telecom industry in india

TRANSCRIPT

Telecom Industry in India

• Indian Telecom Industry ranks 3rd among the world. It’s the 2nd largest network in Asia.

•Telecom along with Information Technology has provided the platform to accelerate the Indian economy.

•The Contribution of telecom to GDP has sparked its growth level to 3 % as on 2011 from 0.91 in 2006.

• Indian Telecom Sector operates with a customer base of approx 951 million.

•It has attracted a Foreign Direct Investment of US$ 1093 million as on 2010-2011 at present 49% is allowed as FDI and 74 % is permitted through Foreign Investment Promotion Board - a Government Body.

• In the Economic Context Telecom has identified itself from being an Luxury to Need.

•The demand for telecom services only seems to increase as the tariffs decrease. As the graphs show, the wireless subscribers have increased dramatically from 150 million in 2007 to 850 in 2012, almost 2/3 of our population!

oIntroduction

oChronological growth in Telecom industry

oDemand & Supply

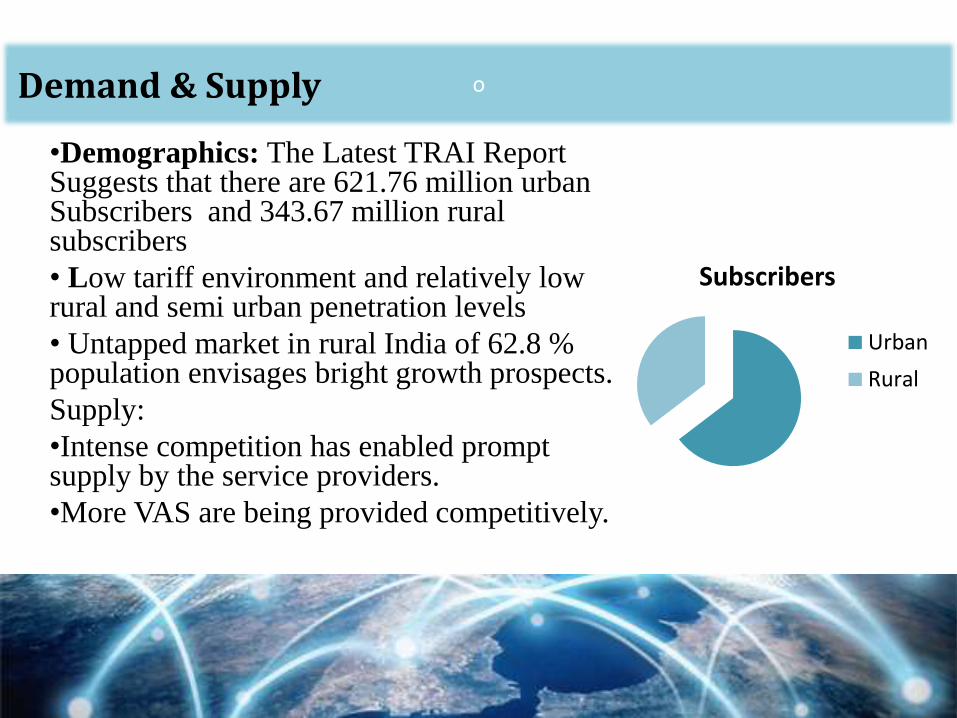

•Demographics: The Latest TRAI Report Suggests that there are 621.76 million urban Subscribers and 343.67 million rural subscribers

• Low tariff environment and relatively low rural and semi urban penetration levels

• Untapped market in rural India of 62.8 % population envisages bright growth prospects.

Supply:

•Intense competition has enabled prompt supply by the service providers.

•More VAS are being provided competitively.

Subscribers

Urban

Rural

oBarriers to Entry

•High capital investments, well-established players who have a

nationwide network, license fee, continuously evolving technology

and lowest tariffs in the world are Barriers to entry:

a) Termination Fee: The Incremental Marginal Costs is directly proportional to the

amount of traffic happening in the network and the service provider will get additional

revenue for inbound call from other network. These charges are normally set by the

regulator.

b) Customer Acquisition Costs : Other than the capital costs to acquire Spectrum to

build out network and overcome initial losses the companies also require huge money to

acquire enough customers to reach equilibrium. These Costs are generally High and are

huge Barriers for new entrants.

c) Low ARPU (avg revenue per cost) due to really low tariff makes profits hard to make

0

100

200

300

400

500

600

700

800

900

1000

FY01 FY02 FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12

Wireless

Wired

mill

ion

financial year

oTele-subscribers – Wired & Wireless comparison

2012, 78.10

oTeledensity

Source: TRAI, Dot Reports and Hindu Business line

oMarket Share – 2013 index

Airtel, 21.75

Reliance, 13.98

Vodafone, 17.47

Idea, 13.9

BSNL, 11.325

Tata, 7.808

Aircel, 7.09

Uninor, 3.7

Sistema, 1.68

Videocon, 0.24

MTNL, 3.2Loop, 0.36

Quadrant, 0.16

Market Share in percentage

oOligopoly - Overview

1. Market Power: In an Oligopoly competition, few firms produce most of the market output and enjoy substantial market power

2. Concentration Ratio: The top 5 companies constitute 70% of the market share The key players in the Telecom industry are Airtel, Vodafone, Idea, Reliance and BSNL. The top players make up more than 70%

of the market, thus indicating that it is an Oligopolymarket structure.

3. Entry Barriers: Huge investments, strict government regulations and scams

4. Economies of Scale: The rapid growth and size of the Indian market has enabled great economies of scale for the key market player

oOligopoly - Pricing

•Pricing is a crucial phenomenon for the telecom service providers as the competition is cut throat and high.

•From the onset of telecom service being deregulated in 1991, and the entry of new players into the market, the pricing has been reducing drastically, YoY.

•A number of times, the top players make pricing changes which affects the industry as a whole, as the others are forced to follow suit.

•Prime example would be when TATA DoCoMo entered the market, it priced the call rates at 1p/sec, while the rest were charging Re.1/minute. Immediate market reaction was to cut down the price to compete with DoCoMo.

•Today, the costs are as low as 30p/minute , a price that’s provided by some of the top players like Airtel and Vodafone.

Re

.1

300 million

60

p

500 million

oOligopoly

•This typical Oligopolic nature of business

hinders the industry to rake above normal profits

.

•Recent Issue of Tata Docomo and RCom

reducing the prices but still failed to impact the

market share, which has landed them in debts.

•India currently has the lowest ARPU (ARPU –

A primary element of valuation and analysis of

wireless companies, Avg Revenue Per User)

across the world, low enough to raise questions

on the sustainability of the current business

model.

oOligopoly

•The operators today are indulging in unrealistic pricing margins to win new

subscribers that its putting a pressure on their profit margins.

•Most operators have taken huge loans to fund their 3G spectrum obligations. Now

they would have to raise more funds to fund the 2G spectrum licenses. With such

low margins and high debt to equity ratios, banks have been sceptical about lending

further to the telecom companies. As a result, most of them are exploring other

options of raising funds including listing of unlisted subsidiaries.

oWinner’s Curse

•The winner's curse is a phenomenon that may occur in common value

auction with incomplete information.

• The winner may be cursed in two ways :

1) the winning bid exceeds the value of the auctioned asset such that the winner is

worse off in absolute terms

2) the value of the asset is less than the bidder anticipated, so the bidder may still

have a net gain but will be worse off than anticipated.

Example :

•SSTL placed a bid of Rs 3639 Cr but now they are incurring a loss Rs 845 Cr and

a dept of Rs 4187 Cr.

•Same is the case with Reliance, its profit has gone down from 182 Cr to 108 Cr.

oThe Reliance Case

Reliance Communication is still trying to emerge from a phase of a gruelling price war, which had led to rock bottom call rates, though regularity uncertainties surrounding the pricing of spectrum and merger and acquisition rules persist.

The competition has eased off late after the Supreme Court last year cancelled some 122 licences granted in and after 2008, leading to increases in voice tariffs.

Reliance Communications itself was badly hit by the competition, which hurt revenue and profitability.

Its net profit was dragged further by huge debt taken mainly to buy expensive 3G bandwidth and efforts to divest stake in the company or some of its units haven't borne fruits so far.

RCom is said to be concentrating on it’s other means such as Broadband Talks though are ongoing to offload stakes in Reliance Globalcom BV, its wholesale telecommunications unit, and in its unit running direct-to-home operations, Reliance Digital TV

oTelecom Regulatory factors

Telecom industry has been subjected to multiple regulations. The following are the most important.

1. TRAI – Telecom Regulatory Authority of India 1997 was established by an act of Parliament (by the same name) to regulate telecom services, including fixation of tariffs. In 24th January, 2000 another body was established - Telecommunications Dispute Settlement and Appellate Tribunal(TDSAT) to take over the adjudicatory and disputes functions from TRAI. TRAI’s functions include Consumer protection, ensure Quality of Service, affordable Tariff, Regulate interconnections, Directions, Orders and Recommendations

2. Unified Access Service Licensing Regime: It marked the end of licensing regime in the Indian Telecom industry. It eliminated the need for different licenses for different services. Players were now allowed to offer both mobile and fixed-line services under a single license after paying an additional entry fee.

oTelecom Regulatory factors

3. Access Deficit Charges (ADC): ADC makes it mandatory for a service provider at the Caller’s end to share a percent of the revenue earned with the service provider at the receiver’s end in long-distance telephony. This is the reason why Incoming is charged for roaming.

4. Universal service Obligation (USO): The USO policy was laid to widen the reach of telephony services in rural India. This system was put in place to bridge the wide gap between urban and rural teledensity. All telecom operators are bound to contribute 5 percent of their revenues to this fund.

5. Foreign direct Investment: India in the past 15 years has received 10,000 Cr of FDI and 26 % of the sum have been invested on the cellular segment. Telecom is the 3rd

largest sector to attract FDI in India in the post-liberalisation era. FDI ceilings have been raised from 49 % to 74% in telecom services sector. For telecom equipment manufacturing and provision of IT enabled services, 100% FDI is permitted.

oOpportunities In The Future

•Rural Telephony - Connecting The Real India

•3G Services - Potential Growth Driver

•Mobile Value Added Services(VAS) - An Opportunity To Increase The

ARPU

•Infrastructure Sharing - A Profitable Proposition

•Managed Services - Outsourcing In Telecom

oChallenges for the Industry

Market Saturation : With the national Average Density reaching 76 % . The

Chance for further Expansion of market looks bleak. The telecom Companies

have reached the point of Saturation.

Price War : The Call Rates in the Industry has steeped Down from being in

16.80 rs per Minute in 1985 to 0.30 paise in 2012. So the Telecom Companies

are living amidst the Perfect Oligoplistic Competition with Least Market

Power.

Declining ARPU: Average Revenue Per Minute is falling every year with

Major players Loosing more than 20 % of revenue , with Subsequent Fall in

EPS . The Growth Seems to be almost muted in the Following Years

oFuture

Number Portability: With Number Portability Schemes still Running in the Pipeline . This

Feature if made a simple process has a good probability of maximizing revenues for the

telecom sector in the near Futnure.

Infrastructure Sharing: The upgrade of Infrastructure becomes mandatory owing to

Increased Customer Base. Infrastructure Sharing seems to be one of the profitable options

for the players involved in the market. It would lead to good decline in the Initial Set up

Costs for new and existing Service providers. This Infrastructure Sharing Will also enable

the Companies to expand their rural market thereby avoiding market Saturation.

Outsourcing of Managed Services: Managed Services Provider is an alternative to

outsourcing, it involves partially or Wholly outsourcing the infrastructure management

Services , given the Increased customer Base Managed Service Providers would enable the

telecom Companies to concentrate on Innovation rather than managing Existing Customers.

oConclusion

With promising growth rate increasing every year ,ever increasing customer base,

excellent talent Workforce, Decreasing Tariffs and Dynamic Handset Market at lower

costs there are good prospects for growth in Indian telecom Sector. But the recent

scams, lowered ARPU, Reaching a saturation in Urban Markets the challenges ahead

are not Less as well .

Companies with good Infrastructure management, increased rural penetration and

quality service will stand ahead in the current market scenario .

There are possibilities for a change in the market Structure with the players forming

Cartels Among themselves. Today it is the age of Intra-Company Mergers, tomorrow it

can be for Inter-Company mergers.