the emerging virtual reality landscape: a primer

TRANSCRIPT

Virtual Reality Introduction & Market Overview

by Brian Radmin ©BDMI,Nov2015 1

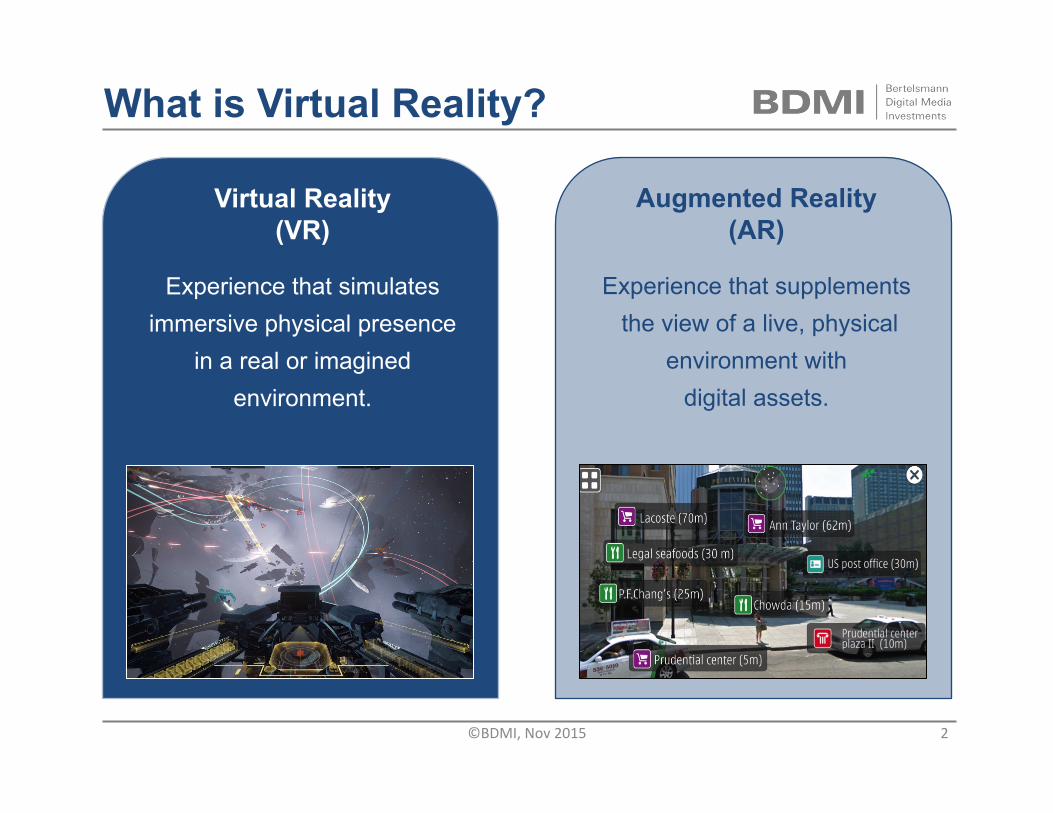

Virtual Reality (VR)

Experience that simulates immersive physical presence

in a real or imagined environment.

What is Virtual Reality?

Augmented Reality (AR)

Experience that supplements the view of a live, physical

environment with digital assets.

©BDMI,Nov2015 2

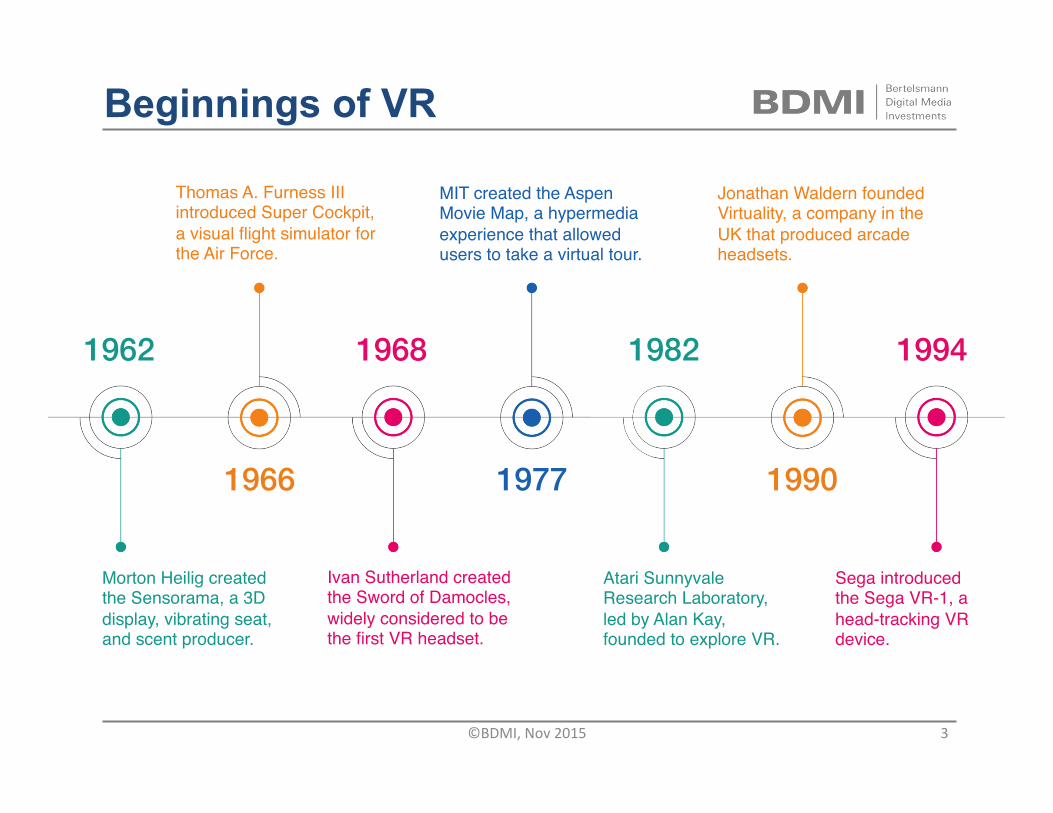

Beginnings of VR

1962!

1966!

1968!

1977!

1982!

1990!

1994!

Morton Heilig created the Sensorama, a 3D display, vibrating seat, and scent producer.

Ivan Sutherland created the Sword of Damocles, widely considered to be the first VR headset.

Atari Sunnyvale Research Laboratory, led by Alan Kay, founded to explore VR.

Sega introduced the Sega VR-1, a head-tracking VR device.

Thomas A. Furness III introduced Super Cockpit, a visual flight simulator for the Air Force.

Jonathan Waldern founded Virtuality, a company in the UK that produced arcade headsets.

MIT created the Aspen Movie Map, a hypermedia experience that allowed users to take a virtual tour.

©BDMI,Nov2015 3

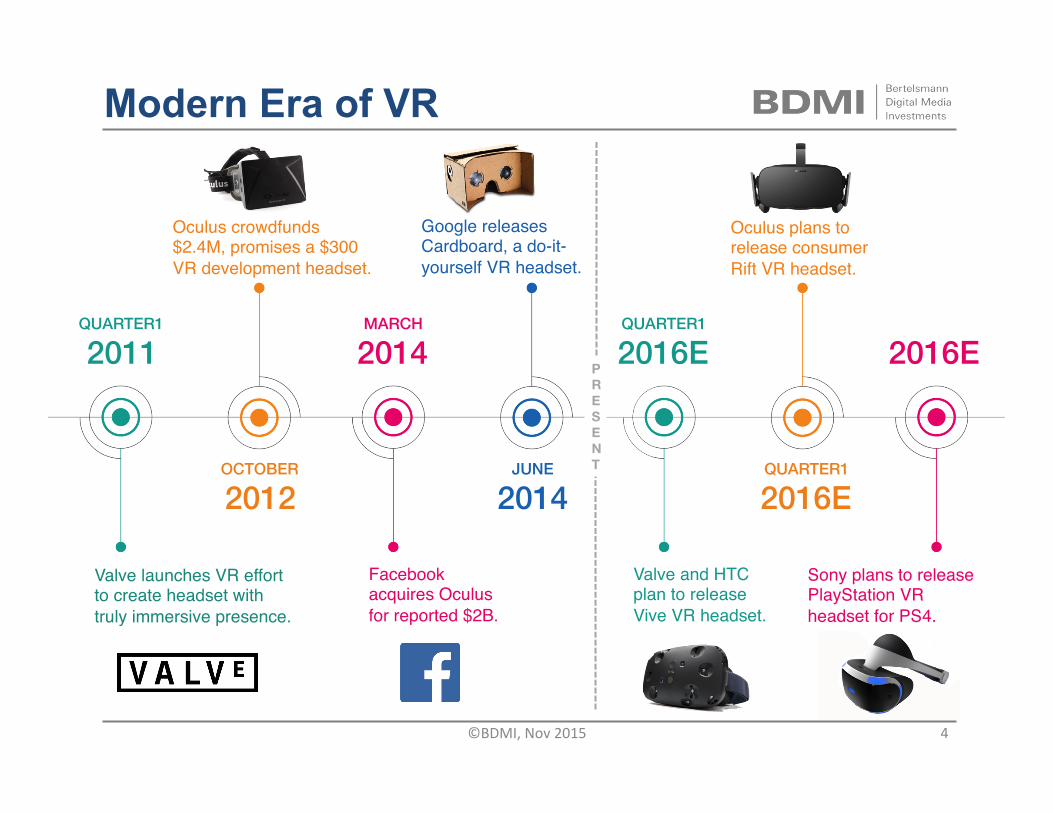

Modern Era of VR

QUARTER1!

2011!

OCTOBER!

2012!JUNE!

2014!

MARCH!

2014!QUARTER1!

2016E!

QUARTER1!

2016E!

!

2016E!

Valve launches VR effort to create headset with truly immersive presence.

Oculus crowdfunds $2.4M, promises a $300 VR development headset.

Facebook acquires Oculus for reported $2B.

Google releases Cardboard, a do-it-yourself VR headset.

Valve and HTC plan to release Vive VR headset.

Oculus plans to release consumer Rift VR headset.

Sony plans to release PlayStation VR headset for PS4.

PRESENT

©BDMI,Nov2015 4

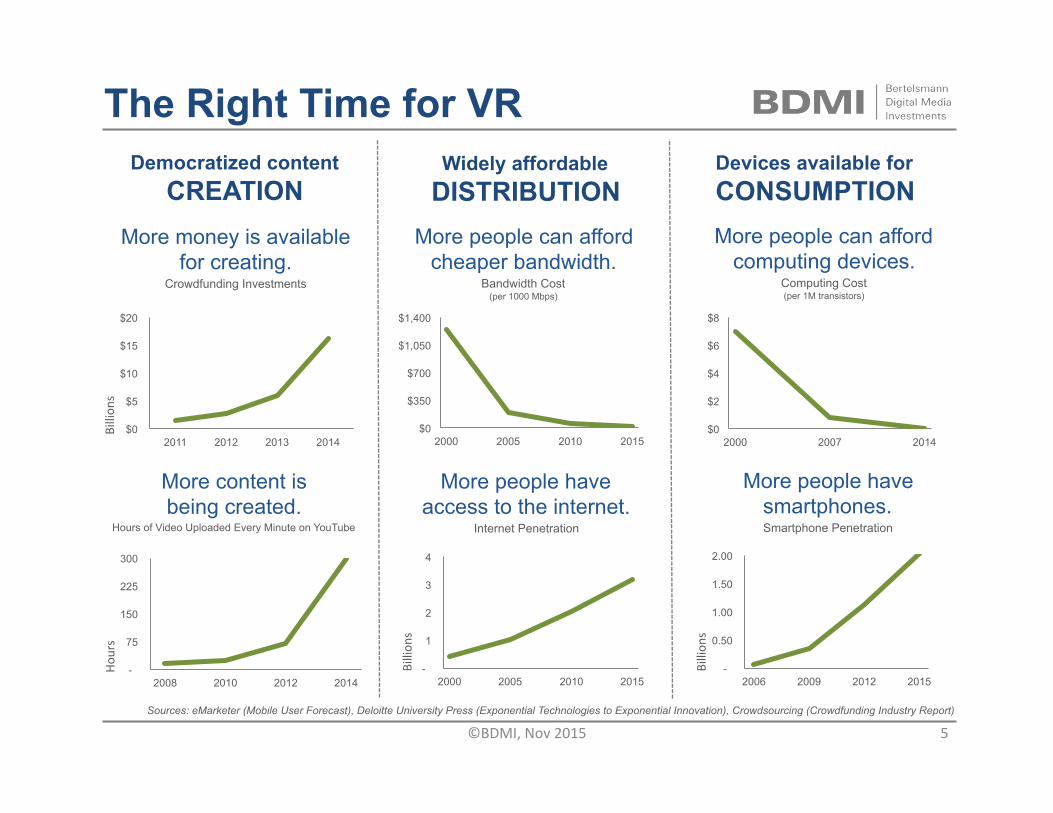

The Right Time for VR

$0

$5

$10

$15

$20

2011 2012 2013 2014

Billion

s

-

75

150

225

300

2008 2010 2012 2014

More content is being created.

Hours of Video Uploaded Every Minute on YouTube

Democratized content CREATION

Widely affordable DISTRIBUTION

Devices available for CONSUMPTION

$0

$350

$700

$1,050

$1,400

2000 2005 2010 2015

-

1

2

3

4

2000 2005 2010 2015

Billion

s

-

0.50

1.00

1.50

2.00

2006 2009 2012 2015

Billion

s

$0

$2

$4

$6

$8

2000 2007 2014

More money is available for creating.

Crowdfunding Investments

More people can afford cheaper bandwidth.

Bandwidth Cost (per 1000 Mbps)

More people have access to the internet.

Internet Penetration

More people can afford computing devices.

Computing Cost (per 1M transistors)

More people have smartphones.

Smartphone Penetration

Hours

Sources: eMarketer (Mobile User Forecast), Deloitte University Press (Exponential Technologies to Exponential Innovation), Crowdsourcing (Crowdfunding Industry Report)

©BDMI,Nov2015 5

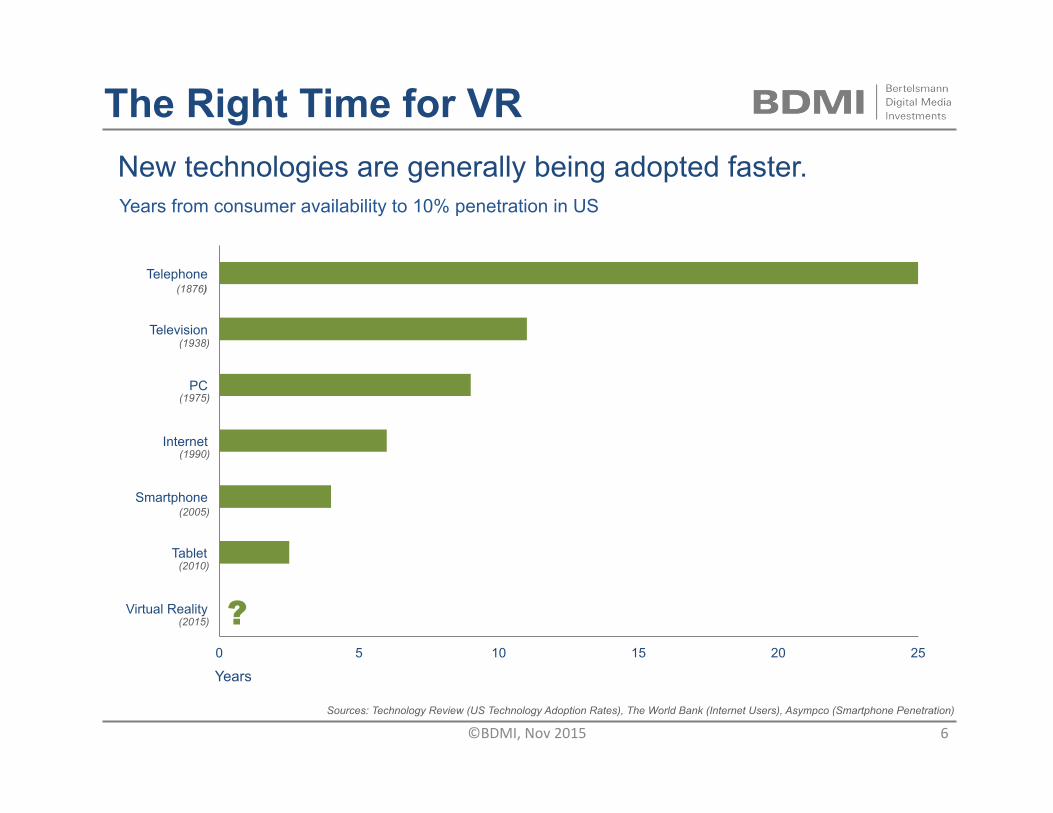

The Right Time for VR New technologies are generally being adopted faster.

0 5 10 15 20 25

Virtual Reality

Tablet

Smartphone

Internet

PC

Television

Telephone

?

(1876)

(1938)

(1990)

(2005)

(2010)

(1975)

(2015)

Years

Years from consumer availability to 10% penetration in US

Sources: Technology Review (US Technology Adoption Rates), The World Bank (Internet Users), Asympco (Smartphone Penetration)

©BDMI,Nov2015 6

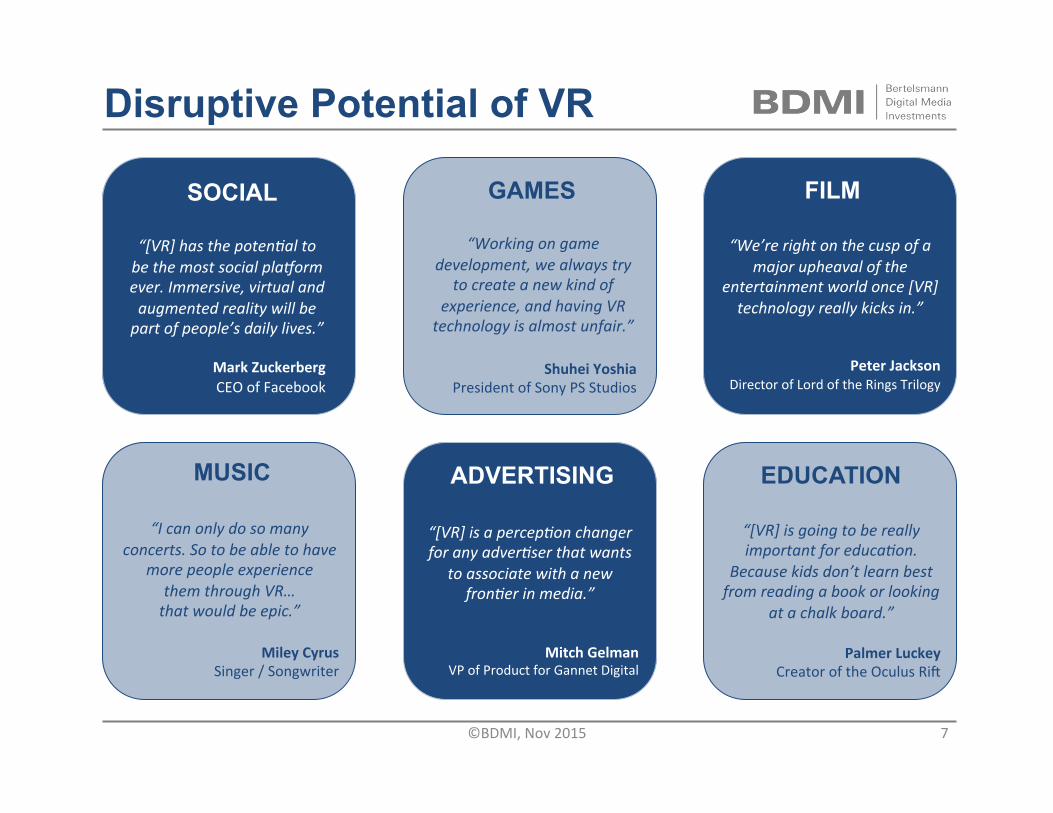

GAMES

ADVERTISING

FILM

“Workingongamedevelopment,wealwaystry

tocreateanewkindofexperience,andhavingVRtechnologyisalmostunfair.”

ShuheiYoshia

PresidentofSonyPSStudios

“We’rerightonthecuspofa

majorupheavaloftheentertainmentworldonce[VR]technologyreallykicksin.”

PeterJacksonDirectorofLordoftheRingsTrilogy

“[VR]isapercepConchangerforanyadverCserthatwants

toassociatewithanewfronCerinmedia.”

MitchGelmanVPofProductforGannetDigital

SOCIAL

“[VR]hasthepotenCaltobethemostsocialplaEormever.Immersive,virtualandaugmentedrealitywillbepartofpeople’sdailylives.”

MarkZuckerbergCEOofFacebook

Disruptive Potential of VR

EDUCATION

“[VR]isgoingtobereallyimportantforeducaCon.

Becausekidsdon’tlearnbestfromreadingabookorlooking

atachalkboard.”

PalmerLuckeyCreatoroftheOculusRiO

MUSIC

“Icanonlydosomanyconcerts.Sotobeabletohave

morepeopleexperiencethemthroughVR…thatwouldbeepic.”

MileyCyrus

Singer/Songwriter

©BDMI,Nov2015 7

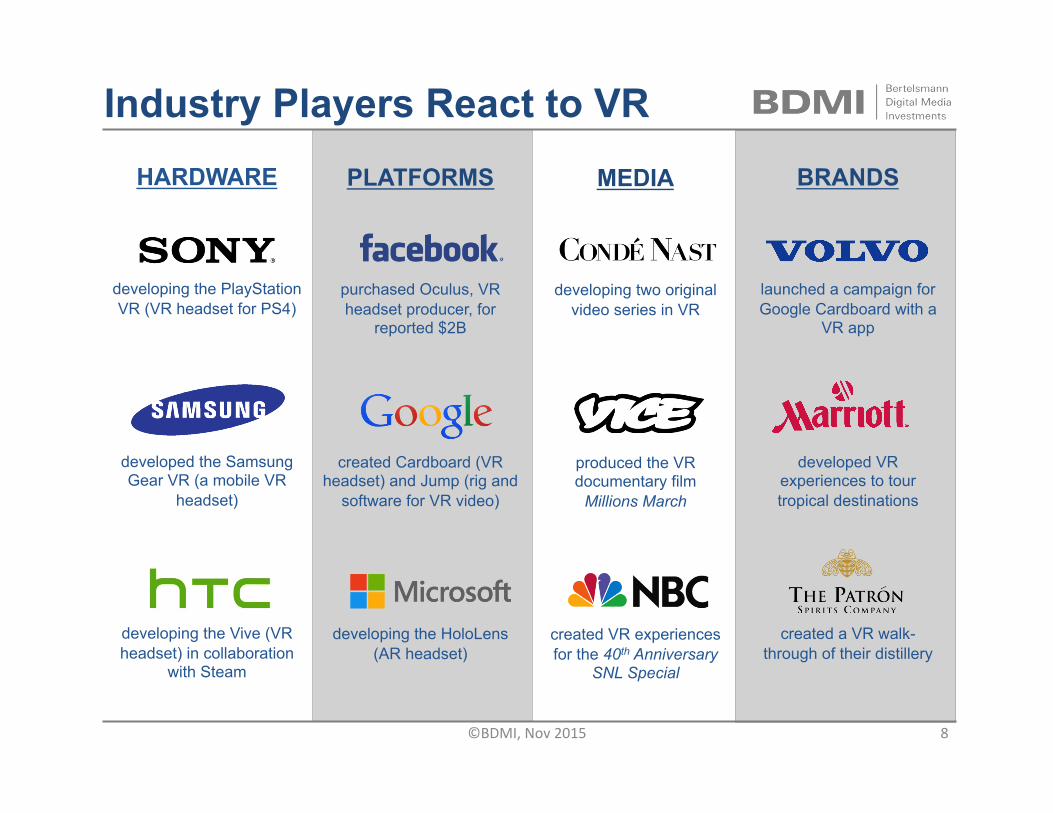

Industry Players React to VR

PLATFORMS

purchased Oculus, VR headset producer, for

reported $2B

created Cardboard (VR headset) and Jump (rig and

software for VR video)

developing the HoloLens (AR headset)

HARDWARE

developing the PlayStation VR (VR headset for PS4)

developed the Samsung Gear VR (a mobile VR

headset)

developing the Vive (VR headset) in collaboration

with Steam

MEDIA

developing two original video series in VR

produced the VR documentary film

Millions March

created VR experiences for the 40th Anniversary

SNL Special

BRANDS

launched a campaign for Google Cardboard with a

VR app

developed VR experiences to tour tropical destinations

created a VR walk-through of their distillery

©BDMI,Nov2015 8

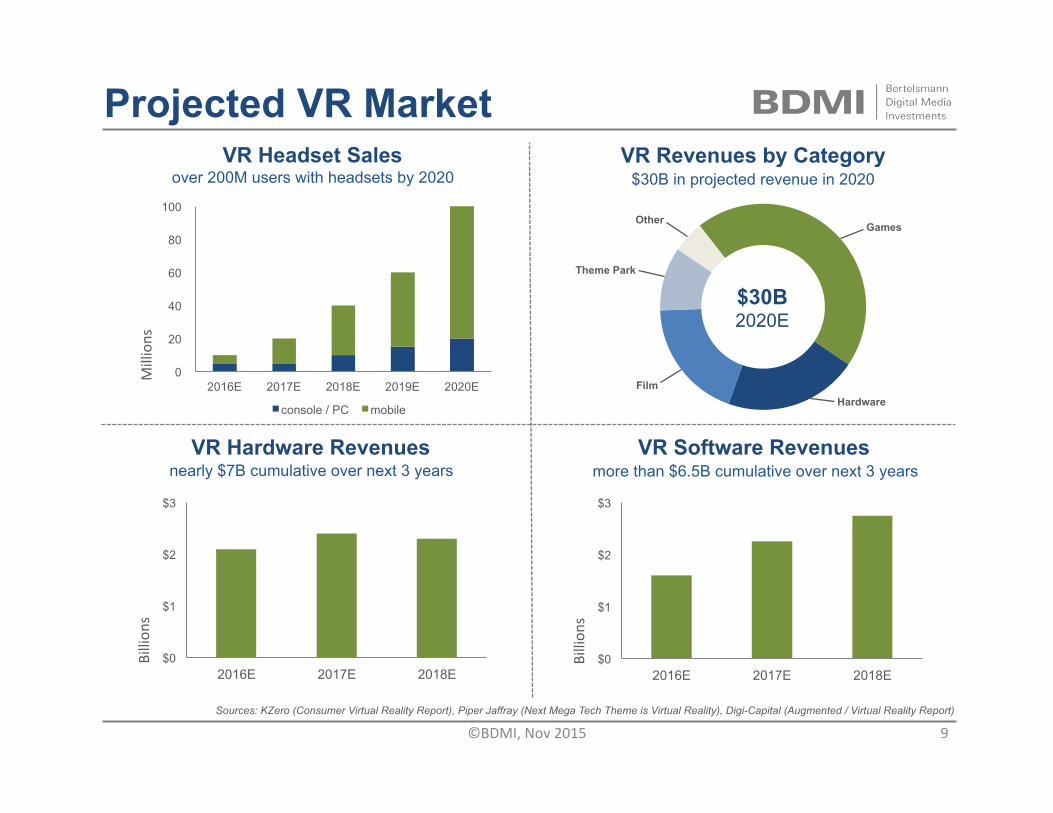

Games

Hardware Film

Theme Park

Other

Projected VR Market

0

20

40

60

80

100

2016E 2017E 2018E 2019E 2020E

Millions

console / PC mobile

VR Headset Sales

VR Hardware Revenues VR Software Revenues

VR Revenues by Category

$30B 2020E

nearly $7B cumulative over next 3 years more than $6.5B cumulative over next 3 years

over 200M users with headsets by 2020 $30B in projected revenue in 2020

$0

$1

$2

$3

2016E 2017E 2018E

Billion

s

$0

$1

$2

$3

2016E 2017E 2018E

Billion

s

Sources: KZero (Consumer Virtual Reality Report), Piper Jaffray (Next Mega Tech Theme is Virtual Reality), Digi-Capital (Augmented / Virtual Reality Report)

©BDMI,Nov2015 9

Games

Hardware Film

Theme Park

Other

Projected VR Market

0

20

40

60

80

100

2016E 2017E 2018E 2019E 2020E

Millions

console / PC mobile

VR Headset Sales

VR Hardware Revenues VR Software Revenues

VR Revenues by Category

$30B 2020E

more than $8B cumulative over 4 years more than $7.5B cumulative over 4 years

over 200M users with headsets by 2020 $30B in projected revenue in 2020

Sources: KZero (Consumer Virtual Reality Report), Piper Jaffray (Next Mega Tech Theme is Virtual Reality), Digi-Capital (Augmented / Virtual Reality Report)

$0

$1

$2

$3

2015E 2016E 2017E 2018E

Billion

s

$0

$1

$2

$3

2015E 2016E 2017E 2018E

Billion

s

©BDMI,Nov2015 10

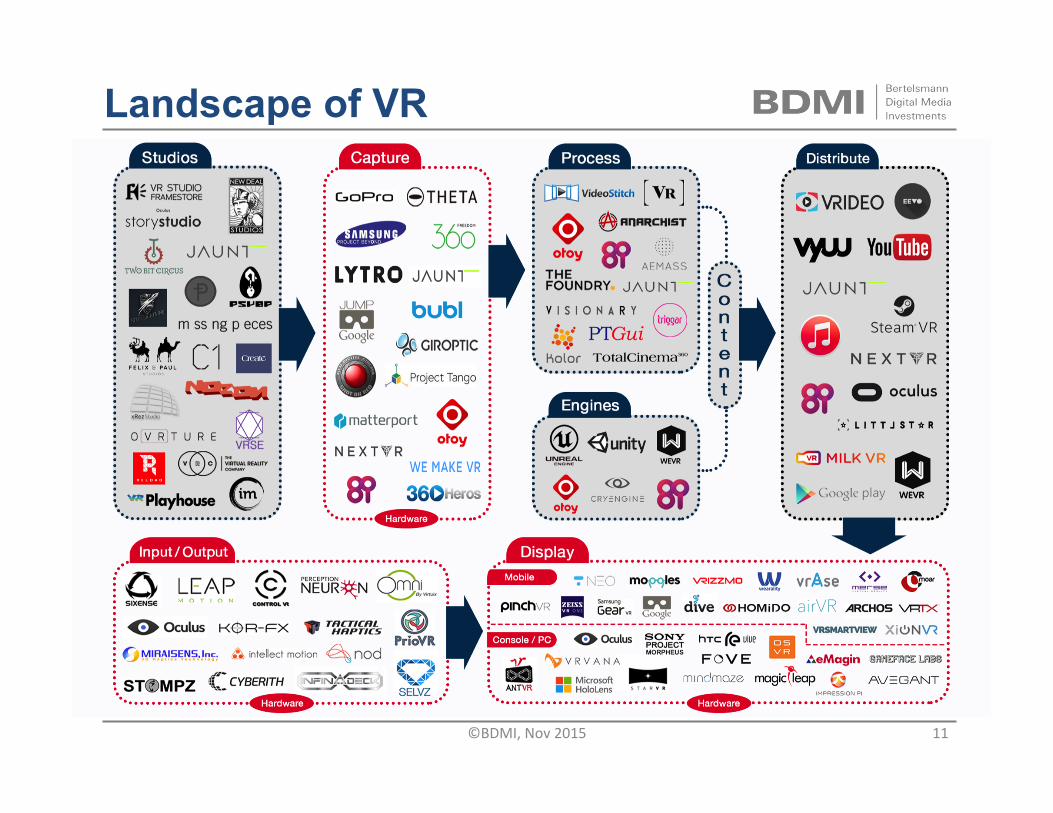

Landscape of VR

©BDMI,Nov2015 11

VR Studios Jurassic World FILM | COMPUTER-GENERATED

Interact with an Apatosaurus up close and personal in this companion experience.

Watch Sir Paul McCartney in concert performing Live and Let Die in a cinematic VR experience.

Paul McCartney MUSIC | LIVE-ACTION

Volvo Reality ADVERTISING | BLENDED

Test drive the Volvo XC90 in a beautiful journey through Vancouver.

©BDMI,Nov2015 12

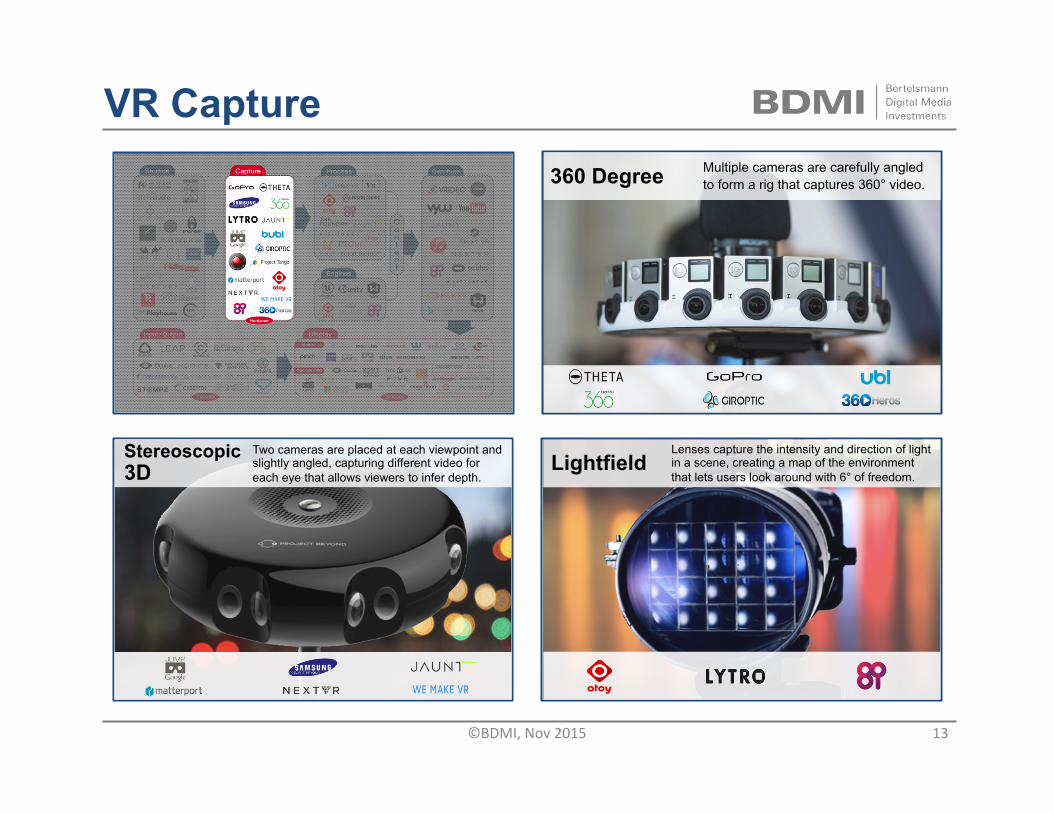

VR Capture 360 Degree

Stereoscopic 3D Lightfield

Multiple cameras are carefully angled to form a rig that captures 360° video.

Two cameras are placed at each viewpoint and slightly angled, capturing different video for each eye that allows viewers to infer depth.

Lenses capture the intensity and direction of light in a scene, creating a map of the environment that lets users look around with 6° of freedom.

©BDMI,Nov2015 13

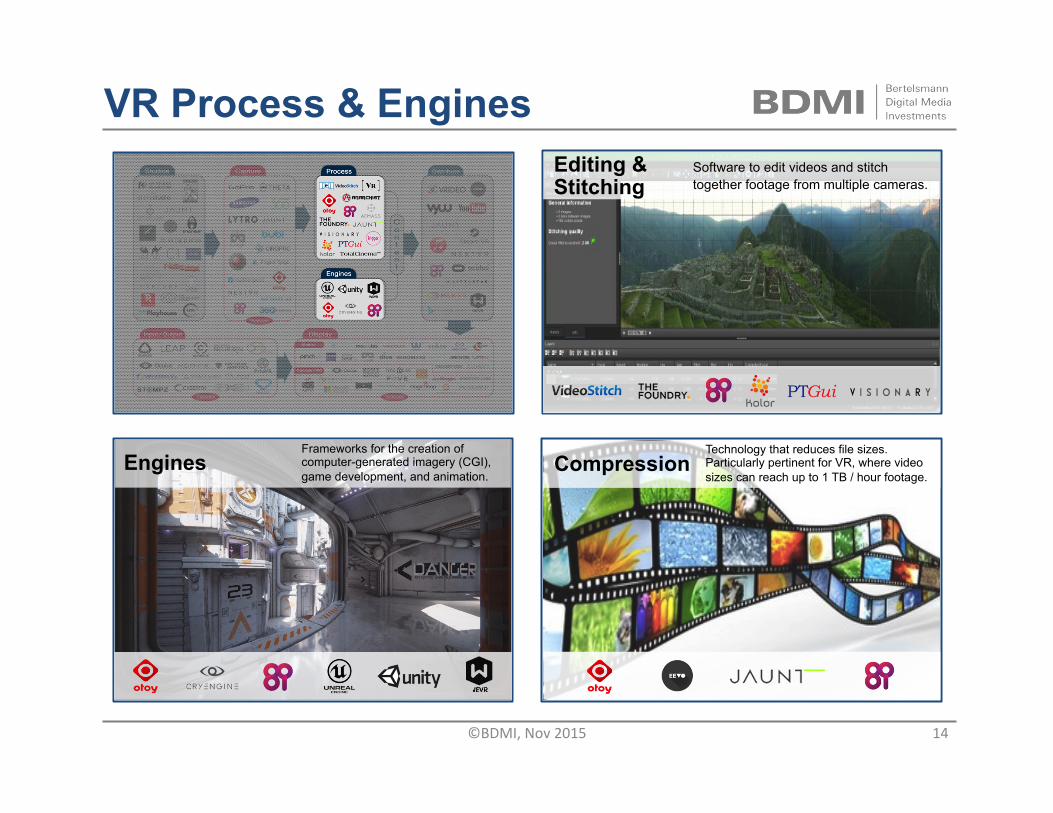

VR Process & Engines Editing & Stitching

Compression Engines

Software to edit videos and stitch together footage from multiple cameras.

Frameworks for the creation of computer-generated imagery (CGI), game development, and animation.

Technology that reduces file sizes. Particularly pertinent for VR, where video sizes can reach up to 1 TB / hour footage.

©BDMI,Nov2015 14

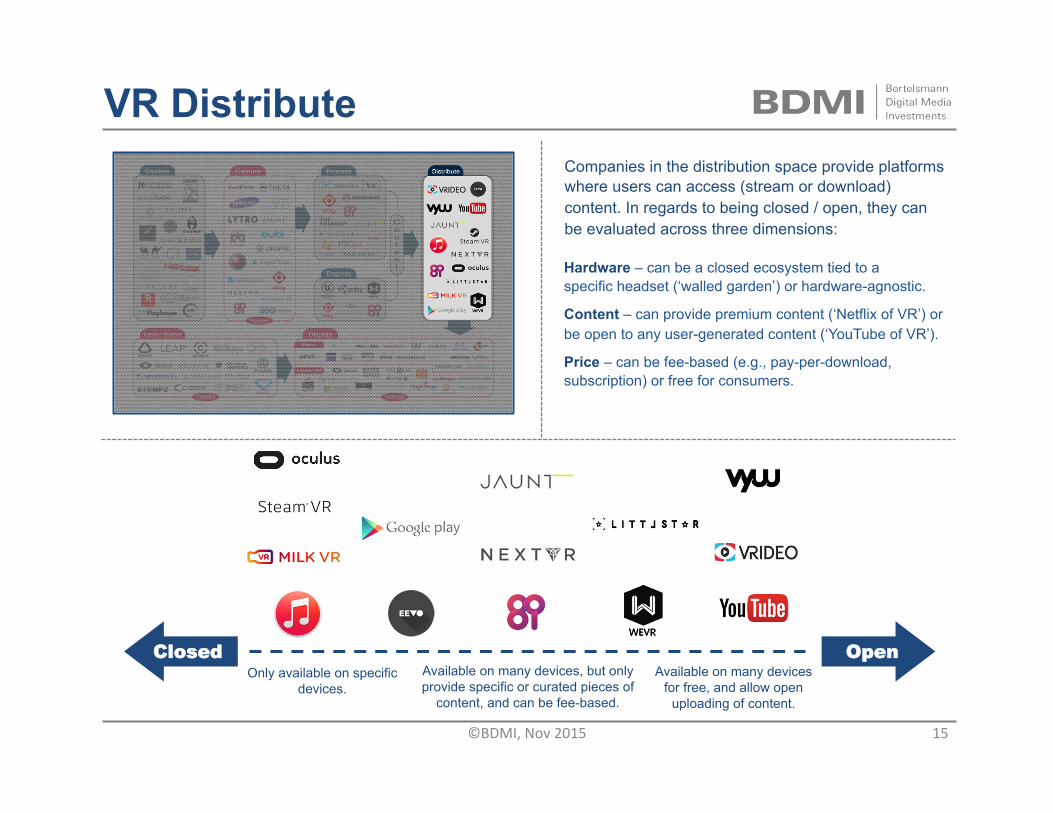

VR Distribute

Closed Open

Companies in the distribution space provide platforms where users can access (stream or download) content. In regards to being closed / open, they can be evaluated across three dimensions:

Only available on specific devices.

Available on many devices, but only provide specific or curated pieces of

content, and can be fee-based.

Available on many devices for free, and allow open

uploading of content.

Hardware – can be a closed ecosystem tied to a specific headset (‘walled garden’) or hardware-agnostic.

Content – can provide premium content (‘Netflix of VR’) or be open to any user-generated content (‘YouTube of VR’).

Price – can be fee-based (e.g., pay-per-download, subscription) or free for consumers.

©BDMI,Nov2015 15

VR Display Mobile Low-End – Best for first, introductory VR experiences and quick demonstrations.

§ Pros – least expensive, portable, only requires smartphone § Cons – basic tracking, limited input (i.e., button)

Mobile High-End – Best for casual consumption and viewing short-form content.

§ Pros – input included, moderate tracking ability, portable, only requires smartphone

§ Cons – limited computing power, basic input, can require specific smartphone

PC / Console – Best for early adopters and hardcore gaming enthusiasts.

§ Pros – best tracking, most computing power, best content § Cons – most expensive, not very portable, requires external computer

Mobile Low-End Mobile High-End PC / Console

Name Google Cardboard Wearality MergeVR Samsung Gear VR Oculus Rift PlayStation VR

Price ~$20-30 ~$69 ~$129 $200 $350-450 $300-400

Display requires smartphone requires smartphone

requires smartphone

requires Samsung S6 or Note 4 integrated integrated

Computing requires smartphone requires smartphone

requires smartphone

requires Samsung S6 or Note 4

requires gaming PC (~$1000)

requires PS4 ($399)

Tracking requires smartphone requires smartphone

requires smartphone / integrated integrated integrated integrated

Input button on headset not included included touchpad on headset included included

©BDMI,Nov2015 16

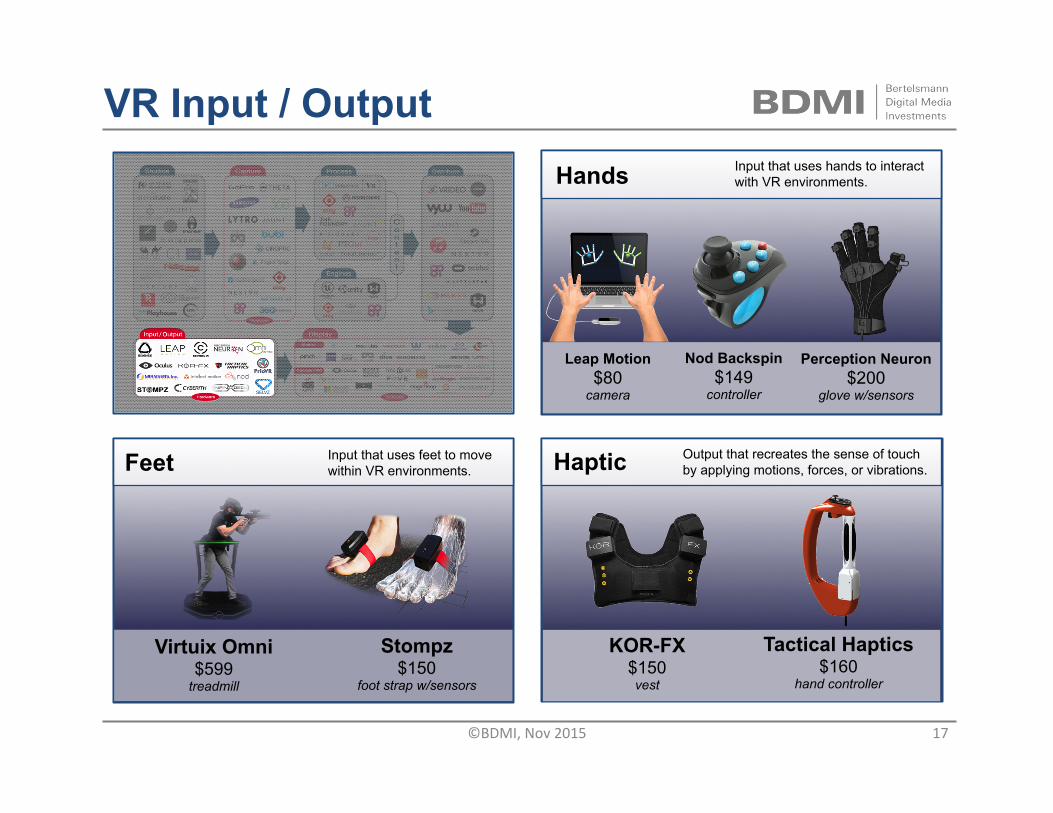

VR Input / Output Hands

Haptic Feet

Input that uses hands to interact with VR environments.

Leap Motion $80

camera

Nod Backspin $149

controller

Virtuix Omni $599

treadmill

KOR-FX $150 vest

Tactical Haptics $160

hand controller

Perception Neuron $200

glove w/sensors

Input that uses feet to move within VR environments.

Stompz $150

foot strap w/sensors

Output that recreates the sense of touch by applying motions, forces, or vibrations.

©BDMI,Nov2015 17

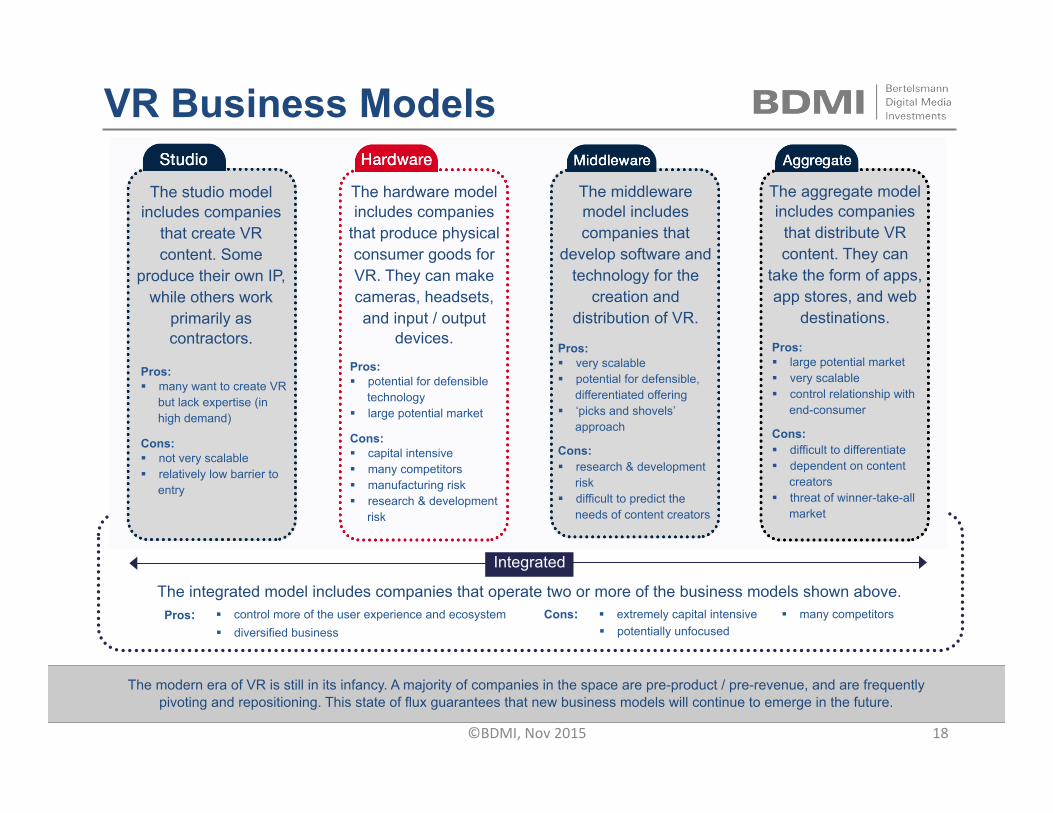

VR Business Models

Integrated

The modern era of VR is still in its infancy. A majority of companies in the space are pre-product / pre-revenue, and are frequently pivoting and repositioning. This state of flux guarantees that new business models will continue to emerge in the future.

The studio model includes companies

that create VR content. Some

produce their own IP, while others work

primarily as contractors.

The hardware model includes companies

that produce physical consumer goods for VR. They can make cameras, headsets, and input / output

devices.

The middleware model includes companies that

develop software and technology for the

creation and distribution of VR.

The aggregate model includes companies

that distribute VR content. They can

take the form of apps, app stores, and web

destinations.

The integrated model includes companies that operate two or more of the business models shown above.

Pros: § many want to create VR

but lack expertise (in high demand)

Cons: § not very scalable § relatively low barrier to

entry

Pros: § potential for defensible

technology § large potential market

Cons: § capital intensive § many competitors § manufacturing risk § research & development

risk

Pros: § very scalable § potential for defensible,

differentiated offering § ‘picks and shovels’

approach

Cons: § research & development

risk § difficult to predict the

needs of content creators

Pros: § large potential market § very scalable § control relationship with

end-consumer

Cons: § difficult to differentiate § dependent on content

creators § threat of winner-take-all

market

Pros: Cons: § diversified business

§ many competitors § potentially unfocused

§ control more of the user experience and ecosystem § extremely capital intensive

©BDMI,Nov2015 18

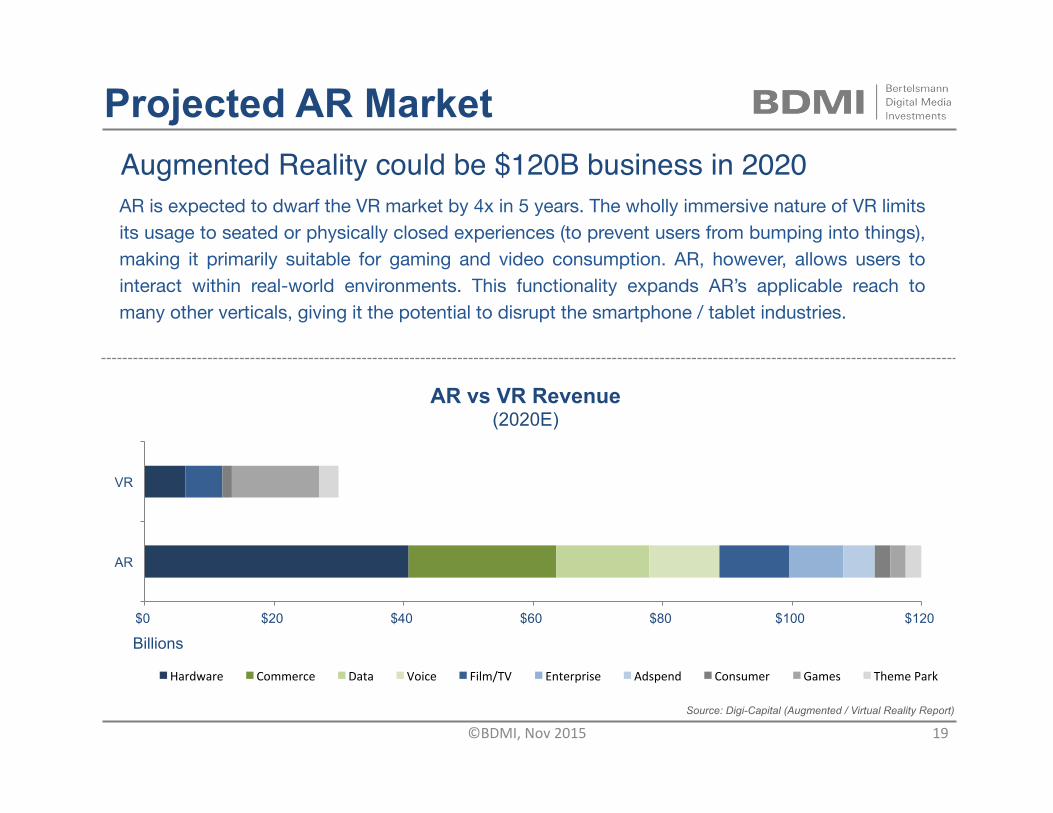

Augmented Reality could be $120B business in 2020

$0 $20 $40 $60 $80 $100 $120

AR

VR

Billions

Hardware Commerce Data Voice Film/TV Enterprise Adspend Consumer Games ThemePark

Projected AR Market

AR vs VR Revenue (2020E)

AR is expected to dwarf the VR market by 4x in 5 years. The wholly immersive nature of VR limits its usage to seated or physically closed experiences (to prevent users from bumping into things), making it primarily suitable for gaming and video consumption. AR, however, allows users to interact within real-world environments. This functionality expands AR’s applicable reach to many other verticals, giving it the potential to disrupt the smartphone / tablet industries.

Source: Digi-Capital (Augmented / Virtual Reality Report)

©BDMI,Nov2015 19