the export exe'erience of developing...

TRANSCRIPT

QCPs3I

BAREND A. DE VRIES

THE EXPORT EXE'ERIENCEOF

DEVELOPING CC)UNTRIES

WORLD BANK STAFF OCCASIONAL PAPERS NUMBER THREE

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT

WORLD BANK STAFF OCCASIONAL PAPERS NUMBER THREE

This paper may not be quoted as representing the viewof the Bank and affiliated organizations. They do not accept

responsibility for its accuracy or completeness.

|WBG

BAREND A. DE VRIES

EXPORT EXPERIENCES OFDEVELOPING COUNTRIES

Distributed by The Johns Hopkins PressBaltimore, Maryland

Copyright © 1967by International Bank for Reconstruction and DevelopmentManufactured in the United States of AmericaAll Rights ReservedLibrary of Congress Catalog Card Number 67-28912

FOREWORD

The benefits of research are greater the further they are spread.Because some of the work done within or for the Bank and itsaffiliated organizations may be useful to others who are engagedin the practice of sound economic development, we have decided topublish papers based on this work from time to time. Most of thepapers likely to be published will have an unashamed pragmaticbias, as indeed has the work of the development economist generally.While these papers are published by the Bank, their premises orconclusions are not necessarily accepted by the Bank either in prac-tice or theory; they are entirely the responsibility of the authors.We hope the papers may be a modest stimulus to further research,particularly in the troubled zone where theory meets real life.

November 15, 1967Washington, D.C.

George D. WoodsPresident

International Bank for Reconstruction and Development

v

TABLE OF CONTENTS

Preface ix

I. Introduction 3

II. Framework and Methods of Analysis 9

III. Export Variations 18Variations Relative to the World Market

and Group Averages 23Changes in Structure of Commodity Trade 26Countries Benefiting Most from Rapidly

Expanding Trade 29

IV. Statistical Analysis of Intercountry Differencesin Export Growth 33

V. Domestic Diversification Versus Export Diversification 43

VI. Conclusion 59Statistical Annex 65

TABLES1. Exports from 29 Developing Countries 182. Variations between 1950-53 and

1960-63 in Export Earnings 223. Estimated Variations in Earnings

from Major, Minor, and Total Exports,1960-63 Annual Averages 25

4. Estimated Variations in Minor Exports:Total, Manufactured Goods, and Other Goods 27

vii

5. Countries' Shares in Major ExportCommodity Markets, 1950-53 and 1960-63 28

6. Countries with Increasing Shares in Marketsfor "Buoyant" Major Export Commodities 31

7. Results of Regression Analysis 358. Averages of Trade Position Indices for

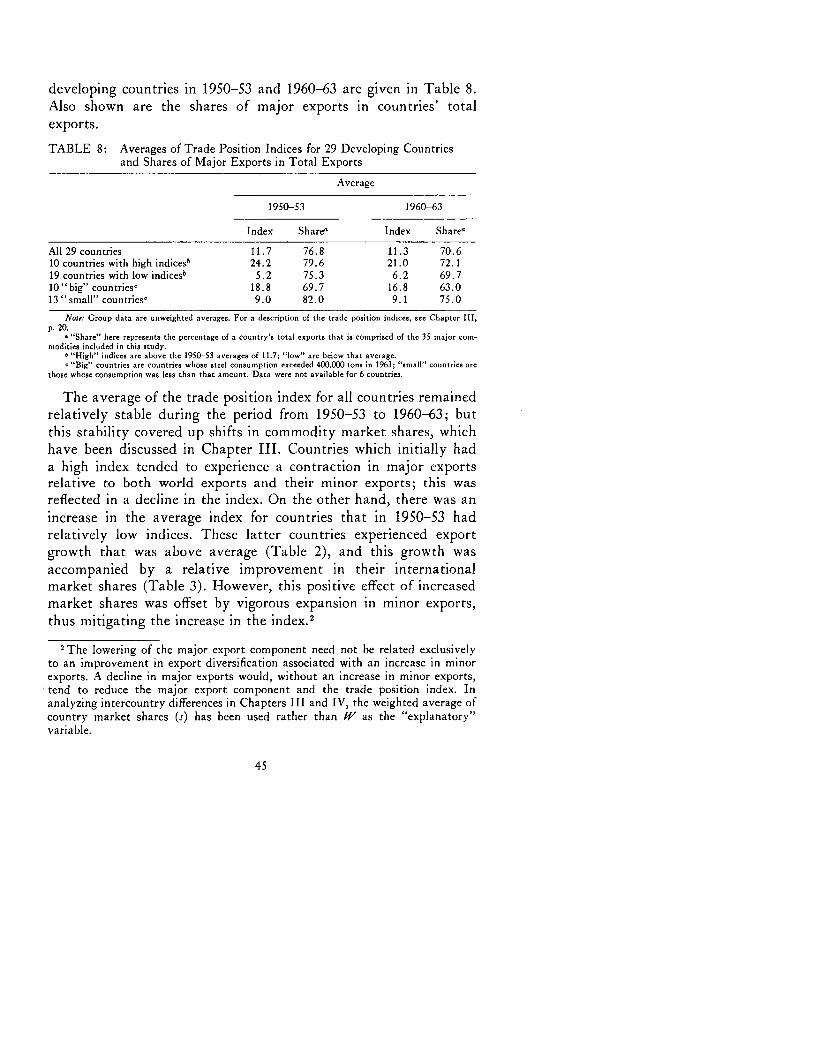

29 Developing Countries and Sharesof Major Exports in Total Exports 45

CHARTS1. Trade Position and Domestic Market Size, 1950-53 482. Trade Position and Domestic Market Size, 1960-63 49

STATISTICAL ANNEX

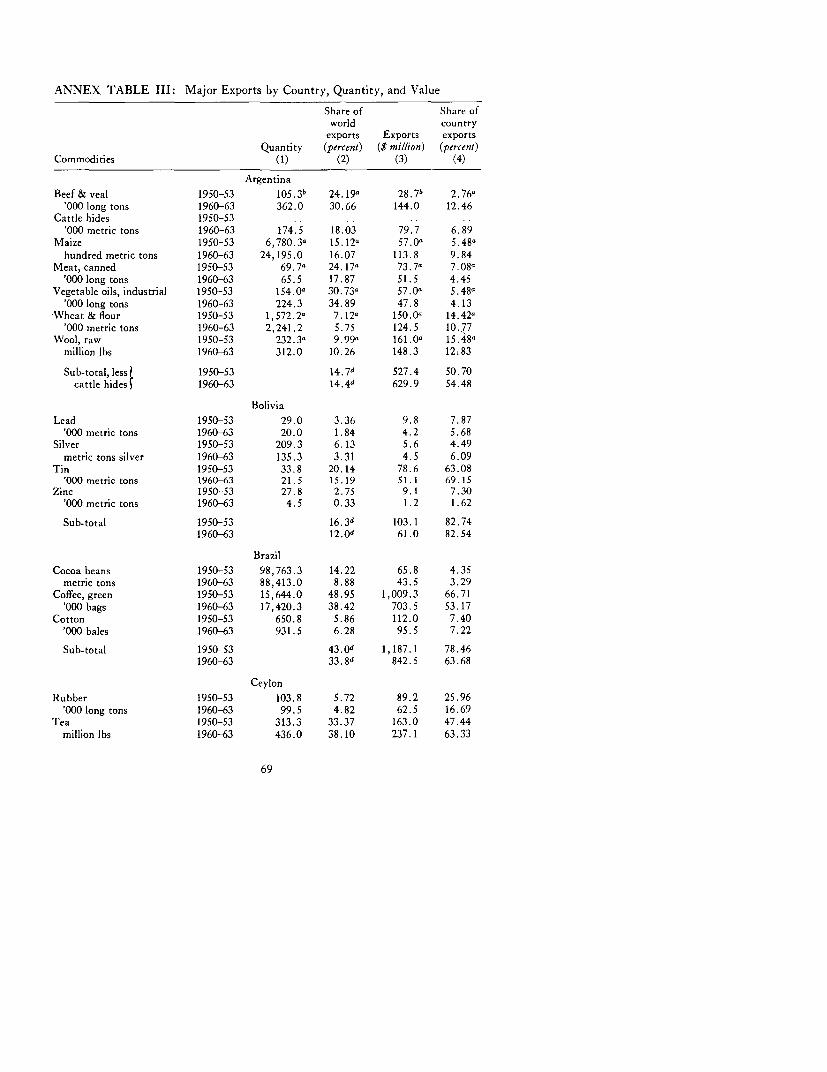

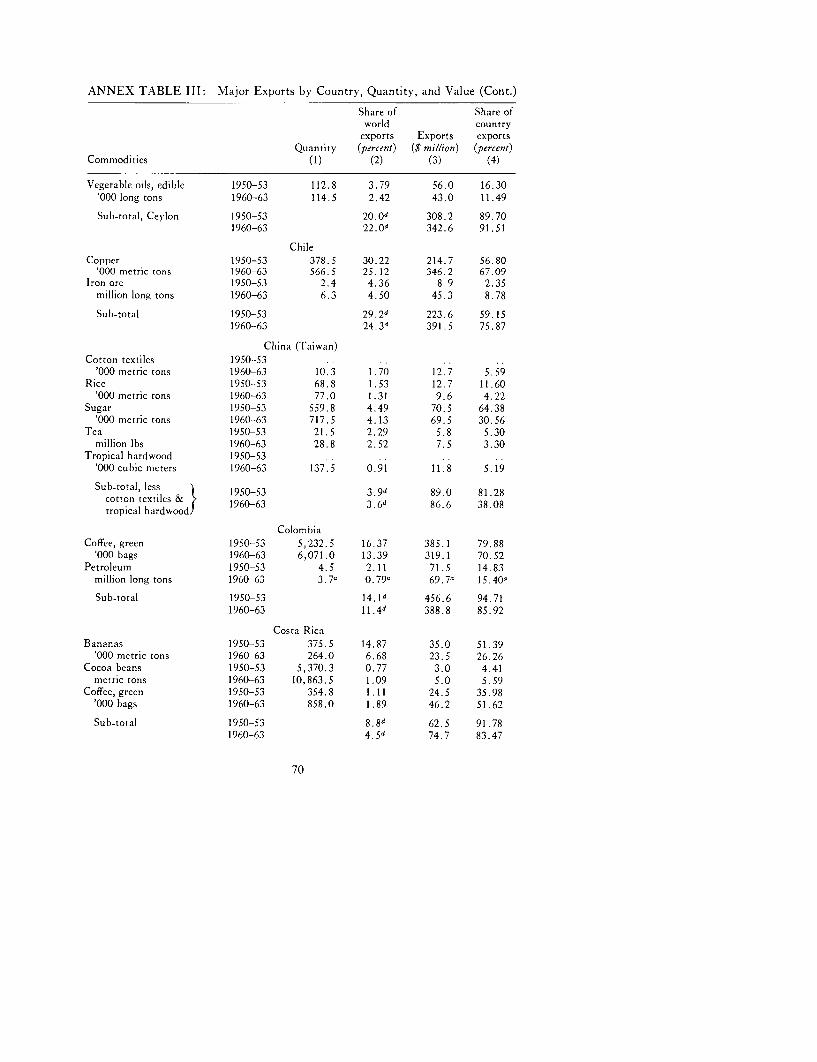

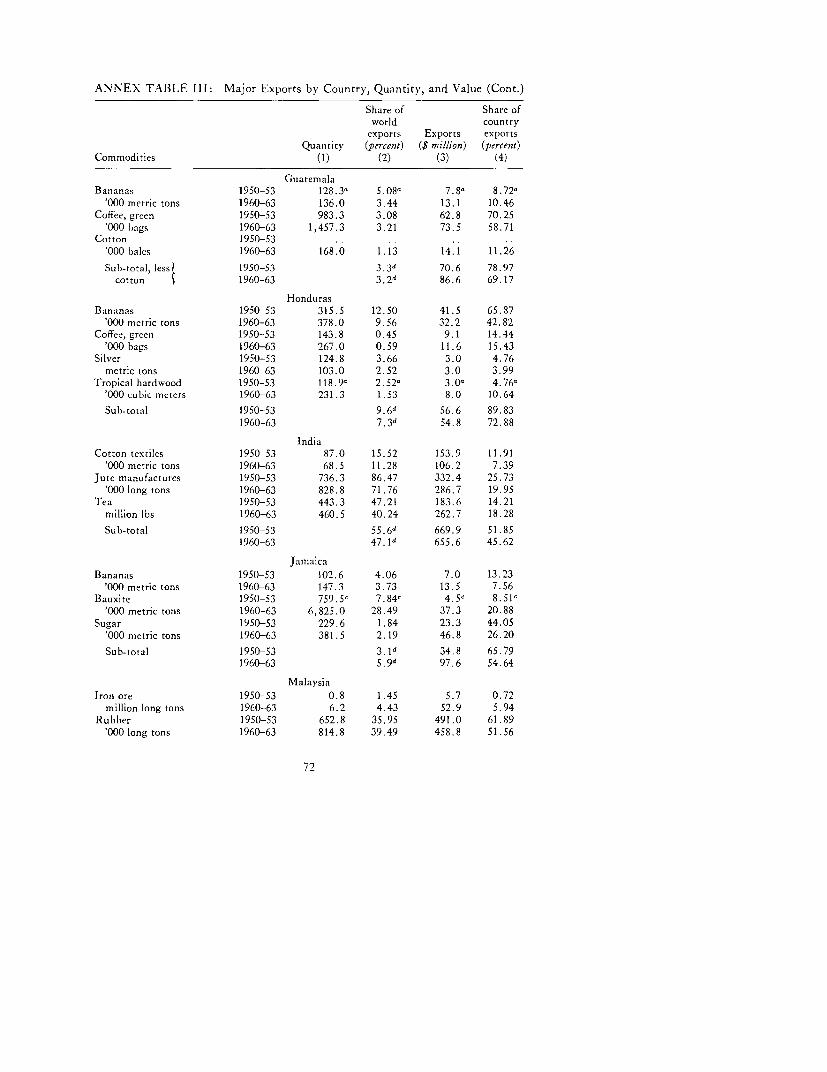

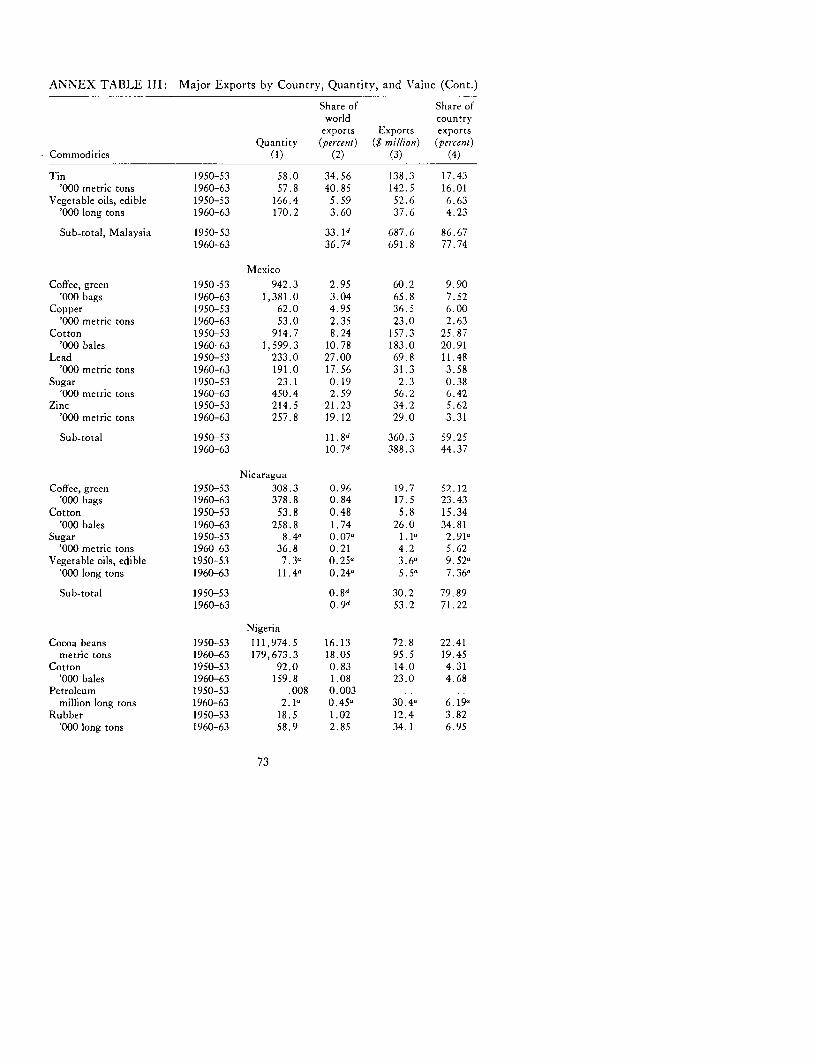

TablesI. Trade Position Index and Average World Market

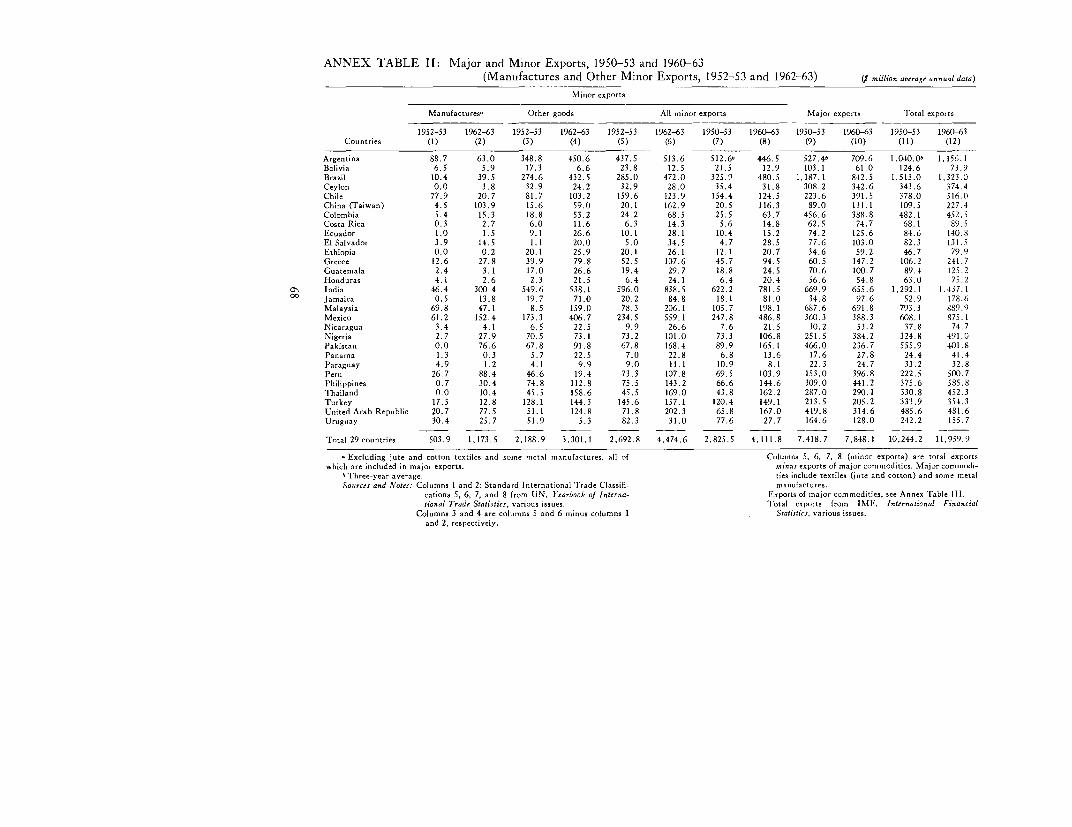

Share, 29 Countries 66II. Major and Minor Exports, 1950-53 and 1960-63 68

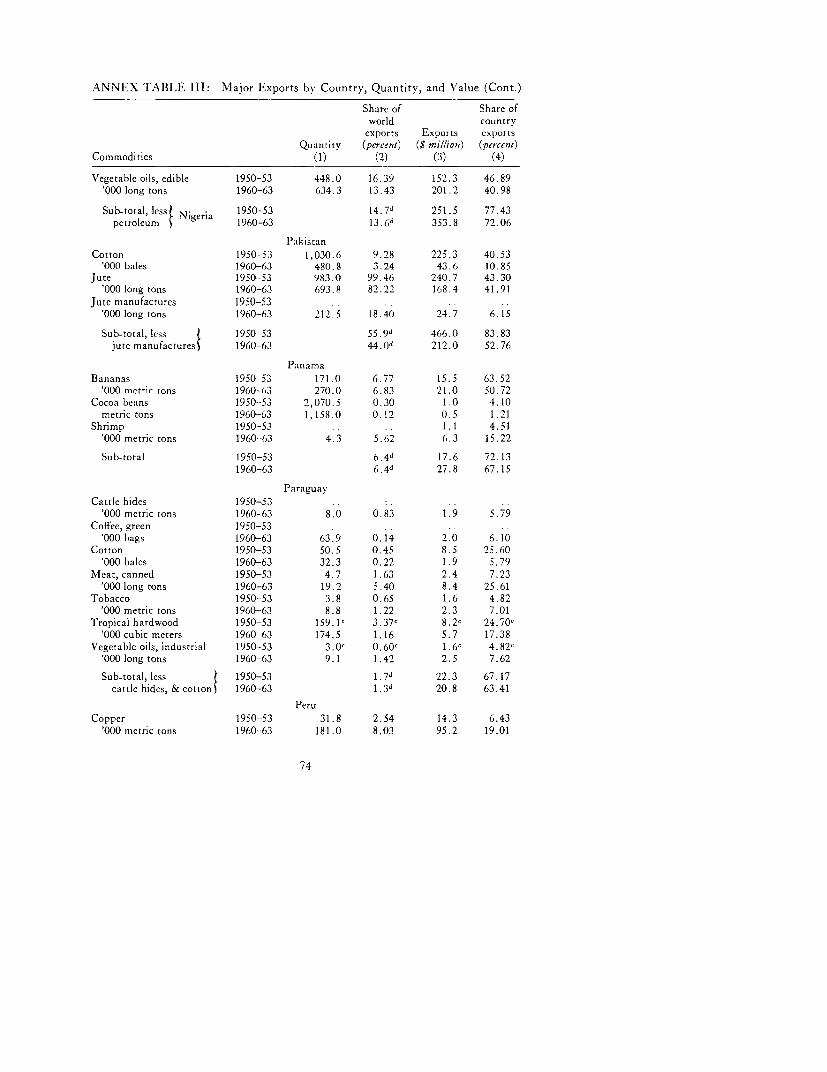

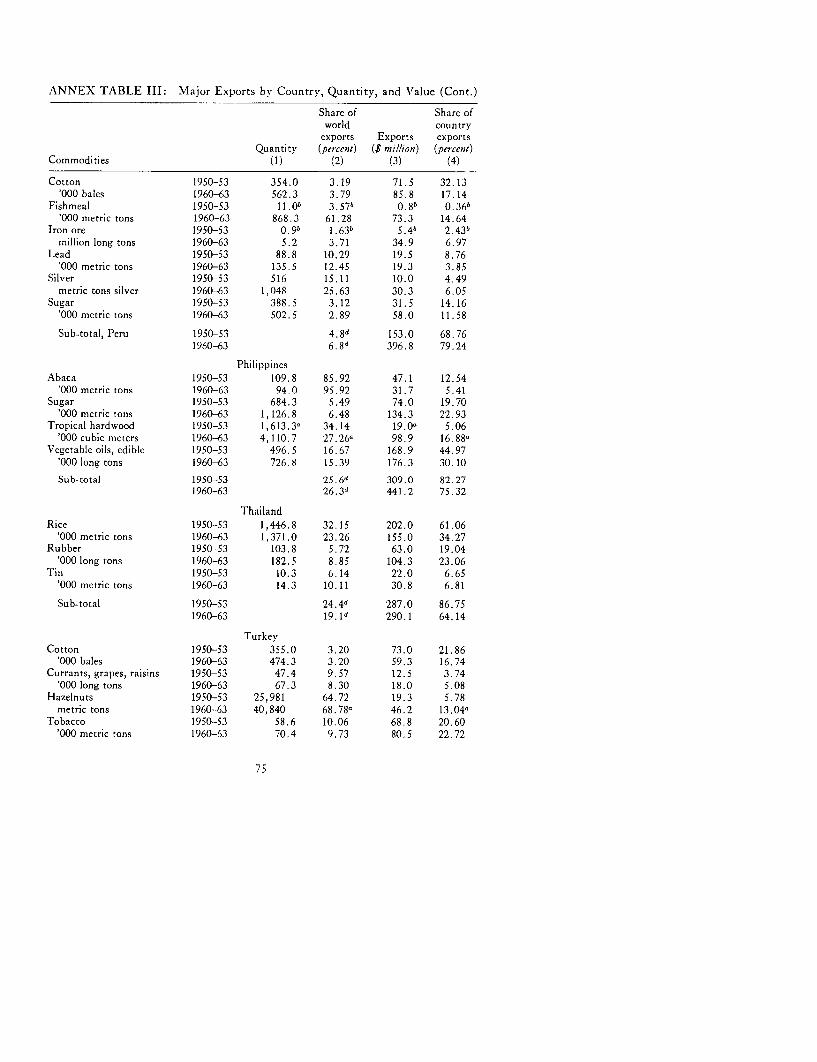

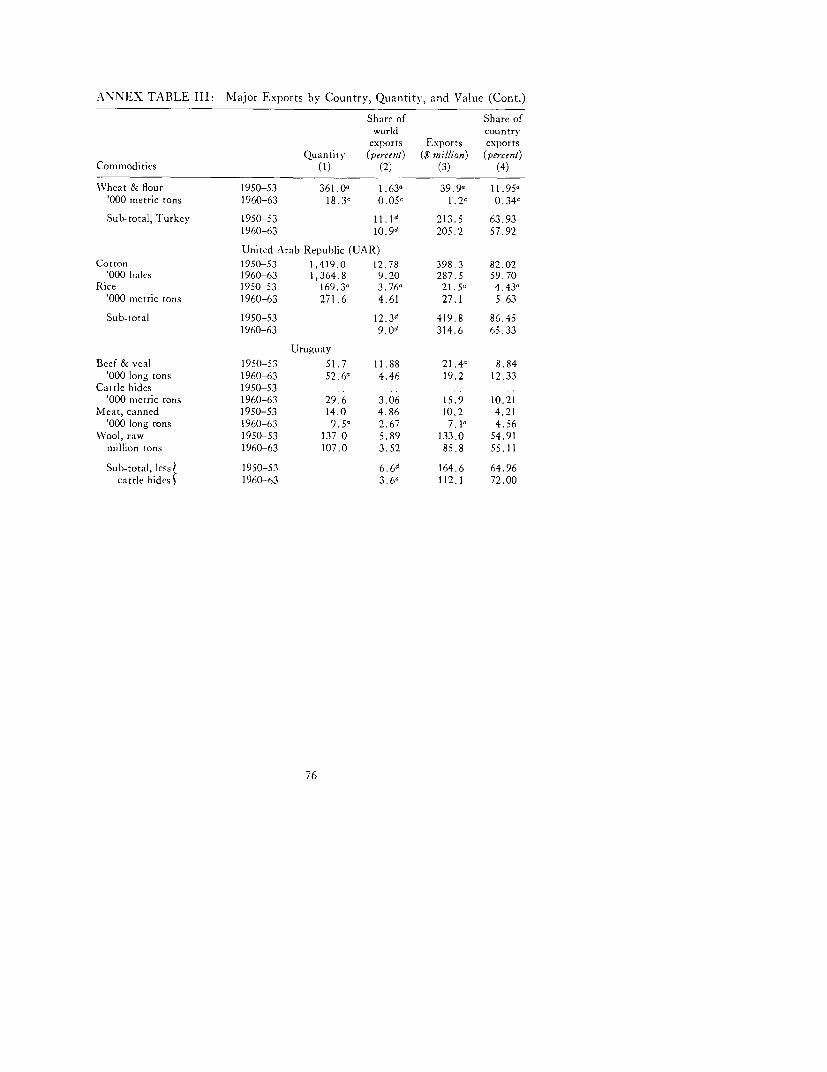

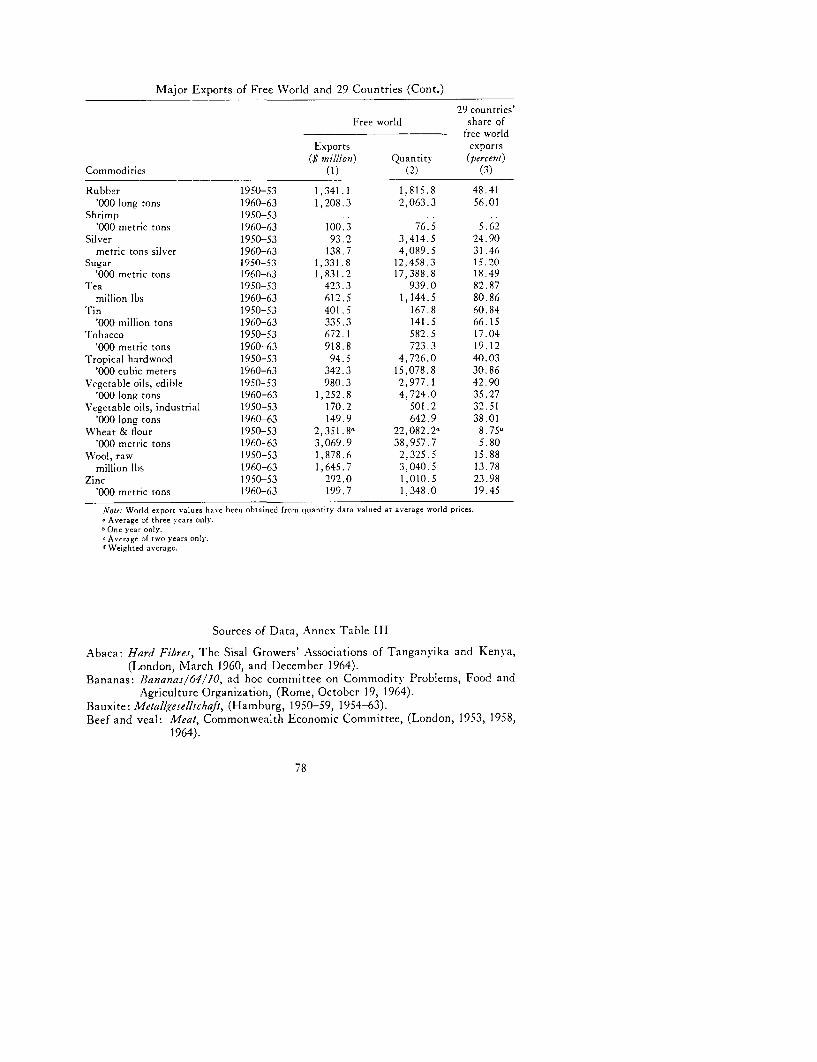

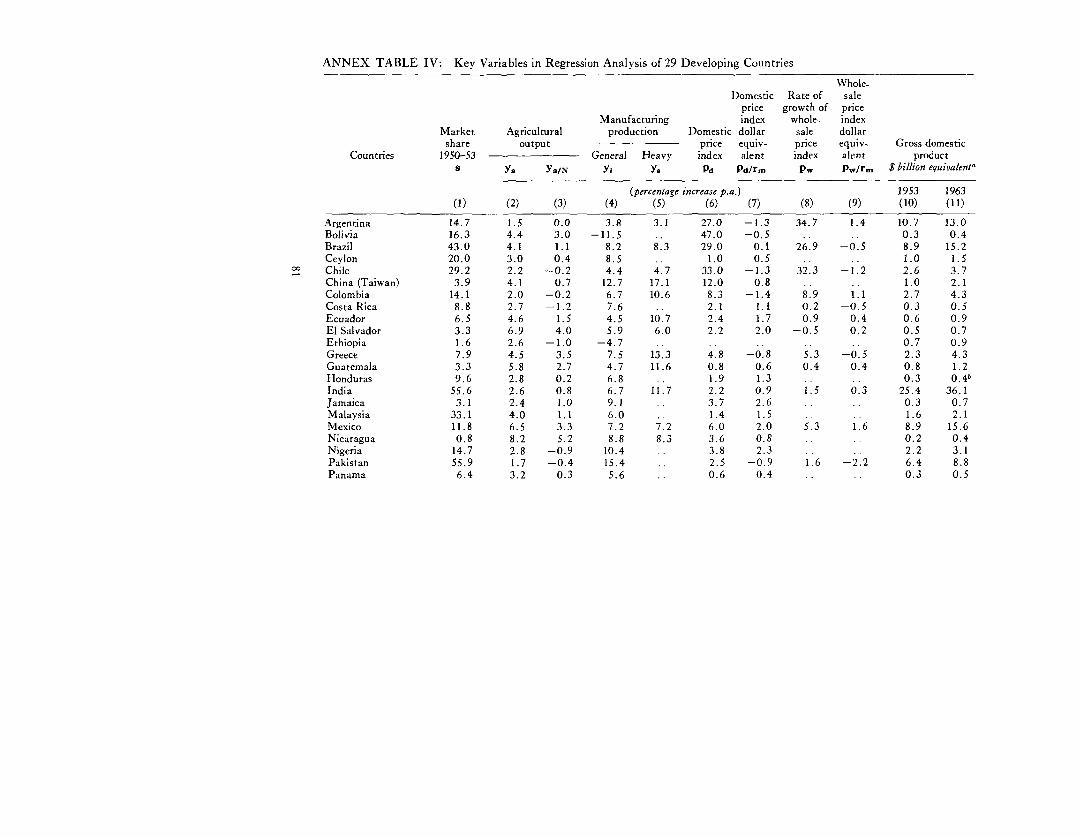

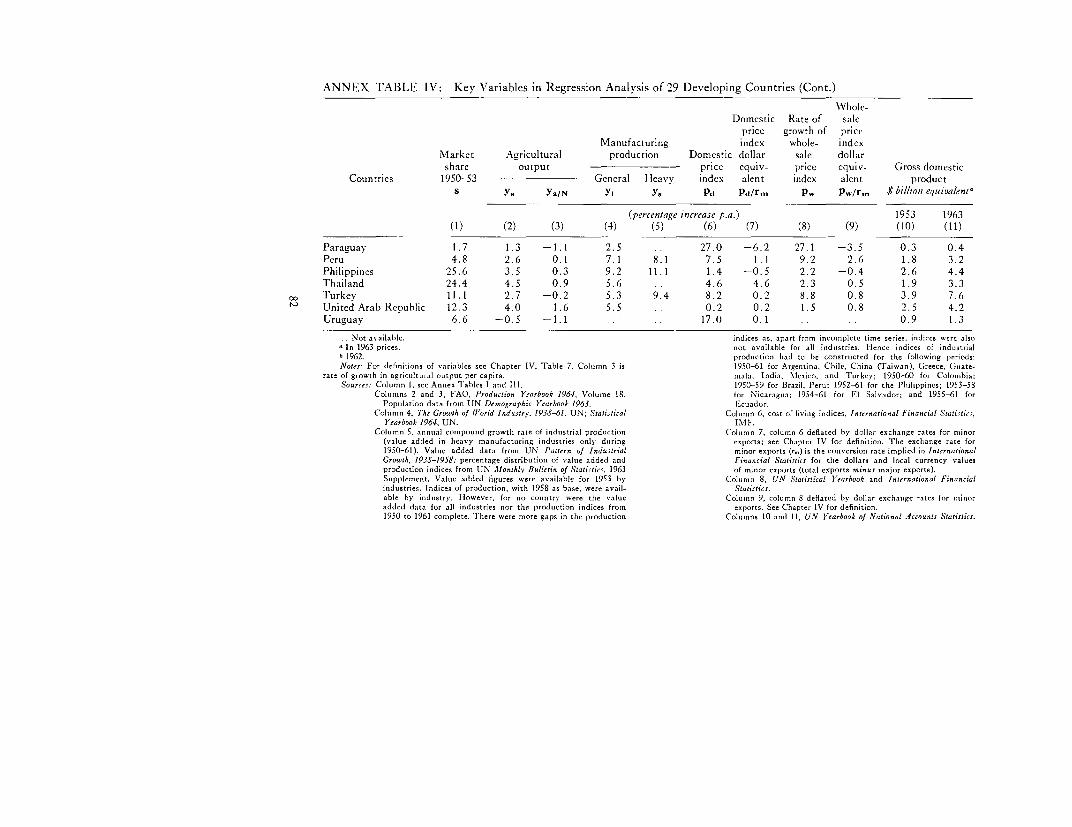

III. Major Exports by Country, Quantity, and Value 69IV. Key Variables in Regression Analysis of

29 Developing Countries 81V. Export Growth Rates, Trade Position Indices, and

Domestic Price Changes 83VI. Grouping of 29 Countries by Characteristics Listed

in Table V 84VII. Consumption and Production of Crude Steel, 1963 85

VIII. Alternative Estimates of Variations inMinor Exports, 1960-63 86

Definitions:Dollars ($) are U.S. dollar equivalents, converted at current par

values.A billion is one thousand million.Averages are mean averages except where otherwise stated.

Notations:. not available-nil or negligible

viii

PREFACE

The World Bank is giving increasing attention to the economicperformance of developing countries, and to the policies which makefor the best utilization of scarce capital resources and for a soundpace and pattern of development. This study deals with a crucialaspect of economic performance-the growth and diversification ofexports and the relation between the export experience of variouscountries and their development policies.

The work originated in a desire to give empirical underpinningto the view that economic development strategy for small countrieshas often been quite different from that of big countries and thatthere may be some good reasons for these differences. The centraltheme became concerned with intercountry variations in the growthof exports since these are often a key element in the differences ingrowth patterns and strategies.

The author has had the benefit of comments on an earlier draftfrom several economists outside the Bank-particularly Harry G.Johnson and Michael Michaely-and from numerous colleagues,including John Adler, Attila Karaosmanoglu, and especially BelaBalassa and Gertrud Lovasy. Messrs. Alfred Conrad, ArabindaKundu, and J. C. Liu have collaborated in the regression analysis.Mrs. Feil, Miss Ryan, Mrs. Curcio, and Mr. Rangachar have alsoprovided assistance in various stages of the study.

November 15, 1967 Andrew M. KamarckDirector

Economics Department

ix

Editorial Commnittee

Barend J. de Vries, chairman

Bernard R. Bell Samuel LipkowitzManfred G. Blobel K. S. KrishnaswamyVinod Dubey K. N. RajHugh Latimer, editor C. H. Thompson

x

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT

WORLD BANK STAFF OCCASIONAL PAPERS NUMBER THREE

INTRODUCTION

The problems that developing countries face in expanding theirexports have been discussed intensively during the past two decades.The characteristics of demand and of supply of individual commodi-ties have been studied in great detail, and attention has been focusedon crucial policy issues. Among the many aspects that have beencovered are the slow growth of world demand for a large number ofcommodities which bulk large in exports of developing countries,the fluctuations in the volume of trade and in prices on importantcommodity markets, and the measures which might be taken todampen these fluctuations or to insulate or insure individualcountries against them. Currently, much analysis and debate con-cerns the measures which the industrial countries might take toincrease imports from the developing countries. In an arena whichis both economic and political, a considerable amount remains to bedone to formulate concrete measures for stabilizing commodityexports, to estimate the cost of such stabilization (and tacklerelated questions of differences in production costs among developingcountries), and to spell out in detail the actions and policies whichdeveloping countries might adopt to achieve a greater diversificationof exports.

3

Most of the discussions on commodity problems are concernedwith the total problem as it affects all developing countries, andwith the policy measures to be considered by the internationalcommunity or by such broad subgroups as the developing countriesand the industrial countries. By their very nature, the discussionsdo not deal with intercountry differences in the growth of exportsexcept in direct relation to exports of individual commodities. Yetthese differences have been very marked, ranging from absolutedeclines in export earnings to substantial increases over the past10-15 years. They are of central concern in the analysis and dis-cussion of what has come to be called development performance anddevelopment finance: the measurement of various elements of growthof poor countries, and the policies and financing needed to accelerateand sustain such growth. The present study analyzes the dimensionsof the differences and attempts to relate them to certain crucialcharacteristics of export supply and resource allocation policies indeveloping countries. In contrast to this study, which focuses onthe exports of the developing countries, the majority of studies madethus far of the problem analyzed here have concentrated on theexports of industrial countries.'

Variations in the growth of exports can, in part, be related to thedifferences in the growth of major consuming markets and todifferential access to these markets under preference arrangements(European Economic Community or Commonwealth) or to special

' See especially Helen B. Junz and Rudolf R. Rhomberg, "Prices and ExportPerformance of Industrial Countries, 1953-63," Staff Papers, International Mone-tary Fund, (July 1965) and the references quoted by them. Studies of variousaspects of the export performance of developing countries, and to which specificreference will be made in subsequent chapters, include Alfred Maizels, IndustrialGrowth and World Trade, (Cambridge, England, 1963), Chapter 5, and "Exportsand Economic Growth in the Overseas Sterling Area, 1960-61 to 1975," NationalInstitute Economic Review, (London, November 1966); Gertrud Lovasy, "Inflationand Exports in Primary Producing Countries," Staff Papers, IMF, (March 1962);"A Note on the Export Performance of Less-developed Countries," InternationalTrade, 1965, (The Contracting Parties to the General Agreement on Tariffs andTrade [GATT], Geneva, 1966), p. 23; and Van Doorn Ooms, Regionalization andExport Performance: X Study of Primary Commodities (unpublished Ph.D. thesis,Yale University, 1966). See also Alasdair G. Macbean, Export Instability andEconomic Development, (Cambridge, Mass., 1966).

4

commodity policies (such as the U.S. sugar legislation). The focusof this study, however, will be on the variations directly related todifferences in the growth of world exports of major commodities.But even after proper allowance has been made for these differences,the variations among countries remain striking. They exist despitethe fact that in exporting to the developed countries-their mostimportant customers-the developing countries must overcomecommon obstacles: sluggishness of demand for certain primaryproducts, various kinds of barriers against imports into industrialcountries, and difficulties of new entry into highly competitive anddeveloped markets. Numerous proposals for overcoming some ofthese obstacles have been made, in particular, that restrictions beliberalized and that tariffs on industrial products be lowered. How-ever, even if the proposals most favorable to the developing countrieswere to be adopted, experience suggests that different countrieswould continue to show marked variations in the growth of theirexports.

The differences in growth are of immediate relevance to the prob-lems of estimating the "trade gap" of the developing countries-atopic closely related to the estimation of the needs of these countriesfor external capital. Estimates have, on occasion, been arrived at byprojecting exports of major commodities and broad categories ofmanufactured products and comparing them with "needed" orlikely imports.2 This method gives one approximation of the magni-tude of development finance requirements, which must be consideredin conjunction with other estimates obtained by different ap-proaches. But global estimates of trade gaps conceal the differencesin the export growth of individual countries which may be caused bydifferent policies affecting the supply and prices of exports. Suchpolicies might affect the trade gaps of individual countries, and alsothe gap of all developing countries taken together.

Variations in export growth are part and parcel of developmentperformance. Among those who are actively working in economic

2 For example, see United Nations, World Economic Survey, 1963, Part II, Tradeand Development: Trends, Needs, and Policies; and Bela Balassa, Trade Prospectsfor Developing Countries, (Economic Growth Center, Yale University, 1964).

5

development, if not among theorists, there is little dispute that thegrowth of exports is an essential element of a healthy developmentprogram It enables poor countries to benefit from rapidly growingexternal markets and to overcome a slack caused by any slowdownin the growth of domestic markets. Participation of foreign interestsin rapidly growing export sectors may be instrumental in increasingthe flow and assimitlatton of technical and managerial know-hiow.An expansion of exports provides the resources to pay for the largerimports required by a successful development program, or for thedebts incurred to finance part of these requirements It is now gener-ally recognized that imports must rise as development proceeds,particularly if industrialization is to platy a strategic role Increasedindustrial output-either through better utilization of existingplants or by the start of new industries-often requires an increasein imports of raw materials and intermediate goods. Even where apolicy of import substitution has succeeded in suppressing imports,the lag in import growth behind output growth has often provedtemporary, if prolonged1 however, it may harm industrial expansionby imposing a limit on the supplies of new capital goods and rawmaterials Over the longer term, export growth is the only satis-factory solution to the problems posed by a high burden of debtincurred to finance development. Among the countries with theheaviest debt burdens are those countries well on their way toindustrialization An increase in their exports is of special impor-tance, both to mitigate the debt problem and to utilize the marketpotentials for manufactured goods

The relation between export growth and factors influencing exportsupply-an essential element in judging a country's developmentperformance-is not easily established with any precision Severalapproaches are possible. In this paper, the approach is to takecertain key characteristics of a country's policies and its exportposition, and attempt to relate them to cross-country variations inexport growth A basic assumption is that most developing countriesmust take the conditions of demand in the developed countries asgiven The conclusions reached by this method are necessarilytentative, also, they are limited because of shortcomings of the dataand statistical methods and because the analysis takes into account

6

only a few of the many factors on which policies are based. Theeffects on exports of alternative allocations of resources by sub-sector or project are nor explored in detail The study needs to besupplemented by time series analysis of individual countries, analysisof supply responses in individual industries, and analysis of theeffects on exports of aspects of policy other than those singledout here

Tl he conceptual framework and the methods followed in analyzingexport growth and performance are described in Chapter II. Empiri-cal findings are discussed in Chapters III and IV; Chapter Vexplores the interrelation and contrasts between opposite tradeand development strategies-a strategy with outward orientationin which domestic and export diversification are combined and astrategy with more exclusive reliance on domestic diversificationto the detriment of export growth

II

FRAMEWORK AND METHODS OF ANALYSIS

A change in the value and volume of exports of a country mustbe viewed in relation to the total market in order to obtain a clearpicture of the performance of one country relative to others. In theintercountry comparisons made in Chapter III, the growth of exportsis gauged by the changes of country shares in major commoditymarkets. The use of export shares as a basic measurement makes itpossible to avoid giving "bad marks" to those countries which havesuffered from deteriorating export prices and contracting or stag-nating markets.

A distinction is made between "major" exports and all otherexports, called "minor" exports.' Major exports include all com-modities which bulk large in the exports of at least some developingcountries. For most of these commodities, world markets are fairlywell organized. The market position of some developing countriesis a factor to be considered in judging the potentialities for expan-

I Major exports are all commodities including manufactures which accountedfor more than 5 percent of merchandise exports in 1950-63 of at least one of thecountries of the group. Minor exports are the remainder. See Chapter III, page 19for further definition.

9

sion of exports. The distinction made here between major and minorexports is somewhat different from the one usually employed incurrent discussions of trade policy, which divides exports into pri-mary commodities and manufactures. Major exports as defined hereinclude not only most primary commodities but also some manu-factured items, e.g. textiles.

Minor exports-a miscellaneous group of all items not includedin the major category-are by definition relatively small in theexport package of developing countries. The markets for these ex-ports are not well organized internationally, and few developingcountries have a dominant position in the trade of these commodi-ties. Items in this group, which include both manufactures andagricultural commodities, have widely varying market character-istics. In the statistical analysis, the growth of minor exports ismeasured by intercountry comparison of the value of this group inabsolute terms rather than in relation to world markets. One pointbrought out clearly is that minor exports account for most of thegrowth of exports of developing countries. The consensus in currentdiscussion is that this is likely to continue in the next decade and-recognizing a limit of say 3-4 percent to the annual growth ofprimary exports (even if international price stabilization measuresshould succeed more generally than heretofore)-the focus is onthe possible growth of exports of manufactures.2 In the presentpaper, the analysis of the variation in, and prospects for, the growthof exports is broadened to include not only new manufactures butalso new agricultural products (e.g. tomatoes from Mexico, tropicalfruit other than bananas, and mushrooms from Taiwan). The basicreason for doing so is the view that economic development is abroad process which affects all sectors of the economy and all stagesof production, and that, if successful in increasing output at com-

2 For recent examples, see UN Conference on Trade and Development(UNCTAD), Trade in Manufactures and Semi-Manufactures, (February 1964);GATT, Preference and Other Policy Measures to Stimulate Exports of Less-developedCountries, (Geneva, July 1966); and Hal B. Lary, Exports of Manufactures by theLess Developed Countries, (draft, National Bureau of Economic Research, Inc.,New York, June 1966).

10

petitive prices, it must produce a broad diversification of exportswhich is not necessarily confined to manufactured products.

In the search for possible explanatioNns of the variations in exportgrowth-as defined in this study-primary emphasis was given tothe initial trade position of a country and to the trade orientationof development policies. Among the countries studied, these factorsdiffered considerably.

A country's trade position can be measured simply by taking avalue-weighted average of that country's volume shares in majorexport commodity markets. In the short and medium run, thisposition is not under the control of many exporting countries.Differences in the trade positions of countries may help to explaindifferences in the growth of exports of major commodities, since thesize of a country's trade shares may restrain that country fromincreasing its exports. The freedom of opportunity that a countryhas in expanding exports without upsetting market prices variesinversely with the size of its share in the commodity markets. Thelarger a country's trade share, the greater is the chance that aproportionate increase in exports will upset the prevailing pricestructure, disturb the workings of an international commodity agree-ment, or call forth retaliation by competitors. It will be argued inChapter V that the trade position may influence the trade orienta-tion of a country's policies.

The trade orientation of a country's development policies is notas easily defined and measured as its trade position. Broadly speak-ing, a distinction can be made between development policies withinward and those with outward orientation.' The characteristics ofthese contrasting policies would seem relevant to the intercountrydifferences in export supply conditions and responses and, conse-

3See Barend A. de Vries, "The Importance of Economic Size for the Orientationof Monetary Policy in Developing Countries" in David Krivine (ed.), Fiscal andMonetary Problems in Developing States, Proceedings of the Third Rehovoth Con-ference, (Fred A. Praeger, New Y'ork, 1967); and D. B. Keesing, Outward LookingPolicies and Economic Development, (Columbia University International EconomicsWorkshop, May 1966).

11

quently, to the variations in export growth. With inward orientation,countries will strive to diversify and expand their industrial pro-duction, with primary emphasis on the domestic market, substitutingdomestic goods for a wide and growing range of imports. There aremany reasons and rationalizations for such a policy, includingsluggish external demand for primary exports, insulation againstexternal fluctuations, wartime shortages of manufactures, the drivetoward a more urban economy, and the presumed advantages-political or economic-of manufacturing over primary production.

The very essence of such a policy is not merely a stepping up ofindustrialization; it is interference with price relationships for thepurpose of forcing a change in production patterns. In many situa-tions, new investments are steered toward manufacturing and awayfrom agriculture. vFew countries following this policy have found itpossible to base investment decisions on a comparison between thecosts of additional imports and the earnings from additional exports.In situations where the resource cost of reducing, or not increasing,imports exceeds that of producing additional exports, import sub-stitution fosters an allocation of resources which does not maximizedomestic output (calculated at international prices)' and whichpenalizes exports. The penalty on exports may be effected in differentways. Usually the exchange rate, tariff, and restrictions policies willturn the internal terms of trade against the agricultural or mineralsectors (which often are the main export suppliers). 4 In the monetarysphere, the country will tend to assign only secondary importanceto international price competitiveness; consequently, when indus-trialization is accompanied by inflation, the country will be slow inadjusting its exchange rate.

Countries with the opposite policy-outward orientation-will,in their choice of new lines of production and the management of

4See Harry G. Johnson, "Tariffs and Economic Development," Journal ofDevelopment Studies, (October 1965); John H. Power, Import Substitution as anIndustrialization Strategy, Society for International Development, 1966 WorldConference Proceedings; and Michael Bruno, The Optimal Selection of Export-Promoting and Import-Substituting Projects, UN First Interregional Seminar onDevelopment Planning, (September 1965).

12

domestic prices, place greater, if not primary, importance on theprospects for exports and the maintenance of a competitive pricelevel. Given the political, as well as technical, difficulties of frequentexchange rate adjustments, they will seek to maintain domesticprice stability. More often than not, these countries will avoid heavyindustrialization at the expense of agriculture and other primaryproduction. Several countries that have adopted an outward orienta-tion policy have achieved a marked increase in agricultural and

mineral exports. When domestic price pressures do develop, thesecountries will tend to adjust their exchange rates more quickly thanwill countries with inward orientation.

There are, of course, many variations in policies among countries,and no classification can be clear-cut at a given moment or for anindividual country over a period of time. Yet the combination of

industrialization, domestic financial, exchange rate, and protectionpolicies suggests that some countries, such as Brazil and Argentina,have had a predominantly inward orientation during much of thepostwar period. And many smaller countries-with a greater degreeof monetary stability, less emphasis on industrialization oriented

toward their domestic markets, and more emphasis on agricultureand mineral production for export-have had a predominantly out-ward orientation. Some smaller countries with outward orientationare industrializing without building a heavy industry complex andare experiencing a rapid increase in exports of manufactures.

The contrast between inward and outward policy orientationextends to financial and commercial policies as well as to resourceallocation and public expenditure policies. Financial policies covergeneral fiscal, credit, and balance of payments management, andaffect the level of development expenditures, the competitivenessof exports, and the degree of protection. Resource allocation policiesenable the government to give special emphasis to individualsectors through the composition of development expenditures,selective credit measures, price supports and such nonfinancial mea-sures as special training and technical help. Both types of policy

have implications for the pattern of development, e.g. the encourage-ment of individual sectors, such as heavy industry as against

13

agriculture. Emphasis on sectors with an early export potential andthe resulting increase in productive capacity on the margin isclearly essential to the strengthening of a country's basic exportcapability and subsequent performance. Given the production pat-tern prevailing at a certain time, exports can be fostered throughspecial and general incentives-the exchange rate, fiscal rebates,subsidies, etc. On the other hand, if maintained over a longer period,these measures will tend to influence the country's productivecapacity. The pattern of production will determine the country'sbasic export position.

It has not been possible to identify inward and outward orienta-tion with precise statistical measurements. It has, however, beenpossible to use statistical indicators-e.g. price and productionindices-to gauge certain major characteristics of developmentpolicies, particularly those bearing on trade orientation and exportperformance. For example, in the intercountry comparisons of pricemovements relevant for exports, use has been made both of thegeneral price level in terms of domestic currency and of its equivalentin dollars (in order to allow for the effect of exchange rate adjust-ments). Comparisons of production growth have been extended toagriculture and manufacturing. A combination of steady priceinflation and rapid increase in heavy manufacturing output willoften indicate inward orientation. Conversely, a relatively high rateof agricultural growth and price stability may be indicative of out-ward orientation. However, in designating a country's policy ashaving an outward or inward orientation, factors other than thosecovered by the statistical indicators have to be taken into account.

Steady inflation will, of course, normally turn price incentivesagainst exports and may increase domestic consumption, often atthe expense of the supply of exports (particularly of foodstuffs andfibers). The adverse impact on export supply schedules can becounteracted temporarily by exchange rate adjustment. Persistentinflation, however, requires an almost continuous process of ex-change rate correction, which is seldom achieved in practice. Priceinflation should, of course, not be confused with noncompetitiveprices which may prevail even under stable conditions. Steady price

14

rises are taken as symptomatic of domestic pressures against ex-ports. At times, these pressures may be offset by rapid improvementsin productivity and exchange rate adjustments.

Changes in the production pattern, as measured by the relativegrowth of agriculture and manufacturing, may be indicative of thetrade orientation of a country's policies and hence help to explaindifferences in exports. More directly, the addition to agriculturalproduction made possible by the application of modern methods(increasing output per acre for instance) will generally be competi-tive, and the greater productivity will extend to the output ofcommodities in which the country already has export connections.In measuring the relative growth of agriculture, output totals them-selves are inadequate; they need to be read against populationincrease and/or the demand for more and better foods associatedwith urbanization and higher living standards.

The possible effects that a rapid growth of manufacturing outputmay have on exports are highly controversial in developmenteconomics.5 The adverse effects which policies of import substitutioncan have on exports in general have been mentioned above. Inaddition, given the lead of developed industrial countries over thedeveloping countries, industrialization will, initially, pay off slowlyin the form of export growth, even under free trade and exchangepolicies. This is especially true of industrialization programs withemphasis on heavy industry or on industries which require a con-siderable volume of output to become competitive. Once an indus-trial base has been established (e.g. as reflected in the scale anddiversification of production and the availability of managerial andtechnical skills), an appropriate orientation policy may, if main-tained over a long period of time, lead to a relatively rapid increasein exports of manufactures. For many countries, however, indus-trialization is often an integral part of the development program,along with improvement in employment opportunities, educationand training, and the growth of urban areas. The very success ofindustrialization in terms of higher living standards will entailhigher consumption by the growing industrial-urban population,

See, for example, Alfred Maizels, Industrial Growth.

15

part of which may need to be satisfied by an expansion of imports.At the same time, new industrial production will increase demandfor raw materials and intermediate goods which will need to besatisfied by new imports or by a reduction of traditional exports,especially of primary products.' Such a reduction in primary exportsmay be most marked in large countries where the size of the domesticmarket makes possible large-scale production, which in turn shouldhold promise for lowering costs and for exports of industrial goods.The acid test of success in industrial development is whether anincrease in exports of manufactures will compensate for the declinein primary exports.

In the comparisons among countries made here, the trade positionsat the start of the period under study and changes in other variableshave been related to the differences in export growth. The vari-ables have been taken as indicative of the supply conditions in theexporting countries. With the exception of the trade positions,the changes in these variables are essentially a reflection of differ-ences in policies and as such are largely subject to the control of theexporting countries.

Other factors that affect the exports of the developing countriesare the basic economic variables of consuming countries, e.g. income,output of industries utilizing the products of the developing coun-tries, and prices (and availability) of substitutes for the importedraw materials. Demand is also affected by changes in preferentialarrangements, import restrictions, and customs duties imposed byconsuming countries.

Variations in conditions of the developed consumer countries affectthe developing exporting countries in different ways. Total demand(and exports) of individual commodities move in varying degreesbecause consumption differs among importing countries and demand

I A clear-cut case is Mexico where domestic industrial demand has reduced thesupply of minerals for export. These are aspects of the structural and transitionalshifts which, according to some economists, make necessary a large influx of externalassistance in the development process. See for example, H. B. Chenery and A. M.Strout, "Foreign Assistance and Economic Development," American EconomicReview, (September 1966).

16

parameters (e.g. income and price elasticities) also differ. Moreover,a relaxation of trade barriers against primary imports by developedcountries is bound to affect individual commodities differently, evenif the relaxation is undertaken in a concerted, nondiscriminatorymanner.7 However, it is assumed here that the changes in com-modity trade shares caused by shifts in demand are determined bythe differences in supply conditions in the exporting country. Putin another way: if the supply parameters of the producing countriesare the same, the assumption is that the countries' shares in com-modity markets will not be affected by a shift in demand. This isclearly a simplifying assumption in that it abstracts from the effectwhich different growth rates in developed countries may have onthe trade shares of the developing countries as a result of the existinggeographic trade pattern as well as such factors as regional ties,preferential arrangements, and transportation. However, as ex-plained in Chapter IV, specific allowance for regional demand wouldnot change the conclusions of the study.

The analysis is, in the first instance, focused on the question ofhow a country's exports in recent years have fared relative to worldmarkets. However, there is no denying that demand for some com-modities increased much faster than for others. Countries whichmaintained their shares in rapidly growing markets obviously didmuch better than those whose markets were stagnant. Thus a ques-tion to be explored is why some countries were more successful thanothers in capturing a share of the more buoyant markets-whetherfinancial and development policies or just plain luck made thedifference.

' The effect of present barriers varies greatly with the commodities concerned.See UNCTAD, Policy Impediments 4ffecting Primary Commodity Imports intoMajor Industrial Countries (National Commoditv Problems): Proceedings, Vol. III,(1964); D. Gale Johnson, "Agriculture and Foreign Economic Policy," Journal ofFarm Economics, (December 1964); Harry G. Johnson, "Sugar Protectionism andthe Export Earnings of Less-Developed Countries: Variations on a Theme byR. H. Snape," Economica, (February 1966); Alfred Maizels, Alternative FiscalPolicies for Tropical Export Products (to be published under FAO Special StudiesProgram). In a review of the estimates in these studies of the effect of the relaxationof trade barriers, G. Lovasy concludes that sugar exports would benefit the most;see Effects on Developing Countries' Exports of Reducing Trade Barriers to PrimaryProducts: Critical Survey of Recent Estimates, (International Bank for Reconstruc-tion and Development, January 31, 1967).

17

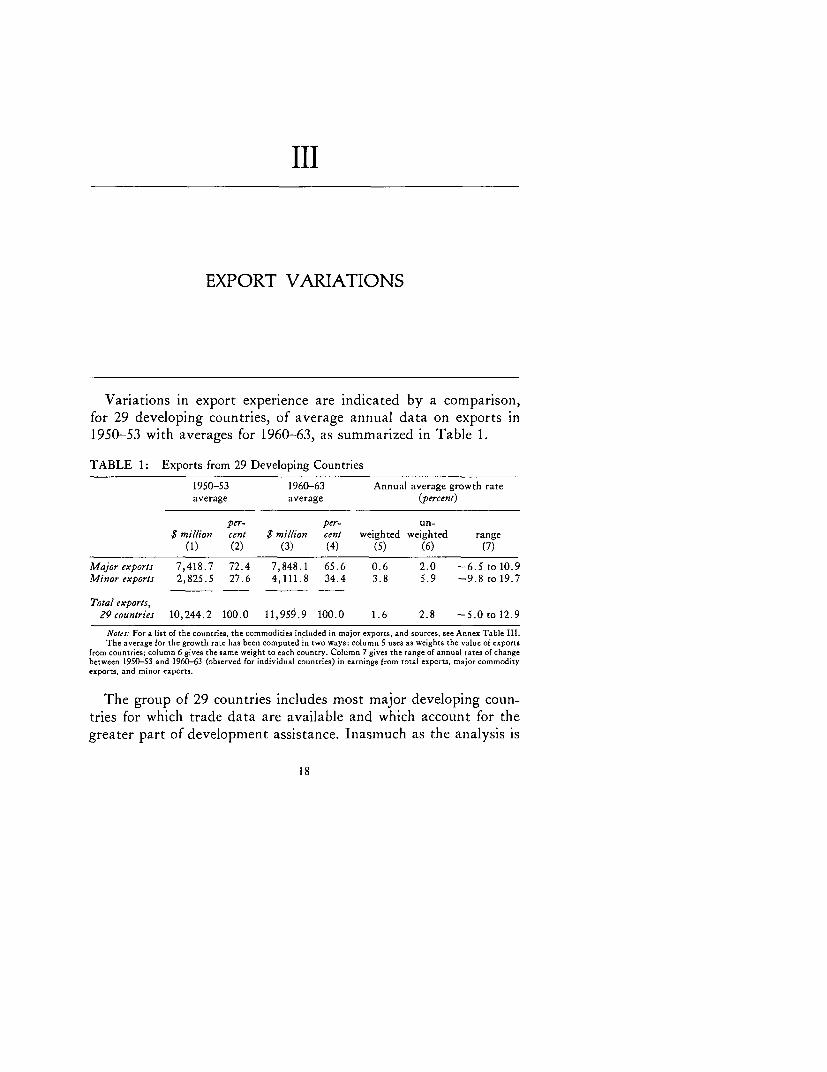

III

EXPORT VARIATIONS

Variations in export experience are indicated by a comparison,for 29 developing countries, of average annual data on exports in1950-53 with averages for 1960-63, as summarized in Table 1.

TABLE 1: Exports from 29 Developing Countries

1950-53 1960-63 Annual average growth rateaverage average (percent)

per- per- un-$ million cent $ million cent weighted weighted range

(1) (2) (3) (4) (5) (6) (7)

Major exports 7,418.7 72.4 7,848.1 65.6 0.6 2.0 -6.5tolO.9Minor exports 2,825.5 27.6 4,111.8 34.4 3.8 5.9 -9.8 to 19.7

Total exports,29 countries 10,244.2 100.0 11,959.9 100.0 1.6 2.8 -5.0 to 12.9

Noses: For a list of the countries, the commodities included in major exports, and sources, see Annex Table 111.The average for the growth rate has been computed in two ways: column 5 uses as weights the value of exports

from countries; column 6 gives the same weight to each country. Column 7 gives the range of annual rates of changebetween 1950-53 and 1960-63 (observed for individual countries) in earnings from total exports, major commodityexports, and minor exports.

The group of 29 countries includes most major developing coun-tries for which trade data are available and which account for thegreater part of development assistance. Inasmuch as the analysis is

18

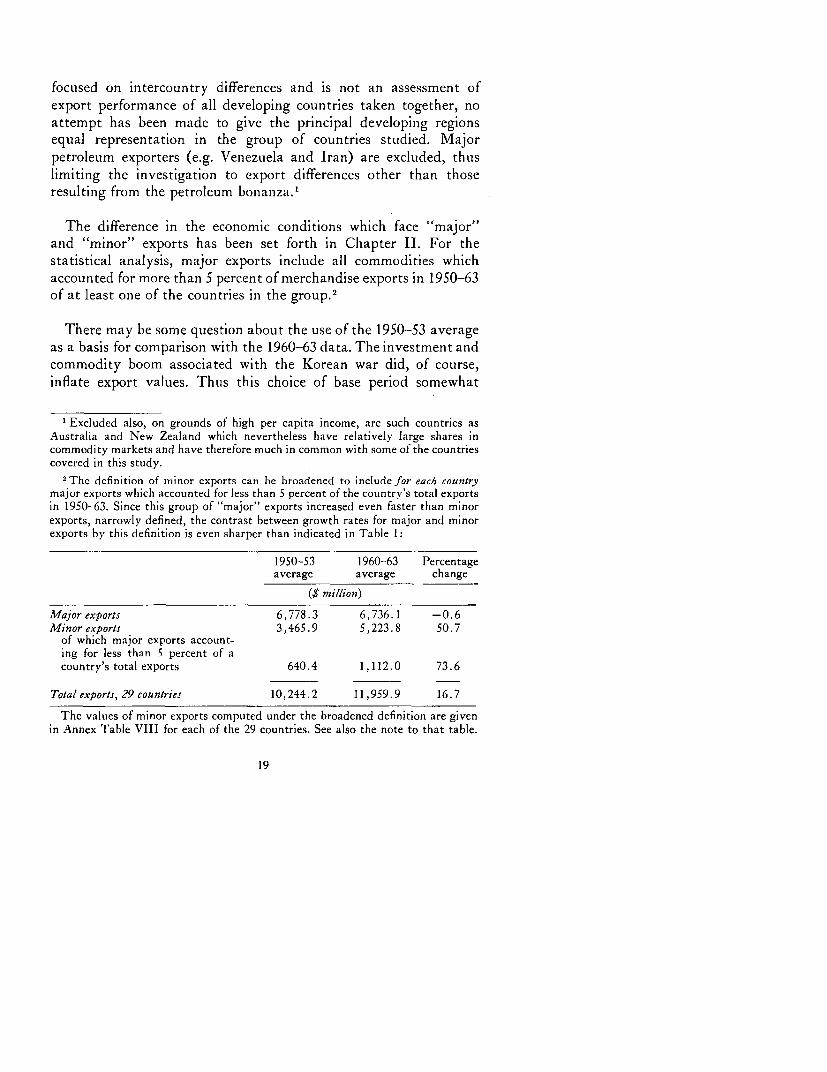

focused on intercountry differences and is not an assessment ofexport performance of all developing countries taken together, noattempt has been made to give the principal developing regionsequal representation in the group of countries studied. Majorpetroleum exporters (e.g. Venezuela and Iran) are excluded, thuslimiting the investigation to export differences other than thoseresulting from the petroleum bonanza.'

The difference in the economic conditions which face "major"and "minor" exports has been set forth in Chapter II. For thestatistical analysis, major exports include all commodities whichaccounted for more than 5 percent of merchandise exports in 1950-63of at least one of the countries in the group.2

There may be some question about the use of the 1950-53 averageas a basis for comparison with the 1960-63 data. The investment andcommodity boom associated with the Korean war did, of course,inflate export values. Thus this choice of base period somewhat

I Excluded also, on grounds of high per capita income, are such countries asAustralia and New Zealand which nevertheless have relatively large shares incommodity markets and have therefore much in common with some of the countriescovered in this study.

2The definition of minor exports can be broadened to include for each countrymajor exports which accounted for less than 5 percent of the country's total exportsin 1950-63. Since this group of "major" exports increased even faster than minorexports, narrowly defined, the contrast between growth rates for major and minorexports by this definition is even sharper than indicated in Table 1:

1950-53 1960-63 Percentageaverage average change

($ mi/lion)

Major exports 6,778.3 6,736.1 -0.6Minor exports 3,465.9 5,223.8 50.7

of which major exports account-ing for less than 5 percent of acountry's total exports 640.4 1,112.0 73.6

Total exports, 29 countries 10,244.2 11,959.9 16.7

The values of minor exports computed under the broadened definition are givenin Annex Table VIII for each of the 29 countries. See also the note to that table.

19

suppresses the growth rates in subsequent years. It may also affectthe differences in growth rates among countries to the extent thatsome countries managed more rapidly to increase supplies of certainexports in the base period and as a result found it difficult to improvefurther upon their export position in subsequent years.' However,this is possible for almost any base period. It is felt that a shiftin the base period, say to the mid-fifties, would not materiallyaffect the conclusions of the analysis. Earlier years were not chosenfor a base period since comparison of 1960-63 data with those for theyears prior to World War II or the immediate postwar years is lessrelevant. The ten-year period for which cross-country comparisonsare made seems long enough for certain financial and resource alloca-tion policies, pursued over the period, to have had an effect on thegrowth of exports. For example, the impact of heavy industrializa-tion accompanied by considerable price inflation, or emphasis onagricultural development and international price competitiveness,should be noticeable within the span of a decade.

Considerable differences in the growth of exports are noted whenthe countries are grouped by their position in international trade,size of domestic market, and degree of price inflation. The com-modity composition of exports is a further factor influencing thedifferences in export growth (see the next subsection).

A country's position in international trade depends on its sharein world markets for its major exports and the relative importanceof major exports and of minor exports in its total exports. Thisposition is measured here by an index (W) which is the weightedaverage of a country's shares in the markets of its major exportcommodities, the weights being the proportion of these exportsin the country's total exports. In calculating the index, it is assumedthat developing countries have a negligible share in the world

3 The choice of the base period may also affect the comparison of growth ratesof major and minor exports since the Korean war boom had a greater impact onexports of major commodities. When 1952-53 is used as a base, the growth in theten-year period to 1962-63 amounted to 11.6 percent for major exports and to66.2 percent for minor exports, compared with 6.0 percent and 45.5 percent re-spectively, in Table 1.

20

markets for items included under "minor exports." 4 The trade posi-tion index ranges between a country's simple export share (i.e. itsexports as a percentage of total world exports) and 100 (the indexobtained when a country is the world's sole exporter of the com-modities that it exports). The index varies positively with the pro-portion of major commodities in a country's exports and the shareof these exports in world markets. More generally, the index reflectsthe total amount of a country's exports, the extent to which itsexports are concentrated on a few commodities, and total inter-national trade in these few commodities.'

For grouping countries into "small" and "large" ones, the bench-mark was chosen at $4 billion equivalent of gross domestic productin 1963. This choice of a benchmark is somewhat arbitrary andrequires qualifications which are discussed in Chapter V. It isinteresting that this benchmark is equivalent to a domestic marketfor steel exceeding 400,000 tons.6 The steel industry has a strategicplace in the development of heavy and complex manufacturingindustry.7 A domestic market large enough to provide a base for

4 In this respect, the trade position index is different from Michaely's commodityweighted export share index. See Michael Michaely, Concentration in InternationalTrade, (Amsterdam, 1962).

6 For example, in the period 1950-53, the Philippines had 85.92 percent of theworld export market for abaca, 5.49 percent of the market for raw sugar, 34.14percent of the market for tropical hardwood, and 16.67 percent of the market foredible vegetable oils. Multiply these percentages by the proportion they bore toPhilippine exports (respectively 12.54 percent, 19.7 percent, 5.06 percent, and44.97 percent), add the total and multiply by 100 (to counteract the effect ofmultiplying a percentage by a percentage) and the trade position index of thePhilippines emerges as 21.1 approximately.

These major exports accounted for 82.27 percent in value of the Philippines'export trade in this period. If this percentage is used as a divisor to the trade index,the weighted average of the Philippines' major export shares is obtained, 25.62percent (see p. 75 below). For 1960-63, the weighting used is the same as for1950-53.

G See Annex Table VII. Chile is an exception since it had steel consumption over400,000 tons and a GDP slightly below $4 billion.

I Heavy industry, such as machinery, steel and transport equipment, is definedhere as industry requiring substantial capital outlays and need not be capitalintensive (as against labor intensive). Of course, some heavy industry (e.g. ma-chinery) may be labor intensive.

21

efficient steel production is significant in the economic developmentof individual countries.8

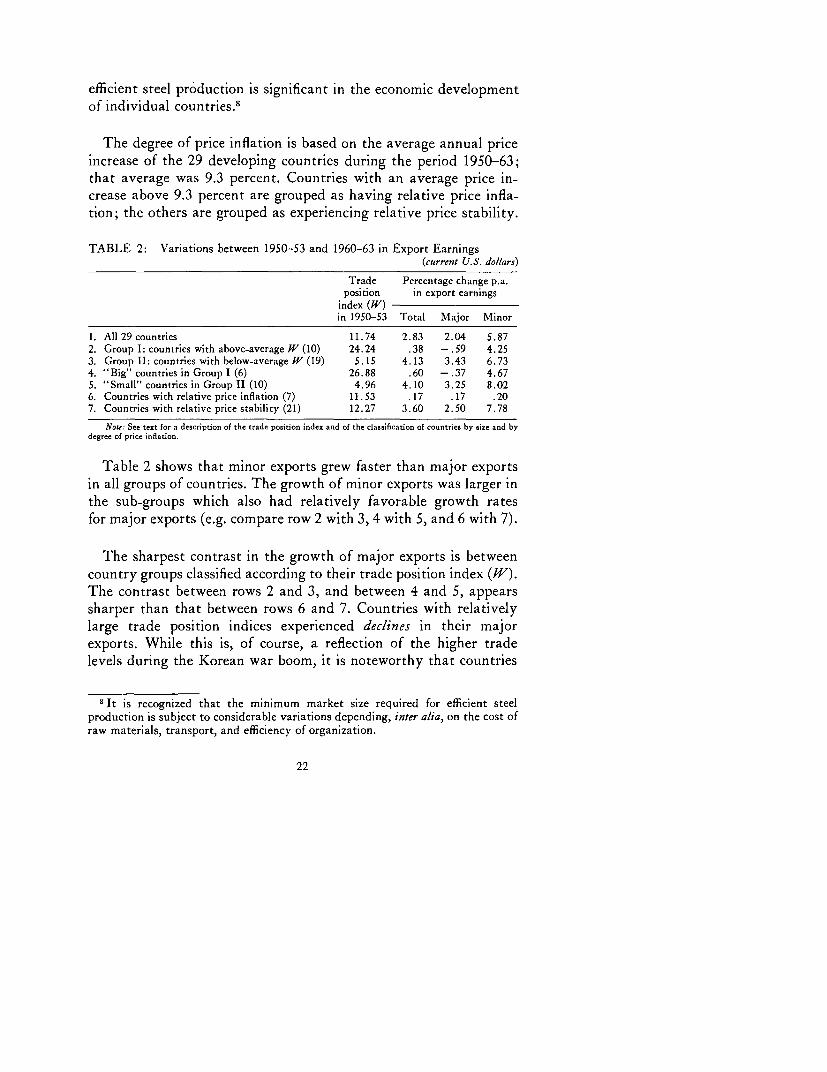

The degree of price inflation is based on the average annual priceincrease of the 29 developing countries during the period 1950-63;that average was 9.3 percent. Countries with an average price in-crease above 9.3 percent are grouped as having relative price infla-tion; the others are grouped as experiencing relative price stability.

TABLE 2: Variations between 1950-53 and 1960-63 in Export Earnings(current U.S. dollars)

Trade Percentage change p.a.position in export earnings

index (W)in 1950-53 Total Major Minor

1. All 29 countries 11.74 2.83 2.04 5.872. Group I: countries with above-average W (10) 24.24 .38 -. 59 4.253. Group ll: countries with below-average W (19) 5.15 4.13 3.43 6.734. "Big" countries in Group 1 (6) 26.88 .60 -. 37 4.675. "Small" countries in Group 11 (10) 4.96 4.10 3.25 8.026. Countries with relative price inflation (7) 11.53 .17 .17 .207. Countries with relative price stability (21) 12.27 3.60 2.50 7.78

Note: See text for a description of the trade position index and of the classification of countries by size and bydegree of price inflation.

Table 2 shows that minor exports grew faster than major exportsin all groups of countries. The growth of minor exports was larger inthe sub-groups which also had relatively favorable growth ratesfor major exports (e.g. compare row 2 with 3, 4 with 5, and 6 with 7).

The sharpest contrast in the growth of major exports is betweencountry groups classified according to their trade position index (W).The contrast between rows 2 and 3, and between 4 and 5, appearssharper than that between rows 6 and 7. Countries with relativelylarge trade position indices experienced declines in their majorexports. While this is, of course, a reflection of the higher tradelevels during the Korean war boom, it is noteworthy that countries

8 It is recognized that the minimum market size required for efficient steelproduction is subject to considerable variations depending, inter alia, on the cost ofraw materials, transport, and efficiency of organization.

22

with small trade position indices experienced growth averaging 3.4percent per annum beyond the Korean war levels.

Comparison of countries grouped by domestic price behavior sug-gests that minor exports clearly did better in countries with relativeprice stability (compare rows 6 and 7). The contrast is sharper thanthat observed for minor exports in countries grouped by their tradeposition index (rows 2 and 3). Major exports also fared betterwhere there was price stability, but the contrast is not as sharp asthat for minor exports. The countries with above-average priceincreases had trade position indices somewhat below those of coun-tries with greater price stability.

It thus is necessary to disentangle further the effects of tradeposition and domestic price behavior. This has been done throughregression analysis, discussed in the next chapter. It will be shownthere that favorable performance of exports of major commoditiesin the period studied was associated more with the size of the marketshare at the start of the period than with domestic price stability.

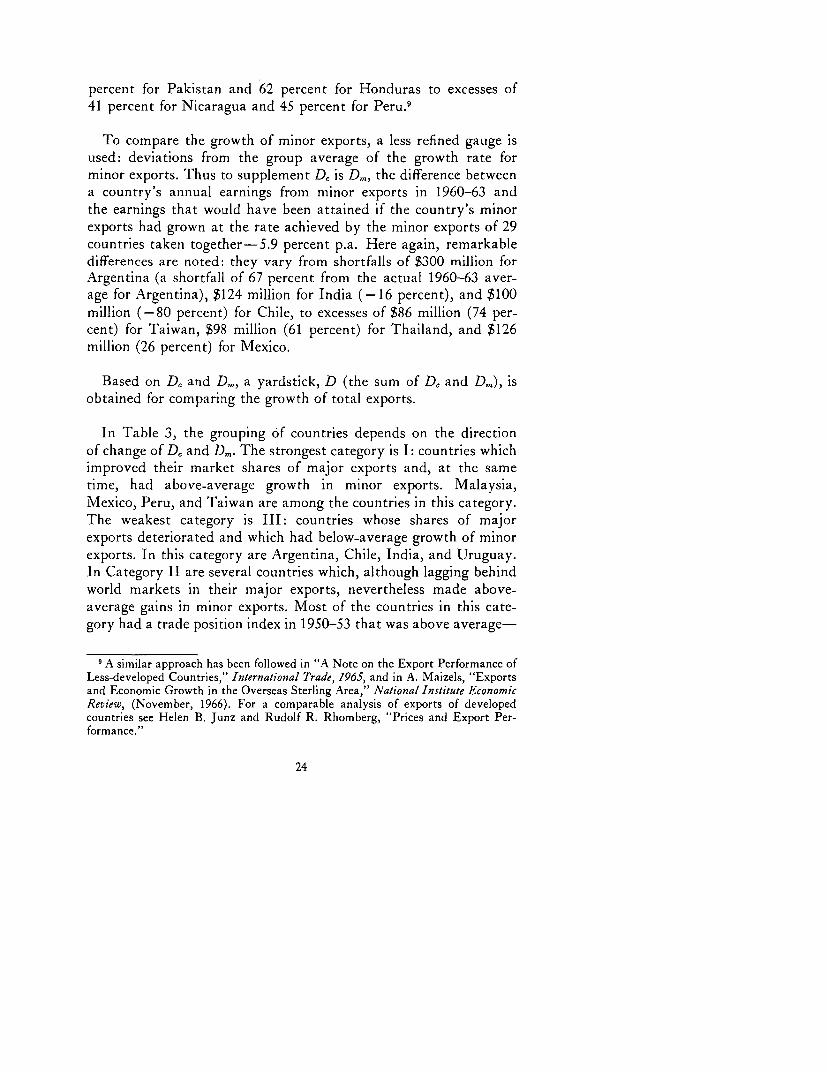

Variations Relative to the World Market and Group Averages

It can, of course, be argued that variations in earnings from majorexports are caused, to a large extent, by the movements-both involume and in price-in world markets; because of the differingcompositions of exports, these movements affect countries in dif-ferent ways. A relatively simple way to calculate export growthdifferences other than those caused by market movements is tocompare the difference between a country's actual earnings frommajor exports in 1960-63 and what the earnings would have beenif the country's shares in its principal commodity markets in1960-63 had been the same as in 1950-53. This difference, DC, isshown in Table 3. A cross-country comparison of D. reveals howcountries' exports have fared relative to world market trends inmajor export commodities. The variations in D. are striking: from ashortfall of $232 million for Brazil and $187 million for India to anexcess of $178 million for Peru; or as a percentage of annual averagesin 1960-63 of major exports of each country, from shortfalls of 65

23

percent for Pakistan and 62 percent for Honduras to excesses of41 percent for Nicaragua and 45 percent for Peru.9

To compare the growth of minor exports, a less refined gauge isused: deviations from the group average of the growth rate forminor exports. Thus to supplement Dc is Di,m the difference betweena country's annual earnings from minor exports in 1960-63 andthe earnings that would have been attained if the country's minorexports had grown at the rate achieved by the minor exports of 29countries taken together-5.9 percent p.a. Here again, remarkabledifferences are noted: they vary from shortfalls of $300 million forArgentina (a shortfall of 67 percent from the actual 1960-63 aver-age for Argentina), $124 million for India (-16 percent), and $100million (-80 percent) for Chile, to excesses of $86 million (74 per-cent) for Taiwan, $98 million (61 percent) for Thailand, and $126million (26 percent) for Mexico.

Based on Dc and Di, a yardstick, D (the sum of D, and Di), isobtained for comparing the growth of total exports.

In Table 3, the grouping of countries depends on the directionof change of D, and Di. The strongest category is I: countries whichimproved their market shares of major exports and, at the sametime, had above-average growth in minor exports. Malaysia,Mexico, Peru, and Taiwan are among the countries in this category.The weakest category is III: countries whose shares of majorexports deteriorated and which had below-average growth of minorexports. In this category are Argentina, Chile, India, and Uruguay.In Category II are several countries which, although lagging behindworld markets in their major exports, nevertheless made above-average gains in minor exports. Most of the countries in this cate-gory had a trade position index in 1950-53 that was above average-

' A similar approach has been followed in "A Note on the Export Performance ofLess-developed Countries," International Trade, 1965, and in A. Maizels, "Exportsand Economic Growth in the Overseas Sterling Area," National Institute EconomicReview, (November, 1966). For a comparable analysis of exports of developedcountries see Helen B. Junz and Rudolf R. Rhomberg, "Prices and Export Per-formance."

24

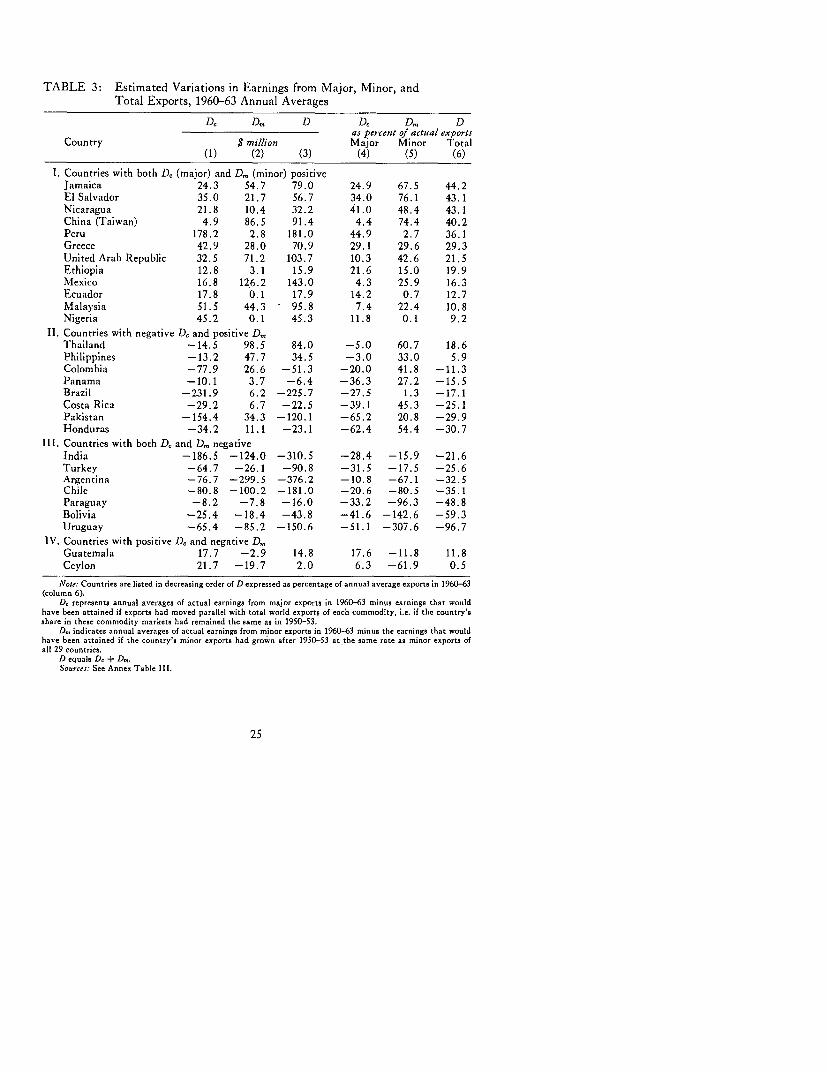

TABLE 3: Estimated Variations in Earnings from Major, Minor, andTotal Exports, 1960-63 Annual Averages

Dc D,, D Dc D. Das percent of actual exports

Country $ million Major Minor Total(1) (2) (3) (4) (5) (6)

1. Countries with both D, (major) and D. (minor) positiveJamaica 24.3 54.7 79.0 24.9 67.5 44.2El Salvador 35.0 21.7 56.7 34.0 76.1 43.1Nicaragua 21.8 10.4 32.2 4i.0 48.4 43.1China (Taiwan) 4.9 86.5 91.4 4.4 74.4 40.2Peru 178.2 2.8 181.0 44.9 2.7 36.1Greece 42.9 28.0 70.9 29.1 29.6 29.3United Arab Republic 32.5 71.2 103.7 10.3 42.6 21.5Ethiopia 12.8 3.1 15.9 21.6 15.0 19.9Mexico 16.8 126.2 143.0 4.3 25.9 16.3Ecuador 17.8 0.1 17.9 14.2 0.7 12.7Malaysia 51.5 44.3 95.8 7.4 22.4 10.8Nigeria 45.2 0.1 45.3 11.8 0.1 9.2

II. Countries with negative Dc and positive D.Thailand -14.5 98.5 84.0 -5.0 60.7 18.6Philippines -13.2 47.7 34.5 -3.0 33.0 5.9Colombia -77.9 26.6 -51.3 -20.0 41.8 -11.3Panama -10.1 3.7 -6.4 -36.3 27.2 -15.5Brazil -231.9 6.2 -225.7 -27.5 1.3 -17.1Costa Rica -29.2 6.7 -22.5 -39.1 45.3 -25.1Pakistan -154.4 34.3 -120.1 -65.2 20.8 -29.9Honduras -34.2 11.1 -23.1 -62.4 54.4 -30.7

III. Countries with both Dc and D. negativeIndia -186.5 -124.0 -310.5 -28.4 -15.9 -21.6Turkey -64.7 -26.1 -90.8 -31.5 -17.5 -25.6Argentina -76.7 -299.5 -376.2 -10.8 -67.1 -32.5Chile -80.8 -100.2 -181.0 -20.6 -80.5 -35.1Paraguay -8.2 -7.8 -16.0 -33.2 -96.3 -48.8Bolivia -25.4 -18.4 -43.8 -41.6 -142.6 -59.3Uruguay -65.4 -85.2 -150.6 -51.1 -307.6 -96.7

IV. Countries with positive Dc and negative D.Guatemala 17.7 -2.9 14.8 17.6 -11.8 11.8Ceylon 21.7 -19.7 2.0 6.3 -61.9 0.5

Note: Countries are listed in decreasing order of D expressed as percentage of annual average exports in 1960-63(column 6).

Dt represents annual averages of actual earnings from major exports in 1960-63 minus earnings that wouldhave been attained if exports had moved parallel with total world exports of each commodity, i.e. if the country'sshare in these commodity markets had remained the same as in 1950-53.

D. indicates annual averages of actual earnings from minor exports in 1960-63 minus the earnings that wouldhave been attained if the country's minor exports had growrn after 1950-53 at the same rate as minor exports ofall 29 countries.

D equals De + D,s.Sources: See Annex Table 111.

25

suggesting an obstacle to expansion of major exports; however, theysucceeded in overcoming at least part of their export problemthrough an expansion of minor exports. Annex Table VIII showsthe Dm calculated for both the "narrow" and "broad" definition ofminor exports (see footnote 2 of this chapter). There is a high rankcorrelation between these two Dm series (0.92).

It has been possible to separate minor exports (Di) into manu-factured (D,) and other (D2) goods. A comparison of these twocategories brings out sharp variations in growth rates, as shown inTable 4. Several countries with growth rates that were aboveaverage for exports of manufactured goods showed below-averagegrowth for non-manufactured goods, and vice versa. The datashow that, for a majority of countries with above-average per-formance in minor exports, growth was concentrated in categoriesother than manufactured goods. For example, of the countrieswhose Dm was more than 40 percent of annual average exports in1962-63, export growth for manufactured goods exceeded that ofnon-manufactures for two (Jamaica and Taiwan), but the reversewas true for six (El Salvador, Honduras, Panama, Colombia, theUnited Arab Republic, and Ecuador).

Changes in Structure of Commodity Trade

The market share for each country may be computed as the aver-age of its quantitative shares in markets for its major exports,weighted by their value in 1950-53. On this basis, Table 5divides countries into those with small (below-average) shares in1950-53 and those with large (above-average) shares. As shownin the table, substantial shifts occurred in the structure of com-modity trade during the period studied. The positions of countrieswith relatively large shares in commodity markets tended todeteriorate and, conversely, the positions of the smaller traderstended to improve.

In this context, it is meaningful to distinguish between commodi-ties exported mostly by the developing countries (A-commodities)and commodities exported by the developing countries in competi-

26

TABLE 4: Estimated Variations in Minor Exports:Total, Manufactured Goods, and Other Goods,(1962-63 Annual Averages)

D. D, D2 D. D, D2($ million) as percent of 1962-63 exports

Manu-Total factures Others

(1) (2) (3) (4) (5) (6)

Countries for which column 5 (manufactures) > column 6 (other)China (Taiwan) 129.5 93.4 35.5 79.5 89.9 60.1Jamaica 51.2 12.6 41.3 60.4 91.6 58.2Costa Rica 3.8 2.0 2.6 26.8 74.1 22.0Philippines 17.7 28.8 -0.0 12.4 94.6 -0.0Brazil -1.6 15.3 18.4 -0.3 38.7 4.3Peru -14.0 26.2 -50.9 -13.0 29.7 -262.3India -151.9 192.4 -290.8 -18.1 64.1 -54.0Nigeria -20.6 21.6 -33.2 -20.4 77.5 -45.4Bolivia -27.1 -9.2 -19.5 -216.4 -156.6 -295.3Uruguay -105.8 -45.1 -73.0 -341.2 -175.5 -1376.8

Countries for which column 5 < column 6El Salvador 26.2 5.4 18.3 75.9 37.4 91.7Honduras 13.5 -7.0 18.0 55.9 -37.4 83.9Panama 11.2 -2.7 13.9 49.0 -910.0 61.8Colombia 28.3 2.7 24.9 41.3 17.8 46.7United Arab Republic 83.0 29.3 47.7 41.0 37.8 38.3Ecuador 11.3 -0.8 12.9 40.3 -55.3 48.4Nicaragua 10.2 -3.8 12.7 38.2 -93.2 56.4Malaysia 76.0 -115.5 146.2 36.9 -245.1 91.9Mexico 169.4 9.9 145.4 30.3 6.5 35.7Greece 20.4 -1.6 19.6 18.9 -5.6 24.6Guatemala -2.5 -2.5 1.0 -8.6 -80.3 3.6Paraguay -3.9 -10.2 3.7 -34.8 -850.8 37.6Argentina -213.4 -143.6 -75.4 -41.6 -227.9 -16.7Turkey -84.8 -28.0 -48.9 -54.0 -218.4 -33.9Chile -141.3 -160.7 -20.0 -114.1 -776.5 -19.4

OtherThailand 93.4 a 90.0 55.3 56.7Pakistan 55.7 a -10.5 33.1 a -11.4Ethiopia -7.3 -4.4 -28.0 a -17.0Ceylon -26.7 a -25.4 -93.3 -_105.0

Notes: Countries are listed in decreasing order of D. expressed as a percentage of actual minor exports in1962-63 (column 4).

D,., represents annual averages of actual earnings from minor exports in 1962-63 minus the earnings that wouldhave been attained if the country's minor exports had grown after 1952-53 at the same rate as minor exports ofall 29 countries, taken together.

Di for manufactured goods, is based on Standard International Trade Classifications 5, 6, 7, and 8. Di representsannual averages of actual earnings from manufactured minor exports in 1962-63, minus the earnings that wouldhave been attained if the country's exports of these manufactures had grown after 1952-53 at the same rate asexports of these manufactures by the first 25 countries above, taken together.

D2 represents differences (as described for D.) for other goods.a For these countries it was not possible to calculate the manufactured goods component.

27

TABLE 5: Countries' Shares in Major Export Commodity Markets,1950-53 and 1960-63

(percent)

AverageCountry Country marketshares shares share ofbelow above individual

average average All countriesin 1950-53 in 1950-53 countries in group

(1) (2) (3) (4)

.11 commoditiesNumber of countries 20 9 29

1950-53 24.9 49.3 53.4 15.51960-63 25.2 45.5 49.8 13.9Percentage change 1.2 -7.7 -6.7 -10.3

A-commodities,Number of countries 15 8 23

1950-53 25.9 56.9 66.6 19.81960-63 26.0 52.6 62.7 18.3Percentage change 0.4 -7.6 -5.9 -7.6

B-commodities,Number of countries 15 9 24

1950-53 9.4 27.4 34.1 8.41960-63 10.3 22.7 31.1 6.8Percentage change 9.6 -17.2 -8.8 -19.0

Note: For each country the market share was computed as the mean of its quantitative shares in commoditymarkets for its major exports, each export weighted by its value in the periods indicated. Countries were classifiedinto two groups depending on whether their market shares were below or above the unweighted average for all 29countries (shown in column 4). For each group (columns 1, 2, 3), the entries show the average share of the group

in the commodity markets concerned, with each commodity being weighted by the value of total exports of thatcommodity in the group.

.A-commodities are exported mostly by the developing countries. B-commodities are exported by both thedeveloping and developed countries.

tion with developed countries (B-commodities); these two groupsare listed below.1° For all 29 countries, the market share declinedbetween 1950-53 and 1960-63 for both A4- and B-commodities.But developing countries' shares declined more in the markets forcommodities where these countries were in competition withdeveloped countries. Countries with relatively large market shares

10 A-commodities, exported mostly by developing countries, are-abaca, bananas,bauxite, cocoa beans, copper, fishmeal, green coffee, jute, jute manufactures,petroleum, rubber, sugar, tea, and tin (14 commodities).

B-commodities, exported by developing countries in competition with developedcountries, are-beef and veal, canned meat, cattle hides, cotton, cotton textiles,currants, grapes and raisins, hazelnuts, iron ore, lead, maize, pulses, rice, shrimp,silver, tropical hardwood, tobacco, vegetable oils (edible and industrial), wheat andflour, wool, and zinc (21 commodities).

28

(column 2 in Table 5) suffered greater deterioration in their positionthan all 29 countries combined. Countries which had small marketshares in 1950-53 managed to improve their positions, especially incommodities exported by both developing and developed countries.

Countries Benefiting Mostfrom Rapidly Expanding Trade

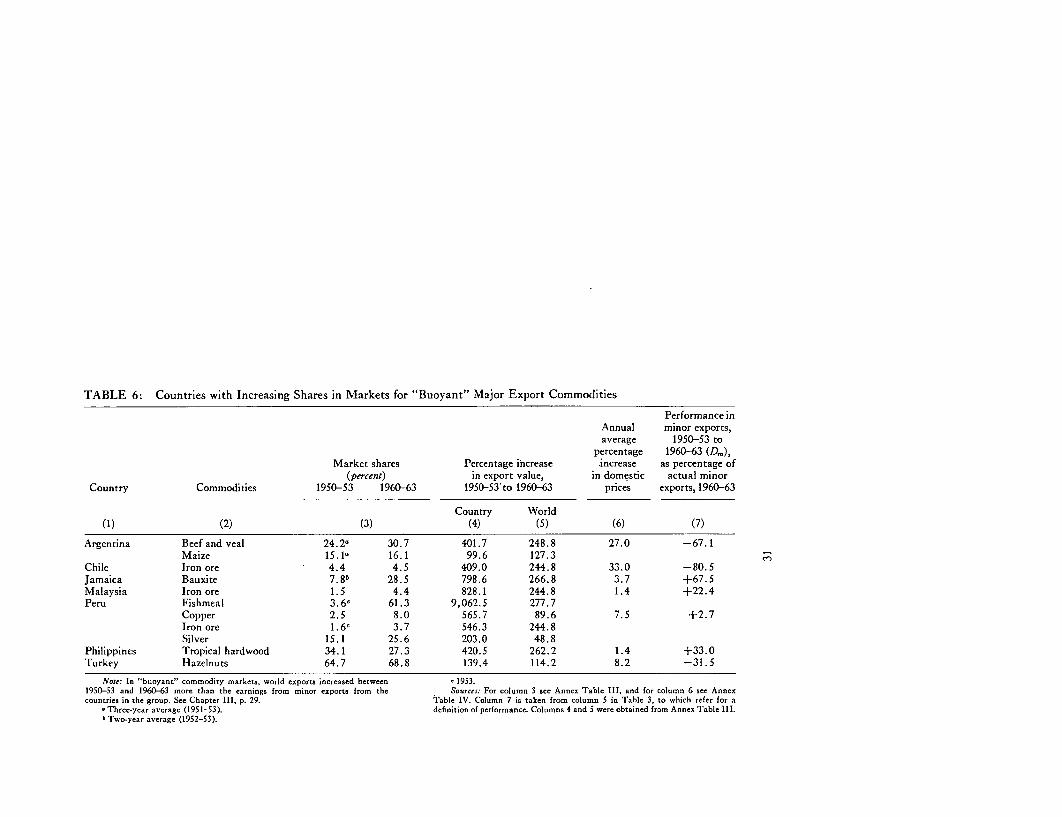

The analysis of variations in major exports is focused on countryperformance relative to world market movements. However, whena country's major markets suffer from stagnation, its export earningswill compare unfavorably with those of others even if it managesto improve its market shares. In the period studied, the most rapidgrowth in export earnings was achieved by those countries whichcaptured a higher share of buoyant markets.

This point is of considerable importance because of the strikingvariations in the growth of world exports of the different commodi-ties studied. In terms of current values, the range was wide-froma net market contraction of 42 percent for lead to an expansion ofmore than 250 percent for timber, bauxite, and fishmeal. In constantprices, the range was from a contraction of 23 percent for abacato an expansion of 360 percent for fishmeal. The current dollarvalue of minor exports of the 29 countries increased, on the average,by 45 percent during the period. For the purpose of this analysis,"buoyant" commodities are defined as those whose world exports(in current dollar values) increased more than "minor" exports.These were hazelnuts, pulses, maize, petroleum, iron ore, beef andveal, tropical hardwood, bauxite, fishmeal, silver, copper, and cur-rants, grapes, and raisins.

Of the 29 countries studied, only six improved their shares inbouyant commodity markets (Table 6). In the case of a seventhcountry, the Philippines, the value of its tropical hardwood exportsincreased considerably faster than the value of world tropicalhardwood exports even though in volume terms its share of the worldmarket declined. Four of these seven countries (Jamaica, Malaysia,Peru, and the Philippines) also had above-average growth in minorexports. These countries tended to have two crucial characteristics

29

operating at the same time. First, for most of the commoditiesconcerned they had very small world market shares at the start(1950-53) of the period. In addition, they followed policies whichencouraged expansion of minor exports; for instance, they hadbetter-than-average price stability, an annual average price increaseof 4.1 percent, compared with 9.3 percent for the 29 countriesduring the period 1950-63.

The three other countries-Argentina, Chile, and Turkey-hadbelow-average growth in minor exports. The market shares at thestart of the period for the major commodities of these countrieswere large for Argentine beef (24 percent) and Turkish hazelnuts(64 percent) and small for Chilean iron ore (4 percent).1 ' In thesesituations, special factors are likely to have accounted for thebetter-than-average growth in buoyant major commodity markets,e.g. unusual natural advantage or marked improvement in supplyof an individual commodity (such as might have resulted from anew mine, or a domestic pricing policy favoring export supply, e.g.Argentine beef).

On balance, it would seem that a combination of small worldmarket shares and the key characteristics of export-minded policyaugur well for a country's chance of cashing in on the potentials ofrapidly growing commodity markets. But there remains, of course,room for special situations-and, it might be added, luck."'

11 Chile's share in the market for iron ore improved only fractionally. Its per-formance in major exports was also below average.

12The problem posed here can also be approached by asking whether countrieswhich had a significant amount of "buoyant" commodity exports in 1950-53tended, on balance, to place less emphasis on export diversification in subsequentyears. Of the 29 countries studied, only five had "buoyant" commodity exportsequal to or exceeding 10 percent of their total exports-Chile (58 percent), Greece(21 percent), Ethiopia (10 percent), Colombia (15 percent), and Paraguay (20percent). In minor exports, performance was substantially below average for Chileand Paraguay and above average for Colombia, Ethiopia, and Greece. Thisevidence is clearly too narrow for generalization, but the problem warrants furtherstudy.

30

TABLE 6: Countries with Increasing Shares in Markets for "Buoyant" Major Export Commodities

Performance inAnnual minor exports,average 1950-53 to

percentage 1960-63 (Di),Market shares Percentage increase increase as percentage of

(percent) in export value, in domestic actual minorCountry Commodities 1950-53 1960-63 1950-53'to 1960-63 prices exports, 1960-63

Country World(1) (2) (3) (4) (5) (6) (7)

Argentina Beef and veal 24.20 30.7 401.7 248.8 27.0 -67.1Maize 15.1, 16.1 99.6 127.3

Chile Iron ore 4.4 4.5 409.0 244.8 33.0 -80.5Jamaica Bauxite 7.8b 28.5 798.6 266.8 3.7 +67.5Malaysia Iron ore 1.5 4.4 828.1 244.8 1.4 +22.4Peru Fishmeal 3.60 61.3 9,062.5 277.7

Copper 2.5 8.0 565.7 89.6 7.5 +2.7Iron ore 1.6' 3.7 546.3 244.8Silver 15.1 25.6 203.0 48.8

Philippines Tropical hardwood 34.1 27.3 420.5 262.2 1.4 +33.0Turkey Hazelnuts 64.7 68.8 139.4 114.2 8.2 -31.5

Note: In "buoyant" commodity markets, world exports increased between c1953.1950-53 and 1960-63 more than the earnings from minor exports from the Sources: For column 3 see Annex Table 111, and for column 6 see Annexcountries in the group. See Chapter III, p. 29. Table IV. Column 7 is taken from column 5 in Table 3, to which refer for a

aThree-year average (1951-53). definition of performance. Columns 4 and 5 were obtained from Annex Table 111.b Two-year average (1952-53).

IV

STATISTICAL ANALYSIS OF INTERCOUNTRYDIFFERENCES IN EXPORT GROWTH

A more systematic and complete analysis of the relationship be-tween variations in export growth and characteristics of countries'economic positions was obtained by means of linear regressionanalysis. In the analysis, the dependent variables were taken ascountries' deviations from a "norm" defined as export earningswhich would have prevailed if, during the period under study

(1950-53 to 1960-63), each country had maintained a constantshare in major commodity markets and experienced average growthin minor exports. These deviations were calculated for total exports,commodity exports, and minor exports classified by manufacturesand non-manufactures.

The independent variables measure the exporting country's posi-tion in major commodity markets, the variations in the growth ofagricultural and industrial output, and changes in domestic prices

during the period. In measuring industrial growth, use was madeof an index for industry in general and one for heavy industrywhich includes such industries as steel, machinery and equipment,

paper, and chemicals.

33

The price variables measure the average compound rate of changein the cost of living and wholesale price indices during the period.Intercountry variations were taken to reflect the relative degreeof price stability or inflation experienced. (Increases for the cost ofliving index averaged 9.3 percent per annum in the period studied,with a median of 3.75 percent.) In view of their wide variations,the price series may be taken as indicative of the intercountrydifferences in movements in the domestic cost of export production.However, the usefulness of the series for the latter purpose islimited, since changes in the price indices reflect movements incomponents (e.g. services and imports) which may have no directbearing on the cost of export production.

The results of the regressions are shown in Table 7. The equationspresented are those in which one or more coefficients are significant(at 5 percent probability level) and there is no multi-collinearityamong the independent variables (as seen from the simple correla-tion coefficients between any two independent variables).

The regressions with performance in major exports as the de-pendent variable (Table 7, equations 1, 2, and 3) confirm the conclu-sion reached in Chapter III that countries with relatively smallover-all positions in world commodity markets at the start of theperiod performed better during the period than those with largemarket positions. In addition, performance tended to be better forcountries with high growth rates in agriculture. The degree of priceinflation showed no significant relationship with performance inmajor exports. Neither was there a significant relationship betweenperformance and the rate of growth of industrialization (eithergeneral or heavy industrialization).

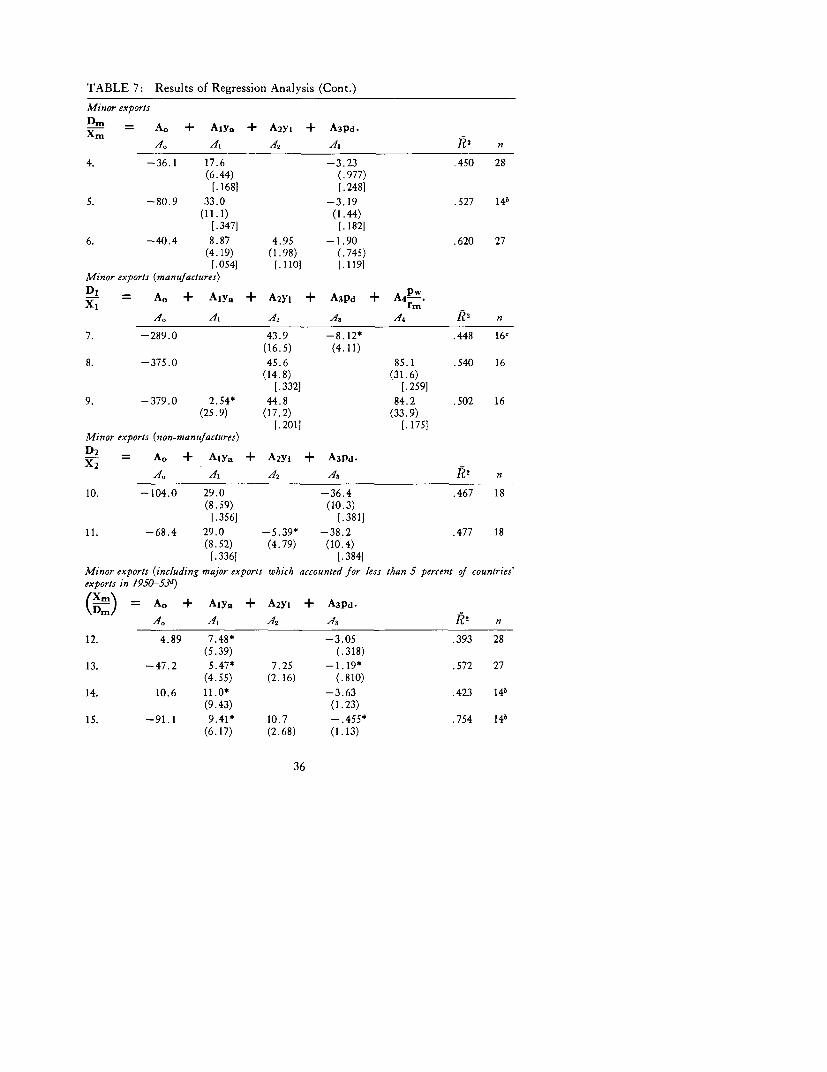

The results of the regressions with performance of minor exportsas dependent variables are shown in Table 7 for aggregate minorexports (equations 4, 5, 6), for manufactures (equations 7, 8, 9),and for non-manufactures (equations 10 and 11). Manufactures donot include certain "major" commodities, such as jute and cottontextiles, which were included in major exports (equations 1, 2, 3).

34

TABLE 7: Results of Regression Analysis

Dependent variables

D D. D. Di D2X-' X", i- X,l x, the numerator expressed as a percentage of the denominator, where

X = Xc + Xm and Xm = Xl + X2 .

X = total exports (average annual dollar value in 1960-63).Xc = major exports (average annual dollar value in 1960-63).Xm = minor exports (average annual dollar value in 1960-63),

of whichXi = manufactured goodsX2 = non-manufactures.

Dc = 1960-63 major exports (average annual value) minus the value that would have beenattained if the country had maintained its 1950-53 share (measured in quantityterms) in commodity markets.

Dm = 1960-63 minor exports (average annual value in current dollars) minus the earningsthat would have been attained if the country's minor exports had grown after 1950-53at the same rate as minor exports of all 29 countries taken together.

D = Dc + Dm.Dl and D2 similar to Dm for Xi and X2.

Independent variabless = share in 1950-53 commodity markets (measured in quantity terms), average weighted

by value of country's major exports.

Ya = agricultural output annual compound rate of change between 1950-53 andYi = industrial output 1960-63.Ys = output of heavy industry 9Pd = rate of increase (annual compound rate of increase) in domestic price level during

1950-63 (as measured by the cost of living index).Pw = same as Pd, but for wholesale price index.

pw = l EP w w) where (Pw) is the ratio of the domestic wholesale price index andrm W1t rm rm t

the index of the exchange rate applicable to minor exports (measured in terms of local cur-rency per dollar), both indices on 1950 = 100 base (t = 0 for 1950).

Regression resultsMajor exports

D, = Ao + Als + A2Ya + A3Yj + A4pd-Xe

aO Al As2 3 A4 n

1. -31.7 -. 719 7.79 1.49* -. 111* .353 27(.336) (3.05) (1.47) (.542)[.022] [.088]

2. -25.9 -. 662 8.38 .370 29(.309) (2.59)[.085] [.233]

3. -2.89 -. 889 5.01* -. 067* .519 150(.339) (2.73) (1.39)

35

TABLE 7: Results of Regression Analysis (Cont.)

Minor exports

Dm = A. + Alya + A2yI + A3pd.

Xm~~~~4 14 , A42 A3 R2 n

4. -36.1 17.6 -3.23 .450 28(6.44) (.977)

[.1681 [.248]5. -80.9 33.0 -3.19 .527 14b

(11.1) (1.44)[.347] [.182]

6. -40.4 8.87 4.95 -1.90 .620 27(4.19) (1.98) (.745)

[.054] [ 110] [.119Minor exports (manufactures)

DI = A0 + AlYa + A2Yj + A3pd + A4 --XT rm'

Ao. A3 A1422 4f 4 n

7. -289.0 43.9 -8.12* .448 16'(16.5) (4.11)

8. -375.0 45.6 85.1 .540 16(14.8) (31.6)

[.332] [.259]9. -379.0 2.54* 44.8 84.2 .502 16

(25.9) (17.2) (33.9)[.201] [.175]

Minor exports (non-manufactures)

D2 - A. + Alya + A2yi + A3Pd.x~2

Ao~ Al, A42 A3 R2 n

10. -104.0 29.0 -36.4 .467 18(8.59) (10.3)

[.356] [.381]11. - 68.4 29.0 -. 5.39* -38.2 .477 18

(8.52) (4.79) (10.4)[.336] [.384]

Minor exports (including major exports which accounted for less than 5 percent of countries'exports in 1950-53d)

(X-) = A. + Alya + A2yI + A3Pd.

A4 A 412 43 R2 n

12. 4.89 7.48* -3.05 .393 28(5.39) (.318)

13. - 47.2 5.47* 7.25 - 1.19* .572 27(4.55) (2.16) (.810)

14. 10.6 11.0* -3.63 .423 14b

(9.43) (1.23)15. -91.1 9.41* 10.7 - .455* .754 14b

(6.17) (2.68) (1.13)

36

TABLE 7: Results of Regression Analysis (Cont.)

Total exports

D = AO + Als + A2ya + A3yi + A4pd-

AO A1 A2 A13 A44

16. -36.3 - .593 8.45 2.90 -. 432* .624 27(.256) (2.33) (1.12) (.413)[.050] [.261] [.095]

17. -24.6 -. 245* 10.2 -1.19 .567 28(.296) (2.52) (.374)

[.333] [.207]

18. 20.0 -. 576* -1.31 .403 180(.302) (.433)

19. -33.5 -. 741 8.02 2.74 .496 28(.285) (2.53) (.859)[.1231 [.2061 [.2101

20. -35.3 - .728 7.19 2.49* .667 15a(.306) (2.46) (1.25)[.161] [.2841

ys has been used instead of yi; for list of countries for which ys is available, see Annex Table IV, column 5.b Countries for which Pd is above the median (3.75 percent).e Pw has been used instead of Pd-d See Chapter III, footnote 2.Notes: Coefficients starred * are not significant at 5 percent probability level. In equations with more than one

significant coefficient, figures in square brackets below the coefficient are partial R2 (coefficients of determination).

The degree of domestic price inflation shows a significant relation-ship with performance of minor exports (aggregate and non-manu-factures). The performance of countries with relatively stronginflation tends to be poor.' The growth rates of agricultural andmanufacturing production also show significant relationships. Inequation 6, all these factors (degree of price inflation, agriculturaland manufacturing growth rates) have significant coefficients.2

The rate of growth in manufacturing production is significant forthe manufactured goods included in minor exports (Table 7, equa-tions 7, 8, 9). The rate of growth in agricultural production shows asignificant correlation with minor exports other than manufacturedgoods.

' A slightly better fit is obtained when the correlation is confined to countrieswith a degree of price inflation above the median (3.75 percent per annum); seeequation 5.

2 In this equation, the dominant explanation (as judged by the value of partialR2) is provided by variations in the industrial growth rate and degree of priceinflation, compared with the agricultural growth rate.

37

Correlations were also carried out with the dependent variablesbeing performance of minor exports including exports of "major"commodities which accounted for less than 5 percent of the totalexports of the countries concerned. The degree of domestic priceinflation again shows up as a deterrent factor in export performance.However, when in multiple regression, the industrial growth rate(yj) was tested with either the agricultural growth rate (Ya) or thedegree of price inflation (Pd) as the independent variable, yi wasthe only significant variable (e.g. equations 13 and 15). Equation 1Shas the best fit (R2 = .75); it is confined to countries for whichthere are statistics on heavy manufacturing production (AnnexTable IV); the growth rate of heavy manufacturing productionhas the only significant coefficient in this equation.

The results of the regressions with performance of total exportsas the dependent variable are shown in equations 16, 17, 18, 19,and 20. In multiple regression, significant coefficients were obtainedfor three of the independent variables-market share, growth ratein agriculture, and growth rate in manufacturing-but the coefficientfor the degree of price inflation was not significant (equation 16).However, the degree of price inflation was significant in the regres-sions which included as additional independent variables marketposition and agricultural growth.3

The regression analysis was used as an aid in determining whichof the independent variables discussed in the earlier chapters havestatistically significant relationships with "export performance."The coefficients of determination range between .35 (equation 1)and .75 (equation 1S). The coefficients of determination in equationswith total exports and minor exports as dependent variables arehigher than in the equations having major exports as the dependentvariable. No attempt was made to improve the "fit" by searchingfor additional explanatory variables, since this was not regarded asnecessary for the main line of argument of this study.

'In equations 16 and 19, the coefficients for market position (s) had a smallerpartial R2 than those for the rate of agricultural and of industrial growth.

38

In the regression equations, the dependent variables are measuredin terms of percentage deviations of actual exports from a norm.Three of the independent variables also are expressed in terms ofpercentages-annual compound percentage rate of increase indomestic prices, agricultural output, and manufacturing output.The coefficients of these independent variables may be regarded aselasticities of export performance with respect to price inflation,agricultural growth, and manufacturing growth. In the equationsin which there are significant coefficients for both the agriculturaland the manufacturing growth rate, the ratio of the elasticity ofexport performance with respect to agricultural growth and theelasticity with respect to industrial growth is 1.8 for minor exports(equation 6) and even larger, 2.9, for total exports (equations 16and 19). The elasticity of export performance with respect to priceinflation ranges from 1.9 to 3.2 for minor exports (equations 4, 5,and 6), and from 1.2 to 1.3 for total exports (equations 17 and 18);for the non-manufactured component of minor exports, it amountsto 36 and 38 (equations 10 and 11).

One group of possible additional independent explanatory vari-ables are the variations in demand factors which can be observedamong major consuming regions. In the present study, the normagainst which actual exports are measured is based on movementsin world markets for commodities. Deviations from this norm,denoted by the symbol D for various export categories, are takenas reflecting the impact of competitive forces (prices, productionrates, market shares, etc.). An alternative set of deviations (R) canbe computed by basing the norm on a model of regional marketsfor commodities, which takes into account the variations amongregions in the growth of demand. In a careful analysis of the impactof regionalization on export performance, Ooms has computeddeviations from the norm in the world market model (similar to theconcept D) and that in a regional market (R). The "regionaleffect"-the difference between D and R-is shown to be importantfor commodities for which transfer costs are relatively high andwhich are more highly differentiated. In his analysis of aggregate

4Ooms, Regionalization and Export Performance.

39

export performance, Ooms makes allowance for the "regionaleffect" and reaches conclusions on the impact of price stability andthe degree of industrialization on export performance that aresimilar to those presented in this study.5