technologies for the conversion of unconventional...

TRANSCRIPT

Technologies For Conversion Of Unconventional and Renewable Feedstocks From BP

Philip M J Hill, BP International

Disclaimer

2

Copyright © 2013 , 2014 BP plc. All rights reserved. Contents of this presentation do not necessarily reflect the Company’s views.

This presentation and its contents have been provided to you for informational purposes only. This information is not advice on or a recommendation of any of the matters described herein or any related commercial transactions.

BP is not responsible for any inaccuracies in the information contained herein. BP makes no representations or warranties, express or implied, regarding the accuracy, adequacy, reasonableness or completeness of the information, assumptions or analysis contained herein or in any supplemental materials, and BP accepts no liability in connection therewith. BP deals and trades in energy related products and may have positions consistent with or different from those implied or suggested by this presentation.

This presentation also contains forward-looking statements. Any statements that are not historical facts, including statements about BP's beliefs or expectations, are forward-looking statements. These statements are based mostly on publicly available information, estimates and projections and you should not place undue reliance on them. These statements are not guarantees of future performance and involve certain risks and uncertainties, which are difficult to predict. Therefore, actual future results and trends may differ materially from what is forecast, suggested or implied in any forward-looking statements in this presentation due to a variety of factors. Factors which could cause actual results to differ from these forward-looking statements may include, without limitation, general economic conditions; conditions in the markets; behaviour of customers, suppliers, and competitors; technological developments; the implementation and execution of new processes; and changes to legal, tax, and regulatory rules. The foregoing list of factors should not be construed as exhaustive. BP disclaims any intention or obligation to publicly or privately update or revise any forward-looking statements, whether as a result of new information, future events, or otherwise.

Participants should seek their own advice and guidance from appropriate legal, tax, financial and trading professionals when making decisions as to positions to take in the market.

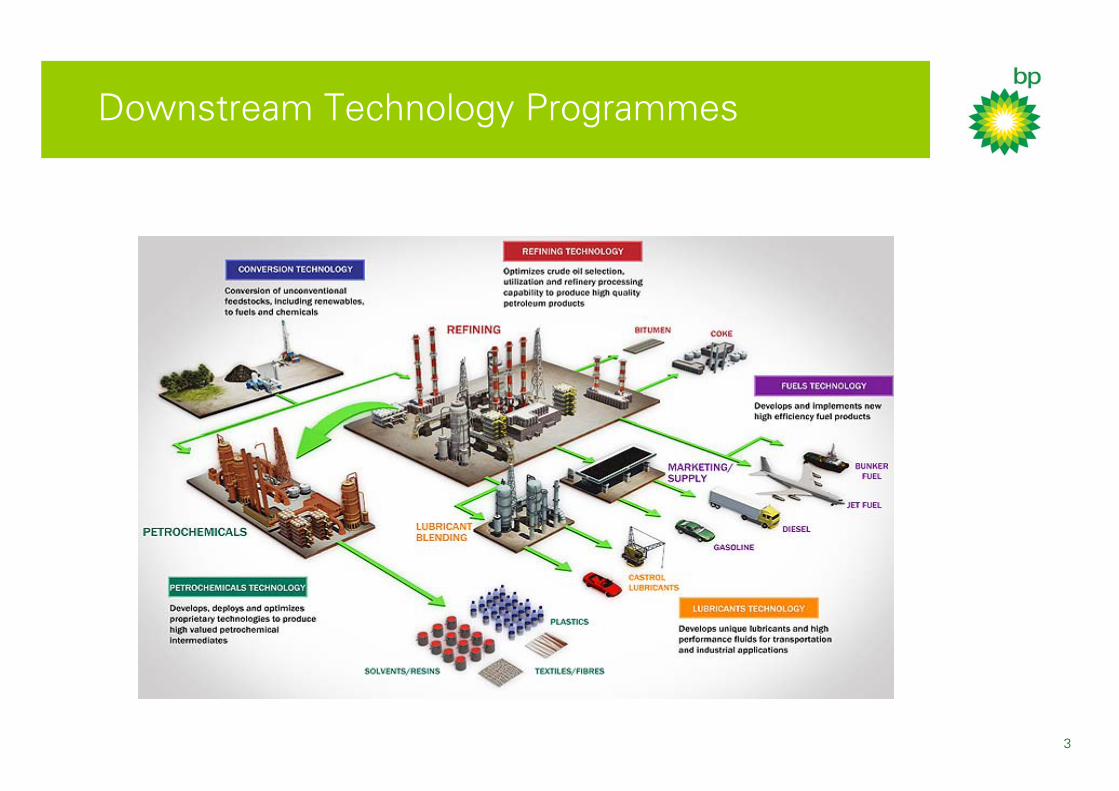

Downstream Technology Programmes

3

4

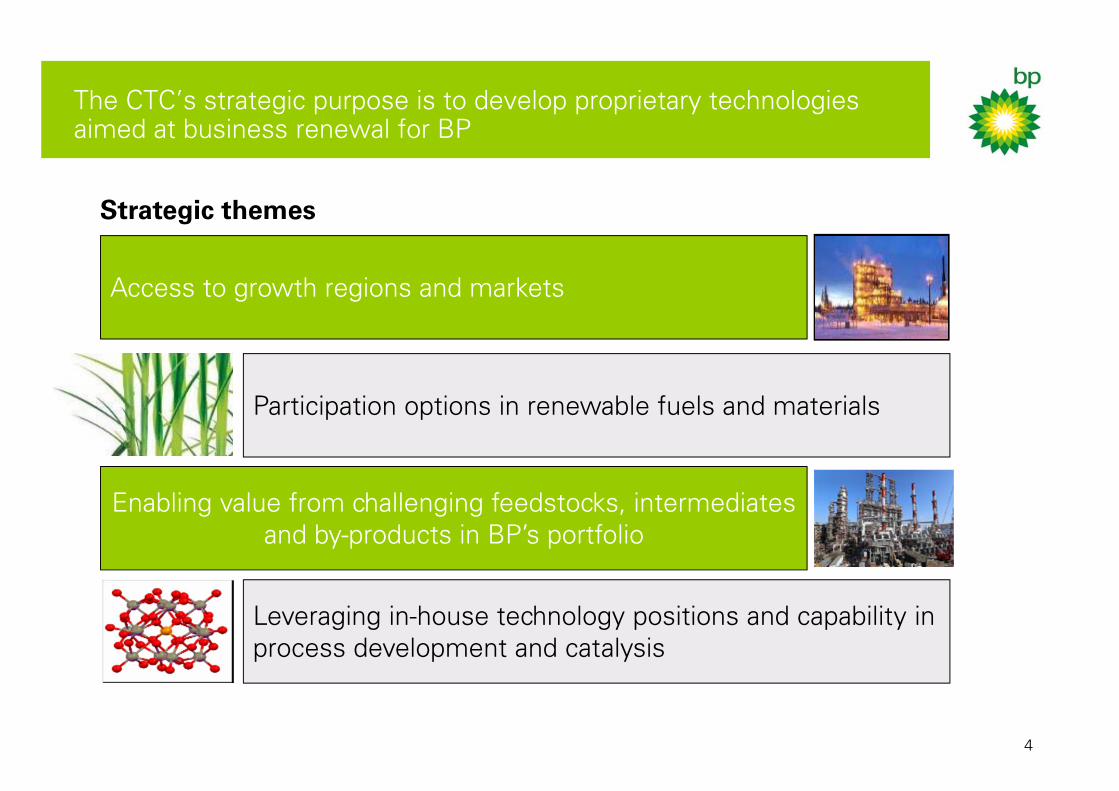

The CTC’s strategic purpose is to develop proprietary technologies aimed at business renewal for BP

Strategic themes

Access to growth regions and markets

Participation options in renewable fuels and materials

Enabling value from challenging feedstocks, intermediates and by-products in BP’s portfolio

Leveraging in-house technology positions and capability in process development and catalysis

CTC is licensing four technologies with its collaboration partners

5

Veba

Com

bi-C

rack

ing

(VC

CTM

)

• A slurry phase hydrocracking/hydrogenation process for converting petroleum residues and coal into directly marketable lighter products

• Our VCCTM technology was operated at commercial scale from 1981 – 2000 in 3.5k bpd unit in Bottrop, Germany

• 4 licenses sold, first commercial plant start up 2014

Com

pact

Ref

orm

er &

Fis

cher

-Tro

psch

• Conversion from biomass, natural gas, coal and or petcokevia syngas to diesel and naphtha at a split of 80% and 20%

• Demonstration plant at 300 barrels/ day scale

• Compact reformer, has innovative mechanical design reducing size and weight.

Hum

min

gbird

®

• Ultra-selective second generation ethanol dehydration technology

• Fully recycling pilot plant

• Identification of a collaboration licensor

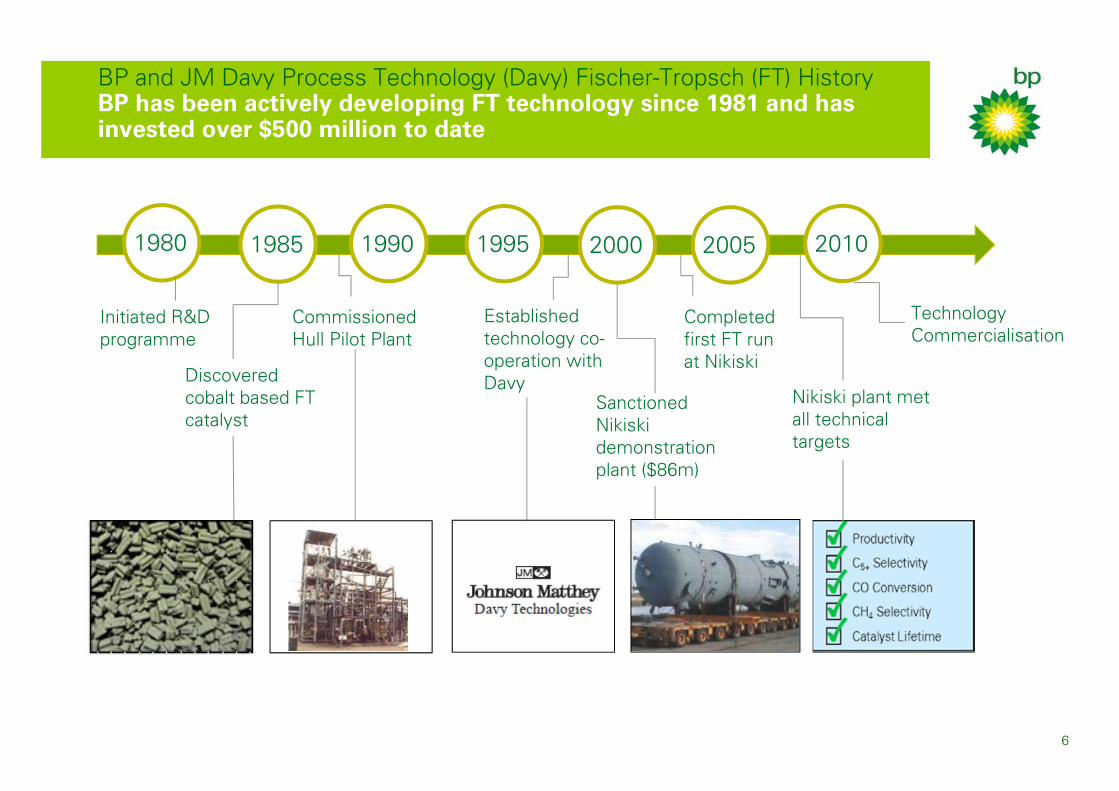

BP and JM Davy Process Technology (Davy) Fischer-Tropsch (FT) HistoryBP has been actively developing FT technology since 1981 and has invested over $500 million to date

6

1980 1985 19951990 2000 2005 2010

Initiated R&D programme

Discovered cobalt based FT catalyst

Commissioned Hull Pilot Plant

Established technology co-operation with Davy

Sanctioned Nikiski demonstration plant ($86m)

Completed first FT run at Nikiski

Nikiski plant met all technical targets

Technology Commercialisation

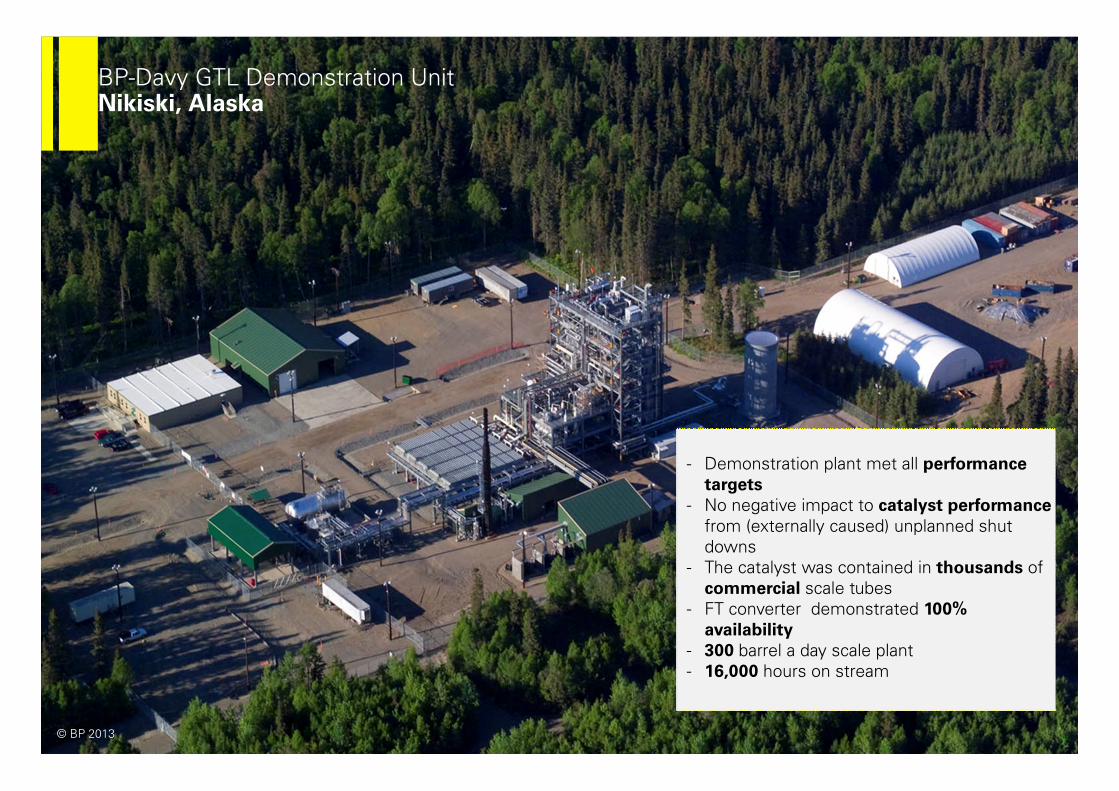

BP-Davy GTL Demonstration UnitNikiski, Alaska

7© BP 2013

- Demonstration plant met all performancetargets

- No negative impact to catalyst performancefrom (externally caused) unplanned shut downs

- The catalyst was contained in thousands of commercial scale tubes

- FT converter demonstrated 100% availability

- 300 barrel a day scale plant- 16,000 hours on stream

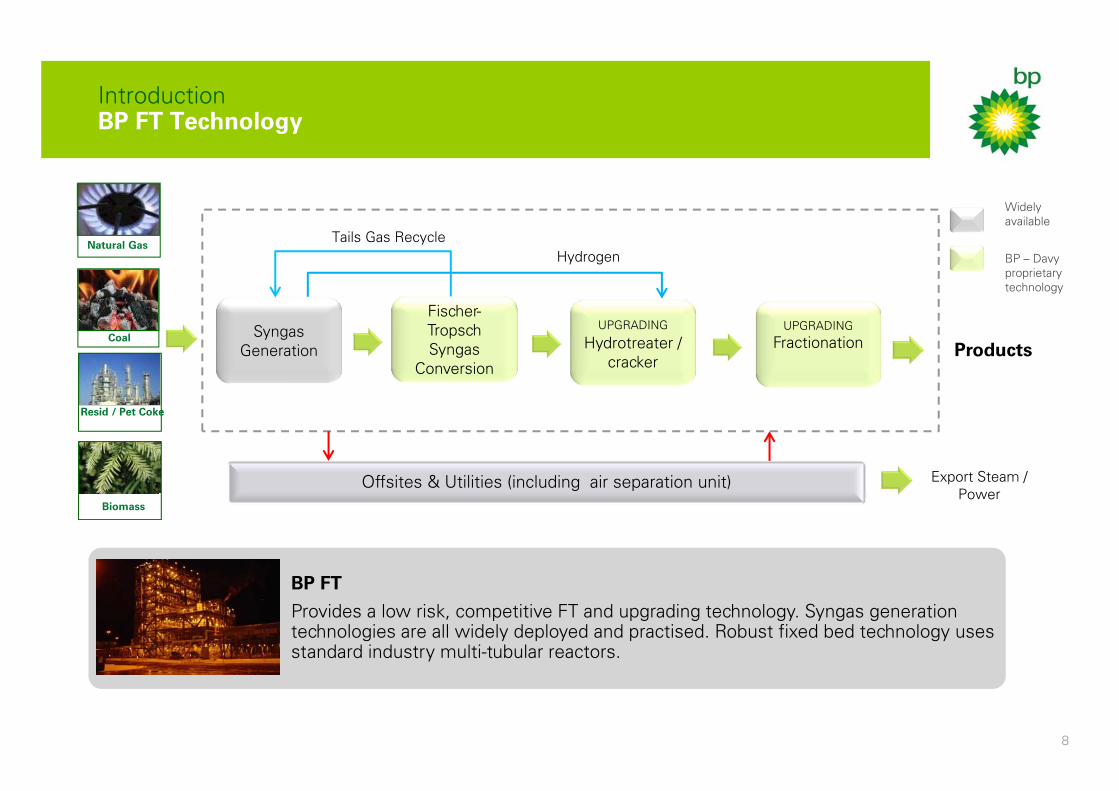

IntroductionBP FT Technology

8

Natural Gas

Coal

Biomass

Resid / Pet Coke

Export Steam / Power

BP FT

Provides a low risk, competitive FT and upgrading technology. Syngas generation technologies are all widely deployed and practised. Robust fixed bed technology uses standard industry multi-tubular reactors.

Syngas Generation

Fischer-Tropsch Syngas

Conversion

UPGRADING

Hydrotreater / cracker

UPGRADING

Fractionation

Offsites & Utilities (including air separation unit)

Products

HydrogenTails Gas Recycle

Widely available

BP – Davy proprietary technology

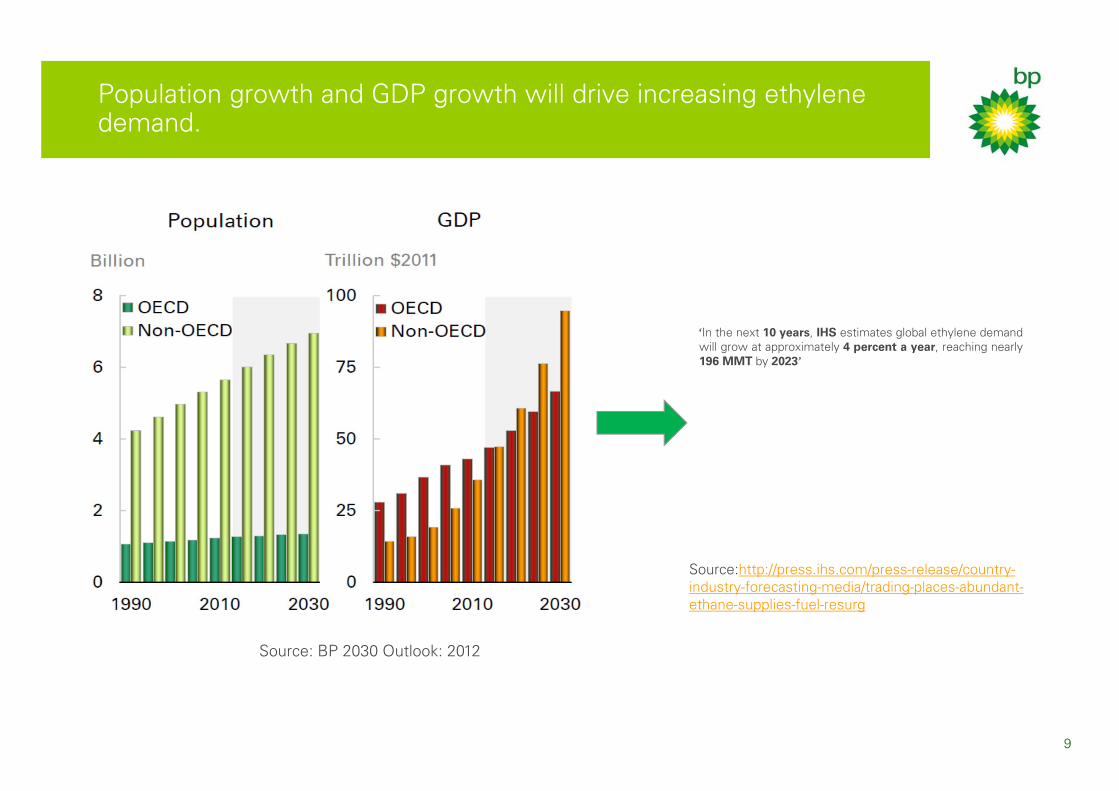

Population growth and GDP growth will drive increasing ethylene demand.

9

‘In the next 10 years, IHS estimates global ethylene demandwill grow at approximately 4 percent a year, reaching nearly196 MMT by 2023’

Source: BP 2030 Outlook: 2012

Source:http://press.ihs.com/press-release/country-industry-forecasting-media/trading-places-abundant-ethane-supplies-fuel-resurg

10

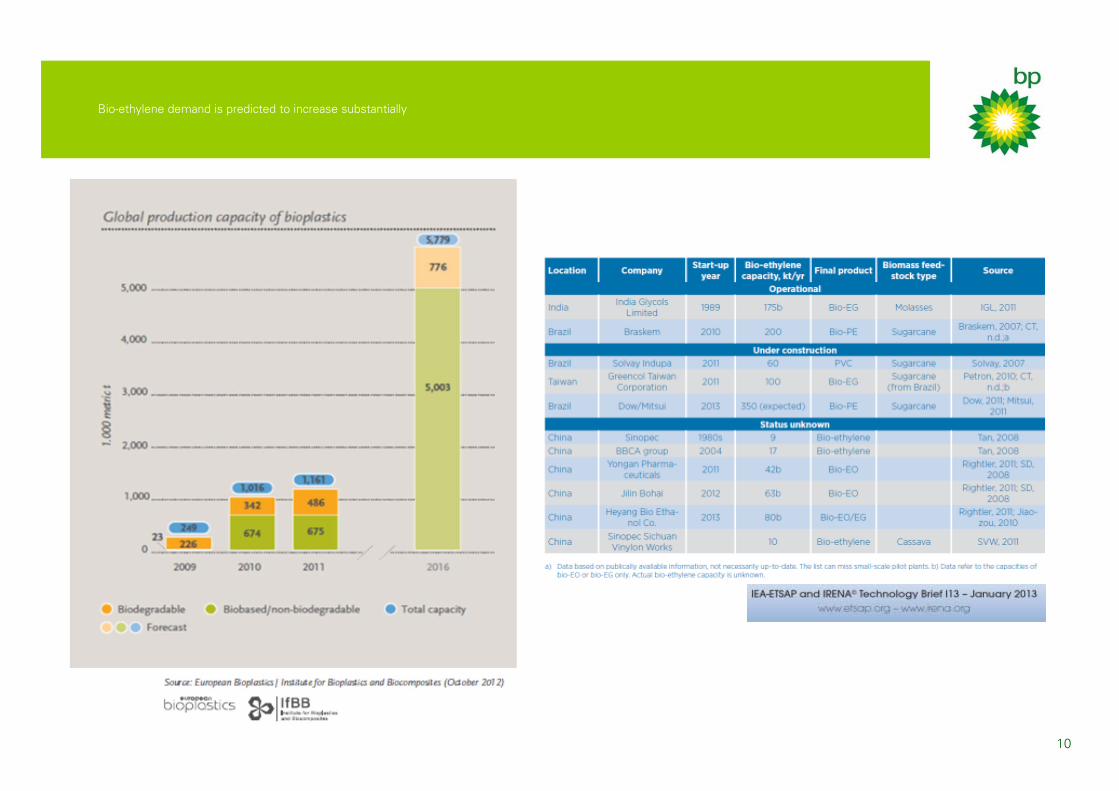

Bio-ethylene demand is predicted to increase substantially

According to the Intergovernmental Panel on Climate Change (IPCC), warming of the climate system is happening. Over the next 20 years, it’s predicted that global energy demand will increase by nearly 40%.

What is driving bio-ethylene demand?

Change in consumer attitudes

Energy demand and Global warming

Awareness of sustainability and global warming has affected consumer preferences creating a market for ‘green products’ where premiums of up to 30% for bio-MEG2 have been publically stated.

1. IEA-ETSAP and IRENA© Technology Brief I13 – January 20132. ICIS news; 09 May 2013 ; APIC '13: Greencol Taiwan Corp to keep 67% ops at bio-EG units

Bio-ethylene product creates substantial environmental benefits

Referencing the International Renewable Energy Agency’s (IRENA) paper; ‘bio-ethylene can reduce GHG emissions by up to 40% and save fossil energy by up to 60% compared to petrochemical ethylene’1 .

11

12

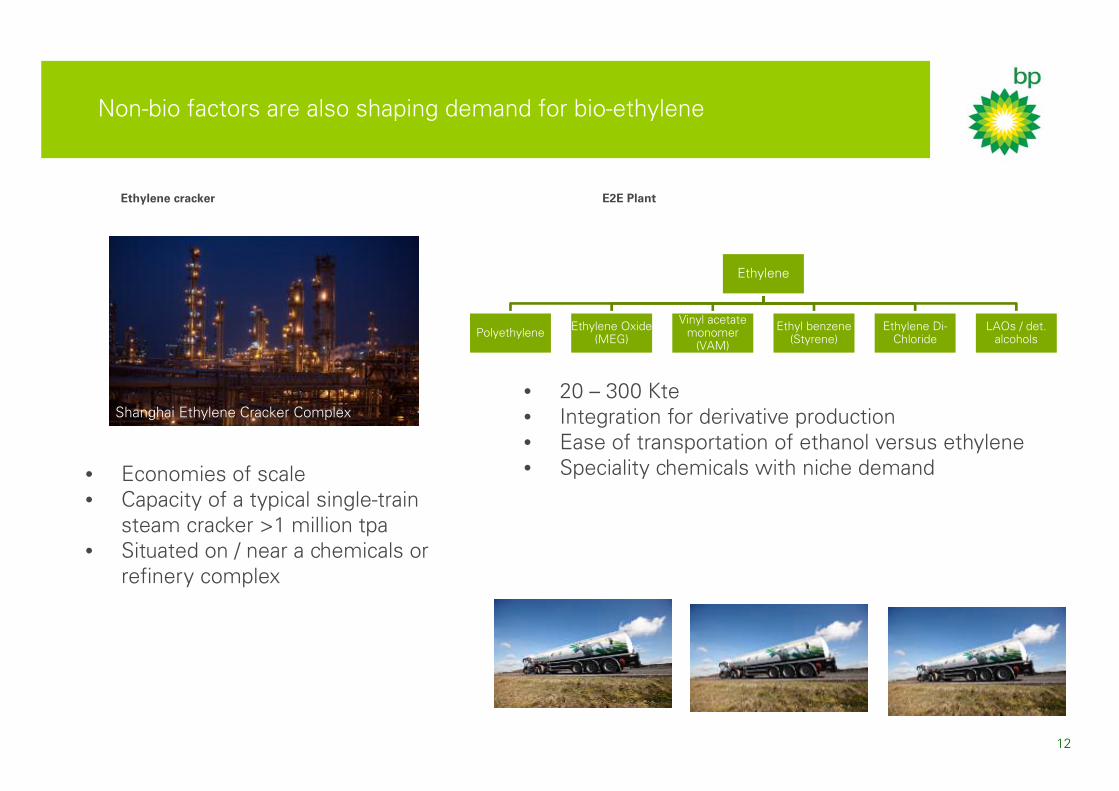

Ethylene cracker E2E Plant

• Economies of scale• Capacity of a typical single-train

steam cracker >1 million tpa• Situated on / near a chemicals or

refinery complex

• 20 – 300 Kte• Integration for derivative production• Ease of transportation of ethanol versus ethylene• Speciality chemicals with niche demand

Ethylene

Polyethylene Ethylene Oxide (MEG)

Vinyl acetate monomer

(VAM)

Ethyl benzene (Styrene)

Ethylene Di-Chloride

LAOs / det. alcohols

Shanghai Ethylene Cracker Complex

Non-bio factors are also shaping demand for bio-ethylene

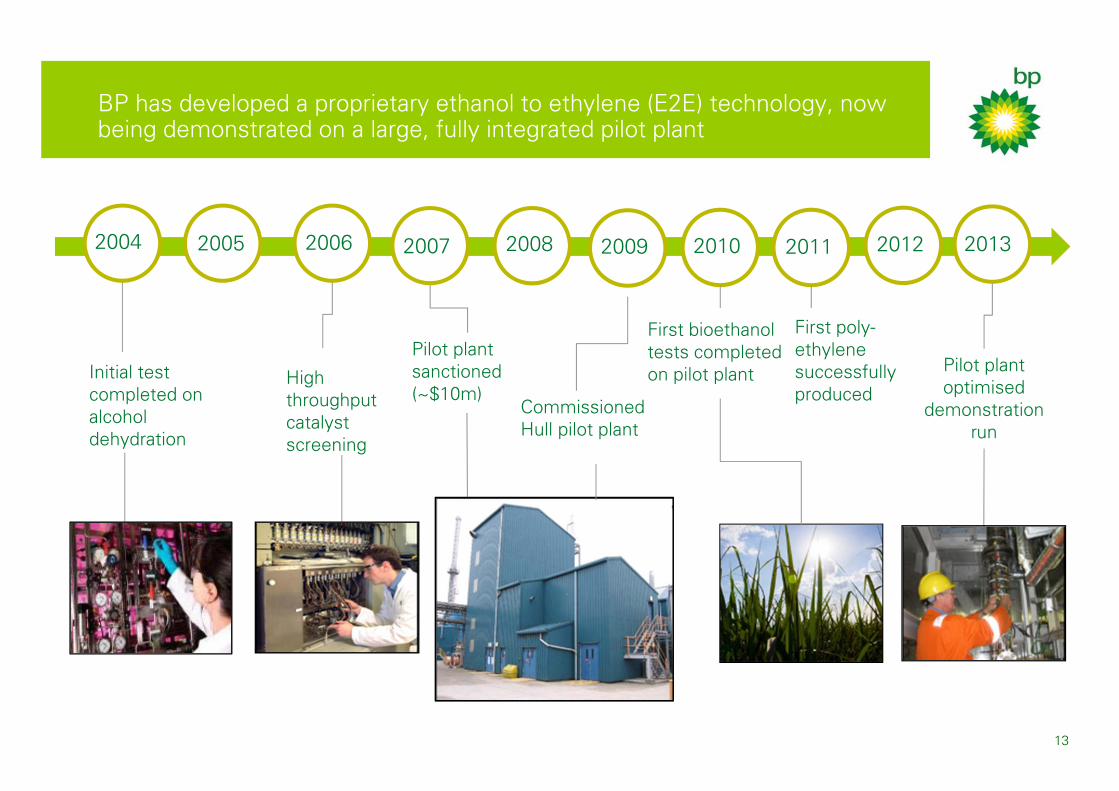

BP has developed a proprietary ethanol to ethylene (E2E) technology, now being demonstrated on a large, fully integrated pilot plant

13

Initial test completed on alcohol dehydration

Commissioned Hull pilot plant

High throughput catalyst screening

First bioethanol tests completed on pilot plant Pilot plant

optimised demonstration

run

Pilot plant sanctioned (~$10m)

20072005 2008 2011 20132004 2006 2009 20122010

First poly-ethylene successfully produced

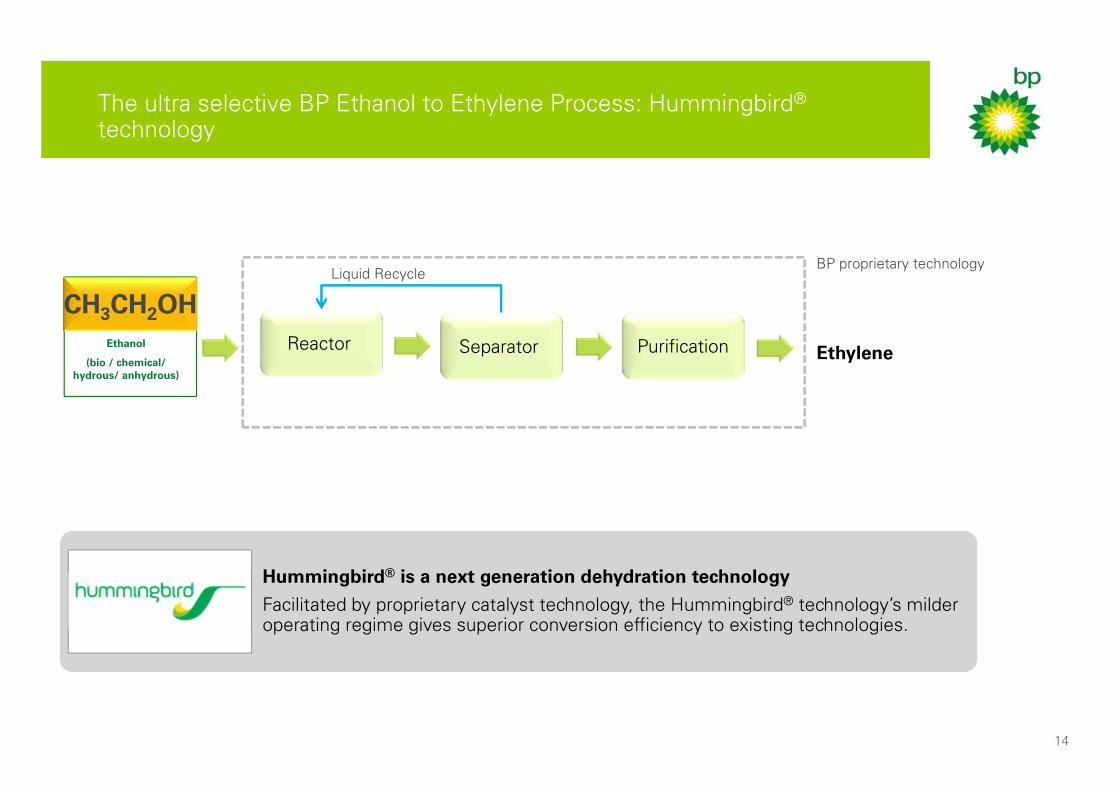

The ultra selective BP Ethanol to Ethylene Process: Hummingbird®

technology

14

Ethanol

(bio / chemical/ hydrous/ anhydrous)

Reactor Separator Purification

Liquid Recycle

Ethylene

BP proprietary technology

CH3CH2OH

Hummingbird® is a next generation dehydration technology

Facilitated by proprietary catalyst technology, the Hummingbird® technology’s milder operating regime gives superior conversion efficiency to existing technologies.

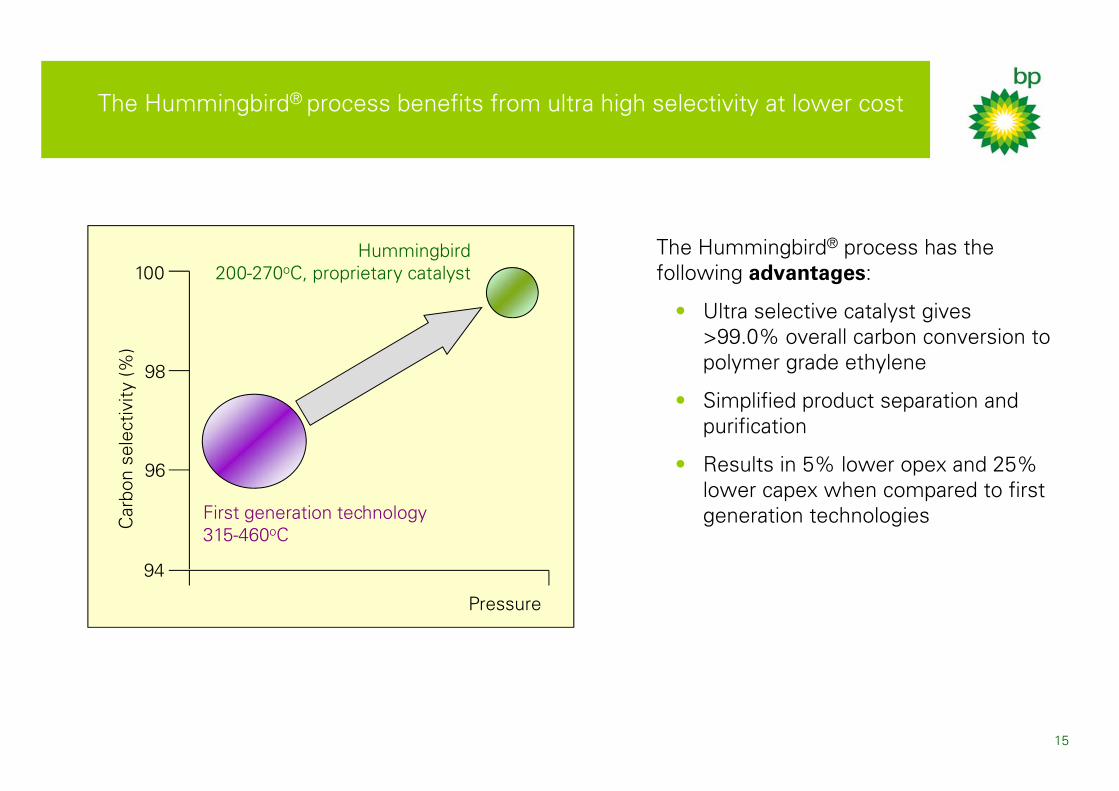

The Hummingbird® process benefits from ultra high selectivity at lower cost

15

The Hummingbird® process has the following advantages:

• Ultra selective catalyst gives >99.0% overall carbon conversion to polymer grade ethylene

• Simplified product separation and purification

• Results in 5% lower opex and 25% lower capex when compared to first generation technologiesC

arbo

n se

lect

ivity

(%)

Pressure

Hummingbird200-270oC, proprietary catalyst

First generation technology315-460oC

94

100

96

98

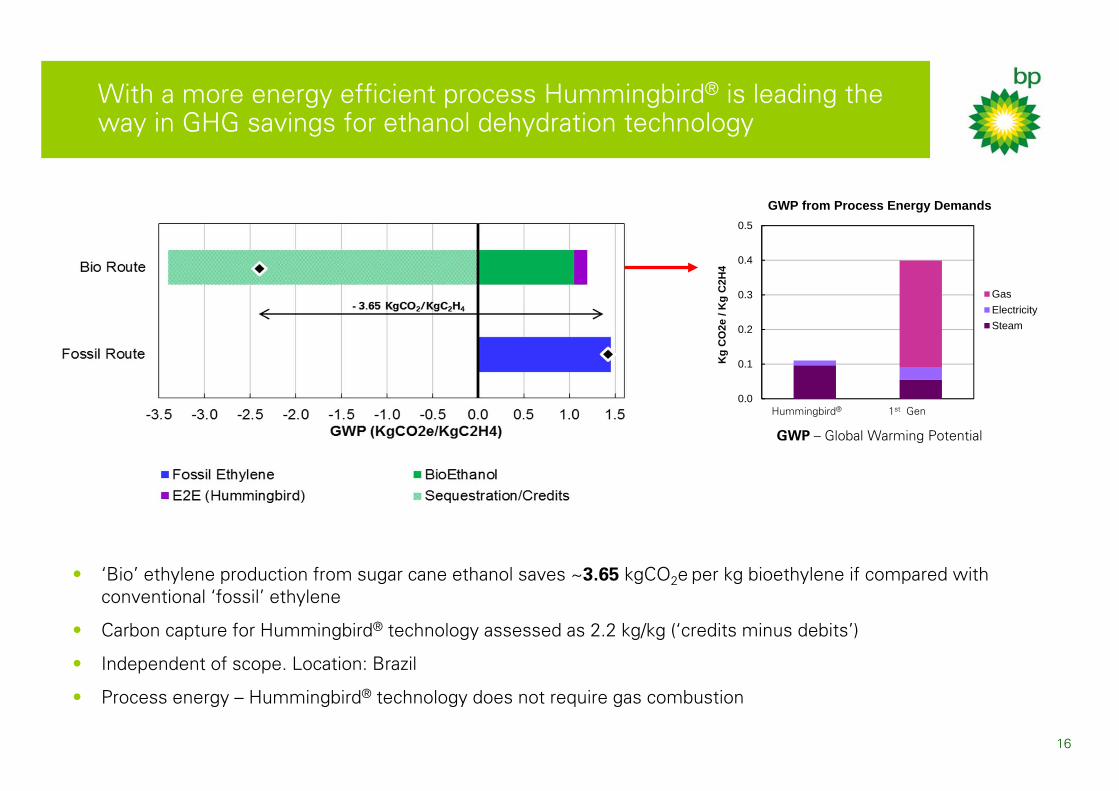

With a more energy efficient process Hummingbird® is leading the way in GHG savings for ethanol dehydration technology

16

• ‘Bio’ ethylene production from sugar cane ethanol saves ~3.65 kgCO2e per kg bioethylene if compared with conventional ‘fossil’ ethylene

• Carbon capture for Hummingbird® technology assessed as 2.2 kg/kg (‘credits minus debits’)

• Independent of scope. Location: Brazil

• Process energy – Hummingbird® technology does not require gas combustion

0.0

0.1

0.2

0.3

0.4

0.5

Kg

CO

2e /

Kg

C2H

4

GWP from Process Energy Demands

GasElectricitySteam

GWP – Global Warming Potential

Hummingbird® 1st Gen

17

Philip M J Hill Project ManagerConversion Technology Centre

BP International LtdChertsey RoadSunbury-on-ThamesMiddlesex TW16 7LNUnited Kingdom

Direct +44 203 401 2177Mobile +44 7825 [email protected]

MEng CEng MIChemE