technology implications and costs of dodd-frank on

TRANSCRIPT

CFTC TAC | Washington DC | March 1, 2011

Technology Implications and Costs of Dodd-Frank on Financial Markets

Larry TabbFounder & CEO

TABB Group

2

Contents

Workflows

High Level Existing

High Level Proposed

SEF

Clearing

Dealers

Prime Brokers

Dealer spending estimates

Dealer Progress

Conclusions

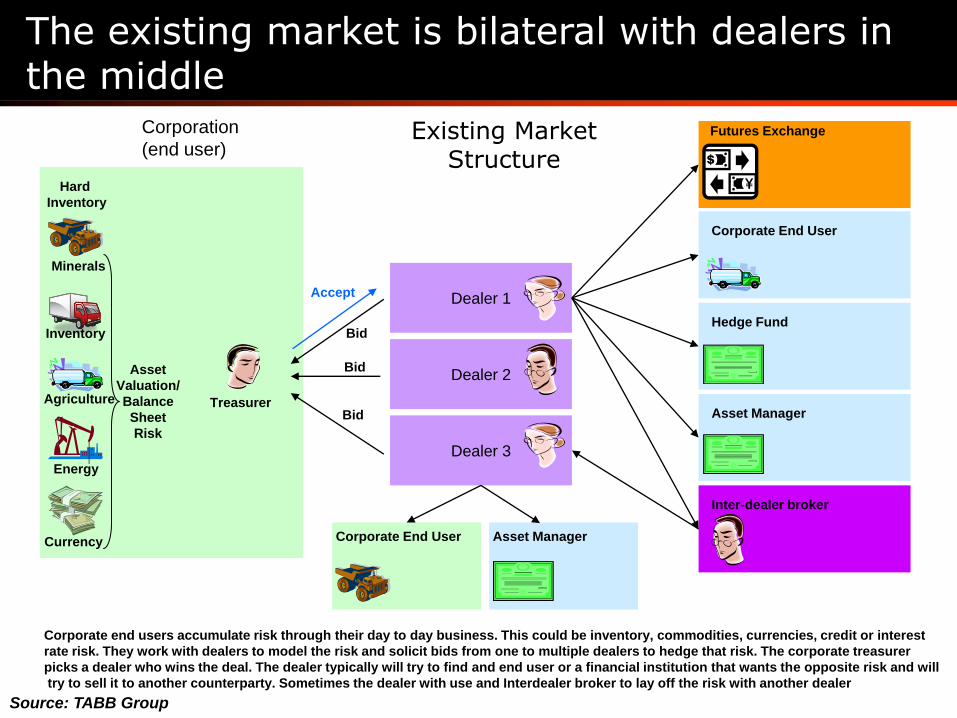

Existing MarketStructure

Corporation

(end user)

Hard

Inventory

Asset

Valuation/

Balance

Sheet

Risk

Treasurer

Minerals

Inventory

Agriculture

Energy

Currency

Dealer 1

Dealer 2

Dealer 3

Bid

Bid

Bid

Accept

Corporate End User

Hedge Fund

Asset Manager

Corporate End User

Inter-dealer broker

Corporate end users accumulate risk through their day to day business. This could be inventory, commodities, currencies, credit or interest

rate risk. They work with dealers to model the risk and solicit bids from one to multiple dealers to hedge that risk. The corporate treasurer

picks a dealer who wins the deal. The dealer typically will try to find and end user or a financial institution that wants the opposite risk and will

try to sell it to another counterparty. Sometimes the dealer with use and Interdealer broker to lay off the risk with another dealer

Asset Manager

Futures Exchange

The existing market is bilateral with dealers in the middle

Source: TABB Group

Proposed MarketCorporation

(end user)

Hard

Inventory

Asset

Valuation/

Balance

Sheet

Risk

Treasurer

Minerals

Inventory

Agriculture

Energy

Currency

Bid

Bid

Bid

Accept

The corporate end-user business is unlikely to change much of the clearing requirements for end-users has been exempt – and under FASB133

only exact hedges can get balance sheet relief and it is not expected that a significant amount of customized products will be centrally cleared

and SEF-traded. However, it is mandated that all standardized swaps be both centrally cleared and traded on an SEF. We anticipate that much

of this business will be done with financial non-dealer financial institutions such as hedge funds, asset managers, insurance cos, and

proprietary trading houses

Corporate End User

Asset Manager

Large

Dealer 1

Large

Dealer 2

Large

Dealer 3

Dealer 1

Clearing

Firm 1

Prime

Broker 1

Hedge Fund

Insurance Co

Small Dealer 1

Asset Manager

Hedge Fund

Insurance CoHedge Fund

Prop

Shop

SEF

Trade Info &

Market Data

Trade Info

Clearing

House

Trade

Repository

SEF MembersSEF Members

Clearing Fund

Margin

Trades &

Margin

Under DF, standardized swaps are matched by SEF, centrally cleared, & centrally reported

Source: TABB Group

SEF Technology

SEF infrastructure is fairly straightforward. The four major technology aspects of a SEF will be managing connectivity and messaging, risk

management (however, not as substantial as the clearing house), matching, and market data. SEFs typically do not pay for connectivity,

however the larger and more successful, the more challenging is the communications and infrastructure requirements. Increasingly there

may also become demand for co-location.

Matching

Engine

Market Data

Ticker Plant

Pre-trade

risk

Connectivity

Messaging &

Networking Support

Post trade

Notice of

Execution

Dealer

Clearing

Firm

Prime

Broker

Credit

Management

Surveillance

SEF Members

Dealer

Clearing

Firm

Prime

Broker

External Market

Data Providers

External Valuation /

Evaluation

Providers

Co location Management

Clearing

Firms

Prime

Brokers

Dealers

Dealers

Clearing

Firms

Prime

Brokers

SEF Members

Clearing house

Communications

SEF

Clearing

House

SEFs, while not fully defined, will need some very specific technology

Source: TABB Group

While Clearinghouse technology is not as real-time as an SEF, the Central Clearing House manages risk. Clearing houses typically receive two

copies of each trade – one from the SEF and the other from the members. They are reconciled, netted/novated, cash is settled and then

placed in a position repository where they are valued each day, and the excess/deficit values are exchanged with dealers on a daily basis.

Connectivity

Messaging &

Networking Support

Dealer

Clearing

Firm

Prime

Broker

Clearing House

Members

Dealer

Clearing

Firm

Prime

Broker

External Market

Data Providers

External Valuation /

Evaluation

Providers

Dealers

Clearing

Firms

Prime

Brokers

ClearinghouseSEF

Trade Feed

New Trade

EntryComparisons

Trade

Reconciliation

Netting / Novation

Cash Management Margin

Firm

Liquidation

Default Fund

Management

Valuation

Risk Management

Cash

Position

Management

Identifier

Management

Trades

Reconciliation

Margin

Cash Settlement

Default Fund Mgt.

Cash

External

Asset Manager

Liquidation

CashPositions

Clearing Bank

Multiple Trade

Repositories

Clearinghouse’s primary job is to manage default risk – but that encompasses a lot

Source: TABB Group

Dealer Technology

Dealers will have significant technology investments to make. SEF’s don’t exist, SEF eligible products don’t exist, all trade repositories don’t

exist, many clearinghouses are just getting started. Also Prime brokerage facilities are not set up, credit lines, as well as ways of modeling

the products are not standardized.

Connectivity

Messaging &

Networking Support

Dealer Clients

External Market

Data Providers

External Valuation /

Evaluation

Providers

DealerCredit Risk

Pre-trade

Risk Management

Comparisons/

Reconciliation

SEF

Communications

Netting / Novation

Cash Management

Market

Liquidity RiskCredit Risk

Valuation

Risk Management

Cash

Position

Management

Identifier

Management

Cash

Cash

Clearing Bank

Dealer

Clearing Firm

Hedge Fund

Small

Dealer

Prop

Shop

Insurance Co

Asset Manager

Multiple

SEFsMultiple

Clearinghouses

Multiple Trade

Repositories

Market Data

Outgoing

MarginClearinghouse

ReconP & L

Regulatory

Compliance

Reporting

Multiple

Regulators

Position Limits

Positions

Credit

LinesProp

Desk

Unfortunately for dealers, much of their infrastructure needs to be added as business is expected to shift

Source: TABB Group

Prime Brokerage Technology

Prime brokers’ provide credit and credit intermediation services (transact using the banks’ credit and not the fund’s credit. This allows the

fund to buy at better prices. Primes also provide financing (for securities – not necessary for derivatives) and manage margin. Because of the

lending relationship the Prime needs to keep a close eye on the financial condition and the leverage of the fund.

Connectivity

Messaging &

Networking Support

Clients

External Market

Data Providers

External Valuation /

Evaluation

Providers

Cash ManagementValuation

Position

Management

Clearing Bank

Prime Brokers

Hedge Fund

Multiple

Clearinghouses

Multiple Trade

Repositories

Margin

Multiple

Regulators

Credit

Lines

Market &

Liquidity RiskCredit Risk

Risk Management

Pre-trade

Risk Management

Reporting

Executing

Dealer

Margin

Hedge Fund

Administrators

Prop

Shop

SEFs

Front End

Portal

Primes will provide leverage and access for hedge funds and prop traders – this business is new too

Source: TABB Group

Largest dealers will spend over $1.8b to restructure OTCD business for Dodd-Frank

Top Tier

(3-4 firms)

Mid Tier

(4-5 firms)

Third Tier

(5-6 firms) TOTAL

eCommerce $ 158 $ 87 $ 35 $ 281

Low-touch

Distribution $ 162 $ 90 $ 36 $ 288

CCP $ 217 $ 120 $ 48 $ 385

Risk $ 347 $ 193 $ 77 $ 617

Collateral $ 129 $ 72 $ 28 $ 230

TOTAL $ 1,015 $ 563 $ 225 $1,804

IT Spending Estimates for large dealers (top 15)

(2010 - 2012

Source: TABB Group

IT spending by US Broker/Dealers took a in credit crisis but back on the positive trend

$0

$5

$10

$15

$20

$25

$30

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

CAGR

-7.9%CAGR

8.2%

CAGR

-13.5%CAGR

6.4%

Source: TABB Group

US Broker / Dealers Financial Markets IT Spending

(in US$ billions)

Source: TABB Group

Client needs, which are focused on new regulations, drive prioritization of IT initiatives

Drivers behind prioritization of OTC derivative reform IT initiatives

1 – Least Important Most Important- 5

Regulations drive client

demand, and responding to

client demand provides

competitive differentiation;

hence the top three drivers

behind IT prioritization

Client demand is the clear

primary driver for major dealers

as that is what will bring more

order flow.

Inter-dealer brokers are more

focused on competitive

differentiation and regulatory

compliance as client demands

have changed little post-

legislation.

Reducing costs/ROI is not the

primary driver for any

participants in our study.

Source: TABB Group

Clearing and execution have been the primary focus for dealers, inter-dealer brokers and service providers

Readiness with major OTC derivatives reform related initiatives

1 - Not Yet Started Completed - 5

Both top and mid-tier brokers

feel confident in their current

readiness for central clearing.

Top tier dealers are generally

more prepared for changes in

the execution landscape than

are mid-tier brokers.

Inter-dealer brokers are

prepared for changes to the

execution landscape and are

less focused on clearing.

Overall compliance, reporting

and reference data changes are

further from completion for all as

many of the detailed rules are

still to be written.

Source: TABB Group

Credit and Rates are the primary focus of dealers, inter-dealer brokers and service providers

Product priorities for OTC derivatives reform IT initiatives

1 – Lowest Priority Highest Priority - 5

The early focus on central

clearing of CDS forced it to the

to top of the priority list for most

market participants.

The last few months have seen

a shift of focus to interest rate

swaps as the asset class will

likely see the high percentage of

positions move to central

clearing.

Commodities (including energy

swaps), OTC equity derivatives

and OTC FX derivatives are

taking a back seat for dealers,

inter-dealer brokers and (for the

most part) with regulators.

Source: TABB Group

Conclusions

The dealers are currently scrambling to build out their capabilities

TABB estimates that the largest 15 dealers will spend

approximately $1.8B to implement the Dodd-Frank rules for

derivatives

While dealers have invested heavily over the decades, products,

clearing, trading, business and distribution models are all

changing

While regulation is significant, client demand driving development

From a business perspective clearing and execution are the key

investment areas

Firms are focused on heavily on credit and rates than

Commodities, Equity, or FX Swaps