the influence of global financial crisis and good

TRANSCRIPT

ROCEEDINGS THE 2nd INTERNATIONAL CONFERENCE OF BUSINESS, ACCOUNTING AND ECONOMICS “Economics Strength, Entrepreneurship, and Hospitality for Infinite Creativity Towards Sustainable

Development Goals (SDGs)”

1

The Influence of Global Financial Crisis and Good

Corporate Governance Mechanisms on Earning

Management (Study of Property and Real Estate

Companies listed on the Indonesia Stock Exchange for the

period 2008-2018)

Dyah Anggraeni Purnomo [email protected]

Student Faculty of Economy and Business, University of Muhammadiyah Purwokerto.

Abstract. This studi aims to analyze the effect of the Global Financial Crisis and Good Corporate Governance Mechanisms (which are proxided by managerial ownership, institusional ownership, board of

commissioners and audit committees) on the Earning Management of Property and Real Estate companies listed on the Indonesia Stock Exchange for the period 2008-2018. The sampling method used is purposive sampling. Based on the purposive sampling method, there were 77 samples obtained. The results showed that global financial crisis did not significantly influenece earnings management, and good corporate governance (which was proxided by managerial ownership had no significant effect on earnings management, while institutional ownership and the independent board of commissioners had a significant effect on earnings management, most recently the audit committee no significant effect on earning management).

Keywords: global financial crisis, good corporate governance, earning management

INTRODUCTION

The global financial crisis that took place in 2008 was the financial crisis caused by

housing credits in the United States. The global financial crisis itself is influential not only in the

United States, but also in other countries, including Indonesia. In addition to the global financial

crisis there is also a global economic throttling.

Such circumstances lead to a wide range of conditions faced by major financial institutions in the United States that affect the liquidity of other financial institutions, both in the

United States and outside of the country. This applies to countries investing through major

financial institutions in the United States.

The term Good Corporate Governance (GCG) is known as Cadbury report. Good

corporate governance is a means or mechanism to provide assurance to the investor in obtaining

the correct return for the invested investment [5].

[6] explained that the application of consistent corporate governance principles will

reduce the possibility of earning managements resulting in the fundamental value of the company

not being described in its financial statements.

In accordance with the problems that have been formulated above, the purpose of this

research is to analyze the influence of the Global financial crisis and the mechanism of Good Corporate Governance (which is proscribed by managerial ownership, institutional ownership,

BOC and Audit Committee) on Earning Management of Property and Real Estate companies listed

on the Indonesia Stock Exchange period 2008-2018.

In this study the Global financial crisis was measured using calculations on the financial

Stress Index, CG was seen from the mechanism using a managerial ownership proxy, institutional

ownership, BOC, and Audit committee while earning management was measured using

discretionary accrual (DAC). Research data is taken from the company's annual report property

and real estate period 2008-2018.

ISBN: 978-602-6697-54-7

2

LITERATURE REVIEW

Global Financial Crisis

The global financial crisis is a condition in which all countries experience instability in

the economy. As we know, the financial crisis that occurred in 2008 made economic growth in all countries run slowly. This crisis originated from the housing credit crisis in the United States

which affected global financial conditions in the United States, Europe, and Asia. The impact

received as a result of the global financial crisis is different for each country, depending on the

policies taken and the economic fundamentals of the country concerned, therefore the handling is

also different.

In 2008, Indonesia economic growth was 6.1 percent. The impact of the global financial

crisis on the Indonesia economy began to be felt in the fourth quarter of 2008, because during that

quarter economic growth decreased by minus 3.6 percent compared to the third quarter which

increased by 5.2 percent.

In Indonesia itself, the global financial crisis in 2008 also had an impact on the property

sector, in 2007 demand for apartments reached 13,400 units with a supply of 13,800 units. Then,

during the crisis, demand for apartments reached -39% which continued until 2010. Learning from the experience of the previous crisis, developers were careful to delay project launches until

conditions improved. With the declining GDP condition, high interest rates, the value of the

Rupiah exchange rate was at Rp. 11,000 certainly affects the property's performance, but it doesn't

last long.

The global financial crisis had 3 main impacts on housing and settlements, namely (1)

drying up of liquidity, which not only affected world businesses, but also government financing of

development; (2) a decrease in the level of demand and Indonesia's main export commodities

without a significant reduction in the rate of imports which causes a trade deficit: and (3) a

decrease in the level of consumer, investor and market confidence in various existing financial

institutions (Handbook 2009). The financial crisis is one of the variables that has an influence on

earnings management. Previous studies have found that companies engage in earnings management in response to financial crises to deal with poor corporate financial conditions (eg [9];

[14]; [33]). There are various indicators of the impact of the American crisis on the Indonesian

nation, including the decline in the stock price index on the IDX sharp, the decline in the rupiah

exchange rate against the US dollar which has already crossed the psychological threshold, so that

the banking sector is experiencing liquidity difficulties and even the Government has difficulty

finding loans on the financial market [28]. In this study, it was measured using calculations on the

financial stress index with the following formula:

FSI = [$ / TL Variation in Nominal Exchange Rate (%)] + [Variation in Interest Rate of TL (%)] -

[Variation in Gross Reserves (%)].

Agency Theory

Agency theory is the theoretical basis used by companies to understand corporate

governance. In this theory, it is explained that there is a contractual relationship between the

principal (owner and shareholder) and the agent (management) (Jensen and Meckling, 1976). This

means that there is a separation between ownership and management of the company. Principals

and agents make work contracts through mutual consent as a form of principal authority and

responsibility to the agent. Contracts that have been made refer to net income, so this agency

theory has an influence on accounting.

In agency theory, this states that earnings management practices are influenced by

conflicts of interest between agents and principals, because each party strives to achieve the desired level of prosperity. The owner (the principal) agrees to carry out the cooperation contract

with the agent because he wants to make himself prosperous increased profitability, while the

manager (agent) wants to carry out a cooperation contract with the principal because it is to fulfill

their economic and psychological needs to the fullest, whether it is obtaining investment, loans or

compensation contracts. Therefore, there are two different interests in the company where each

party tries to achieve or maintain the desired level of prosperity.

ROCEEDINGS THE 2nd INTERNATIONAL CONFERENCE OF BUSINESS, ACCOUNTING AND ECONOMICS “Economics Strength, Entrepreneurship, and Hospitality for Infinite Creativity Towards Sustainable

Development Goals (SDGs)”

3

Problems that arise because of differences in the interests of principals and agents are

called agency problems. One of the causes of agency problems is the presence of asymmetric

information. Asymmetric information is the imbalance of information held by principals and

agents, when principals do not have sufficient information about the agent's performance and vice

versa, and agents have more information about their capacity, work environment and the company

as a whole[28].

Financial Report

The financial report is a process of recording financial transactions that occur in a certain

accounting period. Financial reports according to PSAK No. 1 (2005: 1), financial statements are a

structured presentation of the financial position and financial performance of an entity. This

financial report is prepared by management as the responsibility for the duties assigned to it by the

owner of the company and as a report to parties outside the company. According to [12] financial statements prepared by management consist of:

a. Balance sheet

Balance sheet is a financial report that systematically presents the company's

financial position at a certain date. This report is prepared to present financial

information regarding the company's assets, liabilities and capital. The balance sheet

is presented based on the company's liquidity and financial flexibility, which can be

used as a basis for making estimates of the company's financial conditions in the

future. Liquidity is the company's ability to pay its obligations on time according to a

predetermined time. Meanwhile, flexibility is the company's ability to obtain funds.

b. Income statement

Profit / Loss Report is a financial report that systematically results from the company's operations within a certain period of time. In this case, the profit / loss

statement provides information regarding the determination of profitability,

investment value and creditworthiness or the ability of the company to repay the

loans required by investors and creditors to help them predict the amount, timing and

certainty of future cash flows.

c. Cash flow statement

The cash flow statement is a report that can provide information about the company's

ability to generate cash and cash equivalents during a certain period. This report

presents information systematically about cash receipts and payments during a

certain period based on operating, investing and financing activities.

d. Statement of Changes in Equity

The change in equity report is a financial report that systematically presents information about changes in the company's equity as a result of company operations

and transactions with owners during a certain accounting period.

Financial reports are one of the main sources of financial information that is

important for a number of users for making economic decisions. According to SFAC

No. 2 financial information will be useful if it meets the following quality

characteristics:

1) Relevant

2) Reliability

3) Appealability and Consistency

4) Cost-Benefit Considerations

5) Materiality

Profits

According to [18], it is stated that profit is accounting profit which is the difference

between income and cost measurements. According to SFAC No. 1, earnings information has the

benefit of assessing management performance, helping to estimate the long-term representative

earnings capacity, predicting earnings and assessing risk in investment.

Profits can show the profits earned by the company and are listed in the income

statement. The income statement is a report that shows the revenues and expenses of a business

unit for a certain period. The difference between revenues and expenses is the profit earned or lost

by the company.

ISBN: 978-602-6697-54-7

4

The benefit of financial information contained in the income statement is to (1) assess the

success or failure of the company's operations and management efficiency, (2) estimate the amount

of future profit, (3) assess the profitability or profitability of capital invested by owners.

Corporate Governance

Definition and Objectives of Corporate Governance

In the Cadbury Report, the first time the term Good Corporate Governance (GCG) was

introduced in 1992 by the Cadbury Committee in its report. Corporate governance is the principle

of directly controlling the company in order to achieve a balance between the strength and authority of the company in providing accountability to shareholders in particular and

stakeholders. Good corporate governance is a means or mechanism to provide assurance to

investors in getting the right return for the investment that has been invested [5].

Meanwhile, [16] argues that corporate governance is a set of regulations that regulate the

relationship (in other words as a system that controls the company) between shareholders,

company managers, creditors, government, employees and shareholders. other internal and

external interests relating to their rights and obligations. So that it can be concluded that the

definition of good corporate governance is a system, process, and regulatory tools that regulate the relationship between shareholders, the board of commissioners, and the board of directors in order

to achieve company goals. While the goal of good corporate governance is to create added value

(value added) for all interested parties (stakeholders).

Benefits of Corporate Governance

According to the Forum for Corporate Governance in Indonesia [15] are:

a. Improve company performance through the creation of a better decision-making

process, increase the company's operational efficiency and further improve services to

stakeholders.

b. Make it easier to obtain cheaper financing funds so as to increase corporate value.

c. Restoring investor confidence to invest in Indonesia.

d. Shareholders will be satisfied with the company's performance because at the same

time it will increase shareholder value and dividends.

Principles of Corporate Governance

The basic principles of implementing good corporate governance put forward by the

Forum for Corporate Governance in Indonesia [16] are as follows: a. Fairness (justice). Ensure fair and equal treatment in fulfilling rights shareholders who

arise under the agreement and the prevailing laws and regulations. This principle

emphasizes that all parties, namely both minority and foreign shareholders, must be

treated equally.

b. Transparency (transparency). Requires open, accurate and timely information about all

matters that are important to company performance, ownership and stakeholders.

c. Accountability (accountability). Describe the functions, structures, systems and

responsibilities of company organs so that company management is carried out

effectively. This principle confirms the accountability of management to the company

and its shareholders.

d. Respobsibility (responsibility). Ensuring conformity (compliance) in the management of the company to a healthy corporation and applicable laws and regulations. In this case

the company has a social responsibility towards the community or stakeholders and

avoids abuse of power and upholds ethics business while maintaining a healthy business

environment.

Corporate Governance Mechanism

Mechanism is a systemic way of working something to meet certain requirements. The

corporate governance mechanism is a clear process and relationship between those who make

decisions and those who control or supervise a decision. According to [19] and [21], the

mechanisms for monitoring corporate governance are divided into two groups, namely internal and

external mechanisms. Internal mechanisms are ways to control a company using internal structures

ROCEEDINGS THE 2nd INTERNATIONAL CONFERENCE OF BUSINESS, ACCOUNTING AND ECONOMICS “Economics Strength, Entrepreneurship, and Hospitality for Infinite Creativity Towards Sustainable

Development Goals (SDGs)”

5

and processes such as general meetings of shareholders (GMS), composition of the board of

directors, composition of the board of commissioners and meetings with the board of directors.

Meanwhile external mechanisms are ways of influencing the company other than by using internal

mechanisms, such as control by the company and market control.

There are several corporate governance mechanisms that are often used in research to

determine their effects on earnings management, including managerial ownership, institutional

ownership, the board of commissioners and the audit committee. The concentration of ownership

in the company will put the shareholders in a strong position. Due to the holder stocks hold control

over management to demand that they report finances accurately. Similar to the role of the board

of commissioners in carrying out the supervisory function, the composition of the board can

influence management in preparing financial reports so that a quality earnings report can be

obtained [3]. Meanwhile, the audit committee has an important and strategic role in maintaining the

credibility of the financial report preparation process, maintaining the creation of an adequate

company supervision system and implementing good corporate governance. With the function of

the audit committee running effectively, the control of the company will be better so that agency

conflicts that occur due to management's desire to improve their own welfare can be minimized

[2]. This proves that the corporate governance mechanism is able to reduce the manipulation of

financial reports by managers. The practice of manipulation is commonly known as earnings

management.

Earning Management

Earnings management is a process carried out by financial management on purpose, in

accordance with accounting practices so that profits are what the company wants. Earnings management is a condition in which management intervenes in the process of preparing financial

reports for external parties so that it can even, increase, and decrease earnings (Schipper, 1989).

The concept of earnings management according to Salno and Baridwan (2000) which uses the

agency theory approach states that: "Earnings management practices are influenced by conflicts of

interest of management (agent) and shareholders (principals) that arise because each party tries to

achieve or consider the level of prosperity it wants.

Previous Research Results Some of the test results from previous studies can be seen from table 1 as follows:

Tabel 1

Previous Research

No Author and

year Tittle Variable Result

1.

DeFond &

Jiambalv

(1994)

Debt covenant

violation and

manipulations

of accruals

Contracting,

accounting

choice, debt

covenant

violation,

accruals

manipulation

Implications regarding

the discussion

relationship between

debt restriction and

options accounting

implications regarding

the discussion

ISBN: 978-602-6697-54-7

6

2. Healy &

Wahlen (1999)

A review of

the earnings

management

literature and

its

implications

for standard setting

Earning

management,

earning reported

and accruals

Believe that

contribution will come

from documentation

level and magnitude

for certain accruals of

reconciliation findings

were each other

conflicted on influence

profit management at

the stock price and

allocation resource in

economy and from identifying which

factors

limit earnings

management.

.

3. Chtourou

(2001)

Corporate

Governance

and Earnings Management

Audit committee

board of director

characteristics

The audit committee

and the independent

board of

commissioners have a significant effect on

EM

4. Widyaningdyah

(2001)

Analisis

faktor-faktor

yang

berpengaruh

terhadap

earning management

pada

perusahaan go

public di

Indonesia

Profit

management,

discretionary

accrual, initial public offering

(IPO), leverage

leverage has a

significant effect on earning management

5.

Darmawati

(2003)

Corporate

governance

dan

manajemen laba: suatu

studi empiris

Corporate

governance,

earning

management, accrual

discretioner

No negative

relationship was found

between corporate

governance variables and earnings

management through

discretionary accruals

ROCEEDINGS THE 2nd INTERNATIONAL CONFERENCE OF BUSINESS, ACCOUNTING AND ECONOMICS “Economics Strength, Entrepreneurship, and Hospitality for Infinite Creativity Towards Sustainable

Development Goals (SDGs)”

7

6. Wedari (2004)

Analisis

pengaruh

proporsi

dewan

komisaris dan keberadaan

komite audit

terhadap

manajemen

Audit committee,

board of

commissioners

proportion, big 4

public accountants,

managerial and

institutional

ownership

The audit committee

and the board of

commissioners have a

significant effect on

earnings management, managerial and

institutional ownership

have an effect on

earnings management

positive on earnings

management

7. Cornett et al

(2006)

Earnings

management,

corporate

gpvernance

and true

financial performance

Institutional

ownership of

share, comittee

audit,

characteristic of

BOC (CEO

duality size of

the board directors, CEO's

age, CEO's

tenture)

concentration of

institutional ownership

is not able to reduce

earnings management

activities in the

company

8. Chia, Lapsey &

Lee (2007)

Choice of

auditors and

earnings

management

during the Asian

financial

crisis

Auditing, asian

studies, financial

performance,

earnings, corporate

governance

auditors as an external

governance

mechanism in

influencing earnings

oriented corporate

management in a highly regulated

environment during

the economic financial

crisis

9. Moreira &

Pope (2007)

Earnings

management,

to avoid

losses: A cost of debt

explanation

Earnings

management,

earnings

thresolds, earning discontinuities.

Cost of debt

income distribution is

a shared effect and a

set of firms with

different incentives manipulate earnings

10. Cheng, Johnson

& Liu (2013)

The

supplemental

role of

operating cash

flows on

explaining share returns:

Effects of

earnings

quality

Accounting

earnings, cash

flow, returns,

financial

accounting,

operating

cashflow, earnings quality,

firm valuation,

united satates of

America

Better earnings quality

further increases the

value relevance of operating cash flows

ISBN: 978-602-6697-54-7

8

11. Difa Dini

Asfari (2015)

Analisis

financial

stress

indicator

sebagai alat

ukur stabilitas

sektor

keuangan

Indonesia

Financial

stability,

financial stress,

financial sub-

sector

FSI 1 components

(banking subsector,

bond market and

financial sector) are

sensitive to

fluctuations in the

financial crisis

12. Dutzi &

Rausch (2016)

Earnings

management

before

bankruptcy: a review of the

literature

Earnings

management,

bankruptcy, pemeriksaan

stress levels and audit

opinion are consistent results

13. Xu & Ji, 2016

Earnings

management

by top

Chinese listed

firms in

response to the global

financial

crisis

Discretionary

accruals, cash

flow-based

earnings

management,

income direction management, the

global financial

crisis, Chinese

enterprises

Leading Chinese

companies analyzed

did not engage

earnings management

during the GFC period or its characteristic

earnings behavior

14. Ines Lisboa

(2017)

Impact of

financial

crisis and

family control

on earning management

of

Portuguesed

listed firms

Earnings

management,

family control, financial crisis,

accrual, real

activities

There is a negative

correlation between

operating cash flow / leverage and

discretionary accruals

Source: Developed for this research

FRAMEWORK OF THEORETICAL THINKING AND HYPOTHESIS

FORMULATION

The financial crisis is one variable that affects profit management. Previous studies found

that the company was involved in profit management in response to the financial crisis to address

poor corporate financial conditions e.g. [9]; [14]; [33].

To understand corporate governance using agency theory which is the foundation of the

theory that is usually used by the company. In theory it is explained that there is a contractual

relationship between the principal (owner and shareholder) and the Agent (management) (Jensen

and Meckling, 1976).

The Influence of Global Financial Crisis on Earning Management

Over the last 80 years the worst financial crisis is the global financial crisis that occurred in the year 2008, called the mother of all crises by the world's economists. This crisis was due to

ROCEEDINGS THE 2nd INTERNATIONAL CONFERENCE OF BUSINESS, ACCOUNTING AND ECONOMICS “Economics Strength, Entrepreneurship, and Hospitality for Infinite Creativity Towards Sustainable

Development Goals (SDGs)”

9

the issuance of housing credits in the United States. Not only in the United States, but also

influential in other countries including Indonesia. Previous studies found that the company was

involved in profit management in response to the financial crisis to address poor corporate

financial conditions e.g. [9]; [14]; [33].

H1: Global financial crisis has a significant impact on earning management.

The Influence of Managerial Ownership on Earning Management

The managerial ownership is the shareholder who means the owner in the company of the

management that is actively in the decision making in the company concerned [13]. According to

[4], managerial ownership is the level of shareholding by management who is actively involved in

decision making. So, the shares owned by the management either personally or shares owned by

the subsidiary is a managerial ownership (KM).

H2: Managerial ownership has significant impact on earning management.

The Influenece of Institutional Ownership on Earning Management

Institutional ownership relates to better monitoring of management activities, to reduce

the ability of opportunistic managers to manipulate profits (Kazemian & Sanusi, 2015).

H3: Institutional ownership has significant impact on earning management.

The Influence of Board of Commissioners on Earning Management

The Board of Commissioners is the culmination of internal management system of the

company has a very important role in the company, especially in the implementation of good

corporate governance.

H4: Board of Commissioners has significant impact on Earning Management.

The Influence of the Audit Committee on Earning Management

According to OJK Regulation 55/POJK/. 04/2015, stated that in order to support the effectiveness of the implementation of its duties and responsibilities, the Board of Commissioners

must form the Audit Committee board. The role of the Audit Committee is to examine, advise and

supervise the financial information that will be published regarding adherence to statutory

regulations. Therefore, the role is expected to minimize profit management.

H5: The Audit Committee has significant effect on Earning Management.

RESEARCH METHODS

Research Variables

The global financial crisis is measured using computation on the financial Stress Index,

CG is seen from the mechanism using a managerial ownership proxy, institutional ownership,

BOC, and Audit committee while earning management is measured using discretionary accrual

(DAC).

Sampling The population used in this study were all companies listed on the Indonesia Stock

Exchange and published financial statements during the year 2008-2018. The sample

determination in this study uses purposive sampling. With the method found 7 companies, so the

total sample in the study amounted to 77 samples.

Method of Analysis

Method used in this research is using multiple regression model. This is done because the

independent variables that are applied in the research are more than one. Equation regression with

the following formula:

Description:

Y = earning management

X1 = global financial crisis

X2 = managerial ownership

X3 = institusional ownership

X4 = board of commissioners

X5 = audit comittee

β1 = coefficient global financial crisis

β2 = coefficient managerial ownership β3 = coefficient institutional ownership

Y = α+ β1X1 + β2X2 + β3X3 + β4X4 + β5X5 + e

ISBN: 978-602-6697-54-7

10

β4 = coefficient board of commisioners

β5 = coefficient audit comittee

α = constant

e = error term

RESULTS OF RESEARCH AND DISCUSSION

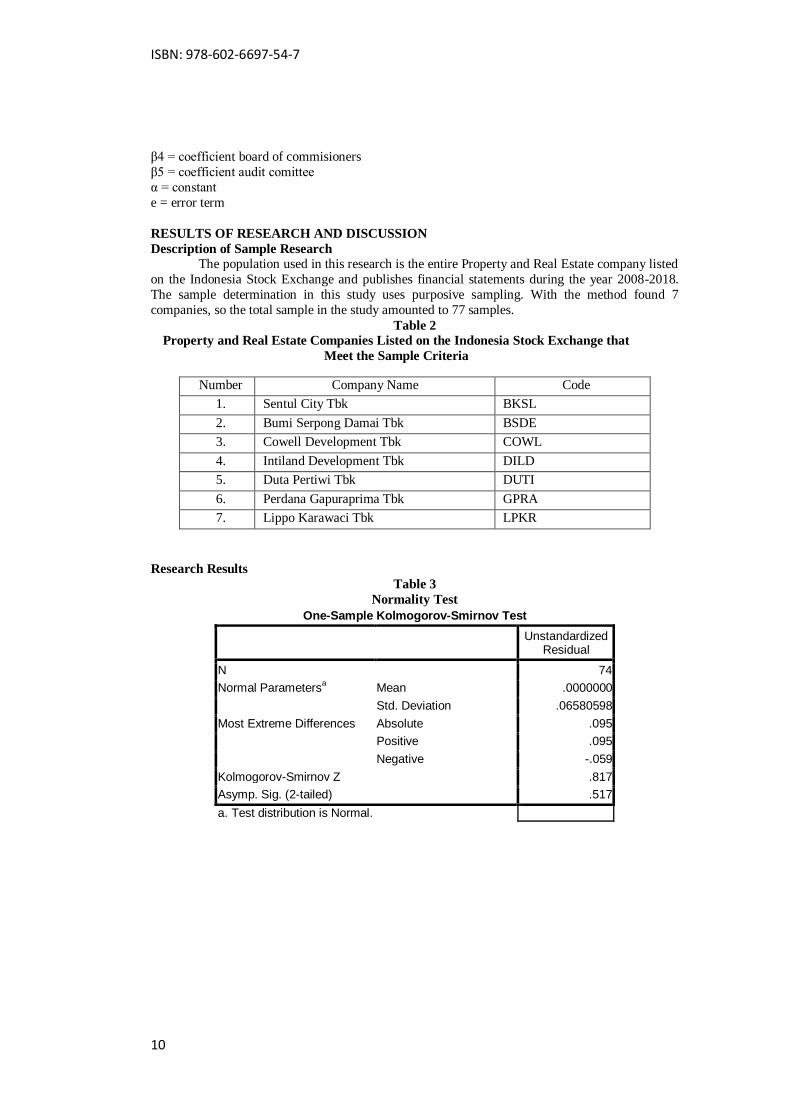

Description of Sample Research

The population used in this research is the entire Property and Real Estate company listed

on the Indonesia Stock Exchange and publishes financial statements during the year 2008-2018.

The sample determination in this study uses purposive sampling. With the method found 7

companies, so the total sample in the study amounted to 77 samples.

Table 2

Property and Real Estate Companies Listed on the Indonesia Stock Exchange that

Meet the Sample Criteria

Number Company Name Code

1. Sentul City Tbk BKSL

2. Bumi Serpong Damai Tbk BSDE

3. Cowell Development Tbk COWL

4. Intiland Development Tbk DILD

5. Duta Pertiwi Tbk DUTI

6. Perdana Gapuraprima Tbk GPRA

7. Lippo Karawaci Tbk LPKR

Research Results

Table 3

Normality Test

One-Sample Kolmogorov-Smirnov Test

Unstandardized Residual

N 74

Normal Parametersa Mean .0000000

Std. Deviation .06580598

Most Extreme Differences Absolute .095

Positive .095

Negative -.059

Kolmogorov-Smirnov Z .817

Asymp. Sig. (2-tailed) .517

a. Test distribution is Normal.

ROCEEDINGS THE 2nd INTERNATIONAL CONFERENCE OF BUSINESS, ACCOUNTING AND ECONOMICS “Economics Strength, Entrepreneurship, and Hospitality for Infinite Creativity Towards Sustainable

Development Goals (SDGs)”

11

Table 4

Multicolinearity Test

Table 5

Heteroskedasticity Test

Coefficientsa

Model

Unstandardized

Coefficients

Standardized

Coefficients

t Sig.

Collinearity Statistics

B Std. Error Beta Tolerance VIF

1 (Constant) .057 .038 1.496 .139

Global Financial Crisis 2.193E-6 .000 .039 .319 .750 .923 1.084

Managerial Ownership -.002 .002 -.149 -1.267 .210 .985 1.016

Institutional Ownership 5.720E-5 .000 .029 .232 .817 .844 1.185

Board of Commisioners .000 .000 .126 .961 .340 .792 1.263

Audit Committee .000 .000 -.193 -1.639 .106 .983 1.017

a. Dependent Variable: ABS_RES

Coefficientsa

Model

Unstandardized Coefficients

Standardized Coefficients

t Sig.

Collinearity Statistics

B Std. Error Beta Tolerance VIF

1 (Constant) .198 .057 3.450 .001

Global Financial Crisis 3.498E-6 .000 .037 .338 .736 .923 1.084

Managerial Ownership -.002 .003 -.092 -.868 .389 .985 1.016

Institusional Ownership -.002 .000 -.485 -4.230 .000 .844 1.185

Board of Commisioners -.002 .001 -.382 -3.231 .002 .792 1.263

Audit Committee .000 .001 .053 .502 .617 .983 1.017

a. Dependent Variable: Earning Management

ISBN: 978-602-6697-54-7

12

Table 6

Autocorrelation Test

Model Summaryb

Model R R Square

Adjusted R

Square

Std. Error of the

Estimate Durbin-Watson

1 .497a .247 .191 .06818 1.856

a. Predictors: (Constant), Audit Committee, Board of Commisioners, Managerial

Ownership, Global Financial Crisis, Institutional Ownership

b. Dependent Variable: Earning Management

Table 7

Determination Coefficient

Model Summaryb

Model R R Square

Adjusted R

Square

Std. Error of the

Estimate Durbin-Watson

1 .497a .247 .191 .06818 1.856

a. Predictors: (Constant), Audit Committee, Board of Commisioners, Managerial

Ownership, Global Financial Crisis, Institutional Ownership

b. Dependent Variable: Earning Management

Table 8

Partial Test (t Test)

Coefficientsa

Model

Unstandardized Coefficients

Standardized Coefficients

t Sig. B Std. Error Beta

1 (Constant) .198 .057 3.450 .001

Global Financial Crisis 3.498E-6 .000 .037 .338 .736

Managerial Ownership -.002 .003 -.092 -.868 .389

Institusional Ownership -.002 .000 -.485 -4.230 .000

Board of Commisioners -.002 .001 -.382 -3.231 .002

Audit Committee .000 .001 .053 .502 .617

a. Dependent Variable: Earning Management

ROCEEDINGS THE 2nd INTERNATIONAL CONFERENCE OF BUSINESS, ACCOUNTING AND ECONOMICS “Economics Strength, Entrepreneurship, and Hospitality for Infinite Creativity Towards Sustainable

Development Goals (SDGs)”

13

Table 9

F Test

ANOVAb

Model Sum of Squares df Mean Square F Sig.

1 Regression .104 5 .021 4.455 .001a

Residual .316 68 .005

Total .420 73

a. Predictors: (Constant), Audit Committee, Board of Commisioners, Managerial Ownership, Global

Financial Crisis, Institusional Ownership

b. Dependent Variable: Earning Management

Based on the test results normality obtained significance value of Kolmogorov Smirnov Z

is 0.517, greater than significance level 0.05. Thus the processed data fulfills the normality

assumption. Multicolinearity testing was conducted to test whether the regression model found

correlation between independent variables. In case of correlation, there is a symptom of

multicolinearity. A good regression Model should not occur intercorrelation between independent

variables. Testing there is no symptom of multicolinearity is performed by observing the value of

the correlation matrix produced during the data processing as well as the value of VIF (Variance

Inflation Factor) and its Tolerance. The values of VIF < 10 and Tolerance > 0.1 indicate there is no

symptom of multicolinearity. From the results of independent variables are eligible. Result of

calculation of the variable VIF of global financial crisis 1,084 < 10, variable of managerial

ownership 1,016 < 10, Institutional ownership variables 1,016 < 10, Variable Board of

commissioners independent 1,185 < 10 Audit Committee variables 1,263 < 10 and the Global financial crisis variable with a value of tolerance 0923 > 0.1, managerial-ownership variables with

a tolerance value of 0985 > 0.1, a variable of institutional ownership with a tolerance value of

0.844 > 0.1, an independent board of Commissioners variable with a tolerance value of 0.792 > 0.1

and an audit committee variable with a tolerance value of 0.983 > 0.1, thus concluded that the

regression model in the study did not occur any symptoms of multicolinearity. The results of

heteroskedastisity testing based on significance values using the Glejser test obtained the value of

each variable greater than the significance level 0.05, with the following details as the global

financial crisis variable has significance value 0.750 > 0.05, the managerial ownership variable has

a significance value of 0.210 > 0.05, the institutional ownership variable has a significance value

of 0.817 > 0.05, the independent Board of Commissioners variable has a significance value of

0.817 > 0.05 and the audit committee variables have significance values 0.106 > 0.05. It can thus be concluded that in this regression model does not occur heteroskedastisity. Autocorrelation test

is performed with Durbin Watson test (DW). From the research results obtained DW results of

1.856 can be explained that if DW = 1.856 located before Du and after 4-Du, based on Durbin

Watson du value of 1.769 and 4-du value of 2,203, then the proposed regression equation model

there is no autocorrelation. Test test of simultaneous significance (test F) is conducted to know

whether the global financial crisis, managerial ownership, institutional ownership, independent

Board of Commissioners and Audit committees influence the earning management. The test result

of regression model obtained significance value of 0.001. Then the sig F (0.001) < α (0.05). So it

can be concluded that collectively the variables of the global financial crisis, managerial

ownership, institutional ownership, independent Board Commissioners and audit committees have

an effect on earning management. Thus the regression model is good and can be used in this

research. The value of the coefficient of determination indicated by the adjusted value of R Square is 0.191. It can be interpreted that independent variables (global financial crisis, managerial

ownership, institutional ownership, independent Board of Commissioners and Audit committees)

can explain the earning management of 19%, while the remainder is described by other variables

not observed in this study.

ISBN: 978-602-6697-54-7

14

Hypothesis Testing

Multiple regression hypothesis testing can be performed by looking at the T-test result

table, coefficient t in a significant column compared to the significance value used (α = 5%). When

the significance level is < 0.05, the H1 cannot be rejected or accepted. If the significance rate is >

0.05, then the H1 is rejected.

Table 10

Hypothesis test Results

Sig. Coef(t)

Global Financial Crisis 0.736* 0.338

Managerial Ownership 0.389* -0.868

Institutional Ownership 0.000 -4.230

Board of Commisioners 0.002 -3.231

Audit Comittee 0.617* 0.502

Description: *) Insignificant

Source: Processed secondary data, 2020.

Based on the results in the table 2 T-count and SIG-T, it can be explained as follows:

The hypothesis testing on the influence of the global financial crisis variable on earning

management showed a T value of 0.338 with a significance value of 0.736. The value of

significance is greater than 0.05 then the 1st hypothesis is rejected.

The hypothesized testing of the influence of the managerial ownership variable on

earning management showed a T value of-0.868 with significance value of 0.389. The value of

significance is greater than 0.05 then the 2nd hypothesis is rejected.

The hypothesis testing on the influence of institutional ownership variables on earning

management showed a T value of-4,230 with significance values of 0.000. The value of such

significance is smaller than 0.05 then the 3rd hypothesis is received.

The hypothesis testing of the influence of the variable board of Commissioners

independent of earning management showed a T value of-3,231 with significance value of 0.002. The value of that significance is less than 0.05 then the 4th hypothesis is received.

The hypothesis testing of the influence of the audit committee variable on earning

management showed a T value of 0.502 with a significance value of 0.617. The value of

significance is greater than 0.05 then the 5th hypothesis is rejected.

CONCLUSIONS, LIMITATIONS, AND SUGGESTIONS CONCLUSIONS

Based on the data analysis in the previous chapter, it can be concluded that:

1. the variables of the global financial crisis did not significantly affect the earning

management. 2. the mechanism of good corporate governance (which was proscribed by managerial

ownership did not significantly affect the earning management, while the institutional

ownership and the independent Board of Commissioners significantly influenced the

earning management).

ROCEEDINGS THE 2nd INTERNATIONAL CONFERENCE OF BUSINESS, ACCOUNTING AND ECONOMICS “Economics Strength, Entrepreneurship, and Hospitality for Infinite Creativity Towards Sustainable

Development Goals (SDGs)”

15

LIMITATIONS

This research has some limitations. First, this study can only explain profit management

by 19% so that there are other factors that are more influential. Secondly, based on the 5

hypotheses previously formulated, there are three rejected hypotheses that are H1: Gobal H2

financial crisis: Managerial and H5 Holdings: Audit committees.

SUGGESTIONS

From the conclusion and limitation of this research, the advice that can be given to the

next study is to add other variables that affect profit management. Further research is also expected

to use samples of companies in different industries so that they can be compared.

REFERENCES [1] Abdullah, Syukriy. (1999). Manajemen Laba dalam Prespektif Teori

Akuntansi. Positif: Analisis Keuangan dan Etika. Media Akuntansi, No.3.

[2] Andri Rachmawati dan Hanung Triatmoko. 2007. Analisis Faktor-Faktor yang

Mempengaruhi Kualitas Laba dan Nilai Perusahaan. Simposium Nasional Akuntansi X

Makassar, 26-28 Juli.

[3] Boediono, Gideon SB. (2005). “Kualitas Laba: Studi Pengaruh Mekanisme Corporate

Governance dan Dampak Manajemen Laba dengan Menggunakan Analisis Jalur”.

Simposium Nasional Akuntansi VIII. [4] Bernandhi, Riza. (2013). Pengaruh Kepemilikan Manajerial, Kepemilikan Institusional,

Kebijakan Deviden, Leverage dan Ukuran Perusahaan Terhadap Nilai Perusahaan.

Skripsi Fakultas Ekonomi dan Bisnis Universitas Diponegoro. [5] Cadbury (1992). “The Financial Aspect of Corporate Governance”.

[6] Chotourou, S.M., Bedard, J., dan Courteau, L. (2001). “Corporate Governance and

Earning Management”.

[7] Carcello, Joseph V. et al. (2006). “Audit Committee Financial Expertise, Competing

Corporate Governance Mechanisms, and Earnings Management”.

[8] Cornett M.M, J Marcuss, Saunders dan Tehranian H. (2006). “Earnings Management,

Corporate Governance, and True Financial Performance”.

[9] Chia, Y., Lapsley, I., & Lee, H. (2007). Choice Of Auditors And Earn-Ings Management

During The Asian Financial Crisis. Managerial Auditing Journal, 22(2), 177---196.

[10] Cheng, C., Johnson, J., & Liu, C. (2013). The supplemental roleof operating cas flows in

explaining share returns: Effects ofvarious measures of earnings quality. International

Journal of Accounting and Information Management, 21(1), 53---71. [11] DeFond, M., & Jiambalvo, J. (1994). Debt Covenant Violation Andmanipulations Of

Accruals. Journal of Accounting and Economics, 17, 145---176.

[12] Donal E. Kieso, Jerry J. Weygandt, and Terry D. Warfield. (2007). Akuntansi

Intermediate. Edisi Keduabelas, Jakarta : Erlangga.

[13] Downes, J dan Goodman, Elliot Jordan. (1999). Kamus Istilah Akuntansi, Jakarta:

Penerbit Elex Media Komputindo.

[14] Dutzi, A., & Rausch, B. (2016). Earnings Management Beforebankruptcy: A review of

the literature. Journal of Account-ing and Auditing: Research & Practice,

http://dx.doi.org/10.5171/2016.245891. ID 245891

[15] Efendi, Andri Sahlal. (2013). Analisis Pengaruh Struktur Kepemilikan, Kebijakan

Deviden dan Kebijakan hutang Terhadap Nilai Perusahaan Dengan Variabel Kontrol Ukuran Perusahaan, Pertumbuhan Perusahaan dan Kinerja perusahaan (Strudi Pada

Perusahaan Manufaktur Yang Terdaftar di BEI Periode 2009-2011). Skripsi. Fakultas

Ekonomi dan Bisnis Universitas Diponegoro. [16] FCGI. (2001). Peranan Dewan Komisaris dan Komite Audit dalam Pelaksanaan

Corporate Governance (Tata Kelola Perusahaan). Jilid II, Edisi 2.

ISBN: 978-602-6697-54-7

16

[17] Ghozali, Imam. (2006). Aplikasi Analisis Multivariate Dengan Program SPSS. Cetakan

IV. Semarang: Badan Penerbit Universitas Diponegoro.

[18] Ghozali, Imam dan Anis Chariri. (2007). Teori Akuntansi. Ed. 3. Semarang: Badan

Penerbit Universitas Diponegoro.

[19] Healy, P., & Wahlen, J. (1999). A Review Of The Earnings Management literature And

Its Implications For Standard Setting. Accounting Horizons, 13(4), 365---383.

[20] Iskander, Magdi R. dan Nadereh Chamlou. 2000. Corporate Governance: A Framework

for Implementation. The International Bank for Reconstruction and Development. The

World bank.

[21] Kazemian, S. & Sanusi, Z.M. (2015). Earnings Management and Ownership. Structure.

Procedia Economics and Finance, 31(15):–624.

[22] Lastanti, Sri Hexana. 2004. Hubungan Struktur Corporate Governance dengan Kinerja

Keuangan dan Reaksi Pasar, Konferensi Nasional Akuntansi: Peran Akuntan dalam Membangun Good Corporate Governance.

[23] Lisboa, Ines. (2016). Impact of Financial Crisis and Family Control on Earning

Management of Portuguesed listed firms. European Journal of Family Business. Vol 6,

118---131. [24] Moreira, J., & Pope, P. (2007). Earnings Management To Avoidlosses: A Cost Of Debt

Explanation. Research Center on Indus-trial, Labour and Managerial. Economics,. DP

2007-04. [25] Palestin, Shatila Halima. (2006). “Analisis Pengaruh Struktur Kepemilikan, Praktik

Corporate Governance dan Kompensasi Bonus terhadap

Manajemen Laba (Studi Empiris di PT. Bursa Efek Indonesia)”.

[26] Otoritas Jasa Keuangan Nomor 55/POJK.04/2015. “Tentang Pembentukan dan Pedoman Pelaksanaan Kerja Komite Audit”

[27] Schipper, K. (1989). Commentary on Earnings Management. Accounting Horizons, 3(4),

91-102.

[28] Salno, H.M. & Z. Baridwan. (2000). “Analisis Perataan Penghasilan (Income Smoothing)

: Faktor – Faktor yang Mempengaruhi dan Kaitannya dengan Kinerja Saham Perusahaan

Publik di Indonesia” Jurnal Riset Akuntansi Indonesia, Vol. 3(1), Hal. 17-34.

[29] Sugema, Iman. (2012). “Krisis Keuangan Global 2008-2009 dan Implikasinya pada

Perekonomian Indonesia” Jurnal Ilmu Pertanian Indonesia

(JIPI). [30] Veronica, S., dan Utama, S., (2005). “Pengaruh Struktur Kepemilikan, Ukuran

Perusahaan, dan Praktik Corporate Governance Terhadap Pengelolaan Laba (Earnings

Management)”. Simposium Nasional Akuntansi VIII. Vol 17 (3): 145-152. [31] Widyaningdyah A.U. (2001). “Analisis Faktor-Faktor Yang Berpengaruh Terhadap

Earning Management Pada Perusahaan Go Public Di Indonesia”. Jurnal Akuntansi &

Keuangan, Vol. 3, No. 2, h. 89-101. [32] Wedari, L. K. (2004). “Analisis Pengaruh Proporsi Dewan Komisaris dan Keberadaan

Komite Audit Terhadap Manajemen Laba”. Simposium Nasional Akuntansi VII.

[33] Xu, G., & Ji, X. (2016). Earnings Management By Top Chinese Listedfirms In Response

To The Global Financial Crisis. International Jour-nal of Accounting and Information

Management, 24(3), 226-251.