67 24 4.77 43WATTS-RL-1990-ACCOUNT-REV-V65-P131 4.86 25 6.67 24 5.05 34 3.25 94SKINNER-DJ-1994-J-ACCOUNTING-RES-V32-P38 4.81 26 1.15 593 5.49 28 6.59 21BROWN-LD-1987-J-ACCOUNT-ECON-V9-P159 4.76 27 9.86 9 3.99 66 2.31 188BERNARD-VL-1989-J-ACCOUNTING-RES-V27-P1 4.73 28 3.28 120 7.57 14 4.11 55OBRIEN-PC-1988-J-ACCOUNT-ECON-V10-P53 4.72 29 7.01 19 4.73 42 3.32 92LANG-M-1996-ACCOUNT-REV-V71-P467 4.69 30 N/A N/A 6.18 21 6.68 20BURGSTAHLER-DC-1997-J-ACCOUNT-ECON-V24-P99 4.63 31 N/A N/A 2.82 143 8.72 9PATELL-JM-1976-J-ACCOUNTING-RES-V14-P246 4.59 32 10.56 6 3.71 78 1.43 409BOTOSAN-CA-1997-ACCOUNT-REV-V72-P323 4.59 33 N/A N/A 5.43 29 6.75 19LAMBERT-RA-1987-J-ACCOUNTING-RES-S-V25-P85 4.58 34 6.21 27 5.09 33 3.41 86DECHOW-PM-1996-CONTEMP-ACCOUNT-RES-V13-P1 4.52 35 N/A N/A 4.74 41 7.20 15ATIASE-RK-1985-J-ACCOUNTING-RES-V23-P21 4.49 36 8.34 12 3.87 73 2.49 160KORMENDI-R-1987-J-BUS-V60-P323 4.48 37 9.10 10 4.00 65 2.15 223FELTHAM-GA-1995-CONTEMP-ACCOUNT-RES-V11-P689 4.43 38 0.86 897 8.84 7 3.86 63LANG-M-1993-J-ACCOUNTING-RES-V31-P246 4.38 39 0.88 882 5.62 26 5.95 25BEAVER-WH-1980-J-ACCOUNT-ECON-V2-P3 4.30 40 8.35 11 4.53 49 1.64 337DEFOND-ML-1994-J-ACCOUNT-ECON-V17-P145 4.28 41 1.63 354 5.66 25 4.85 40MCNICHOLS-M-1988-J-ACCOUNTING-RES-S-V26-P1 4.25 42 6.16 29 4.94 38 2.50 158EASTON-PD-1991-J-ACCOUNTING-RES-V29-P19 4.22 43 5.67 33 6.88 17 1.70 319DYE-RA-1985-J-ACCOUNTING-RES-V23-P123 4.19 44 6.72 23 2.66 159 3.78 67BALL-R-2000-J-ACCOUNT-ECON-V29-P1 4.02 45 N/A N/A 1.83 274 7.71 14SIMUNIC-DA-1980-J-ACCOUNTING-RES-V18-P161 3.91 46 5.02 41 4.21 57 3.25 93BANKER-RD-1989-J-ACCOUNTING-RES-V27-P21 3.87 47 3.73 91 3.88 72 4.13 54WATTS-RL-1978-ACCOUNT-REV-V53-P112 3.70 48 7.75 14 2.64 160 1.81 289SMITH-CW-1979-J-FINANC-ECON-V7-P117 3.59 49 7.38 16 1.41 417 2.64 139FREEMAN-RN-1992-J-ACCOUNTING-RES-V30-P185 3.58 50 2.23 234 6.94 16 2.38 180

Overall 1990-1995 1995-2001 2002-2007

Table 3: 50 most cited references in accounting research

Working Paper: Please do not cite without permission of the authors!

and the relationships between and among these groups constitute the intellectual structure of a field (Leydesdorff and Vaughan 2006). Thereby it does not matter that much, how frequently a reference is cited since the focus is on co-citations. As a result a frequently cited reference may not necessarily be a major contributor to a knowledge group.

The networks illustrated in figures 1 to 3 show the structure of accounting research in each of the three periods

reviewed. The clusters in the figures are numbered and the size of a cluster indicates its significance. The density of a network shows how many of the possible relationships between sources actually exist and is therefore an indicator of the proximity between the sources. The centrality of a source in the cluster shows the relative importance of this particular reference compared to the other references in the cluster. A detailed overview of the included sources, their classification as well as important network measures can be provided by the author.

We will start our analysis with describing the overall co-citation networks for all three time periods. A look at both, the number of the clusters and their density gives us a first idea of the structure of the discussion. For example, a large number of compact clusters points to a differentiated discussion with various areas of focus within each of which a close exchange takes place. This will be followed by a detailed analysis of the different knowledge groups in the network, grouped by thematic focus. We will describe the composition and changes over the three periods of consideration and point out the most central, e.g. important articles.

The first co-citation network for the period from 1990 to 1995 consists of ten knowledge groups and we were able to group these into five thematic foci. On a group-level, the earnings management cluster has a relatively low density whereas the other clusters are fairly dense. The overall density of the entire network is 0.3. This low overall density indicates a not so frequent exchange of ideas between the different research streams.

The second co-citation network covers the period 1996-2001 and includes 15 knowledge groups. The network shows a differentiated structure with three smaller and five major points of focus. The compactness of the clusters indicates that the sources within the clusters are closely related. The fact that all lines of research identified in the previous period can be found again in this period indicates that there is a constant structural framework within which the individual lines of research can develop. Furthermore, there is a high degree of continuity with regard to the theoretical and methodological orientation of the knowledge groups. There are also new foci which emerged in the second period and were able to establish itself as a line of research over the course of time. The overall density of the entire network is 0.37 and hence slightly higher than in the previous period. On an individual level, the clusters in the earnings management category became denser whereas the clusters on executive compensation and audit services became looser.

Figure 2: Co-citation network 1990-1995

Working Paper: Please do not cite without permission of the authors!

In the co-citation network for the third period from 2002 to 2007 eleven knowledge groups with eight thematic foci are present. The sources within the clusters are similar to the previous period and many clusters are consistent in terms of content, theory and methods, used. Two clusters from the previous time-period established itself as independent lines of

research and one new cluster emerged. The overall density of the network increased to 0.49, showing that the discussion became more focused with a higher degree of exchange and communication. The density of the individual clusters has not changed compared to the previous period.

Figure 3: Co-citation network 1996-2001

Figure 4: Co-citation network 2002-2007

Working Paper: Please do not cite without permission of the authors!

We will now present the detailed results of our analysis grouped by thematic foci. Therefore we will trace the development of the clusters over the three time-periods.

In the first period a large number of articles in three distinctive knowledge groups deal with earnings management issues. Cluster A1 has 4 completely interlinked sources on the information content of earning announcements. Cluster A2 is a low density (0.17) cluster with 18 sources. The articles mainly deal with the relation between stock market returns and earning announcements. The most central articles in this cluster are by Beaver/Lambert/Morse (1980) and Kormendi/Lipe (1987), which focus on tests of the information contained in accounting earnings and security prices. Cluster A3 is the biggest knowledge group in this network with 24 sources, consisting of three sub-clusters. Sub-cluster A3a consists of four sources with an article of Leftwich (1981) as central source. All four articles deal with mandatory accounting changes. Sub-cluster A3b has a total of 11 sources, on the consequences of accounting choices. The central article in this cluster is by Daley/Vigeland (1983) on the effects of debt covenants and political costs on the choice of accounting methods. Sub-cluster A3b and sub-cluster A3c are connected by two prominent sources by Watts/Zimmerman (1980/1990) on positive accounting theory. Sub-cluster 3c has 8 sources, combining the discussion about earnings management with accounting choice. The central article in this sub-cluster is by DeAngelo (1986) on accounting numbers as market valuation substitutes.

In the second period 1996-2001 there are also three clusters that deal with earnings management but with considerably less sources. Nonetheless, the high density of all clusters in the second period indicates the intensified exchange of ideas on this topic. Cluster B1 has 4 sources which were all also present in cluster A2. The central source in this knowledge group is the article by Collins/Kothari (1989) on intertemporal and cross-sectional determinants of earnings response coefficients. Cluster B2 has 9 sources which were partly also present in cluster A3c. These articles mainly deal with earnings management, with a focus on the manipulative effect of bonus schemes and accruals. The central source is by Jones (1991) on earnings management during import relief investigations. Knowledge group B3 also consists of 9 sources with a focus on event-studies. The central source is by Bernard/Thomas (1990) which shows evidence that stock prices do not fully reflect the implication of current earnings for future earnings.

In the third time period there is no distinctive cluster which deals with earnings management issues. The earnings management topics merged into the central cluster C1 of this time period. By using Newman grouping3 one can distinguish two sub-clusters which deal

3 Newman grouping is a statistical method which partitions the

network into sub-networks where collaborations occur much

with earnings management as well as related methodological issues and incorporate many articles from the previous time-period. The nine articles in sub-cluster C1a are mainly event studies from cluster B3 of the previous time-period. The central source remains Bernard/Thomas (1990). Sub-cluster C1b includes most of the sources from the previous cluster B2 which deal with bonus schemes and accruals. The central source here is again Jones (1991).

Earnings Management 1990-1995

1996-2001 2002-2007

Using the classification from the Accounting Research

Directory, the strong quantitative and empirical focus of the earnings management discussion gets revealed. This is supported by the fact that the majority of articles uses statistical modeling to test the efficient market hypothesis and can be attributed to financial accounting research. The entire earnings management discussion took place in the US accounting journals JAE, JAR and TAR. There are only a few monographs and sources from outside the field especially economics and finance.

The second main topical area which continuously exists over the entire 18 years time-period is research on disclosure. In the first period there are two quite similar clusters with regard to the content. Articles in both knowledge groups deal with financial, non-financial and discretionary disclosures and their information value. Cluster A4 has ten sources and the central article is Penman (1980), who investigates voluntary disclosure of corporate earnings. In cluster A5 all sources are completely interlinked making it a maximum density cluster. In the second time period there are three knowledge groups with a research focus on disclosures. Cluster B4 has three

more frequently within a group than between groups, with a high statistical confidence level

Working Paper: Please do not cite without permission of the authors!

interlinked sources which all examine the reasons why companies disclose information. Cluster B5 has five sources which partly stem from cluster A4 of the previous time-period and examine the consequences of disclosure under different circumstances.

Disclosure 1990-1995

1996-2001 2002-2007

The central source, interlinked with all other sources, is

Verrecchia (1983) on discretionary disclosure. Cluster B6 has six articles on disclosure policy and the effect on liquidity, cost of capital and external financing with Lang/Lundholm (1993) in the centre. In the third period the clusters B3 and B5 merge into a new, big knowledge group C2 with 26 sources. New topics came up besides the established research streams. The discussions now also deal with the cost of capital or equity premia and the economic consequences of disclosures. The central sources in this cluster C2 are Kasznik/Lev (1995) on management disclosures in the face of earning surprises and Botosan (1997) who examines the disclosure level and the cost of equity capital. Cluster C3 is a small cluster with only four sources mainly from the previous cluster B4. They all contribute to the discussion of the information value of disclosures with Dye (1985) and Verrecchia (1983) as central sources.

The articles over all three time-periods were primarily published in the three big US accounting journals JAE,

JAR and TAR. Unlike before, articles published in finance and economics journals also play a substantive role in this knowledge group, indicating a knowledge transfer from these fields to the accounting. In the majority of the articles, the authors use archival data for their study but there are also a substantial number of articles that use analytical internal logic. The archival studies mainly use regression analysis as mode of reasoning. Almost all of the articles use statistical modeling and either deal with a test of the efficient market hypothesis or information economics. The articles can be attributed to financial accounting research exclusively. From a paradigm perspective, the majority of articles share the capital markets paradigm with a few articles focusing on agency issues.

The third group of articles we are looking at deal with executive compensation. In the first period there is a rather small knowledge group A6 with six sources that deal with moral hazard issues, the performance of executives and their compensation. The central source is on agency theory by Holmstrom (1979). Cluster B7 in the second time-period has 15 sources and all of the sources from the previous period are still present in this cluster. The discussion intensified and now also covers multi-task principal-agent problems and stewardship issues. The central source remains Holmstrom (1979) together with Lambert/Larcker (1987)’s article about the use of accounting and market performance measures in executive compensation contracts. In the third period the discussion becomes less prominent with only ten sources in cluster C4. Four of these ten sources were already present in the previous network B7. The main focus now shifted almost exclusively to performance measurement issues with Feltham/Xie (1994) and Banker/Datar (1989) as central sources.

The majority of the papers in this line of research were published in the most prominent US accounting journals but there are also a considerable number of articles from economics journals. One of the most prominent sources, Holmstrom (1979), for instance, is published in the Bell Journal of Economics. In most of the cases the articles are of an analytical nature. Most of the articles can be attributed to the area of managerial accounting research, using quantitative analysis techniques. Most of the input is drawn either from accounting or the finance and economics literature. The articles share the agency paradigm and contribute to the information economics literature.

Working Paper: Please do not cite without permission of the authors!

Executive Compensation

1990-1995 1996-2001 2002-2007

The fourth thematic group is auditing research. We

labeled this group auditing services because a lot of articles also deal with the quality of audits and similar topics. In the first period there are two knowledge groups, A7 and A8. The first has six sources on audit pricing and audit quality. The central source is Francis/Simon (1987)’s test of audit pricing in the small-client segment of the U.S. audit market. The second has eight sources on auditor expertise and the effects of auditor experience. The central source in this cluster is Libby (1985) with his experiment on the detection of material financial statement errors through preliminary analytical review. In the second time-period there are three knowledge groups on auditing services research. The first network B8 has twelve sources on auditor firm size, audit pricing and audit quality, of which three were also present in the previous cluster A7. The central source in this cluster is Francis (1984) with his study on the effect of audit firm size

on audit prices in Australia. The second cluster B9 has five sources which are all concerned with audit judgment. The central source in this cluster is Kennedy (1993) on debiasing audit judgment with accountability. The last cluster B10 in the second time-period consists of nine sources with three sources that were already present in cluster A8. The articles are about auditor expertise and auditor knowledge with Libby/Luft (1993) on determinants of judgment performance in accounting settings as central reference. In the third time-period the auditing services discussion is integrated in cluster C1. Sub-Cluster C1c consists of several sources which were previously present in Cluster B8. The articles deal with audit pricing, audit quality, auditor brand name recognition and auditor independence. The central source is Frankel/Johnson/Nelson (2002) on the relation between auditors' fees for nonaudit services and earnings management.

Auditing Services 1990-1995 1996-2001 2002-2007

The auditing services discussion exclusively takes

place in accounting journals. The big three US journals publish the most articles in the clusters, with a single source from AOS and one monograph which falls outside this rule. The research method employed in the articles is either archival, using primary data, or empirical with a focus on lab studies. The articles can be attributed to accounting research or psychology as foundation

discipline. The mode of reasoning is predominately quantitative using regression or ANOVA as an analysis technique. The articles contribute either to statistical modeling or the human information processing literature with a strong behavioral focus what also manifests itself in the paradigmatic focus of the knowledge groups.

The fifth major thematic group is research on accounting systems and accounting data. The focus of

Working Paper: Please do not cite without permission of the authors!

these knowledge groups is on the discussion of historic aspect of social and organizational contextual factors of accounting systems and the use of accounting data. In the first time-period there are two accounting systems and data knowledge groups. The first consists of 19 sources which are separated in two sub-clusters A9a and A9b. Articles in sub-cluster A9a are predominately concerned with the organization of the accounting body whereas the sub-

Accounting Systems and Data 1990-1995

1996-2001

2002-2007

cluster A9b deals with the role of accounting in organizations and society and management control issues. The central source in cluster A9 is Miller/O’Leary’s (1987) historical examination of the interrelation of accounting with other projects for the social and organizational management of individual lives. The cluster also contains an article by Watts/Zimmerman (1979) that seems to be displaced. Taking a closer look it gets obvious that the other sources in the cluster tend to dissociate themselves from this line of research what manifests the appearance of this article. The second cluster A10 with six sources is centered on the role of accounting data and budgeting. The central articles in this cluster are Brownell (1982) and Brownell/Hirst (1986) who deal with the role and reliance on accounting data. In the second time-period the discussion about accounting systems is not present, whereas the knowledge group on accounting data gets bigger, now incorporating 15 sources in cluster B11. The articles not only deal with accounting data and budgeting issues, but also management control systems and the effects on competition. The central source in this cluster is Bruns/Waterhouse’s (1975) article on budgetary control

and organization structure. In the third time-period the knowledge group on accounting systems re-emerges and the discussion on accounting data narrows down to management control systems. Cluster C5 has six sources which were mainly also present in sub-cluster A9b, again dealing with the role of accounting in organizations and society. The central source in this cluster is once again Miller/O’Leary (1987). Cluster C6 has four sources with two articles from Langfield-Smith (1997) and Chenhall (2003) on the design and usage of management control systems in its core.

The literature on accounting systems is mainly published in AOS, whereas the literature on accounting data predominately appeared in JAR with a minor share of articles from AOS. This group is the only that shows equal references from the heterodox as well as the mainstream camp. There are also a considerable number of monographs included in all the clusters. Most of the articles use analytical methods, predominately internal logic, as research method. The articles can be attributed to the field of management accounting or the sociology, political science and philosophy literature. Almost all the articles use a qualitative analysis technique and contribute to behavioral accounting research, accounting theory or accounting history which manifests itself in the behavioral paradigm.

There are several lines of research which are not present over the entire period of consideration. Some just came up in the last years; others were able to become an integral part of the accounting research agenda. These knowledge groups deal with topics like research about analyst forecasts, valuation issues and corporate governance.

Analyst forecast 1996-2001

2002-2007

Working Paper: Please do not cite without permission of the authors!

Knowledge groups discussing the formation and consequences of analyst forecasts came up in the second time-period and gained relevance over the course of time. In the beginning four sources in cluster B12 dealt with this topic. The central source is Dugar (1995) and his investigation of the effect of investment banking relationships on financial analysts' earnings forecasts as central source. In the third time-period network C7 already counted 20 sources of which 13 can be directly attributed to research on analysts’ decisions and the resulting consequences. The remaining seven sources in this cluster deal with earnings management, a related topic. The central source in cluster C7 is Lin/McNichols (1998) on underwriting relationships, analysts' earnings forecasts and investment recommendations.

Most of the sources in both networks were published in US journals although the Canadian journal CAR has a strong influence in this knowledge group. The studies most often used primary archival data and employed quantitative analysis techniques. Furthermore they share a capital market paradigm and contribute to the statistical modeling literature about the efficient market hypothesis. Almost all the articles can be attributed to the financial accounting literature.

Valuation 1996-2001 2002-2007

In the second time period a distinct cluster on earnings management and the consequences for valuation emerged and is also detectable with a narrower focus in the third period. Cluster B13 includes seven articles with Feltham/Ohlson (1995) on valuation and clean surplus accounting for operating and financial activities as central source. This article is also present in cluster C8 in the third time-period.

The articles in both clusters are mainly from CAR and use analytical methods to statistically model the relevance of the efficient market hypothesis. The focus lies on capital markets and all articles can be attributed to financial accounting research.

Research on corporate governance issues, is only present in the third time-period. There are two knowledge groups in this last period. In cluster C9 articles deal with the separation of ownership and control and SEC enforcements. The central source in this cluster is Dechow/Sloan/Sweeney (1996) on causes and consequences of earnings manipulation. In cluster C10 the articles deal with conservatism in accounting as well as law and accounting. The central source of this cluster is Ball/Kothari/Ashok (2000) on the effect of international institutional factors on properties of accounting earnings.

Corporate Governance 2002-2007

The articles in both clusters were mainly published in the big US accounting journals; others appeared in finance or economics journals. Almost all rely on primary or secondary accounting data, use quantitative analysis techniques and can be attributed to financial accounting research. There is not yet a clear shared paradigm between the articles showing the relatively young age and diverse approach taken in the articles.

Miscellaneous 1996-2001 2002-2007

There are two related clusters in the second and one in the third time-period which can be regarded as independent research streams. Cluster B14 has six sources and a clear focus on accounting choice in the context of commercial banks. The central source of this cluster is Beatty/Chamberlain/Magliolo (1995) who deal with the influence of taxes, regulatory capital and earnings on financial reports of commercial banks. Cluster B15 with also six sources deals with the effect of fair value accounting in the context of banks and pensions. The central source is Barth (1994) with evidence on fair value accounting from investment securities and the valuation of banks. Cluster C11 in the third time-period has three sources which deal with the relevance and boundaries of financial statements.

In summary, the results show an astonishing continuity with regard to the underlying structures of accounting research. There are five topical areas which are persistent over all three time periods. Two topics that came up in the second period are also present in the third. And only one new topic emerged in the third period. Taking a look at the

Working Paper: Please do not cite without permission of the authors!

paradigms present in accounting research, it gets obvious that the discipline is dominated by a capital market oriented viewpoint which gained influence in recent times. In the earnings management knowledge group, a shift took place from positive theory towards capital markets as underlying paradigm. Similar developments can be seen in auditing services research, where the behavioral focus comes to the fore, at the expense of the protagonists of the positive theory. The accounting systems & data category is the most dynamic in our analysis. Not only the thematic focus shifts from accounting systems in the first to an exclusive cluster of accounting data research in the second period, also the paradigm shifts from accounting theory towards a more accounting history oriented discussion. The discussion on executive compensation is fairly stable, experiencing no shift in either paradigmatic focus or research method. The disclosure discussion is also relatively stable and gets more relevant over the course of time, integrating several previously independent discussions into one.

In this section we addressed our second goal, by identifying and visualizing the evolution of the major knowledge groups in accounting research. We will now move on discuss the results of the citation and co-citation analysis. We will end our analysis by pointing out the limitations and indicating the future direction of research in this area.

Discussion and Implications This paper uses citation and co-citation analysis to

examine key facets of the intellectual structure of accounting research. Relative to our set goals, we first analyzed the most frequently cited publications in the five major accounting journals over a period of 18 years. We found that journal articles published in the North American accounting journals dominate the references. The most cited monographs were either theoretical or guidance books for statistic analysis. We furthermore found the most cited article to be a technical paper from outside the discipline. Besides that, articles from finance and economics journals had the greatest impact on the discipline. We furthermore showed that most of the articles deal with the test of theories from the economics and finance literature using quantitative analysis techniques. This stream of research is likely to increase in popularity as has been showed by the recent changes in the structure. A marginal number of accounting theory papers can be found among the top-50, showing the declining influence and popularity of a-priori research. We then moved on to a co-citation analysis to determine the major knowledge groups, their evolution over the time and their interrelationships.

We first looked on the overall structure of the networks and found that the density increased over the last years, showing that the discussion among the knowledge groups became more focused and that a higher degree of exchange

and communication took place. This is likely to be the result of the shifts in the research agenda of accounting and the ongoing concentration on quantitative analysis techniques to test the efficient market hypothesis. We then looked on the individual knowledge groups in more detail and found a high consistency within them in terms of research method, mode of reasoning and school of thought. Most of the knowledge groups could be attributed to a paradigm in accordance with Brown’s (1996) classification.

This indicates that the structure of accounting research is fairly solid. The structures identified in the co-citation analysis indicate that the topic areas and paradigms of accounting research provide a framework that does not change dramatically over time and within which knowledge can be transferred reasonably efficiently. The individual clusters are homogenous in terms of content, theory and methods used. Furthermore, typical journals can be attributed to the clusters, whereby AOS and the group of North American journals (JAE, JAR and TAR) are identified as crystallization points for different approaches in accounting research. All of these features are stable over time which indicates that the transfer and exchange of knowledge observed in leading accounting journals takes place more and more under one umbrella.

From a theoretical viewpoint, the clusters identified lean toward finance and economics; in terms of methods used, large-scale empirical and formal-based analytical research dominates. This suggests that the knowledge is highly codified and that the clusters are theoretically compatible, both of which are conducive for forming networks as seen over the three periods investigated. To support this conjecture, we can compare it with the development of the heterodox “accounting theory” and “accounting history” clusters, which tend to be less codified due their historical, sociological and philosophical orientation. There is empirical evidence that these clusters defined themselves as being distinct from the mainstream, and based this self-conception on a common canon of basic sources, but over time they differentiated and specialized, leaving a comparatively small core of constitutive sources. As the co-citation analysis also shows, hardly any knowledge is exchanged between the mainstream and the heterodox camp. Increasingly, this development is seen as a major risk for the field. Lukka/Mouritsen (2002) claim that for management accounting the adoption of an economics-based monolithic paradigm would limit the abilities to construct and examine interesting propositions, develop meaningful stories and integrate the research in its social, organizational and behavioral contexts.

Working Paper: Please do not cite without permission of the authors!

Table 4: Summary of results Thematic

focus Cluster Paradigm Description

Earnings management

A1, A2, A3 B1, B2, B3, C1a, C1b

Capital Market/ Positive Theory/ Forecasting

Strong quantitative and empirical focus Majority of articles uses statistical modeling to test the efficient market hypothesis and can be attributed to financial accounting research The entire earnings management discussion took place in the US accounting journals JAE, JAR and TAR. There are only a few monographs and sources from outside the field especially economics and finance.

Disclosure

A4, A5, B4, B5, B6, C2 and C3

Capital Market, Agency

Authors predominately use archival data for their study. There are also a substantial number of articles that use analytical internal logic. Almost all of the articles use statistical modeling and either deal with a test of the efficient market hypothesis or information economics. The articles can be attributed to financial accounting research exclusively. Articles were primarily published in the three big US accounting journals JAE, JAR and TAR. Articles published in finance and economics journals also play a substantive role in this knowledge group

Executive Compensation

A6, B7 and C4

Agency Articles are mostly of an analytical nature and can be attributed to managerial accounting research, using quantitative analysis techniques. Most of the input is drawn either from accounting or the finance and economics literature. The articles share the agency paradigm and contribute to the information economics literature. The majority of the papers in this line of research were published in the most prominent US accounting journals but there are also a considerable number of articles from economics journals.

Auditing Services

A7, A8, B8, B9, B10 and C1c

Positive Theory/ Behavioral

Research method employed in the articles is either archival, using primary data, or empirical with a focus on lab studies. The articles can be attributed to accounting research or psychology as foundation discipline. The mode of reasoning is predominately quantitative using regression or ANOVA as an analysis technique. The articles contribute either to statistical modeling or the human information processing literature with a strong behavioral The discussion exclusively takes place in accounting journals.

Accounting Systems & Data

A9, A10, B11, C5 and C6

Behavioral/ Accounting Theory and Accounting History

Most of the articles use analytical methods, predominately internal logic, as research method. The articles can be attributed to the field of management accounting or the sociology, political science and philosophy literature. Almost all the articles use a qualitative analysis technique and contribute to behavioral accounting research, accounting theory or accounting history The literature on accounting systems is mainly published in AOS, whereas the literature on accounting data predominately appeared in JAR There is also a considerable number of monographs to be found

Analyst forecasts

B12 and C7

Capital Market The studies most often used primary archival data and employed quantitative analysis techniques. They share a capital market paradigm and contribute to the statistical

Working Paper: Please do not cite without permission of the authors!

modeling literature about the efficient market hypothesis. Almost all the articles can be attributed to the financial accounting literature. Most of the sources were published in US journals although the Canadian journal CAR has a strong influence

Valuation

B13 and C8

Capital Market Use of analytical methods to statistically model the relevance of the efficient market hypothesis. All articles can be attributed to financial accounting research Journals: Predominately CAR

Corporate Governance

C9 and C10

n/a n/a

Miscellaneous B14, B15 and C11

n/a n/a

LIMITATIONS Several limitations of our analysis should be recognized