technical assistance performance audit report … · technical assistance performance audit report...

TRANSCRIPT

ASIAN DEVELOPMENT BANK TPA:PAK 2003-02

TECHNICAL ASSISTANCE PERFORMANCE AUDIT REPORT

ON

SELECTED ADVISORY TECHNICAL ASSISTANCE

FOR

CAPITAL MARKET DEVELOPMENT

IN PAKISTAN

January 2003

Currency Equivalent

Currency Unit – Pakistan rupee (PRe/PRs)

TA 2393–PAK

At TA Approval

(September 1995)

At TA Completion

(February 2000)

At Operations Evaluation

(April 2002) PRe1.00 =

0.3184890

0.0192771

0.0166251

$1.00 = 31.3983 51.8750 60.1500 TA 2812–PAK

(June 1997)

(June 1999)

(April 2002) PRe1.00 =

0.0246968

0.0193330

0.0166251

$1.00 = 40.4910 51.7250 60.1500 TA 2825–PAK

(July 1997)

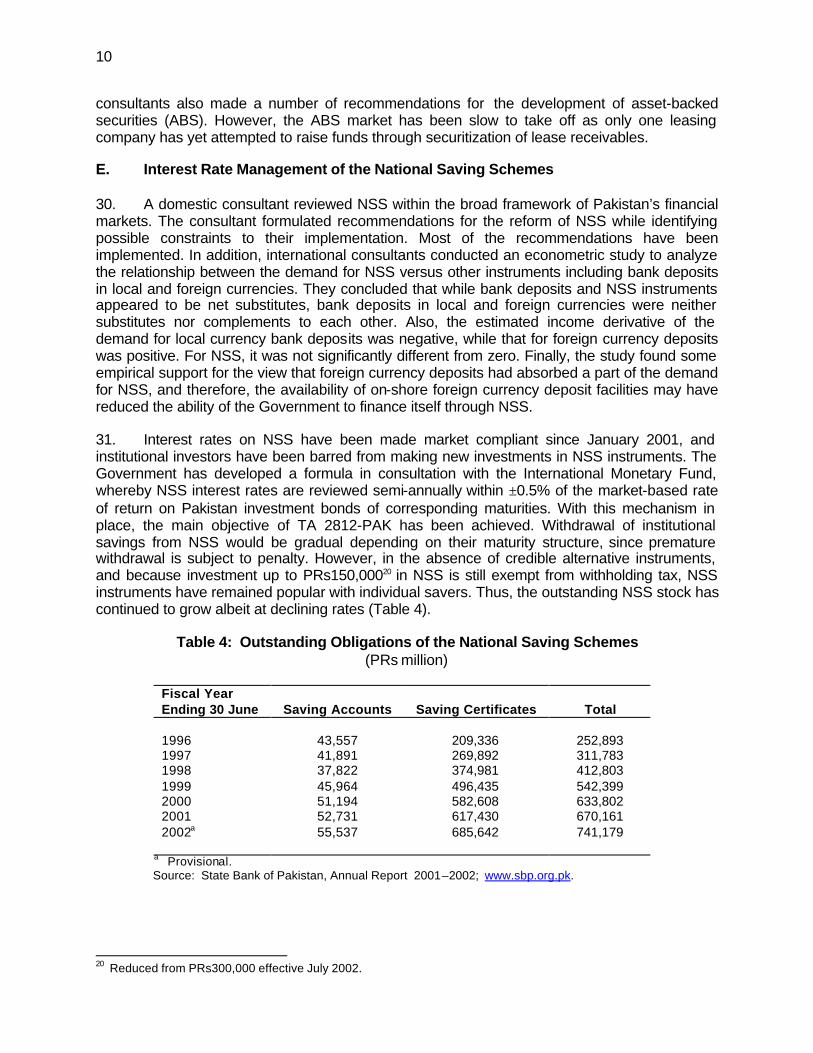

(March 1999)

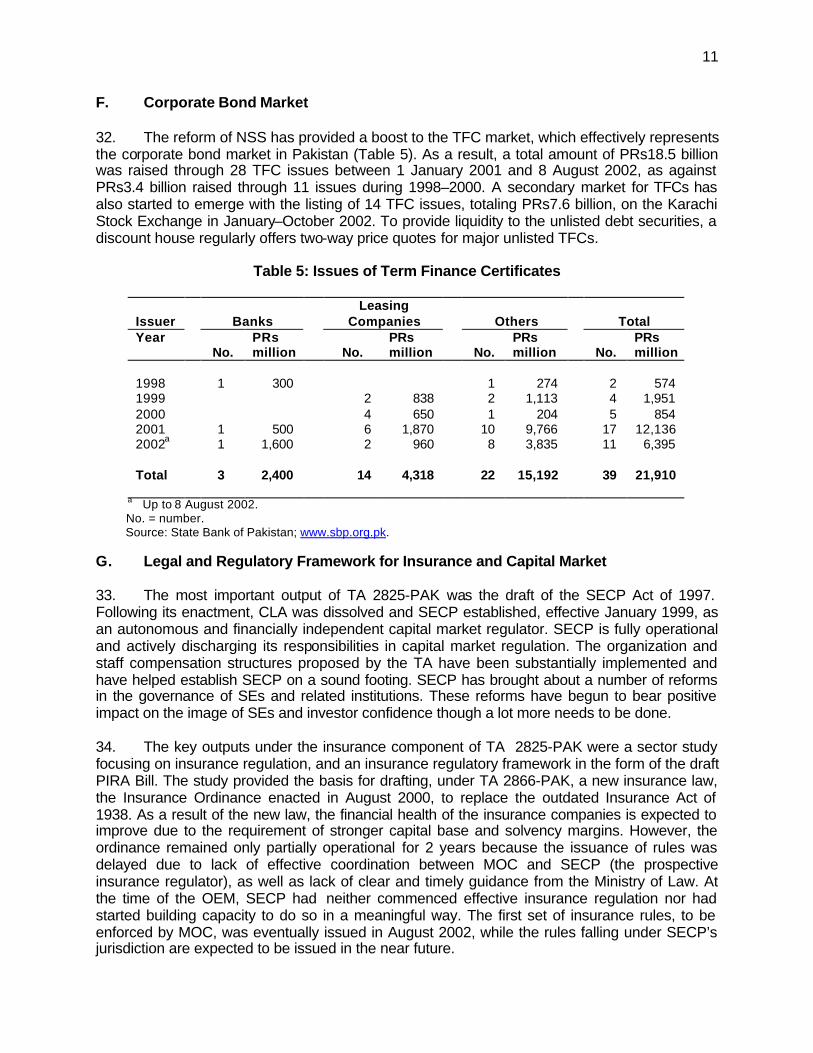

(April 2002) PRe1.00 =

0.0246176

0.0195217

0.0166251

$1.00 = 40.6213 51.2250 60.1500 TA 2865–PAK

(September 1997)

(May 1999)

(April 2002) PRe1.00 =

0.0246176

0.0197531

0.0166251

$1.00 = 40.6213 50.6250 60.1500 TA 2866–PAK

(September 1997)

(August 2000)

(April 2002) PRe1.00 =

0.0246176

0.0187266

0.0166251

$1.00 = 40.6213 53.4000 60.1500 TA 2867–PAK

(September 1997)

(June 2001)

(April 2002) PRe1.00 =

0.0246176

0.0156863

0.0166251

$1.00 = 40.6213 63.7500 60.1500

NOTES

(i) The fiscal year (FY) of the Government ends on 30 June. FY before a calendar year denotes the year in which the FY ends. For example, FY2002 begins on 1 July 2001 and ends on 30 June 2002.

(ii) In this report, “$” refers to US dollars.

Operations Evaluation Department, TE-44

ABBREVIATIONS

ABS – asset-backed securities ADB – Asian Development Bank CLA – Corporate Law Authority CMD – capital market development CMDP – Capital Market Development Program EOBI – Employees’ Old-Age Benefits Institution FMGP – Financial (Nonbank) Markets and Governance Program ICP – Investment Corporation of Pakistan MF – mutual fund MOC – Ministry of Commerce MOF – Ministry of Finance NIC – National Insurance Corporation NIT – National Investment Trust NSS – National Saving Schemes OEM – Operations Evaluation Mission PII – Pakistan Insurance Institute PIC – Pakistan Insurance Corporation PIRA -- Pakistan Insurance Regulatory Authority PRC – Pakistan Reassurance Corporation PSIE -- public sector insurance entity SE – stock exchange SECP – Securities and Exchange Commission of Pakistan TA – technical assistance TCR – technical assistance completion report TFC – term finance certificate TOR – terms of reference TPAR – technical assistance performance audit report

CONTENTS

Page BASIC TECHNICAL ASSISTANCE DATA EXECUTIVE SUMMARY

ii vi

I. INTRODUCTION 1 A. Background 1 B. Rationale and Concept 1 C. Objectives and Scope 2 D. Completion and Self Evaluation 3 E. Operations Evaluation 3 II. ASSESSMENT OF DESIGN AND IMPLEMENTATION 3 A. Design 3 B. Engagement of Consultants 5 C. Implementation and Cost 5 D. Organization and Management 6 III. EVALUATION OF OUTPUTS AND IMPACTS 7 A. Performance of Consultants and Quality of Reports 7 B. Stock Market Operation and Regulation 7 C. Mutual Funds Industry 8 D. Leasing Industry 9 E. Interest Rate Management of the National Saving Schemes 10 F. Corporate Bond Market 11 G. Legal and Regulatory Framework for Insurance and Capital Market 11 H. Restructuring of Public Sector Insurance Entities 12 I. Reform of Pension and Provident Funds 12 J. Capacity Building 13 IV. OVERALL ASSESSMENT 13 A. Relevance 13 B. Efficacy 14 C. Efficiency 14 D. Sustainability 14 E Impacts 15 F. Overall Rating 15 V. CONCLUSIONS 15 A. Key Issues 15 B. Lessons Learned 16 C. Recommendations and Follow-up Actions 17 APPENDIXES 1. Evaluation of TA 2393-PAK: Capital Market Development 18 2. Evaluation of TA 2812-PAK: Interest Rate Management of National Saving Schemes 25 3. Evaluation of TA 2825-PAK: Capital Market and Insurance Law Reform 30 4. Evaluation of TA 2865-PAK: Restructuring of Public Sector Mutual Funds 34 5. Evaluation of TA 2866-PAK: Reform of the Insurance Industry 39 6. Evaluation of TA 2867-PAK: Reform of Pension and Provident Funds 45

BASIC TECHNICAL ASSISTANCE DATA

TA 2393-PAK: Capital Market Development1

Cost ($’000)2 Estimated Actual Foreign Exchange 800 743 Local Currency 65 773 Total 865 820 Number of Person-Months (consultants) 23.0 23.4 Executing Agency Corporate Law Authority Milestones Date President’s/Board Approval 7 Sep 1995 Signing of TA Agreement 6 Oct 1995 Fielding of Consultants 15 May 1996 TA Completion: Expected end–Dec 1997 Actual end–Feb 20004 TCR Circulation 5 Mission Type Number Date Fact-Finding 1 27 Nov–16 Dec 1994 Review 4 7–11 Jul 19966 19 Aug–5 Sep 19967 23 Feb–7 Mar 19977 13–23 Sep 19988 Operations Evaluation9 1 25 Mar–15 Apr 2002

TA 2812-PAK: Interest Rate Management of National Saving Scheme

Cost ($’000)10 Estimated Actual Foreign Exchange 53 41 Local Currency 47 203 Total 100 61 Number of Person-Months (consultants) 9.5 8.3 Executing Agency Ministry of Finance Milestones Date President’s/Board Approval 18 Jun 1997 Signing of TA Agreement not required Fielding of Consultants 15 Nov 1997 TA Completion: Expected May 1998 Actual end–Jun 1999 TCR Circulation not required Mission Type Number Date Fact-Finding 1 3–16 Apr 1997 Review 2 13–23 Sep 19988 28 Apr–12 May 19998 Operations Evaluation9 1 25 Mar–15 Apr 2002 ________________________ TA = technical assistance, TCR = technical assistance report. Note: Footnotes on page v.

iii

TA 2825-PAK: Capital Market and Insurance Law Reform

Cost ($’000)10 Estimated Actual Foreign Exchange 85 71 Local Currency 15 153 Total 100 86 Number of Person-Months (consultants) 4.0 9.2 Executing Agencies Ministry of Commerce (insurance component) and Corporate Law Authority (capital market component) Milestones Date President’s/Board Approval 14 Jul 1997 Signing of TA Agreement not required Fielding of Consultants 4 Aug 1997 TA Completion: Expected end–Oct 1997 Actual 1 Mar 199911 TCR Circulation not required Mission Type Number Date Fact-Finding not required Review 2 13–23 Sep 19988 28 Apr–12 May 19998 Operations Evaluation9 1 25 Mar–15 Apr 2002

TA 2865-PAK: Restructuring of Public Sector Mutual Funds Cost ($’000)2 Estimated Actual Foreign Exchange 638 449 Local Currency 162 1353 Total 800 584 Number of Person-Months (consultants) 32 15.512 Executing Agency Privatization Commission Milestones Date President’s/Board Approval 15 Sep 1997 Signing of TA Agreement 18 May 1998 Fielding of Consultants 6 Jul 1998 TA Completion: Expected Aug 1998 Actual 1 May 1999 TCR Circulation 19 Oct 2000 Mission Type Number Date Fact-Finding 1 8–28 Jul 1997 Review 4 8–11 Jul 19986 13–23 Sep 19988 I Dec 19987 28 Apr–12 May 19998 Operations Evaluation9 1 25 Mar–15 Apr 2002

iv

TA 2866-PAK: Reform of the Insurance Industry

Cost ($’000)2 Estimated Actual Foreign Exchange 495 498 Local Currency 205 1493 Total 700 647 Number of Person-Months (consultants) 40.0 45.6 Executing Agency Ministry of Commerce Milestones Date President’s/Board Approval 15 Sep 1997 Signing of TA Agreement 28 Apr 1998 Fielding of Consultants 29 Jun 1998 TA Completion: Expected Jun 1999 Actual 15 Aug 200013 TCR Circulation 17 Jul 2001 Mission Type Number Date Fact-Finding 1 8–28 Jul 1997 Review 3 13–14 Jul 19986 13–23 Sep 19988 28 Apr–12 May 19998 Operations Evaluation9 1 25 Mar–15 Apr 2002

TA 2867-PAK: Reform of Pension and Provident Funds Cost ($’000)2 Estimated Actual Foreign Exchange 380 404 Local Currency 220 1503 Total 600 554 Number of Person-Months (consultants) 34 15.2 Executing Agency Ministry of Finance Milestones Date President’s/Board Approval 15 Sep 1997 Signing of TA Agreement 28 Apr 1998 Fielding of Consultants 1 Jun 1998 TA Completion: Expected Jun 1999 Actual 30 Jun 200114 TCR Circulation 15 Oct 2001 Mission Type Number Date Fact-Finding 1 22–31 Jul 1997 Review 5 8–11 Jul 19986 13–23 Sep 19988 28 Apr–12 May 19998 25–27 Sep 20007 30 Jan–5 Feb 20017 Operations Evaluation9 1 25 Mar–15 Apr 2002

v

Footnotes 1 Attached to Loan 1371-PAK: Financial Sector Intermediation Loan. 2 Financed by the Asian Development Bank (ADB) from the Japan Special Fund. 3 Operations Evaluation Mission estimate. 4 Consultant final report, including an additional study on National Investment Trust and Investment Corporation of

Pakistan, completed in October 1997. Completion date was extended to accommodate local training staff of Securities and Exchange Commission of Pakistan (formerly Corporate Law Authority).

5 The TA was not rated on stand alone basis. The project completion report rated the associated Loan 1371-PAK as partly successful.

6 Inception mission. 7 Multiproject mission. 8 Review Mission for Loan 1576-PAK: Capital Market Development Program and supporting TAs. 9 The Operations Evaluation Mission comprised A. Qureshi, Principal Evaluation Specialist; and M. Akhtar, Domestic

Consultant (Capital Market Development). 10 Financed by ADB. 11 Submission of the final report. 12 International consultant inputs only. 13 TA completion was delayed due to complex and protracted dialogue with stakeholders and the Government on the

finalization of the Insurance Act, which was enacted in August 2000. 14 TA completion delayed due in part to the political unrest and change of government in 1999, which temporarily

interrupted implementation. The final report was submitted in May 2001.

EXECUTIVE SUMMARY

In the mid-1990s, Pakistan’s capital markets faced a number of critical issues, including a weak and outmoded regulatory framework; an inefficient, non-transparent and stagnant stock market; poorly regulated and public sector-denominated mutual funds (MFs); an insurance industry that contributed little to capital market development (CMD); and an underdeveloped pensions sector. Moreover, financial markets operated in an inappropriate interest rate regime that attracted personal and institutional savings into the National Saving Schemes (NSS) but retarded financial intermediation, CMD and growth of the corporate debt market. To address these issues, the Asian Development Bank (ADB) provided extensive technical assistance (TA) to Pakistan during 1995–1997. This TA performance audit report covers six TAs approved to support CMD.1 The first was approved in 1995 to prepare a CMD agenda. A program loan2 supported the implementation of that agenda subsequently. Three TAs were provided to assist the Government in implementing reforms for MF, insurance and pension sectors, which were to form a part of the CMD agenda. The remaining two TAs supported reform of interest rate management of NSS and initiated insurance and capital market law reform. The TAs were relevant in varying degrees, and generally had a strong justification in terms of sector priority and conformance to ADB’s country and sector operational strategies. Objectives of the TAs were appropriate and their design was consistent with the objectives, with one or two exceptions. The design of TA 2865-PAK was flawed; a more appropriate focus would have been on privatization of the portfolios of the closed-end public sector MFs rather than the MF management function. Under TA 2867-PAK a phased approach to pension sector reform would have been more successful.

All six TAs experienced delay in implementation, from 8 to 26 months, indicating optimistic implementation schedules. However, implementation was generally successful, except in the case of TA 2867-PAK where it was partly so. In some cases, significant variations occurred between the planned and actual consultant inputs, both in terms of total person-months as well as between the services provided by international and domestic consultants. The significant variance between the planned and actual cost of TA 2865-PAK suggests that its inputs and cost were not planned meticulously.

In general, the outputs and impacts of the TAs were significant. The new regulatory framework for the capital market is in place, and the Securities and Exchange Commission of Pakistan (SECP) is functioning effectively, except that it needs to build capacity in regulation of insurance and pension funds. MF regulations have been updated, and substantial progress made towards privatization of public sector MFs. A new insurance law has replaced the outdated Insurance Act of 1938, and new insurance rules have been partially issued, albeit with a 2-year delay. Two public sector insurance entities have been restructured and appear better positioned than before to be privatized. Interest rates on NSS have been rationalized to level the playing field between NSS instruments, bank deposits, and corporate debt-instruments.

1 TA 2393-PAK: Capital Market Development, for $865,000, approved on 7 September 1995; TA 2812-PAK: Interest

Rate Management of National Saving Schemes, for $100,000, approved on 18 June 1997; TA 2825-PAK: Capital Market and Insurance Law Reform , for $100,000, approved on 14 July 1997; TA 2865-PAK: Restructuring of Public Sector Mutual Funds, for $800,000, approved on 15 September 1997; TA 2866-PAK: Reform of the Insurance Industry, for $700,000, approved on 15 September 1997; and TA 2867-PAK: Reform of Pension and Provident Funds, for $600,000, approved on 15 September 1997.

2 Loan 1576-PAK: Capital Market Development Program , for $250 million, approved on 6 November 1997.

vii

TA outputs met expectations fully or substantially in five out of the six TAs under evaluation. TA 2867-PAK was less efficacious because an important output, namely a program of reforms for the pension sector, was not delivered.

It is difficult to segregate the impacts of the TAs under evaluation from those of the

program loan. However, their combined impacts are significant. Stock market indicators are stronger and the corporate debt market appears to have received significant impetus from the NSS reform. A major beneficiary is the leasing industry, which is now much better placed to raise resources in the long-term debt market.

The stock exchanges have been modernized and their managements professionalized.

SECP is seen as an effective regulator of the stock market, thereby helping build investor confidence. However, the market is still narrow and remains highly speculative, and the stock exchanges are still perceived to be manipulated by a few powerful brokers.

Frameworks have been established for the healthy growth of MFs, and insurance; public

sector dominance in these industries is being reduced. Limited reforms in the pension sector have been initiated, but further measures are required for funding of public sector pensions, establishing an effective regulatory regime, promoting private pension funds, and placing the management of pension funds in the hands of professional investment managers.

Of the six TAs covered by this report, one is rated highly successful, three successful,

and two partly successful. As a cluster, the TAs are rated successful. The findings of this report confirm the lesson that strong government ownership is critical

to the success of policy and institutional reforms. Another lesson is that sharply focused TAs have better prospects for success than those covering a broad range of issues. Attempting to deal with too many complex issues under one TA is not effective. Finally, the use of domestic consultants, combined with dedicated and hands-on TA administration by ADB, can be highly cost-effective subject to availability of adequately qualified professionals in the relevant fields.

Major issues arising out of the implementation of these TAs relate to further

capacity-building of SECP in regulation of insurance and pension funds, reducing the preponderance of short-term speculative trades on the stock exchanges, accelerating privatization as a source of supply of quality stocks in the stock market, developing MF management on professional lines, and reforming the pension sector. Based on the real-time feedback provided by the Operations Evaluation Mission, appropriate measures to resolve several of these issues have been included among the policy reforms supported by a program and TA loan package approved by ADB on 5 December 2002.3 Residual issues in need of attention concern the promotion of asset-backed securities particularly of leasing companies, issuance of insurance rules in the area of SECP’s responsibility, and making the financial statements of Pakistan Reassurance Corporation transparent and free of audit qualifications.

3 Comprising a policy loan (Loan 1955-PAK: Financial [Nonbank] Markets and Governance Program , for $260

million); two TA loans (Loan 1956-PAK[SF]: Strengthening Pension, Insurance, and Savings Systems, and Loan 1957-PAK[SF]: Strengthening Regulation, Enforcement, and Governance of Nonbank Financial Markets, for $3.0 million equivalent each); and two political risk guarantee facilities (PRG: PAK 33271, for a total of $150 million).

I. INTRODUCTION

A. Background 1. The involvement of the Asian Development Bank (ADB) in Pakistan’s financial sector dates back to 1968. In the mid-1980s, the focus of ADB assistance to the sector shifted from providing credit lines to developing long-term financial markets. An umbrella credit line approved in 19831 was predicated on binding government commitment to initiate reforms to encourage domestic mobilization of long-term resources. This was followed by reforms to liberalize interest rate, credit allocation and monetary control policies of the Government and the central bank, the State Bank of Pakistan, and to develop the government bond market. These reforms were supported by the Industrial Sector Program2 of 1988, and subsequently by a technical assistance (TA) grant for a study of the country’s securities markets.3 2. In the mid-1990s, Pakistan’s capital market faced a number of critical issues. The securities law was outmoded and the regulatory framework for the capital market was weak. Insurance, pensions and mutual funds (MF) industries required comprehensive review and reform to provide the framework for effective regulation and healthy capital market development (CMD). High interest rates and after tax yields on National Saving Schemes (NSS) were retarding long-term financial intermediation and crowding out private sector investment. To help address these issues, ADB approved a series of TAs during 1995–1997 for CMD and reform of certain related nonbank financial institutions. The first TA4 was provided in conjunction with the Financial Sector Intermediation Loan (FSIL) in 19955 principally to formulate a CMD reform agenda to be supported by the Capital Market Development Program (CMDP).6 In mid-1997, ADB provided two small-scale TAs to review NSS interest rate management,7 and initiate insurance and capital market law reform.8 Finally, three stand-alone TAs were approved in September 1997 to support implementation of reforms that were to be included in the CMDP agenda relating to public sector MFs,9 insurance industry,10 and pension and provident funds.11 B. Rationale and Concept 3. A major thrust of the ADB strategy for the financial sector in Pakistan in the mid-1990s was to assist its structural transformation from directed to market-led operation. ADB’s financial sector operations aimed to rationalize the financial system and enhance the efficiency of the capital market, so as to mobilize resources for expanded private sector investment. Reforms were particularly needed for (i) diversifying the financial instruments available to investors, as well as the funding sources for the leasing sector; (ii) easing capital issue regulations to allow market-determined pricing of new share issues; (iii) enhancing the transparency and efficacy of the stock exchanges (SEs); (iv) empowering, and building the institutional capacity of the capital market regulator, the Corporate Law Authority (CLA); (v) enhancing the efficiency of the MF

1 Loans 678-PAK/679-PAK(SF): Development Finance Loan , for $110 million, approved on 20 December 1983. 2 Loans 931-PAK/932-PAK(SF): Industrial Sector Program , for $200 million, approved on 13 December 1988. 3 TA 1096-PAK: Study on Development of a Secondary Market for Fixed Income Securities, for $176,000, approved

on 3 January 1989. 4 TA 2393-PAK: Capital Market Development, for $865,000, approved on 7 September 1995. 5 Loan 1371-PAK: Financial Sector Intermediation Loan, for $100 million, approved on 7 September 1995. 6 Loan 1576-PAK: Capital Market Development Program , for $250 million, approved on 6 November 1997. 7 TA 2812-PAK: Interest Rate Management of National Saving Schemes, for $100,000, approved on 18 June 1997. 8 TA 2825-PAK: Capital Market and Insurance Law Reform , for $100,000, approved on 14 July 1997. 9 TA 2865-PAK: Restructuring of Public Sector Mutual Funds, for $800,000, approved on 15 September 1997. 10 TA 2866-PAK: Reform of the Insurance Industry, for $700,000, approved on 15 September 1997. 11 TA 2867-PAK: Reform of Pension and Provident Funds, for $600,000, approved on 15 September 1997.

2

industry; and (vi) leveling the playing field between NSS, bank deposits, debt instruments, and the capital market to encourage efficient resource mobilization. C. Objectives and Scope 4. The TAs focused on six important aspects of CMD: (i) interest rates on investment instruments sold by NSS, (ii) legal framework for regulation of insurance and capital market, (iii) operation and regulation of SEs, (iv) restructuring of public sector insurance entities (PSIEs) and MFs, (v) pension and provident funds, and (vi) the leasing industry. 5. The objective of TA 2393-PAK was to assist the Government in (i) increasing the transparency and efficiency of stock market operations, (ii) improving the efficiency of MF industry with a focus on public sector MFs–-the Investment Corporation of Pakistan (ICP; a closed-end fund) and the National Investment Trust (NIT; an open-end fund), (iii) encouraging long-term resource mobilization by the leasing industry, and (iv) capacity building of CLA (Appendix 1). 6. TA 2812-PAK aimed to (i) examine the structure and key determinants of NSS interest rates in order to develop an appropriate mechanism for their future management, (ii) examine interest rate issues such as the impact of dollarization of the economy on interest rates, and (iii) develop an appropriate mechanism for managing the interest rates of the NSS (Appendix 2). 7. The objectives of TA 2825-PAK were to assist the Government in capital market and insurance law reform by (i) helping CLA identify best international practices and different models in key areas of securities and corporate law and regulations, (ii) drafting securities and corporate legislation, and (iii) assisting the Ministry of Commerce (MOC) in preparing a plan for the reform of the insurance regulatory framework, and drafting laws for a new regulatory regime for the insurance industry (Appendix 3). 8. TA 2865-PAK was provided to support the restructuring of public sector MFs and prepare an action plan for privatizing the asset management companies of ICP and NIT with the objective of transferring their management and control to strategic investors (Appendix 4). 9. The main objective of TA 2866-PAK was to promote orderly growth of the insurance industry. This was to be done through strengthening and modernizing the insurance legislation and building the institutional capacity of a new insurance regulatory authority to cover general 12 and life insurance companies, both in public and private sectors. The TA also aimed to support the development of restructuring and divestment plans for the PSIEs handling reinsurance (Pakistan Insurance Corporation, or PIC) and government insurance business (National Insurance Corporation, or NIC), as well as capacity enhancement of the Pakistan Insurance Institute (PII) (Appendix 5). 10. The purpose of TA 2867-PAK was to (i) support a comprehensive study of the prevailing pension and provident schemes, which would analyze their social, economic, and financial implications; (ii) make recommendations on fully or partially funded public and private pension plans to mobilize savings and provide adequate social security coverage to a larger segment of the population; and (iii) develop investment guidelines and a supportive legal, regulatory and institutional framework for more prudent management of the pension and provident funds, thereby contributing to more effective development of the capital market (Appendix 6).

12 Non-life insurance business in Pakistan is referred to as general insurance, and non-life insurance companies as

general insurance companies.

3

D. Completion and Self-Evaluation 11. Four of the six TAs covered by this TA performance audit report were self-evaluated by the operational department concerned. TA 2393-PAK was self-evaluated as part of the project completion report for FSIL, and was rated partly successful. However, this rating does not fully reflect TA achievements (para. 24). This TA prepared a CMD agenda whose implementation was supported by CMDP. The project completion report for CMDP rated it satisfactory.13 The other three TAs were self-evaluated on a stand-alone basis and a TA completion report (TCR) was prepared for each of them. The TCR on TA 2865-PAK14 rated it generally successful. This TCR did not, however, take into account the design flaw relating to privatization of the closed-end MFs managed by ICP, and slow progress in development of the fund management profession (paras. 16, 26–27). The TCR on TA 2866-PAK15 rated it highly successful but did not consider the fact that its implementation had benefited from the outputs of TA 2825-PAK (para. 35). The TCR on TA 2867-PAK16 rated it partly successful. E. Operations Evaluation 12. An Operations Evaluation Mission (OEM) visited Pakistan in March–April 2002 and held discussions with a large number of institutions, market participants, TA executing agencies, regulatory authorities, and other stakeholders. The OEM reviewed relevant ADB records and analyzed pertinent data collected in the field and through research on the internet. Following this, the OEM evaluated the six TAs in terms of (i) relevance of design in relation to the underlying rationale and objectives, as well as consistency with the Government’s priorities for the sector and ADB’s sector strategy; (ii) the achievement of objectives; (iii) the efficiency of implementation and adequacy of outputs; and (iv) outcomes and impacts. The TAs have been rated individually (Appendixes 1–6), as well as a cluster (paras. 43–48).

II. ASSESSMENT OF DESIGN AND IMPLEMENTATION

A. Design 13. The TAs were formulated at a time when government monetary and fiscal policies had created distortions in the financial markets, constraining financial intermediation and crowding out private sector investments. The stock market was stagnating despite liberalization of foreign portfolio investment; public sector MFs were beset with serious portfolio difficulties; and the MF industry as a whole faced issues concerning corporate governance, professional ethics, capital adequacy and regulation. The leasing industry was seeking feasible alternatives to foreign credit lines as their principal funding source while the pension sector was underdeveloped and poorly regulated. TA designs, in general, responded to these issues adequately and were relevant to ADB’s country and sector strategies. The three areas of focus under TA 2393-PAK––SEs, MFs, and the leasing sector––signified a phased approach to CMD, which was appropriate in view of the constraints on the Government’s implementation capacity and readiness to take on reforms simultaneously over a broad spectrum. Terms of reference (TOR) were expanded during TA implementation to conduct detailed studies of NIT and ICP and recommend alternate approaches for their strengthening before privatization.

13 Equivalent to “successful” under the current 4-level evaluation system, i.e., highly successful, successful, partly

successful, and unsuccessful. 14 ADB. 2001. Technical Assistance Completion Report on Restructuring of Public Sector Mutual Funds. Manila. 15 ADB. 2001. Technical Assistance Completion Report on Reform of the Insurance Industry. Manila. 16 ADB. 2001. Technical Assistance Completion Report on Reform of Pension and Provident Funds. Manila.

4

14. TA 2812-PAK comprehensively covered the issues arising out of segmentation of financial markets, interest rate distortions, and the unsustainable yield structure of NSS instruments, as well as their negative impact on financial intermediation by banks and debt and capital markets, and on private sector investment. The TA design was appropriate in providing the analytical framework to bring dialogue on these issues between Government, the International Monetary Fund, and other aid agencies including ADB, to successful closure. The TA also helped in shaping and implementing a key conditionality of CMDP, namely reform of NSS interest rate management.

15. The principal factor leading to formulation of TA 2825-PAK was that while the Government was willing to implement capital market reforms proposed under TA 2393-PAK, and included in the reform agenda of CMDP, it lacked capacity to draft laws and establish regulatory frameworks for the capital market and the insurance industry in line with best international practice. The TA design was thus appropriate and its focus on securities legislation and regulatory framework for insurance was meant to overcome the Government’s most pressing capacity constraints, as well as help meet CMDP conditionalities. 16. The design of TA 2865-PAK had a major shortcoming. It did not fully consider the difference in the approach and strategy that was required for restructuring and privatizing NIT, an open-end fund, and ICP, a closed-end fund. The objective in both cases was to privatize the asset management business, and the TOR for both components were almost identical. However, ICP’s asset management function was neither tradeable nor did the “right to manage” its MFs have a value of its own. What needed to be privatized, in the case of ICP, were the ICP-managed MFs rather than the right to manage them. The TA design also omitted mitigating measures to deal with post-restructuring staff redundancies in NIT and ICP. 17. TA 2866-PAK was intrinsically linked with, and a logical continuation of, the insurance component of TA 2825-PAK, under which a sector study focusing on the regulatory framework for insurance and the blueprint for the Pakistan Insurance Regulatory Authority (PIRA) had been prepared. The TA design did not draw the distinction between what had been achieved under TA 2825-PAK and what remained to be done. Thus, it did not provide an adequate basis for a complete and objective assessment of its inputs, outputs, and impacts, as distinct from those of TA 2825-PAK. In hindsight, and in view of the long delay in framing rules under the Insurance Ordinance of 2000 (para. 34), it might have been better to include drafting of insurance rules in the TA scope. 18. The design of TA 2867-PAK called for a comprehensive study of almost all aspects of public and private pensions, as well as supplementary or alternative instruments of social security, namely gratuity and provident funds. The TA study was to address, among others, the critical but difficult issues of extending the provision of social security to a larger segment of the population, financial sustainability of the unfunded government pension scheme, as well as of the Employees’ Old-Age Benefits Institution (EOBI), and increasing the mobilization of long-term savings and channeling them to the capital market. Though these issues were interrelated, each involved time consuming and complex processes of research, analysis, and consensus building. Moreover, each issue required different expertise and skills. Thus, the TA scope was too broad. A more effective approach would have been to prepare, in the first instance, a roadmap of the required pension reforms, sequentially arranged and prioritized, following structured policy dialogue with the Government and in consultation with other stakeholders.

5

B. Engagement of Consultants 19. The two small–scale TAs (TA 2812-PAK and TA 2825-PAK) were implemented by individual consultants while the others were implemented by consulting firms. The procedures for selection of the consultants were in accordance with ADB’s Guidelines on the Use of Consultants in each case.17 Actual consultant inputs varied considerably from the original implementation scheme in some cases, both in terms of total number of person-months as well as between the services provided by international and domestic consultants (Table 1). The large difference in planned and actual TA inputs under TA 2867-PAK suggests that TA implementation was not planned meticulously.

Table 1: Consulting Services

Planned Actual Item Int’l Domestic Total

Int’l Domestic Total

TA 2393-PAK No. of Consultants Person-months

7

20.0

2

3.0

9

23.0

11

20.4

1

3.0

12

23.4 TA 2812-PAK No. of Consultants Person-months

1

––

2

––

3

9.5

2

2.5

1

5.8

3

8.3 TA 2825-PAK No. of Consultants Person-months

2

3.0

1

1.0

3

4.0

1

1.5

4

7.7

5

9.2 TA 2865-PAK No. of Consultants Person-months

4

15.0

4

17.0

8

32.0

5

15.5

3

––

8

–– TA 2866-PAK No. of Consultants Person-months

2

12.0

4

28.0

6

40.0

3

18.0

6

27.6

9

45.6 TA 2867-PAK No. of Consultants Person-months

2

8.0

4

26.0

6

34.0

6

10.2

5

5.0

11

15.2 –– = not available, Int’l = International, No.= number.

C. Implementation and Cost 20. The implementation of all the TAs was delayed, by 8–26 months (Table 2). However, on the whole, the delays had limited effect on the substance of TA outputs. TA 2393-PAK was substantively complete in terms of formulation of the CMD agenda by October 1997, within the projected completion schedule of end-1997. However, TA completion date was extended to accommodate the training requirements of the new Executing Agency, the Securities and Exchange Commission of Pakistan (SECP), which had been set up to replace CLA. In the case of TA 2825-PAK, an important TA output, the passage of the Securities and Exchange

17 However, in the case of TA 2825-PAK, in view of the urgency to field the consultants, the requirement to list the TA

in ADB Business Opportunities for the required period was waived.

6

Commission of Pakistan Act, was realized within the implementation timeframe. Proactive participation of ADB’s Office of the General Counsel in TA administration was a notable feature of this TA, and was necessitated by the extensive amount of legal drafting required. Implementation of TA 2866-PAK was also effective in terms of end results. However, the delay required additional inputs from domestic consultants, which were accommodated within the TA budget, thanks to favorable exchange rate development. In the case of TA 2867-PAK, implementation was temporarily interrupted by the unexpected change of government in October 1999, which caused loss of momentum and affected the vigor of the officials and implementation agencies concerned. As a result, inputs from these agencies diminished with time. TA implementation also suffered from severe data constraints and limited capability of the consultants’ team leader.18

Table 2: Implementation Delays and their Impacts

Item

Delay (months)

Main Reason for Delay

Impact on Output

TA 2393-PAK 26 Delayed implementation of the training component

because of reorganization of the Corporate Law Authority into the Securities and Exchange Commission of Pakistan

Limited

TA 2812-PAK 13 Coordination of the work of individual consultants not well

planned Limited

TA 2825-PAK 16 Mid-course addition to the TA scope Insignificant TA 2865-PAK 8 Late signing of the TA Agreement by the Government Insignificant TA 2866-PAK 14 Late signing of the TA Agreement by the Government and

delay in consensus-building on the new insurance law and institutional arrangements for insurance regulation

Limited

TA 2867-PAK 24 Late signing of the TA Agreement by the Government,

unexpected change of the Government, frequent changes in the Government and ADB staff assigned to the project, and difficulties in data collection

Substantial

ADB = Asian Development Bank, TA = technical assistance. 21. In some cases, significant cost savings were realized. Implementation of the two small-scale TAs relied substantially on the use of domestic consultants. Careful consultant selection and close TA administration by ADB and effective executing agency support made these TAs highly cost effective. In the case of TAs 2812-PAK and 2865-PAK, consultant inputs and TA costs appear to have been over-estimated.

D. Organization and Management 22. EA arrangements were generally effective with the Ministry of Finance (MOF) or its affiliate organizations assuming the lead role in most cases. The EAs provided adequate official and logistic support to the consultants in their research and fieldwork. This assisted them in interviewing a large number of institutions and individuals associated with capital market related

18 In the last phase of TA implementation, the team leader was replaced by a legal expert and an actuary to conduct

a study on EOBI.

7

activities, besides concerned government agencies. TA administration by ADB was proactive in most cases with the Office of the General Counsel providing effective support where review and drafting of laws was involved. In the case of TA 2867-PAK, MOF had established a coordination group headed by the Secretary, MOF, and comprising representatives of the Ministry of Labor, EOBI, professionals, and the private sector. In practice, this arrangement did not work well, in part due to frequent changes in personnel. Supervision of the implementation of this TA by both the Government and ADB was less than effective. Closer monitoring and supervision by ADB could have optimized TA outputs by replacing the team leader at an earlier stage of TA implementation.

III. EVALUATION OF OUTPUTS AND IMPACTS

A. Performance of Consultants and Quality of Reports 23. The performance of consultants under all the TAs was generally satisfactory with the exception of TA 2867-PAK. The recommendations under TA 2393-PAK became an important input to the formulation of CMDP. The final report recommended the elimination of double taxation of corporate and dividend income but did not specifically address taxation of MFs, as was required under the TOR. Appreciation was expressed to OEM by various stakeholders of the high quality of the final report of the domestic consultant under TA 2812-PAK as well as the underlying research and analytical work. Consultant reports under TA 2825-PAK were of good quality but submission of the reports of the management consultant and insurance regulatory expert was delayed. Under TA 2865-PAK, consultant performance was generally satisfactory although it could have been better in two aspects. Firstly, there should have been a more realistic assessment of the interest of foreign fund managers in taking over the MFs managed by NIT and ICP, and accordingly a focus on approaches and strategies to privatize them through domestic interests. Secondly, with respect to ICP, there should have been more focus on privatizing the MFs rather than the right to manage MFs, which could not be sold because this had no value of its own. The performance of consultants under TA 2867-PAK was below par; a major intended output—a pension and provident funds reform program—was not delivered. On other aspects, however, particularly in respect of actuarial analysis, the quality of the final report was acceptable. B. Stock Market Operation and Regulation 24. TA 2393-PAK helped in initiating a number of reforms to enhance the transparency and efficiency of the stock market (Appendix 1, para. 12). These measures have helped bring the operation of the stock market closer to international standards and improved its transparency considerably. SECP and SEs have also taken a number of measures to reduce the risk of broker default, including redefining the net capital balance of brokers on a conservative basis, and capping the value of a broker’s trades as a multiple of the net capital balance. These measures are expected to bear positive impact in due course. However, public perception as to the credibility of the stock market has not changed much. The secondary market remains largely speculative, driven by a few powerful players. Daily turnover remains concentrated in very few stocks that have large market capitalization. The ratio of average daily trading value to market capitalization, four times that of Mumbai Stock Exchange, is one of the highest in the world. There is a preponderance of short-term and intra-day trades supported in part by “badla” 19 financing. Market participants estimate that about 36% trades are intra-day trades, more than 60% trades are carried over, and just 3% ultimately settled in cash. One reason for this phenomenon is that supply of quality stocks has not kept pace with other aspects of CMD, i.e.,

19 Broker-arranged financing of carried over transactions.

8

demand, intermediation and regulation, because of slow privatization and unfavorable investment climate. Though SECP is generally perceived to be an effective regulator, it has not yet been successful in eliminating market manipulation and maintaining a healthy balance between speculative and non-speculative investment. 25. It is difficult to measure the direct impact of the TAs on the stock market. However, together with the implementation of CMDP, they appear to have helped boost the market in terms of market capitalization, new listings particularly of debt issues, and stock price index, which have all recorded impressive growth during 1998–2002 (Table 3). However, the extraordinary growth of the market in 2002 has also been helped by positive developments in the economy, political climate, and regional security environment.

Table 3: Key Statistics of Karachi Stock Exchange

1998 1999 2000 2001 2002a

Equities Listed Companies b 773 765 741 747 719

Listed Capital (PRs million) 212,619 223,028 236,459 235,683 288,950

Market Capitalization (PRs million) 268,471 366,670 382,730 296,144 550,553

New Companies Listed 1 0 3 2 4

Listed Capital (PRs million) 221 0 2,035 1,948 6,318

Bonus issues listed (PRs million) 2,529 4,243 5,211 4,187 2,854

Rights issues listed (PRs million) 1,177 6,512 3,387 1,531 12,023

Debt Instruments

New Debts Instruments Listed 1 2 3 5 14

Listed Capital (PRs million) 274 1,148 648 5,658 7,556

Funds mobilized (PRs million)c 1,673 7,659 6,070 9,174 25,897

KSE – 100 Index

High 1,746 1,417 2,054 1,550 2,279

Low 768 852 1,276 1,075 1,322

Turnover

Total Shares (million) 18,497 31,330 46,158 23,070 30,942

Average Daily Trade/Day

(million shares)

77

128

187

97

147 KSE = Karachi Stock Exchange.

a January–October 2002. b The difference between the number of cumulative equity listings and the actual number of listed companies

represents de-listing of non-compliant companies. c Capital of new listings plus debt instruments plus rights issues.

Source: Karachi Stock Exchange, www.kse.com.pk. C. Mutual Funds Industry 26. The MF industry has undergone significant developments. TA 2865-PAK helped amend the MF regulations to (i) allow flotation of special purpose MFs, (ii) unify the fee structure of closed-end and open-end funds, (iii) require mandatory declaration of net asset value,

9

(iv) strengthen capital adequacy and disclosure requirements for MFs, and (v) empower SECP to enforce compliance flexibly. Following TA completion, substantial progress has also been made towards restructuring and privatizing the MF business of ICP. However, MF management has not yet developed as a successful profession or industry in Pakistan, and a majority of private MFs have underperformed persistently. Privatization of NIT too has been stalled pending MOF decision on any guarantee or comfort that may need to be provided to private investors on the redemption value of NIT units (para. 28). However, the current buoyancy of the stock market provides a favorable environment to implement the privatization of NIT. 27. The output of TA 2865-PAK relating to restructuring of public sector MFs was significant but somewhat below expectations. The final report on ICP recommended a two-stage privatization approach, first to separate the MF business from other operational functions of ICP, auction the right to manage MFs, and then wind down the rest of ICP business or merge it with another institution. This strategy was inappropriate since ICP’s “right” to manage MFs could not be sold because it had no value of its own per se (para. 16). In the case of NIT, the recommendation was to sell the asset management right in the form of a new asset management company and wind down the remainder of the asset management company. The recommended strategy for ICP assumed the sale of a single MF management contract covering all MFs managed by ICP. In both cases, the consultants recommended sale to foreign fund managers experienced in MF management in a more stringent regulatory environment, so as to improve MF management standards in Pakistan. However, no foreign fund managers were interested in taking strategic stakes in ICP and NIT, probably because of reservations as to the quality of their portfolios and unfavorable investment climate in Pakistan in general. 28. The consultants identified a number of issues that needed to be resolved before the privatization of NIT could move forward. The most critical issue was that, in order to avoid large-scale redemptions, the parties interested in acquiring NIT were insisting on continuation of the government-guaranteed minimum repurchase price of NIT units. This was clearly not acceptable, since withdrawal of this guarantee was the main reason behind the move to privatize NIT, thereby providing a level playing field to private sector open-end MFs. Following implementation of TA 2865-PAK, the Privatization Commission has lately fast-tracked the privatization of ICP and NIT. In the case of ICP, a first package comprising 12 MFs has been sold while the sale of the second package has been approved by the Cabinet. The Privatization Commission expects to move forward with the third package soon. ICP has already started winding down its investment account management activities, and by the time of the OEM, had separated 365 staff under a voluntary retirement scheme. Notwithstanding the difficulties relating to the repurchase price, initial steps toward NIT’s privatization were taken in July 2001 and four parties were subsequently pre-qualified. However, further progress has been stalled as interested parties still insist on government guarantee on the repurchase price. D. Leasing Industry 29. To reduce the dependence of leasing companies on foreign credit lines as a major source of long-term funds, a number of measures were recommended by consultants and have been implemented. These include liberalizing investment rules for institutional investors, strengthening the capital base of leasing companies and tightening their regulation as issuers of certificates of investment to the public. TA consultants identified term finance certificates (TFCs) as an effective instrument of raising long-term funds in Pakistan’s financial markets. However, they highlighted the need for rationalizing the returns on government-guaranteed investment instruments, mainly NSS, since these were retarding the development of the corporate bond market. This rationalization took place under TA 2812-PAK (para. 31), and has greatly helped the primary market for TFCs (para. 32 ), particularly to the benefit of the leasing industry. The

10

consultants also made a number of recommendations for the development of asset-backed securities (ABS). However, the ABS market has been slow to take off as only one leasing company has yet attempted to raise funds through securitization of lease receivables. E. Interest Rate Management of the National Saving Schemes 30. A domestic consultant reviewed NSS within the broad framework of Pakistan’s financial markets. The consultant formulated recommendations for the reform of NSS while identifying possible constraints to their implementation. Most of the recommendations have been implemented. In addition, international consultants conducted an econometric study to analyze the relationship between the demand for NSS versus other instruments including bank deposits in local and foreign currencies. They concluded that while bank deposits and NSS instruments appeared to be net substitutes, bank deposits in local and foreign currencies were neither substitutes nor complements to each other. Also, the estimated income derivative of the demand for local currency bank deposits was negative, while that for foreign currency deposits was positive. For NSS, it was not significantly different from zero. Finally, the study found some empirical support for the view that foreign currency deposits had absorbed a part of the demand for NSS, and therefore, the availability of on-shore foreign currency deposit facilities may have reduced the ability of the Government to finance itself through NSS. 31. Interest rates on NSS have been made market compliant since January 2001, and institutional investors have been barred from making new investments in NSS instruments. The Government has developed a formula in consultation with the International Monetary Fund, whereby NSS interest rates are reviewed semi-annually within ±0.5% of the market-based rate of return on Pakistan investment bonds of corresponding maturities. With this mechanism in place, the main objective of TA 2812-PAK has been achieved. Withdrawal of institutional savings from NSS would be gradual depending on their maturity structure, since premature withdrawal is subject to penalty. However, in the absence of credible alternative instruments, and because investment up to PRs150,00020 in NSS is still exempt from withholding tax, NSS instruments have remained popular with individual savers. Thus, the outstanding NSS stock has continued to grow albeit at declining rates (Table 4).

Table 4: Outstanding Obligations of the National Saving Schemes (PRs million)

Fiscal Year Ending 30 June

Saving Accounts

Saving Certificates

Total

1996 43,557 209,336 252,893 1997 41,891 269,892 311,783 1998 37,822 374,981 412,803 1999 45,964 496,435 542,399 2000 51,194 582,608 633,802 2001 52,731 617,430 670,161 2002a 55,537 685,642 741,179

a Provisional. Source: State Bank of Pakistan, Annual Report 2001–2002; www.sbp.org.pk.

20 Reduced from PRs300,000 effective July 2002.

11

F. Corporate Bond Market 32. The reform of NSS has provided a boost to the TFC market, which effectively represents the corporate bond market in Pakistan (Table 5). As a result, a total amount of PRs18.5 billion was raised through 28 TFC issues between 1 January 2001 and 8 August 2002, as against PRs3.4 billion raised through 11 issues during 1998–2000. A secondary market for TFCs has also started to emerge with the listing of 14 TFC issues, totaling PRs7.6 billion, on the Karachi Stock Exchange in January–October 2002. To provide liquidity to the unlisted debt securities, a discount house regularly offers two-way price quotes for major unlisted TFCs.

Table 5: Issues of Term Finance Certificates

Issuer

Banks

Leasing Companies

Others

Total

Year No.

PRs million

No.

PRs million

No.

PRs million

No.

PRs million

1998 1 300 1 274 2 574 1999 2 838 2 1,113 4 1,951 2000 4 650 1 204 5 854 2001 1 500 6 1,870 10 9,766 17 12,136 2002a 1 1,600 2 960 8 3,835 11 6,395 Total 3 2,400 14 4,318 22 15,192 39 21,910

a Up to 8 August 2002. No. = number. Source: State Bank of Pakistan; www.sbp.org.pk.

G. Legal and Regulatory Framework for Insurance and Capital Market 33. The most important output of TA 2825-PAK was the draft of the SECP Act of 1997. Following its enactment, CLA was dissolved and SECP established, effective January 1999, as an autonomous and financially independent capital market regulator. SECP is fully operational and actively discharging its responsibilities in capital market regulation. The organization and staff compensation structures proposed by the TA have been substantially implemented and have helped establish SECP on a sound footing. SECP has brought about a number of reforms in the governance of SEs and related institutions. These reforms have begun to bear positive impact on the image of SEs and investor confidence though a lot more needs to be done. 34. The key outputs under the insurance component of TA 2825-PAK were a sector study focusing on insurance regulation, and an insurance regulatory framework in the form of the draft PIRA Bill. The study provided the basis for drafting, under TA 2866-PAK, a new insurance law, the Insurance Ordinance enacted in August 2000, to replace the outdated Insurance Act of 1938. As a result of the new law, the financial health of the insurance companies is expected to improve due to the requirement of stronger capital base and solvency margins. However, the ordinance remained only partially operational for 2 years because the issuance of rules was delayed due to lack of effective coordination between MOC and SECP (the prospective insurance regulator), as well as lack of clear and timely guidance from the Ministry of Law. At the time of the OEM, SECP had neither commenced effective insurance regulation nor had started building capacity to do so in a meaningful way. The first set of insurance rules, to be enforced by MOC, was eventually issued in August 2002, while the rules falling under SECP’s jurisdiction are expected to be issued in the near future.

12

35. The draft bill envisaged the establishment of PIRA as an independent insurance regulator outside of MOC. Following extensive consultations between the Government, ADB and other aid agencies, however, it was concluded that capacity and cost constraints weighed against the establishment of a new insurance regulator. Accordingly, the Government abandoned the proposal to establish PIRA and instead made SECP responsible for regulation of the insurance industry. The consultants helped consensus building on this approach through extensive consultations with stakeholders, including the Government, aid agencies (including ADB) and the insurance industry. Since the initial draft of the PIRA Bill was developed under TA 2825-PAK (Appendix 3), it is difficult to judge the adequacy of inputs and outputs of this component of TA 2866-PAK on a stand-alone basis. Nonetheless, the consultants formulated necessary amendments to the SECP Act to provide the legal basis for regulation of insurance by SECP, and prepared action plans for establishment of the Insurance Wing of SECP. Some staff training was provided under the TA in the area of insurance regulation. However, at the time of the OEM, SECP’s Insurance Wing was not fully functional. H. Restructuring of Public Sector Insurance Entities 36. The consultants’ recommendations under TA 2866-PAK provided the basis for corporatization of both NIC and PIC under the company law and inclusion of nongovernment members in their Boards. PIC was restructured as the Pakistan Reassurance Corporation (PRC), and a comprehensive corporate plan was adopted. Before restructuring, PIC was the sole entity allowed to handle reinsurance business in Pakistan. The compulsory cession of reinsurance business to PRC will be phased out by end-2003, which should improve its sustainability on a competitiveness basis. NIC has also successfully streamlined its organization and administrative expenses. 37. However, the diagnostic studies of PIC and NIC conducted under the TA have not helped bring these corporations to a “privatizable” shape. PRC’s financial condition remains non-transparent and uncertain, because the external auditor has qualified its financial statements, notably the balances with counter parties, valuation of foreign exchange assets and liabilities, and assets and liabilities in Bangladesh. Athough PRC is listed with the Privatization Commission, the prospects of its privatization in the near future are slim, as are the prospects of privatization of NIC. NIC enjoys a sound financial position and could attract a fair value from the private sector, but strong arguments have been made against its privatization. First, with the completion of the ongoing process of privatization of public sector enterprises, NIC’s captive insurance business will diminish through a natural process of attrition. Secondly, the Government has begun to exempt public sector enterprises on a case-by-case basis from compulsory insurance with NIC, so as to break its monopoly over public sector insurance business. Finally, NIC also handles the insurance requirements of certain departments and agencies, which the Government would not like to cede to the private sector. I. Reform of Pension and Provident Funds 38. The output of TA 2867-PAK was short of expectations. The final report did not present a comprehensive reform proposal, as was required under the TOR. The TA was not well prepared and was premature. No workshop was held for stakeholder consultation, given the premature stage of strategy development for the pensions sector. However, TA findings provided Government and ADB insights into the complexities of the existing pension and provident fund system in Pakistan, and identified a general framework for formulating practical and well-sequenced reform proposals for the future. The TA could also be a catalyst for partial reform of the existing defined-benefit pension scheme of the Government. It has prompted serious consideration within the Government of funding future public pensions on contributory basis,

13

allowing private sector fund managers to manage public pension funds, and encouraging the private pension funds industry in general. 39. The consultants compiled useful data and conducted actuarial analysis of EOBI. The TA and recent media reports of irregularities in EOBI have highlighted serious problems in its financial management. EOBI is charged with the responsibility to collect contributions from private employers and dispense retirement benefits to private employees, and is the largest holder of financial assets in Pakistan. It operates under its own statute, which is not in line with the needs of modern pension fund operation and management. Its Board of Trustees is dominated by officials of federal and provincial labor ministries, whose financial management capabilities do not match those of professional investment managers. Finally, EOBI is unable to hire capable professional staff with the public sector compensation package that it is obliged to adopt. The TA helped highlight these issues and thus the need for reform of EOBI. 40. Meanwhile, EOBI has introduced the requirement for private workers to contribute PRs20 per month to complement the employers’ contributions. This is a positive step even though the amount of employees’ contribution is small. Another development is that MOF has begun the process of establishing an Actuary’s Department to strengthen its pension policy making and supervisory capacity. Finally, with the urgency of pension reforms gaining increasing recognition, SECP has drafted a new pension law and related rules, which are under government consideration. J. Capacity Building 41. Two of the six TAs had capacity-building components. Under TA 2393-PAK, 53 staff of SECP and 2 staff of SEs were trained. However, the TA outputs in this area were inadequate. There was a considerable delay in the identification of suitable foreign training programs because it was difficult to make a meaningful training needs assessment while CLA was being restructured into SECP. Foreign training of SECP staff, therefore, largely proceeded on ad hoc basis, and a part of the training budget was utilized to participate in annual meetings of securities-related international organizations.21 None of the training programs participated by SECP staff was focused on MF/ABS regulation, and it is not clear whether any capacity enhancement has taken place in these areas where SECP was deficient. 42. TA 2866-PAK did not directly help capacity building of PII. However, the consultants interacted with PII members and helped put in place funding arrangements through periodic contributions of members, so as to enable it to meet the training needs of the industry on a continuous basis. PII has introduced new courses on the basic insurance concepts and principles. At the time of the OEM, however, its training activities on the new insurance law had not commenced in the absence of the new insurance rules.

IV. OVERALL ASSESSMENT

A. Relevance 43. One TA was highly relevant, three were relevant, and two partly relevant. The rationale for all six TAs was generally sound in the context of sector needs, government priorities and ADB’s country and sector operational strategies. The TA designs were consistent with objectives in the case of four TAs. TA 2393-PAK was relevant and addressed priority issues in

21 At SECP’s request, 25% of the budget for foreign training was made available by ADB for domestic training of 30

staff at the Lahore University of Management Sciences.

14

stock market operation and regulation, and MF and leasing industries. Its design was consistent with objectives. TA 2812-PAK was highly relevant and timely, designed to address interest rate distortions that were retarding healthy financial intermediation and resource mobilization for private sector investment. TA 2825-PAK was relevant as it set in motion the urgently needed review of the legal and regulatory frameworks for capital market and insurance. The design of TA 2865-PAK lacked clarity regarding privatization of ICP, and did not call for mitigating the social consequences following privatization of NIT and ICP. The TA is assessed as partly relevant. TA 2866-PAK was relevant and timely, and in part provided continuity to the insurance sector reform initiated under TA 2825-PAK. Its design was sound but the TA could have been more purposeful if its scope had specifically called for drafting rules under the new insurance law. TA 2867-PAK was too wide in scope, considering the lack of government readiness to take on pension reform over a broad spectrum. It should have focused on a narrower agenda based on government capacity and readiness, and as part of a prioritized and sequentially arranged reforms program. It is assessed as partly relevant. B. Efficacy 44. Five TAs are assessed as efficacious, and one as less efficacious. TA 2393-PAK was efficacious as its outputs largely met expectations. Although its capacity building component was delayed, the substantive outputs were delivered within the original schedule. TA 2812-PAK was also efficacious as its outputs provided important inputs to the Government’s review of NSS. TA 2825-PAK was efficacious in that it initiated drafts of the SECP Act and the PIRA Bill even though the latter was not utilized as the proposal to establish an independent insurance regulator was abandoned. TAs 2865-PAK and 2866-PAK are assessed as efficacious as their outputs substantially met expectations, in accordance with their designs and scope. TA 2867-PAK is assessed as less efficacious because the consultant team leader performed poorly and TA output was considerably below expectations. C. Efficiency 45. Implementation of all six TAs was delayed but, in most cases, the impact of the delay on the substance of outputs was insignificant. TA 2393-PAK is assessed as efficient, its substantive output being delivered on time. The two small-scale TAs, i.e., TA 2812-PAK and TA 2825-PAK, were highly cost effective and are assessed as highly efficient. TA 2865-PAK was implemented with substantial cost savings, and is assessed as efficient. TA 2866-PAK was also efficient as the delay in consensus building on the institutional arrangements for insurance regulation occurred mainly because of government indecision. In the case of TA 2867-PAK, some of the key TA activities were not completed, despite considerable implementation delay. The TA is rated as less efficient. D. Sustainability 46. Most of the reforms formulated under TA 2393-PAK, and supported by CMDP, in the areas of operation and regulation of SEs, MFs, and resource mobilization by the leasing industry have been implemented. Sustainability of the TA outputs and impacts is assessed as likely. In the case of the two small-scale TAs, sustainability is most likely because of their direct and significant contribution to the policy, regulatory and institutional reforms. A key recommendation of TA 2865-PAK, i.e., to sell NIT and ICP to foreign fund managers, proved impractical. Sustainability of the outputs of this TA is therefore assessed as less likely. TA 2866-PAK was successful in providing the legal framework for the insurance sector, contributing significantly to restructuring of PSIEs, and generally strengthening the financial standards for non-life insurance industry. Because of these impacts, the sustainability of TA

15

outputs is assessed as likely. TA 2867-PAK produced useful actuarial analysis of EOBI but failed to provide the roadmap of pension reforms, the main expected output. Therefore, sustainability of the impact of this TA is assessed as less likely. E. Impacts 47. Four out of the six TAs have generated impacts fully or substantially in line with expectations. TA 2393-PAK, followed by CMDP, was successful in strengthening the regulatory regime of the stock market and the capacity of SECP and SEs to some extent. It also helped enhance market image and growth, and had favorable impact on the financial soundness and resource mobilization ability of the leasing companies. TA 2812-PAK provided the basis for reform of government policy on NSS. This, in turn, gave a significant impetus to the corporate bond market, particularly to the advantage of the leasing industry. TA 2825-PAK yielded outcomes in reform of the regulatory frameworks for capital market and insurance. Impacts of TA 2865-PAK have been moderate and delayed as a key recommendation of the consultants proved impractical. TA 2866-PAK modernized the insurance law, institutionalized regulation of insurance within SECP, made substantial and positive impacts on the operation and management of PSIEs, and helped create the base for a competitive reinsurance industry by initiating a process of gradual dismantling of PRC’s monopoly. However, the TA impact on capacity building of PII was insignificant. The impact of TA 2867-PAK has been negligible, and limited largely to the actuarial study of EOBI as the basis for its reform in the future. F. Overall Rating 48. Based on the above, TA 2812-PAK is rated highly successful; TA 2393-PAK, TA 2825-PAK and TA 2866-PAK successful; and TA 2865-PAK and TA 2867-PAK partly successful. As a cluster, the TAs are assessed as relevant, efficacious, efficient, sustainable, and bearing substantial impacts. Overall, the TA cluster is rated successful.

V. CONCLUSIONS

A. Key Issues 49. There are several pending issues in the areas covered by TA 2393-PAK and CMDP. The first concerns the regulatory capacity of SECP. While SECP has acquired the reputation of an effective regulator of the stock market, it lacks capacity to regulate insurance and pension funds.22 The second set of issues relates to the preponderance of short-term speculative trades in the stock market and market manipulation by few powerful brokers. This projects a negative image of SEs and discourages investors from participating in the market. A related issue is that, barring very few stocks with large market capitalization,23 the secondary market is illiquid, which is probably the main reason that it is narrow and overly speculative. The third issue is that the MF management industry has not developed on professional grounds and as a result, most private sector MFs have performed poorly. Finally, the ABS market has remained underdeveloped. In view of its vast potential to be the main source of medium and long-term debt funds particularly for the leasing industry, a strong justification exists for further ADB support to develop the ABS market. 22 SECP’s mandate already covers insurance while the mandate to regulate pension funds is expected to be given to it in the near future. 23 Three most actively traded stocks represent 27.4% of market capitalization and 64.4% of turnover by number of

shares, and possibly even higher by value.

16

50. The residual issues in the MF area relate to privatization of NIT. The first is whether the Government should renew the letter of comfort regarding the repurchase price of NIT units in favor of the institutions holding them. Continuing dialogue with the Government is necessary in line with the objective of providing a level playing field to private sector MFs (para. 28). The other issue relates to staff redundancies that will result from NIT’s privatization. In this regard, the consultants’ recommendation, that some staff be absorbed in SECP, needs careful consideration but based only on a proper match between SECP’s needs and the qualifications of the staff separated from NIT. 51. The remaining issues in the insurance sector concern the regulatory capacity of SECP (for which some funding has been made available under Loan 1577-PAK),24 issuance of insurance rules to be enforced by SECP, restoring the credibility of PRC’s financial statements and its gradual privatization, and privatization of that part of NIC’s business which can be handled by the private sector. 52. In the area of pensions and provident funds, the major issue for the future is the financial sustainability of the Government’s pension obligations. The need for a well thought-out plan for funding government pensions, and its management by professional fund managers, is an urgent necessity, and a major challenge. Another issue relates to restructuring of EOBI. The Government needs to redefine the role of this important institution, strengthen its capacity to perform the assigned role, and ensure its financial sustainability. Finally, adoption of a regulatory framework for pensions, covering both public and private pensions, and appointing an independent pension regulator has assumed urgency. To that end, the Government needs to extend SECP’s mandate to cover regulation of the pension sector. 53. ADB has remained engaged with Government and SECP on these issues, and is providing further support to address most of them through a recently approved financial sector program.25 Real-time feedback provided by the OEM during its processing contributed to including several of these issues in the agenda of this program. B. Lessons Learned 54. The successful implementation of TA 2393-PAK confirmed that strong government ownership is critical to the success of any initiative to policy and institutional reform. Even though the TA had no direct bearing on the credit lines provided under the Financial Sector Intermediation Loan, to which it was attached (footnote 5), prior policy dialogue and ownership-building had strengthened the Government’s resolve to address the pressing issues in the stock market, MFs, leasing, and regulatory areas. Another lesson is that for healthy, balanced, and sustainable development of the capital market, it is necessary to develop all the major aspects of CMD, i.e., demand, supply, intermediation, and regulation. In the case of Pakistan, the supply of quality equity issues has lagged behind other CMD aspects, resulting in an overactive but narrow and highly speculative secondary market. 55. The main lesson from TA 2812-PAK is that sharply focused TAs, preceded and backed by effective policy dialogue, have a better chance of success than those that encompass a broad range of issues. This TA was highly successful because: (i) it was basically focused on a

24 Loan 1577-PAK(SF): Capacity Building of the Securities Market, for $5 million, approved on 6 November 1997. 25 The program, which was approved on 5 December 2002, comprises a policy loan (Loan 1955-PAK: Financial

[Nonbank] Market and Governance Program , for $260 million); two TA loans (Loan 1956-PAK[SF]: Strengthening Pension, Insurance, and Savings Systems, and Loan 1957-PAK[SF]: Strengthening Regulation, Enforcement, and Governance of Nonbank Financial Markets, for $3.0 million equivalent each); and two political risk guarantee facilities (PRG:PAK 33271, for a total of $150 million).

17

one-point agenda, (ii) the Government had shown willingness to deal with the issue at hand, and (iii) the consultant possessed the right blend of capabilities. Both small-scale TAs were largely implemented by domestic consultants; both have been assessed as highly efficient. The pertinent lesson from these TAs is that, subject to availability of adequately qualified professionals in the relevant field, as well as dedicated TA administration by ADB, use of domestic consultants is highly cost effective. 56. There are no particular lessons from TAs 2865-PAK and 2866-PAK that may be relevant to future TAs, except that shortcomings of TA design translate into shortcomings of TA outputs. The main lesson from TA 2867-PAK is that attempting to deal with too many complex issues under one TA is not effective. This is particularly so in situations where different sets of specialized skills are required to implement the TA. In those situations, it is difficult to engage a versatile team leader capable of leading from the front and coordinating effectively the inputs and outputs of different TA components or aspects. A related lesson is that TAs involving complex issues should be implemented in phases, and in a proper sequence, after basic understandings have been reached with the Government during the policy dialogue. C. Recommendations and Follow-Up Actions 57. To resolve the residual issues related to the TAs covered by the TA performance audit report following actions are recommended.

(i) ADB and SECP should take additional measures to promote ABS and develop primary and secondary ABS markets. For this purpose, the scope of TA Loan 1957-PAK(SF) (footnote 25) should be amended by 30 June 2003.

(ii) The Government should expedite privatization of NIT. To that end, the Government should resolve the issue of repurchase price guarantee by 30 June 2003. ADB should maintain an active dialogue with the Government, particularly on measures to mitigate the impact of staff redundancy.

(iii) The Government should: (a) by 30 April 2003, approve the draft of the insurance

rules relevant to SECP’s mandate; (b) by 30 June 2003, prepare a time-bound action plan to clean up PRC’s financial statements so as to make them transparent and unqualified and, by 30 June 2004, implement that plan; and (c) by 31 December 2003, place NIC’s commercial business into a separate entity with a view to privatizing that entity subsequently.

58. Further TA possibilities should be explored by the Government, SECP, and ADB to support the actions outlined above.

Appendix 1 18

EVALUATION OF TA 2393-PAK: CAPITAL MARKET DEVELOPMENT

A. Introduction

1. Background 1. The involvement of the Asian Development Bank (ADB) in Pakistan’s financial sector dates back to 1968. Since the mid-1980s, the focus of ADB assistance to the sector shifted from providing credit lines to developing long-term financial markets. An umbrella credit line approved in 19831 was predicated on a binding Government commitment to initiate reforms to encourage domestic mobilization of long-term resources. This was followed by reforms to liberalize interest rate, credit allocation and monetary control policies of Government and the central bank, the State Bank of Pakistan, and to develop the government bond market under the Industrial Sector Program;2 and subsequently by a technical assistance (TA) for a study of the country’s securities markets.3 TA 2393-PAK4 was the first major ADB initiative for capital market development (CMD) in Pakistan, and was provided in conjunction with the Financial Sector Intermediation Loan.5 2. Rationale and Concept 2. At the time of TA formulation, ADB strategy for the financial sector in Pakistan included a focus on assisting its structural transformation from directed to market-led operation. This transformation would address critical capital resource deficiencies, and place greater reliance on a dynamic private sector capable of generating foreign and domestic capital resources to finance industrial growth. This purpose was consistent with ADB’s country operational strategy, which called for greater private sector participation in the pursuit of economic growth. Accordingly, ADB’s financial sector operations aimed to rationalize the financial system and enhance the efficiency of the capital market, thereby transforming it into a significant source of funds to support expanded private sector industrial investment. To give the capital market more depth and make it more responsive to the changing needs of the private sector, reforms were particularly needed for (i) diversifying the financial instruments available to investors, as well as the funding sources for the leasing sector; (ii) allowing market-determined pricing of new share issues; (iii) enhancing the transparency and efficacy of the stock exchanges (SEs); (iv) improving the regulatory operations of the Corporate Law Authority (CLA); and (v) enhancing the efficiency of the mutual fund (MF) industry. The TA was a response to these needs. 3. Objectives and Scope 3. The TA focused on three important aspects of CMD: operation and regulation of SEs, the MF industry, and the leasing industry. Its main objectives were to develop the stock market

1 Loan 678-PAK and Loan 679-PAK(SF): Development Finance Loan, for $110 million approved on 20 December

1983. 2 Loan 931-PAK and Loan 932-PAK(SF): Industrial Sector Program , for $200 million, approved on 13 December

1988. 3 TA 1096-PAK: Study on Development of a Secondary Market for Fixed Income Securities, for $176,000, approved