the economic crisis & what it means for it, idc - ibm · pdf filethe economic crisis &...

TRANSCRIPT

Copyright 2009 IDC. Reproduction is forbidden unless authorized. All rights reserved.

The Economic Crisis & What It Means for ITThe Economic Crisis & What It Means for IT

Jyoti Lalchandani

Vice President & Regional MD

IDC Middle East, Turkey & Africa

Copyright 2009 IDC. Reproduction is forbidden unless authorized. All rights reserved.

IDC in the Middle East, Turkey & AfricaIDC in the Middle East, Turkey & Africa

� Over 90 Analysts, Consultants & Events Associates Across the Region

� ICT Market Coverage Across 25+ Countries

� Advisory Services to the ICT Community, Governments, and Telcos

� IDC Events Reach Out to 4,500+ CIO’s and IT Managers Across 12 Countries

� Upcoming Offices in Cairo, Egypt (Regional Support Center) and Riyadh, Saudi Arabia

Expertise & CoverageExpertise & Coverage

IDC South Africa

Johannesburg

IDC East Africa

Nairobi, Kenya

IDC West Africa

Lagos, Nigeria

IDC MEA HQ

Dubai, UAE

IDC North Africa

Casablanca, Morocco

IDC Turkey

Istanbul

IDC Egypt

Cairo

IDC Saudi

Riyadh

Copyright 2009 IDC. Reproduction is forbidden unless authorized. All rights reserved.

Research & Analysis MethodologyResearch & Analysis Methodology

Channels

• Disty’s

• Resellers/VAR’s

• SI’s

• IT Training Firms

• IT Consulting Firms

• Retailers

ICT Vendors

Supply-Side

End-User

(Customer Behavior & Technology Adoption)

Demand-Side

Industry/Population Demographics

Market Models

Analyst Insight

Standard Definitions &

Methodologies

(Research and Forecasts)

Trade Associations and

Other

Copyright 2009 IDC. Reproduction is forbidden unless authorized. All rights reserved.

AgendaAgenda

Memos from the CIO

The Economic Implosion

IT Budget Fallout

Accelerated Transformations

Copyright 2009 IDC. Reproduction is forbidden unless authorized. All rights reserved.

An Economic ShockAn Economic Shock

Worldwide GDP Forecast

Source: EIU – April 2009

3.8%

2.5%

1.8%

3.1%

3.8% 3.8%

0.2%

1.7%

3.3%

2.0%

-2.6%

1.0%

2.9%

4.0%4.1%

3.8%

2.7%

4.0%

2.9% 2.9%2.4%3.8%

2.5%

3.8%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

2007 2008 2009 2010 2011 2012

June 08 Forecast October 08 Forecast December 08 Forecast April 09 Forecast

Copyright 2009 IDC. Reproduction is forbidden unless authorized. All rights reserved.

The Economic UnknownThe Economic Unknown

$1-3 Trillion For�Bank Bailouts�Tax Cuts�Infrastructure�SMB Incentives�Health Care�Smart Grid�Auto Manufacturers�Green Building

Copyright 2009 IDC. Reproduction is forbidden unless authorized. All rights reserved.

Source: IDC IT spending estimates, April 2009

IT Budget FalloutIT Budget Fallout

WW IT Spending 7.1%

5.2%

2.6%

4.5%

5.5% 5.7%

0.5%

6.2%

7.1%

4.2%

-8.2%

6.0%6.1%

6.3%5.9%

7.1%

5.5%

4.4%

5.9%

4.2%

7.1%

5.6%5.4%

2.8%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

2007 2008 2009 2010 2011 2012

Aug-08 Nov-08 Jan-09 May-09 (Prelim)

Copyright 2009 IDC. Reproduction is forbidden unless authorized. All rights reserved.

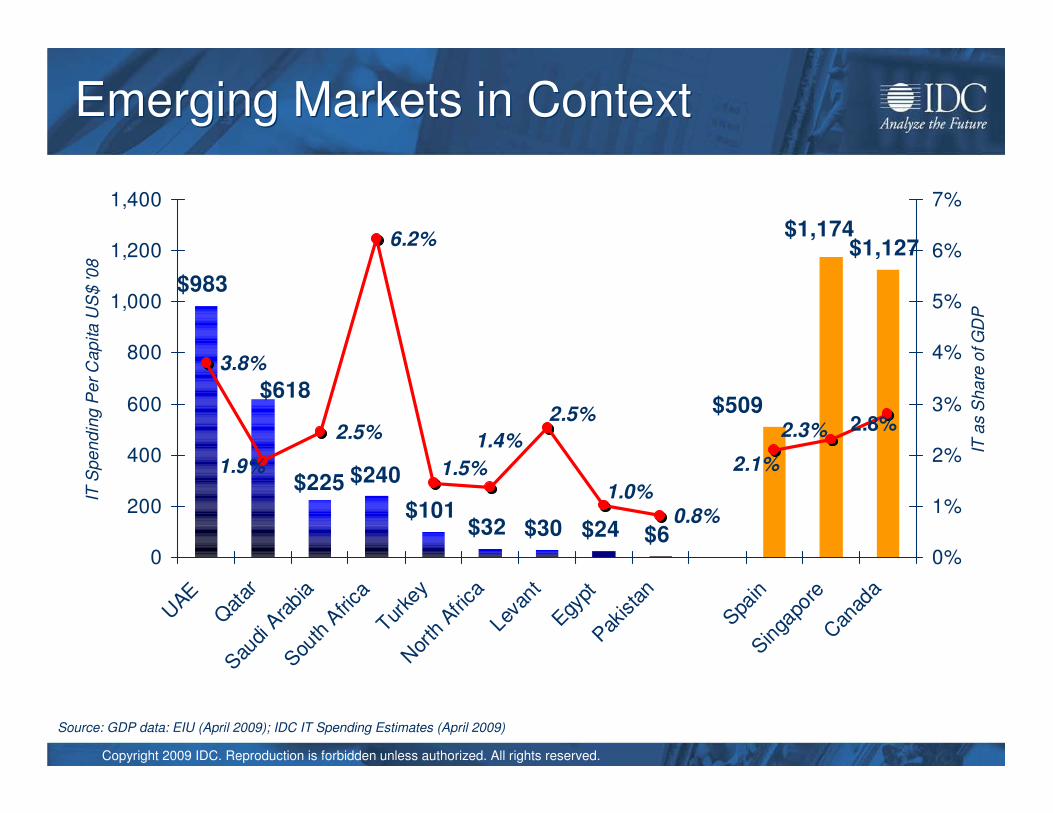

Emerging Markets in ContextEmerging Markets in Context

Source: GDP data: EIU (April 2009); IDC IT Spending Estimates (April 2009)

$983

$32 $30 $24 $6

$1,127$1,174

$509$618

$240

$101

$225

6.2%

0.8%

2.5%

2.1%

2.3%

3.8%

1.4%

1.9% 1.5%

2.8%2.5%

1.0%

0

200

400

600

800

1,000

1,200

1,400

UAE

Qat

arSau

di A

rabi

aSou

th A

frica

Turke

yN

orth

Afri

caLe

vant

Egypt

Pakis

tan

Spain

Singa

pore

Can

ada

IT S

pe

nd

ing

Pe

r C

ap

ita

US

$ '0

8

0%

1%

2%

3%

4%

5%

6%

7%

IT a

s S

ha

re o

f G

DP

Copyright 2009 IDC. Reproduction is forbidden unless authorized. All rights reserved.

Impact in the GCCImpact in the GCC

9.6%

24.0%

28.1%

-11.6%

4.3%

-1.6%

7.7%7.4%9.4%

3.3%-1.0%3.4% 4.2%3.2%

12.2%

17.3%13.4%

23.8%

20.4%

21.8%

-5.8%

8.3%

24.0%26.2%

7.6%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

2006 2007 2008 2009 F 2010 F

GDP UAE GDP Saudi Arabia GDP Qatar

IT Spending GCC IT Spending UAE

Source: GDP data: EIU and IMF (April 2009); IDC IT Spending Estimates (April 2009)

Copyright 2009 IDC. Reproduction is forbidden unless authorized. All rights reserved.

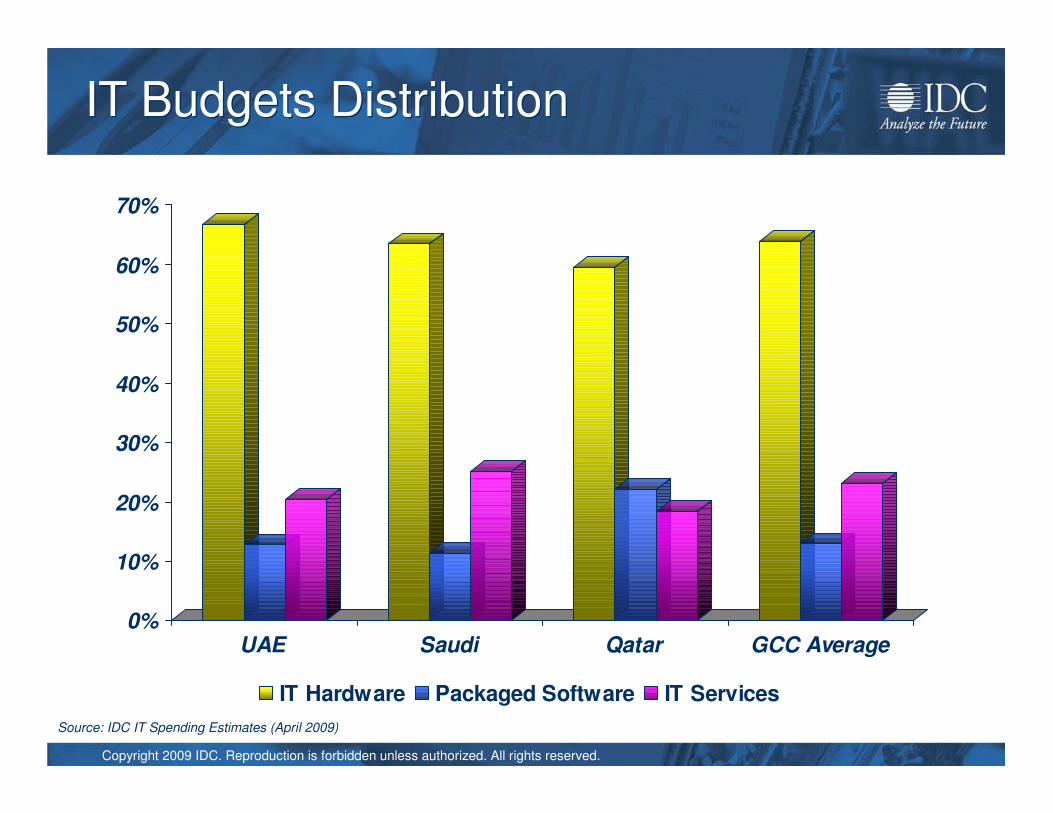

IT Budgets DistributionIT Budgets Distribution

Source: IDC IT Spending Estimates (April 2009)

0%

10%

20%

30%

40%

50%

60%

70%

UAE Saudi Qatar GCC Average

IT Hardware Packaged Software IT Services

Copyright 2009 IDC. Reproduction is forbidden unless authorized. All rights reserved.

The Next Stage of IT AdoptionThe Next Stage of IT Adoption

24%26%

28%

-12%

8%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

2006 2007 2008 2009 2010

IT Spending UAE

+ Healthy Oil Prices+ Infrastructure Enhancements+ Public Sector Reform+ Liberalization/Privatization+ Consumer Sentiment+ Emergence of New Sectors+ SME Adoption Begins- Inflation- Skills Availability

+ IT Asset Utilization/Rationalization+ SaaS, Managed Services, Virtualization+ ROI/TCO Play+ Regulatory/Compliance+ Alignment of IT to Business+ SMB Adoption- Skills

Source: IDC IT spending estimates (April 2009 update)

Copyright 2009 IDC. Reproduction is forbidden unless authorized. All rights reserved.

Memos from the CIO

Copyright 2009 IDC. Reproduction is forbidden unless authorized. All rights reserved.

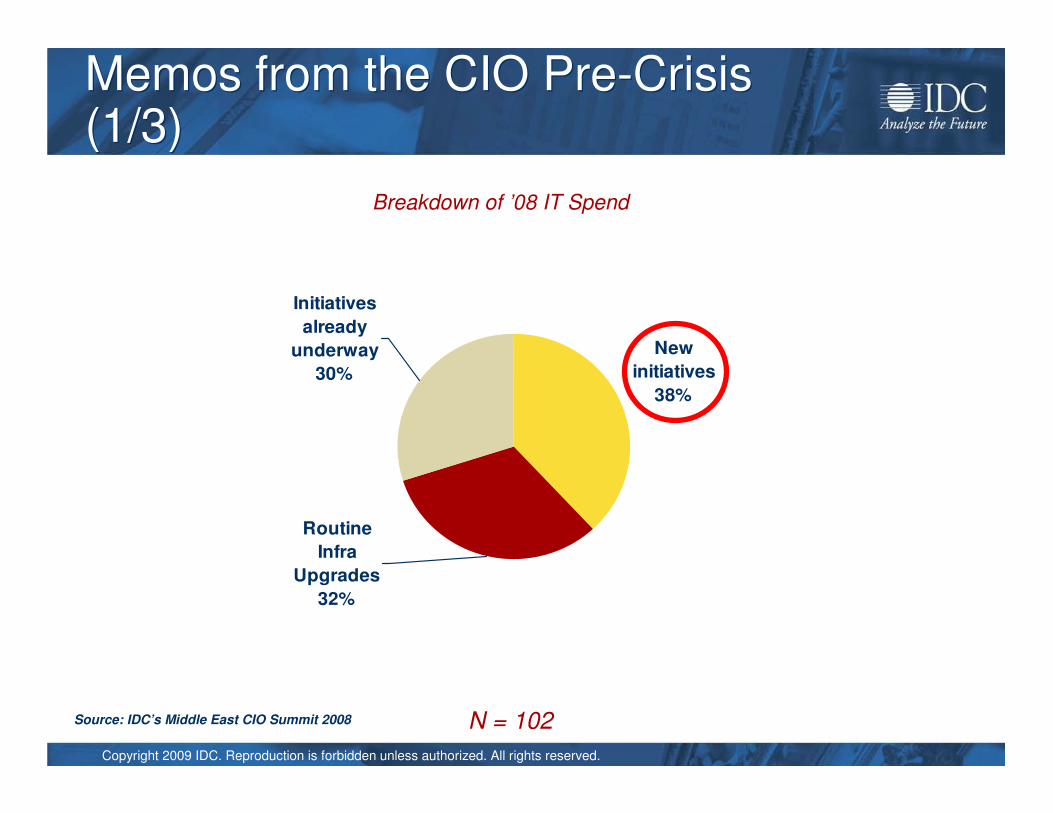

Memos from the CIO Pre-Crisis (1/3)Memos from the CIO Pre-Crisis (1/3)

N = 102Source: IDC’s Middle East CIO Summit 2008

New

initiatives

38%

Routine

Infra

Upgrades

32%

Initiatives

already

underway

30%

Breakdown of ’08 IT Spend

Copyright 2009 IDC. Reproduction is forbidden unless authorized. All rights reserved.

Memos from the CIO Pre-Crisis (2/3)Memos from the CIO Pre-Crisis (2/3)

N = 102Source: IDC’s Middle East CIO Summit 2008

0 0.5 1 1.5 2 2.5 3 3.5 4

IT Infrastructure

Customer service/Care

IT Security

Product development/innovation

Performance tracking

HRM Solns

Mobility/w ireless solutions deployment

Regulatory compliance

Sales performance tracking

Production/Mfring Solns

Branch Automation

Virtualization

Supply chain management

Procurement/sourcing

Marketing performance solutions/tracking

Environment friendly solutions

Priority of IT Investments

Copyright 2009 IDC. Reproduction is forbidden unless authorized. All rights reserved.

CIO Challenges

Source: IDC’s Middle East CIO Summit 2008

Memos from the CIO Pre-Crisis (3/3)Memos from the CIO Pre-Crisis (3/3)

0 5 10 15 20 25 30 35

Staffing issues

Maintaining System Performance

Supporting Operations

Managing Internal Budgets

Managing Outsourced IT Services

Pace of Product Development

Contributing to the Bottom Line

Maintaining a Secure Infrastructure

Regulatory Compliance

Other

# of Responses

Copyright 2009 IDC. Reproduction is forbidden unless authorized. All rights reserved.

2009 Memo (Post-Crisis)2009 Memo (Post-Crisis)

Q: What are the most significant factors driving changes in IT expenditure (budget) allocations in 2009 post crisis?

0 5 10 15 20 25 30 35

Greater focus on ROI/TCO

Greater focus on regulatory compliance

Security of information systems

Improve applications set that better fit our

business processes

To improve the availability and/or

performance of IT systems

Degree of ImportanceN = 114Source: IDC’s MENA CIO Summit 2009

Copyright 2009 IDC. Reproduction is forbidden unless authorized. All rights reserved.

Memos from the CIO Post-CrisisMemos from the CIO Post-Crisis

Improve Utilization of Assets

Explore New Business/Delivery

Models

Bus Continuity Priority

Remains

IT as Business Enabler

(Alignment)

1

2

3

4

Copyright 2009 IDC. Reproduction is forbidden unless authorized. All rights reserved.

Accelerated Transformations

Copyright 2009 IDC. Reproduction is forbidden unless authorized. All rights reserved.

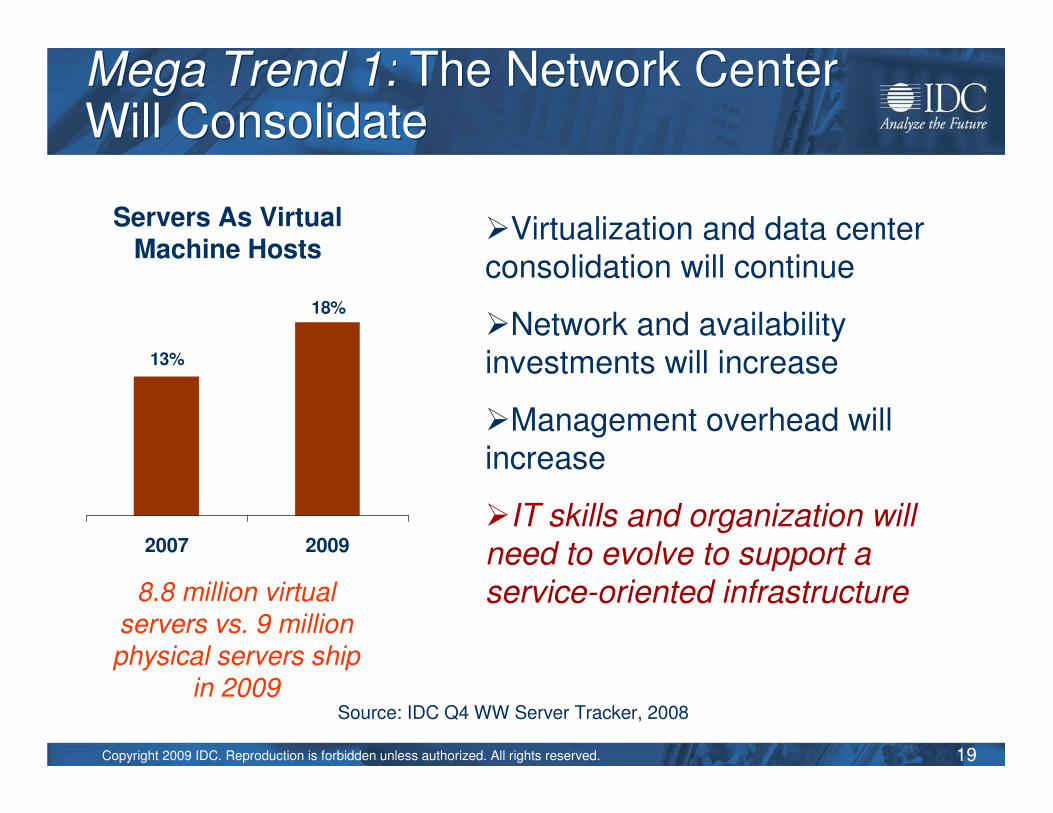

Mega Trend 1: The Network Center Will ConsolidateMega Trend 1: The Network Center Will Consolidate

13%

18%

2007 2009

Servers As Virtual Machine Hosts

8.8 million virtual servers vs. 9 million physical servers ship

in 2009

�Virtualization and data center consolidation will continue

�Network and availability investments will increase

�Management overhead will increase

�IT skills and organization will need to evolve to support a service-oriented infrastructure

19

Source: IDC Q4 WW Server Tracker, 2008

Copyright 2009 IDC. Reproduction is forbidden unless authorized. All rights reserved.

Mega Trend 2: The Network Edge Will ExpandMega Trend 2: The Network Edge Will Expand

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

2008 2009 2010 2011 2012 2013 2014 2015

Millions of Communicating Devices WW*

Computers & Communications Equipment

Mobile DevicesCE & Industrial

* Excludes voice- and SMS-only phones

20Source: IDC Device Universe Model, Jan 2009

�Enterprise bandwidth demands will explode

�Device support and asset management demands will explode

�Data center architectures will have to change

�Operational systems will drive new service level requirements

Copyright 2009 IDC. Reproduction is forbidden unless authorized. All rights reserved.

Mega Trend 3: Enterprise Information Will ExplodeMega Trend 3: Enterprise Information Will Explode

21

342

1,530

2008 2011

Enterprise-Liable ExabytesProduced a Year

User Content

1,234 EB

Enterprise Liable

Content

1,530 EB

Overlap~1,000 EB

�New storage, information management, content management will be needed

�New levels of security and privacy will be needed

�New tools for search and discovery, including video, voice will be needed

�New relationship with business units will be needed – on policy, classification, data ownership

Source: IDC Digital Universe Study, 2008

Copyright 2009 IDC. Reproduction is forbidden unless authorized. All rights reserved.

Mega Trend 4: Web 2.0 Will Create ProblemsMega Trend 4: Web 2.0 Will Create Problems

22

Laptop PC PDA

Text or Instant Messaging

67%

Posting to Blogs, Wikis,

Forums

46%

Percent Hyper Connected Both For Business and Personal Use

79% 64%

�Enterprise-to-customer contacts will grow by an order of magnitude

�Interactivity and mobility will blur work and personal boundaries

�New client access tools will fragment customer relationships

�Web 2.0 will drive new policy needs – with IT in the middle

Source: IDC Study on Hyperconnectivity, 2008

Copyright 2009 IDC. Reproduction is forbidden unless authorized. All rights reserved.

Mega Trend 5: The IT Domain Will GrowMega Trend 5: The IT Domain Will Grow

23

�If it runs on the IP network IT will end up managing it

�IT skill requirements will diversify – internal customers will multiply

�Real time applications will increase IT risk exposure

�Operational IT and general IT will become one and the same

Copyright 2009 IDC. Reproduction is forbidden unless authorized. All rights reserved.

Embedded IT

IT Marketing

Usage-Based

Charges

Business Objectives

New Staff/ Org

Job Rotation

New Reporting Structure

Capital Spending

Visibility

Business Process Responsibility

Six Sigma Process

Management

Mixed Outsourcing

Virtual Teams

Client Contact

�IT performance will be tied to business performance

�Infrastructure money will come from consolidation

�New project money will come from business payback

�IT and business department boundaries will become porous

Mega Trend 6: IT Will Have To ReorganizeMega Trend 6: IT Will Have To Reorganize

24

Copyright 2009 IDC. Reproduction is forbidden unless authorized. All rights reserved.

Impact on ITImpact on IT

25

Copyright 2009 IDC. Reproduction is forbidden unless authorized. All rights reserved.

ContactContact

Jyoti Lalchandani+971 4 391 2741