the global crisis, foreign direct investment and china · pdf fileforeign direct investment,...

TRANSCRIPT

BICCS Asia Paper Vol. 5 (6) 1

Filip De Beule and Daniël Van Den Bulcke

The Global Crisis, Foreign Direct

Investment and China The global crisis, foreign direct investment and China 2

Executive summary - Inevitably the financial and economic crisis which swamped the world economy in 2008 had repercussions on foreign direct investment (FDI) that had become the major driver of the globalization process. UNCTAD has shown that in 2008 the negative impact on the FDI flows was concentrated in the developed countries and concluded from this evolution that the worldwide FDI landscape was being redrawn in favor of the developing countries, especially because of the upsurge of outward FDI from the so-called emerging markets. According to UNCTAD the resilience of these latter economies – especially of China - in general and in terms of FDI would allow them to recover more quickly from the decline than the developed countries. The Chinese stimulus program to get the country through the global crisis was much criticized by western experts, because it was thought to extend the Chinese development model which is strongly based on exports and investments in infrastructure and favors state-owned enterprises. Yet, during the global financial and economic crisis China succeeded to remain a much favored location for inward FDI compared to other destinations of FDI and already registered an early rebound of the incoming flows at the end of 2009. Also despite the crisis China’s outbound FDI continued to expand, not only to get hold of scarce resources in mineral rich countries, but even more so for market seeking reasons in developed countries. Critics have complained that the global crisis allowed the government to strengthen its control over the Chinese economy, which might reduce the space and scope of future economic reforms and consequently make the country less attractive to foreign owned firms. On the other hand, the stimulus program has created new opportunities to lower the regional disparities within China as more foreign investors seem to be moving into the inland provinces. The increased influence of the Chinese government is evident in the outbound FDI, mainly through its incentive measures and the FDI initiatives by its sovereign wealth funds. The financial and economic crisis and its impact on inward and outward FDI therefore clearly strengthened China’s clout as a global player in the world economy. Filip De Beule is Assistant Professor of international business at the Lessius University College. Daniël Van Den Bulcke is Emeritus Professor of the University of Antwerp and Academic Director of the Euro-China Centre-UAMS (University of Antwerp Management School).

BICCS Asia Paper Vol. 5 (6) 3

The Global Crisis, Foreign Direct Investment and China: Developments and Implications

Filip De Beule and Daniël Van Den Bulcke

Abstract. This paper focuses on the implications of the global crisis on foreign direct investment (FDI) flows. It looks more in detail at the impact that the crisis has had on China and its inward and outward flows of FDI. The paper specifically analyzes the consequences of the increased state intervention as a response to the global crisis. The paper also looks into China’s Sovereign Wealth Fund as a new player in the global investment arena. The paper ends by drawing some concluding remarks. Keywords. Foreign direct investment, Global economic crisis, Sovereign Wealth Funds.

1. FDI and the global crisis

The main message delivered by UNCTAD in its World Investment Report 20091 was that during 2008 the global flows of foreign direct investment (FDI) had been severely affected by the financial and economic crisis and that these developments had also changed the FDI landscape because of the increasing share that was taken up by the developing countries and emerging markets. The same report stated that the global crisis had an effect on the components (equity capital, reinvested earnings and intra-company loans) and the modes (greenfield investments and mergers and acquisitions) in which FDI was conducted. Also the global recession had repercussions on the activities of private equity funds and the so-called Sovereign Wealth Funds (SWFs) which had ventured into FDI territory. According to the same source the crisis had also an adverse impact on the current and future investments of the multinational enterprises (MNEs) and consequently would affect the growth prospects of both the countries of destination (or host countries) and the countries of origin (or home countries). Policy changes by the host and home countries about international trade and investment to cope with the crisis and protect their own economy from the onslaught of the crisis might result in ‘beggar thy neighbor policies’, including investment protectionism and unfair incentives to attract or retain investments2, that would have a negative influence on the world economy.

The global crisis, foreign direct investment and China 4

In 2007 the global FDI flows had reached a historic peak that even surpassed the earlier record level of 2000. However, between 2007 and 2008 there was a decline in the worldwide FDI flows of 14 per cent. While the developed countries suffered a fall in FDI of 29 per cent in this period, the developing countries and the transition economies respectively registered an increase of 37 and 17 per cent. In fact the developing continents and regions all benefited from an expansion of FDI in 2008, with rises in Africa (+27 per cent), South, East and South-East (+17 per cent), West Asia (+ 16 per cent), and Latin America (+13 per cent). Even the most often neglected least developing countries received US$ 33 billion more of FDI in 2008 than in 2007.

The 2008 fall in FDI in the developed countries was the result of several factors, which themselves were caused by the crisis, such as diminishing corporate profits, plummeting stock prices, less demand for goods and services and reduced capacity to finance because of the more expensive credit conditions. And because most of the FDI flows take place among the developed countries, the upshot in the developing and transition economies was insufficient to compensate this fall. Also the investment links among developed countries and the global economy are more intensive than for most of the less advanced countries. Besides, most of the FDI in the group of developed countries occurs via mergers and acquisitions (M&As) and this latter mode of investment abroad suffered most from the crisis. Compared to 2007 the M&A deals dropped with 21 per cent in number and 31 per cent in value3 . The leveraged buy-outs dried up and the number of megadeals in the take-over business dropped from 274 in 2007 to 203 in 2008. Greenfield investments also experienced difficulties from the last quarter of 2008 onwards which resulted not only in a postponement of new investments or expansions but even led to disinvestments. The number of examples, as listed by UNCTAD4, of scaled down investment projects or decisions to scrap the subsidiary altogether provide an indication of these developments.

The claim by UNCTAD that the FDI landscape is being redrawn in favour of the developing world because of the crisis is based on the comparison of the share of the three groups of countries between 1999-2001 and 2007-2008. During the first period the developed countries represented more than three quarters (78 per cent) compared to less than two thirds (63 per cent) in the second period. The share of the developing countries went up from about one fifth (21 per cent) to almost one third (31 per cent) between these two periods. The relative expansion of the transition economies was spectacular as it increased from 1 to 6 per cent, even though the total volume was still low. An important reason for this success of the

BICCS Asia Paper Vol. 5 (6) 5

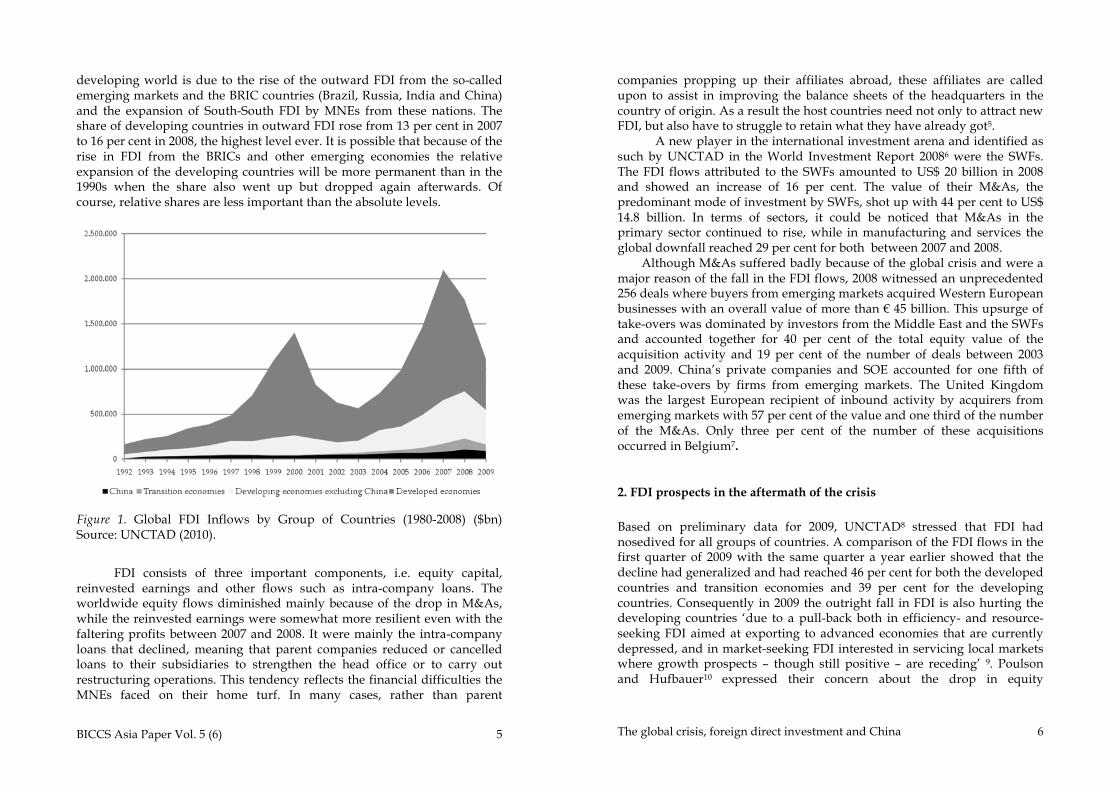

developing world is due to the rise of the outward FDI from the so-called emerging markets and the BRIC countries (Brazil, Russia, India and China) and the expansion of South-South FDI by MNEs from these nations. The share of developing countries in outward FDI rose from 13 per cent in 2007 to 16 per cent in 2008, the highest level ever. It is possible that because of the rise in FDI from the BRICs and other emerging economies the relative expansion of the developing countries will be more permanent than in the 1990s when the share also went up but dropped again afterwards. Of course, relative shares are less important than the absolute levels.

Figure 1. Global FDI Inflows by Group of Countries (1980-2008) ($bn) Source: UNCTAD (2010).

FDI consists of three important components, i.e. equity capital,

reinvested earnings and other flows such as intra-company loans. The worldwide equity flows diminished mainly because of the drop in M&As, while the reinvested earnings were somewhat more resilient even with the faltering profits between 2007 and 2008. It were mainly the intra-company loans that declined, meaning that parent companies reduced or cancelled loans to their subsidiaries to strengthen the head office or to carry out restructuring operations. This tendency reflects the financial difficulties the MNEs faced on their home turf. In many cases, rather than parent

The global crisis, foreign direct investment and China 6

companies propping up their affiliates abroad, these affiliates are called upon to assist in improving the balance sheets of the headquarters in the country of origin. As a result the host countries need not only to attract new FDI, but also have to struggle to retain what they have already got5.

A new player in the international investment arena and identified as such by UNCTAD in the World Investment Report 20086 were the SWFs. The FDI flows attributed to the SWFs amounted to US$ 20 billion in 2008 and showed an increase of 16 per cent. The value of their M&As, the predominant mode of investment by SWFs, shot up with 44 per cent to US$ 14.8 billion. In terms of sectors, it could be noticed that M&As in the primary sector continued to rise, while in manufacturing and services the global downfall reached 29 per cent for both between 2007 and 2008.

Although M&As suffered badly because of the global crisis and were a major reason of the fall in the FDI flows, 2008 witnessed an unprecedented 256 deals where buyers from emerging markets acquired Western European businesses with an overall value of more than 45 billion. This upsurge of take-overs was dominated by investors from the Middle East and the SWFs and accounted together for 40 per cent of the total equity value of the acquisition activity and 19 per cent of the number of deals between 2003 and 2009. China’s private companies and SOE accounted for one fifth of these take-overs by firms from emerging markets. The United Kingdom was the largest European recipient of inbound activity by acquirers from emerging markets with 57 per cent of the value and one third of the number of the M&As. Only three per cent of the number of these acquisitions occurred in Belgium7.

2. FDI prospects in the aftermath of the crisis

Based on preliminary data for 2009, UNCTAD8 stressed that FDI had nosedived for all groups of countries. A comparison of the FDI flows in the first quarter of 2009 with the same quarter a year earlier showed that the decline had generalized and had reached 46 per cent for both the developed countries and transition economies and 39 per cent for the developing countries. Consequently in 2009 the outright fall in FDI is also hurting the developing countries ‘due to a pull-back both in efficiency- and resource-seeking FDI aimed at exporting to advanced economies that are currently depressed, and in market-seeking FDI interested in servicing local markets where growth prospects – though still positive – are receding’ 9. Poulson and Hufbauer10 expressed their concern about the drop in equity

BICCS Asia Paper Vol. 5 (6) 7

investment, normally the most stable part of FDI, during the first quarter of 2009, as it was much larger than in previous crises.

Based on a report of the Economist Intelligence Unit (EIU), Kekic11 concluded from data for 54 countries, that global FDI inflows contracted by 49 per cent during the first half of 2009 compared with the same period in 2008. The cut in FDI was significantly deeper for the developed countries than the developing countries, including the emerging markets and amounted to 54 and 40 per cent, respectively. China, the main emerging market FDI recipient, registered a decline of only 18 per cent compared to 25 per cent for Brazil. Given the discouraging evolution of the cross-border M&As, which took place in the first nine months of 2009, few changes were expected in the global flows for the whole of 2009. Kekic12 even assumes that the FDI landscape will continue to change and that the developing countries and emerging markets are likely to attract more foreign direct investors than the developed world. He posited that, even though the share of the developing countries would not reach the 50 per cent level, their 2009 proportion will almost certainly be the highest on record. Even if the top FDI countries China and India are taken out of the equation the developing and emerging economies should outperform the developed countries. A study carried out by EIU on behalf of UKTI13 also implied that during the next five years the emerging markets will continue to attract more FDI than the developed countries and that this shift in the distribution of the host countries of FDI would become confirmed.

While UNCTAD14 feared that the crisis might result in a lasting downfall of FDI and that the ensuing uncertainty might prolong this trend in the following years, this pessimistic view was rejected because at the same time a number of positive developments were advanced that were likely to relaunch FDI. First, it is stressed that especially the BRICs remain favored locations for the MNE because of their long term growth prospects. Second, it is mentioned that in difficult times the restructuring activities of MNEs might provide new opportunities for companies in emerging economies to buy assets at bargain prices. Third, many companies still feel the need to speed up their internationalization because of pressure in their domestic markets or to better confront their international competitors. Fourth, the SWF, that recently acquired a taste for direct investment, are likely to resume such investments in order to diversify their assets even more. Fifth, the downfall in the flows of FDI has not engulfed all economic sectors or subsectors to the same extent. In fact there are numerous branches, e.g. in life sciences, in transport equipment, in business and personal services, in environmental conservation and in information and

The global crisis, foreign direct investment and China 8

communication technologies that remain promising and offer positive medium-term prospects. How long it will take before the positive factors will offset the negative FDI trend is difficult to estimate, however. Meanwhile FDI will remain a major external source of financing for many developing countries compared to the more volatile portfolio investments and even the slowly moving official development aid (ODA). The high reliance on the more stable forms of private net capital flows, i.e. more in particular FDI, was seen by Goldstein and Xie15 as one of the major reasons why emerging Asia, compared to emerging Europe, had a clear advantage in the run-up to the crisis.

3. The impact of the crisis on FDI and the investment plans of MNEs

In its attempt to evaluate the impact of the financial and economic crisis on worldwide FDI during 2009-2011, three scenarios were distinguished by UNCTAD16, which based on different assumptions were respectively called ‘baseline’ and ‘lower’ and ‘higher limit’. The so-called V or optimistic scenario envisaged a quick upturn that would already be felt at the end of 2009. It is clear that this overly optimistic view – also labeled as such by UNCTAD - was not realized. Even though the protectionist reactions of the countries until now were less restrictive than anticipated, the confidence of the investors has not yet sufficiently returned. The U scenario, also called the base case, assumed that FDI flows will only resume in 2011, because the recession will last longer, the M&A deals will remain relatively low and the internationalization drive of the companies will slowdown. The L scenario is based on pessimistic hypotheses and implies that the crisis is more severe than expected and that the MNEs remain extremely cautious about future investments because of the anticipated risks and the financing difficulties.

‘While FDI prospects are considered favorable in selected industries and markets, cheap asset prices has led to profitable investment opportunities, new countries and types of investors are becoming sources of outward investments, and domestic and international investment regimes remain largely open, this is not enough’ write Poulson and Hufbauer 17. They are inclined to expect that even in 2011 FDI will remain sluggish and that a return to the record level of 2007 of almost US$ 2 trillion is unlikely to be reached by 2013, meaning that the recovery will only occur from 2014 onwards. The survey by UNCTAD18 in its World Investment Prospects for 2009-2011 showed that almost four out of five responding MNEs mentioned that the ‘financial crisis and credit crunch’ had a negative effect on their investment plans, meaning that only one out of five evaluated this in

BICCS Asia Paper Vol. 5 (6) 9

positive terms. Also about one out of five described the crisis impact as ‘very negative’. The appreciation of the ‘global economic downturn’ was more severe as almost two out of five surveyed firms classified the effect as ‘very negative’, while an almost similar proportion was only slightly less pessimistic and used the adjective ‘negative’.

Figure 2. UNCTAD estimate of worldwide FDI inflows under three scenarios

(1990-2012) ($bn). Source: UNCTAD (2010) op.cit.

4. Policy implications at the global level

Already before the financial and economic crisis became a reality, there were some indications that the proportion of restrictive measures with regard to FDI were going up. UNCTAD has kept track of the policy changes that occur in the foreign investment regime since many years. During the 1990s and early years of the new millennium the liberalizing measures largely surpassed the restricting ones. Yet according to UNCTAD19, in 2007 and 2008 the proportion of the restrictions in the FDI regime went up to one out of four compared to only one out of ten in 2003. A number of these new restrictive regulations were directed at new players such as the SWFs, however. The calculation of the impact of policy liberalization in fostering FDI expansion is rather murky according to a study by Adler and Hufbauer20 who tried to estimate this role on the basis of data for the US.

The global crisis, foreign direct investment and China 10

Figure 3. National policy changes towards FDI. Source: UNCTAD (2009e) op.cit.

As the mandated focal point within the United Nations for all

matters related to FDI and development, UNCTAD was asked by the Group of Twenty (G-20) to collaborate with other organizations to investigate the measures in the area of investment taken by these countries to mitigate the adverse impact of the global financial and economic crisis21. The overall purpose of this exercise was to find out if the measures that were taken did not impact negatively on international investment and trade. It was found that between October 2008 and mid June of 2009, 167 measures had been taken by the 42 countries that were surveyed. Forty (or one fourth) were measures that specifically addressed FDI, while 127 (three quarters) consisted of measures that were part of the general framework for the operations of foreign affiliates22. The overall findings of this report were rather positive as most measures did not discriminate between local and foreign enterprises and few of these measures were strongly restrictive. In fact, the report concluded that a substantial number of the policy changes were directed at facilitating FDI or created more clarity and stability about the FDI framework. A number of the G-20 countries even encouraged their companies to venture abroad, thereby stimulating outward FDI.

BICCS Asia Paper Vol. 5 (6) 11

However, the UNCTAD report23 also cautioned about the possibility that some countries might engage in ‘smart’ protectionism and that the stimulus packages might put foreign investors at a disadvantage because of distortive effects. Even in the aftermath of the crisis the possibility of protectionist measures might be extended to less affected sectors and result in retaliation by the countries that would suffer from such policies. This caveat is followed by a warning from UNCTAD that once the crisis is over and privatization would resume, a new wave of economic nationalism might come about to protect ‘national champions’ from foreign take-overs. Therefore it is suggested to continue the monitoring and reporting of policy measures that affect FDI.

In a survey by UKTI24 it was reported that the respondents expressed caution about the prospects of emerging markets over the next two years, but almost three fifths expected to derive more than 20 per cent of their total revenues in emerging markets in the next five years. Two thirds of the sampled companies answered that the main reason for their company investing in emerging markets were the opportunities for rapid market growth, compared to one third which referred to the lower cost base in these markets and about one quarter stressed the competitive pressures in their home markets. When asked about the emerging market countries beyond the BRICs that they might enter in the next five years, Vietnam is quoted by almost two out of five of the respondents, compared to about one quarter (26 per cent) for the United Arab Emirates and one fifth (21 per cent) for Mexico that were ranked in second and third place.

5. China’s IFDI and impact of the crisis

China has been one of the most successful countries in attracting foreign direct investment since the 1990s. Inward foreign direct investment (IFDI) has grown steadily over the last 20 years from the rather low levels in the 1980s to almost $ 100 billion annually in the latter years. Most of this IFDI has however been invested by overseas Chinese, for instance, from Hong Kong and Taiwan, while triad investment in China has been far less. Most of the investment was also oriented towards export processing, while market liberalization has been much slower. Although much progress has been made, especially since China’s access to WTO, market access for foreign firms is still not a level playing field as compared to domestic firms. Yet, with private consumption at $890 billion in 2007, China is the world's fifth-largest consumer market, behind the United States, Japan, the United

The global crisis, foreign direct investment and China 12

Kingdom, and Germany (which China recently surpassed as the world's third-largest economy).

China was listed third by UNCTAD25 in the ranking of the top recipients of FDI flows in 2008, behind the US and France. If the seventh ranked Hong Kong would be added to mainland China, together they would occupy the second position and leave the other BRICs even further behind. Yet, in the latest UNCTAD survey26 about investment intentions China ranked first in the list of favoured locations for future investment abroad. Almost 60 per cent of the surveyed companies placed China at the top of the most attractive economies for the location of FDI, ahead of the US and the three other BRIC countries, i.e. India, Brazil and the Russian Federation. The UNCTAD report stated that: ’In other words companies’ interests in developing and transition economies, albeit growing, remain focused on a relatively limited number of countries. According to this study the location assets of China are to be found in its promising market growth, its market size and its cheap labor’

China also occupied the top position as favored location in several surveys that were conducted by consulting firms. Already in 2008 the UKTI study27 carried out by the EIU, to check the attractiveness of ‘tomorrow’s markets’ put China in the leading position as a priority for future expansion with 49 per cent of the surveyed companies, ahead of India, Brazil and Russia with respectively 42, 33 and 29 per cent of the favorable ‘votes’. IBM’s 2009 ‘Global Location Trends’28, noted that with the financial crisis developing into a fully fledged economic recession during the course of 2008, global investment activity continued its downward trend with an overall reduction of the number of created jobs to 800 thousand, compared with 1.1 million in 2007. In the top ranking of the destination countries by the number of jobs created the top three positions were occupied by India,

the US and China. The UK and Russia came in fourth and fifth place. However, in the manufacturing sector China confirmed its first place from 2007 and was listed ahead of the US, Russia, Mexico and India. In services, India was ranked first, while China registered a serious absolute and

relative decline and dropped from fourth position in 2007 to the eighth place in 2008. In jobs created in R&D activities China moved from the third to the second spot, with less than half of the employment provided by highest ranked India with almost 40,000 research jobs in foreign owned enterprises.

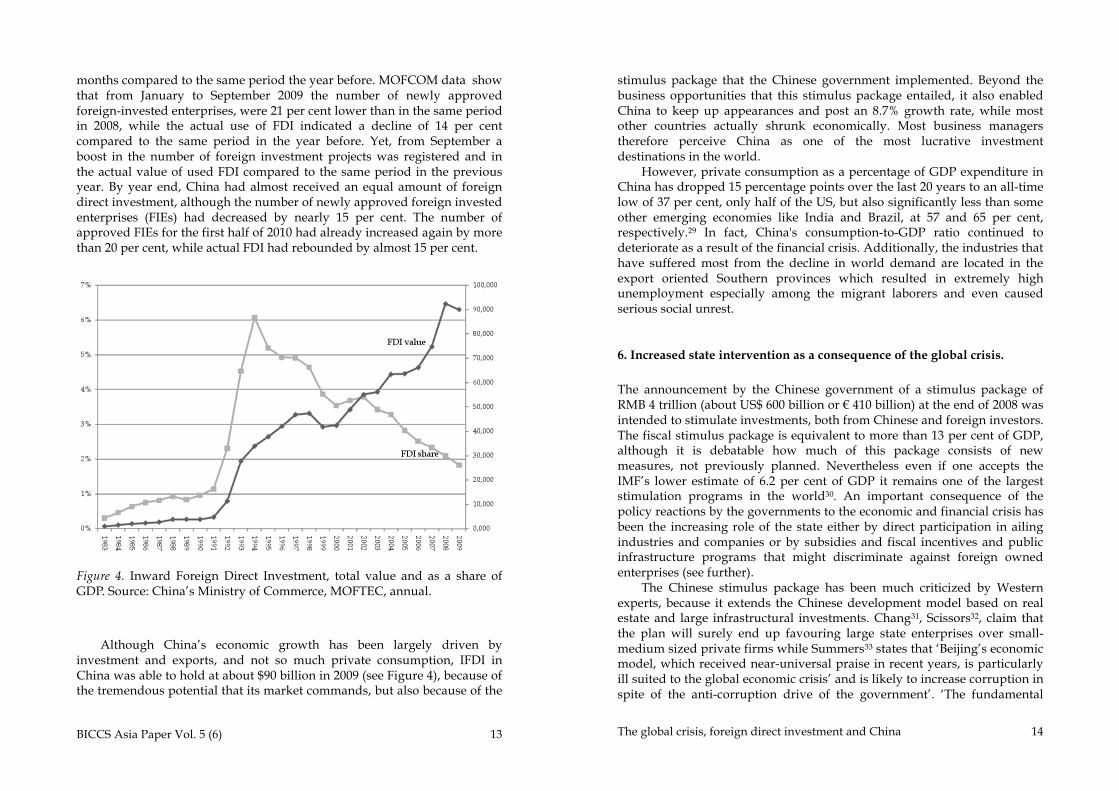

Initially the dramatic decline of FDI in 2009 also counted China under its victims as the inward flow declined with 26 per cent in the first two

China's consumption-to-GDP ratio continued

to deteriorate as a result of the financial crisis.

BICCS Asia Paper Vol. 5 (6) 13

months compared to the same period the year before. MOFCOM data show that from January to September 2009 the number of newly approved foreign-invested enterprises, were 21 per cent lower than in the same period in 2008, while the actual use of FDI indicated a decline of 14 per cent compared to the same period in the year before. Yet, from September a boost in the number of foreign investment projects was registered and in the actual value of used FDI compared to the same period in the previous year. By year end, China had almost received an equal amount of foreign direct investment, although the number of newly approved foreign invested enterprises (FIEs) had decreased by nearly 15 per cent. The number of approved FIEs for the first half of 2010 had already increased again by more than 20 per cent, while actual FDI had rebounded by almost 15 per cent.

Figure 4. Inward Foreign Direct Investment, total value and as a share of GDP. Source: China’s Ministry of Commerce, MOFTEC, annual.

Although China’s economic growth has been largely driven by

investment and exports, and not so much private consumption, IFDI in China was able to hold at about $90 billion in 2009 (see Figure 4), because of the tremendous potential that its market commands, but also because of the

The global crisis, foreign direct investment and China 14

stimulus package that the Chinese government implemented. Beyond the business opportunities that this stimulus package entailed, it also enabled China to keep up appearances and post an 8.7% growth rate, while most other countries actually shrunk economically. Most business managers therefore perceive China as one of the most lucrative investment destinations in the world.

However, private consumption as a percentage of GDP expenditure in China has dropped 15 percentage points over the last 20 years to an all-time low of 37 per cent, only half of the US, but also significantly less than some other emerging economies like India and Brazil, at 57 and 65 per cent, respectively.29 In fact, China's consumption-to-GDP ratio continued to deteriorate as a result of the financial crisis. Additionally, the industries that have suffered most from the decline in world demand are located in the export oriented Southern provinces which resulted in extremely high unemployment especially among the migrant laborers and even caused serious social unrest.

6. Increased state intervention as a consequence of the global crisis.

The announcement by the Chinese government of a stimulus package of RMB 4 trillion (about US$ 600 billion or 410 billion) at the end of 2008 was intended to stimulate investments, both from Chinese and foreign investors. The fiscal stimulus package is equivalent to more than 13 per cent of GDP, although it is debatable how much of this package consists of new measures, not previously planned. Nevertheless even if one accepts the IMF’s lower estimate of 6.2 per cent of GDP it remains one of the largest stimulation programs in the world30. An important consequence of the policy reactions by the governments to the economic and financial crisis has been the increasing role of the state either by direct participation in ailing industries and companies or by subsidies and fiscal incentives and public infrastructure programs that might discriminate against foreign owned enterprises (see further).

The Chinese stimulus package has been much criticized by Western experts, because it extends the Chinese development model based on real estate and large infrastructural investments. Chang31, Scissors32, claim that the plan will surely end up favouring large state enterprises over small-medium sized private firms while Summers33 states that ‘Beijing’s economic model, which received near-universal praise in recent years, is particularly ill suited to the global economic crisis’ and is likely to increase corruption in spite of the anti-corruption drive of the government’. ‘The fundamental

BICCS Asia Paper Vol. 5 (6) 15

causes of depressed consumption rates are systemic – hardwired in a development model that values investment over household income – rather than unique consumer preferences rooted in culture’34. To create a sustainable growth model an increase in consumption and development of the service industries is urged by de Jonquières35. A more consumer-centric economy would generate more jobs, allocate capital and resources more efficiently, spread the benefits of growth more equitably, and also enrich the global economy with a substantial increase in net consumption.

Because the effects of the economic crisis struck China later than most other countries and apparently were less severe, some analysts described the country as ‘the only green shoot’36 , ‘the leader’37 or ‘the gold standard’38 and some even thought that China might ‘save the world’39. The McKinsey report 40acknowledged that no likelier than others the Chinese executives do not yet see an upturn, but that they are particularly hopeful about the prospects of their own country as 82 per cent expected the Chinese GDP to increase in 2009 and 30 per cent thought that GDP would regain its pre-crisis level as soon as 2010. With respect to China, the measures taken since the crisis about FDI, i.e. between January and August 2009, are regarded as mostly positive by Poulson and Hufbauer41, i.e. :

. the streamlining of the FDI review process;

. the easing of restrictions on the provision of financial information services by foreign institutions;

. the authorization for two foreign banks to issue Yuan bonds in China;

. the simplification of the approval processes for OFDI;

. the allowance for Chinese companies to lend up to 30 per cent of their equity to their overseas subsidiaries;

. the banned foreign investment in express postal services;

. the restrictive conditions on the Mitsubishi acquisition.

Bremmer42 stated that over the past several years ‘an era of state capitalism has dawned, one in which the governments are again directing huge flows of capital with profound implications for free markets and international politics’. He assumes that given the vast sums its government is spending via its stimulating program, China will emerge from the global recession before most of the developed world. At the same time ‘this will further persuade the Chinese leadership that state control of much of the country’s economic development is the most reliable path toward prosperity – and, therefore, domestic tranquility’43.

Even though most experts are convinced that China’s policy measures will succeed in stimulating short-term economic growth, there are serious

The global crisis, foreign direct investment and China 16

doubts if it will be sufficient to ensure sustainable economic growth. The program might even entail new risks according to Zhang44 . First, most Western experts are convinced that China’s growth model is too much dependant on export-driven growth and that household consumption should be increased in order to expand domestic demand. Another objection is that too many resources are directed to infrastructure which will result in overinvestment and excess capacity in certain areas, while property investments will cause price bubbles in the major cities and Southern provinces. In addition, the surge in bank loans to state owned enterprises (SOE) which still benefit from a monopoly position and other advantages, risks to recreate the problem of so-called ‘non-performing loans’ (NPLs). While solving the problem of the undervalued exchange rate of the Renminbi would help to lower China’s export dependence, the opinions about the necessity of such a change in the exchange rate is strongly debated among financial experts and government officials.

The global crisis has strengthened the role of the state in the Chinese economy. This is likely to reduce the pace and scope of any future economic reforms which might increase the influence of state-owned enterprises45. The political clout of the SOE will be enhanced through the government’s policy during the crisis, because the strategic national sectors and companies will receive continued and increased protection. Foreign MNEs also feared that they would be discriminated against and would not be allowed to fully participate in the construction programs of the stimulus package. Ma and Summers46 argue that Beijing’s response to the crisis, including the sizable stimulus program, has created opportunities to rebalance the country’s regional disparities between the poor rural western provinces and the richer coastal provinces. The ‘go west’ policy announced in 1999 and launched in 2000 is receiving a renewed impetus under the omnibus crisis program, also by becoming more attractive to FDI. Although the gap between the eastern and western parts of China remains quite wide, since 2007 the growth rates of the west have overtaken the eastern region. Whereas the eastern provinces attract major inflows of FDI as part of global supply chain management, or for manufacturing or assembly for export markets, such projects are less suited for the western part of the country largely for geographic reasons leading to higher costs of transportation. ‘However, as foreign enterprises increasingly focus their investment on serving the

The global crisis has strengthened the role of the

state in the Chinese economy. This is likely to reduce the pace and scope of any future economic

reforms which might increase the influence of state-owned enterprises.

BICCS Asia Paper Vol. 5 (6) 17

domestic Chinese market, this pattern of FDI may begin to change’47. Rather than being integrated in the global supply chain activities, the western region is likely to develop more intense linkages with central Asia. China also needs to dismantle its internal obstacles to trade within China which result from all kinds of local restrictions to keep out goods from other parts of the country48 .

7. China’s outward direct foreign investment

During a first, mainly experimental, stage that lasted more or less to the end of the 1990s, China’s OFDI was strongly supervised by the government. A second stage, situated in the 1990s witnessed an important increase in the number of Chinese subsidiaries abroad but was also characterized by the lack of strategic vision of most of these state-owned enterprises49. The third stage started with China’s accession to the World Trade Organization (WTO) in 2001, when some leading Chinese firms went multinational with the intention to become global players in the international markets50. From then on it looked like Chinese firms had come of age, as they demonstrated spectacular progress over the previous stages. It is also after the beginning of the millennium that the Chinese government switched to a policy of stimulating the outbound ventures of its companies51. According to some analysts there are even indications that China’s OFDI might be underestimated52. China’s global footprint is larger than the Indian one, both in number of affiliates and countries, as there were more than 5000 Chinese MNEs owning about 10,000 foreign affiliates located in 172 countries53 .

Although outward investment has traditionally been opposed in home countries as substituting for exports and reducing domestic capital investment and causing losses of jobs, it has been defended as necessary for the growth and prosperity of home-based firms in the contest for worldwide markets and the competitiveness of firms from the countries of origin. For all intents and purposes, China does not seem to share these concerns. Previous research has been inconclusive as regards the effect of outward foreign direct investment on domestic investments. Some studies concluded that a positive relationship exists between investment at home and abroad.54 Other studies have shown a negative relationship between FDI and home-country investment.55 The latter studies argue that the firm’s capital constraints would mean that an outward foreign direct investment crowded out domestic investment. Braunerhjelm et al. found that a complementary relationship can be expected to come through in vertically

The global crisis, foreign direct investment and China 18

integrated industries, whereas a substitution relationship can be expected in horizontally organized production.56 The empirical analysis confirmed a significant difference between these two categories of industry with regard to the impact of OFDI on domestic investment for Sweden. China, however, has a tremendous savings glut, making it impossible to invest all these funds efficiently in the domestic market. Furthermore, most of China’s investments are not horizontal but vertical upstream or downstream investments. Therefore, China does not suffer from a crowding out effect of domestic investment, while, on average, OFDI projects are more likely more efficient applications of available funds.

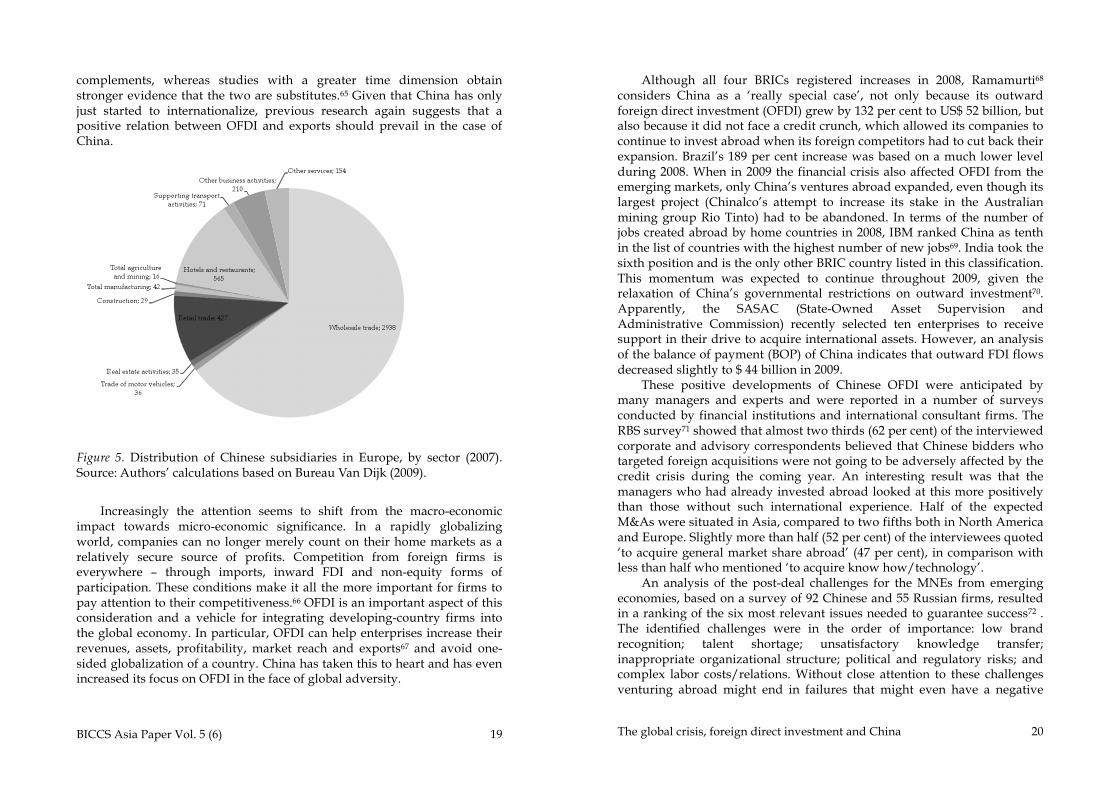

Studies about the home-country employment effect have also obtained mixed results. A first group of studies on the employment effect of FDI found a substitution effect between a foreign subsidiary’s activity and its parent’s employment.57 Several studies have concluded that substitution occurs between countries with comparable factor endowments.58 Other studies have shown that U.S. multinationals using the resource-seeking FDI model appear to reduce employment at home, relative to production, by allocating labor-intensive stages of their production to their affiliates in developing countries.59 Konings and Murphy60 also concluded that labor substitution is more likely to take place when factor proportions are different in various locations and vertical FDI dominates. Although Chinese investments can also be characterized as either market-seeking or resource-seeking, the Chinese are more interested in upstream raw material resource projects and downstream trade enhancing market projects, while maintaining the labor-intensive production processes in their home country. An analysis of the Chinese affiliates in Europe in terms of sectors shows that CMNEs clearly prefer the service sector, and more in particular trading services (see Figure 5). The employment effect is most likely a positive one, with increased export markets, for instance, in Europe.

The existing empirical evidence on the impact of outward investment on exports is similarly mixed. Some research, especially using cross-sectional data, typically concluded that FDI had a complementary net effect on domestic exports.61 Some studies find a significant negative impact on home country exports.62 Svensson63, for instance, obtains evidence of a substitution effect using Swedish data, with exports to third parties from the foreign affiliates of Swedish companies being at the expense of exports from the parent firm. Other studies suggest that the time series relationship between outward investment and exports may vary across countries and across time.64 Any initial stimulus to exports of intermediate goods may fade over time. On balance the evidence from cross-section studies and panel studies with a limited time dimension suggests that the two are

BICCS Asia Paper Vol. 5 (6) 19

complements, whereas studies with a greater time dimension obtain stronger evidence that the two are substitutes.65 Given that China has only just started to internationalize, previous research again suggests that a positive relation between OFDI and exports should prevail in the case of China.

Figure 5. Distribution of Chinese subsidiaries in Europe, by sector (2007). Source: Authors’ calculations based on Bureau Van Dijk (2009).

Increasingly the attention seems to shift from the macro-economic

impact towards micro-economic significance. In a rapidly globalizing world, companies can no longer merely count on their home markets as a relatively secure source of profits. Competition from foreign firms is everywhere – through imports, inward FDI and non-equity forms of participation. These conditions make it all the more important for firms to pay attention to their competitiveness.66 OFDI is an important aspect of this consideration and a vehicle for integrating developing-country firms into the global economy. In particular, OFDI can help enterprises increase their revenues, assets, profitability, market reach and exports67 and avoid one-sided globalization of a country. China has taken this to heart and has even increased its focus on OFDI in the face of global adversity.

The global crisis, foreign direct investment and China 20

Although all four BRICs registered increases in 2008, Ramamurti68 considers China as a ‘really special case’, not only because its outward foreign direct investment (OFDI) grew by 132 per cent to US$ 52 billion, but also because it did not face a credit crunch, which allowed its companies to continue to invest abroad when its foreign competitors had to cut back their expansion. Brazil’s 189 per cent increase was based on a much lower level during 2008. When in 2009 the financial crisis also affected OFDI from the emerging markets, only China’s ventures abroad expanded, even though its largest project (Chinalco’s attempt to increase its stake in the Australian mining group Rio Tinto) had to be abandoned. In terms of the number of jobs created abroad by home countries in 2008, IBM ranked China as tenth in the list of countries with the highest number of new jobs69. India took the sixth position and is the only other BRIC country listed in this classification. This momentum was expected to continue throughout 2009, given the relaxation of China’s governmental restrictions on outward investment70. Apparently, the SASAC (State-Owned Asset Supervision and Administrative Commission) recently selected ten enterprises to receive support in their drive to acquire international assets. However, an analysis of the balance of payment (BOP) of China indicates that outward FDI flows decreased slightly to $ 44 billion in 2009.

These positive developments of Chinese OFDI were anticipated by many managers and experts and were reported in a number of surveys conducted by financial institutions and international consultant firms. The RBS survey71 showed that almost two thirds (62 per cent) of the interviewed corporate and advisory correspondents believed that Chinese bidders who targeted foreign acquisitions were not going to be adversely affected by the credit crisis during the coming year. An interesting result was that the managers who had already invested abroad looked at this more positively than those without such international experience. Half of the expected M&As were situated in Asia, compared to two fifths both in North America and Europe. Slightly more than half (52 per cent) of the interviewees quoted ‘to acquire general market share abroad’ (47 per cent), in comparison with less than half who mentioned ‘to acquire know how/technology’.

An analysis of the post-deal challenges for the MNEs from emerging economies, based on a survey of 92 Chinese and 55 Russian firms, resulted in a ranking of the six most relevant issues needed to guarantee success72 . The identified challenges were in the order of importance: low brand recognition; talent shortage; unsatisfactory knowledge transfer; inappropriate organizational structure; political and regulatory risks; and complex labor costs/relations. Without close attention to these challenges venturing abroad might end in failures that might even have a negative

BICCS Asia Paper Vol. 5 (6) 21

impact on the parent company. The CCPIT 2009 study about the Chinese MNEs in particular73 showed that the most quoted challenge (as measured on a Likert scale from 1 to 5) proved to be the concern of foreign consumers of the quality and safety of Chinese products, the difficulty of raising funds, the inadequate understanding of foreign laws, regulations and risks, the poor recognition of Chinese brands abroad, the lack of management and other professionals and the lack of knowledge of international operations and strategies.

Several studies have shown that the main reason for Chinese companies to invest abroad is based on considerations of market expansion. The CCPIT 74 survey found that for 39 per cent of the Chinese MNEs market growth was the major motive, compared to 30 per cent for the acquisition of advanced technologies and experience, while 24 per cent was based on cost considerations. One fifth each (19 per cent) referred to the development of natural resources and the acquisition of famous international brands. Although the impact of the global recession was already a reality at the time of the CCPIT75 survey, only 4 percent of the sampled companies were convinced that during the next two years it would result in less OFDI, contrary to more than two out of five respondents (43 per cent) who mentioned that it would grow, five percent ‘significantly’ and 38 per cent ‘moderately’. About the same proportion (42 per cent) thought that they would not engage in investment abroad, while 4 per cent anticipated a reduction. In three out of five cases the size of the foreign investment would be higher than one million US dollar. A similar proportion of the firms were likely to direct their investment projects to Asian countries, compared to one fifth to North America and Europe. Strangely enough –at least when one takes their earlier answers into account- more than half (54 per cent) of the responding firms thought that after the financial crisis the outbound FDI from China would be reduced.

The APFC 2009 survey76 was carried out at about the same time as the CCPIT study and came up with rather similar results. About three out of five of the sampled firms that realized investments abroad expected an increase (7 per cent mentioned a substantial rise and 52 per cent a moderate expansion). Fifty seven percent or almost three out of five MNEs planned an investment of more than one million US dollar. To the question about the impact of the global crisis on Chinese OFDI more than half (53 per cent) described it as only minor, although two fifths were of the opinion that the impact was strong. Of the companies with OFDI, 56 per cent thought that the impact of the crisis had been adverse and had resulted in a decline of the outbound initiatives. In 2009 China’s OFDI was concentrated in the

The global crisis, foreign direct investment and China 22

third quarter, during which the accumulated amount of US$ 20.71 billion was 190 per cent higher than in the third quarter of 2008 (MOFCOM).

Both the information that is available until now about Chinese OFDI and the answers of the Chinese and Asian managers as to how they perceived the global recession and how it affected their investment plans, clearly show that there are some basic characteristics that set them apart from most of the other investors in the BRICs and the rest of the world. Pradhan77 is convinced that ‘the extraordinarily rapid growth of Chinese OFDI during the global crisis is (otherwise) not explainable by the usual economic forces ascribed by theories of foreign investment’. He notices that, unlike Indian OFDI which has been primarily led by private enterprises, except a few public sector firms operating in the energy sector, Chinese investment abroad is still dominated by state-owned companies and is largely state driven. China’s ‘go out’ or ‘go global’ policy seems to have succeeded to successfully continue its search for foreign markets, resources, technology and brands.

The losses made by the Chinese SWFs CIC (China Investment Corporation) and CDC (China Development Corporation) in Europe and the US, the failures of a number of M&As such as TCL in Europe and SAIC in Korea and even the political opposition in countries such as the US (CNOOC) and Australia (Chinalco) have not stopped the Chinese OFDI surge. To what extent the influence by the government has been instrumental for the Chinese companies in their multinationalization process is hard to measure. Yet, the satisfaction of the Chinese MNEs about the support they received under the governments ‘go global’ policy was moderate as it received a score of close to 3 on a 1-5 Likert scale in the CCPIT survey78. Both the funding and credit support and the simplification of the outbound investment management procedures received the highest appreciation and were cited by almost two thirds of the interviewed companies (56 per cent). Also two thirds of these firms expected the government ‘to carry out economic and trade activities and build cooperation platforms’.

8. Sovereign Wealth Funds as new players

New players in the international investment arena are the SWFs. After 2005, when the SWFs started to make FDI-style investments, that is, to take equity positions into foreign firms of 10 per cent or more, this resulted in a lot of anxiety in developed, mainly G-7 countries, that resulted in a tightening of the FDI rules.79 Although SWFs are not a totally new phenomenon as half of

BICCS Asia Paper Vol. 5 (6) 23

them existed before 1990, their size and visibility has grown enormously since the last few years, also because of their establishment in countries such as China and their direct investments in developed countries. In the case of China the western politicians and media were very much concerned about the influence of government controlled interventions in their economies via SWFs and the lack of transparency of such operations. Although the Asian SWFs have subscribed to the newly decreed voluntary code of conduct known as the ‘Santiago Principles’ which have been worked out by the OECD and the IMF and these funds seem to be taking them into account, Ramamurti80 is rather pessimistic about the possibilities that they will develop into major FDI players. On the one hand he thinks that the developed countries will remain sceptical about their activities and might use so-called security threats as an excuse to limit their activities. On the other hand SWFs lack the expertise to manage FDI-type investments. Yet, Ramamurti81 admits that Singapore’s ‘Government and Investment Corporation’ (GIC) and Temasek are exceptions and have realized high returns on their investments. He also thinks that China with the CIC might be equally successful in the near future, at least if it would receive sufficient autonomy to run an independent business and would be protected from political meddling. Meanwhile, CIC and the CDC suffered losses of 20 to 60 per cent on their initial investments in western financial institutions such as Blackstone and Barclays, to the extent that even in China they were strongly criticized for squandering China’s exchange reserves. These negative experiences might push the SAFE, CIC and Chinese state financials and corporations away from the financial sector towards assets which range from physical resources such as farmland to equity stakes in business accounting firms82.

9. Concluding remarks

In the early 1980s borrowing from governments and international organizations was the most important capital inflow to China. But since the 1990s these have been overshadowed by FDI. One reason for the predominance of FDI, of course, is that China’s financial markets were virtually closed to portfolio investments. Furthermore, Chinese policy makers displayed a preference for FDI, primarily because it brought technology and commercial expertise as well as capital. Besides, China has maintained restrictions on capital account convertibility. However, an analysis of China’s balance of payments (BOP) indicates that there is considerable fluctuation (see Figure 6.). The balance of trade of goods and

The global crisis, foreign direct investment and China 24

services has been positive and above two per cent of GDP since 1996, but jumped in 2005 before plunging as a result of the global economic crisis. Net FDI flows initially increased but have been declining since 1994. The data indicate that OFDI will sooner rather than later overtake IFDI, as the net position has slowly but surely dropped, especially as a result of the financial crisis. China was able to maintain and even slightly increase its OFDI while IFDI has slipped a bit.

Figure 6. China’s balance of payments, 1985-2009. Source: State Administration of Foreign Exchange. Note: The BOP has been divided into the balance of trade, foreign direct investment and all other capital flows.

But the ‘all other’ component has been huge and highly volatile.

Clearly, these flows of ‘hot money’ are influenced by expectations of devaluation (in the outflow period) or appreciation (in the inflows period). These flows resemble those experienced by the countries of East Asia afflicted by the Asian financial crisis (1997-1998) in their size and instability. Although China was not affected significantly by the Asian crisis with respect to FDI and trade flows, it did have a large decrease in other capital flows due to the uncertainty whether it would depreciate its currency like some other Asian countries did. However, China was able to hold its

BICCS Asia Paper Vol. 5 (6) 25

currency stable (in part as a result of a previous devaluation in 1994), and it actually played a positive role in the recovery of those countries. The remarkable thing is that the capital flows from China look just like those from other countries, notwithstanding the fact that theoretically China has capital controls. Obviously, the capital controls do not work.83 The most powerful argument for China to liberalize its capital account is not that capital account liberalization is necessarily better, but that a legal, regulated open capital account might function better than a hidden black or grey market with de facto openness.84 Besides, it would be more efficient to put a stop to the excessive foreign exchange accumulation and allow a more market-oriented exchange rate of the Chinese Yuan.

Although other capital flows dropped slightly in 2008, they have however increased in 2009 in the assumption that China would appreciate its currency, similar to the inflow of hot money in 2003 and 2004 before China let its currency appreciate from 2005; an appreciation trend, which was quickly interrupted by China’s central bank, as soon as the crisis hit. As a result of increased international pressure by the US, China has decided to slowly appreciate its currency. The decision, however, also fits a change in China’s economic model of cheap labor-intensive export-oriented economy towards a higher value-added consumption-oriented economy.

It is indeed likely that the global recession will also have a permanent effect on the so-called FDI landscape, meaning that the developing countries will acquire a larger share in the global FDI. However, this is mostly due to the rise of the Emerging Markets which have succeeded in luring more foreign investors to their growing markets, while at the same time more and more of their own companies are venturing abroad. Among the BRICs China has certainly shown the most impressive record. Besides, practically all surveys that tried to gauge the prospects for China’s inward and outward direct investment based on the perceptions of international managers and experts confirmed these positive expectations. Contrary to the prospects of an L shaped recovery for worldwide FDI, the indications at the end of 2009 convincingly show that China will achieve a V shaped rebound of its economy and FDI.

Undoubtedly, the Chinese investment climate for foreign enterprises over the years has gradually and systematically improved. For instance, wholly owned subsidiaries are now allowed while earlier on only joint ventures were acceptable; mergers and acquisitions have been authorized while until a few years ago the foreign investor could only enter via a greenfield investment; and the whole of China has become accessible to foreign ventures while at the beginning the activities were restricted to special economic zones or development cities. Yet, there are still surprises

The global crisis, foreign direct investment and China 26

that shake the confidence of foreign firms such as the Rio Tinto spy case, and the problems of companies such as Danone with its former partner and the rejection of Coca Cola’s bid of a major take-over on the basis of the new anti-trust law.

In an article titled ‘A new code of conduct’ the China Daily85 wrote in September 2009 that such cases ‘renew questions about the boundary of the multinational companies’ acceptable commercial behavior in China, and the cost of crossing the line’86. And the article continued by stating: ’Multinational companies that arrived in China in the early stages of its reform and opening are facing a different China now. These companies face a stricter regulatory environment, the phasing out of preferential policies toward foreign investors, a rising number of local consumers who fill online chat rooms with comments and local media that are quick to pick up on foreign firms’ blunders’. While all of these examples elevate the uncertainty factor, it looks like the foreign investor does not worry all that much about these new developments as inward FDI in China has rebounded much faster than expected in the aftermath of the global crisis.

The increased influence of the Chinese government is clearly evident in the outbound investment. This is reflected in the expansion of its SWFs, which are diversifying China’s vast foreign exchange reserves towards FDI and are acquiring higher ownership participations in several projects abroad87. Because of the crisis and the large financial ‘pockets’ of the SWFs certain western countries even became more lenient towards these state controlled investment funds88. The fact that the SWFs took steps to become more transparent and to subscribe to voluntary international regulations such as the ‘Santiago code’ were also instrumental to make them more acceptable. Meanwhile China continues to offer financial and other support to its internationalizing firms and to develop its own ‘global champions’.

BICCS Asia Paper Vol. 5 (6) 27

Notes and references:

1 UNCTAD (2009e) Transnational Corporations, Agricultural Production and Development, World Investment Report 2009, United Nations, New York - Geneva 2 Gurria, A. (2009) The crisis and its impact on cross-border investment? OECD, Speech at the US Council for International Business, Washington, June, 3 pp. 3 UNCTAD (2009e) op.cit. 4 UNCTAD (2009a) Assessing the impact of the current financial and economic crisis on global FDI flows, Geneva, April, p. 25-28 5 Poulson L. and G. Hufbauer (2009) The Great Crisis and Global FDI Flows, Paper, Fourth Columbia International Investment Conference, FDI, the Global Crisis and Sustainable Recovery, Columbia University, New York, November. 6 UNCTAD (2008) Transnational Corporations and the Infrastructure Challenge, World Investment Report 2008, United Nations, New York – Geneva, 294 pp. 7 PriceWaterhouseCoopers (2009a) Going West… Maximising success with Western European vendors, Crossboarder Briefing; Zhang, H. and D. Van Den Bulcke (2007) Attracting Chinese Investors. An Assessment of the Belgian Inward Foreign Direct Investment Promotion Websites from an Investor Perspective, Federation of Belgian Industries – University of Antwerp Management School, 2007, pp.61 8 UNCTAD (2009e) and UNCTAD (2009f) World Investment Prospects Survey 2009-2011, United Nations, New York-Geneva, 71 pp. 9 UNCTAD (2009a) op. cit. p.viii 10 Poulson L; and G. Hufbauer (2009) The Great Crisis and Global FDI Flows, Paper, Fourth Columbia International Investment Conference, FDI, the Global Crisis and Sustainable Recovery, Columbia University, New York, November, 33 pp. 11 Kekic, L. (2009) The global economic crisis and FDI flows to emerging markets, Columbia FDI Perspectives, No 15, Vale Columbia Center on Sustainable International Investment, October, 5 pp. 12 Kekic, L. (2009) op.cit. 13 UKTI (2009) Survive and Prosper: Emerging Markets in the Global Recession, United Kingdom Trade and Investment and Economist Intelligence Unit, London 14 UNCTAD (2009a) op.cit. p. 30-34 15 Goldstein, M. and D. Xie (2009) The impact of the financial crisis on Emerging Asia, Peterson Institute for International Economics, Working Paper Series, October, p. 37 16 UNCTAD (2009a) op. cit. and UNCTAD (2009e) op.cit. 17 Poulson L. and G. Hufbauer (2009) op.cit. 18 UNCTAD (2009f) World Investment Prospects Survey 2009-2011, United Nations, New York-Geneva, 71 pp.

The global crisis, foreign direct investment and China 28

19 UNCTAD (2008) op.cit., UNCTAD (2009a) op.cit.; UNCTAD (2009e) op.cit 20 Adler, M. and C. Hufbauer (2008) Policy liberalization and FDI growth, 1982-2006, Working Paper, Peterson Institute, August 21 UNCTAD (2009c) Investment Policy Developments in G-20 Countries, United Nations, New York-Geneva, 29 pp.; OECD, WHO and UNCTAD (2009) Report on G20 Trade and Investment Measures, September, 60 pp. 22 UNCTAD (2009c) op.cit. 23 Ibidem 24 UKTI (2009) op.cit. 25 UNCTAD (2009e) op. cit. 26 Ibidem p. 54 27 UKTI (2008) op.cit. 28 IBM (2009) Global Location Trends, Annual Report, IBM Corporation, Global Business Services, October, 26 pp. 29 McKinsey (2009b) If you’ve got it, spend it: Unleashing the Chinese consumer, McKinsey Company: McKinsey Global Institute. 30 UNCTAD (2009d) Trade and Development Report, United Nations, New York-Geneva 31 Chang, G (2009) ) China’s Role in the Origin of and Response to the Global Recession, Testimony before the US-China Economic and Security Commission, Washington, February, p. 4--5 32 Scissors, D. (2009c) China refuses to adjust its economy, Web Memo, The Heritage Foundation, July 33 Summers, T. (2009) Chinese Politics in the Global Financial Crisis, Asia Programme Briefing Note, Chatham House, London, 10 pp. 34 Devan J., M. Rowland and J. Woetzel (2009) A consumer paradigm for China, McKinsey Quarterly, August 35 de Jonquières, G. (2009) op.cit. 36 Powell, B. (2009) Can China Save the World? Time Magazine, August 1 37 de Jonquières, G. (2009) China and the global economic crisis, ECIPE, Policy Briefs, No 2, Brussels 38 Lardy, N (2009b) Is China’s Srimulus Program Protectionism? Peterson Perspectives, Peterson Institute for International Economics, June, 4 pp. 39 Powell, B. (2009) op. cit. 40 McKinsey (2009) The crisis-one year on: McKinsey Global Economic Conditions Survey results, McKinsey Quarterly, September 41 Poulson L. and G. Hufbauer (2009) op.cit. 42 Bremmer, I. (2009) State capitalism and the crisis, McKinsey Quarterly, July 43 Ibidem 44 Zhang, M. (2009) The Impact of the Global Crisis on China and its Reaction, ARI, Institute of World Economics and Policies, CASS, Beijing, April, 7 pp. 45 Summers, T. (2009) op. cit.

BICCS Asia Paper Vol. 5 (6) 29

46 Ma, D and T. Summers (2009) Is China’s Growth moving Inland? A Decade of ‘Develop the West’, Chatham House, Asia Programme Paper, October, 14 pp. 47 Ibidem p. 9 48 Cassidy, R. (2009) China’s Role in the Origin of and Response to the Global Recession, Testimony before the US-China Economic and Security Commission, Washington, February 49 Zhang, H and D.Van Den Bulcke (1996) International Management Strategies of Chinese Multinational Firms. Chapter 8 in J. Child and Y.Liu (eds.), Management Issues for China in the 1990s: International Enterprises, London 1996 Routledge, p. 141-164 50 Child, J. and S. Rodrigues (2005) The Internationalization of Chinese Enterprises: A Case for Theoretical Extension? Management and Organization Review, No 3, p. 381-410 51 De Beule, F. and D. Van Den Bulcke (2010) Changing Policy Regimes in Outward Foreign Direct Investment: From Control to Promotion, Chapter 14 in K. Sauvant, W. Maschek and G. MacAllister (eds), Foreign Direct Investment from Emerging Markets. The Challenges Ahead, Palgrave MacMillan, New York 52 De Beule F., D. Van Den Bulcke and H. Zhang (2010) Chinese Outward Direct Investment in Europe and Belgium. Characteristics and Policy Issues, in L. Brennan (ed) The Emergence of Southern Multinationals and their Impact on Europe, Palgrave MacMillan. 53 Pradhan, J. (2009) Emerging Multinationals from India and China: Origin, Impetus and Growth, MPRA Paper, No18210 54 Noorzoy, S. (1980) “Flows of direct investment and their effects on U.S. domestic investment”, Economics Letters, 5, pp. 311–317. 55 Belderbos, Rene. (1992) ‘Large multinational enterprises based in a small economy: effect on domestic investments’, Weltwirtschaftliches Archiv, 128, pp. 543–583. 56 Braunerhjelm, Pontus, Lars Oxelheim, and Per Thulin (2006) ‘The relationship between domestic and outward foreign direct investment: the role of industry-specific effects’, International Business Review, 14 (6), pp. 677–-694. 57 Kravis, I. B. & and R.E. Lipsey (1988) ‘The effects of multinational firms’ foreign operations on their domestic employment’, NBER Working Paper 2760; Brainard, S. Lael and David A. Riker (1997) ‘Are U.S. multinationals exporting U.S. jobs?’, NBER Working Paper No. 5958; Braconier, Henrik and Karolina Ekholm (2001) ‘Foreign direct investment in Central and Eastern Europe: employment effects in the EU’, CEPR Working Paper No. 3052; Cuyvers, Ludo, Michel Dumont, Glenn Rayp, and Katrien Stevens (2005) ‘Home employment effects of EU firms' activities in Central and Eastern European countries’, Open Economies Review, 16 (2), pp. 153–-174; Konings, J. and A. Murphy (2003) ‘Do multinational enterprises relocate employment to low wage regions? Evidence

The global crisis, foreign direct investment and China 30

from European multinationals’, LICOS Centre of Institutions and Economic Performance, Paper No. 131. 58 Hansson, P. (2005) ‘Skill upgrading and production transfer within Swedish multinationals in the 1990s’, Scandinavian Journal of Economics, 107 (4), pp. 673–692; Slaughter, M. (2000) ‘Production transfer within multinational enterprises and American wages’, Journal of International Economics, 50, pp. 449–72. 59 Blomström, Magnus, Gunnar Fors, and Robert E. Lipsey (1997) ‘Foreign direct investment and employment: home country experience in the United States and Sweden’, Economic Journal, 107, pp. 1987–-1997; Brainard, S. Lael and David A. Riker (1997) ‘Are U.S. multinationals exporting U.S. jobs?’, NBER Working Paper No. 5958; Slaughter, M. (2000) ‘Production transfer within multinational enterprises and American wages’, Journal of International Economics, 50, pp. 449–-472. 60 Konings, J. and A. Murphy (2003) ‘Do multinational enterprises relocate employment to low wage regions? Evidence from European multinationals’, LICOS Centre of Institutions and Economic Performance, Paper No. 131. 61 Lipsey, R.E. and M.Y. Weiss (1984) ’Foreign production and exports of individual firms’, Review of Economics and Statistics, 66, pp. 304–-8; Head, Keith and John Ries (2001) ‘Overseas investment and firm exports’, Review of International Economics, 9 (1), pp. 108–-122. 62 Horst, Thomas (1972). “The industrial composition of U.S. exports and subsidiary sales to the Canadian market,” The American Economic Review, 62 (1), pp. 37–-45; Pain, Nigel and Katharine Wakelin (1997) ‘Export performance and the role of foreign direct investment’, Discussion Paper 131, National Institute of Economic and Social Research, http://www.niesr.ac.uk/pubs/dps/dp131.pdf; Blonigen , Bruce (2001) ‘In search of substitution between foreign production and exports’, Journal of International Economics, 53 (1), pp. 81–-104. 63 Svensson, R. (1996) “Effects of overseas production on home country exports: Evidence based on Swedish multinationals”, Weltwirtschaftliches Archiv, 132, pp. 304–-329. 64 Johnson, Andreas (2006) “FDI and exports: The case of the high performing East Asian Economies,” Working Paper Series in Economics and Institutions of Innovation, 57, Royal Institute of Technology, CESIS– Centre of Excellence for Science and Innovation Studies. 65 Pain and Wakelin (1997) op cit. 66 Sauvant, Karl. P. (2005) ‘New sources of FDI: the BRICs: outward FDI from Brazil, Russia, India, and China’, Journal of World Investment and Trade, 6 (5), pp. 639–709. 67 UNCTAD (2009) op cit.

BICCS Asia Paper Vol. 5 (6) 31

68 Ramamurti, R. (2009) Impact of the Crisis on New FDI Players, Paper, Fourth Columbia International Investment Conference, FDI, the Global Crisis and Sustainable Recovery, Columbia University, New York, November 69 IBM (2009) op.cit. 70 Skolkovo (2009a) Global Expansion of Emerging Multinationals: Post Crisis Adjustment, SIEMS Monthly Briefing, Skolkovo Research, May, 23 pp. 71 RBS (2009) Reaching Beyond the Great Wall, Royal Bank of Scotland, February 72 Skolkovo (2009) Operational Challenges Facing Emerging Multinationals from Russia and China, SIEMS Monthly Briefing, Skolkovo Research, June 73 CCPIT (2009) Survey on Current Conditions of and Intention for Outbound Investment by Chinese Enterprises, China Council for the Promotion of International Trade, Beijing 74 Ibidem 75 Ibidem 76 APFC (2009) China goes Global. 2009 Survey of Outward Direct Investment Intentions of Chinese Companies. Preliminary Results, Asia Pacific Foundation of Canada and China Council for the Promotion of International Trade, Vancouver-Beijing 77 Pradhan, J. (2009) op.cit. p.19 78 CCPIT (2009) op.cit. 79 Ramamurti, R. (2009) op.cit. 80 Ibidem 81 Ibidem 82 Pettis, M. (2009) The Effect of the Crisis on the US-China Relationship, Testimony before the US-China Economic and Security Commission, Washington, February 83 Naughton, B. (2005) The Chinese economy: Transitions and growth, The MIT Press. 84 Prasad, Eswar, Thomas Rumbaugh, and Qing Wang (2005) “Putting the Cart before the Horse? Capital Account Liberalization and Exchange Rate Flexibility in China.” IMF Policy Discussion Paper, Asia and Pacific Department PDP/05/1.Washington, DC: International Monetary Fund. 85 China Daily (2009) A new code of conduct, July 7 86 Ibidem 87 Cognato, M. (2008) China Investment Corporation. Threat or Opportunity?, NBR Analysis, Vol 19, No1, July, p.9-36 88 Fotak, V. and W. Megginson (2009) Are SWFs Welcome Now? Columbia FDI Perspectives, No 9, July, pp.3