the asset owners’ 02€¦ · horizon who can tolerate some volatility. however, the financial...

TRANSCRIPT

DECEMBER 2012

02 Background: the Endowment Model

04 Asset Allocation Trends

06 Liquidity Management Best Practices

10 Operational Challenges

13 Success Factors for Future Investing

The Asset Owners’ Perspective: Evolving Investment and Operational ModelsDuring the financial crisis, many asset owners discovered unexpected weaknesses in their investment portfolios, causing them to reconsider their asset allocation strategies. The endowment model of investing — a widely embraced method that includes increased allocations to alternative investment classes — was among the approaches that experienced challenges. While institutional investors continue to build on the foundation of the endowment model today, they are using their experiences from the crisis to change the way they approach the model and investing in general. A new emphasis on liquidity is at the forefront of investors’ priorities. They are also broadening asset allocation tools and focusing on risk management within investment portfolios. And, as investors seek to balance the need for liquidity with the need for returns, alterna-tives are playing a more vital role in portfolio construction.

State Street’s Vision Series distills our unique research, perspective

and opinions into publications for our clients around the world.

This is State Street

With $22.4 trillion in assets under custody and administration, and $1.9 trillion in

assets under management* as of June 30, 2012, State Street is a leading financial

services provider serving some of the world’s most sophisticated institutions.

We offer a flexible suite of services that spans the investment spectrum, including

investment management, research and trading, and investment servicing.

With operations in 29 countries serving clients in more than 100 geographic markets,

our global reach, expertise, and unique combination of consistency and innovation

help clients manage uncertainty, act on growth opportunities and enhance the value

of their services.

*This AUM includes the assets of the SPDR Gold Trust (approx. $66 billion as of June 30, 2012), for which State Street Global Markets, LLC, an affiliate of State Street Global Advisors, serves as the marketing agent.

THE ASSET OWNERS’ PERSPECTIVE: EVOLVING INVESTMENT AND OPERATIONAL MODELS • 1

THE ASSET OWNERS’ PERSPECTIVE: EVOLVING INVESTMENT AND OPERATIONAL MODELS • 1

Five years after the start of the crisis, State Street has undertaken a comprehensive study of institutional asset owners to explore new thinking around investment and operating models — including the endowment model — as well as challenges and opportunities related to data integration, talent management and technology. This paper outlines the findings of our research, including investors’ new strategies around asset allocation, continued reliance on alternative investments, approaches to liquidity management and manager selection. Using this insight and our own experience, this paper also delves into where portfolio management is headed and the actions asset owners must take to be successful in this new environment.

THE ASSET OWNERS’ PERSPECTIVE: EVOLVING INVESTMENT AND OPERATIONAL MODELS • 32 • VISION FOCUS

Pioneered by the world’s leading university endow-

ment programs at Harvard and Yale during the

1980s, the endowment model of investing played

a significant role in opening the doors to alternative

investing across the spectrum of institutional inves-

tors. By including allocations to alternative assets,

such as hedge funds, private equity and real estate,

the goal was to maintain a highly diversified port-

folio while limiting exposure to asset classes with

lower expected returns, such as fixed income. The

model gained deep traction, as other institutions

began to adopt its core tenets.

While this approach had a transformational influ-

ence on many institutional portfolios, investors were

surprised and disappointed by the high levels of

correlation between alternative assets and equity

markets during the most recent financial crisis. As

illustrated in Figure 1, nearly 84 percent of respon-

dents to our survey found that the financial crisis

exposed some weakness of the endowment model.

For example, during the crisis, some asset owners

found that the excessive amounts of leverage

inherent within the model made it difficult to

sustain this approach during a prolonged financial

downturn. Many asset owners faced liquidity chal-

lenges due to their high allocations to private

markets. Meanwhile, some were surprised at the

extent to which their portfolios were exposed to core

equity risk.

Despite these challenges, State Street’s research

found that the endowment model is still considered

a highly effective framework for today’s markets,

and a viable approach for investors with a long-term

horizon who can tolerate some volatility. However,

the financial crisis also changed the way investors

approach the model, as they are learning to better

estimate their own risk tolerance and liquidity needs,

as well as understand how to sufficiently diversify.

Figure 1: Did the financial crisis expose any weaknesses in the endowment model of investing, industry-wide?(All Respondents)

Background: the Endowment Model

A. 47% Yes, the crisis underscored fundamental weakness in liquidity and risk manage- ment for the endowment model

B. 37% The crisis may have exposed some slight weaknesses, but the endowment model of investing is still valid

C. 8% No, the crisis did not expose any weaknesses in the endowment model of investing

D. 9% Don’t know

A

B

C

D

Source: State Street 2012 Asset Owner Study

THE ASSET OWNERS’ PERSPECTIVE: EVOLVING INVESTMENT AND OPERATIONAL MODELS • 3

The 2012 Asset Owner Study, sponsored by State Street and conducted by Asset

International, was fielded online during July and August of 2012. A total of 116 responses

were received, with 84 percent of respondents located in the US and the remainder located

in Canada, Europe and Asia Pacific. We also spoke with 13 senior decision makers at 11

endowment, foundation and healthcare organizations in the US to gain additional insights.

About the Research

“I am still a big believer in the endowment model. I think it works better than everything else…but the two big

weaknesses that came out [of the crisis] are the two Ls – leverage and liquidity.”

– US private endowment investment manager

Respondents by Type Respondents by Investable Assets(Online Survey)

A. 49% Defined-Benefit Pensions

B. 43% Endowments, Foundations and Healthcare

C. 8% Other

A

B

C A. 12% Less than $100 million

B. 12% $100 million–$500 million

C. 16% $500 million–$1 billion

D. 29% $1 billion–$5 billion

E. 13% $5 billion–$10 billion

F. 16% More than $10 billion

G. 2% Did not disclose

A

B

C

D

E

F

G

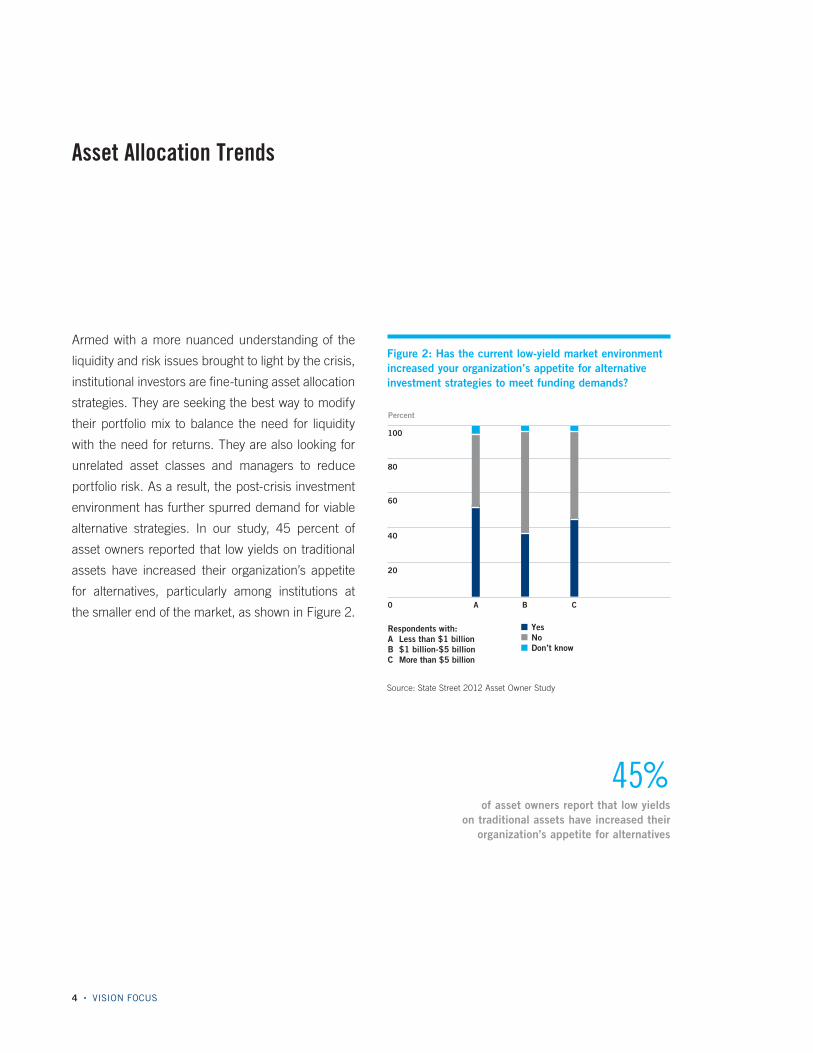

Armed with a more nuanced understanding of the

liquidity and risk issues brought to light by the crisis,

institutional investors are fine-tuning asset allocation

strategies. They are seeking the best way to modify

their portfolio mix to balance the need for liquidity

with the need for returns. They are also looking for

unrelated asset classes and managers to reduce

portfolio risk. As a result, the post-crisis investment

environment has further spurred demand for viable

alternative strategies. In our study, 45 percent of

asset owners reported that low yields on traditional

assets have increased their organization’s appetite

for alternatives, particularly among institutions at

the smaller end of the market, as shown in Figure 2.

4 • VISION FOCUS

Asset Allocation Trends

45%of asset owners report that low yields

on traditional assets have increased their organization’s appetite for alternatives

Figure 2: Has the current low-yield market environment increased your organization’s appetite for alternative investment strategies to meet funding demands?

100

80

60

40

0

Respondents with:A Less than $1 billionB $1 billion-$5 billionC More than $5 billion

CBA

Percent

20

Yes No Don’t know

Source: State Street 2012 Asset Owner Study

The shift toward alternatives is not the only signifi-

cant trend. Pension funds are increasingly employing

strategies, such as liability-driven investing or

LDI, which focuses on managing the portfolio for

outcome versus the liabilities, rather than asset-only

returns. As a result, many are also adding to fixed

income positions to better align with liability streams.

Among defined-benefit (DB) pension plans, 39

percent of corporate plans expect to increase

allocations to corporate investment-grade debt in

the coming year, likely to better align the asset

portfolio to the liability discount rate. Meanwhile, 30

percent of public plans anticipate expanding alloca-

tions to emerging-market debt investments in the

coming year, which indicates they are looking for

higher return.

A New Mindset

While some major shifts are taking place in institu-

tional asset allocation decisions post-crisis, another

hallmark of the post-crisis environment is a shift

away from thinking about a portfolio in terms of

traditional asset classes and toward a focus on

the underlying exposures, or factors. For many,

the “factor model” approach is a more useful way

to achieve a holistic view of a portfolio’s alpha

sources and risk exposures. However, investment

managers are still largely organized around asset

class, creating challenges for practitioners of the

factor model.

THE ASSET OWNERS’ PERSPECTIVE: EVOLVING INVESTMENT AND OPERATIONAL MODELS • 5

“We don’t have asset classes. We don’t have large growth, large value, bonds, equity. We have momen-

tum growth, duration spread, liquidity. So our model is a little different, and we hedge too so we look at

exposures we don’t like and hedge them out.”

– US endowment

“In Australia, we follow a static strategic asset allocation approach. It has been found very wanting. Funds focus on peer risk and relative outcomes, not

on meeting investor needs.”

– Australian public pension fund

6 • VISION FOCUS

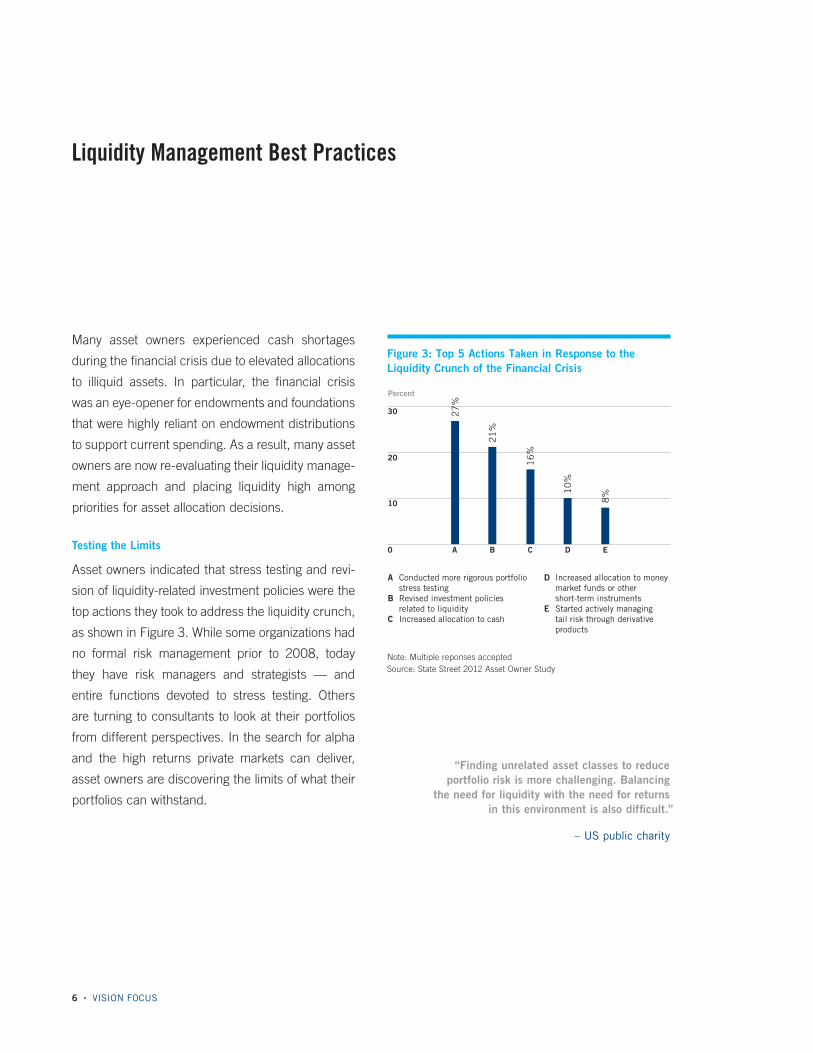

Many asset owners experienced cash shortages

during the financial crisis due to elevated allocations

to illiquid assets. In particular, the financial crisis

was an eye-opener for endowments and foundations

that were highly reliant on endowment distributions

to support current spending. As a result, many asset

owners are now re-evaluating their liquidity manage-

ment approach and placing liquidity high among

priorities for asset allocation decisions.

Testing the Limits

Asset owners indicated that stress testing and revi-

sion of liquidity-related investment policies were the

top actions they took to address the liquidity crunch,

as shown in Figure 3. While some organizations had

no formal risk management prior to 2008, today

they have risk managers and strategists — and

entire functions devoted to stress testing. Others

are turning to consultants to look at their portfolios

from different perspectives. In the search for alpha

and the high returns private markets can deliver,

asset owners are discovering the limits of what their

portfolios can withstand.

“Finding unrelated asset classes to reduce portfolio risk is more challenging. Balancing

the need for liquidity with the need for returns in this environment is also difficult.”

– US public charity

Liquidity Management Best Practices

Figure 3: Top 5 Actions Taken in Response to the Liquidity Crunch of the Financial Crisis

Note: Multiple reponses accepted Source: State Street 2012 Asset Owner Study

30

20

10

0

A Conducted more rigorous portfolio stress testingB Revised investment policies related to liquidityC Increased allocation to cash

D Increased allocation to money market funds or other short-term instrumentsE Started actively managing tail risk through derivative products

D

10

%

E

8%

C

16

%

B

21

%

A

27

%

Percent

0

10

20

30

THE ASSET OWNERS’ PERSPECTIVE: EVOLVING INVESTMENT AND OPERATIONAL MODELS • 7

No perfect combination of liquid and illiquid assets

exists that is suitable for all investors. The optimal

mix depends on an investor’s time horizon as well

as any explicit liabilities, and can also be specified

based upon cash flow analysis and risk-adjusted

return analysis. Typically both historical analysis

and forward-looking analysis should be conducted

to stress test the performance of different asset

class combinations over various economic and

market conditions.1

Key Liquidity Strategies

The new emphasis on liquidity has prompted the

availability of a wide array of liquidity management

solutions. We went to the experts at State Street

Global Advisors (SSgA) — State Street’s asset

management business — to better understand

what options are available, and they identified four

broad approaches they use with investors:

1 Strategic Balanced Strategy: The objective of

this approach is to reduce cash drag related

to the myriad cash accounts and exposures

that asset owners may have, including benefit

payments, routine expenses or buffers against

unanticipated cash needs. Using liquid commin-

gled vehicles, a custom balanced strategy can

be created to attempt to mirror the overall

asset allocation of an entity’s strategic mix.

Funded from actual cash assets, this approach

does decrease assets available for other under-

lying managers. However, it also makes the

liquidity manager the central point of contact for

cash needs.

This approach may best fit: Asset owners who

are concerned about the effect of cash drag

on their portfolio, but are hesitant or prohibited

from using derivatives.

2 Dynamic Balanced Strategy: This strategy adopts

a holistic view of the portfolio. Cash is invested

in the asset class most underweight at the total

portfolio level versus policy. In this way, the

strategy addresses cash drag and minimizes the

variance of overall returns relative to the portfo-

lio’s strategic asset allocation. The logistical and

operational transfer of information is established

to provide a picture of the total portfolio (at the

manager or asset class level) without having

look-through into the actual positions held by

active managers.

This approach may best fit: Asset owners

who are concerned about cash drag, are sensi-

tive to tracking error and are reluctant to

use derivatives.

3 Cash Overlay: Cash overlay programs, similar to

the dynamic balanced strategy, are designed to

alleviate cash drag and minimize tracking error

while facilitating periodic cash flows without

disrupting underlying manager positions. The

key difference is that derivatives are added to

the mix, and the liquidity management program

no longer needs to be fully funded with cash

assets. Investors may designate which cash

accounts are considered part of the overlay

and move just enough cash to satisfy initial and

daily variation margin. Cash overlay strategies

increase flexibility, limit exposure to long only,

and can help equitize underlying manager cash

and receivables.

1 Marino, Stacy L., “Managing Liquidity Needs in a Changing Market,” State Street Global Advisors, 2011.

8 • VISION FOCUS

This approach may best fit: Asset owners who

want to gain market exposure with manager

cash positions and increase flexibility to meet

unexpected cash flows, or those who are looking

to restructure their manager mix, as managers

can be removed without losing market exposure.

4 Strategic Overlay: Strategic overlay programs

go beyond simpler cash overlays by creating a

more flexible structure that can go both long and

short, thereby expanding its potential uses to

include cash equitization, strategic rebalancing,

portable alpha, duration extension and tactical

asset allocation. This approach can help cover

any cash overlay needs and facilitate the rebal-

ancing function of the total portfolio.

This approach may best fit: Asset owners with

relatively sophisticated portfolios — including

numerous active managers — who are seeking

a way to streamline both liquidity management

and broad oversight of the portfolio.

Liquidity and Portfolio Choice

One of the biggest challenges asset owners

face as they navigate uncertain markets is being able

to properly account for liquidity when constructing a

portfolio. New research by State Street Associates,

State Street’s research partnership with academia

and industry, can help institutional investors

value liquidity and incorporate it into asset

allocation decisions.2

Traditional portfolio construction frameworks, which

focus on optimizing the trade-off between risk

and return, do not explicitly address liquidity. As a

result, over-allocation to illiquid asset classes is an

inherent risk. Some investors attempt to correct this

by assigning liquidity scores to individual investment

types in their portfolio. Parameters are then set so

that the combined weighted average liquidity score

of the portfolio may not exceed a predetermined

value. However, given the divergent identities and

needs of asset owners, the liquidity score method

can prove too simplistic of a framework to achieve

the desired effect.

2 Kinlaw, William B.; Kritzman, Mark; and Turkington, David, “Liquidity and Portfolio Choice: A Unified Approach,” Forthcoming in the Journal of Portfolio Management, 2012.

Figure 4: Comparing Liquidity Management Strategies

Liquidity Management FeatureStrategic

Balanced StrategyDynamic

Balanced Strategy Cash Overlay Strategic Overlay

Takes Long and Short Positions x

Securitizes Manager Cash x x

Reduces Tracking Error x x x

Mitigates Cash Drag x x x x

Source: State Street Global Advisors

State Street Associates’ research suggests that it is

natural to think of liquidity as a shadow allocation.

Whenever investors employ liquidity to improve

upon a portfolio’s expected utility, they should

attach a shadow asset to tradable assets to reflect

that benefit. Alternatively, when investors deploy

liquidity to prevent a portfolio’s expected utility

from falling — as in the case of rebalancing, for

example — they should attach a shadow liability

to non-tradable assets to reflect the illiquidity cost

those assets entail. The expected return and risk

of the shadow illiquidity allocation depends on how

a particular investor exploits liquidity. By casting

liquidity in units of expected return and risk, this

approach allows institutional investors to analyze

liquidity in the same context as other investment

decisions and to expand upon existing portfolio

allocation techniques.

Liquidity imparts different benefits to different inves-

tors, such as the ability to rebalance a portfolio,

meet capital calls at times of market illiquidity,

exercise market timing skills, allocate funds to new

investment opportunities and respond to shifts in

risk appetite. These benefits can be measured and

expressed in units of expected return and risk to

help investors make more efficient decisions on

portfolio choice. Correcting expected returns for

liquidity in this manner provides a powerful analyt-

ical framework for making asset allocation decisions

involving illiquid investment strategies.

Case Study: Optimal Asset Allocations

*We assume a risk aversion of 2. For the multiple funds scenario, we assume that hedge funds and private equity each consist of 10 managers, and reduce the expected return of both asset classes by 0.70 percent to reflect the multi-fund return impact that results from performance fees.

Source: Kinlaw, William B.; Kritzman, Mark; and Turkington, David, “Liquidity and Portfolio Choice: A Unified Approach,” Forthcoming in the Journal of Portfolio Management, 2012.

Regardless of the extent to which they revised

liquidity and risk management practices after the

financial crisis, today’s asset owners are devoting

more attention to these topics, particularly at the

board level. Boards and investment committees

are focusing on liquidity and risk, considering

whether they need new policies to address these

concerns, and requesting more detailed reporting

than ever before. More than three-quarters

(76 percent) of the asset owners in our study

reported that demands from internal governance

and risk management functions pose a challenge

for their organizations.

THE ASSET OWNERS’ PERSPECTIVE: EVOLVING INVESTMENT AND OPERATIONAL MODELS • 9

76%of asset owners report demands from internal

governance and risk management functions pose challenges for their organizations

35

%4

7%

56

%

A

20

% 25

% 28

%

B

25

%1

4%

7%

C

20

%1

4%

10

%

D

A EquitiesB Fixed Income

C Hedge FundsD Private Equity

70

60

50

40

30

20

10

0

Title

Percent

■ Ignoring liquidity■ Accounting for liquidity, single funds■ Accounting for liquidity, multiple funds*

THE ASSET OWNERS’ PERSPECTIVE: EVOLVING INVESTMENT AND OPERATIONAL MODELS • 1110 • VISION FOCUS

Among the operational challenges for asset owners

in today’s complex market, the issue of data inte-

gration is at the forefront. Nearly half (46 percent) of

asset owners rated their ability to achieve a compre-

hensive look-through of their portfolio across all

security types and investment structures as less

than good, as illustrated in Figure 5. Institutions

are also not optimistic about what the future holds.

Over the next three years, almost two-thirds (63

percent) of asset owners expect their data manage-

ment challenges to increase.

More extensive investment in alternatives has

contributed to concerns around data integration.

Asset owners reported that increased complexity

stemming from alternative asset classes is a key

factor, with nearly one-third (31 percent) citing it

as “significant.”

With respondents reporting that their biggest

data challenges are risk exposure and investment

costs, as shown in Figure 6, some owners say

that managers lack of disclosure compromises

their ability to integrate data, especially at the hold-

ings level.

Operational Challenges

Figure 5: How would you rate your ability to integrate data from disparete sources to achieve a comprehensive “look-through” of your portfolio across all security types and investment structures?(All Respondents)

All

0Percent

Very poor Somewhat poor

Corp DB

Public DB

E&F

5% 13% 28% 41% 13%

6% 11% 26% 49% 9%

7% 14% 29% 25% 25%

14% 32% 50% 5%

20 40 60 80 100

Fair Good

Excellent

Source: State Street 2012 Asset Owner Study

THE ASSET OWNERS’ PERSPECTIVE: EVOLVING INVESTMENT AND OPERATIONAL MODELS • 11

Data management is an overall industry challenge.

While potential relief may be found in new tech-

nologies that help investors consider risk factors

and exposures, asset owners remain concerned

that the problem will worsen as markets become

more complex.

Mind the Talent Gap

Our research revealed that, just as asset owners

are considering their portfolios more holistically

today, they are also looking at talent from new

perspectives — closely examining the types of skills,

expertise and characteristics they require for port-

folio construction and manager selection. According

to the asset owners we surveyed, acquiring and

retaining talent in several key areas is a significant

challenge. A new set of expectations has replaced

the old when it comes to the selection and manage-

ment of external asset managers and other service

providers. These new priorities have refocused

asset owners’ attention as they go forward.

Not only do investors need to hire effective external

managers, they also must build and nurture the

internal talent necessary to ensure they are well

positioned for the future. As illustrated in Figure

7, asset owners cite investment management, risk

management and investment operations as the

areas of greatest challenge in the search for expe-

rienced staff members. In addition, the balance

between generalists and specialists within an orga-

nization is paramount to securing deep knowledge

within each investment type, while retaining requi-

site talent to allocate effectively across strategies.

Figure 6: Asset Owners’ Insight into Risk and Cost (All Respondents)

Two-thirds of asset owners expect data management challenges to increase

Our organization has access to portfoilio investment data that:

A Allows us to understand our total risk exposureB Provides insight into all investment costs

0Percent

Strongly disagree Somewhat disagree

A

B4% 12% 24% 34% 26%

2% 18% 25% 37% 18%

20 40 60 80 100

Neutral Somewhat agree

Strongly agree

Source: State Street 2012 Asset Owner Study

12 • VISION FOCUS

Manager Selection Tools

While asset owners may struggle to acquire talent

in certain key areas, new tools and technologies

are emerging that support the manager selection

process, such as the increased use of technology

and consultative advice. Rather than substituting

for traditional face-to-face due diligence discussions

with managers, these tools are complementary.

Today, sophisticated asset owners are leveraging

more sophisticated quantitative tools when selecting

managers. For example, using a bespoke quantita-

tive methodology, State Street Associates examines

managers’ historical returns throughout different

risk regimes, performing the analysis blindly (i.e.,

with no indication of the managers’ identities). Asset

owners can then determine whether a given manag-

er’s performance is truly aligned with their portfolio

objectives, and if the manager is providing adequate

diversification benefits. This due diligence makes it

easier to assess whether investment managers are

truly “earning their keep,” or whether a portion of

the portfolio could perhaps be replicated in a less

expensive manner. It is also important for asset

owners to truly understand how their managers

generate returns, and to seek diversification along

those lines, as well as by simple style boxes.

Regardless of the manager selection approach,

asset owners must remain in charge of all aspects of

their manager relationships. Adequate due diligence

of managers’ operations has also become increas-

ingly important. This is a key challenge for many

asset owners who realized during the crisis that

they did not have the level of control over manager

relationships they once thought. For example, asset

owners should have confidence that they under-

stand the legal documents associated with all asset

management relationships — an administrative but

highly important task that will equip them with the

information they need to successfully manage these

key relationships.

Figure 7: Does your organization experience difficulty in hiring knowledgeable, qualified staff in any of the following areas?

30

20

10

0

A Investment managementB Risk managementC Investment operations

D Asset allocation E TechnologyF Other

D

14

%

E

9%

C

15

%

B

22

%

A

23

%

Percent

0

10

20

30

F

4%

Note: Multiple reponses accepted Source: State Street 2012 Asset Owner Study

THE ASSET OWNERS’ PERSPECTIVE: EVOLVING INVESTMENT AND OPERATIONAL MODELS • 13

Five years after the crisis began, asset owners are still

incorporating lessons learned from that period, and

the continuing volatility and uncertainty is allowing

them to test the validity of these new investment

approaches. For example, while alternatives remain

instrumental investments for institutions seeking to

achieve above-market returns, asset owners know

that effective use of alternatives requires the right

oversight, staff and understanding.

Asset owners have also renewed their focus post-

crisis on risk management and liquidity. Going

forward, thoughtful institutions will continue to work

to incorporate a true understanding of liquidity and

an ability to effectively review investment decisions

from both risk and return perspectives. Central to

that understanding is an acknowledgement that

illiquid investments come with an opportunity cost.

The key is recognizing whether the return is worth

the cost within the context of the entire portfolio.

To be successful, a more holistic approach to

portfolio management is required. Proactively

constructing portfolios to maintain performance

that supports long-term objectives is one part of the

equation. Asset owners should consider allocating

to alternatives as a diversification strategy, as well as

one to gain returns. In addition, effective manage-

ment of external asset manager and consultant

relationships is critical. Asset owners are already

recognizing the necessity of hiring the right internal

and external talent to select and conduct appro-

priate due diligence of external resources.

Operational issues are another area of ongoing

concern for institutional investors. More widespread

use of the factor model in portfolio construction

has further accelerated institutions’ desire for data

integration, as they attempt to understand how each

factor of an investment strategy affects results.

A key challenge lies in extracting this data from

external managers and consultants and integrating

it successfully to satisfy risk management needs.

Going forward, other influences, such as regulation

and increased automation — particularly within the

realm of alternative assets — will continue to affect

data demands.

To successfully meet ongoing challenges in the

post-crisis landscape, asset owners can partner

with third-party service providers in a number of

areas, including liquidity and risk management,

asset manager selection, and data collection and

integration. While technology can be brought to

bear in each of these areas, the necessity of

human interaction and involvement also remains

an important element. High-touch service providers

who have mastered all of the requisite skills to help

institutions effectively navigate this ever-changing

investment environment will emerge as the partners

of choice for asset owners.

Success Factors for Future Investing

Design and production by State Street Global Marketing ©2012 STATE STREET CORPORATION CORP-0617 12-15725-1112

State Street Corporation

State Street Financial Center

One Lincoln Street

Boston, Massachusetts 02111–2900

+1 617 786 3000

www.statestreet.com

NYSE ticker symbol: STT

This material is for your private information. The views expressed are the views of State Street and are subject to change based on market and other conditions and factors. The opinions expressed reflect general perspectives and information, are not tailored to specific circumstances, and may differ from those with different investment philosophies. The information we provide does not constitute investment advice or other recommendations and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security or to pursue any trading or investment strategy. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon, and individuals should evaluate and assess this material independently in light of those circumstances. We encourage you to consult your tax or financial advisor. All material, including information sourced from or attributed to State Street, has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. Past performance is no guarantee of future results. In addition, forecasts, projections, or other forward-looking statements or information, whether by State Street or third parties, are similarly not guarantees of future performance, are inherently uncertain, are based on assumptions at the time of the statement that are difficult to predict, and involve a number of risks and uncertainties. Actual outcomes and results may differ materially from what is expressed in those statements. State Street makes no representation or warranty as to the accuracy of, nor shall it have any liability for decisions or actions based on, the material, forward-looking statements and other information in this communication. State Street does not undertake and is under no obligation to update or keep current the information or opinions contained in this communication. This communication is directed at Professional Clients (this includes Eligible Counterparties as defined by the Financial Services Authority) who are deemed both Knowledgeable and Experienced in matters relating to investments. The products and services to which this communication relates are only available to such persons, and persons of any other description (including Retail Clients) should not review or rely on this communication. The information contained within this marketing communication has not been prepared in accordance with the legal requirements of Investment Research. As such this document is not subject to any prohibition on dealing ahead of the dissemination of Investment Research. Generally, among asset classes, stocks are more volatile than bonds or short-term instru-ments. Government bonds and corporate bonds generally have more moderate short-term price fluctuations than stocks, but provide lower potential long-term returns. US Treasury Bills maintain a stable value if held to maturity, but returns are generally only slightly above the inflation rate.

For questions or comments about our Vision

series, e-mail us at [email protected].

Contact Information

If you have questions regarding State Street’s services and

capabilities for asset owners, please contact:

Daniel Farley

State Street Global Advisors

+1 617 664 3319

Will Kinlaw

State Street Associates

+1 617 234 9496

Rebecca Schechter

State Street Global Services

+1 617 664 0964