the current state of consumer expectations and purchase drivers around sustainability: analysis of...

TRANSCRIPT

Claudia Suárez-Gapp Veridical Lead Public Development and Sustainability - Europe The Nielsen Company

The Current State of Consumer Expectations and Purchase Drivers around Sustainability: Analysis of the Latest Data

#SB15London

THE CURRENT STATE OF CONSUMER EXPECTATIONS AND PURCHASE DRIVERS AROUND SUSTAINABILITY: ANALYSIS OF THE LATEST DATA

THE SUSTAINABILITY IMPERATIVE

Claudia Suárez-‐Gapp The Nielsen Company 17 November 2015

Copyrig

ht ©

2014 The

Nielse

n Co

mpany. Con

fiden

Val and

proprietary.

3

LET’S DEFINE SUSTAINABILITY

Environmental Governance Social

Copyrig

ht ©

2014 The

Nielse

n Co

mpany. Con

fiden

Val and

proprietary.

4

SUSTAINABILITY AND PROFITABILITY ARE NOT MUTUALLY EXCLUSIVE

the success of your business is directly related to the health of the communiVes in which you operate sustainability is a

leading factor in the relevance,

viability and growth of your organizaVon

integraVng sustainability into your

strategy enables responsible

growth

Copyrig

ht ©

2014 The

Nielse

n Co

mpany. Con

fiden

Val and

proprietary.

5

HOW DO WE KNOW SUSTAINABILITY AND PROFITABILITY ARE NOT MUTUALLY EXCLUSIVE? Key Insights From 2015 The Sustainability ImperaVve Report

Source: The Sustainability ImperaVve, Nielsen Report 2015

of consumers say they are willing to pay more for brands with a commitment to sustainability

greater sales in brands with a demonstrated commitment to sustainability, while those without grew less than 1%

social responsibility is one of the most influenVal factors for corporate reputaVon for consumer goods companies

>4% 66% 1 2 3

CONSUMERS ARE WILLING TO PAY MORE

The number of consumers willing to pay more

for brands commi1ed to posi4ve social and environmental impact con0nues to rise— reaching 66% in 2015

Copyrig

ht ©

2014 The

Nielse

n Co

mpany. Con

fiden

Val and

proprietary.

8

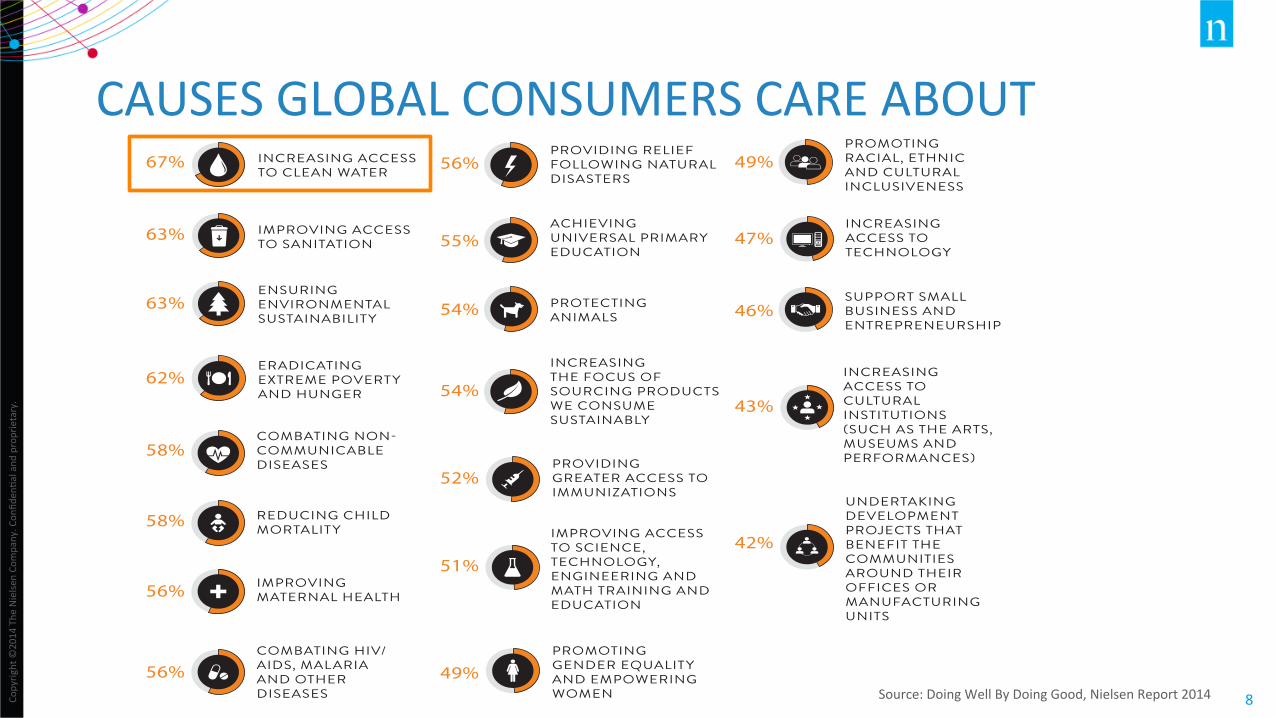

CAUSES GLOBAL CONSUMERS CARE ABOUT

Source: Doing Well By Doing Good, Nielsen Report 2014

THE CAUSES CONSUMERS CARE ABOUT

AMONG GLOBAL RESPONDENTS WILLING TO PAY EXTRA FOR PRODUCTS FROM COMPANIES COMMITTED TO POSITIVE SOCIAL AND ENVIRONMENTAL IMPACT

PERCENT THAT INDICATE EXTREME CONCERN

INCREASING ACCESS TO CLEAN WATER

67%

63% IMPROVING ACCESS TO SANITATION

63%ENSURING ENVIRONMENTAL SUSTAINABILITY

62%ERADICATING EXTREME POVERTY AND HUNGER

52%PROVIDING GREATER ACCESS TO IMMUNIZATIONS

49%PROMOTING GENDER EQUALITY AND EMPOWERING WOMEN

43%

INCREASING ACCESS TO CULTURAL INSTITUTIONS (SUCH AS THE ARTS, MUSEUMS AND PERFORMANCES)58%

COMBATING NON-COMMUNICABLE DISEASES

58% REDUCING CHILD MORTALITY

56% IMPROVING MATERNAL HEALTH

56%COMBATING HIV/ AIDS, MALARIA AND OTHER DISEASES

51%

IMPROVING ACCESS TO SCIENCE, TECHNOLOGY, ENGINEERING AND MATH TRAINING AND EDUCATION

47%INCREASING ACCESS TO TECHNOLOGY

42%

UNDERTAKING DEVELOPMENT PROJECTS THAT BENEFIT THE COMMUNITIES AROUND THEIR OFFICES OR MANUFACTURING UNITS

56%PROVIDING RELIEF FOLLOWING NATURAL DISASTERS

55%ACHIEVING UNIVERSAL PRIMARY EDUCATION

54% PROTECTING ANIMALS

54%

INCREASING THE FOCUS OF SOURCING PRODUCTS WE CONSUME SUSTAINABLY

49%PROMOTING RACIAL, ETHNIC AND CULTURAL INCLUSIVENESS

46%SUPPORT SMALL BUSINESS AND ENTREPRENEURSHIP

Copyrig

ht ©

2015 The

Nielse

n Co

mpany. Con

fiden

Val and

proprietary.

9

SUSTAINABILITY IS GAINING INFLUENCE Top purchasing drivers for global consumers

Source: The Sustainability ImperaVve, Nielsen Report 2015

Drivers: Overall: Gen Z: Millennials:

The products are made by a brand/company that I trust 62% 63% 65%

The product is known for its health & wellness benefits 59% 58% 64%

The product is made from fresh, natural and/or organic ingredients 57% 56% 61%

The product is from a company known for being environmentally friendly 45% 46% 51%

The product is from a company known for its commitment to social value 43% 46% 50%

The product’s packaging is environmentally friendly 41% 41% 46%

The product is from a company known for its commitment to my community 41% 38% 47%

I saw an ad on TV about the social and/or environmental good the product’s company is doing 34% 38% 41%

Copyrig

ht ©

2015 The

Nielse

n Co

mpany. Con

fiden

Val and

proprietary.

10

COMMITMENT TO SOCIAL AND ENVIRONMENTAL SUSTAINABILITY IS OF UTMOST IMPORTANCE

Source: The Sustainability ImperaVve, Nielsen Report 2015

For those willing to pay more, the importance of these factors increased the most

Drivers: Overall: Premium:

The products are made by a brand/company that I trust 62% 72%

The product is known for its health & wellness benefits 59% 70%

The product is made from fresh, natural and/or organic ingredients 57% 69%

The product is from a company known for being environmentally friendly 45% 58%

The product is from a company known for its commitment to social value 43% 56%

The product’s packaging is environmentally friendly 41% 53%

The product is from a company known for its commitment to my community 41% 53%

I saw an ad on TV about the social and/or environmental good the product’s company is doing 34% 45%

Copyrig

ht ©

2014 The

Nielse

n Co

mpany. Con

fiden

Val and

proprietary.

11

WHAT IS THE KEY SUSTAINABILITY PURCHASING DRIVER FOR EUROPEAN CONSUMERS?

FRESH, NATURAL, ORGANIC INGREDIENTS

FRESH, NATURAL, ORGANIC INGREDIENTS ARE PARAMOUNT TO 52% OF EUROPEAN RESPONDENTS.

Copyrig

ht ©

2014 The

Nielse

n Co

mpany. Con

fiden

Val and

proprietary.

12

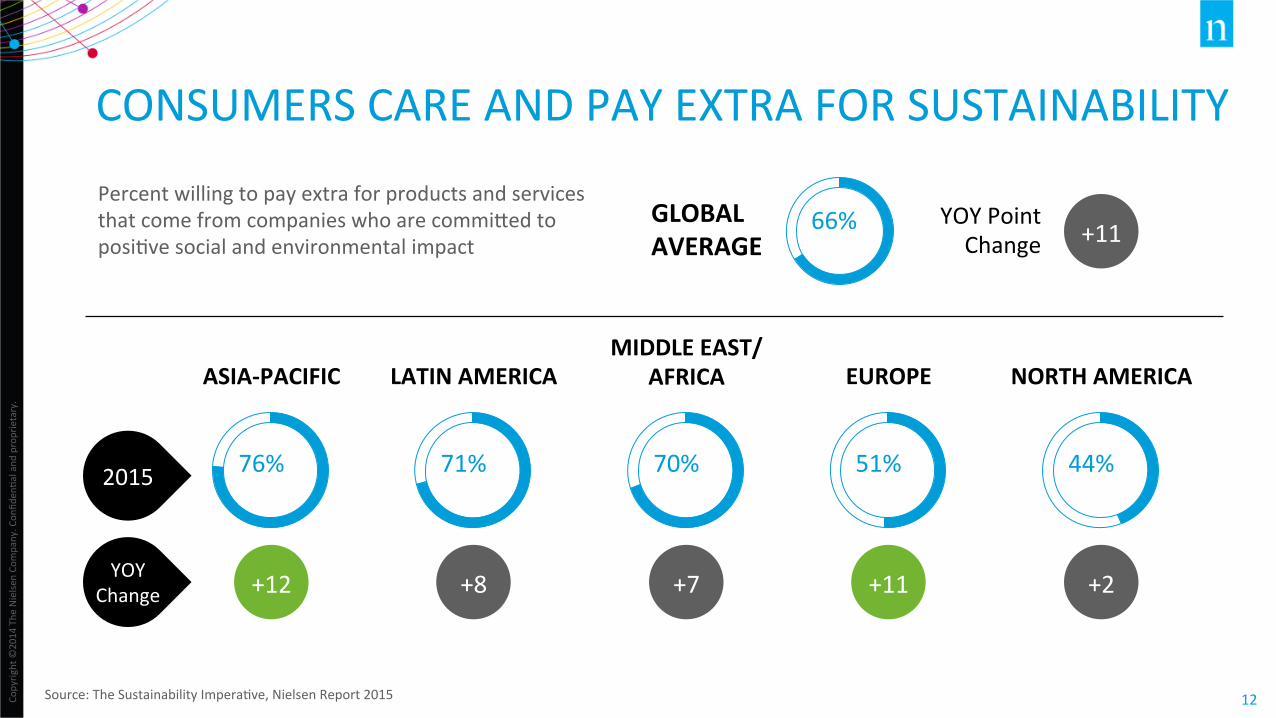

CONSUMERS CARE AND PAY EXTRA FOR SUSTAINABILITY

Percent willing to pay extra for products and services that come from companies who are commiked to posiVve social and environmental impact

ASIA-‐PACIFIC

GLOBAL AVERAGE

66% +11 YOY Point Change

76%

LATIN AMERICA

71%

MIDDLE EAST/AFRICA

70%

EUROPE

51%

NORTH AMERICA

44%

Source: The Sustainability ImperaVve, Nielsen Report 2015

2015

YOY Change +12 +8 +7 +11 +2

Copyrig

ht ©

2014 The

Nielse

n Co

mpany. Con

fiden

Val and

proprietary.

13

CONSUMERS UNDER 34 ARE WILLING TO PAY MORE

GROWING: GENERATION Z

72%

MOST LIKELY TO BUY: MILLENNIALS

73%

DON’T FORGET: BABY BOOMERS

51%

Copyrig

ht ©

2014 The

Nielse

n Co

mpany. Con

fiden

Val and

proprietary.

14

SMART CONSUMERS DO THEIR HOMEWORK AND TAKE ACTION

more connected millennials emerging middle class

SUSTAINABLE BRANDS OUTPERFORM

Copyrig

ht ©

2014 The

Nielse

n Co

mpany. Con

fiden

Val and

proprietary.

16

1,300+ brands 13 categories 13 markets

ON AVERAGE, PRODUCTS WITH SUSTAINABILITY EFFORTS CONTRIBUTED TO…

OVER 4% GREATER SALES

Source: The Sustainability ImperaVve, Nielsen Report 2015

Copyrig

ht ©

2014 The

Nielse

n Co

mpany. Con

fiden

Val and

proprietary.

17

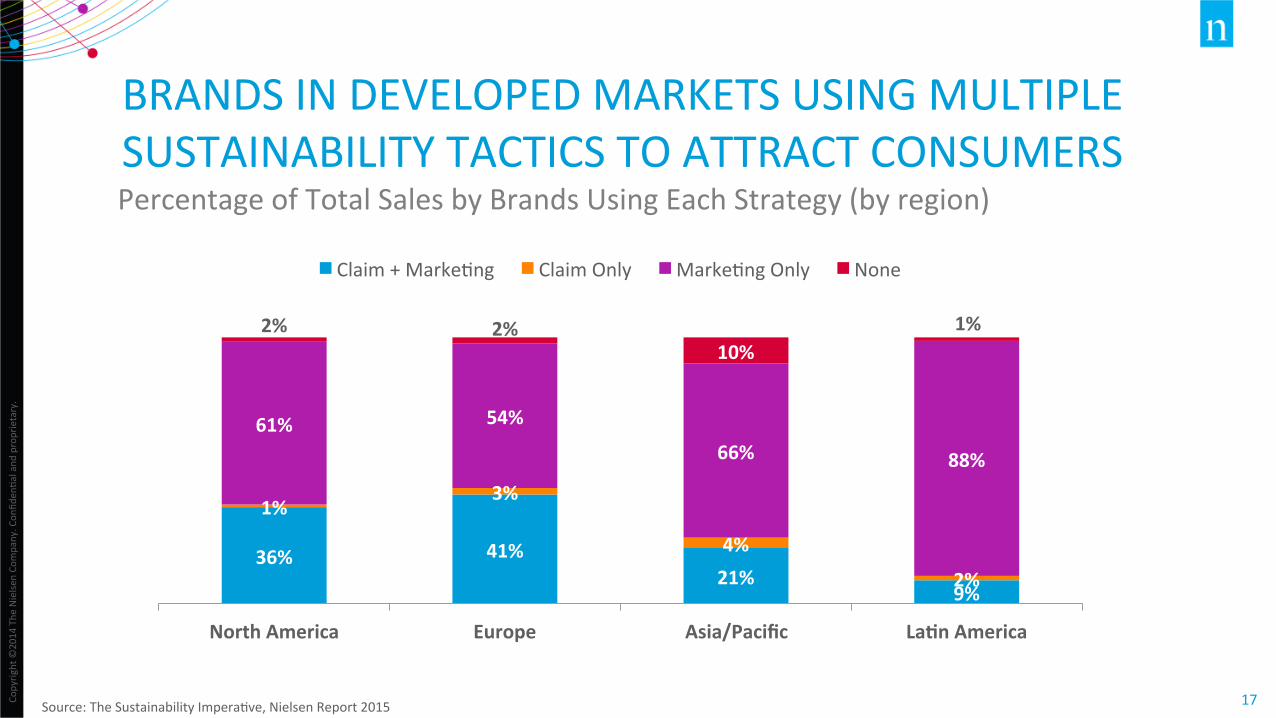

BRANDS IN DEVELOPED MARKETS USING MULTIPLE SUSTAINABILITY TACTICS TO ATTRACT CONSUMERS

36% 41% 21%

9%

1% 3%

4%

2%

61% 54%

66% 88%

2% 2% 10%

1%

North America Europe Asia/Pacific LaSn America

Claim + MarkeVng Claim Only MarkeVng Only None

Percentage of Total Sales by Brands Using Each Strategy (by region)

Source: The Sustainability ImperaVve, Nielsen Report 2015

Copyrig

ht ©

2014 The

Nielse

n Co

mpany. Con

fiden

Val and

proprietary.

18

CURRENT CATEGORY LANDSCAPE PRIMARILY FOCUS ON MARKETING

Source: The Sustainability ImperaVve, Nielsen Report 2015

0%

61%

44%

85%

48%

78%

15%

60%

16% 23%

8% 12% 12% 0%

13%

4%

3%

1%

1%

2%

1%

3% 0%

0% 6% 1%

99%

22%

51%

8%

48%

13%

79%

28%

69% 76%

91% 82% 86%

0% 3% 2% 4% 3% 7% 4% 11% 12%

1% 0% 0% 1%

CSD Tea Water Baby Food Cereal Coffee Cookies Snacks Bath Tissues

Diapers Paper Towels

Laundry Det.

HH Cleaner

Claim + MarkeVng Claim Only MarkeVng Only None

Consumables Non-‐Consumables

42% OF GLOBAL CONSUMERS WANT

MORE NEW PRODUCTS IN THE MARKET THAT ARE SOCIALLY

RESPONSIBLE AND

ENVIRONMENTALLY FRIENDLY

Source: Global New Product InnovaVon, Nielsen Report 2015

Copyrig

ht ©

2014 The

Nielse

n Co

mpany. Con

fiden

Val and

proprietary.

20

OPPORTUNITY TO MEET CONSUMER DEMAND FOR SUSTAINABLE PRODUCTS

Source: Global New Product InnovaVon, Nielsen Report 2015

Copyrig

ht ©

2014 The

Nielse

n Co

mpany. Con

fiden

Val and

proprietary.

21

COMPANIES ARE RESPONDING Globally, Number of Concepts with Sustainable Claims Tested is Growing; 7% of all concepts tested have sustainable posiVoning (up 3% points)

ORGANIC ENVIRONMENTALLY FRIENDLY

ALL NATURAL

% of concepts including the message/sustainable posiVoning

0.7% 0.8% 2.3% 4.8% 1.3% 0.5%

Source: BASES Line Extension DATABASE Past 10 years (2003-‐2008 vs. 2009-‐2013) All Categories and Countries

YOUR BUSINESS – AND REPUTATION – DEPEND ON IT

Copyrig

ht ©

2014 The

Nielse

n Co

mpany. Con

fiden

Val and

proprietary.

23

68%

53%

81% 79%

61%

49%

57% 62%

74%

44%

79% 73%

53% 56% 60%

47%

RUS AUS US

AMERICAS

CAN MEX BRA GER UK FRA ITA ME IND CHI KOR SNG JPN

EUROPE & MIDDLE EAST ASIA

2015 Global ReputaVon Study -‐ Opinion Elites Personally Done in the Past Year

PEOPLE PROACTIVELY TRY TO LEARN MORE ABOUT THE COMPANIES THEY HEAR ABOUT OR DO BUSINESS WITH

Copyrig

ht ©

2014 The

Nielse

n Co

mpany. Con

fiden

Val and

proprietary.

24

45% 31% 32% 40% 40% 19% 19% 29% 28% 27% 34%

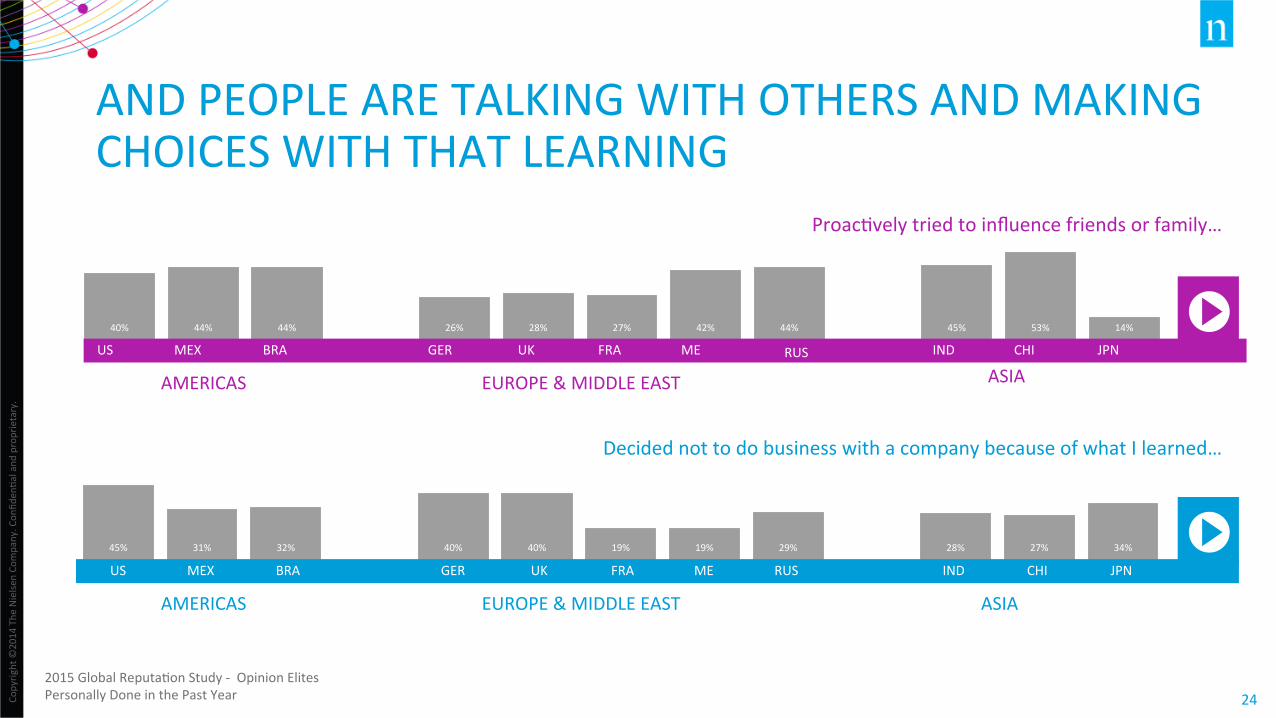

AND PEOPLE ARE TALKING WITH OTHERS AND MAKING CHOICES WITH THAT LEARNING

40% 44% 44% 26% 28% 27% 42% 44% 45% 53% 14%

AMERICAS EUROPE & MIDDLE EAST ASIA

FIN SVC

IND US MEX BRA GER UK FRA ME CHI JPN

ProacVvely tried to influence friends or family…

Decided not to do business with a company because of what I learned…

AMERICAS EUROPE & MIDDLE EAST ASIA

RUS US MEX BRA GER UK FRA ME IND CHI JPN

2015 Global ReputaVon Study -‐ Opinion Elites Personally Done in the Past Year

RUS

Copyrig

ht ©

2014 The

Nielse

n Co

mpany. Con

fiden

Val and

proprietary.

25

SOCIAL RESPONSIBILITY IS ONE OF THE TOP MOST INFLUENTIAL FACTORS FOR REPUTATION

emoVonal appeal

Financial Performance

Vision & Leadership

Workplace Environment

High Product Quality

social responsibility

Source: Harris Poll ReputaVon QuoVent U.S. Study, 2015

Copyrig

ht ©

2014 The

Nielse

n Co

mpany. Con

fiden

Val and

proprietary.

26

EFFECTIVE SUSTAINABILITY = IMPROVED REPUTATION = POSITIVE BUSINESS OUTCOMES

Source: Harris Poll ReputaVon QuoVent U.S. Study, 2015

Would say something posiVve

Would purchase

Would invest in

COMPANIES WITH EXCELLENT REPUTATION

COMPANIES WITH POOR REPUTATION

95%

92%

75%

50%

55%

36%

SUMMARY AND IMPLICATIONS

Copyrig

ht ©

2014 The

Nielse

n Co

mpany. Con

fiden

Val and

proprietary.

28 Copyrig

ht ©

2014 The

Nielse

n Co

mpany. Con

fiden

Val and

proprietary.

• Consumers more than care, it’s an expectaVon

• Rising in utmost importance; Millennials and Gen Z leading the way

• New, innovaVve products to meet consumer demand

• Sustainable brands outperform their counterparts and drive business growth

• Social responsibility greatly influences corporate reputaVon

• Align your brand promise to the causes consumers care most about

THANK YOU