the bangchak petroleum plc. - listed companybcp.listedcompany.com/misc/analystmeet/bcp...

TRANSCRIPT

0

PRIVATE & CONFIDENTIAL | OCTOBER 2006

The Bangchak Petroleum Plc.

1

STRICTLY PRIVATE & CONFIDENTIAL

The information contained herein is being furnished on a confidential basis for discussion purposes only and only for the

use of the recipient, and may be subject to completion or amendment through the delivery of additional documentation.

Except as otherwise provided herein, this document does not constitute an offer to sell or purchase any security or

engage in any transaction. The information contained herein has been obtained from sources that The Bangchak

Petroleum Public Company Limited (“BCP”) considers to be reliable; however, BCP makes no representation as to, and

accepts no responsibility or liability for, the accuracy or completeness of the information contained herein. Any

projections, valuations and statistical analyses contained herein have been provided to assist the recipient in the

evaluation of the matters described herein; such projections, valuations and analyses may be based on subjective

assessments and assumptions and may utilise one among alternative methodologies that produce differing results;

accordingly, such projections, valuations and statistical analyses are not to be viewed as facts and should not be relied

upon as an accurate representation of future events. The recipient should make an independent evaluation and

judgment with respect to the matters contained herein.

The Bangchak Petroleum Public Company LimitedThe Bangchak Petroleum Public Company Limited210 210 SukhumvitSukhumvit 64 Rd., 64 Rd., PhrakhanongPhrakhanong, Bangkok 10260, Bangkok 10260

Disclaimer

2

STRICTLY PRIVATE & CONFIDENTIAL

Contents

Company Background►Oil Refinery and Marketing Business in Thailand

►Company Development

Phase I: Capital Restructuring (2003-2004)

Phase II: Business Improvement (2005 onward)►Oil Price vs. Demand & Supply

►Product Quality Improvement Project (“PQI”)

►Strategic Partner Participation

►PQI Financing

Current Status►PQI Progress

►Capital Structure

►BCP’s Instruments and Features

►CSDR Trading Price

►Shareholding Structure

►Refinery Performance

►Marketing Performance

►Company Performance

Forward Looking►Future Plan

Appendix

3

Company Background

4

STRICTLY PRIVATE & CONFIDENTIAL

Oil Refinery and Marketing Business in Thailand

75215ComplexTPI

3220(2)ComplexThai Oil

-150ComplexStar

-150(2)ComplexRayong (RRC)

602165ComplexEsso

590590(+co(+co--op 549)op 549)

120120SimpleSimpleBangchakBangchak

3617SimpleRayong Purifier (RPC)

147--Conoco

12,501--Independent Gas Stations

340--Others(1)111--Petronas

158--Susco

421--Chevron

570--Shell

1,248--PTT

17,35117,3511,0371,037TotalTotal

ServiceServiceStationStation

Refinery Refinery CapacityCapacity

(KBD)(KBD)

Refinery Refinery TechnologyTechnology

PlayersPlayersIn ThailandIn Thailand

• BCP is an integrated oil company of which operation ranges from refinery business to marketing business.

Note: (1) including Cosmo, PC, and PT(2) Thai Oil plans to expand its refinery capacity for additional 5 KBD in 3Q06 and another 50 KBD in 2007(3) Rayong (RRC) plans to expand its refinery capacity for 65 KBD in 3Q08

IntegratedIntegratedIntegrated

RefineryOnlyRefineryRefineryOnlyOnly

MarketingOnly

MarketingOnly

Jobbers

ThaiAirways

IndustrialCustomers

Jobbers ServiceStations

BCP’sRefineryBusiness

BCPBCP’’ss

RefineryRefinery

BusinessBusiness

ImportImportCrudeCrude(86%)

LocalLocalCrudeCrude(14%)

SimpleSimpleRefineryRefinery120 KBD120 KBD

Wholesalers

PTT Wholesalers

Export

Wholesale Customers

Retail Customers

RefinedRefinedProductsProducts

BCP’sMarketingBusiness

BCPBCP’’ss

MarketingMarketing

BusinessBusiness

GRM

MKM

CrudeCost

Ex-RefPrice

WholesalePrice

RetailPrice

HSDHSD 35%35%MogasMogas 18%18%IK/JPIK/JP--11 11%11%LPGLPG 3%3%FOFO 30%30%

MKM

5

STRICTLY PRIVATE & CONFIDENTIAL

SituationDifficulties

SituationDifficulties

• Construction period estimated to be 28 months

• Construction period estimated to be 28 months

• To turn BCP’s existing simple refinery to be a complex refinery.

• To turn BCP’s existing simple refinery to be a complex refinery.

• Debt & Equity fund raising of USD 398 million

• PTT became a major shareholder with nearly 30% holding percentage

• Study for future opportunity investment

• Debt & Equity fund raising of USD 398 million

• PTT became a major shareholder with nearly 30% holding percentage

• Study for future opportunity investment

Company Development

2004 2005 2006

• Strengthen the management team

• Synergize with other operators & Sourcing crude from domestic fields

• Separate marketing business accounting from

refinery business accounting for more efficient monitoring

• Implementation of Mercury Removal Units (MRU)

• Strengthen the management team

• Synergize with other operators & Sourcing crude from domestic fields

• Separate marketing business accounting from

refinery business accounting for more efficient monitoring

• Implementation of Mercury Removal Units (MRU)

• Refinancing total debt by new source of money

• Changing status from State Enterprise to pure public company

• Refinancing total debt by new source of money

• Changing status from State Enterprise to pure public company

CapitalCapitalRestructuringRestructuring

PQIPQIFeasibility StudyFeasibility Study

PQI Financial ClosePQI Financial Close& Participation of & Participation of Strategic PartnerStrategic Partner

PQIPQIConstructionConstruction

Commencement Commencement

2007

I. Capital RestructuringI. Capital Restructuring II. Business ImprovementII. Business Improvement III. Capture OpportunityIII. Capture Opportunity

2008

• COD is expected to be by end 2008.

• Cogeneration power plant

• Bio-diesel plant

• Using natural gas as fuel instead of fuel oil

• COD is expected to be by end 2008.

• Cogeneration power plant

• Bio-diesel plant

• Using natural gas as fuel instead of fuel oil

PQI Commercial PQI Commercial OperationOperation

MarketVolatility

MarketVolatility Future

Challenge

FutureChallenge

2009

BCP is turning to be a competitive operator after striving from financial distress.

FoundationFoundationRevampRevamp

6

Phase I : Capital Restructuring

2003 - 2004

7

STRICTLY PRIVATE & CONFIDENTIAL

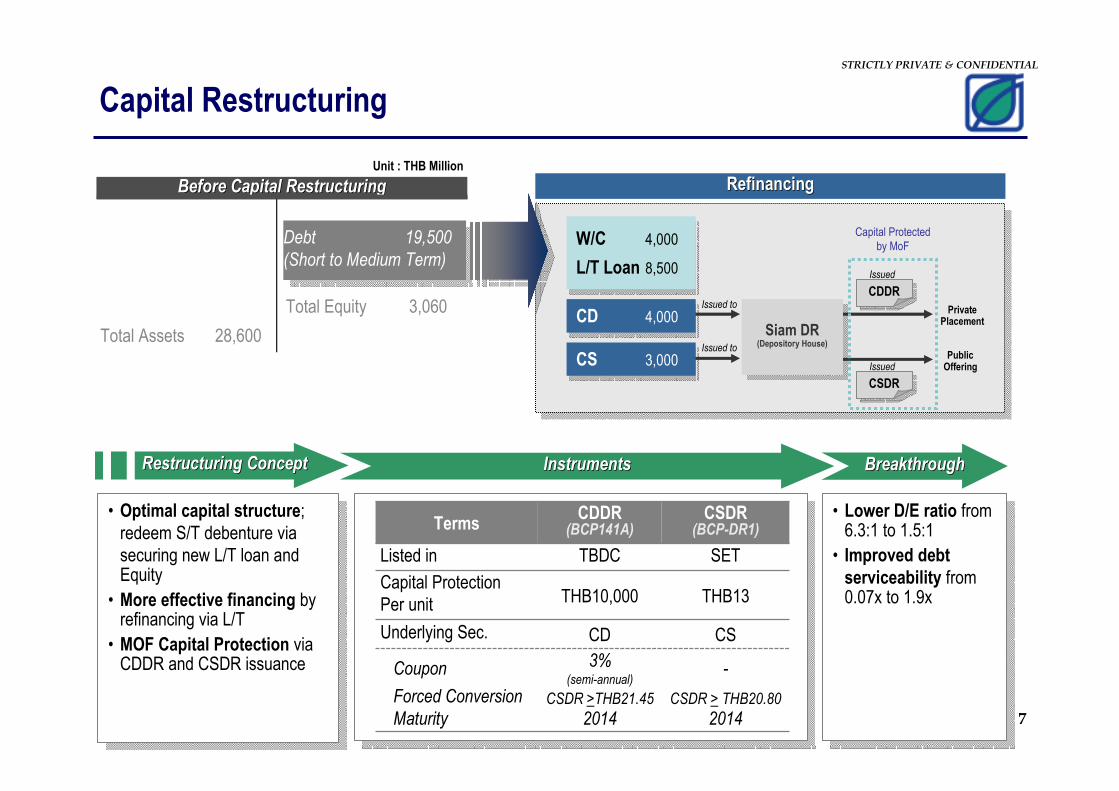

Debt 19,500

(Short to Medium Term)

Debt 19,500

(Short to Medium Term)

Capital Restructuring

Total Assets 28,600

BeforeBefore CapitalCapital RestructuringRestructuring

Total Equity 3,060

Siam DR(Depository House)

Siam DR(Depository House)

W/C 4,000

L/T Loan 8,500

W/C 4,000

L/T Loan 8,500

CS 3,000CS 3,000

CD 4,000CD 4,000Private

Placement

• Optimal capital structure;

redeem S/T debenture via

securing new L/T loan and Equity

• More effective financing by refinancing via L/T

• MOF Capital Protection via CDDR and CSDR issuance

• Optimal capital structure;

redeem S/T debenture via

securing new L/T loan and Equity

• More effective financing by refinancing via L/T

• MOF Capital Protection via CDDR and CSDR issuance

• Lower D/E ratio from 6.3:1 to 1.5:1

• Improved debt

serviceability from 0.07x to 1.9x

• Lower D/E ratio from 6.3:1 to 1.5:1

• Improved debt

serviceability from 0.07x to 1.9x

SETTBDCListed in

2014

THB13

2014MaturityCSDR > THB20.80CSDR >THB21.45Forced Conversion

-3%(semi-annual)

Coupon

CSCDUnderlying Sec.

THB10,000Capital Protection

Per unit

CSDR(BCP-DR1)

CDDR(BCP141A)Terms

RefinancingRefinancing

Restructuring ConceptRestructuring Concept InstrumentsInstruments BreakthroughBreakthrough

Issued to

Issued to

CSDRCSDR

PublicOffering

CDDRCDDR

Issued

Issued

Unit : THB Million

Capital Protected

by MoF

8

Phase II : Business Improvement

2005 onward

9

STRICTLY PRIVATE & CONFIDENTIAL

-

2,000

4,000

6,000

8,000

10,000

12,000

2003

2004

2005

1H06

2006F

2007F

2008F

2009F

2010F

2011F

THB mil

-

2

4

6

8

10

12

USD/bbl

EBITDA

EBITDA (feasibility study)

GRM

GRM (feasibility study)

Oil Price vs. Demand & Supply

Return from investment competitive in long-term, hence BCP decided to pursue PQI project

New CDU Capacity Thailand Capacity vs. Demand

Oil Price2003 – Jul 2006

BCP’s EBITDA2003 – 2011F

Note: (1) EBITDA 2007F-2011F based on GO/DB USD16.73/bbl and DB/FO USD12.31/bbl(2) EBITDA (feasibility study) 2007F-2011F based on GO/DB USD10.5/bbl and DB/FO USD3/bbl

Both cases based on gradually growing crude run from 65 KBSD before COD after that run 100 KBSD

(1)

(2)

Barrel per Day

-

20

40

60

80

100

1-Jan-03

1-Apr-03

1-Jul-03

1-Oct-03

1-Jan-04

1-Apr-04

1-Jul-04

1-Oct-04

1-Jan-05

1-Apr-05

1-Jul-05

1-Oct-05

1-Jan-06

1-Apr-06

1-Jul-06

USD/bblDubai Gas Oil Fuel Oil

-

2 0 0

4 0 0

6 0 0

8 0 0

1 , 0 0 0

1 , 2 0 0

1 2 3 4 5 6 7 8 9

T o ta l R e f in e r y C a p a c it y to ta l P r o d u c t D e m a n d

2004 2005 2006 2007 2008 2009 2010 2011 2012

KBD

7,785,3821,390,0001,920,0002,481,4991,024,983968,900Total World

451,000

4,225,405

450,000

1,116,400

1,009,500

303,077

230,000

-

1,000,000

-

-

-

250,000

140,000

-

1,300,000

-

440,000

180,000

-

-

230,000

1,038,405

300,000

475,000

330,000

18,094

90,000

218,000

347,000

150,000

15,000

260,000

34,983

-

3,000

540,000

-

186,400

239,500

-

-

Total Africa

Total Asia Pacific

Total FSU

Total Middle East

Total North

America

Total South

America

Total OECD Europe

Total20102009200820072006Country

7,785,3821,390,0001,920,0002,481,4991,024,983968,900Total World

451,000

4,225,405

450,000

1,116,400

1,009,500

303,077

230,000

-

1,000,000

-

-

-

250,000

140,000

-

1,300,000

-

440,000

180,000

-

-

230,000

1,038,405

300,000

475,000

330,000

18,094

90,000

218,000

347,000

150,000

15,000

260,000

34,983

-

3,000

540,000

-

186,400

239,500

-

-

Total Africa

Total Asia Pacific

Total FSU

Total Middle East

Total North

America

Total South

America

Total OECD Europe

Total20102009200820072006Country

10

STRICTLY PRIVATE & CONFIDENTIAL

USD/bbl

10

8

6

4

2

0

Product Quality Improvement Project (“PQI”)

Fuel Oil

31%

Diesel

37%

ULG

15%

Jet Fuel

14%

LPG 3%

Fuel Oil

31%

Diesel

37%

ULG

15%

Jet Fuel

14%

LPG 3%

ULG

25%

Diesel

52%

Fuel Oil9%

Jet Fuel9%

LPG 5%

ULG

25%

Diesel

52%

Fuel Oil9%

Jet Fuel9%

LPG 5%

What is PQI ?What is PQI ? Result from PQIResult from PQI

CounterpartiesCounterparties

• PQI is the Investment in “Hydrocracking Unit” and other

supporting units

• These units enable BCP to turn current fuel oil output to

be gas oil without increasing the capacity

• Feasibility Study UOP LLC & Foster Wheeler Corporation

• Technology License UOP LLC

• EPC Contractor CTCI Corporation

• Project Mgnt Consultant Foster Wheeler Corporation

• Investment Cost USD 378 million

• Construction Period May’06 – Sep’08 (28 months)

Investment & ConstructionInvestment & Construction

MEME FEFEMEME FEFE

CurrentSimple Refinery

AfterPQI Completion

EnhanceEnhance

Crude MixCrude Mix

FlexibilityFlexibility

Less FOLess FO

OutputOutput

PortionPortion

SurgeSurge

GRMGRM

Current

Spread

Current

Spread

Feasibility

Spread

11

STRICTLY PRIVATE & CONFIDENTIAL

•• Products to be swap is based on mutual Products to be swap is based on mutual

agreementagreement

•• Benefit sharing as per commercial basis Benefit sharing as per commercial basis

based on mutual agreementbased on mutual agreement

Product SwapProduct Swap

•• Create synergy between BCP and PTTCreate synergy between BCP and PTT

•• Ranging from refinery management to Ranging from refinery management to

product marketing collaborationproduct marketing collaboration

Marketing & Refinery CollaborationMarketing & Refinery Collaboration

Strategic Partner Participation

• Business synergy from PTT Plc., a strategic partner, help enhance BCP’s return from PQI

•• Up to 30%Up to 30%

•• Secure market for additional output Secure market for additional output

after PQIafter PQI

•• Optimize capacity utilizationOptimize capacity utilization

Product OffProduct Off--take Agreementtake Agreement

•• Up to 100% Up to 100%

•• Ensure Ensure BCPBCP’’ss crude supplycrude supply

•• Better bargaining powerBetter bargaining power

•• Better economy of scale of freightBetter economy of scale of freight

Crude Supply AgreementCrude Supply Agreement

12

STRICTLY PRIVATE & CONFIDENTIAL

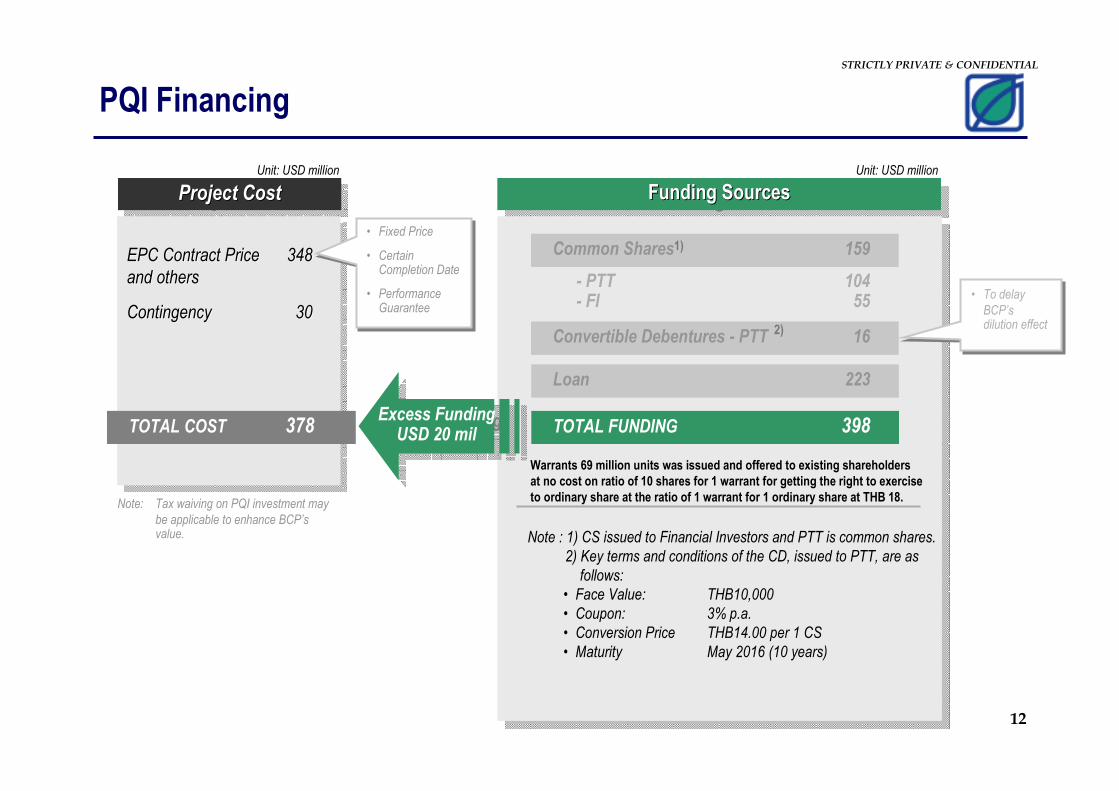

Funding SourcesFunding SourcesFunding Sources

PQI Financing

Project CostProject CostProject Cost

Note : 1) CS issued to Financial Investors and PTT is common shares.

2) Key terms and conditions of the CD, issued to PTT, are as

follows:

• Face Value: THB10,000

• Coupon: 3% p.a.

• Conversion Price THB14.00 per 1 CS

• Maturity May 2016 (10 years)

Unit: USD million

EPC Contract Price 348

and others

Contingency 30

EPC Contract PriceEPC Contract Price 348348

and othersand others

ContingencyContingency 3030

Excess FundingUSD 20 mil

Excess FundingUSD 20 milTOTAL COST 378

- PTT 104- FI 55

Common Shares 159

Convertible Debentures - PTT 16

Loan 223

TOTAL FUNDING 398

Unit: USD million

• To delay

BCP’s dilution effect

• To delay

BCP’s dilution effect

• Fixed Price

• Certain Completion Date

• Performance Guarantee

• Fixed Price

• Certain Completion Date

• Performance Guarantee

Note: Tax waiving on PQI investment may

be applicable to enhance BCP’svalue.

Warrants 69 million units was issued and offered to existing shareholders

at no cost on ratio of 10 shares for 1 warrant for getting the right to exercise

to ordinary share at the ratio of 1 warrant for 1 ordinary share at THB 18.

1)

2)

13

Current Status

2006

14

STRICTLY PRIVATE & CONFIDENTIAL

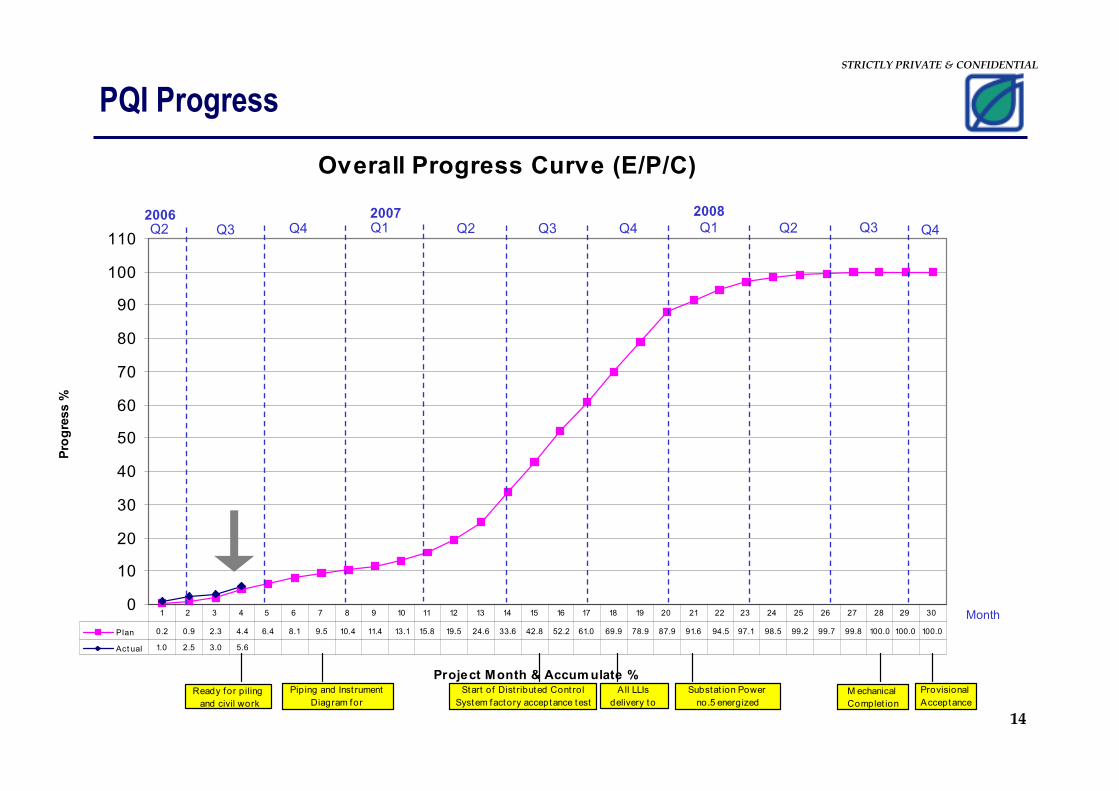

Overall Progress Curve (E/P/C)

0

10

20

30

40

50

60

70

80

90

100

110

Project Month & Accumulate %

Progress %

Plan 0.2 0.9 2.3 4.4 6.4 8.1 9.5 10.4 11.4 13.1 15.8 19.5 24.6 33.6 42.8 52.2 61.0 69.9 78.9 87.9 91.6 94.5 97.1 98.5 99.2 99.7 99.8 100.0 100.0 100.0

Act ual 1.0 2.5 3.0 5.6

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30

Ready for piling

and civil work

Piping and Inst rument

Diagram for

Start of Dist ributed Cont rol

System factory acceptance test

A ll LLIs

delivery to

Substat ion Power

no.5 energized

M echanical

Complet ion

Provisional

Acceptance

PQI Progress

Q22006

Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q32007 2008

Month

Q4

15

STRICTLY PRIVATE & CONFIDENTIAL

Capital Structure

S/T Loan 2,414

L/T loan 8,929

CDDR 2,175

CD to PTT 586

Paid-up Capital 1,119

CSDR 520

CS 599

Premium on Shares 7,694

Surplus on Assets Revaluation 4,393

R/E 6,287Total Equity 19,493

Total Assets 41,918

Total Liabilities 22,425

As of Jun 30, 2006

Unit : THB Million

16

STRICTLY PRIVATE & CONFIDENTIAL

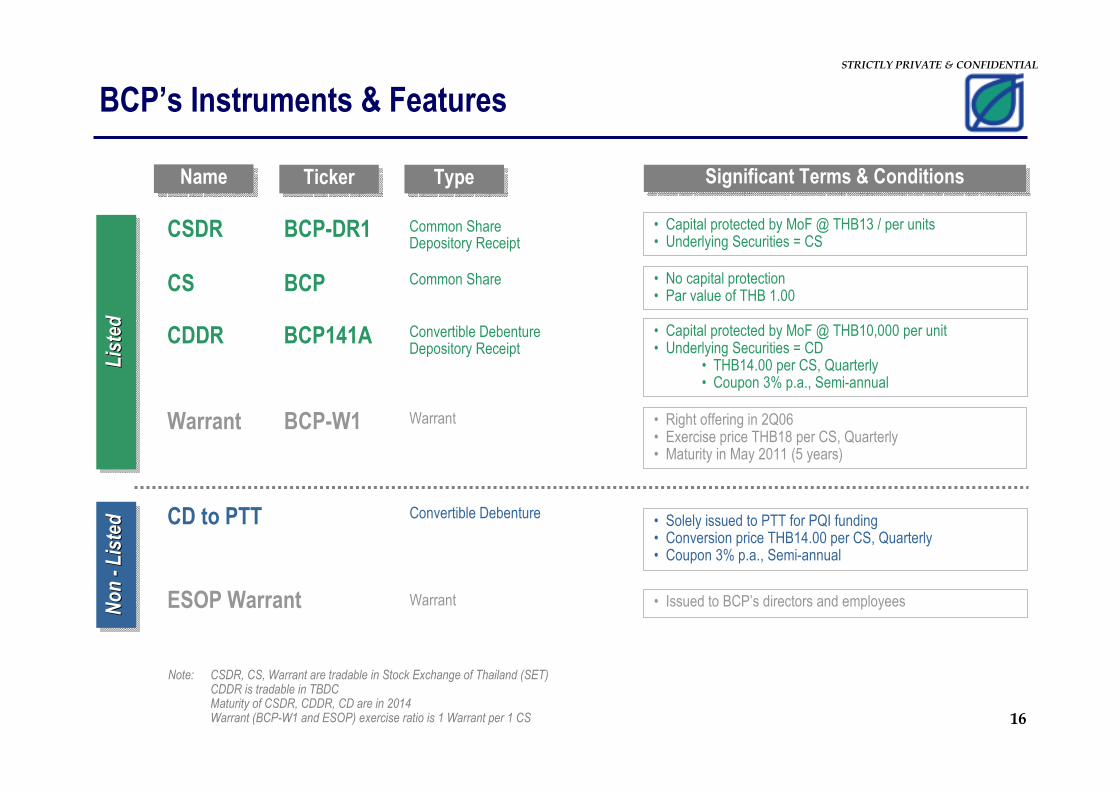

BCP’s Instruments & Features

CSDR

CD to PTT

CS

Warrant

CDDR

ESOP Warrant

Lis

ted

Lis

ted

Lis

ted

No

n -

Lis

ted

No

n

No

n --

Lis

ted

Lis

ted

• Capital protected by MoF @ THB13 / per units• Underlying Securities = CS

• No capital protection• Par value of THB 1.00

• Right offering in 2Q06• Exercise price THB18 per CS, Quarterly• Maturity in May 2011 (5 years)

• Capital protected by MoF @ THB10,000 per unit• Underlying Securities = CD

• THB14.00 per CS, Quarterly• Coupon 3% p.a., Semi-annual

• Solely issued to PTT for PQI funding• Conversion price THB14.00 per CS, Quarterly• Coupon 3% p.a., Semi-annual

BCP-DR1

BCP

BCP-W1

BCP141A

TickerTickerNameName

• Issued to BCP’s directors and employees

Note: CSDR, CS, Warrant are tradable in Stock Exchange of Thailand (SET)CDDR is tradable in TBDCMaturity of CSDR, CDDR, CD are in 2014Warrant (BCP-W1 and ESOP) exercise ratio is 1 Warrant per 1 CS

Significant Terms & ConditionsSignificant Terms & ConditionsTypeType

Common Share Depository Receipt

Convertible Debenture

Common Share

Warrant

Convertible Debenture Depository Receipt

Warrant

17

STRICTLY PRIVATE & CONFIDENTIAL

CSDR Trading Price

Capital ProtectedBy MoF @ THB13/share

0

5

10

15

20

24/9/2004 4/2/2005 22/6/2005 1/11/2005 13/3/2006 31/7/2006

THB/Share

18

STRICTLY PRIVATE & CONFIDENTIAL

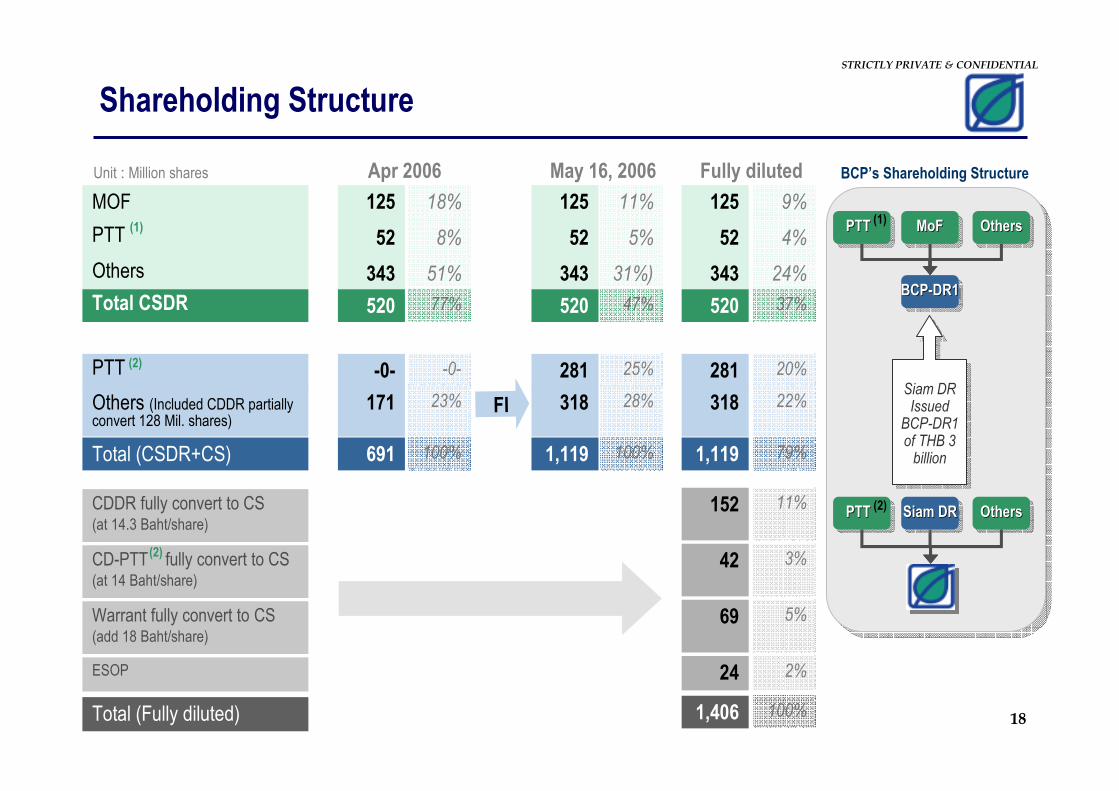

Shareholding Structure

MOF

PTT

Others

125

52

343

11%

5%

31%)

FI

Total CSDR 520

PTT -0-

Total (CSDR+CS) 691

47%

25%

100%

Unit : Million shares

CDDR fully convert to CS(at 14.3 Baht/share)

Total (Fully diluted)

Warrant fully convert to CS(add 18 Baht/share)

CD-PTT fully convert to CS(at 14 Baht/share)

Fully dilutedMay 16, 2006

125

52

343

520

281

1,119

ESOP

18%

8%

51%

77%

-0-

100%

Apr 2006

125

52

343

520

281

1,119

9%

4%

24%

37%

20%

79%

Others (Included CDDR partially convert 128 Mil. shares)

171 28% 31823% 318 22%

152 11%

42 3%

69 5%

24 2%

1,406 100%

BCP’s Shareholding Structure

PTT PTT PTT OthersOthersOthers

MoFMoFMoFPTT PTT PTT OthersOthersOthers

BCP-DR1BCPBCP--DR1DR1

Siam DRSiam DRSiam DR

Siam DR Issued

BCP-DR1of THB 3 billion

Siam DR Issued

BCP-DR1of THB 3 billion

(1)

(2)

(1)

(2)

(2)

19

STRICTLY PRIVATE & CONFIDENTIAL

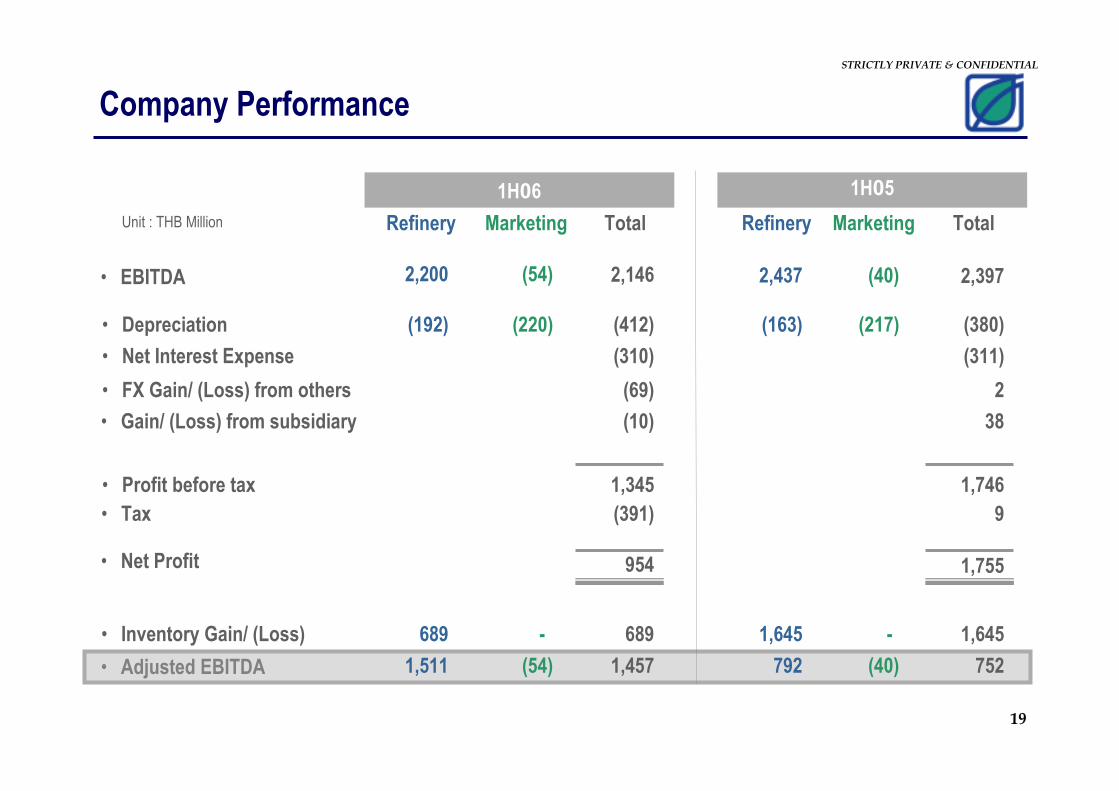

Company Performance

• EBITDA

Total

• Depreciation

• Net Interest Expense

• FX Gain/ (Loss) from others

2,397

(380)

(311)

2

• Net Profit 1,755

• Inventory Gain/ (Loss) 1,645

Refinery

2,437

(163)

1,645

Marketing

(40)

(217)

-

• Gain/ (Loss) from subsidiary 38

• Tax 9

• Profit before tax 1,746

Unit : THB Million

• Adjusted EBITDA 752792 (40)

Total

1H06

2,146

(412)

(310)

(69)

954

689

Refinery

2,200

(192)

689

Marketing

(54)

(220)

-

(10)

(391)

1,345

1,4571,511 (54)

1H05

20

STRICTLY PRIVATE & CONFIDENTIAL

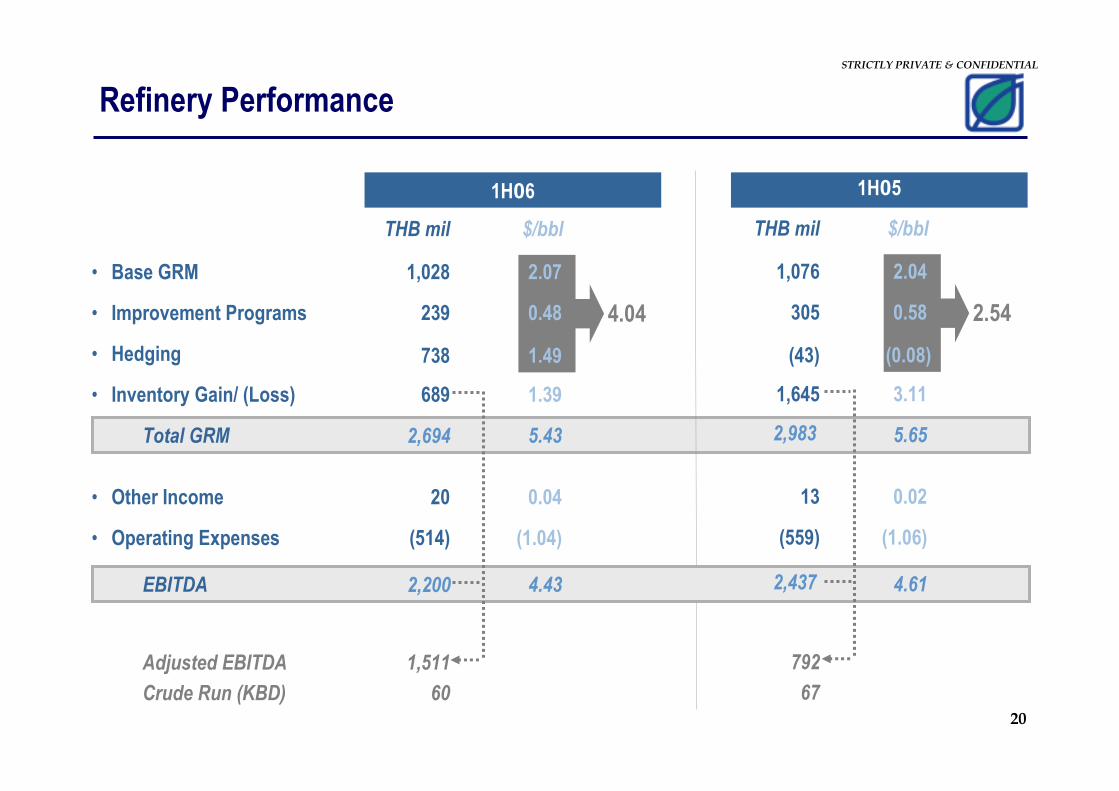

Refinery Performance

• Base GRM 1,028

• Improvement Programs 239

• Inventory Gain/ (Loss) 689

• Other Income 20

2.07

0.48

1.39

0.04

Crude Run (KBD) 60

• Operating Expenses (514) (1.04)

Adjusted EBITDA 1,511

Total GRM

• Hedging 738 1.49

5.43

4.04

1H06

THB mil $/bbl

1H05

1,076

305

1,645

13

2.04

0.58

3.11

0.02

67

(559) (1.06)

792

(43) (0.08)

5.65

2.54

THB mil $/bbl

2,694 2,983

EBITDA 4.43 4.612,200 2,437

21

STRICTLY PRIVATE & CONFIDENTIAL

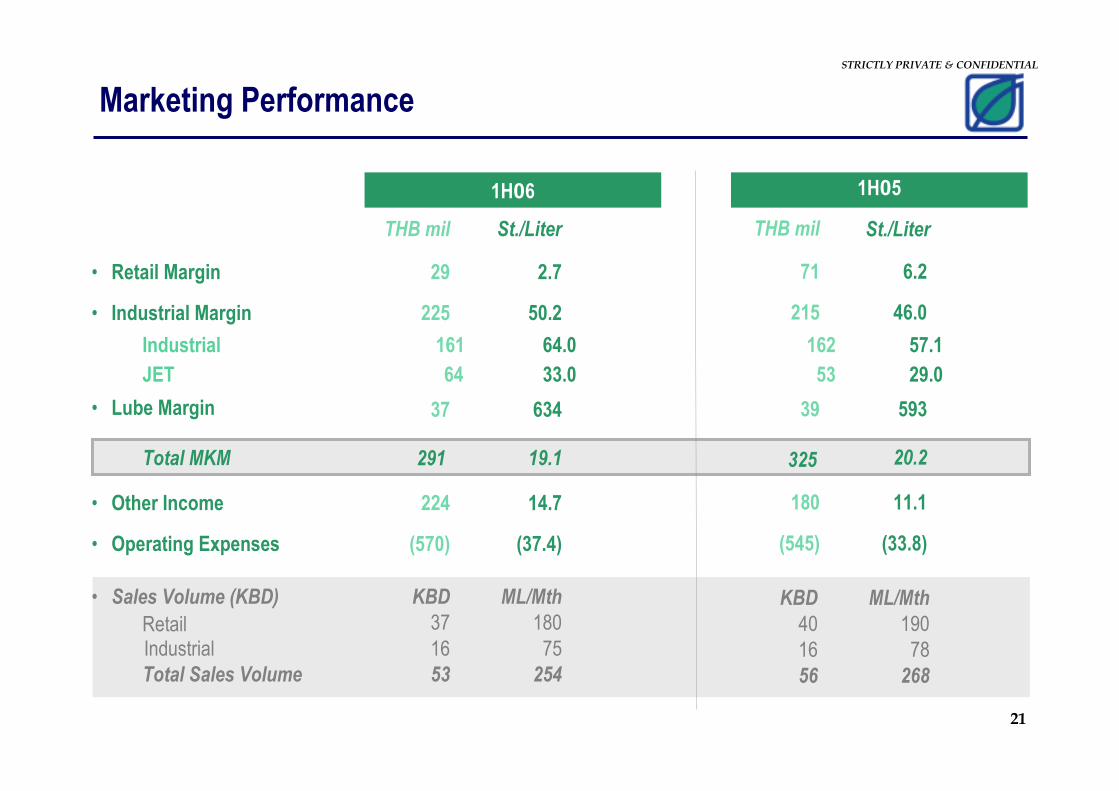

Marketing Performance

• Retail Margin 29

• Industrial Margin 225

• Other Income 224

2.7

50.2

14.7

Retail 37

• Operating Expenses (570) (37.4)

• Sales Volume (KBD) KBD

Total MKM

• Lube Margin 37 634

19.1

1H06

THB mil St./Liter

1H05

71

215

180

6.2

46.0

11.1

(545) (33.8)

39 593

20.2

THB mil

Industrial

JET

Industrial

ML/Mth180

7516

Total Sales Volume 53 254

40

KBD ML/Mth

190

7816

56 268

161

64

64.0

33.0

162

53

57.1

29.0

St./Liter

291 325

22

STRICTLY PRIVATE & CONFIDENTIAL

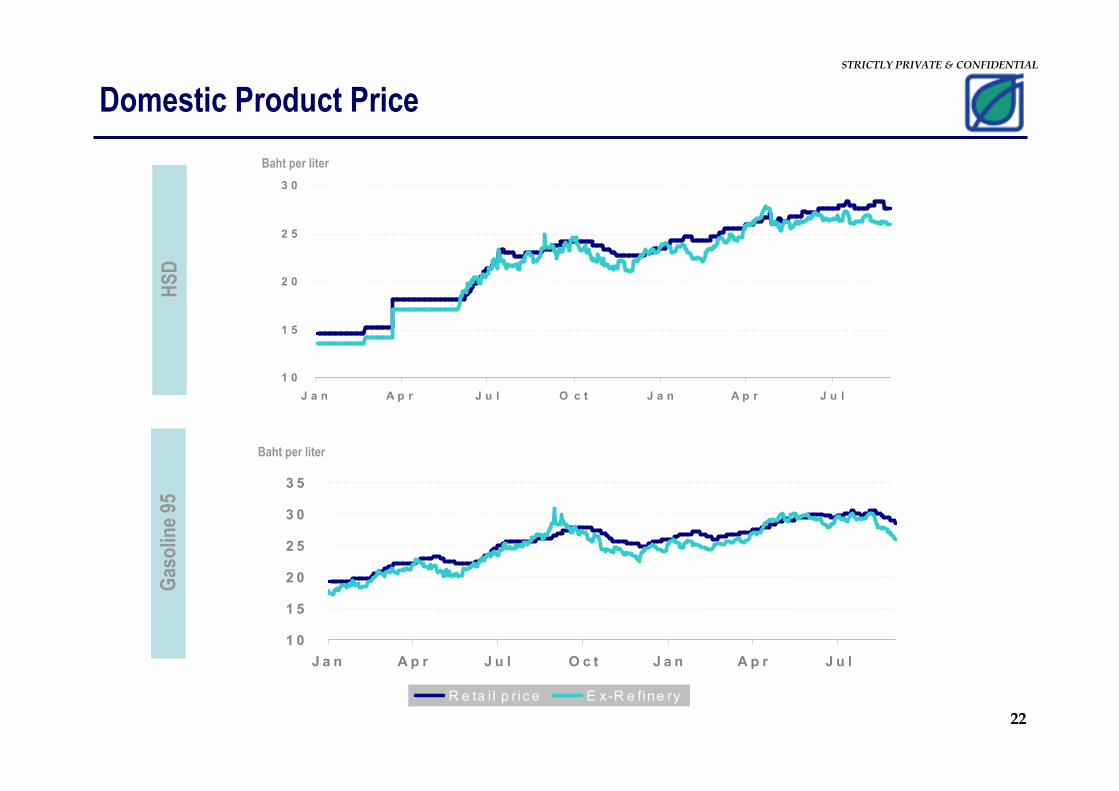

Baht per liter

Baht per liter

HSD

Gasoline 95

Domestic Product Price

1 0

1 5

2 0

2 5

3 0

J a n A p r J u l O c t J a n A p r J u l

1 0

1 5

2 0

2 5

3 0

3 5

J a n A p r J u l O c t J a n A p r J u l

R e ta i l p ric e E x-R e fine ry

23

Forward Looking

2006 onward

24

STRICTLY PRIVATE & CONFIDENTIAL

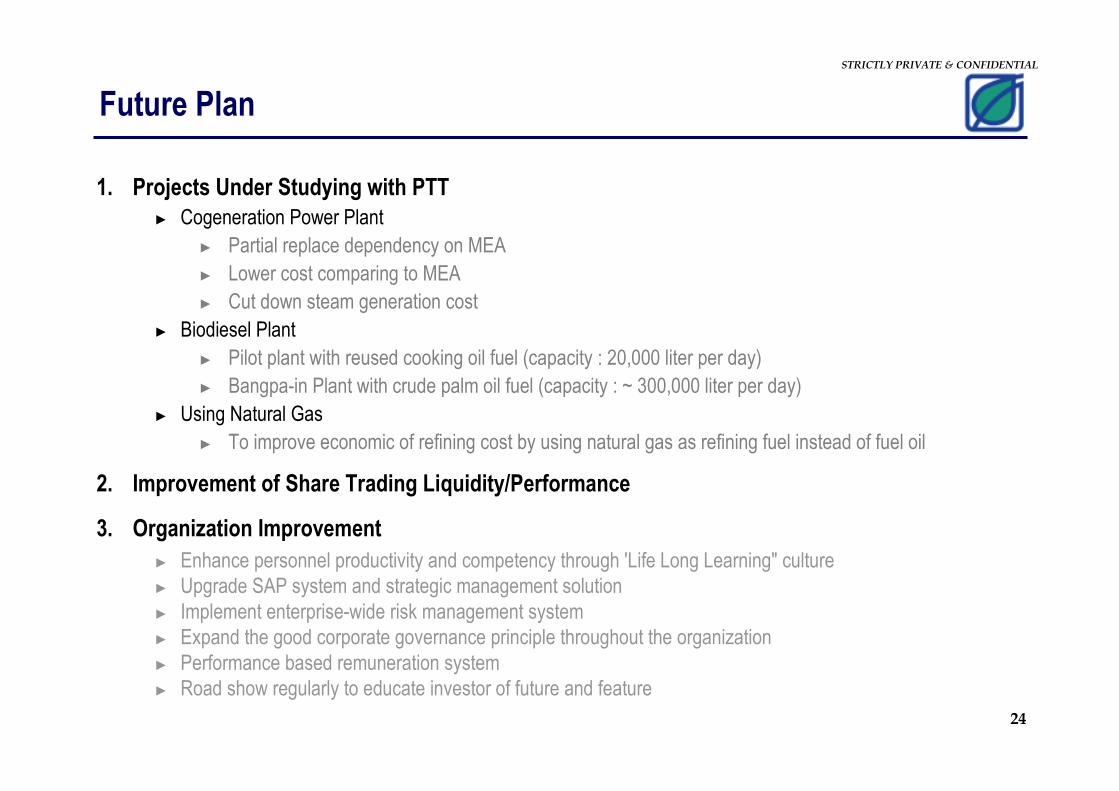

Future Plan

1. Projects Under Studying with PTT

► Cogeneration Power Plant

► Partial replace dependency on MEA

► Lower cost comparing to MEA

► Cut down steam generation cost

► Biodiesel Plant

► Pilot plant with reused cooking oil fuel (capacity : 20,000 liter per day)

► Bangpa-in Plant with crude palm oil fuel (capacity : ~ 300,000 liter per day)

► Using Natural Gas

► To improve economic of refining cost by using natural gas as refining fuel instead of fuel oil

2. Improvement of Share Trading Liquidity/Performance

3. Organization Improvement

► Enhance personnel productivity and competency through 'Life Long Learning" culture

► Upgrade SAP system and strategic management solution

► Implement enterprise-wide risk management system

► Expand the good corporate governance principle throughout the organization

► Performance based remuneration system

► Road show regularly to educate investor of future and feature

25

Appendix

26

STRICTLY PRIVATE & CONFIDENTIAL

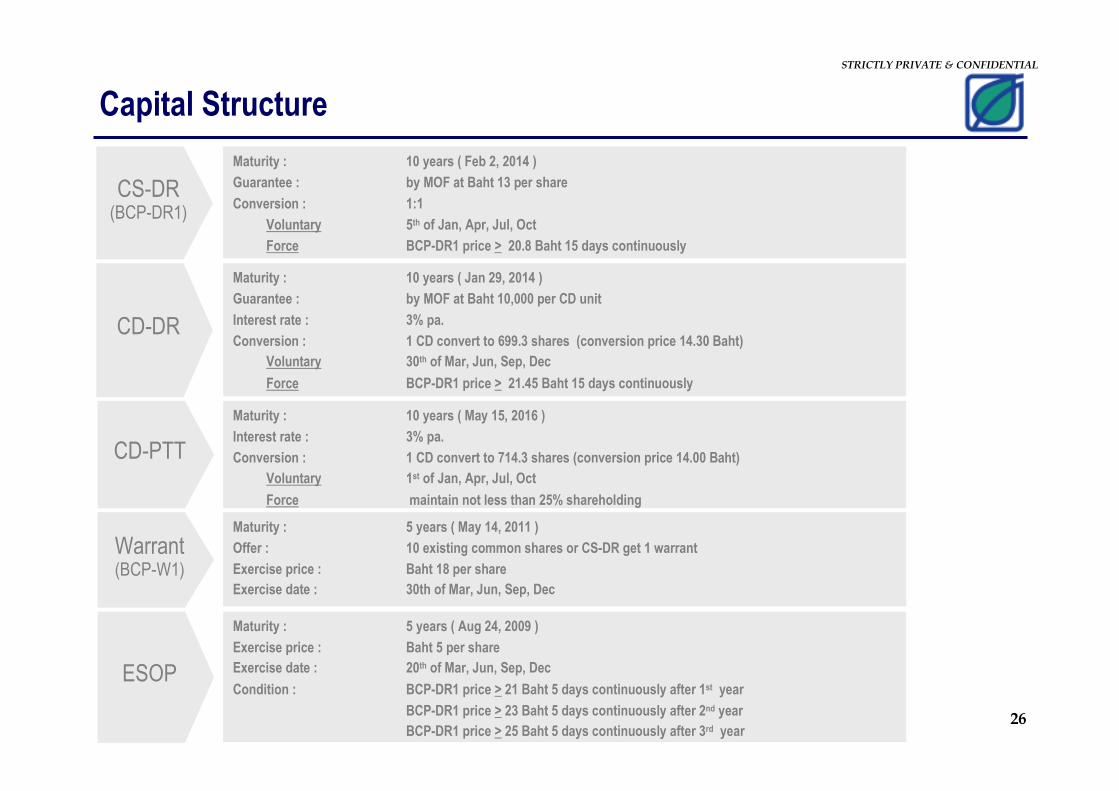

Capital Structure

Maturity : 10 years ( Feb 2, 2014 )

Guarantee : by MOF at Baht 13 per share

Conversion : 1:1

Voluntary 5th of Jan, Apr, Jul, Oct

Force BCP-DR1 price > 20.8 Baht 15 days continuously

CS-DR(BCP-DR1)

Maturity : 10 years ( Jan 29, 2014 )

Guarantee : by MOF at Baht 10,000 per CD unit

Interest rate : 3% pa.

Conversion : 1 CD convert to 699.3 shares (conversion price 14.30 Baht)

Voluntary 30th of Mar, Jun, Sep, Dec

Force BCP-DR1 price > 21.45 Baht 15 days continuously

CD-DR

CD-PTT

Maturity : 5 years ( May 14, 2011 )

Offer : 10 existing common shares or CS-DR get 1 warrant

Exercise price : Baht 18 per share

Exercise date : 30th of Mar, Jun, Sep, Dec

Warrant(BCP-W1)

Maturity : 10 years ( May 15, 2016 )

Interest rate : 3% pa.

Conversion : 1 CD convert to 714.3 shares (conversion price 14.00 Baht)

Voluntary 1st of Jan, Apr, Jul, Oct

Force maintain not less than 25% shareholding

Maturity : 5 years ( Aug 24, 2009 )

Exercise price : Baht 5 per share

Exercise date : 20th of Mar, Jun, Sep, Dec

Condition : BCP-DR1 price > 21 Baht 5 days continuously after 1st year

BCP-DR1 price > 23 Baht 5 days continuously after 2nd year

BCP-DR1 price > 25 Baht 5 days continuously after 3rd year

ESOP

27

STRICTLY PRIVATE & CONFIDENTIAL

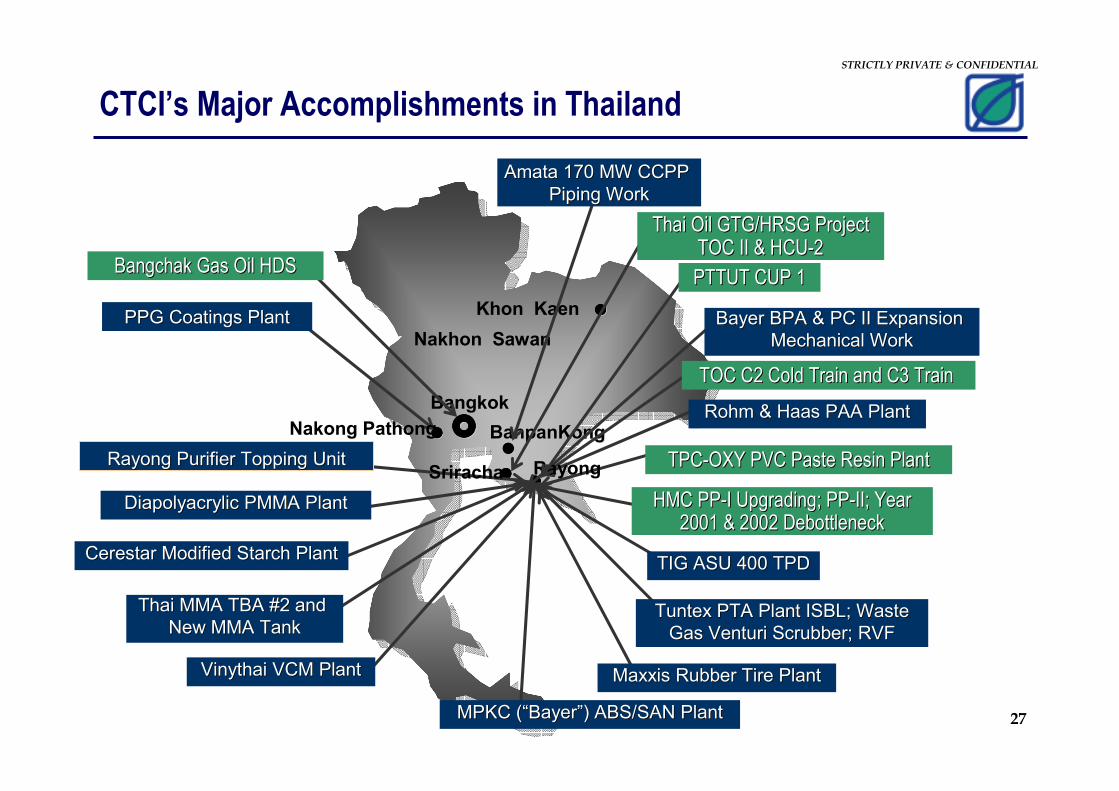

CTCI’s Major Accomplishments in Thailand

�������� BanpanKongBanpanKong��������

Nakhon Sawan

Bangkok

����������������

Khon Kaen ��������

��������

TOC C2 Cold Train and C3 Train TOC C2 Cold Train and C3 Train

VinythaiVinythai VCM PlantVCM Plant

MPKC (MPKC (““BayerBayer””) ABS/SAN Plant) ABS/SAN Plant

AmataAmata 170 MW CCPP 170 MW CCPP

Piping WorkPiping Work

Bayer BPA & PC II Expansion Bayer BPA & PC II Expansion

Mechanical WorkMechanical Work

TPCTPC--OXY PVC Paste Resin PlantOXY PVC Paste Resin Plant

HMC PPHMC PP--I Upgrading; PPI Upgrading; PP--II; Year II; Year 2001 & 2002 2001 & 2002 DebottleneckDebottleneck

TIG ASU 400 TPDTIG ASU 400 TPD

TuntexTuntex PTA Plant ISBL; Waste PTA Plant ISBL; Waste

Gas Gas VenturiVenturi Scrubber; RVF Scrubber; RVF

MaxxisMaxxis Rubber Tire PlantRubber Tire Plant

Bangchak Gas Oil HDSBangchak Gas Oil HDS

PPG Coatings PlantPPG Coatings Plant

Rayong Purifier Topping UnitRayong Purifier Topping Unit

DiapolyacrylicDiapolyacrylic PMMA PlantPMMA Plant

CerestarCerestar Modified Starch PlantModified Starch Plant

Thai MMA TBA #2 and Thai MMA TBA #2 and

New MMA TankNew MMA Tank

Rohm & Haas PAA PlantRohm & Haas PAA Plant

Rayong

Thai Oil GTG/HRSG ProjectThai Oil GTG/HRSG ProjectTOC II & HCUTOC II & HCU--22

PTTUT CUP 1PTTUT CUP 1

Nakong Pathong

Sriracha

28

STRICTLY PRIVATE & CONFIDENTIAL

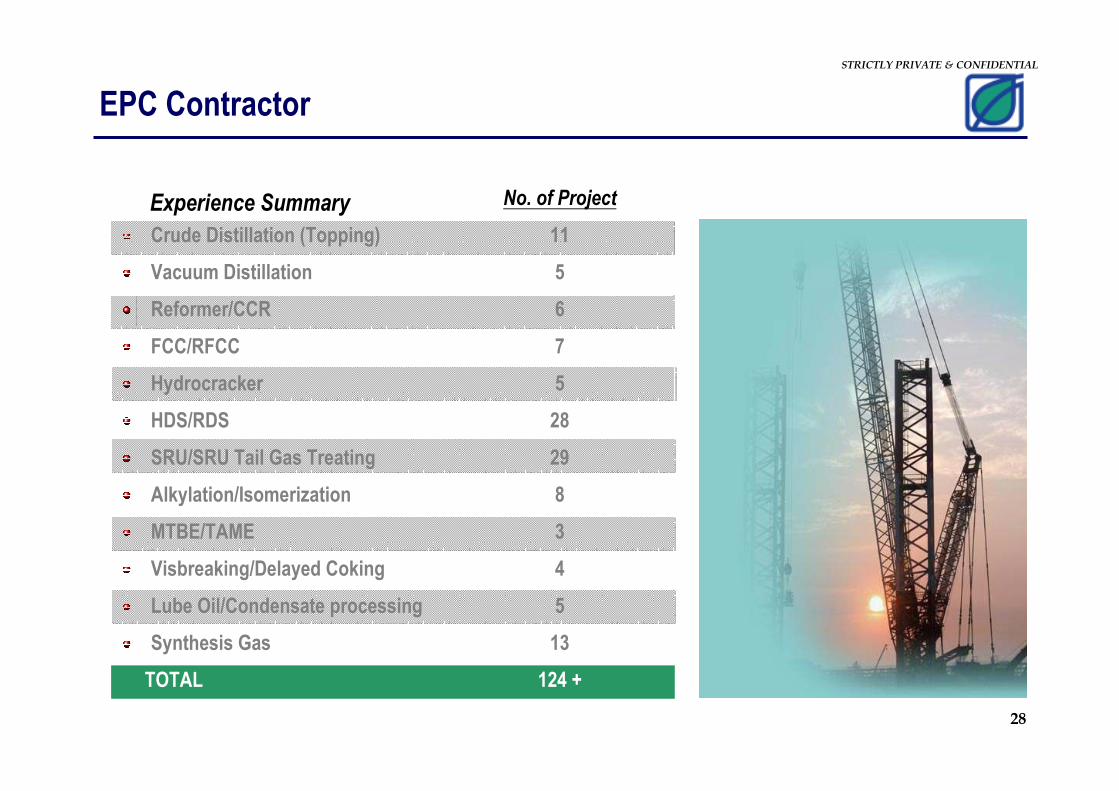

No. of Project

Crude Distillation (Topping) 11

Vacuum Distillation 5

Reformer/CCR 6

FCC/RFCC 7

Hydrocracker 5

HDS/RDS 28

SRU/SRU Tail Gas Treating 29

Alkylation/Isomerization 8

MTBE/TAME 3

Visbreaking/Delayed Coking 4

Lube Oil/Condensate processing 5

Synthesis Gas 13

TOTAL 124 +

Experience Summary

EPC Contractor

29

STRICTLY PRIVATE & CONFIDENTIAL

DOMESTIC

• E & C Engineering Corp.

• Advanced Control & Systems Inc.

• Resources Engineering Services Inc.

• CTCI Chemicals Corp.

• Sino Environmental Service Corp.

• KD Energy Corp.

• Leading Energy Corp.

• Envi Energy Recycling Corp.

• HD Resources Management Corp

• Fortune Energy Corp.

• Kuo Kuang Power Co., Ltd.

OVERSEAS

• CTCI (Thailand) Co. Ltd., Thailand

• Jing Ding Engineering &Construction Co. Ltd.,

Beijing, China

• Shang Ding Engineering &Construction Co. Ltd.,

Shanghai, China

• CIMAS Engineering Co., Ltd.,Vietnam

• CTCI Engineering & Construction Sdn. Bhd.,

Malaysia

• CIPEC Construction, Inc., Philippine

• CTCI Overseas Corporation Ltd.,Hong Kong

• CTCI Arabia Ltd., Saudi Arabia

• CTAS Corporation, USAEnergy & Resources Business

Operation

Major Subsidiaries & Affiliates

EPC Contractor (con’t)

30

STRICTLY PRIVATE & CONFIDENTIAL

ISO 9001ISO 9001ISO 9001ISO 9001

EPC Contractor (con’t)

31

STRICTLY PRIVATE & CONFIDENTIAL

Rewards

“Good Corporate Governance Report of

Thai Listed Companies 2005”

From Thai Institute of Directors (IOD)

(Top ten from 371 companies)

“Good Corporate Governance Report of

Thai Listed Companies 2005”

From Thai Institute of Directors (IOD)

(Top ten from 371 companies)

“Board of the year for Exemplary Practices”

from Thai Institute of Directors (IOD)

November 28, 2005

“Board of the year for Exemplary Practices”

from Thai Institute of Directors (IOD)

November 28, 2005

32

STRICTLY PRIVATE & CONFIDENTIAL

Rewards

“Best Corporate Governance Report”

in SET AWARDS 2005

July 18, 2005

“Best Corporate Governance Report”

in SET AWARDS 2005

July 18, 2005

“Best Corporate Social Responsibility”

in SET AWARDS 2006

July 26, 2006

“Best Corporate Social Responsibility”

in SET AWARDS 2006

July 26, 2006