the corporate responsibility report* - pwc · cal supply chain management; provide a retail case...

TRANSCRIPT

Dear Colleagues,

Sustainable development in the retail indus-try is a business imperative for a number of reasons—to manage risks in a global supply chain, to raise

compliance standards, but of increas-ing significance, to supply well-infor-med, socially conscious consumers who demand brands from social and eco-friendly companies with values that reflect their own.

In the United States, a recent Fleish-man-Hilliard survey of attitudes towards corporate responsibility shows that 65% of respondents buy products and services from companies with values and principles that mirror their own. Furthermore, one need not look far to see the fast developing trend of ‘ethical consumerism.’ According to the Financial Times, from 2003 to 2005 the UK witnessed a 30% increase in sales of organic cotton, fair-trade clothes and garments made of recycled content. As of 2004, UK’s fair-trade market was valued at £240 million, while spending on green goods and services totalled $7 billion in the United States.

Given consumer and stakeholder demand, these exciting new business opportunities for the retail industry are proliferating and the industry is well

positioned to respond. In this issue of the Corporate Responsibility Report, we feature an interview with global retailer, Armor Développement, who is address-ing the challenge of fair trade business practices. In addition, we report on ethi-cal supply chain management; provide a retail case study; include an update on PwC’s involvement in the World Busi-ness Council for Sustainable Devel-opment; and we interview Lars-Olle Larsson, author of PwC Sustainability’s new publication: Corporate Governance and Sustainable Business Development.

Thank you for your continued input into this newsletter. Internally, this publica-tion is received by PwC partners and staff worldwide; externally its circula-tion reaches clients, governments, businesses, NGOs and academia, totalling in the several thousands.

We sincerely value your thoughts about our publication and encour-age you to submit feedback through the Rate our newsletter section of this issue. If you would like further information on our practice or would like to learn more about our network, please see our new global website at www.pwc.com/sustainability.

Regards,

Sunny Misser Global Sustainability Leader

Welcome message from PwC Global Sustainability Leader: Sunny Misser

The corporate responsibility report*Volume 5 | June 2006

Contents

Industry focus: retail and consumer goods 2

PwC leading the way in CSR and fair trade practices: client interview 5

Information disclosure at Seiyu: case study 8

Perspectives: the Canadian Sustainability practice 10

PwC at the World Business Council for Sustainable Development 12

Corporate governance and sustainable development: an interview with Lars-Olle Larsson 17

Calendar of sustainability events 20

Useful links 20

2 The Corporate responsibility report, June 2006 | PricewaterhouseCoopers

Industry focus: retail and consumer goodsRose-Marie Brandwein, PwC-USTeresa Fabian, SBS UKSylvain Lambert, SBS France

Corporate Social Responsibility (CSR) and the role of ethical supply chain managementIn the last decade, few industries have undergone more scrutiny than retailers and food companies. Europe witnessed a great deal of public unrest about food safety. Consumer skepticism about genetically modified organisms (GMOs) was so fervent that major supermarket chains across Europe pledged to eradicate them from their own-brand produce, followed by consumer products companies like Unilever and Nestlé, who have taken similar stances.

Campaigns have targeted a wide range of issues such as:• Animal rights—in the beauty, pharmaceutical and food sectors;• Labour standards and working conditions—across a wide range

of consumer products;• Fair prices paid to producers—particularly in relation to agricultural

sector including coffee; • Air miles of products and the impact on carbon emissions and climate change;• Impact on biodiversity, particularly of large-scale agricultural processes in

places where delicate eco-systems exist;• Water usage and water pollution—particularly where this impacts

local communities;• Food safety, including GMOs; and• Use of pesticides and other hazardous chemicals leading to rising

demands for organically produced foods.

However, all those examples only show social, ethical and environmental issues from their negative side—putting brands at risk, undermining shareholder value and hindering the development of new future markets. Nonetheless, is the retailing and consumer-goods industry prepared to move on to a more positive business paradigm? Do they seize the opportunities?

The answer: yes. Some companies are beginning to seize these opportunities. All these negative events have fueled the demand for more socially and ecologically friendly products. For example, organic food sales in certain European countries are soaring—in the United Kingdom, for instance, at an annual rate of more than 40%. Fair-trade Labelling Organisations International estimates that between 2003 and 2004, Fairtrade-labelled sales grew globally by 56% to over 125,000 tonnes and sales have consistently grown year after year, since 1997.

The early sustainability pioneers, who innovated in the eighties and believed in the rise of the ethical consumer, can now harness the “organic” fruit of their work. And more is yet to come. However, with progress comes challenge and one challenge is embodied in ethical supply chain management.

Mother and daughter picking tea in Yunnan Province, China

“The early sustainability pioneers, who innovated in the eighties and believed in the rise of the ethical consumer, can now harness the ‘organic’ fruit of their work.”

3 The Corporate responsibility report, June 2006 | PricewaterhouseCoopers

Moving forward with ethical supply chain management Modern supply chains are increasingly expanding into developing countries where production costs are cheaper, levels of compliance with local labour and environmental laws may be lower and where standards of performance may not be in accordance with international best practices.

This can leave buyers with unprecedented levels of corporate social, ethical and environmental risk in their supply chains which they must take steps to manage. How many large companies can say that they fully understand the environmental and social practices of their upstream suppliers tier one and beyond? Companies and their brands can be damaged easily through “high profile exposés” on corporate responsibility issues.

What should companies do? Key steps in an effective supply chain risk management programme are included in the table on the left.

Specifically, companies should consider the following:• Integration of ethical sourcing considerations within the context of broader

supply chain issues such as brand impact, quality and product safety;• Integration of ethical supply chain management objectives within wider

business objectives and planning (i.e., integration within buyers’ performance metrics and targets);

• Training of global procurement teams and local buying agents to be conversant in ethical sourcing issues; and

• Ethical standards should be translated into local information and reinforced through planned communication, as part of the company’s supplier development programme.

Industry initiativesIncreasingly, companies are coordinating their efforts to tackle ethical sourcing issues at an industry level in order to protect and enhance the reputation of a product in which they have collective interests. Examples in the food sector include the Marine Stewardship Council (MSC), the Roundtable for Sustainable Palm Oil (RSPO), the Ethical Tea Partnership (ETP), and the Common Code for the Coffee Community (4C), to name but a few. This approach has the key benefits of an inclusive approach, a wide pool of available resources to draw on and, critically, avoidance of duplication of effort.

MSC: The MSC is an independent, global, non-profit organisation which was set up to find a solution to the problem of overfishing, and was first established by Unilever and WWF in 1997. In 1999, MSC became fully independent and today is funded by a wide range of organisations including charitable foundations and corporate organisations around the world. MSC has developed an environmental standard for sustainable fisheries, following worldwide consultation with stakeholders including scientists, fisheries experts and environmental organisations. MSC uses independent accredited auditors to certify sustainable fish products which can carry a distinctive blue product label.

RSPO: Driven by ever increasing global demand for edible oils, the past few decades have seen rapid expansion in the production of palm oil in the tropics. From the 1990s to the present time, the area under palm oil cultivation increased by about 43%, mostly in Malaysia and Indonesia. Development of new plantations has resulted in the conversion of large areas of forests with high conservation value and has threatened the viability of ecosystems. Use of fire for preparation of land for palm oil planting has been reported to contribute to forest fires in

Establish internal leadership and commitment

Map supply chain and assess product and country risk

Develop a strong supplier code aligned to internal policies

Develop a risk-based implementation strategy

Commence supplier compliance and monitoring

Develop mechanisms to support ongoing supplier recertification and long-term capacity building

• Performance measurement

• Continuous improvement mechanisms

• Strong internal and supplier reporting and communications

Key steps of effective supply chain risk management

4 The Corporate responsibility report, June 2006 | PricewaterhouseCoopers

the late 1990s. To ensure proper conservation and eco-system viability, RSPO was established to develop a globally acceptable definition of sustainable palm oil production and use as well as to implement better management practices that comply with this definition. Retailer members include: Unilever, Cadbury Schweppes, Coop, CSM NV and Asda, with Waitrose and Northern Foods currently applying.

ETP: This industry partnership sources tea from over 1,200 tea estates globally, accounting for over 70% of the UK’s annual tea import. Its members have undertaken a shared responsibility to work with overseas tea growers and manufacturers (producers) to develop a clear factual understanding of the current situation and to improve social conditions on tea estates. PwC was engaged to provide credible, independent monitoring of current standards against local labour law and collective bargaining agreements for approximately 300 tea producers annually. This service forms the long-term basis for encouraging continuous improvements in social conditions.

4C: The 4C is a joint initiative of coffee producers, trade and industry, trade unions and social as well as environmental NGOs to develop a global code of conduct aimed at overall sustainability in the production, post-harvest processing and trading of mainstream green coffee. The 4C is supported and facilitated by European Coffee Federation 4C Group, Staatssekretariat für Wirtschaf (SECO) and Deutsche Gesellschaft für Technische Zusammerarbeit (GTZ) Gmbh.

Benefits• Companies develop a clear understanding of their supply chain—and the risks

it represents. This helps them take steps in managing risk and protecting their reputation.

• The integration of responsible supply chain management within a wider op-erational framework also helps improve supply chain management processes, while streamlining the agenda and reducing inefficiencies and silo effects.

• Companies develop a robust and credible action plan. If challenged, or if problems do occur, they can demonstrate that they are collaborating with suppliers and taking proactive steps to improve social, ethical and environmental performance in their supply chain.

Ethical supply chain management presents a way forward for responsible food manufacturers and retailers. Major players must set high standards in their promotion of ethical sourcing and supply practices; align internal structures and processes to achieve integrated risk management; and, where applicable, work with both peers and business partners within the supply chain to achieve the best results. When shareholders and others come asking crucial questions about your approach to CSR, let ethical supply chain management demonstrate your commitment.

5 The Corporate responsibility report, June 2006 | PricewaterhouseCoopers

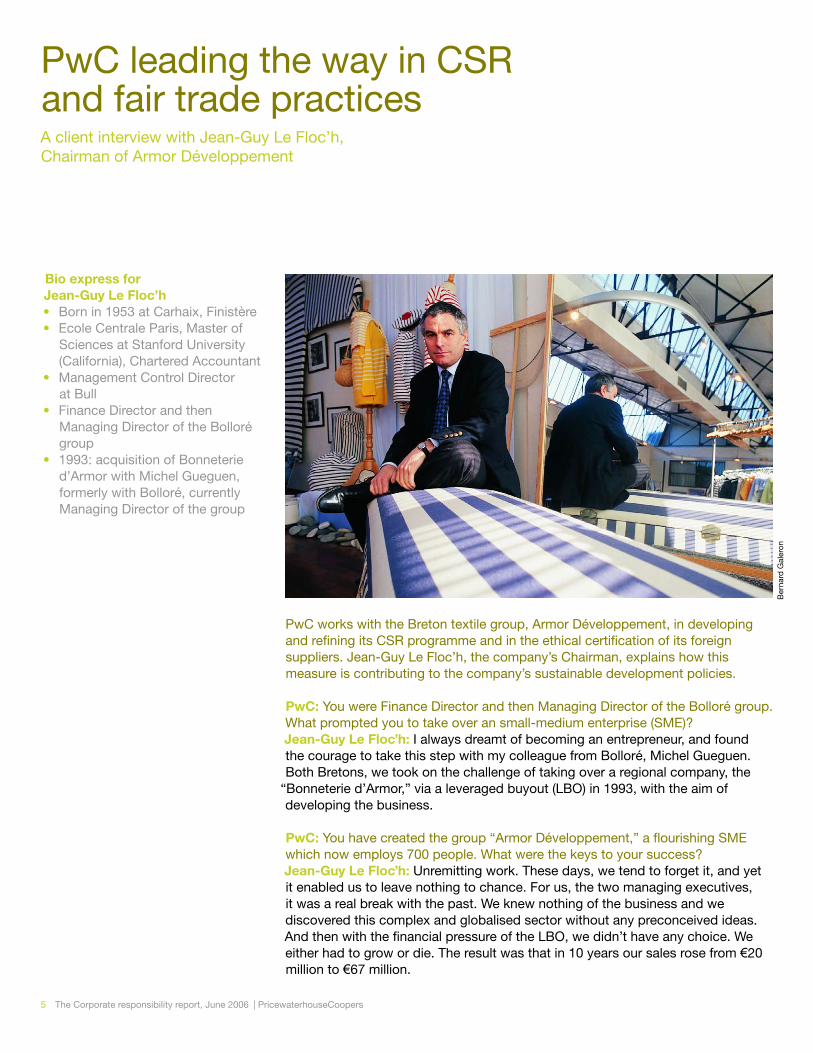

PwC leading the way in CSR and fair trade practicesA client interview with Jean-Guy Le Floc’h, Chairman of Armor Développement

PwC works with the Breton textile group, Armor Développement, in developing and refining its CSR programme and in the ethical certification of its foreign suppliers. Jean-Guy Le Floc’h, the company’s Chairman, explains how this measure is contributing to the company’s sustainable development policies.

PwC: You were Finance Director and then Managing Director of the Bolloré group. What prompted you to take over an small-medium enterprise (SME)? Jean-Guy Le Floc’h: I always dreamt of becoming an entrepreneur, and found the courage to take this step with my colleague from Bolloré, Michel Gueguen. Both Bretons, we took on the challenge of taking over a regional company, the

“Bonneterie d’Armor,” via a leveraged buyout (LBO) in 1993, with the aim of developing the business.

PwC: You have created the group “Armor Développement,” a flourishing SME which now employs 700 people. What were the keys to your success?Jean-Guy Le Floc’h: Unremitting work. These days, we tend to forget it, and yet it enabled us to leave nothing to chance. For us, the two managing executives, it was a real break with the past. We knew nothing of the business and we discovered this complex and globalised sector without any preconceived ideas. And then with the financial pressure of the LBO, we didn’t have any choice. We either had to grow or die. The result was that in 10 years our sales rose from €20 million to €67 million.

Bio express for Jean-Guy Le Floc’h• Born in 1953 at Carhaix, Finistère• Ecole Centrale Paris, Master of

Sciences at Stanford University (California), Chartered Accountant

• Management Control Director at Bull

• Finance Director and then Managing Director of the Bolloré group

• 1993: acquisition of Bonneterie d’Armor with Michel Gueguen, formerly with Bolloré, currently Managing Director of the group

Ber

nard

Gal

eron

6 The Corporate responsibility report, June 2006 | PricewaterhouseCoopers

“If one takes the example of a cotton polo shirt costing €12 in France, €7 in a North African country, €6 in Eastern Europe and €3.50 in China, one can appreciate the difficulty of finding a delicate balance between quality and cost.”

We focused on developing and diversifying our brands; a difficult challenge at the beginning given that the basic brand, Armor Lux, had a rather dowdy image. To inject new life into it, we drew on the magic of creators. We didn’t hesitate on several occasions, ending or eliminating collections that didn’t seem attractive enough or too “flashy.” It was a delicate alchemy. Then, at the same time we were creating and acquiring other complementary “generalist” brands, we developed a broad range of professional clothing for companies and administrations.

PwC: You set yourself the objective of contributing to the economic dynamism of Brittany by producing 40% of your output in France. Is it possible to be profitable under such circumstances given foreign competition is particularly ferocious in this sector?Jean-Guy Le Floc’h: Yes, provided a reasonable mix can be found between French and foreign production, with a focus on product quality and strict manufacturing standards—key criteria for consumers.

However, it is certainly the case that the challenge is unending. If one takes the example of a cotton polo shirt costing €12 in France, €7 in a North African country, €6 in Eastern Europe and €3.50 in China, one can appreciate the difficulty of finding a delicate balance between quality and cost. And in this regard, as an SME, we come up against the problem of product traceability. Although it’s possible to control the manufacturing quality of our products abroad in regions that are close, such as North Africa and Eastern Europe, it is far more difficult in distant countries such as China.

PwC: In January 2005, you became among the first companies in the textile sector to hold a Max Havelaar license enabling you to commercialise a range of articles labelled fair trade cotton. Do you think there is a market for this type of product in France?Jean-Guy Le Floc’h: If we seized this opportunity as soon as the licence was created, it wasn’t out of pure philanthropy. It was because we were convinced that this type of consumption was going to grow very fast and would generate substantial sales. For the time being, the facts have proven us right: in 2005, we generated €500,000 of sales with these products and in 2006, we exceeded €1,000,000.

PwC: In May 2004, you won a contract with the French Post Office in which you were entrusted with managing clothing for its 130,000 employees. What were the criteria that enabled your group to be selected in this European bid?Jean-Guy Le Floc’h: First, our technical expertise in a wide range of clothing at competitive prices is widely recognised. Also, thanks to our know-how in logistics, we convinced the Post Office that we were capable of setting up a

An Armor Lux store

Ber

nard

Gal

eron

7 The Corporate responsibility report, June 2006 | PricewaterhouseCoopers

sufficiently sophisticated system to manufacture and deliver 130,000 units in a very short time frame. Lastly, we were selected on the criteria of our attention to CSR and sustainable development, not only through the measures we have taken to preserve jobs in France but also through our commitment to controlling the production of our foreign suppliers from an ethical standpoint.

PwC: How has PwC been helping you with this contract?Jean-Guy Le Floc’h: We have signed a partnership agreement under which PwC audits the factories of our foreign producers. These reports have shown us the extent to which these audits are absolutely necessary in enabling us to take corrective action and remedy deficiencies in the social domain. It isn’t unusual for us to ask for further investigations and controls. Indeed, we intend to intensify our efforts in this area and reinforce this collaboration, which has proven so effective.

If we decide, for example, to manufacture certain products in China, we have to have the ability to check the production process. This is a key area of concern today because the market is increasingly focusing on this low-cost country, but one which remains difficult to control. You have given us a list of fair trade companies under US standards, and this should help us to identify good suppliers, but we won’t be stopping there.

PwC: Why did you choose PwC to help you?Jean-Guy Le Floc’h: Thierry Raes, SBS Leader for France, and I had a common friend. We signed a contract very quickly, and PwC had a lot of references. I also knew of PwC’s reputation as a classic consultant and auditor.

PwC: How do you see your group in 10 years? What are your growth objectives?Jean-Guy Le Floc’h: We currently see four areas of growth. Development of clothing services for large organisations such as our contract with the Post Office; an enlargement of our distribution network with the creation of new boutiques; sales from direct sales outlets and mail order (Galeries Lafayette, La Redoute…) and the opening of a web site. Lastly, we expect an increase in export sales (mainly North America, Japan and Northern Europe) which currently only represents 12% of total sales. With profitability constraints being what they are, we will not be creating any production jobs in France, but undoubtedly clothing-related service jobs instead. Our objective is to maintain growth of around 10% to 15% per year.

PwC: What more can PwC do to help you achieve your objectives? Jean-Guy Le Floc’h: Not being a high-profile company, Armor Développement doesn’t need a well-known signature such as yours in the audit area. On the other hand, we do need advice on asset management and transactions and we often need good mediators when having to resolve problems on delicate subjects. No doubt these will be avenues worth exploring in widening our collaboration.

A factory worker

Key figures• €50 million in sales at year end 2004

of which 15% were international• 700 staff• Production: 40% in France; the rest

mainly in North Africa and Eastern Europe

• 3 plants in France, at Quimper (Armor-Lux) and Troyes (Guy de Bérac)

• 10 brands: Armor-Lux, Armor Kids, Molène, Classe de Mer, Bérac Homme, Terre et Mer, Bermudes, Tricomer, Lepoutre and Chairman

• 4 million articles sold a year• 3,000 retailers• 30 shops

8 The Corporate responsibility report, June 2006 | PricewaterhouseCoopers

Description of client’s businessSeiyu, Ltd. (Seiyu) was established in 1963 as a supermarket chain and operates 405 stores in Japan (December 31, 2005), including stores operated by its consolidated subsidiaries. In December 2005, Seiyu became a subsidiary of US-based Wal-Mart Stores Inc. (Wal-Mart) after years of affiliation. Seiyu is listed on the FTSE4Good Index Series and the Ethibel Sustainability Index.

For more information on Seiyu, please visit: http://www.seiyu.co.jp/english/corporate_e.shtml

Seiyu’s major activities on environmental and social issuesSince the early 1990s, Seiyu has addressed environmental issues. In order to promote environmental management as a business challenge, Seiyu created the Eco Council as a cross-functional organization to promote the implementation of environmental management. In 1997, Seiyu gained ISO 14001 certification and adopted the Environmental Management System (EMS) as their internal management system. In addition, in 2001 Seiyu established “Green Board,” a forum where external experts and Seiyu executives could exchange opinions. Specific examples of Seiyu’s environmental efforts include the establishment of a recycling route for packaging and containers, specification criteria for its eco-friendly products, and holding environmental workshops at stores for children in various neighbourhoods.

Regarding information disclosure, Seiyu published the “Seiyu Ecobook” in 1992, prior to its environmental reports. The report included its policy, structure, challenges and activities as a retailer as well as environmental information including data on packaging and containers. Seiyu has issued environmental reports every year since 1995 (from 2002, Sustainability Report), outlining not only environmental activities but also store-based social welfare activities. Seiyu has held various dialogues with stakeholders such as environmental workshops and round-table discussions with consumers. Cooperation between stakeholders and Seiyu was also initiated early on. Seiyu has prepared Sustainability Reports cooperating with Japan for Sustainability (JFS), a nongovernmental organization, since 2003. These efforts have been highly praised and recognized externally. Most notably, Seiyu’s reports have received many awards and top rankings in surveys: Nikkei Environmental Management Survey by Nihon Keizai Shimbun Inc., Environmental Communication Awards by the Global Environmental Forum, and the Environmental and Sustainability Report Award by Toyo Keizai Inc.

For more information on Seiyu’s Sustainability Report, please visit: http://www.seiyu.co.jp/english/report_e.shtml

Information disclosure at Seiyu: case studyAyako Shimizu, SBS Japan

9 The Corporate responsibility report, June 2006 | PricewaterhouseCoopers

The client’s challengeIn 2005, Seiyu established the CSR Management System based on EMS with ISO 14001 certification. The in-house directors and heads of 11 functions are responsible for promoting CSR activities and have prepared objectives and targets and run a PDCA (plan-do-check-act) cycle to evaluate and review their implementation. In order to define CSR policy, Seiyu included external advisors in addition to the members on the Green Board. The CSR Management System defines the reporting procedure of sustainability reports, which are published regularly as a tool to disclose information to the public about the system.

The challenge for Seiyu is both to integrate reporting procedure with the CSR Management System and to improve the level of information disclosure. If successful, we hope it will improve management operations and the quality of the Sustainability Report. In order to meet the challenge, it will be necessary to include discussions with stakeholders in the preparation process of reports, establish a reporting procedure, clarify reporting standards and improve data accuracy in reporting.

The PricewaterhouseCoopers approachWe, ChuoAoyama Sustainability Certification Co., Ltd. (CASCert)1 have provided either Independent Assurance Reports or Third Party Evaluation Comments as an independent third party on Seiyu’s Sustainability Reports since 2000.

• Sustainability Report 2000-2002: We provided Independent Assurance Reports and submitted our recommendations on social and environmental issues that needed improvement. The summary of our recommendations which is regarded as most useful for readers appeared as “Our Recommendations” in the Report.

• Sustainability Report 2003-05: We provided Independent Assurance Reports, but the scope of the assurance in the Sustainability Reports was limited to environmental performance since no clear international standards have been established for assurance on sustainability information.

• Sustainability Report 2006: We changed our approach to provide Seiyu with Third-Party Evaluation Comments, in which we focus on the preparation process of the report with reference to GRI Guidelines. We suggested the option in order to expand the scope from Independent Assurance on environmental performance to an evaluation of the whole report as a third party.

Benefits for the clientAchievement in management: In responding to our recommendation as a result of our Independent Assurance work, Seiyu has established a data-collection system and improved its process in order to enhance data accuracy. These improvements also contributed to improving the EMS.

Efforts in information disclosure: Seiyu was the first entity to disclose recommendations from an independent third party in Japan. Seiyu was willing to illustrate the meaning of the Independent Assurance Report in ways that readers found easy to understand. This was based on Seiyu’s stance on the reliability and readability of the reports.

In our Third Party Evaluation Comments this year, we have pointed out challenges described under “The Client’s Challenge.” We hope Seiyu will meet further challenges by improving disclosure of non-financial information to the public and by increasing awareness among readers of these reports.

¹ CASCert: A 100% subsidiary of ChuoAoyama PwC in Japan, www.chuoaoyama-cert.com/eg/index.html

Ayako Shimizu, Senior Researcher, SBS Japan

10 The Corporate responsibility report, June 2006 | PricewaterhouseCoopers

Q: Where is the Canadian Sustainability practice based? PwC Canada’s Sustainable Business Solutions (SBS) practice is primarily based in four cities: Vancouver, Calgary, Edmonton and Toronto.

Q: How long has PwC had a Sustainability practice in Canada? The roots of the practice go back to the early 1990s. It was primarily an environmental practice for the first five years or so before broadening into other areas such as health and safety, and social performance. The practice has evolved significantly as our clients’ needs have evolved and new sustainability issues have risen on the corporate agenda.

Q: What kinds of educational and work backgrounds do the Canadian SBS staff have?The Canadian SBS team is a diverse group including Professional Engineers, Professional Foresters, Professional Biologists, Chartered Accountants, some PhDs and many with Masters degrees. Most have worked for PwC or other professional service firms for much of their careers and several have deep industry experience as well. We find diverse backgrounds a huge asset as we work on challenging and interdisciplinary engagements for clients.

Q: What are the key driving forces for our Sustainability services in Canada?Like most companies in other parts of the world, Canadian companies tend to manage their sustainability issues and disclosures from a variety of perspectives, including risk management, corporate governance and reputation enhancement. From the risk management perspective, most companies want to ensure that they are in compliance with applicable regulations and industry codes of conduct, and that their sustainability performance will not inhibit their ability to achieve other business goals. From a reputation enhancement perspective, companies want to

be seen as “doing the right thing” because this can facilitate access to resources, markets and new clients, as well as improve alignment with employee goals and help to ensure community support for the business.

Q: What are some of the key sustainability services PwC Canada provides?Like many national SBS practices outlined in the recent PwC publication,

Perspectives: the Canadian Sustainability practiceDr. Mel Wilson, SBS Canada

Dr. Mel Wilson, Associate Partner, SBS Canada, speaks at the ForestLeadership Conference in Toronto

“Like most companies in other parts of the world, Canadian companies tend to manage their sustainability issues and disclo-sures from a variety of perspectives, including risk management, corporate governance and reputation enhancement.”

11 The Corporate responsibility report, June 2006 | PricewaterhouseCoopers

Corporate Responsibility, PwC-Canada provides a wide range of services with a different emphasis in each region depending on local market and client needs. Some of our key services include:• We are an accredited Registrar providing environmental, quality and safety

management system certification to programs such as ISO 14001, ISO 9001, OHSAS 18001 and Sustainable Forest Management standards.

• Supply chain assessments, especially regarding wood and paper products. • Sustainability reporting advisory and assurance, including non-financial

assurance to the ISAE 3000 standard.• Climate change advisory and assurance, including emissions inventory

verification, project validation and client training. • Advisory services, including consulting to industry, governments and customers

on natural resources management issues.

Q: What are the main industries the practice works in?We have numerous clients in the mining, retail, telecommunications and transportation industries, with the largest client groups being in the energy (petroleum and electricity) and forest products sectors.

Q: Clients? Public reporting clients include:• Management system assessments: Shell Chemicals, BP Canada,

ConocoPhillips Canada, TransAlta, Teck Cominco, Government of British Columbia

• Sustainability reporting: Shell Canada, Nexen Energy, Talisman Energy, Office Depot, TELUS, Canadian Association of Petroleum Producers

• Supply chain of custody and/or sustainable forestry certification: Catalyst Paper, Abitibi-Consolidated, Pope & Talbot, Boise, Georgia Pacific, Plum Creek

Q: Do Canadian SBS staff get involved in international projects?Yes, regularly. Many of our Canadian-based clients have international operations which require field visits. Some of our clients are also based outside of Canada; however, due to location or specialized service requirements, PwC Canada provides staff to complement local project teams. Over the years, Canadian SBS staff have worked on engagements across the United States, Russia, Mexico, Brazil, the UK, the Middle East and Africa.

Q: Whom can we contact for more information about the Canadian SBS practice?Bruce McIntyre (Vancouver office) is the Partner responsible for the SBS practice in Canada. You can reach Bruce at (604) 806-7595, or at [email protected].

12 The Corporate responsibility report, June 2006 | PricewaterhouseCoopers

After the successful publication of Beyond Reporting at the World Expo in Nagoya, Japan last June, the Accountability and Reporting Working Group Co-Chairs—PwC CEO Sam DiPiazza and Alcan CEO Travis Engen—were asked to co-lead one of the three new WBCSD focus areas—Business’ Role in Society.

The boundaries that define the roles of business, governments and NGOs are shifting and must be redefined continually to serve changing needs and times. As this landscape transforms, what are the roles of business as well as the respective roles and responsibilities of the other players?

Increasingly, society looks to business for solutions to global challenges. It is a new playing field. NGOs have society’s trust but no money; trust in and money from government have declined; and finally business has money; however, society’s trust in business has declined in recent years.

To begin scoping this project, Sam DiPiazza and Bjorn Stigson hosted a lunch discussion at the World Economic Forum’s Annual Meeting in Davos in January. Chief Executives representing over a dozen multinational companies headquartered in eight different countries on four continents provided many differing and valuable perspectives. Business leaders around the world are thinking and concerned about this topic. However, it is not clear yet how they will address it. The dialogue focused primarily on two areas:

Expectations of business• What is the role of business in society today and in the future?• How will it be defined? • What are the societal and stakeholder expectations of business?

Business’ response • How do these expectations affect business today? How will they in the future?• What should CEOs do? What can CEOs do? • How can the gap be bridged?

All agreed that business must define its role in society or else risk someone else defining it. Now is the time to do it because NGOs and governments recognise they need business’ help in developing solutions. This process can help business build much needed trust. Without trust, it is difficult for business to discuss sustainable development and even more difficult to integrate sustainable development into their business.

With shifting boundaries, responsibilities are not as clear as they once were. Many stakeholders don’t understand business. However, they recognise that most busi-nesses could understand their stakeholders better. While the majority of business-

PwC at the World Business Council for Sustainable Development (WBCSD)Tess Mateo, PwC-US

“…business must define its role in society or else risk someone else defining it. Now is the time to do it because NGOs and governments recognise they need business’ help in developing solutions.”

Tess Mateo, Director, PwC-United States

13 The Corporate responsibility report, June 2006 | PricewaterhouseCoopers

es intend to act responsibly, the few bad apples are what people read about in the headlines. Could it be the disconnection with stakeholders that creates conflict and confrontation? If so, it won’t be easy to resolve. Different sectors require dif-ferent answers, since all companies do not have the same stakeholders.

Undoubtedly, this contributes to the increasing gap in people’s understanding of what the role of business in society. For example, what is the business role in developing a future workforce, managing a global talent pool or assisting workers with dislocation? Addressing social issues like corruption, healthcare and education? Dealing with security and its impact on mobility, privacy and labour flow? The group agreed to take the dialogue further within their circles and report back.

A February debate on the role of business was organized in Geneva in connection with a WBCSD Executive Committee meeting. Roughly 250 people, representing key stakeholders from business, civil society and government engaged in a very lively debate led by BBC news anchor Nik Gowing. Overall, the message to business was that companies have a crucial role to play but cannot do everything and cannot replace governments. The need for partnerships and building trust was emphasised.

In March, the WBCSD bi-annual Liaison Delegate Meeting was held in Beijing. It could not have been better timed, following the Chinese Government’s launch of its 11th five-year plan only two weeks earlier. Sustainable development is central to the plan and includes the following targets:• 7.5% annual GDP growth• Energy consumption per unit of GPD down 20%• Water consumption per unit of industrial added value down 30%• Total discharge of major pollutants down 10%• A circular economy with the 3R concept: Reduce, Re-use and Recycle• Strengthened rural development• Improve the nation’s innovation capacity

Achieving these targets requires Chinese industry to enhance capacity for resource efficiency. Comments from Wang Jiming, Chairman of the China BCSD and Vice Chairman of Sinopec, and Captain Wei Jiafu from China Ocean

The WBCSD Liaison Delegate Meeting, Beijing, China

“… what is the business role in developing a future workforce, managing a global talent pool, or assisting workers with dislocation? Addressing social issues like corruption, healthcare and education? Dealing with security and its impact on mobility, privacy and labour flow?”

14 The Corporate responsibility report, June 2006 | PricewaterhouseCoopers

Shipping (Group) Company (COSCO) provided insight on how Chinese leaders are approaching sustainable development. Other foreign members with affiliates in China including George David, UTC; Anne Lauvergeon, Areva; and Andrew Brandler of CLP Holdings, who provided additional perspectives.

These scoping sessions highlighted the complex interplay among three strong forces affecting business and society: the legal environment, the market culture and the global forces of integration and fragmentation. These forces will define future scenarios. While the fundamental role of business will be the creation of value for its owners, employees, customers and society as a whole, the boundary lines that define and divide the role of business from those of governments and NGOs will continue to blur and shift. Globalisation, the vigorous dissemination of information technology, the acceptance of apparent knowledge and facts are all drivers that are rapidly changing our world and the way business is conducted. As the debate about the role of business in society intensifies, so will the need for clarity.

Against this backdrop, it is crucial for proactive businesses to participate in and help shape the debate. This will, in turn, enable them to influence conclusions as well as the overall framework of conditions set by society for business.

In addition to Alcan and PricewaterhouseCoopers, the core team of the WBCSD Business in Society Focus Area includes the following: Allianz, DuPont, KPMG, Pakistan State Oil, Podravka, SGS, Sony, Storebrand and Suez. For more information, please contact Tess Mateo in New York at [email protected].

In addition to Sam DiPiazza, other PwC people involved with the WBCSD included the following: Liaison Delegate Geoff Lane (UK); FACT core team, Tess Mateo (US); Young Manager’s Team, Muna Ali (India); and Working Group, Thomas Scheiwiller (Switzerland).

PwC is on the host committee for the next WBCSD Council and Liaison Delegate Meeting, which is scheduled to be held on 24–26 of October in New York.

Pathways for a sustainable futurePricewaterhouseCoopers has participated in the Young Managers Team (YMT) programme of WBCSD for four consecutive years. The YMT’s overall objective is to develop sustainable development ambassadors by engaging and creating a network of young business leaders. Over a one year period, young managers who were nominated by their companies and selected by WBCSD, work on focus areas that enable them to enhance their leadership and professional skills as well as to gain an understanding of sustainability principles and their application. To date, more than 100 ambassadors have emerged worldwide as a result of the YMT programme.

The kick-off meeting for YMT 2006 was held March 25–30, 2006 in Beijing, China. It coincided with the Liaison Delegates Meeting on Focusing East: Business and Sustainable Development in China. YMT 2006 is one of the largest groups ever convened—comprised of 30 organizations and 21 nationalities. This diverse group addressed the common theme of business leadership as a catalyst for change towards sustainable development and to support the business license to operate, innovate and grow. Towards this goal, the YMT 2006 programme will develop pathways for a sustainable future on WBCSD’s three key focus areas: Energy and Climate, Development and Business’ Role.

About World Business Council for Sustainable DevelopmentThe World Business Council for Sustainable Development (WBCSD) brings together some 180 international companies in a shared commitment to sustainable development through economic growth, ecological balance and social progress. Members are drawn from more than 30 countries and 20 major industrial sectors and include a global network of 50+ national and regional business councils and partner organizations. The WBCSD’s mission is to provide business leadership as a catalyst for change toward sustainable development, and to support the business license to operate, innovate and grow in a world increasingly shaped by sustainable development issues.

15 The Corporate responsibility report, June 2006 | PricewaterhouseCoopers

Drawing inspiration from Peter Drucker on creating the future, the young manag-ers have been assigned the exciting task of developing scenarios up to 2050 on each of these three focus areas. These scenarios will be important tools that will allow organizations to expect the unexpected. These scenarios will detail credible, challenging and coherent stories describing plausible futures and outcomes. This year, the focus of the YMT is on the consumer, and each focus area workstream has been assigned its topic for developing a scenario.

The Energy and Climate workstream will focus on changing consumer behaviour by developing a scenario on the role of consumers in reducing our carbon footprint; the Development workstream will analyse how the needs of new consumers can be met sustainably; and the Business Role workstream will look at what will make business trustworthy in 2050. From April to October, each workstream will research the topic, identify relevant drivers and pathways, agree on structure and communicate virtually. In October, the three workstream groups will reassemble in New York for a midpoint meeting. During this meeting, the pathways developed for each workstream will be presented and communications activities will be outlined.

The final meeting of the YMT 2006 is scheduled to be held in Geneva in February 2007. At this time, new information learned will be presented along with plans to integrate key information and the action steps to be taken.

The commitment and enthusiasm of the young managers remain unswerving as they try to map the futures of their respective workstreams. In doing so, they have realized that they may well be mapping their own.

For more information on YMT 2006, please contact Muna Ali in India at [email protected].

Young Managers for the Future 2006 group

“The YMT’s overall objective is to develop sustainable development ambassadors by engaging and creating a network of young business leaders.”

Dr. Muna Ali, Deputy Manager, SBS India

16 The Corporate responsibility report, June 2006 | PricewaterhouseCoopers

Michelin Challenge BibendumAaron Caplan, SBS London and PwC’s first YMT member, was invited along with four other YMT alumni to participate in the Michelin Challenge Bibendum, an event organised by Michelin to explore the future of sustainable mobility. “Michelin’s vision for the Challenge Bibendum is to spotlight the most significant advances in sustainable mobility, to help find new ways forward and to demonstrate responsibility to future generations.”

This year the discussion at the Bibendum focused on three areas: The energy challenge, urban mobility and road safety. Alumni from the YMT were invited to each roundtable discussion in order challenge conventional thinking and to stimulate an exchange of ideas. Aaron participated in the roundtable discussion on energy, where he challenged the participants to define the role of industry, government and the consumer and how the three groups can work together.

During the final session of the Bibendum, YMT alumni highlighted common themes heard throughout the event and shared their perspective as today’s consumers and tomorrow’s business leaders. They concluded:• In addition to technological advancement, there is a need to address

assumptions of increased demand and consumption;• There isn’t a strong sense of urgency as decisions made now not

only shape our future, but also shape this generation’s and the following generation’s ability to respond adequately; and

• This generation is relying on future generations to deal with the dilemmas inherent in creating sustainable levels of consumption.

“Michelin’s vision for the Challenge Bibendum is to spotlight the most significant advances in sustainable mobility, to help find new ways for-ward and to demonstrate responsibility to future generations.”

Aaron Caplan, Manager, SBS London

17 The Corporate responsibility report, June 2006 | PricewaterhouseCoopers

The Corporate Responsibility Report recently interviewed Lars-Olle Larsson whose seventh book, Corporate Governance and Sustainable Business Development was published last autumn. Lars-Olle has been Chairman of the European Federation of Accountants’ Sustainability Assurance Group for many years. He is also a member of the Sustainability Experts Advisory Panel established by IFAC/IAASB and is the Swedish representative serving on the ICC’s Commission on Business in Society.

For his unwavering support of ongoing dialogue with the public, Lars-Olle was the 1991 recipient of the European Public Relations Confederation’s “The European Public Relations Professional of the Year” award. He also received The International Public Relations Association’s “Golden World Awards of Excellence” the same year.

Q: Global Compact, OECD Guidelines, ILO’s declarations, UN Norms, ISO 26000 and now also Principles for Responsible Investment. Where are we heading?This question refers to the management of companies strengthened by enhanced governance regulations and accounting regulations, as well as non-obligatory commitments in the context of responsible business management. There is, of

Corporate governance and sustainable business developmentInterview with Lars-Olle Larsson, Principal Director, PricewaterhouseCoopers

“Lars-Olle Larsson documents the emerging focus within the capital markets on environ-mental, social and governance per-formance.”

Carina Lundberg, Corporate Governance Asset Management, Folksam

18 The Corporate responsibility report, June 2006 | PricewaterhouseCoopers

course, no other institution or body other than the business community itself, that can ensure economic well-being and sustainable development. This is also the reason that increasing demands are placed on companies.

Q: What should companies do?Through the work of the board of directors and management, companies must broaden their view of risks, business possibilities and the assumption of respon-sibility. It is no longer enough to take responsibility vis à vis delineated target groups, such as shareholders, clients and personnel. Interested parties impacting on shareholder value are, in fact, comprised of a much larger number of vary-ing stakeholders, and it can be profitable for a company to take responsibility for environmental effects and human rights in interaction with these stakeholders.

As a result of the Enron, Ahold and the Parmalat scandals, the Sarbanes Oxley Act, national governance codes and changed accounting regulations have been implemented. Today board issues are given high priority, while at the same time, questions regarding a company’s responsibility for working conditions in the supply chains in Third World countries are increasingly discussed in the mass media. These questions are often actively followed up by institutional investors. The reason for this is simple—investors want to minimise these new business risks in their own portfolios.

Q: How important, in real terms, is confidence? Is this just an issue of good media exposure in which the company seeks to establish a positive image?All shareholder value development in a company is based on faith and confidence in the company’s capacity in the markets in which it operates. This confidence is dependent on the information regarding the company, its products, competitive situation and reported results that are accurate, sufficient and timely. In all aspects of a company’s activities, including the establishment of policies and codes of conduct, control of suppliers, dialogues with interested parties, etc., confidence is dependent on the supporting and transparent information and communication. In this context, the reality and the image are one and the same. A company receives positive results from transparency and clarity.

Q: Who should take responsibility for corporate governance and sustainable business development?The ultimate responsibility is always at the highest level of the organisation. Those companies who understand how to establish and correctly communicate the basic values inherent in their business concepts will perform best in the markets. We now have a really good chance to introduce work with basic values by focusing on policies and codes of conduct in establishing corporate governance on the basis of the Sarbanes Oxley Act and on national governance codes. Now, when an increasing number of companies locate their production with suppliers in Third World countries, or move their own production to these new markets, we can count on seeing the environmental conditions and human rights in the supply chains being much more critically studied and questioned.

IKEA found itself under scrutiny a number of years ago, but has subsequently developed into a good example. Having worked with IKEA for a number of years, I can say that confidence comes through the establishment of codes of behaviour, internal controls and external auditing.

Q: What do you mean by connecting Corporate Governance with Corporate Social Responsibility?I developed my reasoning behind this in the book but can note briefly that to achieve Sustainable Business Development, a company must work to ensure

“Interested parties impacting on share value are

… a much larger number of varying stakeholders, and it can be profitable for a company to take responsibility for environmental effects and human rights in interaction with these stakeholders.”

19 The Corporate responsibility report, June 2006 | PricewaterhouseCoopers

that CSR is integrated within its Corporate Governance framework. This implies that the internal control and reporting should include both areas: governance and responsibility. In Principles for Responsible Investment, launched by Kofi Annan in April, there are references to “ESG” issues—environmental, social and corporate governance. This reflects the same approach and implies an all-in view of risks and possibilities.

Q: How does this affect a company’s accounting and reporting?All information provided by a company should mirror the factors, and not only financial factors—that are significant for the users of such information. It is for this reason we now see that Best Practice within accounting integrates sustainability information in annual accounts, including specific disclosure of the various sec-tions referring to CSR reporting regarding Global Reporting Initiatives’ Guide-lines. The disclosure of extra-financial information is now widely demanded. The International Accounting Standards Board has now requested responses regard-ing Management Commentary (MC) via a Discussion Paper. MC should focus on meeting the needs of investors. These comments should not be expanded to fulfil the information needs of an extended range of users. Furthermore, MC should not be seen as a replacement for other forms of reporting addressed to a wider stakeholder group. In the near future we will continue to see a clear differentiation between standards and extra-financial reporting standards, but we will also see innovative narrative reporting (www.corporatereporting.com) and a call for assur-ance on all disclosed information.

Q: What role does the accounting profession have in this development?I have had the pleasure and advantage of actively participating in developments in the area of assurance, an area which now also includes assurance on Sustainability Reports. Ten years ago, I signed the first independent statement in a Review Report included in an Environmental Report, issued by one of the leading global forest industry corporations. Since that time, the European Federation of Accountants has issued a variety of Discussion Papers addressing assurance methodology on sustainability. After our Call for Action Paper (2004), in which we made a series of recommendations applicable to corporations, standard setters, assurance providers, sustainability indexes and NGOs, the IFAC and IAASB are really on the right track. The ISAE 3000 is very helpful but needs to better incorporate specific issues addressed in sustainability assurance. IFAC/IAASB’s Consultation Paper, “Assurance Aspects of GRI G3,” issued this spring is a step in the right direction.

Speaking from a PricewaterhouseCoopers Nordic market approach, we see a clear trend in companies increasingly coming to us (in the accounting profession) for help and support in understanding and implementing these new standards and recommendations. For example, Helle Bank Jørgensen, Director in SBS Denmark, initiated the Nordic Market approach partly in answer to this trend where my colleague, Fredrik Franke, and I, as well as the entire SBS Sweden team are working to support this development. There is a need for convergence in standard setting on sustainability and I am happy not only for the support received from all of the dedicated and competent staff in PricewaterhouseCoopers, but also to be a part of these developments—developments which are directly related to the real needs of our clients and simultaneously in the public interest.

“Every communications and investor relations professional should carefully consider the issues raised in this book.”

Bodil Eriksson, Senior Vice President, SCA

20 The Corporate responsibility report, June 2006 | PricewaterhouseCoopers

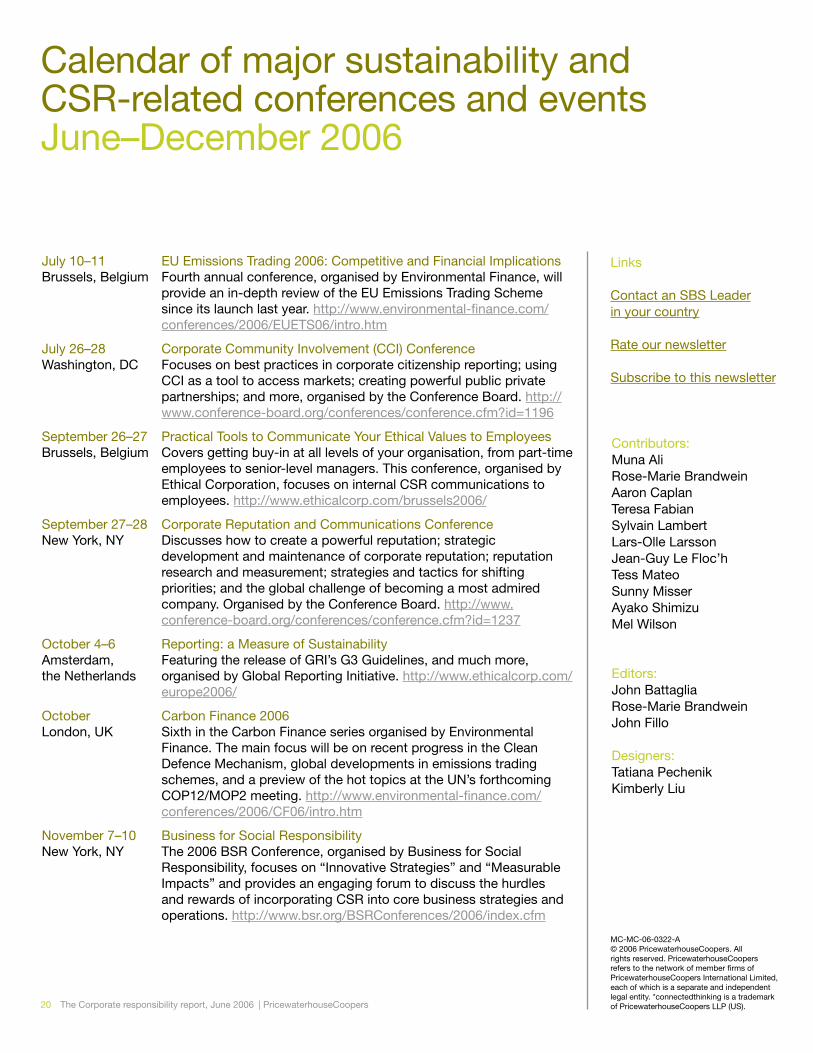

July 10–11 EU Emissions Trading 2006: Competitive and Financial ImplicationsBrussels, Belgium Fourth annual conference, organised by Environmental Finance, will

provide an in-depth review of the EU Emissions Trading Scheme since its launch last year. http://www.environmental-finance.com/conferences/2006/EUETS06/intro.htm

July 26–28 Corporate Community Involvement (CCI) Conference Washington, DC Focuses on best practices in corporate citizenship reporting; using

CCI as a tool to access markets; creating powerful public private partnerships; and more, organised by the Conference Board. http://www.conference-board.org/conferences/conference.cfm?id=1196

September 26–27 Practical Tools to Communicate Your Ethical Values to EmployeesBrussels, Belgium Covers getting buy-in at all levels of your organisation, from part-time

employees to senior-level managers. This conference, organised by Ethical Corporation, focuses on internal CSR communications to employees. http://www.ethicalcorp.com/brussels2006/

September 27–28 Corporate Reputation and Communications ConferenceNew York, NY Discusses how to create a powerful reputation; strategic

development and maintenance of corporate reputation; reputation research and measurement; strategies and tactics for shifting priorities; and the global challenge of becoming a most admired company. Organised by the Conference Board. http://www.conference-board.org/conferences/conference.cfm?id=1237

October 4–6 Reporting: a Measure of SustainabilityAmsterdam, Featuring the release of GRI’s G3 Guidelines, and much more,the Netherlands organised by Global Reporting Initiative. http://www.ethicalcorp.com/

europe2006/

October Carbon Finance 2006London, UK Sixth in the Carbon Finance series organised by Environmental

Finance. The main focus will be on recent progress in the Clean Defence Mechanism, global developments in emissions trading schemes, and a preview of the hot topics at the UN’s forthcoming COP12/MOP2 meeting. http://www.environmental-finance.com/conferences/2006/CF06/intro.htm

November 7–10 Business for Social ResponsibilityNew York, NY The 2006 BSR Conference, organised by Business for Social

Responsibility, focuses on “Innovative Strategies” and “Measurable Impacts” and provides an engaging forum to discuss the hurdles and rewards of incorporating CSR into core business strategies and operations. http://www.bsr.org/BSRConferences/2006/index.cfm

Calendar of major sustainability and CSR-related conferences and eventsJune–December 2006

Links

Contact an SBS Leader in your country

Rate our newsletter

Subscribe to this newsletter

Contributors:Muna AliRose-Marie Brandwein Aaron CaplanTeresa FabianSylvain LambertLars-Olle LarssonJean-Guy Le Floc’hTess MateoSunny MisserAyako ShimizuMel Wilson

Editors:John BattagliaRose-Marie BrandweinJohn Fillo

Designers:Tatiana PechenikKimberly Liu

MC-MC-06-0322-A © 2006 PricewaterhouseCoopers. All rights reserved. PricewaterhouseCoopers refers to the network of member firms of PricewaterhouseCoopers International Limited, each of which is a separate and independent legal entity. *connectedthinking is a trademark of PricewaterhouseCoopers LLP (US).