the effect of deadline imposed time pressure on …...the effect of deadline imposed time pressure...

TRANSCRIPT

The Effect of Deadline Imposed Time Pressure on Audit Quality

Steven M. Glover

School of Accountancy

Marriott School of Business

Brigham Young University, Provo, UT

James C. Hansen

School of Accounting and Taxation

Goddard School of Business and Economics

Weber State University, Ogden, UT

and

Timothy A. Seidel

School of Accountancy

Jon M. Huntsman School of Business

Utah State University, Logan, UT

February 2015

Acknowledgements: We thank Linda Myers, Tom Omer, Roy Schmardebeck, Jacob Haislip,

Keith Jones, Brant Christensen, Derek Oler, Matt Sherwood, Erik Beardsley, workshop

participants at Utah State University, and conference participants at the 2014 BYU Accounting

Research Symposium and the 2015 American Accounting Association Auditing Section Midyear

Meeting for helpful comments and suggestions.

The Effect of Deadline Imposed Time Pressure on Audit Quality

ABSTRACT: We examine the association between deadline imposed time pressure and audit

quality. Using different measures of audit quality, we find consistent evidence of lower audit

quality when auditors are under heightened deadline imposed time pressure. We find that these

negative effects persist even among auditors with more resources at their disposal. Our findings

suggest that auditors completing procedures at or near the required (or extended) filing deadline

may compromise audit quality to meet the reporting requirement. There is substantial interest by

regulators and the auditing profession in identifying observable indicators of audit quality. Our

results suggest that the audit report date could be such an indicator—unfortunately, an accounting

standard change in 2009 had the unintended consequence of essentially eliminating the

information content of the audit report date and as a result financial statement users now have less

opportunity to identify auditors under heightened deadline imposed time pressure.

Keywords: audit quality; deadline imposed time pressure; misstatements

1

I. INTRODUCTION

The Public Company Accounting Oversight Board (PCAOB) issued Staff Audit Practice

Alert No. 10 on December 4, 2012, which addresses professional skepticism in audits. The

PCAOB Office of the Chief Auditor issued the report because of observations from PCAOB

oversight activities that “raised concerns about whether auditors consistently and diligently apply

professional skepticism” (PCAOB 2012a, 1). In the section titled “Impediments to the

Application of Professional Skepticism” the alert reads:

“…scheduling and workload demands can put pressure on partners and other engagement

team members to complete their assignments too quickly, which might lead auditors to

seek audit evidence that is easier to obtain rather than evidence that is more relevant and

reliable, to obtain less evidence than is necessary, or to give undue weight to confirming

evidence without adequately considering contrary evidence” (PCAOB 2012a, 7).

Jay Hanson, PCAOB Board Member, highlighted similar concerns in a speech on March 28,

2014 stating that:

“One of the biggest impediments to auditor skepticism, however, in my view, is the

calendar. Public companies have filing deadlines to meet, and they are rarely missed.

When they are missed, the consequences can be serious, including declining share prices

and harm to investors. If potential issues are discovered late in the audit process, or an

issue is not resolved in a timely manner, auditors may feel pressure to cut corners. We

have seen it in inspections and enforcement matters: Auditors recognize that there may be

a problem with management's estimates or conclusions but allow themselves to be talked

out of doing anything about it. Staying organized and proactively dealing with problems

far ahead of filing deadlines will help the auditor avoid running out of time as well as the

pressure to accept insufficient audit evidence” (Hanson 2014).

These concerns suggest that impediments to auditor skepticism, such as imposed time pressure,

can result in lower quality audits. Prior academic studies have examined the effect of time

pressure (i.e., time budget pressure, deadline time pressure, etc.) on auditor judgment and

performance in experimental settings (e.g. McDaniel 1990; Choo 1995; Glover 1997). In

general, these studies find that time pressure produces negative effects, although there are

2

specific contexts where time pressure does not affect or can positively affect auditor judgment.1

A recent survey of public company auditors indicates that the timeliness of completing audit

fieldwork is associated with audit quality (Christensen et al. 2014). In this study we use archival

evidence to examine broadly whether deadline imposed time pressure affects audit quality.

Auditors of public companies with periodic Securities and Exchange Commission (SEC)

reporting requirements subject auditors to a compressed timeframe in which to obtain sufficient

evidence to form a basis for their opinion on the financial statements. Thus, periodic financial

reporting deadlines create deadline imposed time pressure. Although prior experimental and

qualitative findings suggest deadline imposed time pressure produces negative effects in general,

consistent evidence from qualitative, experimental, and archival methodologies can strengthen

the robustness of findings and enhance the generalizability of results by mitigating concerns

about internal and external validity (Allee et al. 2007).2

We construct our proxy for deadline imposed time pressure by identifying the date of the

auditor’s report and counting the days between the audit report date and a company’s required

10-K filing deadline. We use the audit report date because it is the date the auditor has gained

sufficient evidence to form the opinion on the financial statements.3 We consider firms to be

under high deadline pressure when the audit report date is near (within seven days), at, or slightly

1 For example, Glover (1997) finds that deadline pressure can reduce the influence of irrelevant information on

auditors’ judgment. 2 See Allee et al. (2007) as an example of the benefit of examining a research question with multiple methodologies.

Although they examine an unrelated research question, they use archival data to complement prior experimental

findings. 3 Although it may be argued that substantial evidence has been gathered by the time earnings are released, the

earnings release is not audited and firms insist that audit procedures are typically still in process after the earnings

release (see U.S. Securities and Exchange Commission (SEC). 2002a. Summary of Comments Relating to Proposed

Amendments to Accelerate Periodic Report Filing Dates and Disclosure Concerning Website Access to Reports.

Release No. 33-8089. Washington, D.C.: SEC. Available at: http://www.sec.gov/rules/extra/33-8089summary.htm.)

In addition, prior research finds that since 2002, the earnings announcement release lag has shortened. Bronson et

al. (2014) find that only 32 percent of companies waited until the date of the auditor’s report to release earnings in

2004 and this percentage declined even further to less than 10 percent by 2011.

3

beyond the original (or extended) required filing deadline. We proxy for compromised audit

quality using material misstatements (as revealed through subsequent financial statement

restatements) and the subsequent receipt of an SEC comment letter related to a company’s Form

10-K for Generally Accepted Accounting Principles (GAAP) or disclosure related issues—

consistent with findings in a recent survey of auditors and investors that both financial statement

restatements and SEC comment letters are leading indicators of lower audit quality (Christensen

et al. 2014). In our analysis, we control for variables that have been shown in prior literature to

affect our measures of audit quality.

We find a positive association between audits completed under deadline imposed time

pressure and our measures of compromised audit quality.4 We find consistent results using a

matched sample based on the propensity to be under high deadline imposed time pressure. These

results are robust to: (1) separately examining subsamples of large (i.e., large accelerated filers),

mid-size (i.e., accelerated filers), and small (i.e., non-accelerated filers) companies with a similar

required deadline; (2) controlling for internal deadline pressure; (3) controlling for engagement-

level budget pressure; (4) excluding companies with high uncertainty (i.e., high volatility in

revenues); (5) excluding companies that release fourth quarter earnings well in advance of the

audit report date; and (6) different types of misstatements (i.e., those related to accounts or

transactions that are typically completed late in the audit process and all others). In additional

analyses, we examine whether auditors with more resources are able to mitigate the negative

effect of deadline imposed time pressure. With certain exceptions, we find little evidence to

suggest that large auditors (Big N auditors), auditors in larger offices, and auditors of clients with

4 In terms of economic magnitude, the odds of misstatement (subsequent receipt of an SEC comment letter) among

companies where the audit report date is on the required SEC filing deadline is 40 (17) percent higher than the odds

of misstatement (subsequent receipt of an SEC comment letter) among companies whose audit report date is not on

the required filing deadline.

4

non-busy season fiscal year-ends are able to effectively mitigate the negative impact of deadline

imposed time pressure on audit quality. Consistent with the negative effects of deadline imposed

time pressure found in prior experimental studies, our findings suggest that auditors completing

procedures at or near the required filing deadline (or extended deadline) may compromise audit

quality, consistent with regulator concerns of foregoing audit procedures or obtaining less than

sufficient evidence to meet the required filing deadline.

These findings also have implications for regulators, standard setters, academics, audit

professionals, and investors. Initiatives to identify observable indicators of audit quality are on

the agendas of the International Auditing and Assurance Standards Board (IAASB 2013), the

Public Company Accounting Oversight Board (PCAOB 2012b, 2013, 2014), the American

Institute of Certified Public Accountants (AICPA 2014), the Center for Audit Quality (CAQ

2014), as well as audit firms themselves (KPMG 2011; PwC 2014). Although the opening quotes

from the PCAOB suggest a concern with the potential negative effect of deadline imposed time

pressure, the PCAOB’s discussion of audit quality indicators (AQI) does not include a measure

of the timeliness of the completion of audit fieldwork (PCAOB 2013). Our results suggest that,

in addition to the other potential AQIs suggested by the PCAOB, a potentially observable

indicator of audit quality would be the date the auditors completed fieldwork. Prior to 2009, that

date coincided with the auditor’s report date. However, this reporting convention changed in

response to Statement of Financial Accounting Standards (SFAS) No. 165 (now codified in

Accounting Standards Codification (ASC) Topic 855). SFAS No. 165, issued in 2009, requires

companies to evaluate subsequent events through the date the financial statements are issued

(i.e., the filing date of the financial statements with the SEC). In response to this change in

GAAP, current auditor practice is to date the audit report in conjunction with the filing of the

5

financial statements with the SEC. As such, users of the financial statements have less visibility

into when auditors obtain sufficient audit evidence to support their opinion and therefore, less

opportunity to identify auditors under heightened deadline imposed time pressure. Although

unintentional, this highlights one potential negative effect of SFAS No. 165 (ASC 855). We

believe this has important implications for the PCAOB’s project regarding potential AQIs and

their project to improve the auditor’s reporting model.5 Our findings suggest that an important

AQI could be provided in the auditor’s report in the form of dual-dating of the audit opinion to

clearly convey the date of the end of audit fieldwork (first date) as well as the date through which

subsequent events were considered (second date). Therefore, our findings suggest in the

PCAOB’s consideration of additional communication and enhancements to the auditors’ report,

they consider requiring auditors to report the date fieldwork was completed.

The remainder of the paper is organized as follows. We discuss prior research and

develop our hypothesis in Section II. We provide a description of our sample selection and

empirical methods in Section III. We describe our results in Section IV. In the final section, we

summarize the key results and provide conclusions.

II. PRIOR LITERATURE AND HYPOTHESIS DEVELOPMENT

Ordonez and Benson (1997, 122) state the following:

“Time constraint exists whenever there is a time deadline, even if the person is able to

complete the task in less time. Time pressure indicates that the time constraint induced

some feeling of stress and created a need to cope with the limited time.”

The increased levels of stress associated with time pressure, impacts cognitive processes

(Lundberg 1993; Maule and Hockey 1993) and negates benefits obtained from receiving training

5 In August 2013, the PCAOB issued for public comment proposed auditing standards and related amendments on

the auditor’s report. Proposed enhancements include the communication of critical audit matters, new elements of

the report related to auditor independence, auditor tenure, the auditor’s responsibilities for other information outside

the financial statements, and enhanced communication related to auditors’ responsibilities for fraud.

6

in a specific task (Zakay and Wooler 1984). DeZoort (1998) suggests two primary types of time

pressure in the audit literature: time budget pressure and time deadline pressure.6 Deadline

pressure arises from the anticipation of penalties (implicit and/or explicit) of not meeting a goal

by a predetermined point in time (Hogarth 1990). Mano (1990) posits that in daily life

individuals adjust their actions to avoid the penalties associated with missing deadlines. These

adjustments in action can include working faster at the task at hand, lowering the quality of

performance on the task, or disregarding less important tasks. In our study, we refer this type of

time pressure as deadline imposed time pressure.

Although time budget pressure and deadline imposed audit pressure are often related and

overlapping, prior research suggests they are not identical. Kelley et al. (1999) survey both Big-

6 and non Big-6 auditors (audit staff and seniors) and find that senior auditor respondents report

that they face deadline imposed time pressure more often than time budget pressure. Seniors

report that they experience more pressure and stress from deadline imposed time pressure than

from time budget pressures. Staff auditors report that they face deadline imposed time and

budget pressures equally, and report equal pressure and stress from each. Both senior and staff

auditors associate poorer audit quality with time budget pressure than with deadline imposed

time pressure. Christensen et al. (2014) survey audit professionals and investors and find that

audit partners view the timely completion of the audit as relating to higher quality, but neither

audit partners nor investors view profitability as being related to quality, suggesting time

pressure rather than budget pressure affects audit quality.

Several experimental studies find, in general, that time pressure can negatively impact

audit quality (see e.g., Rhode 1978; Alderman and Deitrick 1982; Kelley and Margheim 1990;

6 See DeZoort and Lord (1997) and DeZoort (1998) for a discussion of research that examines time budget pressure.

7

McDaniel 1990; Ragunathan 1991; Willet and Page 1996; Bennett et al. 2014). However, prior

research also suggests that this negative impact may depend on the type of time pressure (i.e.,

time budget pressure vs. deadline imposed time pressure), the setting (i.e., the risk of

misstatement), and the experience of the auditor. Margheim et al. (2005) find that although both

time budget and deadline imposed time pressures increase stress levels, deadline imposed time

pressure does not affect all levels of auditors the same. In their experiment, they find that staff

auditors under deadline imposed time pressure will exhibit more dysfunctional behaviors that

negatively affect audit quality than senior auditors in the same setting.7 Coram et al. (2004)

examine experimentally whether auditors faced with differing levels of both budget time

pressure and the risk of misstatement will respond with reduced audit quality choices (i.e.

accepting doubtful audit evidence and truncating a selected sample). They find that auditors will

accept doubtful audit evidence when working under high budget time pressure, regardless of

whether the risk of misstatement is high or low. Coram et al. (2004) also find that auditors will

truncate a selected sample when time pressure is high, but only when the risk of misstatement is

low. Other experimental studies have examined whether the experience of the auditor

determines whether time pressure affects audit quality. Bamber and Bylinski (1987) examine

how managers estimate review hours needed (opinion formulation phase) to review audit testing

on accounts that are either generally considered material or immaterial. Audit deadline imposed

time pressure is manipulated between groups when the managers are estimating the time actually

needed to review accounts. They find that managers budget more time for accounts that are

material and accounts identified as critical in the planning phase. When estimating the time

7 Margheim et al. (2005) report that both staff and senior auditor subjects exhibit dysfunctional behaviors when

faced with time deadline pressure, although the staff auditors are expected to exhibit a larger variety of

dysfunctional behaviors.

8

actually needed to review accounts when audit testing is completed, time pressure had no effects

on the managers’ judgments.

Prior experimental studies focusing exclusively on deadline imposed time pressure

generally suggest that it has a negative effect on auditor judgments and decisions. For example,

McDaniel (1990) examines whether audit effectiveness is decreased in the presence of deadline

imposed time pressure and a structured audit program. She finds that greater levels of deadline

imposed time pressure result in more errors in auditing inventory, regardless of whether a

structured audit program is used. In contrast, Glover (1997) finds that deadline imposed time

pressure can reduce the influence of irrelevant information on auditors’ judgment. Consistent

with this finding, Choo (1995) finds that auditors’ judgment improved when deadline imposed

time pressure moved from low to moderate levels. However, Choo (1995) finds that when

deadline imposed time pressure moves from moderate to high levels, auditors’ judgment

performance declines, due to the disregard of relevant cues. Psychology research shows that

time pressure and job effectiveness exhibit an inverted U-shaped function (Easterbrook 1959).

Choo (1995) finds that this theory has the highest explanatory power for his results. A typical

audit would be at the uppermost point of the inverted U-shaped function (i.e. a standard audit

will have a moderate level of deadline imposed time pressure). Therefore as deadline imposed

time pressure increases in an audit, the job effectiveness will decrease. McDaniel (1990)

supports this argument and sets up her study where the lowest level of deadline imposed time

pressure is at the apex of the U-shaped function.

Additionally, prior research also provides some evidence that the cause of the deadline

imposed time pressure influences whether time pressure affects audit quality. Bennet and

Hatfield (2014) perform an experiment examining whether deadline imposed time pressure

9

affects auditors’ judgments about materiality and sufficiency of audit evidence in relation to

reporting on the effectiveness of internal control over financial reporting. They find that auditors

under deadline imposed time pressure assess a higher level of materiality thus reducing sample

sizes when they are, at least in part, responsible for the deadline imposed time pressure (i.e.,

started internal control testing late in the year, etc.).

Although the effect of time pressure, including deadline pressure, on audit quality has

been examined experimentally, there is a dearth of archival studies related to this topic. One

related archival study by Lambert et al. (2014) examines whether mandated changes in required

filing deadlines (shortening of required filing deadlines) negatively impacts earnings quality. In

periods of shortened deadlines, they find higher discretionary accruals. Blankley et al. (2014)

examines the relationship between audit report lags and future restatements and find that higher

abnormal audit report lags have a greater likelihood of future restatement.8 Another study by

Lopez and Peters (2012) examines whether auditor workload compression, measured as the

number of clients within an auditor office with a similar fiscal year-end, affects audit quality.

They find Big-N auditors with greater workload compression have larger discretionary accruals.

These studies suggest that shortened filing deadlines and more compressed auditor workloads

can have a negative effect on clients’ earnings quality.

Public companies with required reporting deadlines subject auditors to a compressed

timeframe in which to obtain sufficient evidence to form a basis for their opinion on the financial

statements. When auditors are completing required audit procedures at or very near the SEC 10-

8 In additional analysis, Blankley et al. (2014) include an indicator variable in their restatement model for whether

the company is within 5 days of the SEC deadline. They do not find a significant result on this variable, but do find

that the interaction of this indicator with abnormal audit lag is positively related to future restatements. Given that

the abnormal audit lag variable in essence captures missing an internal deadline, which we identify and include as a

control in additional analysis, and given the dynamics of accurately capturing external deadline pressure (i.e.,

identifying the right filer status and year, adjusting for weekends and holidays, etc.), we believe our results add

further insight into the direct effects of external deadline imposed time pressure on audit quality.

10

K filing deadline the deadline imposed time pressure is high and may compromise audit quality.

Thus, we hypothesize the following (stated in the alternative form):

Hypothesis: Audit quality is lower for auditors under tight deadline imposed time

pressure relative to auditors under less deadline imposed time pressure.

III. SAMPLE SELECTION AND RESEARCH DESIGN

Sample Selection

Our sample is comprised of all client-year observations with a fiscal year-end between

June 1, 2000 and June 15, 2009 with sufficient data from Compustat, the Center for Research in

Security Prices (CRSP), and Audit Analytics to construct our model variables. We exclude

foreign filers subject to different filing deadlines,9 as well as client-year observations where the

company delists from a public stock exchange between the filing date and the subsequent year

filing date.10 Our sample period begins in 2000 due to availability of restatement data, and ends

in 2009 due to changes in practice related to the dating of audit reports as a result of accounting

standard changes. In May 2009, the Financial Accounting Standards Board (FASB) issued

SFAS No. 165, Subsequent Events (now codified in ASC 855), effective for fiscal years ending

after June 15, 2009. Before the issuance of SFAS No. 165, auditors would date their report when

sufficient evidence was obtained to support the audit opinion. As such, in many instances, the

auditor dated the audit opinion before the financial statements were widely distributed.

Following the adoption of SFAS No. 165, public companies are required to evaluate subsequent

events through the financial statement filing date. Although there are no auditor requirements in

9 Foreign filers are identified using Audit Analytics variable FORM_FKEY. We exclude those where

FORM_FKEY is listed as 20-F or 40-F. We only include observations where FORM_FKEY is listed as 10-K,

10KSB, or 10-K405. 10 We identify observations of delisting due to bankruptcy, liquidation, or other events using Compustat variable

DLRSN. We exclude observations where DLRSN equals 02 (bankruptcy), 03 (liquidation), 07 (Other - no longer

files with SEC among other reasons but pricing continues), 09 (now a private company), or 10 (Other - no longer

files with SEC among other reasons).

11

the standard, auditors began dating their opinions on the date the financial statements are filed

with the SEC.11

To examine whether the practice of dating of the audit report date changed after SFAS

No. 165, we provide descriptive statistics of the reporting lag (the number of days between the

company’s fiscal year-end and the filing of the 10-K), the audit report lag (the number of days

between the company’s fiscal year-end and the date of the auditor’s report), and the number of

days between the audit report date and the 10-K filing date (DAYSBTW). We obtain dates for

all company-year observations filing a 10-K, 10-KSB, or 10-K405 in Audit Analytics from 2000

through 2013. Table 1 provides the distributions of each of these variables in both the pre- and

post-SFAS No. 165 periods. Panel A provides the distributions for all available company-year

observations and Panel B provides the distributions for all company-year observations with a Big

N auditor. In the pre-SFAS No. 165 period, we find that mean reporting lag is approximately 81

days while the mean audit report lag is approximately 61 days. In the post-SFAS No. 165

period, the mean reporting lag is approximately 74 days while the mean audit report lag is

approximately 72 days. In addition, the distribution of the number of days between the audit

report date and the filing date (DAYSBTW) varies widely in the pre-SFAS No. 165 period,

while in the post-SFAS No. 165 period, the entire distribution is close to zero providing

empirical support for the practice of dating the audit report close to or on the date of filing.

Next, we perform tests of our hypothesis by first identifying the required filing deadline

for each company-year observation in the sample. We calculate the required filing date using the

company’s fiscal year-end and adding the appropriate number of days based on the company’s

11 The PCAOB Standing Advisory Group discussed this in their meeting on July 15, 2010. A webcast of the

discussion can be found at http://pcaobus.org/News/Webcasts/Pages/07152010_SAGMeeting.aspx

12

filer status and fiscal year, adjusted for holidays and weekends.12 Historically, SEC registrants

had ninety days to file the annual report. However, in September 2002, the SEC approved a

Final Rule that changed the deadlines for submitting periodic financial reports (e.g., 10-K and

10-Q) for accelerated filers. Accelerated filers are SEC registrants that have a public float of at

least $75 million, have been subject to the SEC’s reporting requirements for at least twelve

calendar months, previously have filed at least one annual report, and are not eligible to file their

quarterly and annual reports on Forms 10-QSB and 10-KSB. Beginning in December 2003,

accelerated filers are required to file their annual financial reports within 75 days of the

company’s fiscal year-end. Although the SEC’s rule would eventually shorten this window to 60

days, this ruling was postponed and eventually, in 2005, overruled. In December 2005, the SEC

voted to adopt amendments to create a new category of large accelerated filers, which would

include companies with a public float of $700 million or more. Large accelerated filers were

subject to a sixty-day window to file the annual report. For further details on the SEC’s Final

Rules and current reporting requirements, refer to Appendix A.

Next, we identify the number of days between the audit report date (using Audit

Analytics variable SIG_DATE_OF_OP_S, which is the signature date on the audit opinion) and

the required filing deadline. We then reconcile to Audit Analytics’ Non-timely Filer Information

and Analysis database to determine if the observations in our sample where the audit report date

follows the required filing deadline filed an NT 10-K. If an SEC registrant cannot file Form 10-

K within the required filing deadline, the company must file within one business day of the due

12 We adjust required filing deadlines falling on weekends by utilizing the SAS command ‘weekday’. When the

calculated required filing deadline falls on a weekend (i.e., Saturday or Sunday), we change the required filing

deadline to the following Monday. We also obtain a list of holidays when the stock exchanges are closed for trading

and adjust the required filing deadline to the next weekday (see http://nyseholidays.blogspot.com/2012/11/nyse-

holidays-from-2000-2010.html).

13

date a Form 12b-25 (designated as an “NT 10-K” in the EDGAR filing system). If the company

is unable to file “without unreasonable effort or expense” then the report will be deemed filed on

time if the company files an NT 10-K and then files the annual report no later than the 15th

calendar day following the due date for the missed report. From this procedure we find very few

discrepancies, suggesting minimal error in identifying the required filing date. For each

discrepancy identified, we manually adjust the required filing deadline based on review of the

related SEC filings in EDGAR.

Table 2 presents our sample selection procedures and the composition of the samples for

both of our audit quality measure tests. When audit quality is measured using misstatements, our

sample consists of 31,676 company-years with available data to construct model variables.

When audit quality is measured using the subsequent receipt of a GAAP or disclosure related

SEC comment letter, our sample consists of 31,608 company-year observations. We find that for

65.3 percent of each sample, the audit report date precedes the required filing deadline by more

than a week. We find that the audit report date is within a week of the required filing deadline

for 24.1 percent of the samples and on the required filing deadline for 5.2 percent of the samples.

We find that 5 percent of the samples file an NT 10-K and subsequently file within the fifteen-

calendar-day extension provided by the SEC, where 3.5 percent later file within twelve calendar

days and 1.5 percent file in the last three days. For the samples, 0.4 percent file late (during the

thirty days after the fifteen day extension provided by filing an NT 10-K). We exclude

company-years from the samples where the 10-K is filed more than thirty days after the extended

deadline.

14

Research Design

To test our hypothesis of whether deadline imposed time pressure affects audit quality,

we measure deadline imposed time pressure as the proximity of the auditor’s report date to the

required filing deadline and measure audit quality in two ways. DeFond and Zhang (2014) state

that each proxy for audit quality has its own strengths and weaknesses and that no single proxy

portrays a complete picture. As such, they recommend that researchers examine different

measures when making inferences about audit quality. In a recent survey, Christensen et al.

(2014) find that auditors and investors believe that financial statement restatements and the

receipt of SEC comment letters are the two leading indicators of lower audit quality. As such,

we measure audit quality using material misstatements (as revealed through subsequent financial

statement restatements) and the subsequent receipt of a GAAP or disclosure related SEC

comment letter related to a company’s Form 10-K.

Misstatements

We first capture audit quality using material misstatements (revealed through subsequent

financial statement restatements). Restatements are identified using Audit Analytics’ Non-

Reliance Restatements database. Because auditing standards require the auditor to plan and

perform the audit to obtain reasonable assurance about whether the financial statements are free

of material misstatement (PCAOB 2003), a subsequently revealed misstatement suggests that the

auditor failed to detect and/or report the misstatement. A number of studies use misstatements to

proxy for audit quality (e.g., Kinney et al. 2004; Stanley and DeZoort 2007; McGuire et al. 2012;

Schmidt 2012; Francis and Michas 2013; and Lobo and Zhao 2013).

To test our hypothesis where audit quality is measured using material misstatements, we

estimate the following logistic regression model:

15

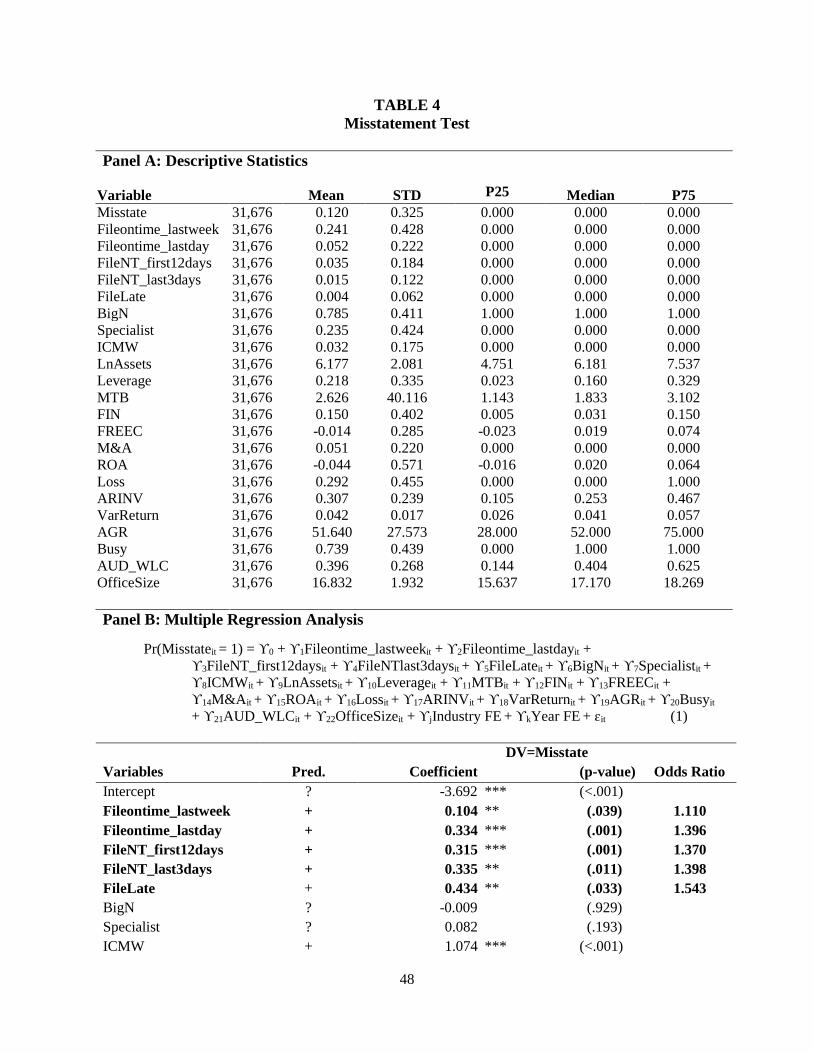

Pr(Misstateit = 1) = ϒ0 + ϒ1Fileontime_lastweekit + ϒ2Fileontime_lastdayit +

ϒ3FileNT_first12daysit + ϒ4FileNTlast3daysit + ϒ5FileLateit + ϒ6BigNit +

ϒ7Specialistit + ϒ8ICMWit + ϒ9LnAssetsit + ϒ10Leverageit + ϒ11MTBit + ϒ12FINit

+ ϒ13FREECit + ϒ14M&Ait + ϒ15ROAit + ϒ16Lossit + ϒ17ARINVit +

ϒ18VarReturnit + ϒ19AGRit + ϒ20Busyit + ϒ21AUD_WLCit + ϒ22OfficeSizeit +

ϒjIndustry FE + ϒkYear FE + ɛit (1)

where:

Misstate = an indicator variable set equal to one if the annual financial

statements were misstated (as revealed through a subsequent

restatement), and zero otherwise;

Fileontime_lastweek = an indicator variable set equal to one if the audit report date is within

one week of the required filing date (excluding the required filing date),

and zero otherwise;

Fileontime_lastday = an indicator variable set equal to one if the audit report date is the

same as the required filing date, and zero otherwise;

FileNT_first12days = an indicator variable set equal to one if the company files an ‘NT 10-

K’ and the company files the 10-K within the first twelve calendar days

of the fifteen day extension, and zero otherwise;

FileNTlast3days = an indicator variable set equal to one if the company files an ‘NT 10-

K’ and the company files the 10-K during the last three calendar days

of the fifteen day extension, and zero otherwise;

FileLate = an indicator variable set equal to one if the company files an ‘NT 10-

K’ and the company files the 10-K during the thirty days after the

fifteen day extension, and zero otherwise; and

all other variables are as defined in Appendix B. The coefficients of interest in equation (1) are

ϒ1 through ϒ5, which indicate whether the likelihood of misstatement differs when auditors

complete audit procedures at or near the required (or extended) filing deadline. Positive and

significant coefficients would indicate that auditors completing procedures at or near the required

(or extended) filing deadline compromise audit quality in an effort to help the client meet the

reporting requirement.

16

Control variables follow prior literature. We control for auditor characteristics, company

characteristics, and transactions that have been shown to affect the likelihood of misstatement to

the extent that these variables are widely available for our sample (e.g., Dechow et al. 1996;

Summers and Sweeney 1998; Kinney et al. 2004; Blankley et al. 2012; Cao et al. 2012; Lobo and

Zhao 2013). In addition, because clients with greater financial reporting risk may be more likely

to file at or near the reporting deadline, we control for financial reporting risk using a

commercially-developed accounting and governance risk score (AGR). Charles et al. (2010)

find that AGR scores effectively proxy for an element of risk beyond what has traditionally been

captured by various risk measures in audit fee models. Prior research also finds that AGR scores

perform as well or better than academic measures and other commercially-developed measures,

including the F-score, at detecting misstatements (see e.g., Price et al. 2011 and Daines et al.

2010). We also include controls for auditor resource constraints. Lopez and Peters (2012) find

evidence that workload pressures, as proxied by the audit busy season and auditor workload

compression, within an office are associated with lower audit quality (greater magnitudes of

abnormal accruals). We include industry and year fixed effects to control for variation in

misstatements across industry and time, and we cluster standard errors by company to control for

serial dependence (Petersen 2009).

SEC Comment Letters

We also capture audit quality using the subsequent receipt of a GAAP or disclosure

related SEC comment letter related to a company’s Form 10-K. Receipt of such a letter would

indicate a potential deficiency in the appropriate application of or disclosure required by GAAP.

Prior research suggests that SEC comment letters are negatively correlated with input measures

of audit quality such as the use of a large auditor and unexplained audit fees and positively

17

correlated with indicators of poor corporate governance (see Cassell et al. 2013 and Hribar et al.

2014). Additionally, in a survey of audit professionals, Christensen et al. (2014) find that SEC

comment letters and enforcement actions were the second most frequently mentioned publicly

available signals of low audit quality (restatements being the most frequently mentioned signal).

To test our hypothesis where audit quality is measured using the subsequent receipt of an

SEC comment letter, we estimate the following logistic regression model:

Pr(Commentletterit =1) = α0 + α1Fileontime_lastweekit + α2Fileontime_lastdayit +

α3FileNT_first12daysit + α4FileNTlast3daysit + α5FileLateit + α6LnMVEit + α7Ageit

+ α8Leverageit + α9MTBit + α10FINit + α11M&Ait + α12Lossit + α13ICMWit +

α14Restateit + α15Rank_zscoreit + α16VarReturnit + α17BigNit + α18Secondtierit +

α19Specialistit + α20AGRit + α21Busyit + α22AUD_WLCit + α23OfficeSizeit +

αjIndustry FE + αkYear FE + ɛit (2)

where:

Commentletter = an indicator variable set equal to one if the company receives a GAAP or

disclosure related SEC comment letter related to a company’s Form 10-K

during the twelve months subsequent to the annual report filing date, and

zero otherwise; and

all other variables are as defined in Appendix B. Similar to the misstatement test, the

coefficients of interest in equation (2) are α1 through α5, which indicate whether the receipt of a

GAAP or disclosure related SEC comment letter in the subsequent year differs when the auditor

completes audit procedures at or near the required filing deadline.

Following Cassell et al. (2013), we control for company size, age, leverage, growth, the

extent of financing, merger and acquisition activity, financial distress, the presence of a material

weakness in internal controls over financial reporting, the announcement of prior financial

reporting misstatements, volatility in stock returns, auditor characteristics, and financial

reporting risk. In addition, we include controls for auditor resource constraints, industry and

18

year fixed effects to control for variation across industry and time, and we cluster standard errors

by company to control for serial dependence (Petersen 2009).

Propensity-Score Matched Samples

To alleviate concerns that the relation between external deadline pressure and audit

quality is driven by risk factors likely influencing the deadline pressure, we also test our

Hypothesis using propensity-score matched (PSM) samples. Matched samples are typically used

to deal with nonlinearities that are not well specified (Cram et al. 2009). Rosenbaum and Rubin

(1983) propose a matching technique using a function of covariates rather than by separately

matching covariates. We obtain PSM samples by first grouping company-year observations in

each of our external deadline pressure categories (Fileontime_lastweek, Fileontime_lastday,

FileNT_first12days, FileNT_last3days, and FileLate) into one grouping, which we label

Ext_Deadline_Press. We then estimate the propensity to be a company with external deadline

time pressure using the following probit regression:

Pr(Ext_Deadline_Pressit = 1) = β0 + β1BigNit + β2Specialistit + β3ICMWit + β4LnAssetsit +

β5Leverageit + β6MTBit + β7FINit + β8FREECit + β9M&Ait + β10ROAit + β11Lossit

+ β12ARINVit + β13VarReturnit + β14AGRit + β15Rank_zscoreit + β16Busyit +

β17AUD_WLCit + β18OfficeSizeit + βjIndustry FE + βkYear FE + ɛit (3)

where:

Ext_Deadline_Press = an indicator variable set equal to one if the company is in one of the

external deadline time pressure categories (i.e., Fileontime_lastweek,

Fileontime_lastday, FileNT_first12days, FileNT_last3days, and

FileLate ), and zero otherwise; and

all other variables are as defined in Appendix B. For each company-year observation where

Ext_Deadline_Press equals one, we identify the company-year observation where

Ext_Deadline_Press equals zero with the closest propensity score (where the difference in

propensity score does not exceed 0.5). This procedure generates 4,811 successful matches for

19

the misstatement test and 4,795 successful matches for the SEC comment letter test. Panel B of

Table 6 provides the differences in mean and median values for these control variables between

the external deadline pressure observations and the control observations. Although we do not

achieve covariate balance for all variables (BigN, Specialist, ICMW, Leverage, ROA, Loss,

Rank_zscore, AGR, Busy, AUD_WLC, and OfficeSize), we note that the differences in the mean

and median values of these variables between the treatment and matched sample, although

statistically significant, are similar in magnitude. Additionally, we control for each of these risk

characteristics in our tests.

IV. EMPIRICAL RESULTS

Correlations

Table 3 presents the correlations of our audit quality measures and our variables

capturing deadline imposed time pressure. We do not find significant positive correlations

between our audit quality measures suggesting that these measures capture different aspects of

audit quality. We find that misstatements are positively correlated with companies filing during

the extension period (i.e., those filing an NT disclosure) and those that file after the extension

period. We find that the subsequent receipt of an SEC comment letter related to GAAP or

disclosure issues in the 10-K is positively correlated with each of our measures of deadline

imposed time pressure with the exception of filing during the first twelve days of the extension

period.

Tests of Hypothesis

Misstatements

Table 4 presents the results of the test of our Hypothesis using misstatements as a proxy

for audit quality and Panel A provides descriptive statistics for the sample. Panel B provides the

results of our test. We find that the area under the ROC curve is close to 0.7, which indicates

20

adequate model fit (Hosmer and Lemeshow 2000). After controlling for financial reporting risk

and company and auditor characteristics that have been shown to affect the likelihood of

misstatement, we find a greater likelihood of misstatement when the audit report date is near, at,

or slightly beyond the original required filing deadline relative to companies with an audit report

date preceding the required filing deadline by more than a week. Although the likelihood of

misstatement is greater for companies with an audit report date within a week of the required

filing deadline relative to companies with an audit report date preceding the required filing

deadline by more than a week, tests of equality of the coefficients between Fileontime_lastweek,

Fileontime_lastday, FileNT_first12days, FileNT_last3days, and FileLate reveal that the

likelihood of misstatement for companies with an audit report date within a week of the required

filing deadline is less than that of companies with an audit report date on the required filing date

or during the first 12 days of the extended deadline period. We do not find a significant

difference in the likelihood of misstatement among companies with an audit report date on the

required filing deadline and companies that file an NT 10-K and then file subsequently.

Examination of the odds ratios suggests meaningful economic impact. Holding other predictor

variables fixed, the odds of having a material misstatement with high deadline imposed time

pressure over the odds of having a material misstatement without high deadline imposed time

pressure ranges from 1.110 to 1.543. In terms of percent change, the odds for high deadline

imposed time pressure companies are 11 to 54 percent higher than the odds for companies not

under high deadline imposed time pressure. These results suggest that auditors completing

21

procedures at or near the required filing deadline (or extended deadline) may compromise audit

quality in an effort to help the client meet the reporting requirement.

SEC Comment Letters

Table 5 presents the results of the test of our Hypothesis using the receipt of an SEC

comment letter as a proxy for audit quality. Panel A provides descriptive statistics for the

sample and Panel B provides the results of our test. We find that the area under the ROC curve

is approximately 0.8, which indicates good model fit (Hosmer and Lemeshow 2000). Results

using SEC comment letters are consistent with our test of misstatements. After controlling for

company and auditor characteristics that have been shown to affect the likelihood of receiving an

SEC comment letter, we find a greater likelihood of receiving an SEC comment letter when the

audit report date is near, at, or slightly beyond the original required filing deadline relative to

companies with an audit report date preceding the required filing deadline by more than a week.

A test of equality of the coefficients between Fileontime_lastweek, Fileontime_lastday,

FileNT_first12days, FileNT_last3days, and FileLate indicate some differences in the likelihood

of receiving an SEC comment letter among these groups, but a greater likelihood relative to

companies with an audit report date preceding the required filing deadline by more than a week.

Examination of the odds ratios suggests meaningful economic impact. Holding other predictor

variables fixed, the odds of subsequently receiving a comment letter with high deadline imposed

time pressure over the odds of subsequently receiving a comment letter without high deadline

imposed time pressure ranges from 1.123 to 1.730. In terms of percent change, the odds for

high deadline imposed time pressure companies are 12 to 73 percent higher than the odds for

companies not under high deadline imposed time pressure. Again, these results are consistent

with the notion that auditors completing procedures at or near the required filing deadline (or

22

extended deadline) may compromise audit quality in an effort to help the client meet the

reporting requirement.

Propensity-Score Matched Samples

Table 6 presents the results of our Hypothesis using the PSM samples. Panel A presents

the results of the first stage probit regression estimating the propensity to file with external

deadline pressure. We find that the likelihood of external deadline imposed time pressure (where

the audit report date is near, at, or slightly beyond the required filing deadline) is higher among

companies with internal control material weaknesses, companies with higher leverage,

companies that issue debt or equity securities, companies involved in merger or acquisition

activity, companies with a net loss, companies with more financial reporting risk, auditors with

greater office level workload compression, and companies with auditors from larger offices. We

find that the likelihood of external deadline imposed time pressure is lower for larger companies,

companies audited by Big N auditors, companies with a higher market-to-book ratio, companies

with a greater proportion of receivables and inventory, companies with a larger variance in stock

returns, and companies with a fiscal year-end in December or January.

Panel B presents the differences in mean and median values of variables in equation (3)

between companies with external deadline pressure and the matched companies without external

deadline pressure. Although there is a significant difference in mean and median values for

many of these variables, we note that many of these differences, although statistically significant,

are not of a large magnitude. In addition, we find that a slightly higher proportion of the

companies with external deadline pressure have a Big N or industry specialist auditor and that

the auditor office is larger relative to matched control sample. Although we do find significant

23

differences in mean and median values of certain client risk characteristics, we control for these

characteristics in our tests.

Panel C presents the results of the test of our Hypothesis using misstatements as a proxy

for audit quality. Similar to Table 4, we find consistent evidence of a greater likelihood of

misstatement when the audit report date is near, at, or slightly beyond the original required filing

deadline relative to companies with an audit report date preceding the required filing deadline by

more than a week. Panel D presents the results of the test of our Hypothesis using the receipt of

an SEC comment letter as a proxy for audit quality. Consistent with Table 5, we find that when

the audit report date is within the last week or the day of the required filing deadline, there is a

greater likelihood of receiving an SEC comment letter. We also find a greater likelihood of

receiving an SEC comment letter when the audit report date is within the first 12 days of the

extension period or when the company files late (after the 15 day extension period). Overall,

these results corroborate the results in Tables 4 and 5 and suggest that auditors completing

procedures at or near the required filing deadline (or extended deadline) may compromise audit

quality in an effort to meet the reporting requirement.

Additional Analyses

In this section we examine whether auditors with more available resources and/or

specialized knowledge are able to mitigate the negative effect of deadline imposed time pressure

on audit quality. A number of prior theoretical and empirical studies suggest that Big N auditors

provide higher audit quality (e.g., DeAngelo 1981; Teoh and Wong 1993; Craswell et al. 1995;

Becker et al. 1998; Francis et al. 1999; Eshleman and Guo 2014). DeAngelo (1981) argues that

the larger client base of Big N auditors increases incentives to protect reputation and reduces

incentives to compromise independence, suggesting that Big N auditors will be less likely to

24

compromise audit quality even when facing deadline imposed time pressure. In addition,

because Big N auditors are larger, they may be able to effectively allocate resources in order to

avoid low quality audits when under external deadline time pressure. Thus, we examine whether

the negative effect of deadline imposed time pressure on audit quality is lower for Big N

auditors.13 Likewise, auditors in larger offices may be able to effectively allocate resources to

client engagements under deadline imposed time pressure. Francis and Yu (2009) find that audit

quality is higher among clients in larger Big 4 auditor offices. They suggest that this result is

likely due to greater knowledge and resource sharing. If auditors in larger offices are able to

effectively utilize more audit personnel when faced with external deadline pressure, audit quality

may not suffer. As such, we examine whether the negative effect of deadline imposed time

pressure is lower for auditors in large offices.14 Finally, because auditor resources may be

constrained during certain times of the year, thus reducing the effectiveness of

resource/personnel allocation, we examine whether auditors during non-busy times of the year

(non-busy season) are able to mitigate the negative effect of deadline imposed time pressure.15

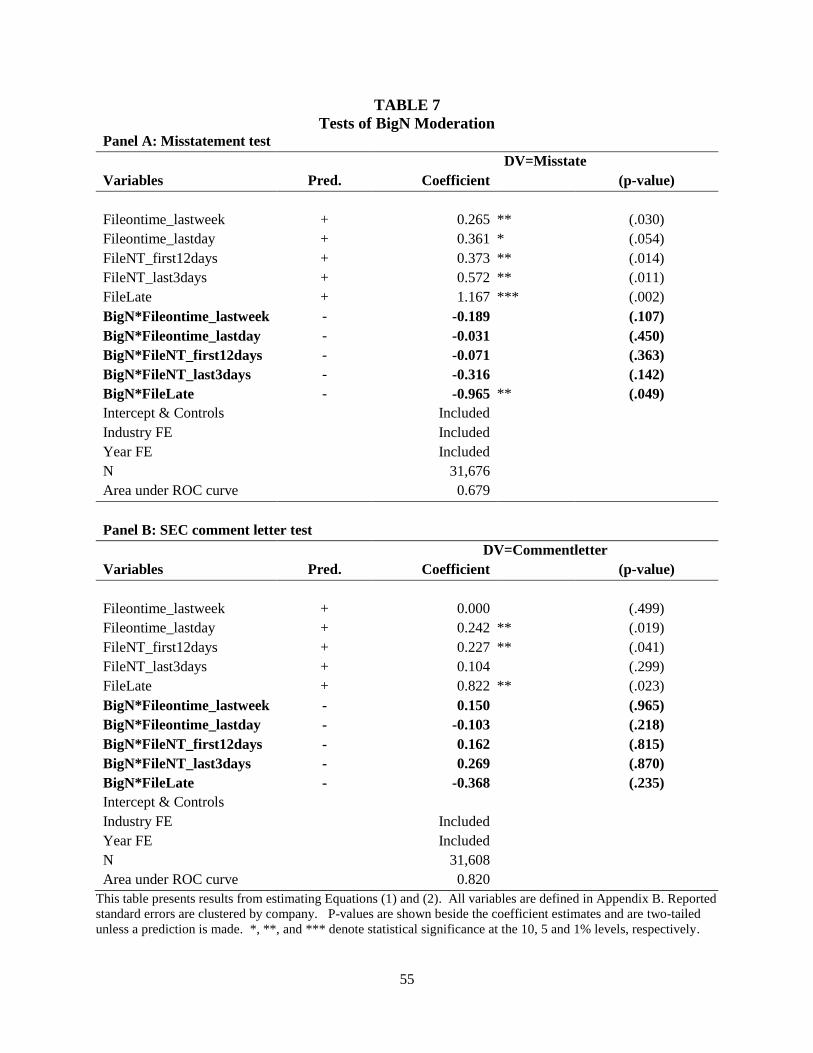

Table 7 presents the results of our tests examining the moderating effect of Big N

auditors. Panel A presents the results using misstatements as a proxy for audit quality. Here, we

find that Big N auditors reduce the higher likelihood of misstatement due to deadline imposed

13 To test whether Big N auditors moderate the negative effect of deadline time pressure on audit quality, we re-

estimate equation (1) and (2) including interactions between BigN and each of the deadline time pressure category

variables. 14 To test whether auditors in larger offices moderate the negative effect of deadline time pressure on audit quality,

we re-estimate equation (1) and (2) replacing OfficeSize with an indicator variable set equal to one for the highest

quartile of office size in the sample (and zero otherwise) and including interactions between each of the deadline

time pressure category variables and this indicator variable for large office size. 15 To test whether auditors of clients with non-busy season fiscal year-ends moderate the negative effect of deadline

time pressure on audit quality, we re-estimate equation (1) and (2) replacing Busy with an indicator variable set

equal to one for non-busy season clients (i.e., clients with a fiscal year-end other than December or January) and

zero otherwise, and including interactions between each of the deadline time pressure category variables and this

indicator variable for non-busy season fiscal year-end companies.

25

time pressure when a company files late (after the 15 day extension period). However, when the

audit report date is near or on the required filing deadline, or during the extension period, we do

not find a moderating effect. This suggests that even among large auditors, deadline imposed

time pressure negatively affects audit quality. Panel B presents the results using the receipt of an

SEC comment letter as a proxy for audit quality. Here, we do not find a moderating effect for

Big N auditors in any of the deadline time pressure categories. Taken together, although Big N

auditors are less likely to succumb to compromising audit quality when the audit report date is

after the extension period (at least in terms of misstatements), deadline imposed time pressure

appears to negatively impact audit quality, even among the largest auditors.

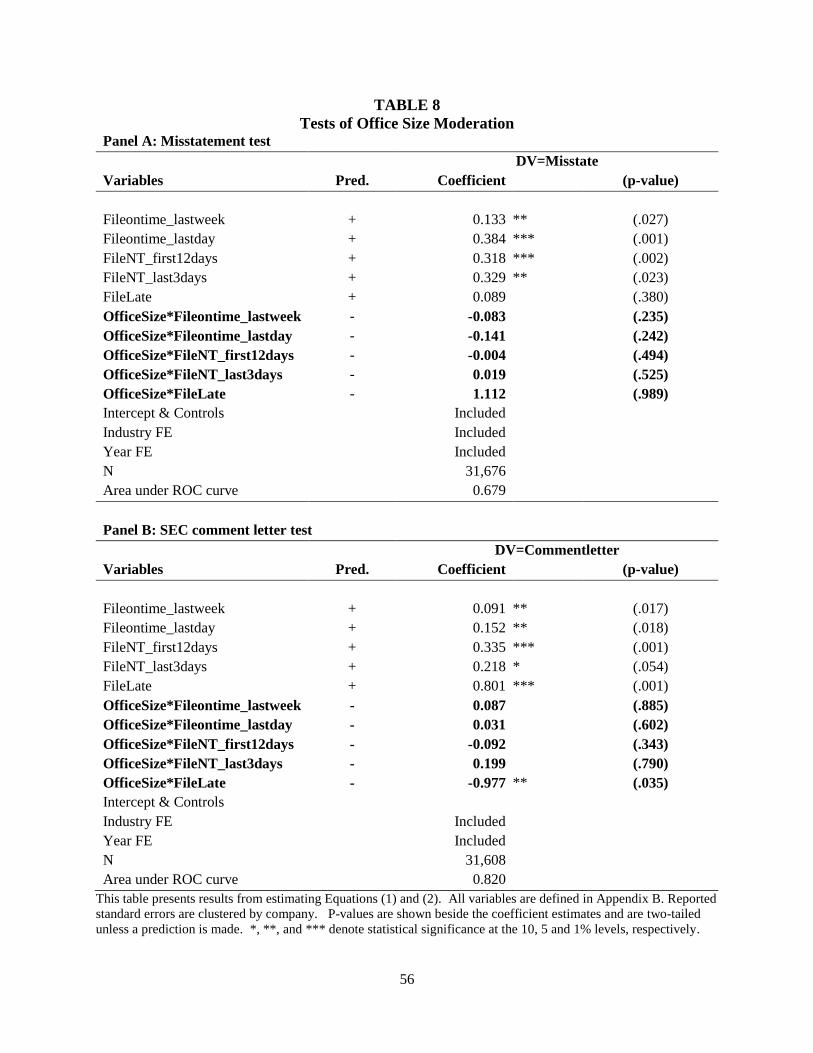

Table 8 presents the results of our tests examining the moderating effect of large auditor

offices. Panel A presents the results using misstatements as a proxy for audit quality. Here, we

do not find that large auditor offices reduce the higher likelihood of misstatement due to deadline

imposed time pressure. Panel B presents the results using the receipt of an SEC comment letter

as a proxy for audit quality. We only find a moderating effect on the likelihood of receiving an

SEC comment letter due to deadline imposed time pressure when a company files late (after the

15 day extension period) for large auditor offices. Thus, we find little evidence that even among

auditors in large offices, deadline imposed time pressure appears to negatively impact audit

quality.

Table 9 presents the results of our tests examining the moderating effect of auditors

during less busy times of the year (i.e., non-busy season). Panel A presents the results using

misstatements as a proxy for audit quality. Panel B presents the results using the receipt of an

SEC comment letter as a proxy for audit quality. We find consistent evidence in both tests, that

auditors are able to mitigate the negative effects of deadline imposed time pressure during the

26

early part of the extension period (i.e., during the first 12 days of the 15 day extension period).

However, we do not find a mitigating effect in any of the other time pressure categories (near or

at the required filing deadline, or at the extended deadline). Thus, even during times of the year

when auditors are less constrained, the negative effects of deadline imposed time pressure

remain.

Robustness Tests

Separate Analyses by Required Time to File

To ensure that the results from our primary analyses are not driven solely by smaller,

more problematic companies, we segregate our sample by the different deadline requirements.

Only large accelerated filers are subject to the 60 day filing requirement beginning in 2006.

Over the sample period, accelerated filers were initially subject to the 90 day requirement and

then beginning in 2006, the 75 day requirement. Non-accelerated filers, the smallest companies,

are subject to the 90 day filing requirement.

Table 10 presents the results of these tests. Panel A presents the misstatement tests.

Here, we find even with the largest filers, that deadline imposed time pressure increases the

likelihood of misstatement. Specifically, in the first column, which includes companies-years

subject to a 60 day filing requirement, we find an increased likelihood of misstatement when the

audit report date is on the required filing deadline or during the first 12 days of the NT extension.

In the second and third columns, we find evidence suggesting that deadline imposed time

pressure for companies filing within 75 days or 90 days generally increases the likelihood of

misstatement. Overall, these results suggest that external deadline pressure affects audit quality

for large, mid-size, and small companies.

27

Panel B presents the SEC comment letter tests. In general, we do not find an increased

likelihood of receiving a comment letter when examining separately companies subject to

different required filing deadlines. The only exceptions are companies filing during the first

twelve days of the extension period and those filing after the extension period that are subject to

the 75 day filing requirement, where there is an increased likelihood of receiving an SEC

comment letter. As such, it appears that on average, the effect of an increased likelihood of an

SEC comment letter only manifests in the aggregate.

Internal Deadline Pressure

Although imposed external deadlines subject auditors to a compressed timeframe in

which to obtain sufficient evidence to form a basis for their opinion on the financial statements,

companies may also exert pressure on auditors to complete audit procedures in an effort to meet

internally set deadlines.16 Prior research suggests there are potential benefits to filing the annual

report earlier (relative to the prior year). Choudhary et al. (2013) find a decrease in information

asymmetry in the form of decreased percentage changes in bid/ask spreads for companies that

file early relative to companies that file within the required filing time permitted. In addition, for

companies filing on time but near or at the externally imposed deadline, it is possible that the

reduction in audit quality is a result of internal deadline pressure rather than external deadline

pressure. As such, we examine the effect of internal deadline pressure on audit quality.

To do this, we re-estimate equations (1) and (2) including an additional variable to

capture internal deadline pressure. We examine two different measures of internal deadline

pressure. The first measure, IDP1, is an indicator variable set equal to one if the current year

16 For example, in a disciplinary proceeding issued on August 11, 2009, the PCOAB barred Thomas J. Linden from

being associated with a registered public accounting firm. This was due to the dysfunctional audit behavior of Mr.

Linden in order to help his client, Navistar, meet an internally set deadline (PCAOB 2009).

28

audit report date and filing date are within 2 days of the expected filing date (prior year filing

date adjusted forward for weekends and holidays) and the expected filing date is within the

required filing deadline, and zero otherwise. The second measure, IDP2, is an indicator variable

set equal to one if the current year audit report date and file date are within -3 to +6 days of the

expected filing date (prior year filing date adjusted forward for weekends and holidays), the audit

report date and filing date are within a day of each other, and the expected filing date is within

the required filing deadline, and zero otherwise.17

In untabulated analyses, for both measures, we continue to find an increased likelihood of

misstatement when the audit report date is near, at, or slightly beyond external deadlines

(including extended deadlines). When internal deadline pressure is measured using IDP1, we

find a lower likelihood of misstatement. When internal deadline pressure is measured using

IDP2, we do not find that internal deadline pressure affects the likelihood of misstatement. In

addition, we do not find that internal deadline pressure affects the likelihood of receiving a

GAAP or disclosure related SEC comment letter in the subsequent year related to the 10-K.

However, we continue to find consistent results with our primary tests related to external

deadline imposed time pressure. Overall, we do not find evidence suggesting that audit quality is

diminished under internal deadline pressure. However, controlling for internal deadline pressure,

we continue to find evidence suggesting that audit quality is negatively impacted, on average, by

external deadline imposed time pressure.

17 In untabulated analysis, we examine alternative measures of internal deadline pressure by altering the window of

time around the expected filing date (based on the prior year filing date for companies that filed timely, adjusted for

weekends and holidays). Results of these alternative windows are qualitatively consistent with those presented in

Table 7.

29

Engagement-level Budget Pressure

Because deadline imposed time pressure and audit engagement budget pressure can often

be related, we re-perform our tests including a control for engagement-level budget pressure. To

capture engagement-level budget pressure we take the absolute value of the percentage change in

audit fees relative to the prior year. We multiply this by negative one so that higher values of

this measure capture observations where the current year audit fee is very close to the prior year

audit fee. Because audit fee data is only available beginning in the year 2000, our sample is

reduced to fiscal years 2001 through 2009 with available audit fee data. We find results remain

robust with the inclusion of this additional control for budget pressure.

Removing Companies with High Sales Volatility

Given the possibility that companies with greater uncertainty and higher risk are more

difficult to audit and more likely to face external deadline imposed time pressure, we re-perform

our tests after excluding company-year observations with high sales volatility (over the previous

three years) in order to reduce this concern. Specifically, we rank the observations in the sample

by sales volatility and drop the highest quartile. We find consistent results in our misstatement

and comment letter tests with these subsamples.

Removing Observations where the Earnings Announcement Date is Early

Although the auditor has no responsibility for client’s public earnings announcements

and recent trends suggest that audit procedures are still in process for many companies when

fourth quarter earnings are released to the public (see e.g., Bronson et al. (2014) and U.S. SEC

Summary of Comments Relating to Proposed Amendments to Accelerate Periodic Report Filing

Dates and Disclosure Concerning Website Access to Reports. Release No. 33-8089), we re-

perform our tests after excluding observations where the fourth quarter earnings release is more

30

than twenty days or fifteen days before the audit report date. We find consistent results in our

misstatement and comment letter tests with these subsamples.

The Nature of the Restatement

We recognize that audit procedures around certain types of accounts and events are likely

to be completed late in the audit. As such, we examine misstatements of tax-related accounts,

impairments of assets (including intangible assets), and merger and acquisition related issues

separately from all other misstatements. This captures 1,210 misstated company-years (or

approximately 32 percent) of the total 3,791 misstated company-years in our sample. Among

these types of misstatements, we find consistent evidence of lower audit quality when the audit

report date is at, on, or slightly beyond the original or extended required filing deadline. When

separately examining all other types of misstatements, we find lower audit quality when the audit

report date is on the required filing deadline or during the fifteen day extension period. Thus,

while accounts that are typically audited later in the audit process have a higher likelihood of

subsequent restatement, we find evidence that the negative effects of deadline imposed time

pressure is pervasive across other types of misstatements as well.

Sensitivity Analysis of Deadline Imposed Time Pressure

In our primary analyses, we identify deadline imposed time pressure as those companies

with an audit report date within a week of the required filing deadline. In untabulated analyses,

we find consistent results with those presented when limiting this to within 6, 5 or 4 days of the

required filing deadline or expanding this to within 10 days of the required filing deadline.

V. SUMMARY AND CONCLUSION

PCAOB Staff Audit Practice Alert No. 10 (PCAOB 2012a) raises concerns that audit

scheduling can cause auditors to feel pressured to ‘complete assignments too quickly’ which can

lead to dysfunctional audit behavior (e.g. gathering easy to obtain evidence as opposed to

31

relevant and reliable evidence; insufficient amounts of evidence; giving undue weight to

confirming evidence without adequately considering contrary evidence). With these concerns in

mind, we examine whether audits completed under deadline imposed time pressure, as proxied

by the proximity of the audit report date to a company’s 10-K filing deadline, are associated with

measures of low audit quality.

We find evidence that audits that are completed under deadline imposed time pressure

(i.e., the audit report date is near, at, or slightly beyond the original (or extended) required 10-K

filing deadline) are associated with different measures of compromised audit quality. These

results are robust to: (1) separately examining subsamples of large (i.e., large accelerated filers),

mid-size (i.e., accelerated filers), and small (i.e., non-accelerated filers) companies with a similar

required deadline; (2) controlling for internal deadline pressure; (3) controlling for engagement-

level budget pressure; (4) excluding companies with high uncertainty (i.e., high volatility in

revenues); (5) excluding companies that release fourth quarter earnings well in advance of the

audit report date; and (6) different types of misstatements. We also find that these negative

effects persist among larger auditors, auditors from larger offices, and in certain circumstances

among auditors of clients with non-busy season fiscal year-ends. Our findings suggest that

auditors completing procedures at or near the required (or extended) filing deadline may

compromise audit quality in an effort to meet the reporting requirement. These results

complement and strengthen the robustness of results from prior experimental research, and

thereby mitigate concerns about internal and external validity.

Our results suggest that a potentially observable indicator of audit quality would be the

date the auditors completed fieldwork. Prior to 2009, that date coincided with the auditor’s

report date. However, the audit report date no longer is a useful indicator of the date auditors

32

complete fieldwork. In response to SFAS No. 165, issued in 2009, auditors now date the audit

report in conjunction with the SEC filing. This provides less opportunity for users of the

financial statements to identify auditors under deadline imposed time pressure. Although

unintentional, this highlights an unintended consequence to financial statement users from the

issuance of SFAS No. 165. We believe this has important implications for the PCAOB’s project

regarding potential indicators of audit quality and their project to improve the auditor’s reporting

model. Our findings suggest that an important indicator of audit quality could be provided in the

auditor’s report in the form of dual-dating of the audit opinion to clearly convey the date of the

end of audit fieldwork (first date) as well as the date through which subsequent events were

considered (second date). Therefore, our findings suggest that improvements to the auditor’s

report, include a requirement to report the date fieldwork was completed.

33

REFERENCES

Alderman, C. W., and J. W. Deitrick. 1982. Auditors’ perceptions of time budget pressures and

premature sign-offs: A replication and extension. Auditing: A Journal of Practice and

Theory 1 (2): 53-68.

Allee, K. D., N. Bhattacharya, E. L. Black, and T. E. Christensen. 2007. Pro forma disclosure

and investor sophistication: External validation of experimental evidence using archival

data. Accounting, Organizations and Society 32 (3): 201-222.

American Institute of Certified Public Accountants (AICPA). 2014. Enhancing Audit Quality.

Plans and Perspectives for the U.S. CPA Profession. August 2014, New York, NY.

Ashbaugh, H., R. LaFond, and B. W. Mayhew. 2003. Do nonaudit services compromise auditor

independence? Further evidence. The Accounting Review 78 (3): 611-639.

Bamber, E. M., and J. H. Bylinski. 1987. The effects of planning memorandum, time pressure

and individual auditor characteristics on audit managers’ review time judgments.

Contemporary Accounting Research 4 (1): 127-143.

Becker, C. L., M. L. DeFond, J. Jiambalvo, and K. R. Subramanyam. 1998. The effect of audit

quality on earnings management. Contemporary Accounting Research 15 (1): 1-24.

Bennet, G. B., and R. C. Hatfield. 2014. Do approaching deadlines influence auditors’

materiality assessments and audit sampling decisions? Working paper, University of

Massachusetts Amherst and University of Alabama.

Bennet, G. B., R. C. Hatfield, and C. M. Stefaniak. 2014. The effect of deadline pressure on pre-

negotiation positions: A comparison of auditors and client management. Working paper,

University of Massachusetts Amherst, University of Alabama, and Oklahoma State

University.

Blankley, A. I., D. N. Hurtt, and J. E. MacGregor. 2012. Abnormal audit fees and restatements.

Auditing: A Journal of Practice & Theory 31 (1): 79-96.

Blankley, A. I., D. N. Hurtt, and J. E. MacGregor. 2014. The Relationship between audit report

lags and future restatements. Auditing: A Journal of Practice & Theory 33 (2): 27-57.

Bronson, S. N., A. Masli, and J. H. Schroeder. 2014. Jumping the gun: Consequences of

announcing earnings when the audit is less complete. Working paper, University of

Kansas and Indiana University.

Cao, Y., L. A. Myers, and T. C. Omer. 2012. Does company reputation matter for financial

reporting quality? Evidence from restatements. Contemporary Accounting Research 29

(3): 956-990.

34

Cassell, C. A., L. M. Dreher, and L. A. Myers. 2013. Reviewing the SEC’s review process: 10-K

comment letters and the cost of remediation. The Accounting Review 88 (6): 1875-1908.

Center for Audit Quality (CAQ). 2014. CAQ Approach to Audit Quality Indicators. Washington,

DC. Available at http://www.thecaq.org/docs/reports-and-publications/caq-approach-to-

audit-quality-indicators-april-2014.pdf?sfvrsn=2

Charles, S. L., S. M. Glover, and N. Y. Sharp. 2010. The association between financial reporting

risk and audit fees before and after the historic events surrounding SOX. Auditing: A

Journal of Practice & Theory 29 (1): 15-39.

Choo, F. 1995. Auditors’ judgment performance under stress: A test of the predicted relationship

by three theoretical models. Journal of Accounting, Auditing & Finance 10 (3): 611-641.

Choudhary, P., K. J. Merkley, and J. D. Schloetzer. 2013. Does filing form 10-K early matter?

Working paper, Georgetown University and Cornell University.

Christensen, B. E., S. M. Glover, T. C. Omer, and M. K. Shelley. 2014. Understanding audit

quality: Insights from audit professionals and investors. Working paper, Texas A&M

University, Brigham Young University, and the University of Nebraska–Lincoln.

Coram, P., J. Ng, and D. R. Woodliff. 2004. The effect of risk of misstatement on the propensity

to commit reduced audit quality acts under time budget pressure. Auditing: A Journal of

Practice and Theory 23 (2): 159-167.

Cram, D. P., V. Karan, and I. Stuart. 2009. Three threats to validity of choice-based and

matched-sample studies in accounting research. Contemporary Accounting Research 26

(2): 477-516.

Craswell, A. T., J. R. Francis, and S. L. Taylor. 1995. Auditor brand name reputations and

industry specializations. Journal of Accounting and Economics 20 (3): 297-322.

Daines, R. M., I. D. Grow, and D. F. Larcker. 2010. Rating the ratings: how good are

commercial governance ratings? Journal of Financial Economics 98 (3): 439-461.

DeAngelo, L. E. 1981. Auditor size and audit quality. Journal of Accounting & Economics 3 (3):

183-199.

Dechow, P. M., R. G. Sloan, and A. P. Sweeney. 1996. Causes and consequences of earnings

manipulation: An analysis of firms subject to enforcement actions by the SEC.

Contemporary Accounting Research 13 (1): 1-36.

DeFond, M. L., and J. Zhang. 2014. A review of archival auditing research. Journal of

Accounting & Economics 58 (2-3): 275-326.

35

DeZoort, F. T., and A. T. Lord. 1997. A review and synthesis of pressure effects research in

accounting. Journal of Accounting Literature 16: 28-85.

DeZoort, F. T. 1998. Time pressure research in auditing: Implications for practice. The Auditor’s

Report 22 (1): 11-12, 14.

Easterbrook, J. A. 1959. The Effect of Emotion on Cue Utilization and the Organization of

Behavior. Psychological Review 66 (6): 183-201.

Eshleman, J. D., and P. Guo. 2014. Do Big 4 Auditors Provide Higher Audit Quality after

Controlling for the Endogenous Choice of Auditor? Auditing: A Journal of Practice and

Theory 33 (4): 197-219.

Francis, J. R., E. L. Maydew, and H. C. Sparks. 1999. The role of big 6 auditors in the credible