tackling global payment challenges - c.ymcdn.com · uetr cgi pain camt fcc 2fa tch/fed tch/fed dlt...

TRANSCRIPT

Tackling Global Payment Challenges

Laura McGortey

Global Payments Product Line Manager

BNY Mellon Treasury Services

Kevin O’Neil

Regional Account Manager

SWIFT | Americas & UK Region

May 17, 2017

2 Information Classification: Confidential

• Causes behind today’s challenges within cross-border payment processes

• Potential implications of new and alternative payment channels and

technologies

• Examples of innovative solutions in pilot or readily available

• What the future holds for the industry, and where we are headed

Tackling Cross-border Payments Challenges

3 Information Classification: Confidential

Todays Agenda

4 Information Classification: Confidential

CCT

CSP CVSSv3

NIST/PCI KYC OFAC

PSD

Dodd Frank

CISO SIP

STP SCORE

ISO AL2/SAA/SB

ACMT

PACS

CDD/EDD

DOJ

USA Patriot Act

FIN/FileAct PSR

BIC/IBAN

SSI

UCC (4A)

GPI

UETR

CGI

PAIN

CAMT

FCC

2FA TCH/FED

TCH/FED

DLT

Grouped by Themes – Brought To You by SWIFT SCRL

5 Information Classification: Confidential

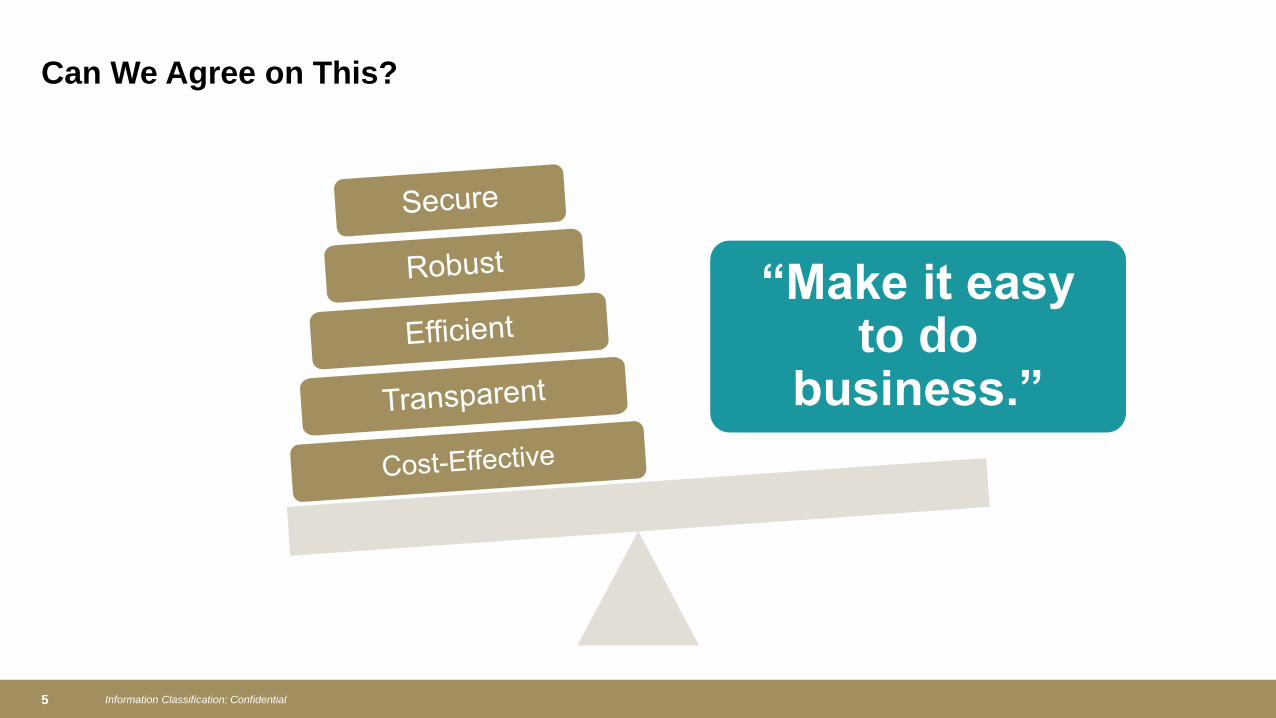

Can We Agree on This?

“Make it easy to do

business.”

6 Information Classification: Confidential

Potential for Additional Intermediaries with Any Transaction

Beneficiary Correspondent Beneficiary Bank

Cross-border Payments End-to-end View

*Such as:

• ISO 20022

• X12 820

• EDIFACT

• SWIFT FIN or File Act

• Bank Proprietary

Company

XYZ

TMS and

or ERP

“When and for what amount was beneficiary’s account credited?”

Bank

Access

and

Routing

Infrastructure

File Acknowledgement(s)

Potential for

Foreign Exchange

Debit Advice/Acknowledgement

Debit from

Funding

Account

FILE Upload

User Interface/Web

*File Transfer

Mobile Initiation

Third Party Initiation

(e.g., Payroll)

Central Bank

Beneficiary Correspondent Beneficiary Bank

Beneficiary

Correspondent

Beneficiary Correspondent Beneficiary Bank

Beneficiary Correspondent Beneficiary Bank Central Bank

Beneficiary Correspondent Beneficiary Bank

Foreign Currency

Drafts

IACH (Domestic

Low Value

Clearing)

USD ACH (IAT)

Wire Transfer

(Domestic and Int’l

Foreign Currency)

Bank

Clearing

Settlement

Accounts

Advising or Statement

Possible Currency Conversion (FX)

Possible Principle Deduction

Currency Conversion (FX)

7 Information Classification: Confidential

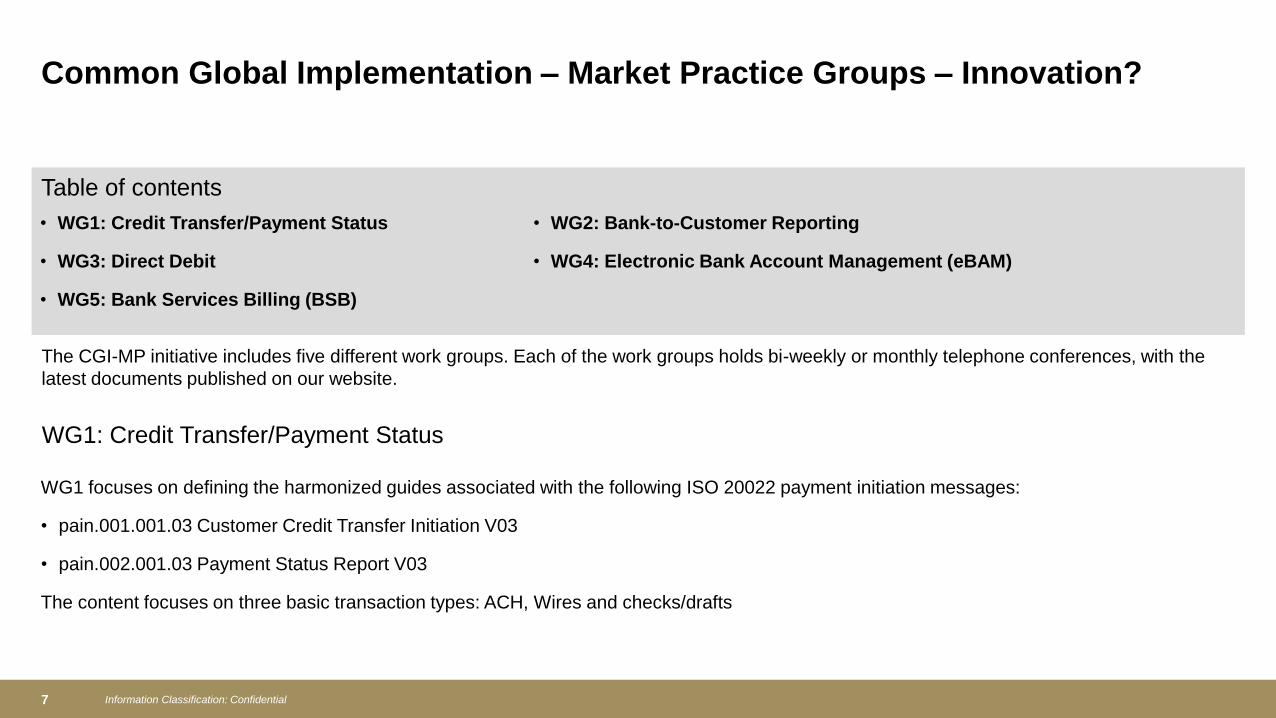

Common Global Implementation – Market Practice Groups – Innovation?

Table of contents

• WG1: Credit Transfer/Payment Status

• WG3: Direct Debit

• WG5: Bank Services Billing (BSB)

• WG2: Bank-to-Customer Reporting

• WG4: Electronic Bank Account Management (eBAM)

The CGI-MP initiative includes five different work groups. Each of the work groups holds bi-weekly or monthly telephone conferences, with the

latest documents published on our website.

WG1: Credit Transfer/Payment Status

WG1 focuses on defining the harmonized guides associated with the following ISO 20022 payment initiation messages:

• pain.001.001.03 Customer Credit Transfer Initiation V03

• pain.002.001.03 Payment Status Report V03

The content focuses on three basic transaction types: ACH, Wires and checks/drafts

8 Information Classification: Confidential

Innovation?

3,022 Number of relationships between

corporates and banks

exchanging ISO20022

680 654 740

675

463

21.9%

26.0%

21.3% 22.1%

29.3%

0

100

200

300

400

500

600

700

800

900

1000

Send Receive Total Payments* MT940 & 20022**

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

ISO20022 Based on Live traffic in Q3 2016

# of corporates inQ3 2016

Growth vs PY

*Send/receive pain.001.001 and pain.008.

**Send/receive both FIN MT940 and ISO20022

9 Information Classification: Confidential

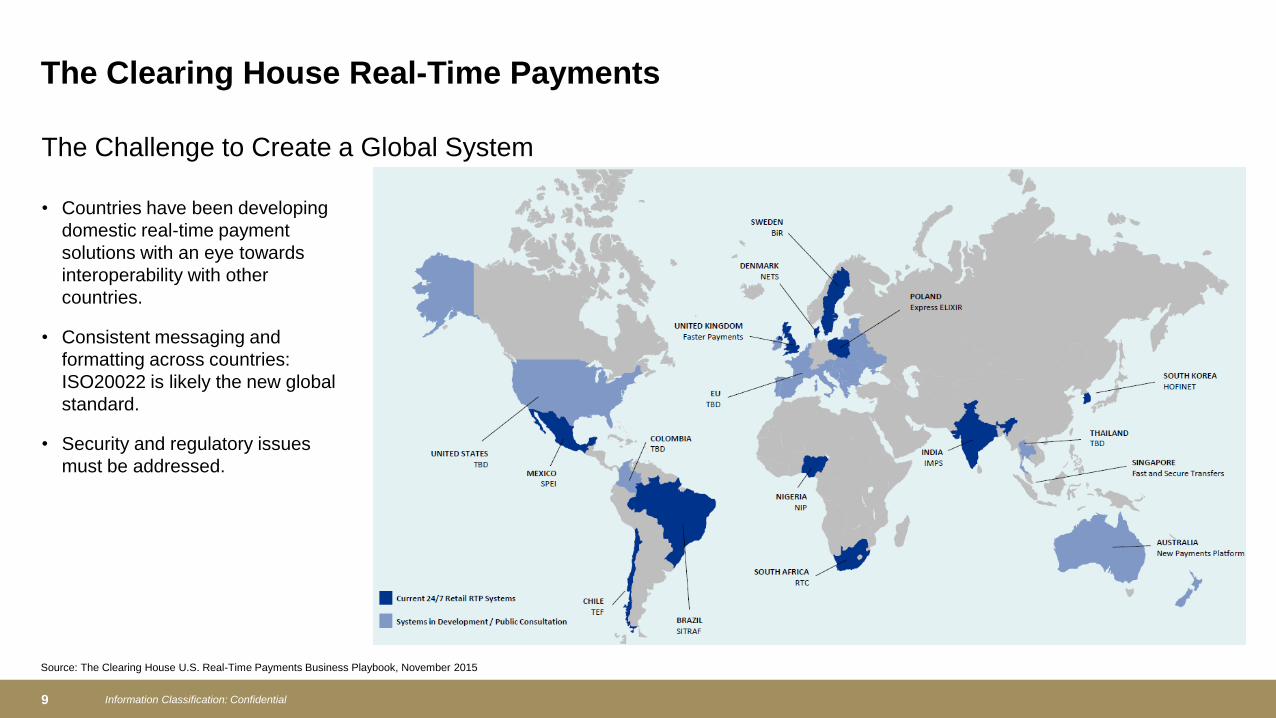

The Challenge to Create a Global System

Source: The Clearing House U.S. Real-Time Payments Business Playbook, November 2015

• Countries have been developing

domestic real-time payment

solutions with an eye towards

interoperability with other

countries.

• Consistent messaging and

formatting across countries:

ISO20022 is likely the new global

standard.

• Security and regulatory issues

must be addressed.

The Clearing House Real-Time Payments

10 Information Classification: Confidential

Internal actions

Your

Counterparts

Your

Community

• Secure your local environment

• Sign up to our Security Notification Service

• Register Chief Information Security Officer (CISO)

• Attestation for bilateral transparency/discussions

• ‘Clean-up’ your RMA/relationships

• Put in place fraud detection measures

• Engage with us on market practice

• Bilateral discussions with bank

counterparties

• Provide contact details of your

company’s CISO for incident escalation

Many applicable regardless of channel

Tackling Customer Security

Corporate/Industry Discussion Points

11 Information Classification: Confidential

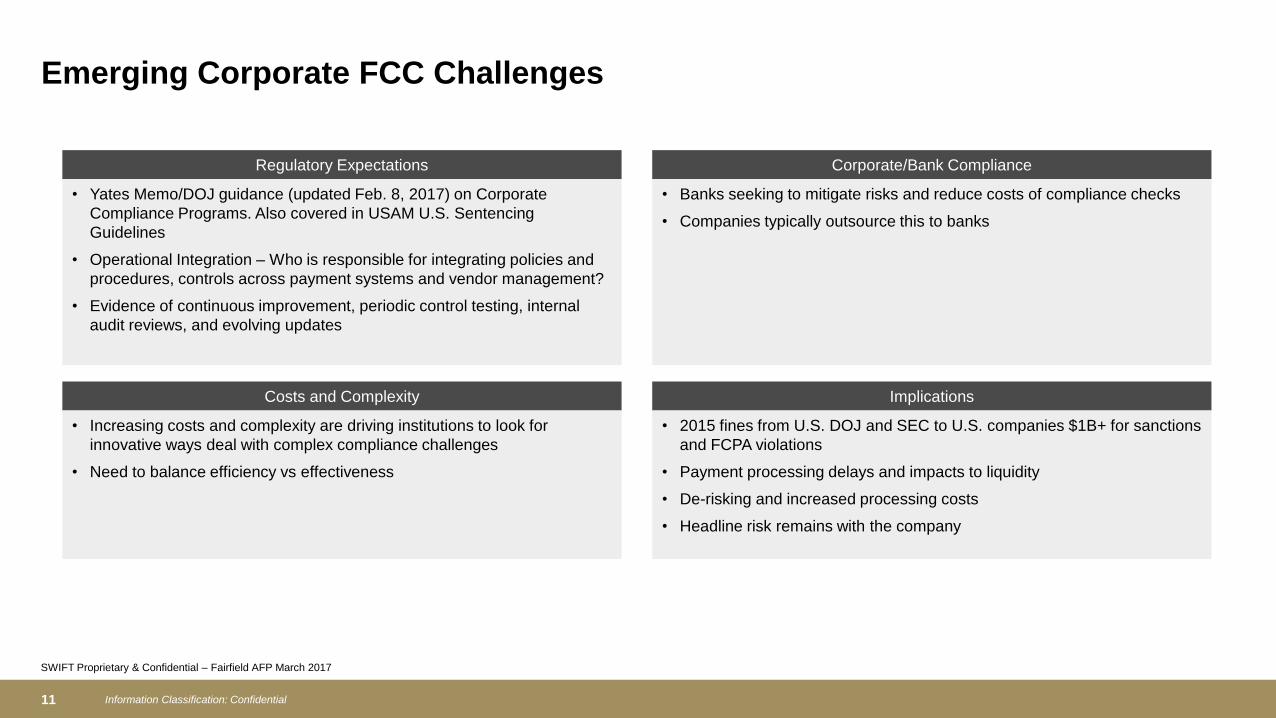

Regulatory Expectations

• Yates Memo/DOJ guidance (updated Feb. 8, 2017) on Corporate

Compliance Programs. Also covered in USAM U.S. Sentencing

Guidelines

• Operational Integration – Who is responsible for integrating policies and

procedures, controls across payment systems and vendor management?

• Evidence of continuous improvement, periodic control testing, internal

audit reviews, and evolving updates

Costs and Complexity

• Increasing costs and complexity are driving institutions to look for

innovative ways deal with complex compliance challenges

• Need to balance efficiency vs effectiveness

Corporate/Bank Compliance

• Banks seeking to mitigate risks and reduce costs of compliance checks

• Companies typically outsource this to banks

Implications

• 2015 fines from U.S. DOJ and SEC to U.S. companies $1B+ for sanctions

and FCPA violations

• Payment processing delays and impacts to liquidity

• De-risking and increased processing costs

• Headline risk remains with the company

Emerging Corporate FCC Challenges

SWIFT Proprietary & Confidential – Fairfield AFP March 2017

12 Information Classification: Confidential

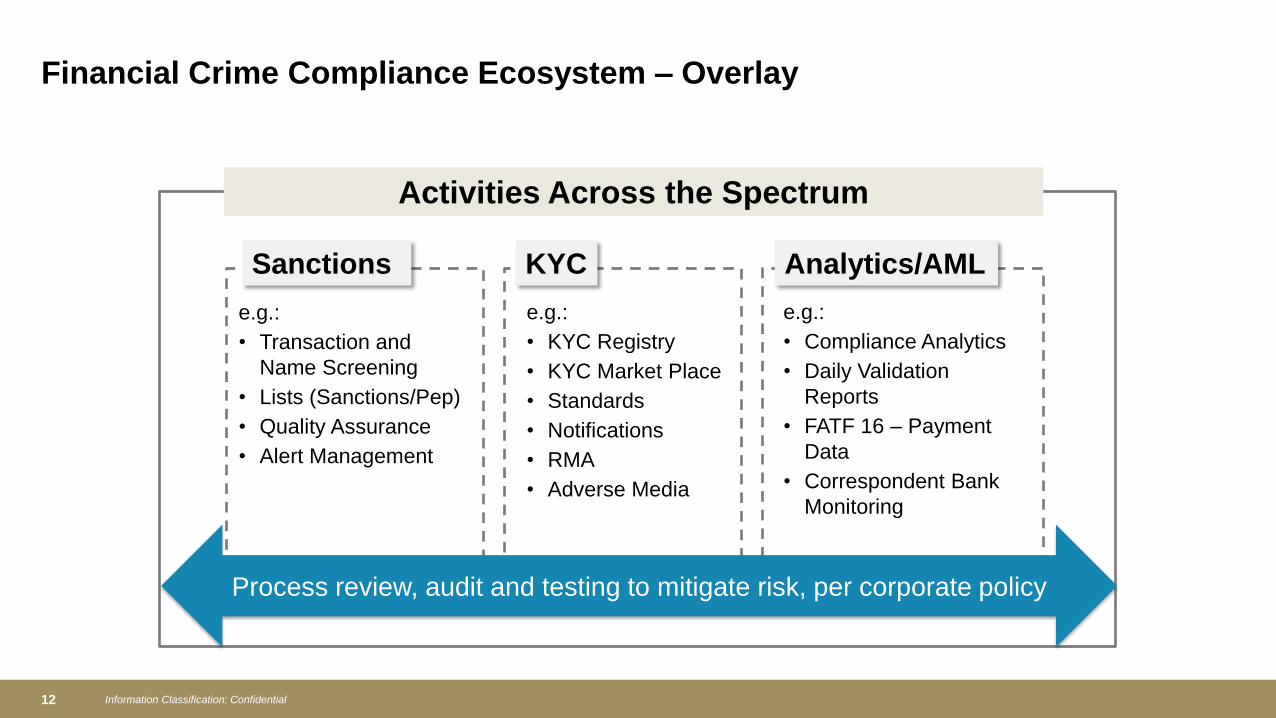

Financial Crime Compliance Ecosystem – Overlay

Sanctions Analytics/AML KYC

Activities Across the Spectrum

e.g.:

• Transaction and

Name Screening

• Lists (Sanctions/Pep)

• Quality Assurance

• Alert Management

e.g.:

• KYC Registry

• KYC Market Place

• Standards

• Notifications

• RMA

• Adverse Media

e.g.:

• Compliance Analytics

• Daily Validation

Reports

• FATF 16 – Payment

Data

• Correspondent Bank

Monitoring

Process review, audit and testing to mitigate risk, per corporate policy

13 Information Classification: Confidential

“I’m not able to tell when

the money hits the

beneficiary’s bank

account.”

“Many times we don’t

have visibility on the fees

lifted along the way.”

“Critical business requires

faster payment

execution.”

“We miss information

regarding the invoice and

the payer for timely

reconciliation.”

Tracking Transparency Speed Remittance Information

Sound Familiar?

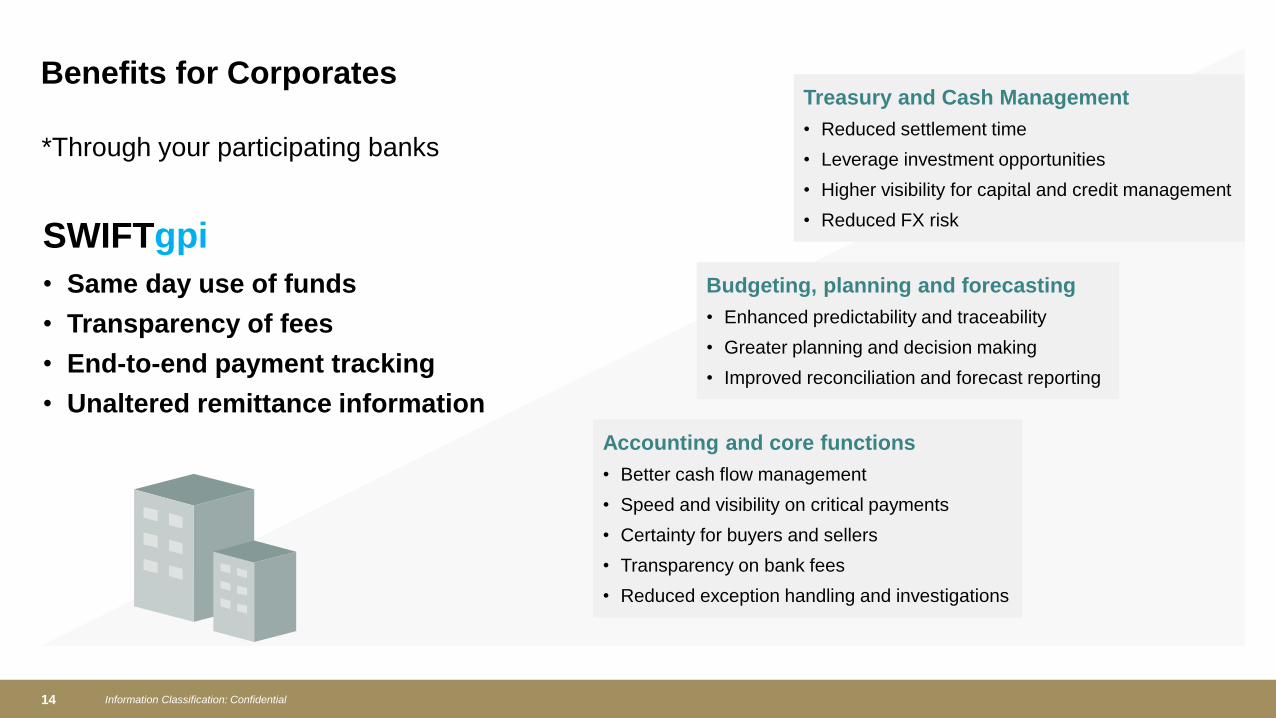

14 Information Classification: Confidential

*Through your participating banks

Benefits for Corporates

• Same day use of funds

• Transparency of fees

• End-to-end payment tracking

• Unaltered remittance information

SWIFTgpi

Accounting and core functions

• Better cash flow management

• Speed and visibility on critical payments

• Certainty for buyers and sellers

• Transparency on bank fees

• Reduced exception handling and investigations

Budgeting, planning and forecasting

• Enhanced predictability and traceability

• Greater planning and decision making

• Improved reconciliation and forecast reporting

Treasury and Cash Management

• Reduced settlement time

• Leverage investment opportunities

• Higher visibility for capital and credit management

• Reduced FX risk

15 Information Classification: Confidential

Rich Payment Data Request For Cancellation International Payment Assistant

SWIFTgpi

Rich remittance information, invoices,

compliance documents, etc.

Stopping unsolicited payments

(double payment, manual errors, fraud)

STOP

SWIFTgpi

Validation of payments before execution

SWIFTgpi

Account number?

BIC?

Passport required?

Beneficiary?

v2 – Q4 2017 – 2018

Evolution of Functionality…

16 Information Classification: Confidential

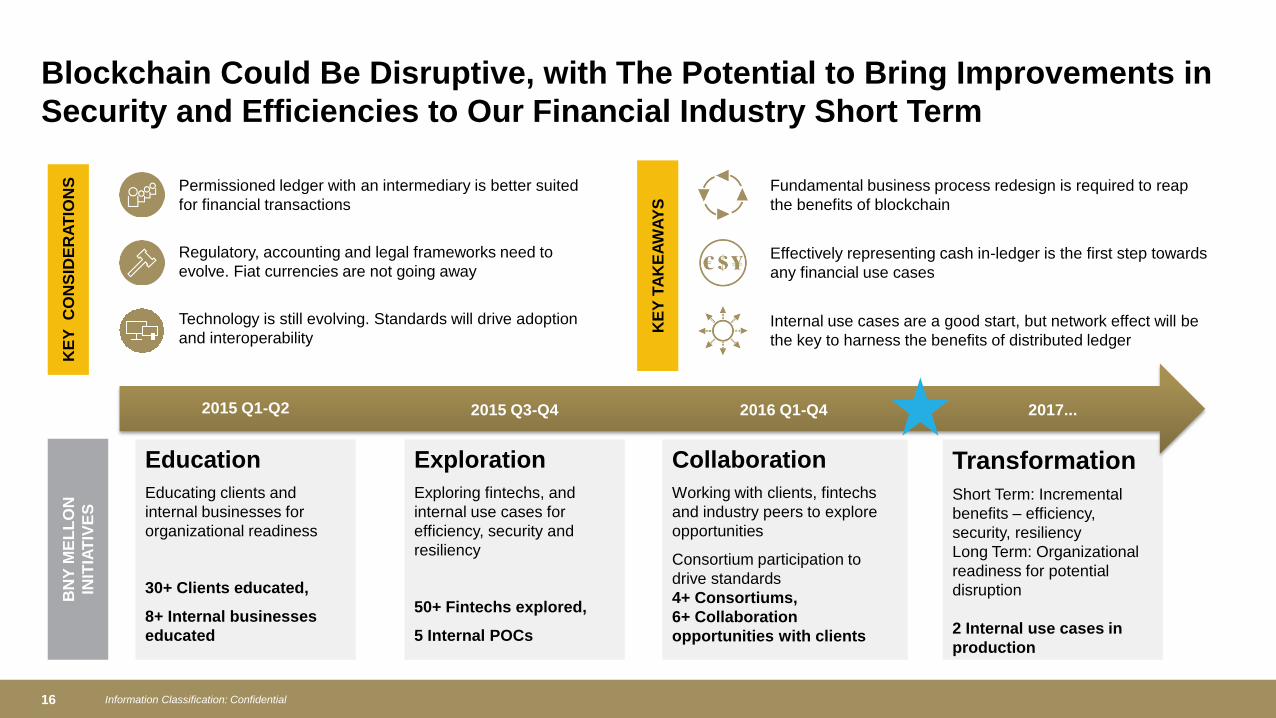

BN

Y M

EL

LO

N

INIT

IAT

IVE

S

Education

Educating clients and

internal businesses for

organizational readiness

30+ Clients educated,

8+ Internal businesses

educated

Exploration

Exploring fintechs, and

internal use cases for

efficiency, security and

resiliency

50+ Fintechs explored,

5 Internal POCs

Collaboration

Working with clients, fintechs

and industry peers to explore

opportunities

Consortium participation to

drive standards

4+ Consortiums,

6+ Collaboration

opportunities with clients

Transformation

Short Term: Incremental

benefits – efficiency,

security, resiliency

Long Term: Organizational

readiness for potential

disruption

2 Internal use cases in

production

Permissioned ledger with an intermediary is better suited

for financial transactions

Technology is still evolving. Standards will drive adoption

and interoperability

Blockchain Could Be Disruptive, with The Potential to Bring Improvements in

Security and Efficiencies to Our Financial Industry Short Term

KE

Y

CO

NS

IDE

RA

TIO

NS

KE

Y T

AK

EA

WA

YS

Fundamental business process redesign is required to reap

the benefits of blockchain

Effectively representing cash in-ledger is the first step towards

any financial use cases

Regulatory, accounting and legal frameworks need to

evolve. Fiat currencies are not going away

Internal use cases are a good start, but network effect will be

the key to harness the benefits of distributed ledger

2017... 2016 Q1-Q4 2015 Q3-Q4 2015 Q1-Q2

17 Information Classification: Confidential

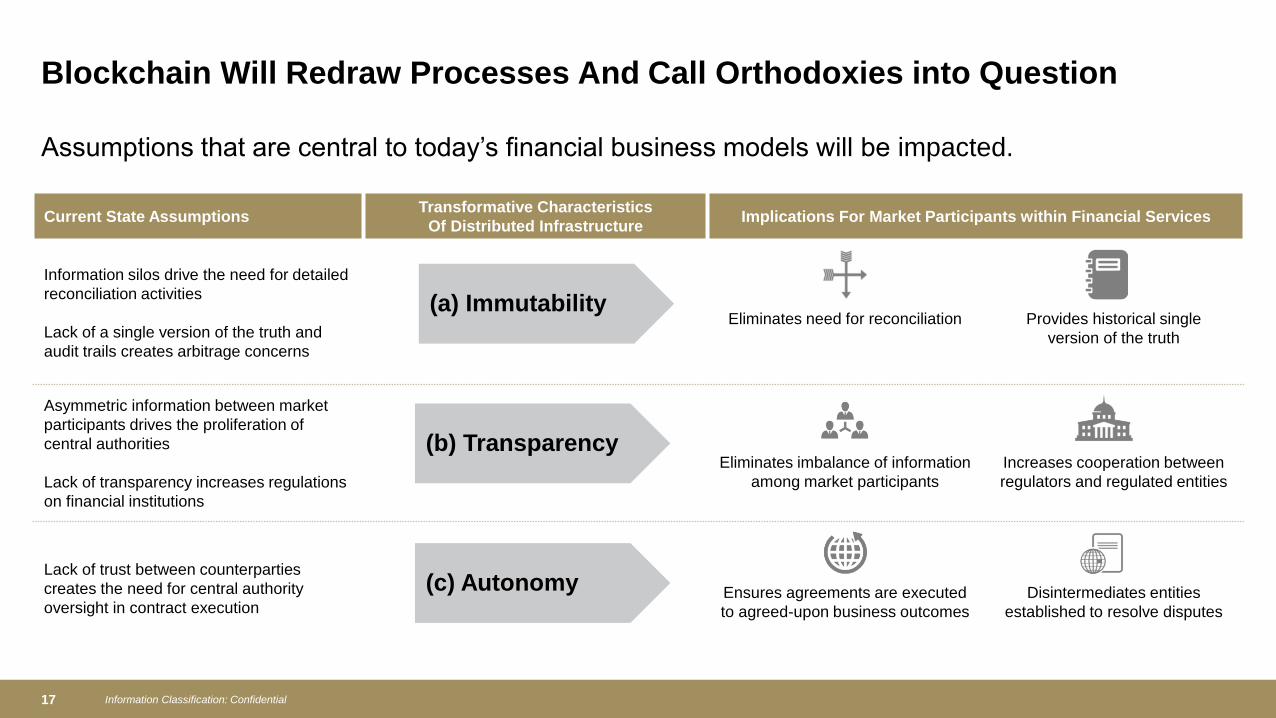

Assumptions that are central to today’s financial business models will be impacted.

Blockchain Will Redraw Processes And Call Orthodoxies into Question

Current State Assumptions Transformative Characteristics

Of Distributed Infrastructure Implications For Market Participants within Financial Services

Information silos drive the need for detailed

reconciliation activities

Lack of a single version of the truth and

audit trails creates arbitrage concerns

Eliminates need for reconciliation Provides historical single

version of the truth

Asymmetric information between market

participants drives the proliferation of

central authorities

Lack of transparency increases regulations

on financial institutions

Eliminates imbalance of information

among market participants

Increases cooperation between

regulators and regulated entities

Lack of trust between counterparties

creates the need for central authority

oversight in contract execution Ensures agreements are executed

to agreed-upon business outcomes

Disintermediates entities

established to resolve disputes

(a) Immutability

(b) Transparency

(c) Autonomy

18 Information Classification: Confidential

• A convergence of market forces and new entrants

have spurred payment innovation to overcome

various challenges

• Banks and payment operators have launched

significant payment modernization efforts

• Blockchain has the potential to dramatically

modernize payments, but impact and timing is TBD

• BNY Mellon is invested in payment modernization,

with efforts underway to:

– Extend our capabilities with new solutions

– Play a leadership role in industry initiatives to

modernize payments

– Explore the transformative potential of blockchain

technology and other fintech solutions

Payment Modernization Is Underway…

19 Information Classification: Confidential

• Key industry requirements and evaluation of “maturity”

• When does emerging technology/business model

take hold? Business use cases will evolve

Distributed Ledger Technologies (DLTs) – SWIFT and Accenture

2016 White Paper

20 Information Classification: Confidential

• Existing DLTs are currently not mature enough to fulfil the requirements identified

• There are promising developments in each of these requirements

• Significant extra R&D work is needed in all these domains before DLTs can be

applied at the scale required by the financial industry

DLTs – Conclusions of the

Technology Assessment

21 Information Classification: Confidential

BNY Mellon is the corporate brand of The Bank of New York Mellon Corporation and may be used as a generic term to reference the corporation as a whole and/or its various subsidiaries generally. This material and any

products and services may be issued or provided under various brand names in various countries by duly authorized and regulated subsidiaries, affiliates, and joint ventures of BNY Mellon, which may include any of the

following. The Bank of New York Mellon, in New York, New York a banking corporation organized pursuant to the laws of the State of New York, and operating in England through its branch at One Canada Square, London

E14, England and registered in England and Wales with numbers FC005522 and BR000818. The Bank of New York Mellon is supervised and regulated by the New York State Department of Financial Services and the US

Federal Reserve and authorized by the Prudential Regulation Authority. The Bank of New York Mellon, London Branch is subject to regulation by the Financial Conduct Authority and limited regulation by the Prudential

Regulation Authority. The Bank of New York Mellon SA/NV, a Belgian public limited liability company, with company number 0806.743.159, whose registered office is at 46 Rue Montoyerstraat, B-1000 Brussels, Belgium,

authorized and regulated as a significant credit institution by the European Central Bank (ECB), under the prudential supervision of the National Bank of Belgium (NBB) and under the supervision of the Belgian Financial

Services and Markets Authority (FSMA) for conduct of business rules, and a subsidiary of The Bank of New York Mellon. The Bank of New York Mellon SA/NV operates in England through its branch at 160 Queen Victoria

Street, London EC4V 4LA and is registered in England and Wales with numbers FC029379 and BR0014361. The Bank of New York Mellon SA/NV (London Branch) authorized by the ECB, NBB and the FSMA and subject to

limited regulation by the Financial Conduct Authority and the Prudential Regulation Authority. Details about the extent of our regulation by the Financial Conduct Authority and Prudential Regulation Authority are available from

us on request. The Bank of New York Mellon, Singapore Branch is subject to regulation by the Monetary Authority of Singapore. The Bank of New York Mellon, Hong Kong Branch is subject to regulation by the Hong Kong

Monetary Authority and the Securities & Futures Commission of Hong Kong. If this material is issued or distributed in Japan, it is issued or distributed by The Bank of New York Mellon Securities Company Japan Ltd. as

intermediary for The Bank of New York Mellon. Not all products and services are offered in all countries.

BNY Mellon Capital Markets EMEA Limited, an indirect wholly owned broker dealer subsidiary of The Bank of New York Mellon Corporation, is an investment firm authorised and regulated by the Financial Conduct Authority

UK (FCA) under registration number 580200 and provides services to Professional Clients and Eligible Counterparties but not to Retail Clients (in each case as defined in the FCA Rules) in the European Economic Area. BNY

Mellon Capital Markets EMEA Limited is not licensed in any other jurisdiction and accordingly, it does not target, promote or offer its products and services to clients outside of the European Economic Area (EEA) and nothing

in this communication shall be construed as intended for any persons outside the EEA or for any non-EEA persons. BNY Mellon Capital Markets EMEA Limited is registered in England with company number 03766757 and

operates from its registered office and place of business at 1 Canada Square, London E14 5AL. Past performance is not a guide to future performance of any instrument, transaction or financial structure and a loss of original

capital may occur. Calls and communications with BNY Mellon Capital Markets EMEA Limited may be recorded, for regulatory and other reasons.

The information contained in this material is intended for use by wholesale/professional clients or the equivalent only and is not intended for use by retail clients. If distributed in the UK, this material is a financial promotion.

This material, which may be considered advertising, is for general information purposes only and is not intended to provide legal, tax, accounting, investment, financial or other professional advice on any matter. This material

does not constitute a recommendation by BNY Mellon of any kind. Use of our products and services is subject to various regulations and regulatory oversight. You should discuss this material with appropriate advisors in the

context of your circumstances before acting in any manner on this material or agreeing to use any of the referenced products or services and make your own independent assessment (based on such advice) as to whether the

referenced products or services are appropriate or suitable for you. This material may not be comprehensive or up to date and there is no undertaking as to the accuracy, timeliness, completeness or fitness for a particular

purpose of information given. BNY Mellon will not be responsible for updating any information contained within this material and opinions and information contained herein are subject to change without notice. BNY Mellon

assumes no direct or consequential liability for any errors in or reliance upon this material.

22 Information Classification: Confidential

This material may not be distributed or used for the purpose of providing any referenced products or services or making any offers or solicitations in any jurisdiction or in any circumstances in which such products, services,

offers or solicitations are unlawful or not authorized, or where there would be, by virtue of such distribution, new or additional registration requirements.

Money market fund shares are not a deposit or obligation of BNY Mellon. Investments in money market funds are not insured, guaranteed, recommended or otherwise endorsed in any way by BNY Mellon, the Federal Deposit

Insurance Corporation or any other government agency. Securities instruments and services other than money market mutual funds and off-shore liquidity funds are offered by BNY Mellon Capital Markets, LLC.

The terms of any products or services provided by BNY Mellon to a client, including without limitation any administrative, valuation, trade execution or other services shall be solely determined by the definitive agreement

relating to such products or services. Any products or services provided by BNY Mellon shall not be deemed to have been provided as fiduciary or adviser except as expressly provided in such definitive agreement. BNY Mellon

may enter into a foreign exchange transaction, derivative transaction or collateral arrangement as a counterparty to a client, and its rights as counterparty or secured party under the applicable transactional agreement or

collateral arrangement shall take precedence over any obligation it may have as fiduciary or adviser or as service provider under any other agreement.

Pursuant to Title VII of The Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 and the applicable rules thereunder, The Bank of New York Mellon is provisionally registered as a swap dealer with the

Commodity Futures Trading Commission (“CFTC”) and is a swap dealer member of the National Futures Association (NFA ID 0420990).

BNY Mellon (including its broker-dealer affiliates) may have long or short positions in any currency, derivative or instrument discussed herein. BNY Mellon has included data in this material from information generally available

to the public from sources believed to be reliable. Any price or other data used for illustrative purposes may not reflect actual current conditions. No representations or warranties are made, and BNY Mellon assumes no liability,

as to the suitability of any products and services described herein for any particular purpose or the accuracy or completeness of any information or data contained in this material. Price and other data are subject to change at

any time without notice.

Pershing Prime Services is a service of Pershing LLC, member FINRA, NYSE, SIPC, a wholly owned subsidiary of The Bank of New York Mellon Corporation (BNY Mellon). Member of SIPC. Securities in your account

protected up to $500,000. For details, please see www.sipc.org.

The financial products (other than deposit products) mentioned are not insured or protected by any government, state or federal agency (including the Federal Deposit Insurance Corporation), are not deposits

of or guaranteed by BNY Mellon or any bank or non-bank subsidiary thereof, and are subject to investment risk, including the loss of principal amount invested. References to Assets Under Management and

Assets Under Custody and/or Administration are as of June 30, 2015 and are preliminary.

This material may not be reproduced or disseminated in any form without the prior written permission of BNY Mellon. BNY Mellon information, as presented on slides 2, 6, 9 and 16-18, does not undertake to update or amend

this information and expressly disclaims any liability for any loss arising from this information or data.

Trademarks, logos and other intellectual property marks belong to their respective owners.

1Assets under management include investment boutiques and wealth management.

The Bank of New York Mellon, member FDIC.

© 2017 The Bank of New York Mellon Corporation. All rights reserved.