the fiscal policy impact on economic

TRANSCRIPT

THE FISCAL POLICY IMPACT ON ECONOMIC

PERFORMANCE IN ASEAN5+3:

EMPIRICAL ANALYSES

Pisit Puapan

A Dissertation Submitted in Partial

Fulfillment of the Requirements for the Degree of

Doctor of Philosophy (Economics)

School of Development Economics

National Institute of Development Administration

2011

THE FISCAL POLICY IMPACT ON ECONOMIC

PERFORMANCE IN ASEAN5+3: EMPIRICAL ANALYSES

Pisit Puapan

School of Development Economics

Assistant Professork~~ ,..~ Major Advisor

(Amornrat Apinunmahakul, Ph.D.)

~ ~~Assistant professor. Co-Advisor

(Sasatra Sudsawasd, Ph.D.)

.AssIstant Professor

~ fCX: ., .. Co-AdVIsor

(Yuthana Sethapramote, Ph.D.)

The Examining Committee Approved This Dissertation Submitted in Partial

Fulfillment of the Requirements for the Degree of Doctor of Philosophy (Economics).

Assistant Professor !I~ , Committee Chairperson

(Wisarn Pupphavesa, ~

Assistant Professor. ~~ j.~ :Committee

(Amornrat Apinunmahakul, Ph.D.)

Assistant Professor..... ~~...Committee

(Sasatra SUdS~ Assistant Professor Yrl!:.-:. ~~' Committee

(Yuthana Sethapramote, Ph.D.)

Associate professor Deand h.~ l ~: (Adis Israngkura, Ph.D.)

May,2012

ABSTRACT

Title of Dissertation The Fiscal Policy Impact on Economic Performance in

ASEAN5+3: Empirical Analyses Author Pisit Puapan Degree Doctor of Philosophy (Economics) Year 2011

This dissertation consists of two research papers to examine the impact of

fiscal policy on overall economic performance in ASEAN5+3 and Thailand. The

relationship between fiscal policy and economic growth has been a highly contentious

issue among economists. Main economic theories differ in their proposition on the

role of fiscal policy. Classical economics believes that fiscal policy has no long-term

implication on output growth, while Keynesian economics put forth its theory that

fiscal policy does have both temporary and permanent impact on the economy. With

these seemingly opposing views, it is crucial for the policy-makers and the public to

understand the role of fiscal policy particularly taxation and government expenditure

on economic growth. It is imperative for policy-makers to better understand the role

and implication of fiscal policy.

This dissertation titled “The Fiscal Policy Impact on Economic Performance in

ASEAN5+3: Empirical Analyses” comprises of two research studies as follows: 1)

“Assessment of Fiscal Policy Impact on Economic Performances in ASEAN5+3” and

2) “Thailand’s Fiscal Policy Impact Analysis.” The first paper would focus on

examining the role of fiscal policy and economic growth using the panel data for the

five ASEAN countries and the Plus Three countries (China, Japan, and Republic of

Korea) using cross-sectional data during the periods from 1979-2008. This study

classifies fiscal policy into productive versus non-productive expenditure and

distortionary versus non-distortionary taxation to examine in details how fiscal policy

implemented by ASEAN5+3 countries has impacted growth. Other non-fiscal

variables are also included such as domestic investment, international trade, and labor

iv

force. The overall results strongly suggest that fiscal policy in the ASEAN5+3 does

have discernable impact to explain the strong growth performances in the region.

Moreover, economic growth can also be attributed to higher domestic investment,

international trade, and prudent fiscal policy as the underlying factors in supporting

growth in the past decades.

The second paper would focus specifically on Thailand using the Vector

Autoregression (VAR) and Vector Error Correction Model (VECM) methods to

identify the implication of fiscal policy shocks on growth as well as analyze detailed

components of tax and expenditure policies on economic growth in Thailand. The

study finds that, contrary to a priori expectation, the short-run fiscal policy

implemented through tax and public spending does not have significant impact on

economic growth. However, in the longer-term, fiscal policy show discernable

impact on growth particularly tax exhibiting negative impact and government

expenditure showing positive impact on growth. However, in the case of Thailand,

public consumption and its components show positive effects on growth, while public

investment does not seem to have positive impact on economic performance in the

longer-term. This serves as a critical illustration for Thai policy-makers to improve

the productivity of Thailand’s public investment spending in the coming years.

Overall, the main finding of the two researches is that fiscal policy does have

impact on growth in both positive and negative ways. Tax policy generates negative

impact on economic growth in which the government must consider the costs and

benefits of implementing specific tax policies in order to minimize economic

distortions and to ensure that the negative effect from raising the fiscal resources

would be offset by the positive effect after the fiscal resources are deployed through

spending policies. Public expenditures can have positive impact on growth by its

provisions of public goods, infrastructure development, national security, law and

order. However, some public spending generates more positive economic effects than

others. In Thailand, public investment has not generated discernable positive growth

impact on the economy. Public expenditure policy should reorient spending towards

more productive types in order to maximize the positive impact on economic growth

and development. Last but not least, it is hoped that these studies would shed

insightful findings and analyses that would benefit policy-makers in Thailand as well

as the Asian region responsible for fiscal policy formulation for the years to come.

ACKNOWLEDGEMENTS

This dissertation would not have been possible without the guidance and

support of several people who in one way or another graciously extended their

valuable assistance in the completion of this work.

Foremost, I would like to express my warm and sincere gratitude to my

adviser, Assistant Professor Dr. Amornrat Apinunmahakul for her detailed and

constructive comments, and for her patience and constant support throughout this

study. I am deeply grateful to my committees, Assistant Professor Dr. Sasatra

Sudsawasd and Assistant Professor Yuthana Sethapramote, for their insightful

comments and guidance that enabled me to complete my work. Also, I would like to

thank my committee chairperson, Associate Professor Dr. Wisarn Pupphavesa,

Advisor to the Thailand Development Research Institute (TDRI), for his valuable

contribution in finalizing my work. In completing my work, I am also thankful to

various officials at the National Economic and Social Development Board (NESDB)

and Ministry of Finance (MOF) for their facilitation in providing all the necessary

data that makes this research work possible.

I would like to also extend my sincere appreciation to the faculty members at

the School of Development Economics at the National Institute of Development

Administration (NIDA) for their contribution in advancing my knowledge in the past

6 years of my PhD study. This dissertation is dedicated to my parents who have

always encouraged me to learn and improve myself. I am indebted to my family for

their constant support in every aspect throughout my life. My special gratitude is due

to my dear friend, Dr. Pat Pattanarangsun, for his generosity and kindness to me both

academically and personally. Last but not least, I also wish to thank my wife for her

understanding in letting me pursue my academic goal, and my newly born son,

Pongsit, whom I most eagerly look forward to spend with my time with after the

completion of my study.

Pisit Puapan

June 2012

TABLE OF CONTENTS

Page

ABSTRACT iii

ACKNOWLEDGEMENTS v

TABLE OF CONTENTS vi

LIST OF TABLES viii

ESSAY 1 ASSESSMENT OF FISCAL POLICY IMPACT 1

ON ECONOMIC PERFORMANCES IN ASEAN5+3

ABSTRACT 1

CHAPTER 1 INTRODUCTION 2

Background and Research Motivation 4

CHAPTER 2 LITERATURE REVIEW 7

2.1 Taxation and Economic Growth 7

2.2 Government Expenditures and Economic Growth 12

2.3 Fiscal Balance and Economic Growth 15

2.4 Investment and Economic Growth 17

2.5 Education and Economic Growth 20

2.6 Population and Economic Growth 22

2.7 Economic Growth in the Asian Context 24

CHAPTER 3 THEORETICAL MODEL AND METHODOLOGY 26

Methodology 27

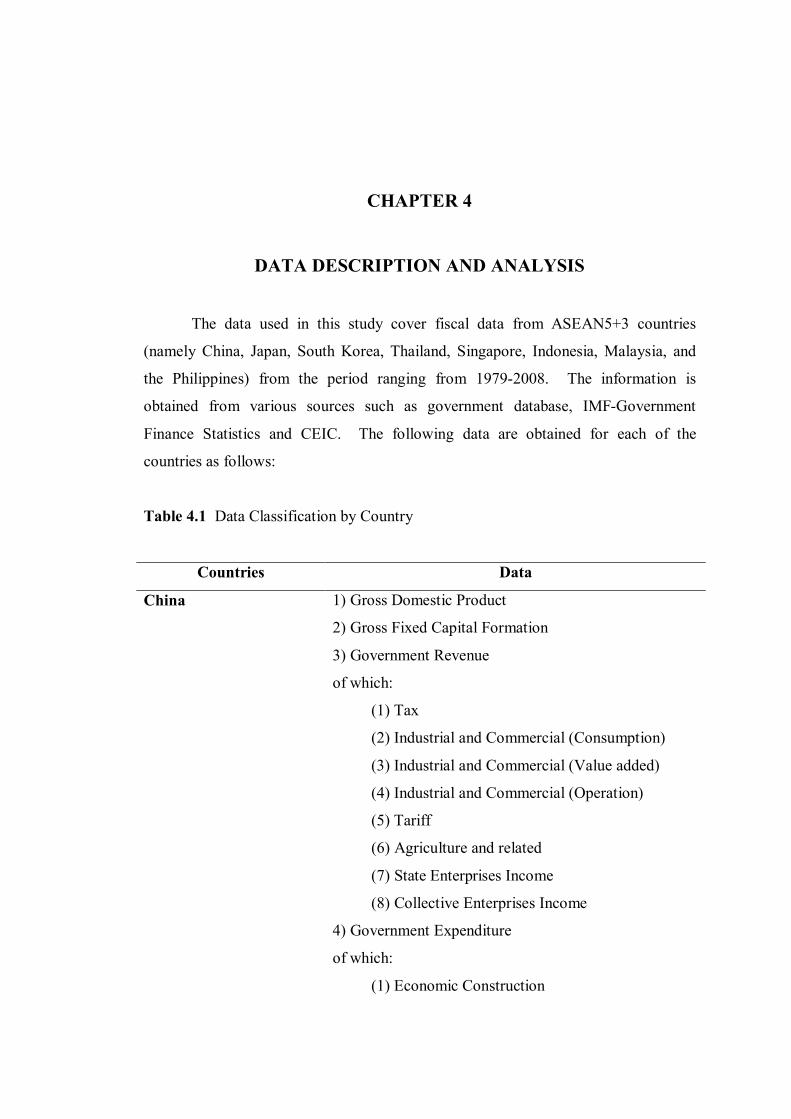

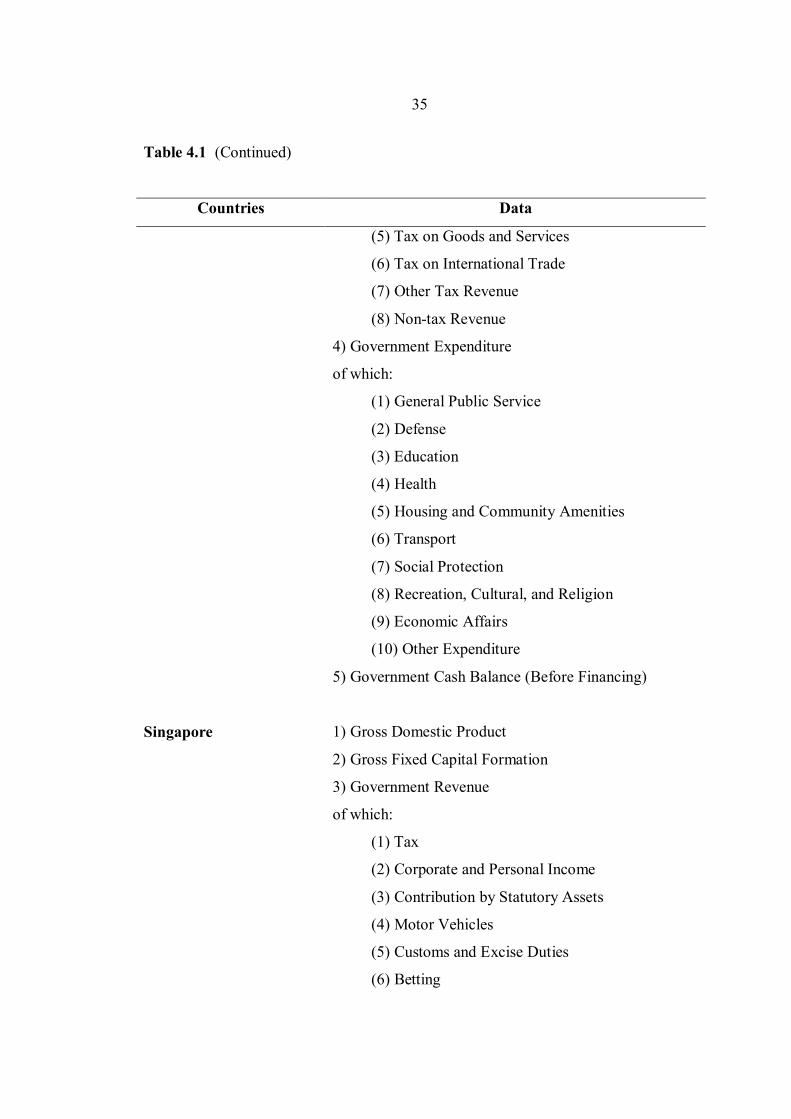

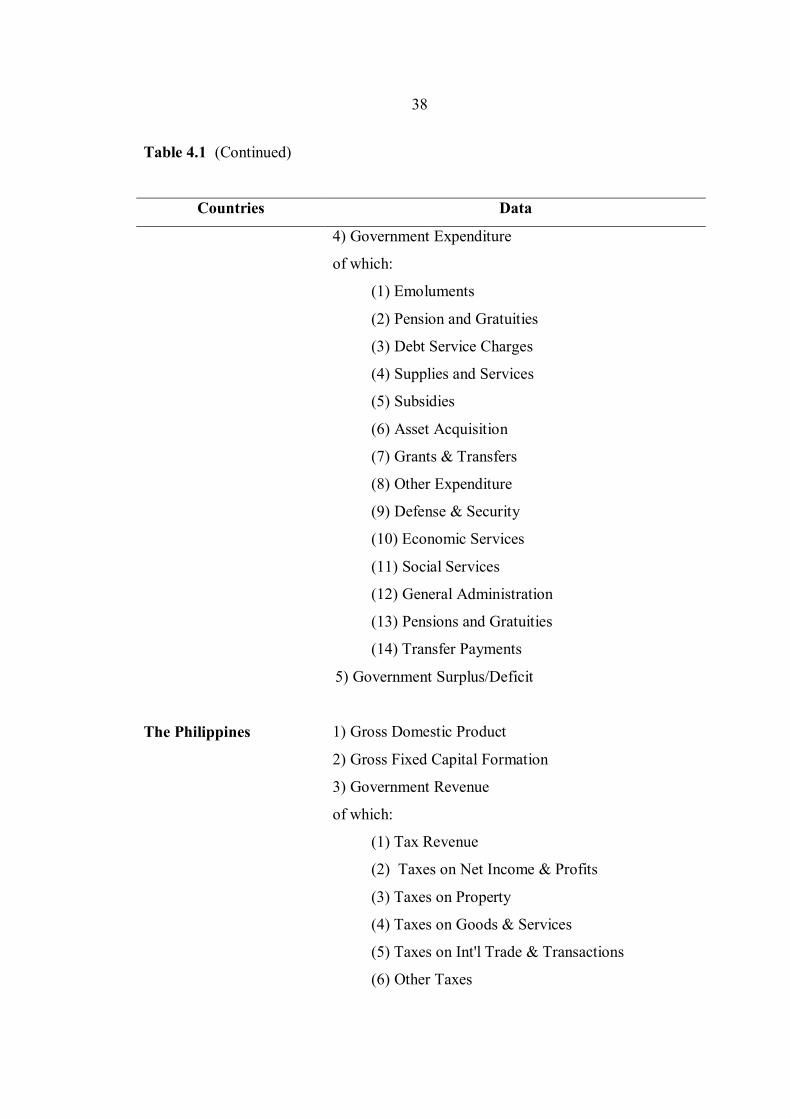

CHAPTER 4 DATA DESCRIPTION AND ANALYSIS 32

CHAPTER 5 EMPIRCAL RESULTS 55

Conclusion and Policy Recommendations 59

BIBLIOGRAPHY 62

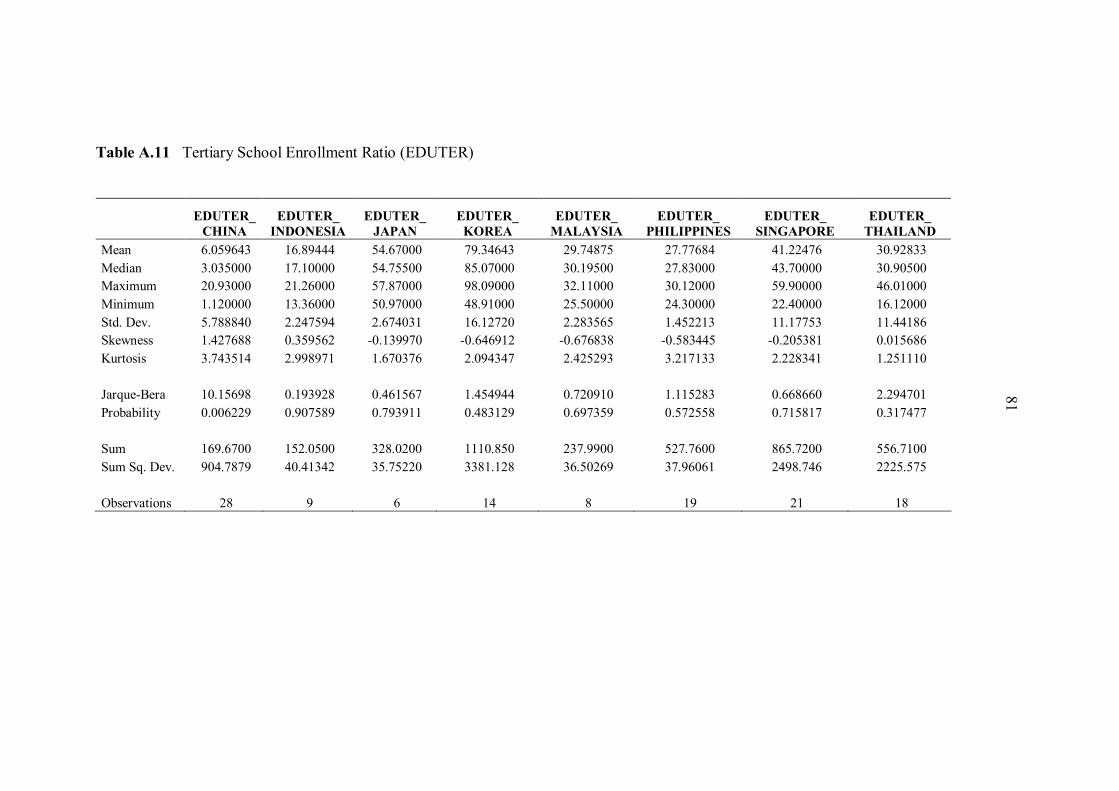

APPENDIX Summary of Data Statistics 70

vii

ESSAY 2 THAILAND’s FISCAL POLICY IMPACT ANALYSIS 83

ABSTRACT 83

CHAPTER 1 INTRODUCTION 84

Background and Research Motivation 85

CHAPTER 2 LITERATURE REVIEW AND THEORETICAL 89

MODEL AND METHODOLOGY

Conceptual Framework and Methodology 97

CHAPTER 3 FISCAL POLICY IN THAILAND: OVERVIEW, DATA 102

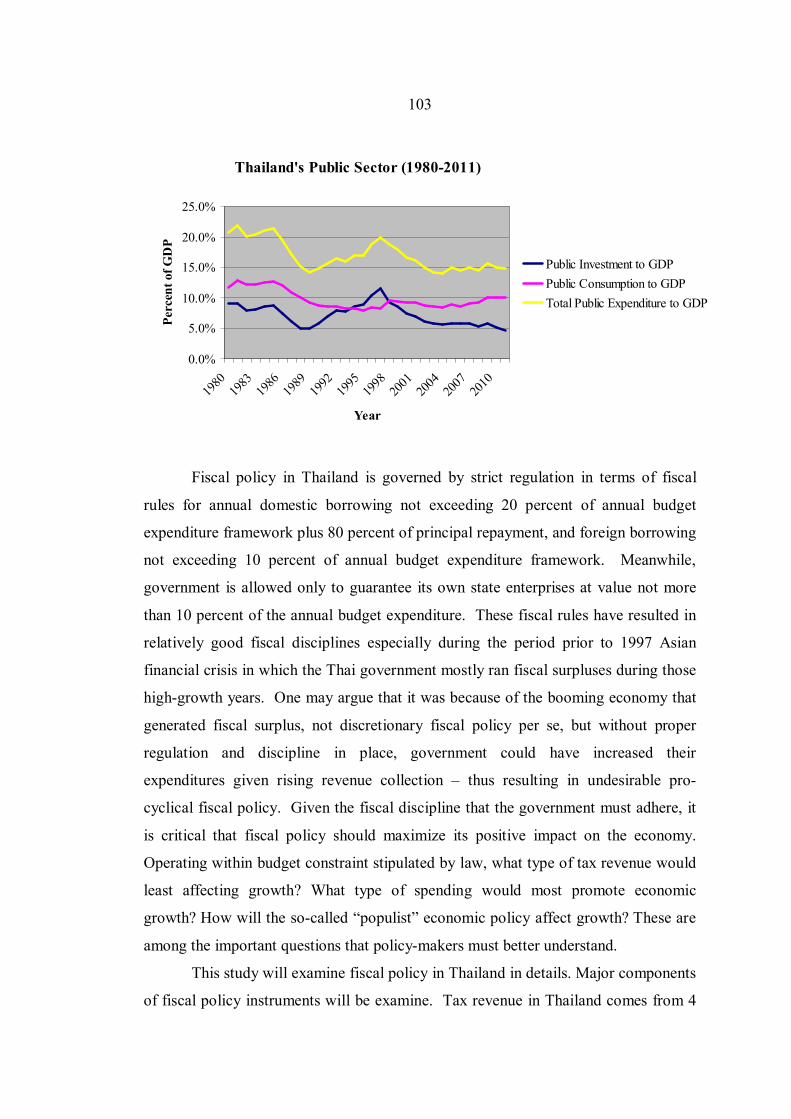

DESCRIPTION AND ANALYSIS 3.1 Overview of Fiscal Policy in Thailand 102

3.2 Data Description and Analysis 105

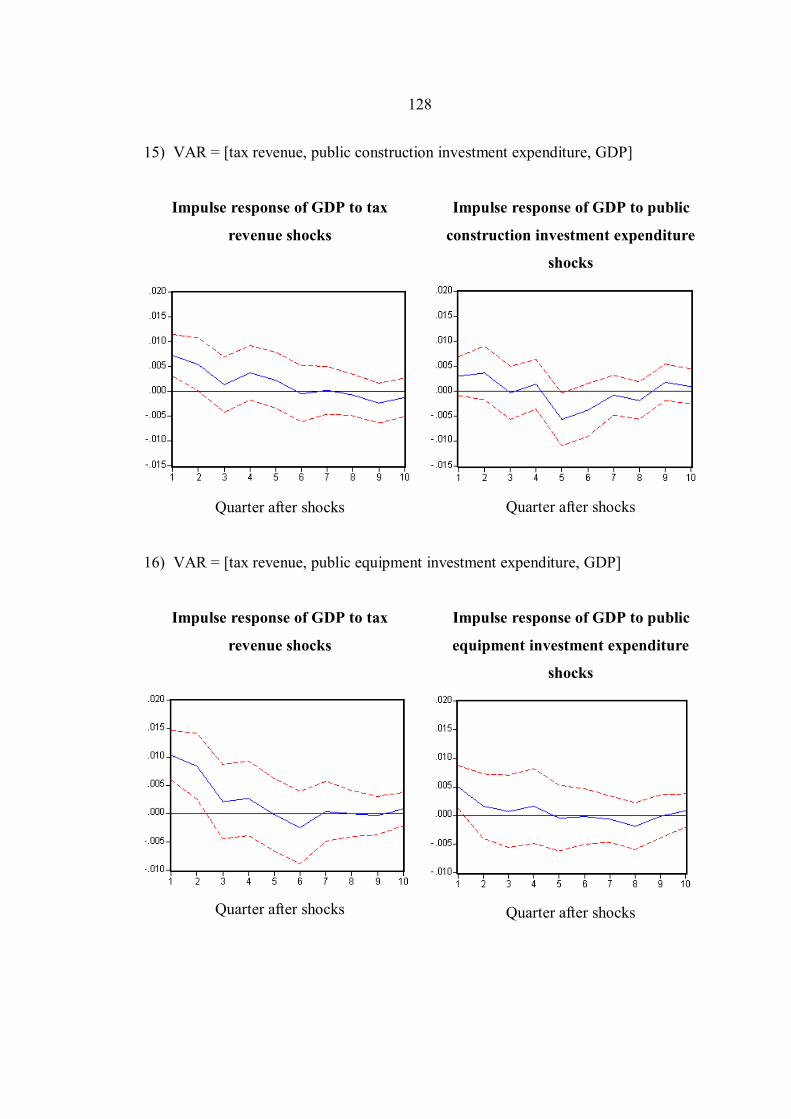

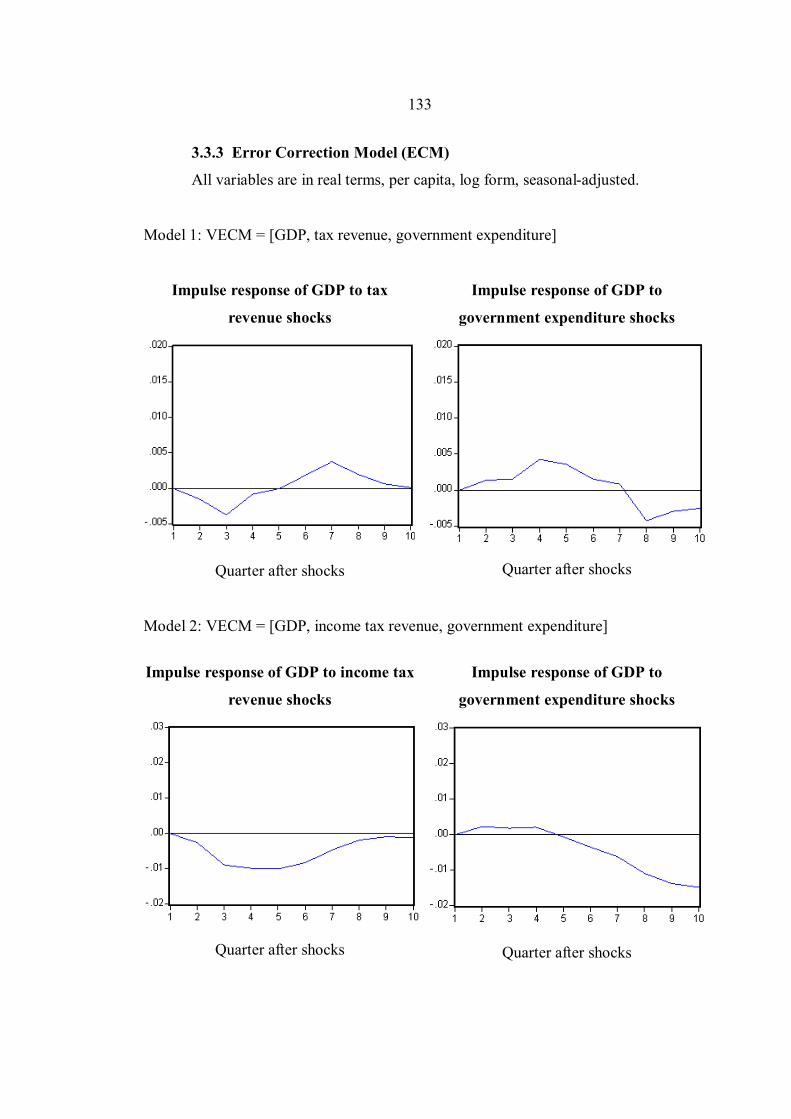

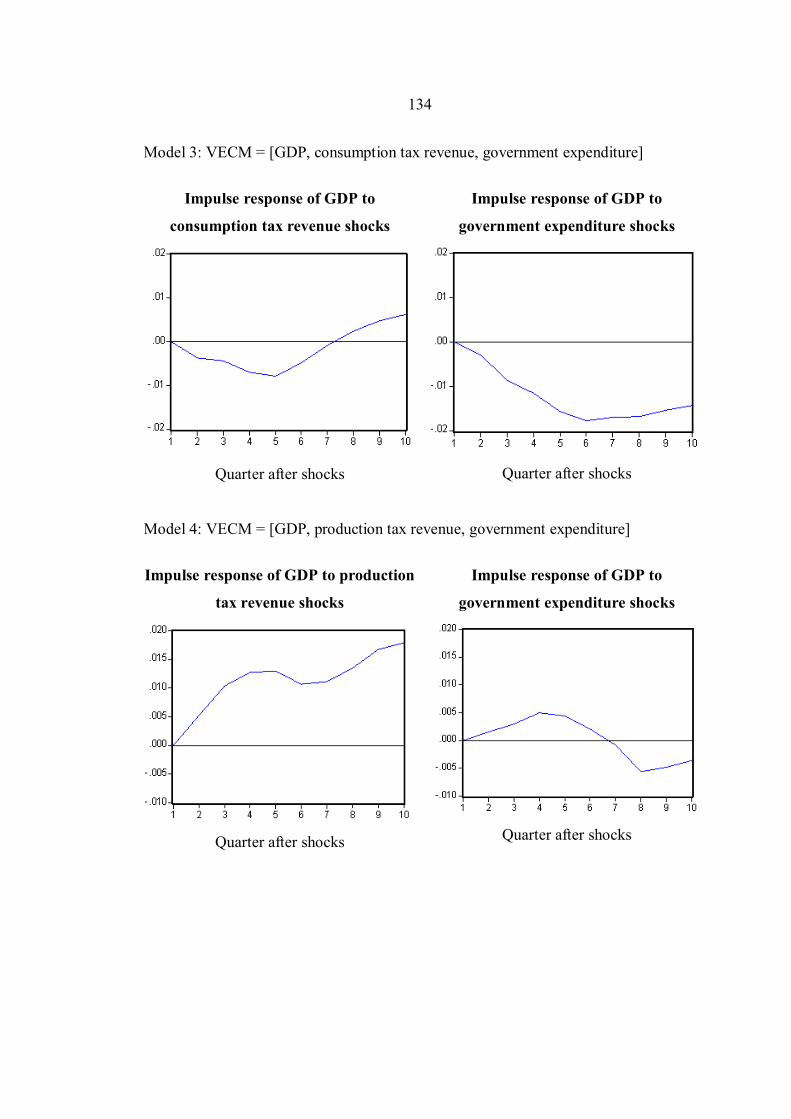

3.3 Empirical Models and Results 118

BIBLIOGRAPHY 145

APPENDIX 149

BIOGRAPHY 176

viii

LIST OF TABLES

Tables Page

ESSAY 1

4.1 Data Classification by Country 32

4.2 Fiscal Data Classifications 40

5.1 Summary of ASEAN5+3 Results 56

5.2 Summary of ASEAN5 Results 58

ESSAY 2

3.1 Data Sources 106

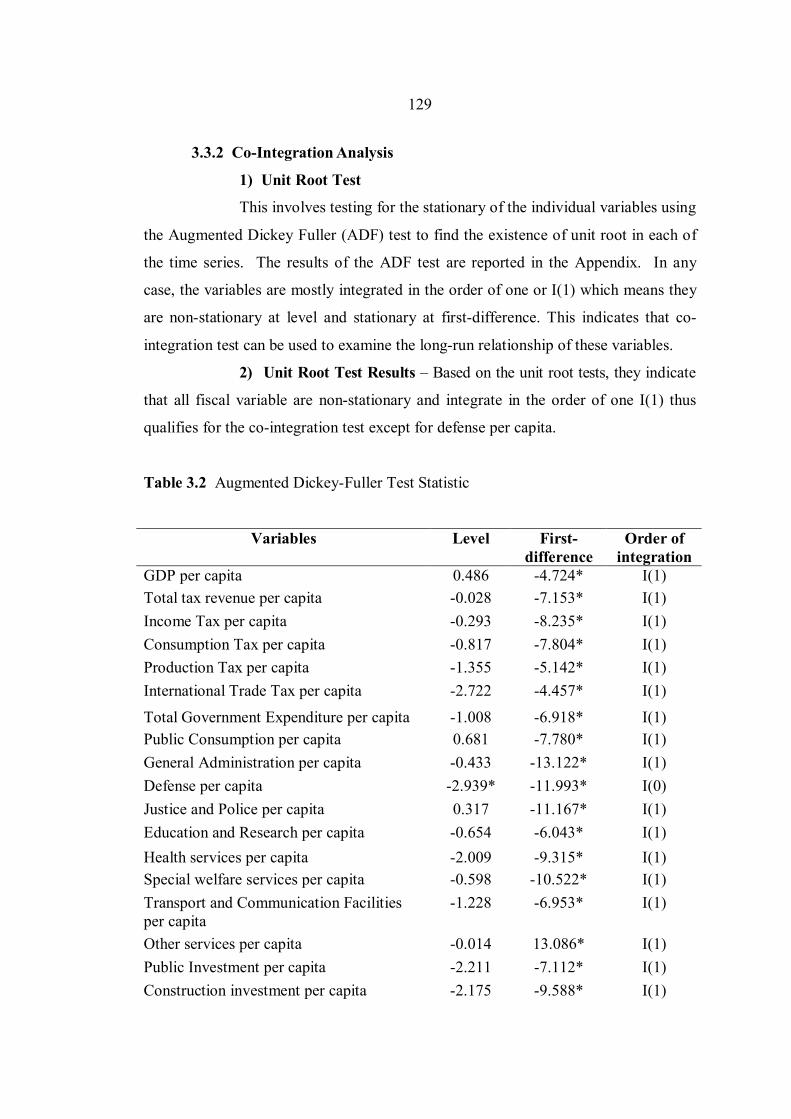

3.2 Augmented Dickey-Fuller Test Statistic 129

3.3 Co-Integration Test Results 131

ESSAY 1

ASSESSMENT OF FISCAL POLICY IMPACT ON ECONOMIC PERFORMANCES IN ASEAN5+3

ABSTRACT

Previous studies have emphasized on the role of public sector in promoting rapid growth among the ASEAN5+3 countries. In East Asia, the role of the State is assumed to have played active role in channeling resources toward productive uses, and hence enhancing economic growth This study aims to test this proposition using the panel data for the five ASEAN countries (Thailand, Singapore, Indonesia, Malaysia and the Philippines) and the Plus Three countries (China, Japan, and Republic of Korea) in the periods ranging from 1979-2008. This study classifies fiscal policy into productive versus non-productive expenditure and distortionary versus non-distortionary taxation to examine in details how fiscal policy implemented by ASEAN5+3 countries has impacted growth. Other non-fiscal variables are also included such as domestic investment, international trade, and labor force. The overall results strongly suggest that fiscal policy in the ASEAN5+3 does have discernable impact to explain the strong growth performances in the region. Moreover, economic growth can also be attributed to higher domestic investment, international trade, and prudent fiscal policy as the underlying factors in supporting growth in the past decades. Prudent fiscal policy is crucial to economic growth because excessive fiscal deficits can lead to crowding out of private investment, higher interest rate, and real exchange rate appreciation. These findings are mostly consistent with Bleaney, Gemmell and Kneller (2001) for OECD countries where productive expenditure and distortionary taxation also show positive and negative effects on growth, respectively. The study, therefore, suggests that the role of public sector and fiscal policy in ASEAN5+3 should be carefully analyzed as it has strong potentials to affect growth performances either positively and negatively with the aim to achieve better growth results in the coming years.

CHAPTER 1

INTRODUCTION

The subject of economic growth is one of the most intensely studied and

debated in the field of economics. Certainly, the growth process can be readily

observed by rising income and standard of living of the people. Many countries have

experienced unprecedented growth particularly among the North-east and South-east

Asian economies that have consistently recorded close to double-digit GDP growth in

the past few decades.

However, economic progress should not be taken for granted. Some countries

have seen little or no growth over the years such as the Sub-Saharan African and

Caribbean nations, while a few others have seen their living standards have actually

declined compared to their prior generation. Material well-being can therefore be

readily seen and observed, but less is clear about how it can come about.

One of the most controversial issues on economic growth is how the role of

the government and public sector can affect economic growth. In 1956, Robert M.

Solow proposed what is now called neoclassical growth model that the long-run

growth rate is driven by population growth and the rate of technological progress.

Based on his proposition, government policies through taxation and expenditure may

affect the incentive to invest in human or physical capital, but in the long-run this

affects only the equilibrium factor ratios, not the growth rate, although in general

there will be transitional growth rates. Therefore, fiscal policy may only have the

“level effect” on economic growth, but not the “growth effect.” On the other hand,

more recent theoretical growth model particularly the endogenous growth theory

proposed by Robert Barro in 1990 predicts that, among other things such as scale

economies, research and development, there are certain types of taxation and

expenditures that can determine long-run growth rate in a given economy.

Given these contrasting theoretical views, economists are keen to better

understand the key determining factors of economic growth particularly on the role of

3

fiscal policy which are crucial to economic policy formulation. Would productive

investments in physical infrastructure such as road and railway and social

infrastructure such as public education and public health help to promote growth in a

country?

Thus, this study aims to examine and empirically analyze the growth impact of

fiscal policy using panel data from selected 8 countries under the ASEAN Five and

Plus Three countries (China, Japan, South Korea, Thailand, Singapore, Indonesia,

Malaysia, and the Philippines) from periods ranging from 1979 to 2008. The

methodologies used are two-way fixed effect model (Least Square Dummy Variables),

dynamic fixed effect model, and Generalized Methods of Moment (GMM). Fiscal

policy components are classified into productive versus non-productive expenditure

and distortionary versus non-distortionary taxation to examine in details how fiscal

policy by ASEAN5+3 countries could impact growth. The definition of particular

expenditures as productive or non-productive or particular taxes as distortionary or

non-distortionary may be open to debate. However, in this study, the theoretical

classification of tax and public expenditures are based on Professor Barro (1990)

classification. Distortionary taxation and productive investments are those that affect

incentive to invest in human or physical capital. Income-based taxes are considered to

be distortionary in the sense that it affected work incentive, while consumption-based

taxes have relatively less effect on labor-leisure choices. Productive expenditures are

those spending that could increase economic capacity and productivity, while non-

productive expenditures are consumption-type such as social security and welfare

spending. Other non-fiscal variables are also included such as domestic investment,

international trade, and labor force. Previous study by Bleaney et al. (2001) only

includes the two non-fiscal variables, but ASEAN+3 growth may also come from

international trade openness, so export-import to GDP is included as a proxy for trade

openness. There are other measures of openness to trade as well such as average tariff

rate that could potentially be used as the non-fiscal explanatory variable, but due to

data limitation, only export-import to GDP will be used in this study. Human capital

formation is also important to growth in ASEAN+3, so school enrollment ratio is

included as proxy for human capital. Dummy variable for 1997 Asian financial crisis

is also included.

4

Contrary to conventional wisdom, the results strongly suggest that the fiscal

policy implemented in the ASEAN5+3 does have discernable impact to explain the

growth performances in the region. Moreover, the region’s economic growth can also

be attributed to other factors as well particularly domestic investment, international

trade, and prudent fiscal policy as the underlying factors in supporting growth in the

past decades. These findings are different from Bleaney et al. (2001) for OECD

countries where productive expenditure and distortionary taxation also show positive

and negative effects on growth, respectively. The study, therefore, suggests that the

role of public sector and fiscal policy in ASEAN5+3 should be carefully analyzed as

it has strong potentials to affect growth performances either positively and negatively

with the aim to achieve better growth results in the coming years.

Background and Research Motivation

In Asia, the role of fiscal policy in promoting economic growth has been

controversial in whether the Asian States have had a positive role in promoting

growth or active policies implemented by these countries have been growth-neutral or

even growth-inhibiting. The economic core of Asia is now gravitated towards the

Eastern part of the continent with the major driving force in the regional formation

called ASEAN+3 which started in 1997 after the Asian financial crisis comprising of

13 member countries (the 10 ASEAN countries and China, Japan, and South Korea).

Many countries outside regions are closely observing the developments within

ASEAN+3 given its increasing economic power, new and innovative cooperation in

trade and finance, and the future prospect for the eventual formation of East Asia

Economic Community in the years ahead.

By all accounts, economic data in ASEAN+3 have shown that economic

performances in the region have been consistently outperformed other regions. This

phenomenon then offers one of the most interesting inquiries for policy-makers and

professional economists to identify the growth contributors for ASEAN+3 region.

These economies have grown impressively over a period of nearly 30 years. The

region now has 2.17 billion people representing over 30 percent of world population.

In 1960, the GDP of ASEAN+3 was approximately 40 percent of US GDP, with

5

Japan contributing more than 80 percent of total East Asian GDP, followed by China

(Mainland only), with not quite 8 percent. By 2000, the GDP of ASEAN+3 was

approximately 75 percent of US GDP, with Japan contributing more than 60 percent

of total GDP, followed by China (Mainland only), which contributed somewhat more

than 15 percent. Ten years later, China would become the second largest economy in

the world, overtaken Japan and second only to the U.S. Real per capita GDP

expanded in excess of four times during the period, while average global income

registered less than a two-fold increase. Such robust, prolonged growth has clearly

raised incomes, lifted millions out of poverty, and expanded ASEAN+3 region’s

global economic influence.

Per capita GDP in ASEAN+3 remains below the global average at $6,837, but

is rapidly catching up. In 1980, the income of the average person living in ASEAN+3

region was just over a quarter of the world average; by 2010, it had risen to nearly

three-fourth. As in all world regions, the wealth of individual ASEAN+3 countries

differs widely between, and within, states. This is due to its vast size, meaning a huge

range of differing cultures, environments, historical ties and government systems. The

largest economies within ASEAN+3 in terms of nominal GDP are China, Japan,

South Korea, and Indonesia. In terms of GDP by purchasing power parity, China

followed by Japan, and South Korea are the largest economies in decreasing order.

Wealth (if measured by GDP per capita) is mostly concentrated in Northeast

Asian territories such as Hong Kong, Japan, South Korea, Singapore and Taiwan.

Within ASEAN+3, with the exception of Japan, South Korea, Hong Kong and

Singapore, is currently undergoing rapid growth and industrialization spearheaded by

China – one of the fastest growing major economies in the world. Over the years,

with rapid economic growth and large trade surplus with the rest of the world,

ASEAN+3 has accumulated over USD 5.5 trillion of foreign exchange reserves -

more than half of the world's total.

Sustained and rapid growth in ASEAN+3 in the past five decades (1960s

onward) needs analyses to explain the growth determinants. In the current literature

of growth theory, the neoclassical growth model of Solow (1956) postulates that long-

run growth rate is driven by population growth and the rate of technological progress.

Fiscal policy implemented through taxation and government expenditures may affect

6

the incentive to invest in human and physical capital, but it only affects the

equilibrium ratios, not growth rate, in the long-run. On the other hands, endogenous

growth models proposed by Barro, King and Rebelo (1990) predicts that fiscal policy

will affect long-run growth rate. Government spending and taxation should have both

temporary and permanent effects on growth. In particular, fiscal policy in the

endogenous growth model is often classifies into various categories of taxations and

public expenditures to examine growth implications.

This paper aims to develop on the theoretical framework of endogenous

growth model to test for the underlying factors contributing to economic growth

among the ASEAN5 (Thailand, Singapore, Indonesia, Malaysia and the Philippines)

and the Plus Three countries (China, Japan, and Republic of Korea) (hereafter called

“ASEAN5+3”) in the periods ranging from 1979-2008. A particular focus is given to

the role of fiscal policy through public expenditure and taxation implemented by

ASEAN5+3 in their respective impact on economic growth. However, this study will

expand from Bleaney et al. (2001) by examining the role of non-fiscal variables

beyond those covered by the previous study to include the role of trade openness and

education as non-fiscal determinants of growth in the region.

CHAPTER 2

LITERATURE REVIEW

2.1 Taxation and Economic Growth

The starting point of conventional economic growth theorization is the

neoclassical model of Solow (1956). The basic assumptions of the model are: constant

returns to scale, diminishing marginal productivity of capital, exogenously determined

technical progress and substitutability between capital and labor. As a result, the

model highlights the savings or investment ratio as important determinant of short-run

economic growth. Technological progress, though important in the long-run, is

regarded as exogenous to the economic system. In this model, the incentives to save

or to invest in new capital are affected by fiscal policy; this alters the equilibrium

capital-output ratio and therefore the level of the output path, but not its slope (with

transitional effects on growth as the economy moves onto its new path).

On the other hand, endogenous growth models “endogenize” the role of

technological progress as a key driver of long–run economic growth with both

constant and increasing returns to capital. These new growth theories propose that the

introduction of new accumulation factors, such as knowledge, innovation, etc., will

induce self-maintained economic growth. Triggered by Romer’s (1986) and Lucas’

(1988) seminal studies, work within this framework highlighted three significant

sources of growth: new knowledge particularly in the presence of positive externalities

from human capital accumulation (Romer, 1990, Grossman and Helpman, 1991),

endogenous technological change and innovation (Aghion and Howitt, 1992) and

permanent changes in variables potentially affected by government policies lead to

permanent changes in growth rates (i.e. public infrastructure) (Barro, 1990).

Following this third source of growth, the novel feature of the public-policy

endogenous growth models of Barro (1990), Barro and Sala-i-Martin (1992) and

8

Mendoza, Milesi-Ferretti, and Asea (1997) is that fiscal policy can determine both the

level of the output path and the steady-state growth rate.

There are various studies that have examined the relationship between fiscal

policy and growth. A recent study titled Testing the endogenous growth model:

public expenditure, taxation, and growth over the long run by Bleaney et al. (2001)

examines the endogenous growth model to observe the relationship among public

expenditure, taxation and growth over the long-run using the data from OECD

countries during the period from 1970-1995. They have found strong support for

endogenous growth model and suggest that long-run fiscal effects have impact on

growth performances. It is found that distortionary taxation (i.e. income-based and

profit taxes, social security contributions, and property taxes) have negative effect on

growth, while productive expenditures (i.e. general public service expenditures,

education expenditures, health expenditures, and housing expenditures) generate

positive effect on growth. Budget surplus has a statistically significant positive effect

on growth as it can be used to compensate future deficits anticipated under Ricardian

equivalence that may partially finance productive expenditure or cuts in distortionary

taxation, raising the anticipated returns to investment and hence growth. A non-fiscal

variable, domestic investment ratio to GDP, is also found to have positive impact on

growth.

The associations of fiscal policy on economic growth have been examined and

discussed in other research papers. On the implications of taxation and economic

growth, there seems to be a consensus that “high taxes are bad for economic growth.”

Taxation and Economic Growth by Eric Engen and Jonathan Skinner illustrates the

theatrical framework that catalogs five ways that taxes might affect output growth.

First, higher taxes can discourage investment as it discourages the investment rate (or

the net growth in capital stock), through high statutory tax rates on corporate and

individual income, high effective capital gain tax rates, and low depreciation

allowances. Second taxes may attenuate labor supply growth by discouraging labor

force participation or hours of work, or by distorting occupational choice or the

acquisition of education, skills, and training. Third, the tax policy has the potential to

discourage productivity growth by attenuating research and development and

entrepreneurial activities that may generate innovation and positive spill-over effects.

9

Fourth, tax policy can also influence the marginal productivity of capital by distorting

investment from heavily taxed sectors into more lightly taxed sectors with lower

overall productivity. And fifth, heavy taxation on labor supply can distort the

efficient use of human capital by discouraging workers from employment in sectors

with high social productivity but a heavy tax burden. In the conventional Solow

growth model, however, postulate that taxes should have no impact on long-term

growth rates. Using cross-country data, Koester and Kormendi (1989) estimated that

the marginal tax rates- conditional on fixed average tax rates- has an independent,

negative effect on output growth. Skinner (1988) used data from African countries to

conclude that income, corporate, and import taxation led to greater reductions in

output growth than average export and sales taxation. Dowrick (1992) also found a

strong negative effect of personal income taxation, but no impact of corporate taxes,

on output growth in a sample of Organization for Economic Cooperation and

Development (OECD) countries between 1960 and 1985. Easterly and Rebelo (1993b)

found some measures of the tax distortion (such as an imputed measure of marginal

tax rates) to be correlated negative with output growth, although other measures of tax

distortion were insignificant in the growth equations.

Of course, nearly any tax will tend to distort economic behavior along some

margin, so the objective of a well designed tax system is to avoid highly distortionary

taxes and raise revenue from the less distortionary ones. There is some evidence that

how a country collects taxes matters for economic growth. Mendoza, Milesi-Ferretti,

and Asea (1996), shows the correlation among the OECD countries between income

taxes and economic growth and consumption taxes and economic growth, over the

period from 1965 to 1991. They found that income taxation is more harmful to growth

than broad-based consumption taxes.

To this point, the results of the cross-country econometric studies have been

taken at face value. Any empirical study must be treated with some caution; but, in

many of the studies cited above, particularly the cross-country studies, one must be

particularly careful in the interpretation of the coefficients (Levine and Renelt, 1992;

Slemrod, 1995). There are four potential problems in interpreting the results as

follows:

10

First, studies of taxation and growth may find negative growth effects

resulting from taxation, but it is more difficult to measure the potential benefits of the

spending financed by the revenue collected. The combined impact of distortionary

taxes and beneficial government expenditures may yield a net improvement in the

workings of the private sector economy (e.g., Barro, 1990, 1991a, 1991b). An

example of the deleterious effects caused by the absence of government spending

comes from the World Development Report (World Bank, 1988: 144):

According to the Nigerian Industrial Development Bank (NIDB),

frequent power outages and fluctuations in voltage affect almost every

industrial enterprise in the country. To avoid production losses as well

as damage to machinery and equipment, firms invest in generators....

One large textile manufacturing enterprise estimates the depreciated

capital value of its electricity supply investment as $400 per worker....

Typically, as much as 20 percent of the initial capital investment for

new plants financed by the NIDB is spent on electric generators and

boreholes.

That is, when the government of Nigeria did not provide the necessary

electricity supply, private firms were forced to generate electricity on their own, and

presumably at much higher cost. Clearly, a tax in Nigeria earmarked for (new)

government expenditures on improving the electrical system would be likely to

enhance economic growth even if the taxes distorted economic activity. The problem

is that taxes are not necessarily earmarked to those expenditures most conducive to

economic growth, either because of political “inefficiencies” or because of

redistributional policies that may yield benefits for society but will not be reflected in

robust GDP growth rates (Atkinson, 1995). Thus, one must be careful in interpreting

the coefficients on tax and output growth studies to remember that these estimates

reflect just one part—the costs— of a combined tax and expenditure system. Second,

one should be very wary of the data, particularly from developing countries with large

agricultural or informal sectors where the measurement of income is difficult indeed.

Even in developed countries, it is well known that GDP measures suffer from biases

11

and mis-measurement of productivity in service sectors, for example. Measuring

“the” effective tax rate is even more difficult, given the wide variety of tax distortions,

methods for measuring them, and variation across countries in administrative

practices. Third, there are real difficulties with reverse causation; one does not know

whether regression coefficients reflect the impact of investment on GDP growth rates,

for example, or the reverse influence of GDP growth rates on investment, or both

effects combined (Blomstrom, Lipsey and Zejan, 1996). Sometimes these biases creep

in because of the way the regression variables are constructed. Suppose one wanted to

estimate an explicitly short-term relationship between the change in the tax burden,

typically measured as the ratio of tax revenue to GDP, and the percentage growth rate

in GDP. Any positive measurement error (or short-term shock) in GDP will shift GDP

growth rates up but also tend to shift the tax-to-GDP ratio down, thereby introducing

a spurious negative bias in the estimated coefficient. One can try to avoid such bias

by introducing as explanatory variables the percentage growth rate in the level of

taxation, or of government expenditures, rather than the change in the ratio, as above.

In this case, the bias would go in the opposite direction, because countries that grow

rapidly also tend to experience rapid growth in tax collection and in spending. One

approach for both of these problems is to use instrumental variables for changes in

government spending and taxation (Engen and Skinner, 1992), although the problem

still remains to find appropriate exogenous instruments. Another “reverse causality”

problem comes in deciding what factors to include on the right-hand side of a growth

regression. Should one control for other factors such as inflation, political unrest, and

the share of agriculture in total output? On the one hand, these are factors that could

be spuriously correlated with tax policy, and one would clearly want to control for

them. But, on the other hand, a shrinking share of agriculture in output, or political

unrest, or inflation could be symptomatic of the underlying growth rate of the

economy. During severe recessions, countries often resort to high inflation rates as a

means of financing expenditures after their tax collection efforts have collapsed. This

reverse causation makes it harder to argue that inflation “causes” poor economic

growth, as well as making it difficult to interpret the coefficients on all other

variables. In sum, reverse causality is really the Achilles’ heel of the typical cross-

country regression. Nearly every variable on the right-hand side of the regression is

suspect.

12

Fourth, as noted by Slemrod (1995), countries may differ both in their tastes

for government-sector spending (the demand side) and in their ability to raise tax

revenue (the supply side). Suppose that more developed countries experience a lower

cost of raising tax revenue, perhaps because industrial production is much easier to

tax than agricultural production. Then countries that grow quickly may also

experience a more pronounced drop in their cost of raising tax revenue, which could

in turn lead to more rapid growth in tax revenue. The researcher might well find a

spurious positive correlation between tax rates and output growth. By the same token,

countries that grow fast may exercise a greater taste for government spending

(sometimes known as Wagner’s law), leading to a shift to the right in the demand for

government spending. As Slemrod points out, such a model would imply that, in a

cross section of countries, there could be little correlation between output growth,

government spending, and taxation.23 Slemrod’s point is therefore a cautionary one,

that the regression coefficients one actually estimates may have little to do with the

Solow-style production function written in equation 1 (see also Islam, 1995). But this

point also suggests that, even if taxes affect growth rates adversely, cross-country

regression models would be biased against detecting such effects.

2.2 Government Expenditures and Economic Growth

Research studies examining the relationship between government expenditure

and economic growth have found inconclusive results. Empirical works have led to

positive association, but many studies have found negative influence of government

expenditure on economic growth, while others have shown no correlation between

government spending and economic growth.

On the positive relationship between government expenditures and economic

growth, Wager’s Law in 19th century Greece: a Co-integration and causality analysis

by Dimitrio Sideris, uses co-integration to test long-run relationship between

government expenditure and national income and granger causality to test causality

run using annual data from 1833-1938. This study found positive long-run relationship

between government expenditure and national income. Causality runs from income to

government expenditure (supporting Wager’s hypothesis). Another study, Government

13

Expenditure and Economic Growth: Evidence from Trivariate Causality Testing by

John Loizides examines three countries: Greece, United Kingdom, and Ireland. Using

panel regression, the study aims to examine if relative size of government (measured

as share of total expenditure to GNP) can be determined to Granger cause the rate of

growth, or if the rate of growth can be determined to Granger cause the relative size

of government. With the bivariate error correction model within a Granger causality

framework as well as adding unemployment and inflation (separately) as explanatory

variables. Using data on Greece, UK, and Ireland, it shows: 1) government size

Granger causes economic growth in all countries of the sample in the short-run and in

the long-run for Ireland and the UK 2) economic growth Granger causes increases in

the relative size of government in Greece, and when inflation is included, in the UK.

Government Spending and Economic Growth: Econometric Evidence from South

Eastern Europe by Constantinos Alexiou examines seven transitional economies in

South Eastern Europe (SEE) using dynamic panel data regression model and finds

that the empirical evidence generated indicate that four out of the five variables used

in the estimation i.e. government spending on capital formation, development

assistance, private investment and trade-openness all have positive and significant

effect on economic growth. Population growth in contrast, is found to be statistically

insignificant.

On the other hand, there are many studies that have found no correlation or

even negative relationship between government spending and growth. An Examination

of the Government Spending and Economic Growth Nexus for Malaysia Using the

Leveraged Bootstrap Simulation Approach by Chor Foon Tang applies bounds testing

for co-integration and the leveraged bootstrap simulation approaches to examine the

relationship for three different categories of government spending (Health, Defense,

and Education) and Malaysian national income using yearly data from 1960-2007.

The study finds no evidence of co-integrating relation between government spending

on health and income in Malaysia. Modified WALD causality test shows strong

evidence of unidirectional causal relationship running from national income to the

three major government spending in Malaysia. However, bi-causality exists between

health spending and income. Government Spending and Economic Growth in Saudi

Arabia by Khalifa H. Ghali uses vector autoregressive (VAR) analysis, the study

14

examines intertemporal interactions among growth rate per capita real GDP and Share

of Government Spending to GDP. The study finds no consistent evidence that

government spending can increase Saudi Arabia’s per capita output growth.

Therefore, the study suggests that fiscal policy aiming the control of budget deficit in

Saudi Arabia has to consider shirking the size of government and limiting its role in

the economy. Causality between Public Expenditure and Economic Growth: the

Turkish Case by Muhlis Bagdigen examines growth using co-integration test and

Granger Causality test to examine Wagner’s Law of long-run relationship between

public expenditure and GDP over the period of 1965-2000. The study finds no

causality in both directions; neither Wager’s Law nor Keynes Hypothesis is valid for

the Turkish case. An Examination of the Government Spending and Economic

Growth Nexus for Turkey Using the Bound Test Approach by Sami Taban uses bonds

testing approach and MWALD Granger Causality test covering the period from

1987:Q1 to 2006:Q4. It findings are 1) Share of total government spending and share

of government investment to GDP are negative impacts on growth of real per capita

GDP in the long-run 2) No evidence of co-integrating relation between government

consumption spending to GDP ratio and per capita output growth 3) MWALD

causality test indicates strong bi-directional causality between total government

spending and economic growth 4) No statistically significant relationship between the

share of government consumption spending to GDP and economic growth, a uni-

directional causality has been found running from the per capita output growth to the

ratio of government investment to GDP. Government Spending and Economic Growth

in Tanzania, 1965-1996 by Josaphat P. Kweka and Oliver Morrissey (1997) investigates

the impact of public expenditures on economic growth using time series data on

Tanzania (32 years). Total government expenditure is disaggregated into expenditure on

(physical) investment, consumption spending, and human capital investment. The study

finds that 1) increased productive expenditure (physical investment) appears to have a

negative impact on growth 2) consumption expenditure relates positively to growth

(mostly associated with increased private consumption) 3) expenditure on human capital

investment is insignificant in the regressions, probably because any effects would

have very long lags 4) confirm that public investment in Tanzania has not been productive,

and counter the view that government consumption is growth-reducing 5) foreign aid

appears to have had a positive impact on growth after reform in mid-1980s.

15

Government Expenditures, Military Spending and Economic Growth: Causality

Evidence from Egypt, Israel, and Syria by Suleiman Abu-Bader and Aamer Abu-Qarn

(2003) investigates growths in Egypt, Israel, and Syria with multivariate cointegration

and variance decomposition techniques to investigate the causal relationship between

government expenditure and economic growth for Egypt, Israel, and Syria, for the

past three decades. The study classifies government expenditures into civilian and

military expenditures. It finds that 1) bi-directional causality from government

spending to economic growth with a negative long-term relationship between the two

variables 2) testing causality within a trivariate system, the share of government

civilian expenditure in GDP, military burden, and economic growth, the study finds

military burden negatively affects economic growth for all three countries, and that

civilian government expenditures cause positive economic growth in Israel and Egypt.

Government spending and economic growth: the G-7 experience by Edward Hsieh

and Kon S. Lai (1994) looks at the data from G-7 Member Countries to examine

intertemporal interactions among the growth rate of per capita real GDP, the share of

government spending, and the ratio of private investment to GDP of G-7 countries

using vector autoregression (VAR) and multivariate time series analysis. No consistent

evidence is found that government spending can increase per capita output growth.

Neither is there consistent support for the negative argument. For most countries

under study, public spending is found to contribute at best a small proportion to

economic growth.

2.3 Fiscal Balance and Economic Growth

On fiscal balance (fiscal discipline) and its implications on economic growth,

experiences suggest that fiscal discipline seem to show complementary relationship

with buoyant economic performance. Fiscal indiscipline—seen when governments

consistently spend more than they collect and more than they can easily finance

through sustainable borrowing—has had high costs for the developing economies.

Budget deficits have many effects, but they all follow from a single initial effect:

deficits reduce national saving. National saving is the sum of private saving (the after-

tax income that households save rather than consume) and public saving (the tax

revenue that the government saves rather than spends). When the government runs a

16

budget deficit, public saving is negative, which reduces national saving below private

saving. The effect of a budget deficit on national saving is most likely less than one-

for-one, for a decrease in public saving produces a partially-offsetting increase in

private saving. Nonetheless, when budget deficits reduce national saving, they must

reduce investment, reduce net exports, or both. Economic theory says that the total

fall in investment and net exports must exactly match the fall in national saving.

These changes are brought about by interest rates and exchange rates. Interest rates

are determined in the market for loans, where savers lend money to households and

firms who desire funds to invest. A decline in national saving reduces the supply of

loans available to private borrowers, which pushes up the interest rate (the price of a

loan). Faced with higher interest rates, households and firms choose to reduce

investment. Higher interest rates also affect the flow of capital across national

boundaries. When domestic assets pay higher returns, they are more attractive to

investors both at home and abroad. The increased demand for domestic assets affects

the market for foreign currency: if a foreigner wants to buy a domestic bond, he must

first acquire the domestic currency. Thus, a rise in interest rates increases the demand

for the domestic currency in the market for foreign exchange, causing the currency to

appreciate. The appreciation of the currency, in turn, affects trade in goods and

services. With a stronger currency, domestic goods are more expensive for foreigners,

and foreign goods are cheaper for domestic residents. Exports fall, imports rise, and

the trade balance moves toward deficit. Therefore, government budget deficits reduce

national saving, reduce investment, reduce net exports, and create a corresponding

flow of assets overseas. These effects occur because deficits also raise interest rates

and the value of the currency in the market for foreign exchange.

Furthermore, the accumulated effects of the deficits alter the economy’s

output and wealth. In the long run, an economy’s output is determined by its

productive capacity, which, in turn, is partly determined by its stock of capital. When

deficits reduce investment, the capital stock grows more slowly than it otherwise

would. Over a year or two, this crowding out of investment has a negligible effect on

the capital stock. But if deficits continue for a decade or more, they can substantially

reduce the economy’s capacity to produce goods and services, thus negatively

affecting long-term economic growth.

17

Nonetheless, against the conventional economic theory, there are some studies

that show slight fiscal deficits may have a growth-enhancing effect particularly for

developing economies. In Fiscal Deficits and Growth in Developing Countries by

Christopher S. Adam and David L. Bevan (2005), it examines the relation between

fiscal deficits and growth for a panel of 45 developing countries. Based on a

consistent treatment of the government budget constraint, it finds evidence of a

threshold effect at a level of the deficit around 1.5% of GDP. While there appears to

be a growth payoff to reducing deficits to this level, this effect disappears or reverses

itself for further fiscal contraction. The magnitude of this payoff, but not its general

character, necessarily depends on how changes in the deficit are financed (through

changes in borrowing or seigniorage) and on how the change in the deficit is

accommodated elsewhere in the budget. They also find evidence of interaction effects

between deficits and debt stocks, with high debt stocks exacerbating the adverse

consequences of high deficits.

2.4 Investment and Economic Growth

On investment and growth relationship, over the past 20 years, there has been

an explosion of theoretical and empirical research that examines the relationship

between investment, productivity and long-term economic growth.

The neoclassical model originally focused on investment in tangible assets,

and the resulting accumulation of physical assets to help explain economic growth.

Recently the concept of investment has been broadened from private investment in

tangible assets to include human capital, research and development expenditures and

investment in public infrastructure. While emphasizing a broader view of investment,

this literature remains in the neoclassical tradition where benefits of investment are

internal in the form of enhanced productivity or higher wages.

New growth theory moves away from the neoclassical model and explores

alternate productivity channels through which investment affects growth. This school

attaches greater significance to certain types of investment that create externalities

and generate an additional productivity boost through production spillovers or the

associated diffusion of technology. Thus, both models share similarities concerning

18

the central importance of investment and capital accumulation to economic growth,

but differences between these models have important implications for the impact of

investment on productivity and economic growth. The empirical literature also shows

this duality.

Some researchers have extended the neoclassical model by incorporating a

broader concept of investment and by improving the measures of investment and

capital accumulation used in the empirical research, for example, Jorgenson and

Stiroh (2000), Oliner and Sichel (2000) and Jorgenson (2004) among others.

According to recent estimates, asset accumulation and labor growth now explain more

than 80 percent of economic growth, with the accumulation in tangible assets the most

important factor. Jorgenson (2004) found that “investment in tangible assets is the

most important source of economic growth in the G7 nations. The contribution of

capital input exceeds that of productivity for all countries for all periods.”

Other researchers have concentrated on elements of new growth theory to try

to explain technological progress, productivity and long-term economic growth. There

are three branches of new growth theory that emphasize different drivers of long-term

productivity and economic growth: machinery and equipment, human capital, and

research and development. Some propose hybrid models whereby two or more of

these drivers are needed to boost productivity.

The empirical research has found a strong link between investment in general

and machinery and equipment investment in particular with economic growth—De

Long and Summers (1991, 1992, 1993 and 1994), De Long (1991), McGrattan

(1998), Sala-i-Martin (1997), Hoover and Perez (2004), and Abdi (2004) among

others. These results are suggestive that machinery and equipment investment has a

central role to play in long-term economic growth, possibly because technological

change is embodied in recent vintages of capital. De Long and Summers examines in

Equipment Investment and Economic Growth using disaggregated data to examine

the association between different components of investment and economic growth

over 1960–85. They find that producers’ machinery and equipment has a very strong

association with growth: in their cross section of nations each percent of GDP

invested in equipment raises GDP growth rate by 1/3 of a percentage point per year.

This is a much stronger association than can be found between any of the other

components. This association is interpreted as revealing that the marginal product of

19

equipment is about 30 percent per year. The cross nation pattern of equipment prices,

quantities, and growth is consistent with the belief that countries with rapid growth

have favorable supply conditions for machinery and equipment. De Long (1991)

replicated the analysis for industrialized nations for a period in excess of 100 years—

1870 to 1979—and found similar results, with a one percentage point rise in M&E

investment share leading to a 0.7 percentage point rise in GDP per capita.

A number of studies use Canadian data as part of their cross country analysis,

which generally support the findings of De Long and Summers (1991) showed that

there is a strong relationship between M&E investment, economic and total factor

productivity growth. He used panel data on 20 Canadian manufacturing industries

over the period from 1961 to 1997, and time series data from 1961 to 2000 for the

entire manufacturing sector in his analysis. He found the elasticity of output with

respect to M&E capital stock of 0.67, and non-M&E capital stock of 0.24, both of

which are well above their share of national income. This suggests that M&E and

non-M&E investment could be complements, and not substitutes. It was also found

that both M&E and non-M&E investment positively affect TFP levels. A doubling of

M&E investment could raise TFP levels by about 20 percent and doubling non-M&E

investment could raise TFP levels by almost 23 percent.

Most other researchers that examined Canada did not differentiate between

M&E and non-M&E investment, but their results seem to support the view that there

are positive spillovers from investment onto productivity and growth. Li (2002) finds

that the aggregate physical capital investment rate is positive, with a 1 percent rise in

the investment rate leading to a 0.2 percent rise in long-term growth, but the results

are not particularly robust. Sargent and James (1997) estimated the effect of physical

capital on output growth in Canada over the period from 1947 to 1995. They found

estimates for the elasticity of output with respect to capital were in the range 0.61–

0.88, which is well above capital’s share of national income. Therefore, economic

research has found that business investment and the accumulation of physical capital

is a significant source of economic and labor productivity growth over the medium

term in the neo-classical tradition. And machinery and equipment investment has been

found to be directly or indirectly associated with the key drivers of knowledge in the

economy as advocated by new growth theories and by the evidence.

20

2.5 Education and Economic Growth

On education and growth, numerous empirical studies have investigated the

link between education and growth and/or productivity. Islam (2010) using a panel

data set of 87 sample countries over the period of 1970 to 2004 shows that the effect

of skilled human capital on growth increases as the distance to the technology frontier

narrows, but this is true only for high- and medium-income countries. They also show

that a larger stock of old workers with tertiary education yields higher growth for

high- and medium-income countries, while young workers with secondary education

do for low-income countries. Ha, Kim and Lee (2009) also provide empirical

evidence, using panel data covering 1989–2000 from Japan; the Republic of Korea;

and Taipei, China; as the distance to the technology frontier narrows, basic research

and development (R&D) investment in highly skilled labor shows the higher growth

effect than development R&D investment in less skilled labor. They also provide

evidence that the quality of tertiary education has a significantly positive effect on the

productivity of R&D.

Barro’s Education and Economic Growth concludes that growth is positively

related to the starting level of average years of school attainment of adult males at the

secondary and higher levels. Since workers with this educational background would

be complementary with new technologies, the results suggest an important role for the

diffusion of technology in the development process. Growth is insignificantly related

to years of school attainment of females at the secondary and higher levels. This result

suggests that highly educated women are not well utilized in the labor markets of

many countries. Growth is insignificantly related to male schooling at the primary

level. However, this level of schooling is a prerequisite for secondary schooling and

would, therefore, affect growth through this channel. Education of women at the

primary level stimulates economic growth indirectly by inducing a lower fertility rate.

Data on students’ scores on internationally comparable examinations in science,

mathematics, and reading were used to measure the quality of schooling. Scores on

science tests have a particularly strong positive relation with economic growth. Given

the quality of education, as represented by the test scores, the quantity of schooling —

21

measured by average years of attainment of adult males at the secondary and higher

levels— is still positively related to subsequent growth.

On the other hand, there are some studies find that education does not

contribute to growth. Pritchett (1996)’s where has all the education gone? shows that

cross-national data on economic growth rates show that increases in educational

capital resulting from improvements in the educational attainment of the labor force

have had no positive impact on the growth rate of output per worker. After

establishing that this negative result about the education-growth linkage is robust,

credible, and consistent with previous literature, Pritchett explores three possible

explanations that reconcile the abundant evidence about wage gains from schooling

for individuals with the lack of schooling impact on aggregate growth: 1) that

schooling creates no human capital. Schooling may not actually raise cognitive skills

or productivity but schooling may nevertheless raise the private wage because to

employers it signals a positive characteristic like ambition or innate ability 2) that the

marginal returns to education are falling rapidly where demand for educated labor is

stagnant. Expanding the supply of educated labor where there is stagnant demand for

it causes the rate of return to education to fall rapidly, particularly where the sluggish

demand is due to limited adoption of innovations. 3) that the institutional

environments in many countries have been sufficiently perverse that the human

capital accumulated has been applied to activities that served to reduce economic

growth. In other words, possibly education does raise productivity, and there is

demand for this more productive educated labor, but demand for educated labor

comes from individually remunerative but socially wasteful or counterproductive

activities - a bloated bureaucracy, for example, or overmanned state enterprises in

countries where the government is the employer of last resort - so that while

individuals' wages go up with education, output stagnates, or even falls.

Jess Benhabib and Mark M. Spiegel’s (1994) The role of human capital in

economic development evidence from aggregate cross-country data uses cross-

country estimates of physical and human capital stocks by running growth accounting

regressions implied by a Cobb-Douglas aggregate production function. Their results

indicate that human capital enters insignificantly in explaining per capita growth rates.

However, they next specify an alternative model in which the growth rate of total

22

factor productivity depends on a nation's human capital stock level. Tests of this

specification do indicate a positive role for human capital.

2.6 Population and Economic Growth

Economists have been the main contributors to the rich literature on the

relation between this rapid population growth and the development process itself.

The assumption that rapid population growth slowed development prevailed in the

1950s and 1960s- when the emphasis in the economic development literature was on

lack of physical capital and surplus labor in agriculture as the major impediments to

economic growth. In early one-sector neoclassical growth models and in the dualistic

models with an agricultural and an urban sector, population growth was treated as

exogenous. A higher rate of population and thus labor force growth implied a lower

rate of capital formation per worker and slower absorption of surplus agricultural

labor into the high productivity urban sector, resulting in lower per capita

consumption. Later models by Coale and Hoover (1958) emphasized the possible

negative effects of rapid population growth on savings and thus on physical capital

formation.

By the 1970s, with attention shifting to the efficiency with which capital and

other factors of production are used, and to the role of the state in creating an

environment encouraging (or discouraging) efficiency, challenges arose to the then

conventional view that the apparent abundance of labor in poor countries compared

with capital and land was a factor inhibiting growth and development. Optimists

about the effects of population growth began emphasizing and modeling several

reasons why rapid population growth might actually encourage economic growth:

economies of scale in production and consumption such as Glover and Simon (1975);

technological innovation induced by population pressure by Boserup (1965, 1981);

and the likelihood that with more births there will be more great minds to produce

new ideas and show human ingenuity by Simon (1981).

Critical overviews by the World Bank (1984) and National Research Council

of the National Academy of Sciences (1986) conclude that rapid population growth

can slow development, but only under specific circumstances and generally with

23

limited or weak effects. In these assessments, the population problem, to the extent it

exists, is seen not at all as one of global food scarcity or other natural resource

scarcities. These reviews emphasize that rapid population growth is only one among

several factors that may slow development, and see rapid population growth as

exacerbating (rather than causing) development problems caused fundamentally by

other factors, especially government-induced market distortions (such as subsidies to

capital that discourage labor-intensive production). Reflecting the influence of the

microeconomic literature on the determinants of fertility, these "revisionist" assessments

emphasize population change as the aggregate outcome of many individual decisions

at the micro or family level, and thus as only one aspect of a larger complex system.

The micro or family-level decisions are made in response to signals provided by the

larger system. Under the Smithian logic of an invisible hand, these family decisions

should be presumed to maximize not only individual welfare, but also social welfare,

unless there are clear market failures. Among revisionists, differences in the

quantitative importance of the negative effects of rapid population growth depend on

differences in views on the pervasiveness and relevance of market failures, with for

example the World Bank (1984) and Demeny (1986) emphasizing market (and

institutional) failures, and the National Research Council of the National Academy of

Sciences (1986) emphasizing the ability of the market and institutions to adjust.

The revisionist emphasis on micro-level decisions leads to two related ideas

regarding the consequences of population growth for development. First, rapid

population growth is not a primary impediment to economic development, but under

certain conditions interacts with and exacerbates the effects of failings in economic

and social policy. Second, the negative effects of rapid population growth are likely to

be mitigated, especially in the long run, by family and societal adjustments; indeed,

insofar as families choose to have many children, certain short-term adjustments, for

example a decline in family consumption per capita, are not necessarily a sign of

welfare loss. Revisionists thus refuse to admit to any generalization; the effects of

population growth vary by time, place and circumstance, and must be studied

empirically. Mainstream debate is now likely to center on the quantitative importance

of rapid population growth in particular settings over particular time periods

(historical as well as current)- whether any negative effects are minimal, and in any

24

event so interlinked with more central problems such as poor macroeconomic policies

or weak political institutions as to hardly merit specific attention; or are large enough

to warrant some kind of policy intervention to reduce fertility.

The issue warrants new empirical research for economies with two

characteristics: in which there is some likelihood that the social costs of high fertility

exceed the private costs, as signaled, for example, by societal and parental difficulties

in educating children (e.g. in Bangladesh and in parts of sub-Saharan Africa, where

population growth rates remain high and per capita income is low); and in economies

in which particular market failures, such as lack of property rights or policy induced

market distortions that discourage labor-using technology, are likely to heighten any

negative effect of rapid population growth.

Recent work by Barro (1997) indicates that economic growth is significantly

negatively related to the total fertility rate. Thus, the choice to have more children per

adult — and, hence, in the long run, to have a higher rate of population growth —

comes at the expense of growth in output per person. It should be emphasized that this

relation applies when variables such as per capita GDP and education are held

constant. These variables are themselves substantially negatively related to the

fertility rate. Thus, the estimated coefficient on the fertility variable likely isolates

differing underlying preferences across countries on family size, rather than effects

related to the level of economic development.

2.7 Economic Growth in the Asian Context

Overall, in the application of growth theory to Asia, several determining

factors have been cited as potential explanations for growth. While Asia’s economic

growth had been considered a “miracle” in the 1990s (World Bank 1993, Lucas

1993), a number of empirical studies have been done to explain the determinants.

They highlight the role of investment, human resources, fertility, and institutional and

policy variables. For example, Radelet, Sachs and Lee (2001) find that East Asia’s

rapid growth was due to its 1) large potential for catching up; 2) favorable geography

and structural characteristics; 3) demographic dividend; and 4) economic policies and

strategy that were conducive to growth. The empirical studies show that the role of

25

economic policies, particularly those relating to openness, played a highly significant

role in the region’s sustained growth.

Lawrence J. Lau and P.A. Yotopoulos’s (1989) The Sources of East Asian

Economic Growth Revisited (2003) uses the extended meta-production function

approach pooling time-series aggregate data across economies to examine and

compare the characteristics of economic growth of different groups of developed and

developing economies in East Asia. The rapid accumulation of tangible inputs, in

particular, tangible capital, is identified as the major source of growth in the post-war

period for the East Asian developing economies. Furthermore, the finding of positive

measured technical progress for the East Asian developing economies in the more

recent sub-period of 1986-1995 is also suggestive of the role played by investment in

intangible capital at different stages of economic development. Different types of

measured inputs play different roles at different stages of economic growth. The study

provides support for the view that tangible capital accumulation is the most important

source of growth in the early stages of economic development. However, it states that

mere accumulation of tangible capital however is not sufficient for rapid economic

growth--efficient allocation of tangible capital is necessary to achieve it. The major

achievement of the East Asian NIEs in the postwar period is the efficient

accumulation of tangible capital. As it is observed, over time, the East Asian NIEs

have been becoming more like Japan, and Japan has been becoming more like the

non-Asian developed economies, in terms of the sources of their economic growth

(growth from intangible capital- or technical progress- based).

Ari Aisen’s (2007) Growth Determinants in Low-income and Emerging Asia:

a Comparative Analysis investigates the determinants of economic growth in low-

income countries in Asia. Estimates from standard growth regressions using data for

Emerging Asia for the period 1970-2000 indicate that a higher investment-to-GDP

ratio, trade openness, primary school enrolment and rule of law all positively affect

growth. Conversely, a higher government expenditure-to-GDP ratio is associated

with lower growth in Asia.

CHAPTER 3

THEORETICAL MODEL AND METHODOLOGY

Based on the model from Barro and Sala-i-Martin (1992), there are n

producers, each producing output (y) according to the Cobb-Douglas production

function:

gAky 1 (1)

where k represents private capital and g is a publicly provided input. The

government balances its budget in each period by raising a proportional tax on output

at rate and lump-sum taxes of L. The government budget constraint is therefore

nyLCng (2)

where C represents government-provided consumption (‘non-productive’)

goods. The lump-sum (or non-distortionary) taxes do not affect the private sector’s

incentive to invest in the input good, whereas the taxes on output distorts behavior of

both producers and consumers. With the isoelastic utility function, Barro and Sala-i-

Martin (1992) show that the long-run growth rate in this model ( ) can be expressed

as:

)1/()1/(1 )/()1)(1( ygA (3)

Where and are constants that reflect parameters in the utility function.

Equation (3) shows that the growth rate is decreasing in the rate of distortionary tax

( ) , increasing in government productive expenditure (g), but is unaffected by non-

distortionary taxes (L) or non-productive expenditure (C).

27

This is the model that this study seeks to test. In practice, one must take into

account of the fact that the government budget is not balanced in every period, so the

constraint becomes

nyLbCng (4)

where b is the budget surplus. The predicted signs for these components in a

growth regression would be: g - positive; - negative. C , L and b would have no

influence on long-run growth provided that Ricardian equivalence holds and that the

composition of expenditure and taxation remains unchanged.

Moreover, non-fiscal variables that are deemed important to determining

growth should also be included into the model. These non-fiscal variables used in the

model are: 1) Domestic investment to GDP 2) Labor force growth 3) Export-import to

GDP (proxy for trade openness) and 4) School enrollment ratio (proxy for human

capital).

To see the implications of this empirical testing, suppose that growth, , at

time t is a function of conditioning (non-fiscal) variables, itY , and the fiscal variables

from equation (4), itX :

m

jtjtjit

k

iit uXY

11

(5)

Methodology

The theoretical model requires the classification of expenditures into

productive and non-productive and of taxation into distortionary and non-

distortionary. The data used in this study cover fiscal data from ASEAN5+3

countries (namely China, Japan, South Korea, Thailand, Singapore, Indonesia,

Malaysia, and the Philippines) from the period ranging from 1979-2008. The

information is obtained from various sources such as government database, IMF-

Government Finance Statistics and CEIC. The author has to assimilate these primary

28

data into the theoretical classification to be tested in the empirical investigation

(details are elaborated in Section IV Data Description and Analysis).

The regression uses the two-way fixed-effects model (or Least Square Dummy

Variable - LSDV) with time and country specific intercepts, and follows the form of

equation 5) Fixed-effect model would assist in controlling for unobserved heterogeneity

when this heterogeneity is constant over time and correlated with independent

variables. In differentiating between fixed effect model versus the random effect

model, there are two common assumptions made about the individual specific effect,

the random effects assumption and the fixed effects assumption. The random effects

assumption (made in a random effects model) is that the individual specific effects are

uncorrelated with the independent variables. The fixed effect assumption is that the

individual specific effect is correlated with the independent variables. If the random

effects assumption holds, the random effects model is more efficient than the fixed

effects model. However, if this assumption does not hold (i.e., if the Durbin–Wu test

fails), the random effects model is not consistent.

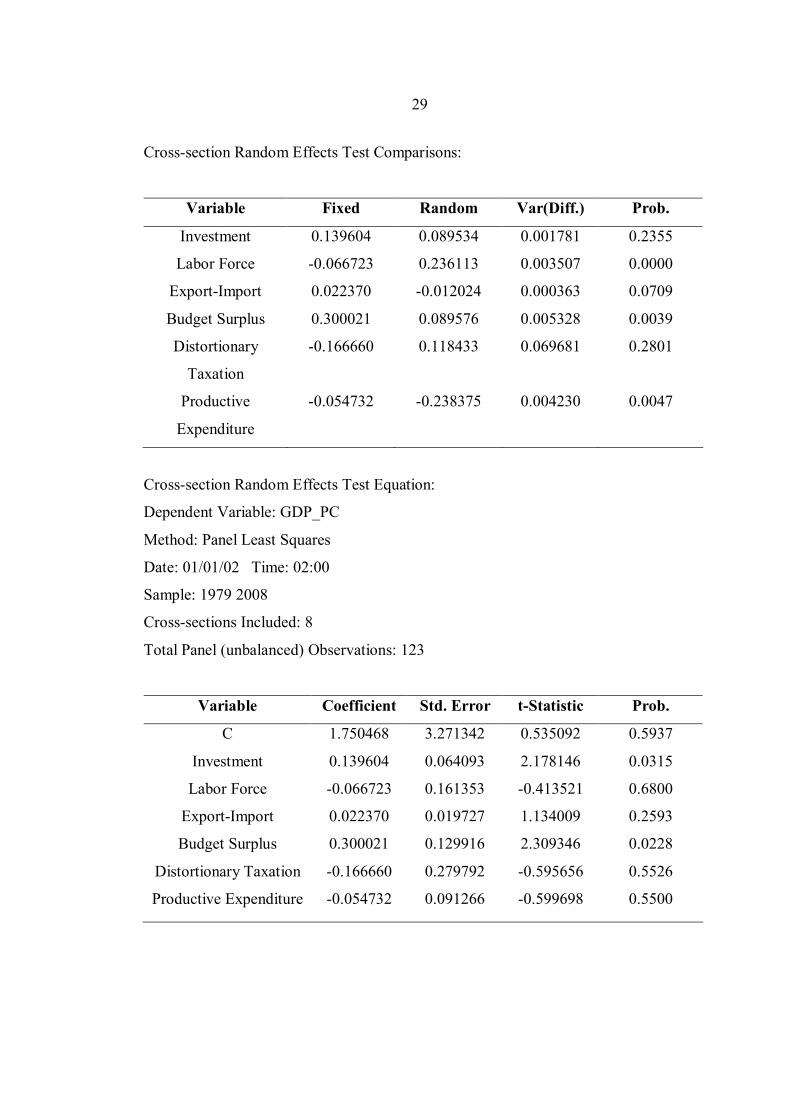

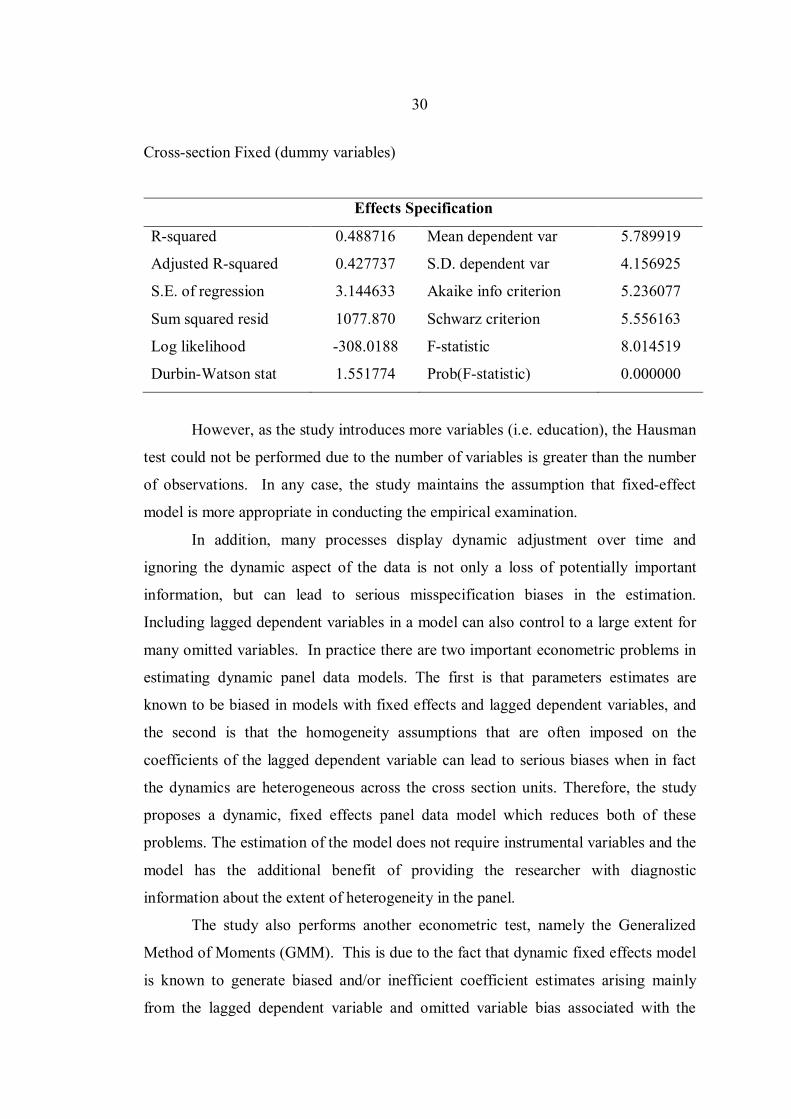

In determining whether to use the fixed effect or random effect model, the

study performs the Hausman Test with the major interested variables (Investment

ratio to GDP, Labor force growth, Export-import ratio to GDP, distortioary taxation,

productive expenditure) and determines that the fixed effect model is the appropriate

model for this empirical study as follows:

Correlated Random Effects - Hausman Test

Equation: EQ01

Test Cross-section Random Effects

Test Summary Chi-Sq.

Statistic

Chi-Sq. d.f.

Prob.

Cross-section random 60.805807 6 0.0000

29

Cross-section Random Effects Test Comparisons:

Variable Fixed Random Var(Diff.) Prob.

Investment 0.139604 0.089534 0.001781 0.2355

Labor Force -0.066723 0.236113 0.003507 0.0000

Export-Import 0.022370 -0.012024 0.000363 0.0709

Budget Surplus 0.300021 0.089576 0.005328 0.0039

Distortionary

Taxation

-0.166660 0.118433 0.069681 0.2801

Productive

Expenditure

-0.054732 -0.238375 0.004230 0.0047

Cross-section Random Effects Test Equation:

Dependent Variable: GDP_PC

Method: Panel Least Squares

Date: 01/01/02 Time: 02:00

Sample: 1979 2008

Cross-sections Included: 8

Total Panel (unbalanced) Observations: 123

Variable Coefficient Std. Error t-Statistic Prob.

C 1.750468 3.271342 0.535092 0.5937