technology disruption and the future of wholesale banking€¦ · technology disruption and the...

TRANSCRIPT

Image: for position only (FPO)

Technology disruption and the future of wholesale banking

1

FinTech disrupts the financial services industryRapid technology advances are reshaping the entire banking ecosystem, and wholesale banking is not immune.

Client expectations are being influenced by new technology. Drawing on experiences with providers throughout the digital economy, clients now expect simple, consistent digital experiences that allow them to perform key transactions seamlessly from any electronic channel.

New FinTech competitors have entered the financial services marketplace with several advantages. Highly scalable cloud-based infrastructure makes it easier for innovators to capitalize upon a new idea. At the same time, the widespread adoption of powerful smartphones puts a broad client base within the immediate reach of new and integrated services powered by intelligent analytics and location-enabled personalization.

Investments in FinTech have grown exponentially, with private equity firms and hedge firms ramping up their investments into money transfer and payments, savings and investments, insurance and borrowing. Although many FinTech companies currently have a retail or small-business (SMB) focus, the underlying capabilities are able to transition into the wholesale banking services space.

These technology-enabled new entrants pose a significant challenge to incumbent banks. At the same time, the incumbent banks continue to struggle with the following burdens:

• Legacy costs, including, but not limited to:

• People who are trained to develop on old mainframe systems vs. new technologies

• Processes (waterfall vs. agile) that are not suited to enable faster time to market

• Monolithic technology systems that are difficult or delicate to change

• Stringent regulations

• Heightened information security concerns in an age of high-profile hacks and data breaches

2Technology disruption and the future of wholesale banking |

FinTech strengths vs. bank weaknesses(% of executives: responding agree or strongly agree)

80%Absence of legacy software/systems

75%

79%

81%

79%

FinTech strength

70%

77%

78%

76%

66%

80%

75%

Constrained by legacy technology

Capacity to innovate

Lack clear strategic vision

Less regulatory pressure

Under regulatory pressure

Agility and speed to market

Culture not suited to rapid change

Technology expertise

Inability to recruit/retain tech talent

Able to improve current products

Unwillingness to cannibalize products

Bank weakness

FinTech start-ups include thousands of companies globally wedging themselves into markets that have been traditionally dominated by banks. With an average funding of $44 million,2 start-ups have been precise about selecting a single-product market. This narrow focus represented one of the key initial strengths of the FinTech start-up. Recently, and only after solidifying their brand in a particular niche, FinTechs have begun to leverage their brand to expand even further and diversify their portfolios and product sets.

From a technology standpoint, start-ups leapfrog the capabilities of incumbent banks with open networks, the latest cloud-based platforms and innovative methodologies (e.g., leveraging data and tech, such as AI and advanced analytics) to understand and evaluate credit risk in entirely new ways. In addition, as a result of their narrow focus, start-ups have been able to sidestep many of the more complex regulatory requirements that apply to traditional banks, conferring an additional (if temporary) advantage. As a result, FinTech companies are capturing market share in numerous lines of business, despite having started without the credibility and trust associated with long-standing client relationships.

Nonbank players include major technology, telecom and retail companies creating integrated value propositions that deliver optimized experiences directly to clients. Products include prepaid accounts that serve as an alternative to traditional checking accounts and mobile-payments facilities that cut into traditional bank debit and credit card revenue.

For nonbank players, handling the financial component of a transaction is not necessarily the end goal in itself but rather a way to incorporate financial aspects to an existing client experience. This makes nonbank players a formidable threat, as they can set prices with regard to the entire client relationship rather than just based on the mechanics of the financial transaction.

In addition, nonbank players are investing in the growing start-up ecosystem. In this way, nonbank players and FinTech start-ups are facets of the same competitive threat. To respond, banks need to consider the short-term market share incursions of FinTech companies while remaining aware of the long-term strategies of larger nonbank competitors.

Banks are introducing updated strategies into the marketplace, including the following:

• Direct banks: nonbanks (and banks themselves) are building new relationships by offering online-only lending or deposit services to retail and small and medium-sized enterprise (SME) clients.

• Digital onboarding: lenders can leverage a more streamlined and accurate account opening or onboarding process to make it easy for consumers to switch and close the old account. FinTech companies allow account holders to initiate the switch of automated payments and direct deposits. The process is quick and paperless and can be accomplished using a mobile device or personal computer, and the client does not need to speak to his or her existing lender to initiate the process of account switching.

• Instant credit assessments: banks are assessing creditworthiness by leveraging state-of-the-art credit-decision tools and technology with robust analytics, often using information external to the typical bank decision process.

• Loan origination: online-only, proprietary technology and analysis, lower interest rates and customized support allow for a quicker, efficient consumer loan origination process. This will enable banks to eventually close loans quicker than historic industry averages through advanced algorithms and processing functionality. The application process enables clients to tap into several loan originators with lower-than-market rates aggregated in one place.

1

In general, client-focused business models are designed to earn low margins on a very large volume of inquiries, using technology that enables real-time response with straight-through processing.

By contrast, incumbent banks rely upon account-focused business models that require high margins, high transaction volumes and the presence of a branch network. Furthermore, legacy bank technology uses monolithic software that relies on batch processes and human interventions. This architecture is the result of the past decade of economic and regulatory uncertainty, which drove banks to maintain rather than upgrade their technology platforms.

3 | Technology disruption and the future of wholesale banking

FinTech disrupts US wholesale bankingWithin wholesale banking, the most critical areas of FinTech innovation are as follows:

1. Marketplace lenders (MPLs) are disrupting traditional credit-underwriting models with lower overhead, higher transparency, faster loan approval and higher returns on capital.

2. Blockchain-based supply chains have the potential to disrupt entrenched payments and credit processes. As supply chains adopt distributed ledger technology to manage the physical and financial flows associated with commerce, participants may rely less upon wholesale banks to perform the traditional roles than they have in the past.

Although these innovations are operating on different time scales — MPLs are an immediate consideration, and blockchain-based supply chains could take a few years to mature — wholesale bankers need to get up to speed on each, at an equal degree of urgency. That’s because both MPLs and blockchain have multiple points of contact with wholesale credit products and processes. Process changes made now to accommodate MPLs should also be made with consideration of blockchain.

MPLs are innovating in application processing and credit assessment of simple loans, as well as in the deal-shaping and underwriting of complex financial products. Furthermore, MPLs are changing wholesale banking business models across the entire product lineup.

Blockchain technology is most commonly associated with payments (e.g., bitcoin) and other situations having large numbers of participants who need to share a common ledger without a prior contractual or trust-based relationship. Although wholesale banking is characterized by trust-based relationships with other institutions, there are still opportunities for blockchain applications, as with supply chains, that bring in external parties to a significant degree.

In the next section, we will explore these two areas of FinTech innovation in more detail.

Wholesale credit products and processesWholesale credit organization impacts

Simple lending Complex finance

Deal shaping and UW

Account servicing

Portfolio management

Syndication

Special assets management

Proj

ect

finan

ce

Com

mod

ityfin

ance

Stru

ctur

edfin

ance

Ass

etfin

ance

Secu

red

lend

ing

Uns

ecur

edle

ndin

g

Cons

umer

finan

ce

Application processing

Credit assessment

Account servicing

Portfolio management

Securitization

Collections and default

Leas

ing

Cred

it ca

rd

and

revo

lver

Smal

lbu

sine

ss

PaymentsPayments and transactions Information processing

1

3

4

5

6

Blockchain technology

1. Payments2. Supply chain finance

Marketplace lending

3. Application processing4. Credit assessment5. Deal shaping and underwriting (UW)6. Business model

Supp

ly c

hain

finan

ce

2

4Technology disruption and the future of wholesale banking |

Direct lender model Platform lender model

Cert

ifica

tes

(tru

st –

priv

ate)

Capital source

(venture capital,

hedge fund, depository institution, institutional

investors)

Online marketplace

lender

Equity/ warehouse

line

Cash

BorrowersApplication

Loan proceeds

Direct lender model

Online marketplace lender

Application

Loan

Proceeds

Borrowers

Investors, banks, institutional whole loan buyers

Capi

tal

Not

es (p

ublic

)

Loan

s (p

rivat

e)Issuing

depository institution

Loan

pr

ocee

ds

Loan

Platform lender model

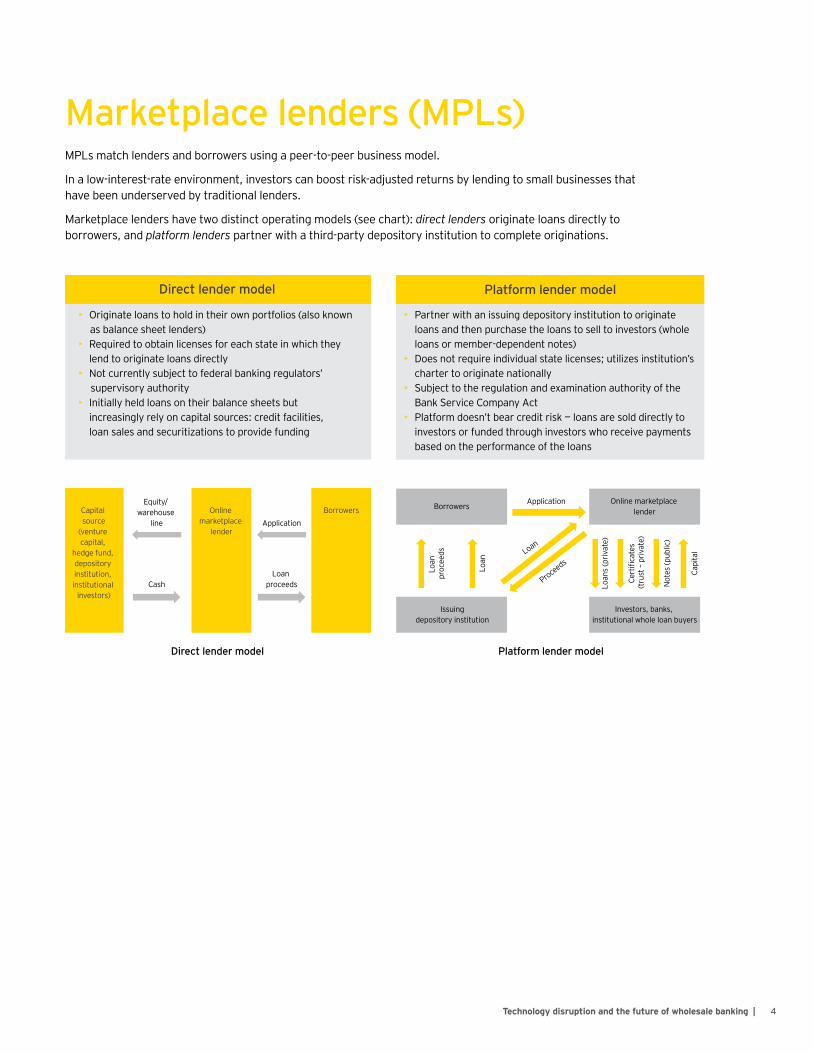

• Originate loans to hold in their own portfolios (also known as balance sheet lenders)• Required to obtain licenses for each state in which they lend to originate loans directly• Not currently subject to federal banking regulators’ supervisory authority• Initially held loans on their balance sheets but increasingly rely on capital sources: credit facilities, loan sales and securitizations to provide funding

• Partner with an issuing depository institution to originate loans and then purchase the loans to sell to investors (whole loans or member-dependent notes)• Does not require individual state licenses; utilizes institution’s charter to originate nationally• Subject to the regulation and examination authority of the Bank Service Company Act• Platform doesn’t bear credit risk — loans are sold directly to investors or funded through investors who receive payments based on the performance of the loans

Marketplace lenders (MPLs)MPLs match lenders and borrowers using a peer-to-peer business model.

In a low-interest-rate environment, investors can boost risk-adjusted returns by lending to small businesses that have been underserved by traditional lenders.

Marketplace lenders have two distinct operating models (see chart): direct lenders originate loans directly to borrowers, and platform lenders partner with a third-party depository institution to complete originations.

5

Technology innovation represents one of the hallmarks of MPLs. In the past, due to the variety and complexity of small businesses, it has been cost prohibitive for banks to conduct traditional origination and underwriting processes. MPLs have automated these processes using technology-driven methods for data aggregation and analytics. While some stakeholders and investors have expressed low confidence in specific business models and credit-scoring methodologies, the MPLs that survive a full credit cycle are likely to become more trusted by the marketplace.

The continued growth of marketplace lending faces four key challenges:

• Scarcity and volatility of funding: a rapidly saturating market and investors’ ability to find similar returns elsewhere have led to a rise in the cost of capital across the industry. Continued funding decreases could force many of the weaker marketplace lenders to slow or even halt originations.

• Uncertain regulatory environment: MPLs are lightly regulated at present, not being subject to the burdensome capital requirements and reporting obligations of traditional banks. This advantage will not last. Rapid growth in the industry has prompted calls for stronger regulation over MPLs and shadow banking in general. Changes may include small-business protections, increased capital requirements, skin-in-the-game rules and additional reporting requirements.

• Normalizing interest rate environment: normalizing interest rates will exacerbate the funding struggles of marketplace lenders as investors will increasingly be able to find better risk-adjusted returns elsewhere.

• Unproven business model and credit scoring: many third-party stakeholders and investors do not have full confidence in the validity of the marketplace-lending business models and credit-scoring methodologies. MPLs will have to prove they can survive a full credit cycle before the broader market is fully confident in the industry.

6Technology disruption and the future of wholesale banking |

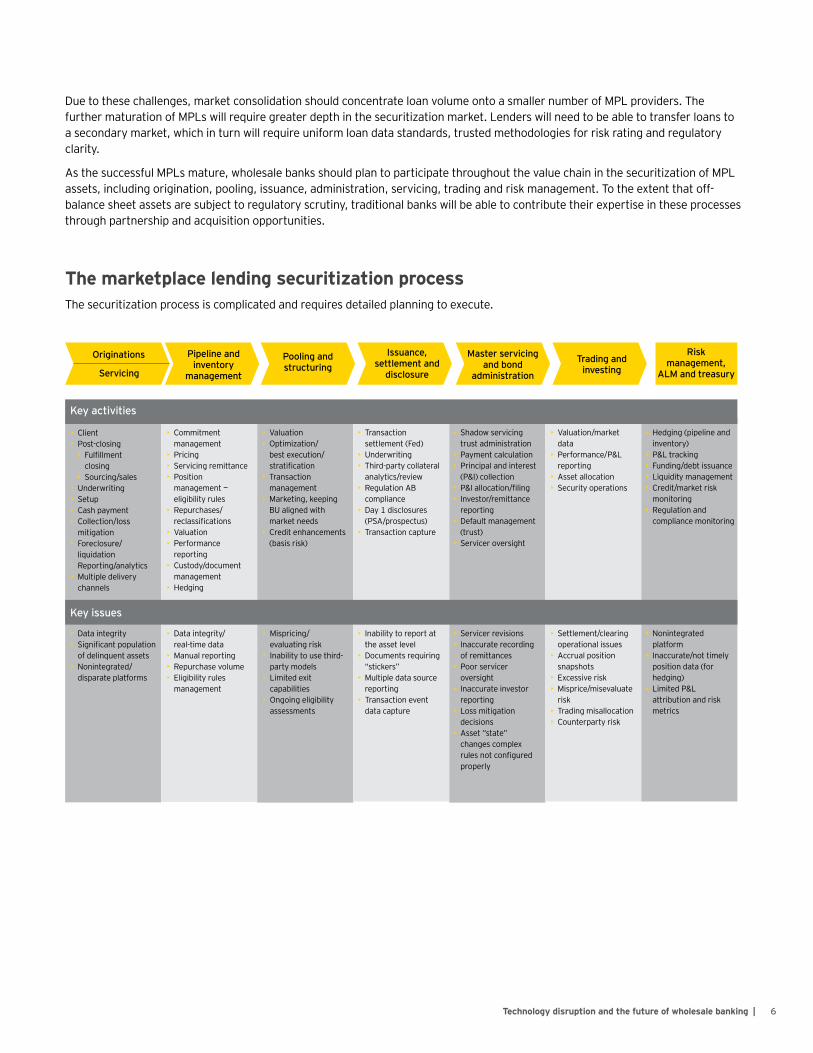

Due to these challenges, market consolidation should concentrate loan volume onto a smaller number of MPL providers. The further maturation of MPLs will require greater depth in the securitization market. Lenders will need to be able to transfer loans to a secondary market, which in turn will require uniform loan data standards, trusted methodologies for risk rating and regulatory clarity.

As the successful MPLs mature, wholesale banks should plan to participate throughout the value chain in the securitization of MPL assets, including origination, pooling, issuance, administration, servicing, trading and risk management. To the extent that off-balance sheet assets are subject to regulatory scrutiny, traditional banks will be able to contribute their expertise in these processes through partnership and acquisition opportunities.

Originations

Servicing

Pipeline and inventory

management

Pooling and structuring

Issuance, settlement and

disclosure

Master servicing and bond

administration

Trading and investing

Risk management,

ALM and treasury

Key issues

• Client• Post-closing

• Fulfillment closing• Sourcing/sales

• Underwriting• Setup• Cash payment• Collection/loss mitigation• Foreclosure/ liquidation• Reporting/analytics• Multiple delivery channels

• Data integrity• Significant population of delinquent assets• Nonintegrated/ disparate platforms

• Data integrity/ real-time data• Manual reporting• Repurchase volume• Eligibility rules management

• Mispricing/ evaluating risk• Inability to use third- party models• Limited exit capabilities• Ongoing eligibility assessments

• Inability to report at the asset level• Documents requiring “stickers”• Multiple data source reporting• Transaction event data capture

• Servicer revisions• Inaccurate recording of remittances• Poor servicer oversight• Inaccurate investor reporting• Loss mitigation decisions• Asset “state” changes complex rules not configured properly

• Settlement/clearing operational issues• Accrual position snapshots• Excessive risk• Misprice/misevaluate risk• Trading misallocation• Counterparty risk

• Nonintegrated platform• Inaccurate/not timely position data (for hedging)• Limited P&L attribution and risk metrics

• Commitment management• Pricing• Servicing remittance• Position management — eligibility rules• Repurchases/ reclassifications• Valuation• Performance reporting• Custody/document management• Hedging

• Valuation• Optimization/ best execution/ stratification• Transaction management• Marketing, keeping BU aligned with market needs• Credit enhancements (basis risk)

• Transaction settlement (Fed)�• Underwriting�• Third-party collateral analytics/review�• Regulation AB compliance• Day 1 disclosures (PSA/prospectus)�• Transaction capture

• Shadow servicing trust administration • Payment calculation• Principal and interest (P&I) collection• P&I allocation/filing• Investor/remittance reporting• Default management (trust)• Servicer oversight

• Valuation/market data• Performance/P&L reporting• Asset allocation• Security operations

• Hedging (pipeline and inventory)• P&L tracking• Funding/debt issuance• Liquidity management• Credit/market risk monitoring• Regulation and compliance monitoring

Key activities

The marketplace lending securitization processThe securitization process is complicated and requires detailed planning to execute.

7

Blockchain-based supply chainsBlockchain is a low-cost, near-instantaneous method for settling transactions without the need for a central authority. Blockchain technology leverages a decentralized, peer-to-peer, consensus-driven platform that can be put to use as a distributed ledger for financial transaction data. A blockchain has no central authority that can control transactions and no central server. Instead, the entire database exists in multiple places, with new transactions only added according to rules established by the consensus of network participants.

Blockchain technology is being envisioned for a wide range of applications in financial services, with the most compelling use cases involving situations where multiple parties need to agree upon a single shared ledger without having to trust or even know one another. Since wholesale banking typically involves interinstitutional relationships between known parties, the business benefits of blockchain will be harder to achieve for wholesale banking businesses. In aggregate, banks have already invested billions of dollars in managing payment flows between a relatively fixed number of participants, and they already transact with one another on a trusted basis through existing mechanisms. As such, it’s unlikely that the industry will move to blockchain absent any broader, compelling reasons to do so, and those reasons are presently absent.

Nevertheless, supply chain finance stands out as having significant potential for blockchain technology in wholesale banking. In the typical supply chain, geographically dispersed counterparties do business with a wholesale bank client, or the client of a client, without having a direct relationship to the wholesale bank. By establishing a shared, distributed ledger that can be trusted by all participants, entire business processes can be simplified in ways that benefit buyers and sellers.

In support of supply chain financing, blockchain-based distributed ledgers can record the ownership of goods and services, provide an unalterable record of the delivery and payment terms of a trade, and denote the identity of trading partners as needed for regulatory and tax compliance. With blockchain technology, contracts can be authenticated and validated without the need for a trusted third party. In addition, simpler documentation processes should result in reduced fraud and corrupt business practices.

Challenges include dealing with anonymous transactions, overcoming growing pains of the technology and instituting the required suite of standards, risk management frameworks and applications. Adoption will also require participation by a wide variety of stakeholders, including buyers, sellers, shippers, banks and governments. The need to comply with burdensome regulatory requirements for know your customer (KYC), anti-money laundering (AML) and customer due diligence (CDD) will also slow adoption.

8

Blockchain-based supply chainsBlockchain has the potential to dramatically streamline supply chain financing through shared, distributed ledgers that enable geographically distributed buyers and sellers to share information with multiple banks throughout the financial supply chain.

Wholesale credit products and processes

Simple lending Complex finance

Deal shaping and UW

Account servicing

Portfolio management

Syndication

Special assets management

Proj

ect

finan

ce

Com

mod

ityfin

ance

Stru

ctur

edfin

ance

Ass

etfin

ance

Trad

efin

ance

Secu

red

lend

ing

Uns

ecur

edle

ndin

g

Cons

umer

finan

ce

Application processing

Credit assessment

Account servicing

Portfolio management

Securitization

Collections and default

Leas

ing

Cred

it ca

rd

and

revo

lver

Smal

lbu

sine

ss

PaymentsPayments and transactions Information processing

Challenges

Description

Benefits

• Record the ownership of goods and services• Provide an unalterable record of the delivery and payment terms of a trade• List the identity of trading partners as needed for regulatory and tax compliance• Authenticate and validate contracts • Provide documentation for fraud

• Uncertainty about how, when and whether it will be adopted• Needs adoption by a large number and variety of stakeholders to achieve full benefits• More complex regulatory requirements regarding KYC, AML and CDD need to be addressed in a solution

• Reduce the time and expense required to manage supply chain financing• Simplify documentation by establishing a single source of trusted data• Eliminate opportunities for fraud and corrupt business practices

Wholesale credit products and processes

Simple lending Complex finance

Deal shaping and UW

Account servicing

Portfolio management

Syndication

Special assets management

Proj

ect

finan

ce

Com

mod

ityfin

ance

Stru

ctur

edfin

ance

Ass

etfin

ance

Trad

efin

ance

Secu

red

lend

ing

Uns

ecur

edle

ndin

g

Cons

umer

finan

ce

Application processing

Credit assessment

Account servicing

Portfolio management

Securitization

Collections and default

Leas

ing

Cred

it ca

rd

and

revo

lver

Smal

lbu

sine

ss

PaymentsPayments and transactions Information processing

Challenges

Description

Benefits

• Record the ownership of goods and services• Provide an unalterable record of the delivery and payment terms of a trade• List the identity of trading partners as needed for regulatory and tax compliance• Authenticate and validate contracts • Provide documentation for fraud

• Uncertainty about how, when and whether it will be adopted• Needs adoption by a large number and variety of stakeholders to achieve full benefits• More complex regulatory requirements regarding KYC, AML and CDD need to be addressed in a solution

• Reduce the time and expense required to manage supply chain financing• Simplify documentation by establishing a single source of trusted data• Eliminate opportunities for fraud and corrupt business practices

Wholesale credit products and processes

Simple lending Complex finance

Deal shaping and UW

Account servicing

Portfolio management

Syndication

Special assets management

Proj

ect

finan

ce

Com

mod

ityfin

ance

Stru

ctur

edfin

ance

Ass

etfin

ance

Trad

efin

ance

Secu

red

lend

ing

Uns

ecur

edle

ndin

g

Cons

umer

finan

ce

Application processing

Credit assessment

Account servicing

Portfolio management

Securitization

Collections and default

Leas

ing

Cred

it ca

rd

and

revo

lver

Smal

lbu

sine

ss

PaymentsPayments and transactions Information processing

Challenges

Description

Benefits

• Record the ownership of goods and services• Provide an unalterable record of the delivery and payment terms of a trade• List the identity of trading partners as needed for regulatory and tax compliance• Authenticate and validate contracts • Provide documentation for fraud

• Uncertainty about how, when and whether it will be adopted• Needs adoption by a large number and variety of stakeholders to achieve full benefits• More complex regulatory requirements regarding KYC, AML and CDD need to be addressed in a solution

• Reduce the time and expense required to manage supply chain financing• Simplify documentation by establishing a single source of trusted data• Eliminate opportunities for fraud and corrupt business practices

9

Key questions and opportunities for wholesale banksIT spendingUS banks have had to increase IT spending in response to these new FinTech challenges and investments and, in doing so, have focused on three areas:

1. Banks are driving higher operational efficiency by simplifying document management, workflow and business processes. These initiatives include better data management to facilitate regulatory compliance and reporting.

2. Banks are aiming to improve digital solutions and the overall client experience. This involves seamless unification across channels to deliver an “omnichannel” client experience, with a “single view of the client” that assists employees with serving and selling. Successful integration of digital channels promises to reduce costs and increase return on equity.

3. Banks have had to respond to challenging new cybersecurity threats by improving privacy and data protection measures.

InnovationGlobal banks have taken the following four strategies in the wake of the FinTech innovation:

1. Custom build: banks have pursued internal innovation projects related to areas such as digital transformation and process automation.

2. Acquisition/partnership: banks can purchase FinTech innovation outright with deals such as BBVA’s acquisition of Simple, Santander’s acquisition of Kredyt Bank (Poland) and Funding Circle, and Citibank’s acquisition of money-transfer service PayQuik.com.

3. Venture capital (VC): banks can provide capital to start-ups through strategic investment funds in areas ranging from digital delivery and online lending to online investment and big data analytics.

4. Incubator: banks can search for disruptive solutions and innovations by providing not only capital, but also mentoring, workshops, networking events and interim office space.

10Technology disruption and the future of wholesale banking |

Four key strategies for adopting FinTech innovations now and moving forward

The four primary strategies for banks to adopt FinTech innovations require varying levels of investment and offer different levels and speeds of return.

Time horizon: medium to long term

1Custom build

2Partner/buy

3VC model

4Incubator

Larger investment Smaller investment

The custom build strategy requires banks to use internal or third-party resources to design and build a custom version of the technology they wish to adopt.

Time horizon: short to medium term

The partner/buy strategy requires banks to purchaseor partner with one or more FinTech companies to gain access to the technologythey wish to adopt.

Time horizon: medium to long term

The VC model strategy requires banks to provide capital to FinTech start-ups. Both parties will profit from the FinTech’s success andhave the chance to pursuea partnership in the future.

Time horizon: long term

The incubator model strategy requires financial institutions to provide mentoring, workshops, office space and networking to start-ups working on disruptive innovations.

11 | Technology disruption and the future of wholesale banking

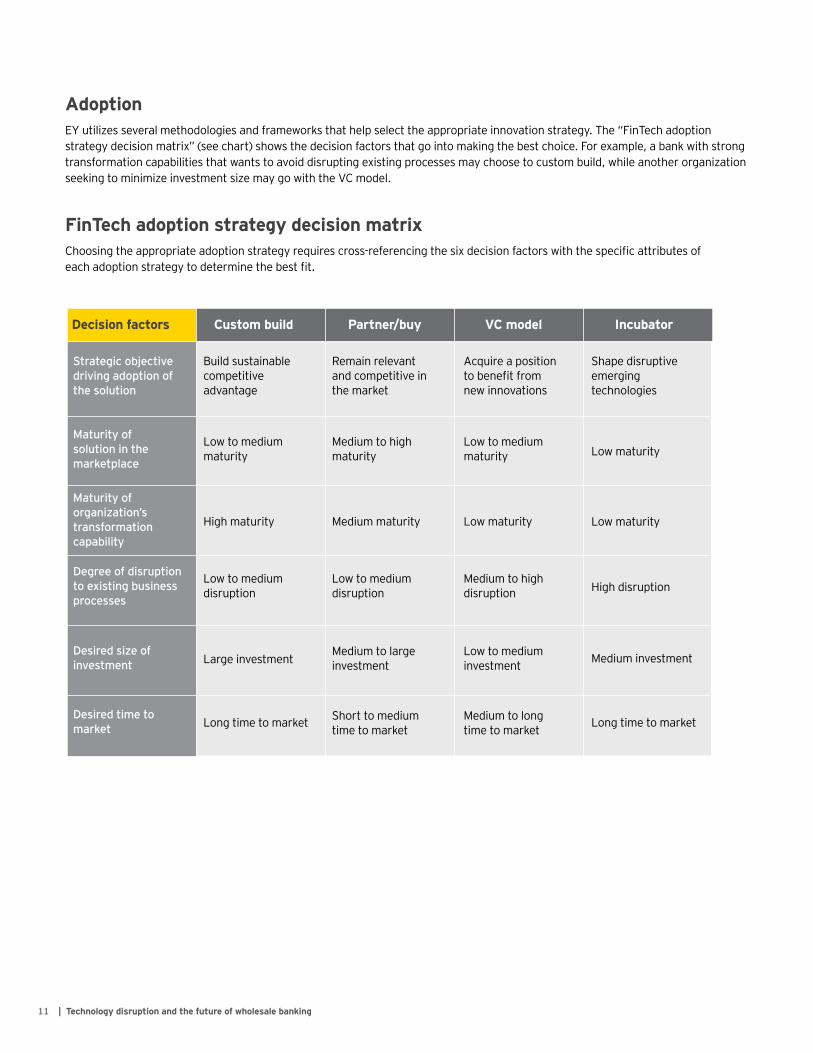

AdoptionEY utilizes several methodologies and frameworks that help select the appropriate innovation strategy. The “FinTech adoption strategy decision matrix” (see chart) shows the decision factors that go into making the best choice. For example, a bank with strong transformation capabilities that wants to avoid disrupting existing processes may choose to custom build, while another organization seeking to minimize investment size may go with the VC model.

Decision factors Custom build Partner/buy VC model Incubator

Strategic objective driving adoption of the solution

Build sustainable competitive advantage

Low to medium maturity

Low to medium disruption

Large investment

Long time to market Short to medium time to market

Medium to long time to market

Medium to large investment

Low to medium investment Medium investment

Low to medium disruption

Medium to high disruption High disruption

Low to medium maturity Low maturity

Low maturity

Medium to high maturity

Remain relevant and competitive in the market

Acquire a position to benefit from new innovations

Shape disruptive emerging technologies

Maturity of solution in the marketplace

Maturity of organization’s transformation capability

Degree of disruption to existing business processes

Desired size of investment

Desired time to market

Low maturityMedium maturityHigh maturity

Long time to market

FinTech adoption strategy decision matrixChoosing the appropriate adoption strategy requires cross-referencing the six decision factors with the specific attributes of each adoption strategy to determine the best fit.

12Technology disruption and the future of wholesale banking |

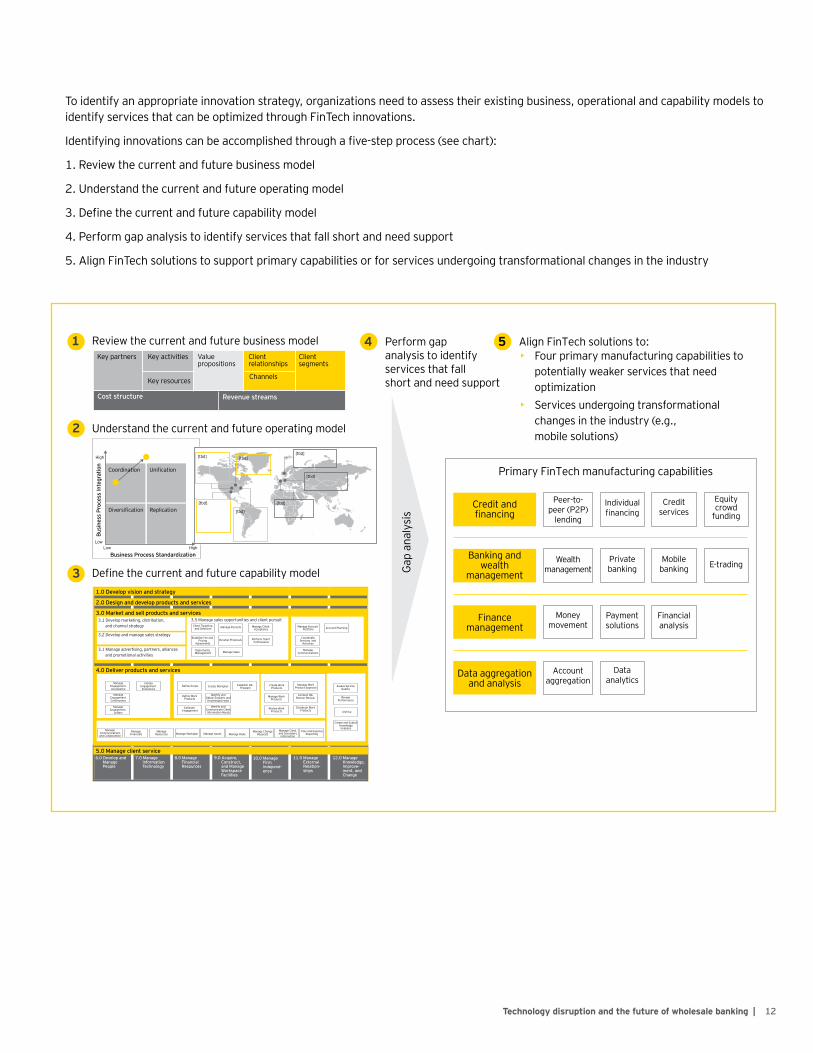

To identify an appropriate innovation strategy, organizations need to assess their existing business, operational and capability models to identify services that can be optimized through FinTech innovations.

Identifying innovations can be accomplished through a five-step process (see chart):

1. Review the current and future business model

2. Understand the current and future operating model

3. Define the current and future capability model

4. Perform gap analysis to identify services that fall short and need support

5. Align FinTech solutions to support primary capabilities or for services undergoing transformational changes in the industry

Banking andwealth

management

Accountaggregation

[tbd]

[tbd]

[tbd] [tbd]

[tbd]

[tbd][tbd]

Key partners

Coordination

High

HighLow

Low

Diversification

Business Process Standardization

1.0 Develop vision and strategy

2.0 Design and develop products and services

3.0 Market and sell products and services

4.0 Deliver products and services

5.0 Manage client service

Busi

ness

Pro

cess

Inte

grat

ion

Replication

Unification

Key activities

Cost structure Revenue streams

Valuepropositions

Key resources

ManageCommunicationsand Collaboration

Manage Account Portfolio Account Planning

CoordinateServices and

Activities

ManageCommunications

Client Targeting and Selection Manage Pursuits Manage Client

Acceptance

Establish Fee and Pricing

AgreementsDevelop Proposals

Opportunity Management Manage Sales

Perform Client Continuance

Define Scope Create Workplan Establish QA Program

Define Work Products

Identify andObtain Enablers and

KnowledgeCreate

Estimate Engagement

ManageEngagement Acceptance

InitiateEngagement

Economics

ManageEngagement Continuance

ManageFinancials

ManageResources Manage Workplan Manage Issues Manage Risks

Manage ChangeRequests

Manage Clientand Secondary

information

Time and ExpenseReporting

ManageEngagement

Letters

Identify and Communicate Client Information Needs

Create WorkProducts

Manage WorkProduct Approval

Manage WorkProducts

Conduct QAPartner Review

Review WorkProducts

Distribute WorkProducts

Assess ServiceQuality

ReviewPerformance

Archive

Create and SubmitKnowledgeEnablers

Clientrelationships

Credit andfinancing

Peer-to-peer (P2P)

lending

Individualfinancing

Financemanagement

Data aggregationand analysis

Clientsegments

Channels

Review the current and future business model

Understand the current and future operating model

Define the current and future capability model

1

Gap

anal

ysis

2

Perform gap analysis to identify services that fall short and need support

Primary FinTech manufacturing capabilities

4

3

Align FinTech solutions to:5• Four primary manufacturing capabilities to

potentially weaker services that need optimization

• Services undergoing transformational changes in the industry (e.g., mobile solutions)

Credit services

Equity crowd

funding

Wealthmanagement

Privatebanking

Mobilebanking E-trading

Moneymovement

Paymentsolutions

Financialanalysis

Data analytics

3.1 Develop marketing, distribution,and channel strategy

3.5 Manage sales opportunities and client pursuit

3.2 Develop and manage sales strategy

3.1 Manage advertising, partners, alliances and promotional activities

6.0 Develop and Manage People

7.0 Manage Information Technology

8.0 Manage Financial Resources

9.0 Acquire, Construct, and Manage Workspace Facilities

10.0 Manage Firm Independ-ence

11.0 Manage External Relation-ships

12.0 Manage Knowledge, Improve-ment, and Change

13 | Technology disruption and the future of wholesale banking

RegulationFinTech regulation is an evolving concept; accordingly, implementation timeline and level of regulation will be subject to factors that include client exposure, time and regulatory bodies’ understanding of FinTech firms.

As one example of the regulatory gap, P2P lending is not regulated at the federal level by a single regulator. Nevertheless, there has been some federal oversight, and in 2008, the U.S. Securities and Exchange Commission required P2P companies to register their offerings as securities.

Some regulations are emerging on the state level, and this has affected the growth of FinTech firms. Generally speaking, what happens next depends on whether federal and state governments begin regulating FinTech companies more like banks, or whether they try to foster further FinTech innovation by reining in compliance efforts.

Generally speaking, what happens next depends on whether federal and state governments begin regulating FinTech companies more like banks, or whether they try to foster further FinTech innovation by reining in compliance efforts.

ConclusionAlthough FinTech start-ups and nonbank players may have sparked the present wave of innovation, traditional wholesale banks still have immense opportunities. By building services for existing clients while drawing upon their unmatched industry knowledge, regulatory expertise and market presence, today’s traditional banks have the capability to reshape the industry.

Marketplace lending and blockchain applications remain key focus areas, but there are numerous other areas of interest, including applications for artificial intelligence. Yet before diving into these technologies, wholesale banks should take a step back to evaluate their readiness for innovation.

As outlined above, IT spending needs to support improved operations, omnichannel client experiences and cybersecurity improvements. Then, banks need to evaluate whether they are best positioned to build their own solutions, acquire technology, or invest as VC partners or through incubator funding. Finally, banks should evaluate their own current and future business and operating models to determine which innovations should be given priority toward the transformation of the industry.

By establishing a foundation for continual innovation, wholesale banks can not only fend off the competitive threat posed by FinTech start-ups and nonbank players — they can set the pace for ongoing success.

Whatever happens next, the evolution of existing rules to accommodate new business models will affect FinTech companies and the traditional banking industry in different ways. As such, banks should be ready with the flexibility to take advantage of new opportunities while maintaining the discipline to protect the balance sheet through any market turbulence. To that end, EY recommends that banks:

• Evaluate FinTech company controls and compliance. Before entering a partnership with a FinTech firm, make certain that it has sufficient compliance capabilities. This should be considered to be a prerequisite to forming a partnership or making a VC investment.

• Incorporate compliance into incubation. Compliance support should be a core component of a FinTech incubator and a key consideration during development of business models and products.

• Consider providing compliance as a service. If your bank has a sufficiently flexible operating model for compliance, you may be able to extend those capabilities to FinTech providers. Already, FinTech firms are starting to work with a new breed of FinTech-focused companies (e.g., CompliTech) that offer compliance as a service. However, these offerings are in the very early stages and still require testing and extensive manual intervention. That’s why banks now have an opportunity to support FinTech firms with compliance services as part of a more comprehensive relationship, including access to FinTech technologies and business models.

14Technology disruption and the future of wholesale banking |

How can EY help?In a digital world, our clients recognize the need to adapt and innovate in order to grow. EY’s wholesale banking advisory services comprises professionals with experience across commercial lending, transaction banking, treasury and cash management products, covering domains such as operations, technology, digital and robotics, risk and compliance, and data and analytics. Our team members have prior industry experience as underwriters, lenders, credit officers, treasury and payments senior managers, and bank examiners.

EY is a leader in blockchain technology and in the FinTech industry. EY has launched its global network of growth and innovation centers to help clients catch the next wave in radical breakthroughs in business transformation by tapping into innovative thinking across EY disciplines, experience and industry sectors. In addition, we have several active partnerships and collaborations within the FinTech industry, both as an investor and an innovator. We continually monitor the market for potential innovations. This market research enables companies to support or accelerate the achievement of specific elements of their strategic plan.

Our FinTech practice works with banks to:

• Evaluate their own FinTech capabilities

• Identify functionality gaps

• Analyze marketplace competitors

• Develop a strategic plan and road map

• Evaluate opportunities for partnerships and acquisitions

• Integrate new business units into existing infrastructure

• Optimize processes

• Reduce risksErnst & Young LLP contacts

Ryan Battles +1 704 258 7756 [email protected]

Matt Cox +1 704 280 4327 [email protected]

Angus Champion de Crespigny +1 212 773 6717 [email protected]

David Demsko +1 704 338 0671 [email protected]

David Heiner +1 212 773 6074 [email protected]

Matt Hatch +1 415 894 8219 [email protected]

EY | Assurance | Tax | Transactions | Advisory

About EYEY is a global leader in assurance, tax, transaction and advisoryservices. The insights and quality services we deliver help build trust andconfidence in the capital markets and in economies the world over. Wedevelop outstanding leaders who team to deliver on our promises to allof our stakeholders. In so doing, we play a critical role in building a betterworking world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, ofthe member firms of Ernst & Young Global Limited, each of which is aseparate legal entity. Ernst & Young Global Limited, a UK company limitedby guarantee, does not provide services to clients. For more informationabout our organization, please visit ey.com.

EY is a leader in serving the global financial services marketplaceNearly 51,000 EY financial services professionals around the world provide integrated assurance, tax, transaction and advisory services to our asset management, banking, capital markets and insurance clients. In the Americas, EY is the only public accounting organization with a separate business unit dedicated to the financial services marketplace. Created in 2000, the Americas Financial Services Organization today includes more than 11,000 professionals at member firms in over 50 locations throughout the US, the Caribbean and Latin America.

EY professionals in our financial services practices worldwide align with key global industry groups, including EY’s Global Wealth & Asset Management Center, Global Banking & Capital Markets Center, Global Insurance Center and Global Private Equity Center, which act as hubs for sharing industry-focused knowledge on current and emerging trends and regulations in order to help our clients address key issues. Our practitioners span many disciplines and provide a well-rounded understanding of business issues and challenges, as well as integrated services to our clients.

With a global presence and industry-focused advice, EY’s financial services professionals provide high-quality assurance, tax, transaction and advisory services, including operations, process improvement, risk and technology, to financial services companies worldwide.

© 2018 EYGM Limited. All Rights Reserved.

EYG no. 00190-181Gbl1705-2289204 BDFSOED None

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other professional advice. Please refer to your advisors for specific advice.

ey.com

1 Source: https://thefinancialbrand.com/55543/partnership-competition-fintech-banking-disruption/

2 Source: “FinTech at a Glance,” Venture Scanner, 15 October 2015, https://venturescannerinsights.wordpress.com/2015/10/15/fintech-at-a-glance/.