tandem or solo selecting an ownership approach in … · tandem or solo: selecting an ownership...

TRANSCRIPT

Perspective Edward Tse

Tandem or SoloSelecting an OwnershipApproach in China

Originally published as:

Tandem or Solo: Selecting an Ownership Approach in China, by Edward Tse, Booz Allen Hamilton, 2006.

CONTACT INFORMATION

Edward Tse is managing partner with Booz & Company in Greater China. With twenty years of management consulting and senior corporate management experience, Dr. Tse is one of the most experienced strategy consultants in China. He was the partner-in-charge of the first authorized office in China (Shanghai) among all international strategy consulting firms in the early 1990s. He has advised hundreds of Chinese and foreign companies on their growth strategies, organizations, corporate transformation, M&As and alliances. His experience covers a wide range of industries. He also consults to public sector organizations such as the World Bank, the Asian Development Bank and the Chinese Government on issues related to policies, state-owned enterprise reform and competitiveness. He can be reached at [email protected].

Booz & Company is a leading global management consulting firm, helping the world’s top businesses, governments, and organizations. Our founder, Edwin Booz, defined the profession when he established the first management consulting firm in 1914.

Today, with more than 3,300 people in 58 offices around the world, we bring foresight and knowledge, deep functional expertise, and a practical approach to building capabilities and delivering real impact. We work closely with our clients to create and deliver essential advantage.

For our management magazine strategy+business, visit www.strategy-business.com. Visit www.booz.com/cn to learn more about Booz & Company in Greater China.

1

Tandem or Solo: Selecting an Ownership Approach in China

Due to China’s continuous economic rise, the

country is becoming an increasingly important

part of the CEO’s agenda at many multinational

companies. Not only are companies trying to

capture a share of the growing Chinese market,

but increasingly larger numbers of them are

also integrating their China operations with

their global operations—from production to

brand development to sourcing to research and

development, in whole or in combination. In order

to operate successfully in China, companies need

to address a whole series of questions related

to their strategies, organizations, operations, and

enabling technologies. In light of this situation,

we are often asked by our foreign company clients

with what form of ownership they should operate

in the China market. Should they set up a joint

venture (JV) with one or more local partners, or

should they operate in the market alone through

a wholly foreign-owned enterprise (WFOE)?

This question is critical because the ownership

approach that a company chooses to take could

have a significant impact on the success (or

failure) of its operations in China, affecting its

risks, its revenue and profit potential (and sharing

of such, in the case of a JV), and the degree of its

management control.

Many foreign companies have already entered the China market: The Chinese government reported that more than 450 of the Fortune 500 companies have

set up some kind of operations in China already. But many others are still seeking first-time entry into this rapidly developing—and increasingly globally integrated—market, and they need to determine the most appropriate ownership entry approach. The quest for this approach is part of a larger set of entry strategy questions, such as most appropriate product market approach, competitive positioning, value chain participation, human resources deployment, capital investment, and expected financial performance.

Historical ContextThe ownership models that are available to foreign companies in China, like almost everything else that pertains to foreign companies’ operations in this country, have gone through major changes in the last 15 years as China’s own economic reform has evolved. In the early 1990s, many companies entered China thinking that they would need to have a JV partner or partners. Often, their motto was, “Just get me into China with a JV—any JV.”

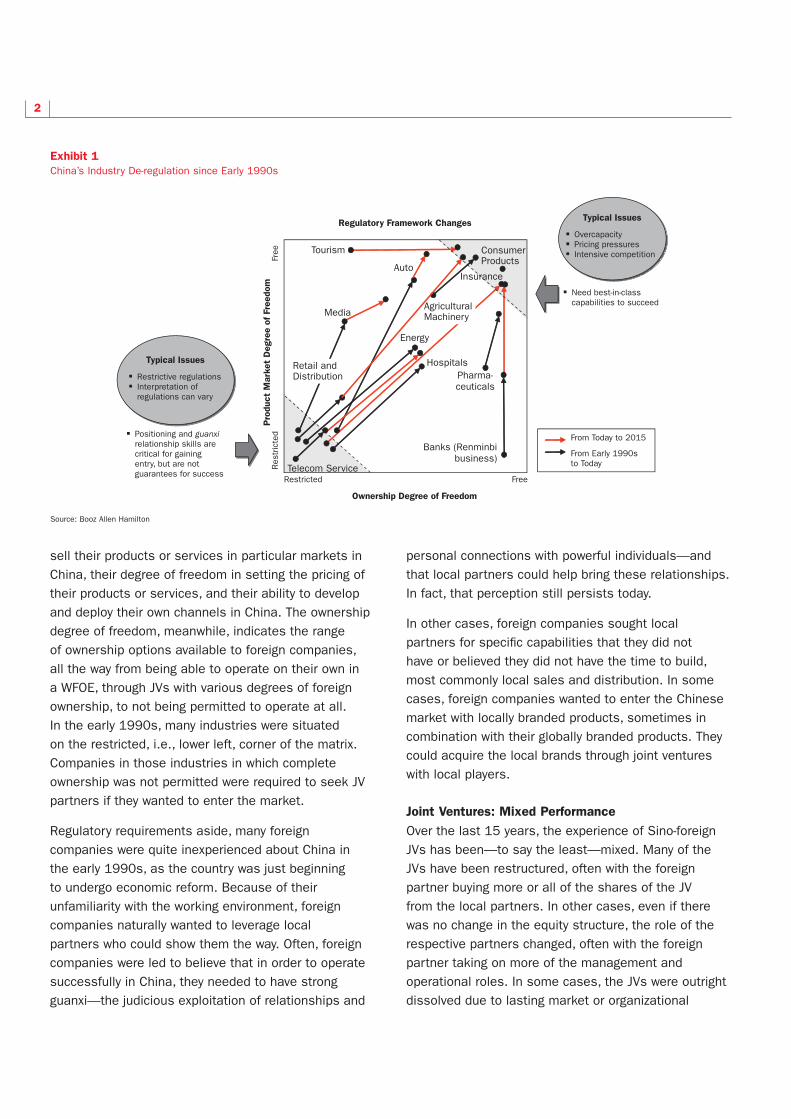

There were a number of reasons for this attitude. First and foremost, the Chinese government at that time had a relatively restrictive policy toward foreign companies’ participation in ownership of their subsidiaries. While foreign companies were allowed to operate on their own in some industries, including the majority of consumer products, in many other industries the ownership options were still restricted. Companies had varying degrees of freedom in two dimensions: product market and ownership (see Exhibit 1, page 2).

The product market degree of freedom represents the extent to which foreign companies were allowed to

2

sell their products or services in particular markets in China, their degree of freedom in setting the pricing of their products or services, and their ability to develop and deploy their own channels in China. The ownership degree of freedom, meanwhile, indicates the range of ownership options available to foreign companies, all the way from being able to operate on their own in a WFOE, through JVs with various degrees of foreign ownership, to not being permitted to operate at all. In the early 1990s, many industries were situated on the restricted, i.e., lower left, corner of the matrix. Companies in those industries in which complete ownership was not permitted were required to seek JV partners if they wanted to enter the market.

Regulatory requirements aside, many foreign companies were quite inexperienced about China in the early 1990s, as the country was just beginning to undergo economic reform. Because of their unfamiliarity with the working environment, foreign companies naturally wanted to leverage local partners who could show them the way. Often, foreign companies were led to believe that in order to operate successfully in China, they needed to have strong guanxi—the judicious exploitation of relationships and

personal connections with powerful individuals—and that local partners could help bring these relationships. In fact, that perception still persists today.

In other cases, foreign companies sought local partners for specific capabilities that they did not have or believed they did not have the time to build, most commonly local sales and distribution. In some cases, foreign companies wanted to enter the Chinese market with locally branded products, sometimes in combination with their globally branded products. They could acquire the local brands through joint ventures with local players.

Joint Ventures: Mixed Performance Over the last 15 years, the experience of Sino-foreign JVs has been—to say the least—mixed. Many of the JVs have been restructured, often with the foreign partner buying more or all of the shares of the JV from the local partners. In other cases, even if there was no change in the equity structure, the role of the respective partners changed, often with the foreign partner taking on more of the management and operational roles. In some cases, the JVs were outright dissolved due to lasting market or organizational

Exhibit 1China’s Industry De-regulation since Early 1990s

Source: Booz Allen Hamilton

From Today to 2015

FreeRestrictedTelecom Service

Free

Res

tric

ted

� Restrictive regulations� Interpretation of

regulations can vary

� Positioning and guanxi relationship skills are critical for gaining entry, but are not guarantees for success

� Need best-in-class capabilities to succeed

� Overcapacity� Pricing pressures� Intensive competition

Ownership Degree of Freedom

Typical Issues

Typical IssuesRegulatory Framework Changes

Pro

duct

Mar

ket

Deg

ree

of F

reed

om

From Early 1990s to Today

Retail and Distribution

Media

Tourism

Auto

Energy

HospitalsPharma-ceuticals

Banks (Renminbi business)

Agricultural Machinery

Consumer Products

Insurance

3

problems, or irreconcilable differences between the partners. Several common causes have led to this.

Often the original advantages that the local partners claimed to possess—or that the foreign partners perceived—did not fully materialize. For instance, while guanxi is still quite important in restricted industries in China, it has become less important than real capabilities in those industries that are deregulated. Because more and more industries have been deregulated by the Chinese government over the last 15 years, the importance of guanxi has dwindled.

Furthermore, even real sources of capabilities offered by the local partners, such as sales and distribution, were often not as relevant as originally envisioned because those capabilities were primarily developed by the Chinese partners during the planned economy era. Sales and distribution in the planned economy focused merely on physical movement of goods, with none of the value-added services that those activities need to provide in a market economy.

From the Chinese perspective, many companies entered into JVs with foreign partners hoping that they could gain information about technology, management practices, and, in some cases, the opportunity to expand overseas. A typical Chinese approach was to

use their knowledge of the market to exchange for technology from the foreign partners. But many Chinese partners felt that their foreign counterparts did not bring the best product or technology; therefore, they felt they could not really learn from the foreign partner and that the inferior product or technology could not position the JV in the most advantaged position in the marketplace—which, across many sectors, was becoming very competitive in a short time.

Finally, the biggest roadblocks in many JVs were the divergent visions and strategic intents of the Chinese and foreign partners. In many cases, foreign partners wanted to continue investing in the JV in and growing the business in China long-term, while the Chinese partners often wanted the JV to make short-term dividends.

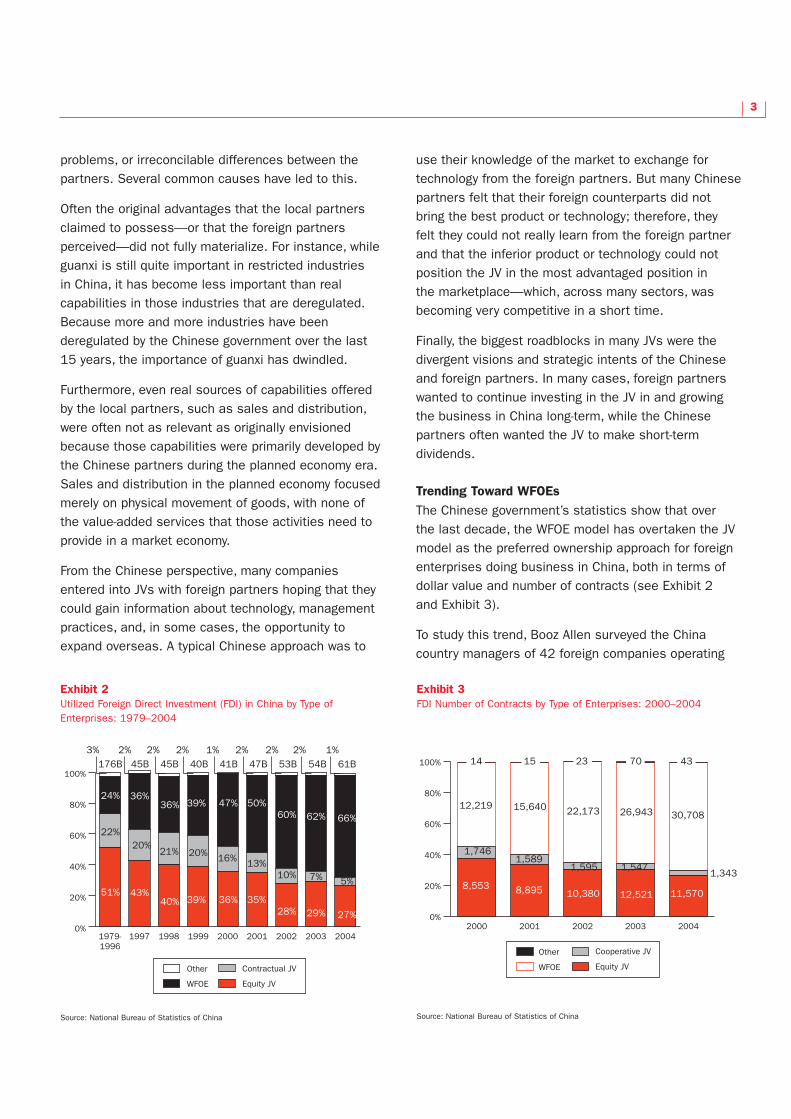

Trending Toward WFOEsThe Chinese government’s statistics show that over the last decade, the WFOE model has overtaken the JV model as the preferred ownership approach for foreign enterprises doing business in China, both in terms of dollar value and number of contracts (see Exhibit 2 and Exhibit 3).

To study this trend, Booz Allen surveyed the China country managers of 42 foreign companies operating

Exhibit 2Utilized Foreign Direct Investment (FDI) in China by Type of Enterprises: 1979–2004

Source: National Bureau of Statistics of China

0%

20%

40%

60%

80%

100%

Other

WFOE

Contractual JV

Equity JV

2004

2003

2002

2001

2000

1999

1998

1997

1979- 1996

51%

22%

3% 2% 2% 2% 2% 2% 2% 1% 1% 176B

24%

43%

20%

45B

36%

40%

21%

45B

36%

39%

20%

40B

39%

36%

16%

41B

47%

35%

13%

47B

50%

28%

10%

53B

60%

29%

7%

54B

62%

27%

5%

61B

66%

0%

20%

40%

60%

80%

100%

Other

WFOE

Cooperative JV

Equity JV

20042003200220012000

8,553 8,895 10,380 12,521 11,570

1,3431,5471,595

1,5891,746

15,640 22,173 26,943 30,70812,219

14 15 23 70 43

Exhibit 3FDI Number of Contracts by Type of Enterprises: 2000–2004

Source: National Bureau of Statistics of China

4

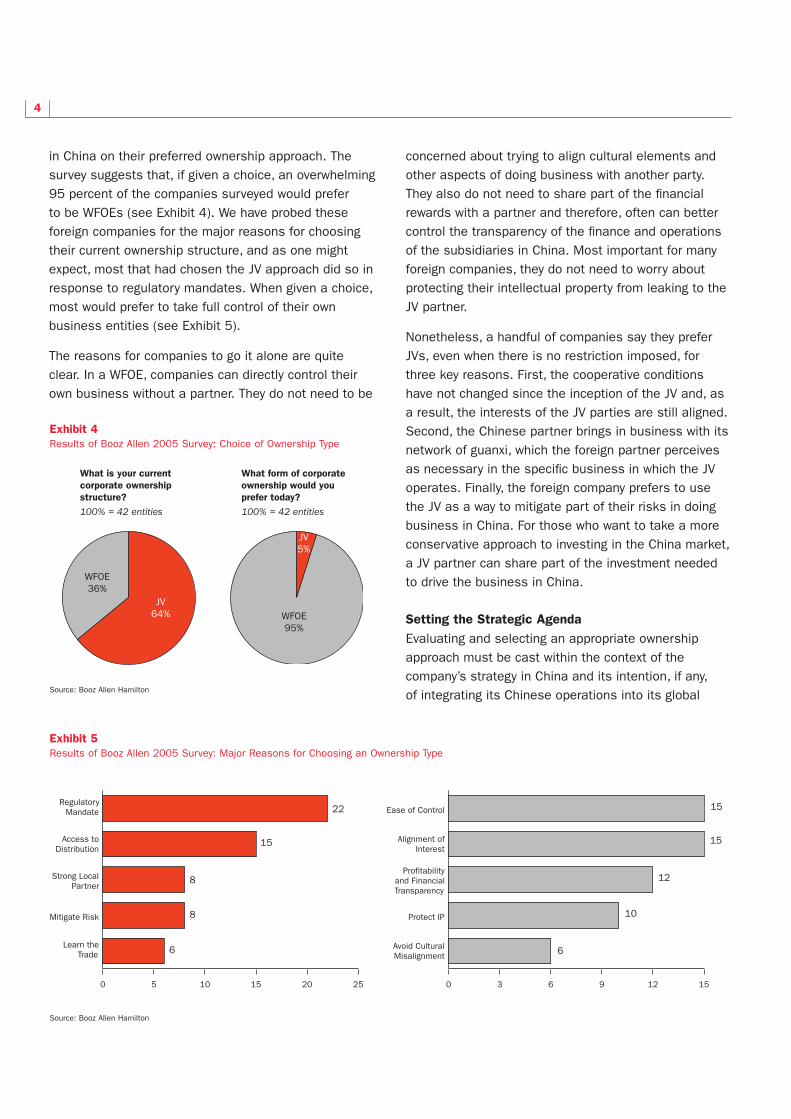

in China on their preferred ownership approach. The survey suggests that, if given a choice, an overwhelming 95 percent of the companies surveyed would prefer to be WFOEs (see Exhibit 4). We have probed these foreign companies for the major reasons for choosing their current ownership structure, and as one might expect, most that had chosen the JV approach did so in response to regulatory mandates. When given a choice, most would prefer to take full control of their own business entities (see Exhibit 5).

The reasons for companies to go it alone are quite clear. In a WFOE, companies can directly control their own business without a partner. They do not need to be

concerned about trying to align cultural elements and other aspects of doing business with another party. They also do not need to share part of the financial rewards with a partner and therefore, often can better control the transparency of the finance and operations of the subsidiaries in China. Most important for many foreign companies, they do not need to worry about protecting their intellectual property from leaking to the JV partner.

Nonetheless, a handful of companies say they prefer JVs, even when there is no restriction imposed, for three key reasons. First, the cooperative conditions have not changed since the inception of the JV and, as a result, the interests of the JV parties are still aligned. Second, the Chinese partner brings in business with its network of guanxi, which the foreign partner perceives as necessary in the specific business in which the JV operates. Finally, the foreign company prefers to use the JV as a way to mitigate part of their risks in doing business in China. For those who want to take a more conservative approach to investing in the China market, a JV partner can share part of the investment needed to drive the business in China.

Setting the Strategic Agenda Evaluating and selecting an appropriate ownership approach must be cast within the context of the company’s strategy in China and its intention, if any, of integrating its Chinese operations into its global

Exhibit 4Results of Booz Allen 2005 Survey: Choice of Ownership Type

Source: Booz Allen Hamilton

What is your current corporate ownership structure?100% = 42 entities

What form of corporate ownership would you prefer today?100% = 42 entities

JV64%

WFOE36%

WFOE95%

JV5%

Exhibit 5Results of Booz Allen 2005 Survey: Major Reasons for Choosing an Ownership Type

Source: Booz Allen Hamilton

15

15

12

10

6

22

15

8

8

6

0 5 10 15 20 25

Learn theTrade

Mitigate Risk

Strong LocalPartner

Access toDistribution

RegulatoryMandate

0 3 6 9 12 15

Avoid CulturalMisalignment

Protect IP

Profitabilityand FinancialTransparency

Alignment ofInterest

Ease of Control

5

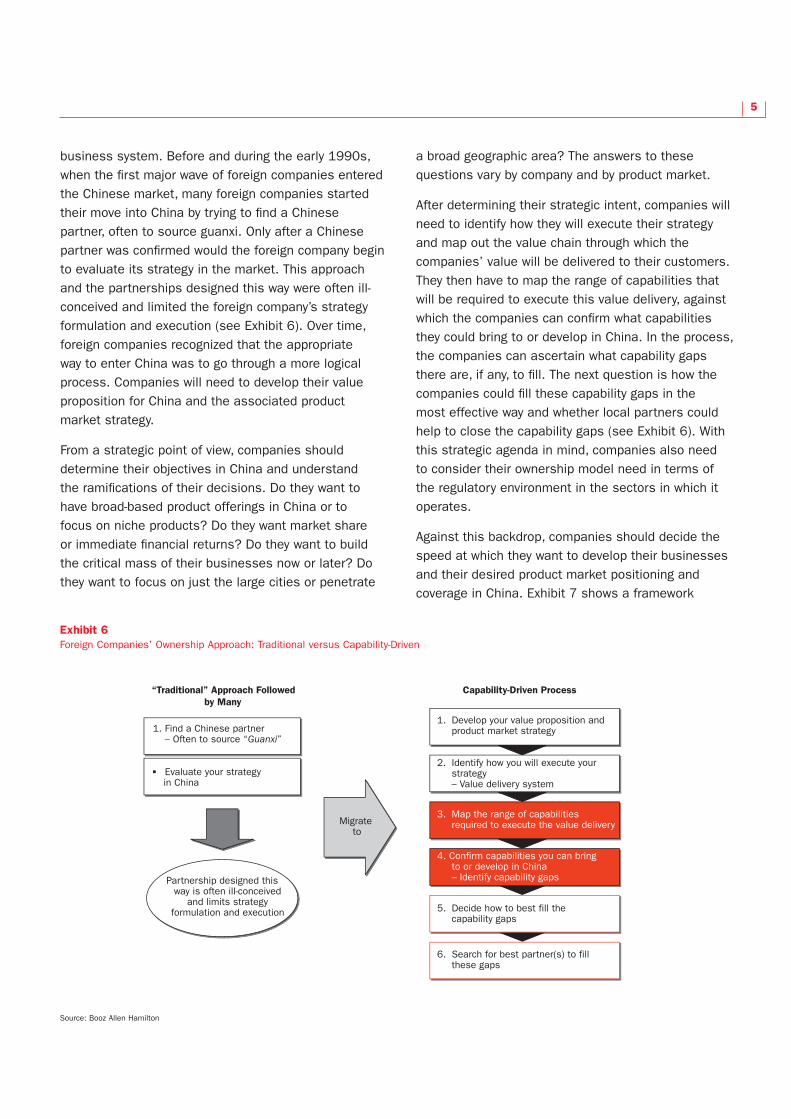

business system. Before and during the early 1990s, when the first major wave of foreign companies entered the Chinese market, many foreign companies started their move into China by trying to find a Chinese partner, often to source guanxi. Only after a Chinese partner was confirmed would the foreign company begin to evaluate its strategy in the market. This approach and the partnerships designed this way were often ill-conceived and limited the foreign company’s strategy formulation and execution (see Exhibit 6). Over time, foreign companies recognized that the appropriate way to enter China was to go through a more logical process. Companies will need to develop their value proposition for China and the associated product market strategy.

From a strategic point of view, companies should determine their objectives in China and understand the ramifications of their decisions. Do they want to have broad-based product offerings in China or to focus on niche products? Do they want market share or immediate financial returns? Do they want to build the critical mass of their businesses now or later? Do they want to focus on just the large cities or penetrate

a broad geographic area? The answers to these questions vary by company and by product market.

After determining their strategic intent, companies will need to identify how they will execute their strategy and map out the value chain through which the companies’ value will be delivered to their customers. They then have to map the range of capabilities that will be required to execute this value delivery, against which the companies can confirm what capabilities they could bring to or develop in China. In the process, the companies can ascertain what capability gaps there are, if any, to fill. The next question is how the companies could fill these capability gaps in the most effective way and whether local partners could help to close the capability gaps (see Exhibit 6). With this strategic agenda in mind, companies also need to consider their ownership model need in terms of the regulatory environment in the sectors in which it operates.

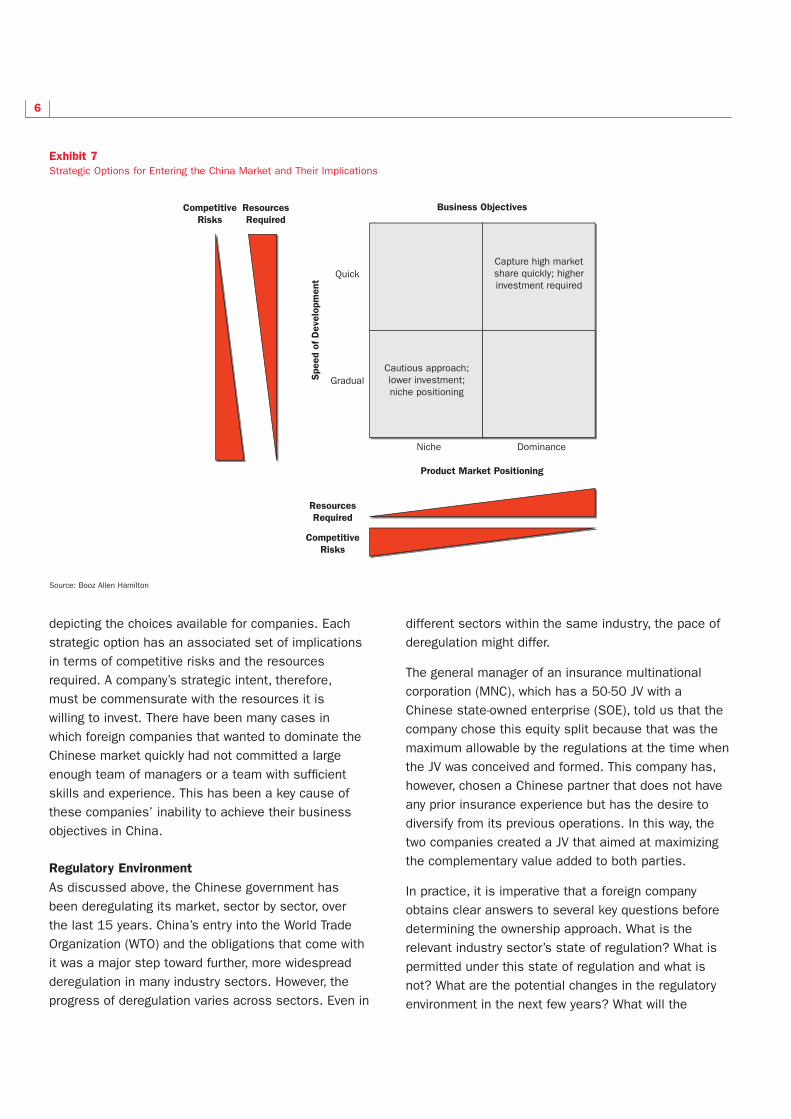

Against this backdrop, companies should decide the speed at which they want to develop their businesses and their desired product market positioning and coverage in China. Exhibit 7 shows a framework

Exhibit 6Foreign Companies’ Ownership Approach: Traditional versus Capability-Driven

Source: Booz Allen Hamilton

“Traditional” Approach Followed by Many

Capability-Driven Process

1. Develop your value proposition and product market strategy

2. Identify how you will execute your strategy

– Value delivery system

3. Map the range of capabilities required to execute the value delivery

4. Confirm capabilities you can bring to or develop in China

– Identify capability gaps

5. Decide how to best fill the capability gaps

6. Search for best partner(s) to fill these gaps

Migrate to

1. Find a Chinese partner – Often to source “Guanxi”

Partnership designed this way is often ill-conceived

and limits strategy formulation and execution

� Evaluate your strategy in China

6

depicting the choices available for companies. Each strategic option has an associated set of implications in terms of competitive risks and the resources required. A company’s strategic intent, therefore, must be commensurate with the resources it is willing to invest. There have been many cases in which foreign companies that wanted to dominate the Chinese market quickly had not committed a large enough team of managers or a team with sufficient skills and experience. This has been a key cause of these companies’ inability to achieve their business objectives in China.

Regulatory EnvironmentAs discussed above, the Chinese government has been deregulating its market, sector by sector, over the last 15 years. China’s entry into the World Trade Organization (WTO) and the obligations that come with it was a major step toward further, more widespread deregulation in many industry sectors. However, the progress of deregulation varies across sectors. Even in

different sectors within the same industry, the pace of deregulation might differ.

The general manager of an insurance multinational corporation (MNC), which has a 50-50 JV with a Chinese state-owned enterprise (SOE), told us that the company chose this equity split because that was the maximum allowable by the regulations at the time when the JV was conceived and formed. This company has, however, chosen a Chinese partner that does not have any prior insurance experience but has the desire to diversify from its previous operations. In this way, the two companies created a JV that aimed at maximizing the complementary value added to both parties.

In practice, it is imperative that a foreign company obtains clear answers to several key questions before determining the ownership approach. What is the relevant industry sector’s state of regulation? What is permitted under this state of regulation and what is not? What are the potential changes in the regulatory environment in the next few years? What will the

Exhibit 7Strategic Options for Entering the China Market and Their Implications

Source: Booz Allen Hamilton

Business Objectives Competitive Risks

Competitive Risks

Resources Required

Resources Required

Quick

Dominance

Gradual

Niche

Spe

ed o

f D

evel

opm

ent

Product Market Positioning

Capture high market share quickly; higher investment required

Cautious approach; lower investment; niche positioning

7

implications of the upcoming regulatory changes be for the company?

Generally speaking, in restricted industries in China, guanxi can be useful for helping a foreign company to gain entry, but it is not a guarantee for success. In deregulated industries where overcapacity often exists, at least for a certain period, pricing of products and services can be under tremendous downward pressure and competition can be intense. Companies will need to bring or cultivate best-in-class, if not world-class, capabilities in order to succeed.

Companies’ Capabilities in ChinaAs discussed above, foreign companies will need to assess what capabilities are needed across the entire value chain of their business in order to succeed in China. In that context, companies will need to assess what capabilities they already possess and can bring to China and what they would need to bring in from outside, for instance, through a JV or alliance with external parties.

One of the MNCs we surveyed has more than a dozen operations in China, and the majority of them are WFOEs. However, when the company set up its first medical equipment unit in China in 2004, it decided to create a 51-49 JV with a local partner. The company’s vice president of strategy explained, “We didn’t have the people or skills that it would take to compete in the segment against the established players. Our partner’s management was all trained engineers (half of them teach at a local university), and they understood medical systems. It would have taken us at least two years to train our people to that level.”

Clearly, it is critical for companies to answer a few key questions about their operations. Depending on where the company stands on its development curve in China, what are the required skills and capabilities to win in the current stage? Does the company have such capabilities? What is the most effective and efficient way to close the gaps, for now and for the future?

A multinational construction equipment manufacturing company that was a late entrant to the Chinese market decided to take the JV route because it did not have much on-the-ground knowledge in place, even though

the industry itself is fully liberalized and there is no exogenous force mandating JV. The company’s general manager told us, “Although we recognize that there are some drawbacks to the JV, our late arrival to the market and inexperience in China sort of forces our hand.”

It is not only companies that are new to the market that need to question themselves in this way. Companies that are already operating in China, which have accumulated some experience, need to review what they have learned and what kind of resources they have built up. Such knowledge and resources are crucial to the companies’ strategic direction going forward. Has the company acquired the requisite experience, knowledge, and capabilities to operate effectively in China? To what extent have these capabilities been institutionalized in China, and are they transferable from one part of the organization to another? What mechanisms does the company need to put in place to ensure that these “corporate memories” will not be lost?

As foreign companies accumulate knowledge and experience in China, many of them will choose to go it alone. In 2004, after operating in China for more than a decade and accumulating tremendous knowledge of the market, Procter & Gamble, arguably one of the most successful foreign companies in China, paid Hutchison Whampoa, its Hong Kong-based partner, US$1.8 billion for the remaining 20 percent of the JV, thereby creating a WFOE. In 2002, seven years after it formed its washing machine JV with a Chinese partner, Narcissus, major U.S. electric appliances maker Whirlpool paid Narcissus US$9.2 million for the last 20 percent of the JV to become a WFOE. In both of these cases, the foreign companies had accumulated significant operating experience after their entries to China; when they decided the time was right, they bought out their local partners to gain management control.

ImplicationsForeign companies need to determine their ownership approach by considering the factors mentioned above. While there are conditions under which a JV would be more favorable than a WFOE, it is clear that where it’s possible, the trend in the last decade is toward WFOEs, either as start-ups or as a result of restructuring of

8

previous JVs. The forces bringing about this change include a continuing process of deregulation, continued high levels of direct investment by foreign companies, and the resulting accumulated volume of knowledge of foreign companies about operating in China. This has been particularly obvious since China’s accession to the WTO in December 2001.

To cite some examples of the trend toward WFOEs, in 2004, Toshiba paid Shanghai Jinqiao, its local partner, US$920,000 for Jinqiao’s 10 percent of Toshiba Personal Computer & Network (Shanghai) Co. Ltd., turning the JV into a WFOE. In 2005, Johnson & Johnson paid US$39 million to turn its pharmaceutical JV in Shanghai into a WFOE. Finally, in 2005, Avon paid US$39 million to buy 6.2 percent of Avon Products (China) Co. Ltd. and turned that into a WFOE as well.

As WFOEs are increasingly becoming prevalent, the implications can be far-reaching. In a JV environment, as mentioned above, it is often difficult and sometimes impossible for the foreign company and local partner to be totally aligned in terms of their vision, strategy,

operations, and investment plans. One particular area of concern from the foreign companies’ standpoint is whether or not they should bring their “best” product or technology to China and to what extent they should integrate their Chinese operations into the global business systems. Many foreign companies would be relatively hesitant to do so if the Chinese operation is a JV. With more WFOEs, we can expect foreign companies will have a stronger say on every step of their value chains. As a result, we expect increasingly more foreign companies will bring a broader set of their capabilities to operate in China and will further integrate the Chinese operations into their global operations, making China not only a key market for the companies, but also a critical source of competitive advantages for these companies on a global basis. For many MNCs, this could have far-reaching implications on their global competitive positioning and potential for sustainable growth. This is yet another force that is driving the development of a “flat world,”(1) as Thomas Friedman calls it, where China is playing an increasingly significant role.

The author wishes to thank Yichin Lee and Matthew Sweeny for their help with this article.

08/08 Printed in Greater China©2006 Booz & Company Inc.

The most recent list of our office addresses and telephone numbers can be found on our Greater China Web site, www.booz.com/cn.

Asia Beijing Hong Kong MumbaiSeoul ShanghaiTaipeiTokyo

Australia, New Zealand, and Southeast Asia Adelaide Auckland Bangkok Brisbane Canberra Jakarta Kuala Lumpur Melbourne Sydney

BOOZ & COMPANY WORLDWIDE OFFICES

Europe Amsterdam Berlin Copenhagen Dublin Düsseldorf Frankfurt Helsinki London Madrid Milan Moscow Munich Oslo Paris Rome Stockholm Stuttgart Vienna Warsaw Zurich

South America Buenos Aires Rio de Janeiro Santiago São Paulo

Middle East Abu Dhabi Beirut Cairo Dubai Riyadh

North America Atlanta Chicago Cleveland Dallas Detroit Florham Park Houston Los Angeles McLean Mexico City New York City Parsippany San Francisco