the decision to buy or lease equipment from an engineering

TRANSCRIPT

The decision to buy or lease equipment from an engineering

economics perspective

By

Cebsile Mkhatshwa

28319461

Submitted in partial fulfilment for the degree of

BACHELORS OF INDUSTRIAL ENGINEERING

In the

FACULTY OF ENGINEERING, BUILT ENVIRONMENT AND

INFORMATION TECHNOLOGY

UNIVERSITY OF PRETORIA

October 2011

1

Executive Summary

Leasing and purchasing equipment forms some of the expenses on the capital budget hence,

affects the net profit of a company. When deciding whether to lease or purchase equipment it

is essential to understand the cash flows associated with each option and the effects of certain

parameters on the cash flows in order to select the option that will give the highest return to

the investment. In this study the net present value (NPV) is used to decide whether to lease or

purchase equipment, with the help of spreadsheet models that represent the cash flows

associated with each option. Then the effect of inflation rates, project life, interest rates, loan

payback period and percentage equity used to purchase the asset on the NPVs of the

spreadsheet models is determined using sensitivity analysis.

2

Table of Contents Executive Summary ................................................................................................................................ 1

CHAPTER 1: Introduction and Background .......................................................................................... 4

1.1 Background and Problem Statement ....................................................................................... 4

1.2 Project Aim ............................................................................................................................. 4

1.3 Project Scope .......................................................................................................................... 5

Chapter 2: Literature Review .................................................................................................................. 6

2.1 Capital Budget ........................................................................................................................ 6

2.1.1 Importance of the capital budget ................................................................................... 6

2.1.2 Influence of the capital structure on capital budget decisions ........................................ 6

2.1.3 Influence of interest, tax and inflation rates on cost of capital ....................................... 7

2.2 Lease of Equipment ................................................................................................................ 8

2.2.1 Typical lease agreement .................................................................................................. 8

2.2.2 Different types of leases available .................................................................................. 8

2.2.3 Tax and leasing agreements ............................................................................................ 9

2.2.4 Influence of interest changes on a lease agreement ........................................................ 9

2.3 Purchasing of equipment ....................................................................................................... 10

2.3.1 Tax implications ............................................................................................................ 10

2.3.2 Depreciation .................................................................................................................. 10

2.4 Existing methodologies of making the lease-buy decision ................................................... 10

Chapter 3: Solution ............................................................................................................................... 13

3.1 Engineering methods and tools ............................................................................................. 13

3.2 Method selection and development..................................................................................... 14

Chapter 4: Analysis ............................................................................................................................... 22

Chapter 5: Conclusions ......................................................................................................................... 31

APPENDIX A – Purchasing models with different equity ................................................................... 32

APPENDIX B – Purchasing models with varying project life ............................................................. 36

APPENDIX C- Purchasing models with different pay back periods .................................................... 40

APPENDIX D-Purchasing models with different inflation rates ......................................................... 43

APPENDIX E- Leasing models with different inflation rates .............................................................. 46

APPENDIX F- leasing models with varying project lives .................................................................... 49

3

Appendix G – purchasing models with varying interest rates .............................................................. 52

Appendix H- leasing models with varying interest rates ....................................................................... 55

Bibliography ......................................................................................................................................... 58

List of tables

TABLE 1: INPUT DATA TO THE PURCHASE SPREADSHEET MODEL ...................................................................... 16

TABLE 2: PURCHASING SPREADSHEET MODEL ................................................................................................... 18

TABLE: 3 INPUT DATA FOR THE LEASING SPREADSHEET MODEL ....................................................................... 20

TABLE: 4 SPREAD SHEET THAT REPRESENTS THEN LEASING OPTION ................................................................ 20

TABLE 5: NPV AND EQUITY ................................................................................................................................ 23

TABLE: 6 CHANGE IN NPV AS THE PROJECT LIFE VARIES ............................................................................... 24

TABLE 7: NPV FOR VARYING PAYBACK PERIODS ............................................................................................... 25

TABLE 8: NPV AND INFLATION RATES WHEN PURCHASING ............................................................................................... 26

TABLE 9: NPV ASSOCIATED WITH DIFFERENT INFLATION RATES WHEN LEASING ........................................... 27

TABLE 10: NPV FOR DIFFERENT PROJECT DURATIONS IN THE LEASING OPTION ............................................. 28

TABLE 11: NPV FOR DIFFERENT INTEREST RATES ............................................................................................. 29

TABLE 12: NPV AND DIFFERENT INTEREST RATES WHEN THE ASSET IS LEASED .............................................. 30

List of figures

FIGURE 1: HYDRAULIC MIXER ................................................................................................................................................. 15

FIGURE 2: SENSITIVITY ANALYSIS OF NPV TO THE VARIATION IN THE % OF EQUITY USED TO PURCHASE THE ASSET .......... 22

FIGURE 3: SENSITIVITY ANALYSIS OF NPV TO THE VARIATION IN PROJECT LIFE IF ASSET IS PURCHASED ............................. 24

FIGURE 4: SENSITIVITY ANALYSIS OF NPV TO THE VARIATION IN PAYBACK PERIODS IF ASSET IS PURCHASED ...................... 25

FIGURE 5: SENSITIVITY ANALYSIS OF NPV TO THE VARIATION IN INFLATION IF THE ASSET IS PURCHASED........................... 26

FIGURE 6: SENSITIVITY ANALYSIS OF NPV TO THE VARIATION IN INFLATION RATES IF ASSET IS LEASED .............................. 27

FIGURE 7: SENSITIVITY ANALYSIS OF NPV TO THE VARIATION IN PROJECT LIFE IF THE ASSET IS LEASED............................. 28

FIGURE 8: SENSITIVITY ANALYSIS OF THE AFFECT OF INTEREST RATE ON THE NPV AN ASSET IS PURCHASED ...................... 29

FIGURE 9: SENSITIVITY ANALYSIS OF THE AFFECT OF INTEREST RATE ON THE NPV AN ASSET IS LEASED ............................. 30

4

CHAPTER 1: Introduction and Background

1.1 Background and Problem Statement Prior to the 1950s only land and buildings were leased. Today, however almost any fixed

asset can be leased. For example about 50% of all new commercial aircraft sold is purchase

by aircraft leasing companies (Brigham et al., 1999).

At times companies make the decision to buy or lease equipment while not taking into

account all the factors that will have a positive or negative effect on the cash flow associated

with the decision made. This could be due to the fact that the management of a trading entity

may not be aware of the long term impact that acquiring an asset through leasing or buying

has on the capital budget of the company.

Most published literature that discusses the decision to lease or purchase equipment only

addresses the matter from a certain perspective and hence leaves out other factors that are

relevant to management faced with the task of deciding to lease or purchase equipment. For

example some publications present mathematical models that can be used to decide whether

to lease or purchase equipment but leaves out the detailed theoretical explanations of the cash

flows incorporated into the formulas of the models and the effect that these cash flows will

have on the capital budget of the company, which is what management is interested in. These

models can prove to be of little help since they can be difficult to understand and implement

and require extensive mathematical knowledge to solve them.

There is a great need for a comprehensive analysis of leasing and purchasing equipment and a

simplified approach of deciding whether to lease or purchase equipment that will be relevant

and easy to implement for all companies.

1.2 Project Aim The aim of this study is to provide a detailed research on the following:

The cash flows associated with leasing and purchasing equipment.

The factors that companies should consider when contemplating to lease or purchase

equipment.

The effect that leasing and purchasing equipment has on a company’s capital budget.

Then finally provide a structured approach that can be followed by any company when

deciding to lease or purchase equipment.

5

1.3 Project Scope To conduct the study the following problem solving approach will be used (Tarquin, 2008:8)

Step 1: understand the problem.

Step 2: Collect information.

Step 3: Define feasible alternative solution and make realistic estimations.

Step 4: Identify criteria for decision making.

Step 5: Evaluate each alternative.

Step 6: Select the best alternative.

To accomplish the first two steps, an in depth study of the literature currently available about

buying and leasing equipment and how the capital budget is affected by leasing or purchasing

equipment. The effect that the size of the loan acquired to purchase the equipment, period to

pay back the loan, inflation rate and project life on the decision to purchase or lease

equipment.

With regards to step 3; the alternative solutions will be the different techniques of evaluating

capital investment decisions. Keep in mind that the solution in this case would be the best

suited technique to be used when deciding to lease or purchase equipment.

According to step 4, a decision making criteria must be selected for each technique

mentioned in step3.

In step 5 each decision making technique will be evaluated and compared against each other.

Lastly a conclusion will be reached on which technique is to be used when deciding to lease

or purchase equipment.

6

Chapter 2: Literature Review

2.1 Capital Budget A capital budget consists of an outline of planned long term investments on fixed assets.

Capital budgeting is the process of analyzing projects and deciding which ones to include in

the company’s capital budget. Assets included in the capital budget have the following

characteristics (du Toit et al., 2001):

The expected life of the asset is longer than one year.

They are not traded in the normal course of the firm’s business.

The equipment to be discussed in this study present the features or characteristics mentioned

above therefore they are recorded in the capital budget and can be referred to as capital

budget investments.

2.1.1 Importance of the capital budget The distribution of resources in the capital budget determines whether management will

be able to produce a minimum return on the investor’s money that the investor would

have received on an alternative investment. This factor determines whether investors keep

investing in the company or they take their investments elsewhere (Brigham et al.,2005).

From the capital budget potential investors and current investors can determine the firm’s

strategic direction.

The acquisition of assets or projects that the company decides to finance will affect the

company’ cash flow for a number of years still to come, that is why capital budgeting is

preceeded by a forecast of future expences and future income. A significant amount of

this forecast is done during the analysis of the cash flows associated with leasing or

purchasing equipment.

2.1.2 Influence of the capital structure on capital budget decisions

To acquire an asset buy leasing or purchasing a company needs capital. Capital structure

refers to the different sources of capital that a company uses, the fixed amount of capital

that the company gets from each source and the cost of each capital source. These

different sources of capital are referred to as capital components. According to Brigham

et al., (1999) the three major capital components are: common stock, preferred stock and

debt capital. Companies may choose to use only one of these sources of capital or a

combination of two sources or a combination of all three sources.

7

Common stock refers to the amount that shareholders have invested in the organisation

plus retained earnings, which is the amount earned from income generating activities

(Walter & Charles, 2008). Preferred stock is a hybrid of common stock and long-term

debt. Preferred stock can be referred to as long term debt because if it is used as capital to

acquire an asset then a fixed dividend must be paid to the preferred stockholders. It can

also be referred to as common stock because the dividend is not paid out to the preferred

stock holders unless the board of directors declare the dividend, as this is the case with

common stock (Walter & Charles, 2008). Debt capital refers to raising capital by

acquiring debt; it can be through a loan or issuing bonds. Each company ought to have an

optimal capital structure that is aimed at providing the highest possible economic value

added (EVA).

According to Brigham et al., (1999) the capital structure is used to determine the cost of

capital by using the weighted average cost of capital equation (WACC).

WACC = 𝒘𝒅𝒌𝒅 𝟏 − 𝑻 + 𝒘𝒑𝒔𝒌𝒑𝒔 + 𝒘𝒄𝒆𝒌𝒔 [𝟐. 𝟏]

wd, wps and wce are the weights used for debt, preferred and common equity respectively.

kd is the interest rate of the debt.

T is the marginal tax of the firm.

Kps is the preferred dividend divided by the net issuing price, 𝑘𝑝𝑠 = 𝐷𝑝𝑠

𝑃𝑛

Ks is the rate of return required by investors.

The weights for debt, preferred equity and common equity are determined by each

company on the company’s capital structure policy.

Capital structure enables management to determine beforehand the projects that will

require a minimum cost of capital. By considering the capital structure management can

determine the capital component that costs the most at that specific time, and then use less

of that capital component when financing new capital investments.

2.1.3 Influence of interest, tax and inflation rates on cost of capital

When interest rates in the economy increase the cost of debt capital will also increase

because bondholders and banks will require a higher interest rate. Higher interest rates

will also increase the cost of preferred equity capital. Variation in the tax rate will affect

the cost of capital equity. An increased tax rate will lead to a low cost of debt capital

according to the WACC equation (Brigham et al., 1999). An increase in inflation tends to

8

increase the required rates of return by the investors, this leads to a higher cost of capital

(du Toit et al., 2001).

2.2 Lease of Equipment

2.2.1 Typical lease agreement

Leasing is characterised by the separation of ownership of the asset and right of use of the

asset between the lessor and the lessee. The lessor owns the asset but the lessee has the right

to use the asset (du Toit et al., 2001). According to the Internal Revenue Service an

agreement is regarded as a lease agreement if the following requirements are met (Brigham

1999):

The period of leasing the asset (including renewals and extensions of the lease

agreement) should not exceed 80% of the estimated useful life of the asset. The

remaining useful life of the asset after the lease term must not be less than a year.

The residual value of the asset at the end of the lease term must at least equal 20% of

the value of the asset at the start of the lease period.

The lessee or any other party is not allowed to purchase the equipment at a price

determined at the start of the lease term.

A lease agreement usually contains the following information:

The duration of the lease contract.

The specific lease payments and the number of payments.

Conditions of renewal of the lease agreement.

Individual responsible for maintenance costs.

How the residual value will be incorporated in the cash flows.

The description of the leased assets.

2.2.2 Different types of leases available

Leasing takes place in four different forms, being, the operating lease, financial or capital

lease and a sale and sale back lease agreement (Brigham et al., 1999).

Operating lease

The lessor is required to maintain and service the leased equipment, the cost of

maintaining is built into the lease payment.

The lease payments are not sufficient for the lessor to cover the full capital

coat of the asset.

Operating lease agreements contain a cancellation clause which allows the

lessee to cancel the lease and return the asset before the end of the lease term.

9

Financial or capital lease

The lessor does not provide maintenance services.

The lease payments fully amortize the capital cost of the equipment.

The lease agreement is not cancellable, unless the asset is fully amortized.

Sale – and - Leaseback

A company that owns an asset sells the asset to another firm and

simultaneously executes an agreement to lease the equipment at specific terms

and period.

The seller gets the purchase price immediately from the buyer.

The seller still retains the use of the equipment.

2.2.3 Tax and leasing agreements

According to the Income Tax Act 1962, administered by the Commissioner of the South

African Revenue Services (SARS), tax payments and other expenditures incurred in the

production of income not of capital nature can be deducted from income for tax purposes.

These deductions grant tax savings for the lessee and are referred to as general deductions.

The tax savings are calculated in the following manner:

𝑻𝒂𝒙 𝒓𝒂𝒕𝒆 × 𝒍𝒆𝒂𝒔𝒆 𝒑𝒂𝒚𝒎𝒆𝒏𝒕 + (𝑶𝒕𝒉𝒆𝒓 𝒆𝒙𝒑𝒆𝒏𝒅𝒊𝒕𝒖𝒓𝒆𝒔 × 𝑻𝒂𝒙 𝒓𝒂𝒕𝒆) [2.2]

2.2.4 Influence of interest changes on a lease agreement

Interest rates influence the lease payments determined by the lessor on the lease agreement.

The internal rate of return (IRR) that will allow the net present value of the cash flows

experienced by the lessor equal to zero is the IRR that the lessor selects to determine the lease

payments.

The lessor determines the internal rate of return (IRR) required by considering the net

present value of the cash flows experienced while acquiring the asset and maintaining it.

These cash flows from the lessor perspective include: the net purchase price, maintenance

costs, tax on residual value and lease payment, depreciation and maintenance tax savings.

If the cost of capital (return required by the capital components) for acquiring and maintain

the asset was high, this will result in the lessor declaring a high IRR in order to pay back the

cost of capital and earn interest. This will result in high lease payments.

On the other hand if the return required by the capital components is relatively low, the lessor

will declare a lower IRR, hence the lease payments on the lease agreement will be lower

(Brigham et al., 1999).

10

2.3 Purchasing of equipment

2.3.1 Tax implications

According to the Legal and Policy division, South African Revenue Service (2009) all goods

purchased from a vendor value added tax (VAT) is paid as part of the purchase price. The

current vat rate is 14% is South Africa. Therefore when purchasing an asset, the VAT is

included in the purchase prize. Once the asset is purchased and put to use, the tax payer can

declare tax savings based on the operating expenses of the asset and depreciation expenses

(S.A Income tax Act section 6, 1962). If the asset is being resold at a market value that is

higher than the salvage value, a capital gains tax (CGT) is paid on the difference between the

two amounts (South African Income tax Act section 11, 1962).

2.3.2 Depreciation Depreciation refers to the reduction in the value of an asset (Tarquin, 2008). Depreciation

reduces the calculated net profit even though it is not a cash charge. A high depreciation leads

to a low tax bill (Brigham, 1999). Depreciation can be calculated using one of the following

methods

Straight line depreciation: The difference between the initial purchase price of the

asset and the estimated salvage value is divided by the economic life of the project to

find the annual depreciation amount (Tarquin, 2008). This method is mainly used for

stockholder reporting (or book purposes) (Brigham, 1999).

Modified accelerated cost recovery system (MACRS): This method consists of two

steps. In the first step the annual depreciation is determined by multiplying the initial

cost of the asset. In the second step, the book value in a particular year is determined

by subtracting the sum of annual depreciations (from previous years) from the initial

purchase price of the asset (Tarquin, 2008). This method is favoured when calculating

income tax since it yields high net profit reductions due to high depreciation

(Brigham, 1999).

2.4 Existing methodologies of making the lease-buy decision Various tools have been suggested to assist companies make the right choice to lease or

purchase equipment. The Vincil model also known as the Lease-Or-Borrow model is one of

these tools (Sartoris & Paul, 1973, 46:52). The Lease-Or-Borrow model compares the cost of

acquiring an asset through lease financing to the cost of acquiring the asset by purchasing the

asset using debt capital. The first step of the Lease-Or-Borrow model is to determine the net

present value of owning an asset, using the following formula

11

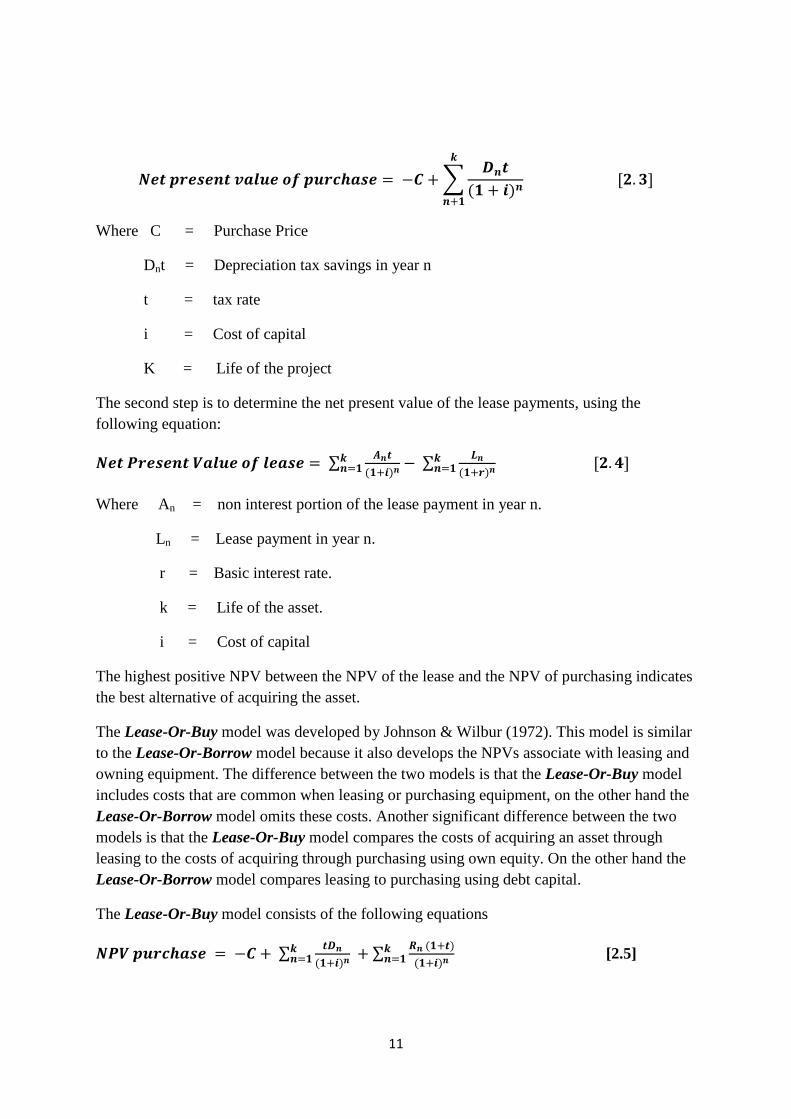

𝑵𝒆𝒕 𝒑𝒓𝒆𝒔𝒆𝒏𝒕 𝒗𝒂𝒍𝒖𝒆 𝒐𝒇 𝒑𝒖𝒓𝒄𝒉𝒂𝒔𝒆 = −𝑪 + 𝑫𝒏𝒕

(𝟏 + 𝒊)𝒏

𝒌

𝒏+𝟏

[𝟐. 𝟑]

Where C = Purchase Price

Dnt = Depreciation tax savings in year n

t = tax rate

i = Cost of capital

K = Life of the project

The second step is to determine the net present value of the lease payments, using the

following equation:

𝑵𝒆𝒕 𝑷𝒓𝒆𝒔𝒆𝒏𝒕 𝑽𝒂𝒍𝒖𝒆 𝒐𝒇 𝒍𝒆𝒂𝒔𝒆 = 𝑨𝒏𝒕

(𝟏+𝒊)𝒏𝒌𝒏=𝟏 −

𝑳𝒏

(𝟏+𝒓)𝒏𝒌𝒏=𝟏 [𝟐. 𝟒]

Where An = non interest portion of the lease payment in year n.

Ln = Lease payment in year n.

r = Basic interest rate.

k = Life of the asset.

i = Cost of capital

The highest positive NPV between the NPV of the lease and the NPV of purchasing indicates

the best alternative of acquiring the asset.

The Lease-Or-Buy model was developed by Johnson & Wilbur (1972). This model is similar

to the Lease-Or-Borrow model because it also develops the NPVs associate with leasing and

owning equipment. The difference between the two models is that the Lease-Or-Buy model

includes costs that are common when leasing or purchasing equipment, on the other hand the

Lease-Or-Borrow model omits these costs. Another significant difference between the two

models is that the Lease-Or-Buy model compares the costs of acquiring an asset through

leasing to the costs of acquiring through purchasing using own equity. On the other hand the

Lease-Or-Borrow model compares leasing to purchasing using debt capital.

The Lease-Or-Buy model consists of the following equations

𝑵𝑷𝑽 𝒑𝒖𝒓𝒄𝒉𝒂𝒔𝒆 = −𝑪 + 𝒕𝑫𝒏

(𝟏+𝒊)𝒏𝒌𝒏=𝟏 +

𝑹𝒏 (𝟏+𝒕)

(𝟏+𝒊)𝒏𝒌𝒏=𝟏 [2.5]

12

𝑵𝑷𝑽 𝒍𝒆𝒂𝒔𝒆 = 𝑹𝒏 +𝑶𝒏 (𝟏−𝒕)

(𝟏+𝒊)𝒏𝒌𝒏=𝟏 −

𝑳𝒏(𝟏−𝒕)

(𝟏+𝒓𝒕𝒊)𝒏𝒌𝒏=𝟏 [2.6]

Where Ri = Operating cash flow from the project in year i.

Oi = Operating costs that would occur under ownership of the asset but not under

the lease agreement.

rt = after tax interest rate.

Ln = Lease payment in year n.

Sartoris & Paul (173, 46:52) compared the two models (Lease-Or-Borrow and Lease-Or-

Buy) and reached a conclusion that Lease-Or-Borrow model leads to the correct decision

while Lease-Or-Buy model leads to an incorrect decision.

13

Chapter 3: Solution

3.1 Engineering methods and tools Leasing and purchasing equipment are both capital budget investments. Brigham et al.,(1999)

define the following capital budgeting decision rules that should be used to decide whether a

capital investment should be included in the capital budget or not.

Payback period – Compares the number of years required to recover the investment in

each project. The project with the lowest payback period is selected. It is applicable to

mutually exclusive projects.

𝑵𝒖𝒎𝒃𝒆𝒓 𝒐𝒇 𝒚𝒆𝒂𝒓𝒔 = 𝑰𝒏𝒊𝒕𝒊𝒂𝒍 𝑰𝒏𝒗𝒆𝒔𝒕𝒎𝒆𝒏𝒕

𝑨𝒏𝒏𝒖𝒂𝒍 𝒏𝒆𝒕 𝒄𝒂𝒔𝒉 𝒇𝒍𝒐𝒘 [𝟑. 𝟏]

Net Present Value (NPV) – NPV refers to the sum of the discounted cash flows at the

cost of capital. If NPV = 0, then the project is acceptable because the cash inflow is

sufficient to repay the initial investment at required rate of return of the capital. If

NPV > 0, then the project is still acceptable since the cash inflows will pay back the

cost of capital at a rate higher than the required cost of capital. If NPV < 0 then the

project is not acceptable since capital will be repaid at a rate that is less than the

required rate of return.

IRR (internal rate of return) –IRR is the rate of return required by a company to

ensures that the NPV of cash inflows is equal to zero. If the rate of return of any

project is less than the IRR of the company then that project is not included in the

capital budget.

MIRR (modified internal rate of return) – This decision making rule is an

improvement of the IRR. When using this rule, the terminal value (TV) has to be

defined. The TV is the future value of cash inflows. The MIRR is the discount rate

that ensures that the present value of cash outflows (PV cost) is equal to the present

value of the terminal value.

Profitability Index (Benefit cost ratio) – Shows the relative profitability of a project. A

project is acceptable if the Profitability index is greater than 1.0.

𝑷𝑰 = 𝑷𝑽 𝒃𝒆𝒏𝒆𝒇𝒊𝒕𝒔

𝑷𝑽 𝑪𝒐𝒔𝒕 [𝟑. 𝟐]

14

Brigham et al.,(1999) further mention that the net present value decision rule is the most

reliable and accurate decision rule.

3.2 Method selection and development To compare purchasing equipment and leasing equipment a cash flow analysis is used and the

cash flows are presented on spreadsheet models. This method is selected because it is easier

to prepare and understand spreadsheet models than to set up and understand mathematical

models. Hence, this method can be applied by any company. The NPV rule is used to analyse

the spreadsheets that represent the options of leasing and purchasing equipment in this study

because according to Brigham et al., (1999) this is the rule that managers prefer to use when

comparing projects. The reason for this is that the NPV value directly links to the economic

value added (EVA) to the company by a certain project and this is the information that

shareholders and investors are interested in. For example the NPV refers to the present value

of the EVA (Brigham et al., 1999). Brigham et al., (1999) further mentioned that well

managed companies cannot purchase equipment cash because cash is usually tied up in

assets.

To implement the method mentioned in the paragraph above, the following steps must be

followed.

I. State assumptions.

II. Collect the information that will be used to develop the spreadsheet models.

III. Present the expected cash flows on spreadsheet models.

IV. Determine the net present value in each of the spreadsheet models and decide on the

best alternative. The alternative with the highest positive NPV value will be accepted.

If the NPV value derived from the spread sheet calculations is negative, the option

represented by that spreadsheet is not accepted.

V. Determine how some inputs of the spreadsheet models affect the NPV, by changing

one input variable while keeping all other parameters and variables the same.

The final step is optional. It can be done if the company would like to know how certain

parameters will affect the cash flows associated with leasing and the cash flows associated

with purchasing. This step will be demonstrated in chapter 4.

To test this methodology, the steps listed above were used to decide whether to purchase or

lease an asset called the hydraulic mixer with scale (see figure 1). The relevant information

about the hydraulic mixer (e.g. purchase price, lease payments, operating costs) was made

available by the Turner and Morris Company located in Pretoria town Skinner Street. The

trade of the Turner and Morris Company is to sell and lease out fixed assets that are used in

the construction industry.

15

Figure 1: Hydraulic mixer

I. State assumptions

A loan is used to finance the purchase of the asset.

Payback period of the loan is 4 years.

The market value of the asset once it has been purchased decreases at a 10%

rate.

Life of the project is 15 years.

The minimum allowed rate of return (MARR) of the company is 15% since it

is normally stated to be higher than the rate of return charged by banks.

The lease presented on the spreadsheet model is an operating lease whereby

the lessor is responsible for the overhaul maintenance cost but the lessee is

responsible for the daily maintenance cost.

16

II. Collect relevant information

The data that is used to prepare the spread sheet models is presented on input tables

and calculations that precede each spread sheet model.

Steps III & IV are presented simultaneously on the spreadsheet models.

Below is the input table which represents data used to prepare the spreadsheet model that

represents the purchasing alternative.

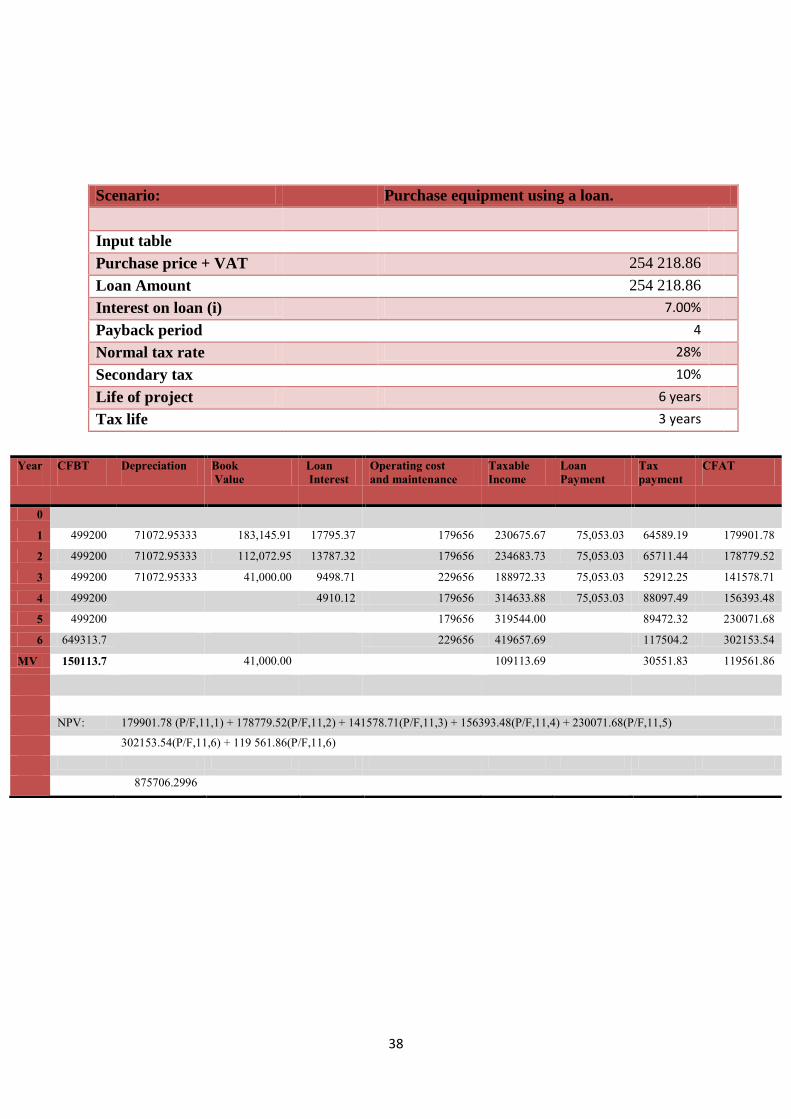

Table 1: Input data to the purchase spreadsheet model

Cash Flow Analysis for purchasing a hydraulic mixer using a loan.

Scenario: Purchase equipment using a loan.

Input table

Purchase price + VAT 254 218.86

Loan Amount 254 218.86

Interest on loan (i) 7.00%

Payback period 4 years

Normal tax rate 28%

Secondary tax 10%

Life of project 15 years

Tax life 3 years

17

Calculations:

Annuity, A (n = 4) P(A/P,7,4)

Depreciation per year: R 75 053.03

(254218.86 - 40 000)/3

R 71 406.28667

Annual interest (n = 4) : A(P/A,7,n)*7% Interest in year 1 17795.37

Annual Income :

Interest in year 2 13787.32

each load = 5 litres at R50 per 5 litres

Interest in year 3 9498.71

In one hour = 4 loads

Interest in year 4 4910.12

operates for 8 hours 6 days per week Assume 52 weeks per year

(6*52*8)*(4*50)

Annual operating expenses

R 499200 diesel (R11 per hour) 440

2 labourers (R18 per hour) 89856 1 Operator ( R35 per hour) 87360

MARR After tax Engine oil and filter service 2000

MARR Before Tax = 15%

Total R 179656

MARR(Before tax) (1 - Tax rate) Assumption: work 8 hrs 6 days a week

0.108

Overhaul service every 3 years R 50 000

11%

Market Value After 15 years: 254 218.86 *( 1- g)^(15-1); g = 10%

58157.12098

The purchase price of this asset was provided by the Turner and Morris Company.

The loan used to purchase this equipment covers the entire purchase price. According

to Brigham et al., (1999) well managed companies cannot afford to purchase such

equipment cash since the company’s cash is tied up in fixed assets. The effect that the

percentage of own equity used to purchase the equipment is still to be investigated

further in this study.

The annuities and interest rates were calculated using discount factors published by

Blank Tarquin (2008).

The interest rate on the loan is 7% as this is the official rate of interest published by the

Legal and Policy division South African Revenue Services, March 2011.

18

The MARR before tax is 15% and it is based on the interest rate charged by the banks.

The MARR expected by management in companies is always higher that the interest

charged by the banks in order to declare a profit.

The depreciation used is straight line depreciation (Brigham et al., 1999:446)

The tax life of this equipment (cement mixer) is 3 years as stated on the Binding

General Ruling (Income Tax Act): NO.7 published 11 April 2011.

The Normal and Secondary tax rates are as published by the South African Revenue

Services.

To determine the market value at the end of the life of the project, it was assumed that

the market value decreases by 10% per year. The formula used is stated under

calculations.

The operating expenses and income are specific to the equipment being evaluated.

Below is the spreadsheet model that represents the option of purchasing the asset.

Table 2: Purchasing Spreadsheet model

Year

CFBT

Depreciation

Book

Value

Loan

Interest

Operating

cost

and

maintenance

Taxable

Income

Loan

Payment

Tax

payment

CFAT

0

1 499200 -71072.95 183,145.91 17795.37 179656 230675.67 75,053.03 64,589.19 179901.78

2 499200 -71072.95 112,072.95 13787.32 179656 234683.73 75,053.03 65,711.44 178779.52

3 499200 -71072.95 41,000.00 9498.71 R 229,656 R 188,972.33 75,053.03 52,912.25 R 141,578.71

4 499200 4910.12 179656 R 314,633.88 75,053.03 88,097.49 R 156,393.48

5 499200 179656 319544 89,472.32 230,071.68

6 499200 R 229,656 269544 75,472.32 R 194,071.68

7 499200 179656 319544 89,472.32 R 230,071.68

8 499200 179656 319544 89,472.32 R 230,071.68

9 499200 R 229,656 269544 75,472.32 R 194,071.68

10 499200 179656 319544 89,472.32 R 230,071.68

11 499200 179656 319544 89,472.32 R 230,071.68

12 499200 R 229,656 269544 75,472.32 R 194,071.68

13 499200 179656 319544 89,472.32 R 230,071.68

14 499200 179656 319544 89,472.32 R 230,071.68

15 499200 R 229,656 269544 75,472.32 R 194,071.68

MV 58,157 41,000.00 17,157.12 4,803.99 R 53,353.13

NPV:

179 901.78(P/F,11,1) + 178 779.52(P/F,11,2) + 141 578.71(P/F,11,3) + 156 393.48(P/F,11,4) + 230 071.68(P/F,11,5)

194 071.68(P/F,11,6) + 230 071.68(P/A,11,2)(P/F,11,6) + 194 071.68(P/F,11,9) + 230 071.68(P/A,11,2)(P/F,11,9)

+ 194 071.68(P/F,11,12) + 230 071.68(P/A,11,2)(P/F,11,12) + 194(P/F,11,15) + 53 353.13(P/F,11,15)

19

1414270.19

EAA (Equivalent Annual Annuity) = P(A/P,11,15)

196682.556

All cash flows are considered to be at the end of the year.

CFBT refers to cash flow before tax, and CFAT refers to cash flow after tax

The CFBT is the income generated by the equipment; in this case it is determined

under calculations.

The depreciation is calculated as stated on the calculations above.

The taxable income is calculated by subtracting the tax saving from depreciation and

expenditure and loses actually incurred during the year of assessment in the

production of income not of a capital nature (Income Tax Act, 1962) from the gross

income. In this case these expenses include the interest rate on the loan and operating

expenses.

𝑫𝒆𝒑𝒓𝒆𝒄𝒊𝒂𝒕𝒊𝒐𝒏 𝑻𝒂𝒙 𝒔𝒂𝒗𝒊𝒏𝒈𝒔 𝒂𝒕 𝒕𝒉𝒆 𝒆𝒏𝒅 𝒐𝒇 𝒕𝒉𝒆 𝒚𝒆𝒂𝒓 =

𝑫𝒆𝒑𝒓𝒆𝒄𝒊𝒂𝒕𝒊𝒐𝒏 𝒑𝒆𝒓 𝒚𝒆𝒂𝒓 × 𝑻𝒂𝒙 𝒓𝒂𝒕𝒆 [𝟑. 𝟑]

𝑶𝒕𝒉𝒆𝒓 𝒆𝒙𝒑𝒆𝒏𝒄𝒆𝒔 𝒕𝒂𝒙 𝒔𝒂𝒗𝒊𝒏𝒈𝒔 =

𝑬𝒙𝒑𝒆𝒏𝒄𝒆𝒔 × 𝒕𝒂𝒙 𝒓𝒂𝒕𝒆 [𝟑. 𝟒]

The loan payment is computed as stated under calculations. This amount includes

both the interest on the loan and the principle amount.

𝑻𝒂𝒙 𝒑𝒂𝒚𝒎𝒆𝒏𝒕 = 𝑻𝒂𝒙𝒂𝒃𝒍𝒆 𝒊𝒏𝒄𝒐𝒎𝒆 × 𝟎. 𝟐𝟖 [𝟑. 𝟓]

𝑪𝑭𝑨𝑻 =

𝑻𝒂𝒙𝒂𝒃𝒍𝒆 𝒊𝒏𝒄𝒐𝒎𝒆 − 𝒕𝒂𝒙 𝒑𝒂𝒚𝒎𝒆𝒏𝒕 − 𝒍𝒐𝒂𝒏 𝒑𝒂𝒚𝒎𝒆𝒏𝒕 + 𝒅𝒆𝒑𝒓𝒆𝒄𝒊𝒂𝒕𝒊𝒐𝒏 +

𝒍𝒐𝒂𝒏 𝒊𝒏𝒕𝒆𝒓𝒆𝒔𝒕. [𝟑. 𝟔]

After the life of the project (15 YEARS) the market value of the equipment is higher

than the book value (40 000). Capital gains tax is paid on the difference between the

market value and book value. The capital gains tax was assumed to be 28% of the

difference between the book value and the market value.

The NPV for the option to purchase equipment using a loan to finance it is positive,

which means that this option is acceptable.

20

Next, the option of leasing the asset is considered. Steps III & IV will be presented in the

same manner as in the option of purchasing the asset.

Table: 3 Input data for the leasing spreadsheet model

Scenario: Acquiring equipment through leasing

Input table

Purchase price +

VAT

254 218.86

Annual lease

payment

215 162.46

Normal tax rate 28%

Secondary tax 10%

Life of project 12 years

Tax life 3 years

Table: 4 Spread sheet that represents then leasing option

Year CFBT lease payment Operating cost Taxable Tax CFAT

and maintenance Income payment

0 -215162.46

1 499200 430324.92 179656 -110780.92 -110780.92

2 499200 215162.46 179656 104381.54 29226.8312 75154.7088

3 499200 215162.46 179656 104381.54 29226.8312 75154.7088

4 499200 215162.46 179656 104381.54 29226.8312 75154.7088

5 499200 215162.46 179656 104381.54 29226.8312 75154.7088

6 499200 215162.46 179656 104381.54 29226.8312 75154.7088

7 499200 215162.46 179656 104381.54 29226.8312 75154.7088

8 499200 215162.46 179656 104381.54 29226.8312 75154.7088

9 499200 215162.46 179656 104381.54 29226.8312 75154.7088

10 499200 215162.46 179656 104381.54 29226.8312 75154.7088

11 499200 215162.46 179656 104381.54 29226.8312 75154.7088

12 499200 179656 319544 89472.32 230071.68

NPV:

- 110 780 (P/F,11,1)+ 75 154.709*(P/A,11,10) (P/F,11,1)+ 230 071.68*(P/F,11,12)

364691.2973

21

EAA (Equivalent Annual annuity) = P(A/P,11,12)

56173.40053

The lease payment is always paid at the beginning of the year. However, the first

lease payment can be paid along with the second payment at the beginning of the first

year.

Lease payments are considered to be an expense, hence, there are tax savings

experienced due to lease payments. Equation [3.4] was used to determine the tax

savings associated with the lease payment.

The value of operating expenses represents the expenses experienced daily, not the

overhaul expenses. This value was calculated in the calculations preceding the

spreadsheet model that represents the purchasing option. Equation [3.4] was used to

determine the tax savings associated with this expense.

The NPV is positive which makes this alternative acceptable.

When considering the NPV values on the spreadsheets we notice that the NPV on the

spreadsheet that represents purchasing is higher (R 1 414 270.19) than the NPV valve on the

spreadsheet that represents leasing (R 364 691.2973). These values suggest that the

purchasing alternative should be implemented. According to the NPV rule the alternative

with the highest positive NPV should be implemented. However, there is still another factor

to consider; the lives of the projects are not the same. In order to compare projects with

different lives the Equivalent Annual Annuity (EAA) value should be used (Brigham et al.,

1999). In each spreadsheet the EAA value is calculated right after the NPV value. The option

with the highest positive EAA value should be chosen. The EAA of the purchasing

calculations is R 1960682.556 and the EAA value of the leasing calculations is R

560173.40053. The purchasing option has a higher EAA value which means the asset should

be purchased rather than leased.

22

Chapter 4: Analysis

To accomplish step V sensitivity analysis was carried out on both spreadsheet models, to

determine how certain parameters affect the cash flows associated with leasing and

purchasing.

To determine how the percentage of own equity used to purchase the equipment affects the

NPV, different purchasing spreadsheet models were prepared where the amount of own

equity used to purchase the asset varied from 0% of the purchase price to 100% of the

purchase price. The spreadsheet model representing 0% own equity can be seen on table 2

and the spreadsheet models representing 25% to 100% own equity can be found in appendix

A. From figure 2 it can be seen that when the percentage of own equity used to finance the

purchase price increases, the NPV or profit that is expected from a project will decrease at a

constant rate. This shows that it would be best to purchase the asset using a loan rather than

use own equity (company’s money) to purchase the equipment.

Figure 2: Sensitivity analysis of NPV to the variation in the % of equity used to purchase the asset

1360000

1370000

1380000

1390000

1400000

1410000

1420000

0% 25% 50% 75% 100%

NP

V

% of own equity used to purchase equipment

Change in NPV as equity changes

NPV

23

Table 5: NPV and Equity

NPV Equity

1414270 0%

1406336 25%

1398381 50%

1390413 75%

1382446 100%

Figure 3, below demonstrates how the NPV of a project changes if the duration of the project

decreases, when the asset is purchased using a loan. When the project life is varying the

market value of the asset at the end of the project life is affected, as well as the total income

generated since the number of operating years is varying. A project life of 15 years is the

normal scenario depicted on table 2, for further investigation the project life was reduced to 3

years (these spreadsheet models are shown in appendix B). On figure 3 it can be shown that

as the project life decreases from 15 years to 3 years the NPV or the return on the project

decreases. This is simply because the number of operating years has decreased hence less

profit is made.

24

Figure 3: Sensitivity analysis of NPV to the variation in project life if asset is purchased

Table: 6 Change in NPV as the project life varies

Project life NPV

3 812085.39

6 875706.2996

9 1141355.46

12 1179742.949

15 1223340.701

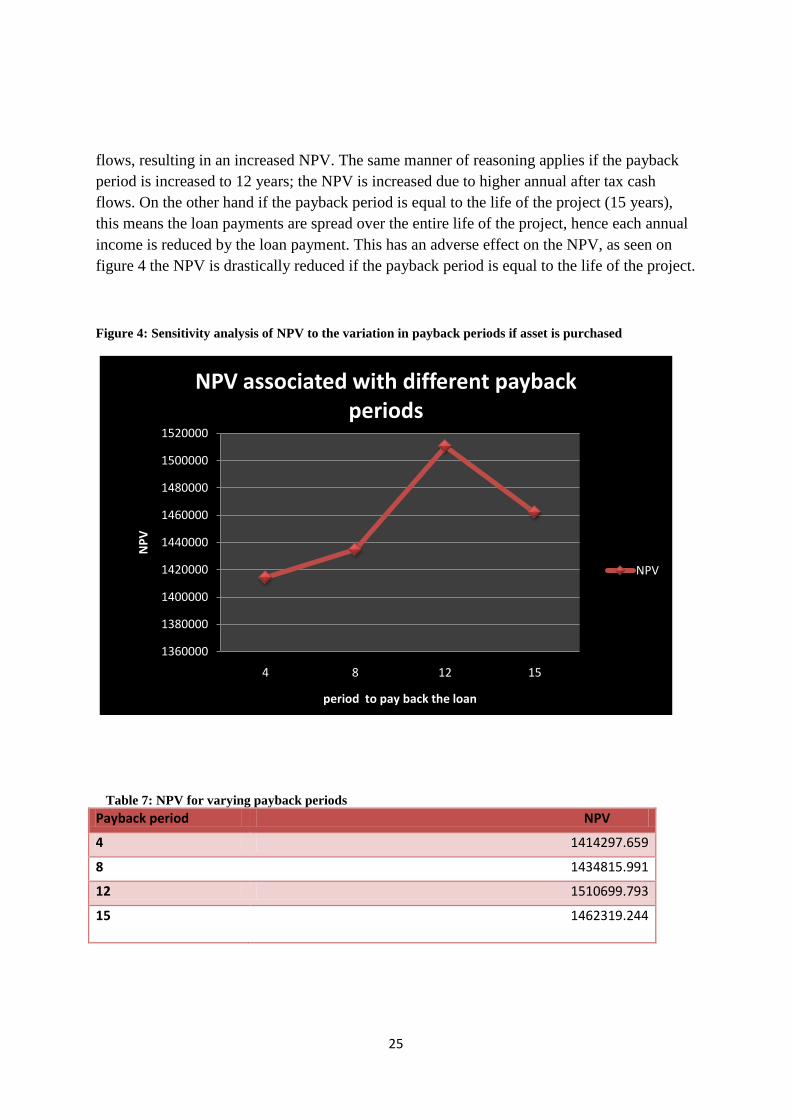

The graph bellow (figure 4) depicts how the payback period of a loan used to purchase an

asset affects the NPV. The payback period is increased from 4 years to 8, 12 and 15 years

(spreadsheet models representing these payback periods are found in appendix C). The

change in the payback period affects the annual loan payment expense. When the payback

period of the loan is increased to 8 years the NPV also goes up. This is because the loan is

paid over a longer period and in smaller quantities which leads to high annual after tax cash

0.00

200000.00

400000.00

600000.00

800000.00

1000000.00

1200000.00

1400000.00

3 6 9 12 15

Pro

ject

life

Project life

Change in NPV as project life changes

NPV

25

flows, resulting in an increased NPV. The same manner of reasoning applies if the payback

period is increased to 12 years; the NPV is increased due to higher annual after tax cash

flows. On the other hand if the payback period is equal to the life of the project (15 years),

this means the loan payments are spread over the entire life of the project, hence each annual

income is reduced by the loan payment. This has an adverse effect on the NPV, as seen on

figure 4 the NPV is drastically reduced if the payback period is equal to the life of the project.

Figure 4: Sensitivity analysis of NPV to the variation in payback periods if asset is purchased

Table 7: NPV for varying payback periods Payback period NPV

4 1414297.659

8 1434815.991

12 1510699.793

15 1462319.244

1360000

1380000

1400000

1420000

1440000

1460000

1480000

1500000

1520000

4 8 12 15

NP

V

period to pay back the loan

NPV associated with different payback periods

NPV

26

Figure 5 below illustrates how inflation affects the NPV associated with purchasing

calculations. The spreadsheets that support the information presented in figure 5 are

presented in appendix D. Inflation is the annual increase in the amount of money required to

purchase the same amount of goods. If the inflation rate is incorporated into the spreadsheet

model that represents purchasing, this results in the operating expenses increasing yearly at

the rate of inflation. As the inflation rate increases from 5% to 6.6% to 9.6% the NPV value

decreases since the yearly operating expenses also increases. The current inflation in South

Africa at the moment is estimated to be 6.6%, this estimate was determined through a process

called inflation targeting (de Jager & Kahan, 2011).

Figure 5: Sensitivity analysis of NPV to the variation in inflation if the asset is purchased

Table 8: NPV and inflation rates when purchasing

NPV inflation rate

1016691.3 5%

795365.58 6.60%

447344.19 9.60%

Further analysis was also done on the leasing spreadsheet. To investigate the effect of

inflation on the NPV if an asset is leased multiple leasing spreadsheets were prepared with

varying inflation rates. These spreadsheets can be seen in appendix E. Figure 6 below

0

200000

400000

600000

800000

1000000

1200000

5% 6.60% 9.60%

NP

V

Inflation rate

Change in NPV as inflation changes

NPV

27

demonstrates the results. The change in the inflation rate affects only the operating expenses

if the asset was leased. The lease payment expense is not affected because these payments are

determined at the beginning of the lease period and cannot be adjusted for inflation during the

duration of the lease; the inflation rate is considered when the payments are first established

at the beginning of the lease period. In figure 6, as the inflation rate increases from 5%, to

6.6% and to 9.6% the NPV of the leasing spread sheet is decreasing, the reason for this is that

as inflation gets higher the operating expenses get even more expensive. Once the inflation

hits 9.6%, the NPV will be negative, which makes the leasing option unacceptable. If the

inflation rate were to actually rise to 9.6% the asset would not be leased since the NPV when

the asset is leased is negative, the asset would be purchased because as seen in figure 5 the

NPV is positive when the asset is purchased and the inflation rate is 9.6%.

Figure 6: Sensitivity analysis of NPV to the variation in inflation rates if asset is leased

Table 9: NPV associated with different inflation rates when leasing

Inflation NPV

5% 313449.1171

6.60% 149529.2973

9.60% -305128.07

-400000

-300000

-200000

-100000

0

100000

200000

300000

400000

5% 6.60% 9.60%

NP

V

Inflation rate

Change in NPV as inflation changes

NPV

28

Figure 8 shows how different project lives can affect the NPV if an asset is leased. The

relevant spreadsheets are in Appendix F. As the life of the project is decreased from 12 to 9

years the NPV is also decreasing. The reason is that when the project life gets shorter, there

are less operating years hence, less income. When the asset is leased the market value of the

asset at the end of the project duration does not affect the NPV of profit from the project.

Figure 7: Sensitivity analysis of NPV to the variation in project life if the asset is leased

Table 10: NPV for different project durations in the leasing option

Project life Net Present Value

3 129421.4442

6 233247.6083

9 359744.6624

12 364691.2973

0

50000

100000

150000

200000

250000

300000

350000

400000

3 6 9 12

Ne

t P

rese

nt

Val

ue

Project Life

Change in NPV as project life increases

Net Present Value

29

To investigate how an increase in the interest rates would affect the profit expected from a

project whether the asset is leased or purchased further analysis was done on the leasing and

purchasing spreadsheet models and the results are show on figure 8 and figure 9. The

spreadsheet models supporting these graphs are on appendix G and appendix H respectively.

Figure 8: Sensitivity analysis of the affect of interest rate on the NPV an asset is purchased

Table 11: NPV for different interest rates

Interest rate NPV

0.07 1414270.194

0.08 1410565.397

0.11 1399170.018

0.14 1387507.857

1370000

1375000

1380000

1385000

1390000

1395000

1400000

1405000

1410000

1415000

1420000

0.07 0.08 0.11 0.14

NP

V

Interest rate

Change in NPV as interest rates increase

npv

30

Figure 9: Sensitivity analysis of the affect of interest rate on the NPV an asset is leased

Table 12: NPV and different interest rates when the asset is leased

INTERST RATE NPV

7% 364691.2973

8% 267922.9641

11% 231634.5301

14% 178398.398

From figure 8 and 9 it is evident that when the interest rate increases the return that is

expected on a project decreases, whether the asset was leased or purchased. However the

slope of the graph on figure 8 is –R 382 466.44 and the slope of the graph in figure 9 is

-R 3.7041E-07, these values show that an increase in the interest rates will have a higher

effect on the profit of a project if the assets used on the project are purchased.

0

50000

100000

150000

200000

250000

300000

350000

400000

7% 8% 11% 14%

NP

V

interest rates

Change in NPV as interest rate increases

npv

31

Chapter 5: Conclusions Based on the analysis in chapter 4, certain conclusions can be made regarding the effect that

inflation, interest rates and project life has on the decision to lease or purchase equipment.

The analysis also gave further insight on the effect of the loan payback period and the

percentage of equity used to purchase the equipment on the NPV if the asset is purchased.

The sensitivity analysis in figure 5 and 6 demonstrates the effect of different inflation

rates on the NPV when an asset is purchased and leased, respectively. The slope of

the graph in figure 5 is –12 277 451 and the slope of the graph in figure 6 is

-13 666 561, since figure 6 has a greater slope than figure 5 this implies that inflation

has a greater effect on the NPV if the asset is leased than when the asset is purchased.

Therefore, when an increase in inflation rate is expected it would be best to purchase

than to lease the asset.

The sensitivity analysis in figure 3 and in figure 7 show how the duration of the

project affects the NPV if the asset is purchased and leased respectively. The graph in

figure 3 has a slope of 37 551.576 and the slope of the graph in figure 7 is 27

743.55378. The slope of the sensitivity analysis graph (37 551.576) that reflects the

effect of the project life on the NPV when the asset is purchased is higher than the

slope of the sensitivity analysis graph (27 743.5) that shows the effect of the project

life when the asset leased. Therefore it can be concluded that it is best to lease the

asset than to purchase if the project life of the asset is less than 15 years.

Figure 8 demonstrates that as the interest rate increases the profit expected on a

project decreases at a rate of -382466 if the asset is purchased. On the other hand

figure 9 shows that as the interest rate increases the profit expected if the asset is

leased will decrease at a rate of -3.041E-07. From this it can be concluded that if a

rise in interest rates is anticipated it is best to lease the equipment.

If the decision to purchase the asset has been made the following conclusions can be made

based on figure 2 and 4.

Figure 2 shows the effect of using different values of own equity to purchase an asset

on the NPV when the asset is purchased. From this graph it can be concluded that it is

best to use a loan to purchase equipment since the return or profit of a project

decreases if own equity if used to finance the purchase price.

Figure 4 illustrates how different payback periods affect the NPV. Based on this

graph it can be concluded that as the loan payback period in increased the NPV will

also increase however, if the payback period is equal to the project life this leads to a

decrease in the NPV.

32

APPENDIX A – Purchasing models with different equity

Scenario: Purchase equipment using 25% equity.

Input table

Purchase price + VAT 254 218.86

Own equity 63 554.72

Loan Amount 190 664.15

Interest on loan (i) 7.00%

Payback period 4

Normal tax rate 28%

Secondary tax 10%

Life of project 15 years

Tax life 3 years

Year

CFBT

Depreciation

Book

Value

Loan

Interest

Operating cost

and maintenance

Taxable

Income

Loan

Payment

Tax

payment

CFAT

0 -63,554.72 -63,554.72

1 499200 -71072.9533 183,145.91 13346.53 179656 235124.516 56289.77553 65834.86 197419.36

2 499200 -71072.9533 112,072.95 10340.49 179656 238130.559 56289.77553 66676.56 196577.668

3 499200 -71072.9533 41,000.00 7124.034 229656 191347.013 56289.77553 53577.16 159677.061

4 499200 3682.59 179656 315861.41 56289.77553 88441.19 174813.03

5 499200 179656 319544 89472.32 230071.68

6 499200 229656 269544 75472.32 194071.68

7 499200 179656 319544 89472.32 230071.68

8 499200 179656 319544 89472.32 230071.68

9 499200 229656 269544 75472.32 194071.68

10 499200 179656 319544 89472.32 230071.68

11 499200 179656 319544 89472.32 230071.68

12 499200 229656 269544 75472.32 194071.68

13 499200 179656 319544 89472.32 230071.68

14 499200 179656 319544 89472.32 230071.68

15 499200 229656 269544 75472.32 194071.68

MV 58,157.12 41,000.00 17,157.12 4803.994 53,353.13

NPV:

-63 554.72 + 197 419.36(P/F,11,1) + 196 577.668(P/F,11,2) + 159 677.061(P/F,11,3) + 174 813.03(P/F,11,4)

230 071.68(P/F,11,5) + 194 071.68(P/F,11,6) + 230 071.68(P/A,11,2)(P/F,11,6) + 194 071.68(P/F,11,9)

230 071.68(P/,11,2)(F/P,11,9)+ 194 071.68(P/F,11,12) + 230 071.68(P/A,11,2)(P/F,11,12) + 194 071(P/F,11,15)

+ 53 353.13(P/F,11,15)

1406335.857

33

Scenario: Purchase equipment using 50% equity.

Input table

Purchase price + VAT 254 218.86

Own equity 63 554.72

Loan Amount 190 664.15

Interest on loan (i) 7.00%

Payback period 4

Normal tax rate 28%

Secondary tax 10%

Life of project 15 years

Tax life 3 years

Year

CFBT

Depreciation

Book

Value

Loan

Interest

Operating cost

and maintenance

Taxable

Income

Loan

Payment

Tax

payment

CFAT

0 -127,109.43 -127,109.43

1 499200 71072.95333 183,145.91 8923.956 179656 239547.091 37526.52 67073.19 214944.298

2 499200 71072.95333 112,072.95 6893.659 179656 241577.388 37526.52 67641.67 214375.814

3 499200 71072.95333 41,000.00 4749.356 R 229,656 193721.691 37526.52 54242.07 177775.41

4 499200 2455.06 179656 317088.94 37526.52 88784.9 193232.58

5 499200 179656 319544 89472.32 230071.68

6 499200 R 229,656 R 269,544 75472.32 194071.68

7 499200 179656 319544 89472.32 230071.68

8 499200 179656 319544 89472.32 230071.68

9 499200 R 229,656 269544 75472.32 194071.68

10 499200 179656 319544 89472.32 230071.68

11 499200 179656 319544 89472.32 230071.68

12 499200 R 229,656 269544 75472.32 194071.68

13 499200 179656 319544 89472.32 230071.68

14 499200 179656 319544 89472.32 230071.68

15 499200 R 229,656 269544 75472.32 194071.68

MV 58,157.12 41,000.00 17,157.12 4803.994 53,353.13

NPV:

-127 109.43 + 214 944(P/F,11,1) + 214 375.814(P/F,11,2) + 177 775.41(P/F,11,3) + 193 232.58(P/F,11,4)

230071.68(P/F,11,5) + 194 071.68(P/F,11,6) + 230 071.68(P/A,11,2)(P/F,11,6) + 194 071.68(P/F,11,9)

230 071.68(P/A,11,2)(P/F,11,9) + 194 071.68(P/F,11,12) + 194 071.68(P/F,11,12) + 230 071.68(P/A,11,2)(P/F,11,12)

194 071.68(P/F,11,15) + 53 353.13(P/F,11,15)

1398380.508

34

Scenario: Purchase equipment using 75% equity.

Input table

Purchase price + VAT 254 218.86

Own equity 63 554.72

Loan Amount 190 664.15

Interest on loan (i) 7.00%

Payback period 4

Normal tax rate 28%

Secondary tax 10%

Life of project 15 years

Tax life 3 years

Year

CFBT

Depreciation

Book

Value

Loan

Interest

Operating

cost

and

maintenance

Taxable

Income

Loan

Payment

Tax

payment

CFAT

0 -190,664.15 -190,664.15

1 499200 71,072.95 183,145.91 4448.8436 179656 244,022.20 18763.25851 68326.2168 232,454.52

2 499200 71,072.95 112,072.95 3446.8294 179656 245,024.22 18763.25851 68606.7808 232,173.96

3 499200 71,072.95 41,000.00 2374.678 229656 196,096.37 18763.25851 54906.9832 195,873.76

4 499200 1227.5299 179656 318,316.47 18763.25851 89128.6116 211,652.13

5 499200 179656 319,544.00 89472.32 230,071.68

6 499200 229656 269,544.00 75472.32 194,071.68

7 499200 179656 319,544.00 89472.32 230,071.68

8 499200 179656 319,544.00 89472.32 230,071.68

9 499200 229656 269,544.00 75472.32 194,071.68

10 499200 179656 319,544.00 89472.32 230,071.68

11 499200 179656 319,544.00 89472.32 230,071.68

12 499200 229656 269,544.00 75472.32 194,071.68

13 499200 179656 319,544.00 89472.32 230,071.68

14 499200 179656 319,544.00 89472.32 230,071.68

15 499200 229656 269,544.00 75472.32 194,071.68

MV 58157.12 41,000.00 17,157.12 4803.9936 53,353.13

NPV:

-190 664.15 + 232 454.52(P/F,11,1) + 232 173.96(P/F,11,2) + 195 873.76(P/F,11,3) + 211 652.13(P/F,11,4)

+ 230 071.68(P/F,11,5) + 194 071.68(P/F,11,6) + 230 071.68(P/A,11,2)(P/F,11,6) + 194 071.68(P/A,11,9)

+ 230 071.68(P/A,11,2)(P/F,11,9) + 194 071.68(P/F,11,12) + 230 071.68(P/A,11,2)(P/F,11,12)

+ 194 071.68(P/A,11,15) + 53 3553.13(P/A,11,15)

1390412.58

35

Scenario: Purchase equipment using 100% equity.

Input table

Purchase price +

VAT

254 218.86

Own equity (100%) 254 218.86

Loan Amount 0.00

Normal tax rate 28%

Secondary tax 10%

Life of project 15 years

Tax life 3 years

Year

CFBT

Depreciation

Book

Value

Operating cost

and maintenance

Taxable

Income

Tax

payment

CFAT

0 -254,218.86 -254,218.86

1 499200 71072.95333 183,145.91 179656 248471.047 69571.89307 249972.107

2 499200 71072.95333 112,072.95 179656 248471.047 69571.89307 249972.107

3 499200 71072.95333 41,000.00 229656 198471.047 55571.89307 213972.107

4 499200 179656 319544 89472.32 230071.68

5 499200 179656 319544 89472.32 230071.68

6 499200 229656 269544 75472.32 194071.68

7 499200 179656 319544 89472.32 230071.68

8 499200 179656 319544 89472.32 230071.68

9 499200 229656 269544 75472.32 194071.68

10 499200 179656 319544 89472.32 230071.68

11 499200 179656 319544 89472.32 230071.68

12 499200 229656 269544 75472.32 194071.68

13 499200 179656 319544 89472.32 230071.68

14 499200 179656 319544 89472.32 230071.68

15 499200 229656 269544 75472.32 194071.68

MV 58,157.12 41,000.00 17,157.12 4803.9936 53,353.13

NPV:

-254 218.86 + 249972.107(P/A,11,2) + 213972.107(P/F,11,3) + 230071.68(P/A,11,2)(P/F,11,3)

+ 194071.68(P/F,11,6) + 230071.68(P/A,11,2)(P/F,11,6) + 194071.68(P/F,11,9) + 230071.68(P/A,11,2)(P/F,11,9)

+ 194071.61(P/F,11,12) + 230071.68(P/A,11,2)(P/F,11,12) + 194071.68(P/F,11,15)

+ 53353.13(P/F,11,15)

1382446.222

36

APPENDIX B – Purchasing models with varying project life

Scenario: Purchase equipment using a loan.

Input table

Purchase price + VAT 254 218.86

Loan Amount 254 218.86

Interest on loan (i) 7.00%

Payback period 4

Normal tax rate 28%

Secondary tax 10%

Life of project 12 years

Tax life 3 years

Year

CFBT

Depreciation

Book

Value

Loan

Interest

Operating

cost

and

maintenance

Taxable

Income

Loan

Payment

Tax

payment

CFAT

0

1 499200 71072.95333 183,145.91 17795.37 179656 230675.67 75,053.03 64589.19 179901.78

2 499200 71072.95333 112,072.95 13787.32 179656 234683.73 75,053.03 65711.44 178779.52

3 499200 71072.95333 41,000.00 9498.71 229656 188972.33 75,053.03 52912.25 141578.71

4 499200 4910.12 179656 314633.88 75,053.03 88097.49 156393.48

5 499200 179656 319544.00 89472.32 230071.68

6 499200 229656 269544.00 75472.32 194071.68

7 499200 179656 319544.00 89472.32 230071.68

8 499200 179656 319544.00 89472.32 230071.68

9 499200 229656 269544.00 75472.32 194071.68

10 499200 179656 319544.00 89472.32 230071.68

11 499200 179656 319544.00 89472.32 230071.68

12 499200 229656 269544.00 75472.32 194071.68

MV 79776.572 41,000.00 38,776.57 10857.44 68,919.13

NPV:

179901.78(P/F,11,1) + 178 779.52(P/F,11,2) + 141 578.71(P/F,11,3) + 156 393.48(P/F,11,4) + 230 071.68(P/F,11,5)

194 071.68(P/F,11,6) + 230 0071.68(P/A,11,2)(P/F,11,6) + 194 071.68(P/F,11,9) + 230071.68(P/A,11,2)(P/F,11,9)

+ 194 071.68(P/F,11,12)+ 68 919.13(P/F,11,12)

1179742.95

37

Scenario: Purchase equipment using a loan.

Input table

Purchase price + VAT 254 218.86

Loan Amount 254 218.86

Interest on loan (i) 7.00%

Payback period 4

Normal tax rate 28%

Secondary tax 10%

Life of project 9 years

Tax life 10 years

Year

CFBT

Depreciation

Book

Value

Loan

Interest

Operating cost

and maintenance

Taxable

Income

Loan

Payment

Tax

payment

CFAT

0

1 499200 71072.95333 183,145.91 17795.37 179656 230675.67 75,053.03 64589.19 179901.78

2 499200 71072.95333 112,072.95 13787.32 179656 234683.73 75,053.03 65711.44 178779.52

3 499200 71072.95333 41,000.00 9498.71 179656 238972.33 75,053.03 66912.25 177578.71

4 499200 4910.12 179656 314633.88 75,053.03 88097.49 156393.48

5 499200 179656 319544.00 89472.32 230071.68

6 499200 179656 319544.00 89472.32 230071.68

7 499200 179656 319544.00 89472.32 230071.68

8 499200 179656 319544.00 89472.32 230071.68

9 499200 179656 319544.00 89472.32 230071.68

MV 109432.9 41,000.00 68,432.88 19161.21 90271.68

NPV:

179 901.78(P/F,11,1) + 178 779.52(P/F,11,2) + 177 578.71(P/F,11,3) + 156 393.48(P/F,11,4) +

230071.68(P/A,11,5)(P/F,11,4) + 90 271.68(P/F,11,9)

1141355.46

38

Scenario: Purchase equipment using a loan.

Input table

Purchase price + VAT 254 218.86

Loan Amount 254 218.86

Interest on loan (i) 7.00%

Payback period 4

Normal tax rate 28%

Secondary tax 10%

Life of project 6 years

Tax life 3 years

Year

CFBT

Depreciation

Book

Value

Loan

Interest

Operating cost

and maintenance

Taxable

Income

Loan

Payment

Tax

payment

CFAT

0

1 499200 71072.95333 183,145.91 17795.37 179656 230675.67 75,053.03 64589.19 179901.78

2 499200 71072.95333 112,072.95 13787.32 179656 234683.73 75,053.03 65711.44 178779.52

3 499200 71072.95333 41,000.00 9498.71 229656 188972.33 75,053.03 52912.25 141578.71

4 499200 4910.12 179656 314633.88 75,053.03 88097.49 156393.48

5 499200 179656 319544.00 89472.32 230071.68

6 649313.7 229656 419657.69 117504.2 302153.54

MV 150113.7 41,000.00 109113.69 30551.83 119561.86

NPV: 179901.78 (P/F,11,1) + 178779.52(P/F,11,2) + 141578.71(P/F,11,3) + 156393.48(P/F,11,4) + 230071.68(P/F,11,5)

302153.54(P/F,11,6) + 119 561.86(P/F,11,6)

875706.2996

39

Scenario: Purchase equipment using a loan.

Input table

Purchase price + VAT 254 218.86

Loan Amount 254 218.86

Interest on loan (i) 7.00%

Payback period 4

Normal tax rate 28%

Secondary tax 10%

Life of project 3 years

Tax life 3 years

Year

CFBT

Depreciation

Book

Value

Loan

Interest

Operating cost

and maintenance

Taxable

Income

Loan

Payment

Tax

payment

CFAT

0

1 499200 71072.95 183,145.91 17795.37 179656 410331.67 75,053.03 114,892.87 309254.10

2 499200 71072.95 112,072.95 13787.32 179656 414339.73 75,053.03 116,015.12 308131.84

3 705117.277 71072.95 41,000.00 9498.71 R 229,656 624545.61 75,053.03 174,872.77 455191.47

4 4910.12 75,053.03 -75053.03

NPV: 309254.10 (P/F,11,1) + 308131.84(P/F,11,2) + 455 191.47(P/F,11,3) - 75053.03(P/F,11,4)

812085.39

40

APPENDIX C- Purchasing models with different pay back periods

Scenario: Purchase equipment using a loan.

Input table

Purchase price + VAT 254 218.86

Loan Amount 254 218.86

Interest on loan (i) 7.00%

Payback period 8 years

Normal tax rate 28%

Secondary tax 10%

Life of project 15 years

Tax life 3 years

Year

CFBT

Depreciation

Book Value

Loan Interest

Operating cost and maintenance

Taxable Income

Loan Payment

Tax payment

CFAT

0

1 499200 71072.95333 183,145.91 17795.56 179656 230675.48 42,574.03 64589.14 212380.83

2 499200 71072.95333 112,072.95 16061.10 179656 232409.95 42,574.03 65074.79 211895.18

3 499200 71072.95333 41,000.00 14205.04 229656 184266.01 42,574.03 51594.48 175375.49

4 499200 12219.34 179656 307324.66 42,574.03 86050.9 190919.06

5 499200 10094.47 179656 309449.53 42,574.03 86645.87 190324.10

6 499200 7820.89 229656 261723.11 42,574.03 73282.47 153687.50

7 499200 5388.17 179656 314155.83 42,574.03 87963.63 189006.33

8 499200 2785.28 179656 316758.72 42,574.03 88692.44 188277.53

9 499200 229656 269544.00 75472.32 194071.68

10 499200 179656 319544.00 89472.32 230071.68

11 499200 179656 319544.00 89472.32 230071.68

12 499200 229656 269544.00 75472.32 194071.68

13 499200 179656 319544.00 89472.32 230071.68

14 499200 179656 319544.00 89472.32 230071.68

15 499200 229656 269544.00 75472.32 194071.68

MV 58157.121 41,000.00 17,157.12 4803.994 53353.13

NPV:

212 380.83(P/F,11,1) + 211 895.18(P/F,11,2) + 175 375.49(P/F,11,3) + 190 919.06(P/F,11,4) + 190 324.10*(F/P,11,5) +

153 687.50(P/F,11,6) + 189 006.33(P/F,11,7) + 188 277.53(P/F,11,8) + 194 071.68(P/F,11,9) + 230 071.68(P/A,11,2)(P/F,11,9)

+ 194 071.68(P/F,11,12) + 230 071.68(P/A,11,2)(P/F,11,12) + 194 071.68(P/F,11,15)

+ 53353.13(P/F,11,15)

1434815.991

41

Scenario: Purchase equipment using a loan.

Input table

Purchase price + VAT 254 218.86

Loan Amount 254 218.86

Interest on loan (i) 7.00%

Payback period 12 years

Normal tax rate 28%

Secondary tax 10%

Life of project 15 years

Tax life 3 years

Year

CFBT

Depreciation

Book

Value

Loan

Interest

Operating cost

and maintenance

Taxable

Income

Loan

Payment

Tax

payment

CFAT

0

1 499200 71072.95333 183,145.91 15778.68 179656 232692.36 32,006.15 65153.86 222383.98

2 499200 71072.95333 112,072.95 16800.32 179656 231670.73 32,006.15 64867.8 222670.04

3 499200 71072.95333 41,000.00 15735.89 229656 182735.16 32,006.15 51165.84 186372.00

4 499200 14596.85 179656 304947.15 32,006.15 85385.2 202152.64

5 499200 13378.28 179656 306165.72 32,006.15 85726.4 201811.45

6 499200 12074.35 229656 257469.65 32,006.15 72091.5 165446.34

7 499200 10679.01 179656 308864.99 32,006.15 86482.2 201055.65

8 499200 9186.21 179656 310357.79 32,006.15 86900.18 200637.67

9 499200 7588.79 229656 261955.21 32,006.15 73347.46 164190.39

10 499200 5879.56 179656 313664.44 32,006.15 87826.04 199711.80

11 499200 4050.70 179656 315493.30 32,006.15 88338.12 199199.72

12 499200 2093.91 229656 267450.09 32,006.15 74886.03 162651.82

13 499200 179656 319544.00 319544.00

14 499200 179656 319544.00 319544.00

15 499200 229656 269544.00 269544.00

MV 58157.12 41,000.00 17,157.12 4803.994 53353.13

NPV:

222 238.98 (P/F,11,1)+ 222 670.04(P/F,11,2) + 186 372.00(P/F,11,3) + 202152.64(P/F,11,4) +

201 811.45(P/F,11,5)+165 446.34(P/F,11,6) + 201 055.65(P/F,11,7) + 200 637.67P/F,11,8) + 164 190.39(P/F,11,9)

+199 199.80(P/F,11,10)+ 199 199.72(P/F,11,11) + 162 651.82(P/F,11,12) +319 544(P/A,11,2)(P/F,11,12)

+ 269 544(P/F,11,15) + 53353.13(P/F,11,15)

1510699.793

42

Scenario: Purchase equipment using a loan.

Input table

Purchase price + VAT 254 218.86

Loan Amount 254 218.86

Interest on loan (i) 7.00%

Payback period 4

Normal tax rate 28%

Secondary tax 10%

Life of project 15 years

Tax life 3 years

Year

CFBT

Depreciation

Book

Value

Loan

Interest

Operating cost

and maintenance

Taxable

Income

Loan

Payment

Tax

payment

CFAT

0

1 499200 71072.95333 183,145.91 17794.54 179656 230676.50 27,910.69 64589.42 227043.89

2 499200 71072.95333 112,072.95 17086.50 179656 231384.54 27,910.69 64787.67 226845.64

3 499200 71072.95333 41,000.00 16757.30 229656 181713.75 27,910.69 50879.85 190753.46

4 499200 15518.04 179656 304025.96 27,910.69 85127.27 206506.04

5 499200 14650.57 179656 304893.43 27,910.69 85370.16 206263.15

6 499200 13722.35 229656 255821.65 27,910.69 71630.06 170003.25

7 499200 12729.06 179656 306814.94 27,910.69 85908.18 205725.13

8 499200 11666.42 179656 307877.58 27,910.69 86205.72 205427.59

9 499200 10529.34 229656 259014.66 27,910.69 72524.11 169109.21

10 499200 9312.54 179656 310231.46 27,910.69 86864.81 204768.50

11 499200 8010.76 179656 311533.24 27,910.69 87229.31 204404.00

12 499200 6422.36 229656 263121.64 27,910.69 73674.06 167959.25

13 499200 5163.76 179656 314380.24 27,910.69 88026.47 203606.84

14 499200 3532.38 179656 316011.62 27,910.69 88483.25 203150.06

15 499200 1825.97 229656 267718.03 27,910.69 74961.05 166672.26

MV 58157.12 41,000.00 17,157.12 4803.994 53,353.13

NPV:

227 093.12(P/F,11,1) + 226 845.64(P/F,11,2) + 190 753.46(P/F,11,3) + 206 506.04(P/F,11,4) + 206 263.15(P/F,11,5) +

170003.25(P/F,11,6) + 205725.13(P/F,11,7) + 205 527.59(P/F,11,8)+ 169 109.21(P/F,11,9) + 204 768.50(P/F,11,10) +

204 404.00(P/F,11,11)+167 959.25(P/F,11,12) + 203 606.84(P/F,11,13) + 203 150.06(P/F,11,14) + 166 672.26(P/F,11,15)

+ 53 353.13(P/F,11,15)

1462319

43

APPENDIX D-Purchasing models with different inflation rates

Scenario: Purchase equipment using a loan.

Input table

Purchase price + VAT 254 218.86

Loan Amount 254 218.86

Interest on loan (i) 7.00%

Payback period 4

Normal tax rate 28%

Secondary tax 10%

Life of project 15 years

Tax life 3 years

Inflation rate 9.60%

Year

CFBT

Depreciation

Book

Value

Loan

Interest

Operating cost

and maintenance

Taxable

Income

Loan

Payment

Tax

payment

CFAT

0

1 499200 71072.95 183 145.91 17795.37 179656 230675.67 75 053.03 64 589.19 179901.78

2 499200 71072.95 112 072.95 13787.32 179656 234683.73 75 053.03 65 711.44 178779.52

3 499200 71072.95 41 000.00 9498.71 R 229 656 188972.33 75 053.03 52 912.25 141578.71

4 499200 4910.12 179656 314633.88 75 053.03 88 097.49 156393.48

5 499200 179656 319544.00 89 472.32 230 071.68

6 499200 R 229 656 269544.00 75 472.32 194 071.68

7 499200 179656 319544.00 89 472.32 230 071.68

8 499200 179656 319544.00 89 472.32 230 071.68

9 499200 R 229 656 269544.00 75 472.32 194 071.68

10 499200 179656 319544.00 89 472.32 230 071.68

11 499200 179656 319544.00 89 472.32 230 071.68

12 499200 R 229 656 269544.00 75 472.32 194 071.68

13 499200 179656 319544.00 89 472.32 230 071.68

14 499200 179656 319544.00 89 472.32 230 071.68

15 499200 R 229 656 269544.00 75 472.32 194 071.68

MV 58 157 41 000.00 17 157.12 4 803.99 53 353.13

NPV :

179 901.78(P/F,11,1) + 178 779.52(P/F,11,2) + 141 578.71(P/F,11,3) + 156 393.48(P/F,11,4) + 230 071.68(P/F,11,5)

194 071.68(P/F,11,6) + 230 071.68(P/A,11,2)(P/F,11,6) + 194 071.68(P/F,11,9) + 230 071.68(P/A,11,2)(P/F,11,9)

+ 194 071.68(P/F,11,12) + 230 071.68(P/A,11,2)(P/F,11,12) + 194(P/F,11,15) + 53 353.13(P/F,11,15)

1223341

44

Scenario: Purchase equipment using a loan.

Input table

Purchase price + VAT 254 218.86

Loan Amount 254 218.86

Interest on loan (i) 7.00%

Payback period 4

Normal tax rate 28%

Secondary tax 10%

Life of project 15 years

Tax life 3 years

Inflation rate 6.60%

Year

CFBT

Depreciation

Book

Value

Loan

Interest

Operating cost

and maintenance

Taxable

Income

Loan

Payment

Tax

payment

CFAT

0

1 499200 -71072.95 183 145.91 17795.37 196902.976 213428.70 75 053.03 59 760.03 167483.96

2 499200 -71072.95 112 072.95 13787.32 215805.6617 198534.07 75 053.03 55 589.54 152751.77

3 499200 -71072.95 41 000.00 9498.71 R 302 350 116278.69 75 053.03 32 558.03 89239.29

4 499200 4910.12 259229.2137 235060.67 75 053.03 65 816.99 99100.77

5 499200 284115.2182 215084.78 60 223.74 154861.04

6 499200 R 398 053 101146.80 28 321.10 72825.69

7 499200 341283.746 157916.25 44 216.55 113699.70

8 499200 374046.9856 125153.01 35 042.84 90110.17

9 499200 R 524 050 -24850.07 -24850.07

10 499200 449311.2239 49888.78 13 968.86 35919.92

11 499200 492445.1014 6754.90 1 891.37 4863.53

12 499200 R 689 929 -190729.07 -190729.07

13 499200 591532.9349 -92332.93 -92332.93

14 499200 648320.0966 -149120.10 -149120.10