the challenge of meeting freight infrastructure demands: public-private partnerships the answer? jim...

TRANSCRIPT

The Challenge of MeetingFreight Infrastructure Demands: Public-Private Partnerships the Answer?

Jim Hixon

Exec. Vice President Law & Corporate Relations

Norfolk Southern Corporation

June 2007

Overview

I. Freight Capacity Constraints and the Need for New Rail Infrastructure

II. Rail Infrastructure Economics – An Overview

III. Two PPP Models

IV. Public Benefits of Rail

Summary

Freight demand growing rapidly; more rail infrastructure needed

Both public and private investment will be required to meet future rail infrastructure needs

Federal incentives would increase private investment in rail infrastructure

More rail infrastructure would produce substantial public benefits

Major Freight Growth Projected(Domestic Tons All Modes)

90%

100%

110%

120%

130%

140%

150%

160%

2005 2010 2015 2020 2025

ATA DOT

AASHTO*

All figures indexed with each source’s 2005 traffic levels equal to 100 percent*AASHTO: American Association of State Highway and Transportation Officials

Highway Capacity Already Strained

50%

75%

100%

125%

150%

175%

200%

225%

250%

1980 1984 1988 1992 1996 2000 2004

Interstate traffic has grown

much faster than lane miles

Source: Dept. of Transportation, National Transportation Statistics

VMT perLane Mile

Vehicle MilesTraveled (VMT)

Lane Miles

More Highway Gridlock Coming

Source: Dept. of Transportation, FHWA Freight Analysis Framework

Truck Traffic

1998 2020

Rail Capacity Already Strained

0%

50%

100%

150%

200%

250%

300%

350%

1980 1984 1988 1992 1996 2000 2004

Class I Rail ton-miles have

increased dramatically without

growth in track miles

Source: Dept. of Transportation, National Transportation Statistics

Ton Miles perMile of Track

Ton Miles

Track Miles

Variety of Forces Pushing More Freight to Railroads

$1.00

$1.50

$2.00

$2.50

$3.00

Jan-

99Ja

n-00

Jan-

01Ja

n-02

Jan-

03Ja

n-04

Jan-

05Ja

n-06

Jan-

07

U.S. DieselPrices

$9

$10

$11

$12

$13

$14

2000

q220

01q2

2002

q220

03q2

2004

q220

05q2

2006

q220

07q1

Tri

llio

ns

of

Do

llar

s

U.S. GDP

Source: Census Bureau, STBAll figures based on 2002 economic census except railroads and truckingAll transportation includes NAICS 48 industries including: air, rail, trucking, water and pipeline transportationTrucking figures are 1999-2005 average for NAICS 484 based on Census Services Annual SurveyRailroad figures are 1999-2005 average based on STB R-1 filings (Class I railroads cash capital)

Capital Investment as a % of Revenue

Railroads Are Highly Capital Intensive

4.3%

4.2%

12.0%

6.2%

16.2%

0% 5% 10% 15% 20%

All Sectors

Manufacturing

All Transportation

Trucking

Railroads

Source: AAR

0

50

100

150

200

250

300

1964 1969 1973 1977 1981 1985 1989 1993 1997 2001 2005

Revenue

Volume

Productivity

Price

Staggers Act Passed Oct. 1980

U.S. Freight Railroad Performance Since Staggers

Index 1981=100

Freight Rail Investment Challenge

AASHTO (American Association of State Highway and

Transportation Officials)

issued a study in 2003 analyzing the state of freight rail capacity

concluded that freight railroad investment must grow sharply over next 20 years to maintain railroads’ share of growing freight traffic

also found that freight railroads may not be able to attract necessary investment to handle their share of growing freight demand

AASHTO Investment Goal

0

5

10

15

20

25

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Bill

ion

s o

f D

olla

rs

Maintain same share of freight

Meet AASHTO goal to increase share of freight carried by rail

AASHTO projected investment;reduced rail share of freight

Based on averages of AASHTO estimates adjusted for inflation

Investment needed to…

Support for AASHTO Findings

Subsequently, similar concerns about the ability of the industry to attract necessary capital have been expressed by:

CBO

Transportation Research Board

Hudson Institute

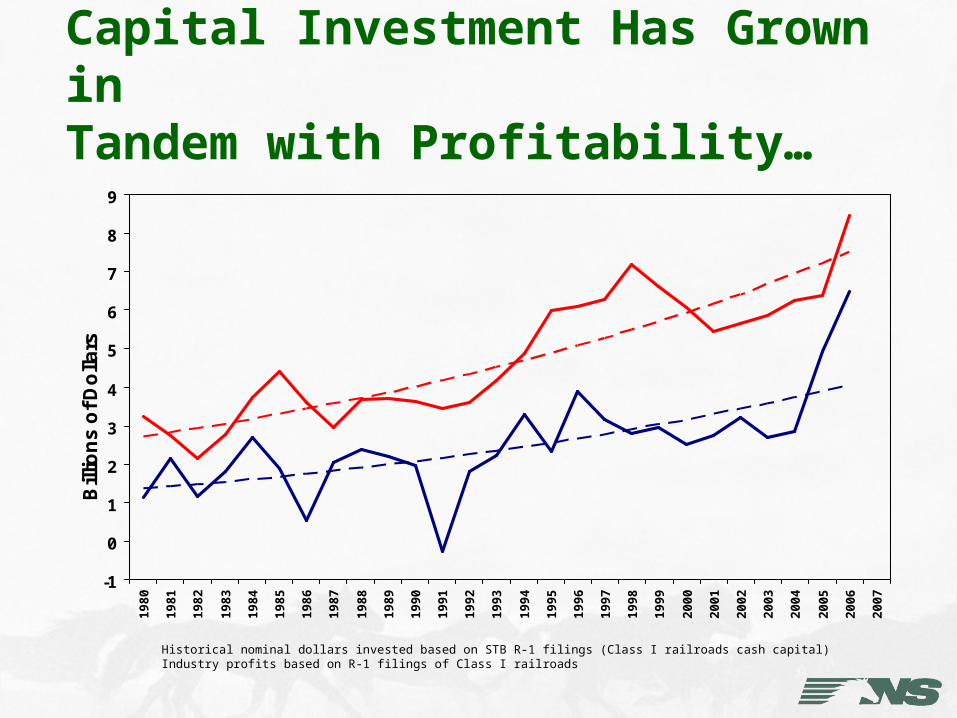

Capital Investment Has Grown inTandem with Profitability…

-1

0

1

2

3

4

5

6

7

8

9

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

Bill

ion

s o

f D

olla

rs

Industry Capital Investment

IndustryProfits

Historical nominal dollars invested based on STB R-1 filings (Class I railroads cash capital)Industry profits based on R-1 filings of Class I railroads

Yet Industry Capital Investment StillInsufficient to Meet AASHTO Goal

0

5

10

15

20

25

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

Bill

ion

s o

f D

olla

rs

Maintain same share of freight

Meet AASHTO goal to increase share of freight carried by rail

Industry Capital Investment

Industry Profits

Based on averages of AASHTO estimates adjusted for inflation to nominal dollarsTrend in actual investment levels based on regression of historical nominal dollars invested (from STB R-1 filings, Class I railroads cash capital) Trend in industry profits based on regression of historical nominal profits excluding 1991 losses (from STB R-1 filings, Class I railroads)

Investment needed to…

Past Industry Capital Investment Shortfalls Will Require Even Higher Levels Than Projected

0

5

10

15

20

25

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Bill

ion

s o

f D

olla

rs

Maintain same share of freight

Meet AASHTO goal to increase share of freight carried by rail

Actual IndustryCapital Investment

AASHTO projected investment;reduced rail share of freight

Based on averages of AASHTO estimates adjusted for inflation to nominal dollarsActual investment levels from STB R-1 filings (Class I railroads cash capital)

Investment needed to…

0

5

10

15

20

25

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Bill

ion

s o

f D

olla

rs

Maintain same share of freight

Meet AASHTO goal to increase share of freight carried by rail

Actual Industry Capital Investment

Past Industry Capital Investment Shortfalls Will Require Even Higher Levels Than Projected

Necessary investment levels based on averages of AASHTO estimates adjusted for inflationActual investment levels from STB R-1 filings (Class I railroads cash capital)

Investment needed to…

An Overview

Rail Infrastructure Economics

The Fundamental Infrastructure Financing Issue Issue is not whether capital exists – capital

markets have effectively unlimited capital

Issue is the number of infrastructure projects where expected risk-adjusted investment returns meet or exceed capital costs

Much of infrastructure “need” being discussed are projects that have high returns to customers and for the country, but low returns to the railroad, at least at current pricing

Rail Infrastructure Economics

Infrastructure Investment Level

Market Return

Cost of Capital

HIGHER RETURN PROJECTS LOWER RETURN PROJECTS

Rail Infrastructure Economics

Infrastructure Investment Level

Market Return

Depressed Return

Cost of Capital

--Subsidies to competition-- Sector-specific government mandates (e.g., HAZMAT)-- Price regulation-- Risk of increased regulation

ACTUAL

HIGHER RETURN PROJECTS LOWER RETURN PROJECTS

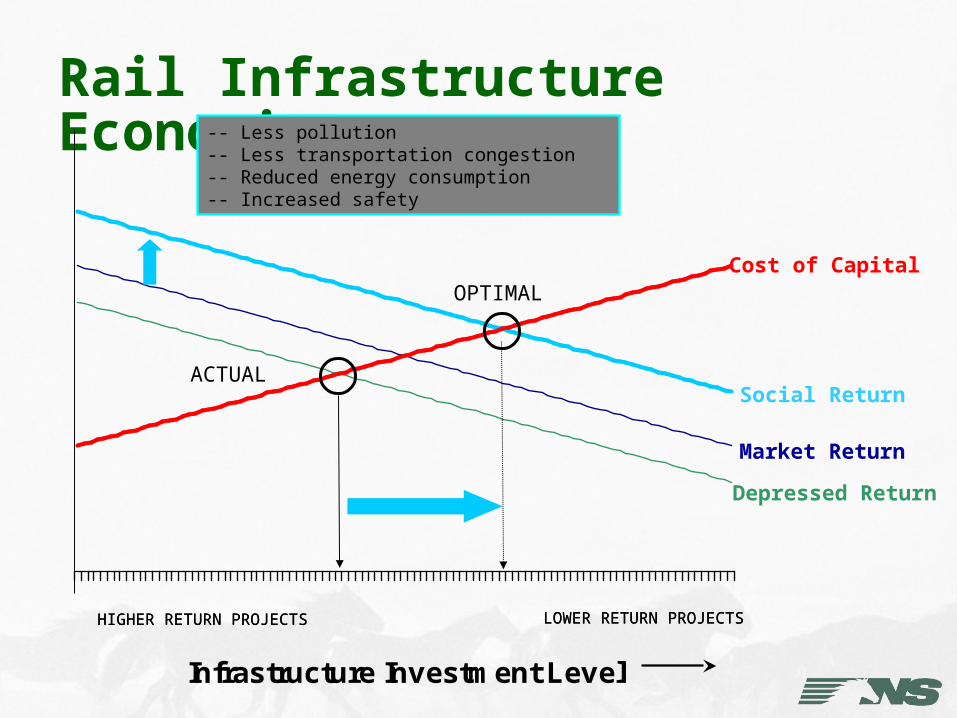

Rail Infrastructure Economics

Infrastructure Investment Level

Market Return

Depressed Return

Social Return

Cost of Capital

-- Less pollution-- Less transportation congestion-- Reduced energy consumption-- Increased safety

OPTIMAL

ACTUAL

HIGHER RETURN PROJECTS LOWER RETURN PROJECTSHIGHER RETURN PROJECTS LOWER RETURN PROJECTS

Rail Infrastructure Economics

Infrastructure Investment Level

Market Return

Depressed Return

Social Return

Cost of Capital

…Proposed

PPPs objective: Reduce gap by lowering cost of capital

PROGRESS

HIGHER RETURN PROJECTS LOWER RETURN PROJECTS

Two PPP Models

Direct Investment by BOTH the Public and the Private Sector

“Indirect” Support by the Public: Investment Tax Credits for Rail

Direct Federal Investment: Highway Bill Principal Sections

Section 1301 – Projects of National & Regional Significance Track, Technology, Facilities

Section 1702 – High Priority Projects Technology, Small Facilities

Section 11143 – Private Activity Bonds Large Facilities

Other Mechanisms [CMAQ, TIFIA, RRIF]

Heartland Corridor

ColumbusColumbus

RickenbackerRickenbacker

AshvilleAshville

HuntingtonHuntingtonKenovaKenova

PrichardPrichard

WilliamsonWilliamsonWelchWelch

BluefieldBluefield

RoanokeRoanokePetersburgPetersburg

RichmondRichmond

Washington, DCWashington, DC

ChristiansburgChristiansburg

PortsmouthPortsmouth

To Chicago, Detroit, and Points West

VA

OH

WV

KYPortsmouthPortsmouth

664

664264

264

464

Western Freeway Rail Corridor

564

64

1. Central Corridor Double-Stack Initiative, and Roanoke and Pritchard Intermodal Facilities

2. Related Terminal Capacity

3. Western Freeway Rail Corridor

L E G E N D

The Heartland Corridor

PortsmouthPortsmouth

NorfolkNorfolk

16`4

CIDMMACIDMMA

PMTPMT

NITNITNITNIT

MaerskMaerskMaerskMaersk

CIMTCIMT(Proposed)(Proposed)

CIMTCIMT(Proposed)(Proposed)

Chicago’s Rail Corridors

Charlotte IM Terminal

Bring in the PAB leveraging effect!!

Indirect Federal Support

Investment Tax Incentive Legislation Introduced Last Congress and this Congress Provides for 25 % Credit for “new” capacity Applies to track, technology, facilities, and locomotives

The rail industry has a number of corridor projects, like the I-81 Crescent Corridor on NS, that could be facilitated by this type of PPP

Why Are Tax Incentives Needed?

2006 CBO Report recognizes that a variety of forces complicate railroads’ ability to attract capital: Tax policies tilt infrastructure playing field in favor of

competitors Railroads bear complex risk on immobile investment Continued government regulation imposes pricing and

operational constraints and many industry- specific financial burdens

Tax Credit for Qualifying Property

25% tax credit for investment in property that allows for an increase in the speed, weight, or volume of freight moved

“Star Trek” property Bridge or tunnel expansion Qualified new locomotives

Public Benefits ofFreight Rail Incentives

A single intermodal train can remove up to 280 trucks from roadway travel …

… saving lives and fuel; reducing congestion, pollution and greenhouse gases

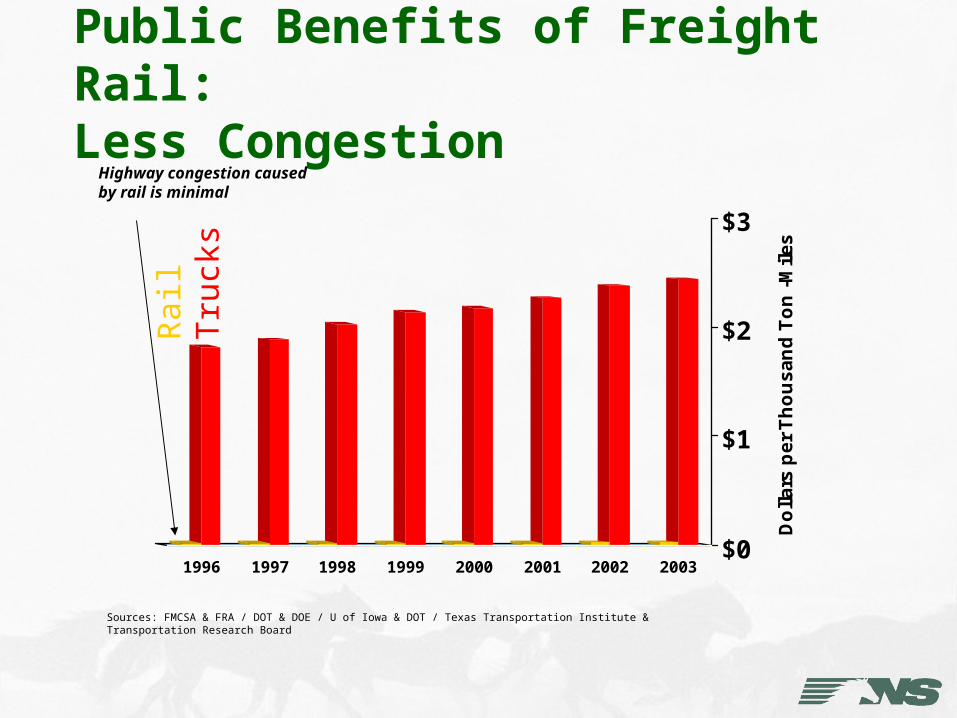

Public Benefits of Freight Rail: Less Congestion

Sources: FMCSA & FRA / DOT & DOE / U of Iowa & DOT / Texas Transportation Institute & Transportation Research Board

$0

$1

$2

$3

Do

lla

rs p

er

Th

ou

sa

nd

To

n -

Mil

es

1996 1997 1998 1999 2000 2001 2002 2003

Rai

lT

ruck

sHighway congestion caused by rail is minimal

Public Benefits of Freight Rail: Less Pollution and Greenhouse Gas

Sources: FMCSA & FRA / DOT & DOE / U of Iowa & DOT / Texas Transportation Institute & Transportation Research Board

0

1

2

3

4

5

Ra

tio

SO2 VOC PM10 NOx CO2

Ratio of Emissionsper ton-mile

(2003)

Rai

lT

ruck

s

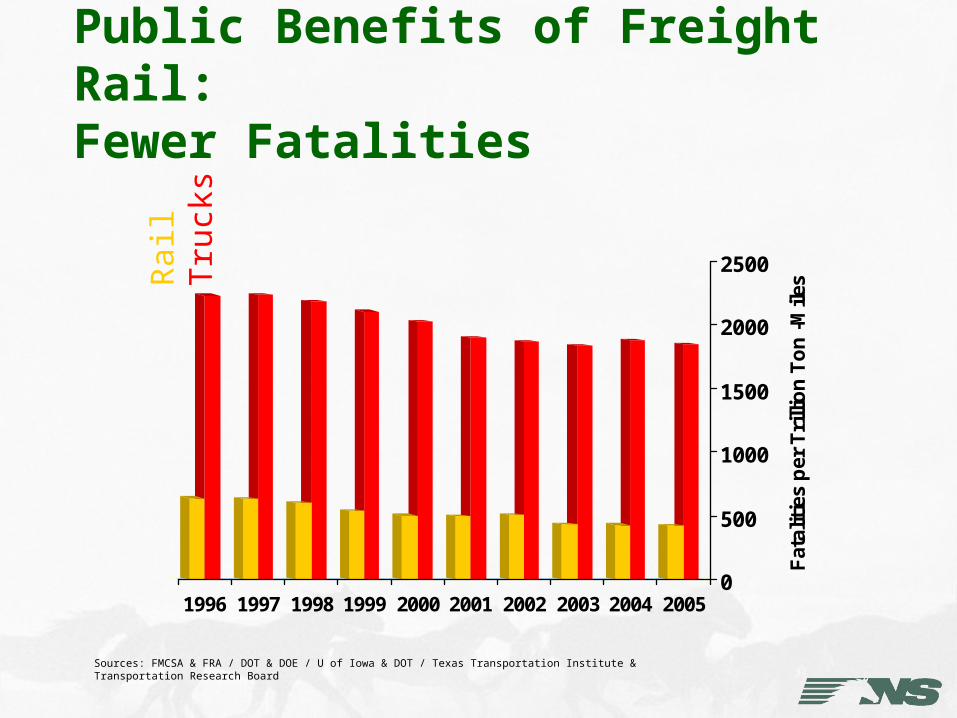

Public Benefits of Freight Rail: Fewer Fatalities

Sources: FMCSA & FRA / DOT & DOE / U of Iowa & DOT / Texas Transportation Institute & Transportation Research Board

0

500

1000

1500

2000

2500

Fat

alit

ies

per

Tri

llio

n T

on

-M

iles

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Rai

lT

ruck

s

Public Benefits of Freight Rail: Reduced Energy Consumption

Sources: FMCSA & FRA / DOT & DOE / U of Iowa & DOT / Texas Transportation Institute & Transportation Research Board

0

2

4

6

8

10

12

14

Gal

lon

s p

er T

ho

usa

nd

To

n-M

iles

1996 1997 1998 1999 2000 2001 2002 2003 2004

Rai

lT

ruck

s

Public Benefits From Expanded Rail Capacity

Projections based on costs of congestion, accidents, air pollution derived from FHWA, Texas Transportation Institute, EPA and other sourcesToxic air pollution does not include the costs of carbon dioxide emissions

Social Costs Rail vs. Trucks

$0

$2

$4

$6

$8

$10

$12

Rail Trucks

Do

llar

s p

er T

ho

usa

nd

To

n M

iles Toxic Air Pollution

Accidents

Congestion

Shipping by rail results in social costs approximately 80% lower than shipping by truck.

Public Benefits From Expanded Rail Capacity

0

5

10

15

20

25

2005 2007 2009 2011 2013 2015 2017 2019 2021 2023 2025

Projections based on costs of congestion, accidents, air pollution derived from FHWA, Texas Transportation Institute, EPA and other sourcesToxic air pollution does not include the costs of carbon dioxide emissions

Social Cost Differential Between AASHTO Reduced Share and Increased Share Scenarios:Totals $200 Billion Over 20 Years

The Challenge of MeetingFreight Infrastructure Demands

Questions?