the compass winter 2016 - tcts. · pdf filethe compass winter 2016 3 seeking wisdom - part 2...

TRANSCRIPT

b e c a u s e w e a l t h m a n a g e m e n t i sm o r e t h a n m a n a g i n g m o n e y

T H E C O M PA S S T H I S I S S U E

Refining Your Investment Risk Exposure 2

Seeking Wisdom 3

W I N T E R 2 0 1 6

NOTABLE QUOTE: “FOCUS ON WHAT YOU CAN CONTROL – COSTS, ASSET ALLOCATION, RISKS, AND DISCIPLINE. IGNORE WHAT YOU CANNOT CONTROL –THE MEDIA, PROGNOSTICATORS, MARKET RETURNS, AND YOUR GUT.” BRAD STEIMAN, DIMENSIONAL FUND ADVISORS

I f you have a revocable trust as part of your estate plan (andyou should), it is essential that you fund it during yourlifetime in order to take advantage of all of its benefits.

Funded revocable trusts can provide for proper managementof your assets in the event of incapacity, prevent publicinspection of your assets and their disposition upon yourdeath, and reduce certain estate administration burdens.

What is a revocable trust? In essence, it is an agreementyou establish that identifies (1) a person or entity to manageassets in the trust (the “trustee”), (2) how those assets are to bemanaged and distributed, and (3) for whose benefit the trustassets are to be held (the “beneficiaries”). During yourlifetime, typically you are the trustee and beneficiary of yourrevocable trust so that you have complete control over and useof the trust assets. You are treated as the owner of the trust fortax purposes, so all items of income are reported to you. Asthe name implies, you can revoke or change the trustagreement at any time prior to your incapacity. Upon yourdeath, the trust becomes irrevocable and its assets pass toindividuals or charities named in the trust agreement ratherthan in accordance with your will.

What are the benefits of a revocable trust? A revocabletrust can be used to manage your assets during your lifetime.You can serve as trustee and perform this function yourself

during your lifetime, but should you become incapacitated orsimply desire someone else to manage the assets for you, asuccessor trustee designated by you takes over. If you becomeincapacitated and your assets are held in your individual namerather than in a revocable trust, unless you have signed adurable power of attorney, a guardian would have to beappointed for you via a costly court proceeding and thereafteryour assets would be managed within the purview of thecourt.

In addition, a revocable trust can help you avoid or reduceprobate. Probate is a legal process pursuant to which theprobate court confirms a personal representative’s authority toaccess a decedent’s property, pay the decedent’s debts andexpenses, and transfer the decedent’s assets pursuant to hiswill, or if there is no will, in accordance with state law. Thisprocess is public record and can cause delays in theadministration of your estate. In addition, probate fees arecharged on the decedent’s probate assets. Assets transferredinto your revocable trust during your lifetime are not subjectto probate. As a result, probate-related expenses on the assetscan be avoided, and the nature and extent of those assets andhow and to whom they will be distributed upon your deathwill not be subject to public inspection.

Funding Your Revocable Trustb y W e s t r a y V e a s e y , J . D .

C o n t i n u e d o n b a c k p a g e

2 THE COMPASS Winter 2016The information contained in the Compass is not intended as investment, legal, or tax advice. Please consult with your professional advisor to determine the appropriateness of anystrategies to your specific circumstance. Copying this publication without permission of Trust Company of the South is prohibited. © Copyright 2016 Trust Company of the South.

b e c a u s e w e a l t h m a n a g e m e n t i s m o r e t h a n m a n a g i n g m o n e y

Refining Your Investment Risk Exposureb y D a n T o l o m a y , C F A

Unfortunately, investment risk is unavoidable. Picture risk asa continuum. At one end of the spectrum is inflation risk(a.k.a. purchasing power risk). This is the danger that you

don’t earn enough return to keep up with rising prices and yourstandard of living goes down. At the other end is market risk.This is what people typically think about when discussing theirinvestment portfolio. Market risk is the volatility of the value ofone’s holdings. The threat is that investments have to be sold at adepressed value. This can be the result of an inability to stomachvolatility or the necessity to sell to meet expenses. The goal -when setting an asset allocation - is to find the point on thecontinuum that allows a portfolio to meet the investor’s goals,and allow him or her to sleep at night.

Once the correct asset allocation has been set, the decisionmust be made on how to deploy the funds. Active managers tryto pick the best stocks at the right times. As a result, they chargemore to research and trade. These higher costs work againstthem, as the majority of active funds consistently fail to besttheir benchmark. For example, according to the 2014 year-endStandard and Poor’s Index Versus Active (SPIVA) study, thepercent of active fund managers in the Large Value category thatunderperformed their index were: 79% for one year, 81% forthree years, 87% for five years, and 59% for ten years. Bydeviating from the benchmark’s holdings, active managers exposea portfolio to manager risk. And, as the numbers above show,this bet is not worth taking as the odds are not in your favor.

The obvious choice to eliminate manager risk is to use anindex fund. Such an approach buys the entire asset class and isalways fully invested. The fund can be managed veryinexpensively as research and trading costs are low. However, by striving to reduce the noise of their returns around thebenchmark, the fund gives up the opportunity to outperform it.Further, the fund is destined to underperform the benchmark by roughly its expense ratio. Take the Vanguard Value Index, for example. The fund charges 0.23%. As of 12/31/15, itunderperformed its index by -0.17% for one year, -0.24% forthree years, -0.23% for five years, and -0.16% for ten years.Tacking on an investment advisor fee leads to a further drag on returns.

There is a third, hybrid option. Dimensional Fund Advisors(DFA) maintains many of the benefits of an index fund: DFAbuys the entire asset class, remains fully invested and the fundcosts are low. Rather than have trades dictated by a third-partycommercial benchmark provider like Standard & Poor’s orRussell, they remain flexible and trade patiently. This can lead toholdings and performance variances with the index. However, tohave a chance to beat the benchmark, you must differ from thebenchmark. DFA diverges by targeting academically-provensources of higher expected return.

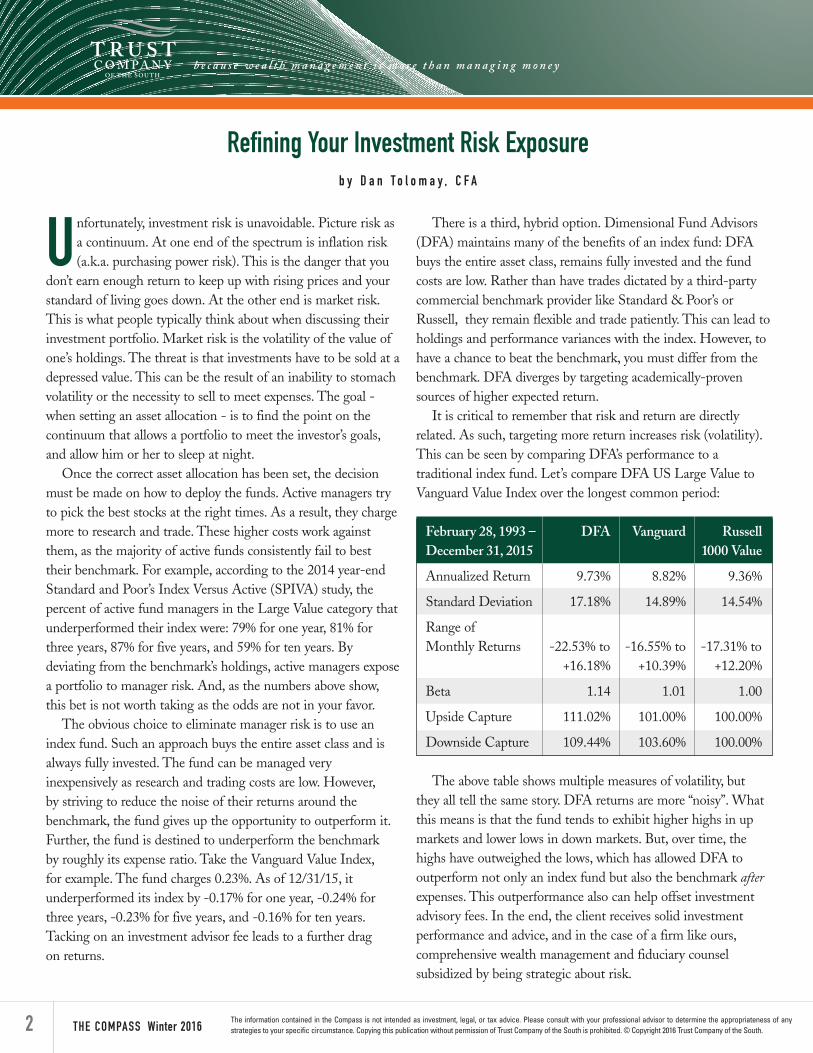

It is critical to remember that risk and return are directlyrelated. As such, targeting more return increases risk (volatility).This can be seen by comparing DFA’s performance to atraditional index fund. Let’s compare DFA US Large Value toVanguard Value Index over the longest common period:

February 28, 1993 – DFA Vanguard RussellDecember 31, 2015 1000 Value

Annualized Return 9.73% 8.82% 9.36%

Standard Deviation 17.18% 14.89% 14.54%

Range of Monthly Returns -22.53% to -16.55% to -17.31% to

+16.18% +10.39% +12.20%

Beta 1.14 1.01 1.00

Upside Capture 111.02% 101.00% 100.00%

Downside Capture 109.44% 103.60% 100.00%

The above table shows multiple measures of volatility, butthey all tell the same story. DFA returns are more “noisy”. Whatthis means is that the fund tends to exhibit higher highs in upmarkets and lower lows in down markets. But, over time, thehighs have outweighed the lows, which has allowed DFA tooutperform not only an index fund but also the benchmark afterexpenses. This outperformance also can help offset investmentadvisory fees. In the end, the client receives solid investmentperformance and advice, and in the case of a firm like ours,comprehensive wealth management and fiduciary counselsubsidized by being strategic about risk.

THE COMPASS Winter 2016 3

Seeking Wisdom - Part 2b y C h r i s S u t h e r l a n d , C P A

The Education of a Value Investorby Guy SpierThe title is a bit misleading as the bookis really a personal memoir. It is moreabout life than investing (although thereare some very good investment tipsincluded!). Guy Spier details his youngcareer on greed-filled Wall Street and hispersonal transformation that includes a$650,000 lunch with Warren Buffet.

Being Mortalby Atul Gawande – This is a must readfor anyone facing the challenges of caringfor elderly or sick family. Dr. Gawande, asurgeon, understands the limits of hisprofession. Medicine has madetremendous strides in the last half-century. Birth, disease and relativelyminor injuries were once much more life-threatening. But these advances havecreated a new problem - dealing with

end-of-life challenges, specificallyweighing quality of life versus extensionof life. Gawande believes medicine iscapable of dealing with this challenge.

Zealot: The Life and Timesof Jesus of Nazarethby Reza AslanMost of us know Jesus through the lensof the Gospels. Aslan takes a step backand attempts to get to know Jesus, theman, by examining the era in which helived. And what a different era it was!Jesus was a man full of conviction, butalso contradiction.

The Conservative Heartby Arthur BrooksIt’s time for the conservative movementto change – change from a movement ofthe head to a movement of the heart.Why does the political divide have to be

about ineffective compassion versusheartless practicality? Brooks offers up anew conservatism, a movement based onunity and social justice that fights povertyand provides equal opportunity for all.

The Road to Characterby David Brooks Brooks challenges us to focus more onour eulogy virtues rather than our resumevirtues. The eulogy virtues are those thatexist at our core…integrity, honesty,kindness, trustworthiness… the traitsthat make you a truly good friend.Brooks uses his great storytelling abilityto look back at some the world’s mostremarkable leaders and thinkers.

The Case for Godby Karen ArmstrongStarting out in the Paleolithic era andmoving to present day, Armstrong details

Another year and a few more books consumed. I’d like to think I’m growing wiser, but wisdom is very subjective. With all myreading over the past several years, I have learned to keep an open mind and not take every word as truth. All human beingsare biased. It’s in our nature and not necessarily bad. We should all keep that in mind as we read anything non-fiction.

For me, reading has been a thought stimulator and it has helped that I’m part of a couple of different book groups. More sothan the reading, the group discussion and relationships have provided valuable personal growth. Below are some of my favoritebooks from last year.

C o n t i n u e d o n b a c k p a g e

44 THE COMPASS Winter 2016 T R U S T C O M P A N Y O F T H E S O U T H 800.800.9440 www.tcts.com

GREENSBORO OFFICEWilliam H. Smith, CFP

®

CEO, President

Mitchell H. Paul, CPA

Principal

Matthew E. Hornaday, CPA

Wealth Advisor

RALEIGH OFFICEWilliam H. Noble

Principal

Jonathan S. Henry, CPA, CFP®

Director of Financial Planning

Westray B. Veasey, J.D.

Fiduciary Counsel

CHARLOTTE OFFICEJay D. Eich, CFP

®, CPA

Principal

Christopher N. Sutherland, CPA

Principal

F u n d i n g Yo u r R e v o c a b l e Tr u s t C o n t i n u e d f r o m p a g e 1

How do you “fund” your revocable trust? “Funding” meanstransferring title into the name of your revocable trust. Youshould review your assets with your advisors to determine theappropriateness of moving each asset to your revocable trustand how that can be accomplished. For your investmentaccounts, your investment advisor can provide a form to retitlethe accounts into the name of your revocable trust. Real estatecan be transferred into your revocable trust by deed. If there isa mortgage on the property, you should make sure any suchtransfer does not violate your mortgage terms. If you own realestate in a state other than your domiciliary state, unless youtransfer that property into your revocable trust, your heirs willhave to go through ancillary probate administration in thatother state in order to transfer title to that property at yourdeath. If the property is owned by your revocable trust at yourdeath, the trustee can simply deed the property to the heirs.Business interests can be transferred into your revocable trustby assignment or reissuance of stock certificates, but careshould be taken to review with your advisors any agreement

governing the business that may limit your ability to transfersuch assets. Certain assets, such as IRAs, retirement planaccounts and life insurance, can be made payable to yourrevocable trust upon your death by beneficiary designation.While these assets are generally not subject to probate anywayunless made payable to your estate, making them payable toyour revocable trust may be appropriate so that theirdisposition is consistent with your overall estate plan. Becausequalified retirement accounts are subject to complex incometax rules, make sure to consult with your advisors beforemaking such accounts payable to your revocable trust.

Funding a revocable trust during your lifetime will not saveyou income or estate taxes and will not protect the trust assetsfrom your creditors. A revocable trust can offer privacy, ensurecontinued management of your assets upon incapacity andreduce expense and potential delays in the administration ofyour estate after your death. In order to take advantage ofthese benefits, however, it is essential you fund your revocabletrust during your lifetime.

S e e k i n g W i s d o m C o n t i n u e d f r o m p a g e 3

the history of religion and thetranscendence of God. She advises thatreligion was never meant to solvehuman problems; rather it is “to help uslive creatively, peacefully and evenjoyously with realities for which thereare no easy explanations.”

Economics in One Lessonby Henry HazlittWritten in 1946, Hazlitt’s mostinfluential work has sold over a millioncopies. Economists on both sides ofthe political spectrum have creditedHazlitt with foreseeing the most recentglobal collapse. He focuses on non-government solutions that key on freemarkets and liberty.

My reading list is always expandingand changing. If you read anythingnoteworthy, please let me know,[email protected]. Also, if you areinterested in my list from 2014, pleasesee the 2015 Winter Compass containedon the Resources page of our website,www.tcts.com.