© 2010 deloitte touche tohmatsu transfer pricing challenges in a difficult economic environment...

TRANSCRIPT

© 2010 Deloitte Touche Tohmatsu

Transfer Pricing Challenges in a Difficult Economic Environment

Mark Atkinson

May 27, 2010

© 2010 Deloitte Touche Tohmatsu

What were the effects of the global financial crisis?

• Since 2008, there have been significant changes in:

‒ Input prices of goods and commodities;

‒ Foreign exchange rates;

‒ The availability of credit; and

‒ Interest rates.

How did this affect transfer pricing?

• These resulted in transfer pricing systems giving anomalous results.

• As a result, many transfer pricing systems were now “broken”, as they did not work as intended.

• To fix the transfer pricing systems, it is necessary to consider:

‒ Measurement: how do you measure performance against market circumstances when there is a lag before the market data is available?

‒ Risk allocation: for each business risk, who should bear the effect of these changes?

2

© 2010 Deloitte Touche Tohmatsu

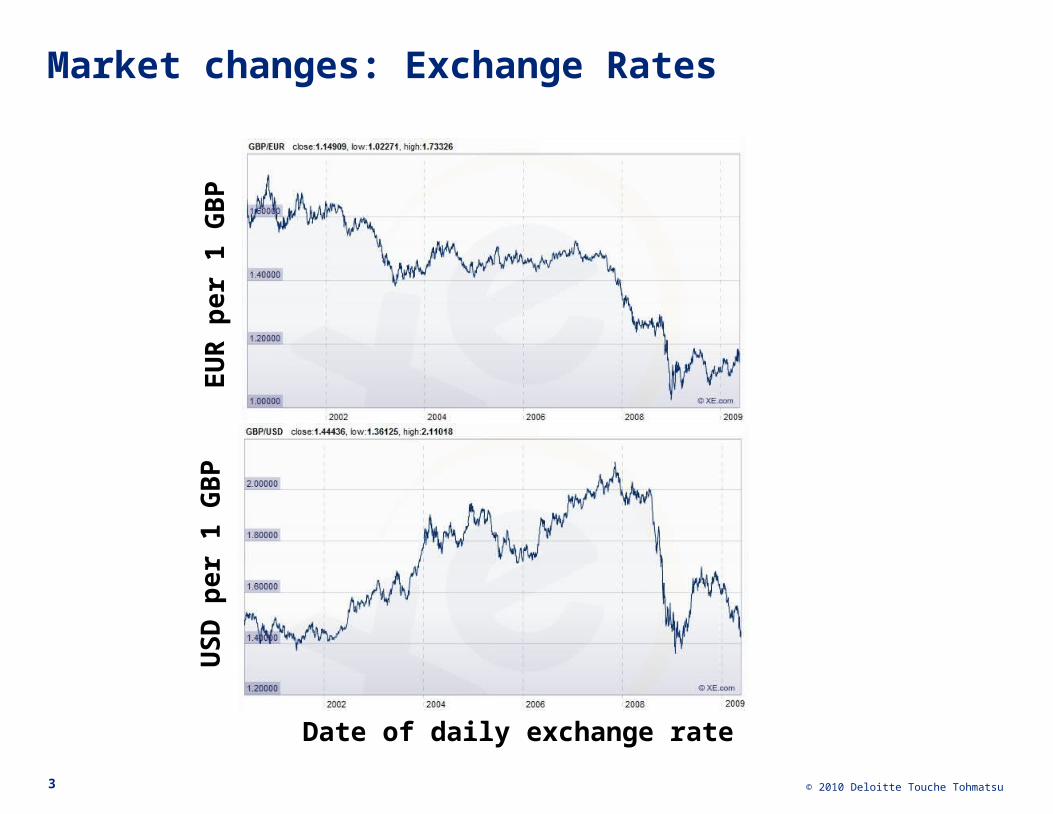

Market changes: Exchange Rates

3

Date of daily exchange rate

US

D p

er

1 G

BP

EU

R p

er

1 G

BP

© 2010 Deloitte Touche Tohmatsu

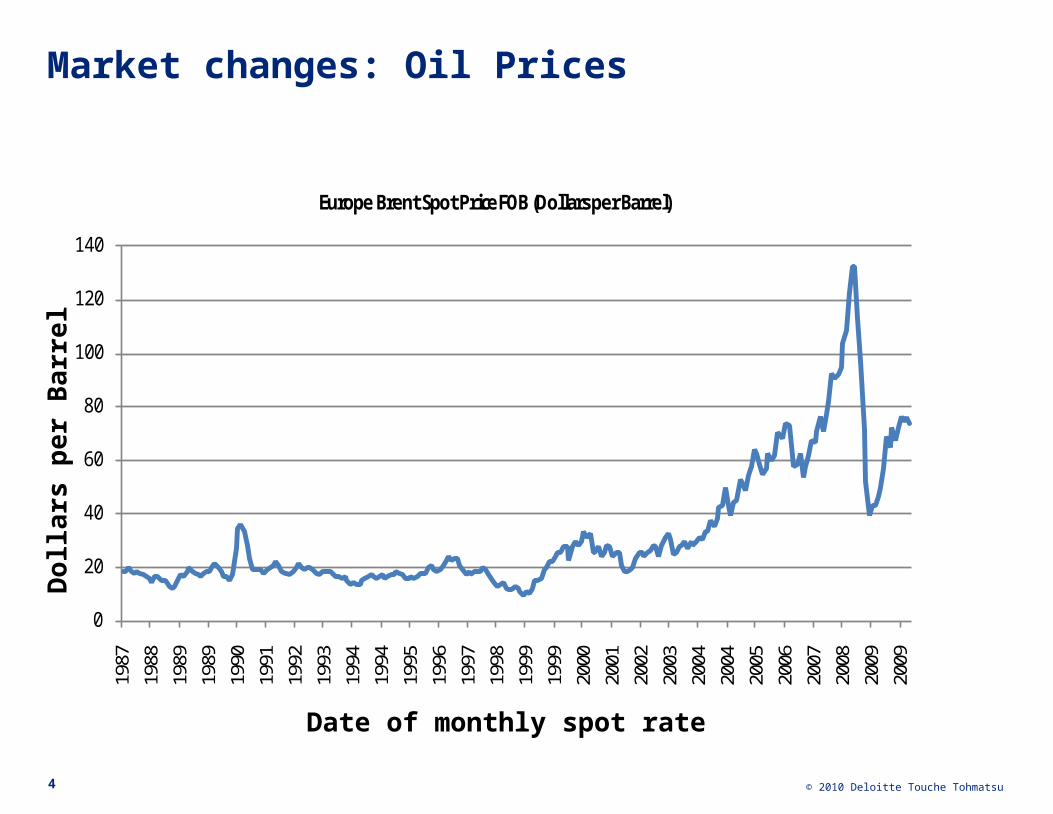

Market changes: Oil Prices

4

0

20

40

60

80

100

120

140

1987

1988

1989

1989

1990

1991

1992

1993

1994

1994

1995

1996

1997

1998

1999

1999

2000

2001

2002

2003

2004

2004

2005

2006

2007

2008

2009

2009

Europe Brent Spot Price FOB (Dollars per Barrel)

Date of monthly spot rate

Do

llars

per

Ba

rre

l

© 2010 Deloitte Touche Tohmatsu

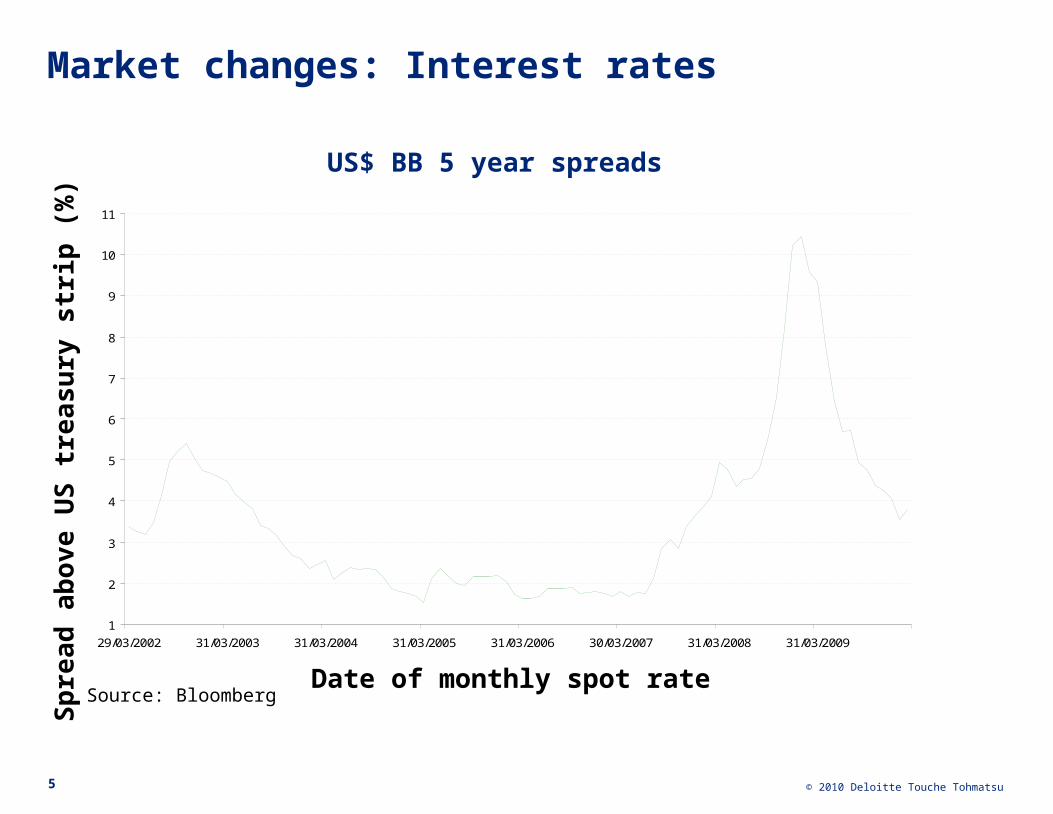

Market changes: Interest rates

5

1

2

3

4

5

6

7

8

9

10

11

29/03/2002 31/03/2003 31/03/2004 31/03/2005 31/03/2006 30/03/2007 31/03/2008 31/03/2009

Date of monthly spot rateSp

read

ab

ov

e U

S t

rea

sury

str

ip (

%)

Source: Bloomberg

US$ BB 5 year spreads

© 2010 Deloitte Touche Tohmatsu

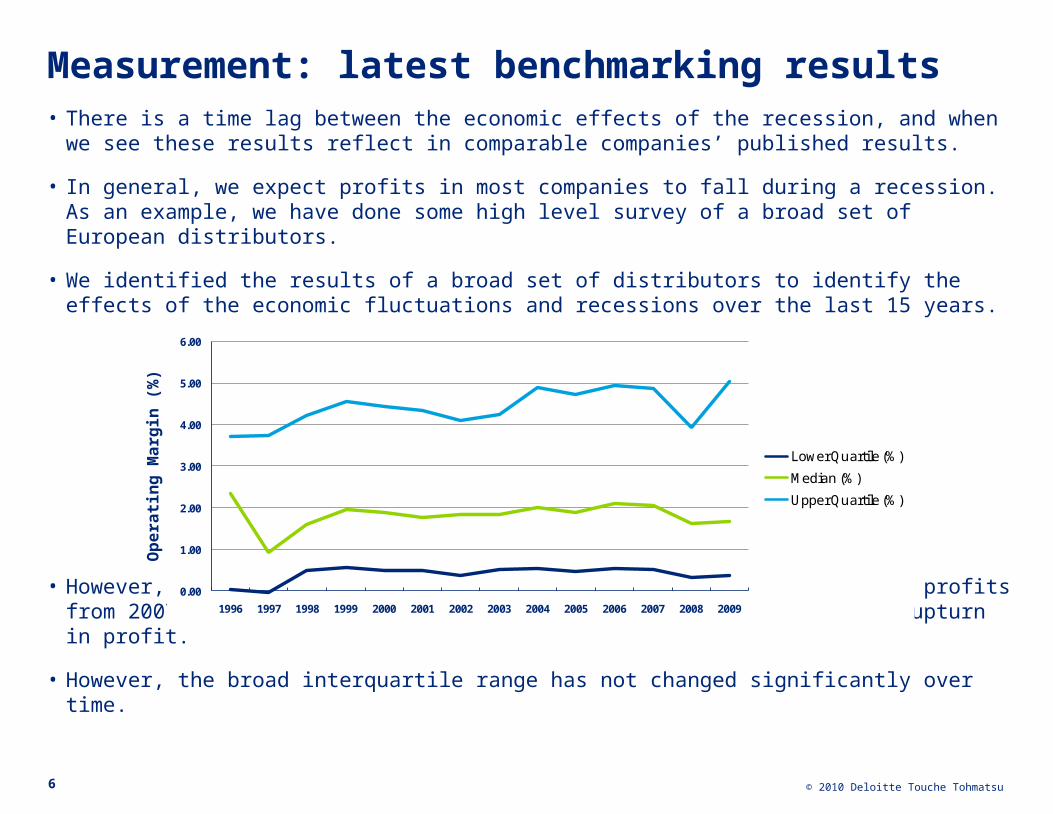

Measurement: latest benchmarking results• There is a time lag between the economic effects of the recession, and when we see

these results reflect in comparable companies’ published results.

• In general, we expect profits in most companies to fall during a recession. As an example, we have done some high level survey of a broad set of European distributors.

• We identified the results of a broad set of distributors to identify the effects of the economic fluctuations and recessions over the last 15 years.

• However, the 3-year average calculated now will still include higher profits from 2007. The results from 2009 are not yet complete, but show an upturn in profit.

• However, the broad interquartile range has not changed significantly over time.

6

0.00

1.00

2.00

3.00

4.00

5.00

6.00

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Lower Quartile (%)

Median (%)

Upper Quartile (%)

Op

era

tin

g M

arg

in (

%)

© 2010 Deloitte Touche Tohmatsu

Measurement: adjustments to benchmarking results• There is a significant amount of transfer pricing literature on potential adjustments which can be made to

continue to make use of benchmarking studies.

• Adjustments can be made to both tested party and comparable companies’ financial data.

• Examples of possible adjustments are:

‒ Decreasing the tested party’s SG&A expenditure in line with sales to adjust for the effect of lower levels of gross profit, in cases where variable / gross profit has declined to below the level of fixed costs. In similar situations, the comparison could be performed at the gross margin level, instead of at operating profit level.

‒ Making adjustment to construct the results which would have been achieved by the tested party, in the absence of the effects of risks which neither party would have been able to control (such as macroeconomic conditions). Specific restructuring costs could be excluded from the results of the tested party and comparable companies.

‒ Updating comparable companies’ financial data using projected, interim or forecast data to give more weight to more relevant periods.

‒ Targeting a lower point (such as the lower quartile) or a lower range (such as between the 10th and 60th percentiles) within the full range of results of comparable companies’ data from existing periods. Alternatively, a secondary PLI could be used as corroboration of a low point within the range.

‒ Including loss-making companies in the selection of comparable companies, and using a shorter (2008/09 only) or longer multi-year period for comparison.

‒ Where profitability is directly related to a commodity price or other economic indicator, a linear regression analysis could be used to show the link between an entity’s profitability and the external independent variable.7

© 2010 Deloitte Touche Tohmatsu

Risk allocation: intercompany contracts

• Intercompany contracts tend to be quite short or generic, and may only address basic structural issues and basic specific transaction related risks such as ownership of inventory, operating as a toll manufacturer or flash title distributor etc.

• Intercompany contracts often do not specify which party will bear risks which were not anticipated at the outset, for example where:

‒ More marketing expenditure was required;

‒ Input prices increased; or

‒ There were significant changes in foreign exchange rates.

• To address this, there are two options:

‒ Consider the impact of these effects under the existing intercompany agreements, and make adjustments to cater for these; or

‒ Go back to basic principles, and consider what the treatment of these risks would be between two unrelated parties operating at arm’s length.

8

© 2010 Deloitte Touche Tohmatsu

Risk allocation: exchange rate volatility

• Significant changes in exchange rates, combined with decreased margins, can have exaggerated effects on distribution of profits; e.g. Sterling declined 21% against the Euro during 2008.

• Intra-group agreements often do not adequately cover the assignment of foreign exchange risks between related parties.

• Often, foreign exchange risks are dictated by the group’s functional or reporting currency, which is used for all intra-group transactions, but do not reflect how exchange rate risks would be shared between third parties.

• In some cases, both parties could incur exchange rate risk on the same transaction; e.g. if a UK company sells to a Swedish company in Euros.

• What would the allocation of currency risks be in an arm’s length transaction? Is it appropriate to update agreements to reflect this? To what extent should losses be compensated arising from

a) Price lists set in a foreign currency

b) Exchange rate losses arising on settlement of intercompany invoices

• . 9

© 2010 Deloitte Touche Tohmatsu

APAs as a solution to uncertainty

• APAs seem to grow even in an economic downturn, as they offer certainty in a situation when the results of a transfer pricing analysis are open to interpretation.

• In an APA, the effects of market risks or the economic downturn can be agreed by making adjustments to the benchmarking approach.

• It may also be possible to revise an existing APAs where, for example, critical assumptions may not be met, or the fundamentals of the business have changed.

10

© 2010 Deloitte Touche Tohmatsu

Intra-group financing

• Interest rates applicable to intra-group financing have fluctuated significantly over the last two years; including both risk-free and LIBOR rates, as have risk premiums. The difference between short-term and long-term interest rates is also greater due to low short-term base rates and a steeper yield curve.

• Therefore, the terms of intra-group debt are important to establish what the arm’s length interest rate would be.

• The key consideration is at what point the pricing of the loan should be evaluated; normally, this is the time at which the loan was made.

• However, there could be a challenge from a tax authority if a loan was made at the time of the spike in interest rates. Alternatively, the average risk premium during a previous period could be used.

• Most official interest rates used as safe harbours are low and don’t reflect the higher risk premiums required for most borrowers.

• The applicable credit spreads can be very different, and risk-free / base rates change significantly depending on the term of the loan; so the choice of using 1, 3, 6 or 12 month LIBOR can be significant.

• The changes also mean that a previously benchmarked interest rate or risk premium is likely to no longer be appropriate for use with new debt.

11

© 2010 Deloitte Touche Tohmatsu

Summary

• The global financial crisis resulted in effects which included volatility in the price of inputs (such as goods and commodities), exchange rates, and the availability and price of credit.

• This resulted in transfer pricing systems being broken, as they no longer provided results as intended.

• To fix the transfer pricing systems, it is necessary to consider the measurement of market data when there is a time lag before market data is available, and the allocation risks, where these had not been considered in advance.

• There are various adjustments which can be made to the tested party and comparable data, in the absence of current comparable market data.

• In particular, the changes will significantly affect the pricing of intra-group financing arrangements.

• The allocation of business risks can be addressed by either catering for the impact of the effects, or by recharacterising the intercompany agreements based on what would be done in an arm’s length situation.

12

About DeloitteDeloitte refers to one or more of Deloitte Touche Tohmatsu, a Swiss Verein, and its network of member firms, each of which is a legally separate and independent entity. Please see www.deloitte.com/about for a detailed description of the legal structure of Deloitte Touche Tohmatsu and its member firms. Please see www.deloitte.com/us/about for a detailed description of the legal structure of Deloitte LLP and its subsidiaries.

Copyright © 2010 Deloitte Development LLC. All rights reserved.Member of Deloitte Touche Tohmatsu