texas real estate law 11e

DESCRIPTION

TEXAS REAL ESTATE LAW 11E. Charles J. Jacobus. Chapter 16 Closings. The Closing Process. The final consummation of a transaction is commonly called “closing”. - PowerPoint PPT PresentationTRANSCRIPT

Charles J. Jacobus

TEXAS REAL ESTATE LAW 11E

2

Chapter 16

Closings

3

The Closing Process

• The final consummation of a transaction is commonly called “closing”.

• The documents are signed and transmitted to the parties, the funds are distributed, and all obligations of all parties have been fulfilled.

• A closing is not a purely legal function; it is also a business function.

• The papers are prepared by attorneys and reviewed by the parties prior to closing to eliminate potential misunderstandings.

• The vast majority of closings in Texas are held at title companies, or a third-party escrow agent.

• The escrow agent is a disinterested third party who accumulates the various instruments and funds into “escrow”.

• There is no need for all the parties to attend the closing together and may be best if they don’t.

4

• In the typical residential transaction, there are actually two closings involved rather than just one.

• First, there is the closing of the sale from the seller to the buyer; and second is the closing of the loan between the buyer and the lender.

The Closing Process

CLOSING THE SALEAND

CLOSING THE LOAN

5

Escrows

• The escrow function is one of the keys to a successful closing.

• The escrow officer is normally one who is trusted by both parties.

• The agent represents neither party and has a duty to both parties.

• He cannot give legal advice nor explain the legal effect of documents.

• The escrow should be created pursuant to an escrow agreement with specific instructions for the escrow officer or in a sales contract.

• Escrow officer holds the instruments and funds until the conditions required in the sales contract or escrow instructions are performed.

• When all conditions have been performed, he distributes the funds and signed instruments, and the transaction is considered to be completed.

6

Relation Back Doctrine

• When a document is given to an escrow officer the date of delivery relates back to the time of deposit into escrow.

• Title does not pass to the grantee until all the conditions have been performed and the document has been delivered by the escrow agent.

• After the document is placed in escrow, the grantee has control over its ultimate delivery.

• This doctrine has application when instruments are deposited into escrow and the grantor subsequently dies or becomes insane.

• The Relation Back Doctrine supports the theory of irrevocability by vesting delivery from the grantor at the time of deposit into escrow.

7

Closing into Escrow

• Allows different closing times for each of the parties.

• One party who may be forced to leave town early may sign all the instruments on one date and the other party may close on a later date.

• This is called closing into escrow.

• As long as all parties performed their obligations within the time specified, there should be no conflicts in utilizing this method.

• It is sometimes best that the parties not close at the same time because of the amount of emotion and tension that may exist at closing.

8

Liability of Escrow Agent

• The escrow agent is held to a duty of due care, honesty, and integrity.

• The liability of the escrow officer in the event of a mistake or negligent error is to pay the expense of restoring the status quo.

• Texas Insurance Code requires escrow agents be licensed and bonded.

• One of the more perilous undertakings by the escrow officer is when one of the parties indicates the other party has breached the contract.

• Escrow agent normally waits for a judicial determination before returning any of the documents or escrowed funds to either party.

• To do so would be running the risk of breaching the duty of care as an escrow agent.

9

Funding

• Many title companies have offered “table funding” so that real estate brokers and sellers could get their cash at closing.

• It tends to keep good customers happy and makes sellers feel more comfortable if they can receive their proceeds at closing.

• The TDI adopted rules as to how title companies can fund at closing known as the “good funds” rule.

10

1. Cash or wire transfer.

2. Certified checks, cashier’s checks, and teller’s checks.

3. Uncertified funds in amounts of less than $1,500.

4. Uncertified funds in amounts of $1,500 or more when collected by the financial institution.

5. State of Texas warrants.

6. United States treasury checks.

7. Checks drawn on a bank, savings bank, or savings and loan association insured by the FDIC and for which a transaction code has been issued pursuant to, and in compliance with, a fully executed immediately available funds procedure agreement (Form T-37).

8. Checks by city and county governments located in the State of Texas.

Good Funds

11

Documents for the Closing

• Virtually all documents needed for a closing are deposited into escrow.

• Agents and lawyers should make a closing checklist.

• The closing checklist is created by carefully reading the earnest money contract and making a list of which documents and which funds your client should have in his possession upon leaving the closing.

• Keep in mind that there are certain documents that will not leave the closing but will be transferred to the courthouse for recordation.

12

Seller’s Closing Checklist

1. Cash in an amount that should be predetermined (this may be delayed upon funding of the purchaser’s loan).

2. The deed of trust (if the seller is going to finance the transaction, but will usually be sent to the courthouse to record).

3. A promissory note (if the seller is going to finance the transaction).

4. A closing statement.

5. Hopefully, a smile.

13

Buyer’s Closing Checklist

1. The deed (which is normally forwarded to the courthouse for recording before being delivered to the purchaser).

2. Warranties as requested or required [(1) mechanical equipment inspection, (2) termite inspection, (3) slab inspection, (4) roof inspection].

3. The owner’s title policy.

4. A bill of sale (if any personalty is to be transferred).

5. Estoppel certificates to evidence the payoff figure for the underlying indebtedness, if any.

6. A receipt for the purchase price paid.

7. A closing statement.

8. Seller Disclosure Form.

9. Disclosures required in the contract for sale or required by state law.

14

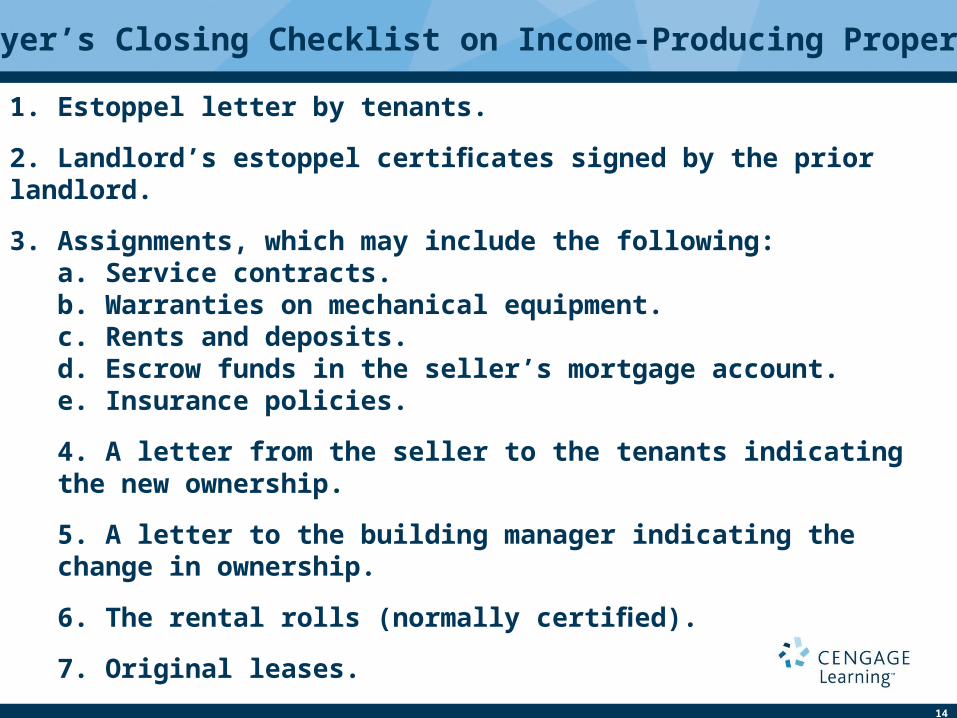

Buyer’s Closing Checklist on Income-Producing Property

1. Estoppel letter by tenants.

2. Landlord’s estoppel certificates signed by the prior landlord.

3. Assignments, which may include the following:a. Service contracts.b. Warranties on mechanical equipment.c. Rents and deposits.d. Escrow funds in the seller’s mortgage account.e. Insurance policies.

4. A letter from the seller to the tenants indicating the new ownership.

5. A letter to the building manager indicating the change in ownership.

6. The rental rolls (normally certified).

7. Original leases.

8. Employment contracts.

9. Assignment of trade name.

15

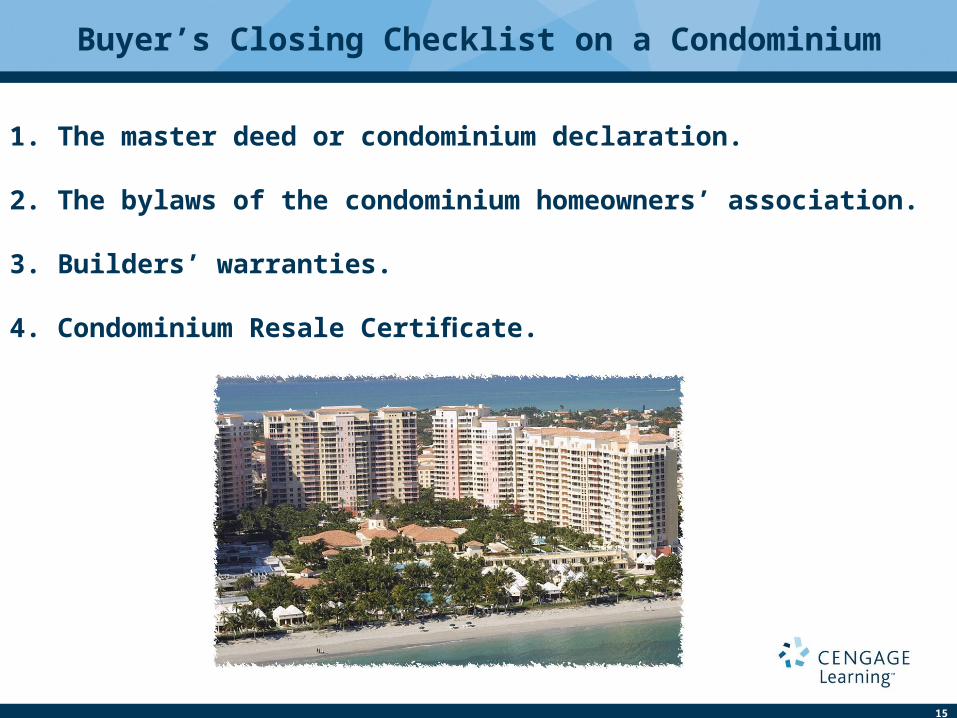

Buyer’s Closing Checklist on a Condominium

1. The master deed or condominium declaration.

2. The bylaws of the condominium homeowners’ association.

3. Builders’ warranties.

4. Condominium Resale Certificate.

16

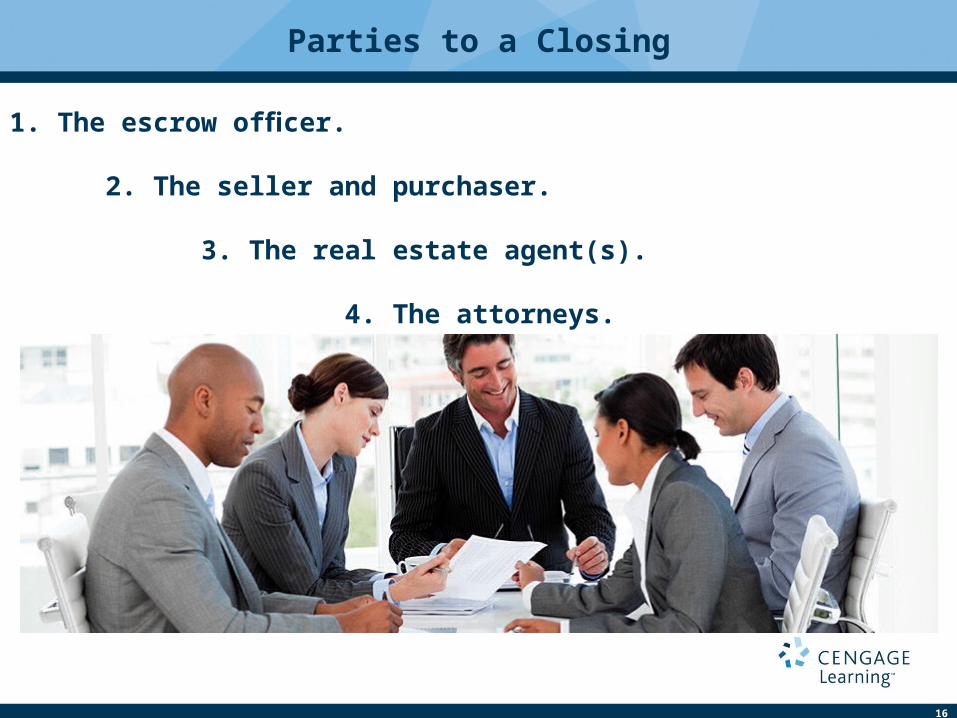

Parties to a Closing

1. The escrow officer.

2. The seller and purchaser.

3. The real estate agent(s).

4. The attorneys.

17

• Performs only two functions: that of being an escrow agent and that of being the agent of the title guarantor.

• Not a “gofer,” negotiator, soothsayer, or salver of all wounds.

• The escrow agent should not be involved with the problems of either party, or real estate agents or attorneys, unless it relates to his function as an escrow agent or title insurer.

• It is not his job to make phone calls, check on loan proceeds, or talk to anyone’s relatives or friends with respect to said closing.

• The escrow officer normally has enough responsibility without having to be concerned with all the other parties’ problems!

The Escrow Officer

18

• The seller or purchaser is normally a client whose property and funds are involved in consummating the sale.

• He is represented by a real estate agent and preferably also by an attorney.

• It is anticipated that this client is a true “consumer”.

• It is the interest of the consumer that must be protected.

Seller and Purchaser

19

• The chief negotiator and arbiter between the parties.

• Making sure that all parties stay convinced that they have each made a good deal.

• The transfer of real estate is considered a very personal transaction; that is, it is people-oriented.

• The assistance of a qualified real estate agent should help to solve many problems, since he understands the relationship between the parties and what each party is expecting to obtain from the consummation of the sale.

Real Estate Agent

20

• All clients should be represented by an attorney.

• The attorney understands the legal ramifications of the escrow agent’s function, the representations made by both parties, and the instruments at closing.

• He is capable of explaining an individual’s legal rights as these pertain to the transaction.

• Anyone else who attempts to interpret the documents or to explain an individual’s legal rights is practicing law without a license.

• This applies to the escrow agent as well as to the real estate agent.

The Attorneys

21

The Real Estate Settlement Procedures Act

• Requires certain disclosures to all parties prior to a closing and the use of certain forms during the closing.

• These requirements are of particular importance in residential transactions.

• Most of the provisions of RESPA were passed to control practices of certain states that had a large number of fees going to the escrow officer, attorneys, and other various and sundry parties – fees that came as a surprise to the consumer when he attended the closing.

• Texas is not considered one of the states with a reputation for charging a large amount of closing costs.

• All the provisions of RESPA apply to Texas, as they do to all the states.

22

Resource – www.hud.gov/respa

23

Transactions Covered by RESPA

• RESPA is construed to apply to all “federally related loans”:1. Any loan that is secured by a first or subordinate lien.2. Upon a one-to four-family residential structure, either presently existing or to be constructed from the loan proceeds, or a condominium or co-op unit.3. The loan must be made by a lender whose accounts are insured by, or the lender regulated by, an agency of the federal government.

• It is not difficult to see that RESPA applies to all institutional lenders and to virtually all residential transactions.

24

Exemptions from RESPA

(1) farms of 25 acres or more.

(2) home equity line of credit transactions.

(3) transactions involving only modification of existing obligations.

(4) “bridge” loans.

(5) assumptions, if no lender approval is required.

(6) temporary financing such as a construction loan.

(7) secondary market transactions.

25

• The lender must give a “special information booklet in any RESPA-covered transaction to every person who submits a loan application”.

• The booklet provides information about the borrower’s rights and obligations in connection with the closing of the loan transaction.

• The booklet must be provided to the borrower not later than the third business day after the lender receives the loan application.

• The book is basically in the format provided by HUD, although certain variations are allowed to be made as long as they are HUD-approved.

HUD’s Special Information Booklet

26

HUD’s Special Information Booklet

27

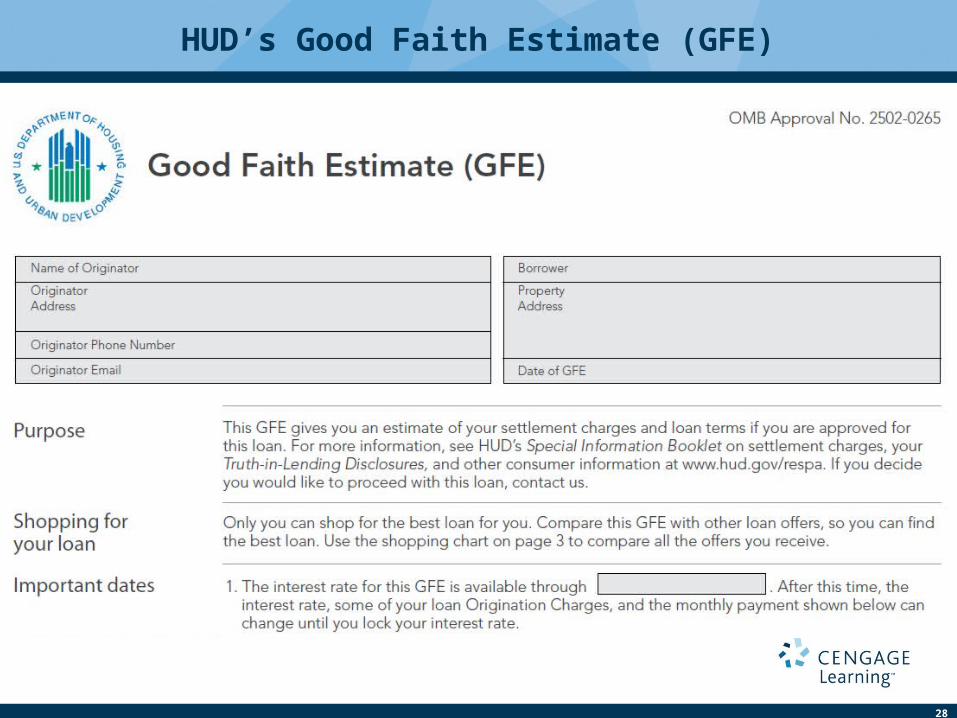

• The lender must furnish the borrower a good faith estimate (GFE) of settlement charges that the borrower is likely to incur with the loan.

• The costs quoted in the GFE are subject to “tolerances” that the lender charges for taking, underwriting and processing the application.

• The cost for origination fees and the real property transfer tax must be exact and fall in the category of “zero tolerance”.

• When the lender requires a specific settlement service provider tolerances are allowed to increase 10% over the original GFE.

• If the borrower chooses providers, there is an unlimited tolerance, as the lender has no control over the costs.

• If the tolerances don’t match, the title company sends the documents back to the lender to make the revisions.

HUD’s Good Faith Estimate (GFE)

28

HUD’s Good Faith Estimate (GFE)

29

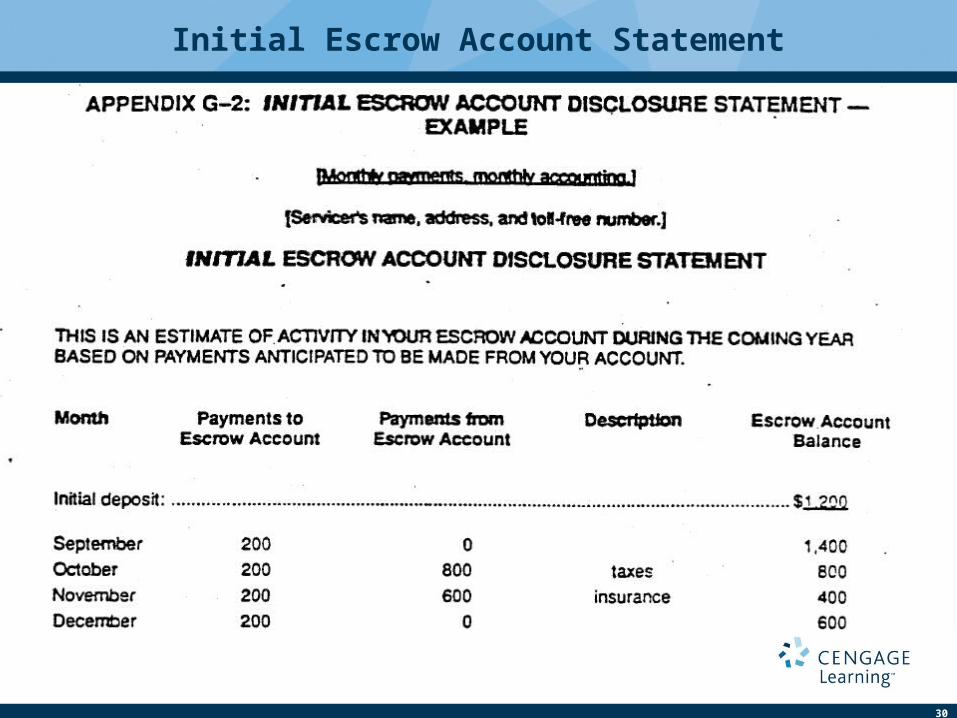

• Lenders and servicers must provide borrowers disclosure statements concerning the establishment and maintenance of escrow accounts.

• The lender must provide an “initial escrow account statement” within 45 days of closing, or show it on the HUD-1 statement at closing.

• The form to be used is promulgated by the federal government.

Initial Escrow Account Statement

30

Initial Escrow Account Statement

31

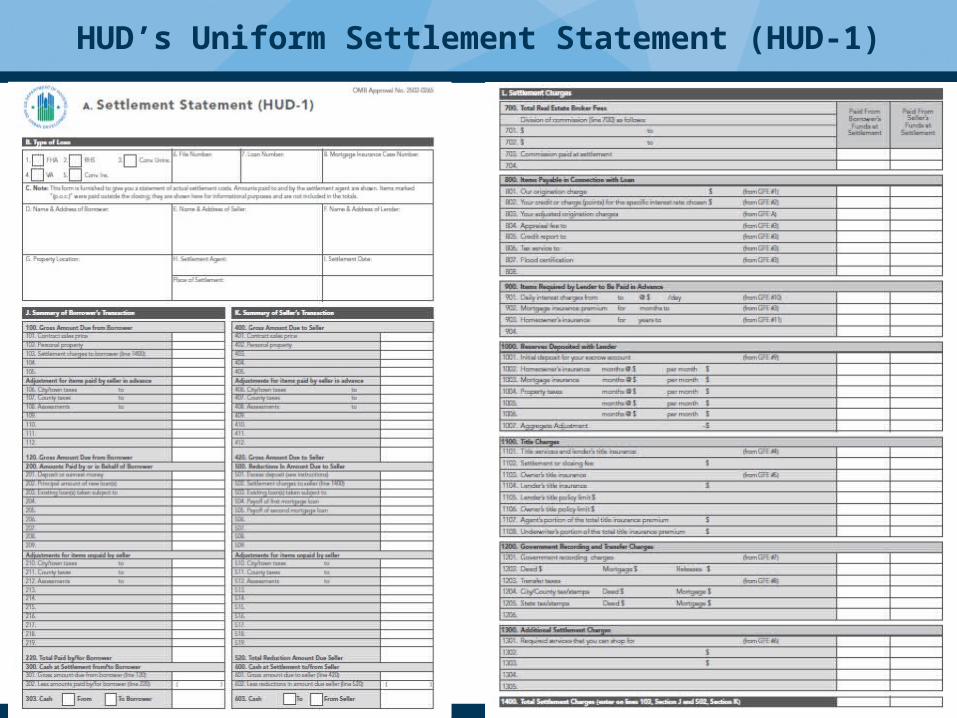

HUD’s Uniform Settlement Statement (HUD-1)

• Escrow agent must use the standard settlement statement (HUD-1).

• There have been some complaints about the use of the HUD forms because they are confusing in parts and sometimes difficult to explain.

• There is a requirement to itemize all charges paid by borrower & seller.

• If there are any costs required by the lender paid outside the closing, they must still be noted on the settlement form; marked “P.O.C.”.

• The seller’s columns may be deleted from the buyer’s copy and the buyer’s columns may be deleted from the seller’s copy.

• The settlement agent must provide lender with a copy of each HUD-1.

32

• Everything that involves an exchange of money at the closing must be on the HUD-1 form.

• The HUD-1 forms now disclose the GFEs as a part of the HUD-1 form.

• A title company needs to review the original GFE versus the new GFE to make sure they are within tolerances.

• If they are not, they should send the documents back to the lender for review and adjustments.

• The title company has to disclose the title insurance agent’s portion of the premium along with the underwriter’s portion of the title premium.

• The borrower may inspect the HUD forms at any time during the business day before the closing.

• The final statement is to be delivered to the borrower and seller at or before the time of the settlement.

HUD’s Uniform Settlement Statement (HUD-1)

33

HUD’s Uniform Settlement Statement (HUD-1)

34

Controlled Business and Referral Fees

• There have been some problems in closings as to the seller requiring the buyer to purchase title insurance from a particular title company.

• RESPA prohibits “controlled businesses” wherein a lender or other person is in the position to refer business as a part of a real estate settlement service.

• This prevents kickbacks and unearned fees from going to a party who might take advantage of the other person’s lack of bargaining power.

• These kinds of referral fees are strictly prohibited.

• RESPA eliminates those kickbacks or referral fees that tend to unnecessarily increase the cost of settlement services to the consumer.

35

Controlled Business and Referral Fees

Controlled business arrangements are allowed provided that:

1. A disclosure is made of the arrangement and such person is provided a written estimate of the charge or range of charges generally made by the provider to which the person is referred.

2. Such person is not required to use any particular provider of settlement services.

3. The only thing of value that is received from the arrangement, other than the permitted payments, is a return on the ownership interest or franchise relationship.

A settlement service provider may offer combined services at a price lower than the sum of individual services if:

(1) the use of the services is optional to the consumer, and (2) the lower price is not made up by higher costs elsewhere.

36

Penalties for Violations of RESPA

• Any person who violates RESPA “shall be fined not more than $10,000.00 or imprisoned for not more than one year, or both.”

• Those who violate the prohibitions are also jointly and severally liable to the person charged with the settlement service involved in the violation in an amount equal to three times the amount of any charge paid for such settlement service.

• There are separate provisions for referrals to title insurance companies.

• Anyone who violates this provision is liable in an amount equal to three times the charge for such title insurance.

37

Escrow Accounts

• Any amounts collected for escrow accounts can only be so much as would equal the amount to be sufficient to pay such taxes, insurance premiums, and other charges attributable to the period between the closing and the time the amount is to be paid, plus one-sixth (two months) of the estimated annual amount to be paid.

• All future collections for payment into the escrow account are limited to one-twelfth of the charges to become due within the next year.

ONE-SIXTH = TWO MONTHSONE-TWELFTH = ONE MONTH

38

Payment Shock

• Frequently occurs in new home construction, wherein the taxes calculated for the initial year were on a substantially lower value than the newly constructed home.

• Many homeowners suffer “payment shock” in the second year when their escrow account contributions are substantially increased.

• The increase is not only because of the increased value but also to make up escrow shortages if the increased tax was not collected in prior months.

• With the consent of the borrower, the lender may calculate the escrow payments over a 24-month basis, thereby mitigating the deficiency.

• It is not required, but it is encouraged as a best practice.

39

Curing Violations

• The loan originator has an opportunity to cure any violation by reimbursing the borrower for any charge in which the allowed tolerance has been exceeded.

• This reimbursement may be made at settlement or within 30 days after the settlement.

40

Questions for Discussion

1. What is the Relation Back Doctrine?

2. In a typical real estate closing how many transactions are being closed and what are they?

3. What are “good funds” and what constitutes good funds under Texas law?

4. Let us assume that all of the parties and their various representatives show up at closing. Name these persons and briefly explain the role of each.

5. Summarize the major provisions of the Real Estate Settlement Procedures act (RESPA).