the agenda

DESCRIPTION

SMM Press Conference 8 th Sept 2014 World Shipbuilding Dr Professor Martin Stopford Managing Director, Clarkson Research. The Agenda. Shipyards surviving better than expected. Wow, it says I’m going to make $ billions. Shipping Market Trends World Economy & Ship Demand - PowerPoint PPT PresentationTRANSCRIPT

CLARKSON RESEARCH SERVICES LTD

SMM Press Conference 8th Sept 2014

World ShipbuildingDr Professor Martin Stopford

Managing Director, Clarkson Research

CLARKSON RESEARCH SERVICES LTD

“This is turning into a long shipping recession. Meanwhile the increase in fuel costs and regulatory standards presents the biggest technical challenge for fifty years”

Shipyards surviving

better than expected

1. Shipping Market Trends2. World Economy & Ship Demand3. Newbuilding Contracts & Future Supply4. Shipyard Capacity & Orderbook5. Regional Shipbuilding Trends6. Energy, Environment & Innovation

CLARKSON RESEARCH SERVICES LTD

Recession now in year 6 and still

searching for light at the end

of the tunnel

CLARKSON RESEARCH SERVICES LTD

0

5

10

15

20

25

30

35

40

45

5019

93

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

Cla

rkse

a In

dex

$000

/day

(Clarksea Index shows weighted average earnings of tankers, bulkers, containerships & gas.)

2004$39,000/day

2008$50,000/day

2000$24,000/

day

$8,500/day$12,000/day

Chart 1: Shipping Market Earnings 1993-2014

$12,145/day

$27,178/day

Earnings are NOT adjusted for inflation

CLARKSON RESEARCH SERVICES LTD

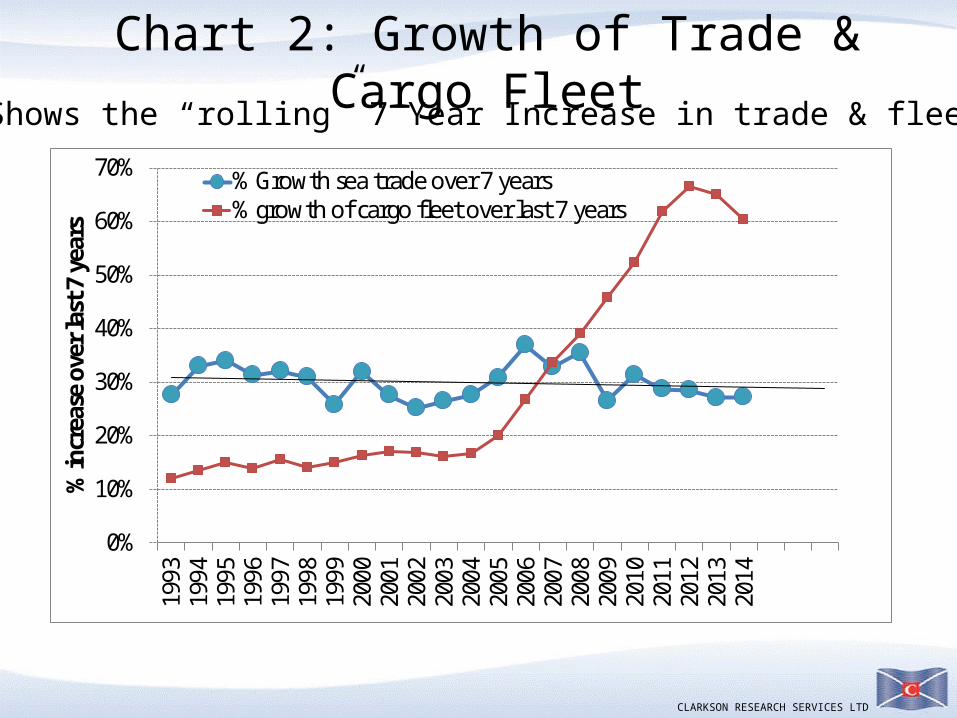

Chart 2: Growth of Trade & Cargo Fleet

0%

10%

20%

30%

40%

50%

60%

70%19

9319

9419

9519

9619

9719

9819

9920

0020

0120

0220

0320

0420

0520

0620

0720

0820

0920

1020

1120

1220

1320

14

% in

crea

se o

ver l

ast 7

yea

rs

% Growth sea trade over 7 years% growth of cargo fleet over last 7 years

Shows the “rolling” 7 Year Increase in trade & fleet

World Fleet grows faster than trade

Sea trade steady at 4%

growthFleet grows slower than trade

CLARKSON RESEARCH SERVICES LTD

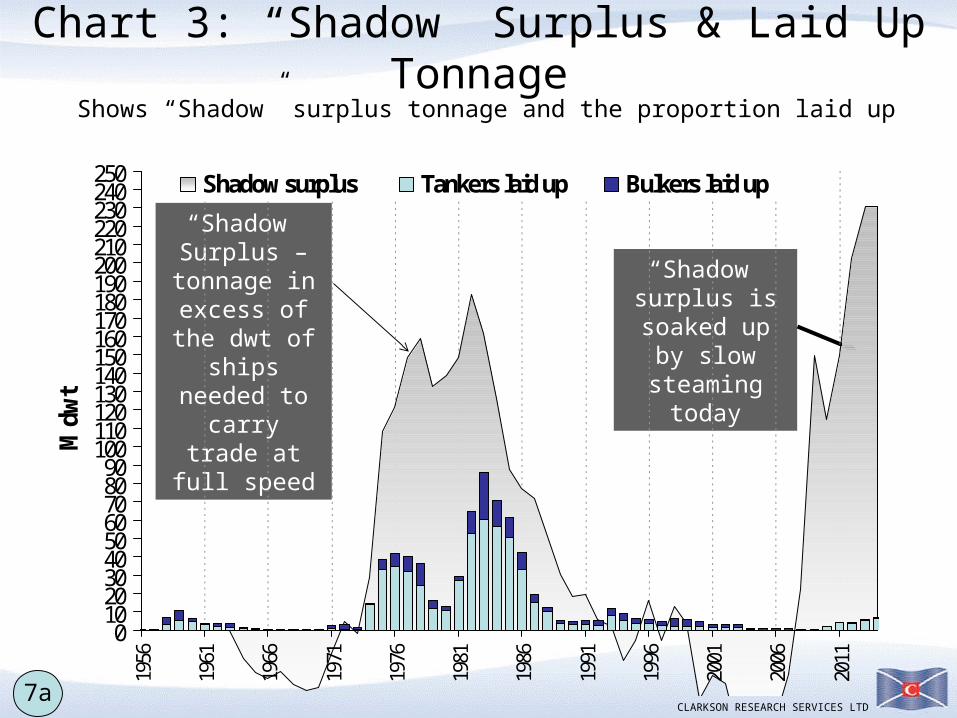

Chart 3: “Shadow” Surplus & Laid Up Tonnage

0102030405060708090

100110120130140150160170180190200210220230240250

1956

1961

1966

1971

1976

1981

1986

1991

1996

2001

2006

2011

M d

wt

Shadow surplus Tankers laid up Bulkers laid up

Shows “Shadow” surplus tonnage and the proportion laid up

“Shadow” surplus is

soaked up by slow steaming

today

“Shadow” Surplus – tonnage in

excess of the dwt of ships needed to

carry trade at full speed

7a

CLARKSON RESEARCH SERVICES LTD

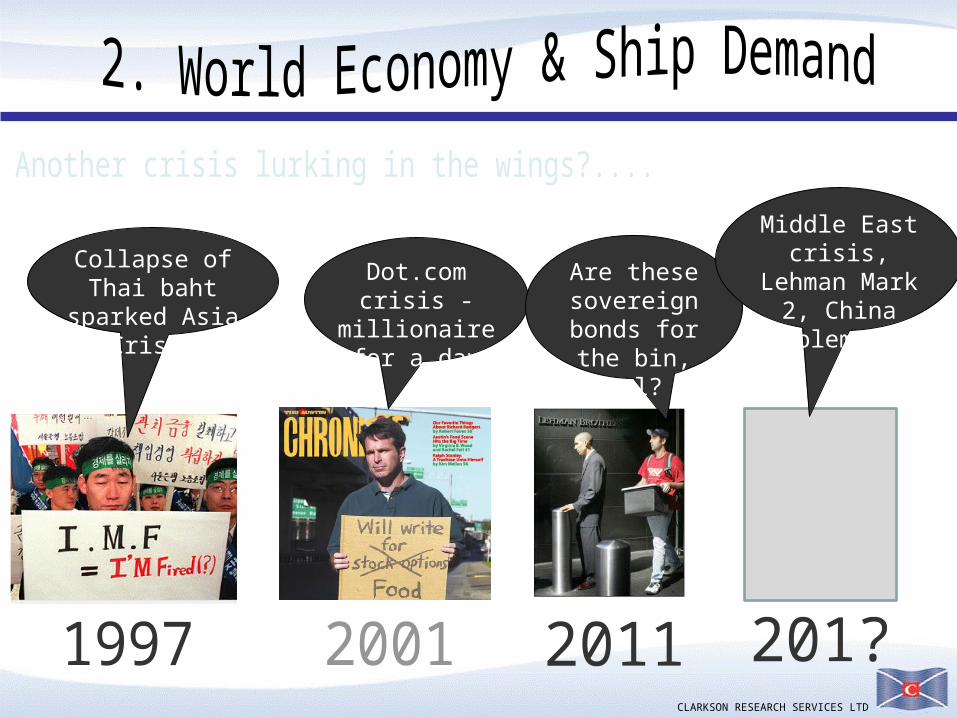

Dot.com crisis - millionaire for

a day

Are these sovereign

bonds for the bin, pal?

Collapse of Thai baht sparked Asia Crisis

Middle East crisis, Lehman Mark 2, China problems???

CLARKSON RESEARCH SERVICES LTD

-10%-8%-6%-4%-2%0%2%4%6%8%

10%12%14%

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

Chart 4: World GDP & Sea Trade GrowthWorld GDP (red line) and sea trade (blue line)

Crisis 11973

1st Oil Crisis

2001Dot.com

crisis

Crisis 219792nd OilCrisis

1991 Financial

Crisis

1997Asia Crisis

Crisis 62007

Credit Crisis

% change Oil Crisis

Credit Crisis

?

The sea trade

growth trend is 3.8% pa

CLARKSON RESEARCH SERVICES LTD

I LOVE ordering

new ships

I ‘ve really gone off

ordering ships

I should never have ordered those bulkers

Loan

I made millions ordering against

timecharters

One of those nice shipyards arranged some

credit, sir

2

CLARKSON RESEARCH SERVICES LTD

Chart 5: Shipbuilding Orders 1963-2014

020406080

100120140160180200220240

1963

1965

1967

1969

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

Millio

nDW

T De

liver

ies

Source Maritime Economics 3rd Ed Martin Stopford (Updated August 2012)

OrdersOrders in 2013 for 169.7m dwt was the 3rd highest

ever!

15

CLARKSON RESEARCH SERVICES LTD

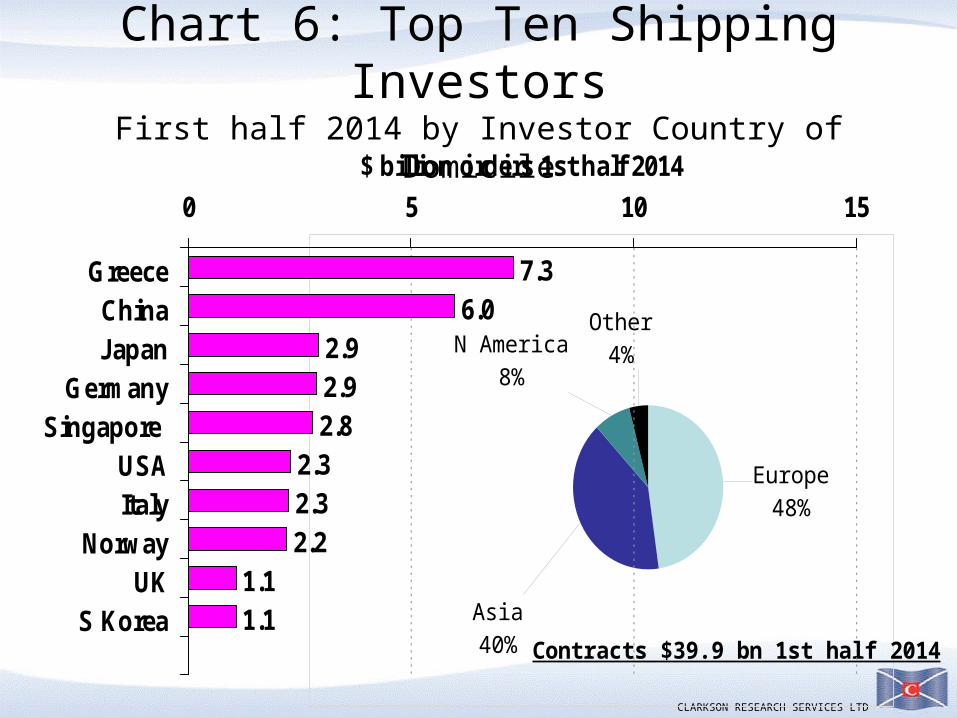

Chart 6: Top Ten Shipping InvestorsFirst half 2014 by Investor Country of Domicile

7.36.0

2.92.92.8

2.32.32.2

1.11.1

0 5 10 15

GreeceChinaJapan

GermanySingapore

USAItaly

NorwayUK

S Korea

$ billion orders 1st half 2014

Europe48%

Asia40%

N America8%

Other4%

Contracts $39.9 bn 1st half 2014

CLARKSON RESEARCH SERVICES LTD

The shipyards are winding down from the biggest boom ever, but

sales still active and volatile . Marine

equipment sales about $70 bn in 2013, up 30%

from $53 bn in 2012Marine equipment market busy with eco-ships

CLARKSON RESEARCH SERVICES LTD

Chart 7: The Shipbuilding Cycle

0

20

40

60

80

100

120

140

160

180

1963

1967

1971

1975

1979

1983

1987

1991

1995

1999

2003

2007

2011

2015

Million DwtShipyards adjust capacity downwards after 2000s boom

Deliveries

Tankers; 21.4; 20%

Bulkers; 62.8; 58%

Containers; 15.9; 15%

Offshore; 2.2; 2% Other; 5.6; 5%

2013 Deliveries m dwt

In 2010 deliveries peaked at 169m dwt

Forecast106 m dwt

in 2015

Demolition

CLARKSON RESEARCH SERVICES LTD

Chart 8: Number of Active Shipyards

677637 618 625

664 696759

808

907983

11231168

10201098

696

918

0100200300400500600700800900

100011001200

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Num

ber o

f Yar

ds

Source: Clarkson Research

CLARKSON RESEARCH SERVICES LTD

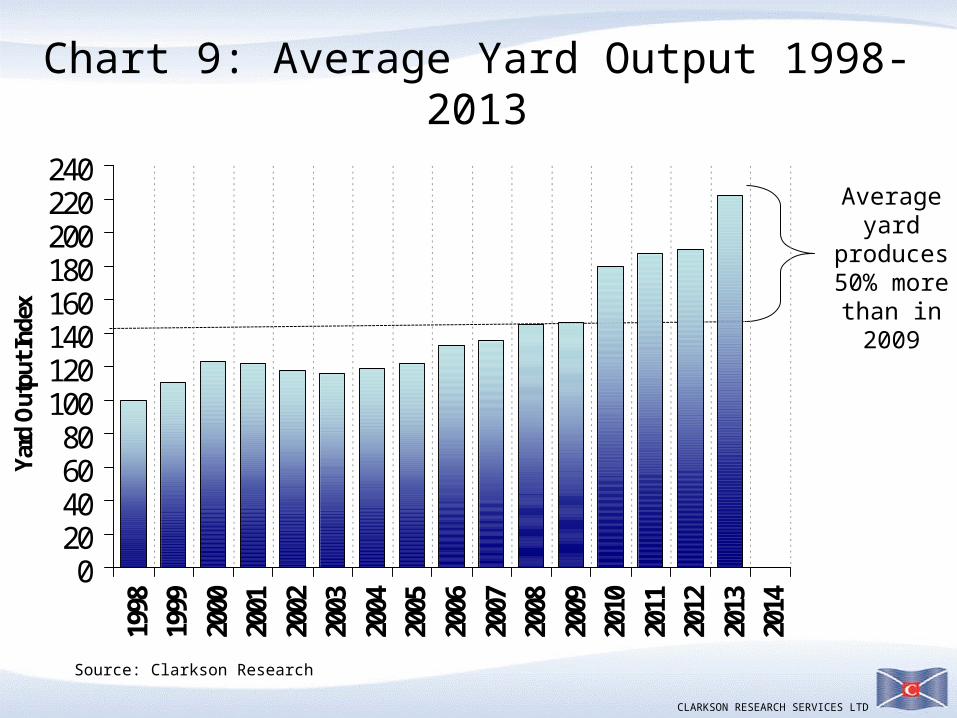

Chart 9: Average Yard Output 1998-2013

020406080

100120140160180200220240

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Yard

Out

put I

ndex

Average yard

produces 50% more

than in 2009

Source: Clarkson Research

CLARKSON RESEARCH SERVICES LTD

Chart 10: World Cargo Ship Demolition

0

10

20

30

40

50

60

7019

73

1976

1979

1982

1985

1988

1991

1994

1997

2000

2003

2006

2009

2012

0%

1%

2%

3%

4%

5%

6%

7%

8%

Shows the demolition (bars) on left axis & % fleet demolished on right

Million Dwt % fleet

M Dwt demolished in year (left

axis)

% cargo fleet scrapped

(right axis)

CLARKSON RESEARCH SERVICES LTD

China and S Korea “neck & neck” for top

position

CLARKSON RESEARCH SERVICES LTD

0

10

20

30

40

50

60

70

80

90

10019

0319

0819

1319

1819

2319

2819

3319

3819

4319

4819

5319

5819

6319

6819

7319

7819

8319

8819

9319

9820

0320

0820

13

% to

tal s

hips

laun

ched

Source; Lloyds Register of Shipping, Clarkson Research

FIGURE 15.1 Shipbuilding market shares 1902-2013

Korea

Japan

EuropeBritain

other countries

Scandin-avia

USA China

See: page 616

Chart 11: Regional Shipbuilding Shares 1903-2013

CGT35.9%GT35.4%

CGT33.8%GT35%

CGT18.4%GT20.4%

GT1.7%

CLARKSON RESEARCH SERVICES LTD

www.clarksons.com 19August 2014

Bulker Tanker Containership Gas Offshore Other Total

Builder M.CGT M.CGT M.CGT M.CGT M.CGT M.CGT M.CGT

China P.R. 7.8 1.4 1.8 0.2 0.9 1.1 13.3

S. Korea 1.4 3.5 4.8 1.6 0.7 0.5 12.5

Japan 5.1 0.6 0.3 0.3 0.1 0.6 6.8

Philippines 0.4 0.0 0.1 0.0 0.6

Norway 0.3 0.0 0.4

Vietnam 0.2 0.0 0.1 0.0 0.3

Germany 0.0 0.3 0.3

Taiwan 0.3 0.0 0.3

USA 0.0 0.2 0.2

France 0.2 0.2

Other 0.1 0.3 0.1 0.0 1.0 0.6 2.2

Total 15.1 5.8 7.3 2.1 3.2 3.5 37.0

Chart 12: 2013 Shipyard Output by Country2013 Output by Country and Ship Type

CLARKSON RESEARCH SERVICES LTD

• After 30 years of technical stability shipping faces technical challenge

• The key issues are:_– Bunker price

escalation– Regulations & carbon

footprint

CLARKSON RESEARCH SERVICES LTD

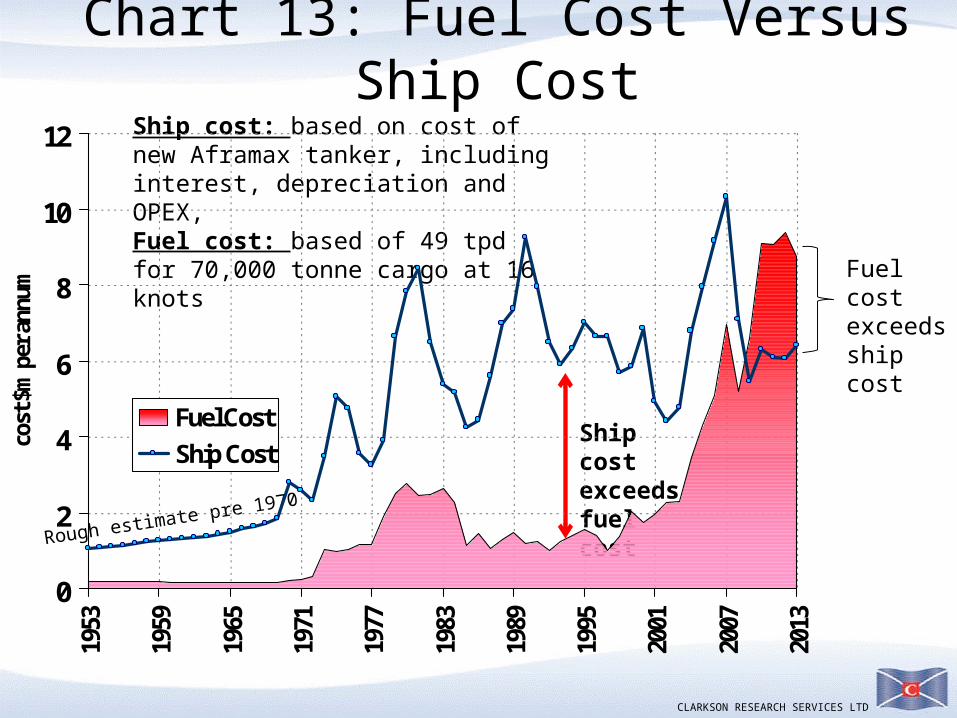

Chart 13: Fuel Cost Versus Ship Cost

0

2

4

6

8

10

12

1953

1959

1965

1971

1977

1983

1989

1995

2001

2007

2013

cost

$m

per

ann

um

Fuel Cost

Ship Cost

Ship cost: based on cost of new Aframax tanker, including interest, depreciation and OPEX, Fuel cost: based of 49 tpd for 70,000 tonne cargo at 16 knots

Rough estimate pre 1970

Fuel cost exceeds ship cost

Ship cost exceeds fuel cost

CLARKSON RESEARCH SERVICES LTD

Chart 14: Fuel Consumption 60,000 dwt Bulkers

0

20

40

60

80

100

120

140

20

25

30

35

40

45

50

55

60

1965

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1991

1994

1997

2004

2006

2008

2010

2012

2014

2016

Oil Priceat $2013 pricesPre 2014 vessel service speedOrderbook vessel's service speed

Year of Build

Fuel consumptionTPD at 14.5 knots Oil price in

2013 $s

Bulkers delivered in

2013 no more fuel

efficient than in 1986

New generation ecoships on way

CLARKSON RESEARCH SERVICES LTD

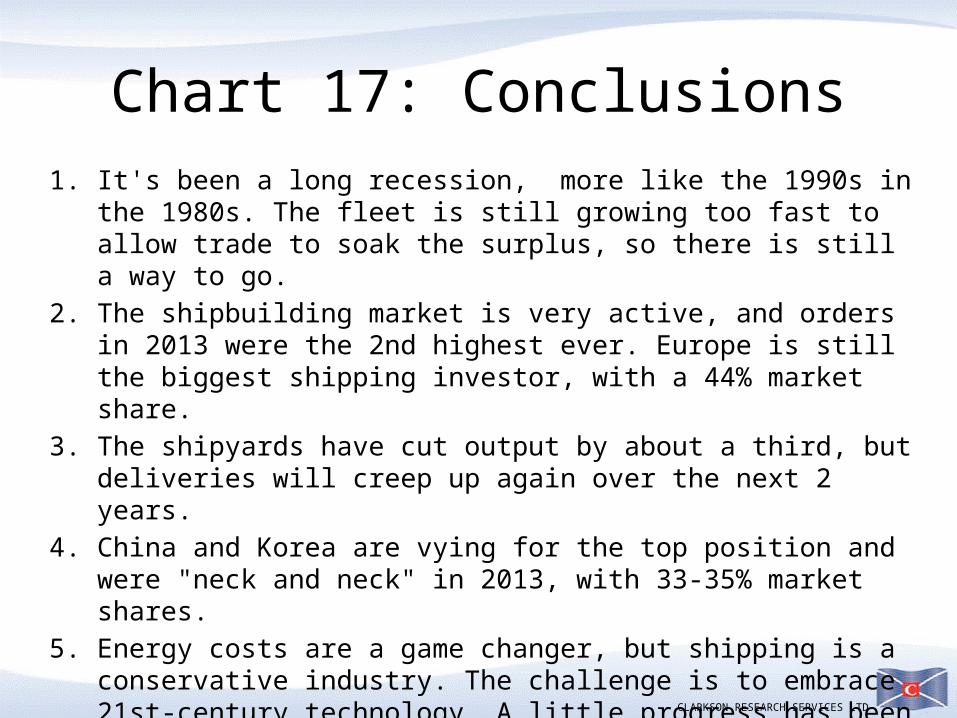

Chart 17: Conclusions1. It's been a long recession, more like the 1990s in the 1980s. The

fleet is still growing too fast to allow trade to soak the surplus, so there is still a way to go.

2. The shipbuilding market is very active, and orders in 2013 were the 2nd highest ever. Europe is still the biggest shipping investor, with a 44% market share.

3. The shipyards have cut output by about a third, but deliveries will creep up again over the next 2 years.

4. China and Korea are vying for the top position and were "neck and neck" in 2013, with 33-35% market shares.

5. Energy costs are a game changer, but shipping is a conservative industry. The challenge is to embrace 21st-century technology. A little progress has been made but there’s still along way to go.

6. •Change is vital and the new technology is on show at SMM. So enjoy the exhibition and see how shipping is facing up to the challenge