the historical role of accountants as ceos and … historical role of accountants & engineers as...

TRANSCRIPT

THE HISTORICAL ROLE OF ACCOUNTANTS & ENGINEERS AS CEOS AND BOARD

MEMBERS IN AN AUSTRALIAN CONGLOMERATE: AN ANALYSIS USING A

WEBERIAN PERSPECTIVE.

Les H HardyDepartment of Accounting and FinanceMonash UniversityGippsland Campus, ChurchillVictoria, 3842Phone 61 3 9902 6652Fax 61 3 9902 6524Email: [email protected]

THE HISTORICAL ROLE OF ACCOUNTANTS & ENGINEERS AS CEOS AND BOARD

MEMBERS IN AN AUSTRALIAN CONGLOMERATE: AN ANALYSIS USING A

WEBERIAN PERSPECTIVE.

Abstract

This paper presents the outcome of a longitudinal cross sectional analysis of the accounting andengineering profession’s representation at a Board and CEO level from 1920-1995 in the Australianconglomerate Pacific Dunlop Limited (Dunlop). The research methodology used being adapted fromMcKinnon (1986) and the findings being interpreted using a Weberian perspective. Previous researchprovides conflicting empirical evidence on interprofessional competition at the apex of organizations.This research provides evidence that the conflict between professions is an ongoing struggle and thatthe most suitable interpretative perspective must be contingent and contextual.

Key Concepts: Weberian perspective, professional competition.

1

INTRODUCTION

Conflict between professionals and competition between them has been highlighted inthe accounting, management and sociological literature (Refer: Abbott, 1988;Armstrong, 1985, 1987, 1987b; Fligstein, 1987, 1991). Armstrong (1985, 1987) hasdrawn attention to what he sees as the comparative advantage of accountants (broadlydefined) vis-à-vis other professions and particularly engineers at the apex oforganizations within the UK. Armstrong bases his view of accountants’ comparativepre-eminence on statements from the British Institute of Management (Armstrong,1985, 1987) and on a study by Tricker [1967] (Tricker quoted in Armstrong, 1985).

Armstrong (1985, p129) has contended that, “This comparative ascendancy ofaccountants (broadly defined) in management hierarchies, although it is the occasionfor thanksgiving in the profession itself – and corresponding grumbles from engineers– has attracted little analysis from either.”

The empirical data provided by Armstrong is now somewhat dated, readers beinglargely encouraged to accept at face value the comparative preeminence ofaccountants over other professions, particularly engineers. This research argues that itis appropriate to revisit Armstrong’s argument both empirically and analytically. Theanalysis is undertaken from a Weberian perspective, the contingent nature of whichoffers multiple perspectives on the professional roles of accountants and engineerswithin organizations.

This paper proposes to explore the tension that may exist between the accounting andengineering professions in the context of a case study of Dunlop, an Australianconglomerate. (pp 8-19) The Weberian perspective suggests that professions willemploy both means and end type rationalities to achieve their ultimate goals. (pp 2-4)This research will seek to show that the pattern of representation of accountants at theBoard and CEO level from 1920 to 1995 within Dunlop vis-à-vis the engineeringprofession could provide some evidence as to the extent to which both means and endtypes of rationalities have been used by both of the professions over time. Thelongitudinal nature of the research (pp 6-8) will indicate how the emphasis onparticular rationalities could be expected to change and adapt over time with asubsequent impact on the two professions.

This research supported by Mintzberg (1983) and Pfeffer (1981) argues thatorganizations (as ideal types) operating within a capitalistic environment would wishto ensure that those individuals who filled their chief symbols of power, the board andCEO positions respectively would provide social legitimacy via both a means and endtype rationality. (pp 4-6)This paper accepts that professions as substantive interestgroups are able to gain power at the board and CEO level of organizations becausethey are able to provide means (Armstrong, 1985, 1987) required by suchorganizations. The Weberian perspective draws attention to an expected ongoingstruggle between professions due to end type rationalities and political struggles beingseen as an endemic feature of the relationship between professions. It also suggests

2

that although there is wide agreement on means type rationalities, their use arecontestable between competing interest groups. (pp19-22) 1 2

THE WEBERIAN PERSPECTIVEThe potential of a Weberian perspective in regard to accounting research has beencanvassed by Colignon & Covaleski [1991] and Hardy [1998]. Weber insisted thatsocial science is primarily concerned with ‘Verstehen’ (understanding andcomprehension) (Bernstein, 1976); it was this that motivated Weber to develop hisconcept of ideal types. Essential to Weber’s ‘Verstehen’ is the notion of action.Weber’s famous definition of action states:

‘We shall speak of “action” insofar as the acting individual attaches asubjective meaning to it - be it overt or covert, omission or acquiescence.’(Weber, 1978, p4)

By definition all action is therefore subjectively rational. However, it will vary in itsdegree of rational objectivity. Of particular interest is Weber’s ‘Wertrational’(conscious belief in the intrinsic value of acting in a certain way, regardless of theconsequences of so acting) or value rationality and ‘Zweckrational’ (a consciouslycalculating attempt to achieve desired ends with appropriate means) or instrumentalrationality. While there is clearly tension between the value and instrumentalrationality it is the tension between the ends and means of the ‘Zweckrational’, thatallows a rich and varied approach in this research.

Weber’s use of the notion of rationality is far from unequivocal. Albrow (1970)considers the concept of rationality is the most difficult and disputed of all of Weber’sconcepts. Weber considers that the essence of modern capitalism is rationality(Brubaker, 1984). Of particular interest to this research is that it results in ends beingdominated by means, (Brubaker, 1984) and bureaucratization becoming irreversiblealong with the growth of functional specialization (Giddens, 1971). It is argued(Abbott, 1988; Armstrong, 1985) that both the accounting and engineering professionsplace a strong emphasis on means [formal rationality] with a lesser emphasis on ends[substantive rationality].

Weber’s analysis of modern society established a link between capitalism, theenterprise and capital accounting. With that link recognized rationality andcalculability are seen as underlying concepts (Collins, 1986). These links areimportant to the research here, as its core focus is the professional struggle forrepresentation between accountants and engineers at the enterprise [corporate] leveland specifically within Dunlop. These links establish the importance of “capitalaccounting” in capitalistic organizations and the notion of managerial capitalismexpounded by Chandler (1977). The rational enterprise is linked to Weber’s ideal typebureaucracy. Weber considered “capital accounting” a most effective means ofachieving rationality by providing rules to allow economic enterprises and capitalismto develop. It could be expected those skilled in the exercising of the art ofaccounting would play a prominent role in the institutions of capitalism. The controlof capital accounting need not be the sole province of the accounting profession,

1 Means - extent of quantitative calculation, technically possible, which provides a basis forinstrumental action.2 Ends - social action based upon choice between incommensurable ultimate values.

3

cross-cultural studies indicate that within German and Japanese economic enterprisesat least some of these controls are carried out by engineers. Armstrong recognizes thecultural context of his analysis by indicating that the domination of the accountingprofession is largely an Anglo-Saxon phenomenon with Engineers being dominate inother cultural contexts, as is the case in Germany and Japan. (Hutton et al., 1977;Lawrence, 1980; Coke, 1983, quoted in Armstrong, 1985: Franko, 1983, quoted inArmstrong, 1987.)

It is however acknowledged that within the Anglo-Saxon context accountants largelycontrol the formal rationality of capital accounting, (Armstrong, 1985) althoughaspects of the jurisdiction can and have been challenged by other professions byborrowing, adapting and contributing technical techniques. Weber’s view of the threenotions essential to modern society can provide a lens as to how capitalisticorganizations will seek legitimacy over time from those professions which canprovide the appropriate form of rationality to both enable and justify their operations.It should be stressed that the Weberian perspective does not predict the hegemony of aparticular profession. Rather it suggests that professions will constantly andcontinually be engaged in a struggle for preeminence.

While there is clearly tension between formal and substantive rationality, it is alsoacknowledged that there is tension between varieties of substantive rationalities wherethe individual must choose between incommensurable ultimate values (Brubaker,1984). Formal rationality is primarily characterized by the calculability of means andprocedures (Brubaker, 1984). It is a consequence of empirical knowledge often in amathematical form and there is often a presumption about its universal application(Colignon et al., 1991). Substantive rationality represents value spheres, it is notuniversally applicable but is dependent upon people’s agreed judgment in regard tothe rationality of beliefs and end points. The Weberian perspective allows us toconsider whether elite accountants using the formal rationality of accounting alongwith the substantive rationality of shared beliefs and common ends to advance theirsocial group, will achieve prominence within the economic enterprise. If suchprominence is achieved it will to some extent be at the expense of other professionalgroups, particularly engineers.

Armstrong (1985 & 1987) suggests that it is accountants who have triumphed overengineers within the UK due largely to techniques offered by accountants to controllabour. The Weberian perspective argues that both means and ends can be employedby interest groups [professions] to achieve their ultimate goals. It is suggested thatwhile both professions as interest groups would be able to employ both rationalities intheir struggle to gain influence in economic organizations, the profession where bothtypes of rationalities coincide empirically will be advantaged. The Weberianperspective would suggest that there are more contingent factors at work thanArmstrong’s analysis of accountants’ apparent success considers. Rather companieswill choose groups who are able to offer both formal and substantive rationalities,which legitimize their operations within the changing requirements of a capitalisticsociety.

Weber’s notion of action includes a second axis of tension based upon the concepts ofdomination and resistance (Weber, 1978). They are considered by Weber in a general

4

sense to be one of the most important elements of social action (Weber, 1978). Theyintroduce concepts of legitimacy, power and authority and suggest that dominationwithin the bureaucracy of organizations is a political process. This political process islinked by Collins (1986) to the relative organizational resources of different groupsand is expressed in the credentialism of some occupational status groups. Collins(1986) also notes that status groups sharing a common culture and outlook are able todominate the business system, and that the control of finances is the key to businesspower. The second axis linking action within organizations to a political processwould apply to the examination of CEOs and Board members of Dunlop andconsiderably broadens the insights that a Weberian perspective can provide.

Weber’s notion of the bureaucracy (ideal type) can be used to explore the balance andmaintenance of power between conflicting interest groups (Reed, 1985). This paperargues that an elite group of accountants and of engineers (as a substantive interestgroup) would seek power within the economic enterprise. The literature has linkedelite accountants as key participants within the techno structure of economicenterprises to competition with other professional groups for advancement[Armstrong, 1985,1987, 1987b; Fligstein, 1987]. In examining the interprofessionalcompetition between engineers and accountants to the board and CEO level ofDunlop, critical events and actions of individuals within the organization can beexamined. This can contribute to the fabric of that company’s history but also helprefine our perspective of the accounting profession and the legitimacy it offers ascompared with other professional groups.

The formal rationality of capital accounting has been linked to the rise of capitalismand the economic enterprise. It is the substantive rationality of interest groups the‘battle of man with man’ that will be explored. This tension between the professionswill be examined in the context of the representation of engineers and accountants atthe board and CEO level at Dunlop over time, both professions being linked to therise of corporations and both capable of employing the rationality of capitalaccounting. It will be argued Dunlop is worthy of being the focus of such aninterpretative endeavor because of the way its organizational and corporate form hasevolved.

ISSUES FROM PRIOR RESEARCH

Professions are generally linked to and serve capitalistic clients accepting the generalvalues of such clients as their dominant ideology (Larson, 1977). Whileprofessionalism gives both accountants and engineers the possibility of asserting theirneutrality and objectivity via their formal rationality and calculation, the reality is thatthey are both corporate dependent (Larson, 1977; Abbott, 1988; Chandler, 1992). Theliterature (Abbott, 1988; Fligstein, 1987; Armstrong, 1987b; Larson, 1977) indicatesthat professions compete for opportunities within organizations and that ‘elite’ groupsof professionals wish to be represented at the apex of organizations. It is widelyaccepted that a managerial hierarchy largely controls corporations despite de jurepositions to the contrary (Berle and Means, 1992; c\f Tricker, 1984; Herman, 1981;Galbraith, 1992; Chandler, 1977). To conclude that accountants and engineers alongwith other professionals would represent substantively rational interest groups within

5

the managerial hierarchy and would be concerned to promote those substantiveinterests is therefore reasonable.

Mintzberg (1983) suggests that the power of boards is largely a matter of empiricalfact. The position adopted here from Mintzberg (1983) is that the board represents asymbolic representation of power. From the research’s perspective the board becomesan ideal type, the essence of which is the means whereby groups formally try to definetheir power. While the CEO (Mintzberg, 1983) is arguably the most powerfulindividual in and around an organization, Pfeffer (1981) also sees the CEO, like theboard, as a symbol of the organization and change in this symbolic source of power asa relatively rare event. While recognizing that change in symbols is rare, if asignificant change in professionals at the apex of Dunlop were to be found then theWeberian lens based on the tensions identified could provide a useful interpretativetool. This then provides the basis for examining the empirical evidence. Changes inthe power equilibrium towards particular professions would have perceptibleoutcomes. Evidence of the change in the power equilibrium towards them should inpart be reflected in their representation at the board and CEO level and in the actionsand decisions that are taken (Karpik, 1978; Pfeffer, 1981; Fligstein, 1987; Armstrong,1985, 1987). Once entrenched Pfeffer (1981) and Fligstein’s (1987, 1991) analysissuggests that successful interest groups would attempt to replicate and replacethemselves with members from their own interest group.

The literature takes up the intercompetition between professions in different ways.Armstrong (1985 & 1987) using Stacey (1954) traces the rise of the accountingprofession within the UK via the liquidation, bankruptcy, and audit trail. Armstrong(1985 & 1987) agrees with Stacey that the use of accounting means as a managementtool in the context of the 1930s depression was a watershed for the accountingprofession. The key to the accounting profession’s relative success was in their abilityto convert their professional techniques to enable capitalistic enterprises to bothcontrol and make labour profitable. Another factor was the financial abstraction thatwas required of the new multi-divisional firm, which was developed by business as aresponse to the 1930s crisis. Accounting techniques are largely indeterminate beingundertaken in a high trust environment, which Armstrong (1987b) argues putaccountants at a distinct advantage in regard to engineers in the managementenvironment. Armstrong (1987b, p430) concludes that in the eyes of a predominantlynon-technical managerial elite, “unreconstructed engineers tend to fail the ‘cultural’test of trustworthiness”; and are therefore at a competitive disadvantage when theywish to enter the apex of capitalistic enterprises. Armstrong (1985 & 1987) arguesthat the empirical evidence from the UK support his conclusions.

Research by Abbott (1988) and Fligstein (1987 & 1991) suggest a differentrelationship between the professions. Abbott (1988) argues that the central feature ofprofessionalism is the interprofessional competition formed over particular workjurisdictions. Abbott (1988) provides evidence that both engineers and accountants areinvolved in such competition particularly in the context of the management function.Fligstein’s (1987 & 1991) longitudinal study from 1919-1979 on the USA’s top 100companies Presidential positions provides empirical evidence to supportinterprofessional competition. Fligstein’s (1987 & 1991) research demonstrates arising proportion of President’s with a finance background as a recent phenomenon

6

being linked to the multi-divisional firm as a conglomerate. Fligstein (1987) identifiesthe multi-divisional firm of the 1930s with the production and marketing of multipleproducts rather than a financial device to allocate capital. This is supported by the riseof marketing professionals during this period. While finance professionals provide thelargest single group of Presidents in 1979 over 70% of the Presidents still have abackground other than finance, including technical and marketing backgrounds.

It is suggested that an examination of the Australian conglomerate Dunlop as a casestudy will enable the issues of prior research and the generalizations they generated tobe reexamined. In particular it should help to provide further empirical evidence and anew interpretative and historical perspective for the apparent conflict in the literaturein regard to interprofessional competition.

RESEARCH METHODS

The research required a determination of why a phenomenon exists in time in relationto constancy and change, the phenomenon “being the representation of variousprofessions at the CEO and Board Level of Dunlop from 1920 to 1995”. The chosenmethodology has adapted parts of McKinnon’s (1986) socio-historical methodologydealing with constancy and change. 3 This adapted methodology is consistent andrequired by the longitudinal nature of the research and facilitates a Weberianperspective. Ontologically this research assumes that reality is a concrete process withan epistemological stance that is concerned with the study of change within systems.

Socio-historical research requires the management and collection of a large amount ofempirical material. Apart from the extensive research in the sociological literature todevelop and refine the Weberian framework a protocol was developed to collect theempirical evidence in regard to both Dunlop and the general environmentalbackground for this research. [Haag & Hedland and Mintzberg referred to in,(McKinnon 1986, pp58-60) and (Yin 1984, p 45, 52-57)] The protocol was dividedinto two main sections dealing with environmental background and specific companydata. The specific company data was then subdivided into general company andresearch specific material. The protocol required that data be collected from a diverserange of primary and secondary sources. The specific company protocol wherepossible has relied on primary sources which include annual reports, press releases,chairman’s addresses and other company documents although secondary sources havebeen used to fill in the gaps that naturally develop in such research.

The methodology is linked to the Weberian theoretical perspective in two importantways; first, via the Weberian notion of the ideal type and second by emphasizing theimportance of action. Weber developed the notion of the ideal type as a conceptualsociological tool that could be used to develop analytical generalizations againstwhich the concrete empirical evidence of history could be compared. The concreteempirical evidence of history is evidence of human action described as an event.Events are viewed as the “decisive referents” in change analysis because they‘...constitute the concrete and incontrovertible substance of the historical record and

3 McKinnon’s methodology being developed from the work of Smith (1973, 1976); refer to McKinnon(1986), chapter three.

7

provide the data for change analysis’ (McKinnon, 1986, p35). In comparing analyticalgeneralizations of the ideal type with the empirical record of history the concretehistorical pattern can by measured alongside the abstract pattern forminggeneralizations.

Apart from events, a further two key terms, ‘change’ and ‘transformation’ based uponMcKinnon’s methodological approach, need to be operationalised. Change is definedas;‘...a succession of events which produce, over time, transformations of the systemunder study through replacement or modifications of pre-existing patterns in thatsystem’ (Smith quoted in McKinnon, 1986, p33). Transformation is defined as the ‘...replacement or modification of a pre-existing pattern in the system’ (McKinnon, 1986,p7).

The use of the ideal type allows generalizations to be formed within the researchcontext but avoids the problems of reification that so often accompany suchgeneralizations within the social sciences. Ideal types that are conceptualized throughthe research relate to the terms bureaucracy, professions and corporations. These idealtypes should not be considered, ideal in a normative sense but as conceptualconstructs to be used for methodological purposes (Giddens, 1971). It allows the studyof history to be seen as both a product of the human will and the individual actingwithin a social framework. The methodology consistent with the Weberianperspective finds a middle ground between general abstractions and individualactions. Also consistent with the ontological base of this research and Weberianthinking, the methodology allows exploration of the individual’s will and action thatcreates history.

To manage the longitudinal nature of the processual change being studied the researchdivided the company’s history into four periods of time. The use of periodisation isjustified because it allows change to be considered on the basis of a continuum, ratherthan on the basis of single events or great people and is linked to the researchmethodology of transformational change (O’Hara, 1985). Within each of the timeperiods, empirical evidence of decisive referent events leading to eithertransformational change or potential transformational change were gathered andpatterned traced. To enable the data collected to be more manageable the surveyswere taken at five yearly intervals.

The time periods and justifications are as follows:

1920-1945 - A period of relatively small capital markets in Australia when the postWW1 patterns of economic activity became established. Major historical events thatimpinged on business included the 1930s depression and the command economy ofWW2.

1946-1965 - This period included the post war boom period and saw thecommencement of putting into effect the ‘unrelated’ and ‘selective’ diversificationpolicy of Dunlop.

1966-1985 - This period saw the end of the post WW 2 boom and the beginning of aperiod of economic instability including stagflation and recession. The financial

8

markets began a deregulation phase. Dunlop became established as a successfulconglomerate.

1986-1995 - The period was marked by continued financial deregulation andincreased interest in the share market from many different social sectors. Anincreasing internationalization and global focus was under way. Dunlop’sconglomerate strategy was becoming problematic.

The classification of the directors and CEO’s into professions was based on a range ofsource documents, some primary others secondary. If a profession was listed in anauthoritative source such as Who’s Who, biographical dictionaries, or companydocuments, that was accepted as evidence of belonging to a particular profession.Completion of a course or a degree that could be used for professional purposes wasalso accepted. For instance a completion of a LLB would result in a classification as alawyer although the profession may not have been practiced. While profession wastaken to include those of a scientific and military category, generic terms such asmanager, investor or gentleman were not classified as a profession. Thus genericterms, along with those individuals where information was unavailable, wereclassified together as non-professional. The classification of directors into executiveand non-executive was based upon whether the director had ever worked in anexecutive capacity with the company. If a director had been employed by thecompany then they were classified as an executive director despite the fact that theymay have retired or resigned from the executive position.

The patterns that emerged from the research are discussed initially at a general leveland then at a more specific level based on each time period. The patterns identifiedwill not be expected to be normative or predictive but rather will entail a comparisonbetween analytical generalizations based upon the literature and the generalizationsformed from examining the empirical data.

DUNLOP – THE BACKGROUND

Throughout the 20th century Dunlop has been both a public company and a majormanufacturing company within Australia. Dunlop’s history is a chequerboard ofsuccess and failure, fortuitous acquisitiveness and failure to recognize the potential ofhomegrown research and development. The early Australian company retained linkswith the UK family entrepreneurs who began the company in the UK. Once floated itestablished links via the Baillieu family with Collins House, arguably the mostinfluential investment house in Australia in the first part of the 20th century. Thelinks with Collins House resulted in a number of the board members of Dunlophaving links with Australia’s business and social elite. In several instances a familypattern of board membership was established although the links with the Baillieufamily were extraordinary and lasted over sixty years. These links were both relatedto Australian members of the family and Baillieus who emigrated from Australia backto England and became involved with the UK Dunlop.

Dunlop was floated as a public company in Victoria, Australia in 1899, beingeffectively a management buyout from its UK parent company. The primary activityof the company was in manufacturing rubber products and its main revenue base was

9

the selling of bicycle tyres. The early public nature of its ownership while not uniquewas unusual (Blainey, 1993) and enables the CEO and board to be considered from alongitudinal perspective that would not be available in the context of most othermanufacturing companies within Australia, which were mainly held in private handsuntil after WW2. From its inception Dunlop although having an Australian board hadmany links with both the UK and North America.

The links with the UK and USA came about for a variety of reasons and are importantin this research as they provide a means by which both manufacturing andmanagement technical techniques were and could have been introduced into Australia.These overseas links initially were due to the links between the UK parent and itsAustralian subsidiary, which were also linked by family connections with the Du Crosfamily the majority shareholders of UK Dunlop. The management buyout by an Irishborn, Canadian, Garland, who then immediately floated Dunlop publicly provided alink with North America. Despite the fact that Dunlop was an Australian company thelinks with both the UK and the USA were to remain strong. The manufacturing ofrubber was a relatively secretive business and technical know how was vital. Duringthe period 1900 - 1920 Dunlop acquired key personnel from both the USA and the UKto manage the technical manufacturing of its products. The importance of rubber in arange of industrial, mining and domestic uses has largely been forgotten but at the turnof the century it was a new and exciting industry where profits were made relativelyeasily. The emergence of the automobile industry caused the rubber industry to boomparticularly in the production of tyres. However with the boom in rubber productscame increased competition and Dunlop like many companies tried to diminish thatcompetition by acquisition and merger. As part of that strategy Dunlop reestablisheda strategic alliance with UK Dunlop in 1927 when 19% of the Australian companywas purchased.

Despite endeavors to diversify away from its reliance on tyres Dunlop continued for alarge part of its history to rely upon tyre manufacturing for its profit and revenue base.At the end of the 1950s the most prosperous decade in the companies history thepolicy for diversification gathered pace. In the late 1960s Dunlop entered one of themost acquisitive period of any manufacturing company in Australia’s history. In thespace of five years Dunlop became through a policy of unrelated and selectivediversification a conglomerate, arguably the first example of such a business inAustralia. It however came at a huge cost and the consequent debt crisis almostcaused the collapse of the company. An executive led recovery, and a capitalrestructure restored the fortunes of the company and the company established itself asa successful international conglomerate during the 1980s, with the head office actingas a mini bank. Dunlop represents a core piece of Australian industrial history andBlainey (1993, Preface) suggests ‘No Australian company has ever controlled so manyhousehold names’. It is also arguable that Ansell a company within Dunlop’s stableis the most successful industrial manufacturer ever to come out of Australia, whichnow dominates its sector internationally (Blainey, 1993).

While in the 1990s the company’s viability as a conglomerate has been questioned (ashas become the fashion with this organizational form) the above ‘potted’ historyprovides an Australian context in which many of the quintessential forces that haveimpacted on and shaped business organizations can be examined. In the context of

10

the research it would be anticipated that such a history would provide the opportunityto examine the professional struggle between accountants and engineers.

DUNLOP - THE GENERAL PATTERNS.

The general trends evident within Dunlop based on a five-year sectional analysis overthe specified period presents evidence within this company of a struggle between theprofessions particularly between accountants and engineers. The best-representedprofessions on the Dunlop board of directors during the survey period wereaccountants representing 30% of directors (Appendix - Table I). Up to the 1980sthere appears to be a fairly evenly balanced struggle between accountants andengineers (Appendix - Table II) and the more broadly classified finance and technicalpersonnel (Appendix - Table III). 4

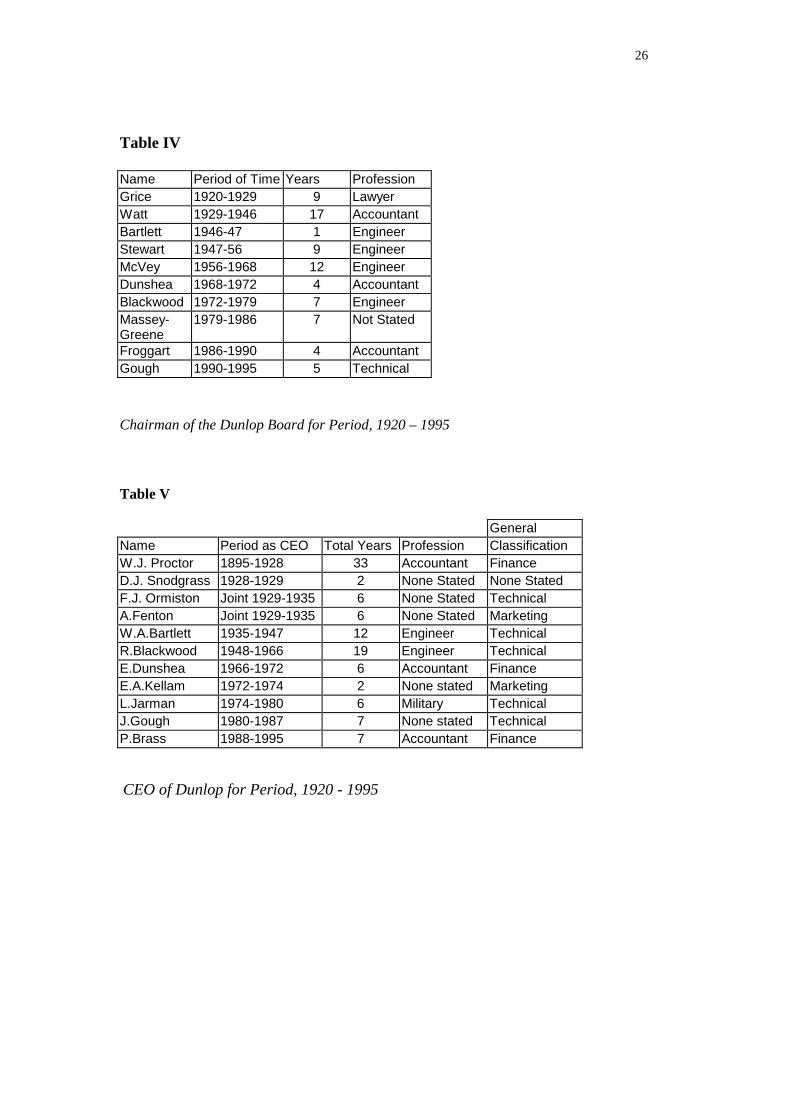

The evenness of the struggle between accountants and engineers is also evident whenthe chair of the board is considered (Appendix – Table IV). Over the period of theanalysis accountants and engineers regardless of the total numbers of particularprofessions on the board largely shared the chair of the board. Engineers from 1920 -1995 spent 29 years as chair of the board and accountants spent 25 years. Clearly thisevenness supports the view that the accounting and engineering professions areequally involved in this key position within the apex of Dunlop. The pattern alsoshows that accountants as chairs are interspersed between the engineers andtechnically qualified staff.

A similar pattern emerges when the CEO’s of Dunlop are considered (Appendix –Table V). Although most CEOs do not have a stated profession out of those that do,there are three accountants and two engineers. Thus both the key professions that thisresearch is based upon are clearly represented. From the period 1920 to 1995, Dunlophad three accountants serve as CEO for a total of 21 years with engineers serving for atotal of 31 years. The general pattern that appears to emerge is one of competition andstruggle between professions rather than dominance and hegemony. These generalpatterns would suggest that the formal rationality of both engineers and accountantshave over time been equally suited to the needs of this firm both at the CEO and chairlevel.

Another key pattern that emerged from studying Dunlop’s board and CEOs is theimportance of family and entrepreneurial connections. For instance W.J. Proctor wasthe first CEO, an accountant, who largely owed his position to his family connectionswith the Du Cros family, the founding entrepreneurs of the UK Dunlop firm. Theimportance of the owner entrepreneur cannot be ignored in this type of research(Fligstein, 1987 cf Chandler, 1977) from the rise of professions into the apex oforganizations. The rise of a profession under these circumstances could be linked tofamily connections, rather than the technical skills offered by that profession.Entrepreneurs’ choice in terms of professions chosen for family members and the

4 Table III, a broader ‘adhoc’ professional classification, enabling a number of the ‘not stated’ in TableII to be reclassified based upon their role in Dunlop although they did not meet the stricter criteriaapplied in Table II.

11

promotion offered because of those connections clearly need to be considered in thestruggle between professions.

On six occasions throughout the time period, sons of previous board membersappeared on the board, typically with long-term appointments. In many instances thesons’ educational status was markedly different from their fathers, indicating anupward mobility, typically tertiary, general and often UK based. Clearly for theseentrepreneurial and well-connected families the professional road was not seen as anessential component of gaining access to the apex of Dunlop and other corporateorganizations. The tension between the substantive rationalities and the politicaltensions within the Weberian perspective offer an interpretative device to explain boththe struggle between the professions and the role of entrepreneurial and well-connected families within Dunlop.

Table I (Appendix) indicates that as a general pattern non-executive members ratherthan executive members at least numerically dominated Dunlop’s board. There wereonly two periods in the company history when this was not the case, 1929-1935 andthe late 60s to the mid 70s. It will be argued in the specific pattern section that it wasonly in the later time period that some form of managerial capitalism existed. Thefirst period of executive domination was the result of family members ofentrepreneurial owner-managers coming onto the board as the result of mergers andacquisitions; analysis of executive rationalities favored by the board in this context islimited. In terms of the professional executives who moved through the firm ranksonto the board it can be seen from Table I (Appendix) that there were four accountantsand three engineers. Once again this underscores the argument that both professionsand presumably their technical techniques have been valued within the Dunlop firm.It does not suggest that there was rapid advancement within the firm for a particularprofession that controlled a technical jurisdictional area that was deemed critical to thefirm’s prosperity. It also reinforces the point that advancement was a struggle with noprofession achieving hegemony in terms of executive promotion.

The time period for the promotion of particular executive professions is of someinterest. The promotion of the three executives who were engineers occurred duringthe 1940s, 1950s and the 1990s. The promotion of the four executives who wereaccountants, apart from one who was appointed in the 1950s, all occurred after thecompany had transformed itself into a conglomerate from 1975 until 1995. Thisperiod also saw a sharp increase in the total number of accountants from non-executive sources. Table II and Table III (Appendix), clearly show a rise in theimportance of the accounting profession to the top of the Dunlop board since 1980 to1995, which can be linked to the rise of Dunlop as a successful conglomerate. Whilethe recent rise of the accounting profession within Dunlop in part can be linked to theformal rationality of the profession, the Weberian perspective also suggest that thesubstantive rationality of those groups and the political processes within organizationsshould be considered.

DUNLOP - THE SPECIFIC PATTERNS.

1920-1945

12

The profit performance of Dunlop in the early 1920s waned, demonstrated in part bythe market capitalization of the firm almost halving between 1920 and 1925 (Hardy,1998). This can largely be explained by the intense competition that engulfed tyremanufacturers throughout this period and Dunlop’s inappropriate response. Dunlopwas losing market share to its competitors although it was still maintaining growthdue to the buoyant car industry (Blainey, 1993) cf (Anon, 1925). Dunlop’s responseto this competition was twofold, it sought stronger links with its UK counterpart in theUK, which purchased 19% of the company in 1927 and then arranged mergers with itstwo greatest competitors Perdriau Rubber Company and Barnet Glass (Blainey, 1993).

This has several implications for this research. Firstly although Dunlop was veryseverely impacted by the 1930s depression, action had been taken well before thedepression to enable profit to be extracted from a competitive market a classicalcapitalistic response. Secondly the links with the UK already strong via family andpatent connections were now linked directly with board representation althoughdistance meant this was via substitution. Technological transfers could now morereadily be made and make UK management innovations, if any, readily available toDunlop. Thirdly the mergers bought into the firm a number of owner-managers andfamily entrepreneurs from both Perdriau Rubber and Barnet Glass.

This background then highlights the way in which Dunlop entered into the 1930depression crisis, the depth of which in the Australian context was arguably evenmore severe than in the UK and USA. As Blainey (1993) argues, the motor vehicleindustry was the barometer to the health of the economy and tyres, Dunlop’s majoractivity, was to take the brunt of that barometer’s fall. In 1929 there were 98,000 carssold in Australia, while two years later there were just 9,000. The 1930s provided acrisis for Dunlop and the company’s actions in response to that crisis is critical indeciding whether transformational change that often accompanies such crisesoccurred.

The merger between the competing rubber manufacturers in Australia was not areaction to the 1930 crisis but rather to competition. It became however a major factorin Dunlop’s reaction to the 1930 crisis reflected in the political machinations of theboard. The board from 1929 to 1935 became large, factional and dysfunctional.Board members were in many instances representing their antecedent company ratherthan the new entity. During this period there were joint managing directors one fromPerdriau and the other from Barnet Glass controlling administration and factoriesrespectively. Rather than seeking technical solutions during this period the board ofDunlop were engaged in the struggle of man against man involving primarilysubstantive rationalities and related political tensions (Hardy, 1998).

The company during this period attempted to increase sales from a diversifiedmanufacturing base. In 1934 over 50% of the company’s revenue came from sourcesother than tyres (Blainey, 1993). However despite this the company’s profitabilityposition continued to worsen as the 1930s progressed even though its competitors'positions were improving. While reasons for this are manifold a major contributingfactor was the tolerance that Dunlop showed for inefficiency. Inefficiency wastolerated in a number of ways, including overstaffing, incompetence and poor qualitycontrol (Blainey, 1993).

13

“The evidence is overwhelming that Dunlop clung to more employees, especiallysalesmen, than its volume of work justified. An efficiency drive a few years laterproved the extent of the over-staffing. Meanwhile employees, as distinct fromshareholders, were delighted that Dunlop tolerated inefficiency in such lean times”(Blainey, 1993, p138).

Despite the depression and the competitive spirit that it engendered in some, it wasnot evidenced at Dunlop. In fact Dunlop’s lack of competitiveness and inefficiencywas highlighted by the fact that the Australian Beaurepaire tyre company was to beginand prosper, a company that was to provide spirited competition to Dunlop for nearlyfifty years.

This inefficiency and its tolerance can in part be explained by the machinations at theapex of the Dunlop organization, (Blainey, 1993) providing a context to examine theactions of key professionals. The chair of the Dunlop board from 1929-1946 was anaccountant Willy Watt. Watt was both a businessman and a liberal leaning politicianhaving been the treasurer of both Australia and Victoria. Rather than ruthlesslypursue efficiency at the expense of workers, Watt took a contrary view. Heconsidered that the 1930s crisis was of such severity that beyond a certain pointworkers should not be penalized for the sake of shareholders. Watt’s perspective wasthe result of a number of factors, his liberal political leanings, the role of the tariff inAustralia but probably most importantly his links with Barnet Glass one of the nowmerged competitors. From the time of the merger in 1929 until 1934 Watt was notprepared to take advantage of consolidating the factories and operations of the mergerbut rather let the three firms continue as a loose federation. The reasons although notcompletely clear would suggest that the political tensions of the merger had to be dealtwith at both the board and management level before efficiency would be pursued.Although the depression crisis was indirectly responsible for events that were about totranspire the catalyst to change was the fact that as other manufacturing companieswere recovering Dunlop was slipping back. In the 1934-1935 financial year thecompany was unable to pay a dividend. Urgent action was required and after six yearsof indecision, decisive action was taken. This action was to appoint a new CEO, whocould cut out the inefficiencies and return the company to profitability.

The appointment of W.A Bartlett an electrical engineer provided a transformationalchange in both the companies operations and its profitability (Hardy, 1998). Bartlett,English born had wide experience both in the UK and in North America. Unlikeprevious appointments to the CEO position he had no experience in the rubberindustry but saw himself as a manager. Bartlett then applying the techniques ofcapital accounting, began to implement efficiencies on a scale that has previouslybeen unimagined. These involved large retrenchments particularly in the clerical andsales staff, the selling of unprofitable businesses and the rationalization of existingbusinesses. In the first year of his office Bartlett achieved savings of 130, 152 poundsequivalent to almost the entire profit of the year before. These savings were not just aone off but would continue into the future, nor were they at the cost of the long-termhealth of the company. Evidence of this is the critical role that Dunlop was to play inthe Australian war effort, in a bewildering range of activities. Bartlett wasexperienced in selling and it was an area that he administered personally.

14

Despite the fact that Bartlett initially created large retrenchment and did not likemilitant trade unionism, he did not employ a bludgeoning approach to Dunlop’semployees. Blainey (1993) indicates that by the 1940s Dunlop by the standards of thetime was almost a paternal employee. Evidence of this includes a superannuationscheme that included staff down to the second foreman, a ground insurance schemewithout employee payment in the case of death and sick leave arrangements. Bartlettwas also heavily involved in devising post-war training schemes for return servicepeople and had purchased land to build a model factory and city for Dunlopemployees at Beaumaris, a Melbourne suburb.

It is argued that the tensions within Dunlop during this period, linked to therationalization of the firms productive capacity and staff levels are best explained byreference to a Weberian perspective, where the struggle between man and man isemphasized rather than concentrating on a technical jurisdiction that is arguablyavailable to a number of professions. This is to be found in the tensions between thesubstantive rationalities that existed within the merged firms and the political tensionsin regard to which merged firm was going to dominate. It is also suggested that whatcaused Dunlop to act decisively was not so much the depression but the fact that theywere not sharing in the post depression prosperity. While in this instance the keyprofession to implement change was an engineer, the Weberian perspective suggeststhat the context always needs to be examined, as the struggle is ongoing.

1946 - 1965

This period provided the most consistent growth in profits both in current andconstant terms than in any other period (Blainey, 1993; Chairman, 1948; Hardy,1998). Towards the end of the period Dunlop embarked on a deliberate policy todiversify away from the extremely competitive tyre industry (Dunlop, 1960), as formost of this period over 70% of its sales were from tyres (Dunlop, 1956).

The research’s interest in this period is focused on both the beginning and end. Watt,the Chair of Dunlop since the mergers of 1929, resigned from the board in 1946 andwas replaced by Bartlett, the appointment indicative of the success that he hadachieved. At this time several other long-term board members also died or resigned asDunlop was positioning itself for the post World War 2 boom. UnfortunatelyBartlett’s dual roles were short lived due to his death and Dunlop found itself lookingfor both a chair and a CEO.

The company now had a choice in terms of the management skills that were going tobe sought to take it forward. As chair, it initially chose A. A. Stewart an Engineerwith strong business connections including the previously mentioned ‘Collins House’,Stewart was to remain Chair from 1947 to 1956. D. McVey also an engineer who wasto remain in that position from 1956 to 1968 then replaced him. Thus after the longtenure of Watt the accountant, two Engineers were to hold the position of Chair of theboard for the next 21 years. While these circumstances should not be overstated it isevidence of the fact that accountants were not dominating engineers and that there isan ongoing struggle and tensions between interest groups.

15

The company’s choice in replacing Bartlett as CEO with no obvious successor wasmore vital. The board then made a rather unpredictable although as it turned outfortuitous choice in appointing R. B Blackwood who had recently been appointed asprofessor in mechanical engineering at Melbourne University. Blackwood’sconnection with the company had gone back to 1933 when he was appointed toimprove the quality control of the tyres he also contributed technical knowledge toDunlop’s war effort. He had recently left the company however for as Blainey (1993)suggested he was not on Bartlett’s wavelength and did not see a long-term future withDunlop.

The appointment of Blackwood once again demonstrates the contingent nature of suchappointments. Blackwood brought no particular management ideology to theposition but rather a sense of pragmatism being content if the system worked.Blackwood was in part appointed to ensure cordial relationships between managementand the workers which he considered would best be achieved by a system ofdecentralized factories containing no more than 1500 workers (Chairman, 1950).However it was technical matters relating to manufacturing that provided the keyreason for his appointment ‘...the board felt that a technical manufacturing industrysuch as ours should be under the control of a senior executive with a sound technicalbackground...’(Chairman, 1948). Blackwood considered that the company wouldremain profitable if it remained conscious of its technical needs and research anddevelopment, which can clearly be linked to his background and the Weberianperspective of rationality both formal and substantive (McLean, 1997 cf Dunlop,1955). Blackwood’s appointment and success as CEO clearly demonstrate theindeterminate and contingent nature of the skills required to successfully operate atthat level. While it must be acknowledged that the 1950s was a relatively easy time toearn profits in Australia, Dunlop had not always taken advantage of good economictimes. Blackwood’s appointment also suggests the on going struggle of man againstman for such positions, as there were four other Dunlop executives, who wereoverlooked. Blackwood’s tenure as both CEO and later chair of Dunlop providesclear evidence of an engineer able to bring both technical and business acumen to thecompany.

1966-1985

This period was dominated by a diversification strategy that was to make Dunlop aconglomerate, one of the first companies in Australia to do so. This drive towardsdiversification although successful provoked the specter of bankruptcy in the early70s. It is linked to the research in a number of ways, for at the end of this periodaccountants were certainly the dominate profession on the board and theorganizational structure of the conglomerate would appear to be moving towardsfavoring accountants as prospective CEOs. It also shows that whereas in 1948 a CEOwith a sound technical background in manufacturing was required in 1966 abackground in administration was considered acceptable.

Associated with plans for diversification was a managerial reorganization of Dunlopinto a divisional structure (Hardy, 1998), a relatively innovative move for Australia at

16

the time. The driving force behind this process was E. Dunshea an accountant whowas to replace Blackwood as CEO when he stepped down in 1966. Dunshea’sorganizational vision had been influenced by both the way that UK Dunlop hasorganized its operations and in rubber operations overseas (Blainey, 1993). Thereorganization which begun on the 1\1\1963 saw executive directors becoming moreinfluential within the organization and was quickly perceived as a strategic strength ofthe company (McVey, 1963; Anon, 1963; Chairman, 1964). It was the organizationalarrangement that suited Dunshea’s push to diversify Dunlop away from rubber andbecome a conglomerate. After nearly four decades of having a technical person incharge of the company the fact that an administrator was now the CEO had clearimpacts.

Dunshea’s push for diversification both ‘unrelated and selective’ were to enableDunlop to ride out the traditional business cycles and reduce its’ dependence uponrubber it was to provide transformational change. The eclectic nature of this processcan be seen in the wide range of companies taken over, textile manufacturers,clothing, footwear and Ansell. The speed at which it occurred was stunning. Withinthe space of three years from 1966 to 1969 the profit contribution of the tyre divisionto Dunlop declined from 70% to under 40%, at a time when real profit was growing(Dunlop, 1969). The takeovers had largely been friendly and had been funded by amixture of debt and equity (Blainey, 1993). The level of debt for a time being hid byDunshea’s overvaluing of inventory. Dunshea’s death in 1972 meant that hepersonally never had to accept the responsibility for what was about to occur, asDunlop’s capitalization in 1975 was in real terms half of its 1970 value. It wouldhave been worse except for institutional support from broking houses, linked to whatremained of the Collins House coterie (Anon, 1975; Hardy, 1998).

Dunlop was required to go into a period of reorganization and reconstruction. For thefirst time in its history the board was for a short period of time dominated byexecutive personnel who were not linked to entrepreneurs. The CEO who wasprimarily responsible for the reconstruction and reorganization was L. Jarman whohad a military background he was succeeded by J.Gough in 1980 with a technicalbackground in textiles. Dunshea who was also made Chair of the Board during histenure as CEO was after his death replaced by Robert Blackwood.

A number of points can be made that are relevant to this research. Firstly whileDunshea was the main driving force behind both the management reorganization anddiversification push, the need to do so was widely recognized within the apex ofDunlop. The manner in which Dunshea went about the reorganization anddiversification of Dunlop could in part be linked to his professional training and inpart to his personality. While Dunshea had instituted the new management structureof divisions he exercised little control over them as CEO, evidenced by Dunlop’sliquidity crisis where managers went about solving that problem by further borrowing(Blainey, 1993). As already indicated Dunshea was to use his formal rationality toengage in some creative accounting in terms of valuing Dunlop’s inventory.Dunshea’s ascent in the company had been a struggle, not well educated or sociallyconnected his rise to the CEO level is evidence of man’s struggle against man. Thesuccess that he had in reorganizing Dunlop into divisions can be linked to the formalrationality of an administrative background that was linked to accounting. Although

17

political factors such as Dunshea’s links with McVey the Chair of Dunlop at the time(Blainey, 1993), cannot be ignored.

The financial controls on the multi-divisions within Dunlop were initially extremelylax. When Jarman took control as CEO it was in the area of finance that he first tookaction, insisting that all requests for loans should come to head office (Blainey, 1993).Under Dunshea the divisions and new acquisitions under the policy of diversificationwere financially unsupervised, indicating the contingent nature of the multi-divisionalform. Dunlop in this period was in the process of learning about the managementstructure of the multi-divisional firms, despite its USA contacts where suchorganizational forms were more advanced.

Jarman along with the board showed further evidence in understanding therequirements of capital accounting by proposing in December 1977 what at the timewas a radical plan, a return of 25% of the company’s capital and a share restructure.As Blainey (1993) suggests it captured the psychology of the market and could beconsidered the final plank in the company’s restructure and birth as a viableconglomerate. The transformational change, which the board under went can in part,be linked to those events. For suddenly, as the 1980 survey of board membersdemonstrates it was accountants who were dominating the board, representing at least50% of the board members for all future survey periods.

Dunlop was now an organization making allocations of resources to the manydissimilar operations under its umbrella. It was an organization whose apex was nowdominated by the accounting profession, domination that in some respects appears tobe unbalanced. The evidence however would suggest that accountants did not arrivein a position of such dominance merely because they provided means of managerialcontrol. These means have also been evident and provided from other professionalgroups particularly engineers in the history of Dunlop. It is suggested that the rise ofaccountants within Dunlop at this time can be linked to the Weberian perspective ofan ongoing struggle between man and man and institutional factors (Fligstein, 1987&1991). This struggle being exemplified in Dunshea’s rise and exercising of powerfollowed by the increasing role of executive officers at the board level who wereinvolved in the struggle for the company’s survival. Once that survival was assuredand the conglomerate structure was firmly in place, the board quickly becamedominated by accountants. While accountants no doubt had particularly skillsrequired by such an organizational structure such complete domination is more fullyexplained by considering an institutional view where symbols of power are subject tothe forces of replication. The Weberian perspective would however suggest that sucha rise would be contingent and subject to challenge from other professional groups.

1985-1995This period saw Dunlop operating as a mature conglomerate engaged in acquisitionsand divestments both in Australia and overseas, at the end of this period 45% of thecompanies profit and 50% of its assets being outside of Australia. This period asTable II & V (Appendix) indicate saw accountants dominate the organizational apexof Dunlop. The conglomerate structure of the organization began to be questioned bythe market towards the end of this period with a decision in 1995 to return to its corebusiness. Whether a return to core activities will represent a further transformational

18

change for Dunlop is still to be decided. As the company divested, the board tooksteps to ensure that the nomination process of board membership would become moretransparent and that criteria would be established to look for a range of skills thatwould help in decision-making. It is suggested that such a process would moreexplicitly reflect the recognition that particular professional skills have in the decisionmaking process (Hardy, 1998).

The Weberian perspective would suggest that there will be a reduction in the numberof accountants on the board based on the ongoing struggle between man and man asexemplified in the competition between professions. It would also suggest that ifDunlop as a conglomerate undergoes transformational change that the professionalsthat will be employed in such a move are not predetermined but will depend on arange of contingent and contextual factors. IMPLICATIONS IN THE CONTEXT OF PREVIOUS RESEARCHGENERAL TRENDS

The general trends of this research indicate, as does previous research, that there is astruggle between professions (Armstrong, 1985 & 1987; Fligstein, 1987; and Abbott,1988). There is also some evidence that supports the contention that accountants havecome to dominate engineers (Armstrong, 1985 & 1987). The literature as indicatedpreviously disagrees on the timing on the rise of finance personnel within particularorganizational forms. Armstrong (1985) linked the rise of accountants to the 1930depression and the multidivisional firm that arose in that period while Fligstein (1987)had made a link with the rise of finance personnel to the conglomerate, which heargued was a different organization than the multidivisional firm of the 1930s.

The evidence from Dunlop broadly supports Fligstein’s (1987) interpretation of thesematters with accountants in particular and finance personnel in general coming todominate the board of Dunlop once a conglomerate had been established. It issuggested that Armstrong (1985 & 1987) has by combining the USA and UKmultidivisional form to support the rise of accountants with labour techniquesmisunderstood and thus misinterpreted the significance of the multidivisional form ofthe 1930s. Fligstein (1987 & 1991) provides evidence that the multidivisional firm inthe USA of the 1930s arose to allow multi-product firms to exploit market segmentsand rather than being linked to the rise of finance personnel it was linked to marketingprofessionals. It is suggested that Fligstein’s (1987 & 1991) view and interpretation isconsistent with the empirical evidence of this case study. The tensions shown inFligstein’s (1987) research can also be interpreted by the Weberian perspective, whichwas predictive of ongoing tension within professional ranks.

Up until the 1980s there appears to be a fairly balanced struggle between accountantsand engineers (Appendix Table II) and the more broadly classified finance andtechnical personnel (Appendix Table III). The evenness of the struggle is particularlyevident when the chairman of the board and CEO positions is considered. Fligstein’s(1991) institutional view in regard to why particular professions are replaced bysimilar professions would in the case of Dunlop be more appropriately applied toengineers and technical staff than accountants. The Weberian perspective indicatingthe tensions between rationalities and the political struggles at the apex of

19

organizations is both instructive and supportive of Abbott’s (1988) view thatcompetition exists between professions. Armstrong’s (1985 & 1987) historicallydeterministic interpretation of the rise of the accounting profession during the 1930sand the early multidivisional stage is not as strongly supported. Based on theWeberian perspective it is suggested that the rise of accountants under theconglomerate form within Dunlop probably will only be a temporary phenomena ascontingent factors arise that influence the means and ends required.

The general pattern of gaining access to the CEO position within Dunlop wouldsuggest that the means (formal rationality) of both engineers and accountants haveover time been required. Armstrong’s (1985, 1987) view that engineers would beprevented from gaining access to the apex of organizations because their means is toodeterminate whereas accountants means are largely indeterminate would appear tohave limited application in this case. The Weberian perspective would suggest thatalthough means are important in the rise of professions so are the struggles connectedto ends (substantive rationality) and political processes within groups. It alsoacknowledges the importance of entrepreneurial and family connections in this type ofresearch, which is linked to the literature (Armstrong, 1985; Fligstein, 1987;Chandler, 1977). While Armstrong (1985) acknowledges the importance of familyconnections the critical role that he suggests for the multidivisional firm in the 1930sis a USA, not a UK phenomena (Chandler, 1977). The UK experience largelyparallels the Australian experience and is illustrated within Dunlop where suchconnections were important at the board and CEO level up until the 1980s. Undersuch circumstances it is difficult to promote multidivisions of firms in the 1930s as areason for the ascent of accountants.

SPECIFIC TRENDS

The specific trends of Dunlop provide evidence that the role of a particularprofessional are contingent on a range of factors other than the technical means thattheir professional bent may bring to an organization. Individual professionals canhave a well-developed sense of the indeterminate nature of management and given theappropriate contexts can use accounting techniques to achieve their objectives.Evidence for this is to be found in the activities of the following Dunlop CEOs -Bartlett, Blackwood and Jarman, two of them being engineers and one a militarygraduate.

Despite Dunlop’s links through UK Dunlop there is no evidence that particularlymanagement techniques based on a particular profession were sought during the 1930scrisis, although UK Dunlop was in a position to offer such a technique if one was onoffer. Armstrong’s (1985 & 1987) position that firms during the 1930s usedaccounting techniques to extract value from labour and in so doing promotedprofessional accountants to the apex of organizations cannot be supported in this case.Rather what emerges is a complex picture of various professions including engineersand accountants sharing the apex of Dunlop’s board and CEO positions withentrepreneurs, family owners and a coterie of the social and business elite. The 1930scrisis for Dunlop was a protracted affair and as has been indicated involved a numberof political tensions. Rather than being a time to extract maximum value from theDunlop labour force the evidence is that efficiency was not pursued at all costs.

20

Rather what was pursued and is supportive of Fligstein’s (1987 & 1991) analysis ofthe 1930s crisis was the manufacture of multiple products by Dunlop and an emphasison marketing. As Bartlett implemented his financial and labour efficiencies he asindicated took control of marketing. This once again indicates the contingent natureof this type of research and would suggest the usefulness of the Weberian perspectivewhen dealing with competition between professions. Although neither Bartlett norWatt should be considered Fabians, they certainly did not have anti-worker sentimentand worked together well as both were influenced by Fabian attitudes in regard toemployees. Thus while some literature may suggest a ruthlessness when dealing withworkers during the 1930s based on accounting techniques (Armstrong, 1985 & 1987),this case indicates that there were other threads as well that were shared acrossprofessions, indicative of the various ends (substantive rationalities) and politicalmachinations that the Weberian perspective reveals.

The replacement of Bartlett by Blackwood, a fellow engineer, in part reflected theview of the board that the company should have a CEO with a strong technicalbackground in manufacturing, although cordial relationship between management andworkers was also a factor. The success of Blackwood both as a CEO and Chair of thecompany underscores the indeterminate skills that successful management requires.While Blackwood never had the strong business background that Bartlett had, hisbusiness sense both as CEO and Chairman cannot be questioned. Evidence includesthe successful 1950s, the initial moves away from tyre dependence in the late 50s andearly 60s and his role as chair when Dunlop became a successful conglomerate.Blackwood’s appointment supports Fligstein’s (1987) empirical evidence thatproduction professionals would dominate single-product companies, for althoughDunlop was making many different products they were primarily linked to oneproduct, rubber. The appointment of Blackwood can in many ways be seen as aninstitutional response to executive appointment a view also consistent with theliterature (Fligstein, 1991). It certainly does challenge Armstrong’s (1985 & 1987)view that engineers are unable to compete at the apex of the corporate form.

Dunshea’s appointment as CEO, showed that Dunlop no longer consider technicalmanufacturing experience a necessary factor in that appointment. Dunshea, anaccountant had broad administrative experience and had successfully reorganizedDunlop into a multi-divisional firm (an innovative organizational structure forAustralia at the time). While it may have been expected that a multidivisionalstructure undertaken by an accountant in the mid 1960s would have been primarilymotivated by financial considerations this was not the case. The evidence is thatDunlop’s primary motivations for reorganization were not financial but linked tocustomer service and marketing (McVey, 1963 cf Dunlop Announcement 1963). Thisis in line with Fligstein’s (1987) interpretation that multidivisions were initially beganin the 1930s for marketing purposes and it is of some interest that this was stated asthe primary reason for their introduction into Dunlop in Australia some thirty yearslater.

The evidence is that Dunlop went through a learning curve in regard to themultidivisional form and despite many overseas contacts Dunlop had access to, it canat least be tentatively concluded based on this case study that the institutional effect oftransferring multidivisional techniques were not financially based as Armstrong

21

(1985) suggested. Further that the implementation of multidivisional techniques arenot dependent upon the technical skills unique to those of accountants but areavailable as the indeterminate means of competent managers from a range ofbackgrounds. The financial controls on the multi-divisions within Dunlop wereinitially extremely lax. When Jarman took control as CEO it was in the area offinance that he first took action, insisting that all requests for loans should come tohead office (Blainey, 1993). Under Dunshea the divisions and new acquisitions underthe policy of diversification had largely been allowed to operate in the financial areain an unsupervised manner. This once again indicates the contingent nature of themultidivisional organizational form and the wide range of uses that it can be put to byany particular professional group.

Once Dunlop had achieved the status of a stable and successful conglomerate thenumber of accountants at the board level increased dramatically which has widesupport within the literature (Armstrong, 1985 & 1987; Fligstein, 1987 & 1991) albeitbased on a timing difference and with a different interpretative approach. Theevidence however would suggest that accountants did not arrive in a position of suchdominance merely because of means that were suited to the control of particularaspects of the firm. The means of managerial control have also been evident fromother professional groups particularly engineers in the history of Dunlop. Nor wouldit appear that Dunlop was to follow the pattern of accountants’ ascendancy into theapex of the organization as suggested by Armstrong (1985). Rather than explainingsuch a pattern as resting on techniques to control labour it is suggested that theinstitutional explanations of Fligstein (1987 & 1991) along with the Weberianperspective of an ongoing struggle between man and man have much to offer. Theseexplanations are not deterministic but contingent and able to deal more adequatelywith future change.

CONCLUSIONS.

While it is recognized that any conclusions drawn from a single case study must betentative, this research does raise a number of doubts about the conclusions drawn byArmstrong in regard to the domination of the accounting profession and the reasonsfor that domination. Fligstein (1987 & 1991) and Abbott (1988) have providedgeneral evidence, both theoretical and empirical, that interprofessional competition isalive and well. This individual case study generally confirms their findings. UnlikeArmstrong who concludes that engineers are poorly positioned to compete withaccountants at the apex of organizations this research would suggest that this iscontingent on the circumstances. It has also been argued that the indeterminate natureof management at the apex of organizations rather than providing unique advantagesto accountants actually enable a wide range of professions to compete at that level.Furthermore other professions in their decision making at that level can use the formalrationality of accounting due to its indeterminacy.

This individual case study challenges the universal application of Armstrong’sanalysis particularly in regard to the timing and reasons for the rise of themultidivisional firm and its impact on the accounting profession. It suggests that any

22

interpretative framework as to the role of professions within organizations needs to bemore broadly and contingently based, a strength that the Weberian perspective bringsallowing both the formal and substantive rationalities and the political struggle oforganizations to be considered. More multi-disciplinary research is needed in this areato offer a broader interpretative framework as to the role of professions withinorganizations. Finally this research confirms that the application of accountingtechniques are not limited to the accounting profession which, rather than being asource of concern should be both encouraged and researched as a means ofinvigorating both accounting techniques and professional life generally.

23

APPENDIX

TABLE I

Profession Executive % Non-Executive % Total %None Stated 11 19% 11 19% 22 39%Accountant 4 7% 13 23% 17 30%Lawyer 0 0% 3 5% 3 5%Engineer 3 5% 5 9% 8 14%Military 1 2% 2 4% 3 5%Medical 0 0% 2 4% 2 4%Scientist 1 2% 1 2% 2 4%Total 20 35% 37 65% 57 100%

Dunlop’s Directors Classified by Profession, Australian Directors only, includingsubstitutes. Based on Cross Sectional Analysis from 1920 – 1995.

24

TABLE II

Year Total Subs Accountant % Engineer % Military % Medical % Scientist % Lawyer % Not Stated %1920 5 2 40% 0% 1 20% 0% 0% 1 20% 1 20%1925 5 1 20% 1 20% 1 20% 0% 0% 1 20% 1 20%1930 11 2 3 23% 2 15% 1 8% 0% 0% 1 8% 6 46%1935 14 3 3 18% 2 12% 2 12% 0% 0% 2 12% 8 47%1940 9 2 3 27% 2 18% 2 18% 0% 0% 0% 4 36%1945 8 3 3 27% 2 18% 1 9% 0% 0% 1 9% 4 36%1950 6 2 0% 2 25% 1 13% 0% 0% 1 13% 4 50%1955 11 2 1 8% 3 23% 1 8% 0% 0% 2 15% 6 46%1960 11 2 1 8% 2 15% 1 8% 0% 0% 3 23% 6 46%1965 10 2 1 8% 2 17% 0% 1 8% 0% 3 25% 5 42%1970 10 4 1 7% 2 14% 0% 1 7% 0% 2 14% 8 57%1975 12 3 2 13% 1 7% 1 7% 0% 1 7% 1 7% 9 60%1980 14 2 7 44% 0% 1 6% 0% 0% 1 6% 7 44%1985 13 7 54% 0% 1 8% 0% 0% 0% 5 38%1990 13 8 62% 1 8% 1 8% 0% 1 8% 0% 2 15%1995 12 7 58% 3 25% 0% 1 8% 0% 0% 1 8%

Dunlop’s Directors classified according to Professions, includes Australian and UK directors, plus substitutesBased on Cross Sectional Analysis from 1920 - 1995

25

TABLE III

Year Total Finance % Technical % Legal % Marketing % Medical % NotStated

%

1920 5 3 60% 1 20% 1 20% 0% 0% 0%1925 5 2 40% 2 40% 1 20% 0% 0% 0%1930 11 3 27% 4 36% 1 9% 1 9% 0% 2 18%1935 13 2 15% 3 23% 1 8% 1 8% 0% 6 46%1940 9 2 22% 3 33% 0% 0% 0% 4 44%1945 8 2 25% 3 38% 0% 0% 0% 3 38%1950 6 0% 3 50% 0% 0% 0% 3 50%1955 11 1 9% 4 36% 1 9% 1 9% 0% 4 36%1960 11 2 18% 3 27% 2 18% 1 9% 0% 3 27%1965 10 2 20% 2 20% 2 20% 1 10% 1 10% 2 20%1970 10 1 10% 2 20% 2 20% 1 10% 1 10% 3 30%1975 12 2 17% 5 42% 1 8% 1 8% 0% 3 25%1980 14 7 50% 4 29% 1 7% 0% 0% 2 14%1985 13 7 54% 4 31% 0% 0% 0% 2 15%1990 13 8 62% 5 38% 0% 0% 0% 0%1995 12 7 58% 4 33% 0% 0% 1 8% 0%

Dunlop’s Directors classified under a more ‘ad hoc’ General Classification. Australian directors only including Substitutes.Based on Cross Sectional Analysis from 1920-1995

26

Table IV

Name Period of Time Years ProfessionGrice 1920-1929 9 LawyerWatt 1929-1946 17 AccountantBartlett 1946-47 1 EngineerStewart 1947-56 9 EngineerMcVey 1956-1968 12 EngineerDunshea 1968-1972 4 AccountantBlackwood 1972-1979 7 EngineerMassey-Greene

1979-1986 7 Not Stated

Froggart 1986-1990 4 AccountantGough 1990-1995 5 Technical

Chairman of the Dunlop Board for Period, 1920 – 1995

Table V

GeneralName Period as CEO Total Years Profession ClassificationW.J. Proctor 1895-1928 33 Accountant FinanceD.J. Snodgrass 1928-1929 2 None Stated None StatedF.J. Ormiston Joint 1929-1935 6 None Stated TechnicalA.Fenton Joint 1929-1935 6 None Stated MarketingW.A.Bartlett 1935-1947 12 Engineer TechnicalR.Blackwood 1948-1966 19 Engineer TechnicalE.Dunshea 1966-1972 6 Accountant FinanceE.A.Kellam 1972-1974 2 None stated MarketingL.Jarman 1974-1980 6 Military TechnicalJ.Gough 1980-1987 7 None stated TechnicalP.Brass 1988-1995 7 Accountant Finance

CEO of Dunlop for Period, 1920 - 1995

27

Bibliography

Abbott, Andrew. (1988), The System of Professions - An Essay on the Division of Expert

Labour, The University of Chicago Press, Chicago.

Albrow, M. (1970), Bureaucracy, Pall Mall Press, London.

Anon (1925), “Dunlop Rubber Company: Increase in Profits”, Argus. Melbourne.

Anon (1963), Dunlop Announces Reorganisation Plans, Dunlop Rubber Australia Ltd.

Anon (1975), Australian Financial Review, Sydney.

Armstrong, P. (1985), “Changing Management Control Strategies: The role of Competition

between Accountancy and other Organisational Professions”, Accounting, Organisations and

Society 10 (2): 129-148.

Armstrong, P. (1987), “The Rise of Accounting Controls in British Capitalistic Enterprises”,

Accounting, Organisations and Society 12 (5): 415-436.

Armstrong, P. (1987b), “Engineers, Managment and Trust”, Work, Employment & Society 1

(4): 421-440.

Berle, A. A. J., & Means, Gardiner C., (1992), The Modern Corporation and Private Property.

New York: Macmillian, 1-9, 112-16, 309-16. The Rise of Big Business, B. E. Supple. Edward

Elgar Publishing Ltd. 5: 1-24, Aldershot, England

Bernstein, R.J. (1976), The Restructuring of Social and Political Theory, University of

Pennsylvania Press, Philadelphia.

Bernstein, R. J. (1983), Beyond Objectivism and Relativism, Basil Blackwood, Oxford.

Blainey, G. (1993), Jumping over the Wheel, Allen & Unwin, St Leonards.

Brubaker, R. (1984), The Limits of Rationality, An essay on the Social and Moral Thought of

Max Weber, George Allen & Unwin, London.

28

Burchell, S., C. Clubb, et al. (1980), “The roles of Accounting in Organisations and Society”,

Accounting, Organisations and Society 5(1): 5-27.

Burger, T. (1976), Max Weber's Theory of Concept Formation.. History, Laws, and Ideal

Types, Duke University Press, Durham, North Carolina.

Chairman (1948), Chairman’s Report, Dunlop Rubber Australia Ltd, Melbourne.

Chairman (1950), Chairman’s Report, Dunlop Rubber Australia Ltd, Melbourne.

Chairman (1964). Chairman’s Report, Dunlop Rubber Australia Ltd, Melbourne.

Chandler, A. D. J. (1977), The Visible Hand. The Managerial Revolution in American

Business, Harvard University Press, Cambridge, Mass.

Chandler, A. D. (1992), “The Emergence of Managerial Capitalism”, Business History

Review, 58 (4), Winter, 473 - 503. The Rise of Big Business, B. Supple. Edward Elgar

Publishers, Aldershot, England.

Chua, W. F. (1986), “Radical Developments in Accounting Thought”, The Accounting

Review LXI (No 4): 601-632.