t4- part b case study toy case march 2012 report

TRANSCRIPT

© The Chartered Institute of Management Accountants 2012 Page No: 1

Note: This report is far more comprehensive than would be expected from a candidate in exam conditions. It is more detailed for teaching purposes.

T4- Part B – Case Study

Jot – toy case – March 2012

REPORT

To: Jon Grun, Managing Director, Jot From: Management Accountant Date: 28 February 2012

Review of issues facing Jot Contents 1.0 Introduction 2.0 Terms of reference 3.0 Prioritisation of the issues facing Jot 4.0 Discussion of the issues facing Jot 5.0 Ethical issues and recommendations on ethical issues 6.0 Recommendations 7.0 Conclusions Appendices Appendix 1 SWOT analysis Appendix 2 PEST analysis Appendix 3 Selection of new outsourced manufacturer for products YY and ZZ Appendix 4 VP “own brand” proposal Appendix 5 Inventory valuation Appendix 6 Calculations for outsourced manufacturers P and Q for licensed action figures Appendix 7 Email on the key criteria for the selection of outsourced manufacturers 1.0 Introduction Jot is a small unlisted company which designs and outsources the manufacture of a range of children’s toys. It has grown rapidly since it was established in 1998. It is currently experiencing manufacturing problems due to an earthquake affecting 2 of its outsourced manufacturers and also quality problems with another outsourced manufacturer. The quality of the company’s products, upon which its reputation is based, must not be compromised. The Jot brand name is known for quality toys but it is important that its products appeal to cost-conscious retailers and price sensitive customers. Jot can use the cost-leadership strategy, using Porter’s generic strategy framework, to select the minimum cost in its choice of manufacturers for products YY and ZZ. 2.0 Terms of reference I am the Management Accountant appointed to write a report to Jon Grun, Managing Director of Jot, a toy company, which prioritises, analyses and evaluates the issues facing Jot and makes appropriate recommendations.

© The Chartered Institute of Management Accountants 2012 Page No: 2

I have also been asked to write an email to the management team to set out the key criteria for the selection of new outsourced manufacturers in general, together with my recommendation on which manufacturer(s) should be appointed for products YY and ZZ. This is included in Appendix 7 to this report. 3.0 Prioritisation of the issues facing Jot 3.1 Top priority – Manufacturing problems The top priority is the loss of 2 outsourced manufacturers following the recent earthquake. They are unable to manufacture any products for Jot for the remainder of 2012. Therefore new outsourced manufacturers need to be identified and appointed urgently in order to manufacture products YY and ZZ, which total 150,000 units in 2012. This volume of products represents over 17% of Jot’s planned sales of 868,500 units in 2012. 3.2 Second priority – Quality problem The second priority is considered to be the quality problem with outsourced manufacturer Q for the licensed action figure products. The current quality is not acceptable and the order of 80,000 need to be started again. However, it needs to be considered whether the order is retained by outsourced manufacturer Q at a higher price than the current contract or whether Jot should appoint outsourced manufacturer P. 3.3 Third priority – VP proposal This is considered to be the third priority as this is a large contract for this key customer. Additionally, there is a risk that Jot could lose VP as a customer, if Jot were to decline the “own brand” proposal. Jot has never produced branded products for any retailer before, only its own “Jot” brand, so this is a new venture for the company, but this could see high growth in sales volumes. 3.4 Fourth priority – Inventory The revised inventory valuation is considered to be the fourth priority issue. A realistic valuation for these slow-moving products needs to be established to ensure that the accounts for the year ended 31 December 2011 are accurate and reflect realistic valuations. However, the proposed valuations suggested by Boris Hepp, Sales Director, would result in a significant write-down. A SWOT analysis summarising the strengths, weaknesses, opportunities and threats facing Jot is shown in Appendix 1. A PEST analysis is shown in Appendix 2. 4.0 Discussion of the issues facing Jot 4.1 Overview Jot is growing fast and is experiencing problems with some of its outsourced manufacturers. It needs to urgently address the problems caused by the loss of 2 outsourced manufacturers caused by the earthquake and the quality problems on the licensed products. It must maintain the quality of its products to retain and enhance its reputation. Late delivery of products, or poor quality, could result in reputational damage to the Jot brand and have long-term consequences. Jot has seven main customers which account for almost 70% of Jot’s sales and are therefore key players with high power, in respect of Mendelow’s stakeholder analysis. One of these seven main customers is VP, a major toy retailer in the USA. VP has approached Jot with a proposal to produce toys for it under an “own brand” label. This could be a huge opportunity for Jot but also has a range of risks.

© The Chartered Institute of Management Accountants 2012 Page No: 3

4.2 – Manufacturing problems With the volume of products growing, Jot has only 20 outsourced manufacturers. Following the recent earthquake, the factories of 2 of these outsourced manufacturers have been destroyed and cannot be re-built in time in order to meet the required production of products YY and ZZ for 2012. The total volume of units of products YY and ZZ is 150,000 units for 2012. Of the three manufacturers being considered only B has the capacity to supply all of products YY and ZZ. Jot would appear to have three options:

Place the order for all of products YY and ZZ with one manufacturer – but only Manufacturer B has this capacity.

Place the order for product YY with one manufacturer and ZZ with another – but Manufacturer C would only have the capacity to produce all of product ZZ.

Place orders for products YY and ZZ with more than one of the three manufacturers or even spread the orders over all three of the shortlisted manufacturers.

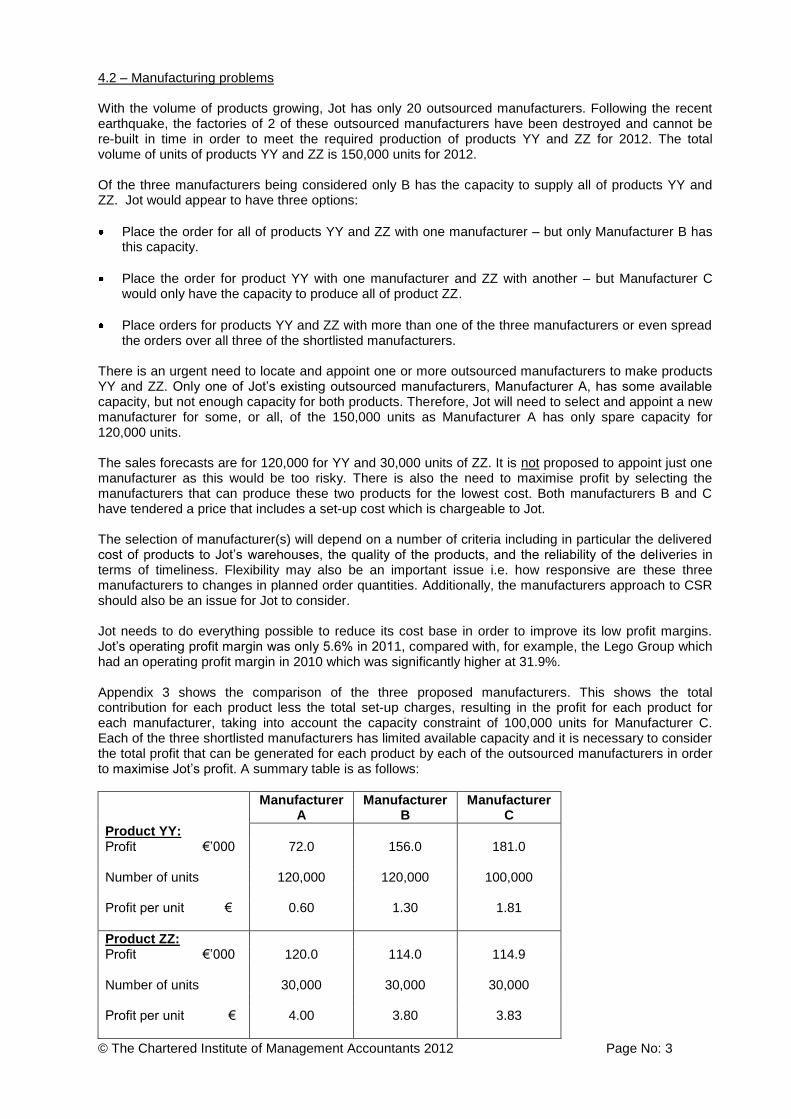

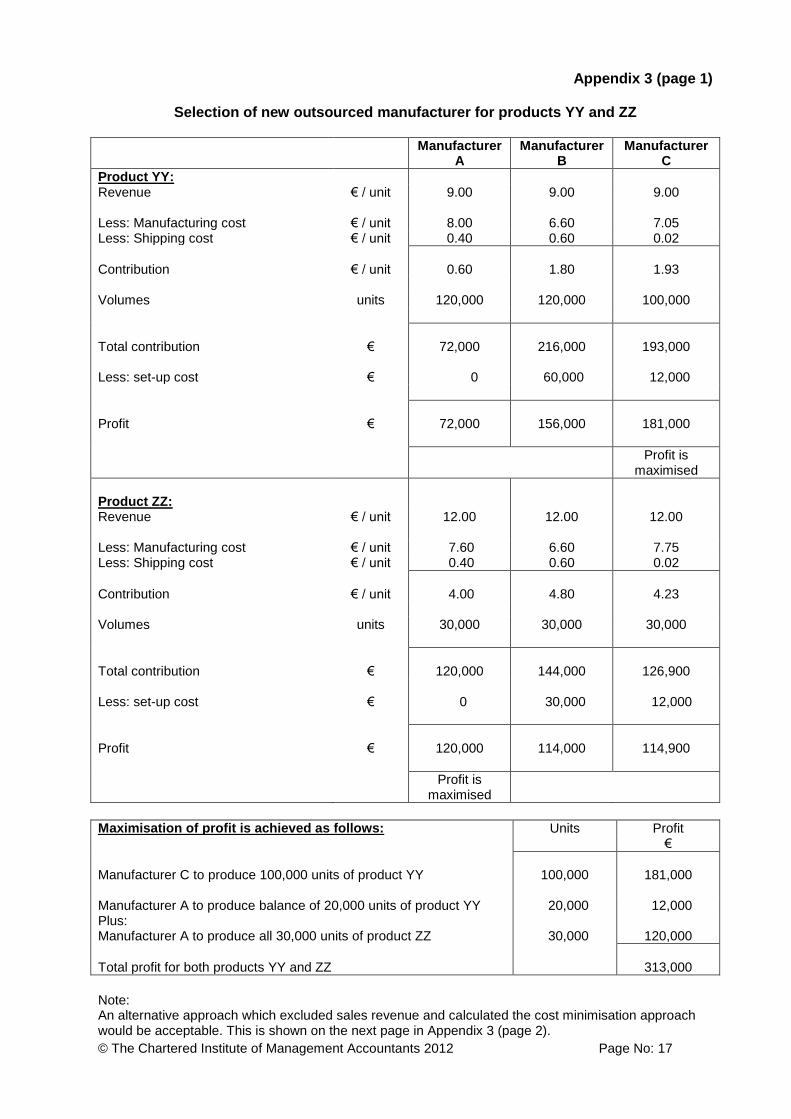

There is an urgent need to locate and appoint one or more outsourced manufacturers to make products YY and ZZ. Only one of Jot’s existing outsourced manufacturers, Manufacturer A, has some available capacity, but not enough capacity for both products. Therefore, Jot will need to select and appoint a new manufacturer for some, or all, of the 150,000 units as Manufacturer A has only spare capacity for 120,000 units. The sales forecasts are for 120,000 for YY and 30,000 units of ZZ. It is not proposed to appoint just one manufacturer as this would be too risky. There is also the need to maximise profit by selecting the manufacturers that can produce these two products for the lowest cost. Both manufacturers B and C have tendered a price that includes a set-up cost which is chargeable to Jot. The selection of manufacturer(s) will depend on a number of criteria including in particular the delivered cost of products to Jot’s warehouses, the quality of the products, and the reliability of the deliveries in terms of timeliness. Flexibility may also be an important issue i.e. how responsive are these three manufacturers to changes in planned order quantities. Additionally, the manufacturers approach to CSR should also be an issue for Jot to consider. Jot needs to do everything possible to reduce its cost base in order to improve its low profit margins. Jot’s operating profit margin was only 5.6% in 2011, compared with, for example, the Lego Group which had an operating profit margin in 2010 which was significantly higher at 31.9%. Appendix 3 shows the comparison of the three proposed manufacturers. This shows the total contribution for each product less the total set-up charges, resulting in the profit for each product for each manufacturer, taking into account the capacity constraint of 100,000 units for Manufacturer C. Each of the three shortlisted manufacturers has limited available capacity and it is necessary to consider the total profit that can be generated for each product by each of the outsourced manufacturers in order to maximise Jot’s profit. A summary table is as follows:

Manufacturer A

Manufacturer B

Manufacturer C

Product YY: Profit €’000 72.0 156.0 181.0 Number of units 120,000 120,000 100,000 Profit per unit € 0.60 1.30 1.81

Product ZZ: Profit €’000 120.0 114.0 114.9 Number of units 30,000 30,000 30,000 Profit per unit € 4.00 3.80 3.83

© The Chartered Institute of Management Accountants 2012 Page No: 4

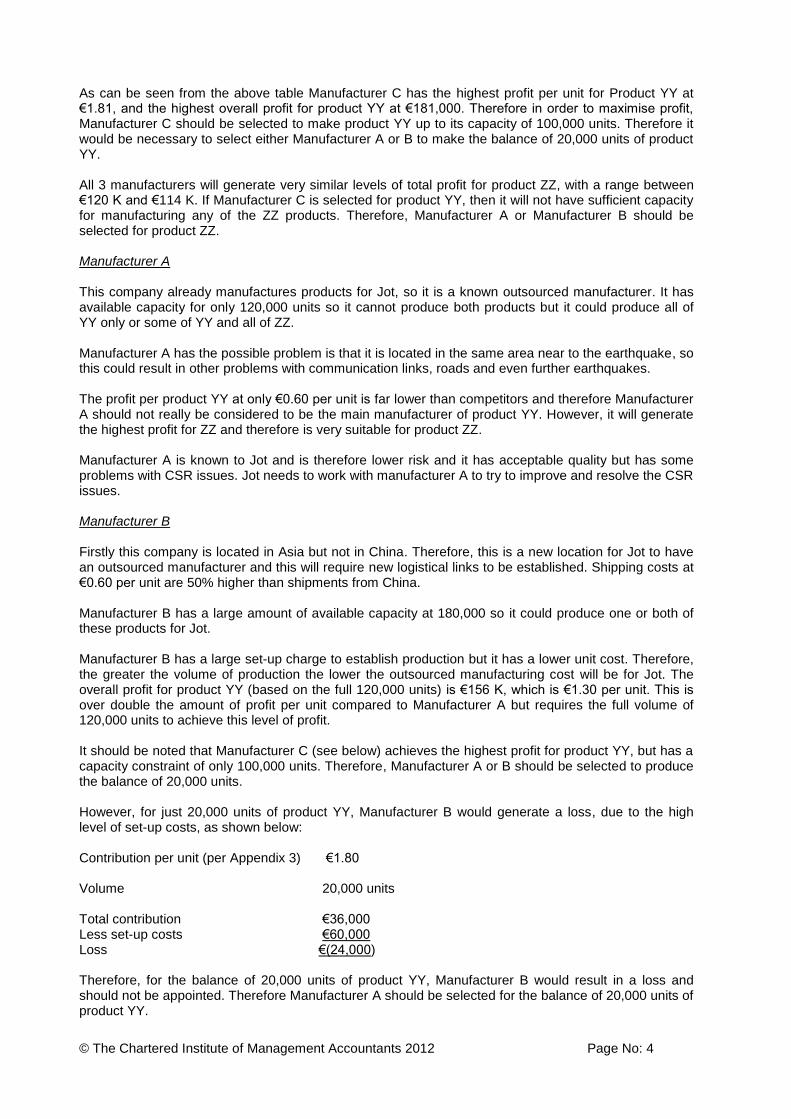

As can be seen from the above table Manufacturer C has the highest profit per unit for Product YY at €1.81, and the highest overall profit for product YY at €181,000. Therefore in order to maximise profit, Manufacturer C should be selected to make product YY up to its capacity of 100,000 units. Therefore it would be necessary to select either Manufacturer A or B to make the balance of 20,000 units of product YY. All 3 manufacturers will generate very similar levels of total profit for product ZZ, with a range between €120 K and €114 K. If Manufacturer C is selected for product YY, then it will not have sufficient capacity for manufacturing any of the ZZ products. Therefore, Manufacturer A or Manufacturer B should be selected for product ZZ. Manufacturer A This company already manufactures products for Jot, so it is a known outsourced manufacturer. It has available capacity for only 120,000 units so it cannot produce both products but it could produce all of YY only or some of YY and all of ZZ. Manufacturer A has the possible problem is that it is located in the same area near to the earthquake, so this could result in other problems with communication links, roads and even further earthquakes. The profit per product YY at only €0.60 per unit is far lower than competitors and therefore Manufacturer A should not really be considered to be the main manufacturer of product YY. However, it will generate the highest profit for ZZ and therefore is very suitable for product ZZ.

Manufacturer A is known to Jot and is therefore lower risk and it has acceptable quality but has some problems with CSR issues. Jot needs to work with manufacturer A to try to improve and resolve the CSR issues. Manufacturer B Firstly this company is located in Asia but not in China. Therefore, this is a new location for Jot to have an outsourced manufacturer and this will require new logistical links to be established. Shipping costs at €0.60 per unit are 50% higher than shipments from China. Manufacturer B has a large amount of available capacity at 180,000 so it could produce one or both of these products for Jot. Manufacturer B has a large set-up charge to establish production but it has a lower unit cost. Therefore, the greater the volume of production the lower the outsourced manufacturing cost will be for Jot. The overall profit for product YY (based on the full 120,000 units) is €156 K, which is €1.30 per unit. This is over double the amount of profit per unit compared to Manufacturer A but requires the full volume of 120,000 units to achieve this level of profit. It should be noted that Manufacturer C (see below) achieves the highest profit for product YY, but has a capacity constraint of only 100,000 units. Therefore, Manufacturer A or B should be selected to produce the balance of 20,000 units. However, for just 20,000 units of product YY, Manufacturer B would generate a loss, due to the high level of set-up costs, as shown below: Contribution per unit (per Appendix 3) €1.80 Volume 20,000 units Total contribution €36,000 Less set-up costs €60,000 Loss €(24,000) Therefore, for the balance of 20,000 units of product YY, Manufacturer B would result in a loss and should not be appointed. Therefore Manufacturer A should be selected for the balance of 20,000 units of product YY.

© The Chartered Institute of Management Accountants 2012 Page No: 5

Manufacturer C Manufacturer C is based in Eastern Europe, which is near to the European sales markets. This would result in Jot “near-shoring” some of its outsourced manufacturing. Near-shoring is defined as the transfer of business processes to a company in a nearby country. Shipping costs are low at only €0.02 per unit. It would be useful for Jot to appoint a more local manufacturer so that the outsourced manufacturer can be more responsive to late increases in sales volumes and could result in Jot carrying lower inventory levels. Manufacturer C has limited capacity at 100,000 and therefore could only produce part of the order for product YY or all of product ZZ. Manufacturer C also has a set-up charge for the production of each product, although its set-up charges are lower than Manufacturer B. Manufacturer C could generate the highest total profit for product YY at €181,000 but it could only manufacture 100,000 units of the required 120,000 units for product YY. The difference between the profit that could be made for product YY by appointing Manufacturer B, rather than Manufacturer C, is €25,000 (as Manufacturer B generates a total profit of €156,000 but this is for the total of 120,000 units). Perhaps the balance of 20,000 units of product YY could be produced by Manufacturer A (as Manufacturer B would be too expensive if the set up charge was incurred for only 20,000 units as shown above). Manufacturer C is only a little more expensive that Manufacturer A for product ZZ but as Manufacturer C is the cheapest for product YY and it has limited capacity, it is proposed that it should not be considered for product ZZ. Manufacturer C has acceptable CSR credentials and produces good quality products. Overall

It seems realistic that Jot should appoint two or even all three of these outsourced manufacturers to ensure that enough products are manufactured to meet sales forecasts and spread the risk of losing production capacity if there were to be any further problems. The costs and profits for all three outsourced manufacturers for product ZZ are very similar. However, as Manufacturer C will result in a far higher profit for product YY than the other two shortlisted outsourced manufacturers, it should definitely be selected to manufacturer product YY up to its maximum capacity. 4.3 - Quality problem Jot appears to have a problem here with the outsourced manufacturing of 80,000 units of the licensed products, with very little time to sort the problem out. Jot requires 80,000 units to be delivered to Europe by the end of May, which is just over 2 months away, and therefore Jot must act quickly. Michael Werner, Operations Director, conducted aggressive negotiations with Manufacturer Q (Q) on price, and the contract price was agreed at €6.00 per unit. However, this has resulted in Q reducing the quality of its products to an unacceptable level. Following further discussions, Q now stated that if Jot agrees to the higher price of €7.00, then it will meet the required quality standards. However, should Jot work with a manufacturer which is producing low quality products due to cost constraints. Can Q be trusted? Jot has already incurred significant costs. Jot has already received 10,000 units for which it owes Q €60,000, and in addition is also liable to pay a further €60,000 for 10,000 units manufactured by Q but not yet shipped. Jot is also liable to pay the license fee of €0.70 for each unit manufactured, resulting in a further cost of €14,000. Therefore the cost of these poor quality products manufactured to date by Q will cost €134,000 in total plus any shipping costs. This is a significant amount and this should influence Jot’s decision as to whether it should work with Q and increase the price to €7.00 per unit or move the outsourced manufacturing for the 80,000 products to another manufacturer.

© The Chartered Institute of Management Accountants 2012 Page No: 6

Jot could try and avoid paying the above €120,000 on the grounds that Q agreed to supply the products in the first place and that the quality is not what was agreed. However, it would appear that Jot could also shoulder some responsibility here. In the first place, Jot’s contract did not specify the quality of the plastic. This could be viewed as an error on Jot’s part. Also it would appear that Jot has been careless in not sampling some of the initial production run of 10,000 units before they were delivered. Although Michael Werner had “signed off the master moulds”, the final products made should also have been inspected by Jot’s quality control team. However Q has manufactured products for Jot before and therefore presumably is aware of Jot’s typical product quality requirements for its toys. It is fairly clear what has happened. In this very competitive toy market, where price competitiveness is one of the major keys to success (and buyers, in this case Jot, have high power in the market place, using Porter’s 5-forces analysis framework), Q was “forced” to agree to a price that was too low at €6.00 a unit, to enable Q to produce the licensed products at an acceptable quality. This is evidenced by Q’s initial quote of €7.00 a unit, and P’s recent quote of €7.10 per unit. However, at the end of the day Q did sign up to this contract but has produced poor quality products. There is plenty of room for Jot to negotiate with Q as no payments have been made to date. Calculations comparing the costs for manufacturers Q and P are shown in Appendix 6. It would appear that Jot has two alternative options: 1. Agree to pay Q €7.00 per unit to produce 80,000 items, replacing the 20,000 units already

manufactured. 2. Place the order for 80,000 units with manufacturer P (P). Jot could probably get P to agree to a price

of €7.00, instead of €7.10, but the concern is whether P could actually make the new moulds for the products and then manufacture and deliver 80,000 products by the end of May 2012.

If Jot chooses to stay with Q, then Jot would be in a better negotiating stance to enable it to reduce the amount due for the 20,000 units of poor quality products that Q it has already produced. A €120,000 write-off would have a big impact on Jot’s 2012 operating profits, currently forecast at €694,000. If Jot decides to move the production of the 80,000 products to P for this work, then the important question is whether the moulds and production can be achieved in the tight deadlines. If the products are not available to Jot’s customers when the film is released than it may miss the sales and then this could result in Jot holding a large inventory of these items.

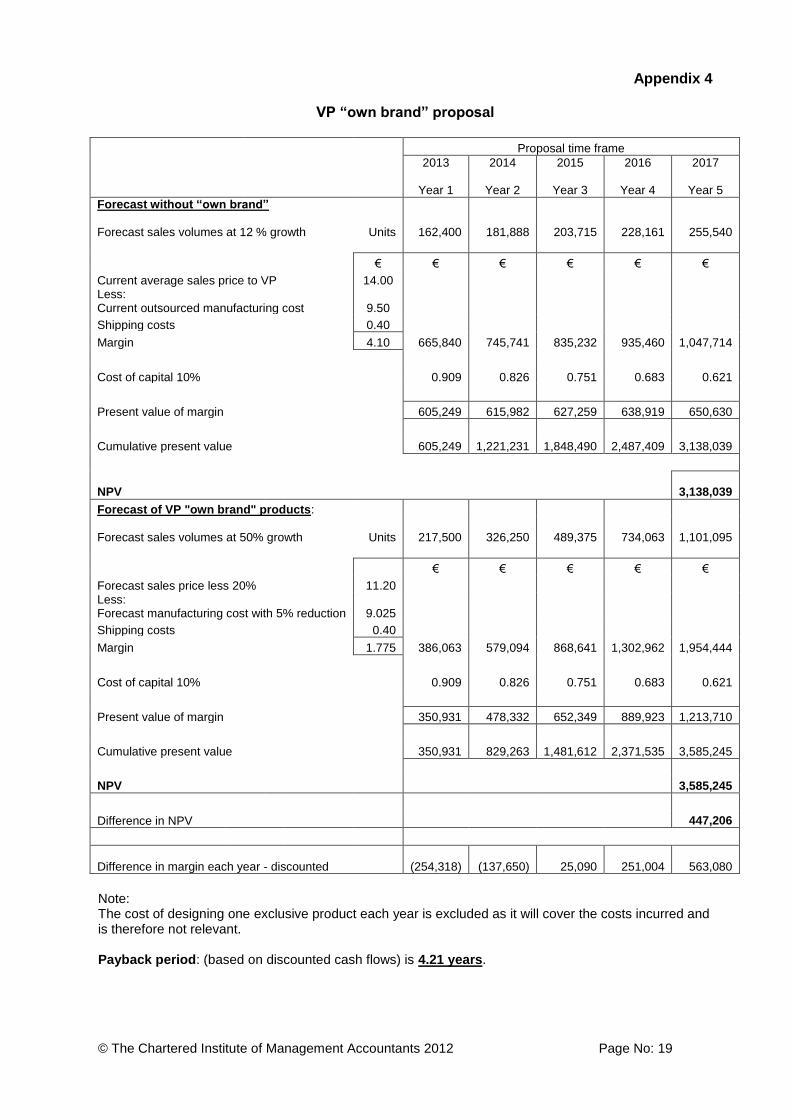

It may be possible for Jot to try to negotiate with Q and perhaps offer to pay Q for some of the faulty production and in exchange, Jot could try to obtain the master moulds for the characters from Q, which have been made by Q (and are owned by Q). If Jot were able to obtain these moulds, then it would save time not having to make new moulds and this would allow Jot to appoint P, and to give the moulds directly to P for it to use for the manufacturing of these products. There is a need for closer quality control and inspection of production at the early stages to eliminate the manufacture of poor quality toys. Jot’s contract with its manufacturers should specify all aspects including the quality of the plastics. Furthermore, all outsourced manufacturing contracts must specify delivery dates and perhaps penalties for late delivery, as it is crucial that delivery of all 80,000 units are made by end May 2012 in order to meet customers orders for the film release in July 2012. 4.4 – VP proposal One of Jot’s seven main customers, VP, has approached Jot with an opportunity to supply products using an “own brand” range of products. This is a great opportunity for Jot and would increase the volume of sales significantly, from the current level of 145,000 units to a forecast level of over 1,100,000 units by 2017. The proposal is for a 5 year period only. VP is one of Jot’s seven main customers and therefore holds significant power over Jot (Porter’s 5 forces).

© The Chartered Institute of Management Accountants 2012 Page No: 7

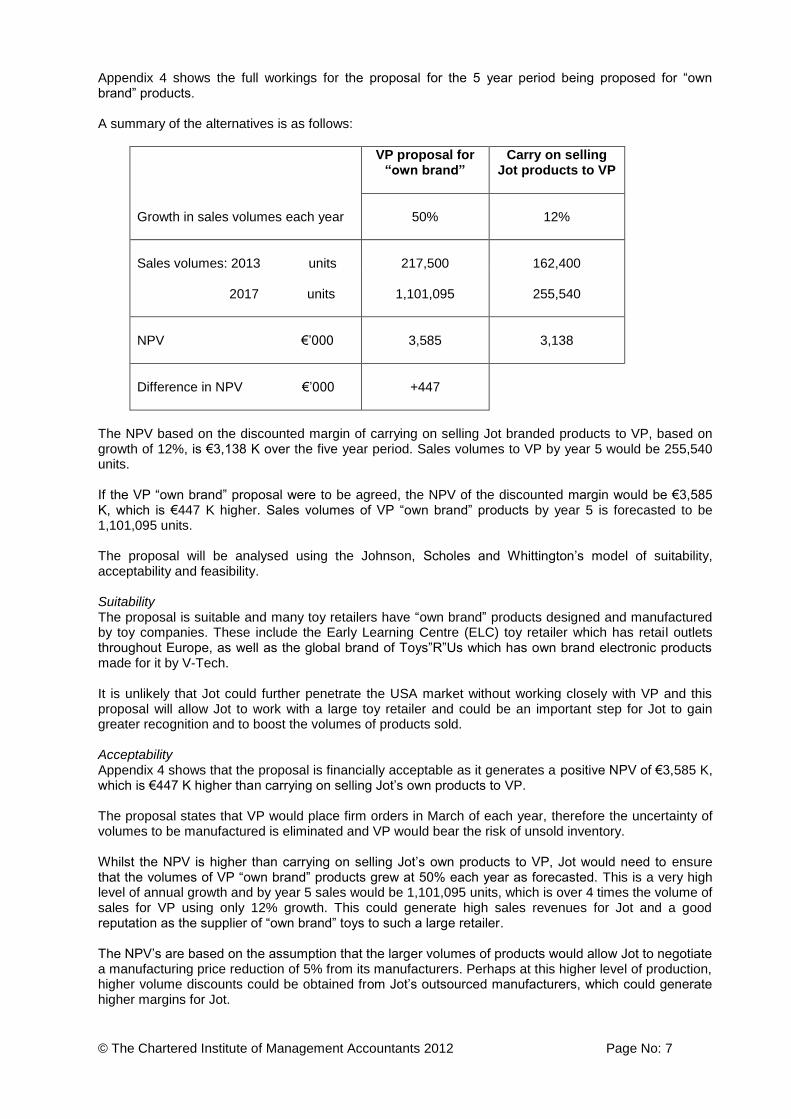

Appendix 4 shows the full workings for the proposal for the 5 year period being proposed for “own brand” products. A summary of the alternatives is as follows:

VP proposal for “own brand”

Carry on selling Jot products to VP

Growth in sales volumes each year

50%

12%

Sales volumes: 2013 units

217,500

162,400

2017 units

1,101,095

255,540

NPV €’000

3,585

3,138

Difference in NPV €’000

+447

The NPV based on the discounted margin of carrying on selling Jot branded products to VP, based on growth of 12%, is €3,138 K over the five year period. Sales volumes to VP by year 5 would be 255,540 units. If the VP “own brand” proposal were to be agreed, the NPV of the discounted margin would be €3,585 K, which is €447 K higher. Sales volumes of VP “own brand” products by year 5 is forecasted to be 1,101,095 units. The proposal will be analysed using the Johnson, Scholes and Whittington’s model of suitability, acceptability and feasibility. Suitability The proposal is suitable and many toy retailers have “own brand” products designed and manufactured by toy companies. These include the Early Learning Centre (ELC) toy retailer which has retail outlets throughout Europe, as well as the global brand of Toys”R”Us which has own brand electronic products made for it by V-Tech. It is unlikely that Jot could further penetrate the USA market without working closely with VP and this proposal will allow Jot to work with a large toy retailer and could be an important step for Jot to gain greater recognition and to boost the volumes of products sold. Acceptability Appendix 4 shows that the proposal is financially acceptable as it generates a positive NPV of €3,585 K, which is €447 K higher than carrying on selling Jot’s own products to VP. The proposal states that VP would place firm orders in March of each year, therefore the uncertainty of volumes to be manufactured is eliminated and VP would bear the risk of unsold inventory. Whilst the NPV is higher than carrying on selling Jot’s own products to VP, Jot would need to ensure that the volumes of VP “own brand” products grew at 50% each year as forecasted. This is a very high level of annual growth and by year 5 sales would be 1,101,095 units, which is over 4 times the volume of sales for VP using only 12% growth. This could generate high sales revenues for Jot and a good reputation as the supplier of “own brand” toys to such a large retailer. The NPV’s are based on the assumption that the larger volumes of products would allow Jot to negotiate a manufacturing price reduction of 5% from its manufacturers. Perhaps at this higher level of production, higher volume discounts could be obtained from Jot’s outsourced manufacturers, which could generate higher margins for Jot.

© The Chartered Institute of Management Accountants 2012 Page No: 8

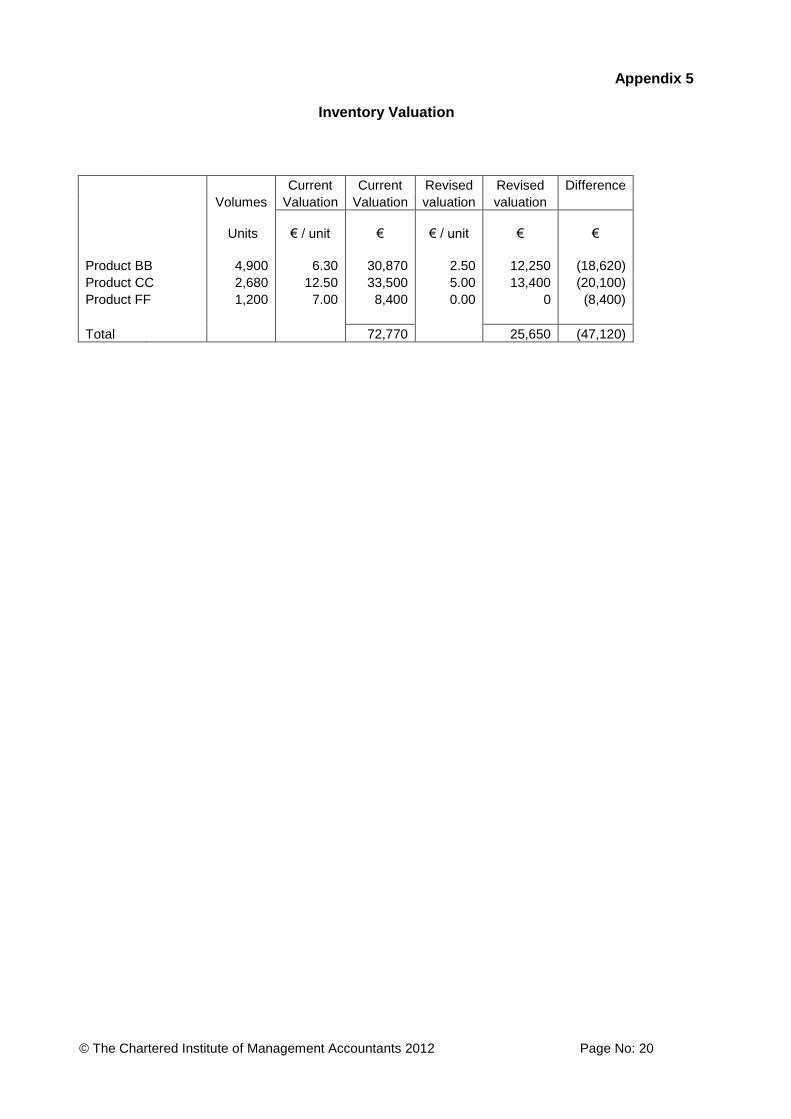

Feasibility The proposal is feasible as Jot has the experience and skills to produce a range of products using its outsourced manufacturers. Jot also has the skills to design and produce one exclusive product for VP each year. Jot would need to ensure that the cost of design and prototypes did not exceed the fixed charge of €0.25 million each year. The proposal is that Jot would design an exclusive product for VP each year, but this could detract from new products developed by Jot for its other customers. How will VP choose the new product? Would it work with one of Jot’s designers? Jot would not wish to allow VP to have its best new product exclusively for VP. In respect of the price reduction agreed with VP for “own brand” products, perhaps Jot should negotiate a price reduction which is based on a sliding scale depending on the volumes of “own brand” products ordered rather than a flat 20%. It is suggested that Jot tries to negotiate the selling price reduction from 20% down to between 15% and 18% or to vary the price discount depending on volumes. Additionally, perhaps a minimum volume of units for 2013 and 2014 should be written into the contract with VP. The proposal only generates a positive NPV from year 3, so it is the first 2 years and the volume increases of 50% which are crucial here. Perhaps the contract could have minimum volumes for the first 2 years, to protect Jot. In terms of feasibility Jot would appear to be able to finance this growth in sales from operating profits. However, care would have to be taken with cash flow management caused by the build up of inventories for VP before the high quarter 4 sales period. Jot also needs to consider the cash flow implications for the design and pre-production cost for designing an exclusive product for VP each year. Would this have to be initially funded by Jot, or could an up-front payment from VP be negotiated? The case material states that VP wishes to increase its range of own brand products and therefore if Jot were to decline the VP “own brand” proposal, then Jot runs the risk of losing VP as a customer entirely. It is possible that VP could select a different toy company to produce “own brand” products for it, if Jot declined this proposal. VP is Jot’s main customer in the USA with over 90% of its sales and the loss of this single customer would be significant, as sales to VP in 2011 were over €2.0 million (20.3% of Jot’s total sales). A disadvantage of the “own brand” proposal is that Jot would have to manage a more complex manufacturing process with two brands (the “Jot” brand and the “VP” brand) and different packaging for each branded product. A potential disadvantage for Jot of VP’s proposal would be a much lower brand awareness of Jot’s name with consumers in the USA, since these consumers will only know the products as being VP branded products. Furthermore, this proposal would make Jot’s plans to expand further into the USA market difficult and could result in the loss of sales to other USA customers. VP currently generates 90% of sales to the USA and if it were to retail identical products using the VP “own brand” label, then it may make it difficult for other retailers to compete. Therefore, potentially Jot could lose sales from other small USA customers worth €222 K (VP = €2.0 million / 90% x 10%). At Jot’s average gross margin of 32.3% (plan for 2012) this potential loss of sales could result in a fall in gross margin of around €72 K each year. Overall, this is a good proposal which could see Jot’s sales revenue from this customer rise from €2.0 million now to almost €12.4 million in 5 years time (1,105,095 x €11.20 per product) based on volume rises of 50% per year for these “own brand” products. This is a significant proposal which demonstrates that this key customer has confidence in Jot’s products in the competitive USA market. 4.5 - Inventory This issue has both a business and an ethical aspect. From a business point of view Jot would appear to be facing a potential further inventory write-down of €47,120, as shown in Appendix 5. This would be a significant figure compared with the €351,000 profit before tax shown in the unaudited accounts for the year ended 31 December 2011.

© The Chartered Institute of Management Accountants 2012 Page No: 9

The external auditor is insisting that this adjustment must be made, and unless Jot can come up with a good argument as to why it should not, then this adjustment will have to be made. Jot cannot risk having a “qualified” audit report. A “qualified” audit report is issued when the external auditors encounter a situation which does not comply with generally accepted accounting principles. It is particularly important for Jot to get a “clean” audit report, as Jot is so reliant on bank finance for support. It is likely that the company’s bankers would automatically request a copy of Jot’s annual accounts each year. However, the question that needs to be asked is why Boris Hepp, Sales Director, has not offered these products to Jot’s existing customers at reduced prices, which has been done in previous years. Inventory valuations must be realistic and should reflect the lower of the cost or net realisable value, i.e. at what price Jot could sell these products to any of its customers. Instead of arguing as to whether Boris Hepp’s valuations are correct or too high or too low, it is suggested that the sales department speaks to Jot’s customers urgently (perhaps just the seven main customers) and establish:

Whether any of the seven main customers is interesting in buying any (or all) of the remaining inventory for these 3 products.

What price they are willing to pay for these products.

If any of the customers is interested in buying these products, then a formal letter of intent to buy should be obtained as proof of intention (or a purchase order from Jot’s customers) and this price can be used for inventory valuation purposes.

It is unlikely that the 1,200 units of product FF are really “worthless” as it is probable that they could be sold at a substantially reduced price. Only if none of Jot’s customers is interested in product FF, should it then be written down to zero. Jot should use what management information it possesses in respect of which customers have previously purchased products BB, CC and FF and to ask these customers if they are interested in purchasing Jot’s remaining inventory. It is suggested that Boris Hepp and his sales department are given a deadline of 1 week to contact customers to see if any customers are interested in procuring these products and at what price. After the 1 week deadline, then Tani Grun, Finance and IT Director, should meet with Boris Hepp to jointly agree on realistic values for each of these 3 products and to establish how many can be sold and at what price. In future, inventory valuations should occur on a regular basis and Boris Hepp should not be advising revised valuation figures directly to auditors before he has discussed and agreed the valuations with Tani Grun. It is recommended that Boris Hepp be reminded of the importance of accuracy in respect of the data being used for Jot’s financial statements. The level of profitability is a key indicator for business valuation purposes and for securing loan finance. An incorrect inventory valuation could have far reaching effects. The ethical aspects of Tani Grun telling Boris Hepp to tell the auditors that his previous valuations were incorrect will be discussed in the Ethics section of this report below. 5.0 Ethical issues and recommendations on ethical issues 5.1 Range of ethical issues facing Jot There are a range of ethical issues facing Jot including the following:

1. Inventory – pressure being put on Boris Hepp, Sales Director 2. Incorrect marketing material 3. Pressure that was put on outsourced manufacturer Q to reduce its original tender price

© The Chartered Institute of Management Accountants 2012 Page No: 10

5.2 – Inventory - pressure being put on Boris Hepp, Sales Director 5.2.1 Why this is an ethical issue Boris Hepp, Sales Director, should establish a realistic valuation for these 3 products based upon feedback from customers after establishing whether they would buy any of these older products. Tani Grun should not be allowed to unduly influence his valuation. She should not “instruct him to revise the valuations to a higher level and tell the auditors that his previous valuations were incorrect”. This is unprofessional and unethical behaviour for a Finance Director. 5.2.2 Recommendations for this ethical issue It is recommended that Boris Hepp speaks to Jot’s seven main customers to see whether any are interested in buying any of these products and at what price they would buy them. The inventory should be valued at the lower of the current written-down price or the possible selling price, if this is even lower. If the sales of these three products cannot be secured, then the product valuation should be written-off. Tani Grun should be disciplined for trying to put pressure on a fellow director concerning the valuation of the inventory. She should attend a training course on the responsibilities of a company director. 5.3 – Incorrect marketing material 5.3.1 Why this is an ethical issue The marketing material and packaging is knowingly making claims for the product to possess functions that the product does not have. This is a poor indication of the values of Sonja Rosik, Marketing Director, that she remains unconcerned and is trying to allow the product to be sold, even though she is aware of the exaggerated claims for the product. This demonstrates a lack of integrity and this could damage Jot’s reputation. It is unfair for Jon Grun, Managing Director, to ask Sonja Rosik to resign. However, she should be disciplined and perhaps given a written warning. 5.3.2 Recommendations for this ethical issue It is recommended that the product packaging and marketing material should be amended and reprinted. It is recommended that sales orders are not despatched to customers until the packaging and the marketing material is amended to ensure that only the true functions of the product are included. It is recommended that Sonja Rosik is disciplined and sent on a training course to ensure that she fully understands the responsibilities of being a director and the importance of truthful and accurate product data. Jot should also formalise its CSR charter and ensure that all employees are aware of the importance of truthful marketing material. 5.4 – Pressure that was put on outsourced manufacturer Q to reduce its original tender price

5.4.1 Why this is an ethical issue Whilst this could be considered to be normal business practice to negotiate on price, excessive pressure that has been put on outsourced manufacturers is not ethical or a sustainable practice.

© The Chartered Institute of Management Accountants 2012 Page No: 11

Michael Werner has pressurised outsourced manufacturer Q into reducing its tender price for the 80,000 units of the licensed action figures, down from €7.00 to €6.00. The reduced price has now resulted in poor quality of production. A different outsourced manufacturer, P, has now tendered a price of €7.10. This indicates that Q’s price of €7.00 was realistic. Jot should not exert undue pressure to reduce tender prices. 5.4.2 Recommendations for this ethical issue It is recommended that Jot negotiates with all of its outsourced manufacturers on price but that it should not put significant pressure on them to reduce prices as this could have a detrimental effect on the final quality of the manufactured products. It is recommended that tenders should be sent to at least three outsourced manufacturers for each product and that fair negotiations take place. 6.0 Recommendations 6.1 – Manufacturing problems 6.1.1 Recommendation It is recommended that Manufacturer C, in Eastern Europe, is appointed to manufacture 100,000 units of product YY as this maximises the profit for Jot. It is also recommended that the balance of 20,000 units of product YY should be produced by Manufacturer A, as Manufacturer C only has available capacity for 100,000 units. It is recommended that Manufacturer B, based in a different Asian country, should be appointed to manufacture all 30,000 units of product ZZ. 6.1.2 Justification This combination of products and manufacturers will generate a total margin for these products of €307,000, which is just lower than the profit maximisation option. This compares to a margin of only €270,000 if Manufacturer B were to be appointed for both products, which is a reduction of €37,000 compared to the recommended mix which will generate €307,000. Neither Manufacturer A or C has the capacity to produce both products. Manufacturer C is the cheapest for product YY and therefore should be selected for this high volume product up to the level of its capacity constraint of 100,000 units. Using Manufacturer C also has the advantage of dealing with an outsourced manufacturer with very good quality, short transportation (based in Europe) and an acceptable CSR status. The selection of Manufacturer A for the balance of 20,000 units is due to the lack of set up costs, which make Manufacturer B too expensive for only 20,000 units of product YY. Whilst the cheapest manufacturer of product ZZ is Manufacturer A, with a total profit of €120,000, it is recommended that Manufacturer B is appointed. This will result in a slightly lower total profit for this product of €114,000, which is only €6,000 lower. However the justification for this recommendation to appoint Manufacturer B, rather than Manufacturer A, is:

Jot should widen its choice of outsourced manufacturers as it has growing volumes of sales.

Manufacturer B is located away from the earthquake area in China, should there be any further natural disasters.

It will give Jot an opportunity to work with a manufacturer in a different Asian country.

The difference in the profit between Manufacturer A and B is only €6,000.

© The Chartered Institute of Management Accountants 2012 Page No: 12

The choice of using all three of the shortlisted manufacturers, A, B and C, will generate a profit of €307,000 which is only €6,000 lower than the profit maximisation option shown in Appendix 3. 6.1.3 Actions to be taken 1. It is recommended that before the order for product ZZ is placed with Manufacturer B that meetings

should be held with the company to discuss Jot’s concerns over its CSR status. The rationale is that Jot would not wish to damage its reputation by dealing with an outsourced manufacturer with known CSR problems without making some clear attempt at resolving the situation. It is suggested that Jot follow The Lego Group’s approach of requiring all its outsourced manufacturers to sign up to a Code of Conduct covering issues such as child labour and health and safety.

2. Jot should work closely to resolve CSR issues with Manufacturer A. 3. Jot should monitor product quality closely with these two new outsourced manufacturers, B and C. 4. Jot should establish shipping and transportation links with its outsourced global logistics company

for the transportation of goods from the new Asian country and the Eastern European country to Jot’s warehouses.

6.2 – Quality problem 6.2.1 Recommendation It is recommended that the contract with outsourced manufacturer Q is terminated. It is recommended that outsourced manufacturer P is appointed to produce the 80,000 units of the licensed products. 6.2.2 Justification Q has produced poor quality products at the current contracted price of €6.00 per unit. If Jot were to agree to increase the price paid to €7.00 per unit, there is no guarantee that it will deliver the required quality of product. Q appears not to be a reliable and trusted manufacturer and Jot should not continue to work with a company which does not deliver the right quality product at the price specified in the agreed contract. Q allowed the contract price negotiations to happen and it signed a contract at the price of €6.00 per unit and it should have forewarned Jot of the ways in which it would cut costs and the impact this could have on quality. It is recommended that Jot negotiates what should be paid to Q for the 20,000 units it has already manufactured to date, which are of poor quality. It is unfair for Jot to pay the full contracted cost of €120K (20,000 x €6.00). Perhaps Jot can negotiate to pay part of this in exchange for obtaining the master moulds from Q. The justification for recommending that outsourced manufacturer P is appointed is that quality is an important aspect of Jot’s products, despite the slightly higher cost per unit of €7.10. Perhaps this could be negotiated down slightly to €7.00 to match Q’s revised price. If the master moulds cannot be obtained from Q quickly, then P will have to make them and these will need to be approved to ensure that they are accurate and meet the licensing terms for each character. 6.2.3 Actions to be taken 1. Negotiations with Q following the termination of the contract to agree whether Q will give the master

moulds to Jot, or not, in lieu of Jot agreeing to make part payment for the €120,000 that is due.

© The Chartered Institute of Management Accountants 2012 Page No: 13

2. Alternatively, if Q will not give the master moulds to Jot, then a reduced payment by Jot should be negotiated for the poor quality products. A cost of 25% of the value due to Q is suggested i.e. €30,000 with the ability to negotiate up to 50% of the value. Q would not wish to take the case to court as Q is at fault in the quality of the production. Therefore, negotiations on what level of payment should be made, should take place urgently.

3. A contract with P should be prepared urgently, and the contract should include quality issues and

specify the quality of the plastics to be used, as well as an agreed and realistic delivery schedule. 4. It is important that all 80,000 units of these products are available to Jot by the end of May 2012, to

allow time to deliver the products to its customers to coincide with the release of the children’s film and therefore the contract should specify delivery dates and include a penalty for late delivery.

6.3 - VP proposal 6.3.1 Recommendation It is recommended that the VP “own brand” proposal be accepted. It is recommended that Jot tries to negotiate the selling price reduction from 20% down to between 15% and 18% or to vary the price discount depending on volumes ordered by VP each year. It is further recommended that the forecast growth of 50% be written into the contract, or the minimum number of products to be bought by VP for years 1 and 2 are written into the contract, in order to protect Jot from lower levels of orders from VP. 6.3.2 Justification By accepting the VP “own brand” proposal, this will allow Jot to generate high growth in sales volumes and could allow significant revenue growth in the competitive USA market. If Jot were to decline the VP proposal, then it could lose its major US customer and €2.0 million sales revenue, as VP could choose a competitor to make its “own brand” products. The risk of losing VP is too great to decline this proposal. The rationale is also that the VP “own brand” proposal has a higher NPV than that from carrying on selling Jot products, with the difference in NPV’s over 5 years at €447 K. The rationale for the recommendation concerning the pricing structure proposed by VP is because Jot will make significantly lower profits in both 2013 and 2014 than it would have done without the “own brand” proposal. Jot needs to protect itself from overly ambitious sales projections, especially in the first two years. 6.3.3 Actions to be taken 1. Jot should enter into negotiations with VP regarding the accuracy of the ambitious sales growth

targets, with a view to having a sliding scale of price reductions up to 20% only if the 50% annual growth targets are achieved.

2. Jot should negotiate with VP concerning a minimum volume of products to be ordered in years 1

and 2. 3. Jot should negotiate with VP regarding the timing of the payment for the annual €0.25 million for

designing an exclusive product for VP. 4. Before Jot makes its final decision on the “own brand” proposal it should discusses this major

strategic initiative with its bankers. The rationale for this is to get the bank “on-board” in the event of a further overdraft facility being required to fund the possible extra working capital requirements caused by the projected high sales growth.

© The Chartered Institute of Management Accountants 2012 Page No: 14

6.4 – Inventory 6.4.1 Recommendation It is recommended that Boris Hepp should speak to Jot’s current customers, especially Jot’s seven main customers, to see whether they would be interested in purchasing some or all of these products at reduced prices. It is recommended that a deadline for this contact with Jot’s customers to be made is one week from today. After this one week of contact with customers, it is recommended that Tani Grun should meet with Boris Hepp to establish what volume and at what price any of the inventory for products BB, CC and FF could be sold. They should discuss and agree on a realistic valuation for any remaining unsold inventory for each of these 3 product lines or write off the entire value of any remaining inventory if it cannot be sold. The revised valuation, after establishing what volume of these three products can be sold, and at what price, should be adjusted in the accounts for last financial year. 6.4.2 Justification The justification is that Boris Hepp should make efforts to sell the remaining items of inventory for these three products rather than just write-down the value of inventory. After customers have been contacted to try to sell some (or all) of the inventory for these products, then the remaining inventory should be written-down, or potentially written-off entirely. The inventory value should be a realistic value of what these products can be sold for. If they cannot be sold, then they should be written-off so that the Statement of Financial Position is not overstated. 6.4.3 Actions to be taken 1. Boris Hepp to contact Jot’s customers to try to sell the remaining inventory of these three products. 2. Any unsold inventory should be written down or written off, depending on whether it is realistic that

these products could be sold in the future. 3. Tani Grun should liaise with the external auditors to advise on the what actions are being taken to

sell these old product lines. 4. Tani Grun to finalise the inventory write-down or write-off, after customers have been contacted, and

then adjust last year’s accounts for the revised inventory valuation. 7.0 Conclusions Jot’s management team has been very successful since Jot was established in 1998 and the business has grown considerably. It has continued to be innovative and create new toys and has expanded its geographical markets substantially. There is every reason to consider that Jot will continue to be successful and profitable but it needs to urgently address the problems with, and shortage of, its outsourced manufacturers. Jot’s management team needs to ensure that it works closely with its outsourced manufacturers so that a good business understanding is established and that the outsourced manufacturers can produce the right quality products at the right time, for Jot to supply to its customers. This will allow Jot’s management team to concentrate on the business of designing and selling a range of innovative toys.

© The Chartered Institute of Management Accountants 2012 Page No: 15

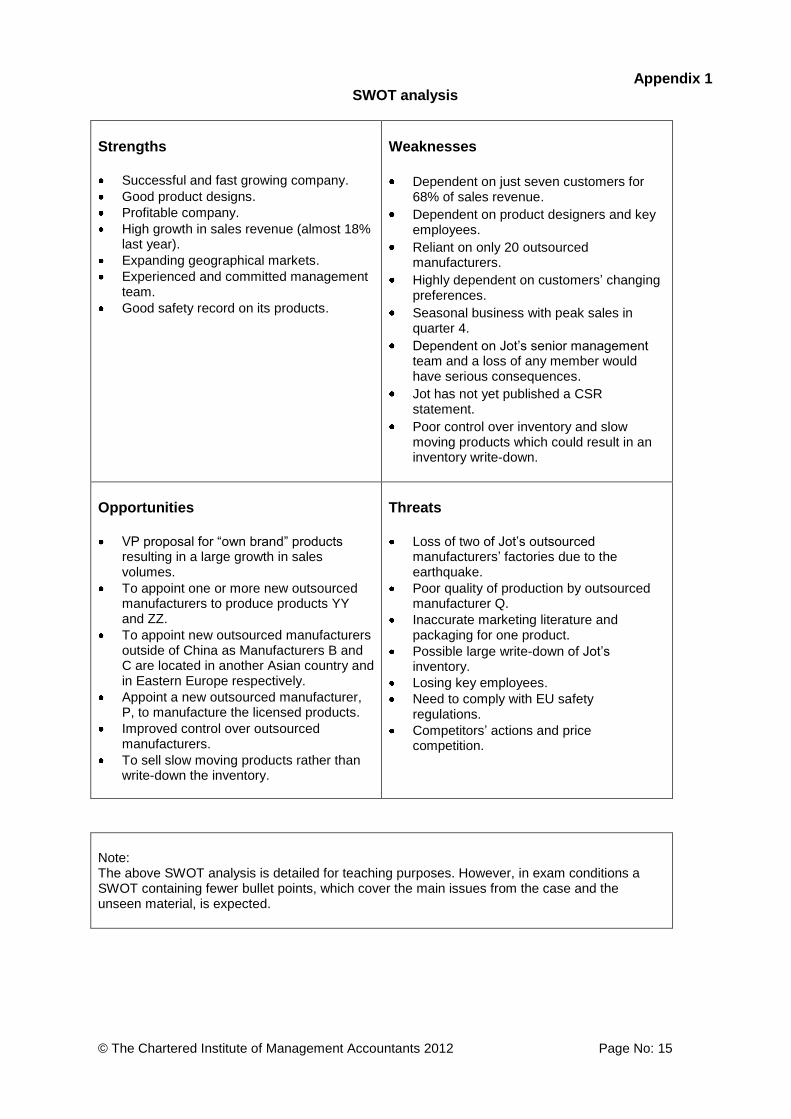

Appendix 1 SWOT analysis

Strengths Successful and fast growing company.

Good product designs.

Profitable company.

High growth in sales revenue (almost 18% last year).

Expanding geographical markets.

Experienced and committed management team.

Good safety record on its products.

Weaknesses

Dependent on just seven customers for 68% of sales revenue.

Dependent on product designers and key employees.

Reliant on only 20 outsourced manufacturers.

Highly dependent on customers’ changing preferences.

Seasonal business with peak sales in quarter 4.

Dependent on Jot’s senior management team and a loss of any member would have serious consequences.

Jot has not yet published a CSR statement.

Poor control over inventory and slow moving products which could result in an inventory write-down.

Opportunities VP proposal for “own brand” products

resulting in a large growth in sales volumes.

To appoint one or more new outsourced manufacturers to produce products YY and ZZ.

To appoint new outsourced manufacturers outside of China as Manufacturers B and C are located in another Asian country and in Eastern Europe respectively.

Appoint a new outsourced manufacturer, P, to manufacture the licensed products.

Improved control over outsourced manufacturers.

To sell slow moving products rather than write-down the inventory.

Threats Loss of two of Jot’s outsourced

manufacturers’ factories due to the earthquake.

Poor quality of production by outsourced manufacturer Q.

Inaccurate marketing literature and packaging for one product.

Possible large write-down of Jot’s inventory.

Losing key employees.

Need to comply with EU safety regulations.

Competitors’ actions and price competition.

Note: The above SWOT analysis is detailed for teaching purposes. However, in exam conditions a SWOT containing fewer bullet points, which cover the main issues from the case and the unseen material, is expected.

© The Chartered Institute of Management Accountants 2012 Page No: 16

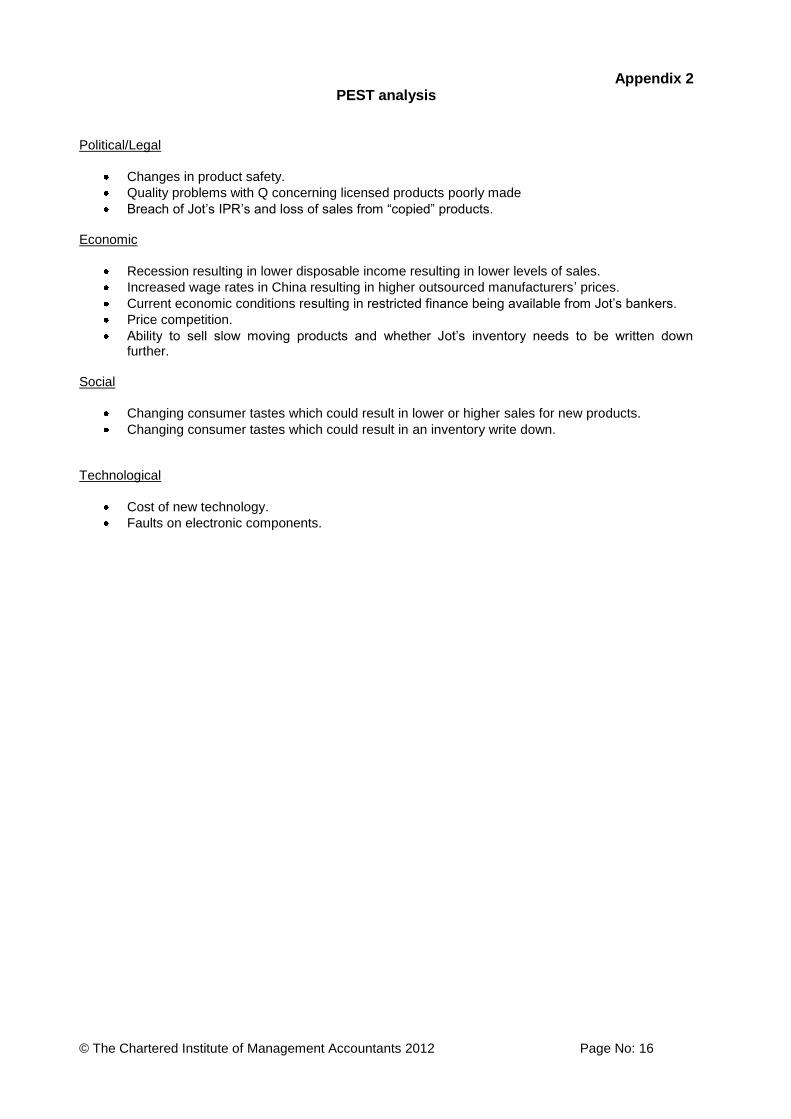

Appendix 2 PEST analysis

Political/Legal

Changes in product safety.

Quality problems with Q concerning licensed products poorly made

Breach of Jot’s IPR’s and loss of sales from “copied” products. Economic

Recession resulting in lower disposable income resulting in lower levels of sales.

Increased wage rates in China resulting in higher outsourced manufacturers’ prices.

Current economic conditions resulting in restricted finance being available from Jot’s bankers.

Price competition.

Ability to sell slow moving products and whether Jot’s inventory needs to be written down further.

Social

Changing consumer tastes which could result in lower or higher sales for new products.

Changing consumer tastes which could result in an inventory write down. Technological

Cost of new technology.

Faults on electronic components.

© The Chartered Institute of Management Accountants 2012 Page No: 17

Appendix 3 (page 1)

Selection of new outsourced manufacturer for products YY and ZZ

Manufacturer A

Manufacturer B

Manufacturer C

Product YY: Revenue € / unit 9.00 9.00 9.00

Less: Manufacturing cost € / unit 8.00 6.60 7.05 Less: Shipping cost € / unit 0.40 0.60 0.02

Contribution

€ / unit

0.60

1.80

1.93

Volumes units 120,000 120,000 100,000

Total contribution

€

72,000

216,000

193,000

Less: set-up cost

€

0

60,000

12,000

Profit

€

72,000

156,000

181,000

Profit is maximised

Product ZZ:

Revenue € / unit 12.00 12.00 12.00

Less: Manufacturing cost € / unit 7.60 6.60 7.75 Less: Shipping cost € / unit 0.40 0.60 0.02

Contribution

€ / unit

4.00

4.80

4.23

Volumes units 30,000 30,000 30,000

Total contribution

€

120,000

144,000

126,900

Less: set-up cost

€

0

30,000

12,000

Profit

€

120,000

114,000

114,900

Profit is maximised

Maximisation of profit is achieved as follows: Units Profit €

Manufacturer C to produce 100,000 units of product YY

100,000

181,000

Manufacturer A to produce balance of 20,000 units of product YY 20,000 12,000 Plus: Manufacturer A to produce all 30,000 units of product ZZ

30,000

120,000

Total profit for both products YY and ZZ

313,000

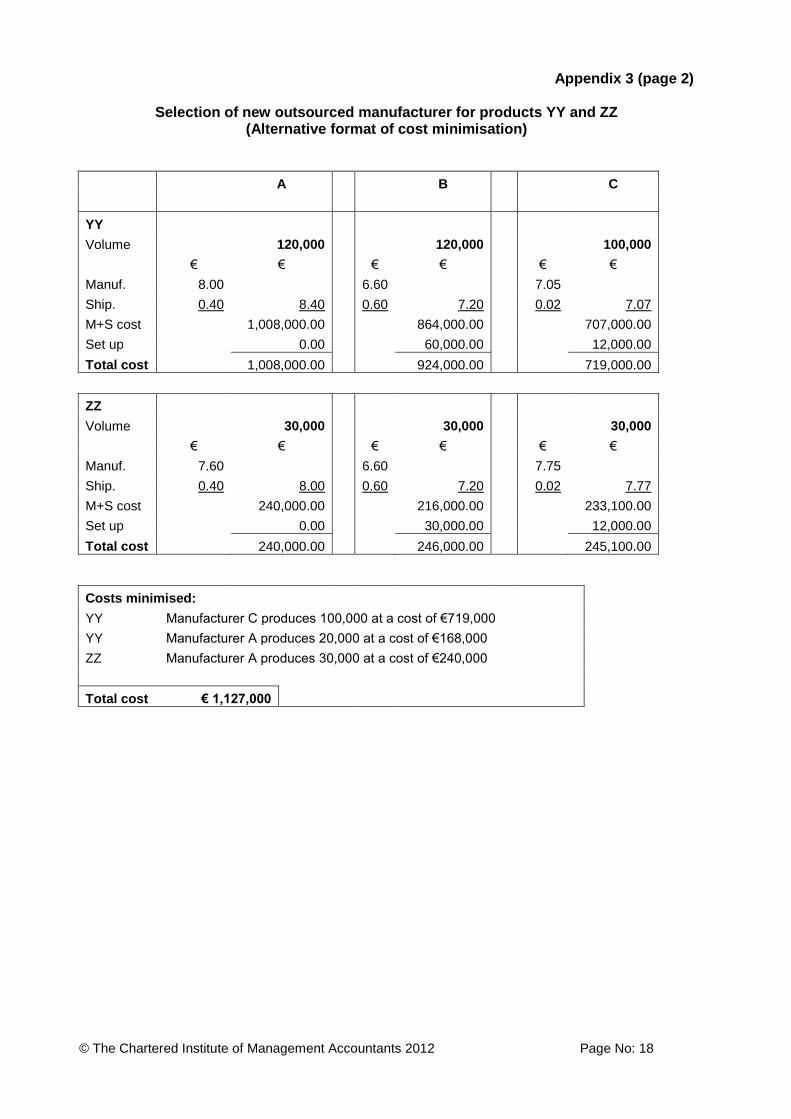

Note: An alternative approach which excluded sales revenue and calculated the cost minimisation approach would be acceptable. This is shown on the next page in Appendix 3 (page 2).

© The Chartered Institute of Management Accountants 2012 Page No: 18

Appendix 3 (page 2)

Selection of new outsourced manufacturer for products YY and ZZ (Alternative format of cost minimisation)

A B C

YY

Volume 120,000 120,000 100,000

€ € € € € €

Manuf. 8.00 6.60 7.05

Ship. 0.40 8.40 0.60 7.20 0.02 7.07

M+S cost 1,008,000.00 864,000.00 707,000.00

Set up 0.00 60,000.00 12,000.00

Total cost 1,008,000.00 924,000.00 719,000.00

ZZ

Volume 30,000 30,000 30,000

€ € € € € €

Manuf. 7.60 6.60 7.75

Ship. 0.40 8.00 0.60 7.20 0.02 7.77

M+S cost 240,000.00 216,000.00 233,100.00

Set up 0.00 30,000.00 12,000.00

Total cost 240,000.00 246,000.00 245,100.00

Costs minimised:

YY Manufacturer C produces 100,000 at a cost of €719,000

YY Manufacturer A produces 20,000 at a cost of €168,000

ZZ Manufacturer A produces 30,000 at a cost of €240,000

Total cost € 1,127,000

© The Chartered Institute of Management Accountants 2012 Page No: 19

Appendix 4

VP “own brand” proposal

Proposal time frame

2013

Year 1

2014

Year 2

2015

Year 3

2016

Year 4

2017

Year 5

Forecast without “own brand”

Forecast sales volumes at 12 % growth

Units

162,400

181,888

203,715

228,161

255,540

€ € € € € €

Current average sales price to VP 14.00 Less: Current outsourced manufacturing cost 9.50

Shipping costs 0.40

Margin 4.10 665,840 745,741 835,232 935,460 1,047,714

Cost of capital 10% 0.909 0.826 0.751 0.683 0.621

Present value of margin 605,249 615,982 627,259 638,919 650,630

Cumulative present value 605,249 1,221,231 1,848,490 2,487,409 3,138,039

NPV

3,138,039

Forecast of VP "own brand" products:

Forecast sales volumes at 50% growth

Units

217,500

326,250

489,375

734,063

1,101,095

€ € € € €

Forecast sales price less 20% 11.20 Less: Forecast manufacturing cost with 5% reduction 9.025

Shipping costs 0.40

Margin 1.775 386,063 579,094 868,641 1,302,962 1,954,444

Cost of capital 10% 0.909 0.826 0.751 0.683 0.621

Present value of margin 350,931 478,332 652,349 889,923 1,213,710

Cumulative present value 350,931 829,263 1,481,612 2,371,535 3,585,245

NPV 3,585,245

Difference in NPV 447,206

Difference in margin each year - discounted (254,318) (137,650) 25,090 251,004 563,080

Note: The cost of designing one exclusive product each year is excluded as it will cover the costs incurred and is therefore not relevant. Payback period: (based on discounted cash flows) is 4.21 years.

© The Chartered Institute of Management Accountants 2012 Page No: 20

Appendix 5

Inventory Valuation

Current Current Revised Revised Difference

Volumes Valuation Valuation valuation valuation

Units

€ / unit

€

€ / unit

€

€

Product BB 4,900 6.30 30,870 2.50 12,250 (18,620)

Product CC 2,680 12.50 33,500 5.00 13,400 (20,100)

Product FF 1,200 7.00 8,400 0.00 0 (8,400)

Total 72,770 25,650 (47,120)

© The Chartered Institute of Management Accountants 2012 Page No: 21

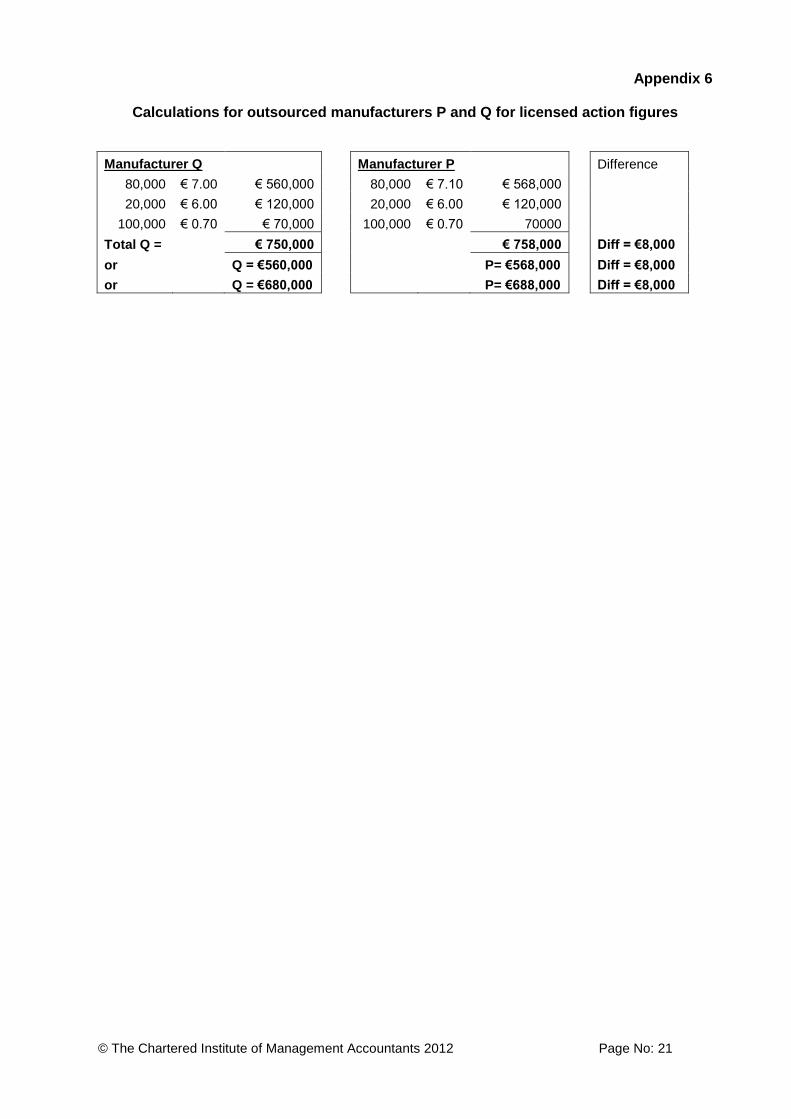

Appendix 6

Calculations for outsourced manufacturers P and Q for licensed action figures

Manufacturer Q Manufacturer P Difference

80,000 € 7.00 € 560,000 80,000 € 7.10 € 568,000

20,000 € 6.00 € 120,000 20,000 € 6.00 € 120,000

100,000 € 0.70 € 70,000 100,000 € 0.70 70000

Total Q = € 750,000 € 758,000 Diff = €8,000

or Q = €560,000 P= €568,000 Diff = €8,000

or Q = €680,000 P= €688,000 Diff = €8,000

© The Chartered Institute of Management Accountants 2012 Page No: 22

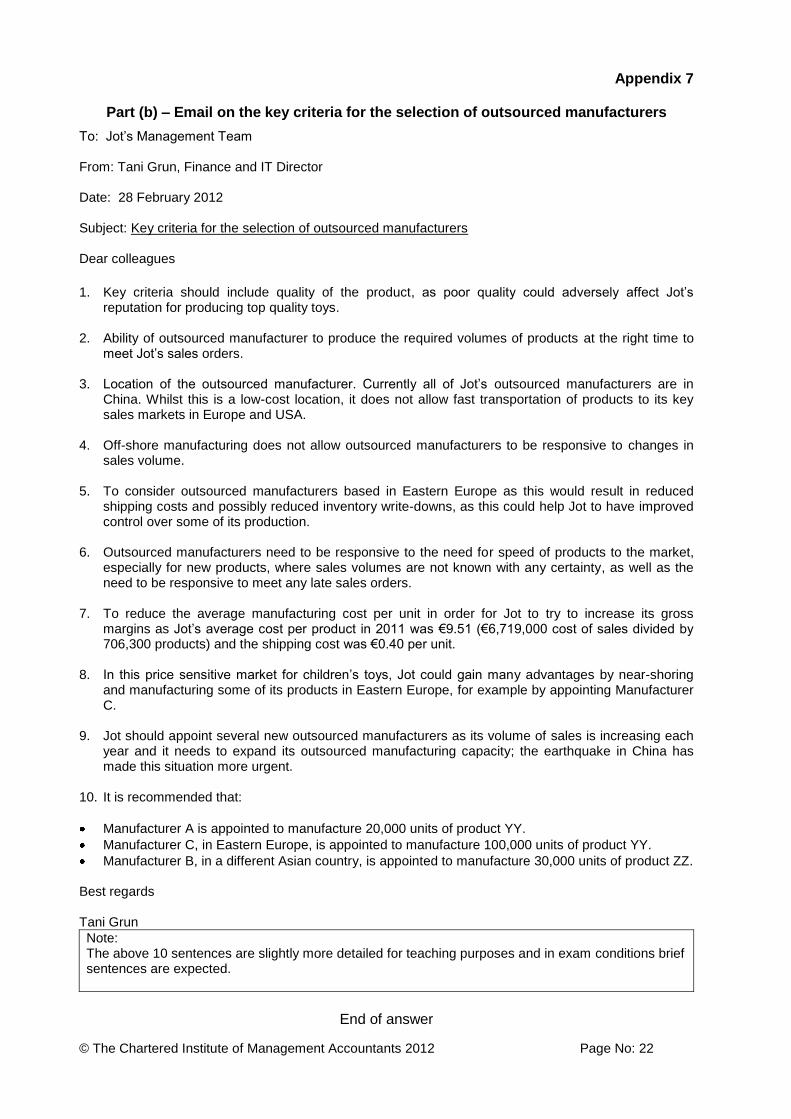

Appendix 7

Part (b) – Email on the key criteria for the selection of outsourced manufacturers

To: Jot’s Management Team From: Tani Grun, Finance and IT Director Date: 28 February 2012 Subject: Key criteria for the selection of outsourced manufacturers Dear colleagues

1. Key criteria should include quality of the product, as poor quality could adversely affect Jot’s

reputation for producing top quality toys. 2. Ability of outsourced manufacturer to produce the required volumes of products at the right time to

meet Jot’s sales orders. 3. Location of the outsourced manufacturer. Currently all of Jot’s outsourced manufacturers are in

China. Whilst this is a low-cost location, it does not allow fast transportation of products to its key sales markets in Europe and USA.

4. Off-shore manufacturing does not allow outsourced manufacturers to be responsive to changes in

sales volume. 5. To consider outsourced manufacturers based in Eastern Europe as this would result in reduced

shipping costs and possibly reduced inventory write-downs, as this could help Jot to have improved control over some of its production.

6. Outsourced manufacturers need to be responsive to the need for speed of products to the market,

especially for new products, where sales volumes are not known with any certainty, as well as the need to be responsive to meet any late sales orders.

7. To reduce the average manufacturing cost per unit in order for Jot to try to increase its gross

margins as Jot’s average cost per product in 2011 was €9.51 (€6,719,000 cost of sales divided by 706,300 products) and the shipping cost was €0.40 per unit.

8. In this price sensitive market for children’s toys, Jot could gain many advantages by near-shoring

and manufacturing some of its products in Eastern Europe, for example by appointing Manufacturer C.

9. Jot should appoint several new outsourced manufacturers as its volume of sales is increasing each

year and it needs to expand its outsourced manufacturing capacity; the earthquake in China has made this situation more urgent.

10. It is recommended that:

Manufacturer A is appointed to manufacture 20,000 units of product YY.

Manufacturer C, in Eastern Europe, is appointed to manufacture 100,000 units of product YY.

Manufacturer B, in a different Asian country, is appointed to manufacture 30,000 units of product ZZ. Best regards Tani Grun

Note: The above 10 sentences are slightly more detailed for teaching purposes and in exam conditions brief sentences are expected.

End of answer