the global economic environment policy challenges per... · 2016-11-26 · the global economic...

TRANSCRIPT

Odd Per Brekk

Director

IMF Regional Office for Asia and the Pacific

June 3, 2015

The Global Economic Environment

Policy Challenges

Global Economic Outlook

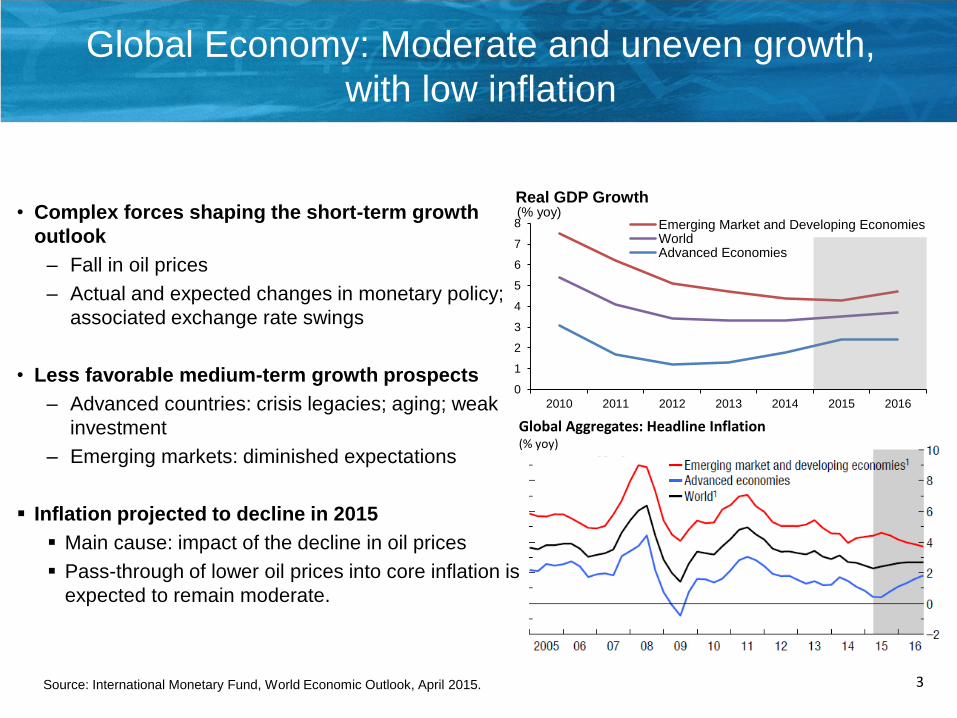

Global Economy: Moderate and uneven growth,

with low inflation

• Complex forces shaping the short-term growth

outlook

– Fall in oil prices

– Actual and expected changes in monetary policy;

associated exchange rate swings

• Less favorable medium-term growth prospects

– Advanced countries: crisis legacies; aging; weak

investment

– Emerging markets: diminished expectations

Inflation projected to decline in 2015

Main cause: impact of the decline in oil prices

Pass-through of lower oil prices into core inflation is

expected to remain moderate.

3Source: International Monetary Fund, World Economic Outlook, April 2015.

Global Aggregates: Headline Inflation(% yoy)

0

1

2

3

4

5

6

7

8

2010 2011 2012 2013 2014 2015 2016

(% yoy)Real GDP Growth

Emerging Market and Developing EconomiesWorldAdvanced Economies

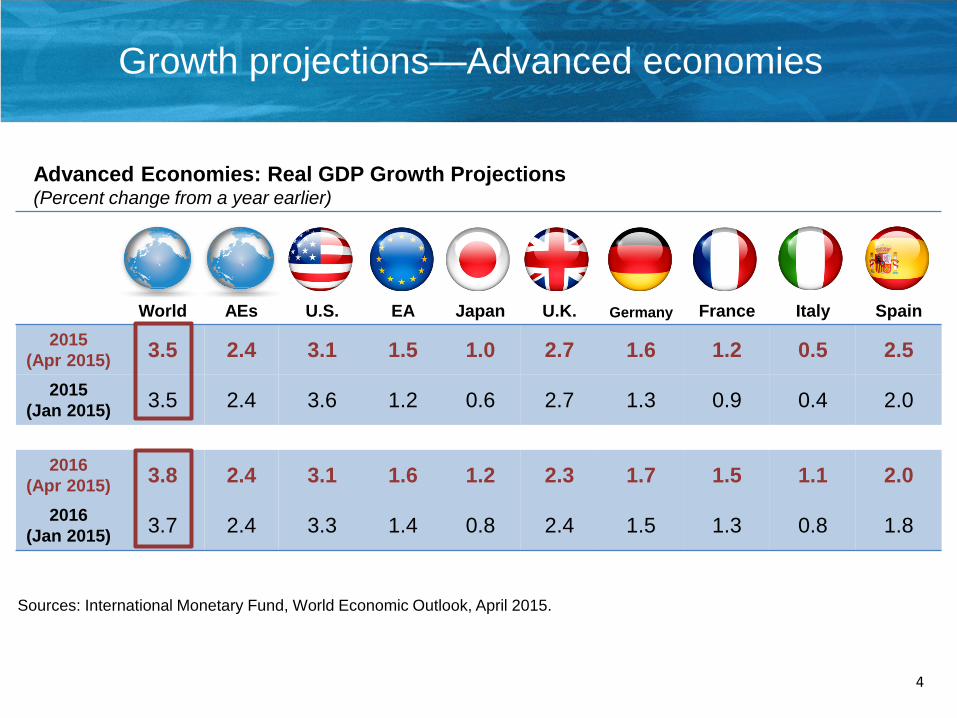

Growth projections—Advanced economies

4

World AEs U.S. EA Japan U.K. Germany France Italy Spain

2015

(Apr 2015)3.5 2.4 3.1 1.5 1.0 2.7 1.6 1.2 0.5 2.5

2015

(Jan 2015)3.5 2.4 3.6 1.2 0.6 2.7 1.3 0.9 0.4 2.0

2016

(Apr 2015)3.8 2.4 3.1 1.6 1.2 2.3 1.7 1.5 1.1 2.0

2016

(Jan 2015)3.7 2.4 3.3 1.4 0.8 2.4 1.5 1.3 0.8 1.8

Advanced Economies: Real GDP Growth Projections (Percent change from a year earlier)

Sources: International Monetary Fund, World Economic Outlook, April 2015.

5

EMDEs China India Russia LAC Brazil Mexico LIDCs

2015

(Apr 2015)4.3 6.8 7.5 -3.8 0.9 -1.0 3.0 5.5

2015

(Jan 2015)4.3 6.8 6.3 -3.0 1.3 0.3 3.2 5.9

2016

(Apr 2015)4.7 6.3 7.5 -1.1 2.0 1.0 3.3 6.0

2016

(Jan 2015)4.7 6.3 6.5 -1.0 2.3 1.5 3.5 6.1

Emerging Market and Developing Economies: Real GDP Growth Projections (Percent change from a year earlier)

Sources: International Monetary Fund, World Economic Outlook, April 2015.

Growth projections—Emerging market

and developing economies

0

40

80

120

160

200

DJ Euro Stoxx

S&P 500

MSCI Emerging Market

TOPIX

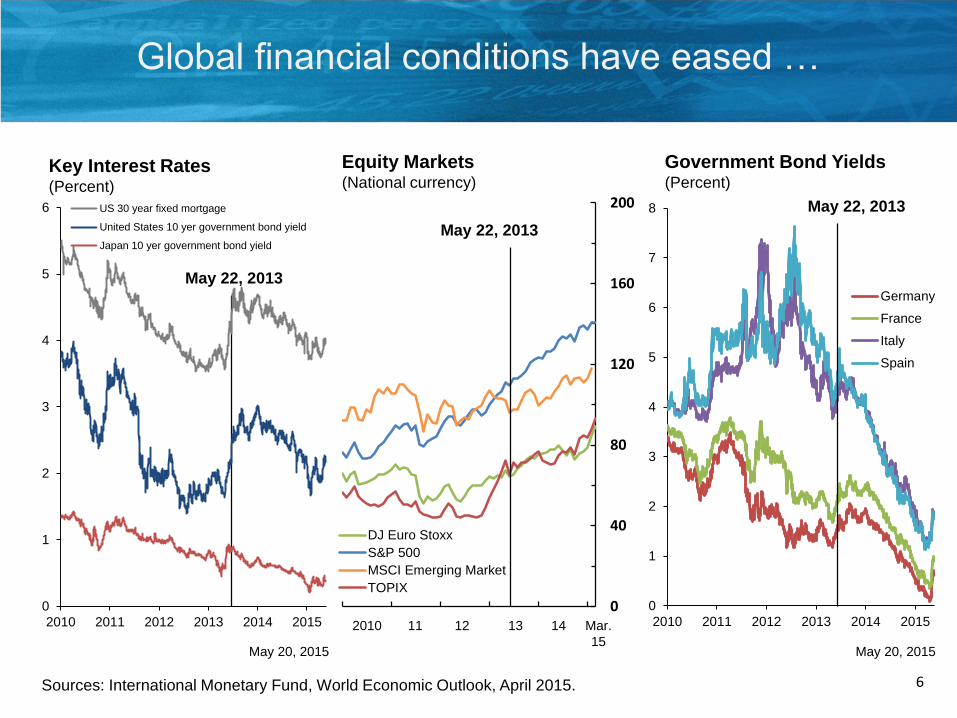

Equity Markets(National currency)

Key Interest Rates(Percent)

Government Bond Yields(Percent)

May 22, 2013

May 22, 2013

May 22, 2013

Global financial conditions have eased …

2010 11 1312 Mar.

15

14

Sources: International Monetary Fund, World Economic Outlook, April 2015. 6

0

1

2

3

4

5

6

7

8

2010 2011 2012 2013 2014 2015

Germany

France

Italy

Spain

0

1

2

3

4

5

6

2010 2011 2012 2013 2014 2015

US 30 year fixed mortgage

United States 10 yer government bond yield

Japan 10 yer government bond yield

May 20, 2015 May 20, 2015

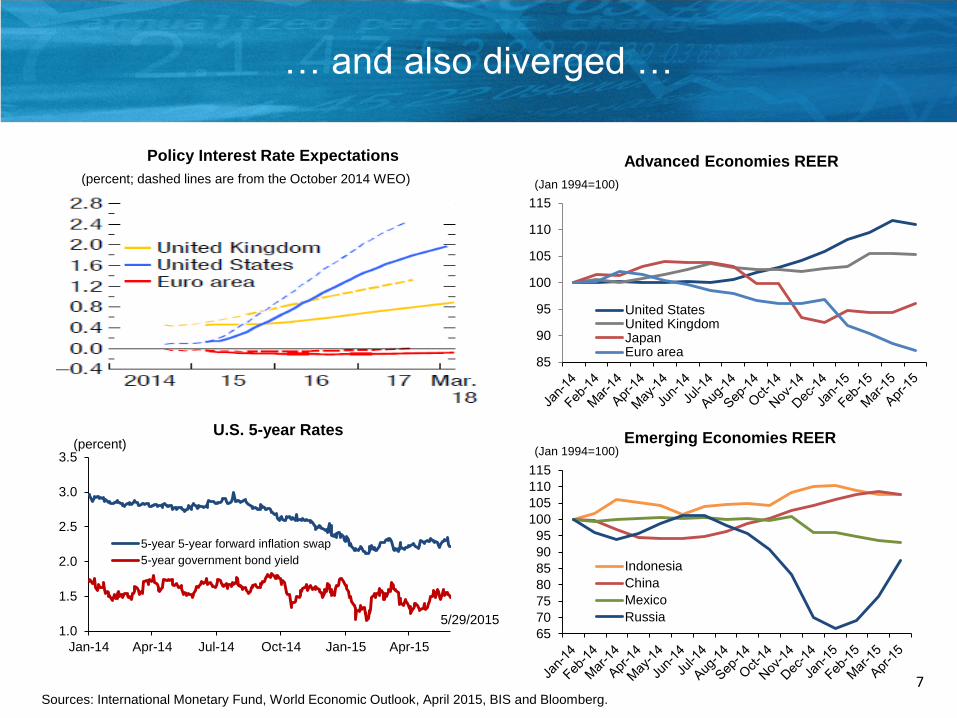

… and also diverged …

7

U.S. 5-year Rates

Sources: International Monetary Fund, World Economic Outlook, April 2015, BIS and Bloomberg.

5/29/2015

Advanced Economies REER

Emerging Economies REER

(Jan 1994=100)

(Jan 1994=100)

85

90

95

100

105

110

115

United StatesUnited KingdomJapanEuro area

Policy Interest Rate Expectations

65

70

75

80

85

90

95

100

105

110

115

Indonesia

China

Mexico

Russia1.0

1.5

2.0

2.5

3.0

3.5

Jan-14 Apr-14 Jul-14 Oct-14 Jan-15 Apr-15

5-year 5-year forward inflation swap

5-year government bond yield

(percent; dashed lines are from the October 2014 WEO)

(percent)

Forecast assumptions:

Partial and gradual reversal of oil price decline

8

Oil Spot and Futures Prices(IMF APSP, U.S. dollars per barrel)

Sources: IMF, GAS Live database; International Energy Agency (IEA).

40

60

80

100

120

2011M1 2012M1 2013M1 2014M1 2015Q1 2016Q1

Oil Price

April 2015 projection

October 2014 projection

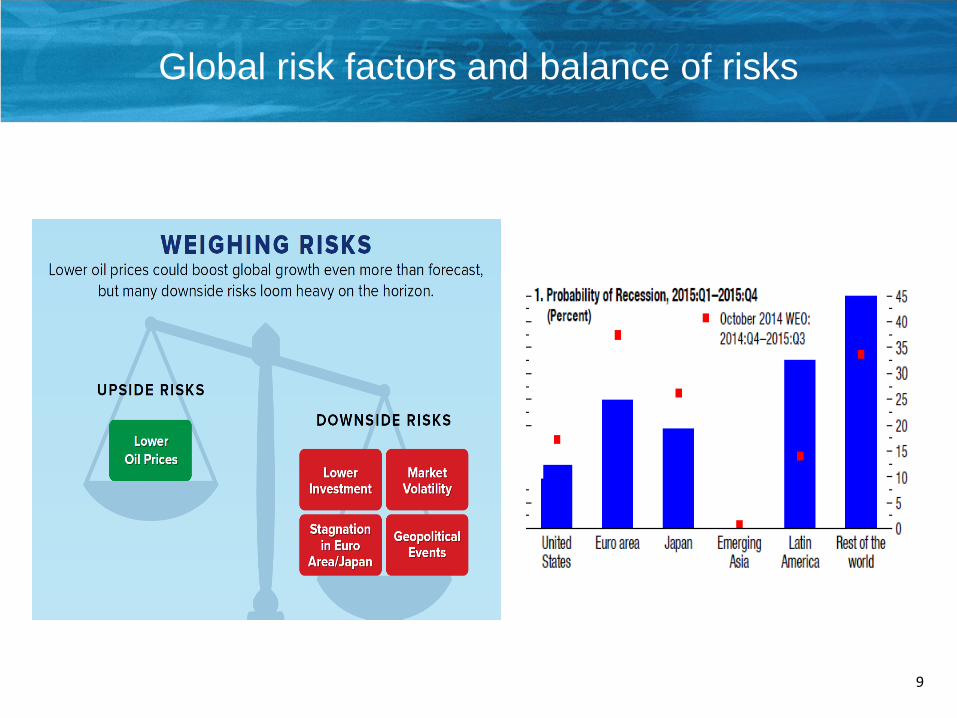

Potential Impact of the Decline in

Oil Prices since Aug 2014(percent change)

9

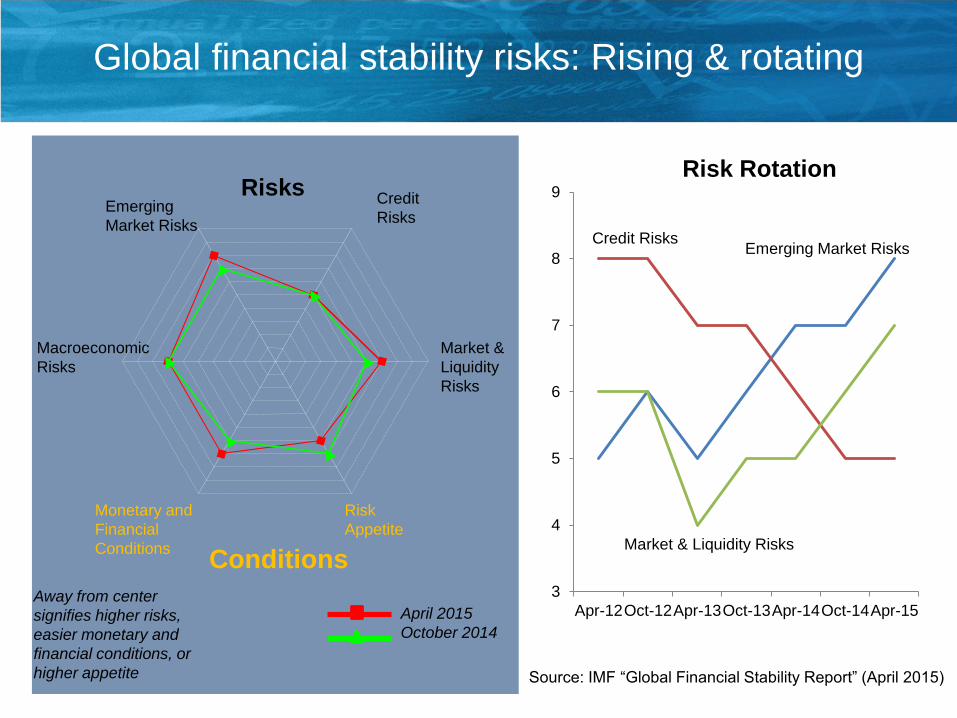

Global risk factors and balance of risks

3

4

5

6

7

8

9

Apr-12Oct-12Apr-13Oct-13Apr-14Oct-14Apr-15

Credit Risks

Market & Liquidity Risks

Emerging Market Risks

Risk Rotation

2

Emerging

Market Risks

Credit

Risks

Market &

Liquidity

Risks

Macroeconomic

Risks

Monetary and

Financial

Conditions

Risk

Appetite

Conditions

Risks

Away from center

signifies higher risks,

easier monetary and

financial conditions, or

higher appetite

Global financial stability risks: Rising & rotating

Source: IMF “Global Financial Stability Report” (April 2015)

April 2015

October 2014

Asian Economic Outlook

(percent change from a year earlier)

12

Asia—Growth outlook

Note: East Asia includes China, Hong Kong SAR, Korea, Taiwan POC. South Asia includes Bangladesh, India and Sri Lanka.

Source: International Monetary Fund, Regional Economic Outlook, May 2015.

2014 2015 2016

Asia 5.6 5.6 5.5

Japan -0.1 1.0 1.2

East Asia 6.7 6.3 5.9

China 7.4 6.8 6.3

Korea 3.3 3.3 3.5

South Asia 7.1 7.4 7.4

India 7.2 7.5 7.5

ASEAN 4.6 5.1 5.3

Indonesia 5.0 5.2 5.5

Malaysia 6.0 4.8 4.9

Philippines 6.1 6.7 6.3

Singapore 2.9 3.0 3.0

Thailand 0.7 3.7 4.0

Vietnam 6.0 6.0 5.8

13

Asia: Region will benefit from oil price decline

Impact of Oil Price Decline on Macro–forecasts

(In percentage points of GDP; growth in percent)Oil Price Windfall: Impact on the Oil Trade Balance in 2015

(In percent of GDP)

Less than 1.5%

Between 1.5-3%

Greater than 3%

Country Oil Price windfall

Australia 0.2

Vietnam 0.4

Malaysia 0.7

New Zealand 0.9

China 0.9

Indonesia 1.1

Japan 1.4

Philippines 1.8

Singapore 1.9

India 2.0

Taiwan Province of China 2.1

Korea 2.7

Hong Kong SAR 2.8

Thailand 5.0

Asia (simple average) 1.7

Asia (weighted average) 1.4

Source: IMF staff estimates.Note: Based on 2014 oil trade balance, assuming unchanged quantities and the April 2015 WEO oil

price projections for 2015.

-4

-3

-2

-1

0

1

2

GDP Growth S-I (public) S-I (private) Current accountbalance

Commodity exporters

Simple average Weighted average

Max

Min

-1

0

1

2

3

GDP Growth S-I (public) S-I (private) Current accountbalance

Net oil importers

Simple average

Weighted averageMax

Min

Asia: Domestic demand remains the growth driver

-2

0

2

4

6

8

10

2014 2015 2014 2015 2014 2015 2014 2015 2014 2015 2014 2015

Asia Australia,Japan & New

Zealand

China East Asia(excl. China)

India ASEAN

Net exports Investment Consumption Growth

Contributions to Projected Growth(in percentage points; year over year)

Sources: IMF, World Economic Outlook; and IMF staff calculations.

Note: ASEAN includes Indonesia, Malaysia, the Philippines, Singapore, Thailand, and Vietnam

14

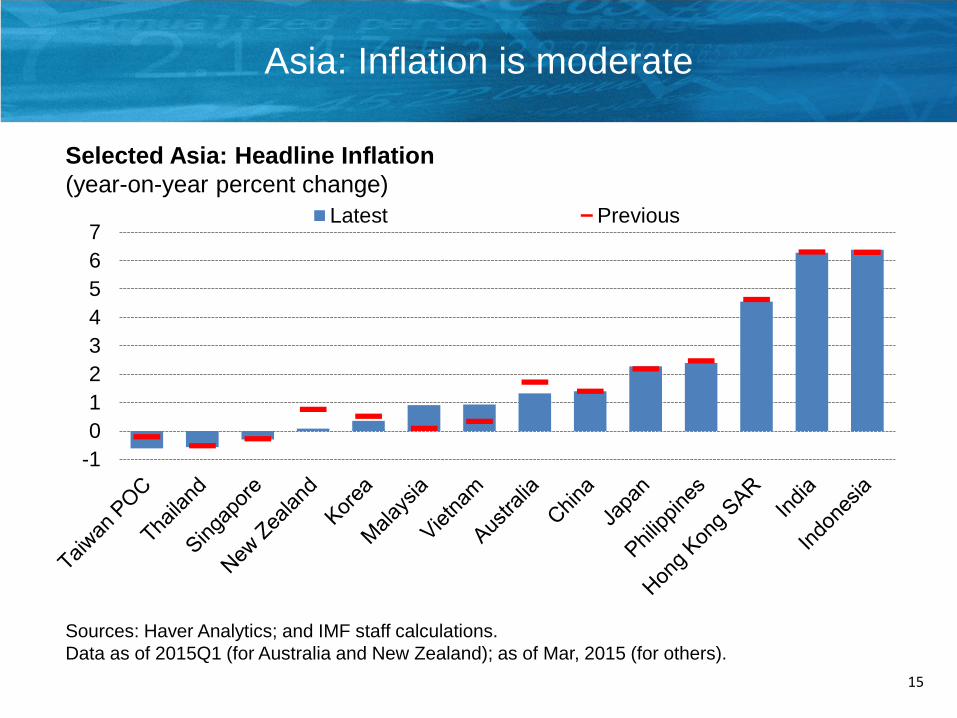

Asia: Inflation is moderate

15

Sources: Haver Analytics; and IMF staff calculations.

Data as of 2015Q1 (for Australia and New Zealand); as of Mar, 2015 (for others).

-1

0

1

2

3

4

5

6

7Latest Previous

Selected Asia: Headline Inflation

(year-on-year percent change)

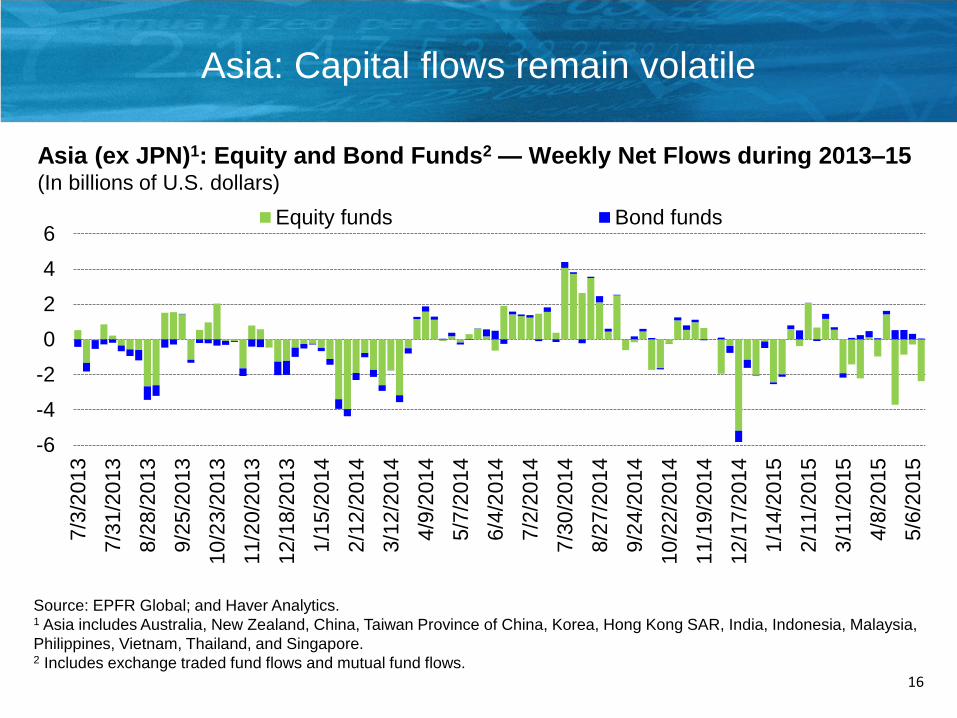

Asia: Capital flows remain volatile

16

Source: EPFR Global; and Haver Analytics.1 Asia includes Australia, New Zealand, China, Taiwan Province of China, Korea, Hong Kong SAR, India, Indonesia, Malaysia,

Philippines, Vietnam, Thailand, and Singapore.2 Includes exchange traded fund flows and mutual fund flows.

-6

-4

-2

0

2

4

6

7/3

/2013

7/3

1/2

013

8/2

8/2

013

9/2

5/2

013

10/2

3/2

013

11/2

0/2

013

12/1

8/2

013

1/1

5/2

014

2/1

2/2

014

3/1

2/2

014

4/9

/2014

5/7

/2014

6/4

/2014

7/2

/2014

7/3

0/2

014

8/2

7/2

01

4

9/2

4/2

014

10/2

2/2

014

11/1

9/2

014

12/1

7/2

014

1/1

4/2

015

2/1

1/2

015

3/1

1/2

015

4/8

/2015

5/6

/2015

Equity funds Bond funds

Asia (ex JPN)1: Equity and Bond Funds2 — Weekly Net Flows during 2013–15(In billions of U.S. dollars)

Real exchange rates have appreciated

17

Sources: Haver Analytics; and IMF staff calculations.

CHN

HK IND

IDN

KOR

MYS

PHL

SGP

THL

AUS

NZ

JPN

USA

EUR

-15

-10

-5

0

5

10

15

20

REER appreciation since June vs 2014 external assessment

External position

<-- weaker stronger-->

Ap

pre

cia

tio

n --

>

"moderately" "substantially""moderately"

Sources: IMF Global Data Source; IMF Staff Reports; IMF staff calculations.

0

5

10

15

20

25

30

35

40

45

To

tal

No

nfin

ancia

l

To

tal

No

nfin

ancia

l

To

tal

No

nfin

ancia

l

To

tal

No

nfin

ancia

l

To

tal

No

nfin

ancia

l

To

tal

No

nfin

ancia

l

To

tal

No

nfin

ancia

l

To

tal

No

nfin

ancia

l

Korea TaiwanProvince of

China

Indonesia Malaysia Philippines Thailand China India

Resident

Nonresident national

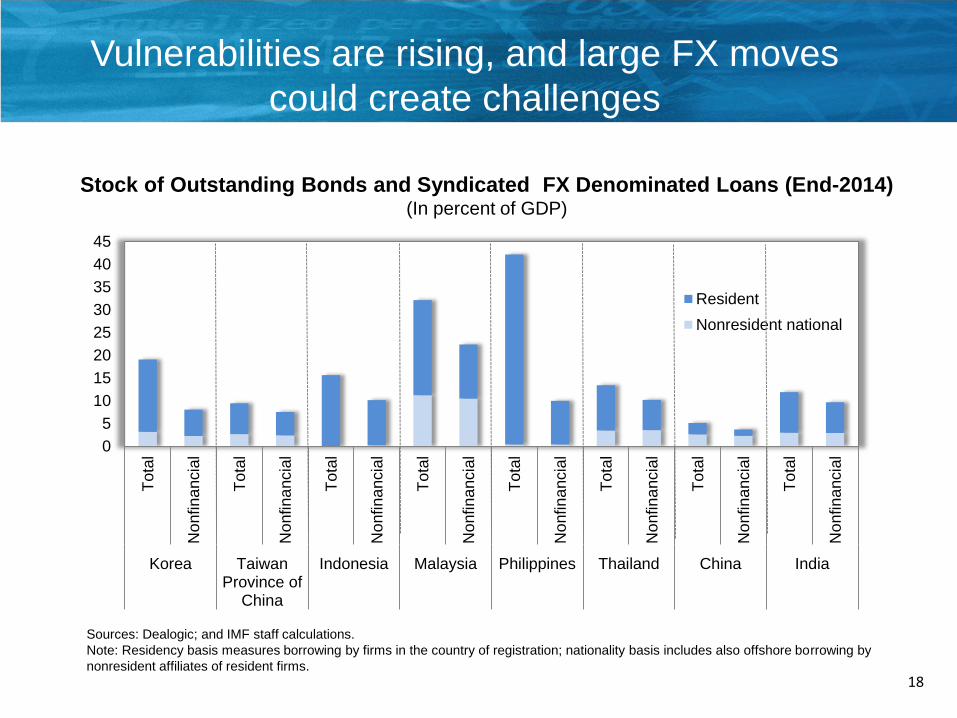

Stock of Outstanding Bonds and Syndicated FX Denominated Loans (End-2014)(In percent of GDP)

Vulnerabilities are rising, and large FX moves

could create challenges

Sources: Dealogic; and IMF staff calculations.

Note: Residency basis measures borrowing by firms in the country of registration; nationality basis includes also offshore borrowing by

nonresident affiliates of resident firms.

18

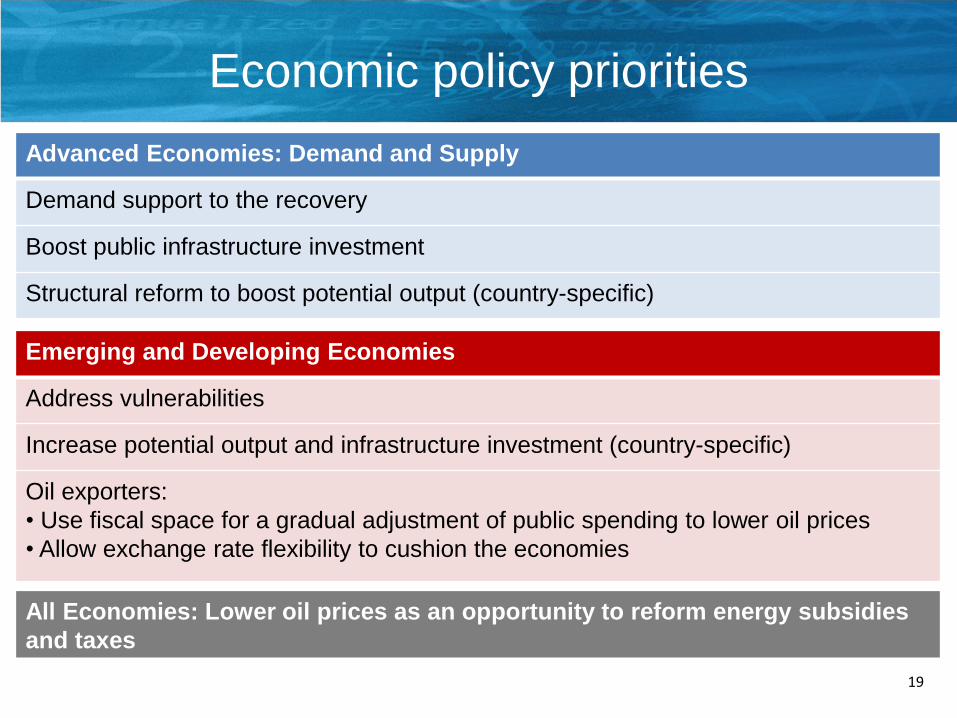

Economic policy priorities

Advanced Economies: Demand and Supply

Demand support to the recovery

Boost public infrastructure investment

Structural reform to boost potential output (country-specific)

All Economies: Lower oil prices as an opportunity to reform energy subsidies

and taxes

Emerging and Developing Economies

Address vulnerabilities

Increase potential output and infrastructure investment (country-specific)

Oil exporters:

• Use fiscal space for a gradual adjustment of public spending to lower oil prices

• Allow exchange rate flexibility to cushion the economies

19

Thank you!