tax 1 reviewer

DESCRIPTION

Finals reviewer based on syllabus of Prof LafortezaTRANSCRIPT

Tax 1– Laforteza Camille Umali | FINALS REVIEWER

1

INCOME TAXATION

A. Introduction

Fisher v. Trinidad Income is the return in money from one‘s

business, labor, or capital invested; gains, profit or private revenue.

An Income Tax is a tax on the yearly profits arising from property, profession, trades and offices.

Capital is the tree or land while Income is the fruit or the crop. The former is a reservoir supplied from springs while the latter is the outlet stream, to be measured by its flow during a period of time.

1. History

Madrigal v. Rafferty The income tax law of the US, extended to the

Philippines, is a canon of taxation and social reform put into statutory form. It aims to mitigate the evils from inequalities of wealth by a progressive scheme of taxation, which places the burden on those best able to pay.

The Income tax law, as extended by the US Congress to the Philippines, being a law of American origin and intricate in its provisions, the authoritative decision of the official charged with its enforcement has force for the Philippines.

2. Meaning of Income

Eisner v. Macomber Income is not merely a growth or increment of

value in an investment, but a gain, a profit in excess or capital as a result of exchange transaction.

Income is a gain, a profit or something of exchangeable value proceeding from the property, severed from the capital, however invested or employed and coming in, being ‗derived‘.

It is received or drawn by recipient (taxpayer) for his separate use, benefit and disposal, that is income derived from property.

RR 2-40 Income – all earnings derived from service

rendered (labor, from capital (business or investment), or both including gain derived from sale or exchange of personal or real property either ordinary or capital asset.

Test: increase in net worth

Return OF capital v. return ON capital Capital v. Income Revenue v. Income Receipt v. Income Taxable income pertinent items of gross income specified in

the Tax Code less the deductions, if any, and/or personal and additional exemptions authorized by such types of income in the tax code or other special laws

income less statutory deductions Characteristics: 1. There must be gain or profit 2. The gain must be realized or received 3. The law or treaty does not exclude the gain

from taxation. 3. Classification of income taxpayers Individual i. Citizen 1) resident 2) non-resident ii. Alien 1) resident 2) non resident a. engaged in T/B b. not engaged in T/B Corporation i. domestic ii. foreign 1) resident (engaged in T/B) 2) nonresident (not engaged in T/B) General partnership i. general professional ii. general co-partnership Estate and Trust 4. General Principle GR taxable only for income derived from

sources within the Philippines E taxable within or without 1. Resident citizen 2. Domestic corporation Criteria: 1. Citizenship 2. Residence 3. Source

Tax 1– Laforteza Camille Umali | FINALS REVIEWER

2

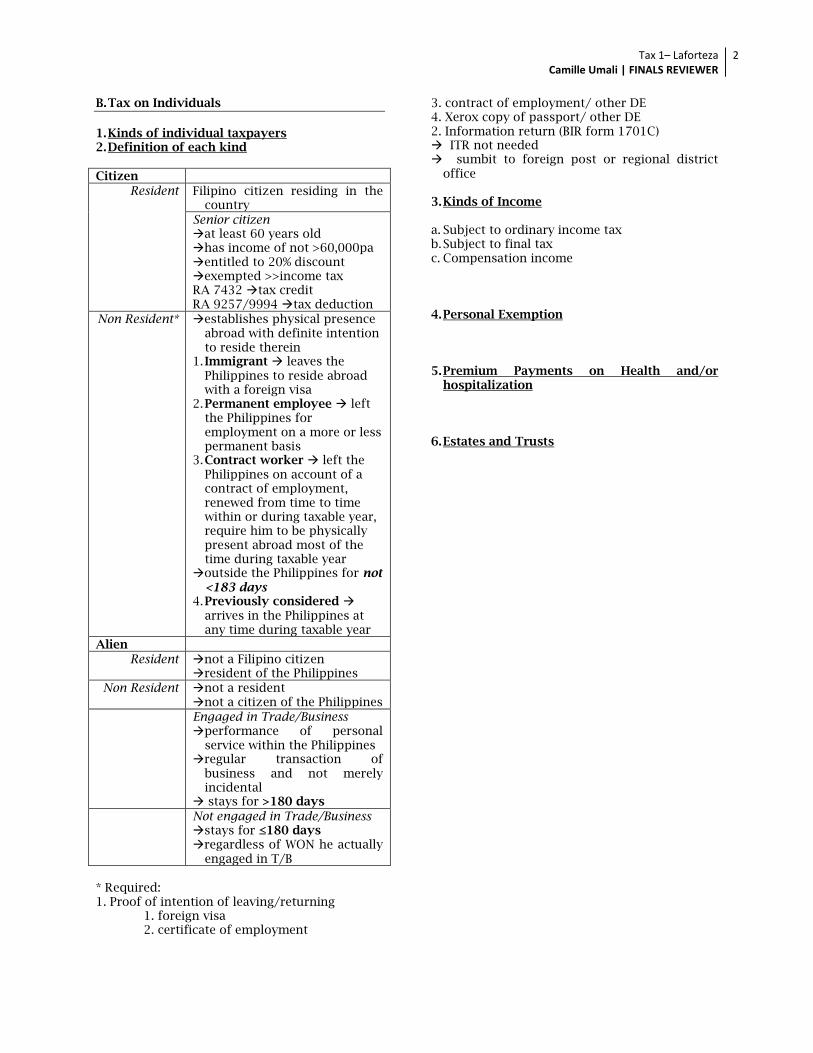

B. Tax on Individuals

1. Kinds of individual taxpayers 2. Definition of each kind

Citizen

Resident Filipino citizen residing in the country

Senior citizen at least 60 years old has income of not >60,000pa entitled to 20% discount exempted >>income tax RA 7432 tax credit RA 9257/9994 tax deduction

Non Resident* establishes physical presence abroad with definite intention to reside therein

1. Immigrant leaves the Philippines to reside abroad with a foreign visa

2. Permanent employee left the Philippines for employment on a more or less permanent basis

3. Contract worker left the Philippines on account of a contract of employment, renewed from time to time within or during taxable year, require him to be physically present abroad most of the time during taxable year

outside the Philippines for not <183 days

4. Previously considered arrives in the Philippines at any time during taxable year

Alien

Resident not a Filipino citizen resident of the Philippines

Non Resident not a resident not a citizen of the Philippines

Engaged in Trade/Business performance of personal

service within the Philippines regular transaction of

business and not merely incidental

stays for >180 days

Not engaged in Trade/Business stays for ≤180 days regardless of WON he actually

engaged in T/B

* Required: 1. Proof of intention of leaving/returning 1. foreign visa 2. certificate of employment

3. contract of employment/ other DE 4. Xerox copy of passport/ other DE 2. Information return (BIR form 1701C) ITR not needed sumbit to foreign post or regional district

office 3. Kinds of Income a. Subject to ordinary income tax b. Subject to final tax c. Compensation income 4. Personal Exemption 5. Premium Payments on Health and/or

hospitalization 6. Estates and Trusts

Tax 1– Laforteza Camille Umali | FINALS REVIEWER

3

C. Tax on Corporations

1. Definition Corporation include: 1. partnerships, no matter how created or

organized 2. Joint stock companies 3. Joint accounts 4. Association 5. Insurance companies not include 1. General professional partnership 2. Joint venture or consortium for construction

project or engaging in petroleum, coal, geothermal and other energy operations pursuant to an operating consortium agreement under service contract with government

CIR v. Batangas Transport Corporation Two bus companies undertook a ―Joint

Emergency Operation‖ an appointed 1 manager to save on overhead expenses.

Single entity, company or partnership The companies contributed to a common fund to

pay for the expenses of the JEO. The gross income were merged and the net income divided equally between them.

Although no legal personality may have been formed by JEO, it nevertheless operated the affairs of the companies as though constituting a single entity, company or partnership.

Ona v. CIR Inheritance of the children was not divided. It

remained in the management of one of the children who used it in business of leasing or selling and investing the proceeds in real properties and securities.

partnership The co-ownership of inherited properties is

automatically converted to an unregistered partnership the moment the common properties or income derived therefrom are used as a common fund with intent to produce profits for the heirs in proportion to their respective shares in the inheritance as determined by the project of partition in an extrajudicial settlement or with court approval.

If after the partition, the heir allows his share to be held in common with the co-heirs under single management for use with intent of making profit, even if no document is executed, an UNREGISTERED PARTNERSHIP is formed.

BIR Ruling 317-92 ALI and API intends to pool together their

resources to construct a building and then lease it out to 3rd party tenants.

MOA(Agreement) per se is not a joint venture. Leasing of the floors separately owned will create a joint venture.

Rentals are income of the JV. Net income distributed are considered as dividends of API and ALI and are exempt from tax.

Obillos v. CIR Land inherited by children was sold. Income tax

was paid on capital gain but CIR assessed for corporate income tax.

Isolated transaction and not a joint venture The sale of the land was with intention to

dissolve the co-ownership and the division of profit was merely incidental.

Note: possibly donor’s tax

2. Classification

Domestic Created or organized under Philippine Laws

Foreign

Resident FC engaged in T/B in the Philippines

Non-resident FC NOT engaged in T/B in the Philippines

Special corporations: 1. Private education institutions and non-profit

hospitals 2. Non-resident cinematographic film owner,

lessor or distributor 3. International carrier* 4. NRFC owner of vessel 5. NRFC lessor of aircraft, machineries and

other equipments 6. FCDU/OBU 7. Petroleum service contractor and sub-

contractor** 8. Enterprises under BCDA and PEZA***

*United Airlines v. CIR If an international air carrier maintains flights to

and from the Philippines, it shall be taxed at the rate of 2½% of its GPB, otherwise, income from other activities in the country will be taxed at 32%. (now, 30%)

**Tax on subcontractor 8% gross income from petroleum operations 30% (regular tax) other income

Tax 1– Laforteza Camille Umali | FINALS REVIEWER

4

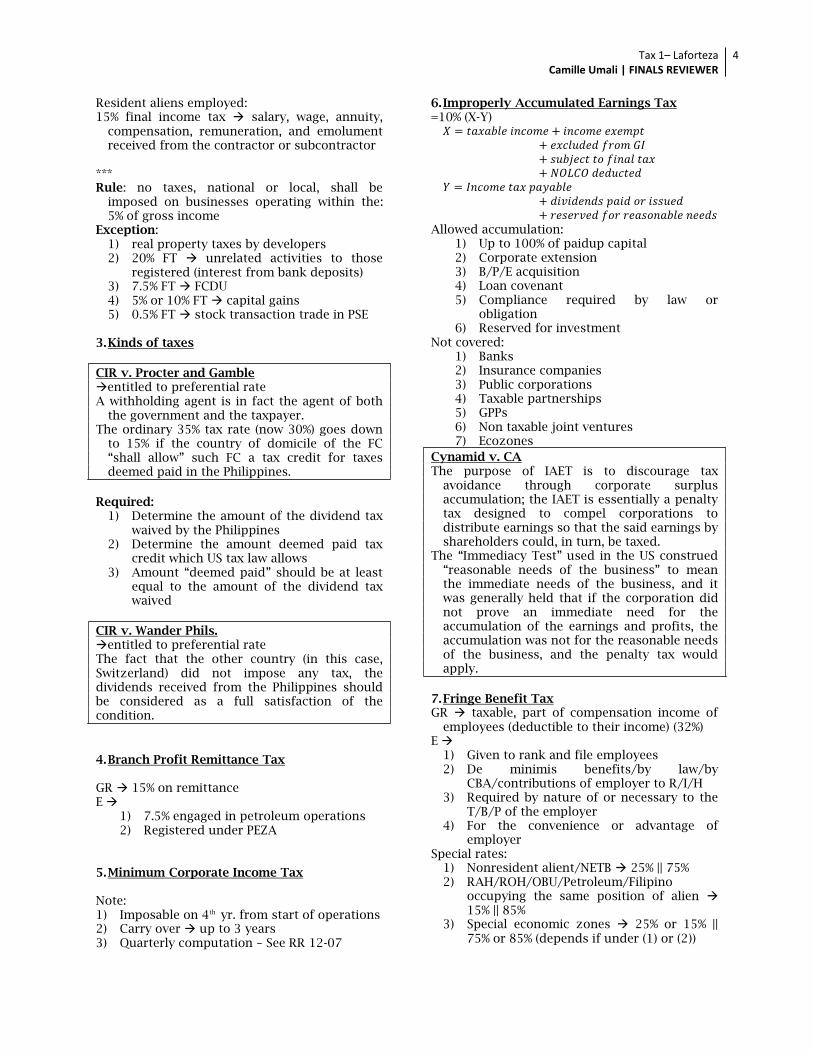

Resident aliens employed: 15% final income tax salary, wage, annuity,

compensation, remuneration, and emolument received from the contractor or subcontractor

*** Rule: no taxes, national or local, shall be

imposed on businesses operating within the: 5% of gross income

Exception: 1) real property taxes by developers 2) 20% FT unrelated activities to those

registered (interest from bank deposits) 3) 7.5% FT FCDU 4) 5% or 10% FT capital gains 5) 0.5% FT stock transaction trade in PSE

3. Kinds of taxes

CIR v. Procter and Gamble entitled to preferential rate A withholding agent is in fact the agent of both

the government and the taxpayer. The ordinary 35% tax rate (now 30%) goes down

to 15% if the country of domicile of the FC ―shall allow‖ such FC a tax credit for taxes deemed paid in the Philippines.

Required:

1) Determine the amount of the dividend tax waived by the Philippines

2) Determine the amount deemed paid tax credit which US tax law allows

3) Amount ―deemed paid‖ should be at least equal to the amount of the dividend tax waived

CIR v. Wander Phils. entitled to preferential rate The fact that the other country (in this case, Switzerland) did not impose any tax, the dividends received from the Philippines should be considered as a full satisfaction of the condition.

4. Branch Profit Remittance Tax GR 15% on remittance E

1) 7.5% engaged in petroleum operations 2) Registered under PEZA

5. Minimum Corporate Income Tax Note: 1) Imposable on 4th yr. from start of operations 2) Carry over up to 3 years 3) Quarterly computation – See RR 12-07

6. Improperly Accumulated Earnings Tax =10% (X-Y)

Allowed accumulation: 1) Up to 100% of paidup capital 2) Corporate extension 3) B/P/E acquisition 4) Loan covenant 5) Compliance required by law or

obligation 6) Reserved for investment

Not covered: 1) Banks 2) Insurance companies 3) Public corporations 4) Taxable partnerships 5) GPPs 6) Non taxable joint ventures 7) Ecozones

Cynamid v. CA The purpose of IAET is to discourage tax

avoidance through corporate surplus accumulation; the IAET is essentially a penalty tax designed to compel corporations to distribute earnings so that the said earnings by shareholders could, in turn, be taxed.

The ―Immediacy Test‖ used in the US construed ―reasonable needs of the business‖ to mean the immediate needs of the business, and it was generally held that if the corporation did not prove an immediate need for the accumulation of the earnings and profits, the accumulation was not for the reasonable needs of the business, and the penalty tax would apply.

7. Fringe Benefit Tax GR taxable, part of compensation income of

employees (deductible to their income) (32%) E

1) Given to rank and file employees 2) De minimis benefits/by law/by

CBA/contributions of employer to R/I/H 3) Required by nature of or necessary to the

T/B/P of the employer 4) For the convenience or advantage of

employer Special rates:

1) Nonresident alient/NETB 25% || 75% 2) RAH/ROH/OBU/Petroleum/Filipino

occupying the same position of alien 15% || 85%

3) Special economic zones 25% or 15% || 75% or 85% (depends if under (1) or (2))

Tax 1– Laforteza Camille Umali | FINALS REVIEWER

5

D. Exempt Entities

1) Partnership / joint ventures – energy

operations 2) Co-ownership 3) By law (NIRC)* 4) Under special laws**

* Under NIRC

Sinco v. CIR Every responsible organization must be run as to

at least insure its existence by operating within the limits of its own resources, especially its regular income—i.e. it should strive to operate at a surplus. The benefits of the exemption under Sec. 30(E) do not apply only to institutions on the verge of bankruptcy.

** Under special laws

1) RP-US tax treaty 2) Registered enterprises under Omnibus

investment code 3) Jewelry Manufacturing Industry – excise

tax 4) Cooperatives on their transactions to

members 5) Barangay micro-business enterprise

E. Inclusions and Exclusions from Gross Income

Test in determining income:

Flow of wealth WON gain is derived from transaction

Realization/ Severance

WON there is separation from capital of something of exchangeable value

Claim of right WON there is receipt of cash or property that ordinarily constitutes income

Economic Benefit

WON there is economic benefit that increases net worth

All-events 1. Fix right to income or liability to pay

2. Availability of reasonable accurate determination of such income or liability

Capital v. Income

Capital Income

Fund or property Flow of wealth

Not subject to tax Subject to tax

Tree Fruit

Types: 1. Compensation rendering service

2. Professional engaging in an endeavor requiring special training as professional

3. Business gains or profits derived from trade or business

4. Passive received by merely waiting for the amount to come in (interest, royalty, dividend, winnings, and prizes)

5. Capital Gain dealings in capital assets

Tax 1– Laforteza Camille Umali | FINALS REVIEWER

6

F. Items on Gross income

G. Interest Income

Citizen Alien DC FC

R NR R NRETB NRNETB ETB NETB

Interest from bank deposits, etc.*

20% 20% 20% 20% 25% 20% 20% 20%

Interest from FCDU/OBU

7.5% Exempt 7.5% Exempt Exempt 7.5% 7.5% Exempt

Interest from loans, other than those

enumerated** GIT GIT GIT GIT 25% 30% 30% 20%

Interest from long term deposit loans

GR: Exempt E: pre-terminated (GIT or 25%)

20% or 30%

20% or 30%

20%

* Except: employee trust fund or retirement plan EXEMPT ** Except: loan granted by foreign government EXEMPT

Filinvest v. CIR New SC decision (2011) Requisites for non-recognition of gain or lossL 1) The transferee is a corporation 2) Transferee exchanges its shares of stock for

properties of the transferor

3) Transfer is made by a person (not exceeding 4 persons)

4) As a result of exchange, transferor gains control of the transferee.

H. Income under Lease Agreement

Citizen Alien DC FC

R NR R NRETB NRNETB ETB NETB

Rent Income GIT GIT GIT GIT 25% 30% 30% 30%

Improvements by lessee: 1) Report the FMV upon completion 2) Report depreciated value over remaining life after expiration of lease period

I. Dividend Income

Citizen Alien DC FC

R NR R NRETB NRNETB ETB NETB

Paid by domestic corporation

10% 10% 10% 10% 25% Exempt Exempt 15% or

30%

Paid by foreign corporation**

GIT Exempt Exempt Exempt Exempt 30%* Exempt Exempt

*Except: lower rate is imposed under a tax treaty ** Treated as income from source NOT within

the Philippines Cash taxable Property taxable Stock Not taxable Liquidating taxable, treated as ordinary

income

CIR v. Manning A stock dividend, being one payable in capital

stock, cannot be declared out of outstanding corporate stock, but only from retained earnings:

The respondents, using the trust instrument as a convenient technical device, bestowed unto themselves the full worth and value of corporate holdings with the use of the very earnings of the companies. Such package device, obviously not designed to carry out the usual stock dividend purpose of corporate expansion reinvestment, e.g. the acquisition of additional facilities and other capital budget items, but exclusively for expanding the capital base of the respondents in MANTRASCO, cannot be allowed to deflect the respondents' responsibilities toward our income tax laws

Tax 1– Laforteza Camille Umali | FINALS REVIEWER

7

Cash dividend Stock dividend

-disbursement to the stockholders of accumulated earning

- corporation at once parts irrevocably with all interest thereon

- whether large or small, are regarded as "income"

- no disbursement by the corporation and parts with nothing to the stockholders

- not an actual dividend, but certificates of stock which evidence in a new proportion his interest in the entire capital

- property of the corporation and not the stockholder

Wise v. Meer Where a corporation, partnership, association,

joint-account, or insurance company distributes all of its assets in complete liquidation or dissolution, the gain realized or loss sustained by the stockholder, whether individual or corporation, is a taxable income or a deductible loss as the case may be.

CIR v. CTA (ANSCOR) General Rule: A stock dividend representing the

transfer of surplus to capital account shall not be subject to tax.

Exception - If a corporation cancels or redeems stock issued as a dividend at such time and in such manner as to make the distribution and cancellation or redemption, in whole or in part, essentially equivalent to the distribution of a taxable dividend, the amount so distributed in redemption or cancellation of the stock shall be considered as taxable income to the extent it represents a distribution of earnings or profits accumulated after March 1, 1913

For the exempting clause of Section, 83(b) to apply, it is indispensable that:

(a) there is redemption or cancellation; (b) the transaction involves stock dividends

and (c) the "time and manner" of the transaction

makes it "essentially equivalent to a distribution of taxable dividends." (this is the most important)

J. Income from any source whatsoever

1) Bad debt recovery 2) Forgiveness of debt

a. Compensation of service b. Gift c. Payment of dividend

3) Tax refund 4) Damage recovery

5) Prizes and winnings Exceptions:

a. Less than 10,000 b. PCSO and lotto winnings c. In recognition of religious,

charitable, scientific, educational, artistic, literary or civic achievement

Selected without any action on his part

Not required to render service

d. Given to athletes in local or international sports competitions and tournaments

6) Any other source (not expressly excluded or exempted)

Gutierrez v. CTA Although the condemnation or expropriation of

properties was provided for in the treaty, the exemption from tax of the compensation to be paid for the expropriation of privately owned lands located in the Philippines was not given any attention, and the internal revenue exemptions specifically taken care of by said Agreement applies only to members of the U.S. Armed Forces serving in the Philippines and U.S. nationals working in these Islands in connection with the construction, maintenance, operation and defense of said bases

K. Classes of Deductions

1) Optional Standard deduction

Individual: 40% of gross sales/receipts Corporation: 40% of gross income

2) Itemized deductions

a. Expenses b. Interest c. Taxes d. Losses e. Bad debts f. Depreciation g. Depletion h. Charitable and other contributions i. Research and development j. Pension trust

Tax 1– Laforteza Camille Umali | FINALS REVIEWER

8

L. Expenses in General

1) Business expenses 1) Reasonable 2) ordinary and necessary 3) Paid or incurred during the taxable year 4) directly attributable to the development, management, operation

and/or conduct of the trade, business or exercise of profession 5) Supported by adequate invoices or receipts 6) Not Contrary to law, public policy or morals. Operating expenses of

illegal or questionable business are deductible, but expenses of an inherently illegal nature, such as bribery and protection payments are not

7) The tax required to be withheld on the amount paid or payable is shown to have been paid to the BIR.

2) Travelling expenses

Otherwise: Fringe benefit

GR considered as taxable compensation income of employee (graduated rate)

E Fringe benefit 1) not connected with T/B/P 2) travel of family members

3) Cost of materials 1) Actually consumed and used in operations 2) During year for which return is made 3) Not deducted in determining the net income in prior years

4) Repairs

Otherwise: depreciation

1) Did not materially add to the value of property 2) Did not prolong its life 3) For keeping it in ordinarily efficient operating condition 4) PPE did not increase by the amount of repair

5) Professional expenses 1) Cost of supplies used in practice of profession 2) Expenses and repairs in transportation used 3) Dues to professional societies 4) Rent paid and utilities expense 5) Books, furniture and other instruments (if not permanent)

6) Compensation for Personal Service

1) Reasonable 2) ordinary and necessary 3) Paid or incurred during the taxable year 4) directly attributable to the trade, business or exercise of profession 5) for services actually rendered

7) Bonuses to employees 1) Made in good faith 2) Services actually rendered 3) Do not exceed reasonable compensation

8) Pension, compensation for injuries

1) Amount not compensated by insurance

9) Rentals 1) Acquired for business purposes (see income from leasehold)

10) Entertainment expense 1) Not contrary to L/M/PP/PO 2) Substantiated by sufficient evidence 3) Limited to ceiling requirement (0.5% of net sales or 1% of net

revenue) 4) For definite purpose – connected to business

Visayan v. CIR Court looked at the representation expenses for

the previous years and compared it with the corresponding gross income and net profit to come up with the representation expense for the year being questioned whereas the company did not present any supporting evidence.

Kuenzle v. CIR GR bonuses to employees made in good faith

and as additional compensation for services actually rendered are deductible

No fixed test for determining the reasonableness. Factors to be considered: (as a whole:

1) the amount and the quality of the services performed with relation to the business

2) made in good faith 3) the character of the taxpayer's business,

Tax 1– Laforteza Camille Umali | FINALS REVIEWER

9

4) the volume and amount of its net earnings, 5) its locality, 6) the type and extent of the services rendered, 7) the salary policy of the corporation"; 8) the size of the particular business 9) the employees' qualifications 10) contributions to the business venture 11) general economic conditions

Alhambra v. CIR whenever a controversy arises on the

deductibility, for purposes of income tax, of certain items for alleged compensation of officers of the taxpayers (this case also involves bonuses given to non-resident Pres and VP) two questions become material, namely:

a) have ―personal service‖ been ―actually rendered‖ by said officers?

b) in the alternative case, what is the ―reasonable allowance‖ therfore?

Calanoc v. CIR The payment for police protection is illegal as it

is a compensation given for the latter‘s functions and required by them to render by law.

M. Interest

Required a) There must be indebtedness. Indebtedness is

something owned by one who is unconditionally obligated or bound to pay.

b) There should be an interest expense paid or incurred upon such indebtedness.

c) The indebtedness must be of the taxpayer. d) The indebtedness must be connected with

the taxpayer‘s trade, business or exercise of profession.

e) The interest expense must have been paid or incurred during the taxable year.

f) The interest must have been stipulated in writing

g) The interest must be legally due. h) The interest payment arrangement must not

be between related taxpayers. i) The interest must not be incurred to finance

petroleum operations. j) In case of interest incurred to acquire

property used in trade, business or exercise of profession, the same was not treated as a capital expenditure.

Not included:

1) Amortization 2) Related persons 3) Finance petroleum operations 4) Obligation is tax exempt

Rule reduced by 33% of the interest income subjected to final tax

CIR v. Vda. De Prieto Interest on account of delinquency in payment of taxes may be deducted as interest expense but not as taxes paid.

N. Taxes

Required:

1) Paid and incurred within taxable year 2) In connection with T/B/P 3) Imposed directly on the taxpayer 4) Connected with income from sources

within the Philippines

Deductible 1) DST 2) Occupational tax 3) Privilege/license tax 4) Excise tax 5) Import duties 6) Local business tax 7) Automobile registration fees 8) Community tax 9) Municipal tax

Not deductible

1) Income tax 2) Estate/donor‘s tax 3) Foreign income tax as tax credit 4) Percentage tax on stock transactions 5) VAT 6) Taxes not related to T/B/P 7) Special assessment tax 8) Surcharges 9) Compromise penalty

CIR v. Lednicky Alien resident is precluded from deducting the foreign income taxes from his gross income unless he has a right to claim the same as tax credit.

CIR v. Bicolandia Rule now: 20% discount to senior citizens may now be claimed as tax deduction (RA 9257)

Gutierrez v. CIR Deductions from gross income are matters of legislative grace; what is not expressly granted by Congress is withheld. Moreover, when acts are condemned by law and their commission is made punishable by fines or forfeitures, to allow them to be deducted from the wrongdoer's gross income, reduces, and so in part defeats, the prescribed punishment.

Tax 1– Laforteza Camille Umali | FINALS REVIEWER

10

O. Losses

By individuals: (not compensated by insurance)

1) Incurred in T/B/P 2) Incurred in transaction entered into for

profit 3) Casualty losses (fire, storm, shipwreck,

robbery, embezzlement etc.) By corporation: (not compensated by insurance)

1) Actually sustained and charged off Required 1. The loss must be that of the taxpayer. 2. Actually sustained and charged off within

the taxable year; 3. Evidenced by a closed and completed

transaction; 4. Not claimed as a deduction for estate tax

purposes; 5. In the case of an individual, the loss must be

connected with his profession, trade or business, or incurred in any transaction entered into for profit though not connected with his trade or business;

6. In the case of casualty loss, declaration of loss is filed within 45 days from the occurrence of the casualty loss;

7. Not arise from a sham sale. 8. Not compensated by insurance or otherwise. Special rules:

1) Voluntary removal of building 2) Loss of useful value of assets 3) Shrinkage in value of stocks

NOLCO

1) 3 year period 2) No substantial change in ownership

(75%) P. Bad debts

Required:

1) Existing, valid and legally demandable obligation

2) Connected with T/B/P 3) Not between related parties 4) Actually charged off the books of the

taxpayer at year end 5) Actually ascertained to be worthless and

uncollectible

CIR v. Goodrich The requirement of ascertainment of worthlessness requires proof of two facts: (1) that the taxpayer did in fact ascertain the debt to be worthlessness, in the year for which the

deduction is sought; and (2) that, in so doing, he acted in good faith. Good faith on the part of the taxpayer is not enough. He must show, also, that he had reasonably investigated the relevant facts and had drawn a reasonable inference from the information thus obtained by him.

PHILEX v. CIR Not bad debts there was no stipulation to

actually repay the cash and property advanced, but only to return the amount pegged at a ratio which the manager‘s account had to the owner‘s account.

Q. Depreciation

Required:

1) Reasonable 2) Arising out of its use in T/B/P 3) Charged off during taxable year 4) Statement of the allowance attached 5) Located in the Philippines (for NRA/FC) 6) Have limited useful life

Methods:

1) Straight line 2) DB/DDB 3) Sum of years digit

Zamora v. CIR Bulletin F has no binding force, but it has a

strong persuasive effect considering that the same has been the result of scientific studies and observation for a long period in the United States after whose Income Tax Law ours is patterned.

R. Depletion

Depletion expense =

Cost = extent of capital invested Adjusted cost does NOT include:

1) Amounts recoverable through depreciation

2) Residual value of improvements 3) Exploration expense* 4) Development expense*

* capitalized

Tax 1– Laforteza Camille Umali | FINALS REVIEWER

11

S. Pension Trust

Required:

1) Reasonable and actuarially sound 2) During the taxable year 3) In excess of contribution 4) Not yet allowed as deduction

apportioned equally over a period of 10 years

5) Approved by BIR T. Charitable and other contributions

Required:

1) Engaged in T/B/P 2) Actual payment 3) Recipient is one specified by law 4) Not inure to benefit of an individual or

private stockholder Fully deductible:

1) Government (GOCC, subdivision) a. Education b. Health c. Youth/Sports development d. Human settlement e. Science and culture f. Economic development

2) International organization 3) Accredited NGO

a. Not >30% is for admin purposes b. Utilized not later than 15th day, 3rd

month of taxable year c. Distribute asset to another NGO or

to the state upon dissolution Limit: Individual: (lower)

1) 10% of taxable income 2) Actual contribution

Corporation (lower)

1) 5% of taxable income 2) Actual contribution

U. Research and Development expenses

GR ordinary and necessary expenses deductible during the taxable year E Deferred expense (60 months)

1) In connection with T/B/P 2) Not treated as expense (ordinary) 3) Chargeable to capital account but not to

any specific property which is subject to depreciation or depletion

V. Imposition of ceilings

By SOF:

1) upon recommendation of CIR 2) after public hearing

Factors

1) adequacy of prescribed limits on actual expenditure requirements

2) effects of inflation Except: those already subject to a ceiling W. Additional requirement for

deductibility

Required: shown to be have been paid to BIR X. Items not deductible

1) Personal, living and family expenses 2) Improvements to increase value of property 3) Restoration of property 4) Premiums paid on life insurance 5) Losses from sales or exchange of property:

a. Between family members b. Between individual and corporation

individual owns >50% of the corp EXCEPT: distribution in liquidation

c. Corporation owning >50% of another d. Grantor and fiduciary e. 2 fiduciaries, same grantor f. Fiduciary and beneficiary

Atlas v. CIR Statutory Test of Deductibility: 1. The expense must be ordinary and

necessary, 2. It must be paid or incurred within the

taxable year, and 3. It must be paid or incurred in carrying in a

trade or business. Ordinarily, an expense will be considered

"necessary" where the expenditure is appropriate and helpful in the development of the taxpayer's business. It is "ordinary" when it connotes a payment which is normal in relation to the business of the taxpayer and the surrounding circumstances

Tax 1– Laforteza Camille Umali | FINALS REVIEWER

12

Y. Sale or exchange of property

The term ―capital assets‖ means property held

by the taxpayer (whether or not connected with his trade or business), but DOES NOT include:

1) Stock in trade of the taxpayer or other property of a kind which would properly be included in the inventory of the taxpayer if on hand at the close of the taxable year;

2) Property held by the taxpayer primarily for sale to customers in the ordinary course of his trade or business;

3) Property used in trade or business, of a character which is subject to the allowance for depreciation provided in Subsection (F) of Section 34; OR

4) Real property used in trade or business of the taxpayer.

Calasanz v. CIR There is no rigid rule or fixed formula by which

it can be determined with finality whether property sold by a taxpayer was held primarily for sale to customers in the ordinary course of his trade or business or whether it was sold as a capital asset. Although several factors or indices have been recognized as helpful guides in making a determination, none of these is decisive; neither is the presence nor the absence of these factors conclusive. Each case must in the last analysis rest upon its own peculiar facts and circumstances.

Determination of gain or loss: If cost > fmv

a. SP > cost: gain = SP – Cost (V) b. SP < cost, SP > FMV: loss = SP – FMV (II) c. FMV < SP < cost: not deductible (IV)

If cost < fmv

a. SP > fmv: gain = SP – FMV (I) b. Cost < SP < FMV : not deductible (III) c. SP < fmv, SP < cost: loss = SP – Cost (VI)

CIR v. Aquafresh Zonal value is determined for the purpose of

establishing a more realistic basis for real property valuation. Since internal revenue taxes are assessed on basis of valuation existing at the time of the sale should be taken into account.

CIR v. Rufino One indication of a scheme to evade the capital gains tax is the subsequent dissolution of the new corporation after the transfer to it of the properties of the old corporation and the liquidation of the former soon thereafter.

Gregory v. Helvering Rule: The rule which excludes from consideration the motive of tax avoidance is not pertinent to the situation, because the transaction upon its face lies outside the plain intent of the statute. To hold otherwise would be to exalt artifice above reality and to deprive the statutory provision in question of all serious purpose. Case: the Court found simply an operation having no business or corporate purpose- a mere device which put on the form of a corporate reorganization as a disguise for concealing its real character, and the sole object and accomplishment of which was the consummation of a preconceived plan, not to reorganize a business or any part of a business, but to transfer a parcel of corporate shares to the petitioner. No doubt, a new and valid corporation was created. But that corporation was nothing more than a contrivance to the end last described. It was brought into existence for no other purpose; it performed, as it was intended from the beginning it should perform, no other function.

Z. Situs of Taxation

Within the Philippines

1) Interest on bonds, etc. of residents and corporations

2) Dividends received by domestic corporation or foreign corporation (Except if <50% for the past 3 years was derived from sources within the Philippines)

3) Services performed in the Philippines 4) Rentals and Royalties of property

located in the Philippines 5) Sale of real property located in the

Philippines 6) Sale of personal property*

Interest residence of debtor Dividend residence of payor-corporation Service Place of performance Sale of real property location of property *Sale of personal property GR Purchased where sold Produced partly

E shares of stock of domestic corporation Philippines

CIR v. CTA, Smith Kline where an expense is clearly related to the

production of Philippine-derived income or to Philippine operations (e.g. salaries of Philippine personnel, rental of office building in the Philippines), that expense can be deducted from the gross income acquired in

Tax 1– Laforteza Camille Umali | FINALS REVIEWER

13

the Philippines without resorting to apportionment. The overhead expenses incurred by the parent company in connection with finance, administration, and research and development, all of which direct benefit its branches all over the world, including the Philippines, fall under a different category however. These are items which cannot be definitely allocated or identified with the operations of the Philippine branch

GENERAL RULE. – Deduct the expenses, losses

and other deductions properly allocated thereto and a ratable part of expenses, interests, losses and other deductions effectively connected with the business or trade conducted exclusively within the Philippines which cannot definitely be allocated to some items or class of gross income: Provided, That such items of deductions shall be allowed only if fully substantiated by all the information necessary for its calculation. The remainder, if any, shall be treated in full as taxable income from sources within the Philippines.

EXCEPTION. - No deductions for interest paid or

incurred abroad shall be allowed unless indebtedness was actually incurred to provide funds for use in connection with the conduct or operation of trade or business in the Philippines.

Philamlife v. CTA It is not the presence of any property from

which one derives rentals and royalties that is controlling. As long as the services fall from any of the items mentioned in Sec. 37 of the NIRC, such would be considered as income from sources within the Philippines.

AA. Accounting Periods and Methods

Accounting methods 1. Cash receipts and disbursements method – all

items of gross income received during the year shall be accounted for in such taxable year and that only expenses actually paid shall be claimed as deductions during the year.

Income is realized upon actual or constructive

receipt of cash or its equivalent, and expenses are deductible only upon actual payment thereof.

2. Accrual method – method of accounting for

income in the period it is earned, regardless of whether it has been received or not.

Expenses are accounted for in the period they are incurred and not in the period they are paid.

3. Installment method – method considered

appropriate when collections of the proceeds of sales and incomes extend over relatively long periods of time and there is strong possibility that full collection will not be made.

4. Percentage of completion method –

applicable in the case of a building, installation, or construction of contract covering a period in excess of one year, whereby gross income derived from such contract may be reported upon the basis of percentage of completion.

5. Crop year basis – applicable only for farmers

engaged in the production of crops which take more than a year from the time of planting to the process of gathering and disposal of the harvest.

Expenses paid or incurred are deductible in the

year the gross income from the sale of the crops is realized.

Consolidated mines v. CTA The Company was not using a "hybrid" method of accounting in the preparation of its income tax returns, but was consistent in its use of the accrual method of accounting. We have to distinguish between: (1) the method of accounting used by the Company in determining its net income for tax purposes; (2) the method of computation agreed upon between the Company and Benguet in determining the amount of compensation that was to be paid by the former to the latter.

Required for changing of accounting period

1. Designating the proposed date for the closing of its new taxable year,

2. With a statement of the date on which the books of account were opened and closed each year for the past 3 years,

3. The date on which the taxable year began and ended as shown on the returns filed for the past 3 years, and

4. The reasons why the change in accounting period is desired.

Yutivo v. CIR money of the articles sold, batertered,

exchanged, transferred x x x is the total amount of money or its equivalent which the purchaser pays to the vendor to receive or get

Tax 1– Laforteza Camille Umali | FINALS REVIEWER

14

the goods. However, if a manufacturer, producer, or importer, in fixing the gross selling price of an article sold by him has included an amount intended to cover the sales tax in the gross selling price of the articles, the sales tax shall be based on the gross selling prices less than the amount intended to cover the tax, if the same is billed to the purchaser as a separate item

Perez v. CTA The networth method is based upon the general

theory that money and other assets in excess of liabilities of a taxpayer (after an accurate and proper adjustment of non-deductible items) not accounted for by his income tax returns, leads to the inference that part of his income has not been reported.

BB. Returns and Payment

Individual Corporate

Who are required 1) Resident citizen 2) Non-resident citizen 3) Resident alien 4) Non-resident citizen ETB

1) Domestic 2) Resident foreign

Not required 1) Gross income < exemption 2) One employer, already withheld 3) Income solely of royalties, interests etc.

(already subject of final tax) 4) Employed by RAH/ROH 5) Employed by contractor engaged in

petroleum operation 6) Minimum wage earner

1) Nonresident foreign corporation

Where to file 1) Accredited Agent Bank 2) Revenue District Officer, Revenue

Collection Officer 3) duly authorized treasurer of city or

municipality a. Legal residence b. Office of CIR c. Place of work or employment d. Philippine embassy or nearest

consulate or mailed directly to CIR

1) Accredited Agent Bank 2) Revenue District Officer, Revenue

Collection Officer 3) duly authorized treasurer of city

or municipality having jurisdiction over the principal office of the corporation

When to file GR On or before April 15 E extension granted by CIR

GR 60 days following the close of each of the first 3 quarters of the taxable year Final adjustment April 15 or 15th day of the 4th month following the close of the fiscal year

Where/When to pay

Place/time return is filed Place/time return is filed

Capital gain 1) Within 30 days after transaction 2) April 15

1) Within 30 days after transaction 2) Before the 15th day of the 4th

month following the close of the taxable year

Quarterly 1) Receiving self-employment income 2) Engaged in T/B/P

April, August, November 15

GR 60 days following the close of each of the first 3 quarters of the taxable year Final adjustment April 15 or 15th day of the 4th month following the close of the fiscal year

Tax 1– Laforteza Camille Umali | FINALS REVIEWER

15

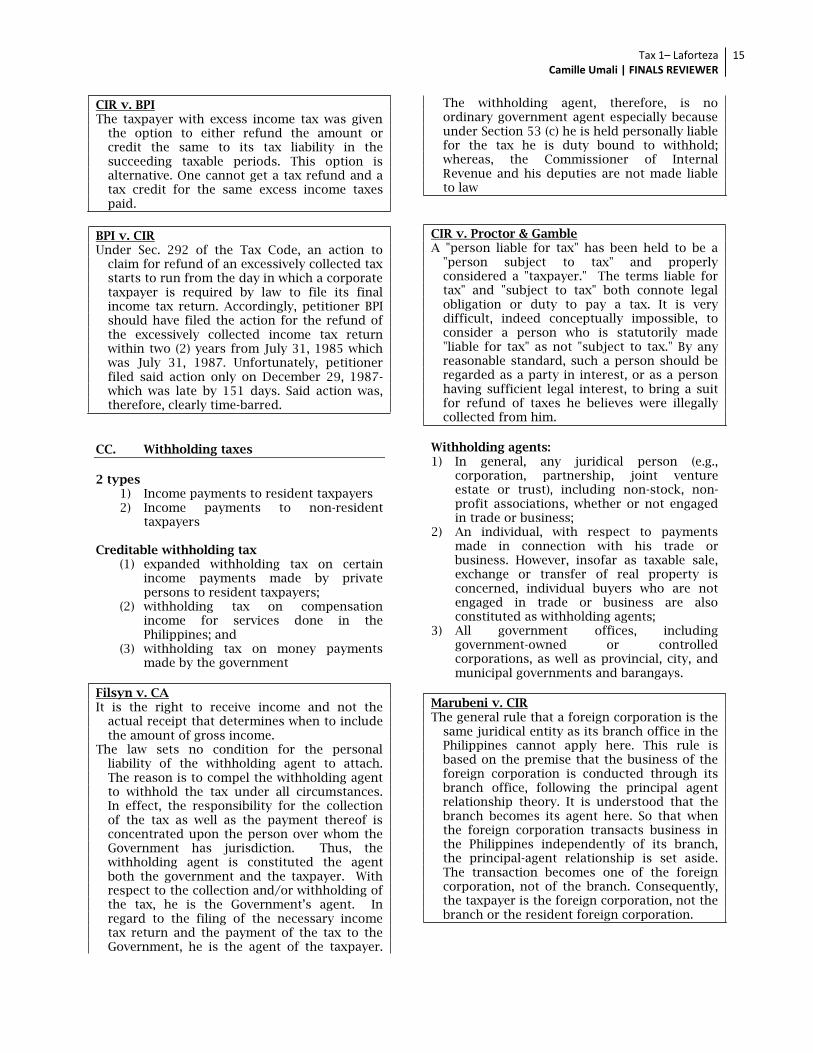

CIR v. BPI The taxpayer with excess income tax was given

the option to either refund the amount or credit the same to its tax liability in the succeeding taxable periods. This option is alternative. One cannot get a tax refund and a tax credit for the same excess income taxes paid.

BPI v. CIR Under Sec. 292 of the Tax Code, an action to

claim for refund of an excessively collected tax starts to run from the day in which a corporate taxpayer is required by law to file its final income tax return. Accordingly, petitioner BPI should have filed the action for the refund of the excessively collected income tax return within two (2) years from July 31, 1985 which was July 31, 1987. Unfortunately, petitioner filed said action only on December 29, 1987-which was late by 151 days. Said action was, therefore, clearly time-barred.

CC. Withholding taxes

2 types

1) Income payments to resident taxpayers 2) Income payments to non-resident

taxpayers Creditable withholding tax

(1) expanded withholding tax on certain income payments made by private persons to resident taxpayers;

(2) withholding tax on compensation income for services done in the Philippines; and

(3) withholding tax on money payments made by the government

Filsyn v. CA It is the right to receive income and not the

actual receipt that determines when to include the amount of gross income.

The law sets no condition for the personal liability of the withholding agent to attach. The reason is to compel the withholding agent to withhold the tax under all circumstances. In effect, the responsibility for the collection of the tax as well as the payment thereof is concentrated upon the person over whom the Government has jurisdiction. Thus, the withholding agent is constituted the agent both the government and the taxpayer. With respect to the collection and/or withholding of the tax, he is the Government‘s agent. In regard to the filing of the necessary income tax return and the payment of the tax to the Government, he is the agent of the taxpayer.

The withholding agent, therefore, is no ordinary government agent especially because under Section 53 (c) he is held personally liable for the tax he is duty bound to withhold; whereas, the Commissioner of Internal Revenue and his deputies are not made liable to law

CIR v. Proctor & Gamble A "person liable for tax" has been held to be a

"person subject to tax" and properly considered a "taxpayer." The terms liable for tax" and "subject to tax" both connote legal obligation or duty to pay a tax. It is very difficult, indeed conceptually impossible, to consider a person who is statutorily made "liable for tax" as not "subject to tax." By any reasonable standard, such a person should be regarded as a party in interest, or as a person having sufficient legal interest, to bring a suit for refund of taxes he believes were illegally collected from him.

Withholding agents: 1) In general, any juridical person (e.g.,

corporation, partnership, joint venture estate or trust), including non-stock, non-profit associations, whether or not engaged in trade or business;

2) An individual, with respect to payments made in connection with his trade or business. However, insofar as taxable sale, exchange or transfer of real property is concerned, individual buyers who are not engaged in trade or business are also constituted as withholding agents;

3) All government offices, including government-owned or controlled corporations, as well as provincial, city, and municipal governments and barangays.

Marubeni v. CIR The general rule that a foreign corporation is the

same juridical entity as its branch office in the Philippines cannot apply here. This rule is based on the premise that the business of the foreign corporation is conducted through its branch office, following the principal agent relationship theory. It is understood that the branch becomes its agent here. So that when the foreign corporation transacts business in the Philippines independently of its branch, the principal-agent relationship is set aside. The transaction becomes one of the foreign corporation, not of the branch. Consequently, the taxpayer is the foreign corporation, not the branch or the resident foreign corporation.

Tax 1– Laforteza Camille Umali | FINALS REVIEWER

16

CIR v. Johnson and Son, Inc. In the case at bar, the state of source is the

Philippines because the royalties are paid for the right to use property or rights, i.e. trademarks, patents and technology, located within the Philippines. The United States is the state of residence since the taxpayer, S. C. Johnson and Son, U. S. A., is based there. Under the RP-US Tax Treaty, the state of residence and the state of source are both permitted to tax the royalties, with a restraint on the tax that may be collected by the state of source. Furthermore, the method employed to give relief from double taxation is the allowance of a tax credit to citizens or residents of the United States (in an appropriate amount based upon the taxes paid or accrued to the Philippines) against the United States tax, but such amount shall not exceed the limitations provided by United States law for the taxable year.

Golden Arches v. CIR It must be emphasized that the RP-US, RP-Russia,

RP-Denmark, RP-Sweden and RP-China Tax Treaties are just a few of the bilateral agreements which the Philippines has entered into, for the purpose of avoiding, if not eliminating, double taxation and its effects on the national fiscal legislations of the contracting parties. Double taxation usually takes place when a person is a resident of a contracting state and derives income from, or owns capital in, the other contracting state and both states impose tax on that income or capital. More precisely, the tax conventions are drafted with a view towards the elimination of international juridical double taxation.

In this instant case, both the Philippines, as the state of source, and the United States, as the state of residence, are permitted to tax the royalties paid by the petitioner for the adoption and right to use McDonald's food and beverages which have been designated by it, the trade names, trademarks and service marks which it shall designate, from time to time, to be part of the McDonald's system. To allow both countries to tax the royalty payments is a clear case of double taxation, thus, the applicability of the provisions of the tax treaties.

Final withholding tax

Creditable Withholding tax

Liability for payment rests primarily on the payor as withholding agent. (liable for deficiency tax)

Withheld with intention to equal or at least approximate the tax due of the payee on said income.

Payee is not required to file an income tax

Payee is still required to file his ITR

Finality is limited only to the payee‘s income tax on the particular income

Interest income, Dividends, other subject to final tax

Expanded withholding tax from compensation income.

Withholding tax on compensation income GR all salaries E

1) Insurance agents 2) Service to foreign government 3) Casual labor not in the course of

employer‘s T/B 4) Private service by maids, cooks, etc. 5) Agricultural labor

When Time income is paid or payable, whichever is sooner Where AAB, RDO, Collection officer or duly authorized Treasurer of city or municipality Exempted from withholding: 1) Minimum wage earners 2) Government employees (salary grade 1 to 3) 3) National government and instrumentalities 4) Exempted from tax by law