tata group: game of thrones - iias: india's leading...

TRANSCRIPT

Institutional EYE IiAS Comment | 7 November 2016

1 iias.in November 2016

Related Research Turbulence at Tata Sons: What stakeholders are asking; October 2016

Subscribe to IiAS Research Write to us [email protected]

Disclosure: The Tata group, through Tata Investment Corporation Limited, holds equity in IiAS. This Institutional EYE is based entirely on publicly available information.

Focus

First Reaction

Governance Spotlight

Regulatory Overview

Thematic Research

Event Based Research

General

Tata Group: Game of Thrones

Cyrus Mistry’s position as Chairperson of listed companies of the Tata group is now being questioned. Whatever be Tata Sons’ opinion in this matter, IiAS believes independent directors of the listed companies must provide comprehensive guidance to shareholders on whether Cyrus Mistry should remain Chairperson. And, if boards of listed Tata group companies are divided in their of support Cyrus Mistry, there is a risk of boards becoming dysfunctional which has operational implications for the companies. Cyrus Mistry’s ouster in Tata Sons as Chairperson and Executive Director has raised several questions. For investors in the seven major listed companies, the immediate question is whether he will remain Chairperson1 and its consequences. The Tata Sons (Tata Sons or Tata group or group) has stated that Cyrus Mistry was removed because of a ‘growing trust deficit’, and because of ‘repeated departures from the culture and ethos of the Tata group’. Having said this, the group has left itself with no option but to push for his removal from the boards of group companies. Box 1: Shareholders can requisition a meeting under section 100 of the Companies Act 2013

(1) The Board may, whenever it deems fit, call an extraordinary general meeting of the company. (2) The Board shall, at the requisition made by -

(a) in the case of a company having a share capital, such number of members who hold, on the date of the receipt of the requisition, not less than one-tenth of such of the paid-up share capital of the company as on that date carries the right of voting; (b) in the case of a company not having a share capital, such number of members who have, on the date of receipt of the requisition, not less than one-tenth of the total voting power of all the members having on the said date a right to vote,

To pass a resolution supporting the removal of Cyrus Mistry as director with a 51% majority, the Tata group will need shareholders support – it owns about 30% - 35% of equity in the listed companies of the group, other than in Tata Consultancy Services (See Annexure A). Independent Directors of the listed companies need to provide guidance As a dominant shareholder with over 30% holding in each of the companies, the Tata group can call an extraordinary general meeting (See Box 1 and Annexure B) and present a resolution to remove Cyrus Mistry as a director. But, for the resolution to pass, it needs the support of at least 51% of shareholder votes i.e those present and voting. When and if, a proposal is put to shareholders to vote, IiAS believes the independent directors of the listed companies need to provide shareholders with guidance on how they should vote on a resolution to remove Cyrus Mistry as Chairperson – independent of whether the company or Tata Sons presents the resolution. To that extent, Indian Hotels Company Limited’s (IHCL) Independent

1 A Chairperson is appointed and removed by the board members. A director is appointed and removed by shareholders.

Tata Group: Game of Thrones

2 iias.in November 2016

Institutional

EYE

Directors’ public stand on the Cyrus Mistry’s position in IHCL is a step in the right direction. The Independent Directors, in forming an opinion, will likely consider Cyrus Mistry’s performance during his tenure, and whether his strategy for the company is the best possible strategy given where the company is. They will also likely consider the issues raised by Tata Sons directors, and then make a balanced decision. IHCL’s Independent Directors, in reposing full confidence in Cyrus Mistry, will no doubt have done this - and more. The reasoning behind Tata Sons’ decision to remove Cyrus Mistry as Chairperson and Executive Directors is yet unknown publicly2: Tata Sons’ board is asking investors to blindly trust them. IHCL’s Independent Directors – who individually command the same public stature as that of Tata Sons’, and one of whom is on the board of two Tata Trusts (Annexure C) – have reposed their confidence in Cyrus Mistry. Stakeholders are baffled by this discord, not knowing which side to believe – the independent directors of listed Tata company boards, or Tata Sons. The conflict will have operational implications even as Boards risk becoming dysfunctional The boards of listed companies risk becoming dysfunctional, if independent directors and the Tata Sons nominees hold divergent views on their support to Cyrus Mistry, or even if Independent Directors differ within themselves on this debate. This will have consequences. Tata group companies’ ease of access to finance and the cost of finance tend to be favourable – driven by the implicit understanding that these belong to the Tata group, and that credit support from group companies will always be available, whether explicitly provided or not. But, there is now, a real possibility that boards of listed companies may choose to ignore Tata Sons. This is likely to make lenders nervous, and they may show restraint in extending any further credit, until there is clarity regarding the evolving relationship between Tata Sons and the operating businesses. This will have operational implications for listed companies – on 31 March 2016, the Tata group of companies3 had outstanding debt aggregating around Rs.2.5 trillion, of which about 24% is due within twelve months4. Consequently, it has implications for India’s banking system. Tata Sons diminishing control The relationship between the operating companies and the group is symbiotic. The group no doubt defines these operating entities – but the companies also defines the Tata group. If shareholders do not support the resolution, Cyrus Mistry will continue as Chairperson on the seven listed companies’ boards. If so, Tata Sons’ control over the listed companies may diminish and the question will be: are these then Tata companies? At the extreme, this may create an alternate power structure raising fear of a throwback to when Ratan Tata took control after battling satraps including Russi Modi, Ajit Kerkar, and Darbari Seth.

2 Publicly, just Cyrus Mistry’s version of the issue (from Cyrus Mistry’s email to the members of the Tata Sons’ board, that leaked) is available. Tata Sons’ public statement on his removal is vague, at best. 3 Listed companies only 4 Short term debt and current portion of long term debt, most of which will likely need to be rolled over

Tata Group: Game of Thrones

3 iias.in November 2016

Institutional

EYE

Investors can take comfort that the listed companies are of reasonable size and have the ability and the talent to chart their own course. Much like several other Tata Group companies, these seven companies do not need Tata Sons control at the Chairperson level. Others will view the whole as being greater than the sum of its parts. It is in this context that there is value in having the Chairperson of Tata Sons as the Chairperson of the listed company is more than just board control – it signals the importance of that company in the pecking order of the Tata group, and the immediacy and level of support that it can garner from group. Equally, important it gestures the adherence to a set of values. Will Tata Sons’ continued silence cause it to be unseated? While one may argue that it is the responsibility of independent directors to understand the basis of Tata Sons’ decision, it is equally important for Tata Sons to communicate to its companies’ boards the rationale to dethrone Cyrus Mistry. Tata Sons can begin by sharing the details of the board evaluation, and the process it followed to conclude that Cyrus Mistry must be unseated. Tata Sons’ silence has not only led to excessive speculation, but is possibly haemorrhaging the current chain of command within the group. With public perception veering towards Cyrus Mistry, the Tata group needs to provide factual and cohesive information supporting its decision to balance the discourse. Else it must back down. A century-old reign risks being unhinged on one decision The Tata group has held a totemic position in corporate India for over a century. But this one action – of unseating Cyrus Mistry – is allowing stakeholders to doubt the Tatas. What seems to be most unsettling is the abruptness of the decision and the limited communication that has followed. Given that all facts are not available, IiAS believes it is impossible to decide whether the Tata group made the right decision or not.Yet, in its silence, the group is testing the limits of stakeholders’ faith in the brand. While skeptics will doubt and believers will believe, the group has hinged its public equity on this decision. Purging the opacity of Tata group’s governance structure and chain of command The current uncertainty is, no doubt, troubling for all stakeholders While investors have had a broad understanding of the working dynamics, there was no need to establish clarity since the group was operating under an accepted status-quo. IiAS believes that the end of this boardroom war will bring clarity to markets on the terms of engagement between the three power structures - Tata Trusts, Tata Sons, and the listed Tata group companies. This will also determine how succession planning will happen in the three entities. And it will answer who sits on the Iron Throne.

Tata Group: Game of Thrones

4 iias.in November 2016

Institutional

EYE

Annexure A: Board composition and shareholding pattern of Tata companies in which Cyrus Mistry is on a board member

Table 1: The board of Tata Sons Limited Executive Directors Non-Executive Non-Independent

Directors Independent Directors

Ishaat Hussain Ratan Tata Cyrus Mistry Vijay Singh Nitin Nohria Amit Chandra Ralf Speth N Chandrasekharan Venu Srinivasan

Ronen Sen Ajay Piramal Farida Khambata

Table 2: The board of Tata Consultancy Services Limited

Executive Directors Non-Executive Non-Independent Directors

Independent Directors

N. Chandrasekaran Ms. Aarthi Subramanian

Cyrus Mistry Ishaat Hussain

Vijay Kelkar Ron Sommer O.P. Bhatt Aman Mehta ** V. Thyagarajan ** Prof. C. M. Christensen **

Table 3: The board of Tata Steel Limited

Executive Directors Non-Executive Non-Independent Directors

Independent Directors

TV Narendran Koushik Chatterjee

Cyrus Mistry Ishaat Hussain DK Mehrotra

Jacobus Schraven Andrew Robb Ms. Mallika Srinivasan O P Bhatt Subodh Bhargava ** Nusli N. Wadia **

Table 4: The board of Tata Motors Limited

Executive Directors Non-Executive Non-Independent Directors

Independent Directors

Guenter Butschek Satish Borwankar Ravi Pisharody

Cyrus Mistry Ralf Speth

Raghunath Mashelkar Nasser Munjee Subodh Bhargava Vineshkumar Jairath Ms. Falguni Nayar Nusli N. Wadia **

Tata Group: Game of Thrones

5 iias.in November 2016

Institutional

EYE

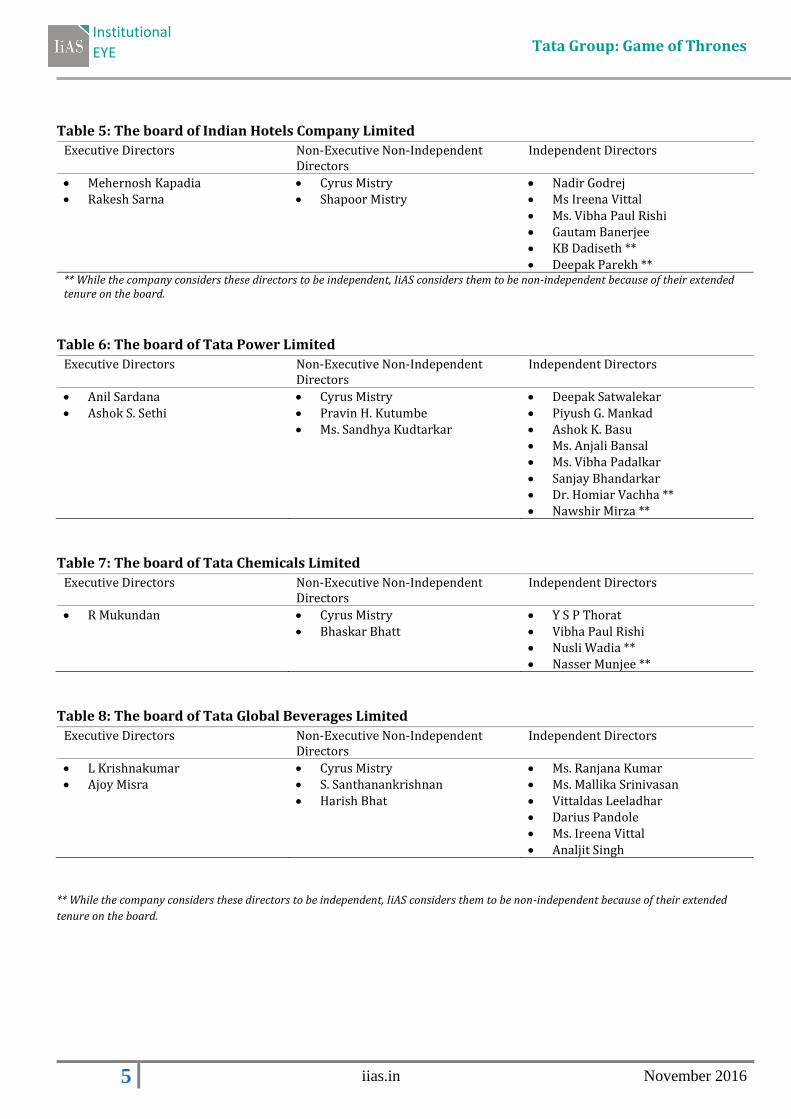

Table 5: The board of Indian Hotels Company Limited

Executive Directors Non-Executive Non-Independent Directors

Independent Directors

Mehernosh Kapadia Rakesh Sarna

Cyrus Mistry Shapoor Mistry

Nadir Godrej Ms Ireena Vittal Ms. Vibha Paul Rishi Gautam Banerjee KB Dadiseth ** Deepak Parekh **

** While the company considers these directors to be independent, IiAS considers them to be non-independent because of their extended tenure on the board.

Table 6: The board of Tata Power Limited

Executive Directors Non-Executive Non-Independent Directors

Independent Directors

Anil Sardana Ashok S. Sethi

Cyrus Mistry Pravin H. Kutumbe Ms. Sandhya Kudtarkar

Deepak Satwalekar Piyush G. Mankad Ashok K. Basu Ms. Anjali Bansal Ms. Vibha Padalkar Sanjay Bhandarkar Dr. Homiar Vachha ** Nawshir Mirza **

Table 7: The board of Tata Chemicals Limited

Executive Directors Non-Executive Non-Independent Directors

Independent Directors

R Mukundan Cyrus Mistry Bhaskar Bhatt

Y S P Thorat Vibha Paul Rishi Nusli Wadia ** Nasser Munjee **

Table 8: The board of Tata Global Beverages Limited

Executive Directors Non-Executive Non-Independent Directors

Independent Directors

L Krishnakumar Ajoy Misra

Cyrus Mistry S. Santhanankrishnan Harish Bhat

Ms. Ranjana Kumar Ms. Mallika Srinivasan Vittaldas Leeladhar Darius Pandole Ms. Ireena Vittal Analjit Singh

** While the company considers these directors to be independent, IiAS considers them to be non-independent because of their extended

tenure on the board.

Tata Group: Game of Thrones Institutional EYE IiAS Comment | 7 November 2016

6 iias.in November 2016

Institutional

EYE

Table 9: Shareholding pattern (voting rights) on 30-Sep-2016 of the listed Tata companies in which Cyrus Mistry is Chairperson

Investor / Investor group

(Shareholding is in %)

Tata Consultancy

Services Limited

Tata Steel

Limited

Tata Motors Limited

Indian Hotels

Company Limited

Tata Power

Limited

Tata Chemicals

Limited

Tata Global

Beverages Limited

Sh

are

ho

ldin

g

pa

tte

rn o

f li

ste

d

com

pa

nie

s

Tata group 73.3 32.0 32.4 38.7 33.0 30.8 35.7 Foreign portfolio investors 17.0 13.1 26.7 - 26.0 19.3 15.5 LIC 3.2 13.9 5.1 8.8 13.1 3.3 10.2 Institutions (others) 2.0 16.1 9.6 30.1 11.6 25.4 8.9 Bodies corporate 0.3 2.8 0.4 7.6 0.6 - - ADR / GDR / Other DRs (by voting rights) - - 18.4 - 0.2 - - Others - public 4.2 22.2 7.5 14.9 15.5 21.1 29.7 Total shareholding 100.0 100.0 100.0 100.0 100.0 100.0 100.0

Key

sh

are

ho

ldin

gs –

ho

ldin

g m

ore

th

an

1%

equ

ity

LIC 3.2 13.9 5.1 8.8 13.1 3.3 10.2 GIC - - - 1.6 2.5 1.5 - National Insurance Company - - - - - - 1.1 New India Assurance - 1.2 - 1.5 2.5 1.3 - Reliance Capital Mutual Fund - 2.2 - 5.5 - - - HDFC Mutual Fund - 4.8 - 1.4 - - - Franklin Templeton Investment Funds - - - 1.9 - 3.8 - Abu Dhabi Investment Authority - - 1.4 - - - - Government of Singapore - - 1.7 - - - - ICICI PruLife Insurance - - 1.5 2.5 - 4.9 - Government Pension Fund Global - - - 2.8 - 3.0 1.5 SBI Magnum - - - - 1.1 - - First State Investments - - - - 3.4 - 1.8 Matthews Pacific Tiger Fund - - - - 6.1 - - ICICI Prudential Mutual Fund - - - - - 4.9 - UTI - - - - - 1.8 - Birla Sun Life - - - - - 2.1 - Platinum International Brand Fund - - - - - - 1.1 Dimensional Emerging Markets Value Fund - - - - - - 1.1

Notes:

1. Tata Motors shareholding pattern has been adjusted for voting rights of the DVR shares.

2. Tata Steel’s Depository Receipts do not carry voting rights. The shareholding pattern in the above table follows voting rights.

3. Institutions (Others) includes holding by state and central government bodies

Tata Group: Game of Thrones

7 iias.in November 2016

Institutional

EYE

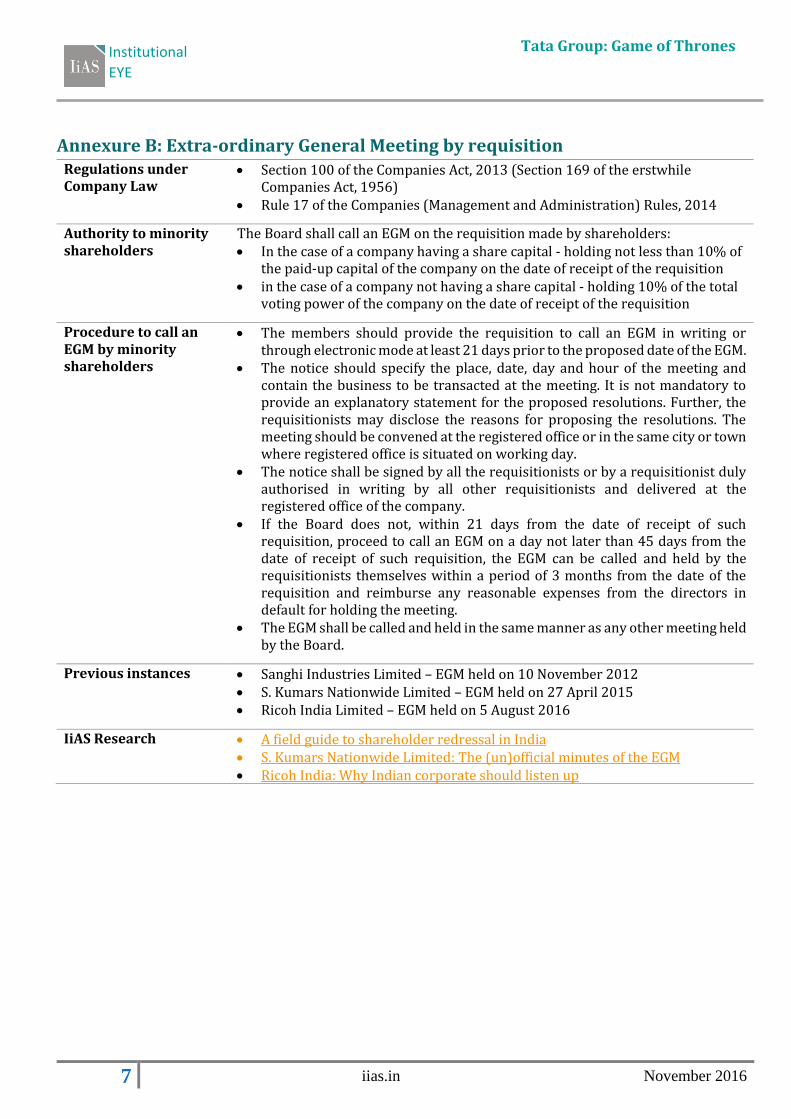

Annexure B: Extra-ordinary General Meeting by requisition Regulations under Company Law

Section 100 of the Companies Act, 2013 (Section 169 of the erstwhile Companies Act, 1956)

Rule 17 of the Companies (Management and Administration) Rules, 2014

Authority to minority shareholders

The Board shall call an EGM on the requisition made by shareholders: In the case of a company having a share capital - holding not less than 10% of

the paid-up capital of the company on the date of receipt of the requisition in the case of a company not having a share capital - holding 10% of the total

voting power of the company on the date of receipt of the requisition

Procedure to call an EGM by minority shareholders

The members should provide the requisition to call an EGM in writing or through electronic mode at least 21 days prior to the proposed date of the EGM.

The notice should specify the place, date, day and hour of the meeting and contain the business to be transacted at the meeting. It is not mandatory to provide an explanatory statement for the proposed resolutions. Further, the requisitionists may disclose the reasons for proposing the resolutions. The meeting should be convened at the registered office or in the same city or town where registered office is situated on working day.

The notice shall be signed by all the requisitionists or by a requisitionist duly authorised in writing by all other requisitionists and delivered at the registered office of the company.

If the Board does not, within 21 days from the date of receipt of such requisition, proceed to call an EGM on a day not later than 45 days from the date of receipt of such requisition, the EGM can be called and held by the requisitionists themselves within a period of 3 months from the date of the requisition and reimburse any reasonable expenses from the directors in default for holding the meeting.

The EGM shall be called and held in the same manner as any other meeting held by the Board.

Previous instances Sanghi Industries Limited – EGM held on 10 November 2012 S. Kumars Nationwide Limited – EGM held on 27 April 2015 Ricoh India Limited – EGM held on 5 August 2016

IiAS Research A field guide to shareholder redressal in India S. Kumars Nationwide Limited: The (un)official minutes of the EGM Ricoh India: Why Indian corporate should listen up

Tata Group: Game of Thrones

8 iias.in November 2016

Institutional

EYE

Annexure C: Board of Trustees of the Tata Trusts

Mr. Ratan Tata is the Chairperson of all the Tata Trusts listed below.

Sir Ratan Tata Trust and allied trusts Sir Dorabji Tata Trust and allied trusts Sir Ratan Tata Trust

Tata Education and Development Trust

Navajbai Ratan Tata Trust

Bai Hirabai J N Tata Navsari Charitable Institution

Sarvajanik Seva Trust

Sir Dorabji Tata Trust

Lady Tata Memorial Trust

JRD Tata Trust

Jamsetji Tata Trust

Tata Social Welfare Trust

J N Tata Endowment Trust

Tata Education Trust

R D Tata Trust

The JRD and Thelma J Tata Trust

R Venkataramanan

N A Soonawala

J N Tata

K B Dadiseth

R K Krishna Kumar

S K Bharucha

N M Munjee

Amit Chandra

J N Mistry

Dr. Amrita Patel

V R Mehta

Venu Srinivasan

F K Kavarana

Dr. P B Desai

S N Batliwala

Dr. M Chandy

Prof S M Chitre

Dr. Suma Chitnis

Dr. Armaity Desai

F N Petit

Source: www.tatatrusts.org

Tata Group: Game of Thrones

9 iias.in November 2016

Institutional

EYE

Disclaimer This document has been prepared by Institutional Investor Advisory Services India Limited (IiAS). The information contained herein is solely from publicly available data, but we do not represent that it is accurate or complete and it should not be relied on as such. IiAS shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report. This document is provided for assistance only and is not intended to be and must not be taken as the basis for any voting or investment decision. The user assumes the entire risk of any use made of this information. Each recipient of this document should make such investigation as it deems necessary to arrive at an independent evaluation of the individual resolutions referred to in this document (including the merits and risks involved). The discussions or views expressed may not be suitable for all investors. The information given in this document is as of the date of this report and there can be no assurance that future results or events will be consistent with this information. This information is subject to change without any prior notice. IiAS reserves the right to make modifications and alterations to this statement as may be required from time to time. However, IiAS is under no obligation to update or keep the information current. Nevertheless, IiAS is committed to providing independent and transparent recommendation to its client and would be happy to provide any information in response to specific client queries. Neither IiAS nor any of its affiliates, group companies, directors, employees, agents or representatives shall be liable for any damages whether direct, indirect, special or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information. The disclosures of interest statements incorporated in this document are provided solely to enhance the transparency and should not be treated as endorsement of the views expressed in the report.

Confidentiality This information is strictly confidential and is being furnished to you solely for your information. This information should not be reproduced or redistributed or passed on directly or indirectly in any form to any other person or published, copied, in whole or in part, for any purpose. This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject IiAS to any registration or licensing requirements within such jurisdiction. The distribution of this document in certain jurisdictions may be restricted by law, and persons in whose possession this document comes, should inform themselves about and observe, any such restrictions. The information provided in these reports remains, unless otherwise stated, the copyright of IiAS. All layout, design, original artwork, concepts and other Intellectual Properties, remains the property and copyright of IiAS and may not be used in any form or for any purpose whatsoever by any party without the express written permission of the copyright holders.

IiAS Voting Policy IiAS' voting recommendations are based on a set of guiding principles, which incorporate the basic tenets of the legal framework along with the best practices followed by some of the better governed companies. These policies clearly list out the rationale and evaluation parameters which are taken into consideration while finalizing the recommendations. The detailed IiAS Voting Guidelines are available at www.iias.in/IiAS-voting-guidelines.aspx. The draft report prepared by the analyst is referred to an internal Review and Oversight Committee (ROC), which is responsible for ensuring consistency in voting recommendations, alignment of recommendations to the IiAS’ voting criteria and setting and maintaining quality standards of IiAS’ proxy reports. Details regarding the functioning and composition of the ROC committee are available at www.iias.in. In undertaking its activities, IiAS relies on information available in the public domain i.e. information that is available to public shareholders. However, in order to provide a more meaningful analysis, IiAS, generally seeks clarifications from the subject company. IiAS reserves the right to share the information provided by the subject company in its reports. Further details on IiAS policy on communication with subject companies are available at www.iias.in.

Analyst Certification The research analyst(s) for this report certify/ies that no part of his/her/their compensation was, is or will be, directly or indirectly related to specific recommendations or views expressed in this report. IiAS’ internal policies and control procedures governing the dealing and trading in securities by employees are available at www.iias.in.

Conflict Management IiAS and its research analysts may hold a nominal number of shares in companies IiAS covers (including the subject company), as on the date of this report. A list of IiAS’ shareholding in companies is available at www.iias.in.

However, IiAS, the research analyst(s) responsible for this report, and their associates or relatives, do not have actual/beneficial ownership of one per cent or more securities of the subject company, at the end of the month immediately preceding the date of publication of this report. A list of shareholders of IiAS as of the date of this report is available at www.iias.in. However, the preparation of this report is monitored by an internal Review and Oversight Committee (ROC) of IiAS and is not subject to the control of any company to which such report may relate and which may be a shareholder of IiAS.

Tata Group: Game of Thrones

10 iias.in November 2016

Institutional

EYE

Other Disclosures IiAS further confirms that, save as otherwise set out above or disclosed on IiAS’ website (www.iias.in):

IiAS, the research analyst(s) responsible for this report, and their associates or relatives, do not have any financial interest in the subject company.

IiAS, the research analyst(s) responsible for this report, and their associates or relatives, do not have any other material conflict of interest at the time of publication of this report.

As a proxy advisory firm, IiAS provides subscription, databased and other related services to various Indian and international customers (which could include the subject company). IiAS generally receives between INR 10,000 and INR 25,00,000 for such services from its customers. Other than compensation that it may have received for providing such services to the subject company in the ordinary course, none of IiAS, the research analyst(s) responsible for this report, and their associates or relatives, has received any compensation from the subject company or any third party for this report.

None of IiAS, the research analyst(s) responsible for this report, and their associates or relatives, has received any compensation from the subject company or any third party in the past 12 months in connection with the provision of services of products (including investment banking or merchant banking or brokerage services or any other products and services), or managed or co-managed public offering of securities of the subject company.

The research analyst(s) responsible for this report has not served as an officer, director or employee of the subject company. None of IiAS or the research analyst(s) responsible for this report has been engaged in market making activity for the subject company.

About IiAS Institutional Investor Advisory Services India Limited (IiAS) is a proxy advisory firm, dedicated to providing participants in the Indian market with independent opinion, research and data on corporate governance issues as well as voting recommendations on shareholder resolutions for over 650 companies. IiAS provides bespoke research, valuation advisory services and assists institutions in their engagement with company managements and their boards.

In addition to voting advisory, IiAS offers two cloud based solutions - IiAS ADRIAN, and comPAYre. IiAS ADRIAN captures shareholder meetings and voting data and provides packaged data that can be used to gain insights on how investors view specific issues and gain greater predictability regarding how they might vote. comPAYre provides users access to remuneration data for executive directors across S&P BSE 500 companies over a five-year period.

Office Institutional Investor Advisory Services Ground Floor, DGP House, 88C Old Prabhadevi Road, Mumbai - 400 025 India Contact [email protected] T: +91 22 6123 5509

markets ∩ governance